FedEx: The Overnight Revolution

I. Introduction & Episode Preview

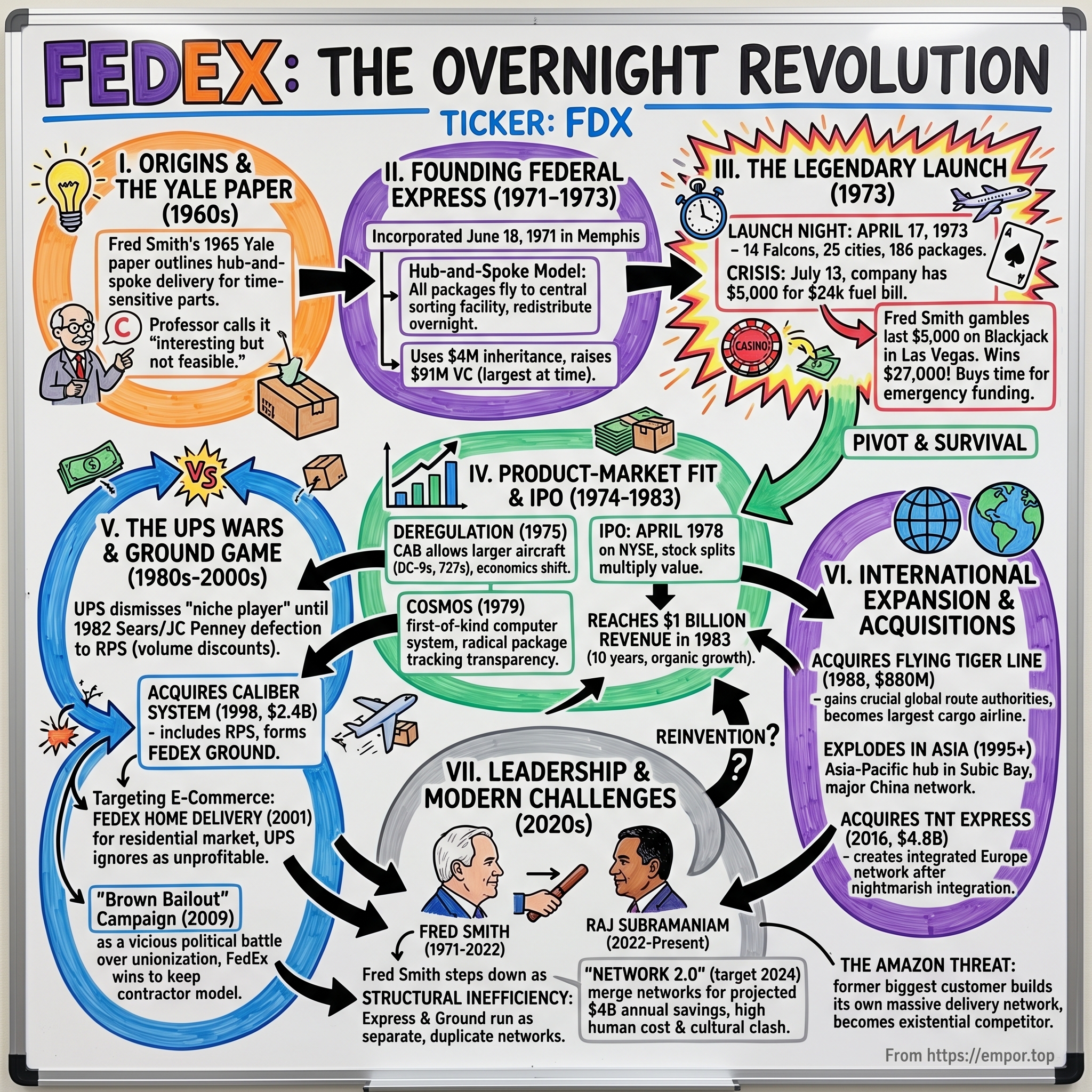

Picture this: It's 1973, and Fred Smith is sitting in a Las Vegas casino at 4 AM, the company's last $5,000 riding on blackjack. Federal Express has $24,000 in jet fuel bills due Monday morning. The cards flip. Twenty-one. Again. And again. By sunrise, he's turned that desperate $5,000 into $27,000—enough to keep the planes flying for another week. This wasn't just gambling; it was the difference between creating a $90 billion logistics empire and becoming another failed startup footnote.

"Absolutely, positively overnight"—those three words didn't just describe a service; they invented an entire industry. Before Federal Express, the idea of guaranteed overnight delivery across America was science fiction. The postal service took days. Air freight was unpredictable. Yet here was a Marine Corps veteran with a mediocre college term paper, insisting he could move packages from New York to Los Angeles faster than you could drive across town.

The central question isn't just how Fred Smith built FedEx—it's how he created an entire market category while dancing on the edge of bankruptcy, fighting off skeptical investors who called him delusional, and eventually building a duopoly with his fiercest rival, UPS. This is a story of creating demand where none existed, of building physical network effects before Silicon Valley made the term fashionable, and ultimately, of birthing the very e-commerce giant that would become both your biggest customer and existential threat.

We'll trace the journey from that infamous Yale paper to a global infrastructure moving $2 trillion in goods annually. We'll explore how a company built on speed became the circulatory system of modern commerce. And we'll examine the profound irony: FedEx enabled the rise of Amazon, which now threatens to disintermediate the very company that made its two-day—then one-day—delivery promises possible.

The themes that emerge are timeless for any founder or investor: When do you create markets versus enter them? How do you build defensible moats in capital-intensive industries? What happens when operational excellence becomes table stakes? And perhaps most critically: How do you compete with your own customers without destroying yourself?

This isn't just the story of packages and planes. It's about how one company rewired global commerce, turned "logistics" from a back-office function into a strategic weapon, and proved that sometimes the best businesses aren't about doing something new—they're about doing something everyone needs but nobody realized was possible.

II. Origins: Fred Smith & The Yale Paper

The Mississippi Delta in 1944 wasn't where you'd expect to find the seeds of a logistics revolution. Frederick Wallace Smith was born in Marks, Mississippi—population 2,500—into unusual privilege. His father, Frederick Sr., had built a fortune from Dixie Greyhound bus lines and a restaurant chain, amassing enough wealth that when he died in 1948, four-year-old Fred would inherit $4 million (roughly $50 million today). But wealth came with complications: young Fred suffered from a bone disease called Calve-Perthes, spending years in braces and crutches, watching other kids play while he studied systems and patterns from the sidelines.

By the time Smith reached Yale in 1962, the crutches were gone but the systems thinking remained. While his classmates at Skull and Bones were planning Wall Street careers, Smith was flying charter planes on weekends, observing something broken in American logistics. In 1965, for a term paper in his economics class, he outlined a radical idea: an integrated air-ground delivery system designed specifically for time-sensitive shipments. The professor's response? A C grade, with a note that the concept was "interesting but not feasible."

The paper's core insight was deceptively simple yet revolutionary: existing air freight treated packages like passengers—point to point, with multiple stops, unpredictable timing. Smith proposed something different: a hub-and-spoke system where all packages would fly to a central sorting facility, get redistributed overnight, then fan out for morning delivery. Think of it like a massive airline, but instead of people choosing their destinations, every package would follow the same choreographed midnight dance through Memphis.

His economics professor saw impracticality. Smith saw inevitability. "I became convinced," he'd later say, "that the world was becoming automated, computerized, and miniaturized. Companies would need to move high-value, time-sensitive parts and documents quickly. The passenger route systems just couldn't handle it."

But first came Vietnam. Smith joined the Marines in 1966, not out of patriotic duty but practicality—he figured military service would help in business. What followed exceeded all expectations: two tours, 200 combat missions as a forward air controller, company command of Marines, and decorations including the Silver Star, Bronze Star, and two Purple Hearts. One citation described him carrying wounded Marines to safety under heavy fire. Another detailed him calling in airstrikes danger-close to his own position.

The Marine Corps gave Smith more than medals—it gave him an operational philosophy. "I learned that you can't manage people, you can only lead them," he'd reflect. "You have to give them a mission, the tools to accomplish it, then get out of their way." The Marines also taught him about logistics under pressure: how to move supplies through hostile territory, coordinate complex operations with imperfect information, and most critically, that when systems break down, people die.

Returning to Memphis in 1969, Smith saw America differently. The economy was shifting from manufacturing to services. Computers were proliferating. Companies like IBM needed to move parts overnight to fix million-dollar mainframes. The financial sector needed to clear checks faster. Yet the logistics infrastructure remained stuck in the railroad era. His stepfather, a former FBI agent, tried to interest him in local politics. His sisters expected him to manage the family trust. Instead, Smith bought two aircraft and started doing charter flights while studying the feasibility of his Yale concept.

The epiphany crystallized in 1970 when he visited the Federal Reserve. The Fed was flying checks between its twelve regional banks using an inefficient patchwork of carriers. Smith proposed a dedicated overnight network—planes specifically configured for packages, not passengers, all routing through Memphis. He'd call it Federal Express, banking on the gravitas of the "Federal" name to suggest reliability and authority. The Fed seemed interested. Smith incorporated Federal Express Corporation on June 18, 1971, using his $4 million inheritance as seed capital.

Then came the first lesson in entrepreneurial heartbreak: the Federal Reserve pulled out, citing regulatory concerns and bureaucratic inertia. Smith was left with a company named for a customer he'd never have, two Falcon jets he couldn't afford to operate, and a vision that suddenly needed a completely different market. Most would have folded. Smith doubled down, deciding if the Fed wouldn't be his anchor customer, he'd build a network so compelling that every business in America would have to use it.

The Marine in him saw it as a mission: American business was fighting with one hand tied behind its back, unable to move critical items quickly. He'd build the logistics equivalent of air support—reliable, fast, and available on demand. The question was whether anyone would pay for a service they didn't yet know they desperately needed.

III. The Launch: 1971-1973 — Building the Network

The winter of 1973 should have been the death of Federal Express. Smith had burned through his inheritance, convincing venture capitalists to pour $91 million into what was then the most highly financed new company in U.S. history in terms of venture capital. The original plan—shuttling checks for the Federal Reserve banks—had collapsed. Now he needed to convince investors that businesses would pay premium prices for guaranteed overnight delivery when they'd never had it before. His pitch was simple: in an automated society, when a computer breaks, you need the part immediately or you're out of business. The investors bit, but not without skepticism.

Smith's masterstroke was the hub-and-spoke model. Unlike traditional airlines that flew packages point-to-point like passengers, every Federal Express package would fly to Memphis, get sorted between midnight and 3 AM, then fly out for morning delivery. It was counterintuitive—why fly a package from Nashville to Knoxville via Memphis?—but it was the only way to guarantee next-day delivery between any two points. The math was elegant: instead of needing direct flights between every city pair (which would require hundreds of routes), you only needed flights from each city to Memphis and back.

The company moved from Little Rock to Memphis in 1973, chosen for its central location and remarkably stable weather—fog and snow rarely grounded planes there. Smith leased fourteen French-built Dassault Falcon 20 jets, small enough to avoid CAB regulations on larger aircraft but big enough to carry meaningful cargo. He hired 389 employees, many of them fellow Vietnam veterans who understood military-style precision and wouldn't quit when things got tough.

Launch night arrived April 17, 1973. Fourteen Falcons took off from Memphis, carrying 186 packages to 25 U.S. cities. Smith watched from the Memphis hub as the planes departed, knowing that if even one package missed its deadline, the entire premise would crumble. Every package arrived on time. But 186 packages wouldn't pay for jet fuel, let alone salaries.

The next months were brutal. Federal Express lost nearly $30 million in its first 26 months, hemorrhaging over a million dollars monthly. The 1973 oil embargo quadrupled fuel costs overnight. Investors grew nervous. By Friday, July 13, 1973, the company had $5,000 in the bank and a $24,000 fuel bill due Monday. The planes would be grounded. Game over.

What happened next became Silicon Valley legend before Silicon Valley existed. Smith flew to Las Vegas with the company's last $5,000. At the blackjack tables, he played through the night. The $27,000 he won wasn't decisive, but as Smith later said, "it was an omen that things would get better". It bought another week of operations, enough time to secure emergency funding from General Dynamics.

The gamble wasn't just financial—it was existential. Smith was betting that American business was about to transform, that just-in-time manufacturing would replace massive inventories, that speed would become the ultimate competitive advantage. He was creating demand for something customers didn't know they needed. As one early employee put it: "We weren't selling a service. We were selling time itself."

By late 1973, volume was growing—slowly. The company handled 1,000 packages nightly by year's end, still far below the 10,000 needed for profitability. But something was changing. IBM signed on, needing to move computer parts overnight. Banks discovered they could clear checks days faster. Medical companies could ship blood samples and organs. Federal Express wasn't just delivering packages; it was rewiring how American business operated.

The hub-and-spoke system proved its genius nightly. At midnight, Memphis International Airport transformed into organized chaos. Planes landed every few minutes. Packages flew down conveyor belts. Sorters had exactly 90 minutes to unload, sort, and reload everything. By 3 AM, the planes departed like spokes from a wheel, racing sunrise to deliver before 10:30 AM. It was a ballet of logistics, choreographed to the minute.

But the financial bleeding continued. Smith mortgaged his house, sold the family trust's holdings, and begged investors for patience. He gave speeches to half-empty rooms, evangelizing overnight delivery to executives who saw no need for it. One investor recalled: "Fred would stand there with his charts and graphs, insisting this would change everything. We thought he was delusional. Thank God we were wrong."

The turning point came from an unexpected source: the employees themselves. When Smith couldn't make payroll in early 1974, he gathered the workers in a hangar. "I can't pay you this week," he said. "But if you can hold your checks for a few days, I promise we'll make this work." Nearly everyone agreed. These weren't just employees; they were believers in a mission. Many were Vietnam veterans who'd followed Smith from combat to commerce. They understood that some battles are won by refusing to retreat.

IV. Finding Product-Market Fit & Going Public (1974-1983)

The summer of 1974 brought the Arab oil embargo's aftermath—fuel prices that had quadrupled, inflation spiraling toward double digits, and a recession that crushed discretionary spending. Federal Express was burning through $1 million monthly. Daily package volume hovered around 3,000—far below the 10,000 needed for breakeven. Smith's board was fracturing. One director suggested liquidating while they could still recover something. Another proposed selling to Emery Air Freight. Smith refused both, arguing they were three months from profitability. He was lying—he had no idea when they'd turn the corner.

The breakthrough came from deregulation's first whispers. In 1975, the CAB finally allowed Federal Express to fly larger aircraft—DC-9s and Boeing 727s that could carry real volume. Suddenly, the economics shifted. Each flight could carry five times more packages at marginally higher cost. Smith immediately ordered seven used 727s, mortgaging everything to finance them. The gamble was existential: if volume didn't materialize, the debt would destroy them.

But volume did materialize. In 1976, the company became profitable with an average volume of 19,000 parcels per day. The turning point wasn't a single customer or contract—it was the collective realization by American business that overnight delivery had become essential. IBM needed parts for mainframe repairs. Banks needed documents signed and returned same-day. Medical labs needed blood samples analyzed immediately. Federal Express wasn't selling speed; it was selling certainty in an uncertain world.

The introduction of drop boxes in 1975 proved transformative. Instead of requiring customers to drive to Federal Express offices, purple-and-orange boxes appeared on street corners, in office lobbies, at airports. Each box had a pickup time clearly marked—miss it by one minute, and your package wouldn't fly that night. This visibility created urgency and habituated users to Federal Express's rhythm. The boxes became totems of reliability.

By 1977, with the company finally profitable, Smith prepared for the next phase: going public. The IPO prospectus revealed stunning numbers. Revenue had grown from $75 million in 1976 to $160 million in 1977. The company was adding 100 new customers daily. But Wall Street remained skeptical. How sustainable was this growth? What happened when UPS inevitably entered overnight delivery? Could a company built on such thin margins survive the next recession?

FedEx went public in April 1978 at $24 a share and was later listed on The New York Stock Exchange in December 1978. Within a month, the stock had nearly doubled. Early investors who'd risked everything on Smith's vision saw 30-bagger returns. FedEx completed a total of five stock splits in the years 1978, 1980, 1983, 1996 and 1999. Each split was a two-for-one, which doubled the number of shares of FedEx stock held by an investor. The stock splits took the 41.67 shares to a total of 1,333.44 over the course of the five transactions.

The overnight letter, introduced in 1981, marked Federal Express's first direct assault on the U.S. Postal Service. For $9.50, documents could be delivered overnight—compared to the USPS's two-to-three day Express Mail at similar prices. The legal industry adopted it instantly. Contracts that once took a week to negotiate could be completed in days. Wall Street firms could execute trades with signed confirmations by next morning. Federal Express wasn't just moving paper—it was accelerating the velocity of business itself.

The numbers by 1983 defied every precedent. The company had reached $1 billion in revenue, a rarity for a startup company that had never taken part in mergers or acquisitions in its first decade. Federal Express' sales topped $1 billion for the first time in 1983. No American company had ever grown from zero to a billion dollars in ten years through organic growth alone. Daily package volume exceeded 90,000. The hub in Memphis processed more cargo nightly than most airports handled in a month.

But success brought scrutiny. The Interstate Commerce Commission launched investigations into Federal Express's pricing. Labor unions attempted organizing drives, seeing rich targets in the company's 20,000 employees. Competitors like Emery and Airborne Express slashed prices, hoping to bleed Federal Express's margins. And most ominously, rumors swirled that UPS was developing its own overnight service.

Smith's response was counterintuitive: he raised prices and improved service. While competitors promised "next-day" delivery by 5 PM, Federal Express guaranteed 10:30 AM. When others offered money-back guarantees with exceptions, Federal Express made theirs unconditional. The message was clear: Federal Express wasn't competing on price but on reliability. In a world where a missed deadline could cost millions, businesses would pay premiums for certainty.

The introduction of COSMOS (Customer Operations Service Master Online System) in 1979 revolutionized package tracking. For the first time, customers could call and know exactly where their package was—not just "in transit" but "arrived Memphis hub 2:47 AM, departed for Seattle 3:15 AM, on truck for delivery 8:30 AM." This transparency, radical for its time, transformed customer expectations. Suddenly, every shipping company needed tracking systems. Federal Express had again created a market standard that became table stakes.

By decade's end, Federal Express had transcended its startup origins. The company that nearly died over a $24,000 fuel bill now generated over $50 million in monthly profit. The fourteen Falcon jets had grown to a fleet of 50 Boeing 727s. The 389 founding employees had become 17,000. Most remarkably, "FedEx" had entered the vernacular—people didn't ship packages overnight; they "FedExed" them. The brand had become the category.

V. The UPS Wars & Ground Game (1980s-2000s)

The 1980s opened with UPS sleeping soundly, convinced Federal Express would remain a niche player in overnight documents. They controlled 90% of the ground package market, their brown trucks as ubiquitous as mailboxes. Their pricing was simple: uniform rates regardless of volume. A mom-and-pop shop paid the same per package as Sears. This arrogance would prove fatal.

The catalyst came from an unexpected source. In 1982, Sears and JC Penney approached UPS requesting volume discounts—standard practice in every other industry. UPS refused, claiming their uniform pricing was non-negotiable. Within months, both retailers switched to a scrappy upstart called Roadway Package System (RPS), which offered 40% discounts for high-volume shippers. The defection sent shockwaves through the logistics industry. If Sears could leave UPS, anyone could.

Federal Express watched this drama unfold with intense interest. Smith recognized that UPS's ground monopoly was cracking, but Federal Express had no ground network—everything flew. Building one from scratch would take decades and billions. Then, in 1997, opportunity knocked. Caliber System, RPS's parent company, was struggling despite RPS's success. Smith saw his chance.

The 1998 acquisition of Caliber System for $2.4 billion transformed Federal Express overnight. Caliber owned not just RPS but also Viking Freight, Roberts Express, and several logistics companies. Federal Express acquired Caliber in 1998, with RPS becoming FedEx Ground, Roberts Express becoming FedEx Custom Critical, and Viking becoming part of what would later be FedEx Freight.

The genius of FedEx Ground wasn't just its network—it was its operating model. While UPS employed all its drivers as unionized employees with full benefits, FedEx Ground used independent contractors who owned their routes. This wasn't just cost-cutting; it was philosophical. Contractors had skin in the game. They bought their own trucks, hired their own drivers, and kept profits from efficiency gains. Labor costs were 30% lower than UPS. More importantly, FedEx avoided the union negotiations that regularly paralyzed UPS with strikes.

UPS initially dismissed FedEx Ground as irrelevant. "They're just contractors in unmarked vans," one UPS executive sneered in 1999. But those contractors were hungry. They worked Saturdays when UPS didn't. They customized service for local clients. They undercut UPS prices by 15-20% while maintaining 98% on-time delivery. By 2000, FedEx Ground was growing at 25% annually while UPS ground volume stagnated.

The real war began in 2001 when FedEx launched Home Delivery, targeting the nascent e-commerce market. UPS had ignored residential delivery as unprofitable—too many stops, too few packages per stop. FedEx saw the future differently. Every Amazon box, every eBay purchase, every online order would need home delivery. They built the network before demand materialized, betting that e-commerce would explode. They were spectacularly right.

By 2020, the landscape had transformed completely. FedEx and UPS maintained a duopoly in the United States courier market, with a combined market share of around 70% by revenue. But the dynamics had shifted dramatically from the 1990s. The collective market share of FedEx and UPS had decreased from 90% in 1998 to less than 50% by volume, losing ground to private fleets like Amazon and Walmart.

The "Brown Bailout" campaign of 2009 marked the rivalry's most vicious phase. When Congress considered legislation that would make it easier for FedEx Express workers to unionize (moving them from Railway Labor Act to National Labor Relations Act coverage like UPS), FedEx launched a multimillion-dollar campaign accusing UPS of seeking a government bailout. They created BrownBailout.com, ran TV ads, and mobilized customers to lobby Congress. The campaign's brilliance was its framing: FedEx positioned union protection as anti-competitive rather than pro-worker.

UPS fired back with its own campaign, arguing FedEx had an unfair advantage by classifying drivers as contractors rather than employees. They highlighted cases where FedEx Ground contractors worked 70-hour weeks without overtime, lacked health insurance, and bore all vehicle costs. The public relations war raged for two years, with both companies spending over $50 million on lobbying. In the end, FedEx won—the legislation died in committee, preserving their contractor model.

The operational philosophies diverged further through the 2000s. UPS built an integrated network where ground and air operations merged seamlessly. A package could move by truck to a hub, fly to another city, then continue by truck—all tracked through one system. FedEx kept operations separate: FedEx Express for air, FedEx Ground for trucks, different workforces, different facilities. Critics called it inefficient. Smith called it focused: "Each operating company optimizes for its specific market. That specialization drives excellence."

Price wars intensified after 2010. Both companies announced annual "general rate increases" of 4.9-5.9%, but real pricing told a different story. Published rates were fiction—every significant customer negotiated 40-70% discounts. The companies engaged in synchronized pricing, announcing increases within weeks of each other, always identical percentages. The increases were likewise identical across a range of specific services, such as overnight or second-day deliveries. In the US, FedEx typically announced first (usually in September), followed by UPS in October or November, with FedEx consistently publishing rate increases around a month in advance of its competitor.

Market share battles played out customer by customer. When Amazon threatened to leave UPS in 2013, UPS offered unprecedented discounts—reportedly below cost on some routes—to keep the business. FedEx responded by offering Amazon dedicated planes and facilities. The courtship was surreal: two companies fighting to serve a customer openly building its own delivery network to replace them both.

By 2015, the ground game had reached stalemate. UPS held 46-50% share in the domestic US market, while FedEx Ground had carved out a profitable niche. But both faced a new reality: the war wasn't between them anymore. Amazon Logistics was delivering 2 billion packages annually. Regional carriers like OnTrac and LaserShip were cherry-picking profitable routes. The USPS, once left for dead, was resurging with Sunday delivery and last-mile partnerships.

The irony was complete: FedEx and UPS had spent two decades fighting each other for a market that was fragmenting beneath them. They'd built massive infrastructure, sophisticated technology, and operational excellence—only to watch new entrants use asset-light models and gig workers to undercut them. The duopoly remained profitable, but growth belonged to others. As one industry analyst noted in 2020: "FedEx and UPS won the war but lost the peace."

VI. International Expansion & Major Acquisitions

The boardroom at Federal Express headquarters in December 1988 was tense. Fred Smith was proposing the unthinkable: spending $880 million—nearly a quarter of the company's market value—to acquire Flying Tiger Line, a cargo airline bleeding money and burdened with aging planes. The board saw a dying company with $630 million in losses over the previous seven years. Smith saw something invisible to spreadsheets: global route authorities worth their weight in gold.

Flying Tigers wasn't just any cargo airline—it was aviation royalty, founded in 1945 by pilots from General Claire Chennault's legendary "Flying Tigers" squadron. After returning to the United States in 1945, ten former AVG pilots led by Robert William Prescott established the Flying Tiger Line on 24 June 1945 under the name National Skyway Freight using a small fleet of 14 Budd Conestoga freighters purchased as war surplus from the United States Navy. By the 1980s, it operated the world's largest cargo network, serving 58 countries across six continents.

But Flying Tigers was dying. Deregulation had unleashed brutal competition. Management had made disastrous diversification attempts, including launching a passenger airline that hemorrhaged cash. By 1988, CEO Stephen Wolf was desperate to sell. Smith saw opportunity in desperation. Tiger International, the parent company of FT, then the world's largest cargo airline, was purchased by FedEx in December 1988 for US$880 million. This formed part of FX's overseas expansion plans.

The real prize wasn't the fleet of 39 Boeing 747s and DC-8s—it was the route authorities. Flying Tigers held landing rights in Tokyo, Hong Kong, Singapore, Paris, London, and dozens of other cities that Federal Express had been trying to crack for years. These weren't just permissions; they were keys to the kingdom of international commerce. Securing similar rights independently could take decades of negotiations and billions in infrastructure. Smith was buying them overnight.

The merger on August 7, 1989, was operationally brutal. The merger saw FX inherit FT's 39-strong fleet and 6,500 employees. Federal Express inherited 6,500 employees with a completely different culture—old-school cargo cowboys who flew anything anywhere versus Federal Express's precision-obsessed operation. Flying Tigers pilots, many of whom had flown military charters in Vietnam, resented the "package boys" from Memphis. Integration took years, with separate seniority lists and operating certificates maintained to preserve route authorities in certain countries.

But the payoff was immediate. Federal Express could now offer true round-the-world service. A package from Memphis could reach Singapore in 48 hours. Asian manufacturers could ship directly to American consumers. The acquisition made Federal Express the world's largest full-service cargo airline overnight, catapulting it from domestic player to global powerhouse.

The Asian expansion proved prescient. By 1995, Federal Express opened an Asia-Pacific hub at Subic Bay in the Philippines, processing 300,000 packages nightly. China operations, initially limited by regulation, exploded after 2000. The company built a $100 million hub in Guangzhou in 2009, becoming the primary conduit for Chinese goods entering Western markets. What began with Flying Tigers' landing rights became a $10 billion Asian revenue stream.

Europe remained elusive despite Flying Tigers' network. DHL dominated with 40% market share. UPS had established beachheads. Federal Express struggled for decades, losing money consistently. The solution came in 2016 with the audacious $4.8 billion acquisition of TNT Express, Europe's second-largest express delivery company. In April of 2015, FedEx announced its biggest acquisition yet, purchasing Dutch delivery firm TNT Express for €4.4 billion euros. TNT was one of Europe's leading courier services, with extensive operations across the continent.

TNT brought 54,000 employees, 26 sorting centers, and most critically, road networks connecting every major European city. Where Federal Express flew packages, TNT drove them. The combination created the first truly integrated air-ground network spanning Europe. But integration proved nightmarish. IT systems didn't mesh. Labor contracts conflicted. A cyberattack in 2017 crippled TNT's systems for months. The acquisition wouldn't turn profitable until 2019.

The Kinko's acquisition in 2004 for $2.4 billion represented a different strategy: retail presence. With 1,200 locations, Kinko's gave Federal Express storefronts in every major American city. Customers could ship packages, print documents, and access business services. Rebranded FedEx Office, it became the physical manifestation of the brand, though margins remained stubbornly low and the cultural fit proved challenging.

Less visible but equally strategic were the ground acquisitions. American Freightways in 2001 for $1.2 billion. Watkins Motor Lines in 2006. Viking Freight operations expanded. These weren't sexy deals, but they built FedEx Freight into a $8 billion business moving everything too large for small packages but too small for full truckloads. The LTL (less-than-truckload) market was unglamorous but essential—the circulatory system of American manufacturing.

China presented unique challenges. State-owned carriers received preferential treatment. Regulations changed arbitrarily. FedEx needed local partners but risked intellectual property theft. The company acquired 50% of DTW Group's Chinese domestic network, gaining access to 89 cities overnight. But profits remained elusive. By 2018, China generated $2 billion in revenue but minimal margins, a strategic necessity rather than financial win.

The USPS partnership in 2001 was perhaps the strangest bedfellow arrangement. In 2001, FedEx sealed a $9 billion deal with the USPS to transport all of the post office's overnight and express deliveries. FedEx flew mail for its quasi-competitor, generating $1.5 billion annually with minimal marginal cost. Critics called it corporate welfare. Smith called it smart capacity utilization—planes flew anyway; carrying mail just increased revenue per flight.

International expansion brought unexpected challenges. In Japan, acquired route authorities required maintaining Flying Tigers branding for years. In India, regulations mandated local partnerships that diluted control. In Brazil, corruption and infrastructure deficiencies made profitability impossible. Federal Express learned that logistics wasn't just about moving packages—it was about navigating political, cultural, and regulatory mazes unique to each nation.

By 2020, international operations generated 40% of Federal Express revenue but consumed 60% of capital expenditure. The company operated in 220 countries, employed 500,000 people globally, and moved $2 trillion in goods annually. The network that began with 14 jets flying to 25 American cities had become Earth's circulatory system for commerce.

Yet questions persisted. Was global reach sustainable when regional players operated more efficiently in local markets? Could Western logistics models succeed in developing nations with different infrastructure and expectations? Most critically, as trade wars and nationalism rose, was betting on globalization still wise? Smith's successor would inherit not just a global network but the fundamental question of whether "The World on Time" remained a viable promise in an increasingly fractured world.

VII. Technology, Innovation & Cultural Impact

The revolution began with a beep. In 1979, Federal Express introduced COSMOS (Customer Operations Service Master Online System), the logistics industry's first centralized computer system to manage people, packages, vehicles and weather scenarios in real time. Before COSMOS, tracking meant phone calls, paper logs, and prayer. After COSMOS, every package had a digital heartbeat, pulsing location updates as it moved through the network.

The magic wasn't the mainframe computers—everyone had those. It was the philosophy: information about the package was as important as the package itself. Fred Smith famously said in 1978, "The information about the package is just as important as the package itself." This wasn't hyperbole. In a world where a missing part could shut down a factory, knowing where that part was—and when it would arrive—had immense value.

The SuperTracker changed everything. This is a Federal Express SuperTracker handheld barcode scanner, first introduced in 1986. The SuperTracker is a critical part of FedEx's Customers, Operations, and Services Master On-line System (COSMOS) used to track packages and confirm deliveries. The device looked primitive—a black plastic brick with a keyboard—but it gave couriers superpowers. Scan a package at pickup: timestamp recorded. Scan at the hub: location updated. Scan at delivery: proof captured. Suddenly, packages couldn't disappear into the void.

But the real breakthrough came in 1994. In 1994, FedEx launched fedex.com as the first transportation web site to offer online package tracking. For the first time in history, customers could type a tracking number into a website and see exactly where their package was. No phone calls. No hold music. Just instant information. The psychological impact was profound. Anxiety about shipments evaporated when you could check status obsessively, refreshing the page like a slot machine.

UPS scrambled to catch up, launching their own tracking system two years later. But Federal Express had already won the perception war. "FedEx it" meant not just shipping but knowing—with certainty—where your shipment was. The company had commoditized trust through transparency, turning tracking from a feature into an expectation that every logistics company would have to match.

The barcode itself became a cultural artifact. Those zebra stripes on every package represented the digitization of the physical world. Each scan was a data point, millions accumulating daily into patterns that revealed inefficiencies, optimized routes, predicted delays. Federal Express wasn't just moving packages; it was generating intelligence about global commerce flows that governments and economists would kill for.

Then came Hollywood. In 2000, "Cast Away" premiered with Tom Hanks as a FedEx executive obsessed with time, efficiency, and the sacred obligation of delivery. The plane crash that strands him was every logistics professional's nightmare—packages undelivered, promises broken. Smith initially panicked when he heard the plot. "When I told our senior VP of marketing that I'd agreed to let a FedEx plane be crashed with Tom Hanks in it, he almost passed out." But the film became what Smith calls a $100 million infomercial for a company that is always racing the clock.

The product placement was unprecedented. FedEx didn't pay a cent, but their brand appeared in nearly every frame. More importantly, the film humanized logistics. Audiences understood viscerally what it meant when a package didn't arrive. Wilson the volleyball—delivered by FedEx to the island—became a metaphor for connection in isolation. The film's success proved that FedEx had transcended utility to become culture.

E-commerce changed the game entirely. In 1995, Amazon shipped its first book. By 2000, online retail was exploding, and every purchase needed delivery. Federal Express, built for B2B shipping, had to transform overnight into a consumer company. Residential delivery—previously an afterthought—became central. The problem: homes aren't businesses. No loading docks. No receiving departments. No one home during the day.

The solution required rethinking everything. Delivery windows narrowed from "sometime today" to two-hour promises. Drivers became photographers, snapping pictures of delivered packages as proof. Signature requirements gave way to "safe drop" authorizations. The company that once delivered exclusively to businesses now knew the hiding spots behind every flowerpot and under every doormat in America.

Sustainability emerged as both obligation and opportunity. In 2008, Federal Express announced plans for an all-electric delivery fleet. Critics scoffed—battery technology couldn't handle the weight and range requirements. But Federal Express partnered with vehicle manufacturers, essentially funding R&D for the entire industry. By 2020, they had 2,600 electric vehicles operating, with plans for full electrification by 2040. The $2 billion investment wasn't altruism—it was anticipating regulation and customer demands that would make carbon neutrality mandatory.

The drone and autonomous vehicle revolution loomed large. Federal Express tested drone delivery in 2019, flying medical supplies to rural hospitals. Self-driving trucks hauled packages between hubs. The technology worked, but regulation, safety concerns, and labor implications remained unresolved. The question wasn't whether autonomous delivery would happen but who would control it—and whether traditional logistics companies would operate the vehicles or become obsolete.

Meanwhile, Amazon was building its own delivery network at breakneck speed. By 2020, Amazon Logistics delivered more packages than Federal Express. They'd learned everything from being Federal Express's largest customer, then built a better mousetrap. The student had become the master, using Federal Express's own innovations against them.

Federal Express responded with SenseAware—IoT devices that monitored temperature, humidity, location, and shock for sensitive shipments. A pharmaceutical company could track vaccine temperatures in real-time. An art dealer could ensure paintings weren't exposed to moisture. This wasn't just tracking; it was environmental custody, turning Federal Express into guardian rather than mere carrier.

Data became the new battleground. Every package generated hundreds of data points. Multiply by 17 million daily shipments, and Federal Express possessed one of Earth's richest datasets on global commerce. They knew what products were selling where, which supply chains were stressed, which economies were growing or contracting. This information, properly analyzed, was worth more than the delivery revenue itself.

Yet challenges mounted. Cyberattacks threatened to cripple operations—the 2017 NotPetya attack cost Federal Express $400 million. Privacy concerns arose as tracking became surveillance. Environmental activists protested the carbon footprint of overnight delivery. Labor tensions increased as technology threatened jobs. The very innovations that built Federal Express now posed existential questions about its future.

By 2020, Federal Express had become something unprecedented: a physical network with digital intelligence, a logistics company that was really a data company, a business built on speed in an age questioning the necessity of urgency. The company that invented overnight delivery now had to reinvent itself for a world where Amazon delivered in hours, where 3D printing might eliminate shipping entirely, where virtual reality could make physical products obsolete.

The irony was complete: Federal Express had spent 50 years making the impossible possible—overnight delivery anywhere on Earth. Now they faced a new impossible: remaining relevant when the very concept of shipping might become antiquated. The tracking number that once represented innovation now felt quaint in an age of real-time everything. The question for Federal Express's future wasn't whether they could deliver packages faster, but whether packages would need delivering at all.

VIII. Leadership Transition & Modern Challenges

The boardroom at FedEx headquarters on March 28, 2022, witnessed the end of an era. Fred Smith, after 50 years at the helm, announced he would step down as CEO on June 1, becoming Executive Chairman. His chosen successor, Raj Subramaniam, represented both continuity and change—a 30-year FedEx veteran who understood the culture, but also an outsider who grew up in India and brought fresh perspective to an increasingly global company.

Subramaniam's ascension was no surprise. He'd run FedEx Express, the company's largest division, through the pandemic's chaos. When global supply chains seized, when governments closed borders, when demand shifted overnight from commercial to residential delivery, Subramaniam kept the planes flying and packages moving. He'd earned his battlefield promotion by managing the unmanageable.

But the transition highlighted a deeper challenge: FedEx remained synonymous with Fred Smith. For five decades, his personality had shaped every major decision. His Marine Corps background infused the culture. His connections opened doors in Washington and Beijing. His vision of integrated global logistics had become reality. How do you replace someone who isn't just the CEO but the company's soul?

Fred Smith's death on June 21, 2025, at age 80, marked not just the loss of a founder but the end of founder-led logistics companies. UPS's founders were long gone. DHL's Larry Hillblom had died in 1995. Amazon's Jeff Bezos had stepped back from day-to-day operations. The industry built by entrepreneurs was now run by professional managers, and the implications were profound.

Smith's final years had been spent preparing for this transition. He'd restructured the board, bringing in digital natives and international voices. He'd pushed for Richard Smith, his son, to join the board in 2025—not as heir apparent but as family steward of cultural values. The succession plan was meticulous, designed to preserve what Smith called "the Purple Promise"—the commitment to making every FedEx experience outstanding.

Yet Subramaniam inherited challenges that would have taxed even Smith's legendary optimism. The first was structural: FedEx operated separate networks for Express and Ground, duplicating infrastructure while competitors like UPS ran integrated operations. The inefficiency was staggering—two drivers from the same company delivering to the same address on the same day. Customers didn't care about operational divisions; they just saw waste.

The solution, "Network 2.0," aimed to merge operations by 2024. But integration meant eliminating thousands of jobs, closing duplicate facilities, and admitting that the separated structure Smith had defended for decades was wrong. The cultural shift was seismic. Express employees, who considered themselves elite, now worked alongside Ground contractors they'd previously dismissed as inferior. The merger savings were projected at $4 billion annually, but the human cost was immeasurable.

Labor relations presented another minefield. While FedEx Express employees remained covered under the Railway Labor Act, making unionization difficult, FedEx Ground's contractor model faced legal challenges. Courts in several states ruled that contractors were effectively employees deserving benefits and protections. The gig economy that had seemed like innovation now looked like exploitation. Subramaniam had to navigate between maintaining cost advantages and avoiding becoming the next company vilified for worker treatment.

Competition had fundamentally changed. Amazon, once FedEx's largest customer, was now its biggest threat. By 2024, Amazon Logistics delivered 6.1 billion packages annually, approaching FedEx's volume. Worse, Amazon was cherry-picking profitable routes while leaving costly rural deliveries to FedEx and UPS. The density economics that made delivery profitable were being destroyed by Amazon's selective competition.

Regional carriers posed another threat. The 2021 merger of LaserShip and OnTrac created a national competitor with lower costs and hunger to grow. These carriers didn't need global networks or overnight capability—they just needed to deliver packages cheaply in major markets. They were unbundling FedEx's integrated offering, taking the profitable pieces while avoiding the costly obligations.

Technology disruption accelerated. Shopify enabled any business to sell globally without FedEx's logistics expertise. Uber and DoorDash were experimenting with same-day package delivery using their existing driver networks. Blockchain promised to eliminate paperwork and intermediaries in international shipping. Every innovation seemed designed to disintermediate traditional carriers.

The response required fundamental strategy shifts. FedEx Dataworks, launched in 2020, attempted to monetize the company's data assets. The concept was sound—FedEx knew more about global supply chains than anyone—but execution proved difficult. Customers who'd shared data for operational purposes balked at FedEx selling insights to potential competitors. The line between service provider and data broker was treacherous.

Sustainability commitments added complexity. FedEx had pledged carbon neutrality by 2040, requiring $2 billion in annual investment. Electric vehicles, sustainable aviation fuel, and renewable energy weren't just environmental necessities; they were customer demands. But the math was brutal. Electric aircraft couldn't fly transoceanic routes. Hydrogen technology remained decades away. The company built on speed now had to slow down for the planet.

The macro environment provided no relief. Post-pandemic inflation drove wages up 20%. Fuel costs fluctuated wildly. Customers, squeezed by their own cost pressures, demanded discounts while expecting better service. The pricing power FedEx once enjoyed evaporated as alternatives proliferated. The 5.9% annual rate increases became fiction, with real prices declining after negotiated discounts.

International expansion, once FedEx's growth engine, sputtered. China's government favored domestic carriers. Europe's TNT integration remained troubled. Trade wars and reshoring reduced cross-border shipping. The globalization wave FedEx had ridden for 40 years was receding, replaced by regionalization and protectionism.

Digital transformation initiatives multiplied but struggled for coherence. FedEx attempted to build an e-commerce platform to compete with Amazon. They launched Roxo, an autonomous delivery robot, then quietly shelved it. They invested in blockchain shipping documents, augmented reality for warehouse operations, and AI for route optimization. Each initiative had merit, but collectively they lacked strategic focus. FedEx was trying everything, mastering nothing.

The financial markets grew impatient. FedEx stock, which had peaked above $300 in 2021, traded below $250 by 2025. Activists investors circled, demanding split-ups, dividend cuts, and aggressive cost reduction. The quarterly earnings calls became interrogations, with analysts questioning every strategic decision. The company that had once enjoyed a "FedEx premium" now traded at a discount to UPS.

Internally, morale suffered. The company that had pioneered employee stock ownership watched its shares stagnate while tech companies minted millionaires. Talented technologists left for startups. Veteran operators retired early, taking institutional knowledge. The Purple Promise felt hollow when purple-blooded employees were laid off in restructuring.

Yet Subramaniam pushed forward with quiet determination. Unlike Smith's charismatic leadership style, Subramaniam led through systematic analysis and incremental improvement. He didn't promise revolution but evolution. He acknowledged mistakes rather than defending them. He admitted that FedEx couldn't compete everywhere and began strategic retreats from unprofitable markets.

The question facing FedEx in 2025 wasn't survival—the company remained highly profitable with enormous assets. It was relevance. In a world where Amazon delivered in hours, where local production replaced global sourcing, where digital goods replaced physical products, what role did overnight delivery play? The company that had defined urgency in logistics now had to redefine its purpose in an economy where everything was instant and nothing was urgent.

Smith's legacy was secure—he'd built one of the 20th century's most important companies. But Subramaniam's challenge was harder: transforming that company for the 21st century without destroying what made it special. The Marine Corps discipline, the operational excellence, the absolute commitment to delivery—these cultural elements had to evolve without eroding. FedEx had to become a different company while remaining FedEx.

The path forward required painful choices. Abandoning unprofitable markets. Automating jobs held by loyal employees. Competing with customers who might retaliate. Investing billions in transformation while maintaining dividends. Every decision involved tradeoffs between short-term profits and long-term survival, between shareholder returns and stakeholder interests, between what FedEx had been and what it needed to become.

IX. Playbook: Strategic & Investing Lessons

Every business school teaches the FedEx case, but most miss the real lessons. They focus on hub-and-spoke logistics or first-mover advantage. The deeper insights—the ones that matter for founders and investors—are more subtle and more powerful.

Creating Markets vs. Entering Them

The most profound lesson from FedEx is the difference between creating and entering markets. When Smith launched Federal Express, overnight delivery didn't exist as a category. There was no demand to satisfy because customers didn't know such a service was possible. This wasn't market research failure—it was market creation genius.

Consider the implications: Traditional business strategy says identify customer needs then fill them. But the biggest opportunities come from creating needs customers don't yet know they have. Before FedEx, businesses organized around mail delivery times. After FedEx, they reorganized around overnight capability. The service didn't adapt to the market; the market adapted to the service.

This principle extends beyond logistics. Apple didn't enter the smartphone market; it created it. Tesla didn't compete with car companies; it created the luxury EV category. The lesson: True innovation doesn't fight for market share in existing categories but creates new categories where you define the rules.

Network Effects in Physical Infrastructure

Silicon Valley obsesses over network effects in digital platforms, but FedEx proved physical networks could generate similar dynamics. Every new city added to the network made the entire system more valuable. A package from Memphis to Nashville was useful; a network connecting every major American city was indispensable.

The brilliance was recognizing that routes multiply geometrically while costs grow linearly. Adding the 100th city to the network created 99 new city pairs, but only required one new set of flights to Memphis. This mathematics of connectivity created a moat that took competitors decades to cross.

Modern investors should look for similar dynamics in physical businesses. Cloud kitchens, charging networks, fulfillment centers—any business where nodes create value through interconnection rather than isolation. The key question: Does adding the nth location create n-1 new value propositions or just one?

Operational Excellence as Competitive Advantage

FedEx proved that in commodity businesses, operational excellence becomes the product. Every carrier could fly packages overnight once they saw it was possible. But could they do it with 99.6% reliability? Could they track every package? Could they deliver by 10:30 AM instead of 5:00 PM?

The lesson transcends logistics. In any business where the core service becomes commoditized, the winner isn't who does it cheapest but who does it best. Amazon won e-commerce not through selection but through delivery reliability. Netflix won streaming not through content but through recommendation algorithms. Excellence in execution beats innovation in conception.

Capital Intensity as Barrier and Burden

FedEx's massive capital requirements—planes, trucks, hubs, technology—created an enormous barrier to entry. Starting a competing overnight network required billions in upfront investment before delivering the first package. This capital intensity protected FedEx's monopoly for years.

But capital intensity cuts both ways. Those same assets became anchors when the market shifted. Electric vehicles made the truck fleet obsolete. E-commerce demanded different hub configurations. The assets that protected against yesterday's competition prevented adaptation to tomorrow's.

The strategic lesson: Capital-intensive businesses must balance the protection of high barriers with the flexibility to evolve. The key is making capital investments in platforms that can be reconfigured rather than monuments that can't be moved.

Managing Labor Arbitrage

FedEx's contractor model for Ground delivery was either brilliant innovation or cynical exploitation, depending on perspective. By classifying drivers as independent contractors rather than employees, FedEx avoided billions in benefits, overtime, and union obligations. This labor arbitrage created a 30% cost advantage over UPS.

But labor arbitrage is unstable. Courts challenge classifications. Regulations change. Public opinion shifts. The company built on contractor economics faces constant legal and reputational risk. The California AB5 law, forcing reclassification of gig workers, previews FedEx's future challenges.

Investors should view labor arbitrage as temporary advantage, not permanent moat. Any business model predicated on paying workers less than competitors will face pressure—legal, social, or competitive. The question isn't whether the arbitrage will end but when and how.

Competing with Your Customers

FedEx's relationship with Amazon represents the ultimate strategic paradox: your biggest customer becomes your biggest competitor. Amazon learned logistics by shipping through FedEx, then built their own network to replace them. FedEx enabled their future competitor's education.

This pattern repeats across industries. Cloud providers enable SaaS companies that compete with their services. Platforms empower sellers who eventually bypass them. The strategic challenge: How do you serve customers who might destroy you without accelerating your own obsolescence?

The answer involves careful capability boundaries. Serve customers in areas where you have structural advantages. Avoid teaching them capabilities they can replicate. Most importantly, use the relationship to learn their intentions and limitations. FedEx knew Amazon would build delivery capacity but underestimated the speed and scale.

Brand as Premium Pricing Power

"FedEx" became a verb, the ultimate brand achievement. This linguistic dominance translated to pricing power. Customers paid 15-20% premiums for FedEx over generic alternatives because "FedEx" meant certainty. The brand was insurance against failure.

But brand premiums erode when differences disappear. As UPS, USPS, and regionals achieved similar reliability, FedEx's premium shrank. The lesson: Brand value requires continuous differentiation. Past excellence creates present permission to charge more, but only future excellence sustains it.

Regulatory Capture and Competitive Advantage

FedEx's classification under the Railway Labor Act rather than the National Labor Relations Act saved billions in labor costs. This wasn't accident but aggressive lobbying. FedEx spent hundreds of millions influencing regulation, creating competitive advantages through political action rather than operational excellence.

The strategy is uncomfortable but undeniable: Regulatory frameworks often matter more than business models. The company that shapes regulations shapes the market. Uber's fights over driver classification, Amazon's battles over sales tax, Tesla's direct sales model—each represents regulatory capture as business strategy.

The Power and Peril of Integration

FedEx's choice to keep Express and Ground operations separate seemed inefficient but had logic. Specialized operations optimized for their specific requirements. Express focused on speed, Ground on cost. Integration would compromise both.

But markets don't respect operational boundaries. Customers wanted one FedEx, not two. The efficiency gains from integration eventually outweighed the specialization benefits. The lesson: Integration decisions must follow customer needs, not operational preferences. The market defines optimal boundaries, not the organization.

Creating Switching Costs Through Systemic Integration

FedEx embedded itself into customers' operations through technology integration. APIs connected directly to enterprise systems. Tracking integrated with inventory management. FedEx became not just a vendor but infrastructure, making switching costs prohibitive.

This systemic integration strategy—making yourself essential to customer operations—creates stickier relationships than service quality alone. The question for any B2B business: Are you a vendor they buy from or a partner they can't live without?

The playbook that built FedEx—create markets, build networks, achieve excellence, integrate deeply—remains valid. But the timescales have compressed. What took FedEx decades, Amazon did in years. The next logistics revolution might take months. The principles endure but the pace accelerates. Understanding FedEx's history isn't about replicating their path but recognizing patterns that repeat at ever-increasing speed.

X. Analysis & Investment Perspective

Standing in late 2025, FedEx presents the classic value investor's dilemma: a great company at a fair price or a good company at a cheap price? The answer depends on whether you believe the moat is deepening or draining.

The Bull Case: Irreplaceable Infrastructure

The optimistic view starts with physical reality. FedEx operates 700 aircraft, 200,000 vehicles, and 5,000 facilities worldwide. Replicating this network would cost $100 billion and take decades. In a world where everyone wants everything delivered yesterday, this infrastructure is critical and irreplaceable.

The duopoly dynamics with UPS create rational competition. Both companies announce 5.9% annual price increases, maintain similar service levels, and avoid mutually destructive price wars. This isn't collusion but game theory—both players understand that aggressive competition would destroy returns for everyone. As long as this détente holds, both companies can generate consistent returns on capital.

E-commerce growth, despite Amazon's threat, remains a tailwind. Global e-commerce will reach $8 trillion by 2027, doubling from 2020. Even if FedEx loses market share, absolute volume growth could offset losses. The pie is growing faster than their slice is shrinking.

International expansion offers untapped potential. FedEx has 40% revenue exposure to international markets versus UPS's 20%. As global trade recovers and supply chains reconfigure, FedEx's broader network provides more growth optionality. The TNT acquisition, painful as integration has been, positions FedEx to capture European e-commerce growth.

The Network 2.0 integration promises $4 billion in annual savings by 2027. That's pure margin expansion—equal to 20% of current operating income. If management executes, earnings could inflect dramatically. The stock trades at 12x forward earnings, pricing in failure. Any success would drive multiple expansion.

The Bear Case: Structural Decline

The pessimistic view sees existential threats everywhere. Amazon isn't just competing; they're redefining the game. They've proven delivery can be done cheaper with gig workers and flexible capacity. Every year, Amazon handles more volume internally, leaving FedEx with less profitable leftovers.

Labor costs are exploding. The contractor model faces legal challenges nationwide. California's AB5 law could force reclassification, adding billions in costs overnight. Meanwhile, employee wages are rising 5-7% annually while pricing power erodes. The labor arbitrage that enabled profits is ending.

Technology disruption accelerates. Autonomous vehicles will eliminate driver jobs—FedEx's main cost. But tech companies, not logistics firms, will own this technology. FedEx becomes a customer, not a beneficiary, of automation. Worse, local delivery robots and drones will handle last-mile delivery, FedEx's most profitable segment.

Regional competitors are cherry-picking profitable routes. LaserShip-OnTrac doesn't need global networks—just dense local delivery. They're unbundling FedEx's integrated model, taking profitable urban routes while leaving costly rural obligations. This cream-skimming destroys network economics.

China's decoupling threatens international growth. FedEx generates $5 billion from Asia-Pacific, mostly China-related. As supply chains regionalize and trade tensions escalate, this revenue faces secular decline. The globalization tailwind that lifted FedEx for 40 years has become a headwind.

Valuation Framework

Traditional metrics paint conflicting pictures. On asset value, FedEx trades below replacement cost—the planes and facilities alone are worth more than the market cap. But assets are only valuable if they generate returns, and returns are compressing.

On earnings multiples, FedEx looks cheap at 12x forward P/E versus historical averages of 15-16x. But those historical multiples reflected growth; current multiples reflect stagnation. The market is pricing FedEx like a declining industrial, not a growth logistics player.

Free cash flow yield of 7% seems attractive until you consider capital intensity. FedEx must invest $5-6 billion annually just to maintain operations. True owner earnings—after maintenance capex—are half the reported free cash flow. The dividend yield of 2% is sustainable but unlikely to grow meaningfully.

The enterprise value of $70 billion for a company moving $2 trillion in goods seems absurd. That's 0.003% of the value flowing through their network. Surely the toll-taker deserves a bigger toll? But the market recognizes that FedEx doesn't control the toll road—they're just one option among many.

Competitive Dynamics

The UPS rivalry remains the most important dynamic. Both companies are rational actors avoiding mutually assured destruction. But rationality has limits. If volume declines accelerate, one player might break ranks, triggering a price war. The stability investors count on could evaporate overnight.

Amazon's strategy is more complex than simple competition. They need FedEx and UPS for surge capacity and rural delivery. But they also need to pressure margins to prevent excessive profits. Amazon will compete enough to keep FedEx honest but not enough to destroy them. It's controlled competition, but control could slip.

USPS remains the wildcard. With government backing and universal service obligations, they operate by different rules. Their Ground Advantage service is gaining share by undercutting commercial carriers. If political winds shift toward supporting USPS expansion, FedEx faces subsidized competition they can't match.

Regional carriers are proliferating like insurgents. Each takes a small piece, but collectively they're fragmenting the market. OnTrac, LaserShip, Veho, AxleHire—names unknown to most investors but very familiar to FedEx's pricing department. Death by a thousand cuts is still death.

Future Scenarios

The optimistic scenario sees FedEx as the "AWS of logistics"—essential infrastructure that everyone needs but few can build. Network 2.0 succeeds, margins expand, and the company generates consistent 15% returns on capital. The stock re-rates to 16x earnings, delivering 40% upside.

The base case muddles through. Volume growth offsets share losses. Pricing remains rational. Margins compress but remain acceptable. The company generates high-single-digit returns, matching Treasury yields with more risk. The stock trades sideways for years, a value trap that never springs.

The pessimistic scenario sees cascading disruption. Amazon takes more volume. Regionals cherry-pick profitable routes. Autonomous delivery eliminates FedEx's role. International trade collapses. The company enters terminal decline, cutting dividends and selling assets. The stock trades like a dying industrial, which it is.

Investment Decision Framework

For growth investors, FedEx is uninvestable. Growth is low-single-digits at best, with meaningful disruption risk. Better opportunities exist in technology or healthcare with similar returns but higher growth potential.

For value investors, FedEx presents a classic dilemma. It's statistically cheap but potentially a value trap. The key question: Is the moat durable enough to sustain returns through the transition? If yes, the risk-reward is attractive. If no, cheaper stocks will get cheaper.

For income investors, the 2% dividend yield is sustainable but unexciting. With investment-grade credit ratings and consistent cash flow, dividend cuts are unlikely near-term. But growth will be minimal, making this a bond substitute rather than an equity investment.

The Meta Question

Beyond financial metrics lies a philosophical question: Is FedEx a 20th-century company struggling in the 21st century or a bridge between physical and digital commerce? The answer determines whether this is a dying industrial or a transforming logistics platform.

The bull case sees FedEx as essential infrastructure for global commerce, irreplaceable and undervalued. The bear case sees obsolescence accelerating, with technology and competition eroding every advantage. Reality, as always, lies between extremes.

FedEx remains a profitable, cash-generative business with significant assets and capabilities. But profitability isn't the question—it's whether those profits are sustainable as the world reshapes around them. The company that created overnight delivery must now recreate itself overnight. The odds are long, but Fred Smith faced longer odds with less resources and won.

For investors, FedEx represents a bet on execution over disruption, on experience over innovation, on physical infrastructure over digital platforms. It's a contrarian bet in a market obsessed with disruption. That alone might make it interesting. Whether it makes it profitable remains to be seen.

XI. Conclusion & Reflections

Fred Smith's C-grade term paper at Yale proposed something his professor deemed impossible: an integrated air-ground logistics network for overnight delivery. Fifty years later, that impossible idea moves $2 trillion in goods annually, employs 500,000 people, and has become so essential to global commerce that its failure would trigger economic crisis. The distance between academic skepticism and commercial reality measures the gap between thinking and doing, between theory and execution.

What Smith really built wasn't a delivery company but time itself—or rather, the ability to compress it. Before FedEx, geographic distance meant temporal distance. A contract in Los Angeles took a week to reach New York. A broken part in Detroit meant a factory in Memphis shut down for days. FedEx didn't eliminate distance but made it irrelevant. In doing so, they enabled the real-time economy we now take for granted.

The paradox of FedEx's success is that it created the conditions for its own potential obsolescence. By making overnight delivery routine, FedEx enabled just-in-time manufacturing, which enabled lean inventory, which enabled e-commerce, which enabled Amazon, which now threatens to disintermediate FedEx entirely. The company that taught the world to expect everything instantly now struggles with a world that expects everything instantly for free.

This is the entrepreneur's eternal curse: Success breeds competition, innovation invites imitation, and today's breakthrough becomes tomorrow's baseline. Smith built a monopoly in overnight delivery only to watch the entire category commoditize. The moat he spent decades digging filled with competitors who learned by watching him dig.

Yet dismissing FedEx as a declining industrial misses the deeper accomplishment. They didn't just deliver packages; they delivered trust. In a world where physical and digital increasingly blur, where supply chains span continents, where a delay anywhere creates cascades everywhere, FedEx provides something more valuable than speed: certainty. The purple and orange logo is a promise that chaos can be controlled, that distance can be defeated, that tomorrow can be guaranteed.

For founders, FedEx offers timeless lessons wrapped in temporal specifics. First, the biggest opportunities lie in creating markets, not entering them. Smith didn't compete for existing freight business; he invented overnight delivery. Second, operational excellence beats strategic brilliance. FedEx won not through clever positioning but through relentless execution—99.6% on-time delivery, every day, for decades. Third, culture compounds. The Marine Corps discipline Smith instilled created a workforce that would hold paychecks to keep planes flying. No strategy survives without people willing to execute it.

The capital allocation lessons are equally powerful. Smith understood that in network businesses, you must build ahead of demand. The hub in Memphis, the fleet of planes, the technology infrastructure—all required massive investment before generating returns. This willingness to invest before the market materializes separates empire builders from lifestyle businesses. But he also understood when to buy rather than build, acquiring Flying Tigers for international routes, Caliber for ground networks, TNT for European presence. The discipline to know when organic growth beats acquisition—and vice versa—is rare and valuable.

The mistakes teach as much as the successes. The Zapmail failure in 1985—attempting to build a fax network just as fax machines became ubiquitous—cost hundreds of millions. The lesson: Timing matters more than technology. Being too early is indistinguishable from being wrong. The separation of Express and Ground operations, defended for decades as optimal, proved suboptimal when customers demanded integration. The lesson: Organizational preferences must yield to market realities.

Looking forward, FedEx faces existential questions that mirror broader economic transitions. In an economy increasingly moving from atoms to bits, from physical to digital, from ownership to access, what role does physical delivery play? If 3D printing enables local production, if virtual reality replaces physical presence, if digital goods substitute for physical ones, does FedEx become the railroad of the 21st century—essential once, eventually obsolete?

The answer depends on whether you believe the physical world remains paramount or becomes peripheral. The optimist notes that even digital commerce requires physical fulfillment—every Amazon order needs delivery. The pessimist observes that delivery is becoming commoditized, with value accruing to platforms rather than pipelines. FedEx moves packages, but Amazon owns the customer relationship, and relationships matter more than logistics.

Yet perhaps this framing misses the point. FedEx's value was never just about moving things but about enabling commerce, about creating connections, about making distance irrelevant. Those needs persist even if the methods evolve. The company that pioneered overnight delivery might pioneer instant fulfillment. The network that connected cities might connect digital and physical realms. The infrastructure built for packages might become the backbone for whatever commerce becomes.

The deeper reflection is about American dynamism itself. FedEx represents a particularly American achievement: taking an impossible idea, throwing massive resources at it, and through sheer will and operational excellence, making it reality. This combination of audacity and execution, of vision and discipline, of innovation and industrialization, defined American business in the 20th century. Whether it remains viable in the 21st century—when innovation happens in code rather than concrete, when network effects are digital rather than physical—remains uncertain.

Smith's death in 2025 marks not just the end of a founder but potentially the end of an era. The age of industrial entrepreneurs—Ford, Watson, Walton, Smith—who built physical empires through operational excellence may be yielding to digital innovators who build virtual empires through network effects. FedEx stands at this intersection, a physical company in an increasingly digital world, trying to transform without losing its soul.

The investment implications depend on your view of this transformation. If FedEx successfully evolves from package delivery to commerce enablement, from moving boxes to managing supply chains, from competing on speed to competing on intelligence, then the current valuation represents opportunity. If they remain wedded to physical infrastructure while value migrates to digital platforms, then decline is inevitable.

But perhaps the most important lesson from FedEx transcends financial returns. It's about the power of systematic execution to transform impossible ideas into inevitable realities. Smith didn't just dream of overnight delivery; he built the planes, hired the pilots, created the routes, and delivered the packages. In an era of easy capital and easier pivots, of minimum viable products and rapid iterations, FedEx reminds us that some things require maximum viable commitment and relentless execution.

The ultimate judgment of FedEx won't be its stock price or market share but its impact on human possibility. Before FedEx, the world was bigger, slower, more disconnected. After FedEx, distance shrank, time compressed, and the planet became a single marketplace. They didn't just deliver packages; they delivered the future, overnight, absolutely and positively.

Whether FedEx itself has a future remains uncertain. But the future FedEx enabled—a world where everything is accessible, where distance doesn't determine destiny, where overnight isn't fast enough—is now irreversible. That's the real legacy: not the company Smith built but the world he made possible. In that sense, everyone who expects instant everything is a child of FedEx, whether they know it or not.

The question for investors, entrepreneurs, and society isn't whether FedEx will survive but whether the values it embodied—operational excellence, systematic execution, long-term thinking, and absolute reliability—remain relevant in an age of disruption, pivots, and perpetual beta. The answer to that question will determine not just FedEx's fate but the shape of commerce itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube