Ford Motor Company: The American Icon's Century of Reinvention

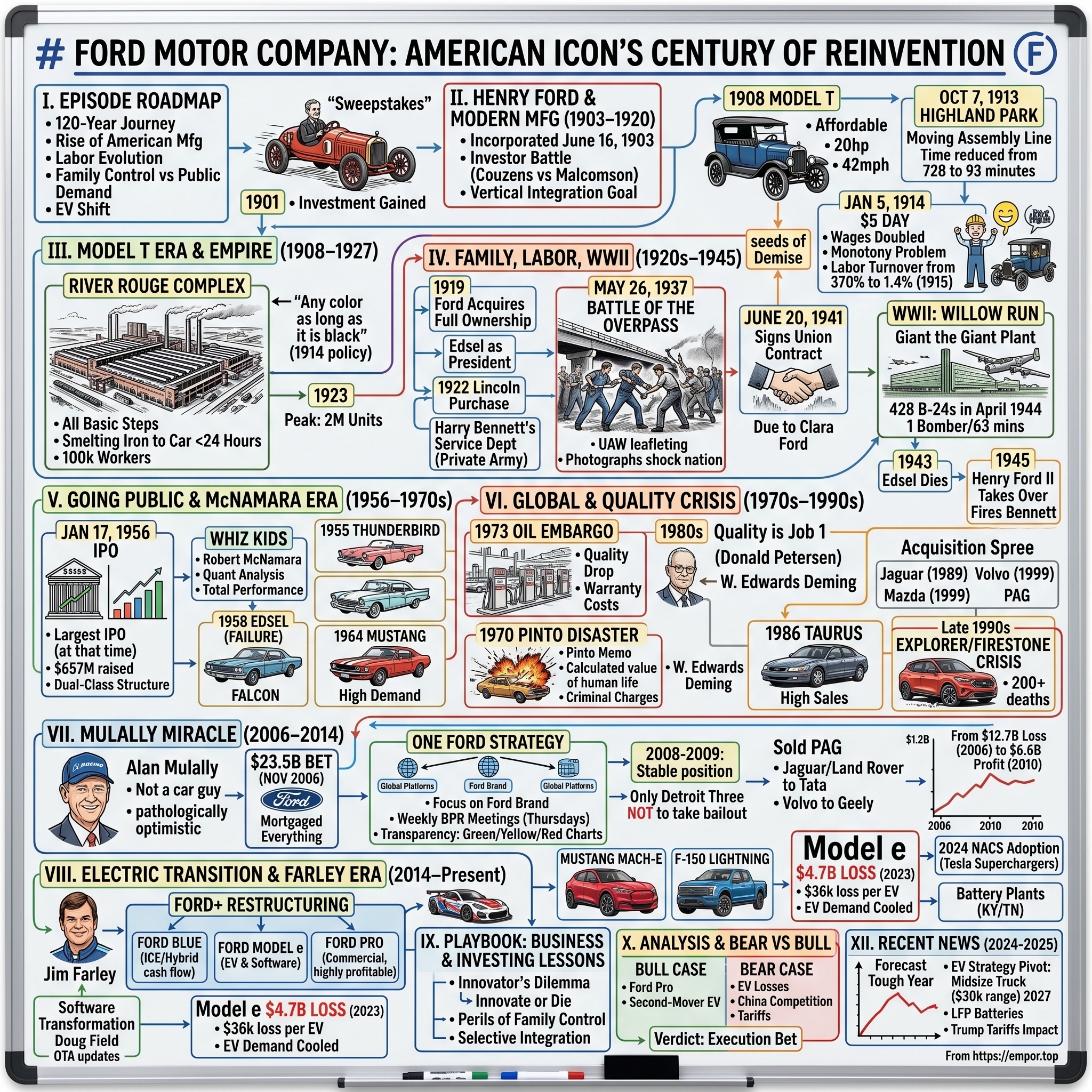

I. Introduction & Episode Roadmap

Picture this: It's a crisp October morning in 1901, and a 38-year-old engineer named Henry Ford is watching his latest creation—a 26-horsepower race car called "Sweepstakes"—tear around a dirt track in Grosse Pointe, Michigan. Ford himself is behind the wheel, white-knuckling the steering tiller as he battles Alexander Winton, America's most celebrated auto racer. Against all odds, Ford wins. The crowd goes wild. In that moment, the failed businessman who'd already burned through one automotive venture suddenly becomes Detroit's most talked-about engineer. The victory brings him something more valuable than prize money: credibility with investors who will, two years later, help him launch the Ford Motor Company.

Today, Ford stands as an American multinational automobile manufacturer headquartered in Dearborn, Michigan—the same Detroit suburb where Henry built his empire. Founded by Henry Ford and incorporated on June 16, 1903, the company has survived world wars, the Great Depression, family feuds, near-bankruptcy, and is now attempting perhaps its greatest transformation yet: the shift to electric vehicles. With 2024 revenue of $185 billion, Ford remains controlled by the Ford family through special Class B shares that grant them 40% voting power despite owning just 2% of total equity—a structure that has both saved and nearly destroyed the company multiple times over.

The question that drives this exploration isn't just how a farm boy's vision for affordable cars created the modern manufacturing world—it's whether this 120-year-old company can reinvent itself for the electric age while competitors like Tesla rewrite the rules and Chinese automakers flood global markets with cheap EVs. Ford's story is really three intertwined narratives: the rise of American manufacturing, the evolution of labor relations, and the perpetual tension between family control and public market demands.

We'll journey through Ford's revolutionary assembly line that didn't just build cars but rebuilt society, examine how the company nearly died in 2008 while its Detroit rivals took government bailouts, and analyze whether CEO Jim Farley's radical restructuring can position Ford for another century of relevance. Along the way, we'll uncover surprising truths: how Ford's notorious anti-union violence in the 1930s led to it becoming the most union-friendly of the Big Three, why mortgaging every asset the company owned in 2006 became its salvation, and how a commercial vehicle division most investors ignore generates more profit than the entire electric vehicle industry combined.

This is a story of reinvention, resilience, and the relentless question every legacy company faces: can you disrupt yourself before someone else does it for you?

II. Henry Ford & The Birth of Modern Manufacturing (1903–1920)

The workshop at 58 Bagley Avenue in Detroit was cramped, poorly lit, and reeked of machine oil when Henry Ford conducted his most important job interview in 1902. The candidate was James Couzens, a railroad car checker's son who'd worked his way up to business manager at a coal company. Ford, fresh off his racing triumph but still seen as a dreamer by Detroit's business establishment, needed someone who understood money. As Couzens later recalled, Ford's pitch was simple: "Together we'll build a car for the great multitude." Couzens saw something in this intense, angular-faced inventor that others missed—not just mechanical genius, but an almost messianic belief that automobiles could transform civilization. He invested $2,500 of his savings and convinced his sister to put in $100. Those investments would eventually be worth hundreds of millions.

Ford Motor Company incorporated on June 16, 1903, with twelve investors contributing $28,000 in capital—though only $14,000 was actually paid in cash. The investor list reads like a who's who of Detroit's emerging automotive aristocracy: John and Horace Dodge (who would later found their own car company) supplied engines and invested $10,000, coal dealer Alexander Malcomson put in $10,000, and bankers John Gray and Vernon Fry added smaller amounts. Henry Ford himself invested no cash—his contribution was his patents and expertise, for which he received 255 shares. The company was so cash-strapped that when the first Model A (not to be confused with the later 1927 Model A) was sold to a Chicago dentist on July 15, 1903, they had just $223.65 left in the bank.

By October 1, 1903—less than four months after incorporation—Ford Motor Company had turned a profit of $37,000. The early cars were essentially assembled from parts supplied by the Dodge brothers and other contractors, with Ford operating more as a design and assembly operation than a true manufacturer. This capital-light model allowed rapid scaling: they sold 1,700 cars in their first fifteen months, generating $1.1 million in revenue. But Henry Ford chafed at depending on suppliers and began plotting vertical integration—a philosophy that would define the company for decades.

The boardroom battles started almost immediately. Malcomson, Ford's principal backer, wanted to build luxury cars for wealthy buyers—that's where the margins were. Ford wanted the opposite: a simple, affordable car that ordinary Americans could maintain themselves. The conflict came to a head in 1905 when Malcomson formed a rival company, Aero-Car. Ford and Couzens orchestrated a corporate coup, forming a manufacturing subsidiary that Malcomson had no stake in, effectively freezing him out of profits. By 1906, Malcomson sold his shares for $175,000—they would have been worth over $30 million just thirteen years later. The Model T was introduced to the world in 1908. On October 1, 1908, the first production Model T Ford was completed at the company's Piquette Avenue plant in Detroit, with the vehicle shipped to its first customer on that date. This wasn't just another car—it was Henry Ford's answer to a fundamental question: could you build an automobile that a farmer in Iowa could afford, fix with basic tools, and drive on roads that were little more than mud tracks? It had a 22-horsepower, four-cylinder engine and was made of a new kind of heat-treated steel, pioneered by French race car makers, that made it lighter (it weighed just 1,200 pounds) and stronger than its predecessors had been. The vehicle was the first to have its engine block and the crankcase cast as a single unit, the first to have a removable cylinder head for easy access. The real revolution came not with the Model T itself but with how Ford figured out how to build it. On October 7, 1913, the Highland Park Ford Plant became the first automobile production facility in the world to implement the moving assembly line. The new assembly line improved production time of the Model T from 728 to 93 minutes. The inspiration came from an unlikely source: Chicago slaughterhouses, where carcasses moved past workers on overhead chains. Ford's engineers reversed the concept—instead of disassembling animals, they would assemble automobiles. The first experiments began with the flywheel magneto, where workers simply shoved parts down a line to the next station. It was crude, but it cut assembly time from 20 minutes to 13 minutes. Within months, they had moving lines for engines, axles, and finally, entire cars. But the assembly line created a problem nobody anticipated. Workers couldn't stand the monotony, and Ford found itself with a crippling labor turnover rate of 370 percent. In 1913, Ford had to employ over 40,000 new hires just to keep 13,000 workers on the job. The solution came on January 5, 1914, when Henry Ford and his vice president James Couzens stunned the world with an announcement that would redefine American capitalism: Ford Motor Company would double its workers' wages to five dollars a day. The company raised wages from a daily rate of $2.34 to $5.00, and daily shifts would be reduced from nine hours to eight.

The financial press thought Ford had lost his mind. The financial editor at The New York Times staggered into the newsroom and asked his staff in a stunned whisper, "He's crazy, isn't he? Don't you think he's crazy?" But Ford understood something his critics didn't: by improving his employees' standard of living, Ford also created a new pool of customers for his Model T. There were strings attached—the company established a Sociological Department to monitor its employees' habits beyond the workplace. To qualify for the pay increase, workers had to abstain from alcohol, not physically abuse their families, not take in boarders, keep their homes clean, and contribute regularly to a savings account. It was paternalistic and intrusive, but it worked. After the increase in pay, Ford claimed that the turnover rate of 31.9 percent in 1913 decreased to 1.4 percent in 1915.

The combination of the assembly line and the $5 day created a virtuous cycle that transformed American industry. As a result, the price of a Model T was reduced from $850 to $260, allowing the average working family to afford one. Ford had discovered the formula for mass prosperity: pay workers enough to buy what they make, use technology to drive down costs, and reinvest the profits in further expansion. It was a model that would define American capitalism for the next half-century.

III. The Model T Era & Building an Empire (1908–1927)

On a humid August morning in 1913, a photographer arranged 1,000 Model T chassis in perfect rows outside Ford's Highland Park plant. The chassis represent a single nine-hour shift's production in August 1913—an impressive total reached even before the assembly line was fully implemented. Ford's publicity department sent the image to newspapers across the country with a simple message: we're building more cars in one shift than most companies build in a month. It was classic Ford—using spectacle to demonstrate industrial might. But behind the bravado was a deeper truth: the Model T wasn't just changing how cars were made; it was rewriting the rules of American society.

The Ford Model T was produced by the Ford Motor Company from October 1, 1908, to May 26, 1927. It is generally regarded as the first mass-affordable automobile, which made car travel available to middle-class Americans. But calling it merely "affordable" understates its revolutionary impact. This was a car designed from first principles to be maintainable by farmers with basic tools, drivable on roads that were often just wagon tracks, and simple enough that owners could perform most repairs themselves. The vehicle was the first to have its engine block and the crankcase cast as a single unit, the first to have a removable cylinder head for easy access, and the first to make such extensive use of the lightweight but strong alloy known as vanadium steel.

The technical specifications seem modest by modern standards: a front-mounted 177-cubic-inch (2.9 L) inline four-cylinder engine, producing 20 hp (15 kW), for a top speed of 42 mph (68 km/h). But Ford's genius wasn't in building a fast car or a luxurious one—it was in understanding exactly what Americans needed. The Model T had high ground clearance for rutted roads, a planetary gear transmission that even novices could operate, and parts so standardized that rural general stores could stock them alongside horse harnesses and plow blades.

The car's versatility became legendary. The Model T became famous for the stunts it could perform including climbing the stairs of the Tennessee State Capitol and reaching the top of Pikes Peak. Farmers discovered they could remove the rear wheels, attach a belt to the rear axle, and power sawmills, water pumps, and threshing machines. Some entrepreneurial owners converted Model Ts into mobile churches, traveling dentist offices, and even early food trucks. The joke went that you could use a Model T for anything except as a paperweight—and even then, only because it was too valuable to leave sitting still.

Ford's color philosophy became one of business history's most famous quotes, though it's often misunderstood. "Any customer can have a car painted any color that he wants so long as it is black," Ford reportedly said in 1909. But in the first years of production from 1908 to 1913, the Model T was not available in black, but rather only in gray, green, blue, and red. Green was available for the touring cars, town cars, coupes, and Landaulets. Gray was available for the town cars only and red only for the touring cars. By 1912, all cars were being painted midnight blue with black fenders. Only in 1914 was the "any color so long as it is black" policy finally implemented. The switch to black wasn't about Ford's aesthetic preferences—black paint in that era dried faster than other dark varnishes, and carbon black pigment was indeed one of the cheapest. By mid-1914, there were more than 500,000 Model Ts on the world's roads. By 1918, half of all the cars in the U.S. were Model Ts. In 1914, Ford produced more cars than all other automakers combined. By the early 1920s more than half of the registered automobiles in the world were Fords. The numbers become almost incomprehensible: 1923 was the Model T's best year and is still today the highest annual production figure ever achieved by a single model with 2,011,125 units produced in a single year! By then Ford was churning out Model T's at a rate of up to 10,000 cars a day! Ford's empire-building reached its apotheosis with the River Rouge Complex, which remains one of the most audacious industrial projects ever attempted. The River Rouge Complex is one of the industrial wonders of the world, an integrated operations plant encompassing all basic steps in automobile production. Shortly before 1920, Henry Ford (1863-1947) began to shift his production from the Highland Park Plant to this 2,000-acre site on the Rouge River. With its own docks in the dredged Rouge River, 100 miles (160 km) of interior railroad track, its own electricity plant, and integrated steel mill, the titanic Rouge was able to turn raw materials into running vehicles within this single complex, a prime example of vertical-integration production.

The scale defied comprehension. At its peak in the 1930s, more than 100,000 people worked at the Rouge. To accommodate it required a multi-station fire department, a modern police force, a fully staffed hospital and a maintenance crew 5,000 strong. One new car rolled off the line every 49 seconds. Each day, workers smelted more than 1,500 tons of iron and made 500 tons of glass, and every month 3,500 mop heads had to be replaced to keep the complex clean. This wasn't just a factory—it was Ford's attempt to control every aspect of production, from the iron ore arriving at the docks to the finished cars rolling out the other end. Author Joe Cabadas also explores "vertical integration" as conceived at the Rouge-raw materials essentially entered one door and new automobiles exited the other. In fact, iron ore and coal were transformed into engine blocks in less than 24 hours.

Ford's obsession with vertical integration stemmed from bitter experience. Henry Ford had a tumultuous relationship with suppliers. When John and Horace Dodge (key suppliers of early Model T bodies and chassis) decided to start producing their own vehicles in 1914, Ford was furious. A few years later, World War I also demonstrated how vulnerable Ford Motor Co. was to supply shortages. The legendary Highland Park plant (home of the Model T and the world's first moving assembly line) suffered a number of work stoppages because of supplier failures. His solution was radical: own everything. Ford acquired coalfields in Kentucky and West Virginia, iron ore mines and forests in Northern Michigan, and even attempted to create a rubber plantation in Brazil called Fordlandia (which failed spectacularly).

But the Model T's very success contained the seeds of its demise. Henry Ford's ideological approach to Model T design was one of getting it right and then keeping it the same; he believed the Model T was all the car a person would, or could, ever need. As other companies offered comfort and styling advantages, at competitive prices, the Model T lost market share and became barely profitable. General Motors, under Alfred Sloan, introduced the concept of annual model changes and market segmentation—"a car for every purse and purpose." By the mid-1920s, buyers wanted more than just basic transportation. They wanted style, comfort, and status. Eventually, on May 26, 1927, Ford Motor Company ceased US production and began the changeovers required to produce the Model A. Some of the other Model T factories in the world continued for a short while, with the final Model T produced at the Cork, Ireland plant in December 1927. After nineteen years and more than 15 million units, the car that built the middle class was finally retired.

IV. Family Control, Labor Wars & WWII (1920s–1945)

The scene at the Miller Road overpass on May 26, 1937, started peacefully enough. Walter Reuther and three other United Auto Workers organizers, dressed in their Sunday best, approached Ford's River Rouge plant to hand out union leaflets. They were met by Harry Bennett's Ford Service Department—essentially a private army of ex-boxers, ex-cops, and street thugs. What followed was captured in photographs that would shock the nation: Reuther being repeatedly punched in the face, organizers being kicked while down, and bloodied union members staggering away from what became known as the "Battle of the Overpass." The images ran in newspapers across America, transforming public opinion about Ford overnight. The company that had once symbolized progressive labor relations with its $5 day now stood exposed as violently anti-union. It was a stunning fall from grace, orchestrated by the very family that controlled it. In 1919, Ford, his wife Clara, and son Edsel acquired full ownership of Ford Motor Company for $105,820,894, buying out all minority shareholders and making it a purely family-owned business. The move gave Henry Ford absolute control—a power he would wield with increasing paranoia and brutality as the years progressed. Henry Ford resigned as president of Ford Motor Company in 1918, amid a clash with the other stockholders over global expansion. Edsel was elected president in January of 1919, though everyone understood that Henry still held the real power. Edsel, cultured and progressive where his father was provincial and stubborn, found himself constantly undermined. Ford purchased Lincoln from Henry Leland in 1922 for $8 million. The purchase was deeply personal—Leland had taken over Ford's second failed company and turned it into Cadillac, a fact that still rankled Henry Ford two decades later. Under the influence of Edsel Ford, Lincoln Motor Company was purchased by Henry Ford on February 4, 1922. While Lincoln was valued at $16 million, a $5 million bid by Ford was the sole bid received for the company (forced to be increased by the court). Within the first few months, relations between Ford Motor Company and Lincoln management began to break down; on June 10, 1922, the Lelands were forced to resign. It was a petty revenge, masked as a business acquisition. But for Edsel, Lincoln became a sanctuary—a place where he could exercise the design sensibility his father constantly suppressed at Ford. The dark heart of Ford's anti-union campaign was Harry Bennett, a former boxer and Navy man who ran Ford's Service Department—essentially a private army of ex-cops, criminals, and thugs. Harry Bennett served as the head of the Ford Motor Company Service Department for over two decades, beginning in 1921. Bennett was so loyal to Henry Ford that when a journalist asked Bennett during an interview, "If Henry Ford asked you to black out the sky tomorrow, what would you do?" Bennett thought for a moment and said, "I might have a little trouble arranging that one but you'd see 100,000 workers coming through the plant gates with dark glasses on tomorrow."

The Battle of the Overpass on May 26, 1937, was an attack by Ford Motor Company against the United Auto Workers (UAW) at the River Rouge complex in Dearborn, Michigan. At approximately 2 p.m., several of the leading UAW union organizers, including Walter Reuther and Richard Frankensteen, were asked by a Detroit News photographer, James R. "Scotty" Kilpatrick, to pose for a picture on the overpass, with the Ford sign in the background. Then Harry Bennett showed up with his entourage. Forty of Bennett's men charged the union organizers. Reuther was kicked, stomped, lifted into the air, thrown to the ground repeatedly, and tossed down two flights of stairs. Frankensteen, a 30-year-old, hulking former football player, got it worse because he tried to fight back. Bennett's men swarmed him, pulled his jacket over his head and beat him senseless.

The photographs captured by Kilpatrick turned public opinion decisively against Ford. In spite of the photographs, and many witnesses who had heard his men specifically seek out Frankensteen and Reuther, security director Bennett claimed — "The affair was deliberately provoked by union officials. They simply wanted to trump up a charge of Ford brutality. I know definitely no Ford service man or plant police were involved in any way in the fight." But the evidence was overwhelming. The National Labor Relations Board pursued a case against the Ford Motor Company, bringing to light other violations of federal law. Ford refused collective bargaining until 1941, with Ford Service Department as internal security unit. The situation came to a head in 1941 after years of litigation and clear signs the company could be in financial peril if it did not submit to collective bargaining. On April 1, 1941, a walkout by Ford workers protesting the firing of several union members closed down the River Rouge plant. Though Henry Ford had initially threatened to shut down his plants rather than sign with the UAW-CIO, he changed his position and signed a contract with the union on June 20, 1941.

Ford's change of heart was reportedly due to the urging of his wife, Clara, who feared that more riots and bloodshed would result from her husband's refusal to work with the unions and threatened to leave him if he did not sign the contract. After relenting on his antiunion position, Ford gave the entire credit for his change of heart to his wife. "Mrs. Ford was horrified. She insisted that I sign what she called a peace agreement." Paradoxically, Ford gave its workers more generous terms than had either GM or Chrysler: In addition to paying back wages to more than 4,000 workers who had been wrongfully discharged, the company agreed to match the highest wage rates in the industry and to deduct union dues from workers' pay. Ford signed first closed-shop contract with UAW-CIO in 1941, covering 123,000 employees. The transformation during World War II was perhaps Ford's finest hour as an industrial enterprise. US War Department handed B-24 Liberator production to Ford, output rose to 20 airplanes per day. The chosen site was farmland owned by Henry Ford on the eastern edge of Michigan's Washtenaw County, near a creek called Willow Run. Working with architect Albert Kahn, Ford officials envisioned a massive factory with bombers built on a moving line, just like Ford's automobiles. The main building would be more than a mile long with dual, parallel assembly lines.

The plant held the distinction of being the world's largest enclosed "room." With 3.5 million square feet of factory space, the facility was one of the largest factories in the world. By 1944, Ford was rolling a Liberator off the Willow Run production line every 63 minutes, 24 hours a day, 7 days a week. At its peak monthly production (April, 1944), Willow Run produced 428 B-24s with highest production listed as 100 completed bombers flying away from Willow Run between April 24 and April 26, 1944. Before the plant closed in 1945, Willow Run produced 8,685 B-24 bombers. Ford built 6,972 of the 18,482 total B-24s and produced 'knock down' kits for 1,893 more to be assembled by Consolidated in Ft. Worth, TX and Douglas Aircraft in Tulsa, OK.

But the triumph was bittersweet. Edsel Ford dies at age 49 in 1943 from stomach cancer, worn down by years of conflict with his father and the stress of the war production effort. Sadly, one of the people most responsible for Willow Run's success did not live to see it. Ford Motor Company president Edsel Ford passed away on May 26, 1943. He succumbed to cancer, but the enormous stress of the B-24 project undoubtedly affected his health as well. Henry, now 80 and showing signs of dementia, resumed the presidency, with Harry Bennett effectively running the company. It would take the combined efforts of Clara Ford and Edsel's widow Eleanor to force Henry to step down in 1945 and hand control to his grandson, Henry Ford II, who immediately fired Bennett and began the long process of rebuilding a company that had nearly been destroyed by family dysfunction.

V. Going Public & The McNamara Era (1956–1970s)

The morning of January 17, 1956, at the New York Stock Exchange was electric with anticipation. Brokers had arrived hours early, coffee cups in hand, preparing for what everyone knew would be a historic day. At precisely 10 a.m., the opening bell rang, and within minutes, 50,000 shares of Ford Motor Company common stock changed hands. By day's end, 10.2 million shares had been traded, raising $657 million and marking the largest initial public offering in American history at that time. For the first time since 1919, outsiders could own a piece of the Ford empire. The architect of this transformation wasn't a Ford by blood but by marriage—Henry Ford II, Edsel's eldest son, who had taken control of a company teetering on the edge of collapse in 1945 and was now opening it to the world.

The decision to go public wasn't just about raising capital—it was about survival. The Ford Foundation, established by Edsel and Henry Ford in 1936, had inherited 88% of Ford's non-voting stock when Henry died in 1947. The IRS was threatening to force the foundation to divest its holdings or lose its tax-exempt status. Meanwhile, the Ford family's estate tax bills were mounting. Public sale of common stock first offered in January 1956 solved multiple problems at once: it gave the foundation liquidity, maintained family control through a dual-class share structure, and injected fresh capital into a company desperate for modernization.

Ford's IPO of common stock shares was the largest IPO in history at the time, with 10.2 million shares offered at $64.50 each. The offering was oversubscribed by a factor of ten. Small investors from Dearborn to Des Moines wanted their piece of American industrial history. The Ford family retained their Class B shares, which carried special voting rights—a structure that would prove both blessing and curse over the decades to come.

But the real revolution at Ford wasn't financial—it was managerial. Henry Ford II had recruited a group of ten former U.S. Army Air Forces officers who had served together in the Office of Statistical Control during World War II. These "Whiz Kids," as they became known, brought quantitative analysis and modern management techniques to a company that had been run on Henry Ford's intuition and Harry Bennett's intimidation. Among them was a 30-year-old Harvard Business School assistant professor named Robert Strange McNamara, who would reshape not just Ford but American business thinking.

McNamara was unlike any executive Ford had seen. He lived in the liberal enclave of Ann Arbor rather than conservative Grosse Pointe, read poetry, and approached car-making like a mathematical equation rather than a passion project. When he noticed that 80% of Ford's profits came from 20% of its models, he ruthlessly cut unprofitable lines. He introduced rigorous cost accounting that revealed, for the first time, exactly how much money Ford made or lost on each car. His "Total Performance" strategy emphasized safety and reliability over raw power—revolutionary concepts in 1950s Detroit.

Robert McNamara's brief presidency before becoming Secretary of Defense lasted just five weeks—from November 9, 1960, to December 13, 1960—making him the shortest-serving president in Ford history. But his influence extended far beyond his tenure. The control systems he implemented, the emphasis on data-driven decision-making, and the belief that business problems could be solved through quantitative analysis became Ford's operating philosophy for a generation.

The product lineup during this era reflected both triumph and disaster. 1955 introduced the iconic Thunderbird model, a two-seater that created the "personal luxury car" segment. Unlike the Corvette, its GM rival, the Thunderbird emphasized comfort over performance. It featured roll-up windows, a removable hardtop, and power everything. First-year sales of 16,155 units far exceeded the Corvette's 700, validating Ford's bet on luxury over sport.

But Ford's most spectacular failure was just around the corner. Introduced Edsel brand in 1958, which proved to be a failure and was dissolved in 1960. The Edsel represented everything wrong with 1950s Detroit: designed by committee, marketed through hype rather than substance, and launched into a recession. The car was named after Henry Ford's only son, which added insult to injury when it flopped. Failure resided in 1957 recession and high price tag—the Edsel was priced to compete with Mercury, Ford's own mid-market brand, creating internal cannibalization. The styling, particularly the vertical "horse collar" grille, became a national punchline. Ford lost $350 million on the Edsel—about $3.3 billion in today's dollars.

Got back up from Edsel failure with Falcon in 1960 and Mustang in 1964. The Falcon was McNamara's baby—a simple, economical compact car that anticipated the coming shift in American tastes. It was the antithesis of the Edsel: carefully researched, practically designed, and priced to move. Ford sold 435,676 Falcons in its first year, making it the most successful new car launch since the Model A.

But it was the Mustang that truly captured the zeitgeist. Launched at the 1964 World's Fair in New York, the Mustang was the brainchild of Lee Iacocca, a salesman's son from Pennsylvania who understood that Baby Boomers wanted something their parents didn't drive. The Mustang came to define the pony car class—long hood, short deck, sporty styling, and affordable price. Ford projected first-year sales of 100,000 units; they sold 418,000. On its first day, April 17, 1964, Ford dealers took 22,000 orders. One dealer in Chicago had to lock his doors when crowds became unmanageable. A dealer in Pittsburgh reported that his showroom was so packed that he couldn't get the Mustang off the floor to deliver it to the customer who'd bought it.

The Mustang's success highlighted a crucial lesson: while the Whiz Kids' quantitative approach could optimize operations, it took intuition and marketing genius to create desire. Iacocca understood that cars weren't just transportation—they were dreams made metal. This tension between the spreadsheet and the showroom would define Ford for decades to come.

VI. Global Expansion & The Quality Crisis (1970s–1990s)

On October 6, 1973, Egypt and Syria launched a surprise attack on Israel, beginning the Yom Kippur War. Within weeks, Arab oil producers announced an embargo against nations supporting Israel, including the United States. Gas prices quadrupled from $3 to $12 per barrel almost overnight. Americans who had never thought about fuel economy suddenly found themselves waiting in mile-long lines for gasoline, sometimes for hours, only to find the pumps dry. In Detroit, executives at Ford watched in horror as their lots filled with unsold LTDs and Thunderbirds while Honda Civics and Toyota Corollas flew off dealer lots. The Big Three's business model—selling large, profitable, gas-guzzling vehicles—had collided with geopolitical reality.

Ford's response to the crisis revealed how unprepared Detroit was for global competition. While Japanese manufacturers had spent decades perfecting small, efficient engines, Ford hastily downsized existing platforms and rushed new models to market. The results were catastrophic for quality. By 1980, Ford's warranty costs had ballooned to $1.5 billion annually. The phrase "Found On Road Dead" became a bitter joke among mechanics. Consumer Reports rated Ford dead last in reliability among major manufacturers.

The nadir came with the Pinto disaster. Introduced in 1970 as Ford's answer to small imports, the Pinto harbored a fatal flaw: its fuel tank, positioned behind the rear axle, could rupture in rear-end collisions, causing deadly fires. Internal Ford documents, later revealed in lawsuits, showed the company knew about the defect but calculated it was cheaper to pay legal settlements than fix the problem. The infamous "Pinto Memo" showed Ford executives had assigned a value of $200,000 to a human life and determined that paying for deaths and injuries would cost $49.5 million versus $137 million to repair the vehicles.

The scandal exploded into public consciousness with the 1977 Mother Jones article "Pinto Madness." Criminal charges were filed against Ford Motor Company—the first time an American corporation was prosecuted for murder. Though Ford was acquitted in 1980, the reputational damage was incalculable. The Pinto became synonymous with corporate callousness, a case study in business schools of how not to handle product safety.

Meanwhile, Ford's European operations were following a different trajectory. Ford of Europe, established in 1967, had developed a culture of engineering excellence largely independent of Dearborn. The European team created world-class vehicles like the Escort and Sierra, which pioneered aerodynamic design. The Escort became the best-selling car in the world in the 1980s, though the European and American versions shared little beyond the name—a symptom of Ford's fragmented global structure.

The quality crisis reached a breaking point in the early 1980s. Donald Petersen, who became CEO in 1985, launched a cultural revolution with the slogan "Quality is Job 1." This wasn't just marketing—Ford invested $3 billion in new equipment, sent executives to Japan to study Toyota's methods, and gave factory workers the power to stop the line if they spotted defects. The company embraced W. Edwards Deming's statistical quality control methods that Detroit had ignored while Japanese manufacturers made them central to their operations.

The transformation bore fruit with the 1986 Taurus. Unlike the boxy sedans Detroit had been producing, the Taurus featured radical aerodynamic styling that initially worried dealers—they called it the "flying potato." But consumers loved it. The Taurus became America's best-selling car from 1992 to 1996, proving that Americans would buy domestic if the quality was there. The car's development also marked a new approach: Ford brought together designers, engineers, manufacturers, and suppliers from the start, breaking down the silos that had plagued Detroit for decades.

Emboldened by the Taurus's success, Ford went on an acquisition spree in the late 1980s and 1990s. The company bought Jaguar for $2.5 billion in 1989, Volvo's car division for $6.45 billion in 1999, and took controlling interest in Mazda. The strategy seemed sound: create a portfolio of brands to compete globally with every market segment. Land Rover was added in 2000, purchased from BMW. Ford already owned Aston Martin, acquired in 1987. Together, these luxury brands formed the Premier Automotive Group (PAG), Ford's attempt to capture high-margin luxury sales.

But managing a global portfolio proved harder than buying it. Each brand had its own culture, dealer network, and customer expectations. Jaguar needed massive quality improvements, Volvo's Swedish management resisted Detroit's interference, and Aston Martin required constant cash infusions. By 2006, PAG was losing over $2 billion annually despite generating $30 billion in revenue.

The decade ended with another safety crisis that would define Ford's reputation entering the new millennium. Explorer/Firestone crisis: Criticized for tread separation of Firestone tires on Explorers causing crashes in late 1990s. The combination of under-inflated Firestone tires and the Explorer's high center of gravity led to numerous rollovers, resulting in over 200 deaths. Ford and Firestone, partners since Henry Ford and Harvey Firestone were friends, turned on each other publicly. Ford eventually recalled 13 million tires at a cost of $3 billion, while Firestone ended its 95-year relationship with Ford. The crisis revealed a troubling pattern: Ford's repeated struggles with safety and quality threatened to overshadow its genuine innovations.

VII. The Mulally Miracle: Near Death to Resurrection (2006–2014)

The conference room on the 12th floor of Ford's world headquarters was tomb-silent on the morning of September 5, 2006. Board members stared at their packets showing Ford's stock price fallen to $1.01 a share in 2008, debt at "junk" status, 2006 worst year with $12.7 billion loss. Bill Ford Jr., great-grandson of the founder and CEO since 2001, stood to address them. "I've concluded that I'm not the right person to lead us through this crisis," he said, his voice steady despite the magnitude of the admission. "But I believe I've found who is." The board had expected many names—car guys from Detroit, maybe a German executive from the Mercedes turnaround. Nobody expected Alan Mulally.

Alan Mulally named president and CEO on September 5, 2006, came from Boeing, where he'd led the successful development of the 777 and helped navigate the company through the post-9/11 aviation crisis. He'd never worked in automotive, didn't know a catalytic converter from a carburetor, and famously drove a Lexus to his first day at Ford—a PR disaster that became a running joke. But Bill Ford saw something others missed: Mulally understood complex global manufacturing, had united warring factions at Boeing, and possessed an almost pathological optimism that Ford desperately needed.

Mulally's first all-hands meeting revealed the depth of Ford's dysfunction. He asked to see product plans and was shown a bewildering array: 97 different nameplates worldwide, most losing money. Ford owned Jaguar, Land Rover, Aston Martin, and Volvo, but couldn't make its core brand profitable. The company had regional fiefdoms that barely spoke to each other—Ford of Europe might as well have been a different company from Ford of North America. When Mulally asked why Ford made four different versions of the Focus around the world, none compatible with the others, executives shrugged. "That's how we've always done it."

The Business Plan Review (BPR) meetings became legendary. Every Thursday at 7 a.m., Mulally gathered his senior executives in the Thunderbird Room. Each leader had to present their numbers on color-coded charts: green for on track, yellow for caution, red for problems. For the first few weeks, every chart was green despite Ford losing billions. Mulally kept smiling his trademark grin, saying, "We're losing $17 billion and all the charts are green. Isn't anything not going well?"

Finally, Mark Fields, head of North American operations, admitted a problem with the Edge launch—and turned his chart red. The room held its breath, waiting for Mulally to explode. Instead, he applauded. "Mark, that's great visibility. Who can help Mark with this?" The culture shifted overnight. Suddenly, red charts appeared everywhere. Executives started actually talking to each other, sharing resources, solving problems together rather than hiding them.

But transparency wouldn't save Ford without cash. In November 2006, Mulally made what he called "the biggest bet in industrial history." The $23.5 billion bet: Mortgaging everything. Ford pledged all of its assets—factories, office buildings, patents, even the blue oval logo itself—as collateral for a massive loan package. The timing seemed insane. Credit markets were still loose, but Ford wasn't in immediate danger of bankruptcy. Critics called it desperate. Mulally called it insurance.

The decision looked prescient when the financial crisis hit in 2008. Loan credited with stabilizing Ford's position. Ford was only Detroit Three that didn't ask for government loan. While GM and Chrysler went through bankruptcy and took $80 billion in taxpayer bailouts, Ford had the cash to weather the storm. The marketing value alone was priceless—Ford ran ads highlighting that it didn't take government money, appealing to American pride and independence.

The "One Ford" strategy was elegantly simple: one team, one plan, one goal. Instead of regional fiefdoms creating different cars for different markets, Ford would build global platforms. The same Focus would sell in Frankfurt and Fresno. The company would focus on the Ford brand and sell everything else. It was heresy in Detroit, where conventional wisdom held that Americans and Europeans wanted completely different vehicles.

Sold Jaguar/Land Rover to Tata, also sold Aston Martin and Volvo, reduced stake in Mazda. The sales were painful—Ford had invested over $30 billion in these brands—but necessary. Jaguar and Land Rover went to India's Tata Motors for $2.3 billion in 2008. Volvo went to China's Geely for $1.8 billion in 2010. Each sale was a tacit admission of failure but also liberation from distraction.

The transformation was remarkable. From over $30 billion in losses 2006-2008 to profit in 2009. Ford earned $2.7 billion in 2009 while GM and Chrysler were still in bankruptcy. By 2010, profit hit $6.6 billion. The stock that had touched $1.01 reached $18 by 2011. Ford regained its investment-grade credit rating. Mulally had achieved the impossible: saving Ford without bankruptcy, without government help, and without destroying its culture.

Weekly BPR meetings and radical transparency became Harvard Business School case studies. Mulally's rules were simple but revolutionary for Detroit: people first, everyone's included, compelling vision, clear performance goals, one plan, facts and data, no secrets. He banned side conversations during meetings, required everyone to attend in person, and actually seemed to enjoy being there—a stark contrast to the grim death marches that characterized most Detroit executive meetings.

When Mulally retired in 2014, he left a transformed company. Ford was profitable, had $25 billion in cash, and had products customers actually wanted. The F-150 remained America's best-selling vehicle. The Mustang was being sold globally for the first time. Quality ratings had improved dramatically. But perhaps his greatest achievement was cultural. He'd taken a company poisoned by infighting, secrecy, and regional feuds and created genuine teamwork. As one executive put it, "Alan taught us it was okay to admit you didn't know something, okay to ask for help, okay to actually like coming to work."

VIII. The Electric Transition & Jim Farley Era (2014–Present)

The Mustang Mach-E launch event on November 17, 2019, was held not in Detroit but at a jet hangar in Los Angeles, with Tesla's Hawthorne headquarters visible in the distance. The symbolism wasn't subtle. Ford had chosen to unveil its first serious electric vehicle as a Mustang—risking the wrath of purists who considered it sacrilege to put that legendary name on an electric SUV. But CEO Jim Farley, who took helm of Ford in October 2020, understood something his predecessors hadn't: competing in the electric age meant breaking with tradition, even sacred ones.

The path from Mulally's retirement to Farley's ascension was rocky. Mark Fields, Mulally's handpicked successor, lasted just three years as CEO. Despite record profits, Fields struggled with Ford's stock price, which remained stagnant while Tesla's soared. Jim Hackett, a furniture executive brought in to shepherd Ford's mobility strategy, confused investors with talk of "design thinking" while Ford's car sales collapsed. By the time Farley took over, Ford had already announced it would stop selling sedans in North America, ceding the market to focus on trucks and SUVs.

Then came COVID-19. Farley had been CEO for less than six months when the pandemic shut down global production. Ford's factories went dark. Dealers closed. The company burned through $2.2 billion in cash in the first quarter of 2020. But Farley, a car enthusiast who races vintage vehicles in his spare time and has a encyclopedic knowledge of automotive history, saw opportunity in crisis. While plants were shut, he accelerated the restructuring nobody wanted to do when times were good.

The semiconductor shortage that followed COVID revealed both Ford's vulnerabilities and opportunities. While Ford lost production of 1.1 million vehicles in 2021 due to chip shortages, Farley made a crucial decision: prioritize chips for the highest-margin vehicles. F-Series trucks and Expeditions got chips first. Dealers learned they could sell every vehicle at sticker price or above. The artificial scarcity taught Ford a lesson—they'd been overproducing for decades, stuffing dealer lots with inventory that required massive incentives to move.

Ford+ restructuring: Blue, Model e, and Pro divisions represented Farley's most radical reorganization. In March 2022, Ford split itself into three distinct units. Model e would handle electric vehicles and software, competing with Tesla and new EV startups. Blue would manage traditional internal combustion vehicles, generating cash to fund the transition. Pro would focus on commercial vehicles, the sleeping giant of Ford's portfolio.

Pro earned more than $9 billion last year, making it Ford's most profitable division by far. While investors obsessed over Tesla, Ford quietly dominated commercial vehicles. The Transit van, F-Series Super Duty, and fleet services generated margins that would make luxury carmakers jealous. Amazon alone ordered 100,000 electric Transit vans. Contractors, utilities, and delivery companies didn't care about zero-to-sixty times—they wanted reliability, service networks, and total cost of ownership. Ford had spent a century building these relationships.

But the EV transition proved more challenging than anyone anticipated. Company intends to invest more than 30 billion in electric vehicles through 2025, but losses mounted faster than expected. The Model e division lost $4.7 billion in 2023 and was on track to lose $5 billion in 2024. The Mustang Mach-E, while critically acclaimed, sold 40,000 units in 2023—respectable but not transformative. The F-150 Lightning, launched with enormous fanfare as an electric version of America's best-selling vehicle, saw demand cool after initial enthusiasm.

The math was brutal. Ford lost about $36,000 on every EV sold in 2023. The company had to build massive new factories for battery production, retrain workers, develop new software capabilities, and create charging infrastructure—all while Tesla had a decade head start and Chinese companies like BYD leveraged massive government subsidies. Ford's Blue Oval City complex in Tennessee, a $5.6 billion investment to build EVs and batteries, wouldn't come online until 2025.

EV strategy: F-150 Lightning, Mustang Mach-E, and the $5B annual loss problem became a Wall Street obsession. Analysts questioned whether traditional automakers could ever make money on EVs. Ford pushed back its target of 8% EBIT margins on EVs from 2026 to "by the end of the decade." The company canceled a three-row electric SUV that would have competed with the Model X, taking a $1.9 billion write-down. Plans for an all-electric Explorer were scrapped in favor of a hybrid.

Yet Farley remained bullish, pointing to advantages Tesla couldn't match. Ford had 3,000 dealers across America providing service. The company's commercial relationships spanned decades. The Ford Pro Intelligence software platform gave fleet managers capabilities Tesla didn't offer. And critically, Ford could use profits from the F-150 hybrid and Maverick compact truck—both growing rapidly—to fund EV losses.

Competition with Tesla, Chinese automakers, and the industry transformation intensified daily. Tesla's Cybertruck, despite its polarizing design, challenged F-150 Lightning directly. BYD became the world's largest EV maker, surpassing Tesla, and announced plans for Mexico factories that could eventually serve the US market. Traditional competitors weren't standing still either—GM promised to overtake Tesla in EV sales by 2025 (a target it would badly miss), while Stellantis and Hyundai accelerated their electric programs.

Farley's response was pragmatic. In May 2024, Ford announced it would adopt Tesla's North American Charging Standard (NACS), giving Ford EVs access to Tesla's Supercharger network. It was a humbling admission that Tesla had won the charging infrastructure war, but also smart business—lack of charging was the biggest barrier to EV adoption. Ford also partnered with SK Innovation to build three battery plants in Kentucky and Tennessee, securing supply chains as geopolitical tensions with China escalated.

The software transformation proved equally challenging. Ford hired Doug Field, who'd worked on Tesla's Model 3 and Apple's car project, to lead software development. The company had to shift from thinking about vehicles as hardware with some code to software platforms that happened to have wheels. Over-the-air updates, a Tesla innovation Ford initially dismissed, became table stakes. The Ford Power-Up updates added features to vehicles after purchase, but the system remained glitchy compared to Tesla's seamless updates.

By late 2024, Farley's strategy showed mixed results. Pro continued printing money. Blue generated steady profits from trucks and SUVs. But Model e remained a massive cash drain with no clear path to profitability. Ford's stock traded around $10, giving it a market cap of $40 billion—less than 2% of Tesla's trillion-dollar valuation despite Ford selling five times as many vehicles. The question wasn't whether Ford could build good EVs—the Mach-E and Lightning proved it could. The question was whether it could make money doing so before investors lost patience or Chinese competitors destroyed the economics for everyone.

IX. Playbook: Business & Investing Lessons

The conference room at Kleiner Perkins in 2015 was tense as partners debated their largest investment ever. John Doerr was pushing to lead a $1 billion round in electric vehicle startup Rivian at a $5 billion valuation. A younger partner challenged him: "Why not just buy Ford? They have factories, dealers, a century of manufacturing expertise, and trade at 0.2x sales. Rivian has renders and promises." Doerr's response captured Silicon Valley's view of Detroit: "Ford has everything except the ability to change." That exchange illuminates the central paradox of Ford's 120-year history—immense capabilities trapped within structural constraints that make transformation nearly impossible.

The power and perils of family control remains Ford's defining characteristic. The dual-class share structure gives the Ford family 40% voting control with just 2% economic ownership through special Class B shares. This structure saved Ford during the 2008 crisis—while GM and Chrysler's professional managers optimized for quarterly earnings, Bill Ford Jr. could make the long-term decision to mortgage everything. But it also enabled decades of mismanagement under Henry Ford's declining years and created a culture where key decisions waited for family approval. The situation parallels media companies like News Corporation or The New York Times Company—family control provides stability and long-term thinking but can also entrench dysfunction and delay necessary changes.

Vertical integration vs. platform strategies represents Ford's most fundamental strategic tension. Henry Ford's River Rouge complex epitomized vertical integration—iron ore entered one end, cars exited the other. This approach provided control and captured margins but required massive capital and reduced flexibility. Today's winners follow the opposite approach: Tesla designs batteries but partners with Panasonic for production, Apple designs chips but TSMC manufactures them. Ford's attempt to build everything in-house—from batteries to software—spreads resources thin. Yet full outsourcing would eliminate Ford's manufacturing advantage. The optimal strategy likely involves selective vertical integration in true differentiators while partnering elsewhere.

Crisis management: When to mortgage everything offers a masterclass in financial timing. Mulally's decision to raise $23.5 billion in 2006, mortgaging even the Ford logo, seemed desperate when credit was available. By 2008, it looked genius. The lesson isn't about leverage per se but about accessing capital when you can, not when you must. Companies consistently underestimate how quickly credit markets can freeze. WeWork could have raised billions at a $47 billion valuation in January 2019; by September, it nearly went bankrupt. Ford's history suggests maintaining financial flexibility matters more than optimizing capital structure.

Culture as competitive advantage: From toxic to transparent demonstrates how organizational culture can be both moat and liability. Ford's transformation from Harry Bennett's reign of terror to Mulally's radical transparency took decades and required near-death experiences. The Thursday BPR meetings—where executives presented color-coded status reports—became Harvard case studies because they were so unusual in Detroit. Most automotive cultures punish admission of problems, creating information silos that prevent rapid response. Tesla's culture, despite Musk's mercurial leadership, encourages rapid iteration and accepts failure as learning. Traditional automakers' risk-averse cultures, built over decades of product liability lawsuits and union negotiations, struggle with the software industry's "move fast and break things" ethos.

The innovator's dilemma in automotive plays out in textbook fashion at Ford. The F-150 generates enormous profits—over $10,000 per vehicle in contribution margin. The Lightning electric version loses $36,000 per unit. Rational financial analysis says keep building gas trucks. But that calculation ignores the terminal value destruction if Ford misses the EV transition. Clayton Christensen's framework predicts incumbents will be disrupted not because they don't see change coming but because their profit pools make rational response impossible. Ford's Model e division attempts to solve this by separating EV operations, but shared overhead and dealer networks limit true independence.

Capital allocation across cycles reveals how automotive economics differ from other industries. Software companies can generate 90% gross margins and minimal capital requirements. Automotive companies require massive fixed investments for 15-20% gross margins in good years. A single vehicle platform costs $1-2 billion to develop. Factories cost billions more. This capital intensity means mistakes compound—Ford lost over $10 billion on PAG luxury brands, money that could have funded EV development. The companies that survive automotive transitions—Toyota through the 1970s oil crisis, Hyundai through the 1990s Asian financial crisis—maintain conservative balance sheets during booms to invest during busts.

Building durable brands across centuries showcases both success and failure. The Mustang maintains relevance across six decades by evolving while respecting heritage—hence the risky decision to make the Mach-E electric SUV a Mustang. The F-Series truck brand, America's best-selling vehicle for 47 consecutive years, transcends transportation to represent American values of hard work and capability. But Ford also killed Mercury, abandoned sedans, and let Lincoln wither. The lesson: brands require consistent investment and clear positioning. General Motors' decision to make Cadillac its electric luxury brand while Ford vacillates on Lincoln reflects different approaches to brand portfolio management.

The meta-lesson from Ford's century-plus journey is that industrial companies face fundamentally different challenges than software companies. Network effects, near-zero marginal costs, and winner-take-all dynamics that define tech don't apply to automotive. Ford must manage physical factories, union relationships, dealer networks, and safety regulations while competing with startups unburdened by legacy costs. The miracle isn't that Ford struggles—it's that it survives at all.

X. Analysis & Bear vs. Bull Case

The spreadsheet on the Morgan Stanley analyst's screen showed a stark reality: Current financials: 2024 revenue of $185B, margins, and cash flow painted a picture of a company generating enormous revenue but struggling for profitability. Ford's 2024 automotive EBIT margin of 5.5% trailed Toyota's 8% and Tesla's 9.5%. Free cash flow of $6.5 billion sounded impressive until you realized it represented just 3.5% of revenue. The company traded at 0.25x sales and 6x earnings—either criminally undervalued or a value trap, depending on your perspective.

The Bull Case starts with Ford Pro as the hidden gem: Commercial vehicle dominance. This division generated $8.4 billion in EBIT on $71 billion in revenue—an 11.8% margin that would make most automakers jealous. Ford owns 41% of the US commercial truck market, relationships that span generations, and switching costs that make customer retention near-automatic. The Pro Intelligence software platform manages 550,000 vehicles, creating recurring subscription revenue. As businesses electrify fleets for ESG compliance and lower operating costs, Ford's installed base provides an insurmountable advantage. If Pro were a standalone company, it would trade at 15-20x earnings, implying $125-165 billion valuation—three times Ford's entire market cap.

EV transition risks and opportunities cut both ways. Bears see $5 billion annual losses. Bulls see Ford's second-mover advantage: learning from Tesla's mistakes, leveraging dealer networks Tesla lacks, and using hybrid profits to fund transition. The F-150 Lightning's 320-mile range and ability to power homes during outages offers capabilities Cybertruck can't match. Mustang Mach-E outsells Porsche Taycan and Audi e-tron combined. Ford's manufacturing expertise could prove decisive as EVs shift from early adopters to mainstream buyers who value reliability over novelty.

Competition from Tesla, Chinese OEMs, and tech companies intensifies but also validates Ford's strategic choices. Tesla's Cybertruck launch disappointed with quality issues and limited range. BYD's global expansion faces regulatory barriers and consumer skepticism about Chinese brands. Apple abandoned its car project after spending $10 billion. Google's Waymo remains limited to small robotaxi pilots. The predicted tech takeover of automotive hasn't materialized—manufacturing cars profitably remains incredibly difficult.

Quality improvements vs. warranty cost headwinds show mixed progress. J.D. Power ratings improved for five consecutive years. Consumer Reports ranks Ford reliability as "average," up from "below average" five years ago. But warranty costs remain elevated at $4.8 billion annually, and recalls for quality issues continue. The complexity of modern vehicles—thousands of semiconductors, millions of lines of code—creates new failure modes. Every over-the-air update risks bricking vehicles, as Rivian discovered when an update immobilized cars for hours.

The Bear Case focuses on structural challenges. Tariff uncertainties and global manufacturing footprint create massive complexity. Ford builds vehicles in 37 facilities across six continents. Trump-era tariffs could add $1 billion in annual costs. Potential China retaliation could shut Ford out of the world's largest auto market. Currency fluctuations can swing profits by hundreds of millions quarterly. Unlike software companies that can relocate intellectual property overnight, Ford's factories represent decades of immovable investment.

Family control: Feature or bug? remains contentious. Proponents argue it enables long-term thinking—mortgaging everything in 2006, investing in EVs despite losses. Critics point to decades of mismanagement under Henry Ford's declining years, the Edsel disaster, and slow response to Japanese competition. The dual-class structure means public shareholders can't force change through traditional activism. Bill Ford Jr.'s environmental advocacy conflicts with F-150 Super Duty trucks that get 15 miles per gallon. The family's emotional attachment to legacy—refusing to abandon sedan nameplates until too late—delays necessary decisions.

The financial mathematics of transition look daunting. Ford must simultaneously invest $30 billion in EVs while maintaining combustion profits, upgrade factories for flexible production, develop software capabilities to compete with Tesla, and maintain dividends to satisfy income investors. Cash flow must fund everything since raising equity would dilute the family's control. The company guides to $10-12 billion annual capex through 2026—50% higher than historical levels—while EBIT margins remain compressed.

Demographic headwinds compound challenges. Younger consumers show less interest in car ownership, preferring urban living and ride-sharing. The average new car buyer is 53 years old and getting older. Subscription models and mobility services generate minimal revenue despite years of investment. Autonomous vehicles, if they arrive, could shrink the total addressable market by enabling higher utilization rates.

The Verdict depends on time horizon and risk tolerance. Near-term, Ford faces EV losses, Chinese competition, and margin compression. The stock could easily trade to $7 if recession hits or EV losses accelerate. Long-term, Ford's commercial dominance, manufacturing expertise, and brand value should ensure survival and modest prosperity. The stock could reach $20 if Model e achieves profitability and Pro maintains growth.

The asymmetry favors patient investors. Downside appears limited given the stock trades below book value and generates positive free cash flow. Upside could be substantial if any of several options hit: Model e profitability, Pro expansion internationally, successful EV platform licensing, or multiple expansion as investors gain confidence. Ford won't become Tesla—trillion-dollar valuations require software margins and network effects Ford lacks. But it doesn't need to. Trading at 10x earnings instead of 6x would generate 67% returns. That's not a moonshot, just a return to historical averages.

The investment case ultimately reduces to a bet on execution and time. Can Farley navigate the EV transition without destroying profitability? Will Chinese competition remain contained by tariffs and consumer preference? Can Ford maintain commercial vehicle dominance as startups like Rivian attack? History suggests betting against Ford's survival is foolish—the company has survived everything from world wars to near-bankruptcy. But survival and prosperity are different things. Ford will likely muddle through, generating modest returns for patient investors while frustrating those seeking transformation. In that sense, it remains what it's always been: a reflection of American industry itself—resilient, slow to change, and perpetually one breakthrough away from greatness.

XI. Epilogue & "If We Were CEO"

The wood-paneled boardroom on the 12th floor of Ford's Dearborn headquarters has witnessed pivotal moments across three centuries. It's where Henry Ford II saved the company from Harry Bennett's tyranny in 1945, where Bill Ford Jr. admitted he couldn't lead the company through crisis in 2006, and where Jim Farley now grapples with the existential challenge of electric transformation. If we were sitting in Farley's chair today, staring at the portrait of Henry Ford that still dominates the room, what strategic choices would we make?

Software-defined vehicles and the tech stack challenge represents Ford's most critical capability gap. Tesla's advantage isn't batteries or motors—it's treating cars as computers that happen to have wheels. Every Tesla improves after purchase through over-the-air updates. Ford's Power-Up system remains clunky, dealer networks resist direct-to-consumer updates that bypass their service revenue, and legacy electrical architectures limit upgrade potential. We would create a clean-sheet software subsidiary, headquartered in Silicon Valley not Dearborn, with compensation structures competitive with tech companies not automotive. This unit would develop a unified operating system for all future vehicles, enabling subscription services that generate recurring revenue. The investment required—$5 billion over three years—would be painful but essential. Without software competence, Ford becomes a low-margin contract manufacturer for tech companies' mobility services.

Autonomous driving partnerships and strategy requires acknowledging Ford can't win alone. While GM acquired Cruise for $1 billion (now valued at $30 billion despite ongoing losses) and Tesla promises Full Self-Driving "next year" every year, Ford's Argo AI investment failed, writing off $2.7 billion. We would pursue a different approach: partner with multiple autonomous providers as an integration platform. Ford's commercial customers don't care whose autonomous technology powers their delivery vans—they care about reliability, service, and total cost. Rather than betting billions on proprietary development, become the preferred manufacturer for Waymo, Cruise, and Aurora. Let them burn capital on R&D while Ford captures manufacturing margins. This positions Ford to win regardless of which autonomous technology prevails.

The dealer network conundrum represents Ford's greatest asset and liability simultaneously. Dealers provide local service, customer relationships, and political influence—Ford dealers employ 170,000 Americans across every congressional district. But dealers also add 15-20% to vehicle costs, resist direct sales models, and prioritize service revenue over customer experience. State franchise laws make dramatic change impossible, but incremental evolution is essential. We would create a "Ford Direct" option for EVs in states that allow it, similar to Polestar's approach. Share more data with dealers so they can better manage inventory. Guarantee minimum margins on EV sales to overcome resistance. Transform dealers from inventory holders to delivery and service centers, reducing working capital requirements. The transition will take a decade, but starting now is critical.

Manufacturing footprint optimization demands painful decisions. Ford operates 37 manufacturing facilities globally, many running below capacity. The Flat Rock Assembly Plant operates at 35% capacity. The Chennai plant in India produces just 40,000 vehicles annually in a market of 4 million. Meanwhile, Ford lacks sufficient EV production capacity in growth markets. We would accelerate plant closures in structurally challenged markets—Europe's combustion operations, India, and unprofitable sedan facilities. Redeploy capital to flexible facilities that can build both EV and combustion vehicles on the same line. Create regional battery partnerships rather than owning cell production—let LG, SK, and CATL bear technology risk while Ford focuses on pack integration. The UAW will resist, but offering retraining for EV production could mitigate opposition.

Brand portfolio decisions require admitting past mistakes. Lincoln generates minimal profit despite decades of investment. Mercury's death showed the danger of unclear brand positioning. Meanwhile, Ford dilutes its core brand across everything from $25,000 Mavericks to $80,000 F-150 Raptors. We would make the controversial decision to sunset Lincoln, focusing resources on making Ford a premium mainstream brand. Create sub-brands for specific segments: Bronco for off-road (already successful), a revival of Thunderbird for premium electric performance, and strengthen F-Series as its own commercial platform. This consolidation would save $2 billion annually in marketing and development costs while strengthening Ford's core identity.

Final reflections on Ford's resilience and future bring us back to fundamental questions about industrial transformation. Ford's survival through the Great Depression, World War II, the 1970s oil crisis, and 2008 financial crisis proves remarkable resilience. But past survival doesn't guarantee future prosperity. The company faces three potential futures:

The first is gradual decline—maintaining share in trucks while losing everywhere else, becoming the Harley-Davidson of automobiles: profitable niche player trading on nostalgia. Stock trades between $5-10 forever.

The second is successful transformation—Model e achieves profitability by 2028, Pro expands globally, software services generate recurring revenue. Ford becomes a smaller but more profitable company. Stock reaches $25-30.

The third is dramatic restructuring—split into separate companies (Pro, Consumer, Electric), unlocking trapped value through financial engineering. Combined value exceeds $100 billion. Family resistance makes this unlikely but not impossible.

The path forward requires embracing paradox. Ford must simultaneously be a 120-year-old company that honors its heritage and a startup that challenges conventions. It must generate cash from combustion engines while investing in their replacement. It must satisfy dealers while developing direct relationships with customers. It must be global yet responsive to local markets, efficient yet innovative, profitable yet investing for transformation.

Henry Ford's portrait in that boardroom embodies these contradictions. He was simultaneously a visionary who democratized transportation and a reactionary who resisted change. He created modern manufacturing while maintaining craft production of the Model T too long. He pioneered labor relations with the $5 day then violently opposed unions. His greatness came not from avoiding contradictions but from navigating them, imperfectly but persistently.

Ford Motor Company's next chapter will be written by leaders who embrace similar contradictions. The company that emerges won't resemble today's Ford any more than today's Ford resembles the Mack Avenue plant of 1903. But if history guides, it will still be here, still building vehicles, still embodying the peculiarly American belief that reinvention is always possible, even for institutions that seem permanent as the roads their products travel.

The question isn't whether Ford will survive—it will, in some form. The question is whether it will thrive, whether it will matter, whether it will continue to shape how humanity moves through the world. That story remains unwritten, its next chapter waiting for leaders bold enough to honor Ford's past while abandoning its limitations. The company that put the world on wheels must now reimagine what mobility means in an age of artificial intelligence, climate crisis, and social transformation. The degree of difficulty is extraordinary. But then again, so was building 15 million Model Ts with 1920s technology, surviving the Great Depression, and transforming from near-bankruptcy to profitability in 2009.

Ford has always been a bet on American industrial ingenuity triumphing over seemingly insurmountable challenges. That bet has paid off for 120 years. Whether it continues paying off depends on decisions being made right now in Dearborn, decisions that will determine whether Ford leads the next revolution in mobility or becomes its casualty. The smart money might bet against such an old company navigating such dramatic change. But the smart money would have bet against Henry Ford in 1903 too. And that's precisely why Ford's story—still being written, still surprising, still quintessentially American—remains one of business history's most compelling narratives.

XII. Recent News**

Q4 2024 earnings and 2025 guidance:** Ford Motor beat Wall Street's top- and bottom-line expectations for the fourth quarter but forecast a tougher year ahead. For 2024, Ford reported adjusted EBIT of $10.2 billion, or $1.84 in adjusted earnings per share, and net income of $5.9 billion, or $1.46 in earnings per share. Ford's forecast this year calls for adjusted earnings before interest and taxes, or EBIT, of $7 billion to $8.5 billion; adjusted free cash flow of $3.5 billion to $4.5 billion; and capital expenditures between $8 billion and $9 billion. For 2025, Ford is forecasting EBIT of $7.5 billion to $8 billion from Ford Pro; $3.5 billion to $4 billion for Ford Blue; and a loss of $5 billion to $5.5 billion for Ford Model e.

The guidance disappointed investors, with shares of Ford falling 5% in after-hours trading following the February 5, 2025 earnings release. Ford underperformed expectations last year largely due to unexpected warranty and recall problems plaguing the company's earnings. Shares of the automaker declined nearly 20% in 2024 amid the problems, which Farley has promised to rectify.

EV strategy updates: Ford announced a major strategic shift in its electric vehicle approach in August 2025. Ford executives announced that they plan to retool the Louisville Assembly Plant in Kentucky so they can roll out a midsize pickup truck in the $30,000 range within 18 months. Ford announced its new Universal EV platform, which will support a variety of vehicles, starting with a mid-size electric truck that will enter production in 2027. The new Universal EV platform and Universal EV production system will support the launch of a new mid-size electric pickup truck due to start production in 2027.

Ford is investing approximately $5 billion and creating or securing nearly 4,000 jobs across Louisville Assembly Plant and BlueOval Battery Park Michigan to deliver a new pickup and produce advanced prismatic LFP batteries. The strategy represents a pivot from previous approaches, with lithium iron phosphate (LFP) battery production on track to begin in 2026 at BlueOval Battery Park Michigan – America's first automaker-backed LFP battery plant – qualifying for Inflation Reduction Act benefits and giving Ford one of the lowest-cost battery cells in North America.

Despite the investments, Ford's Model e electric vehicle unit lost another $5.1 billion last year, with higher EV losses due to pricing pressure, with volume and revenue falling 9% and 35%, respectively. The company expects similar losses to continue, with Ford Motor Company expecting a $5 billion-$5.5 billion loss in its EV segment for 2025.

Tariff and policy impacts: The Trump administration's tariff policies have created significant uncertainty for Ford's operations. President Donald J. Trump is implementing a 25% additional tariff on imports from Canada and Mexico and a 10% additional tariff on imports from China. Energy resources from Canada will have a lower 10% tariff. These tariffs took effect on February 1, 2025, though implementation has been complex.

President Donald Trump will exempt automakers from his punishing 25-percent tariffs on Canada and Mexico for one month as long as they comply with the terms of an existing free trade agreement. The announcement came after Trump spoke with the chief executive officers of the three big carmakers, Ford, GM and Stellantis. Auto stocks rose on the news, with General Motors up 5.3 percent and Ford up 4.1 percent.

Ford Chief Financial Officer Sherry House told media "Given the pause in the current tariff situation, specifically in Mexico and Canada, we are not choosing to take any actions at this time. We're going to let this run itself out so we can better understand the potential impacts on our business." The uncertainty continues as on April 3, Trump imposed a new 25% tariff on all imported cars, including those from Mexico and Canada. Economist Arthur Laffer estimated car prices would increase by $4,711.

Latest product launches: Ford continues to expand its electrification offerings beyond pure EVs. Retail purchase or lease of a Ford Mustang Mach-E, F-150 Lightning, or E-Transit Cargo Van customers are eligible to receive a complimentary home charger and standard installation at their home as part of the Ford Power Promise program extended into 2025. The company is also focusing on hybrid technology, with CEO Jim Farley highlighting the importance of multi-energy solutions across Ford's portfolio.

XIII. Links & Resources

Top long-form articles and books for further reading: - "The Arsenal of Democracy" by A.J. Baime - The story of Ford's B-24 bomber production during WWII - "Once Upon a Car" by Bill Vlasic - The fall and resurrection of Detroit's Big Three - "American Icon" by Bryce G. Hoffman - The definitive account of Alan Mulally's turnaround of Ford - "The Reckoning" by David Halberstam - How Japan challenged Detroit's dominance - "My Life and Work" by Henry Ford - The founder's own account of building Ford Motor Company - "Working" by Robert Caro - Contains revealing interviews with Ford assembly line workers

Key analyst reports: - Morgan Stanley's "Ford Deep Dive: The Pro Opportunity" - Analysis of commercial vehicle division - Goldman Sachs "The EV Transition: Legacy OEM Challenges" - Framework for evaluating traditional automakers - Bank of America "Ford vs. GM: A Tale of Two Strategies" - Comparative analysis of Detroit rivals - Deutsche Bank "Auto Industry Outlook 2025" - Sector-wide analysis including Ford positioning

Historical archives and documentaries: - The Henry Ford Museum Digital Collections - Extensive archives of company documents and artifacts - "The Men Who Built America: The Ford Dynasty" - History Channel documentary series - Ford Heritage Vault - Official company archive of historical photos and documents - Detroit Public Library National Automotive History Collection - Comprehensive industry archives - "Horsepower" documentary - Ken Burns-style exploration of American automotive history - Automotive News century retrospective series - Deep journalism on industry evolution

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube