National Vision Holdings: The Story of America's Value Vision Empire

I. Introduction: A Question of Value

Picture this: a family of four walks into a bright, no-fuss optical store in suburban Atlanta. Mom needs new readers. Their teenage son has outgrown his frames. Dad has been squinting through the same old pair for years because, in his words, “glasses cost too much.” An hour later, three of them walk out with new eyewear and they’ve spent under $300 total—roughly what a single designer frame might cost at the premium boutique down the road.

That moment is the promise National Vision Holdings has delivered millions of times across America: real eye care and real glasses at prices that don’t feel like punishment for having imperfect vision. From a single store in Ohio, it grew into the country’s second-largest optical retailer—and into the kind of scale business that simply shouldn’t exist in an industry where consumers have been trained to accept $400 price tags as normal.

So how did a regional, value-oriented optical chain become a billion-dollar retail empire with more than 1,200 locations?

At its core, National Vision is a massive retail operator. Through its subsidiaries, it sells eyeglasses, contact lenses, and optical accessories, and it offers eye exams through brands that show up in everyday America: America’s Best, Eyeglass World, Vista Optical, and several others, including locations in military settings and inside existing retail footprints.

But the real story isn’t the corporate structure. It’s the central riddle that defines the company:

How do you sell glasses for $79.95 when everyone else charges $400?

The answer is a masterclass in value retail—part retail arbitrage, part private equity-fueled consolidation, and part ruthless operational discipline borrowed from the most demanding partner in American commerce.

National Vision was founded in 1990 and is headquartered in Duluth, Georgia. By October 2025, it traded at $25.47 per share, with a market cap of about $2.02 billion across 79.3 million shares.

This is a story about consolidation and disruption, yes. But more than that, it’s about betting big on a simple idea: if you treat eyewear like an essential instead of a luxury, and you build the machine to deliver it efficiently, you can change what millions of people think glasses are supposed to cost.

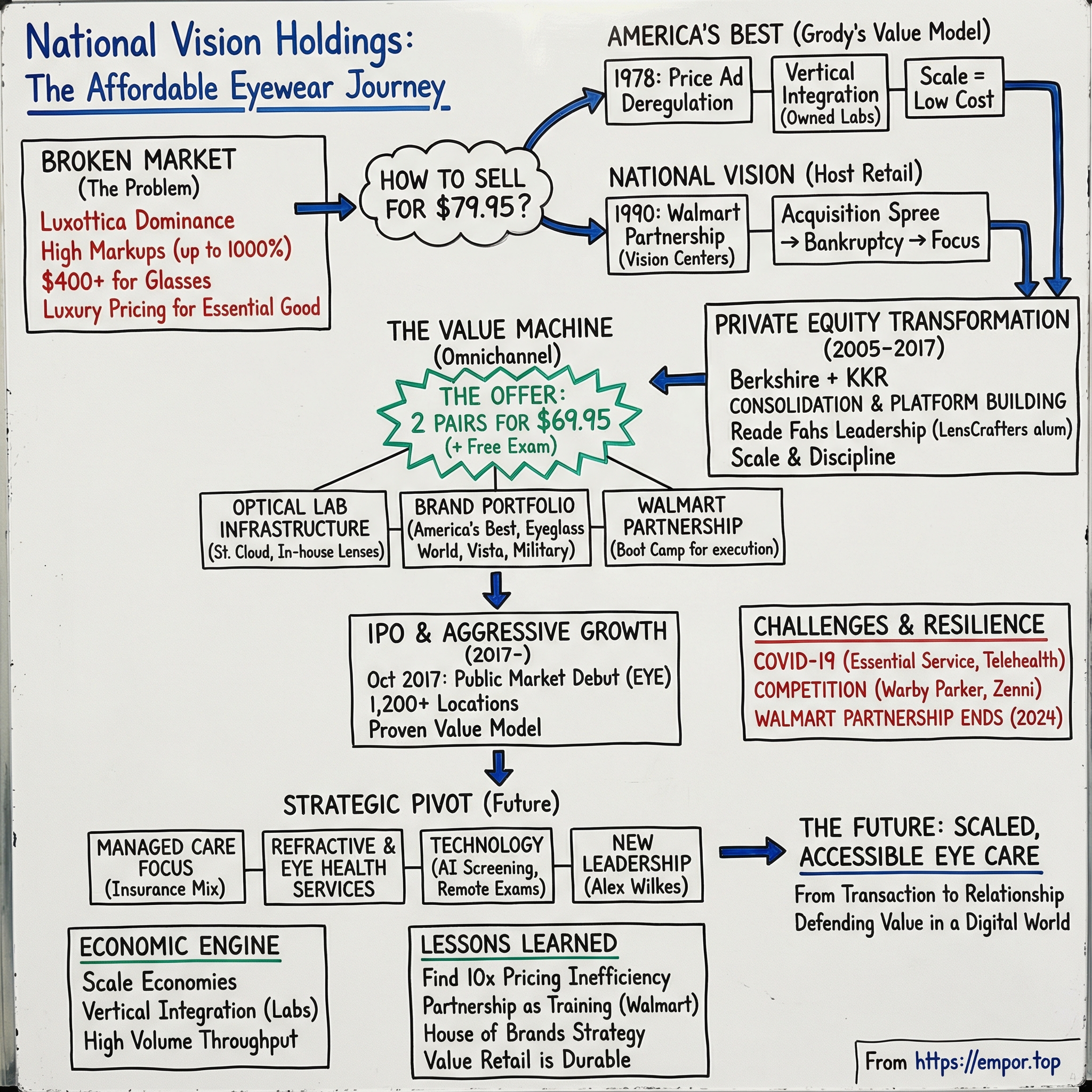

II. The Eyewear Industry: A Broken Market Begging for Disruption

To understand National Vision’s opening, you have to understand the strange economics of eyewear—a category that looks like healthcare on the surface, but often behaves like luxury fashion underneath. The result is a system where the person who needs glasses the most frequently pays the most, and where “normal” prices have been inflated for so long that they feel inevitable.

The Luxottica Problem

The modern eyewear market can’t be explained without one name: Luxottica.

Leonardo Del Vecchio founded Luxottica in 1961 in Agordo, a small town in northern Italy at the heart of the country’s eyewear manufacturing region. He started as a tool-and-die apprentice in Milan, then took those metalworking skills and aimed them at spectacle parts. By 1967, Luxottica wasn’t just supplying components—it was selling complete frames under its own brand.

From there, Luxottica executed one of the most aggressive vertical integration strategies in consumer history. After listing in New York in 1990—and later in Milan in 2000—it had both capital and a currency: its stock. It went shopping. Vogue Eyewear. Persol. LensCrafters. Ray-Ban. Sunglass Hut. OPSM. Pearle Vision. Cole National. Oakley. Deal by deal, Luxottica moved from making frames to controlling the brands people wanted, the stores where they bought them, and the shelves those stores prioritized.

The Oakley saga became the clearest signal of just how much power Luxottica had accumulated. Oakley had pushed back on pricing and distribution. Luxottica responded by pulling Oakley from Luxottica-owned retail channels, hammering Oakley’s business—then ultimately acquiring the company.

And it wasn’t only brands and storefronts. Luxottica also expanded into the plumbing of the industry: vision insurance. Through EyeMed—one of the largest vision benefits providers in the U.S.—it gained influence not just over what consumers wanted to buy, but also over what their insurance would help them pay for.

When a single ecosystem can shape brand desirability, retail availability, and reimbursement dynamics, “competition” starts to look less like a free market and more like a toll road.

The Price Illusion

If you’ve ever wondered why a few grams of plastic and metal can cost as much as a smartphone, you’re not imagining things.

In 2019, E. Dean Butler, the founder of LensCrafters, told the Los Angeles Times that Luxottica’s dominance helped enable eyewear markups that could approach 1,000%. A basic frame might retail for a couple hundred dollars while costing a tiny fraction of that to produce—single digits to low teens per unit in some estimates. In the U.S., a pair of prescription glasses commonly lands in the hundreds of dollars.

This is the trick of the category: eyewear is essential, but it’s priced like a luxury—propped up by brand licensing, controlled distribution, and a retail experience that trains customers to accept the number on the tag.

By the 2010s, Luxottica’s influence was so expansive that it was often described as controlling the vast majority of major eyewear brands. And as Luxottica’s reach grew, it increasingly intersected with another giant on the lens side: Essilor.

The Merger That Completed the Monopoly

In 2018, the European Commission approved the merger of Essilor and Luxottica. On October 1, 2018, EssilorLuxottica was officially born, creating a combined giant valued around $70 billion at the time.

Before the merger, Essilor held enormous sway over lenses; Luxottica held enormous sway over frames and retail. Together, the logic of vertical integration went from strong to nearly complete: lenses, frames, brands, stores, and a meaningful foothold in vision insurance—all under one umbrella.

And that’s the opening National Vision stepped into.

Because when one system can charge 10–20x what products cost to make—and keep doing it—there’s an inevitability to what comes next. A value player shows up, builds a machine to operate cheaper, and sells people the same essential product at a price that feels like a revelation.

That player was National Vision.

III. Founding Era & Early Years: Building Regional Value Chains

National Vision’s origin story isn’t a single founding moment. It’s a set of parallel experiments—entrepreneurs testing the same contrarian idea in different parts of the country: what if you treated glasses like a high-volume retail product instead of a luxury purchase?

Bill Grody and the Birth of Value Optical Retail

One of the cleanest early examples was America’s Best Contacts & Eyeglasses—and it starts with a regulatory shift.

In July 1978, soon after federal deregulation made it legal to advertise eyewear prices, Bill Grody—25 years old and moving fast—founded America’s Best Contacts & Eyeglasses (and its predecessor entities). Price advertising sounds like a small technicality, but it mattered: the moment you can put a price on a sign, you can compete on value in public. That was the opening.

Grody’s first store was an odd choice for a discount concept: the 15th floor of an office building on North Michigan Avenue in Chicago, right off the Magnificent Mile. But it telegraphed the point. This wasn’t a mom-and-pop practice. It was a retail business with ambition.

From 1978 through 1990, Grody reinvested earnings and expanded steadily. By 1990, America’s Best had grown to 34 locations—and, critically, it owned a full-service lens manufacturing facility. That was the real unlock. Vertical integration meant America’s Best could make lenses itself, control cost, and price aggressively in a market where many independents were buying from entrenched supply chains.

That same year, a majority stake was sold to Berkshire Partners for a reported $24 million. But Grody wasn’t done. In December 1993, he led a management-led leveraged buyout, buying back majority control for $40 million while Berkshire kept a minority position. Then in April 1997, he sold the company outright for $50 million to Chrysalis Management.

By the time Grody exited, the machine was sizable: about $103 million in revenue, roughly 1,400 employees, plus 150 independent doctors of optometry, and 100 retail stores across 25 states, the District of Columbia, and Puerto Rico. The playbook—scale plus owned manufacturing to deliver low prices—was no longer theoretical. It was proven.

National Vision's Parallel Rise

While Grody was building America’s Best, another foundational strand of the eventual National Vision story was taking shape through a very different route: host retail.

National Vision, Inc. began in 1990 as National Vision Associates, Ltd., when it entered into a master license agreement with Wal-Mart Stores, Inc. That first deal gave it the right to operate 75 vision centers inside Walmart stores. The relationship expanded quickly—first to up to 190 vision centers in 1992, then to up to 400 in 1994.

But the early Walmart footprint didn’t make the company bulletproof. In late 1997, National Vision made a strategic decision to diversify beyond host departments by acquiring freestanding optical chains. Between October 1997 and October 1998, it bought three sizable players in rapid succession: Midwest Optical, Inc. (October 1997, 51 freestanding centers across four Midwest states), Frame-n-Lens Optical, Inc. (July 1998, 150 freestanding vision centers in California and 120 vision centers inside Sam’s Clubs), and New West Eyeworks, Inc. (October 1998, 175 retail optical centers across 13 states).

It was expansion by acceleration—and it was too much, too fast. During the bankruptcy process that followed, the company closed or disposed of all freestanding stores and also shut down its host vision centers operating in Sam’s Clubs and in Meijer Thrifty Acre stores.

On May 31, 2001, the company emerged from bankruptcy as a more focused optical retailer, operating vision centers inside host departments, including Walmart and Fred Meyer locations. Upon emerging, it changed its name to National Vision, Inc.

That near-collapse became an early lesson etched into the business: growth could be powerful, but only if it was disciplined—built on execution and partnerships, not acquisition sprees.

IV. The Private Equity Era Begins: Consolidation & Platform Building

By the early 2000s, optical retail was exactly the kind of market private equity loves: thousands of small operators, a handful of regional chains, and plenty of profit hiding in inefficiency. Most of these businesses were good local cash generators—but they didn’t have the capital, systems, or scale to expand fast.

That set up the obvious play: roll up the fragments, standardize operations, and build a national platform that could buy smarter, manufacture more efficiently, and market at scale.

Berkshire Partners and the 2005 Transformation

National Vision had been operating since 1990 through its predecessor entities, but 2005 was when the story really pivoted. That year, private equity funds managed by Berkshire acquired both National Vision (NVI) and Consolidated Vision Group, Inc., the operator of America’s Best stores, and merged the two businesses, with NVI surviving.

The logic was powerful. National Vision brought the operating infrastructure and experience of running vision centers inside big-box retail. America’s Best brought the value proposition and the manufacturing muscle that made low prices sustainable. Put them together, and you had the beginnings of a truly national value optical retailer—one that could reach customers where they already shopped and serve them at a price point the rest of the industry couldn’t touch.

From there, the platform kept filling in its missing pieces. In 2009, NVI acquired the Eyeglass World store chain, then set about rebuilding it with refreshed merchandising and marketing. That same period also saw investment in the less glamorous, more important parts of the machine: a new lab in St. Cloud opened in 2009, followed by a new distribution center in 2010. And in 2011, after working together for years, NVI acquired AC Lens—its long-time partner—strengthening its e-commerce business.

Reade Fahs: The Operator Who Built the Machine

Scale and acquisitions were part of the story. The other part was leadership.

Reade Fahs led National Vision as CEO for 23 years, from early 2002 until August 2025, when he transitioned to Executive Chairman. Under Fahs, National Vision grew into one of the largest—and fastest-growing—optical retailers in the United States.

He also had the right kind of résumé for this fight. Before joining National Vision, Fahs was CEO of a European internet start-up called First Tuesday. Before that, he was Managing Director of Vision Express U.K. And earlier still, he cut his teeth inside the heart of the modern optical retail playbook: LensCrafters, where he started in 1986 and, over a decade, took on expanding responsibilities across advertising, strategy, and new product development.

That LensCrafters experience mattered. Fahs understood exactly how the premium, brand-driven model worked—and he didn’t try to copy it. His strategy was the opposite: don’t out-luxury the luxury players. Win by being the place people go when they need vision care and can’t justify a luxury price tag.

National Vision summed up that mission simply: “serving the underserved” by providing eye health care and eyeglasses to people who otherwise wouldn’t have access to affordable vision improvement.

V. The Game-Changing Walmart Partnership

The Walmart relationship actually predated the private equity era. But to understand why National Vision developed such a distinctive operating culture—so obsessed with cost, throughput, and consistency—you have to understand what it means to live inside Walmart.

National Vision had operated Vision Centers inside select Walmart stores for decades under a management and services agreement. And the relationship kept getting renewed. In July 2020, National Vision entered into an amendment to that agreement that extended the term and economics by three years, through February 23, 2024. As National Vision put it at the time: “This contract extension is just another great part of this year’s celebration of our 30th year of optical partnership with Walmart.”

Thirty years is an eternity in retail partnerships. By this point, National Vision operated 231 Vision Centers inside Walmart locations—essentially running an optical business in the aisles of the most demanding retailer on earth.

The Walmart School of Retail Excellence

Operating inside Walmart was retail boot camp. Walmart’s standards for partners are famously unforgiving: keep prices sharp, keep inventory moving, hit service metrics, and never stop hunting for cost savings. You don’t get to “brand” your way out of sloppy execution in a Walmart store. You either run a tight ship or you don’t last.

National Vision did last—and, in the process, absorbed that discipline. The Walmart environment forced a kind of operational muscle memory: a relentless focus on cost structure, high-volume throughput, and delivering value in a way that feels non-negotiable.

The other gift was traffic. Vision Centers inside Walmart benefited from built-in footfall, which helped create a more predictable stream of business. That stability mattered: it gave National Vision cash flow and experience operating at scale—two things you can use to build a much larger machine elsewhere.

The Partnership Ends

Then, in July 2023, National Vision announced that its partnership with Walmart would end in 2024. The ending covered more than just running the Vision Centers—it also included contact lens distribution and related services to Walmart and its affiliate, as well as arranging optometric services at certain Walmart locations in California.

National Vision framed it respectfully: “We value and appreciate the contributions that our partnership with Walmart has had in helping us grow National Vision over the past three decades.” And it pointed to what had changed: “With the progression of growth opportunities in our freestanding brands – America’s Best and Eyeglass World, we have become the second largest optical chain in the U.S.”

It was the end of an era. But it wasn’t the end of the story. By the time Walmart began winding down, National Vision had already used the partnership for what it was always best at: a proving ground for scale and discipline, and a platform that helped fund the rise of its own freestanding brands into the company’s future.

VI. Building the Omnichannel Value Machine

With the core pieces in place—stores, labs, distribution, and a leadership team that understood both premium optical and discount retail—National Vision’s strategy crystallized around a deceptively simple promise: make eye care feel affordable, obvious, and easy.

The "Two Pairs for $69.95" Stroke of Genius

This became the company’s calling card: two pairs of glasses, including lenses, plus a free eye exam—all for under $70.

In an industry where customers had been conditioned to expect $300 to $600 for a single pair, it didn’t just sound like a deal. It sounded like a different set of rules.

But it wasn’t a gimmick. The math worked because National Vision built the system to make it work. America’s Best Contacts & Eyeglasses became the largest buyer of designer overstock eyeglass frames in the United States. That meant it could source the kinds of frames that might sit behind glass at a premium chain—then buy them at a fraction of the cost because they were overstock. Pair that with lenses made in National Vision’s own facilities, and suddenly the “impossible” price point became a repeatable, scalable business.

Optical Lab Infrastructure

To keep prices low without sacrificing quality, National Vision invested in the most unglamorous part of the eyewear business: the back-end.

Optical labs are where lenses are cut, finished, and fit into frames. If you don’t control that step, you’re stuck paying someone else’s margin—and in this industry, that margin adds up fast. National Vision leaned the other way. It opened a new lab in St. Cloud in 2009, then added a new distribution center in 2010. By bringing more of the process in-house, it reduced reliance on outside suppliers and avoided the markups independent practices typically absorb when they outsource lens production.

The Brand Portfolio Strategy

National Vision didn’t try to build one store format for everyone. It built a portfolio—different banners for different shoppers—so it could expand without tripping over itself.

- America's Best Contacts & Eyeglasses: the value flagship, built around the “Two Pairs” offer

- Eyeglass World: a larger superstore format with a broader selection and slightly higher price points

- Vista Optical in Fred Meyer: a Pacific Northwest footprint through grocery store partnerships

- Military FirstSight: locations serving military bases with specialized programs

- DiscountContacts.com: an e-commerce platform for contact lens customers

Collectively, it let National Vision meet customers in multiple places: freestanding stores, partner retail locations, military settings, and online—without losing the one thing that made the whole machine work in the first place: value, delivered at scale.

VII. The IPO & Public Market Debut

KKR Takes the Helm

In early 2014, National Vision got a new owner with a familiar playbook: buy a platform, scale it hard, and professionalize everything that can be systematized.

National Vision and KKR announced they’d signed a definitive agreement for KKR to acquire the company from Berkshire Partners. The terms weren’t disclosed in the announcement, but the reported price was more than $1 billion. By then, National Vision was already one of the few major optical retailers focused almost entirely on value—and it was operating more than 750 low-price vision centers around the country.

KKR didn’t pitch this as a flashy bet. In a Wall Street Journal interview at the time, KKR partner Nate Taylor laid out a simple thesis: America was aging, insurers were pushing vision plans more aggressively, and glasses weren’t the kind of purchase that disappears when markets get choppy. In other words, this wasn’t just retail. It was retail tied to an everyday need.

Operationally, the early KKR years looked less like a reinvention and more like a continuation of what was already working: steady expansion and improving performance. National Vision reportedly grew sales about 7% in 2014 and 8% in the first quarter of 2015. In May 2015, it took out a loan to fund a $145 million dividend. And the growth kept coming. From 2014 to 2016, net revenue climbed from about $933 million to $1.2 billion. Over that same period, adjusted net income rose from around $9 million to $33 million, and adjusted EBITDA increased from about $82 million to $138 million.

The machine was getting bigger—and, crucially, more profitable.

October 2017: Going Public

By 2017, National Vision was ready for the next step: public markets.

The company’s IPO was framed plainly in its own language: it was offering 15.8 million shares of common stock, and there had been no public market for the shares before. The stock would trade on the NASDAQ under the symbol EYE, priced at $22.00 per share.

When National Vision debuted on October 26, it raised roughly $322 million in proceeds at that $22 price. The market response was immediate: the shares surged in their first day of trading, at one point up more than 30%, and finished the day up about 26% to $27.68. At the time of the offering, KKR owned about 77% of the business, while Berkshire Partners held about 18%.

In the months after, the stock traded as high as $43.80 by January 19, 2018.

The IPO thesis was clean and easy to understand: a proven value model, a stable revenue base supported by the Walmart partnership, room to expand in underpenetrated markets, and unit economics that looked compelling at scale. Investors didn’t just nod along. They bought in.

VIII. Aggressive Expansion & Store Growth

With public-market capital behind it, National Vision did what value retailers do when they see open runway: it sped up.

By 2015, the company hit a psychological—and operational—milestone: its 1,000th location. Not “a lot of stores.” A true national footprint. And the pace didn’t stop there. National Vision grew into one of the largest optical retailers in the U.S., with more than 1,100 stores across 44 states, plus Washington, D.C., and Puerto Rico.

The Playbook

This wasn’t random growth. It was a repeatable store-opening machine.

National Vision’s real estate strategy stayed disciplined: strip malls in growing suburban markets, chosen with demographic work and enough spacing to limit stores stealing traffic from each other. Inside, the format was standardized and built for throughput—exam rooms, wall-to-wall frames, and a small on-site lab designed to turn basic prescriptions around quickly.

The point wasn’t to feel boutique. The point was to feel easy. Get the exam. Pick the frames. Get on with your day.

Competition Intensifies

As National Vision expanded, the rest of the market didn’t sit still.

Warby Parker entered as the clean, modern rebuttal to old-school optical retail: prescription glasses online for a flat $95, lenses included. It was simple, direct, and it helped prove that the “glasses have to be expensive” story was optional. Over time, Warby Parker widened its offer to include sunglasses, contact lenses, and eye exams and vision tests, and it built a real physical presence too—more than 300 retail stores across the U.S. and Canada alongside a strong e-commerce business. By 2024, it had grown revenue to $771 million and held roughly 7% of the U.S. eyewear market.

Contacts were competitive too. 1-800 Contacts held a 10.3% market share, maintaining its lead even as Warby Parker pushed further into contact lenses starting in 2019. Around the same time, Warby Parker’s share ticked up to about 7.2%, from 6.8% in 4Q23—small moves that still signaled momentum.

National Vision’s challenge wasn’t just “grow.” It was “grow while the rest of the industry learns the same value lessons—and builds new ways to deliver them.”

IX. COVID-19 Crisis & Resilience

When the pandemic hit in March 2020, optical retail ran straight into the same wall as every other business built on foot traffic. Stores went dark, appointments disappeared, and for a moment it wasn’t clear whether people would treat new glasses as a necessity—or as something they could postpone indefinitely.

The Essential Service Question

Eye care lives in a weird middle ground: part healthcare, part retail. Vision issues don’t politely wait for a public health crisis to end. People still needed to drive, work, and read screens all day. That reality didn’t make optical immune to shutdowns, but it did create a path back sooner than, say, discretionary apparel.

For National Vision, the question quickly shifted from “how do we weather this?” to “how do we keep serving people safely?” And the answer leaned heavily on capabilities it had been building for years.

National Vision, like its competitors, moved fast into telehealth options, pushed online ordering harder, and used curbside pickup to keep the transaction alive even when stores were operating under restrictions. The omnichannel plumbing that used to feel like a nice-to-have suddenly became the business.

Recovery and Resilience

Then came the rebound.

As stimulus checks hit and communities reopened, customers returned—often with a backlog of delayed exams and broken or outdated eyewear. And in an economy full of uncertainty, National Vision’s core promise got even sharper: you could walk in needing help and walk out with a solution that didn’t wreck your budget.

The pandemic also nudged consumer behavior in ways that played into the company’s strengths. More screen time meant more people noticing eye strain and vision issues. And when households started watching every dollar, value retail didn’t just survive—it became a first stop. National Vision was built for that moment, and it showed.

X. The Refractive & Comprehensive Eye Care Push

As glasses and contact lenses started to look more and more like commodities—easy to compare, easy to price-shop—National Vision leaned into something harder to copy: care.

The company began pushing beyond the purely transactional sale and into higher-value services, especially in managed care. The margin logic is straightforward. A pair of glasses is a one-time purchase. But ongoing eye health is a relationship.

If you can become the place a patient trusts for comprehensive exams, treatment for eye conditions, and follow-up care, you’re no longer competing frame-by-frame with whoever has the lowest price that week. You’re building lifetime value—patients who come back, who stay in-network, and who see the store as part of their healthcare routine, not just a retail errand.

National Vision also started investing in technology that signals where it wants to go next. The company has received two FDA breakthrough designations for AI-based assessment tools that use retinal images from routine eye exams to help with early detection of cardiovascular disease and chronic kidney disease.

Taken together, this is National Vision trying to graduate from “cheap glasses, fast” to something broader: an eye health provider that happens to be great at value retail. If it executes, that shift doesn’t just add services—it changes the economic profile of the whole business.

XI. The Walmart Partnership Ends

When National Vision confirmed the Walmart partnership would end in 2024, it wasn’t just losing a channel. It was losing a decades-long operating backbone—and it forced a real strategic reckoning.

Walmart also notified FirstSight Vision Services, Inc., a wholly owned subsidiary of National Vision licensed as a single-service health plan in California, that as of February 23, 2024, it was ending the relationship in which FirstSight arranged optometric services at offices next to certain Walmart stores in California.

At the same time, Arlington Contacts Lens Service, Inc., another wholly owned subsidiary, notified Walmart and its affiliate that it would not renew its agreements for wholesale and e-commerce contact lens distribution and related services. National Vision expected the AC Lens agreements to terminate on June 30, 2024.

Strategic Response

National Vision responded by tightening its focus at home—on the parts of the business it directly controlled.

After a comprehensive store fleet review, the company announced in August 2024 that it had identified an initial list of underperforming locations—less than 5% of its total fleet—that weren’t meeting profitability thresholds, and it was evaluating what to do next.

The decision: take action on 43 stores. National Vision planned to close 39 of them by the end of fiscal 2026, and to convert four Eyeglass World locations into America’s Best stores by the end of fiscal 2024. The company said these moves would improve the overall health of the core business.

And with the Walmart era winding down, it also hit the brakes on expansion—at least temporarily—planning to moderate new store openings in fiscal 2025 to about 30–35 locations.

XII. Current State & Competitive Positioning

National Vision Today

After the Walmart wind-down, the cleanest way to understand National Vision is this: it’s still a scale value retailer, just with more of its destiny in its own hands.

National Vision Holdings, Inc. is one of the largest optical retail companies in the United States, with more than 1,200 stores across 38 states and Puerto Rico. Its mission is straightforward and consistent with the story so far: make eye care and eyewear more affordable and more accessible. It does that through a portfolio of brands and channels that meet customers where they already are: America’s Best, Eyeglass World, Vista Optical locations inside select Fred Meyer stores and on select military bases, plus its e-commerce site, DiscountContacts.com.

In 2024, National Vision reported $1.82 billion in revenue, up from $1.76 billion the year before.

2025 Performance

The business also showed momentum in 2025. Comparable store sales grew 6.8%, and adjusted comparable store sales grew 7.7%—the company’s 11th straight quarter of positive comparable growth. CEO Alex Wilkes credited “focused execution” on National Vision’s initiatives.

That confidence flowed into the outlook: full-year revenue guidance was raised to $1.97–$1.99 billion. National Vision pointed to continued store expansion and new product innovation, and it reported a strong third quarter of 2025, with net revenue up 7.9% to $484.4 million.

The Competitive Landscape

Even as National Vision scales, it’s doing it in one of the most competitive—and oddly concentrated—corners of retail.

On one side is the giant: EssilorLuxottica. As of 3Q24, Luxottica’s retail banners included LensCrafters, Sunglass Hut, and Oakley, and EssilorLuxottica remained the defining force in U.S. eyewear.

On the other side are the newer challengers and the pure online price engines, each pulling the market in a different direction.

EssilorLuxottica: The 800-lb gorilla is still the reference point for the entire category. With roughly 39% of the U.S. eyewear market, it pairs brand power (Ray-Ban, Oakley) with a massive retail footprint—more than 1,000 LensCrafters stores—and the kind of vertical control that lets it shape the economics of the industry. The pressure point is price: Warby Parker has built a mainstream alternative, undercutting the $300-plus “normal” optical ticket with frames priced around $95–$145 and a modern brand image.

Warby Parker: The digital disruptor that went physical. Warby Parker’s retention has stabilized at 4.3%, ahead of traditional players like National Vision at 3.6% and LensCrafters at 2.6%. That gap signals real loyalty—helped by a direct-to-consumer model and design-forward positioning that makes glasses feel like a product you want, not just something you need.

Online pure-plays: Zenni Optical is the purest expression of the internet’s promise in eyewear: extreme price compression. Zenni sells glasses starting at $6.95 and owns its factory in China. It targets the most price-sensitive customers and reported around $500 million in 2023 revenue. The tradeoff is what you’d expect—Zenni can offer huge selection and low prices, but without physical stores, it can’t replicate the in-person exam, fitting, and service experience that still drives a big share of prescription eyewear purchasing.

XIII. Business Model Deep Dive & Unit Economics

The Economic Engine

National Vision runs a straightforward play: take a category with inflated “normal” pricing, then use scale and vertical integration to offer real eyewear for less—without turning it into a race to the bottom on quality.

By 2025, the growth story wasn’t just “more stores, more transactions.” It was also about getting more value out of each visit. In Q3 2025, average ticket rose 7.1%, signaling that National Vision was leaning into merchandising and mix—not just volume—to keep the machine growing.

The Lab Advantage

The secret weapon isn’t on the sales floor. It’s in the lab.

Optical lab infrastructure is expensive to build, but once it’s running at high volume, it becomes a compounding advantage. By manufacturing its own lenses, National Vision spreads fixed costs across a massive base—and avoids the third-party lab markups that many independent optometrists have to absorb. That cost control is what makes the value promise sustainable, not promotional.

Insurance vs. Private Pay Mix

As the company put it:

"Our merchandise strategy is working, our associates are embracing new selling techniques, and our new America's Best branding is resonating with consumers. We continue to see strong traffic growth with Managed Care, Progressive and Outside Rx customers, and are very pleased with the intentional evolution of our customer mix that we expect will lead to a healthier business overall."

That “intentional evolution” matters. A larger share of managed care customers isn’t just a different way to pay—it’s a different kind of demand. Insurance-paying customers tend to buy in more predictable patterns, and they often come with higher average tickets. For National Vision, shifting the mix this way is part of a broader move from one-time bargain shopping to repeatable, relationship-driven care—while still keeping the brand anchored in value.

XIV. Playbook: Business & Strategic Lessons

Lesson 1: Find the Broken Market with 10x Pricing Inefficiency

Eyewear wasn’t just expensive—it was structurally expensive. For years, the industry charged multiples over what it cost to make products that most people simply needed to function day to day. That kind of gap doesn’t last forever. It’s an invitation for someone to come in, rethink the cost structure, and compete on a price that feels almost unbelievable.

Lesson 2: Vertical Integration as Competitive Moat—But Only at Scale

Owning your own optical labs sounds like a silver bullet, but it’s only a moat if you can feed it. Labs have real fixed costs—equipment, technicians, systems, logistics—and if you don’t have enough volume, they turn into an anchor.

National Vision made it work because it built the store base to match. At scale, the lab stops being an expense and becomes leverage: faster turn times, more control over quality, and—most importantly—cost economics that smaller competitors can’t replicate.

Lesson 3: The Walmart Partnership Playbook

Three decades inside Walmart didn’t just provide traffic. It shaped the company.

Walmart is famously unforgiving about execution: pricing discipline, operational consistency, and service standards aren’t suggestions—they’re requirements. National Vision survived and grew in that environment, and then carried those habits into its own fleet. The broader lesson is simple: the right partnership isn’t just distribution. It’s training. A demanding partner can function like real-time business school—if you can keep up.

Lesson 4: House of Brands Strategy

National Vision didn’t try to force one format to serve everyone. Instead, it built a portfolio—different banners for different customer mindsets—so it could expand without tripping over itself.

America’s Best is built for the pure value seeker: clear offers, high throughput, and low prices that feel accessible. Eyeglass World leans into a bigger “superstore” experience, with a wider selection and a slightly different shopper expectation. Same core engine, different packaging—and less self-cannibalization along the way.

Lesson 5: Value Retail in a Luxury-Branded World

In an industry where so much of the price is wrapped up in designer names and brand signaling, there’s always a huge slice of the market that just wants the basics done right: a solid exam, good lenses, frames that look fine, and a bill that doesn’t sting.

National Vision didn’t chase prestige. It chased fairness. And in a category where “normal” pricing had drifted into luxury territory, that positioning created trust as much as it created demand.

Lesson 6: Private Equity as Business Builder

Berkshire Partners and KKR didn’t just buy a chain and squeeze it. They helped turn a set of regional and partner-based assets into a scaled platform—investing in operations, labs, distribution, and repeatable store growth.

The takeaway isn’t that private equity always creates value this way. It’s that, in the right kind of fragmented market, it can. National Vision became a case study in what PE looks like when the playbook is building a better machine, not just reshuffling the balance sheet.

XV. Porter's 5 Forces Analysis

Threat of New Entrants: MODERATE-HIGH

If you want the clearest proof that the walls aren’t that high in eyewear, look at Warby Parker. When it launched in 2008, it didn’t try to squeeze into the traditional retail channel—because many of the shelves and stores were effectively controlled by incumbents. Instead, it went straight to customers online, pairing cost discipline with a brand that felt fresh and premium enough to earn trust.

That’s the split in this force. Online-only players can enter relatively easily. But building a full-service optical business—stores, exam capacity, lab and distribution infrastructure, and consistent quality at scale—is a very different game. That takes capital, operational know-how, and time.

Bargaining Power of Suppliers: LOW-MODERATE

National Vision blunts supplier leverage by doing more itself. It sources frames in ways that keep costs down, including buying designer overstock, and it manufactures a significant portion of its lenses in-house. The more of the value chain you control, the less you’re at the mercy of anyone else’s margins.

Bargaining Power of Buyers: MODERATE-HIGH

Customers have options, and the internet has made price comparisons effortless. Switching costs are low: if someone doesn’t like your price, they can try another retailer or click to an online alternative.

And then there’s insurance. Vision plans and managed care providers effectively set the rules for reimbursement, which gives them meaningful leverage over retailers like National Vision—especially as the industry shifts toward more insured patients.

Threat of Substitutes: MODERATE

Substitutes are real: contact lenses, refractive surgery like LASIK, and the growing set of online-only eyewear retailers. But there’s a floor under the category that makes it resilient. Most people who need vision correction can’t simply opt out, which keeps baseline demand intact even as customers mix and match how they solve it.

Competitive Rivalry: HIGH

This is a knife fight inside a market that’s both fiercely competitive and oddly concentrated. In U.S. eyewear retail, a small set of large players—EssilorLuxottica, Costco Wholesale, National Vision, and Visionworks—collectively dominate the vast majority of the market. When most of the volume sits with a few scaled operators, competition tends to concentrate where it hurts most: price, convenience, service, and the ability to run a more efficient machine than the guy across the street.

XVI. Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

This is the heart of National Vision’s advantage. The more volume you run through optical labs, distribution, and procurement, the cheaper each pair gets to produce and deliver. Scale also makes marketing more efficient: national campaigns and repeatable store formats get amortized across a huge footprint. With more than 1,200 locations, National Vision gets real leverage here—and it’s the reason the value promise can be more than a promotion.

2. Network Effects: WEAK

There aren’t true network effects in optical retail the way there are in marketplaces or social platforms. National Vision can benefit from relationships with optometrists and local referrals, but that’s incremental—not a flywheel that locks the market.

3. Counter-Positioning: HISTORICAL but FADING

For years, National Vision’s identity was a clean counterpunch to the luxury-priced incumbents. “Two pairs for $69.95” in a world of $400 glasses wasn’t just cheaper—it made the old pricing model look absurd.

The catch is that the counter-position has been copied and undercut. Online-first players now offer even lower price points, forcing National Vision to defend its value story with service, speed, and in-person care—not just a headline number.

4. Switching Costs: LOW-MODERATE

Most customers can switch retailers easily. Your prescription can be taken anywhere, and price shopping is painless. The “moderate” part comes from small frictions that still matter: stores keeping prescription records, the convenience of repeat visits, and being in-network with insurance plans.

5. Branding: MODERATE

America’s Best has become a known name in value optical, and that recognition matters because vision care requires trust. But it’s a different kind of brand power than the luxury players. National Vision’s brand isn’t about status; it’s about reliability, affordability, and not feeling taken advantage of.

6. Cornered Resource: MODERATE

In this business, scarce resources look like great sites and great clinicians. Prime real estate and experienced optometrists are hard to secure and harder to scale quickly.

Historically, the Walmart partnership functioned as an even stronger cornered resource—built-in traffic and a defensible footprint inside America’s biggest retailer. That advantage is now largely in the rearview mirror.

7. Process Power: MODERATE-STRONG

A lot of National Vision’s edge lives in the unsexy stuff: lab operations, inventory discipline, training, store execution, and a repeatable playbook that can open and run locations consistently. This is accumulated know-how that competitors can copy in theory, but not quickly. Years operating under Walmart’s standards also baked in a level of discipline that’s hard to replicate without living it.

Overall Assessment: National Vision’s powers are real, but not unbreakable. Scale economies and process power are the main pillars. The next leg—building deeper managed care and comprehensive eye care capabilities—could strengthen the moat by shifting the relationship from a one-time transaction to ongoing care.

XVII. Bull vs. Bear Case

The Bull Case

By November 2025, the stock was up more than 127% year-to-date—a signal that investors were buying into the company’s transformation story: shifting from a business built heavily on traditional cash-pay traffic toward a model with more managed care and broader eye health services.

- Demographics: An aging population is a steady tailwind; vision problems tend to rise with age.

- Value Positioning: In an uncertain economy, shoppers trade down—and value retailers often win.

- Transformation Working: Eleven straight quarters of positive comparable store sales suggests the playbook is executing, not just being promised.

- Managed Care Growth: Bringing in more managed care customers can lift unit economics through higher-value visits and more predictable demand.

- Store Fleet Optimization: Cutting underperforming locations should raise the profitability of the overall fleet.

- Technology Investment: AI-enabled tools for eye disease detection could expand what “an eye exam visit” can do, and widen the addressable market over time.

On growth, National Vision planned to keep expanding, with 32 new stores targeted for fiscal 2025, primarily under the America’s Best banner. And it continued to lean into tech as a differentiator, expanding a pilot of Meta-enabled AI smart glasses to an additional 250 locations by year-end 2025.

The Bear Case

- Online Disruptors: Ultra-low-price players like Zenni (with glasses starting at $6.95) and brand-led challengers like Warby Parker keep pulling share away from traditional retail.

- Luxottica's Scale: EssilorLuxottica’s vertical integration—and roughly 60% market share—makes it a uniquely difficult competitor to outmaneuver.

- Insurance Pressure: More managed care can mean more traffic, but reimbursement rates are under constant pressure.

- Walmart Exit Impact: Losing the Walmart partnership takes away a meaningful revenue stream and forces the business to re-balance around its owned channels.

- Market Saturation: At this footprint, growth gets harder without pushing into new markets or risking stores cannibalizing each other.

- Commoditization: As eyewear becomes easier to price-compare, product margins get squeezed—especially when online players anchor consumer expectations lower and lower.

Financially, the company posted a loss of $28.50 million in 2024, an improvement of 56.75% versus 2023.

XVIII. The Future: Where Does National Vision Go From Here?

Strategic Priorities Under Current Leadership

Reade Fahs · Executive Chairman · Alex Wilkes · Chief Executive Officer

The company is now in a handoff moment. Reade Fahs has moved into the Executive Chairman role after more than two decades running the machine, and Alex Wilkes is the CEO tasked with pushing the next chapter of the strategy—from value optical retail into something that looks more like scaled, accessible eye care.

As management put it:

"We are seeing immediate impact from the initial wave of transformation actions with a return to mid-single digit comp performance and solid growth in bottom line results. The strength of these results reinforces our confidence in the long-term potential of our go-forward strategy and initiatives."

Technology Roadmap

The future National Vision is building is still store-based—but with more tech inside the store to widen access and increase capacity.

Remote exam technology is a major pillar of that plan. In Q1 2024, the company equipped more than 550 locations, with a target of about 700 by the end of 2024. The goal is simple: make it easier for customers to get eye care, even in markets where staffing and scheduling can be the bottleneck.

That roadmap also points toward what the company believes will define the next generation of optical retail: teleoptometry, AI-powered screening tools, and digital selling technology—tools that help stores serve more people, more consistently, without breaking the value promise.

The Existential Questions

The big questions hanging over National Vision are the same ones hanging over the entire category.

Can brick-and-mortar optical retail hold up as online keeps getting cheaper and more convenient? Does eyewear eventually get commoditized the way contact lenses did? And even if National Vision executes perfectly, is there a real path to becoming number one—or is EssilorLuxottica simply too entrenched?

Those answers aren’t settled. What is clear is that National Vision enters that future with real strengths: a value-first position, structural cost advantages, operational discipline forged at scale, and trust with millions of Americans who need to see clearly—but don’t want to pay luxury prices to do it.

XIX. Epilogue & Reflections

The Meta-Story

National Vision is a very specific kind of American success story: private equity looked at a fragmented, inefficient market and did what it often does best—took a set of regional concepts, consolidated them with discipline, invested in the operational plumbing, and scaled the result into a national platform.

From the early 1990s onward, the company kept returning to the same customer and the same promise: value-driven vision care for people who are price-conscious and too often underserved by the “luxury-by-default” economics of the eyewear industry.

What's Surprising

For all the talk about everything going digital—and everything going premium—there is still a huge market for the opposite: affordable, accessible, high-quality essentials. National Vision is proof that value retail didn’t die. It just gets overlooked until the bill comes due.

Key Metrics to Watch

For investors following National Vision, two metrics tend to tell the clearest story:

- Comparable Store Sales Growth: Are existing stores getting healthier, or are they starting to lose momentum? This is the simplest read on whether the model is still resonating in the real world.

- Average Ticket Size: As the mix shifts toward managed care customers and more premium product tiers, this number should rise—one of the clearest signals that the business is improving its economics without abandoning its value identity.

The Bigger Picture

National Vision’s story is a lesson about American retail, healthcare, and consumer behavior: when essential goods are priced like luxury items, disruption isn’t a surprise—it’s a matter of time. Someone will always show up to serve the people who feel overcharged and overlooked. The hard part is building a durable machine that can do it at scale.

That’s what National Vision has tried to become. Beneath the banners and the store count is a purpose that’s stayed consistent: making eye care and eyewear accessible and affordable for a broad base of customers. It’s not just a pricing strategy. It’s the company’s cultural center of gravity—rooted in access, community impact, and patient well-being.

In a world where a pair of glasses can cost more than a smartphone, National Vision’s plain-language promise still lands the same way it always has: quality eyewear at prices people can actually afford. And for millions of Americans, that still feels quietly revolutionary.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube