Expedia Group: Building the World's Travel Platform

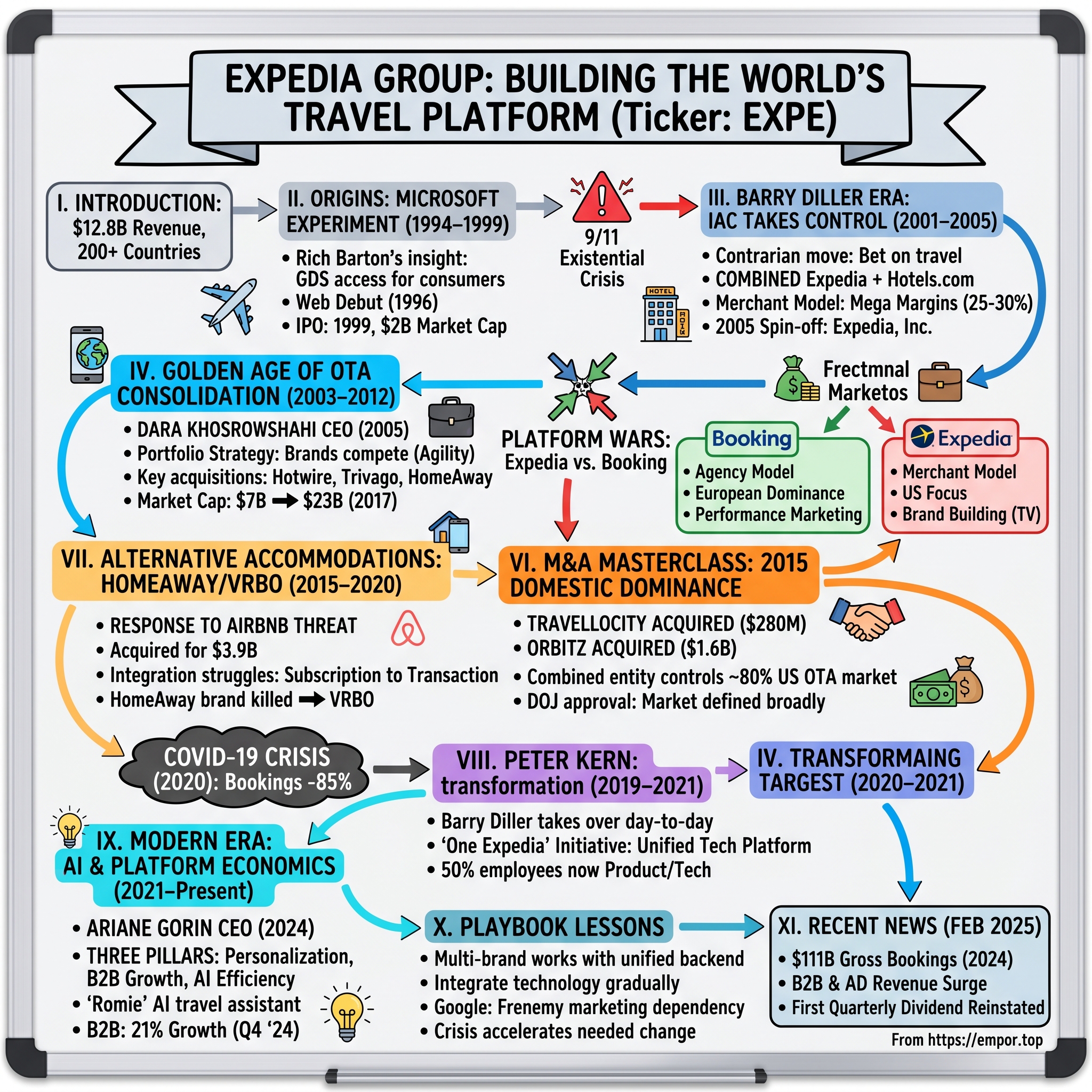

I. Introduction & Episode Roadmap

Picture this: Every second, somewhere in the world, someone books a trip through an Expedia Group property. A family in Tokyo reserves a vacation rental in Hawaii through VRBO. A business traveler in London finds a last-minute hotel on Hotels.com. A couple in São Paulo compares flight prices on Expedia. This happens 24/7, across 200+ countries, generating $12.8 billion in annual revenue. The company processes over 600 million room nights yearly—that's roughly one booking for every thirteen people on Earth.

Yet here's what's remarkable: This global travel behemoth started as a side project inside Microsoft, a tech company that had no business being in travel. The central question driving our story today isn't just how Expedia became one half of the global online travel duopoly alongside Booking Holdings. It's how a company survived multiple near-death experiences—from 9/11 to COVID-19—reinvented itself through aggressive M&A, and built a platform that fundamentally changed how humans explore the world.

The Expedia story is really three intertwined narratives. First, it's a masterclass in platform economics—how network effects, scale advantages, and marketplace dynamics create winner-take-most markets. Second, it's a case study in M&A as core strategy, with over $15 billion deployed on acquisitions that either turbocharged growth or nearly destroyed the company. Third, it's a survival tale of navigating successive waves of disruption: from dial-up to broadband, desktop to mobile, search to social, and now AI.

For investors and operators, Expedia offers critical lessons about building and scaling marketplace businesses. When does a multi-brand portfolio strategy make sense versus consolidation? How do you manage the tension between growth and profitability when your largest supplier (hotels) wants to go direct and your largest marketing partner (Google) is also your biggest competitive threat? What happens when you try to transform a collection of acquired companies into a unified platform while the market is shifting beneath you?

Today we'll explore how Barry Diller saw opportunity where others saw chaos after 9/11, why Dara Khosrowshahi chose domestic dominance over international expansion, and how Peter Kern's pandemic-era transformation might have saved—or doomed—the company's future. We'll dissect the economics of online travel, from take rates to marketing efficiency, and examine whether Expedia's massive scale advantage still matters in an AI-powered future.

II. Origins: The Microsoft Experiment (1994–1999)

In 1994, while most Americans still booked travel by calling 1-800 numbers or visiting strip-mall travel agencies, a Microsoft product manager named Rich Barton noticed something odd. The company's CD-ROM products were selling well, but customers kept asking for something that didn't exist: a way to book travel online. At the time, booking a flight meant either knowing the right phone number or having a relationship with a travel agent who had access to the mysterious GDS (Global Distribution System)—essentially a closed network connecting airlines, hotels, and agencies through terminals that looked like they belonged in a 1970s NASA control room.

The GDS systems—Sabre, Amadeus, Galileo—were the hidden infrastructure of global travel, processing billions in transactions but completely inaccessible to consumers. These systems charged airlines hefty fees for distribution, travel agents paid monthly terminal rentals, and the whole ecosystem operated like a medieval guild system. Barton saw the internet as a way to blow this wide open. In spring 1995, Barton's team was initially tasked with creating a travel CD-ROM. But Barton had bigger ambitions—he persuaded Microsoft leadership to pivot toward an online travel business instead. The pitch was audacious: Microsoft would invest $100 million to build a group of personal computers that could do what only mainframe airline-reservation systems could do—retrieve flight information and purchase tickets, allowing users to build customized trips rather than buy prepackaged ones.

Gates, Ballmer, and Myhrvold gave Barton permission to move forward, and Expedia debuted on the web in 1996. The technological challenge was immense. Barton's team had to reverse-engineer the cryptic command-line interfaces of the GDS systems, create consumer-friendly search and booking flows, negotiate data access with airlines and hotels who saw this as a threat, and build infrastructure that could handle real-time inventory and pricing updates—all while most Americans were still on dial-up internet.

The cultural dynamics within Microsoft added another layer of complexity. Here was a company built on packaged software trying to create a transaction-based internet business. Expedia employees worked in a separate building, operated with startup-like autonomy, and had compensation structures tied to booking volume rather than software licenses. Barton pitched the transformative idea directly to Bill Gates: letting everyday travelers book their own flights and hotels by giving them online access to previously hidden reservation systems. It was democratization through technology—classic Microsoft, yet completely different.

On October 22, 1996, Microsoft officially introduced Expedia.com. Within months, it became clear this wasn't just another Microsoft product—it was a fundamentally different business. By 1998, Expedia was generating hundreds of millions in gross bookings, but Microsoft's board grew increasingly uncomfortable. The company was already facing antitrust scrutiny; owning a platform that competed with thousands of travel agents didn't help the optics.

On November 10, 1999, Microsoft spun off Expedia, with the company debuting on the Nasdaq at $15 per share and soaring to $65.88 on its first day—a 339% gain. The IPO produced a market cap of $2 billion. The timing seemed perfect: It was peak dot-com bubble, online travel was exploding, and Expedia had first-mover advantage. What could possibly go wrong?

III. The Barry Diller Era Begins: IAC Takes Control (2001–2005)

IAC, known at the time as USA Networks Inc, acquired a controlling interest in Expedia in 2001 and acquired the remainder in 2003. But the story of how Barry Diller came to control Expedia—and why he bet everything on travel during the industry's darkest hour—reveals the contrarian genius that would reshape online travel. On July 16, 2001, Barry Diller's USA Networks announced it intended to acquire a controlling stake in Expedia and to purchase outright National Leisure Group, then the largest online cruise and vacations packager. The terms called for Expedia shareholders to receive $35.50 in two classes of USA Networks stock for each share, giving USA Networks a 75% stake. Microsoft agreed to transfer its 70% position. The deal valued Expedia at approximately $1.5 billion.

But then came the terror attacks of September 11, 2001.

Travel stopped cold. Airlines grounded. Hotels empty. The entire industry faced an existential crisis unlike anything since World War II. Diller's board at IAC gathered to discuss whether they should back out of the acquisition. This was the moment that would define Expedia's future.

"And we talked it over and I remember someone at the meeting – Barry and I still debate who it was – said, 'If there's no travel, there's no life.'" The room went quiet. Then someone added: "It's going to come back. Expedia is going to be an important part of it."

Diller made the contrarian call. To his credit, Diller and his IAC went ahead in early 2002 and acquired a controlling stake in Expedia when the flames of September 11 and the toll it took on the travel economy were still reflexive recollections. While IAC did back out of the separate NLG cruise acquisition, they pressed forward with Expedia, ultimately acquiring the remaining shares in 2003.

Diller's philosophy was unique in the internet landscape: build an internet conglomerate through aggressive M&A and cross-pollination of assets. He'd already assembled Hotel Reservations Network (which owned 1-800-HOTELS), Ticketmaster, Match.com, and various media properties. Remember Barry's background: He owned the Home Shopping Network so he understood this idea that you could have a phone number that people could call and you have a catalog or television to drive the demand and everybody calls this phone number, and you have real scale economies and commerce.

The genius move was combining Hotel Reservations Network (later renamed Hotels.com) with Expedia. Diller's IAC paired Hotel Reservations Network, which was renamed Hotels.com, with Expedia, and created a merchant-model hotel-booking powerhouse that made mega margins. The merchant model—where OTAs buy inventory wholesale and mark it up—generated 25-30% margins versus the 5-10% agency commissions. This infuriated hotels but generated massive cash flow that funded further expansion.

By 2004, Barry had realized that the majority of his portfolio within IAC were travel companies. The logic became clear: why not separate them out and create an umbrella company—Expedia Group? The portfolio approach allowed different brands to target different customer segments while sharing technology and supplier relationships. It was platform economics before anyone called it that.

IV. The Golden Age of OTA Consolidation (2003–2012)

In August 2005, the company bundled together its travel-related sites and spun them off as a new public company, Expedia, Inc. The spin-off from IAC marked the beginning of Expedia's golden age—a period of aggressive consolidation that would transform the online travel landscape forever. The story of Dara Khosrowshahi's rise to CEO illuminates the strategic philosophy that would define Expedia's golden age. In 2001, IAC purchased Expedia, and in August 2005, Khosrowshahi became Expedia's chief executive officer after serving as the Chief Financial Officer of IAC Travel. His background—an Iranian refugee who fled during the 1979 revolution, educated at Brown in electrical engineering, trained in finance at Allen & Company—gave him a unique perspective on building global businesses through adversity.

Dara Khosrowshahi's journey with Expedia began in 2005 when he was appointed as the CEO. At the time, Expedia was a fledgling online travel company, grappling with fierce competition and struggling to establish a solid market presence. Under his leadership, Expedia transformed into one of the world's leading online travel agencies.

Khosrowshahi inherited a complex challenge: managing a portfolio of competing brands that Barry Diller had assembled. The solution was counterintuitive—let them compete. "Dara was the CEO at the time and he really felt as if it would create agility and competition amongst the group, if we allowed them to operate independently," internal executives recalled. Early conversations about consolidating marketing, technology, HR, and finance were rejected. Research showed that each brand was tailoring itself to different customer segments.

The portfolio included distinct value propositions: Expedia for full-service bookings, Hotels.com for hotel-only searches with its rewards program, Hotwire for opaque inventory deals. This multi-brand strategy became Expedia's secret weapon—while competitors focused on a single brand, Expedia could capture different segments of the market simultaneously.

Consider the acquisitions they identified and made during this period: Hotel Reservations Network (1999, pre-Khosrowshahi but integrated under him), Expedia itself (2002), Hotwire (2003), China's eLong and TripAdvisor (both 2004). Each acquisition wasn't just about adding revenue—it was about building different moats. TripAdvisor brought user-generated content and meta-search capabilities. eLong provided entry into China. Hotwire captured price-sensitive travelers willing to book blind.

Khosrowshahi transformed Expedia by acquiring companies like Hotels.com, Hotwire, Trivago, and HomeAway, enhancing the technological infrastructure, and expanding the company's international reach. The acquisition strategy was surgical—targeting companies that either expanded geographic reach, added new customer segments, or provided technological capabilities that would take years to build internally.

The numbers tell the story: Expedia's market cap increased more than 300% during Khosrowshahi's tenure, from roughly $7 billion at the 2005 spin-off to $23 billion by 2017. But the real transformation was operational. Khosrowshahi pioneered what he called "test and learn"—running thousands of A/B tests simultaneously across brands, sharing learnings but maintaining brand independence. This approach generated compound improvements in conversion rates, average order values, and customer lifetime value.

The merchant model that Diller had pioneered with Hotels.com became the profit engine. While Priceline (now Booking Holdings) focused on the agency model internationally, taking 12-15% commissions, Expedia's merchant model captured 25-30% margins by taking inventory risk. Hotels initially resisted, but during the 2008 financial crisis, they became desperate for the guaranteed revenue that Expedia's merchant model provided.

By 2012, Expedia had become a consolidation machine, but storm clouds were gathering. Google was becoming more aggressive in travel search. Priceline's Booking.com was dominating Europe. And a new threat was emerging from San Francisco—Airbnb was reimagining what travel accommodation could be.

V. The Platform Wars: Expedia vs. Priceline (2012–2015)

The battle between Expedia and Priceline during 2012-2015 wasn't just competition—it was two fundamentally different philosophies of how to build a global travel platform colliding at massive scale. While the companies looked similar from the outside, their approaches to technology, marketing, and international expansion couldn't have been more different. The European battlefield told the story. Booking started a little bit later than Expedia but growing up in Europe, based in Amsterdam, they really quickly understood multicultural, multicurrency, multilanguage aspects of building websites in Europe. Expedia didn't understand these nuances because they were US based. Booking focused on one product—hotels—and didn't do any TV in the beginning. It was all Google and they just got really good at it.

The fundamental model difference proved decisive. Booking had a different model—an agency model where the consumer pays after the stay, versus Expedia in the US where the customer paid at the time of booking. That was good for the US, but not good for the rest of the world. European travelers were accustomed to booking hotels directly and paying at the property. Requiring prepayment with a foreign company using US dollars created friction that Booking.com avoided entirely.

The marketing strategies couldn't have been more different. Expedia spent hundreds of millions on television advertising, building brand awareness through mass media. Their Super Bowl commercials and celebrity endorsements were designed to make "Expedia" synonymous with travel booking. Meanwhile, Booking.com operated like a performance marketing machine—pouring every dollar into Google AdWords, constantly optimizing conversion rates, and letting the numbers guide every decision.

By 2013, the results were stark. In Europe, Booking.com held over 60% market share in major countries like France, Italy and Spain. Expedia trailed at under 20% share, struggling to shake Booking's reputation for better rates and availability at small charming hotels. The inventory difference was crucial—Booking.com had aggressively signed up small, independent hotels across Europe, while Expedia focused on chain properties that American travelers recognized.

The mobile disruption of 2012-2014 created another divergence point. Booking.com rebuilt their entire platform mobile-first, recognizing that international travelers often booked accommodations on the go. They pioneered features like "book now, pay later" and instant booking confirmation that worked seamlessly on smartphones. Expedia, managing multiple brands with different technology stacks, moved more slowly. Their mobile apps for Expedia, Hotels.com, and Hotwire were essentially separate products, creating confusion and duplication.

The Google dependency problem became existential during this period. Both companies were spending 40-50% of revenue on marketing, with the vast majority going to Google. But as Google introduced its own travel products—Google Hotels, Google Flights—the OTAs faced a terrible dilemma. They were funding their biggest future competitor while becoming increasingly dependent on traffic from that same competitor. Some executives called it the "drug dealer problem"—Google controlled the supply, set the prices, and could cut them off anytime.

Domestically, Expedia made a strategic choice: if they couldn't win internationally against Booking.com, they would dominate North America so thoroughly that no one could challenge them. This set the stage for the most aggressive M&A spree in online travel history.

VI. The M&A Masterclass: Travelocity, Orbitz, and Market Dominance (2015)

The year 2015 would go down as the moment Expedia executed one of the most audacious consolidation plays in internet history. Within months, they would acquire their two largest domestic competitors, fundamentally reshaping the competitive landscape of American online travel. The sequence began in January 2015. After buying Travelocity earlier this month for $280 million, Expedia continues its online travel acquisition spree. The Travelocity deal was almost anticlimactic—the once-mighty brand that had pioneered online travel as a Sabre spinoff was acquired for just $80 million more than TripAdvisor had paid for a tours company. Travelocity, which at one point was the leading online travel company in the world, had been reduced to around 50 employees in North America, essentially functioning as a marketing shell powered by Expedia's technology since 2013.

But Travelocity was just the appetizer. On February 12, 2015, Expedia announced an agreement to acquire Orbitz for $1.6 billion—or $12 per share—in cash, a premium of 29% on Orbitz's current share price. The audacity was breathtaking: Where there were four primary competitors in the online travel booking market as recently as last year, there would only be two.

The strategic rationale was multifaceted. First, scale economics in supplier negotiations. Hotels had been pushing back on OTA commissions, reducing them from 21% to 16% industry-wide. With Orbitz's additional volume, Expedia could resist further commission compression. Second, marketing efficiency. The combined entity could optimize spending across brands, eliminating duplicative keyword bidding that only benefited Google. Third, technology consolidation. Running multiple platforms was expensive; migrating Orbitz to Expedia's infrastructure would save tens of millions annually.

The antitrust scrutiny was intense. Expedia's proposed acquisition of Orbitz would consolidate the largest and third largest online travel agencies in the world, resulting in higher prices, more hidden costs, and fewer choices for booking hotels, flights, and rental vehicles online, critics argued. Investment analyses suggested the acquisition would result in Expedia controlling as much as 80% of the domestic online travel agency market.

But Expedia's legal team had done their homework. They argued that when all channels for booking travel are taken into account, OTAs generate just 16% of total U.S. gross bookings. Hotels could sell directly, through Google, through metasearch sites, through corporate travel managers. The market definition mattered enormously—if you defined it narrowly as "online travel agencies," Expedia would have a monopoly. If you defined it broadly as "travel distribution," they were just one player among many.

On September 16, 2015, the Department of Justice's Antitrust Division issued its verdict: they would not challenge the deal. The DOJ concluded that Expedia's acquisition of Orbitz is not likely to substantially lessen competition or harm U.S. consumers. Their reasoning was revealing: Orbitz is only a small source of bookings for most of these companies and thus has had no impact in recent years on the commissions Expedia charges. The government essentially admitted that Orbitz was already competitively irrelevant.

Expedia, Inc. (NASDAQ: EXPE) today announced that it has completed its acquisition of Orbitz Worldwide, Inc., including all of its brands and assets, for US$12.00 per share in cash, representing an enterprise value of approximately US$1.6 billion. With the stroke of a pen, Expedia had eliminated its last major domestic competitor. The American online travel market was now a duopoly.

VII. The Alternative Accommodations Gambit: HomeAway/VRBO (2015–2020)

While Expedia was consolidating the traditional OTA market, a existential threat was emerging from San Francisco. Airbnb wasn't just another accommodation provider—it was reimagining what travel lodging could be. By 2015, the company was valued at $25 billion and adding more room nights than the entire Hilton chain. Expedia needed a response, and they needed it fast. On November 4, 2015, Expedia Group announced it would acquire HomeAway, including VRBO, for $3.9 billion. The price tag—$38.31 per share, a 20% premium—reflected desperation as much as opportunity. "We have long had our eyes on the fast growing ~$100 billion alternative accommodations space and have been building on our partnership with HomeAway, a global leader in vacation rentals, for two years," Khosrowshahi announced. What he didn't say: Airbnb was eating their lunch, and they needed a response yesterday.

HomeAway wasn't Airbnb. Founded in 2005 in Austin, Texas, it had grown through aggressive M&A of its own, rolling up vacation rental sites like VRBO (acquired 2006), VacationRentals.com, and international properties. By 2015, HomeAway featured more than one million paid vacation rental home listings in 190 countries. But crucially, 95% of HomeAway's inventory was second homes—beach houses, ski chalets, country retreats. These were $500-per-night properties rented by families for week-long vacations, not $50 spare bedrooms for backpackers.

The business models couldn't have been more different. HomeAway operated on an annual subscription model—property owners paid $349-$999 per year to list their properties, regardless of bookings. Airbnb took a transaction fee on each booking. HomeAway catered to professional property managers with multiple listings. Airbnb enabled anyone with a spare room to become a micro-hotelier. HomeAway's average booking was seven nights at $1,400. Airbnb's was 2.4 nights at $160.

The integration would prove to be one of the most challenging in Expedia's history. First came the business model transformation. HomeAway's subscription model had to be converted to a transaction model to integrate with Expedia's platform. Property owners revolted—they'd paid for annual listings and now faced commission fees on each booking. Forums lit up with angry owners threatening to abandon the platform. "VRBO / HomeAway / Expedia is creating rapport with your customer when it should be you creating rapport with your customer," one owner posted.

The technology integration was equally painful. HomeAway's platform was built for long-term rentals with complex availability calendars, cleaning schedules, and owner block-outs. Expedia's platform assumed nightly hotel inventory. Merging these systems while maintaining two different user experiences—one for hotels, one for vacation rentals—created massive technical debt. "Since it was founded 25 years ago, Vrbo has become a leader in the vacation rental industry and a household name in family travel. Through the years, the Vrbo brand has consistently outperformed HomeAway with family travelers. Unifying our vacation rental brands under Vrbo allows us to focus our energies on providing the best travel experience for families everywhere. By consolidating Vrbo and its second largest brand – HomeAway US – into one, Expedia Group can be wholly dedicated to building more brand affinity for Vrbo and its devoted customer base of travelers and vacation home owners and property managers."

The cultural clash was profound. HomeAway's Austin headquarters embodied startup culture—ping pong tables, beer on tap, a "work hard, play harder" mentality. Expedia's Seattle operations ran like a Fortune 500 company—process-driven, metric-obsessed, corporate. HomeAway employees watched their stock options vest while their autonomy evaporated. Within two years, most of the senior leadership had departed.

By 2019, Expedia made a decisive move: kill the HomeAway brand entirely and consolidate everything under VRBO, rebranded as "Vrbo" (pronounced "VER-bo"). "HomeAway acquired VRBO in 2006, and Expedia Group acquired HomeAway in 2015. Despite minimal investment in the brand, VRBO sustained strong brand recall and affinity among its biggest fans for years. In early 2019, VRBO rebranded to Vrbo and introduced a fresh, new logo and pronunciation."

But the integration struggles had cost precious time. While Expedia wrestled with platform migrations and brand consolidations, Airbnb grew from a $25 billion valuation in 2015 to $75 billion by 2019. Expedia had spent $3.9 billion to become a distant second in a market they helped create but couldn't dominate.

VIII. Crisis and Transformation: COVID-19 and Leadership Change (2019–2021)

The cracks in Expedia's foundation became visible long before COVID-19 delivered the knockout blow. In December 2019, the board made a shocking announcement: Mark Okerstrom and Alan Pickerill were resigning as CEO and CFO, respectively, effective immediately. The official reason was a "disagreement over strategy," but insiders knew the truth—the company's aggressive M&A strategy had created an unwieldy monster that no one could control. Barry Diller, never one to mince words, took over day-to-day operations and delivered his verdict in February 2020: The company had become "sclerotic and bloated" and employees were "all life and no work." His assessment was brutal but accurate. Expedia was running seven different technology platforms, maintaining separate marketing teams for each brand, and had ballooned to over 25,000 employees. Integration of acquired companies had stalled. The promise of synergies remained just that—promises.

Then came the pandemic.

In March 2020, global travel essentially stopped. Expedia's bookings fell 85% in a matter of weeks. Revenue dropped from $12 billion annually to a run rate of less than $3 billion. The company was burning $250 million in cash per month. This wasn't a crisis—it was an extinction-level event.

In April 2020, Peter Kern was appointed as CEO of Expedia Group. A board member since 2005 and vice-chairman since 2018, Kern brought a unique perspective. He'd watched the company's M&A binge from the boardroom, understood where the bodies were buried, and had the trust of Barry Diller. His first moves were swift and brutal: 3,000 jobs cut immediately, another 3,000 to follow. Marketing spend slashed to zero. Non-essential projects terminated.

But Kern saw opportunity in catastrophe. "A crisis helps you pick your battles. I bring fresh eyes, I've been seven to eight months in this role in earnest and it gives you latitude to make decisions that were hard before. There is no time for the maybes, you have to focus on what you are good at," he reflected.

The transformation Kern initiated was radical. First, he announced the "One Expedia" initiative—all brands would migrate to a single technology platform. No more seven different booking engines, inventory systems, or customer databases. The technical debt from years of acquisitions would finally be addressed. "Each of our brands had their own technology, and we didn't have as many shared resources as we probably should. We would build and then rebuild and rebuild with the same activities across seven locations and many data lakes," Kern explained.

The numbers tell the story of the transformation. "Kern said Thursday that Expedia Group today has 30% fewer employees than it did in 2019, and has closed 100 offices. In 2019, he said, 30% of employees worked in product and tech. That figure is 50% today." The company went from being a marketing-driven operation to a technology-first platform.

The pandemic accelerated changes that would have taken years. Vacation rentals, particularly Vrbo, became a surprise bright spot as travelers sought whole homes over hotel rooms. "Vrbo is all about the whole home experience and that's attractive during Covid," Kern noted. Direct bookings increased as customers sought flexibility and cancellation options that OTAs could negotiate better than booking directly with suppliers.

Kern's most profound insight came from watching travel patterns during the pandemic: "The day there's a vaccine announced, that people really believe in, will be our highest booking day in history." He was almost right—when vaccines were approved in late 2020, Expedia saw its highest booking day since 2019, with summer 2021 bookings surging 200% week-over-week.

By 2021, a different Expedia was emerging from the ashes. Leaner, more focused, technologically unified. The company that had spent two decades acquiring brands was finally becoming what it had always claimed to be—a true platform. But questions remained: Could this transformation stick? Would the unified platform deliver the promised efficiencies? And most importantly, could Expedia compete in a world where Google, Amazon, and Airbnb were all eyeing the travel space?

IX. The Modern Era: Platform Economics and AI (2021–Present)

The appointment of Ariane Gorin as CEO in May 2024 marked not just a leadership transition but a philosophical shift in how Expedia viewed its role in the travel ecosystem. Gorin, who had been with Expedia since 2013 and led the Expedia Business Services division, represented continuity with Kern's transformation while bringing fresh perspective on what a travel platform could become in the age of AI.The Expedia that Gorin inherited in 2024 was fundamentally different from the acquisition-hungry conglomerate of 2015. The tech migration was complete—all three core brands (Expedia, Hotels.com, and Vrbo) now operated on a single platform with unified data. The One Key loyalty program allowed users to earn and spend points across all properties. The company had successfully transformed from a collection of websites to a true platform business.

But the competitive landscape had shifted dramatically. Google's AI-powered search was becoming increasingly sophisticated at answering travel queries directly. Amazon was quietly building travel capabilities. Airbnb had expanded beyond accommodations into experiences and long-term stays. The question wasn't whether Expedia could compete—it was whether the OTA model itself would survive the AI revolution.

"Ariane Gorin was on the Skift Global Forum stage for the first time since becoming CEO of Expedia Group. Gorin took the role on May 13 and moved to Seattle after living in London and Paris for the past 23 years. She kicked off the final day of the forum on Thursday, her first appearance as CEO at a travel industry conference, with a discussion about the future of Vrbo, loyalty, AI, and more."

Gorin's strategy centered on three pillars, all powered by artificial intelligence. First, delivering more value for travelers through personalization at scale. Second, investing in growth areas like B2B travel and advertising. Third, driving operating efficiencies to expand margins—essentially using AI to do more with less.

The AI initiatives went far beyond consumer-facing chatbots. "Expedia Group CEO Ariane Gorin is extensively testing artificial intelligence (AI) throughout the company's operations. This was revealed during her speech at The Phocuswright Conference 2024 in Phoenix, Arizona. Gorin mentioned that Expedia was among the initial companies to incorporate ChatGPT into its app for testing. Currently, AI is being trialed in diverse aspects of the company's operations, including customer service, product reviews, and destination insights."

The introduction of Romie, Expedia's AI travel assistant, represented a philosophical shift. Rather than competing with Google on search, Expedia would become the execution layer for travel planning. "When you need to know what the price is, are there rooms on that day, can you get a plane on that day, can you get the seats you want, you need us," as Peter Kern had articulated before his departure.

The B2B business, which Gorin had led before becoming CEO, emerged as a surprising growth driver. "The company reported revenue of $3.1 billion in Q4, up 10% year over year. This growth was primarily driven by a 21% increase in B2B revenue and a 25% surge in advertising revenue, alongside growth in all three of its B2C brands—Expedia, Hotels.com, and Vrbo." Banks, airlines, and corporate travel managers were licensing Expedia's technology to power their own travel booking—turning potential competitors into customers.

The platform economics finally started working. With unified technology, the cost of adding new supply dropped dramatically. Marketing efficiency improved as customer data could be shared across brands. The loyalty program created switching costs that hadn't existed before. Expedia was becoming what economists call a two-sided network—the more suppliers joined, the more valuable it became to consumers, and vice versa.

But challenges remained profound. The rise of AI search engines created existential uncertainty about online visibility. "Since the first generative AI model was released in 2022, there's been concern that the tech could dismantle the way online travel agencies operate — or eventually lead to their downfall. Ariane Gorin, president and CEO of Expedia Group, addressed some of those concerns Wednesday at the Phocuswright conference in Phoenix. Expedia faces challenges from AI advancements, particularly regarding its relevance as digital travel agents evolve. The rise of AI search engines creates uncertainty for travel companies about online visibility and advertising."

The modern Expedia is thus a paradox: more technologically sophisticated than ever, yet more vulnerable to disruption. More unified as a platform, yet competing in an increasingly fragmented market. More efficient operationally, yet facing margin pressure from all sides. The company that began as Microsoft's experiment in online commerce had evolved into something neither Rich Barton nor Barry Diller could have imagined—a global travel platform wrestling with its own relevance in an AI-powered future.

X. Playbook: Strategic Lessons

After nearly three decades of evolution, acquisitions, crises, and transformations, Expedia's journey offers profound lessons about building and scaling platform businesses. These aren't just travel industry insights—they're universal principles about marketplace dynamics, M&A strategy, and competitive positioning in the digital age.

The Portfolio Approach: When Multi-Brand Strategies Work

Expedia's multi-brand portfolio—long criticized by Wall Street as inefficient—actually proved remarkably resilient. The key insight: brands aren't just marketing vehicles; they're customer acquisition funnels with distinct psychologies. Hotels.com attracts deal-seekers with its "collect 10 nights, get 1 free" program. Expedia serves full-service travelers booking flights plus hotels. Vrbo captures family vacationers seeking entire homes. Hotwire monetizes distressed inventory through opaque pricing.

The portfolio approach works when: (1) Customer segments have genuinely different needs and behaviors, (2) The cost of maintaining separate brands is offset by improved targeting and reduced channel conflict, (3) Backend operations can be unified while frontend experiences remain distinct, and (4) Brands can share technology and supplier relationships without cannibalizing each other.

Where Expedia struggled was execution. For years, they maintained separate technology stacks, marketing teams, and supplier relationships for each brand. Only when forced by COVID to unify the platform did they realize the true benefits of the portfolio approach—diverse customer acquisition with unified operations.

M&A as Core Competency: Integration Patterns and Mistakes

Expedia executed over 30 acquisitions totaling $20+ billion, making M&A not just a growth strategy but a core competency. The pattern that emerged: successful acquisitions (Hotels.com, Trivago) maintained brand independence while integrating backend operations. Failed integrations (early HomeAway, Orbitz technology) tried to force acquired companies into Expedia's existing model too quickly.

The integration playbook evolved through painful trial and error. First, preserve what made the acquisition valuable—usually its customer relationships and brand equity. Second, migrate technology gradually, starting with non-customer-facing systems. Third, unify supplier relationships to gain negotiating leverage but maintain separate merchandising strategies. Fourth, consolidate overhead functions (HR, finance, legal) immediately but keep product and marketing teams separate initially.

The HomeAway acquisition violated every rule in this playbook. Expedia forced a business model change (subscription to transaction), alienated the core customer base (property owners), and rushed technology integration. The result: five years of integration pain and a missed opportunity to dominate alternative accommodations before Airbnb became unstoppable.

Platform Economics in Travel: Network Effects and Take Rates

Travel marketplaces exhibit unusual economic characteristics. Unlike pure information platforms (Google) or retail marketplaces (Amazon), travel involves complex, high-consideration purchases with significant operational complexity. The network effects are weaker than in social networks but stronger than in traditional retail.

Expedia's take rates—the percentage of booking value they capture—tell the story. Hotel bookings through the merchant model generate 20-25% margins but require working capital and create supplier tension. Agency bookings yield 10-12% but scale infinitely without capital requirements. Vacation rentals produce 8-10% take rates but have higher operational costs. Flights generate just 2-3% margins but drive cross-selling opportunities.

The strategic insight: optimize for lifetime value, not transaction margins. A customer who books flights through Expedia might generate minimal profit on that transaction but becomes far more likely to book hotels, activities, and future trips through the platform. This is why Expedia continued offering flight bookings despite negligible margins—they're customer acquisition tools, not profit centers.

The Marketing Dependency Trap: Google as Frenemy

Expedia's relationship with Google represents one of the most complex strategic challenges in digital commerce. In 2019, Expedia spent $6.03 billion on sales and marketing—over 50% of revenue—with the majority going to Google. They were simultaneously Google's largest travel advertiser and biggest potential competitor.

The trap deepened over time. As Expedia spent more on Google ads, they trained Google's algorithms to understand travel intent, pricing dynamics, and conversion patterns. Google used this intelligence to build its own travel products—Google Hotels, Google Flights, Google Travel—that competed directly with Expedia. The student became the master.

Breaking the Google dependency required fundamental strategic shifts. Direct traffic through mobile apps became priority one. The loyalty program created habitual usage patterns. Email marketing, historically underutilized, became a key retention channel. Content marketing through destination guides and travel inspiration aimed to capture customers earlier in the travel planning funnel. But even today, Google remains Expedia's largest marketing channel and biggest competitive threat.

Technology Debt and the Cost of Acquisitions

Every acquisition brought technology debt—different coding languages, databases, user interfaces, and business logic. By 2019, Expedia was running seven major technology platforms, dozens of data centers, and hundreds of applications. The annual cost of maintaining this technical sprawl exceeded $500 million.

The lesson: acquisition costs extend far beyond the purchase price. For every dollar spent on M&A, Expedia spent another dollar on integration over 3-5 years. Technology migrations that were supposed to take 18 months stretched to 5 years. Customer experience degraded during transitions, causing market share losses that took years to recover.

Peter Kern's radical simplification during COVID—migrating everything to a single platform—should have happened a decade earlier. The unified platform reduced operational costs by 30%, improved development velocity by 50%, and enabled features (cross-brand loyalty, unified inventory) that were technically impossible before. The cost of delay: at least $2 billion in excess operational expenses and immeasurable lost innovation.

Managing Through Crisis: 9/11, 2008, COVID-19 Lessons

Expedia survived three existential crises, each offering distinct lessons. After 9/11, the lesson was speed—Barry Diller's immediate commitment to proceed with the acquisition while competitors hesitated gave Expedia crucial momentum. During the 2008 financial crisis, the lesson was liquidity—having access to capital when hotels desperately needed distribution partners allowed Expedia to gain share.

COVID-19 taught the most profound lesson: crisis enables transformation. Changes that would have taken years—workforce reduction, office consolidation, technology unification—happened in months. Sacred cows were slaughtered. Political resistance evaporated. The company that emerged was fundamentally different from what entered the crisis.

The pattern across all three crises: move fast, preserve liquidity, use disruption to accelerate strategic changes, and remember that travel always recovers. As Kern noted, when vaccines were announced, Expedia saw its highest booking day in history. Human desire to travel is immutable; only the methods change.

XI. Bear vs. Bull Case & Investment Analysis

Bull Case: Scale Advantages and Platform Leverage

The bull case for Expedia rests on five pillars. First, scale still matters enormously in travel distribution. With $111 billion in gross bookings, Expedia has negotiating leverage with suppliers that smaller players can't match. Hotels need Expedia's demand generation, especially in economic downturns when direct bookings decline.

Second, the unified platform finally works. After years of integration pain, Expedia now operates a single technology infrastructure powering multiple brands. This creates operating leverage—every improvement in conversion rate, every new feature, every efficiency gain multiplies across the entire portfolio. The company that spent 50% of revenue on operations in 2019 now spends 35%.

Third, alternative growth vectors are materializing. B2B revenue grew 21% in 2024, as banks and airlines license Expedia's technology. Advertising revenue surged 25% as suppliers pay for prominence on Expedia's platforms. These high-margin revenue streams didn't exist five years ago.

Fourth, the loyalty program creates genuine switching costs. One Key members generate 2.5x the revenue of non-members and churn at half the rate. With 170 million members, this becomes a formidable moat that compounds over time.

Fifth, valuation remains undemanding. At 8x EBITDA compared to Booking's 15x, Expedia trades at a significant discount despite similar fundamentals. If Expedia simply closes half this valuation gap, shares could appreciate 40% without any operational improvement.

Bear Case: Structural Challenges and Disruption Risk

The bear case is equally compelling. Google's travel ambitions represent an existential threat. Every year, more travel searches begin and end on Google without ever reaching an OTA. Google's AI capabilities could eventually eliminate the need for intermediaries entirely—why visit Expedia when Google can plan, book, and manage your entire trip?

Airbnb's expansion beyond accommodations threatens Expedia's bundle advantage. As Airbnb adds flights, car rentals, and experiences, they're building a vertically integrated travel platform that controls unique supply. Expedia sells commoditized inventory anyone can access; Airbnb offers experiences you can't get elsewhere.

The marketing cost structure remains problematic. Despite years of effort, Expedia still spends 40%+ of revenue on marketing, mostly to Google and Meta. This creates a vicious cycle: the more successful Expedia becomes, the more Google can charge for travel keywords. There's no clear path to breaking this dependency.

Integration complexity persists despite unification efforts. Vrbo still operates somewhat independently. International expansion lags Booking.com significantly. The company remains overly dependent on North American leisure travel, making it vulnerable to regional economic shocks.

Finally, generational shifts favor competitors. Younger travelers prefer authentic, unique experiences over standardized hotels. They trust peer reviews over professional marketing. They're comfortable booking directly with suppliers through social media. Every demographic trend points away from traditional OTAs toward more fragmented, experiential travel consumption.

Valuation Framework and Investment Perspective

At current valuations, Expedia appears to offer asymmetric risk/reward for patient investors. The company trades at historical trough multiples despite improved operational metrics. The unified platform reduces execution risk. The brand portfolio provides multiple shots on goal as travel patterns evolve.

The key variables to monitor: (1) Marketing efficiency—if cost per acquisition rises above $50, the model breaks. (2) Take rate stability—compression below 10% would devastate margins. (3) Technology platform performance—any major outages or booking failures could trigger customer exodus. (4) Competitive dynamics—watch Airbnb's expansion and Google's travel product evolution closely.

For long-term investors, Expedia represents a contrarian bet that scale, technology, and brand diversity still matter in travel distribution. The bear case is well understood and arguably priced in. If management executes on platform leverage and AI initiatives, returns could surprise positively. But this requires faith that OTAs remain relevant in an AI-powered future—a bet that's far from certain.

XII. What's Next: The Future of Travel

The future of travel distribution will be shaped by five intersecting forces, each presenting both opportunity and existential threat to Expedia's model.

AI-Powered Trip Planning and the Super App Vision

The vision is compelling: an AI travel companion that knows your preferences, budget, and constraints, automatically planning and booking perfect trips. Expedia's Romie represents early steps toward this future. But the technical challenges are immense. Travel planning involves thousands of variables, real-time inventory, complex pricing, and human preferences that resist algorithmic optimization.

The super app vision—one application managing all travel needs—faces different challenges. Western consumers resist super apps, preferring specialized tools. Regulatory concerns about data concentration grow. Most importantly, suppliers increasingly want direct customer relationships, not intermediation through platforms. The super app future might arrive, but it's unclear whether Expedia or Big Tech wins that game.

Alternative Accommodations Integration

Despite owning Vrbo, Expedia hasn't cracked the alternative accommodations code. The business requires different capabilities: supply acquisition through individual property owners, quality control without standardization, customer service for non-professional hosts. Vrbo remains subscale compared to Airbnb, lacking the network effects that make marketplaces dominant.

The strategic question: double down or divest? Continued investment might never close the gap with Airbnb. But divesting admits defeat in the fastest-growing segment of travel. The likely path: maintain Vrbo as a differentiated family-focused brand while acknowledging it will never dominate alternative accommodations broadly.

Corporate Travel Opportunities

Corporate travel, devastated by COVID, is recovering but transformed. Video conferencing permanently reduced business travel demand. But the travel that remains is higher-value: strategic meetings, sales calls, team building. This creates opportunity for platforms that can handle complex corporate requirements: approval workflows, expense integration, duty of care, negotiated rates.

Expedia's Egencia unit is well-positioned but subscale compared to specialists like Concur or Amex GBT. The strategic choice: invest heavily to gain share in a structurally smaller market, or focus on leisure travel where Expedia has natural advantages? Neither path is obviously correct.

Emerging Market Expansion

International expansion remains Expedia's white whale. Despite decades of effort, the company generates 68% of revenue from North America. Booking.com dominates Europe. Local players control Asia. Latin America and Africa remain fragmented but challenging to penetrate.

The platform unification finally enables efficient international expansion—no longer does Expedia need to build separate infrastructure for each market. But competitive dynamics and consumer behavior vary enormously by geography. What works in Dallas doesn't work in Delhi. The question isn't technical capability but organizational focus and patience for long-term investment.

The Metasearch Threat and Response

Metasearch engines—Kayak, Trivago, Google—increasingly commoditize OTA inventory. Consumers comparison-shop across multiple booking sites, driving up acquisition costs and reducing loyalty. Expedia owns Trivago but can't favor its own inventory without destroying Trivago's credibility.

The strategic response involves moving up the travel funnel: inspiration, planning, packages. If Expedia becomes where trips begin, not just where bookings happen, they can escape commoditization. But this requires content, community, and creativity—capabilities that tech platforms historically struggle to build.

If We Were Running Expedia: Strategic Priorities

Five moves would position Expedia for the next decade:

First, abandon the Google advertising arms race. Accept lower growth but higher profitability by focusing on direct traffic, loyalty, and organic acquisition. The billions saved could fund innovation that actually differentiates.

Second, vertically integrate into unique supply. Partner with independent hotels to create exclusive inventory. Develop Expedia-branded accommodations in underserved markets. Control supply that competitors can't access.

Third, embrace radical transparency. Show customers exactly what Expedia earns on each booking. Explain the value provided: fraud protection, customer service, package assembly. Compete on value, not opacity.

Fourth, open the platform architecture. Let anyone build travel applications on Expedia's infrastructure. Become the AWS of travel—powering thousands of niche travel services while capturing economics through API fees.

Fifth, prepare for post-OTA world. Build capabilities that remain valuable even if traditional OTA model disappears: payment processing, fraud detection, customer service, travel insurance. These services have value regardless of how travel is distributed.

The next decade will determine whether Expedia remains a central player in travel or becomes a cautionary tale about platform disruption. The assets exist for success. The question is whether leadership has the courage to cannibalize today's model to build tomorrow's platform.

XIII. Recent News

Expedia Group reported strong fourth quarter and full year 2024 results on February 6, 2025, demonstrating that the post-pandemic recovery has fully materialized. "Booked room nights grew 12% in the fourth quarter year-over-year and 9% for full year 2024. Total gross bookings and revenue grew 13% and 10% year-over-year, respectively in the fourth quarter. Full year gross bookings and revenue both grew 7% compared to 2023."

The company's financial performance exceeded expectations, with Q4 revenue reaching $3.1 billion, driven by a 21% increase in B2B revenue and a 25% surge in advertising revenue. For the full year 2024, gross bookings hit $111 billion, marking a significant milestone in the company's recovery journey.

Most notably, the Board of Directors approved the reinstatement of a quarterly cash dividend—the first since suspending it during the pandemic in 2020. "Our Board of Directors has approved the reinstatement of a quarterly cash dividend. The Executive Committee of the Board, acting on its behalf, declared a first quarter dividend of $0.40 per share of the company's outstanding common stock, to be paid on March 27, 2025 to holders of record on March 6, 2025. Expedia Group suspended its quarterly cash dividend in the second quarter of 2020 in response to uncertainty driven by the global coronavirus pandemic."

CEO Ariane Gorin outlined three strategic priorities for 2025: delivering more value for travelers through AI-powered personalization, investing in high-growth areas like B2B and international markets, and continuing to drive operating efficiencies. The company is particularly focused on revitalizing Hotels.com and Vrbo, both of which suffered during the technology migration but showed improvement in Q4.

The appointment of Scott Schenkel as CFO marks another leadership transition, replacing Eric Hart who had served since 2020. Schenkel brings extensive experience from previous CFO roles and will oversee the company's disciplined capital allocation strategy, which included $1.6 billion in share repurchases during 2024.

Looking ahead, Expedia provided cautious guidance for 2025, expecting gross bookings and revenue growth in the 4-6% range, roughly in line with 2024 but reflecting foreign exchange headwinds and some softening in travel demand observed in early Q1. The company continues to balance growth investments with margin expansion, targeting long-term profitability improvements while navigating an increasingly competitive and AI-disrupted marketplace.

XIV. Links & Resources

Key SEC Filings and Investor Presentations

- Expedia Group Investor Relations: ir.expediagroup.com

- Latest 10-K Annual Report (2024)

- Q4 2024 Earnings Presentation

- Proxy Statement (DEF 14A) detailing executive compensation and governance

Industry Reports and Analysis

- Skift Research: "The Past, Present, and Future of Online Travel" (2024)

- Phocuswright: "Global Online Travel Overview" (Annual)

- Morgan Stanley: "The Future of Travel Distribution" (2024)

- McKinsey: "The State of Tourism and Hospitality 2024"

Books on Key Figures and Travel Industry

- "The Contrarian: Peter Thiel and Silicon Valley's Pursuit of Power" by Max Chafkin (includes Diller coverage)

- "The Airbnb Story" by Leigh Gallagher (competitive context)

- "Super Pumped: The Battle for Uber" by Mike Isaac (Khosrowshahi's leadership)

- "Direct: The Rise of the Middleman Economy" by Kathryn Judge (platform economics)

Podcast Episodes and Interviews

- Acquired.fm: "Booking Holdings" episode (competitor analysis)

- Masters of Scale: "Rich Barton - Power to the People"

- Skift Podcast: Peter Kern transformation interview series

- How I Built This: Rich Barton on Expedia and Zillow

Academic Papers on Platform Economics

- "Platform Competition in Two-Sided Markets" - Rochet & Tirole (2003)

- "Strategies for Two-Sided Markets" - Eisenmann, Parker & Van Alstyne (HBR)

- "The Antitrust Analysis of Multi-Sided Platform Businesses" - Evans & Schmalensee

- "Network Effects and Market Power" - Katz & Shapiro

Historical Articles and Oral Histories

- Skift: "The Definitive Oral History of Online Travel" (2016)

- GeekWire: "The Expedia Files" series on company history

- Seattle Times: "Expedia's Journey" retrospective coverage

- Wall Street Journal archives on major acquisitions

Industry Data Sources

- STR Global: Hotel performance data

- AirDNA: Vacation rental market analytics

- Phocuswright: Travel research and statistics

- Euromonitor: Global travel market reports

Regulatory and Legal Resources

- DOJ Antitrust Division: Expedia-Orbitz merger review documents

- European Commission: Competition decisions on travel mergers

- FTC: Online travel marketplace studies

- Congressional testimony on OTA market concentration

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube