Evergy: The Power Behind the Heartland

I. Introduction & Setting the Stage

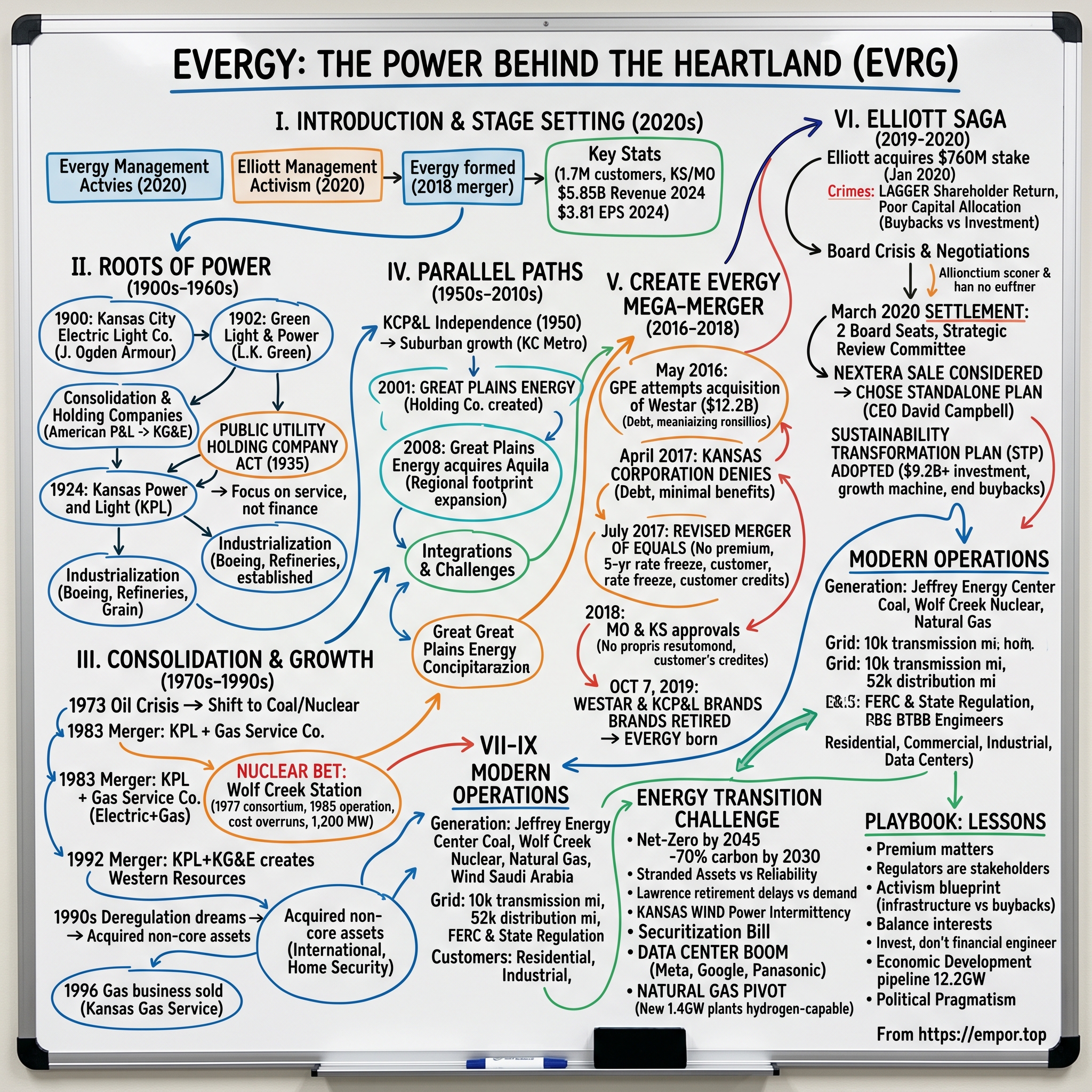

Picture this: It's January 2020, and in a glass tower overlooking Manhattan, Paul Singer's Elliott Management has just accumulated a $760 million stake in a Midwestern utility most New Yorkers have never heard of. Meanwhile, 1,200 miles away in Kansas City, the leadership team at Evergy—a company formed just 18 months earlier from the merger of two century-old utilities—is scrambling to understand why one of Wall Street's most feared activist investors has them in its crosshairs.

The irony? Evergy keeps the lights on for 1.7 million customers across Kansas and Missouri, powering everything from suburban Kansas City homes to massive grain elevators dotting the prairie. It's the unglamorous but essential infrastructure that makes modern life possible in America's heartland. Yet here was Elliott, arguing that this $15 billion market cap utility was leaving billions on the table through poor capital allocation and anemic growth plans. Today, Evergy generates annual revenue of $5.85 billion and posts adjusted earnings per share of $3.81 in 2024, up from $3.54 in 2023. The company serves customers across 28,130 square miles of America's heartland, from the wheat fields of western Kansas to the suburbs of Kansas City. But the real story isn't just about kilowatts and transmission lines—it's about how a collection of frontier-era electric companies navigated a century of technological change, regulatory upheaval, and capital market pressure to become one of the most strategically important utilities in America's energy transition.

What makes Evergy particularly fascinating is the collision of old and new: century-old coal plants being retired while the company fields a more than 10-gigawatt project pipeline and is in advanced negotiations with two large data center customers. This is a company caught between its industrial past and a digital future, between environmental mandates and reliability requirements, between Wall Street expectations and Main Street realities.

Our journey begins at the turn of the 20th century, when electricity was as revolutionary as artificial intelligence is today, and follows the path through mergers, nuclear adventures, activist battles, and ultimately to today's critical question: Can a traditional Midwest utility transform itself fast enough to capture the data center boom while navigating the energy transition? Let's find out.

II. The Roots of Power: Early Origins (1900s–1960s)

The year was 1900, and J. Ogden Armour had a problem. The heir to one of America's great meatpacking fortunes needed electricity—not for refrigeration or lighting, but for something more fundamental: powering the electric railway that moved his products across Kansas City. While other industrialists were content to buy power from existing utilities, Armour had grander ambitions. He purchased the Kansas City Electric Light Company and began building generating capacity with the single-minded focus of a man who understood that controlling your own power meant controlling your own destiny.

Two years later and several hundred miles away, another utility empire was taking shape under the unlikely leadership of Lemuel K. Green. Green's Light & Power Company would undergo multiple transformations—becoming West Missouri Power Company, then Utilicorp, and eventually Aquila—but its DNA would remain constant: serving the smaller communities and rural areas that the big city utilities ignored. This was flyover country before airplanes existed, and Green understood that electrifying these communities wasn't just about profits; it was about fundamentally transforming the economic potential of the American heartland.

By 1909, the consolidation game was already in full swing. The American Power and Light Company swept through Kansas, acquiring electric companies in Wichita, Pittsburg, and Frontenac to create Kansas Gas and Electric (KG&E). This wasn't gentle capitalism—it was the era of the holding company, where financial engineers in New York and Chicago controlled vast utility empires through byzantine corporate structures that would make today's private equity firms blush.

Then came 1924, and with it the birth of Kansas Power and Light (KPL). While KG&E focused on the southern part of the state, KPL rapidly expanded across northeastern Kansas, bringing electricity to farming communities that had never seen an electric light. The competition between these two utilities would define Kansas's electric landscape for the next seven decades.

The story of this era can't be told without understanding the Public Utility Holding Company Act of 1935—arguably the most important piece of legislation in American utility history. The act, born from the excesses of the 1920s when holding companies controlled 75% of the nation's electric generation through leverage that would make Archegos look conservative, fundamentally restructured the industry. Samuel Insull's Middle West Utilities empire had collapsed spectacularly, taking down thousands of investors. The government's response was swift and severe: break up the holding companies, force utilities to focus on defined geographic territories, and subject them to strict regulatory oversight.

For the Kansas utilities, this meant a fundamental shift from financial engineering to actual engineering. No longer could distant holding companies extract profits while underinvesting in infrastructure. The utilities had to focus on what they were meant to do: generate and deliver reliable electricity to their service territories.

This regulatory framework coincided with the massive industrialization of the Midwest. The 1940s and 1950s saw Kansas transform from an agricultural economy to an industrial powerhouse. Boeing's Wichita facility, which would become the "Air Capital of the World," needed massive amounts of reliable power. The oil refineries along the Arkansas River required electricity for their complex petrochemical processes. The grain elevators that dotted the prairie—those concrete cathedrals of American agriculture—needed power for their conveyor systems and climate control.

The utilities responded by building at a scale previously unimaginable. Coal plants sprouted along rivers throughout Kansas and Missouri, using the waterways both for cooling and for barge delivery of Wyoming coal. This was the era of bigger-is-better, when utilities competed on who could build the largest, most efficient generating units. Engineers, not financiers, ruled these companies. The CEO's office walls were more likely to feature heat rate charts than stock price graphs.

By 1960, the foundation was set. KG&E dominated southern Kansas from its Wichita headquarters, KPL controlled the northeastern portion of the state from Topeka, and Kansas City Power & Light ruled western Missouri. Each had built extensive generation and transmission networks, each had developed deep relationships with their industrial customers, and each believed they were destined to remain independent forever.

They were wrong. The age of utility empire building was about to begin, and the comfortable world of engineer-CEOs managing regional monopolies was about to collide with a new reality: scale would determine survival.

III. Consolidation & Growth: The Utility Empire Building (1970s–1990s)

The 1970s oil crisis changed everything. When OPEC quadrupled oil prices in 1973, utilities that had diversified into oil-fired generation watched their fuel costs explode overnight. But for the Kansas utilities, largely dependent on coal and increasingly interested in nuclear power, the crisis presented an opportunity. Natural gas, suddenly valuable for heating and industrial use, became a target for acquisition rather than competition.

This strategic insight led to the transformative 1983 merger between KPL and The Gas Service Company, a natural gas utility serving customers across four states—Kansas, Missouri, Nebraska, and Oklahoma. The deal was revolutionary for its time: a combined electric and gas utility that could offer customers one-stop shopping for all their energy needs. Wall Street loved the diversification, regulators appreciated the potential for shared overhead costs, and customers... well, customers got one bill instead of two.

But the real action was happening in the nuclear field. Wolf Creek Generating Station, located on 9,818 acres of rolling hills near Burlington, Kansas, represented the ultimate bet on scale and technology. The project began in 1977 as a consortium—a structure born of both necessity and prudence. Kansas Gas & Electric owned 47%, Kansas City Power & Light held 47%, and Kansas Electric Power Cooperative took 6%. The arrangement spread the massive capital risk while ensuring no single utility would be crippled if the project went sideways.

And sideways it went, at least initially. Original cost estimates of $1 billion ballooned to $2.9 billion by the time the plant entered commercial operation in 1985. Construction delays, regulatory changes following Three Mile Island, and the general chaos of building something as complex as a nuclear plant in rural Kansas all contributed to the overruns. Yet when Wolf Creek finally came online, its 1,200 megawatts of carbon-free power fundamentally changed the economics of electricity in Kansas. The plant would run at capacity factors above 90%, churning out reliable baseload power that made Kansas electricity among the cheapest in the nation.

The 1992 merger creating Western Resources represented the logical culmination of decades of parallel evolution. KPL and KG&E had spent seventy years as friendly rivals, building duplicative infrastructure and competing for industrial customers in the narrow band where their territories met. The merger synergies were obvious: combined dispatch of generating units, elimination of duplicate transmission lines, shared corporate services. The newly formed Western Resources controlled virtually all of eastern Kansas's electric infrastructure, serving everyone from suburban Johnson County to rural farming communities near the Colorado border.

But the 1990s brought a new philosophy to utility management. The era of deregulation was dawning, and utility executives, watching their peers in telecom and airlines, began to dream of expansion beyond their traditional territories. Western Resources embarked on an acquisition spree that would have been unthinkable in the regulated utility world of the 1960s. They bought interests in international power plants, invested in non-regulated generation, and even acquired a home security company—yes, a home security company—under the theory that utilities needed to become "energy services" companies.

The culmination of this diversification strategy came in 1996 when Western Resources sold its natural gas business to ONEOK for $660 million. The logic seemed impeccable at the time: focus on the higher-margin electricity business, use the proceeds to fund non-regulated ventures, and transform from a sleepy utility into a growth company. The gas assets became Kansas Gas Service, eventually becoming part of ONE Gas, and Western Resources used the capital to chase dreams of deregulated glory.

By 2002, reality had set in. The California electricity crisis of 2000-2001 had shown the dark side of deregulation. Enron's collapse demonstrated the dangers of utilities trying to become trading shops. Western Resources, now rebranded as Westar Energy, retreated to its core business: generating and delivering electricity in Kansas. The home security business was sold, the international ventures were unwound, and the company returned to what it knew best—being a boring, reliable, regulated utility.

Meanwhile, in Kansas City, a parallel drama was unfolding. Kansas City Power & Light had remained more conservative, focusing on its core service territory. But even KCP&L couldn't resist the consolidation wave. After gaining independence from holding company control in 1950, it had steadily expanded, acquiring Eastern Kansas Utilities in 1952 and building a dominant position in the Kansas City metropolitan area.

The formation of Great Plains Energy as a holding company in 2001 signaled KCP&L's ambitions for the new century. The structure would allow for both regulated utility operations and non-regulated ventures, though KCP&L would learn from Western Resources' mistakes and remain more focused on its core competencies.

As the 1990s ended, the stage was set for the next act. Westar Energy dominated Kansas, Great Plains Energy controlled the Kansas City metro, and both were generating strong cash flows from their regulated operations. The question was no longer whether they would merge, but when and how. The forces pushing for consolidation—economies of scale, regulatory efficiency, the need for massive capital investment in infrastructure—were becoming irresistible.

IV. Great Plains Energy & Kansas City Power: Parallel Paths (1950s–2010s)

The story of Kansas City Power & Light's transformation into a regional powerhouse begins with a curious corporate archaeology. In June 1919, the company reincorporated as Kansas City Power and Light Company—no ampersand, just "and." But three years later, after acquiring the Carroll County Electric Company in July 1922, the company reorganized once more, this time adopting "Kansas City Power & Light Company" with the ampersand that would become its signature for the next century. Such attention to corporate nomenclature might seem trivial, but it reflected a company that understood the importance of brand identity long before "brand" became a business school buzzword.

Independence came in 1950 when KCP&L finally broke free from holding company control—a liberation that allowed local management to focus on what they knew best: serving the rapidly growing Kansas City metropolitan area. The timing couldn't have been better. Post-war suburban expansion was exploding across Johnson County, Kansas, and Jackson County, Missouri. Every new subdivision needed power, every new shopping center required transformers, every new office building demanded reliable electricity.

The 1952 acquisition of Eastern Kansas Utilities expanded KCP&L's footprint into the smaller communities surrounding Kansas City. This wasn't a glamorous deal—Eastern Kansas Utilities served small towns and rural cooperatives—but it provided KCP&L with a buffer zone around its core territory and demonstrated management's understanding that controlling the periphery was as important as dominating the center.

For the next five decades, KCP&L pursued a strategy of steady, methodical growth. While other utilities chased international ventures or non-regulated businesses, KCP&L built power plants, strung transmission lines, and focused relentlessly on reliability. The Hawthorn generating station, expanded multiple times between the 1950s and 1970s, became a symbol of this approach: practical, efficient, and utterly lacking in glamour.

The creation of Great Plains Energy on October 1, 2001, marked a philosophical shift. The holding company structure wasn't about financial engineering—KCP&L had learned from the disasters that befell utilities that strayed too far from their core business. Instead, it was about creating flexibility for an uncertain future. Would electricity markets deregulate? Would new technologies disrupt the traditional utility model? Great Plains Energy gave KCP&L options without requiring immediate commitments.

The 2008 acquisition of Aquila brought the story full circle in a way that would have amazed Lemuel K. Green. His company, started in 1902, had undergone numerous transformations—Green Light & Power to West Missouri Power Company to Utilicorp to Aquila—but had always maintained its focus on serving the smaller communities and rural areas that larger utilities overlooked. By 2008, Aquila was struggling, weakened by failed international ventures and unable to invest adequately in its aging infrastructure.

For Great Plains Energy, Aquila represented both opportunity and risk. The opportunity was clear: Aquila's service territory was adjacent to KCP&L's, creating obvious synergies in operations and management. The combined company would serve nearly one million customers across Missouri and Kansas, achieving the scale necessary to compete in an increasingly consolidated industry.

But the risks were substantial. Aquila's infrastructure needed massive investment—decades of deferred maintenance had left many of its systems operating on borrowed time. Integrating two companies with very different cultures would be challenging; KCP&L's corporate Kansas City sophistication versus Aquila's rural Missouri pragmatism. And the regulatory approvals would be complex, requiring negotiations with both the Missouri Public Service Commission and the Kansas Corporation Commission.

The integration took years and billions of dollars, but by 2010, the combined company had emerged as a regional powerhouse. Great Plains Energy now controlled electricity delivery across western Missouri, serving everyone from urban Kansas City to rural farming communities near the Iowa border. The company's generation fleet was diverse—coal, natural gas, nuclear through its ownership stake in Wolf Creek—providing flexibility in an era of increasing environmental regulation.

Yet even as Great Plains Energy celebrated its regional dominance, executives knew that bigger changes were coming. To the west, Westar Energy had built an equally impressive franchise across Kansas. The logic of combination was becoming undeniable. Transmission planning would be more efficient with a single operator. Generation dispatch could be optimized across a larger fleet. Corporate overhead could be reduced through consolidation.

Moreover, both companies faced the same challenges: aging coal plants that would need to be retired or retrofitted, transmission systems that required upgrading for renewable integration, and a regulatory framework that demanded ever-larger capital investments while constraining rate increases. Neither company alone had the scale to efficiently address these challenges.

The financial markets were also pushing for consolidation. Utility investors, burned by the failed diversification strategies of the 1990s, wanted pure-play regulated utilities with predictable earnings and growing dividends. But they also wanted scale—companies large enough to spread regulatory and operational risks across multiple jurisdictions. Great Plains Energy, with a market capitalization of roughly $6 billion, and Westar, valued at about $9 billion, were subscale compared to national players like NextEra or Dominion.

By 2015, informal discussions between the two companies had begun. The industrial logic was compelling, the financial benefits were clear, and both management teams recognized that consolidation was inevitable. The question was structure: Who would acquire whom? What would the combined company look like? And most critically, how would they convince regulators in two states that consolidation would benefit customers, not just shareholders?

V. The Mega-Merger: Creating Evergy (2016–2018)

The conference room at Westar Energy's Topeka headquarters was tense on that May morning in 2016. Mark Ruelle, Westar's CEO, and Terry Bassham, his counterpart at Great Plains Energy, had spent months negotiating in secret. The deal they were about to announce would create a $30 billion Midwest utility colossus, combining two companies that had competed and coexisted for nearly a century. The initial structure seemed elegant: Great Plains would acquire Westar for $12.2 billion, creating immediate scale while preserving both companies' operational identities.

But elegance in the boardroom doesn't always translate to acceptance in the regulatory hearing room. The Kansas Corporation Commission, the state's powerful utility regulator, had other ideas. When the commission's staff analyzed the deal, they saw something very different from what the CEOs had envisioned: a transaction that would saddle Kansas customers with $4.9 billion in acquisition debt while providing minimal benefits. The promised synergies—$65 million annually—seemed paltry compared to the financial engineering involved.

The opposition was swift and fierce. The Citizens' Utility Ratepayer Board, Kansas's consumer advocacy group, argued that the deal was structured primarily to benefit shareholders at the expense of ratepayers. Industrial customers, including the state's massive agricultural processing facilities, worried about rate increases to pay for acquisition premiums. Even the Kansas Attorney General's office expressed concerns about the transaction's structure and its impact on Kansas consumers.

In April 2017, the Kansas Corporation Commission delivered its verdict: application denied. The commission's 146-page order was a devastating rebuke, finding that the transaction failed to meet the statutory standard of being in the public interest. The commissioners were particularly troubled by the acquisition premium—the amount Great Plains would pay above Westar's book value—and how that premium would ultimately be recovered from customers through rates.

For most companies, such a regulatory rejection would have ended the merger dream. But Ruelle and Bassham, along with their boards and advisors, recognized that the industrial logic remained compelling. Within weeks of the rejection, they were back at the negotiating table, this time with a radically different approach.

The revised deal, announced in July 2017, was a masterclass in regulatory navigation. Instead of an acquisition, it would be a "merger of equals" with no premium paid to either company's shareholders. The companies would combine at market value, eliminating the acquisition debt that had troubled regulators. Management committed to maintaining both companies' headquarters—Topeka and Kansas City—preserving local jobs and community involvement. Most importantly, they guaranteed $50 million in bill credits to Kansas customers and committed to not seeking base rate increases for five years.

The regulatory approval process for the revised merger was a marathon of hearings, testimonies, and negotiations. Both companies' executives spent countless hours in hearing rooms in Topeka and Jefferson City, explaining the benefits of consolidation to skeptical commissioners. They brought in expert witnesses to testify about economies of scale in generation dispatch. They presented detailed models showing how combined transmission planning would reduce costs. They committed to maintaining separate operating utilities—Westar in Kansas, KCP&L in Missouri—to preserve local identity and regulatory oversight.

The Missouri Public Service Commission approved the revised merger in January 2018, finding that the no-premium structure and operational synergies would benefit Missouri customers. But Kansas remained the wildcard. The state's regulators had already rejected one version of this deal; would they accept the revision?

On May 24, 2018, the answer came: yes, with conditions. The Kansas Corporation Commission approved the merger but imposed strict requirements: specific capital investment commitments, maintenance of service quality standards, and regular reporting on synergy achievements. The commissioners made clear that they would be watching closely to ensure that the promised benefits materialized.

The combined company needed a new identity—neither Westar nor Great Plains Energy could survive as the parent company name without creating the impression that one had conquered the other. After extensive market research and branding exercises that reportedly cost millions, they landed on "Evergy"—a portmanteau of "energy" and "every" that was meant to convey both the company's business and its commitment to serving everyone in its territory.

The integration process was complex and occasionally painful. Two companies with proud histories and distinct cultures had to become one. Information systems needed to be integrated—a massive undertaking given that utilities run on complex SCADA systems, customer information platforms, and financial reporting tools. Generation dispatch had to be optimized across the combined fleet, requiring new protocols and procedures. Perhaps most challenging was the human element: determining which executives would lead the combined company, which facilities would be consolidated, and how to maintain employee morale during a period of significant uncertainty.

On October 7, 2019, the final step was taken: the Westar and KCP&L brands were officially retired, replaced by the Evergy brand across the entire service territory. For customers in Kansas and Missouri, the companies that had powered their communities for generations simply vanished, replaced by a corporate entity that many struggled to pronounce correctly (it's "EV-er-gee," not "e-VER-gy").

But behind the branding challenges and integration headaches, the merger was already delivering results. Combined dispatch of generating units was reducing fuel costs. Consolidated purchasing was driving down procurement expenses. The elimination of duplicate corporate functions was saving millions annually. By the end of 2019, Evergy was on track to achieve its promised synergies, validating the industrial logic that had driven the merger from the beginning.

Yet even as management celebrated these operational successes, storm clouds were gathering on the horizon. Wall Street had noticed Evergy, and not everyone liked what they saw.

VI. The Elliott Saga: Wall Street Meets Main Street (2019–2020)

Paul Singer's Elliott Management Corporation is not known for subtlety. When the activist investor announced in January 2020 that it had accumulated an 11.3 million share economic interest in Evergy—worth roughly $760 million—utility executives across America took notice. Elliott didn't invest in utilities to be a passive shareholder. They came to shake things up, and their track record of forcing change at companies from AT&T to eBay preceded them like a corporate calling card written in blood.

Elliott's thesis was brutally simple: Evergy was underperforming, full stop. The merger synergies, while real, were insufficient. The company's planned rate base growth was anemic compared to peers. Most damningly, management's strategy of returning capital through share buybacks rather than investing in infrastructure was, in Elliott's view, a fundamental misallocation of capital that would doom the company to perpetual mediocrity.

The activist's initial presentation, released publicly in January 2020, read like a prosecutor's indictment. Slide after slide hammered home the same message: Evergy's total shareholder return lagged peers, its earnings growth projections were uninspiring, and its infrastructure investment plans were inadequate for a utility operating in states with growing economies and aging systems. Elliott particularly focused on the company's plan to buy back $1 billion in shares through mid-2020, arguing that this financial engineering was a poor substitute for actual value creation through infrastructure investment.

What made Elliott's campaign particularly powerful was its sophistication about regulated utilities—a business model that many Wall Street investors find incomprehensible. Elliott understood that utilities create value through rate base growth: investing in infrastructure that regulators allow them to earn a return on. Every dollar invested in approved projects becomes part of the rate base, earning a regulated return of roughly 9-10% essentially in perpetuity. Share buybacks, by contrast, provide a one-time boost to earnings per share but don't create lasting value.

Behind closed doors, Evergy's board was in crisis mode. The company had just completed a complex merger, employees were still adjusting to the new structure, and now they faced one of Wall Street's most feared agitators. The board's initial instinct was to fight—to argue that Elliott didn't understand the complexities of operating in Kansas and Missouri, didn't appreciate the regulatory constraints, didn't recognize the value of the integration work still underway.

But Elliott had done its homework. They had hired former utility executives as advisors. They had analyzed every rate case filing, every integrated resource plan, every capital allocation decision. They had even floated the idea that Evergy should explore a sale to NextEra Energy, the Florida-based utility giant that had been rolling up utilities across the country. The speculation sent Evergy's stock soaring and put immense pressure on the board to engage.

The negotiations that followed were a delicate dance between Wall Street aggression and Midwest pragmatism. Elliott wanted board seats, strategic changes, and a commitment to dramatically increase infrastructure investment. Evergy's board, led by chairman Terry Bassham, wanted to preserve management's credibility and avoid a fire sale of the company they had just created.

On March 3, 2020, the two sides announced a settlement that was a masterpiece of corporate diplomacy. Elliott would get two board seats for independent directors of its choosing. More significantly, the board would establish a Strategic Review & Operations Committee with a specific mandate to explore ways to enhance shareholder value. The committee would conduct a comprehensive review of all strategic alternatives, including but not limited to a potential sale.

The strategic review process that followed was exhaustive. Investment bankers from Goldman Sachs and Guggenheim Securities were hired to run a formal process. Potential acquirers were contacted—discreetly, of course. NextEra was indeed interested, as were several other large utilities and infrastructure funds. The numbers being discussed were eye-watering: reports suggested bids could value Evergy at $90 per share or higher, a massive premium to its pre-Elliott trading price.

But as the review process unfolded, a different path emerged. David Campbell, who would soon be named CEO to replace the retiring Terry Bassham, presented a standalone plan that was audacious in its ambition. Instead of selling to NextEra, Evergy would transform itself into a NextEra-like growth machine. The company would dramatically increase its capital investment, accelerate its renewable buildout, and target rate base growth that would put it among the industry leaders.

The plan, ultimately branded as the "Sustainability Transformation Plan" or STP, called for investing $9.2 billion over five years, later increased further. This wasn't incremental change—it was a fundamental reimagining of Evergy as a growth company. The share buybacks would end immediately. Every dollar of cash flow would be reinvested in infrastructure. The company would build wind farms, solar installations, transmission lines, and grid modernization projects at a pace that would have seemed impossible just months earlier.

Elliott's response was telling: they endorsed the plan and gradually reduced their stake, declaring victory. They had achieved what they wanted—not through a sale, but through forcing a fundamental strategic shift. Evergy would no longer be a sleepy Midwest utility content with modest growth and financial engineering. It would become an infrastructure investment machine, creating value through building rather than buying back.

The transformation was remarkable to watch. Within months, Evergy was announcing new wind farms, partnering on solar projects, and proposing transmission investments that would have taken years to approve under the old regime. The company's investor presentations transformed from defensive explanations of the merger to aggressive growth projections. Management, initially resistant to Elliott's pressure, had internalized the activist's critique and made it their own.

For the utility industry, the Elliott-Evergy saga became a cautionary tale and a blueprint. It showed that even regulated utilities—long considered immune to activist pressure due to their complex regulatory constraints—could be targeted and transformed. It demonstrated that the old utility playbook of modest growth and high dividends was no longer sufficient in an era of energy transition and infrastructure needs. Most importantly, it proved that sometimes the greatest value creation comes not from financial engineering but from simply investing more capital in productive assets—a lesson as old as capitalism itself, yet one that needed a Wall Street activist to remind a Midwest utility.

VII. Modern Operations & Business Model

Standing in the control room of Evergy's system operations center, you're watching the heartbeat of modern civilization. Massive screens display real-time power flows across 10,100 miles of transmission lines and 52,000 miles of distribution lines—enough wire to wrap around the Earth twice. Every few seconds, automated systems adjust generation at more than 40 power plants with 16,000 megawatts of capacity, balancing supply and demand with millisecond precision across a service territory covering 28,130 square miles.

This is the physical reality of Evergy's business model: an enormous, interconnected machine that must work perfectly every second of every day. When a teenager in Overland Park plugs in their phone charger, when a massive data center in Kansas City fires up another server rack, when a grain elevator in western Kansas starts its conveyors—the grid responds instantly, invisibly, reliably.

The generation portfolio tells the story of America's energy evolution in microcosm. Coal still provides the backbone, with plants like Jeffrey Energy Center near St. Marys, Kansas—one of the largest coal plants in the country—churning out baseload power 24/7. But these giants are gradually giving way to a more diverse mix. Wolf Creek Nuclear Generating Station, that $2.9 billion bet from the 1980s, now looks prescient, providing 1,200 megawatts of carbon-free power with capacity factors above 90%.

Natural gas plants provide the flexibility, ramping up and down to follow demand throughout the day. The Dogwood Energy Facility, completed in 2018, represents the new generation of combined-cycle gas plants: highly efficient, relatively clean, and capable of starting up in minutes rather than hours. Wind farms dot the western portions of the service territory, taking advantage of some of the best wind resources in the nation. Kansas, after all, isn't called the Saudi Arabia of wind for nothing—the same flat topography and absence of natural barriers that made it perfect for agriculture also makes it ideal for wind generation.

The regulatory framework governing this infrastructure is Byzantine in its complexity but elegant in its simplicity of purpose. The Kansas Corporation Commission and Missouri Public Service Commission set the rules, approve the investments, and determine the rates. The basic compact hasn't changed since the 1930s: utilities get a monopoly in exchange for an obligation to serve everyone at regulated rates. But within this framework, the details matter enormously.

Rate cases—the formal proceedings where utilities request permission to increase customer rates—are elaborate theatrical productions involving hundreds of participants and thousands of pages of testimony. Evergy must justify every dollar of investment, every operating expense, every allocation of costs between customer classes. Industrial customers, represented by sophisticated law firms, argue that they're subsidizing residential customers. Residential advocates argue the opposite. Environmental groups push for more renewable investment. Business groups warn about rate competitiveness.

The outcome of these cases determines Evergy's financial destiny. The allowed return on equity—currently ranging from 9.3% to 9.8% depending on the jurisdiction—might seem like a rounding error, but applied to a rate base of more than $20 billion, every basis point represents millions in annual earnings. The treatment of specific investments—whether a new wind farm is deemed "prudent," whether storm restoration costs can be recovered—can swing earnings by tens of millions.

FERC, the Federal Energy Regulatory Commission, adds another layer of complexity. While states regulate retail rates, FERC oversees wholesale power markets and transmission rates. Evergy's transmission investments, governed by FERC formula rates, often provide more attractive returns than state-regulated distribution investments. This creates an incentive to build transmission rather than distribution infrastructure when possible—a subtle but important driver of capital allocation decisions.

The customer mix reveals the economic geography of the heartland. Residential customers—about 87% of customer count but only 35% of revenues—are concentrated in suburban Kansas City and the larger Kansas towns like Topeka, Lawrence, and Manhattan. Commercial customers include everything from strip malls to hospitals to universities. But it's the industrial customers that really move the needle: aerospace manufacturers in Wichita, food processors scattered across Kansas, the massive federal facilities at Fort Riley and Fort Leavenworth.

Each customer class has different needs, different usage patterns, different political influence. A Google data center might use as much electricity as a small city but provides stable, predictable demand. A grain elevator uses massive amounts of power but only during harvest season. A suburban homeowner wants reliability above all else—the lights must turn on, the air conditioning must run, regardless of cost.

This diversity of customers creates both stability and complexity. Unlike utilities in single-industry regions that rise and fall with economic cycles, Evergy benefits from economic diversification. When oil prices crash and Kansas's energy sector suffers, the agricultural sector might boom from lower input costs. When agriculture struggles with drought or low commodity prices, the steady growth of the Kansas City metro provides cushion.

The challenge of balancing reliability, affordability, and the clean energy transition plays out in every investment decision. Customers demand 99.99% reliability—they notice even brief outages in an age of constant connectivity. But achieving that reliability requires massive investment in grid hardening, vegetation management, and redundant systems. Environmental mandates require retiring coal plants and building renewable generation, but renewable resources are intermittent and require backup. Industrial customers demand competitive rates to remain viable, but residential customers vote.

These tensions came to a head in 2023 when Winter Storm Elliott tested the grid like nothing since the 2021 Texas freeze. As temperatures plunged below zero and wind chills reached -30°F, electricity demand spiked to record levels. Natural gas plants struggled as wellheads froze. Wind turbines iced up. Even coal plants faced challenges as frozen coal became difficult to pulverize. Evergy implemented rolling blackouts for the first time in recent memory, affecting hundreds of thousands of customers.

The aftermath was predictable: customer outrage, regulatory investigations, political grandstanding. But it also crystallized the fundamental challenge facing Evergy and utilities everywhere: the old system designed for predictable baseload generation and steady demand is giving way to something new—a system with variable renewable generation, extreme weather events, and explosive demand growth from electrification and digitalization. Managing this transition while maintaining reliability and affordability isn't just a business challenge; it's a societal imperative.

VIII. The Energy Transition Challenge

The announcement came on a crisp September morning in 2021: Evergy would achieve net-zero carbon emissions by 2045, with an interim target of 70% reduction by 2030 compared to 2005 levels. For a company that still generated more than 40% of its electricity from coal, this wasn't just ambitious—it was revolutionary. The roadmap to get there would require retiring billions of dollars in still-functional assets, building an entirely new generation fleet, and somehow doing it all while keeping rates affordable and reliability intact.

The mathematics of stranded assets are brutal. Lawrence Energy Center, La Cygne Generating Station, Jeffrey Energy Center—these coal plants represent billions in historical investment with book values that haven't fully depreciated. In a normal business, you'd run these assets until they died natural deaths. But in the energy transition, they must be euthanized while still productive, creating massive write-offs and regulatory battles over who bears the cost.

Consider Jeffrey Energy Center alone: 2,160 megawatts of capacity that has reliably served Kansas for decades. The plant employs hundreds of workers in St. Marys, pays millions in property taxes, and supports an entire ecosystem of suppliers and contractors. Shutting it down isn't just an accounting entry—it's an economic earthquake for rural communities. Yet keeping it running means missing climate targets and facing increasingly stringent environmental regulations that make operations uneconomic. The retirement dance around Lawrence Energy Center perfectly encapsulates the challenge. Initially announced to retire by the end of 2023, the plant's fate has been revised multiple times. The 2023 integrated resource plan pushed the coal unit retirement to 2028, with plans to convert another unit from coal to natural gas power by 2028. Environmental groups were apoplectic—"It's maddening that Evergy said it would close its Lawrence coal plant two years ago, yet here we are with the utility committing to burn fossil fuels at the plant years beyond the original plan," said Nancy Muma of the Sierra Club.

But Evergy's position reflects a genuine operational dilemma. "Our service area is experiencing some of its most robust electricity demand growth in decades, including very large projects like the Panasonic electric vehicle battery manufacturing factory and the Meta datacenter, as well as broad-based economic development in both Kansas and Missouri," CEO David Campbell explained. You can't simultaneously retire baseload generation and meet explosive demand growth without something to fill the gap.

Kansas, paradoxically, has become both a wind energy superpower and a continuing coal dependency. The state ranks third nationally in wind generation, with massive wind farms taking advantage of the consistent prairie winds. On some days, wind provides more than 60% of the state's electricity. But wind doesn't blow on demand. During the polar vortex of February 2021, when temperatures plunged and wind turbines iced up, those coal plants that environmentalists want retired yesterday were the only thing keeping the lights on.

The financial innovation of securitization offers a partial solution to the stranded asset problem. Kansas Governor Laura Kelly signed a bipartisan "securitization" bill, which allows utilities to issue bonds to ease the risk of shuttering coal plants. The mechanism allows utilities to refinance the remaining debt on coal plants at low interest rates—typically 2-4% instead of the 9% return normally required—reducing the customer impact of early retirements. The Sierra Club estimates that securitizing Jeffrey and La Cygne between 2023 and 2030 could save between $333 and $896 million

. But securitization is only a financial band-aid on a structural wound.

The wind story in Kansas is both triumph and challenge. Evergy serves its customers with a balanced generation portfolio that includes approximately 4,600 MW of renewable energy. Later this year, the company expects to surpass a milestone of generating 150 million megawatt hours of wind energy since the inception of its wind portfolio in the early 2000s. Kansas ranks third nationally in wind generation, and on particularly windy days, more than 60% of the state's electricity comes from wind turbines scattered across the prairie.

But wind's intermittency creates operational headaches that coal never did. Grid operators must maintain spinning reserves—typically natural gas plants idling at partial load—ready to ramp up when the wind dies. Battery storage, the holy grail that would solve intermittency, remains prohibitively expensive at grid scale. The Southwest Power Pool's capacity market increasingly values dispatchable resources over intermittent ones, creating economic headwinds for wind development even as environmental mandates push for more renewables.

The grid modernization imperative adds another layer of complexity. The existing transmission system, built for one-way power flow from large central plants to customers, must be reconfigured for bidirectional flow as rooftop solar proliferates. Smart meters, distribution automation, and advanced grid management systems require billions in investment. These aren't sexy investments that make headlines, but they're essential for maintaining reliability in an increasingly complex energy landscape.

Data center demand represents both salvation and stress test. Last May, Evergy announced data center deals with Google and Meta Platforms, as well as an agreement to deliver power to an electric vehicle battery manufacturing plant for Panasonic. In all, the projects represent more than 750 megawatts of load, Evergy said. This explosive load growth—after years of flat demand—justifies infrastructure investment and provides a growth story that Wall Street loves.

But serving data centers isn't like serving traditional industrial customers. As Friestad reports, the energy demand from these facilities is equivalent to 100 Walmarts or 40 hospitals. They require near-perfect reliability—a millisecond outage can cost millions. They demand massive amounts of power delivered to a single point, stressing distribution infrastructure designed for dispersed loads. And increasingly, they want that power to be renewable, adding complexity to an already challenging resource planning equation.

The natural gas pivot reveals the pragmatic reality behind green ambitions. Companywide over the next 20 years, Evergy projects it will need to add 5,100 megawatts of renewable energy from wind and solar and 6,000 MW of firm, dispatchable generation – including 2,500 MW of new, hydrogen-capable natural gas generation across 2029-2032 – as its service area is experiencing record-setting economic development. Evergy, Inc. (NASDAQ: EVRG) today announced it will invest in two new 705 megawatt (MW) combined-cycle natural gas plants that will be built in Kansas. The plants are expected to begin operating in 2029 and 2030.

The hydrogen-capable designation is particularly telling—a hedge against future carbon regulations while acknowledging that hydrogen infrastructure doesn't yet exist at scale. "The new units would also be capable of converting to hydrogen in the future." It's planning for a future that may never arrive while solving the immediate problem of keeping the lights on.

Environmental advocates are understandably frustrated. Nancy Muma, a volunteer with the Wakarusa Group of the organization, said in a news release it was "maddening" that Evergy delayed retiring the Lawrence plant. "That's not a decision utility leaders make while proclaiming to care about climate change and the cost to its customers," Muma said. But Evergy's position reflects operational reality: you can't retire baseload generation while adding massive new loads without something to fill the gap.

The economics of the transition are brutal. Building renewable generation requires massive upfront capital with uncertain cost recovery. Natural gas plants, while cleaner than coal, still represent fossil infrastructure that may become stranded assets if carbon regulations tighten. Grid modernization investments are necessary but don't generate returns like new generation. And through it all, regulators demand that rates remain affordable while reliability improves and emissions decline—a trinity of objectives that often conflict.

IX. Playbook: Lessons from the Heartland

The Evergy story offers a masterclass in navigating the unique challenges of regulated utility M&A—a world where financial engineering meets political theater, where synergies must benefit ratepayers before shareholders, and where success is measured not in quarters but in decades.

The first lesson is that premium matters more than price in regulated utility M&A. Great Plains Energy's initial attempt to acquire Westar failed not because the price was too high—$12.2 billion was reasonable by market standards—but because the acquisition premium created a political liability. Regulators saw debt that would burden ratepayers for decades. The solution—a no-premium merger of equals—was elegant in its simplicity. By eliminating the premium, the companies removed the primary regulatory objection while preserving the industrial logic of combination.

This leads to the second insight: regulatory approval is the product, not a process step. Most M&A practitioners view regulatory approval as a hurdle to clear. In utility M&A, it's the core value creation event. The months Evergy's executives spent in hearing rooms in Topeka and Jefferson City weren't a distraction from integration planning—they were the main event. Every commitment made, every condition accepted, every rate freeze promised shaped the economic reality of the combined company for years to come.

The Elliott saga revealed a new playbook for activist investors in regulated utilities. Traditional activism—demanding buybacks, pushing for sales, replacing management—doesn't translate directly to utilities. Regulators must approve major transactions. Capital allocation is constrained by regulatory requirements. Even management changes require regulatory comfort. Elliott succeeded not by forcing a sale but by reframing the value creation narrative: from financial engineering to infrastructure investment, from buybacks to rate base growth, from defending the status quo to embracing transformation.

The activist's sophistication about the utility model was crucial. They understood that utilities create value through rate base growth—every dollar of approved investment earns a regulated return essentially in perpetuity. Share buybacks provide a one-time EPS boost but don't create lasting value. By pushing Evergy to dramatically increase capital investment, Elliott aligned the interests of shareholders (who want growth), regulators (who want infrastructure investment), and customers (who benefit from modernized systems).

The balance of stakeholder interests emerges as perhaps the most critical lesson. Utilities serve multiple masters: customers who want low rates and high reliability, regulators who enforce public policy objectives, investors who demand returns, employees who need job security, and communities that depend on tax revenue and economic development. Success requires not choosing among these stakeholders but finding solutions that benefit all—or at least don't explicitly harm any.

Consider how Evergy navigated the energy transition challenge. Simply announcing aggressive carbon reduction goals would please environmentalists but alarm industrial customers worried about reliability and affordability. Refusing to set targets would satisfy traditionalists but invite regulatory pressure and activist campaigns. The solution—ambitious long-term targets with pragmatic near-term actions, including natural gas bridges—satisfies no one completely but gives everyone something.

The infrastructure investment versus financial engineering debate that Elliott forced has broader implications. For decades, utilities could generate acceptable returns through steady operations and modest growth. Financial engineering—buybacks, dividend increases, balance sheet optimization—provided the extra juice to keep investors happy. But that era is ending. The energy transition, grid modernization, and electrification of everything require massive capital investment. Utilities that try to financial engineer their way to growth will lose to those that build their way there.

Regional economic development emerges as an underappreciated competitive advantage. The company's economic development pipeline has grown to approximately 12.2 gigawatts (GW), representing more than its current peak demand of 10.6 GW. This pipeline includes 1.1 GW of projects under active construction, with another 1.3 GW in the final stages of agreement. Notably, the "finalizing agreements" category includes two data center projects – one in Kansas and an expansion of an existing customer in Missouri. Evergy's ability to attract data centers, battery plants, and other large loads isn't just about available land or tax incentives—it's about demonstrating the ability to deliver reliable, affordable power at scale.

This economic development focus requires a different organizational capability than traditional utility operations. It means having teams that can speak the language of site selectors and corporate real estate executives. It means understanding the specific power requirements of different industries—data centers need different reliability levels than manufacturing plants. It means being able to move at corporate speed, not utility speed, when opportunity knocks.

Managing energy transition in politically diverse states presents unique challenges. Kansas and Missouri, like much of America, contain multitudes: urban liberals demanding rapid decarbonization, rural conservatives skeptical of climate mandates, industrial customers needing reliable baseload power, and agricultural communities hosting wind farms. Evergy must navigate this political patchwork without alienating any constituency powerful enough to influence regulators.

The solution is pragmatic incrementalism dressed in revolutionary rhetoric. Announce bold long-term goals that satisfy progressives. Take measured near-term steps that don't alarm conservatives. Emphasize reliability and affordability when talking to industrial customers. Highlight economic benefits when siting renewable projects in rural communities. It's political theater, but it's necessary theater that enables real progress.

The lesson for founders and investors outside the utility sector is that regulated industries operate by different rules but not without rules. The constraints of regulation—the need for approval, the requirement to serve all customers, the obligation to maintain reliability—seem limiting. But within those constraints, there's enormous opportunity for value creation. The key is understanding that in regulated industries, value creation must be shared to be sustainable. Trying to capture all the value for shareholders inevitably triggers regulatory backlash. But creating value that benefits all stakeholders generates a virtuous cycle of investment, growth, and returns.

X. Analysis & Investment Case

The financial performance tells a story of steady improvement masked by transformation costs. Evergy's first quarter 2025 adjusted earnings (non-GAAP) and adjusted earnings per share (non-GAAP) were $125.0 million, or $0.54 per share, compared to $124.7 million, or $0.54 in 2024. The flat year-over-year comparison obscures significant underlying changes: massive capital deployment, accelerating rate base growth, and the early stages of what could be transformative demand growth from data centers and electrification.

The competitive positioning versus peers reveals both opportunity and challenge. Against American Electric Power (AEP), Xcel Energy (XEL), and WEC Energy Group (WEC), Evergy trades at a discount despite comparable fundamentals. The market seems to be penalizing Evergy for its Midwest geography, its ongoing transformation efforts, and perhaps lingering skepticism from the Elliott battle. But this discount may represent opportunity if Evergy can execute its growth plan.

The bull case rests on three pillars, each compelling in isolation and potentially transformative in combination:

First, the infrastructure investment opportunity is massive and largely de-risked. With $17.5 billion in planned capital investment over the next decade, Evergy will nearly double its rate base. This isn't speculative growth—it's replacing aging infrastructure, building renewable generation to meet state mandates, and connecting new customers with signed agreements. The regulatory frameworks in both Kansas and Missouri support cost recovery for prudent investments. Both states have approved Plant-in-Service Accounting (PISA), Construction Work in Progress (CWIP) for natural gas investment, and data center tax incentives.

Second, the data center and electrification boom could drive the kind of load growth utilities haven't seen in decades. The 12.2 GW development pipeline represents more than doubling current peak demand. Even if only half materializes, it would transform Evergy's growth profile. Data centers, EV manufacturing, and industrial reshoring all need massive amounts of reliable power—exactly what Evergy provides.

Third, the regional economy shows surprising dynamism. Kansas City is becoming a logistics hub, leveraging its central location and relatively low costs. The Panasonic battery plant represents the kind of advanced manufacturing that creates ecosystems of suppliers and adjacent development. Agricultural technology and renewable energy development provide additional growth vectors. This isn't the Rust Belt—it's the emerging "Silicon Prairie."

The bear case, however, has sharp teeth:

Regulatory risk looms large. Both Kansas and Missouri have historically been constructive regulatory environments, but that could change. Rate fatigue is real—customers seeing bills increase to fund infrastructure investment may push back through the political process. The next rate case could see regulators disallow costs, reduce authorized returns, or impose conditions that constrain growth.

Energy transition costs could spiral beyond current estimates. The securitization mechanism helps but doesn't eliminate stranded asset risk. If carbon regulations tighten faster than expected, those new natural gas plants could become stranded assets themselves. The cost of renewable integration—backup power, transmission upgrades, grid stability investments—remains uncertain.

Political uncertainty adds another layer of risk. Energy policy has become increasingly partisan. A change in federal administration could dramatically alter the economics of renewable development through tax credit changes. State-level political shifts could affect renewable mandates, carbon goals, and regulatory appointments. Evergy must navigate this political volatility while making investment decisions with 40-year horizons.

Execution risk shouldn't be overlooked. Evergy is attempting to transform from a sleepy utility to a growth machine while integrating two legacy companies, modernizing ancient infrastructure, and navigating an energy transition. The sheer complexity of managing multiple billion-dollar construction projects while maintaining day-to-day reliability is staggering. One major project failure or extended outage could derail the entire growth story.

The dividend story adds complexity to the investment case. Evergy's shares rose nearly 18% in 2024, and the stock has a dividend yield of 4.4%. Utility investors traditionally prize dividend stability and growth above all else. But funding massive capital investment while maintaining dividend growth requires careful balance. Too much dividend growth constrains investment capacity. Too little disappoints income-focused investors. Evergy must thread this needle while competing for capital with utilities offering similar yields but potentially less execution risk.

The valuation framework depends on your time horizon and risk tolerance. For income investors, Evergy offers an attractive yield with reasonable coverage and growth prospects. For growth investors, the rate base expansion story could drive sustained earnings growth. For value investors, the discount to peers might represent opportunity if execution concerns prove overblown.

XI. Epilogue & Future Outlook

The next decade will determine whether Evergy becomes a case study in successful utility transformation or a cautionary tale of infrastructure ambition exceeding operational capability. The pieces are in place for dramatic value creation: a massive capital investment program, explosive demand growth from data centers and electrification, supportive regulatory frameworks, and a management team battle-tested by activist pressure.

The data center boom represents both the greatest opportunity and the greatest uncertainty. If Meta, Google, and others follow through on their announced plans, if AI drives the computing demand explosion many predict, if Kansas City becomes a data center hub leveraging its central location and reliable power—then Evergy could see load growth that transforms its financial profile. But data center development is notoriously fickle. Projects get announced with fanfare then quietly canceled. Technology shifts could reduce power demand or shift it elsewhere. The AI bubble could burst, leaving Evergy with infrastructure built for demand that never materializes.

Grid resilience in an era of extreme weather adds another dimension of challenge and opportunity. Climate change isn't a future risk—it's a present reality that Evergy must manage. More frequent and severe storms, extended heat waves, polar vortexes that stress generation and transmission—these aren't anomalies anymore but the new normal. Building resilient infrastructure that can withstand these extremes requires billions in investment but also creates rate base growth opportunity.

The future of regulated utilities in America is being written in real-time through companies like Evergy. The old model—steady but slow growth, reliable dividends, boring predictability—is dying. The new model emerging involves massive capital deployment, technology integration, and navigating complex energy transitions while maintaining affordability and reliability. Utilities that successfully transform will thrive. Those that don't will become acquisition targets or worse.

The key lessons for founders and investors transcend the utility sector:

First, transformation is possible even in the most regulated, traditional industries—but it requires external pressure to overcome institutional inertia. Elliott's activism forced Evergy to reimagine itself not because management couldn't see the opportunity but because they needed political cover to pursue it.

Second, value creation in infrastructure requires patient capital and stakeholder alignment. The investments Evergy is making today won't fully pay off for years or decades. Success requires convincing investors to accept lower near-term returns for greater long-term value creation.

Third, the energy transition creates massive opportunity for those willing to navigate its complexity. The shift from fossil to renewable, from centralized to distributed, from analog to digital grids represents trillions in global investment opportunity. Companies that can manage this transition—technically, financially, politically—will capture enormous value.

Finally, boring businesses in unsexy locations can generate extraordinary returns. Evergy operates in Kansas and Missouri, not Silicon Valley or Manhattan. It provides electricity, not artificial intelligence or social media. Yet it's positioned to benefit from both the digital revolution (through data center demand) and the energy transition (through renewable development and grid modernization).

As I write this in 2024, Evergy stands at an inflection point. The merger is complete, the activist battle is won, the investment program is underway. The next five years will reveal whether this Midwest utility can transform itself into a growth machine while maintaining the reliability and affordability its customers expect. The stakes couldn't be higher—not just for Evergy's shareholders but for the 1.7 million customers depending on it for the electricity that powers their modern lives.

The story of Evergy is ultimately the story of American infrastructure in the 21st century: aging systems requiring massive investment, new technologies disrupting old models, climate change creating new challenges, and the constant tension between public service and private profit. How Evergy navigates these challenges will provide lessons for utilities and infrastructure investors everywhere.

Keep reading to understand how Evergy provides power to 1.7 million customers across Kansas and Missouri, generating revenue of $5.84 billion in 2024, and how it plans to invest $17.5 billion to deliver clean, safe, reliable sources of energy—because in the end, keeping the lights on isn't just a business model, it's a social compact that defines modern civilization.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube