Evommune: The Dermira Mafia and the New Frontier of Neuro-Inflammation

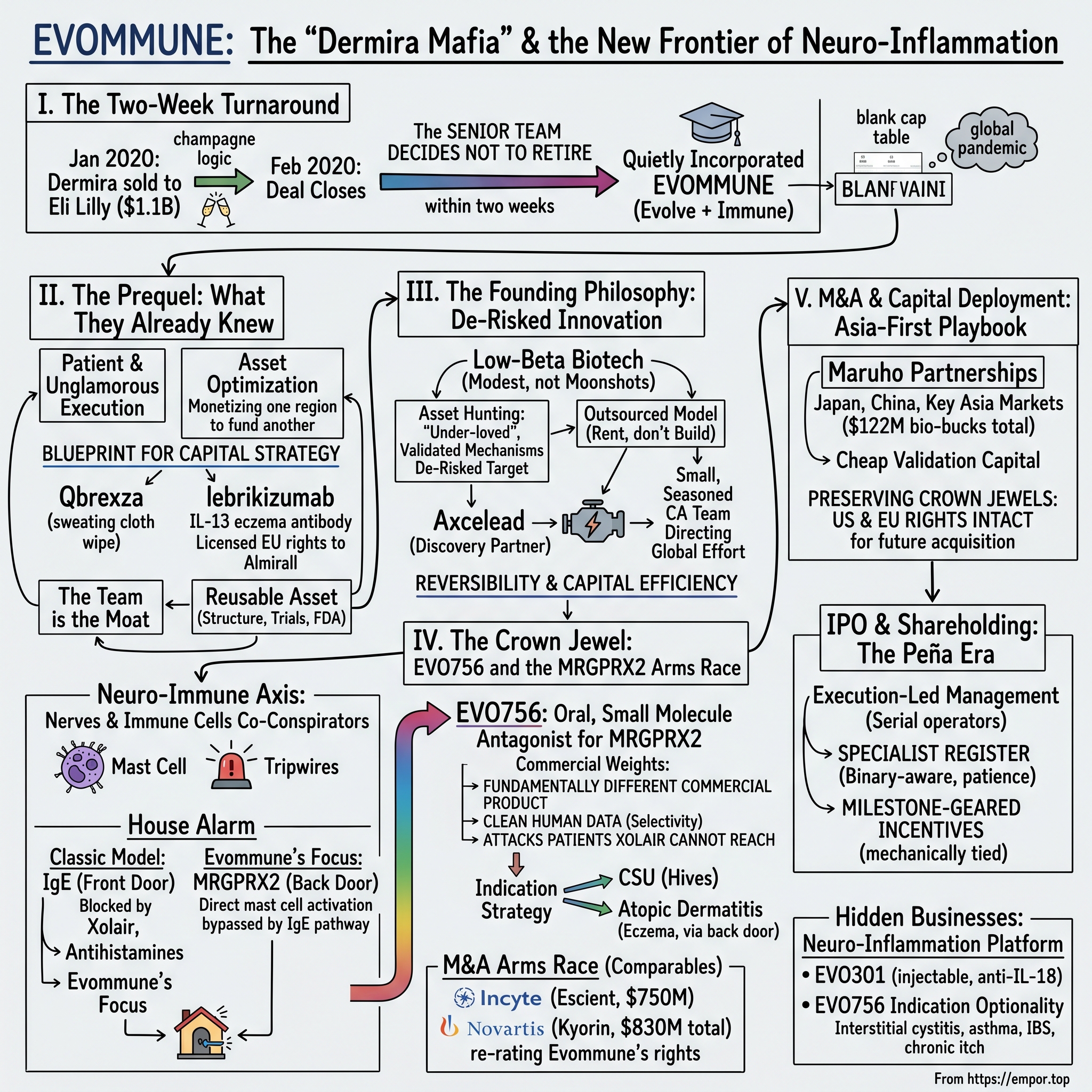

I. The Two-Week Turnaround

Picture the scene in the early weeks of 2020. The conference rooms at Dermira's Menlo Park headquarters were full of champagne logic. Eli Lilly had just agreed to buy the company for $1.1 billion in all cash, tendering $18.75 a share for a business whose crown jewel — an interleukin-13 antibody called lebrikizumab — was being teed up as a direct rival to the biggest blockbuster in dermatology.12 The deal was announced on January 10, 2020, and it closed with unusual speed on February 20.12 For most of the people in those rooms, this was the finish line. You sell to Lilly, your options vest, and you spend the next decade on a boat, on a board seat, or on a beach.

That is not what the senior team did.

Within roughly two weeks of the Lilly transaction closing, a core group of Dermira veterans — led by Luis Peña and the dermatology elder statesman Eugene Bauer — had quietly incorporated a new company. They did not go to Lilly. They did not take the gilded retirement. They started over, from a blank cap table, in the opening weeks of a global pandemic that would shutter labs, freeze clinical trials, and send biotech investors scrambling for cover. The new entity was called Evommune — a portmanteau of "evolve" and "immune" — and its entire premise was that the team had learned something at Dermira that was worth running back, faster and cheaper, on a more interesting biological frontier.

That frontier is the subject of this episode. Evommune is not, at its heart, a story about itchy skin, even though hives and eczema are where its science first shows up in patients. It is a story about the neuro-immune axis — the increasingly inescapable discovery that the nervous system and the immune system are not two separate departments inside the human body but co-conspirators, constantly signaling to each other behind the conscious mind's back. When you scratch at a mosquito bite until it bleeds, when a stress spike triggers a flare of hives, when a drug infusion causes an instant rash before any antibody could possibly have formed — that is the neuro-immune axis talking. Evommune's bet is that an entire generation of inflammatory diseases has been mis-targeted because medicine kept treating the immune cells and ignoring the nerve endings whispering to them.

The bet has, so far, been rewarded by the market. On November 6, 2025, Evommune's shares began trading on the New York Stock Exchange under the ticker EVMN, after the company priced an initial public offering of 9,375,000 shares at $16.00 apiece — a base raise of roughly $150 million that, with the underwriters' over-allotment, lifted gross proceeds toward $172.5 million.1 It was one of the few clinical-stage biotech IPOs to get cleanly out the door in a window when most peers were stuck in registration purgatory. The company arrived on the public market with a single, sharply defined lead asset, a pristine balance sheet, and a reputation that preceded it: in the small, gossipy world of inflammation-and-immunology dealmaking, these people were known as the "Dermira Mafia."

This is the story of how a serial team turned a billion-dollar exit into a second act, why they chose a receptor most of the industry had never heard of five years ago, and what it means that some of the largest pharmaceutical companies on earth are now racing each other to own the same biology. Let's build the rocket.

A word, first, on why this matters to investors and not just to immunologists. Clinical-stage biotech is the most unforgiving asset class in public markets — a category where the median company never earns a dollar of product revenue and where a single trial result can erase, or multiply, the entire enterprise value in an afternoon. The cliché is that biotech investing is a coin-flip dressed up in lab coats. The interesting companies are the ones that quietly bend the odds: that pick targets where the biology is already half-proven, that keep their cash burn low enough to survive a bad year, that retain the rights worth retaining, and that are run by people who have made the walk from molecule to market before and know where the bodies are buried. Evommune was engineered, from incorporation, to be one of those odds-benders. Whether the engineering holds is the question the next two quarters will answer. But the design is worth studying regardless of the outcome, because it is a near-pure expression of a philosophy — capital-efficient, de-risked, team-as-moat drug development — that more and more sophisticated biotech investors have come to prize after a decade of watching cash-incinerating moonshots vaporize.

II. The Prequel: What the Dermira Mafia Already Knew

To understand why a group of executives would walk away from Lilly two weeks after cashing out, you have to understand what they had just lived through — because Evommune is, in a very real sense, Dermira's lessons compounded.

Dermira had been a study in patience and unglamorous execution. Its two commercial-stage achievements could not have been less alike. The first, Qbrexza, was a medicated cloth wipe impregnated with glycopyrronium, approved by the FDA for primary axillary hyperhidrosis — in plain English, a treatment for uncontrollable underarm sweating.12 It is the kind of product that wins no scientific prizes but solves a genuinely miserable problem for real people, and it taught the team how to get a small-molecule dermatology product through regulators and onto pharmacy shelves. The second, lebrikizumab, was the opposite: a high-science monoclonal antibody designed to bind IL-13 with very high affinity and quiet the inflammatory cascade that drives moderate-to-severe atopic dermatitis.12 It was a Phase 3 asset positioned against Dupixent, the Sanofi–Regeneron juggernaut that had redefined eczema treatment and was on its way to becoming one of the best-selling drugs in the world.

Here is the detail that shaped everything that came after. Before Lilly ever bought Dermira, the company had already done something clever with lebrikizumab: in 2019 it had licensed European rights to the Spanish dermatology specialist アルミラール Almirall, S.A., who exercised its option to develop and commercialize the antibody across Europe.17 In other words, the Dermira team had learned, before it was fashionable, how to slice a single asset geographically — to monetize one region to fund another, to partner with a regionally dominant specialist rather than try to build a global commercial army from scratch. That move would become the architectural blueprint for Evommune's entire capital strategy. Hold that thought; we will come back to it when we get to Japan.

Why didn't Peña and Bauer simply ride into Lilly with the asset? Part of the answer is temperament. Eugene Bauer is not a typical biotech operator; he is a physician-scientist of genuine standing — a former dean of the Stanford University School of Medicine and one of the more decorated figures in academic dermatology, who had spent the back half of his career co-founding and shepherding a string of skin-focused companies. For someone like Bauer, the interesting question was never "how do I monetize this antibody one more time" but "what does the next decade of skin-and-immune biology actually look like, and who is going to build it?" Luis Peña, an operator who had helped run Dermira's clinical and corporate machinery, brought the complementary instinct: the conviction that the team itself — the muscle memory of designing trials, talking to the FDA, and structuring deals — was a reusable asset that should not be dissolved into a large-cap org chart.

It is worth lingering on the Almirall structure for a moment, because it is the kind of detail that separates teams that understand value capture from teams that merely understand science. A single drug asset is not one thing to be sold once; it is a bundle of geographic and indication rights that can be unbundled and monetized separately, each piece sold to the partner best positioned to extract value from it. Almirall, a Barcelona-based dermatology house with deep roots in the European prescriber market, could do more with European rights to an eczema antibody than a small California company ever could — so Dermira sold Europe and kept the rest. The cash from that regional deal helped fund the very Phase 3 program that made the whole company attractive to Lilly. That is financial engineering in the best sense: using a partner's regional strength and a partner's checkbook to de-risk and accelerate the rights you keep. The team that designed that structure did not forget how it worked. They simply waited for a better asset on which to run it again.

There is also a structural truth about big-pharma acquisitions that every serial biotech entrepreneur knows in their bones. When Lilly bought Dermira, it bought the molecules and the data; it did not really want the culture. And indeed, just over a year after the acquisition closed, Lilly announced it would shutter Dermira's Menlo Park facility and cut roughly 160 jobs, folding the program into its own immunology infrastructure.13 That is the standard arc — the acquirer keeps the pipeline and discards the team. The Dermira Mafia simply decided to leave before being discarded, taking the one thing Lilly could not buy: themselves.

The final piece was the pivot in scientific worldview. At Dermira, the team had played the conventional immunology game — find the offending cytokine, the IL-13 or its cousins, and build an antibody to neutralize it. That game works, but it is crowded, capital-intensive, and increasingly a contest of who can spend the most on a marginally better antibody. As they scanned for white space, the team's attention drifted toward a stranger and less-traveled idea: that many of the symptoms patients hate most — the itch, the hives, the flush — are not driven purely by the classic immune cascade at all, but by a direct line between nerve-adjacent immune cells and the receptors that fire them. That was the doorway into the neuro-immune axis. And waiting just inside that doorway was a receptor with an unmemorable name and an enormous amount of untapped potential: MRGPRX2.

III. The Founding Philosophy: De-Risked Innovation in a Frozen World

Founding a biotech company in the spring of 2020 was, on paper, an act of poor timing bordering on recklessness. Clinical sites were closing. Patient enrollment was collapsing as hospitals braced for COVID-19. Capital was either fleeing to safety or piling exclusively into vaccines and antivirals. And yet the Evommune team treated the moment not as a deterrent but as a filter — a way of forcing discipline onto a company from day one.

The governing philosophy is best described as "low-beta biotech." Most early-stage drug companies are high-beta machines: they raise enormous sums to discover brand-new biology, then pray that a novel mechanism survives contact with human patients. The failure rate is brutal, and the binary outcomes are why biotech indices swing like seismographs. Evommune's founders had watched that movie too many times. Their alternative thesis was almost contrarian in its modesty: do not try to discover the moon. Instead, identify a moon whose existence is already strongly suggested by published biology, and build a better, cheaper rocket to reach it.

In practice, that meant a particular kind of asset hunting. The team went looking for mechanisms that were scientifically validated — where the underlying biology of a target was increasingly well understood in the literature — but that remained commercially "under-loved," either because the large players had not yet recognized the opportunity, or because earlier attempts had stumbled on execution rather than on the biology itself. Big pharma is full of these orphans: programs shelved in a reorganization, molecules that failed because the delivery was wrong rather than the target, receptors that academia had mapped but industry had not yet monetized. The art Evommune practiced was the art of the polish — taking a rough, undervalued candidate and engineering it into something a regulator and a partner would take seriously.

To do that without building a cathedral-sized internal research organization, Evommune leaned heavily on an outsourced discovery model. Its most important enabler here was the Japanese contract-research powerhouse アクセリード株式会社 Axcelead Drug Discovery Partners, a fully integrated drug-discovery services company spun out of Takeda's research engine, whose medicinal-chemistry and screening capabilities let a lean company run a real discovery pipeline without carrying the fixed cost of hundreds of bench scientists. This is the capital-light heart of the model: rent the rocket factory, don't build it. A handful of seasoned drug developers in California could direct a global research effort, paying for capacity by the project rather than by the payroll, and keep the burn rate low enough that a single asset's data readout — not a constant fundraising treadmill — would determine the company's fate.

It helps to contrast this with how the typical venture-backed biotech is built, because the difference is the whole investment thesis in miniature. The standard model raises a large Series A to stand up an internal research platform — labs, equipment, dozens of PhDs — on the theory that owning the discovery engine creates proprietary value. Sometimes it does. But it also creates a heavy fixed-cost base that must be fed regardless of whether any single program is working, which forces serial dilutive fundraising and ties the company's survival to the mood of the capital markets rather than to the merits of its science. Evommune inverted the logic. By renting discovery capacity from partners like Axcelead and concentrating its own scarce resources on selection, design, and clinical execution, it kept the fixed-cost base low and the variable, project-based spend high — meaning that when a program like EVO101 disappoints, the company can stop spending on it almost immediately rather than carrying the overhead of a lab built around it. Capital-light is not merely cheaper; it is more reversible, and reversibility is enormously valuable in a field where most experiments fail.

There is a subtle elegance to this that long-term investors should appreciate. By selecting de-risked targets and outsourcing the most capital-intensive discovery work, Evommune compressed the two variables that destroy most biotech equity: scientific risk and cash burn. It did not eliminate them — no clinical-stage company can — but it tilted the odds. The team was effectively saying that in a field where most value is destroyed by spending heroic amounts of money to learn that a novel mechanism doesn't work in humans, the smarter game is to spend modest amounts of money to confirm that a probable mechanism does. The whole edifice, though, still rested on choosing the right moon. By 2021 the team had chosen. Its name was EVO756, and the moon it orbited was a mast-cell receptor that, if it behaved as the biology promised, could rewrite the rules of allergic and inflammatory disease.

IV. The Crown Jewel: EVO756 and the MRGPRX2 Arms Race

Let's do the science slowly, because everything about Evommune's valuation, its partnerships, and its competitive position flows from one receptor with an ungainly name: MRGPRX2 — the Mas-related G-protein-coupled receptor X2.

Start with the cell it lives on. Mast cells are the immune system's tripwires. They sit in the skin, the gut, the airways, and the bladder, packed with granules full of histamine and other inflammatory chemicals, waiting to detonate. In the classic allergy story that every biology student learns, mast cells fire when an allergen — pollen, peanut, bee venom — cross-links IgE antibodies bound to their surface. That IgE pathway is the one the entire modern allergy-drug industry was built to interrupt. It is why antihistamines exist, and it is the mechanism that Novartis and Roche's Xolair (omalizumab), an anti-IgE antibody, was designed to block.

To make this concrete with an analogy: think of a mast cell as a house alarm. In the classic allergy model, the alarm is wired to the front door — the IgE antibodies — and it goes off when a known intruder (the allergen) trips that specific sensor. The entire allergy-drug industry is essentially in the business of guarding that front door, either by jamming the sensor (antihistamines, which block the histamine after it's released) or by removing the antibodies that arm it (Xolair, the anti-IgE antibody from ノバルティス Novartis and Roche, which mops up circulating IgE so the front-door sensor has nothing to react to). For a long time, medicine assumed that was the whole house.

Here is the twist that makes MRGPRX2 so interesting. Mast cells have a second ignition switch — a back door that does not require IgE or any prior allergic sensitization at all. MRGPRX2 is that back door. When it is triggered, the mast cell detonates directly, bypassing the entire antibody-mediated pathway that the industry spent decades learning to block. This is the mechanism behind a whole category of reactions that never made sense under the old model: the rash that appears within minutes of an injected drug, certain forms of chronic itch, and — critically — a large fraction of chronic spontaneous urticaria, the medical name for relentless, unexplained hives that erupt for months or years with no identifiable allergen.

Now you can see why this receptor is a strategic earthquake. If a meaningful share of chronic urticaria and related conditions is driven through MRGPRX2 rather than through IgE, then the multi-billion-dollar franchises built on the IgE pathway are, by definition, blind to those patients. You cannot block a back door by guarding the front one. EVO756 is Evommune's key to that back door: an oral, highly potent, highly selective small-molecule antagonist that sits on MRGPRX2 and prevents it from firing.4

Two features of that one-sentence description carry enormous commercial weight. First, "oral." Xolair and the antibody competitors are injectables, with the cost of goods, cold-chain logistics, and patient reluctance that injectables entail. A pill that a dermatologist can simply prescribe is a fundamentally different commercial product — easier to start, easier to stay on, cheaper to make. Second, "small molecule." Antibodies are large, expensive biologics; a well-behaved small molecule is cheap to manufacture and can be dialed for potency and selectivity through classic medicinal chemistry — exactly the kind of work Evommune's outsourced discovery engine was built to do.

The word "selective" in EVO756's description is doing quiet but heavy lifting, and it is worth unpacking for the non-specialist. The MRGPR receptor family has several members, and a small molecule that blocks the intended one while also hitting its cousins can produce off-target effects that show up as side effects in the clinic — the kind of dirty pharmacology that has sunk many an otherwise promising drug. Designing a molecule that locks onto MRGPRX2 alone, potently and cleanly, is a genuine medicinal-chemistry achievement rather than a given, and it is precisely the sort of work that the company's outsourced discovery model was structured to execute and optimize. If EVO756's selectivity and tolerability hold up in larger trials, that clean profile becomes part of the differentiation story against rivals; if it does not, it becomes the bear's first exhibit. Selectivity, in other words, is not a footnote — it is one of the variables on which the entire investment quietly rests.

The competitive question, then, is not whether MRGPRX2 matters — the rest of the industry has now loudly answered that it does — but whether Evommune's particular molecule is differentiated enough to win. Benchmark it against Xolair and you see the counter-positioning: Xolair defends the IgE franchise; EVO756 attacks the patients Xolair structurally cannot reach. Benchmark it against the new wave of MRGPRX2 programs and the contest becomes about selectivity, potency, oral convenience, and — above all — clean human data.

It is worth pausing on what chronic spontaneous urticaria actually is, because the size of the prize depends on it. CSU is not a few days of hives after eating shellfish. It is the eruption of itchy, burning welts, day after day, for six weeks or far longer, with no identifiable trigger — no allergen to avoid, no obvious cause to remove. Patients describe disrupted sleep, disfiguring flares before important events, and a grinding erosion of quality of life that the outside world tends to underestimate because "hives" sounds trivial. The current treatment ladder starts with antihistamines, often at several times the standard dose; when those fail — and for a substantial share of patients they do — the next rung is an injectable biologic such as Xolair. But even after the biologic, a meaningful population still itches, because a chunk of their disease was never running through the IgE pathway the biologic addresses in the first place. That residual, underserved population — patients who have failed the front-door drugs and have nowhere else to go — is exactly the white space an oral MRGPRX2 antagonist is built to fill. It is a market defined not by the absence of treatments but by the persistent failure of the treatments that exist.

On indication strategy, Evommune chose its white whales deliberately. The lead is chronic spontaneous urticaria (CSU), a condition of intense unmet need where patients cycle through antihistamines and biologics and still itch. The second is atopic dermatitis — the same eczema battlefield the team knew intimately from Dermira, but approached this time through the neuro-immune back door rather than the IL-13 front door. The company put both into the clinic: a global Phase 2b trial of EVO756 in moderate-to-severe CSU, and a separate Phase 2b in moderate-to-severe atopic dermatitis that it began enrolling in 2025.14 As of mid-2026 those readouts are the whole ballgame — top-line CSU data is expected in the second quarter of 2026 and the atopic-dermatitis read in the second half.16 We are, in other words, sitting almost exactly on top of the company's defining catalyst as this is being written.

That timing is not lost on the giants. And the reason the Dermira Mafia found itself in a sudden arms race is that, while they were quietly polishing their molecule, some of the largest companies in pharma decided that the MRGPRX2 back door was worth hundreds of millions of dollars to own. To understand how good — or how early — Evommune's own dealmaking was, we have to put it next to theirs.

V. M&A and Capital Deployment: The Asia-First Playbook

In September 2023, long before MRGPRX2 was a fashionable acronym on biotech Twitter, Evommune did something that looked, to outside observers, almost too modest. It signed away the Japanese rights to its crown-jewel asset.

The partner was マルホ株式会社 Maruho Co., Ltd., a privately held Osaka company that is, within Japan, the dominant specialist in dermatology — the kind of regionally entrenched player that owns the relationships with Japanese dermatologists the way few global firms ever could. Under the September 2023 agreement, Evommune granted Maruho rights to develop and commercialize EVO756 in Japan, in exchange for an upfront payment plus milestones that could total up to roughly $60 million, along with royalties on future Japanese sales.3 Eighteen months later, in March 2024, the two companies expanded the relationship: Maruho took on Greater China and a basket of other key Asian markets, a deal worth up to roughly $62 million in upfront and milestone payments.4 Stack the two together and you get the figure that defined Evommune's early capital story — about $122 million of potential "bio-bucks" across Asia, anchored by a relatively small upfront cash component.

To an untrained eye, taking single-digit-millions upfront for the Asia rights to your only real asset looks like selling the family silver. To understand why it was shrewd rather than desperate, you have to do exactly what the team would do: benchmark the price against what the same biology fetched elsewhere, and then ask what was actually being sold.

Start with the comparables, because they are striking. In April 2024, Incyte agreed to acquire Escient Pharmaceuticals — a company whose lead asset was an oral MRGPRX2 antagonist aimed at the very same urticaria market — for $750 million in cash, plus Escient's remaining net cash.5 The deal closed the following month.6 Less than a year later, in March 2025, 杏林製薬 Kyorin Pharmaceutical struck a global license with Novartis for its own preclinical MRGPRX2 antagonist, KRP-M223: $55 million upfront and up to $777.5 million in milestones, plus tiered royalties, with Kyorin keeping the Japanese commercial rights.8 Put plainly, between 2024 and 2025 two of the largest immunology players on earth paid three-quarters of a billion dollars apiece to get into precisely the receptor Evommune had been quietly working since 2021.

So did Evommune sell too early and too cheap? Here is the counter-intuitive answer, and it is a textbook 7 Powers move. Evommune did not sell EVO756. It sold a few geographies — Japan, then Greater China and parts of Asia — while keeping the two prizes that matter most for valuation: the United States and Europe. The Asian deals were never about maximizing headline value; they were about doing three things at once. First, they brought in non-dilutive cash from a partner who would also help fund and run development in its own territories — Maruho's regional trials and regulatory work effectively subsidize the global data package. Second, they validated the asset: when the leading dermatology specialist in Japan writes you a check for your molecule, that is third-party due diligence the market can see. Third, and most importantly, they preserved the crown jewels — US and EU rights — completely intact for the moment that mattered, which turned out to be the IPO and, potentially, a future acquisition.

This is the Dermira lesson, run back. Recall that the original team had carved Europe off lebrikizumab to Almirall while keeping the value-defining rights elsewhere. Evommune did the same thing in reverse geography — carve Asia to a regional champion, keep the West — and for the same reason: in a single-asset company, the geographic rights you retain are your entire equity story, and you protect them at almost any cost. When Incyte paid $750 million for Escient and Novartis committed up to $830 million in total to Kyorin's program, every one of those transactions re-rated the implied value of the US and EU rights that Evommune still held in full. The "low" upfront Evommune accepted from Maruho looks far less like a fire sale and far more like cheap validation capital purchased against rights that competitors' deals were busy making more valuable by the month.

Why Maruho specifically, and not one of the global giants who could have written a far larger check? Because the choice of partner is itself part of the strategy. A global pharma licensing Asia would have wanted more — likely the whole world, or at least an option on it — and would have used its leverage to claw toward the Western rights that are Evommune's entire equity thesis. Maruho, by contrast, is structurally content with its lane: it is the premier dermatology specialist in Japan, with the prescriber relationships and commercial infrastructure to maximize a skin drug in its home region and adjacent Asian markets, and no particular ambition to compete for the US or Europe. That is the ideal counterparty for a company guarding its crown jewels — a partner whose strengths are exactly where you don't want to operate yourself, and whose appetite stops exactly where your value begins. The deal is a study in matching the right rights to the right owner, the same instinct that drove the Almirall carve-out a corporate generation earlier.

There is a second-order benefit that is easy to miss. Because Maruho is running and funding development in its own territories, Evommune gets additional human data and regulatory experience on EVO756 generated partly on someone else's dime. In a single-asset company, every extra patient dosed and every extra safety datapoint — wherever in the world it is generated — incrementally de-risks the program for everyone, including the holders of the US and EU rights. The Asian partnership is therefore not just a financing event but a clinical-acceleration event, and that dual purpose is the sophisticated reading of why the team did it early rather than waiting for a richer headline number.

On the cash side, the model worked as designed. Rather than the serial mega-rounds that bloat most clinical-stage cap tables, Evommune ran a disciplined private financing arc that culminated on October 31, 2024, when it closed a $115 million Series C led by the crossover specialists RA Capital Management and Sectoral Asset Management, with a deep syndicate of healthcare funds — B Capital, Marshall Wace, RTW Investments, ADAR1, Longwood Fund, Beiersdorf Venture Capital and others — joining in.9 That round was explicitly structured to carry the company through the Phase 2 readouts and into the public markets, which is exactly what happened thirteen months later. The presence of pure crossover investors in the Series C was itself a tell: those are the funds that buy private rounds specifically to pre-position for an IPO, and their participation signaled that the bankers already saw a path to the NYSE. The capital efficiency is the whole point — combine the non-dilutive Asian partnership cash with a single tight crossover round, and you reach the public market having given away far less of the company than the typical clinical-stage biotech does to get to the same place.

The IPO itself was the capstone of this efficiency story. Coming to the NYSE in November 2025 with roughly $150 million of fresh primary capital, plus the over-allotment, gave the company the balance sheet to fund its pivotal readouts and the operational runway beyond them without an immediate return to the well.1 In the depressed biotech IPO market of 2025, simply getting a clinical-stage offering priced and out the door was a feat — many comparable companies were stuck unable to launch, and the ones that did often had to cut size or price. That Evommune cleared the bar is partly a function of the asset and the team, and partly a function of the crossover investors who had pre-committed in the Series C and effectively underwrote demand for the public deal. The use of proceeds is the unglamorous but essential part: this is money raised to reach data, not to fund a decade of open-ended discovery, which keeps the company's fate tethered to events rather than to perpetual fundraising.

Which raises the obvious question for any investor: who exactly owns this company, and are their incentives pointed in the right direction?

VI. Management and Shareholding: The Peña Era

There is a quiet tell in how Evommune presents itself, and it shows up in the org chart. This is not an academic-founder company where a celebrated scientist is the face and a rotating cast of hired executives runs the business. It is the inverse: an execution-led company where seasoned operators sit in the chairs that matter, and the science is treated as a problem to be managed rather than a personality to be worshiped.

At the center is Luis Peña, the chief executive, whose entire professional identity is bound up with having done this before. Peña is not a bench scientist; he is a builder of drug-development organizations, and his pitch — implicit in everything Evommune does — is that the scarce resource in biotech is not molecules but the pattern-recognition that lets a small team move a candidate through the FDA without the expensive detours that sink first-timers. Where a typical founder-CEO is learning the regulatory playbook for the first time on the market's dime, Peña and his colleagues are running a sequel. That is the single most important qualitative fact about Evommune, and we will return to it when we get to the analysis: in this company, the team genuinely is the asset.

Alongside him sits the gravitas of Eugene Bauer, whose career — Stanford medical school dean turned serial dermatology entrepreneur — gives the company something money cannot buy in a field where regulators and key opinion leaders all know each other: credibility on first contact. When a company led by these names calls the FDA, or calls Maruho, or calls a crossover fund, the conversation starts several rungs up the ladder of trust. In a business built substantially on relationships and reputation, that head start is a real, if unquantifiable, asset.

On the question of skin in the game, the public disclosures sketch a picture of meaningful but not controlling founder ownership. According to the IPO prospectus, Peña's direct holding sat at a low-single-digit percentage of the company — on the order of well under two percent, roughly 637,000 shares on a direct basis — with a much larger layer of upside delivered through options and equity awards rather than through legacy founder stock.2 For a long-term investor, the structure matters more than the headline percentage. A management team whose wealth is concentrated in options that vest against clinical and regulatory milestones is one whose payday is mechanically tied to the same events shareholders care about: positive Phase 2b data, partnership milestones, and the regulatory progress of EVO756. The incentive is to drive the asset forward, not to harvest a salary. As a newly public company, Evommune's insiders will also conduct any share sales through pre-arranged Rule 10b5-1 trading plans — the standard mechanism that lets executives diversify on a fixed schedule without trading on inside knowledge, and a signal the market reads closely for what it implies about insider conviction.

Behind management sits the ownership structure that funded the journey. The crossover-heavy Series C syndicate — RA Capital and Sectoral chief among them — now anchors a register populated by dedicated healthcare specialists rather than generalist tourists, and earlier venture backers including Andera Partners and EQT Life Sciences shaped the company's governance through its private years.9 The earlier venture backers matter beyond their capital, because in biotech the lead investors typically shape the board and, through it, the discipline of the company. Andera Partners is a long-established European life-sciences investor, and EQT Life Sciences traces to one of the deepest benches of dedicated healthcare venture capital on the continent; the involvement of investors of that pedigree in the formative rounds tends to bring not just money but governance — the insistence on tight trial design, clean data, and the kind of milestone-driven discipline that the company's whole identity now reflects. As the crossover funds entered later and the public float arrived, the register evolved from a private-venture board into a public-company shareholder base, but the through-line is consistent: at every stage, the money has come from specialists who understand exactly what they are underwriting.

This is a register built deliberately for a clinical-stage life-sciences company: investors who understand binary data readouts, who have the capital to follow on through dilution, and who are not going to panic-sell on a single ambiguous press release. For a company whose entire near-term value hinges on a small number of trial outcomes, the patience and sophistication of the shareholder base is itself a form of risk management.

A word of second-layer diligence is warranted here, because no clinical-stage biotech is without overhangs and an honest account should name them. The most material is the obvious one: as a pre-revenue company, Evommune lives entirely on its cash balance and its ability to raise more, and like every business of its kind it carries the standing risk that disappointing data could close the capital window precisely when it needs it most. Investors should watch the disclosed cash runway in each quarterly filing the way they would watch a fuel gauge — the relevant question is always whether the balance sheet comfortably funds the company past its next value-defining catalyst, and management's own go-forward commentary in the FY2025 results pointed to a series of clinical inflection points concentrated in 2026 as the events that will define the year.16 A second, subtler overhang is concentration risk of a different kind: the dependence on a small leadership group whose collective experience is, as we will argue, the company's principal moat. The flip side of "the team is the asset" is that the departure or loss of key members would damage the asset in a way that is hard to insure against. Neither of these is unusual for the category, but both belong on a clear-eyed ledger.

The cultural through-line connecting all of this — the operator-led management, the milestone-geared incentives, the specialist register — is a deliberate move away from the romantic, science-first model of biotech toward something closer to a commercial engine that happens to be pre-revenue. Evommune behaves less like a research institute hoping to get lucky and more like a focused product company executing a known plan. That discipline is most visible not in the lead asset everyone talks about, but in how the company has managed the rest of its pipeline — including the parts it chose to kill.

VII. Hidden Businesses: The Neuro-Inflammation Platform

Every biotech wants to tell you it has a "platform" rather than a "product," because platforms get higher multiples. Most are exaggerating. Evommune's claim to platform status is more credible than most, but it comes with a candid history that the company, to its credit, has not airbrushed — and the most instructive part of that history is a program it abandoned.

Begin with the failure, because it is where the discipline shows. One of Evommune's early candidates, EVO101, was a topical small-molecule inhibitor of IRAK4 — a kinase deep in the inflammatory signaling chain — developed as a cream for atopic dermatitis.11 On paper it fit the de-risked thesis perfectly: a validated target, a topical delivery route, a known indication. The company took it into the clinic, ran it through a Phase 2 study in eczema, looked hard at the data, and then did the thing that distinguishes operators from believers — it killed the program, discontinuing EVO101 after the dermatitis results did not justify the spend, and redeployed resources toward its systemically administered candidates.10 In an industry where teams routinely throw good money after bad to avoid admitting a thesis was wrong, the willingness to walk away quickly is a feature, not a bug. It is the same instinct that made the team leave Lilly: a refusal to be sentimental about sunk cost.

That clears the stage for the genuine second act of the pipeline, EVO301 — and here the outline's instinct that there is a "hidden" asset is correct, even if the biology is different from the conventional telling. EVO301 is not another skin cream; it is a long-acting injectable fusion protein designed to neutralize interleukin-18 (IL-18), a driver of inflammation that runs through a different lane than the crowded IL-13 highway where Dupixent and lebrikizumab fight. Evommune reported positive top-line data from a Phase 2a proof-of-concept trial of EVO301 in moderate-to-severe atopic dermatitis, giving the company a second clinical-stage shot on goal in the same disease, through a mechanism the giants are not saturating.15 For a single-asset story, the presence of a differentiated, de-risked second program materially changes the risk profile — it means a disappointing EVO756 readout would bruise the company but not necessarily end it.

But the real "pipeline-in-a-product" optionality lives inside EVO756 itself, and it flows directly from the neuro-immune thesis we opened with. Because MRGPRX2 sits at the junction of nerves and mast cells, blocking it is not inherently a skin intervention — it is a way of turning down a misfiring alarm wherever that alarm rings. Mast cells loaded with MRGPRX2 sit in the bladder wall, the gut lining, and the airways. So Evommune has publicly flagged that it continues to evaluate EVO756 in additional indications well beyond dermatology — including interstitial cystitis (a debilitating, poorly treated bladder-pain condition), asthma, irritable bowel syndrome, and chronic itch.16 Each of these is a separate, large market reachable not by inventing a new molecule but by running the same oral pill into a new disease. That is the genuine platform logic: one validated mechanism, many doors. Treat the nerve-adjacent receptor, not just the skin cell, and a urticaria drug becomes a potential franchise.

Sustaining that breadth without ballooning costs is where the outsourced research model earns its keep again. The continuing relationship with Axcelead and similar partners is what lets a company of Evommune's modest headcount keep a genuine discovery and indication-expansion engine running in the background — generating the next candidates and the next disease hypotheses — without the fixed overhead of a sprawling internal laboratory. The pipeline is real, but it is rented at the edges and owned at the core, which is exactly the capital posture a low-beta biotech should want. The question for investors is whether that posture, combined with the team and the receptor, adds up to something genuinely defensible — or merely something that worked until the giants showed up.

VIII. Myth vs Reality, and the Strategy Frameworks

Before war-gaming the competitive position, it is worth puncturing three consensus narratives that tend to cling to a story like this one, because each contains a half-truth that can mislead.

The first myth is that Evommune sold its best asset too cheaply to Japan. The reality, as we have seen, is the opposite of a fire sale: the company sold geography, not the asset, retained the two most valuable territories in full, and used a regional champion's cash and clinical effort to validate and partly fund a program whose Western rights were simultaneously being re-rated upward by competitors' billion-dollar deals. "Cheap upfront" and "bad deal" are not the same thing when the upfront is buying validation against rights you keep.

The second myth is that MRGPRX2 is proven, so EVO756 is a safe bet. The reality is that the receptor's biological relevance is increasingly accepted, but its clinical translation — whether blocking it produces large, durable, well-tolerated benefit in a real patient population — is precisely what remains unproven, and the early stumble of Incyte's Escient program is the standing reminder that target validation and drug success are different things.7 De-risked is not the same as risk-free; it means the dice are loaded, not that the game is over.

The third myth is that this is just another dermatology company. The reality is that dermatology is merely the entry point. The underlying bet is on the neuro-immune axis as a platform, with skin diseases as the first, most clinically tractable proving ground and bladder, gut, and airway conditions as the latent optionality. Mistaking the entry point for the thesis is how investors under-price the upside — or, in the bear scenario, over-price an unproven leap.

With the narratives cleaned up, run the strategy frameworks.

Strip away the biology and Evommune is a strategy case study in whether a small, fast company can build durable advantage in a market where the other players have balance sheets a thousand times larger. Let's war-game it through two frameworks.

Begin with Hamilton Helmer's 7 Powers, because two of them apply unusually well here. The first is Cornered Resource, and in Evommune's case the cornered resource is the team. This sounds soft until you remember how biotech actually works: the binding constraint on moving a drug from molecule to market is not capital — capital is abundant for good assets — but the scarce, experiential knowledge of how to design the right trial, read the regulatory tea leaves, and structure the right partnership. The Dermira Mafia has done the full cycle, including a successful $1.1 billion exit, and that pattern-matching is genuinely hard to replicate. You can hire scientists; you cannot easily hire a team that has collectively walked an inflammation asset from bench to Big-Pharma checkout. For as long as that team stays together and keeps making good calls, it functions as a cornered resource that competitors cannot simply outspend.

The second and sharper power is Counter-Positioning. This is the power that incumbents structurally cannot copy without harming their existing business, and Evommune has it in a near-textbook form. The giants of allergy and urticaria built multi-billion-dollar franchises on the IgE pathway — Xolair being the archetype. Evommune is attacking the non-IgE, MRGPRX2 back door: precisely the patients those franchises cannot reach. An incumbent cannot fully embrace MRGPRX2 without implicitly conceding that its flagship IgE mechanism leaves a large population untreated, and without potentially cannibalizing its own injectable biologic with a cheaper oral pill. That tension is real, and it is why the incumbents' instinct has been to buy MRGPRX2 programs rather than build them — which is itself the clearest evidence that the counter-position is valuable.

A third, more tentative power is Process Power — the proprietary medicinal-chemistry and screening know-how required to engineer a small molecule that is potent and selective for a notoriously tricky G-protein-coupled receptor, and that behaves well as an oral drug. This is the least certain of Evommune's powers, because process advantages in chemistry can be eroded by competitors' own programs, but it is a plausible contributor to differentiation if EVO756's selectivity profile proves superior in human data.

Now run Porter's Five Forces, and the picture turns more sober. Intensity of rivalry is the dominant force and it is high and rising: Incyte (via Escient), Novartis (via Kyorin), and others are now all chasing MRGPRX2, alongside the legacy IgE and IL-13 franchises that still own the bulk of these markets today. Evommune's edge in that fight is not scale — it has none relative to these players — but agility and focus: it is a pure-play, undistracted by a marketed portfolio it must defend, able to move faster precisely because it has less to protect.

The bargaining power of buyers is the second force that should keep investors honest. The ultimate buyers in this market are not patients but payers — the large insurers and pharmacy-benefit managers, the UnitedHealths and their peers — who have enormous leverage to negotiate price and restrict access, especially for a new entrant in a category that already has cheap generic antihistamines at the bottom and established biologics at the top. That power is real, but it is partially blunted by the depth of unmet need in chronic urticaria: when existing options fail a large share of patients, payers face genuine pressure to cover something that works, particularly an oral that may carry a lower cost of goods than the injectable biologics it competes with.

The remaining forces are more favorable. The threat of new entrants at the discovery stage is high in the abstract — biotech has low barriers to starting — but the threat of new entrants reaching the market quickly is low, because the regulatory and clinical timelines are measured in years and Evommune has a multi-year head start. The bargaining power of suppliers is modest; the outsourced-research model means Evommune depends on partners like Axcelead, but contract-research capacity is broadly available. And the threat of substitutes is the existing standard of care itself — antihistamines and biologics — which is exactly the gap EVO756 is designed to fill rather than a force that displaces it.

Net it out and you get a company with genuine, if narrow, structural advantages — a cornered-resource team and a counter-positioned mechanism — operating in a market whose rivalry and buyer power are intensifying by the quarter. Whether those advantages convert into durable value depends almost entirely on data that does not yet exist as of this writing. Which brings us to the trade itself.

IX. The Bear Case and the Bull Case

Every single-asset, clinical-stage biotech is ultimately a wager on a small number of future events, and Evommune is no exception. Let's steelman both sides.

The bear case has a name in the industry: the MRGPRX2 graveyard. Targeting this receptor is biologically seductive but clinically unproven at scale, and the early read on the field is not uniformly encouraging. The cautionary tale is Incyte's own $750 million bet on Escient, which the market has watched stumble as its MRGPRX2 skin-disease program ran into disappointing data — a reminder that owning the right receptor is not the same as having the right molecule or the right clinical result.7 For Evommune, the bear case is concentrated and unforgiving: this is substantially a one-asset company whose value is dominated by EVO756, and the Phase 2b readouts in CSU and atopic dermatitis are binary, near-term, and decisive. If those trials fail to show clear, differentiated efficacy — efficacy convincing enough to separate EVO756 from both the incumbents and the other MRGPRX2 contenders — there is no large marketed business to cushion the fall. EVO301's IL-18 program and the indication-expansion optionality provide some ballast, but they are earlier and smaller, and a market that re-rated the stock up on EVO756's promise would re-rate it down just as fast on EVO756's failure. Add the intensifying rivalry and payer power from the prior section, and the downside scenario is a stock that loses the bulk of its value on a single press release.

It is worth being precise about the competitive geometry the bear case implies, because "rivalry is high" is too lazy a summary. There are really three distinct threats, and they operate on different timelines. The near-term threat is the other MRGPRX2 programs — the Incyte/Escient asset, the Novartis/Kyorin candidate, and any others advancing in parallel — which compete for the same patients, the same prescriber mindshare, and ultimately the same strategic acquirers; if a rival posts cleaner data first, Evommune's differentiation narrative weakens even if its own drug works. The medium-term threat is the incumbent IgE and IL-13 franchises themselves, which are entrenched, reimbursed, and physician-familiar, and which set the efficacy and safety bar EVO756 must clear to justify a switch. The long-term threat is the next mechanism entirely — the perennial biotech risk that a newer modality leapfrogs the whole MRGPRX2 thesis before it fully commercializes. A bear does not need all three to bite; any one of them, arriving at the wrong moment, could compress the opportunity.

The bull case is the mirror image, and it is genuinely large. If EVO756 produces clean, differentiated Phase 2b data — an oral pill that meaningfully clears hives or eczema in patients the existing biologics miss — then Evommune is transformed from a hopeful into a strategic must-have. The logic is not primarily about Evommune's own future revenue; it is about what the asset is worth to the incumbents as a defensive acquisition. A validated oral MRGPRX2 antagonist with US and EU rights intact would be exactly the weapon a Sanofi, a Lilly, or a Novartis would want either to extend an immunology franchise or to keep out of a rival's hands. The comparable transactions frame the math: the industry has already shown it will pay roughly three-quarters of a billion dollars for preclinical-to-early MRGPRX2 assets and entire small companies.58 A company with de-risked Phase 2b data and the two most valuable geographies still in hand would plausibly command a multiple of those figures — the kind of multi-billion-dollar outcome that turns a disciplined, capital-efficient cap table into an outsized return for the patient holders who bought before the data.

The acquirer logic deserves a beat of its own, because it is what makes the bull case structurally different from a simple "the drug sells well" story. In immunology, the largest players do not only buy assets they expect to grow; they buy assets they cannot afford to let a competitor own. A validated oral MRGPRX2 antagonist is exactly such an asset: for a company with a marketed IgE or IL-13 franchise, an oral pill that reaches the patients those biologics miss is simultaneously a growth opportunity and a threat — better to own it than to watch a rival use it to chip away at your installed base. That dynamic creates the conditions for a competitive auction rather than a single negotiated price, and auctions are where the asymmetric outcomes live. Layer on the fact that Evommune kept US and EU rights intact precisely so that a single acquirer could obtain global control of the two markets that matter in one transaction, and you can see how deliberately the company has positioned itself as an acquisition target that is clean, focused, and easy to underwrite. The whole structure — single defined asset, crown-jewel geographies retained, lean cap table — reads like it was designed by people who have sat on the other side of the table and know exactly what makes a small biotech irresistible to a large one.

There is also the oral-versus-injectable economics that sharpen the prize. A small-molecule pill carries dramatically lower cost of goods than a manufactured antibody, needs no cold chain, and lowers the friction of both starting and staying on therapy — patients reliably prefer a tablet to a recurring injection, and adherence is itself a commercial moat. For an acquirer modeling peak sales, an oral that can be prescribed broadly by dermatologists and allergists, rather than administered as a specialty biologic, addresses a structurally larger and stickier market. That convenience premium is part of why a differentiated oral MRGPRX2 antagonist could be worth more, per unit of efficacy, than the injectable incumbents it competes against.

So how should a long-term investor actually monitor which world is unfolding, without pretending to predict the binary outcome? Three KPIs matter above all others, and they are worth watching in order.

First and overwhelmingly: the EVO756 Phase 2b readouts — the CSU top-line expected in the second quarter of 2026 and the atopic-dermatitis read in the second half.16 These are the events that determine essentially everything. Nothing else on this list comes close in importance, and as of this writing the first of them is imminent.

Second: clinical-trial enrollment and execution pace. Before the data lands, the most informative operational signal is how quickly and cleanly the company enrolls and runs its trials. In a competitive race where multiple players are chasing the same receptor and the same patients, enrollment speed is both a sign of clinical-site enthusiasm and a determinant of who gets to market first. Slippage in timelines is the canary; on-schedule execution is quiet confirmation that the machine is working.

Third: Maruho milestone payments and partnership progress. The Asian deals are not just past cash; they are a live scoreboard. Each milestone Maruho pays as EVO756 advances in Japan and Greater China is non-dilutive capital and an external validation event — a sophisticated regional partner voting, with money, that the asset is progressing. Watching whether and when those milestones trigger gives investors a read on the program's health that is independent of Evommune's own commentary.

Track those three, in that order, and you will know most of what can be known about this company between data readouts. Everything else is noise.

X. Epilogue: The Playbook of the Second Act

Step back from the receptors and the milestones, and the most durable lesson of the Evommune story is about a particular species of company that recurs throughout business history: the founder-led second act.

There is a pattern, visible across industries, in which a team builds something, sells it, and then — instead of dispersing — runs the play again with the scar tissue and the relationships and the pattern-recognition of the first attempt intact. The second company is almost always sharper than the first. It raises less and wastes less, because the team already knows which expensive mistakes to skip. It moves faster through the parts that bog down first-timers, because it has walked those corridors before. And it tends to be more disciplined about killing what isn't working, because the founders have already had the experience of a clean exit and are not psychologically trapped by the fear of admitting a single program was wrong. Evommune is, in this reading, the Dermira team's compounding interest — the same people, the same instincts, applied to a richer vein of biology with a leaner machine.

The pattern is not unique to biotech, but biotech may be where it pays off most reliably, and the reason is specific to the industry's structure. In most businesses, a second-time founding team's advantage is relationships and confidence. In drug development, the advantage is something more concrete: a working knowledge of the single most expensive and opaque counterparty in the entire process — the regulator — and of the unwritten grammar of how trials get designed, how endpoints get negotiated, and how a data package gets assembled into something a large acquirer's diligence team will bless. That knowledge is acquired almost entirely by doing it, and doing it once successfully compresses the learning curve for the next attempt enormously. It is why the same names recur as founders across multiple successful companies in oncology, in immunology, in rare disease — the experience compounds in a way that capital alone cannot buy. Evommune is a clean instance of the phenomenon: a team running its second lap on a track it has already finished once.

What makes the vein richer is the larger scientific bet underneath it all, the one we started with and have circled back to throughout: that the next great frontier in inflammatory medicine lies not inside the immune system or the nervous system separately, but in the conversation between them. For most of modern pharmacology, neurology and immunology were different buildings with different journals and different drug classes. The neuro-immune axis collapses that wall. MRGPRX2 is one early, commercially tractable doorway into it — a receptor where a nerve-adjacent immune cell can be switched off by an oral pill — but if the thesis is right, it is the first of many. Itch, pain, urticaria, bladder syndromes, gut disorders: a whole catalog of human misery may turn out to be, at root, a miscommunication between nerves and immune cells that we are only now learning to interrupt.

Whether Evommune specifically becomes the company that monetizes that frontier is, as of June 2026, genuinely unknown and rests on data the company has not yet reported. The bear's graveyard and the bull's multi-bagger are both still live. But the structure of the bet is unusually clean for a clinical-stage name: a proven team, a counter-positioned mechanism, a capital-efficient cap table with the crown-jewel geographies intact, and a small number of near-term, binary catalysts that will resolve the uncertainty one way or the other within quarters rather than years. For a long-term investor, that is the rare biotech where the question is not "what does this company even do" but the much cleaner "does the molecule work" — and the answer is about to arrive. The Dermira Mafia bet two weeks of their lives, in early 2020, that they were not finished. The market will soon tell them whether they were right.

References

-

Evommune Announces Pricing of its Initial Public Offering — PR Newswire, 2025-11-05 ↩↩

-

Evommune Announces Strategic Collaboration with Maruho to Develop and Commercialize MRGPRX2 Antagonist EVO756 in Japan — PR Newswire, 2023-09-12 ↩

-

Evommune Announces Expanded Strategic Collaboration with Maruho in Greater China and Key Asian Countries — PR Newswire, 2024-03-25 ↩↩

-

Incyte Announces Acquisition of Escient Pharmaceuticals and its Pipeline of First-in-Class Oral MRGPR Antagonists — Incyte Corporation, 2024-04-23 ↩↩

-

Incyte Completes Acquisition of Escient Pharmaceuticals — Business Wire, 2024-05-30 ↩

-

Incyte's $750M Escient Bet Flops as Skin Disease Assets Stumble — BioSpace, 2025 ↩↩

-

Novartis gains rights to Kyorin's chronic spontaneous urticaria candidate in deal worth $830m — PMLiVE, 2025-03 ↩↩

-

Evommune Announces $115 Million Series C Financing — PR Newswire, 2024-10-31 ↩↩

-

Evommune drops IRAK4 inhibitor after assessing phase 2 dermatitis data — Fierce Biotech ↩

-

Evommune Initiates Phase 1 Study to Evaluate Safety of EVO101, an IRAK4 Inhibitor, in Healthy Volunteers — PR Newswire, 2022 ↩

-

Lilly Announces Agreement to Acquire Dermira — Eli Lilly and Company, 2020-01-10 ↩↩↩↩

-

Just over a year after acquisition, Lilly to shutter Dermira's Menlo Park facility and shed 163 jobs — Fierce Pharma, 2021 ↩

-

Evommune Initiates Phase 2b Trial of its Oral MRGPRX2 Antagonist, EVO756, in Adults with Moderate to Severe Atopic Dermatitis — PR Newswire, 2025 ↩

-

Evommune Announces Positive Top-line Data from Phase 2a Proof-of-Concept Trial of EVO301 in Moderate-to-Severe Atopic Dermatitis — Evommune, Inc. ↩

-

Evommune Reports Fourth Quarter and Full Year 2025 Financial Results and Provides Business Highlights — PharmiWeb / Evommune, 2026-03-06 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube