Fastenal: The Nuts & Bolts Empire

I. Introduction & Episode Roadmap

Picture this: A company that sells nuts, bolts, and screws—the most mundane industrial products imaginable—delivering a 214,200% total return since its 1987 IPO. That's not a typo. While Silicon Valley was chasing the next big software platform, a small-town Minnesota fastener distributor quietly built one of the greatest wealth-creation machines in American business history.

Fastenal today stands as North America's largest fastener distributor, a $46+ billion industrial supply powerhouse that has fundamentally reimagined what distribution means in the digital age. The company that started with five friends and $30,000 in a 20-foot storefront now operates over 1,700 branches, deploys 100,000+ vending machines at customer sites, and maintains embedded operations within the facilities of the world's largest manufacturers.

But here's what makes this story truly remarkable: Fastenal's founding vision—automated vending machines dispensing fasteners—was a complete failure. The technology didn't work, the economics were broken, and the founders had to abandon their core concept before they'd sold a single machine. Yet forty years later, that same "failed" idea would become the cornerstone of their competitive moat.

How did a fastener shop in Winona, Minnesota (population: 27,000) evolve into an industrial distribution empire? How did Bob Kierlin and his team transform the simple act of selling screws into a sophisticated, data-driven service business embedded so deeply in customer operations that switching becomes nearly impossible? And perhaps most intriguingly: why did the vending machine concept that failed in 1967 become the key to dominance in 2012?

This is a story about timing, persistence, and the power of being boring in all the right ways. It's about building switching costs one bolt at a time, about the unexpected competitive advantages of small-town culture, and about why sometimes the best business model is the one that takes forty years to fully realize.

We'll trace Fastenal's journey from its vending machine dreams through its branch empire expansion, examine the counterintuitive strategy of closing stores while doubling sales, and explore how a fastener company became a technology-enabled logistics platform. Along the way, we'll uncover the playbook that turned industrial distribution—perhaps the least sexy corner of American business—into one of the stock market's greatest success stories.

II. Origins: The Vending Machine That Never Was

The seed of a $46 billion empire was planted in the mind of an 11-year-old boy working in his father's auto supply shop in Winona, Wisconsin. Young Bob Kierlin watched as customers drove from store to store, searching for the right fastener—a specific bolt, a particular screw size, an odd washer dimension. When the local hardware stores came up empty, they'd inevitably end up at the Kierlin family shop, desperate and frustrated.

"Why isn't there a better way to do this?" Bob wondered. The inefficiency was maddening: thousands of SKUs, each slightly different, scattered across dozens of stores, with no systematic way to match supply with demand. It was 1956, and the problem seemed both mundane and monumental.

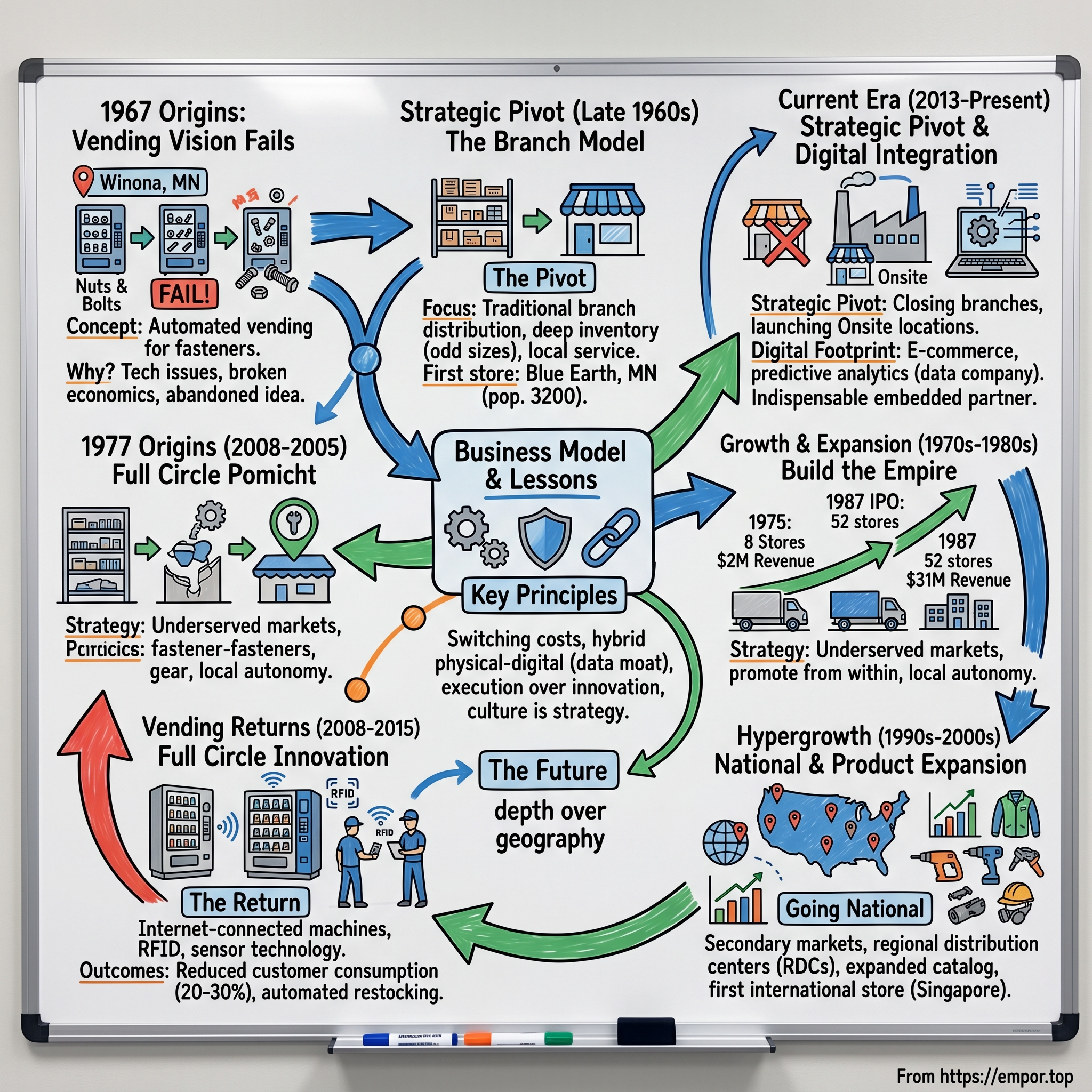

Fast forward to 1967. Bob Kierlin, now 28 and working as a sales engineer at IBM's Rochester, Minnesota facility, couldn't shake that childhood observation. During lunch breaks, he'd sketch out ideas for a radical solution: unmanned retail stores lined with vending machines, each dispensing different sizes and types of fasteners. Customers could walk in any time, insert coins, and get exactly what they needed. No inventory waste. No staffing costs. Pure efficiency.

The IBM connection proved crucial, though not for technical reasons. Kierlin's day job exposed him to the bleeding edge of automation and systems thinking, but more importantly, it surrounded him with ambitious colleagues who understood scale. One of them, Jack Remick, became intrigued by Kierlin's vending machine concept. Soon, Kierlin was recruiting his high school buddies—Michael Gostomski, Dan McConnon, and Steve Slaggie—selling them on a vision of franchised vending operations that could revolutionize industrial supply.

By late 1967, the five partners had assembled $30,000 in capital—roughly $270,000 in today's dollars—with each contributing $6,000. They rented a narrow, 20-foot-wide storefront at 318 Main Street in downtown Winona, sandwiched between a bakery and a bar. The location was deliberately modest; most of the capital would go toward developing the vending machines that would change everything.

Then came the first crisis: what to call the company. Kierlin wanted "Lightning Bolt," envisioning a dynamic, modern brand. Two of the other founders threatened to walk away entirely, calling it juvenile and unprofessional. After heated debates that nearly killed the venture before it started, they compromised on "Fastenal"—a portmanteau of "fastener" and "industrial" that nobody particularly loved but everyone could live with.

The naming drama, in retrospect, was prophetic. This would be a company built on pragmatism over flash, substance over style, compromise over ego. But first, they had to build those revolutionary vending machines.

The engineering challenges emerged immediately. Industrial fasteners aren't candy bars—they come in thousands of varieties, from tiny precision screws to massive construction bolts. The weight variations alone were staggering: a small machine screw might weigh a few grams, while a large hex bolt could weigh several pounds. The dispensing mechanism that worked for one would jam or break with the other.

Then there was the inventory problem. A typical construction project or manufacturing run might need hundreds or thousands of identical fasteners. No vending machine could hold that volume across the necessary SKU range. The team tried larger machines, multiple dispensing mechanisms, even considered separate machines for different fastener categories. Nothing worked.

By early 1968, after months of failed prototypes and burned capital, Kierlin faced reality: the vending machine concept was dead. The five founders gathered in their cramped storefront, surrounded by boxes of inventory they'd accumulated for the machines that would never be built. They had two choices: admit defeat and return to their day jobs, or pivot to something completely different.

"We've got the inventory," Kierlin argued. "We've got the location. We understand the customer need. Let's just... sell fasteners the old-fashioned way. But let's do it better than anyone else."

It was hardly the revolutionary vision that had brought them together. But sometimes the best pivots aren't to something radically new—they're to something radically better. Fastenal would become a traditional branch-based distributor, but with a twist: they'd operate in smaller markets ignored by the big players, maintain deeper inventory than anyone thought economical, and provide a level of service that would make them indispensable.

The vending machine dream was dead. Or so they thought. Four decades later, that "failed" concept would return in a form the founders never imagined, powered by technology they couldn't have conceived, solving problems they hadn't yet encountered. But first, they had to build the foundation—one branch, one customer, one fastener at a time.

III. Building the Branch Empire (1970s–1980s)

Bob Kierlin stood in the empty main street of Blue Earth, Minnesota—population 3,200—studying the foot traffic. Or rather, the lack of it. His four partners thought he'd lost his mind. Who opens an industrial supply store in a town barely large enough to support a McDonald's? But Kierlin saw what they didn't: two small manufacturing plants on the outskirts, a cluster of construction companies, and zero competition for miles.

This was 1969, and Kierlin had discovered Fastenal's first strategic insight: small and medium-sized towns were goldmines hiding in plain sight. The big distributors—Grainger, MSC Industrial—focused on major metropolitan areas where they could justify massive warehouses and large sales forces. They ignored places like Blue Earth, Brookings, and Fergus Falls. These towns had healthy manufacturing and construction sectors, but their supply chain options were limited to whatever the local hardware store happened to stock.

"We're not competing against Grainger," Kierlin explained to his skeptical partners. "We're competing against driving 50 miles to the nearest city."

The Blue Earth store opened with 12,000 SKUs—an almost absurd inventory depth for such a small market. The conventional wisdom said you needed population density to justify that kind of selection. But Kierlin's math was different: if you're the only game in town with professional-grade inventory, you don't need a huge population. You just need to capture 100% of the addressable market.

The strategy worked brilliantly. Within six months, the Blue Earth location was profitable. Construction crews from three counties away would drive past two hardware stores to shop there. Why? Because Fastenal had the odd-sized lag bolt they needed, the specific grade of stainless steel fastener their specs required, the metric threading that nobody else stocked.

But inventory depth alone wasn't enough. Fastenal discovered its second competitive advantage almost by accident. A local manufacturer needed custom-machined bolts for a specialized product line—something no distributor typically handled. Instead of saying no, store manager Dan McConnon said, "Give us a week." They found a local machine shop, coordinated the specifications, managed quality control, and delivered the custom parts on time.

Word spread. Suddenly Fastenal wasn't just a distributor; they were a solutions provider. Can't find it in any catalog? Fastenal will make it for you. Need it modified? Fastenal will handle it. The company began investing in metalworking equipment, hiring machinists, and offering custom manufacturing services that blurred the line between distributor and manufacturer.

By 1975, Fastenal operated 8 stores across Minnesota and Wisconsin, each following the same playbook: small to medium market, massive inventory depth, custom capabilities, and a relentless focus on saying yes to customer requests. Revenue had grown from $18,000 in their first year to over $2 million. More importantly, they'd proven the model was replicable.

The growth acceleration came in 1981 when Kierlin made a crucial decision: promote from within, always. Every store manager had started on the floor. Every regional manager had run a store. This wasn't just about culture—it was about knowledge transfer. A manager who'd spent two years learning the quirks of contractors in Mankato could teach those lessons to a new manager in Sioux Falls. The tribal knowledge accumulated and compound.

The numbers tell the story: 12 stores in 1980, 31 stores in 1984, 50 stores in 1986. Each new location was profitable within 12-18 months—a staggering achievement in retail distribution. The company was entirely self-funded through retained earnings, with no outside capital or debt. Kierlin believed debt would force them to grow too fast, to compromise on market selection or inventory investment.

Then came 1987, and everything changed. The company had reached an inflection point—52 stores across seven states, $31 million in revenue, and ambitious plans for national expansion. But organic growth through retained earnings would take decades to achieve their vision. They needed capital, but Kierlin was adamant: no debt, no private equity, no compromise on control.

The solution was an IPO, but the timing couldn't have been worse. Fastenal went public on August 20, 1987, at $9 per share (split-adjusted: $0.025), raising $8.4 million. Two months later, on October 19, Black Monday hit. The Dow Jones dropped 22% in a single day—the largest one-day percentage decline in stock market history. Fastenal shares plummeted to $5.50.

Most newly public companies would have panicked, perhaps pulled back on expansion plans or reconsidered their strategy. Kierlin's response? "Good. Now our employees can buy shares cheap."

He was playing a different game. While Wall Street obsessed over quarterly earnings, Kierlin thought in decades. The market crash was noise. The fundamental business—selling fasteners to manufacturers and contractors who needed them regardless of stock prices—remained unchanged. If anything, the crash created opportunity: distressed competitors, cheaper real estate, available talent.

By the end of 1989, Fastenal operated 83 stores across 15 states. Revenue had nearly doubled to $58 million. The stock, which had bottomed at $5.50, was trading at $14. Early employees who'd bought shares during the crash had already tripled their money.

But the real test was coming. The 1990s would bring national expansion, international competition, and the rise of e-commerce. The small-town fastener company was about to discover if their model could scale beyond the Midwest—and whether their branch-based strategy could survive the digital revolution.

IV. The Hypergrowth Years: Going National (1990s–2000s)

Will Oberton stepped off the plane in Portland, Oregon, carrying nothing but a briefcase and a mandate: open 15 Fastenal stores on the West Coast within 18 months. It was January 1990, and the 28-year-old regional manager had never lived outside Minnesota. He didn't know a single customer, supplier, or potential employee in the Pacific Northwest. His boss, Bob Kierlin, had given him one piece of advice: "Run it like you own it."

This was Fastenal's approach to national expansion—not careful market studies and corporate planning committees, but entrepreneurial managers with near-absolute autonomy and skin in the game. Oberton would later receive stock options tied directly to his region's performance, making him a millionaire by 1999. But first, he had to figure out how to translate the Fastenal model from the heartland to the coast.

The challenges were immediate. West Coast contractors were used to dealing with established players like White Cap and HD Supply. They didn't know Fastenal, didn't trust Fastenal, and didn't particularly need Fastenal. Unlike those underserved small towns in Minnesota, Portland and Seattle had plenty of industrial supply options.

Oberton's solution was radical: ignore the big cities initially. Instead, he opened stores in Longview, Washington (population: 34,000), Bend, Oregon (30,000), and Yakima, Washington (60,000). It was the same playbook Kierlin had pioneered, but applied to an entirely different geography. Within six months, those stores were outperforming projections by 40%.

The expansion accelerated. 1991: 110 stores. 1992: 150 stores. 1993: 200 stores. Each new region followed the same pattern—start in secondary markets, build density, then attack the metros from a position of strength. By the time Fastenal opened in Los Angeles and San Francisco in 1994, they had dozens of profitable stores throughout California's Central Valley, generating cash flow and training managers.

The infrastructure investments were massive. In 1992, Fastenal opened a 150,000-square-foot distribution center in Dallas, followed by another in Atlanta. The Indianapolis facility, opened in 1994, spanned 400,000 square feet—larger than seven football fields. But here's what made these investments remarkable: Fastenal built them before they needed them.

"We'd operate at 40% capacity for the first year, 60% for the second," recalled Dan Florness, then CFO. "Wall Street hated it. Our margins would compress every time we opened a DC. But Bob [Kierlin] understood—you can't capture growth if you're not ready for it."

The product expansion was equally aggressive. In 1993, Fastenal launched FastTool, a store-within-a-store concept focused on power tools and safety equipment. The logic was simple: the same contractors buying fasteners needed drill bits, saw blades, and safety glasses. Why make them go elsewhere? By 1995, the average Fastenal location carried 37,000 different items, while FastTool sections added another 3,000 SKUs of complementary products.

Then came the small-town experiment that would define Fastenal's next decade. In 1996, they began opening combination Fastenal/FastTool stores in towns with populations between 5,000 and 8,000—markets everyone else ignored completely. The first opened in Thief River Falls, Minnesota (population: 8,000). The store was 1,800 square feet—tiny by industry standards—with one full-time employee and one part-timer.

Industry observers called it insane. How could you possibly justify the inventory investment in such a small market? But the unit economics were beautiful: rent was $800/month, labor costs were minimal, and these stores captured 90%+ market share in their territories. A store doing $400,000 in annual revenue could generate $60,000 in operating profit—a 15% margin that beat many big-city locations.

By 1999, Fastenal operated 728 stores across 48 states. The company had grown from $58 million in revenue in 1989 to $543 million a decade later—a 25% compound annual growth rate. The stock price had increased from $14 to $42 (split-adjusted), creating hundreds of millionaires among early employees who'd received options as part of Kierlin's wealth-sharing philosophy.

The dot-com boom created unexpected challenges. Everyone was talking about "digital disruption" and "disintermediation." Amazon was promising to eliminate traditional distribution. B2B marketplaces like Ariba and Commerce One were supposedly going to connect manufacturers directly with end users, cutting out middlemen like Fastenal entirely.

Kierlin's response was characteristically contrarian. While competitors rushed to build expensive e-commerce platforms, Fastenal doubled down on physical presence. In 2000 alone, they opened 147 new stores—more than one every three days. The company also made its first international move, opening a location in Singapore to serve the Asian operations of existing U.S. customers.

"The internet people don't understand our business," Kierlin told investors. "Our customers don't just buy products. They buy availability, expertise, and problem-solving. You can't download a custom-machined bolt."

The dot-com crash of 2001 proved him right. Ariba's stock fell 99%. Commerce One went bankrupt. But manufacturers still needed fasteners, and they needed them from someone who could deliver them tomorrow, not next week. Fastenal's revenue grew through the recession, hitting $905 million in 2001 while pure-play e-commerce competitors evaporated.

The true validation came from an unlikely source: stock market performance. A 2012 Bloomberg analysis revealed that Fastenal had generated a 38,565% return from October 19, 1987 (the day after Black Monday) through 2012—making it the single best-performing stock in the Russell 1000 over that 25-year period. Better than Microsoft. Better than Apple. Better than any tech highflyer or biotech wonder.

But the most audacious move was yet to come. In 2008, with over 2,000 stores and seemingly unstoppable momentum, Fastenal would revisit the failed idea that had started it all: the vending machine. This time, armed with four decades of customer relationships, sophisticated inventory management systems, and deep pockets, they would succeed where the founders had failed. The vending machine was about to return—and transform everything.

V. The Vending Machine Returns: Full Circle Innovation (2008–2015)

The prototype sat in a Winona warehouse, sleek and imposing: six feet tall, internet-connected, with 54 spiral dispensers and real-time inventory tracking. It was 2007, and Steve Rucinski, Fastenal's head of innovation, was staring at what might be either brilliant or insane—a $15,000 vending machine for industrial supplies.

"You want us to go back to vending machines?" asked Dan Florness, now President. "The idea that nearly killed us before we started?"

But this wasn't 1967. Everything had changed. The machines now had sophisticated weight sensors that could handle anything from tiny washers to heavy bolts. Cloud-based software tracked every transaction. RFID technology enabled instant restocking alerts. Most importantly, Fastenal now had something the founders never imagined: 2,200 branches providing last-mile delivery and 13,000 employees who could service these machines daily.

The first pilot launched at a Toyota supplier in Kentucky. The plant manager was skeptical—why did he need a vending machine when he could just call his Fastenal rep? But Rucinski had done his homework. He'd discovered that the average manufacturing facility experienced 30% "shrinkage" in supplies—workers grabbing extra gloves for home, expensive drill bits disappearing, cutting tools walking off the floor.

"Install our machine," Rucinski proposed. "Every employee gets a code. Every transaction is tracked. You'll cut consumption by 30% in six months, or we'll remove it free."

Six months later, consumption had dropped 47%.

The economics were staggering. A typical manufacturing customer might spend $500,000 annually on industrial supplies. A 47% reduction meant $235,000 in savings—real money that dropped straight to the bottom line. The vending machine cost $15,000, but Fastenal didn't sell it—they provided it free, making money on the product flowing through it. The customer saved money, Fastenal locked in the account, and both parties had perfect data on consumption patterns.

Word spread through the manufacturing community like wildfire. By 2010, Fastenal had installed 2,500 machines. By 2011, that number had exploded to 9,000. The inflection point came in 2012 when the company crossed 15,000 active machines and something remarkable happened: customers started redesigning their facilities around Fastenal vending. Boeing's Everett facility began installing machines in clusters, creating what they called "tool cribs of the future." General Electric redesigned entire factory floors to optimize vending placement. The recent installation at Pierce Manufacturing facility marked Fastenal hitting a major milestone: 100,000-plus active devices at customer sites worldwide.

The technology evolution was relentless. The original spiral-dispenser machines gave way to sophisticated systems: vertical lift modules that could store thousands of SKUs in a footprint smaller than a parking space, scale-based machines that tracked consumption by weight, locker systems for high-value tools. Fastenal's FASTBin system used infrared sensors to monitor bin levels in real-time, automatically triggering replenishment when supplies ran low.

But the real innovation wasn't the hardware—it was the data. Every transaction generated information: who took what, when, for which job, at what frequency. Fastenal's algorithms could predict when a customer would run out of supplies before the customer knew it themselves. They could identify unusual consumption patterns that might indicate theft or process inefficiencies. They could even recommend product substitutions that would save money without compromising quality.

"We became a data company that happens to sell fasteners," explained Florness. "The vending machines were just the collection points."

The customer value proposition was irresistible. The reduction in consumption was often in the range of 20% to 30%, and with roughly $4 billion in vended sales since 2008, that translated to an estimated $1 to $1.7 billion in consumption savings alone for Fastenal's vending customers. But beyond the hard savings, there were soft benefits: eliminated stock-outs, reduced administrative burden, perfect audit trails for compliance, freed-up floor space from inventory rooms.

The competitive moat this created was formidable. Once a Fastenal vending machine was installed, switching costs became astronomical. It wasn't just about removing the machine—it was about losing the data, retraining workers on new systems, rebuilding inventory management processes. Customer retention rates for vending accounts approached 98%.

By 2015, Fastenal had surpassed 55,000 active machines, generating over $2 billion in annual vending sales. The company that couldn't build a working vending machine in 1967 had become the world's largest operator of industrial vending equipment. The founders' original vision—automated, 24/7 access to industrial supplies—had finally been realized, just four decades late and in a form they never could have imagined.

But success created a new challenge. With vending machines providing such intimate customer integration, did Fastenal still need 2,400 physical branches? The answer would reshape the entire company strategy and challenge everything the market thought it knew about distribution.

VI. The Strategic Pivot: Closing Branches, Going Onsite (2013–Present)

Dan Florness stood before a map of North America, covered in blue pins representing Fastenal's 2,600 branches. It was January 2013, and he'd just been promoted to CEO. The board expected him to announce plans for 3,000 locations by 2015. Instead, he picked up a red marker and began crossing out pins.

"We're going to close 800 branches over the next decade," he announced to his stunned leadership team. "And we're going to double our sales while doing it."

The room erupted. This was heresy. Fastenal's entire identity was built on branch density—being closer to the customer than anyone else. Wall Street would panic. Competitors would declare victory. Employees would revolt.

But Florness had seen something others missed. The vending machine data revealed that 60% of customer purchases were predictable, recurring needs. These customers didn't need a branch nearby—they needed inventory inside their facility. Meanwhile, e-commerce was finally mature enough to handle the long-tail of sporadic purchases. The branch, that sacred cow of Fastenal's strategy, was becoming redundant for their best customers. The radical new model emerged in 2014: Onsite locations—essentially mini-Fastenal branches embedded within customer facilities. Instead of customers coming to Fastenal, Fastenal would live inside the customer. A two-person team, 5,000 square feet of inventory, direct integration with the customer's procurement systems. It was the ultimate expression of being close to the customer—literally sharing their roof.

The first major Onsite opened at a Caterpillar facility in Illinois. The skeptics were vocal: why would Caterpillar let a supplier operate inside their plant? The answer became clear within months. Caterpillar eliminated their internal tool crib staff (Fastenal handled it), freed up 15,000 square feet of warehouse space (Fastenal managed inventory more efficiently), and reduced supply costs by 25% (Fastenal's scale brought better pricing). The Onsite model wasn't just distribution—it was outsourced supply chain management.

By December 31, 2024, Fastenal had 2,031 active Onsite locations, representing an 11.5% increase from the previous year. Daily sales through these Onsite locations grew at a mid single-digit rate, but the real value wasn't just sales—it was stickiness. Once Fastenal operated inside a customer's facility, with employees badged into their systems, inventory customized to their operations, the switching costs became prohibitive.

Meanwhile, the branch footprint contracted deliberately. From a peak of 2,637 locations in 2016, Fastenal systematically closed underperforming branches, consolidating territories and redirecting resources to Onsites and digital infrastructure. In 2024 alone, the company signed 358 new Onsite locations, while continuing to optimize its traditional branch network.

The digital transformation accelerated in parallel. Fastenal's Digital Footprint—encompassing FMI (Fastenal Managed Inventory) technology and e-commerce—grew from 15% of sales in 2015 to 62.2% by Q4 2024. But this wasn't Amazon-style e-commerce. It was deeply integrated, customer-specific digital ordering systems that tied directly into ERP platforms, automated reordering based on production schedules, and provided real-time visibility into consumption patterns.

The FASTBin and FASTStock programs exemplified this integration. Sensors monitored inventory levels in bins at customer sites, automatically triggering replenishment when supplies ran low. No human intervention required. The system learned consumption patterns, adjusted for seasonality, and optimized order quantities. Customers got perfect inventory availability with zero administrative burden.

The economics of this transformation were counterintuitive but powerful. Closing branches reduced fixed costs. Onsite locations, while requiring upfront investment, generated 3-4x the revenue of a traditional branch with better margins due to deeper customer integration. Digital sales had virtually zero marginal cost. The company projected that 66% to 68% of sales would flow through digital channels by the end of 2025.

Employee productivity soared. Sales per employee increased 63% from 2013 to 2022, even as the company added sophisticated technical capabilities. The branch managers who might have resisted closures instead became Onsite leaders, often doubling their compensation through performance incentives tied to customer success metrics.

Wall Street initially hated it. Analysts couldn't understand why Fastenal was closing locations while competitors were opening them. The stock traded sideways for two years as investors digested the strategy. But by 2019, the results were undeniable: revenue had grown from $3.33 billion to $5.02 billion despite reducing branches by 30%. Operating margins expanded. Return on invested capital increased.

The COVID-19 pandemic validated the strategy in ways nobody anticipated. While competitors with traditional branch networks struggled with lockdowns and social distancing, Fastenal's Onsite locations were deemed essential—they were literally part of their customers' operations. Digital ordering surged. Vending machines enabled contactless transactions. The company that had been closing branches for five years was perfectly positioned for a world where physical retail became a liability.

By 2024, the transformation was complete. Fastenal operated fewer branches than in 2001, yet generated 3x the revenue with higher margins and deeper customer relationships. The company that started as a branch-based distributor had evolved into something unprecedented: a hybrid physical-digital supply chain partner so embedded in customer operations that they'd become indispensable infrastructure.

VII. The Business Model: Distribution as a Service

Inside the Indianapolis distribution center, a package moves every 1.2 seconds. The facility spans 1.08 million square feet with 547,000 individual storage locations, each tracked by algorithms that optimize placement based on velocity, weight, and shipping patterns. But here's what makes this remarkable: 70% of the products moving through this technological marvel are worth less than a dollar.

This is the paradox of Fastenal's business model. They've built one of the most sophisticated distribution networks in America to sell commodities—screws, bolts, washers—that have existed largely unchanged since the Industrial Revolution. The key insight: the product doesn't matter; the availability does.

"Nobody wakes up excited about buying fasteners," Dan Florness explained to investors. "They wake up worried about not having them when they need them."

Fastenal's true product isn't fasteners—it's certainty. When a production line needs a specific bolt to avoid a shutdown, when a construction crew needs safety equipment to meet OSHA requirements, when a maintenance team needs a replacement part at 2 AM, Fastenal provides the confidence that these items will be available, immediately, without fail.

The numbers tell the story of this evolution. In 1987, fasteners represented 90% of sales. By 2010, despite the company name, fasteners had dropped to 45% of revenue. Today, Fastenal offers 690,000+ individual products across nine major categories. Safety supplies, cutting tools, hydraulics, janitorial supplies—if it keeps an industrial operation running, Fastenal stocks it.

But stocking products is the easy part. The genius lies in how Fastenal delivers them. Consider their Onsite model: a Fastenal employee sits inside a Boeing facility, wearing a Boeing badge, using Boeing systems, managing Boeing inventory. They're not a supplier; they're part of Boeing's operations team. When Boeing needs something, they don't "order from Fastenal"—they pull from their inventory that happens to be managed by Fastenal.

The vending machines take this integration deeper. Consumption typically drops 20% to 30% after installation, generating an estimated $1 to $1.7 billion in savings for customers since 2008. But the real value isn't cost savings—it's data. Every transaction creates a record: who took what, when, for which project. Fastenal's algorithms analyze this data to predict needs, identify inefficiencies, and prevent stockouts.

The FASTBin system pushes automation further. Infrared sensors monitor thousands of bins at customer sites, tracking inventory levels in real-time. When supplies run low, the system doesn't just alert someone—it automatically generates a purchase order, routes it through approval workflows, schedules delivery, and updates the customer's ERP system. The customer never lifts a finger.

This level of integration creates switching costs that approach infinity. Imagine telling Boeing they need to remove dozens of vending machines, retrain hundreds of workers, integrate new suppliers into their systems, and rebuild years of consumption data from scratch. The cost wouldn't just be monetary—it would be operational chaos.

The distribution infrastructure enabling this model is staggering. Fastenal operates 16 distribution centers across North America and Europe, connected by a private trucking fleet that handles 90% of product tonnage. This isn't for cost savings—private trucking is often more expensive than third-party logistics. It's for control. When a customer needs emergency delivery, Fastenal doesn't negotiate with carriers; they dispatch their own truck.

The last-mile delivery showcases the model's elegance. Traditional distributors ship from warehouses to customers. Fastenal ships from warehouses to branches to Onsites to point-of-use. A fastener might move through four Fastenal facilities before reaching its final destination, but each movement adds value: consolidation, customization, kitting, quality control.

Custom manufacturing capabilities add another layer. Fastenal operates metalworking facilities that can produce fasteners to customer specifications. When a customer needs a bolt that doesn't exist in any catalog, Fastenal doesn't say no—they make it. This capability transforms Fastenal from distributor to solution provider, handling not just standard needs but unique challenges.

The financial model underlying this infrastructure is counterintuitive. Fastenal maintains inventory turns of just 4-5x annually—terrible by retail standards. Amazon turns inventory 12x. But Fastenal isn't optimizing for inventory efficiency; they're optimizing for availability. That bolt gathering dust for six months becomes invaluable when it prevents a million-dollar production shutdown.

Gross margins reflect this value: 45%+ on products that are essentially commodities. Customers aren't paying for the bolt; they're paying for the certainty that the bolt will be there when needed, tracked through their systems, delivered by someone who understands their operations, with quality guaranteed and compliance documented.

The model's resilience shows in downturns. During the 2008 financial crisis, while competitors slashed inventory and closed locations, Fastenal maintained stock levels and kept branches open. Customers who'd been abandoned by other suppliers became Fastenal loyalists. The company emerged from the recession with higher market share and stronger customer relationships.

Digital integration amplifies everything. Fastenal's Digital Footprint—including FASTStock, FASTBin, and FASTVend services plus eBusiness—represented 62.2% of sales in Q4 2024. But this isn't e-commerce in the Amazon sense. It's embedded commerce—transactions happening automatically based on production schedules, sensor readings, and predictive algorithms.

The culmination is a business model that transcends traditional distribution. Fastenal doesn't just supply products; they operate supply chains. They don't serve customers; they become part of customer operations. They don't sell fasteners; they sell confidence, efficiency, and peace of mind.

"Distribution as a Service" isn't Fastenal's marketing tagline—they're too understated for such Silicon Valley terminology. But it perfectly captures what they've built: a subscription-like model where customers pay not for products but for outcomes, where switching costs compound daily, where the service becomes so embedded that it's no longer a supplier relationship but operational infrastructure. The vending machine that failed in 1967 was just ahead of its time. The model that emerged is timeless.

VIII. Leadership Transitions & Culture

Bob Kierlin's office in Winona, Minnesota, hasn't changed since 1975. Same metal desk. Same squeaky chair. Same view of the Mississippi River. In 2012, when his net worth crossed $1 billion, a reporter asked if he'd considered upgrading. Kierlin looked genuinely puzzled. "Why? This desk works fine."

This wasn't performative frugality. This was the authentic culture that built Fastenal: Midwestern pragmatism elevated to strategic advantage. While competitors hired McKinsey consultants and launched "transformation initiatives," Fastenal promoted branch managers and avoided debt. While others built gleaming headquarters, Fastenal operated from a converted grocery warehouse. While CEO pay skyrocketed across corporate America, Kierlin never took a salary above $150,000.

The culture starts with hiring. Fastenal doesn't recruit from Ivy League MBA programs—they hire from community colleges in Winona, Mankato, and Fergus Falls. They don't look for industry experience—most employees have never worked in distribution. They seek something more elusive: hunger, hustle, and comfort with ambiguity.

"We hire athletes, not specialists," explained Will Oberton, who rose from branch manager to regional VP. "Give me someone who played Division III football over a Harvard MBA any day. The football player knows how to get hit and keep going."

The promotion philosophy is radical: everyone starts at the bottom. No exceptions. The current CEO started in accounting. The head of sales started in a branch. The board includes multiple members who began as delivery drivers. This isn't sentiment—it's strategy. Leaders who've worked every role understand every problem.

Compensation reinforces ownership mentality. Branch managers receive profit-sharing tied directly to their location's performance. Regional managers get equity stakes in their territory's growth. The company has created over 300 employee millionaires—not through lucky options grants but through sustained performance over decades.

The Winona headquarters embodies this culture physically. No executive parking. No executive dining room. The CEO's office is smaller than most branch manager spaces. When Fortune 500 executives visit, they're often shocked. Where's the marble lobby? The modern art? The executive floor? This is a $46 billion company operating from facilities that look like a 1980s industrial park.

But beneath the modesty lies sophisticated thinking. Kierlin instituted "Fastenal School"—a rigorous internal education program where employees learn everything from inventory management to customer psychology. Sessions are taught by senior employees, not external consultants. Knowledge stays within the company, accumulating and compounding.

The decision-making culture is radically decentralized. Branch managers have more autonomy than most Fortune 500 VPs. They set prices, choose inventory, hire staff, and manage P&Ls. Mistakes are tolerated; bureaucracy isn't. A branch manager can commit $50,000 to solve a customer problem without approval. Try that at Home Depot.

When Kierlin stepped down as CEO in 2012 (remaining Chairman), the succession was seamless. Dan Florness, who'd joined as CFO in 1996, had been groomed for a decade. He knew every branch, every system, every major customer. The transition was so smooth that the stock price barely moved—remarkable for a founder-led company.

Florness brought subtle changes while preserving core culture. He pushed digital transformation but through a Fastenal lens—practical technology solving real problems, not innovation theater. He accelerated Onsite expansion but maintained the emphasis on relationships over transactions. He closed branches but protected employee equity, reassigning rather than terminating.

The cultural resilience showed during COVID-19. While competitors furloughed staff, Fastenal maintained full employment. When supply chains broke, Fastenal employees slept in warehouses to maintain shipments. When customers needed PPE, Fastenal sourced it regardless of margin impact. The company that preached long-term thinking proved it when tested.

Employee retention tells the story. Average tenure exceeds 15 years in an industry where 5 years is exceptional. Voluntary turnover runs below 5% annually. The company receives 100+ applications for every opening, mostly through employee referrals. When your workforce is your recruiting department, culture becomes self-reinforcing.

The international expansion tested cultural exports. Could Winona values work in Singapore, Shanghai, or Amsterdam? The answer: yes, with adaptation. International branches maintain local leadership but follow Fastenal principles—promote from within, maintain high inventory, prioritize service over margins. The accent changes; the approach doesn't.

Critics call it insular. The lack of outside perspectives, the resistance to consulting wisdom, the skepticism of trending management theories. But Fastenal's response is compelling: 214,200% investor returns. You don't achieve that by following conventional wisdom.

The deeper insight is that Fastenal's culture is its strategy. The frugality enables price competitiveness. The promotion-from-within ensures institutional knowledge. The decentralization enables rapid response. The long-term orientation enables patient investment. What looks like stubbornness is actually discipline.

In 2024, as the company approached $8 billion in revenue, the culture remained remarkably intact. New employees still start in branches. Executives still fly coach. The headquarters still lacks pretension. Bob Kierlin, now 85, still drives his 10-year-old pickup truck to board meetings.

"Culture eats strategy for breakfast," Peter Drucker supposedly said. At Fastenal, culture IS strategy. The company that sells the most boring products in business has built one of the most interesting cultures in capitalism—proof that competitive advantage doesn't always come from what you sell, but from who you are.

IX. Playbook: Business & Investing Lessons

The conference room at Berkshire Hathaway's 2018 annual meeting buzzed with anticipation. Warren Buffett had just been asked about "hidden gems" in the market. His response was unexpected: "Look at companies like Fastenal. They do ordinary things extraordinarily well. That's where real wealth is created."

Buffett never invested in Fastenal—it was never cheap enough for his taste—but his observation captured something profound. In an era obsessed with disruption and transformation, Fastenal built one of history's great wealth-creation machines by perfecting the mundane. The playbook they developed offers lessons that transcend industry.

Lesson 1: Start Focused, Expand Deliberately

Fastenal began with fasteners—the most commoditized product imaginable. But instead of immediately diversifying, they spent two decades perfecting fastener distribution. Only after dominating that niche did they expand to adjacent products. Each expansion followed the same pattern: master the core, then extend to logical adjacencies where existing capabilities provide advantage.

The contrast with modern startups is stark. Today's entrepreneurs chase TAM (Total Addressable Market) from day one, building for hypothetical scale before proving unit economics. Fastenal proved that dominating a small market creates the foundation for conquering larger ones.

Lesson 2: Physical Presence in a Digital World

While competitors rushed online, Fastenal doubled down on physical presence—but with a twist. Their Onsite locations and vending machines aren't traditional retail; they're physical APIs into customer operations. The lesson: in B2B, digital doesn't replace physical—it enhances it. The companies winning aren't pure-play digital or pure-play physical; they're hybrids leveraging both.

Lesson 3: Switching Costs Compound Daily

Every vending machine installed, every Onsite opened, every system integrated increases switching costs incrementally. No single action creates lock-in, but thousands of small integrations create unbreakable bonds. Fastenal's active machine count grew from 9,000 in 2011 to nearly 27,000 in 2012, then surpassed 96,000 by 2018. Each machine is a physical switching cost, a data moat, and a revenue stream.

Lesson 4: Efficiency at Scale, Not Before

Fastenal ran inefficiently for decades—too many branches, too much inventory, too many employees. But this "inefficiency" was strategic. Over-investment in infrastructure and service created customer loyalty that enabled later optimization. Only after achieving dominant position did they rationalize branches and improve margins. The lesson: win first, optimize later.

Lesson 5: Data as Byproduct, Not Product

Fastenal never set out to be a data company. Data emerged naturally from operations—vending transactions, consumption patterns, failure rates. This organic data proves far more valuable than purchased datasets because it reflects actual behavior, not surveyed intentions. The best data moats aren't built; they accumulate.

Lesson 6: Timing Matters More Than Innovation

The vending machine idea wasn't wrong in 1967—it was early. The same concept that failed at founding became transformational 40 years later. The difference? Infrastructure, relationships, and technology had matured. Innovation isn't just about new ideas; it's about implementing old ideas when conditions align.

Lesson 7: Stock Splits Signal Confidence

Fastenal completed its ninth stock split in 37 years with a 2-for-1 split in May 2024. While academics claim splits are meaningless, Fastenal's history suggests otherwise. Each split preceded sustained growth periods. Management only splits when confident about trajectory—a signal worth monitoring.

Lesson 8: Employee Productivity Scales Non-Linearly

Sales per employee climbed 63% from 2013-2022 while employee count grew just 29%. This wasn't through automation replacing workers but through technology amplifying human capability. The lesson: in distribution, productivity gains come from augmentation, not replacement.

Lesson 9: Gross Margins Tell Stories

Fastenal's gross margins of 44.8% in Q4 2024 on commodity products reveal pricing power that shouldn't exist. When customers pay 45% margins on bolts available elsewhere for less, they're not buying products—they're buying solutions. High margins on commodities indicate true differentiation.

Lesson 10: Founder Mentality Survives Founders

Despite Bob Kierlin stepping down as CEO in 2012, Fastenal maintains founder intensity. This isn't accident but architecture—promotion from within, aligned incentives, cultural reinforcement. Companies that successfully transition beyond founders don't just transfer leadership; they institutionalize mindset.

For Investors: The Boring Business Premium

Fastenal teaches that boring businesses with exciting economics deserve premium valuations. The company trades at ~35x forward earnings—a "tech multiple" for a nuts-and-bolts distributor. This isn't irrational; it reflects the quality of the business model. Predictable revenue, expanding margins, and deep moats justify valuations that seem excessive on surface analysis.

The investment lesson extends beyond Fastenal. Look for companies with:

- Switching costs that compound

- Physical/digital hybrid models

- Embedded customer relationships

- Cultures that survive transitions

- "Boring" products with exciting unit economics

The Meta-Lesson: Execution Over Innovation

Fastenal's ultimate lesson is that execution beats innovation. They didn't invent fasteners, vending machines, or e-commerce. They didn't pioneer new business models or disrupt industries. They simply executed basic business principles—inventory availability, customer service, operational efficiency—better than anyone else, for longer than anyone else.

In an era that celebrates disruption, Fastenal proves that perfection beats innovation, that consistency beats pivoting, that depth beats breadth. The company that failed to build a vending machine in 1967 succeeded by doing everything else extraordinarily well—a playbook as relevant today as it was in that narrow Winona storefront.

X. Analysis & Bear vs. Bull Case

The spreadsheet on the analyst's screen showed a paradox. Fastenal traded at 35x forward earnings—a valuation typically reserved for high-growth software companies or breakthrough biotechs. Yet this was a distributor of industrial commodities, selling products that hadn't fundamentally changed since the 19th century. Either the market was wildly irrational, or Fastenal had transcended traditional distribution economics.

The Bull Case: Irreplaceable Infrastructure

Bulls argue Fastenal has achieved something unprecedented: transforming commodity distribution into essential infrastructure. With 2,031 active Onsite locations as of December 2024 and 100,000+ vending machines deployed, Fastenal isn't just a supplier—they're embedded in the physical and digital operations of North America's industrial base.

The moat is multilayered. First, physical switching costs: removing vending machines, dismantling Onsite operations, retraining workers. Second, data lock-in: years of consumption patterns, predictive algorithms, integrated systems. Third, relationship capital: Fastenal employees who know customer operations intimately. Combined, these create switching costs that make customer defection economically irrational.

The digital transformation story remains early. With projections for 66-68% of sales through digital channels by end of 2025, Fastenal is building a platform that combines Amazon's convenience with embedded physical presence. No pure-play digital competitor can match this hybrid model.

Margin expansion potential is substantial. As branches consolidate and digital sales grow, fixed costs decline while pricing power remains intact. Even with gross margins at 44.8% in Q4 2024, there's room for improvement through mix shift toward higher-margin services and continued operational efficiency.

International expansion offers decades of growth. With minimal presence outside North America, Fastenal could replicate its model globally. European and Asian manufacturing bases need the same solutions. The playbook is proven; it's just a matter of execution.

The culture ensures longevity. With internal promotion, aligned incentives, and proven succession planning, Fastenal has solved the founder transition problem that destroys many companies. This isn't a business dependent on visionary leadership; it's a system that perpetuates itself.

The Bear Case: Peak Penetration and Digital Disruption

Bears see storm clouds gathering. Industrial production in America faces secular headwinds—offshoring, automation, demographic shifts. Fastenal's core market might be shrinking even as they gain share within it. The soft manufacturing environment throughout 2024 and sharp year-end production cuts by major customers hint at structural challenges.

Amazon Business looms as an existential threat. With $35+ billion in B2B sales and growing 20%+ annually, Amazon could disintermediate traditional distributors. Their advantages—infinite selection, lower costs, superior technology—might eventually overwhelm Fastenal's relationship moat.

The valuation leaves no room for error. At 35x earnings, Fastenal is priced for perfection. Any stumble—a recession, margin compression, slowing growth—could trigger severe multiple compression. The stock has delivered extraordinary returns, but past performance might have created unsustainable expectations.

Branch optimization may have limits. Fastenal has closed hundreds of locations while maintaining growth, but there's a floor somewhere. Too few branches could impair service quality, emergency response, and customer acquisition. The efficiency gains from consolidation might be largely captured.

Competition is intensifying. W.W. Grainger is investing heavily in digital capabilities. MSC Industrial is expanding its specialist expertise. Regional players are consolidating. Chinese manufacturers are going direct. The competitive landscape is more challenging than during Fastenal's hypergrowth years.

Customer concentration risk is rising. As Fastenal focuses on large accounts with Onsite relationships, they become more dependent on fewer customers. The unfavorable customer mix impact on margins reflects the pricing power these large customers wield. A loss of even one major account could materially impact results.

Competitive Positioning: The Moat Test

Against Grainger (2x Fastenal's size), Fastenal wins on cost and culture. Grainger's urban focus and higher cost structure make them vulnerable in secondary markets. But Grainger's scale and sophistication pose threats in large account competition.

Against Amazon Business, Fastenal's embedded presence provides defense. Amazon can't install vending machines, staff Onsite locations, or provide localized inventory and service. But Amazon's technology and cost advantages grow daily.

Against regional players, Fastenal's scale is decisive. Smaller competitors can't match Fastenal's inventory depth, technology investments, or geographic coverage. Consolidation among regionals might create stronger competitors, but Fastenal could be the consolidator.

The Verdict: Quality at a Premium

The weight of evidence favors the bulls, with caveats. Fastenal has built genuine competitive advantages that should endure medium-term. The business model generates predictable cash flows, expanding margins, and deepening customer relationships. International expansion and continued digital evolution provide growth runways.

But the valuation assumes flawless execution. At 35x earnings, investors are paying for the next decade of success today. Any disappointment—macro weakness, competitive pressure, execution stumbles—could trigger significant multiple compression.

For long-term investors, Fastenal represents a case study in competitive advantage construction. They've transformed commodity distribution into a differentiated service business with powerful network effects. The question isn't whether Fastenal is a great business—it clearly is. The question is whether greatness is already fully priced.

The answer might lie in time horizon. For traders and short-term investors, the risk-reward looks challenging. For patient capital seeking compound growth over decades, Fastenal offers something rare: a boring business with exciting economics, a proven model with expansion potential, a culture that survives transitions.

Warren Buffett never bought Fastenal because it was never cheap enough. But he studied it, admired it, and learned from it. Sometimes the best investments are the ones that teach us about business, even if we never own them. Fastenal's lesson is clear: in business, as in investing, extraordinary returns often come from ordinary things done extraordinarily well.

XI. The Future: What's Next for Fastenal

Dan Florness pulled up the heat map on his screen, showing Fastenal's North American coverage. Green dots marked their 1,700+ branches, blue squares showed 2,000+ Onsite locations, red pins indicated the 100,000+ vending machines. It looked like complete saturation. But Florness saw something different: opportunity.

"We're maybe 30% penetrated in our addressable market," he told his leadership team in late 2024. "The next decade isn't about geographic expansion—it's about depth."

The branch footprint will continue shrinking, probably stabilizing around 1,450 locations—a 93.5% coverage rate of the North American manufacturing base. This isn't retreat; it's optimization. Each remaining branch becomes a hub for 5-10 Onsite locations, 50-100 vending installations, and hundreds of digital accounts. The branch transforms from retail location to service center.

Onsite expansion accelerates despite the challenging math. With 358 new Onsite signings in 2024, below the goal of 375-400, Fastenal faces the reality that the best locations are already captured. Future Onsites will be smaller, more specialized, potentially less profitable. But the strategic value—customer lock-in, data generation, competitive defense—justifies continued investment.

The vending evolution enters phase three. First was proving the concept. Second was scaling deployment. Third is intelligence. Next-generation machines won't just dispense products; they'll predict failures, optimize inventory, and integrate with customer manufacturing systems. Imagine vending machines that adjust stock based on production schedules, weather patterns, and supply chain disruptions.

International expansion remains the wild card. Fastenal's conservative culture has limited foreign adventures, but the logic is compelling. European manufacturers face the same challenges as American ones. Asian factories need the same solutions. The question isn't whether to expand internationally, but how. Acquisition? Partnership? Organic growth? Each path has precedents in Fastenal's history.

The technology roadmap focuses on practical automation. While competitors chase AI buzzwords, Fastenal invests in mundane but valuable capabilities: automated purchasing, predictive maintenance, supply chain visibility. The goal isn't to be cutting-edge but to be useful. Technology that solves real problems for real customers in real time.

Supply chain resilience becomes a selling point post-COVID. Fastenal's domestic focus, private trucking fleet, and deep inventory suddenly look prescient. As companies reshore and "friend-shore" production, Fastenal's North American infrastructure becomes more valuable. They're positioned to benefit from deglobalization without explicitly betting on it.

Industry 4.0 creates new opportunities. As factories become "smart," they need smart suppliers. Fastenal's vending machines and sensors already generate data; the next step is integration with customer IoT platforms. When a machine predicts its own failure, Fastenal could automatically deliver replacement parts before breakdown occurs.

The acquisition question looms. Fastenal has grown almost entirely organically, but the math is changing. Bolt-on acquisitions of regional specialists could accelerate capability development. A transformational merger with someone like MSC Industrial or Applied Industrial could create an industrial distribution colossus. But cultural integration challenges and Fastenal's conservative nature make large deals unlikely.

Environmental and safety regulations create hidden opportunities. As requirements tighten, customers need partners who understand compliance, document everything, and ensure proper products. Fastenal's systematic approach and deep expertise position them as compliance partners, not just suppliers.

The demographic challenge is real but manageable. Fastenal's workforce is aging, and recruiting young talent to Winona gets harder each year. But the company's proven ability to develop talent internally, combined with remote work capabilities for support functions, provides solutions. The culture that seemed like weakness—insularity, traditionalism—becomes strength in maintaining continuity.

Private equity interest intensifies. PE firms see Fastenal's cash generation, defensive position, and optimization potential. While the company's ownership structure and culture make hostile action impossible, friendly PE involvement could accelerate transformation. More likely, Fastenal becomes an acquirer as PE-backed competitors struggle.

The ultimate question: can Fastenal reach $10 billion in revenue while maintaining margins? CEO Florness has discussed adding $1 billion annually in revenue, having grown from $7.3 billion in 2023. The math works if Onsite expansion continues, digital penetration deepens, and international growth materializes. But execution risk is real.

Climate change, surprisingly, could accelerate growth. Extreme weather requires infrastructure hardening, equipment replacement, and supply chain redundancy. Fastenal's emergency response capabilities and inventory depth make them essential during disruptions. Climate adaptation might drive demand for decades.

The China wildcard remains. If U.S.-China tensions escalate, supply chains will reconfigure dramatically. Fastenal's limited Asian exposure looks like weakness today but could become strength if decoupling accelerates. Their domestic focus and North American supply base position them for a more fractured global economy.

Looking ahead, Fastenal faces a classic innovator's dilemma: how to disrupt yourself while maintaining what works. The answer likely isn't revolutionary change but continued evolution—deeper customer integration, smarter technology deployment, careful geographic expansion. The company that failed at innovation (vending machines) but succeeded at execution will likely continue that pattern.

The next decade won't deliver 214,200% returns—that math is impossible from this base. But Fastenal could deliver something equally valuable: proof that competitive advantages can endure, that culture can survive transitions, that boring businesses can thrive in exciting times. In a market obsessed with disruption, Fastenal's future might be the most radical proposition of all: more of the same, but better.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube