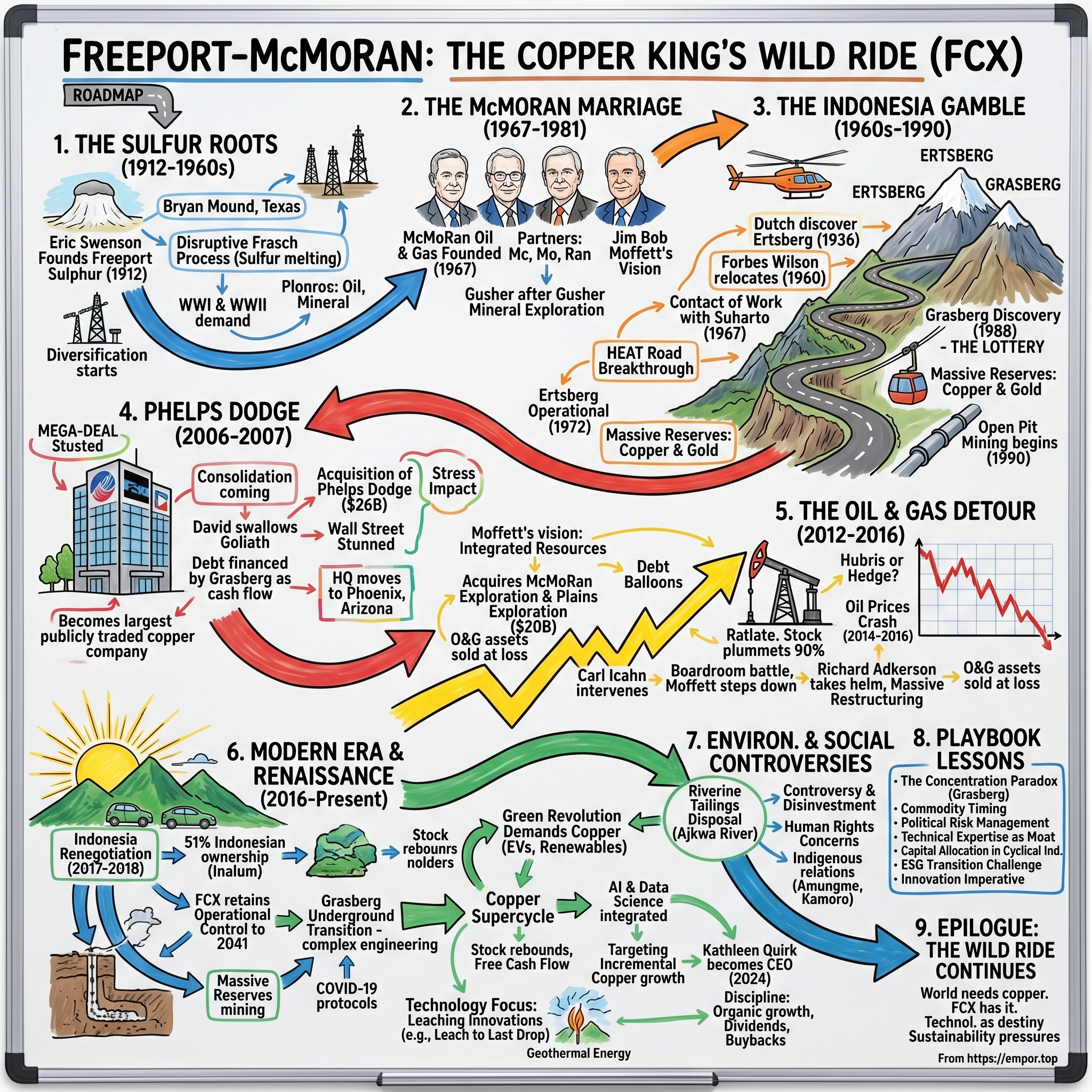

Freeport-McMoRan: The Copper King's Wild Ride

I. Introduction & Episode Roadmap

Picture this: It's 1988, deep in the Indonesian jungle. A helicopter carrying Freeport executives circles above what looks like an ordinary grass-covered mountain. But beneath that green surface lies something extraordinary—a copper and gold deposit so massive it would reshape global mining forever. The geologists on board can barely contain their excitement. They've just discovered Grasberg, which would become the world's largest gold mine and second-largest copper mine. The kicker? This Texas-based company that found it started life mining sulfur from salt domes along the Gulf Coast.

How does a sulfur company founded in 1912 to exploit Texas salt domes end up controlling one of the planet's richest mineral deposits, 10,000 miles away in the mountains of Papua? How does it survive multiple near-death experiences, including a 90% stock price collapse? And why does a copper miner decide to bet $20 billion on oil and gas at exactly the wrong time?

This is the story of Freeport-McMoRan—a company that embodies both the spectacular rewards and terrifying risks of the extractive industries. Today, FCX stands as the world's largest publicly traded copper producer, commanding a $60+ billion market cap and producing roughly 4 billion pounds of copper annually. But getting here required navigating Indonesian politics, environmental controversies, commodity supercycles, and some of the boldest (or most reckless, depending on your view) capital allocation decisions in corporate history. Today, with a market capitalization of approximately $59 billion, FCX stands as one of the world's largest copper miners by volume, producing approximately 4.2 billion recoverable pounds of copper annually. The company owns stakes in 10 copper mines, operates across three continents, and employs approximately 28,500 employees.

What makes this story particularly compelling for investors is the timing. Copper—once just another industrial metal—has become the linchpin of the energy transition. Electric vehicles require four times more copper than conventional cars. Renewable energy systems need millions of tons of it. Data centers powering AI revolutions consume it voraciously. Yet new copper discoveries are rare, and bringing a mine from discovery to production now takes 15-20 years.

We'll explore how a company built on sulfur domes became a copper colossus, why it nearly destroyed itself with oil and gas acquisitions, and what its journey tells us about commodity cycles, political risk, and the future of critical minerals. This is not just a mining story—it's a tale of American industrial ambition, Indonesian realpolitik, and the perpetual tension between resource extraction and environmental stewardship.

Buckle up. We're going from the Texas Gulf Coast to the glaciers of Papua, from boardroom coups to bulldozer miracles, from $5 stock prices to $50 billion valuations. This is Freeport-McMoRan: the copper king's wild ride.

II. The Sulfur Roots: Eric Swenson's Vision (1912-1960s)

The morning of July 12, 1912, in Houston was already sweltering when Eric Pierson Swenson signed the papers incorporating the Freeport Sulphur Company. The 40-year-old banker, eldest son of Swedish immigrant turned cattle baron S.M. Swenson, had a vision that seemed almost absurd: he would revolutionize sulfur mining by melting it underground and pumping it to the surface as liquid.

Eric Pierson Swenson founded Freeport Sulphur Company on July 12, 1912, with a group of investors, to develop sulfur mining at Bryan Mound salt dome, along the US Gulf Coast. The target was Bryan Mound, a salt dome formation near the Texas coast where sulfur deposits lay trapped beneath quicksand and toxic hydrogen sulfide gas—conditions that had killed previous attempts at conventional mining.

Swenson's ace in the hole was the Frasch process, a technique for extracting sulfur that had just come off patent protection in 1908. The Frasch process was a disruptive innovation for the automated mining of previously inaccessible sulfur deposits at a cost lower than that of established mines, where manual labor gained the mineral under the most appalling conditions. The process worked by pumping superheated water down into sulfur deposits, melting them in place, then using compressed air to force the molten sulfur to the surface. It was elegant, efficient, and eliminated the need for miners to descend into hellish underground chambers.

But first, Swenson needed infrastructure—and workers. In November 1912, Freeport, Texas was established to house workers and serve as a port for Houston, rivaling Galveston and Corpus Christi. The new town, built from scratch on the marshy Gulf Coast, would become both company town and shipping hub, complete with houses, stores, and docks capable of handling oceangoing vessels.

The early days were brutal. In 1913, operations proved unsteady as engineers struggled to maintain the precise temperatures and pressures needed for the Frasch process. Equipment failures were common. The caustic environment corroded pipes and valves. Workers battled mosquitoes, hurricanes, and the ever-present danger of hydrogen sulfide exposure. Local skeptics dubbed it "Swenson's Folly."

Yet by 1914, Freeport Sulphur was producing commercial quantities of sulfur purer than anything previously available on the market—99.5% pure, compared to the 90% purity of Sicilian sulfur that had dominated global markets. The timing couldn't have been better. World War I created massive demand for sulfuric acid (for explosives) just as Freeport hit its stride.

The 1920s brought expansion and innovation. Freeport engineers refined the Frasch process, developing better drilling techniques and more efficient heating systems. They expanded to other salt domes along the Gulf Coast—Hoskins Mound, Bryan Heights, and eventually Grand Ecaille in Louisiana, which would become one of the world's most productive sulfur deposits.

By the 1930s, Freeport Sulphur had grown into an industrial powerhouse. The company supplied sulfur for everything from fertilizers to rubber vulcanization, from paper production to petroleum refining. During World War II, Freeport again answered the nation's call, dramatically increasing production to meet wartime demands for explosives and synthetic rubber.

The post-war era brought new challenges and opportunities. As global competition increased and easy sulfur deposits became scarcer, Freeport's leadership recognized the need to diversify. They began exploring other mineral opportunities, acquiring potash operations in New Mexico and investigating copper deposits that geologists claimed existed in far-flung places like Cuba and Indonesia.

By 1960, Freeport Sulphur dominated the global sulfur trade, controlling roughly 10% of world production. The company that Eric Swenson built on a sweaty Houston morning had become a Fortune 500 corporation, with operations spanning the Gulf Coast and revenues exceeding $100 million annually. But sulfur, the foundation of its fortune, was becoming a commodity under pressure. Petroleum refining increasingly produced sulfur as a byproduct, threatening Freeport's core business model.

The board of directors, now led by Langbourne Williams Jr., made a fateful decision: Freeport would transform itself from a sulfur company into a diversified natural resources company. They had the capital, the expertise in handling difficult extraction challenges, and most importantly, the appetite for risk that comes from turning Texas swampland into gold.

Little did they know that their next gamble—a copper mountain in the jungle of Netherlands New Guinea (soon to be Indonesia)—would make their sulfur operations look like a neighborhood lemonade stand. The boy from Texas who melted rocks was about to meet a mountain in Indonesia that would redefine the company forever.

III. The McMoRan Marriage & Transformation (1967-1981)

In 1967, McMoRan Oil and Gas Company was founded by three partners: William Kennon McWilliams Jr. ("Mc"), James Robert (Jim Bob) Moffett ("Mo"), who were both petroleum geologists, and Mack Rankin ("Ran"), a specialist in land-leasing and sales operations. The three men, whose combined initials gave the company its name, set up shop in New Orleans with a simple premise: find oil and gas in the Gulf of Mexico using cutting-edge seismic technology and geological expertise.

Jim Bob Moffett was the dynamo of the trio. A Louisiana native with a geology degree from the University of Texas, Moffett combined technical brilliance with promotional flair that bordered on evangelical. At industry conferences, he didn't just present data—he sold dreams. His colleagues joked that Jim Bob could convince you there was oil under your grandmother's rocking chair, and then actually find it.

That same year, 1967, halfway around the world, Freeport confirmed the Dutch discovery of the Ertsberg copper deposit in Indonesia. The timing was extraordinary. Indonesia had just emerged from the chaos of Sukarno's regime, with new president Suharto eager to attract Western investment. Freeport negotiated one of the first foreign investment contracts in Suharto's "New Order" Indonesia—a 30-year agreement that would prove both lucrative and controversial.

Back in New Orleans, McMoRan was hitting gusher after gusher in the Gulf. By the mid-1970s, the company had grown from three guys with a dream to a significant regional player with proven reserves and steady cash flow. But Moffett saw bigger opportunities. He watched the commodity markets with the eye of a poker player counting cards. Oil was good, but what about minerals? What about copper?

The late 1970s brought the two companies into each other's orbit. Freeport, despite its Indonesian success, faced challenges. The Ertsberg mine required massive capital investments, and sulfur revenues were declining. McMoRan, flush with petrodollars but concerned about the volatility of energy markets, sought diversification. Investment bankers began whispering about synergies.

The courtship was vintage Jim Bob Moffett—part seduction, part hostile takeover threat. He saw in Freeport not just a mining company but a platform for building a global natural resources empire. The Freeport board, initially skeptical of this brash Texan, gradually warmed to his vision. Moffett promised to bring entrepreneurial energy to what some viewed as a stodgy industrial company.

In 1981, McMoRan merged with Freeport Minerals, formerly Freeport Sulphur, to form Freeport-McMoRan. The deal, valued at approximately $750 million, created an unusual hybrid: a company with sulfur operations in Louisiana, oil and gas platforms in the Gulf of Mexico, and a copper mine in the mountains of Indonesia. Wall Street analysts struggled to categorize it. Was it an energy company? A mining company? Moffett's answer: "We're a natural resources company, period."

The merger brought together two radically different corporate cultures. Freeport's engineers, accustomed to methodical planning and conservative projections, clashed with McMoRan's wildcatters, who thrived on risk and moved at the speed of a drilling rig. Board meetings became legendary for their intensity, with Moffett's booming voice dominating discussions about everything from copper grades to completion fluids.

One early initiative showcased the new company's ambitions: the Jerritt Canyon gold joint venture in Nevada. Partnering with other investors, Freeport-McMoRan developed what would become one of North America's largest gold mines. It was a statement of intent—this wasn't your grandfather's sulfur company anymore.

But the real transformation was happening in Indonesia. Under Moffett's leadership, Freeport-McMoRan poured money into expanding Ertsberg, building infrastructure that defied belief. They constructed a 115-kilometer road through some of the world's most challenging terrain, built a port at Amamapare, and installed an aerial tramway system to move ore down the mountain. The price tag ran into hundreds of millions, but Moffett insisted the geology justified the investment.

The 1981 merger marked more than a corporate combination—it represented a philosophical shift. The company founded to extract sulfur from Texas salt domes had become a globe-spanning enterprise with assets on three continents. Jim Bob Moffett, now CEO of the combined entity, had bigger plans still. He spoke of Freeport-McMoRan becoming the "Exxon of mining," a resources giant that could compete with anyone.

Critics called him reckless. Supporters called him visionary. Both would be proven right in the years ahead. As 1981 drew to a close, Freeport-McMoRan's geologists in Indonesia sent back reports that made even Moffett's jaw drop. Near the Ertsberg mine, they'd found something extraordinary—a grass-covered mountain that might contain more copper and gold than anyone had imagined possible.

IV. The Indonesia Gamble: Finding Ertsberg & Grasberg (1960s-1990)

In 1936, Dutch geologist Jean Jacques Dozy was part of an expedition climbing the glaciers of Netherlands New Guinea's Jayawijaya Mountains when he spotted something extraordinary: a black outcropping on a mountainside that looked nothing like the surrounding limestone. Dozy took samples and later confirmed his suspicion—it was copper ore, incredibly rich copper ore. He named it "Ertsberg," meaning "ore mountain" in Dutch. Then World War II erupted, Dozy's discovery gathered dust in colonial archives, and the mountain kept its secret for another two decades.

Fast forward to 1960. Forbes Wilson, a Freeport director and exploration enthusiast, was reading a geological report on Netherlands New Guinea when he stumbled upon Dozy's notes. Wilson, an amateur mountaineer himself, was electrified. He convinced the Freeport board to fund an expedition. In 1960, a team led by geologist Forbes Wilson Jr. (the director's son) helicoptered into the Jayawijaya Mountains to relocate Dozy's discovery.

What they found exceeded all expectations. The Ertsberg deposit contained ore grading 2.5% copper—extraordinarily rich by industry standards. But developing it would require building infrastructure in one of the most remote, challenging environments on Earth. The nearest coast was 70 miles away through dense jungle. The deposit sat at 12,000 feet elevation in a region that received 20 feet of rain annually. Local Amungme and Kamoro peoples had lived in the area for millennia but had minimal contact with the outside world.

The politics were equally treacherous. In 1963, Netherlands New Guinea became part of Indonesia under UN administration. By 1967, when Freeport signed its Contract of Work with the new Suharto government, the company was betting hundreds of millions on a country that had just emerged from political chaos, in a region with active separatist movements, to develop a mine accessible only by helicopter.

Construction began in 1969 and immediately faced seemingly impossible challenges. Engineers had to build a road from the coast to the mountains—except "road" doesn't capture the insanity of the project. They were essentially carving a path up a 12,000-foot wall of jungle-covered rock, crossing rivers that could rise 20 feet in an hour during rainstorms.

The project's savior came from an unexpected source. In 1970, an Indonesian bulldozer operator named Hairudin was working on a particularly treacherous section when he suggested an alternative route his grandfather had told him about—an old tribal path called the HEAT road (named after the project's Heavy Equipment Access Trail). Hairudin's route saved an estimated $20 million and six months of construction time. Without it, the project might have collapsed.

The tramways were needed to move people, supplies and ore because a 2,000-foot cliff separates the Ertsberg mine (at 12,000 feet elevation) from the mill (at 10,000 feet). Moving copper concentrate from that mill to the shipping port required installation of a 109-kilometre (68 mi) slurry pipeline—then the world's longest. Mine construction and startup cost about US$200 million.

By 1972, Ertsberg was operational, but the mine's early financial performance was disappointing. Depressed copper prices and high operating costs kept profits marginal during the 1970s. Critics questioned whether Freeport had made an expensive mistake. Then came 1988—and everything changed.

Freeport geologists had been exploring around Ertsberg when they identified an anomaly about three kilometers away. It was a grass-covered mountain the locals called "Grasberg." Initial drilling results were promising. Then they were shocking. Then they were almost unbelievable.

Grasberg wasn't just a copper deposit—it was THE copper deposit. Initial estimates suggested reserves of 2.5 billion tons grading 1.1% copper and 1.0 grams per ton gold. To put that in perspective: Grasberg contained more gold than most gold mines and more copper than most copper mines. It was, quite literally, a mountain of money.

Jim Bob Moffett flew to Indonesia to see the drilling results himself. The geologist presenting the data was nervous, worried Moffett would think he was exaggerating. Instead, Moffett's response became company legend: "Boys, we just won the lottery. Now let's figure out how to cash the ticket."

Developing Grasberg required another massive capital commitment. Freeport-McMoRan invested over $1 billion to build new processing facilities, expand the mill capacity, and develop the open pit. The Grasberg mine would become the world's largest gold mine and second-largest copper mine.

The social and environmental challenges were immense from the start. The mine's tailings—waste rock and processing residuals—were deposited into the river system, a practice that would generate decades of controversy. Local indigenous communities saw their traditional lands transformed by industrial development. The Indonesian military established a significant presence to protect the operation, leading to human rights concerns that would dog the company for decades.

By 1990, Grasberg began open-pit mining, and the numbers were staggering. The mine was producing over 400,000 tons of ore per day. The gold production alone—essentially a byproduct of copper mining—made Grasberg one of the world's largest gold mines. Freeport-McMoRan had transformed from a mid-sized resources company into a mining giant.

The Indonesia gamble had paid off beyond anyone's wildest dreams. But it had also tied Freeport's fate to one of the world's most politically complex countries, in one of its most contested regions. The company that started mining sulfur in Texas swamps now operated a mountain-moving operation in Indonesian glaciers, generating billions in revenue but also attracting scrutiny from environmental groups, human rights organizations, and indigenous advocates worldwide.

As the 1990s progressed, Grasberg's riches continued to flow, but so did the challenges. The company found itself walking an increasingly precarious tightrope between massive profitability and mounting controversy. The stage was set for the next chapter in Freeport's evolution: using Grasberg's cash flow to make an even bigger bet on becoming the world's copper king.

V. The Phelps Dodge Mega-Deal (2006-2007)

The scene at the Waldorf Astoria in November 2006 looked more like a gathering of war generals than mining executives. In one suite, Freeport-McMoRan's Jim Bob Moffett and his lieutenants pored over spreadsheets showing copper prices at $3.50 per pound—historic highs. In another, the board of Phelps Dodge, a 170-year-old mining institution, debated their company's future. Between them, investment bankers from Morgan Stanley and Goldman Sachs shuttled proposals like diplomatic envoys.

The backdrop was a copper market gone wild. China's industrialization had sent demand soaring. Supply couldn't keep pace. Every major miner knew consolidation was coming—the question was who would eat whom.

Phelps Dodge itself was already in play. The company, founded in 1834 and named after its founders Anson Greene Phelps and William E. Dodge, had built the American Southwest's copper industry. Its Morenci mine in Arizona was legendary. But Phelps Dodge had just launched its own hostile bid for two Canadian miners, Inco and Falconbridge, worth $40 billion combined. If successful, it would create the world's largest mining company.

Moffett saw an opening. If Phelps Dodge was willing to pay $40 billion for Canadian nickel assets, what was Phelps Dodge itself worth? He called Richard Adkerson, Freeport's CFO and soon-to-be heir apparent: "Dick, what if we bought them instead?"

The math was audacious. Phelps Dodge had a market cap of about $18 billion. With a typical 40% premium, Freeport would need to offer $25-26 billion. Freeport's own market cap? Just $16 billion. David would be swallowing Goliath.

On November 19, 2006, FCX announced its $26 billion acquisition of Phelps Dodge. The offer was structured as $88 cash plus 0.67 FCX shares per Phelps Dodge share—a 33% premium to Phelps Dodge's closing price. Wall Street was stunned. How could Freeport finance this?

The answer lay in Grasberg's cash-generating machine and copper's supercycle dynamics. Freeport arranged $17.5 billion in bridge financing from JPMorgan and Merrill Lynch—one of the largest acquisition financings ever. The banks were essentially betting that copper prices would stay elevated long enough for Freeport to pay down the debt with cash flow.

Phelps Dodge's board initially resisted. This was a company that had survived the Great Depression, two World Wars, and countless commodity cycles. Being acquired by a relative upstart led by a flamboyant Texan felt like sacrilege to some directors. But Moffett's offer was too rich to refuse, especially given the risks in Phelps Dodge's own Canadian adventure.

The negotiations revealed fascinating dynamics. Phelps Dodge CEO Steve Whisler had actually approached Moffett months earlier about a potential partnership in Indonesia. Moffett had demurred then, but kept thinking about Phelps Dodge's assets. When Whisler called to discuss Freeport's bid, Moffett reportedly said, "Steve, you opened this door when you came to talk about Grasberg. Now I'm walking through it."

The deal's complexity was staggering. Freeport had to assume Phelps Dodge's obligations, including environmental liabilities at century-old mines. Regulatory approvals were needed in multiple countries. The financing required copper prices to stay above $2.50 per pound for the math to work—if prices collapsed, Freeport would be bankrupt.

Some shareholders revolted. Hedge fund Atticus Capital, owning 5% of Phelps Dodge, publicly opposed the deal, arguing the company was being sold too cheaply at the peak of the copper cycle. Carl Icahn, smelling opportunity, began accumulating shares in both companies, threatening a proxy fight.

But Moffett had momentum. He toured Phelps Dodge's operations, charming miners and engineers with his technical knowledge and folksy manner. He promised no layoffs, pledged to maintain Phelps Dodge's Phoenix headquarters alongside Freeport's, and spoke reverently of Phelps Dodge's heritage. "We're not acquiring a company," he told employees. "We're joining two families."

On March 19, 2007, the deal closed, creating the world's largest publicly traded copper company with 25,000 employees. The combined company controlled approximately 10% of global copper production, with assets spanning Arizona to Indonesia.

The corporate headquarters was moved from New Orleans, Louisiana to Phoenix, Arizona, a symbolic gesture honoring Phelps Dodge's legacy. But make no mistake—this was Moffett's empire now.

The timing initially looked brilliant. Copper prices continued rising, hitting $4.00 per pound in 2008. Freeport's stock reached an all-time high of $60 per share. The debt was being paid down ahead of schedule. Moffett was hailed as a visionary who had pulled off the deal of the decade.

Then came the 2008 financial crisis.

Copper prices crashed to $1.25 per pound. Freeport's stock plummeted to $12. The company that had bet everything on copper's supercycle suddenly faced existential crisis. Critics who had called the Phelps Dodge deal reckless now seemed prophetic.

But Freeport survived, barely. Emergency cost cuts, asset sales, and eventually recovering copper prices pulled the company through. By 2011, with copper back above $4.00, the Phelps Dodge acquisition looked brilliant again. The combined company was generating over $5 billion in annual EBITDA.

The Phelps Dodge deal transformed Freeport from an Indonesia-dependent operator into a globally diversified copper giant. It owned crown jewel assets on three continents, from Morenci's massive open pit to Grasberg's mountain of gold. Moffett had achieved his dream of building a resources major.

But success bred hubris. As copper prices soared and cash poured in, Moffett began eyeing his next transformation. Why just be a copper company when you could be an integrated natural resources giant? The stage was set for Freeport's most controversial chapter yet—a $20 billion bet on oil and gas that would nearly destroy everything Moffett had built.

VI. The Oil & Gas Detour: Hubris or Hedge? (2012-2016)

Jim Bob Moffett stood before Freeport-McMoRan's board in December 2012, his voice carrying the evangelical fervor that had defined his career. Oil was trading at $110 per barrel. Natural gas, though depressed at $3.50 per thousand cubic feet, was projected to soar as America's shale revolution transformed global energy markets. Copper, meanwhile, faced headwinds from slowing Chinese growth. Moffett's pitch was simple: "Gentlemen, we started as an oil and gas company. It's time to come home."

On December 5, 2012, the company announced agreements to acquire affiliated companies McMoRan Exploration Company and Plains Exploration & Production Company for a total enterprise value of over $20 billion. The deals would transform Freeport from a pure-play copper miner into a diversified natural resources company with significant oil and gas exposure in the Gulf of Mexico.

The logic, as Moffett explained it, was compelling. First, it was a natural hedge—when oil prices rose, copper mining costs (heavily dependent on energy) increased, but now Freeport would benefit from both sides. Second, Moffett knew these assets intimately. McMoRan Exploration was literally his baby, a company he'd remained involved with even after focusing on Freeport. Plains Exploration, run by his protégé James Flores, owned prime Gulf of Mexico acreage. Third, the Gulf's ultra-deepwater prospects could be game-changers, with discoveries potentially worth tens of billions.

Wall Street's reaction was swift and brutal. Freeport's stock dropped 16% on announcement day. Analysts were apoplectic. "They're buying cyclical assets at the peak of the cycle with other cyclical assets at the peak of their cycle," one analyst told the Financial Times. "It's doubling down on commodity risk, not hedging it."

The financing was complex. Freeport paid $3.4 billion for Plains Exploration and $2.1 billion for McMoRan Exploration, using a combination of cash and stock. But the total enterprise value exceeded $20 billion when including assumed debt and future development costs. The company's net debt ballooned from $3.5 billion to over $20 billion.

The governance issues were even more problematic. Moffett was co-chairman of McMoRan Exploration—a flagrant conflict of interest. Several Freeport board members had ties to the acquired companies. Institutional Shareholder Services called it "one of the most troubling related-party transactions in recent memory."

Lawsuits flew immediately. Shareholders accused Moffett of self-dealing, using Freeport's balance sheet to bail out his failing energy ventures. The Louisiana Teachers' Retirement System, a major shareholder, sued to block the deal. They noted that McMoRan Exploration had been struggling, with its stock down 75% from its peak. Why was Freeport paying a premium for distressed assets?

Moffett fought back with characteristic pugnacity. At the shareholder meeting to approve the deal, he delivered an impassioned speech about American energy independence, the Gulf of Mexico's untapped potential, and Freeport's unique ability to develop complex resources. "The same people who said we were crazy to develop Grasberg are saying we're crazy now," he thundered. "We've been right before. We'll be right again."

The deals were approved, barely. But almost immediately, everything went wrong.

Oil prices began sliding in June 2014, falling from $115 to $75 by year-end. Natural gas remained stubbornly depressed. Then came the knockout blow: in November 2014, Saudi Arabia announced it would maintain production despite falling prices, effectively declaring war on U.S. shale producers. Oil crashed to $26 per barrel by February 2016.

Freeport's oil and gas assets, which were supposed to generate billions in cash flow, instead became cash incinerators. The ultra-deepwater projects required hundreds of millions in development capital just to maintain optionality. The company's debt load, manageable at $100 oil and $4 copper, became crushing at $30 oil and $2 copper.

By late 2015, Freeport-McMoRan was in full crisis mode. The stock had fallen 90% from its peak to under $4 per share. Credit default swaps implied a 50% chance of bankruptcy. The company that had survived the 2008 financial crisis now faced an even graver threat—one entirely of its own making.

Enter Carl Icahn.

The activist investor, who had been circling Freeport since the Phelps Dodge deal, now pounced. By February 2016, Icahn owned 8.5% of the company and was demanding board seats. His message was blunt: Moffett had to go, the oil and gas assets had to be sold, and the company needed to return to its copper roots.

The boardroom battle was vicious. Moffett, who had built Freeport over 35 years, fought to maintain control. But with the stock in free fall and creditors growing nervous, he had little leverage. In October 2015, Moffett announced he would step down as CEO while remaining chairman—a face-saving compromise that fooled no one about who had really won.

Richard Adkerson, the careful CFO to Moffett's swashbuckling CEO, took the helm with a clear mandate: save the company. He immediately launched a massive restructuring. Non-core assets were sold at fire-sale prices. The oil and gas properties were packaged and sold to Anadarko Petroleum for $2 billion—a fraction of what Freeport had paid. Capital expenditures were slashed. Thousands of employees were laid off.

The company also had to renegotiate its Indonesian operations, with the government demanding increased ownership as Freeport desperately needed to maintain cash flow from Grasberg. It was negotiating from weakness, and everyone knew it.

By mid-2016, Freeport had reduced debt by $10 billion and cut costs by $2 billion annually. The company survived, but it was a shadow of its former self. The oil and gas adventure had cost shareholders over $30 billion in destroyed value.

The lessons were stark. Commodity diversification sounds good in theory but can be disastrous when all commodities collapse simultaneously. Related-party transactions, no matter how well-intentioned, create conflicts that markets punish severely. And even the most successful executives can fall victim to hubris when they confuse a bull market for genius.

As 2016 drew to a close, copper prices began recovering, thrown a lifeline by Chinese stimulus and supply disruptions. Freeport-McMoRan, bloodied but not beaten, began its long climb back. But first, it had to resolve its Indonesian problem once and for all—a negotiation that would determine whether Grasberg remained a crown jewel or became a stranded asset.

VII. Modern Era: The Indonesia Renegotiation & Copper Renaissance (2016-Present)

Richard Adkerson landed in Jakarta in January 2017 knowing this might be his last trip to Indonesia as CEO of a company that controlled Grasberg. The Jokowi government had drawn a line in the sand: comply with new mining regulations requiring 51% Indonesian ownership, or lose your export permits. For a company still reeling from its oil and gas disaster, losing Grasberg would be fatal.

The standoff had been building since 2009 when Indonesia passed a mining law requiring foreign companies to divest majority control to Indonesian entities. Freeport had negotiated extensions and exceptions for years, but patience had run out. In January 2017, Indonesia banned Freeport from exporting copper concentrate, effectively shutting down operations that generated over 30% of the company's revenue.

The negotiations were kabuki theater mixed with genuine brinkmanship. Indonesia held the leverage—Grasberg was physically in their territory, and nationalist sentiment was rising. But Freeport had cards too: the technical expertise to operate one of the world's most complex mines, billions in planned investment for the underground transition, and relationships with international arbitration courts.

For six months, Grasberg operated at reduced capacity while negotiators shuttled between Jakarta, Phoenix, and New York. The Indonesian government wanted 51% ownership, but at what price? Freeport wanted operational control and economic certainty, but how much sovereignty would it sacrifice?

The breakthrough came in August 2017. Freeport agreed to give Indonesia a majority stake in its Grasberg mine. The deal's brilliance lay in its structure: Indonesia would get 51% ownership through state-owned mining company Inalum, but Freeport would retain operational control through 2041 and receive economic benefits approximating 50% ownership through creative structuring.

The price tag was $3.85 billion for the 51% stake, but Indonesia would pay it over time using dividends from the mine itself. Freeport also agreed to build a new $3 billion smelter in Indonesia, creating domestic value-addition and jobs. In exchange, Freeport got export permit certainty and extension of operating rights through 2041—crucial for justifying the underground development investment.

By December 2018, the divestiture was completed, ending a two-year saga that had threatened Freeport's existence. Adkerson had pulled off what seemed impossible: keeping Grasberg economically viable while satisfying Indonesian sovereignty demands.

But the real challenge was just beginning. In 2019, the Grasberg open pit closed after producing 27 billion pounds of copper and 46 million ounces of gold. The transition to underground mining was one of the most complex engineering projects in mining history.

Imagine taking one of the world's largest open pits—a hole visible from space—and moving operations entirely underground. Three separate underground mines (Grasberg Block Cave, Deep Mill Level Zone, and Big Gossan) had to be developed simultaneously. Over a multi-year investment period, PT-FI successfully commissioned these three large-scale underground mines, requiring $7 billion in capital investment.

The technical challenges were staggering. Block cave mining, where you essentially create a controlled collapse of ore that funnels down to collection points, had never been done at this scale and altitude. Ventilation systems had to handle the heat from rock under pressure. Transportation systems had to move 200,000 tons of ore daily through underground tunnels.

COVID-19 nearly derailed everything. In March 2020, with the underground transition at its most critical phase, Indonesia locked down. Freeport had to create bubble protocols, charter special flights, and negotiate with governments to keep essential workers on site. Production dropped 40% in the second quarter of 2020.

But by late 2020, the underground mines were ramping up ahead of schedule. Then copper markets delivered an unexpected gift: the green revolution.

Electric vehicles require 4-5 times more copper than conventional cars. Wind turbines need 3-5 tons each. Solar panels, grid storage, charging infrastructure—everything in the green economy needs copper. Suddenly, copper wasn't just an industrial metal; it was the critical mineral for humanity's energy transition.

Copper prices soared from $2.50 per pound in March 2020 to over $4.50 by 2021. Freeport's stock, which had languished around $10, shot past $40. The company that nearly went bankrupt in 2016 was now generating over $6 billion in annual free cash flow.

Adkerson, vindicated but cautious, refused to repeat past mistakes. Instead of acquisitions or diversification, Freeport focused on technology and innovation. The company achieved its initial incremental annual run rate target of approximately 200 million pounds of copper through leaching innovations. Incremental copper production from these initiatives totaled 214 million pounds for the year 2024

By 2022, all three underground mines at Grasberg were fully operational, making Freeport the only company to successfully complete such a massive underground transition at this scale.

The company also became more disciplined with capital. Quarterly cash dividends of $0.15 per share, consisting of a $0.075 base dividend and a $0.075 variable dividend aligned with FCX's performance-based payout framework, replaced the boom-bust dividend policies of the past. Share buybacks were measured, debt reduction prioritized. The cowboys had become accountants.

Technology became central to the company's growth strategy. By using geothermal energy, the project aims to generate clean, industrial-scale heat to enable the recovery over time of billions of pounds of residual copper through the company's Leach to the Last Drop initiative from already mined material previously considered unrecoverable. The project could increase copper recovery by 25 million pounds or more annually.

Incremental copper production from these initiatives totaled 50 million pounds in fourth-quarter 2024 and 214 million pounds for the year 2024. The company identified 38 billion pounds of contained copper in stockpiles that were previously deemed unrecoverable. Looking ahead, the company is targeting 300-million pounds by the end of 2025 and 400-million pounds by late 2026, with a long-term goal of 800-million pounds a year. "We have got 39-billion pounds of copper that has previously been placed that we've considered waste, and we're trying to get as much of that as we can. If we get 20% of it, that's a huge gain for us," CEO Kathleen Quirk said.

The leadership transition in 2024 marked another turning point. Kathleen L. Quirk was appointed as President and Chief Executive Officer effective at the annual meeting of shareholders on June 11, 2024. Quirk joined Freeport-McMoRan in 1989, becoming Chief Financial Officer and Executive Vice-President on December 10, 2003. Her ascension represented continuity—she had been Adkerson's right hand for decades—but also evolution, bringing a more collaborative, technology-focused approach to leadership.

Under Quirk's leadership, Freeport has maintained its focus on organic growth rather than acquisitions. Quirk emphasized that M&A is not central to Freeport's strategy. "We don't see, as part of our strategy, getting involved in a competitive auction process or something on that order," she stated. Instead, the company will focus on opportunities where it can generate synergies and leverage its technical capabilities to add value to existing operations.

The modern Freeport-McMoRan is a study in contrasts with its past. Where Moffett bet billions on unproven assets, Quirk focuses on extracting value from existing resources. Where the company once chased diversification, it now embraces its identity as a pure-play copper producer. Where it once courted controversy, it now emphasizes ESG metrics and stakeholder engagement.

VIII. Environmental & Social Controversies

The Ajkwa River system in Papua, Indonesia, carries an unusual burden. Every day, approximately 200,000 tons of tailings from the Grasberg mine flow into its waters—a practice that would be illegal in the United States, Canada, or Australia. This riverine tailings disposal system has been Freeport-McMoRan's original sin, a controversy that has shadowed the company for five decades and crystallized the tensions between resource extraction and environmental protection.

The scale is staggering. Since operations began, Grasberg has deposited over 2 billion tons of tailings into the river system. The waste has created a 230-square-kilometer deposition area in the lowlands, transforming rainforest into what critics call a "moonscape." Freeport argues this is the only viable option given the mine's remote location, extreme rainfall, and seismic activity that make conventional tailings dams impossible. Environmental groups call it ecocide.

The Norwegian Government Pension Fund, the world's largest sovereign wealth fund, divested from Freeport in 2006 specifically over environmental concerns. Their ethics council concluded that investing in Freeport constituted "an unacceptable risk of the Fund contributing to severe environmental damage." The fund has never reversed this decision.

But environmental damage is only part of the controversy. The human rights situation around Grasberg has been equally contentious. The mine sits in Papua, a region with an active independence movement that views the Indonesian government as an occupying force. Freeport, as the region's largest taxpayer and employer, became inextricably linked with Indonesian sovereignty.

For decades, Freeport paid the Indonesian military and police for security services—payments that critics argued made the company complicit in human rights abuses. Reports from human rights organizations documented killings, torture, and disappearances around the mine site. While Freeport maintained these were actions of Indonesian forces beyond their control, activists argued the company's payments created a moral hazard.

The 1996 Grasberg riots brought these tensions to a head. Local tribespeople, frustrated by environmental damage and lack of economic benefits, rioted and destroyed millions of dollars of equipment. The Indonesian military's response was brutal, with reports of villages burned and civilians killed. Freeport found itself caught between its need for security and accusations of enabling repression.

Relations with indigenous communities have been consistently fraught. The Amungme and Kamoro peoples, who consider the mountains around Grasberg sacred, have seen their traditional lands transformed by industrial mining. While Freeport has created jobs and development programs, critics argue these benefits are dwarfed by cultural disruption and environmental degradation.

A 2005 New York Times investigation revealed that between 1998 and 2004, Freeport paid Indonesian military and police units approximately $20 million in direct payments, beyond official security costs. The company defended these as necessary for protecting employees and operations in a challenging environment, but the revelations damaged Freeport's reputation and led to SEC investigations.

The company has attempted various remediation efforts. It established the Freeport Partnership Fund for Community Development, committing 1% of annual revenues to local development. It built schools, hospitals, and infrastructure in Papua. It created job training programs prioritizing local hiring. Yet critics argue these efforts are insufficient given the scale of extraction and impact.

Climate change has added new complexity. Mining operations at Grasberg consume enormous amounts of energy, contributing significantly to greenhouse gas emissions. The transition to underground mining actually increased energy intensity. While Freeport has set emission reduction targets and invested in renewable energy, the fundamental carbon footprint of moving millions of tons of rock remains massive.

Water usage presents another challenge. The mine consumes and diverts enormous quantities of water in a region where many communities lack access to clean drinking water. The contrast between industrial-scale water use and local scarcity has become another flashpoint for criticism.

More recently, labor relations have emerged as a concern. Strikes at Grasberg and South American operations have highlighted tensions over wages, safety, and working conditions. A 2017 strike at Grasberg lasted months, costing the company hundreds of millions in lost production and raising questions about its stakeholder management.

The regulatory landscape has also shifted. Indonesia's environmental standards have tightened, though enforcement remains inconsistent. International initiatives like the Extractive Industries Transparency Initiative have increased pressure for disclosure. ESG-focused investors now scrutinize mining companies' environmental and social practices more closely than ever.

Freeport has responded with increased transparency, publishing detailed sustainability reports and submitting to third-party audits. The company points to its economic contributions—over $70 billion in direct benefits to Indonesia since 1992—as evidence of positive impact. It highlights improvements in tailings management, even if the fundamental practice continues.

Yet the controversies persist. In 2023, environmental groups filed new complaints about tailings disposal. Indigenous rights organizations continue to challenge the legitimacy of mining on ancestral lands. As global standards for responsible mining evolve, Freeport's practices—particularly at Grasberg—increasingly appear anachronistic.

The paradox is that Grasberg's copper is essential for the green transition, yet its extraction methods contradict environmental values. This tension—between the materials needed for a sustainable future and the impacts of obtaining them—epitomizes the challenges facing the mining industry and society more broadly.

IX. Playbook: Business & Investing Lessons

1. The Concentration Paradox: When One Asset Defines a Company

Grasberg has been both Freeport's greatest strength and its existential vulnerability. The mine generates roughly 30% of revenues but represents far more in terms of strategic value—it's irreplaceable. This concentration creates a paradox: spectacular returns when things go right, catastrophic risk when they don't.

The lesson isn't to avoid concentration, but to understand its implications. Concentrated bets can create extraordinary value—Grasberg has generated over $100 billion in revenue. But they require exceptional risk management, political sophistication, and the financial strength to survive crises. For investors, companies with single-asset concentration offer leveraged exposure to specific themes but require constant vigilance about operational, political, and regulatory risks.

2. Commodity Timing: The Impossibility and Necessity of Market Timing

Freeport's history is a graveyard of timing decisions. The Phelps Dodge acquisition looked brilliant at $4 copper, disastrous at $1.50, and brilliant again at $4.50. The oil and gas purchases were perfectly timed—if you wanted to buy at the absolute peak. The lesson isn't that timing is impossible, but that survival is paramount.

The playbook: Build balance sheets that can survive the bottom of the cycle. Never assume current prices are sustainable. Diversification within commodities often provides false comfort—correlations approach 1 during crises. Most importantly, resist the intoxication of high prices. More value has been destroyed at the top of commodity cycles than at any other time.

3. Political Risk: The Hidden Asset in Emerging Markets

Freeport's Indonesia experience offers a masterclass in political risk management. The company survived regime change (Suharto to democracy), regulatory overhauls, forced divestments, and export bans. How? By making itself indispensable. Grasberg generates billions in tax revenue, employs thousands, and requires technical expertise Indonesia lacks.

The strategy: Create mutual dependence, not just extraction. Invest in local capacity building. Accept that the terms will get worse over time—plan for it. And crucially, understand that political risk isn't just about expropriation; it's about the slow erosion of economics through changing fiscal terms, local content requirements, and social obligations.

4. Technical Expertise as Moat

Block cave mining at 14,000 feet. Transitioning from open pit to underground without stopping production. Processing complex mineralogy with multiple metals. These aren't just operations; they're technical moats. Freeport's real competitive advantage isn't its ore bodies—others have similar geology. It's the ability to extract value from seemingly impossible situations.

For investors, this suggests looking beyond reserves to technical capability. Can the company actually extract the ore economically? Do they have the expertise to handle increasing complexity as ore grades decline? Technical excellence creates bargaining power with governments, pricing power with customers, and resilience during downturns.

5. Capital Allocation in Cyclical Industries

The Moffett era demonstrated both the best and worst of capital allocation. Best: Using high copper prices to make transformative acquisitions (Phelps Dodge). Worst: Using high commodity prices to buy other commodities at peak prices (oil and gas). The difference? The first enhanced existing competitive advantages; the second was diversification theater.

The framework: Growth capital should enhance core competitive positions. Diversification should be countercyclical, not procyclical. Return cash to shareholders when prices are high rather than empire-building. And always ask: if commodity prices fall 50%, what happens to this investment?

6. The ESG Transition Challenge

Freeport embodies the ESG paradox of mining. Its copper enables electric vehicles and renewable energy—clear environmental positives. Yet its extraction methods, particularly at Grasberg, represent environmental practices from another era. This tension is unresolvable in the short term but manageable through transparency, incremental improvement, and strategic positioning.

The approach: Don't greenwash—acknowledge the tensions. Invest in measurable improvements even if perfection is impossible. Focus on the denominator (copper produced) not just the numerator (absolute emissions). And recognize that ESG leadership in mining is relative, not absolute.

7. Managing Complexity Through Cycles

Freeport operates in multiple countries, deals with dozens of stakeholders, manages commodity price volatility, and navigates technical complexity that would challenge NASA. The company has survived by building systems and cultures that thrive on complexity rather than being overwhelmed by it.

Key principles: Decentralize operational decisions but centralize strategic ones. Build deep technical bench strength—mining engineers can't be created overnight. Maintain financial flexibility even at the cost of "efficiency." And crucially, respect the cycles. They're not anomalies to be conquered but realities to be navigated.

8. The Innovation Imperative

AI and data science are built into the 'leach to the last drop' effort, providing insights and driving some of the actions of this effort. The company is targeting 200 million lb/y of incremental copper by the end of 2023, and then wants to drive that growth up to 800 million lb/y in a longer time horizon. This isn't just operational improvement; it's existential necessity as ore grades decline globally.

The insight: In mature industries, innovation doesn't mean disruption—it means incremental improvements that compound over time. A 1% improvement in recovery rates, multiplied across billions of pounds of copper, creates enormous value. Focus on the boring innovations that actually move the needle rather than the sexy ones that generate headlines.

X. Analysis & Bear vs. Bull Case

The Bull Case: Riding the Copper Supercycle

The bullish thesis for Freeport-McMoRan rests on a simple premise: the world needs vastly more copper than currently exists, and Freeport controls some of the last great deposits. This isn't speculative—it's mathematical.

Start with demand. Each 1 million EVs utilize somewhere around 150 million lbs of additional copper. With China producing 3.3 million EVs last year and Europe buying 2.3 million, the market can quickly see how much additional copper supply is needed to fuel the growing demand for EVs. A single wind turbine requires 3-5 tons of copper. Grid upgrades for renewable integration need millions of tons. Data centers for AI compute are copper-intensive. The International Energy Agency projects copper demand could double by 2040.

Supply response is structurally constrained. Major discoveries have dried up—the last world-class copper discovery was over a decade ago. New mines take 15-20 years from discovery to production. Ore grades are declining globally, requiring more rock to be moved for each pound of copper. Environmental permitting has become increasingly difficult. The supply deficit isn't a risk—it's a certainty.

Freeport's positioning is optimal. Freeport owns stakes in 10 copper mines, led by its 49% ownership of the Grasberg copper and gold operations in Indonesia, 55% of the Cerro Verde mine in Peru, and 72% of Morenci in Arizona. It sold around 1.2 million metric tons of copper (its share) in 2024, making it one of the world's largest copper miners by volume. These aren't marginal assets—they're tier-one operations with decades of remaining life.

The technical innovation provides additional upside. The copper extracted through the leaching initiative currently costs less than $1/lb, compared with the current market price of about $3/lb. If Freeport achieves even half its 800-million-pound annual target, that's 400 million pounds of nearly pure margin copper production.

Valuation remains reasonable despite the positive fundamentals. At current multiples, the market is pricing in copper at $3.50-4.00 per pound long-term. Any sustained move above these levels drives dramatic multiple expansion. The optionality is asymmetric.

The Bear Case: Political, Operational, and Market Risks

The bearish view starts with concentration risk. Grasberg still dominates the equity story, and Indonesia remains politically complex. The 2017 divestiture stabilized the situation, but resource nationalism is cyclical. What happens when Indonesia needs revenue and Grasberg is generating billions in free cash flow? History suggests terms will tighten.

China risk looms large. Emerging economies heavily influence copper demand, especially China, which consumed approximately 6.75 million metric tons in 2023, projected to increase by 5.7% in 2024. But China's property sector remains troubled, and the transition to a consumer economy could reduce copper intensity. A China recession would crater copper prices regardless of long-term EV trends.

Operational challenges are mounting. The underground transition at Grasberg was successful, but underground mining is inherently more complex and expensive than open pit. Labor costs are rising globally. Energy costs for mining are increasing. Even with leaching innovations, the company faces the inexorable challenge of declining ore grades.

Capital allocation concerns persist. While the current management team appears more disciplined, Freeport's history is littered with value-destructive decisions. The next copper boom could tempt management into another poorly timed acquisition or diversification effort.

ESG pressures are intensifying, not abating. The riverine tailings disposal at Grasberg becomes harder to defend each year. A major environmental incident could trigger regulatory crackdowns, legal liabilities, or forced closure. The reputational risk affects cost of capital and could limit access to markets.

Competition from substitution and recycling could surprise. Aluminum can replace copper in many applications if price differentials widen. Recycling technology is improving, potentially adding supply. New extraction technologies could make previously uneconomic deposits viable.

The Balanced View

The reality likely lies between extremes. Copper's fundamental supply-demand dynamics appear favorable for the next decade, supporting prices above historical averages. Freeport will benefit from this environment but won't escape the cyclicality inherent to commodities.

The company's operational excellence and technical innovation provide competitive advantages, but these are relative, not absolute moats. Others can and will develop similar capabilities given sufficient incentive.

Political risk at Grasberg is manageable but permanent. Indonesia will continue extracting value through fiscal and regulatory changes. This is a cost of doing business, not an existential threat, but it caps multiple expansion.

Current valuation appears fair, neither compelling nor excessive. At $40-45 per share, the market is pricing in $3.50-4.00 copper and successful execution of leaching initiatives. There's upside if copper exceeds these levels or leaching surpasses targets, but also downside if China slows or operations stumble.

The investment case depends on time horizon and risk tolerance. For those believing in the electrification megatrend, Freeport offers leveraged exposure with proven assets. For those concerned about near-term cyclical risks, the company's history suggests caution is warranted.

XI. Epilogue & "What's Next for FCX"

As Kathleen Quirk looks out from Freeport-McMoRan's Phoenix headquarters, she leads a company fundamentally transformed yet eerily similar to its founding vision. Eric Swenson sought to extract sulfur from impossible places using innovative technology. Today, Freeport extracts copper from equally impossible places—whether 14,000 feet up an Indonesian mountain or from decades-old waste piles using revolutionary leaching.

The next decade will test whether Freeport has truly learned from its tumultuous history. The copper supercycle thesis appears compelling—electrification, renewable energy, and AI-driven compute all require massive amounts of copper. Yet commodity supercycles have a way of creating the seeds of their own destruction through overinvestment and speculation.

Technology will be central to Freeport's future. The leaching initiatives aren't just about incremental production—they're about reimagining mining itself. If Freeport can economically extract copper from what was previously waste, it essentially creates new ore bodies without exploration risk. The potential 800-million-pound annual target would be equivalent to a world-class mine, achieved through innovation rather than capital.

Succession planning remains critical. Quirk represents continuity, having been with Freeport since 1989. But the next generation of leadership must navigate challenges the mining industry has never faced: true carbon accountability, resource circularity, and social license in an interconnected world. The cowboys and empire builders of Freeport's past won't suffice for its future.

M&A possibilities linger despite management's stated focus on organic growth. The copper industry remains fragmented relative to iron ore or aluminum. As deposits become scarcer and development more challenging, consolidation logic strengthens. Freeport could be acquirer or acquired—its clean balance sheet and premier assets make both scenarios plausible.

The Indonesia question persists. Grasberg's underground mines have decades of life remaining, but the relationship with Indonesia will require constant management. The successful 2017-2018 renegotiation bought time, not permanence. Future administrations may demand different terms, especially as copper prices rise.

Environmental and social pressures will intensify. The mining industry can no longer operate in the shadows, quietly extracting resources while avoiding scrutiny. Transparency, accountability, and genuine stakeholder engagement are now operational necessities. Freeport's practices, particularly at Grasberg, must evolve or risk becoming stranded assets in a world demanding responsible sourcing.

The energy transition supercycle thesis will be tested. Current projections show massive copper deficits, but projections have been wrong before. Substitution, efficiency improvements, and recycling could moderate demand. New extraction technologies could unlock previously uneconomic deposits. The certainty markets currently price in may prove misplaced.

Yet for all the uncertainties, Freeport-McMoRan's core value proposition remains intact: it controls some of the world's best copper assets at a time when copper has never been more essential. The company that started mining sulfur from Texas salt domes has become custodian of mountains of copper needed for humanity's energy transition.

The wild ride isn't over. Commodity cycles will continue their relentless oscillation. Political risks will emerge in unexpected places. Technology will create new opportunities and challenges. But Freeport has survived existential crises that would have destroyed lesser companies. It has transformed from sulfur to copper, from Texas to global, from family-run to corporate giant.

As copper prices fluctuate and markets gyrate, one thing remains certain: the world needs copper, and Freeport-McMoRan has it. Whether that simple fact justifies the risks—operational, political, environmental—is the question every investor must answer. The copper king's wild ride continues, destination unknown but journey guaranteed to be anything but boring.

The story of Freeport-McMoRan is ultimately a story about transformation—of rocks into metal, of waste into resource, of impossibility into profit. It's a story about the messy reality of providing materials essential for modern life. And it's a story that, despite a century of history, is really just beginning. The age of electrification will demand more copper than the world has ever produced. Whether Freeport leads, follows, or fails in meeting that demand will define not just a company, but an industry—and perhaps our energy future itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube