Extra Space Storage: From Utah Startup to America's Storage Giant

I. Introduction & Episode Teaser

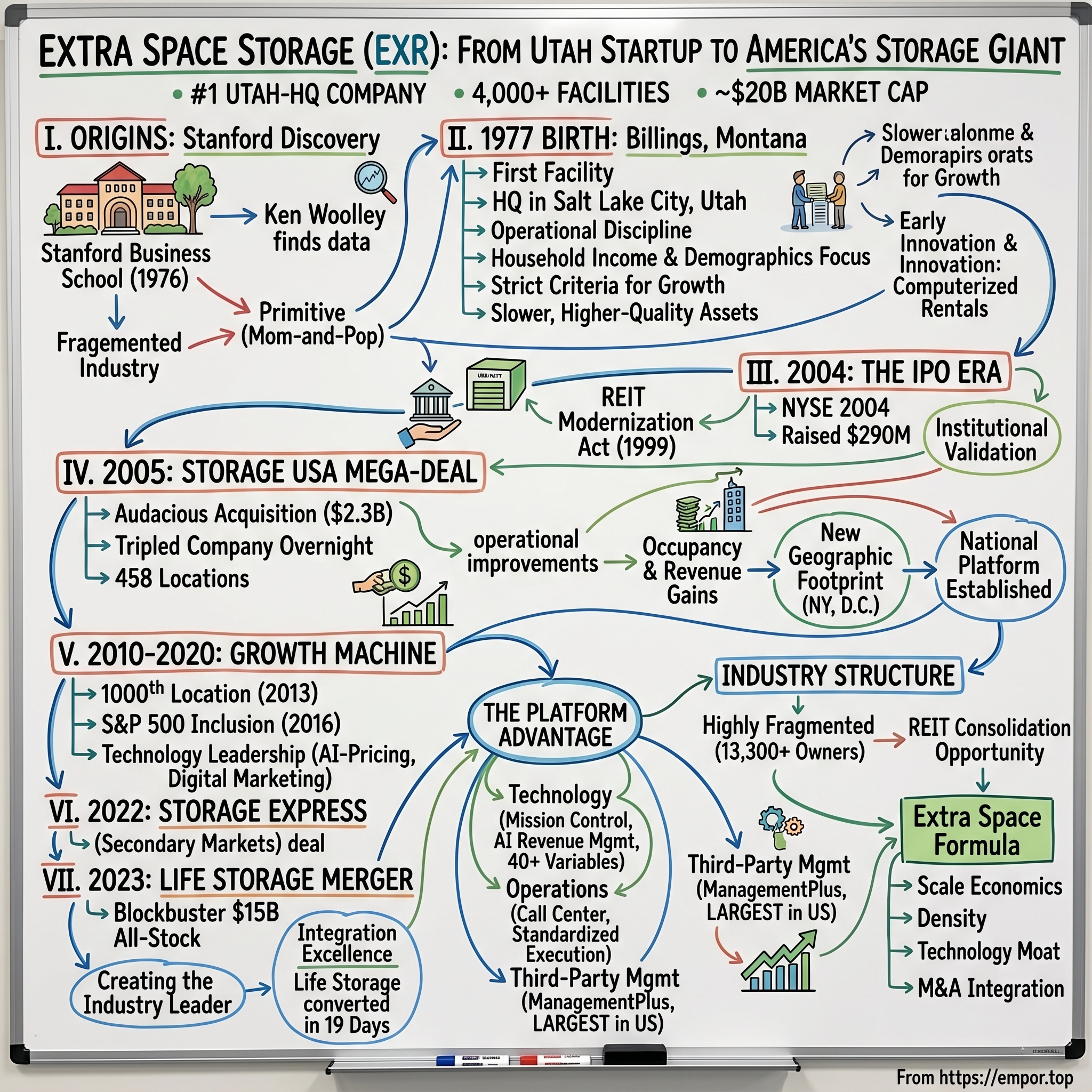

Picture this: A graduate student at Stanford Business School in 1976, hunched over market research data, discovers something peculiar. While everyone else in his class is studying tech startups and Wall Street firms, Ken Woolley is fascinated by metal sheds. Not glamorous Silicon Valley offices or Manhattan skyscrapers—just simple, corrugated steel boxes where Americans stuff their extra belongings. That obsession would spawn Extra Space Storage, which today operates over 4,000 facilities across America with a market cap hovering around $20 billion.

Here's what's remarkable: As of December 31, 2024, Extra Space Storage owns and/or operates 4,011 self-storage stores in 42 states and Washington, D.C., comprising approximately 2.8 million units and 308.4 million square feet of rentable space. To put that in perspective, that's enough square footage to cover all of Manhattan—twice. It's the largest company headquartered in Utah, dwarfing even the state's storied tech unicorns.

But the real question isn't how big Extra Space has become—it's how a single facility in Billings, Montana transformed into America's largest self-storage operator, outmaneuvering giants like Public Storage who had decades of head start. This is a story of perfectly timed acquisitions, technology disruption in the most analog of industries, and the counterintuitive insight that the most boring businesses often make the best investments.

What we're about to explore is how Extra Space cracked the code on an industry that Wall Street ignored for decades. We'll dissect their three transformative acquisitions—Storage USA in 2005, Storage Express in 2022, and the blockbuster Life Storage merger in 2023. We'll examine how they built a technology platform that turned commodity steel boxes into a sophisticated yield management machine. And we'll unpack why, in an era of digital everything, physical storage space has become one of the most resilient asset classes in America.

The journey from that single Montana facility to nationwide dominance reveals fundamental truths about scale economics, operational excellence, and the power of patient capital. As we'll see, Extra Space didn't just grow bigger—they fundamentally reimagined what a storage company could be.

II. Origins: Ken Woolley & The Stanford Discovery (1977-1990s)

The Stanford Graduate School of Business library, spring 1976. While his classmates analyzed Fortune 500 case studies, Ken Woolley stumbled upon data that would change his life. Self-storage—an industry so obscure it barely warranted a footnote in real estate textbooks—was growing at 20% annually. Americans were accumulating stuff faster than their homes could hold it. Divorces were rising, creating sudden needs for temporary space. Urban dwellers in cramped apartments needed overflow capacity. The demand was hiding in plain sight.

Woolley's research project revealed a fragmented industry ripe for professionalization. Most facilities were mom-and-pop operations—a few dozen units behind a gas station, managed with paper ledgers and padlocks. No one had applied systematic business thinking to what was essentially a real estate arbitrage play: buy cheap land on the outskirts of town, erect simple structures, and rent space at surprisingly robust margins.

In May 1977, Woolley took the plunge. His first property in Billings, Montana wasn't much to look at—a modest facility with roll-up doors and concrete floors. But it represented something bigger: the birth of Extra Space Storage Inc., established that same year in Salt Lake City, Utah. The location wasn't accidental. Utah offered favorable tax treatment for REITs, a growing business community, and critically, distance from the established storage operators clustered on the coasts.

The self-storage industry context of the late 1970s was primitive by today's standards. Public Storage, founded in 1972, was just beginning to scale. Most operators viewed storage as passive income—build it, rent it, forget it. Woolley saw it differently. He obsessed over occupancy rates, studied seasonal patterns, and most importantly, recognized that location and convenience mattered more than price. A storage unit three miles closer to someone's home could command 20% higher rent.

The early business model was deceptively simple yet remarkably capital-efficient. Unlike apartments or office buildings, storage facilities required minimal maintenance, no plumbing beyond a single restroom, and generated predictable cash flows. Woolley's insight was that operational excellence—not just property ownership—would differentiate winners from losers. He invested in better lighting, security systems, and crucially, customer service training for on-site managers.

Through the 1980s and early 1990s, Extra Space grew methodically. While competitors chased rapid expansion, Woolley focused on operational discipline. Each new facility had to meet strict criteria: demographics showing household income above certain thresholds, population density sufficient to support 5-7 square feet of storage per capita, and limited existing competition. This analytical approach—unusual for the era—meant slower growth but higher-quality assets.

By 1998, Extra Space had assembled 53 storage facilities across the Western United States. Each property was a learning laboratory. They discovered that climate-controlled units, while more expensive to build, commanded premium rents and attracted stickier customers. They learned that visibility from major roads mattered more than absolute traffic counts. Most importantly, they recognized that customer acquisition costs were falling as word-of-mouth and repeat business grew.

The company culture Woolley instilled was distinctly un-Wall Street. Based in Salt Lake City, Extra Space attracted employees who valued stability over stock options, operational excellence over financial engineering. This Mormon work ethic—though never explicitly stated—permeated the organization. Managers were expected to know every tenant by name, walk their facilities daily, and treat the properties as if they owned them.

Technology adoption, even in these early years, set Extra Space apart. While competitors relied on paper systems well into the 1990s, Extra Space was among the first to computerize rental agreements, automate billing, and track facility-level metrics in real-time. This data infrastructure would prove invaluable when the company eventually went public.

The foundation was set: disciplined growth, operational excellence, and a culture of continuous improvement. But to truly scale, Extra Space needed capital—lots of it. The path to becoming a public company was about to begin.

III. The IPO & Going Public Era (2004-2010)

August 2004. The New York Stock Exchange floor buzzed with unusual energy as traders prepared for the largest IPO ever from a Utah-based company. Extra Space Storage, with its 136 locations, was about to raise $290 million in gross proceeds. For a company that started with a single facility in Montana, ringing the opening bell represented more than a liquidity event—it was validation that self-storage had arrived as an institutional asset class.

The timing was exquisite. The REIT Modernization Act of 1999 had made real estate investment trusts more attractive to institutional investors. Interest rates were at historic lows, driving yield-hungry investors toward alternative assets. And critically, the storage industry was consolidating. Public companies owned less than 10% of facilities nationwide, suggesting massive runway for acquisitions.

Spencer Kirk, who had joined as CEO in 1998, understood that going public wasn't just about raising capital—it was about building a currency for acquisitions. "We knew that to compete with Public Storage, we needed scale," Kirk would later recall. "Being public gave us the ammunition." The IPO priced at $12.50 per share, valuing the company at roughly $700 million.

The early days as a public company were jarring. Quarterly earnings calls replaced informal board updates. Wall Street analysts dissected every basis point of same-store revenue growth. The pressure for consistent quarterly performance clashed with the long-term nature of real estate development. Extra Space had to learn a new language—FFO (funds from operations), NOI (net operating income), RevPAR (revenue per available unit).

But being public also brought discipline. The company implemented sophisticated yield management systems, similar to airlines and hotels, dynamically pricing units based on demand. They discovered that small price increases—$5 or $10 per month—rarely triggered move-outs, as the hassle of relocating belongings outweighed the cost. This pricing power, invisible to private operators, became a crucial competitive advantage.

The competitive landscape in 2004 was dominated by Public Storage's 1,400 locations and $16 billion market cap. They were the 800-pound gorilla, with seemingly insurmountable scale advantages. U-Haul's storage division was growing aggressively. Regional players like Storage USA and Shurgard were expanding rapidly. Extra Space, despite its IPO success, was still a minnow in a pond with several sharks.

What Extra Space lacked in size, it compensated with innovation. They were among the first to embrace online rentals, partnering with aggregators like SpareFoot to capture digital demand. They invested heavily in search engine marketing when Google AdWords was still nascent. While Public Storage relied on their brand recognition, Extra Space had to be scrappier, more targeted, more data-driven.

The public markets quickly validated Extra Space's approach. By year-end 2004, the stock had risen 20%. Same-store revenue grew 6.8% in 2005. Occupancy rates pushed above 90%. Wall Street was beginning to notice that this Utah upstart was delivering Public Storage-like returns with arguably better growth prospects.

But Kirk and his team knew that organic growth alone wouldn't close the gap with Public Storage. They needed a transformative acquisition—something that would instantly establish Extra Space as a serious player. Behind closed doors, they were already negotiating what would become the deal of the decade.

IV. The Storage USA Mega-Deal & First Major Acquisition (2005)

The phone call came on a Friday afternoon in late 2004. General Electric Capital wanted out of the storage business. Their Storage USA portfolio—458 locations concentrated in major markets—was available. The asking price: $2.3 billion. For Extra Space, with its 136 facilities and sub-billion-dollar market cap, it was audacious beyond belief. It would triple the company overnight.

Spencer Kirk flew to Connecticut that weekend. In GE's austere conference room, he made the pitch of his lifetime. Extra Space could close quickly, had proven integration capabilities, and crucially, understood that Storage USA's underperformance was an opportunity, not a liability. GE's facilities were averaging 76% occupancy versus Extra Space's 90%. The revenue upside from operational improvements alone could justify the purchase price.

The financing gymnastics required to pull off the deal were extraordinary. Extra Space issued $400 million in new equity, assumed $700 million of Storage USA's existing debt, and arranged a $1.2 billion bridge loan. Wall Street was skeptical. Analysts questioned whether a company that had been public for less than a year could digest an acquisition three times its size. The stock dropped 8% on the announcement.

But Kirk and his team had done their homework. During due diligence, they discovered that Storage USA's problems were operational, not structural. The facilities were in excellent locations—dense urban markets that Extra Space couldn't have entered organically. The issue was management. Storage USA treated properties as passive investments. Managers were poorly trained, pricing was static, and marketing consisted mainly of Yellow Pages ads.

The integration began before the deal officially closed in July 2005. Extra Space sent tiger teams to every Storage USA facility, documenting current operations, identifying quick wins, and preparing for day-one changes. They discovered treasure troves of inefficiency: units priced the same regardless of size or location within facilities, no systematic approach to rate increases, and perhaps most shocking, no centralized customer database.

The first 100 days post-closing were orchestrated with military precision. Every Storage USA facility received new signage, upgraded lighting, and fresh paint. More importantly, Extra Space implemented their proven operating playbook: dynamic pricing algorithms, centralized call centers, and rigorous revenue management. Managers were retrained or replaced. Marketing shifted from print to digital.

The results were staggering. Within six months, Storage USA's occupancy rose from 76% to 84%. Revenue per occupied square foot increased 8%. Same-store NOI grew 15% in the first year alone. What Wall Street had viewed as integration risk was actually Extra Space's greatest opportunity. They had acquired assets at a discount and were rapidly closing the operational gap.

The technology platform integration proved the most complex challenge. Storage USA ran on antiquated property management software that couldn't communicate with Extra Space's systems. Rather than force an immediate conversion, Extra Space built middleware that allowed gradual migration. This patient approach meant no customer disruption while still capturing operational improvements.

Cultural integration required equal finesse. Storage USA employees, particularly property managers, feared Utah corporate culture would be imposed on East Coast operations. Extra Space wisely retained regional management structures, emphasizing operational excellence over cultural conformity. They instituted performance bonuses tied to occupancy and revenue targets, aligning incentives across the organization.

The acquisition fundamentally changed Extra Space's geographic footprint. Suddenly, they had critical mass in markets like New York, Boston, and Washington D.C.—locations where building new facilities was virtually impossible due to zoning restrictions. This urban concentration would prove invaluable as city-dwellers increasingly turned to storage solutions for their space-constrained lifestyles.

By 2006, the Storage USA integration was largely complete. Extra Space had successfully absorbed 458 facilities, nearly tripling revenue to $365 million. The stock price had recovered and then some, reaching $18 per share. Wall Street analysts who had doubted the deal were now praising Extra Space's execution. The company had proven it could handle large-scale M&A.

The Storage USA acquisition established the playbook Extra Space would refine over the next two decades: identify underperforming portfolios, pay fair prices based on current operations, then create value through operational improvements. It was private equity thinking applied to a public REIT structure. This approach would guide every subsequent acquisition, from SmartStop to Life Storage.

More fundamentally, the deal transformed Extra Space from a regional operator to a national platform. They now had the scale to justify significant technology investments, the geographic diversity to weather regional economic downturns, and the market presence to compete with Public Storage. The student was becoming the master.

V. Building the Growth Machine (2010-2020)

October 2013. Extra Space executives gathered at their Salt Lake City headquarters to celebrate a milestone once thought impossible: the acquisition of their 1,000th location. Spencer Kirk raised a glass of sparkling cider (this was Utah, after all) and made a bold prediction: "Our second thousand will come faster than our first." He was right. By January 2016, Extra Space had grown so substantially that it earned inclusion in the S&P 500—recognition that self-storage had become a core component of American real estate infrastructure.

The decade following the financial crisis proved transformative for Extra Space. While traditional real estate sectors struggled with oversupply and declining rents, self-storage demonstrated remarkable resilience. The Great Recession had actually increased demand as downsizing homeowners and displaced families needed temporary storage. Extra Space's occupancy never dropped below 85%, even during the darkest days of 2009.The 2015 SmartStop acquisition perfectly exemplified Extra Space's evolving M&A sophistication. SmartStop stockholders received $13.75 per share in cash which represents a total purchase price of approximately $1.4 billion, with Extra Space paying approximately $1.31 billion, and the remaining $90 million coming from the sale of certain assets by SmartStop immediately prior to closing. The deal added 121 SmartStop stores owned and 43 third-party managed stores, instantly expanding Extra Space's footprint by over 10%.

What made SmartStop attractive wasn't just scale—it was operational upside. SmartStop had built high-quality facilities in prime locations but operated them like a non-traded REIT focused on distributions rather than growth. Their occupancy lagged Extra Space's by 500 basis points. Their revenue management was rudimentary. This gap represented pure value creation opportunity.

The integration showcased Extra Space's operational machine. Once the acquisition closed, they successfully integrated all 165 properties and immediately put their marketing prowess, revenue management platform and other systems to work. Within months, SmartStop properties saw occupancy gains of 7%, revenue per square foot increases of 10%, and expense reductions of 15% through centralized procurement and management.

But the real story of the 2010s was Extra Space's development of a third-party management platform—ManagementPlus—launched in 2008. By managing properties for other owners, Extra Space gained several advantages: fee income with minimal capital investment, market intelligence on potential acquisitions, and most importantly, scale benefits in marketing and operations that benefited both owned and managed properties. Extra Space Storage became the largest third-party self storage management company in the U.S., a position that provided critical competitive advantages. ManagementPlus properties made up around 35% of Extra Space's current self storage portfolio by 2020, generating high-margin fee income while requiring minimal capital investment.

The technology investments of this decade transformed Extra Space into what analysts called "the technology leader in the self-storage industry". They built proprietary revenue management systems that adjusted pricing daily based on occupancy, seasonality, and competitor rates. Their digital marketing team became industry-leading, capturing online demand when competitors still relied on drive-by traffic. The company's data scientists developed predictive models for customer acquisition costs, lifetime values, and optimal unit mix.

This operational excellence translated directly to financial performance. Extra Space's one-year, two-year, three-year, four-year, five-year and ten-year total returns to shareholders were not only the highest among self-storage REITs, but also #1 across publicly traded REITs of all property types. The market was recognizing that Extra Space had cracked the code on turning commodity real estate into a technology-enabled platform business.

The January 2016 inclusion in the S&P 500 marked Extra Space's arrival as an institutional-grade investment. Pension funds and endowments that couldn't invest in smaller REITs now had access. The increased liquidity and analyst coverage created a virtuous cycle—better access to capital meant more acquisitions, which drove economies of scale, which improved margins, which increased the stock price.

By 2020, Extra Space had built something remarkable: a fully integrated platform combining owned properties, managed facilities, proprietary technology, and operational excellence. They weren't just a storage company anymore—they were a data and logistics business that happened to own real estate. This transformation positioned them perfectly for the next phase of consolidation.

VI. The Storage Express Acquisition & Regional Expansion (2022)

September 2022. In a wood-paneled conference room in Indianapolis, Jefferson Shreve, founder of Storage Express, faced a decision that would define his legacy. His company had built something unique: 107 self-storage properties across Indiana, Ohio, Illinois, and Kentucky that served small towns and rural communities most operators ignored. Now Extra Space was offering $590 million to acquire not just the properties, but Storage Express's entire approach to serving secondary markets.

Total consideration for the acquisition was approximately $590.0 million. But the deal structure revealed something deeper about Extra Space's evolution. The transaction was funded in part by the issuance of $125.0 million in operating partnership units, with the balance in cash drawn from its credit facilities. By taking operating partnership units rather than pure cash, Shreve was betting on Extra Space's future—so much so that he joined their board of directors.

What made Storage Express special wasn't size but innovation. They operated smaller facilities in more rural markets with remote rentals. These weren't your typical storage facilities with on-site managers and office hours. Storage Express had pioneered unmanned, technology-enabled operations that allowed profitable operation of 30-unit facilities in towns of 5,000 people. Their proprietary E-Tracker software platform enabled remote management, automated access control, and centralized customer service.

For Extra Space, this acquisition opened an entirely new growth vector. CEO Joe Margolis explained the strategic rationale: "In addition to increased scale, this acquisition provides a new growth channel for Extra Space Storage to add smaller, remote-managed stores in both new and existing markets through acquisition and third-party management." The traditional storage model required 50,000+ population centers to justify on-site management. Storage Express had proven you could serve markets one-tenth that size profitably.

The integration approach differed markedly from previous acquisitions. Rather than immediately converting Storage Express facilities to Extra Space's standard operating model, they preserved the remote management infrastructure. The 107 properties continued operating with minimal on-site presence, managed through centralized call centers and mobile maintenance teams. This hybrid model—combining Extra Space's marketing muscle with Storage Express's lean operations—created a template for rural expansion.

The Company also purchased E-Tracker, a storage software operating platform, which supports Storage Express locations. This technology acquisition was equally strategic. E-Tracker's remote management capabilities could be deployed across Extra Space's third-party management platform, enabling them to manage smaller facilities that previously wouldn't pencil out economically. A 40-unit facility in rural Kansas suddenly became viable when managed remotely from Salt Lake City.

The cultural integration proved smoother than expected. Storage Express employees, accustomed to entrepreneurial problem-solving in resource-constrained environments, brought fresh perspectives to Extra Space's more corporate culture. Their expertise in rural markets—understanding seasonal agricultural storage needs, working with local contractors, navigating small-town politics—became invaluable as Extra Space expanded beyond metropolitan areas.

Financially, the acquisition immediately proved accretive. The $590 million purchase price implied a cap rate of approximately 6.5%, attractive in a rising rate environment. But the real value lay in the platform: Extra Space could now pursue hundreds of small-market acquisitions previously off-limits, aggregating fragmented rural operators at attractive multiples.

This Storage Express deal represented Extra Space's recognition that the next wave of consolidation wouldn't come from buying large portfolios in gateway cities—those were picked over and pricey. Instead, growth would come from aggregating the 60% of storage facilities still owned by mom-and-pop operators, many in secondary and tertiary markets. Storage Express provided both the operational playbook and technology platform to execute this strategy efficiently.

By early 2023, the Storage Express integration was complete. The 107 facilities were performing above underwriting, with occupancy gains of 4% and revenue growth of 7%. More importantly, Extra Space had successfully deployed the remote management model to an additional 50 third-party managed sites, proving the scalability of the approach. The stage was set for an even more transformative transaction.

VII. The Life Storage Blockbuster: Creating the Industry Leader (2023)

April 3, 2023, 6:00 AM Eastern. Joe Margolis, CEO of Extra Space Storage, was in his Salt Lake City office when the call came through. Joe Saffire, CEO of Life Storage, had news: "We're ready to move forward." After months of negotiations, board meetings, and a dramatic bidding war with Public Storage, the two companies would combine in an all-stock strategic combination with Life Storage shareholders receiving 0.895 shares of Extra Space common stock for each share of Life Storage stock, resulting in a purchase price of approximately $15 billion (including debt).

The backstory was pure corporate drama. Public Storage, frustrated at being overtaken as the industry's largest operator, had initiated a hostile takeover attempt of Life Storage in late 2022. They went public with a "Bear Hug" letter, attempting to pressure Life Storage's board. But Saffire had other ideas. As Margolis later revealed: "Joe Saffire called me and asked if I wanted to get together and talk about this." That conversation changed everything.

The combined company became the largest storage operator in the country (based on the number of self-storage locations) with over 3,500 locations, approximately 270 million square feet of rentable storage space, and over two million customers. The combined entity would be among the largest REITs in the MSCI U.S. REIT Index, with an enterprise value of approximately $46 billion.

The strategic logic was compelling. Life Storage brought strength in northeastern markets where Extra Space was underrepresented. Their facilities in Buffalo, Rochester, and Syracuse gave Extra Space critical mass in upstate New York. Life Storage's presence in Florida—a state experiencing explosive population growth—instantly made Extra Space a major player in markets from Jacksonville to Miami.

But the real opportunity lay in operational improvements. Life Storage's same-store pool lagged that of Extra Space by 400 basis points in occupancy, and net rent per square foot lagged by approximately 15% at original underwriting. These gaps weren't due to inferior properties—Life Storage owned excellent real estate. The issue was systems and execution.

The integration planning began immediately after announcement. Extra Space assembled 15 workstreams covering everything from IT systems to employee communications. The goal was audacious: convert all Life Storage properties to Extra Space's platform within 30 days of closing. Industry observers called it impossible. Storage systems were notoriously complex, with tenant databases, access control systems, and revenue management platforms all needing seamless coordination.

On July 18, 2023, Extra Space stockholders and Life Storage stockholders voted separately to approve the proposed merger. More than 99.9 percent of votes cast at the Extra Space meeting—approximately 90.3 percent of the outstanding shares—were voted in favor. The overwhelming support reflected shareholder confidence in the strategic rationale and Extra Space's execution track record.

What happened next stunned the industry. Extra Space's integration team, led by Chief Operating Officer Scott Stubbs, executed what they called "The Big Bang"—converting all Life Storage properties in just 19 days. Every Life Storage customer received new account access, every property manager was retrained on Extra Space systems, and every facility began using Extra Space's dynamic pricing algorithms. It was the fastest large-scale REIT integration in history.

The Extra Space team integrated and trained over 2,000 new Life Storage team members. A large focus of this training was minimizing customer disruption and quickly adjusting to the Extra Space systems and platform. Through this thorough training and culture assimilation process, employees received regular communication and opportunities to meet with Extra Space leaders.

The financial engineering was equally sophisticated. The merger was expected to generate at least $100 million in annual run-rate operating synergies. The company projected $23 million in corporate overhead savings through G&A cost efficiencies, at least $65 million in property revenue uplift as Extra Space store revenues outperform in overlapping markets, and $12 million in tenant reinsurance uplift.

Early results validated the thesis. Within six months, the occupancy gap between legacy Life Storage and Extra Space properties had narrowed from 400 basis points to 150. Revenue per square foot was converging even faster. Customer acquisition costs dropped 20% as Extra Space's digital marketing engine drove traffic to Life Storage properties. The combined company's scale enabled renegotiation of vendor contracts, insurance policies, and technology licenses, driving millions in cost savings.

The cultural integration proved surprisingly smooth. Life Storage's entrepreneurial culture, forged in Buffalo's rust belt economy, meshed well with Extra Space's operational discipline. Both companies shared a focus on customer service, property-level profitability, and long-term value creation. The combined management team—with three Life Storage directors joining Extra Space's board—brought complementary skills and market knowledge.

For the industry, the Extra Space-Life Storage merger represented a seismic shift. The combined company controlled 13% of institutional-grade storage square footage. Their marketing spend exceeded $100 million annually, dwarfing regional competitors. Their data advantage—with information on over two million customers—enabled pricing and marketing precision competitors couldn't match.

Public Storage, despite inventing the modern storage industry, had been dethroned. The student had not just caught the master—they had decisively surpassed them.

VIII. The Platform Advantage: Technology, Operations & Third-Party Management

Inside Extra Space's Salt Lake City headquarters, a room resembling NASA's mission control operates 24/7. Dozens of screens display real-time data from over 4,000 facilities: occupancy rates, pricing changes, website traffic, competitor moves. This is the nerve center of what industry insiders call "the most sophisticated revenue management system in real estate."

The technology story begins with a simple insight: storage units are perishable inventory, just like airline seats or hotel rooms. Every day a unit sits empty is revenue lost forever. But unlike airlines serving routes or hotels in fixed locations, storage facilities compete in hyperlocal markets where a competitor three blocks away might have completely different supply-demand dynamics.

Extra Space's revenue management system, developed over two decades and refined through billions of pricing decisions, adjusts rates multiple times daily based on proprietary algorithms. The system considers over 40 variables: current occupancy, seasonal patterns, competitor pricing, local economic indicators, weather forecasts, even the day of the week. A facility in Phoenix might raise prices on climate-controlled units during summer heat waves, while a Denver location drops prices on large units in January when moving activity slows.

The pricing sophistication extends to individual unit level. The system recognizes that a ground-floor unit near the entrance commands premium pricing versus an identical unit on the third floor. It knows that customers rarely comparison shop once they've stored belongings, enabling strategic rate increases that maximize revenue while minimizing move-outs. The average Extra Space customer experiences 3-4 price increases annually, each carefully calibrated to stay below the hassle threshold of moving.

Digital marketing represents another technological moat. Extra Space Storage is the largest third-party self storage management company in the U.S., and this scale provides unparalleled data advantages. They know which Google keywords convert, which Facebook demographics respond, and which ZIP codes are undersupplied. Their annual marketing spend—$34 million in 2024, up 12.2% from the previous year—would bankrupt smaller operators attempting to match it.

The customer acquisition funnel is ruthlessly optimized. Website visitors see dynamically generated content based on their location, device, and browsing history. The online rental process, refined through millions of transactions, reduces friction at every step. Abandoned cart emails, retargeting campaigns, and promotional offers are all automated and personalized. The result: industry-leading conversion rates and customer acquisition costs 30% below the sector average.

But technology is just one pillar of Extra Space's platform advantage. Their third-party management business, ManagementPlus, has evolved into a powerful competitive weapon. Managed properties make up approximately 40 percent of Extra Space Storage's facilities, generating high-margin fee income while providing market intelligence and acquisition pipeline.

The third-party management model creates aligned incentives. Property owners pay Extra Space a percentage of revenue, motivating Extra Space to maximize performance. In return, owners gain access to Extra Space's technology platform, marketing muscle, and operational expertise. Their proprietary pricing systems maximize revenue through all stages of occupancy, utilizing complex algorithms made possible through the scale of their data.

For smaller operators, partnering with Extra Space is often the only way to remain competitive. They can't afford sophisticated revenue management systems, national advertising campaigns, or 24/7 call centers. Extra Space provides all of this, typically driving 15-20% revenue increases within the first year of management. The improved performance often convinces owners to eventually sell to Extra Space, creating a natural acquisition pipeline.

The operational excellence extends to property-level execution. Extra Space has perfected the science of storage operations through decades of testing and refinement. They know optimal staffing ratios (one manager per 500 units), ideal marketing mix (60% digital, 40% local), and perfect facility maintenance schedules (parking lot resealing every three years, roof inspection twice annually).

Their centralized call center, handling over 5 million customer interactions annually, exemplifies operational leverage. Rather than each facility answering phones—resulting in missed calls, inconsistent service, and lost rentals—trained specialists handle all inquiries. They can view real-time availability across nearby facilities, offering alternatives if the requested location is full. Call recordings are analyzed using AI to identify training opportunities and optimize scripts.

The bridge lending program, launched in 2018, represents another platform extension. Extra Space provides short-term financing to storage developers and operators, typically for properties in lease-up phase. These loans, totaling over $1.6 billion originated, serve multiple purposes: they generate attractive risk-adjusted returns, create relationships with potential third-party management clients, and provide early visibility into acquisition opportunities.

Ancillary revenue streams, often overlooked by analysts, contribute meaningfully to profitability. Tenant insurance, branded locks, moving supplies, and truck rentals generate minimal marginal costs but significant margins. Extra Space's scale enables better terms with insurance providers and suppliers, advantages smaller operators can't replicate. The average customer generates $15-20 monthly in ancillary revenue beyond base rent.

Store-level economics reveal the power of Extra Space's platform. A typical stabilized facility operates at 92% occupancy, generates 60% NOI margins, and requires minimal capital expenditure. The combination of high margins, predictable cash flows, and low maintenance makes storage one of the most attractive real estate sectors. Extra Space's operational excellence pushes these metrics even higher: 94% occupancy, 65% NOI margins, and industry-leading revenue per square foot.

The platform advantages compound over time. More data improves algorithms. Better algorithms drive higher revenue. Higher revenue attracts more third-party management clients. More clients provide more data. It's a virtuous cycle that becomes increasingly difficult for competitors to disrupt. This is why Extra Space trades at premium multiples—investors aren't just buying real estate, they're buying a technology-enabled platform with sustainable competitive advantages.

IX. Competitive Dynamics & Industry Structure

The self-storage industry structure in 2024 presents a fascinating paradox: massive consolidation at the top, yet still remarkably fragmented overall. As of October 2024, the four public self storage REITs owned 30% of the entire U.S. self storage inventory, up from 17% in 2000. Institutional owners (including public REITs) own an estimated 45% of all self storage space in the U.S. This means over half the industry remains in the hands of smaller operators—a $50 billion consolidation opportunity hiding in plain sight.

Public REITs now operate roughly 40% of national capacity, up from 20% five years earlier, confirming a progressive consolidation trend. The four largest brands—Public Storage, Extra Space Storage, CubeSmart, and National Storage Affiliates—jointly control near-20% of the United States self-storage market, leaving significant fragmentation among small operators. Large platforms leverage centralized marketing, AI revenue management, and lower capital costs to aggregate facilities, especially in secondary markets where independents dominate.

The competitive dynamics have fundamentally shifted since the Life Storage acquisition. Extra Space, now controlling approximately 15% of institutional-grade storage square footage, possesses advantages that compound daily. Their marketing spend—reaching $34 million in 2024, up 12.2% from the previous year—creates a moat smaller operators simply cannot cross. When a mom-and-pop facility in suburban Dallas competes against Extra Space's Google AdWords budget, sophisticated SEO, and retargeting campaigns, the outcome is predetermined.

But the real competitive advantage isn't just scale—it's data. Extra Space's algorithms, trained on millions of customer interactions, can predict with uncanny accuracy when to raise prices, which units will rent fastest, and how much a customer will pay before shopping competitors. A small operator managing 200 units has perhaps 150 customers generating data points. Extra Space has over two million, each creating hundreds of data points annually. This data asymmetry drives pricing power that translates directly to NOI.

Public Storage, despite losing the crown as largest operator, remains formidable. Their balance sheet strength—virtually no debt and massive cash generation—enables them to strike quickly on acquisitions. They've pivoted toward technology investments and operational improvements, attempting to close the efficiency gap with Extra Space. Their recent focus on automation and unmanned facilities suggests they're learning from Extra Space's Storage Express playbook.

CubeSmart has carved out a different niche, focusing on urban markets and climate-controlled facilities. They've accepted they'll never match Extra Space's scale, instead pursuing a differentiation strategy. Their partnership with apartment buildings and moving companies creates unique customer acquisition channels. It's a smart approach—compete where Extra Space isn't rather than going head-to-head.

National Storage Affiliates operates as a consolidator of consolidators. Their unique structure—acquiring regional operators who maintain local branding and management—provides an alternative path to scale. They're betting that local market knowledge and relationships matter more than centralized efficiency. The jury's still out, but their model attracts sellers who want to maintain involvement post-transaction.

The fragmentation opportunity remains enormous. The self storage market remains a highly fragmented industry, 13,300 owners sharing the national stock. Among them, almost 10,000 are small self storage providers managing less than 100,000 square feet. These operators face an impossible choice: compete against REITs with unlimited marketing budgets and sophisticated technology, or sell at attractive multiples while valuations remain high.

The consolidation math is compelling. A typical mom-and-pop facility might operate at 75% occupancy with static pricing. Extra Space can push that to 92% occupancy with dynamic pricing, immediately adding 20-30% to NOI. They can reduce operating expenses by 10-15% through centralized procurement and management. The value creation from operational improvements often exceeds the acquisition premium paid.

Regulatory dynamics increasingly favor large operators. Cities are restricting new storage development, viewing it as low tax-revenue generation compared to retail or office. Municipalities increasingly block new storage construction, preferring retail or industrial developments with higher headcount and tax multipliers. More than 15 U.S. states have enacted moratoria since 2019, and European city councils apply similar caps. Existing operators see occupancy and pricing tailwinds, yet supply constraints hinder new entrants and encourage brownfield conversions over greenfield builds.

These supply constraints create a prisoner's dilemma for small operators. They benefit from restricted new supply supporting occupancy and rates. But they also face relentless competition from REITs with superior operations. Many are choosing to sell now, capitalizing on strong valuations while they still can. Extra Space stands ready to acquire, with proven integration capabilities and access to cheap capital.

The industry structure increasingly resembles airlines or wireless carriers—a few giants dominating while smaller players occupy specialized niches. But unlike those industries, storage's hyperlocal nature means complete consolidation is unlikely. There will always be room for well-run independent operators in tertiary markets or specialized segments. The question is whether that room is shrinking faster than most realize.

X. Playbook: The Extra Space Formula

Study Extra Space Storage's trajectory from 136 facilities to 4,000+, and a clear playbook emerges—one that combines financial engineering, operational excellence, and platform economics in ways the storage industry had never seen. This isn't just about buying properties and raising rents. It's about building a system that gets stronger with every acquisition, every customer interaction, every data point collected.

Scale Economics and Density Advantages

The magic of Extra Space's model starts with a simple insight: storage is a density business. Having ten facilities in Denver is exponentially more valuable than having one facility in ten different cities. Why? Marketing efficiency. When Extra Space buys Google AdWords for "Denver storage," that investment drives traffic to all ten facilities. A mom-and-pop operator buying the same keywords serves just one location. The cost per acquisition drops with each additional facility in a market.

This density advantage extends beyond marketing. Regional managers can oversee multiple facilities more efficiently than single-site operators. Maintenance crews can service several properties in a day. Inventory and supplies can be bulk-purchased and distributed locally. Even customer referrals compound—a satisfied customer at one Extra Space facility is likely to recommend another Extra Space location to friends.

The numbers tell the story. In markets where Extra Space has 10+ facilities, their operating margins run 500-700 basis points higher than single-site operators. That's pure scale economics at work—fixed costs spread across more revenue-generating units, creating a widening competitive moat.

Technology as a Competitive Moat

Extra Space's technology investments, approaching $100 million annually, would bankrupt most competitors. But spread across 4,000 facilities, it's just $25,000 per location—a rounding error against the NOI improvements it generates. Their revenue management system alone, constantly refined since 2004, drives 10-15% revenue uplift versus static pricing.

The technology moat isn't just about fancy algorithms. It's about the entire digital ecosystem. Online rental systems that convert browsers to renters 24/7. Automated access control that eliminates the need for on-site staff during off-hours. Predictive maintenance systems that flag HVAC issues before they become customer complaints. Each system interconnects, creating a platform that would take competitors years and millions to replicate.

Consider their customer acquisition funnel. A prospect searches Google, sees an Extra Space ad dynamically generated based on available inventory, lands on a location page optimized through millions of A/B tests, receives personalized follow-up emails if they don't convert immediately, and can complete the entire rental process on their phone. A small operator might still be answering voicemails and showing units in person.

M&A Integration Excellence

Extra Space has completed over 50 acquisitions, refining their integration playbook with each iteration. The Life Storage integration—converting 1,200 facilities in 19 days—showcased this expertise. They've identified exactly which systems need day-one conversion (pricing, access control) versus those that can migrate gradually (back-office functions, vendor contracts).

The integration philosophy is "stabilize, optimize, then transform." First, ensure no customer disruption and maintain occupancy. Second, implement quick wins like dynamic pricing and centralized marketing. Third, pursue deeper operational changes like staff restructuring and facility upgrades. This staged approach minimizes risk while capturing value rapidly.

Crucially, Extra Space preserves what works. When they acquired Storage Express's rural portfolio, they maintained the remote-management model rather than forcing their traditional approach. This flexibility to adopt best practices regardless of source has made them better acquirers over time.

Capital Allocation Discipline

The REIT structure enforces capital discipline—90% of taxable income must be distributed as dividends. This prevents empire-building and forces rigorous return analysis on every investment. Extra Space's hurdle rates are transparent: acquisitions must be accretive to FFO within 12 months, achieve targeted returns within three years, and strengthen market position or capabilities.

They've also mastered the art of recycling capital. Underperforming assets in non-core markets get sold, with proceeds redeployed into higher-return opportunities. The third-party management platform generates fee income without capital investment. Bridge lending earns attractive returns while building relationships with future sellers. Every dollar works multiple jobs.

The balance sheet management deserves particular praise. Despite massive acquisitions, Extra Space maintains investment-grade ratings and conservative leverage. They've termed out debt to avoid refinancing cliffs, maintained diverse funding sources, and kept sufficient liquidity for opportunistic acquisitions. This financial flexibility becomes a competitive weapon during market dislocations.

Management Alignment and Culture

Extra Space's executive compensation structure aligns management with long-term value creation. Base salaries are modest by REIT standards, but long-term equity incentives are substantial. Performance metrics focus on operational measures (same-store NOI growth, occupancy) not just stock price. This encourages sustainable growth over short-term financial engineering.

The culture, rooted in Utah's conservative business environment, emphasizes operational excellence over financial gymnastics. Employees are encouraged to think like owners—maintaining properties, knowing customers by name, and finding efficiencies. The company promotes from within, creating institutional knowledge and continuity. When they acquire companies, they retain top talent, recognizing that local expertise has value.

The Platform Flywheel

All these elements create a self-reinforcing flywheel. Scale drives technology investment, which improves operations, which generates superior returns, which attracts capital, which funds acquisitions, which increases scale. Each turn of the wheel makes the next turn easier.

Competitors face an impossible challenge. Matching any single element of Extra Space's playbook is difficult. Matching all elements simultaneously is virtually impossible. By the time a competitor builds comparable technology, Extra Space has moved on to the next innovation. It's a playbook that compounds advantages over time.

XI. Bear vs. Bull Case & Investment Analysis

Bull Case: The Consolidation Runway Remains Massive

The bull thesis for Extra Space starts with simple math: they control roughly 15% of institutional-grade storage, leaving 85% available for consolidation. With 10,000+ mom-and-pop operators struggling against rising digital marketing costs and technological demands, the acquisition pipeline could sustain decades of growth. Every Fed rate cut makes Extra Space's cost of capital advantage more pronounced, enabling accretive acquisitions that smaller operators can't match.

The operational excellence story has chapters yet unwritten. Life Storage properties still lag Extra Space standards by 200-300 basis points in occupancy. As these properties converge to Extra Space norms—a process already underway—the NOI uplift could exceed $150 million annually. That's found money, requiring no additional capital investment, flowing straight to the bottom line.

Technology disruption in storage has barely begun. While Extra Space leads the sector, they're still early in deploying artificial intelligence for pricing, predictive analytics for customer behavior, and automation for operations. Their data advantage compounds daily—every customer interaction trains algorithms that become increasingly difficult for competitors to replicate. As technology becomes the primary differentiator, Extra Space's continued investment widens the competitive moat.

Geographic expansion opportunities abound. The Storage Express acquisition proved that rural markets, previously considered unviable, can be profitably served through remote management. Thousands of small towns with 5,000-20,000 residents remain unserved or underserved. Extra Space could roll up these markets at attractive multiples while competitors focus on oversupplied urban areas.

The macro backdrop supports sustained demand. American homes keep shrinking—median square footage has declined 10% since 2015—while consumption continues growing. The gig economy creates volatile income streams, driving frequent relocations. Climate change increases displacement from natural disasters. An aging population downsizes but can't bear to discard possessions. These secular trends ensure storage demand for decades.

Valuation remains reasonable relative to growth potential. At current multiples, Extra Space trades at a discount to past peaks despite stronger competitive position post-Life Storage. If the company achieves its synergy targets and maintains historical same-store NOI growth, the stock could appreciate 40-50% over three years while paying attractive dividends throughout.

Bear Case: The Easy Money Has Been Made

The bear thesis begins with supply dynamics. After years of undersupply, development has accelerated. While national statistics show moderation, specific markets face oversupply. Austin, Nashville, and Phoenix—previous growth darlings—see occupancy pressures from new construction. If supply acceleration continues, pricing power evaporates and the sector enters a painful correction similar to 2016-2017.

Interest rate sensitivity poses multiple risks. Higher rates increase Extra Space's borrowing costs, making acquisitions less accretive. They also pressure cap rates, potentially forcing asset writedowns. Most concerning, higher mortgage rates reduce housing turnover—a primary demand driver for storage. The Fed's higher-for-longer stance could pressure operations for years.

Integration execution risk looms large. While Extra Space successfully converted Life Storage systems, cultural integration takes longer. Losing key Life Storage personnel could disrupt operations in critical markets. IT system complications could emerge months post-conversion. The sheer scale of integration—50% increase in portfolio size—stretches management attention and could enable competitors to gain share.

Economic cyclicality might finally matter. Storage has proven resilient through past recessions, but it's never been tested at current valuation multiples. If unemployment spikes and consumers truly retrench, storage could face its first real demand destruction. The industry's pricing power assumes customers are somewhat price-insensitive, but a severe recession could shatter that assumption.

Competition from alternative storage models intensifies. Valet storage companies like Clutter and MakeSpace, while still subscale, offer convenience that appeals to urban millennials. Peer-to-peer storage platforms like Neighbor.com enable homeowners to rent unused space at prices below traditional storage. While these remain niche, they could cap pricing power in key demographics.

Technology advantages might prove temporary. Public Storage's recent technology investments could close the operational gap. New entrants might leapfrog existing systems with cloud-native platforms. If technology becomes commoditized through vendor solutions available to all operators, Extra Space's moat narrows considerably.

Valuation Framework and Investment View

Extra Space trades at approximately 18x forward FFO, a premium to the REIT sector average but justified by superior growth prospects and operational metrics. The dividend yield of 4.5% provides reasonable current income with growth potential. On a price-to-NAV basis, the stock trades near 1.1x, suggesting modest premium to private market values.

The key sensitivity is same-store NOI growth. Each 100 basis points of NOI growth translates to roughly $0.30 in FFO per share. If Extra Space achieves 3-4% same-store NOI growth—reasonable given Life Storage synergies and normalized demand—the stock appears undervalued. If NOI growth stalls at 1-2%, current valuation is probably fair.

Compared to other REITs, Extra Space offers a superior risk-reward profile. Unlike office or retail REITs facing structural headwinds, storage demand remains robust. Unlike industrial REITs trading at peak multiples, Extra Space has room for multiple expansion. Unlike residential REITs facing political pressure on rents, storage operates below the regulatory radar.

For long-term investors, Extra Space represents a compelling opportunity to own the dominant platform in a fragmented industry with sustained consolidation potential. The combination of acquisition growth, operational improvements, and technology advantages should drive superior returns over a full cycle. While near-term volatility is likely given macro uncertainties, the five-year view remains highly constructive.

XII. Looking Forward: The Next Chapter

The path from here to a $100 billion market cap isn't fantasy—it's arithmetic. At a conservative 20x FFO multiple, Extra Space needs to generate $5 billion in annual FFO, implying roughly $2.30 per share versus today's $2.10. With 3% same-store growth, modest acquisitions, and Life Storage synergy realization, they reach that target by 2028. The question isn't if, but when—and what comes next.

Integration completion remains job one. While systems conversion happened in 19 days, true integration takes years. Revenue management algorithms need training on Life Storage property dynamics. Maintenance schedules must be optimized for different building vintages. Labor models require adjustment for local market conditions. Each refinement adds basis points to margins, compounding into meaningful value creation.

The synergy realization trajectory looks conservative. Management guided to $100 million in annual synergies, but history suggests they're sandbagging. The Storage USA acquisition delivered 40% above initial targets. SmartStop exceeded projections by 30%. If Life Storage follows pattern, actual synergies could reach $130-150 million. That's an extra $0.50-0.75 in FFO per share from execution alone.

Future acquisition opportunities will shift toward technology-enabled rollups. The traditional model—buy undermanaged properties, implement best practices—has limits. The next wave involves acquiring technology platforms that enhance capabilities. Imagine Extra Space buying a smart-locks company, integrating IoT sensors, or acquiring customer relationship management specialists. These bolt-on acquisitions might be smaller but could drive outsized returns through platform enhancement.

Geographic expansion internationally beckons. While Extra Space has remained U.S.-focused, international markets offer intriguing possibilities. Europe's storage penetration is one-third of America's. Asia's middle class is exploding, creating storage demand in cities like Tokyo and Singapore. Extra Space could export their technology platform through joint ventures, earning fees without capital investment while learning new markets.

Climate-controlled and specialty storage represent untapped potential. Only 30% of Extra Space's portfolio is climate-controlled, versus 50%+ for new construction. Retrofitting existing facilities could drive 20-30% rent premiums. Specialty storage—wine, documents, vehicles—commands even higher rates. A systematic upgrade program could add $500 million to NOI over five years.

Automation promises step-function margin improvement. The Storage Express model proved unmanned facilities work in small markets. But automation could transform urban properties too. Robotic systems could retrieve storage units, eliminating the need for customer access to facilities. Drone security could replace human guards. While futuristic, these technologies are being piloted today.

The technology platform itself could become a profit center. Extra Space's revenue management system, honed over two decades, could be licensed to international operators. Their digital marketing expertise could be packaged as a service. The third-party management platform could expand beyond storage to related real estate sectors. The company could evolve from storage operator to technology provider with storage assets.

Capital allocation will evolve with scale. As Extra Space approaches Public Storage's size, massive acquisitions become scarce and potentially problematic from an antitrust perspective. Capital will increasingly flow toward dividends, share buybacks, and technology investments. The company might split into PropCo/OpCo structures, unlocking value through financial engineering.

Partnership opportunities multiply with scale. Amazon needs last-mile delivery points—storage facilities could house lockers and sorting operations. Residential developers want amenity differentiation—Extra Space could operate storage as a service within apartment complexes. Moving companies need temporary storage—Extra Space's network provides natural synergy. Each partnership leverages existing infrastructure while generating incremental revenue.

The defensive characteristics become more valuable over time. As economic uncertainty persists, investors will pay premiums for predictable cash flows. Storage's resilience through multiple cycles, combined with Extra Space's operational excellence, creates a sleep-well-at-night investment. In a world of zero-yield bonds and volatile equities, a growing 4.5% dividend backed by real assets attracts capital.

Environmental, social, and governance (ESG) initiatives could differentiate Extra Space. Solar panels on flat roofs generate electricity while reducing operating costs. Electric vehicle charging stations attract customers and generate fees. Community programs—free storage for disaster victims, discounted units for veterans—build goodwill and regulatory support. ESG excellence is becoming table stakes for institutional investment.

The end game might surprise everyone. Extra Space could acquire Public Storage in a merger of equals, creating a $60 billion storage giant. They could split into regional companies to avoid antitrust scrutiny. They could be acquired by a Blackstone or Brookfield seeking yield-generating assets. Or they could remain independent, slowly consolidating the industry for decades to come.

XIII. Outro & Resources

What makes Extra Space Storage special isn't any single attribute—it's the combination of strategic vision, operational excellence, and relentless execution over nearly five decades. From Ken Woolley's Stanford research project to America's largest storage operator, the journey illustrates fundamental business principles: focus beats diversification, operations trump financial engineering, and competitive advantages compound over time.

The storage industry itself deserves recognition. Often dismissed as boring or commoditized, it's actually a fascinating study in micro-economics, human psychology, and societal trends. Americans accumulate possessions they can't store but won't discard. Life transitions create temporary space needs. Businesses require flexibility traditional real estate can't provide. Storage sits at the intersection of these demands, providing essential infrastructure for modern life.

Extra Space's success offers lessons beyond real estate. They proved that technology can disrupt even the most analog industries. They showed that consolidating fragmented markets creates enormous value. They demonstrated that operational excellence, sustained over decades, builds insurmountable competitive advantages. These principles apply whether you're rolling up HVAC contractors, dental practices, or car washes.

For investors, Extra Space represents a case study in REIT investing done right. The combination of predictable cash flows, growth through consolidation, and operational improvements creates multiple ways to win. The dividend provides downside protection while the platform advantages drive appreciation potential. It's a reminder that boring businesses often make the best investments.

The human element shouldn't be forgotten. Behind every storage unit is a story—a family downsizing after kids leave, an entrepreneur storing inventory, a collector protecting treasures. Extra Space's 4,000 facilities serve over two million customers, each trusting the company with their possessions. That responsibility, taken seriously, has driven the culture of operational excellence that distinguishes Extra Space.

Looking back, the key inflection points seem obvious. Going public in 2004 provided acquisition currency. Buying Storage USA in 2005 achieved national scale. Developing the third-party management platform created capital-light growth. Acquiring Life Storage established industry leadership. But at each moment, success was far from guaranteed. Bold decisions, coupled with flawless execution, made the difference.

The broader lesson is that industry structure matters more than most realize. In fragmented industries with consolidation potential, scaled operators enjoy compounding advantages. Extra Space identified this dynamic early and executed relentlessly. While competitors debated strategy, Extra Space was buying properties, integrating systems, and building scale.

For storage industry participants, Extra Space sets the standard. Their technology investments force everyone to modernize. Their operational metrics become industry benchmarks. Their acquisition activity sets valuation expectations. Whether partner or competitor, everyone in storage must account for Extra Space's presence.

The next decade promises more change than the previous four combined. Technology will continue disrupting operations. Consolidation will accelerate as mom-and-pop operators age out. New storage models will emerge serving specific niches. Through it all, Extra Space's platform approach positions them to adapt, acquire, and thrive.

Perhaps the most remarkable aspect is how Extra Space has democratized wealth creation. A Utah-based company, founded with one facility in Montana, now trades on the New York Stock Exchange with a market cap exceeding many Fortune 500 companies. Retail investors who bought at the IPO and reinvested dividends have seen 20x returns. It's capitalism at its best—creating value for customers, employees, and shareholders alike.

The story continues to unfold. Each quarterly earnings call adds new chapters. Every acquisition creates fresh opportunities. Technology innovations promise unprecedented capabilities. Extra Space Storage, once an unlikely Stanford research project, has become one of American real estate's great success stories. And the best chapters may be yet unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube