EverQuote Inc.: The Story of Online Insurance Marketplaces

I. Introduction & Episode Roadmap

Picture this: two MIT fraternity brothers, a Harvard MBA between them, serial entrepreneurs who had already built a pharmaceutical company and a cybersecurity firm, sitting inside a Cambridge incubator in 2011, deciding that the next great internet opportunity was... auto insurance. Not AI. Not social media. Not fintech in the flashy sense. Auto insurance. The unsexy, heavily regulated, agent-driven world where a trillion dollars in premiums change hands every year in the United States, and where the consumer experience had barely evolved since the days of the Yellow Pages.

That decision led to EverQuote, now the largest online marketplace for insurance shopping in the United States. The company trades on NASDAQ under the ticker EVER, generated nearly $700 million in revenue in 2025, and has set its sights on crossing the billion-dollar mark within the next few years. But the path from a scrappy ad-tech project called AdHarmonics to a publicly traded marketplace was anything but straightforward. It involved a name change, a pivot from advertising technology to insurance, an IPO that opened to lukewarm applause, the sudden death of a beloved founder, a pandemic-era boom followed by a brutal bust, a radical restructuring that cut nearly a third of the workforce, and now what appears to be a remarkable comeback story.

The core question this episode explores is deceptively simple: Can you build a durable technology business in the unglamorous world of insurance lead generation? Insurance is sold, not bought. Consumers hate shopping for it. Carriers spend billions trying to reach them. And in between sits a marketplace operator trying to match the two sides efficiently while skimming enough margin to build a real business. It is a model that has attracted and destroyed venture capital for decades. InsWeb tried it in the 1990s. NetQuote tried it in the 2000s. Both were acquired. A dozen venture-backed startups poured in during the 2010s. Most have consolidated or disappeared.

EverQuote survived. Whether it thrived, and whether the current trajectory represents genuine durable value or simply a cyclical tailwind, is exactly what we are here to examine.

The themes that run through this story include marketplace dynamics and the cold-start problem, the brutal economics of performance marketing, regulatory complexity as both barrier and burden, the art of pivoting under pressure, and the relentless discipline of unit economics in a business where the spread between what you pay for traffic and what carriers pay you for leads determines everything. Along the way, we will encounter an MIT fraternity that produced three companies, a data incubator that pioneered neural network research before it was cool, a pandemic that turned the business upside down and then right-side up, and the question of whether the most boring industries sometimes produce the most interesting business stories.

II. The Insurance Industry Context & Market Opportunity

To understand EverQuote, you first have to understand why insurance distribution is so stubbornly resistant to disruption. The United States insurance market exceeds one trillion dollars in annual premiums. Auto insurance alone represents roughly $350 billion. Homeowners insurance adds another $150 billion. And yet, for most of the industry's history, the way these products reached consumers was remarkably primitive: a local agent, a captive salesperson, or a piece of direct mail.

The reason is structural. Insurance is what economists call a "negative good," something people need but do not want. Nobody wakes up excited to compare auto insurance quotes. The product itself is intangible, the pricing is opaque, and the terms are written in language designed to be incomprehensible. Unlike buying a smartphone or choosing a restaurant, where the consumer derives direct pleasure from the purchase, buying insurance is about mitigating risk, paying today for protection against something you hope never happens. This creates a fundamental distribution problem. Carriers cannot simply post prices and wait for customers to show up. Insurance has to be sold, actively pushed toward consumers through advertising, agent networks, and increasingly, through digital channels.

Consider the magnitude of the distribution challenge. In auto insurance alone, there are roughly 200 million insured vehicles in the United States. The average auto insurance policy costs around $1,700 per year, and policies typically renew every six or twelve months. That means hundreds of millions of renewal decisions happen annually, each one a potential moment of consumer shopping and carrier switching. Yet historically, the vast majority of consumers simply renewed without shopping. Inertia is the insurance industry's best friend and its greatest competitive moat. The whole purpose of an online marketplace like EverQuote is to break that inertia, to catch consumers at the moment they are willing to shop and connect them with carriers willing to compete for their business.

The internet was supposed to change everything. In the mid-1990s, a company called InsWeb launched the first web-based insurance lead aggregation platform. The promise was beautiful: transparency, comparison, consumer empowerment. But InsWeb never achieved profitability as a standalone company and was eventually acquired by Bankrate in 2011 for $65 million, a modest outcome after years of operation. NetQuote, which had actually started in 1989 as a phone-based insurance shopping service before pivoting to the internet, was acquired by Bankrate in 2010 for $205 million. Bankrate went on to consolidate multiple insurance lead-generation assets under one roof, eventually branding them as insuranceQuotes.com before pieces ended up with AllWebLeads.

The pattern was clear: the concept of online insurance comparison worked, but building a standalone, profitable, scaled business around it was extraordinarily difficult. The problem was not demand. Consumers genuinely wanted to compare. The problem was economics. Acquiring consumer traffic, primarily through Google search advertising, was brutally expensive. Insurance keywords are among the most costly in the entire Google Ads ecosystem. A click on "car insurance" costs roughly $40. More specific queries like "best car insurance in North Carolina" can run above $200 per click. Only legal keywords are more expensive. The reason is straightforward: insurance customer lifetime values of $2,000 to $4,000 justify these astronomical acquisition costs for carriers, which means every marketplace and lead generator is competing against deep-pocketed carriers for the same consumer attention.

This creates the core economic challenge that defines EverQuote's business. The company must buy consumer traffic at one price and sell access to those consumers to carriers at a higher price. The spread between those two numbers, what EverQuote calls Variable Marketing Margin, is the lifeblood of the business. When the spread is healthy, the company thrives. When it compresses, from rising traffic costs, declining carrier budgets, or both, the business can deteriorate rapidly.

For decades, the insurance industry's distribution spending was dominated by offline channels. Agents controlled the relationship. Direct mail had its niche. Television advertising, led by GEICO's gecko and Progressive's Flo, consumed billions. But the Google AdWords revolution of the 2000s created an entirely new battlefield. For the first time, carriers could reach consumers at the exact moment of intent, when someone was actively searching for insurance quotes. This created a massive new addressable market for digital intermediaries who could aggregate that intent and sell it efficiently. By the time EverQuote's founders were looking at the space in 2011, digital advertising in insurance had grown to roughly $8 billion annually, a fraction of the $129 billion total insurance distribution and advertising market, but growing fast.

There is one more structural dynamic worth understanding. Insurance is one of the few industries where the customer acquisition cost can be rationally enormous because the lifetime value is so high. A single auto insurance customer who stays for five years at $1,700 per year represents $8,500 in lifetime premium revenue. Even at industry-average loss ratios, the underwriting profit and investment income on those premiums justify paying $300 to $500 to acquire that customer. This is why Google insurance clicks cost $40 to $200: the math works for carriers. And this is why the intermediary business, sitting between Google and the carrier, capturing a piece of that acquisition spend, can generate substantial revenue even with thin margins. The question has always been whether that intermediary position is defensible or whether it gets squeezed from both sides.

The opportunity was real. But so was the graveyard of companies that had tried and failed to capture it.

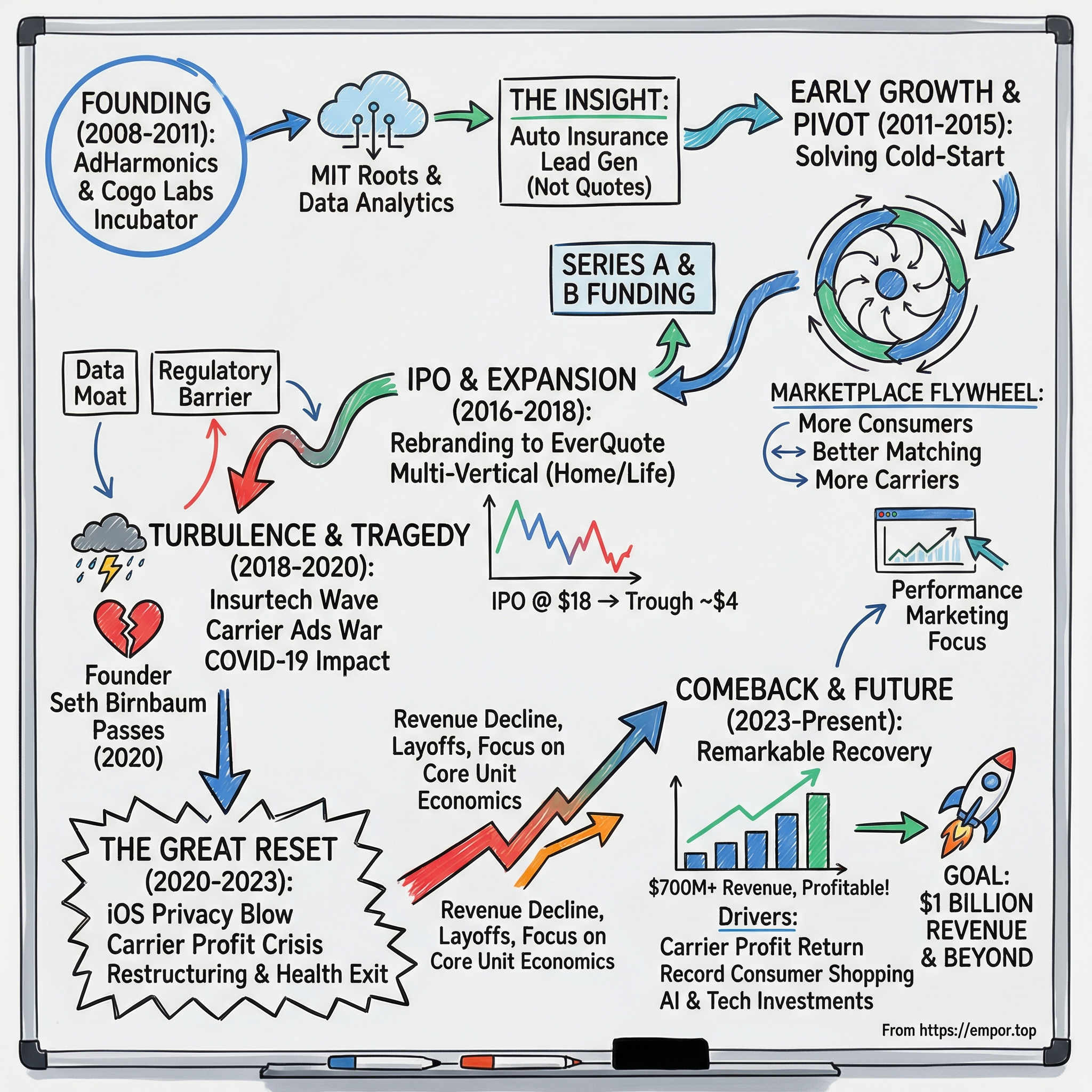

III. Founding Story: From Ad-Tech Incubator to Insurance Marketplace (2008-2015)

Seth Birnbaum and Tomas Revesz first met as freshmen at MIT, pledging the same fraternity. They became fast friends and, eventually, serial co-founders. Their first venture together was NeoGenesis Pharmaceuticals, a drug-discovery company they co-founded in Cambridge in 1997. It was a credible biotech play that ultimately sold to Schering-Plough around 2005. Their second venture was Verdasys, a cybersecurity firm based in Waltham, Massachusetts, which later rebranded as Digital Guardian and remains independent.

By 2008, Birnbaum and Revesz were ready for their third act. They had been friends for nearly twenty years. Birnbaum, who held a BS from MIT and an MBA from Harvard Business School, was the outward-facing visionary who "shined in a big room, packed with people" and "always wanted to hit the gas," as colleagues would later describe him. Revesz, who had studied Management Science and Electrical Engineering at MIT and began his career as a system administrator at the MIT Media Lab, was the quieter technical architect who preferred to work behind the scenes. Together, they were a study in complementary contrasts.

The missing piece was David Blundin. Blundin was an MIT alumnus who had researched neural networks at the MIT AI Lab and had pioneered quantization of neural networks back in 1992, well before deep learning became fashionable. In 2005, he co-founded Cogo Labs, a Cambridge-based technology incubator that used data analytics to systematically identify and build internet businesses. It was through the Cogo Labs ecosystem that Birnbaum and Revesz reconnected with a group of MIT alumni who had built several vertical internet companies with explosive growth trajectories.

In August 2008, they incorporated AdHarmonics, Inc., an internet advertising technology company, within the Cogo Labs incubator. The timing was, by any conventional measure, terrible. Lehman Brothers collapsed the following month. Bear Stearns had already disappeared. The financial crisis was devastating for startups, especially those dependent on advertising budgets. Venture capital dried up. Ad spending plummeted. The entire digital advertising ecosystem was in retreat.

But for AdHarmonics, the timing may have actually been perversely advantageous, in ways that would only become clear years later. The crisis shook up consumer behavior, as households suddenly became far more price-sensitive about recurring expenses like insurance. It forced carriers to reconsider their distribution strategies, as the cost-effectiveness of traditional channels came under scrutiny. And it created a window for new entrants willing to compete on efficiency rather than brand spending. When budgets are tight, performance marketing, where every dollar spent can be measured against a return, becomes more attractive than brand advertising, where the payoff is diffuse and delayed. The financial crisis, in a sense, accelerated the shift toward exactly the kind of data-driven distribution model that AdHarmonics would build.

By 2011, the team had zeroed in on insurance. The original insight was elegantly simple: consumers wanted to compare insurance options, and carriers wanted qualified leads. The gap between those two needs was enormous, and data science could bridge it. Unlike prior attempts at insurance comparison that essentially listed quotes side by side, the EverQuote approach would use algorithmic matching to connect consumers with carriers whose products had historically been purchased by similar drivers. It was not a quote engine. It was a lead-generation machine powered by data.

What made the Cogo Labs incubator particularly well-suited for this approach was its data infrastructure. Blundin had built Cogo Labs to systematically discover business opportunities by analyzing massive datasets. The incubator maintained multi-petabyte data assets and had the engineering talent to process them. When the team began testing the insurance vertical, they could run experiments at scale, testing consumer acquisition channels, questionnaire designs, and carrier matching approaches far more rapidly than a typical startup working from scratch. The insurance marketplace was not Cogo Labs' first experiment; it was one of several vertical internet businesses the incubator had explored. But it was the one that stuck, because the unit economics worked and the market opportunity was enormous.

They launched the insurance marketplace in 2011, secured $3.1 million in seed funding, and chose auto insurance as the entry point.

The logic was compelling: auto insurance was the largest personal lines market by premium volume, it was the product consumers shopped for most frequently due to regulatory requirements and regular rate changes, and it had the highest consumer engagement. Nearly every adult driver needed it, many were dissatisfied with what they had, and the switching costs were low.

The cold-start problem, the classic two-sided marketplace challenge, was real and particularly acute in insurance. Unlike a restaurant marketplace where consumers can see reviews and browse menus even without booking, an insurance marketplace with no carriers is simply an empty form. Consumers would not come without carriers to match with, and carriers would not participate without consumer volume. It is the classic chicken-and-egg problem that kills most marketplace startups before they gain traction.

The team solved it the way most successful early-stage marketplaces do: by hand, starting with a single geography where they could concentrate their efforts. They began in Massachusetts, the team's home state, building relationships with local independent agencies and regional carriers one meeting at a time. The advantage of starting in a single state was that they only needed to learn one set of regulatory requirements, build relationships with a manageable number of carriers, and generate enough consumer volume in one geographic market to demonstrate proof of concept.

They used Cogo Labs' data science capabilities to drive initial consumer traffic through targeted Google search campaigns. The consumer experience was free. Users entered their ZIP code, filled out a roughly ten-minute questionnaire about their vehicle, driving history, and coverage preferences, and received carrier matches. Importantly, EverQuote did not display actual insurance prices. It matched consumers to carriers and facilitated contact, typically through emails and phone calls from matched agents. This distinction mattered because displaying actual quotes would have required real-time integrations with carrier rating systems, a technically complex and regulatory-fraught endeavor. By operating as a lead-generation marketplace rather than a quote-comparison engine, EverQuote could launch faster and scale more efficiently.

By 2015, things were moving fast. The company had hired fifty new workers in just five months, and a Boston Globe profile described it as a high-tech startup generating roughly $100 million in revenue and "moving quickly toward an initial public offering." The user base had exceeded one million. Revenue that year came in at approximately $97 million, virtually all from auto insurance referrals. A $1.6 million Series A closed in April 2015. A $23 million Series B led by Savano Capital Partners followed in October 2016, later expanded by an additional $13 million from Second Alpha Partners and Link Ventures, bringing total Series B capital to roughly $36 million.

In August 2017, EverQuote officially added home and life insurance to the marketplace. The timing was deliberate, coming just before the IPO filing would need to show multi-vertical potential. New verticals saw more than tripled consumer demand and gained access to over 7,000 insurance agencies. The transformation from a single-product lead generator to a multi-vertical insurance marketplace was underway.

The company had formally changed its name from AdHarmonics to EverQuote in November 2014, shedding its ad-tech origins for a consumer-facing insurance brand. But beneath the rebranding, the core DNA remained: this was a data science company that happened to operate in insurance, built by engineers who believed algorithms could solve distribution problems that agents and brokers had owned for a century.

The founding team's lack of insurance industry experience was, paradoxically, an advantage. They approached the problem as engineers and data scientists rather than as insurance people, which meant they were not constrained by the industry's assumptions about how distribution should work. Where industry veterans saw agents as indispensable intermediaries, the EverQuote founders saw data as a more efficient intermediary. Where incumbents invested in brand advertising to build awareness over time, the founders invested in performance marketing to capture demand in real time. This outsider perspective, combined with the Cogo Labs data infrastructure and the founders' track record of building and scaling companies, gave EverQuote a distinctive approach to a market that had resisted disruption for decades.

IV. Building the Marketplace Flywheel (2011-2015)

Building a two-sided marketplace is one of the hardest challenges in business. You need supply and demand simultaneously, and neither side has much reason to show up until the other already has. In EverQuote's case, the supply side was insurance carriers and their agents, and the demand side was consumers shopping for coverage. The flywheel, once spinning, was elegant: more consumers attract more carriers, which improves matching, which improves consumer experience, which attracts more consumers. Getting it started was the hard part.

EverQuote's consumer journey was designed for maximum data capture with minimum friction. A visitor arrives at the site, enters a ZIP code, and begins a structured questionnaire. Over roughly ten minutes, the system collects vehicle details, annual mileage estimates, driving history, coverage preferences, and demographic information. This level of detail matters because it allows the matching algorithm to place consumers into profiles that align with common underwriting criteria. The data is not just used for one-time matching. Over the years, EverQuote accumulated more than 4.5 billion proprietary consumer-submitted data points, a dataset that powers machine learning models for marketing optimization, conversion prediction, and carrier matching.

The economics of lead generation in insurance are straightforward in concept but devilish in execution. EverQuote acquires consumer traffic, primarily through paid search engine marketing on Google, social media advertising on platforms like Facebook, and organic search optimization. Each consumer who completes the questionnaire becomes a "lead," a qualified referral that can be sold to one or more insurance carriers or agents. Leads come in two flavors: exclusive leads, sold to a single buyer at premium prices, and shared leads, distributed to multiple buyers at lower prices. Agent-facing prices typically range from roughly $6 for non-exclusive, non-standard leads to $21 or more for premium exclusive leads. National carriers negotiate different rates through direct relationships.

The key performance metric is the Variable Marketing Margin, or VMM. This is simply revenue minus the cost of the online advertising used to acquire the consumer traffic that generated that revenue. Think of it as gross profit on traffic. If EverQuote spends a dollar acquiring a consumer and earns $1.30 by selling that consumer's lead to carriers, the VMM is 30 cents, or a 30% margin. In recent quarters, VMM has hovered around 29%, meaning that for every dollar of revenue, roughly 29 cents remain after paying for traffic acquisition. Everything else, engineering salaries, office rent, executive compensation, comes out of that 29 cents.

Geographic expansion was necessary but painstaking. Insurance is regulated at the state level in the United States, creating one of the more complex regulatory landscapes in American business. Each of the fifty states has its own insurance department, its own commissioner, its own rules about agent licensing, lead disclosure requirements, consumer consent standards, and advertising guidelines. California, the largest auto insurance market, prohibits the use of credit scores in auto insurance pricing, which affects how leads are qualified and matched. Florida requires specific disclosures about lead-generation practices. New York has particularly strict regulations around insurance marketing communications.

Expanding from Massachusetts to nationwide coverage required navigating fifty different regulatory environments, a process that took years and demanded significant legal and compliance investment. But it ultimately became a competitive advantage. Any new entrant would face the same regulatory maze, and having already solved it gave EverQuote operational knowledge that was difficult to replicate quickly. The compliance infrastructure, legal relationships, and state-by-state playbooks that EverQuote built over years represent institutional knowledge that cannot simply be purchased or hired into existence overnight.

The addition of home and life insurance verticals in 2017 was strategically important. Auto insurance, while the largest market, was also the most competitive. Home insurance offered different consumer demographics and carrier relationships. Life insurance, though smaller in digital penetration, provided higher-value leads. By the time of the IPO, auto insurance still represented 94.5% of revenue, but the trajectory toward diversification was established.

Competition was intensifying. The Zebra, founded in Austin in 2012, would go on to raise $258 million and achieve a unicorn valuation of over $1 billion in its 2021 Series D. Insurify, founded in Cambridge in 2013 practically on EverQuote's doorstep, raised $154 million and later acquired Compare.com. Gabi offered automated policy comparison and would eventually be acquired by Experian for $320 million in 2021. Policygenius raised $288 million before being acquired by Zinnia in 2023. The space was crowded, well-funded, and fiercely competitive.

EverQuote's advantage was not flashy technology or brand recognition. It was operational efficiency. The team obsessed over conversion rates, matching quality, and the unit economics of every marketing dollar spent. In a business where the difference between profit and loss is a few percentage points of margin on traffic acquisition, operational excellence is the only moat that matters.

To put the competitive landscape in perspective, consider what happened to many of these well-funded competitors. The Zebra laid off roughly 40 employees in May 2022 and another 50 in November 2022 as the post-pandemic downturn hit. No subsequent funding rounds were publicly disclosed after the 2021 unicorn valuation. Policygenius, despite $288 million in funding, was acquired by Zinnia in 2023, suggesting the standalone insurance marketplace model for life insurance was not viable. Gabi was absorbed into Experian's broader financial services ecosystem. Compare.com was acquired by Insurify. The historical pattern of the insurance marketplace space is consolidation: standalone lead-generation businesses are capital-intensive and benefit enormously from scale, which inevitably drives them toward either acquisition or extinction. EverQuote, as the largest publicly traded pure-play in the space, has thus far avoided that fate, but the precedent is clear.

V. Inflection Point: The Pivot to Performance Marketing (2014-2016)

Sometime around 2014, EverQuote's leadership made a strategic realization that would define the company's trajectory. The original vision of transparent insurance comparison, letting consumers see quotes side by side, was being commoditized. Multiple startups offered similar experiences. The consumer-facing comparison tool was becoming table stakes, not a differentiator. But something upstream was proving far more valuable: the ability to acquire consumers efficiently and match them to carriers with precision.

The shift was subtle but profound. Instead of positioning as a "comparison shopping" tool, EverQuote repositioned as an "optimized marketplace." The difference matters. A comparison tool is a commodity. Anyone can build one. But a performance marketing engine that can consistently acquire high-intent insurance shoppers, qualify them through detailed data capture, and route them to the carriers most likely to convert them into policyholders, that is operationally complex and takes years of data to refine.

This pivot transformed carrier relationships from transactional to strategic. In the old model, EverQuote was one of many lead vendors competing on price. In the new model, EverQuote became a performance marketing partner that could demonstrate measurably higher conversion rates and lower cost per acquisition for carriers. Better matching meant higher conversion rates, which meant carriers were willing to pay more per lead, which improved EverQuote's revenue per consumer, which allowed the company to bid more aggressively for traffic while maintaining margins. It was a virtuous cycle powered by data.

The data advantage compounded over time. Each consumer interaction generated data about which profiles convert with which carriers in which geographies. Machine learning models trained on millions of these interactions got progressively better at predicting matches. A new competitor starting from scratch would have no such training data and would face a cold-start problem not just on the consumer side but on the algorithmic side as well.

The revenue model evolved alongside the strategic repositioning. Early revenue was purely cost-per-lead, a fixed price for each consumer referral delivered. Over time, EverQuote experimented with cost-per-acquisition models, where payment was tied to actual policy sales rather than just lead delivery. This aligned incentives more closely with carriers and demonstrated confidence in lead quality. The shift also helped differentiate EverQuote from the low-quality "lead mills" that plagued the insurance industry, operations that generated high volumes of poorly qualified leads and sold them to dozens of agents simultaneously.

To understand this more concretely, consider how the matching algorithm works in practice. A consumer in Phoenix, Arizona, fills out the EverQuote questionnaire and reports a clean driving record, two vehicles, and a home bundle preference. The system identifies that this consumer profile historically converts at a 14% rate with Carrier A but only 6% with Carrier B, while a different consumer profile with a DUI on record converts at 8% with Carrier C, which specializes in non-standard risk. By routing each consumer to the carrier most likely to issue a policy, EverQuote increases conversion rates for carriers, which makes them willing to pay more per lead, which allows EverQuote to bid more for traffic and acquire more consumers. The entire flywheel depends on the quality of the match, and the quality of the match depends on data accumulated over years of transactions.

This is what separates a technology-driven marketplace from a commodity lead aggregator. A traditional lead aggregator collects consumer information and sells it to the highest bidder. A marketplace optimizes the match between consumer and carrier using data science, increasing the probability of a successful outcome for both sides. The difference in economics is substantial. A poorly matched lead might convert at 3% and command $8. A well-matched lead might convert at 15% and command $25. The same consumer, routed differently, generates three times the revenue. Multiply that across millions of annual consumer interactions and the advantage compounds rapidly.

By 2016, with the Series B capital in hand and a clear strategic direction, EverQuote had built the foundation for what it would pitch to public market investors: not a commodity lead generator, but a technology-driven performance marketing platform. The distinction was critical for the company's valuation narrative, and for its survival in an increasingly competitive landscape.

VI. The Road to IPO: Scaling & Professionalizing (2016-2018)

The two years leading up to EverQuote's IPO were a period of rapid professionalization. The company brought in experienced board members, including Sanju Bansal, the former COO of MicroStrategy who had spent two decades at the business intelligence giant. John Wagner joined as CFO and would serve for nine years, shepherding the company through its public offering and five subsequent years as a public company. Jayme Mendal joined as Chief Revenue Officer in September 2017, bringing a background in management consulting at Monitor Deloitte and strategic roles at PowerAdvocate, an energy intelligence firm. Mendal held an MBA from Harvard Business School, continuing the HBS thread that ran through EverQuote's leadership DNA.

The marketing machine scaled dramatically. Revenue climbed from roughly $97 million in 2015 to $123 million in 2016 and $126 million in 2017. The growth rate looked modest, but the infrastructure being built underneath would power much faster expansion.

Technology investments in machine learning, predictive analytics, and fraud prevention formed the foundation. The engineering team grew substantially, adding data scientists and machine learning engineers who could build the models that turned raw consumer data into optimized carrier matches. The company invested in real-time bidding infrastructure that could adjust marketing spend across thousands of Google AdWords campaigns simultaneously, allocating budget dynamically based on which keywords and geographies were generating the best returns at any given moment.

The Verified Partner Network, or VPN, was perhaps the most strategically important innovation of this period. The VPN expanded the company's lead supply beyond its own websites by incorporating third-party insurance shopping sites that met EverQuote's quality standards. These partners operated their own consumer-facing insurance comparison sites, but their leads flowed exclusively through EverQuote's marketplace. Partners could not sell the same leads elsewhere, creating exclusive supply at scale. The VPN essentially turned EverQuote into the "operating system" for a distributed network of insurance shopping destinations, each one feeding leads into the centralized matching engine. This was a powerful growth lever because it allowed EverQuote to scale consumer volume without proportionally increasing its own marketing spend.

The S-1 filing landed in mid-2018, and how EverQuote positioned itself told the story of the pivot in full. The filing emphasized that EverQuote was the "largest online auto insurance marketplace in the U.S." and highlighted a total addressable market of $129 billion in U.S. P&C insurance distribution and advertising spend. The digital portion of that market was approximately $8 billion and growing. EverQuote claimed less than 1% of the total market but roughly 7% of the digital segment, framing enormous runway ahead.

On June 28, 2018, EverQuote priced its IPO at $18 per share, above the initial expected range of $15 to $17, signaling strong institutional demand. The offering comprised 4.7 million shares of Class A common stock, with roughly 3.1 million new shares from the company and 1.6 million from selling shareholders. Gross proceeds totaled approximately $84 million. The company adopted a dual-class share structure, with Class B shares carrying ten votes per share, ensuring founders and early investors retained voting control. J.P. Morgan and Bank of America Merrill Lynch led the offering.

The opening market capitalization was roughly $450 million, a respectable but not spectacular debut. To put this in context, 2018 was a strong year for technology IPOs: Spotify had direct-listed in April, Dropbox debuted in March, and DocuSign followed in April, all generating far more attention. EverQuote was a small fish in a very large pond. Shares initially climbed above $20 before retreating back toward the $18 IPO price, lacking the first-day pop that technology IPOs of the era typically enjoyed.

Wall Street's reception was politely skeptical. The key concerns were predictable and, it must be acknowledged, largely valid. Analysts noted the high revenue concentration in auto insurance, which represented 94.5% of 2017 revenue. They questioned the sustainability of margins in a lead-generation business where the primary cost, Google advertising, was controlled by a single dominant platform. They worried about the lack of clear network effects that would create winner-take-all dynamics. And the dual-class structure, which preserved voting control for insiders, raised governance concerns among institutional investors who increasingly demanded alignment between voting rights and economic ownership.

Full-year 2018 revenue came in at $163 million, up 29% from 2017. The auto vertical contributed $141 million, while the nascent home and life verticals added $22 million, a 220% increase that validated the multi-vertical expansion. Variable Marketing Margin reached $48 million, up 28%. But the company posted a net loss of $13.8 million, and the market was not in a forgiving mood. By December 28, 2018, just six months after the IPO, the stock hit its all-time low of $4.05, a staggering 78% decline from the offering price. For a company that had just gone public, it was a brutal introduction to the pressures of quarterly expectations and public market scrutiny.

VII. Inflection Point: Industry Consolidation & the COVID Era (2018-2020)

The period between EverQuote's IPO and the end of 2020 was defined by three seismic forces: a venture-capital-fueled tsunami of insurtech competition, a global pandemic that reshaped consumer behavior overnight, and a personal tragedy that would test the organization's resilience.

The insurtech wave of 2019-2020 flooded the insurance industry with capital and ambition. Root Insurance pursued a full-stack model using telematics data from smartphones to price auto insurance more precisely than traditional actuarial methods, attracting billions in venture funding before its 2020 IPO. The company's thesis was radical: if you could measure how people actually drive, you could price risk more accurately and offer better rates to good drivers, bypassing the entire traditional distribution infrastructure in the process. Lemonade promised AI-driven claims processing and a fresh consumer experience, going public in July 2020 at a valuation that implied the market believed it could reinvent insurance from the ground up. Hippo targeted homeowners insurance with smart-home technology integration and would pursue a SPAC merger in 2021. These companies threatened EverQuote's marketplace model by attempting to disintermediate distribution entirely, going directly to consumers and cutting out intermediaries.

The irony is that the insurtech wave, which initially seemed existential for marketplace models, ultimately validated EverQuote's approach. Full-stack insurance is extraordinarily difficult. Root's stock crashed after its 2020 IPO as the company struggled with underwriting losses before eventually reaching profitability in late 2024. Lemonade remained unprofitable through 2025, posting net losses of $165 million despite $738 million in revenue. Hippo only achieved underwriting profitability in late 2025 after years of combined ratios above 130%. The lesson was clear: taking on underwriting risk is a fundamentally different and far more capital-intensive business than facilitating distribution. Many insurtechs that survived eventually turned to marketplace and agent channels alongside direct distribution, which actually benefited EverQuote's model by adding more buyers to its marketplace.

Simultaneously, traditional carriers fought back with the most potent weapon in their arsenal: money. The advertising arms race in auto insurance escalated to staggering levels. Progressive's ad budget alone hit $1.2 billion in 2019 and would climb to a jaw-dropping $3.5 billion by 2024, making it one of the largest advertisers in the entire United States across any industry. GEICO was spending approximately $1.4 billion annually, funding its iconic gecko and caveman campaigns. State Farm exceeded $1.1 billion. The top three auto insurers were collectively spending more than $6 billion per year on advertising, a sum larger than the GDP of many small countries.

This created a fascinating and somewhat paradoxical dynamic for EverQuote. These carriers were simultaneously competitors and customers. Progressive would bid against EverQuote for the same Google insurance clicks while also purchasing leads from EverQuote's marketplace. GEICO would run nationwide television campaigns that drove consumers to search for insurance online, generating the very search traffic that EverQuote then monetized.

The carrier advertising arms race was, in a sense, creating the demand that fueled EverQuote's marketplace. But it also meant that EverQuote's most important customers were also its most formidable competitors, a structural tension that defined and continues to define the marketplace model.

On the competitive front, well-funded startups were multiplying, and perhaps more concerning, structurally advantaged platforms were entering the space. Credit Karma, with over 130 million members and the advantage of organic traffic from its credit monitoring platform, entered auto insurance comparison in 2018. Credit Karma's advantage was fundamental: it did not need to buy Google clicks because consumers were already on the platform checking their credit scores. Insurance comparison was simply another service offered to an existing audience, meaning the marginal cost of an insurance lead was essentially zero. Intuit acquired Credit Karma in 2020 for approximately $7.1 billion, giving it even more resources to expand into insurance and potentially integrate TurboTax's massive user base into the insurance funnel.

NerdWallet was building its own insurance comparison capability, leveraging strong SEO authority and editorial content to acquire traffic without the paid marketing costs that burdened EverQuote. NerdWallet's approach was to create comprehensive "best car insurance" guides that ranked highly in Google organic search results, then monetize that traffic by connecting consumers with carriers. The economics were fundamentally different: NerdWallet paid content writers and SEO specialists to create pages that generated free traffic indefinitely, while EverQuote paid Google for each individual click. Both approaches had merits, but NerdWallet's organic model had lower variable costs and higher margins once the content investment was made.

Then came COVID-19. The initial disruption in March 2020 was severe. Consumer behavior shifted overnight. Car usage plummeted, reducing the urgency of auto insurance shopping. Carrier marketing budgets were frozen as the industry assessed pandemic impacts. Revenue for Q1 2020 came in below expectations as the advertising market seized up. But the disruption proved temporary and, ultimately, favorable for digital insurance marketplaces in a way that few could have predicted. Consumers who had previously relied on in-person agent visits were forced online. Digital insurance shopping accelerated dramatically. Carriers that had built digital acquisition capabilities, like Progressive, leaned in hard. Meanwhile, the pandemic actually improved carrier profitability temporarily because people were driving far less, which meant fewer claims. This combination of improved profitability and consumer digital adoption created a tailwind that would last through mid-2021. By mid-2020, EverQuote was riding a powerful wave, with revenue accelerating and the stock climbing toward its all-time high.

The stock reflected this optimism. From its December 2018 low of $4.05, shares climbed relentlessly through 2019 and into 2020. On July 13, 2020, EverQuote hit its all-time high of $63.44, a fifteen-fold increase from the post-IPO trough. To put that in perspective, an investor who bought at the December 2018 low and sold at the July 2020 high would have earned a return exceeding 1,400% in eighteen months. Revenue for 2020 reached $347 million, up 39% year over year. Variable Marketing Margin hit $108.6 million, up 48%. The company was generating serious scale and, for the first time, demonstrating the operating leverage that the bulls had been hoping for.

Then, on November 28, 2020, Seth Birnbaum passed away suddenly at the age of 47. The co-founder and CEO who had been the visionary driving force behind EverQuote was gone.

Colleagues described the loss as devastating, not just professionally but personally. Birnbaum was not just a CEO; he was a connector, a mentor, and a force of nature in the Cambridge technology community. A Link Ventures tribute called it "A Legend Lost." Those who worked with him described someone who "shined in a big room, packed with people," who "always wanted to hit the gas," and whose enthusiasm was infectious enough to convince engineers, investors, and insurance executives alike that an online marketplace could transform one of America's oldest industries.

The company he built was now worth more than ten times what it had been at its lowest point, but he would not see what came next. In May 2022, EverQuote's LinkedIn page posted a remembrance on what would have been his birthday, noting that his vision and spirit continued to guide the company. For a startup that was deeply personal to its founding team, the loss of Birnbaum was a wound that went beyond the organizational chart.

Jayme Mendal, who had been promoted to President just days before Birnbaum's passing, stepped into the CEO role. The Harvard MBA who had joined as Chief Revenue Officer three years earlier inherited a company at its peak, and a team in mourning. The transition, by all accounts, was handled with grace. Mendal was well-known internally, having played a central role in scaling the revenue engine. His background at Monitor Deloitte, the strategy consultancy, had trained him in analytical rigor, and his time building EverQuote's commercial operations had given him deep familiarity with the business. But the challenges ahead, challenges that had nothing to do with the leadership transition, would test even the steadiest hand.

Revenue for 2019 had come in at $249 million, a 52% jump from 2018 that demonstrated the power of the post-IPO scaling. The pace continued into 2020, with full-year revenue hitting $347 million and VMM reaching $109 million. The first-generation adjusted EBITDA was positive at $18.4 million. The company that had been left for dead at $4 per share in December 2018 had orchestrated one of the more remarkable recoveries in recent small-cap history. But the seeds of the next crisis were already being planted.

VIII. The Great Reset & Strategic Repositioning (2020-2023)

The period from late 2020 through 2023 was the most challenging chapter in EverQuote's history, a multi-front crisis that brought the company to the brink before a brutal restructuring set the stage for recovery.

The first blow came from an unlikely source: Apple. In April 2021, iOS 14.5 introduced App Tracking Transparency, or ATT, which required apps to ask explicit user permission before tracking activity across other apps and websites. To understand why this mattered so much, a brief explanation of how digital advertising worked before ATT is helpful.

Prior to the change, when a consumer visited an insurance comparison website on their phone or clicked on an insurance-related post on Facebook, a small piece of code called a "tracking pixel" would follow that consumer across the internet. If they later purchased an insurance policy from a carrier, the pixel would report back to Facebook: "This person converted." Facebook's algorithms would then find other people who looked like the converter and show them similar ads.

This feedback loop, track, convert, find more like them, was the engine that powered performance marketing across the entire internet. It was not specific to insurance; every direct-response advertiser from mattress companies to meal kit services relied on the same mechanism.

When Apple required apps to ask for tracking permission, roughly 75% of iOS users opted out. The feedback loop broke. Facebook could no longer reliably see who converted, which meant it could no longer reliably find similar high-value consumers. For performance marketers who relied heavily on Facebook's pixel-based targeting to find high-intent insurance shoppers, the impact was catastrophic. Average cost per acquisition increased nearly 40% across industries. Facebook's signal loss ranged from 12.5% to 37% of conversion events. Meta attributed $10 billion in revenue impact in 2022 alone, and a massive portion of that pain was borne by advertisers like EverQuote who depended on Meta's targeting to efficiently acquire consumers.

The second blow came from the insurance industry itself. Auto insurance carriers entered the worst profitability crisis in a decade. The combined ratio, a critical insurance industry metric, measures the total of claims paid plus operating expenses divided by premiums collected. A combined ratio below 100 means the carrier is profitable on underwriting. Above 100 means it is losing money on every policy. The industry-wide auto combined ratio deteriorated from a healthy 99.4 in 2020, helped by pandemic-era claims reductions, to a painful 112.2 in 2022.

That 112.2 figure meant carriers were paying out $1.12 for every dollar of premium collected, before even accounting for investment returns. The causes were multiple: pandemic-era claims savings evaporated as driving resumed and road congestion returned, used car prices spiked due to supply chain disruptions making total-loss claims far more expensive, and inflation drove up repair costs for both parts and labor.

Carriers responded the only rational way: they slashed marketing budgets. If you are bleeding on every policy written, the last thing you want is more policies. Carrier demand for EverQuote's leads dried up at exactly the moment acquiring those leads was becoming more expensive.

The dual squeeze was punishing. Revenue peaked at $419 million in 2021, a year that also saw adjusted EBITDA swing to negative $18.4 million as marketing costs surged and carrier budgets began to tighten. Revenue then declined 3.4% to $404 million in 2022 with a net loss of $24.4 million. Variable Marketing Margin essentially flatlined at $128.3 million. The VMM percentage actually held up at around 32%, but it was maintained by pulling back on volume, not by improving economics. The company was spending less on traffic acquisition but also generating less revenue, a defensive posture rather than a growth story.

The real pain was the trajectory. The growth narrative that had sustained the stock's recovery from its post-IPO lows was breaking down. Wall Street does not reward companies that are shrinking profitably; it demands either growth or margins, preferably both. The stock, which had been in the $20s after retreating from its 2020 all-time high, began a relentless slide toward single digits. By late 2022, shares were trading below $10, and the company's market capitalization had fallen below $300 million despite generating $400 million in annual revenue.

Management recognized that incremental adjustments would not be enough. The company was facing a classic strategic crossroads: continue trying to grow through the downturn by investing in marketing and new verticals, or radically simplify the business and focus on survival and profitability. Many management teams, especially at public companies, choose the former because cutting revenue feels like admitting failure. Mendal chose the latter.

In June 2023, EverQuote announced a comprehensive cost reduction plan that would reshape the company. The moves were dramatic and swift. Approximately 30% of positions were eliminated company-wide, affecting every department. Non-marketing operating expenses were targeted for a reduction of more than 15%. The direct-to-consumer agency, which had employed dedicated insurance advisors to sell policies directly on behalf of carriers, was scaled down significantly for the auto and home markets. And most significantly, EverQuote announced the complete exit from the health insurance vertical.

The health insurance exit deserves particular attention because it illustrates the kind of strategic clarity that separates survivors from casualties. Health insurance had represented approximately 10% of 2022 revenue and was anchored by EverQuote's 2020 acquisition of Crosspointe Insurance and Financial Services, a sixty-person health insurance agency in Evansville, Indiana. The vertical required significant capital investment, faced an increasingly unpredictable regulatory environment around Medicare and under-65 markets, and demanded specialized expertise that diverted attention from the core auto and home business. CEO Jayme Mendal described it as "making the strategic decision to exit an area that requires significant capital investment and scale to effectively compete amid an increasingly unpredictable regulatory environment."

The health insurance assets, including the Eversurance subsidiary, were sold to MyPlanAdvocate Insurance Solutions for $13.2 million in cash, a fraction of what had been invested. CFO John Wagner, who had shepherded the company through nine years and the IPO, was replaced by Joseph Sanborn, who had served in strategic finance and investor relations roles internally and brought over two decades of technology investment banking experience from J.P. Morgan, Robertson Stephens, Silicon Valley Bank, and JEGI-Clarity.

The PolicyFuel acquisition from August 2021, purchased for $16 million, also deserves mention in this context. PolicyFuel enabled "Policy-Sales-as-a-Service," where dedicated advisor teams sold insurance on behalf of specific carriers. It represented an attempt to move EverQuote beyond pure lead generation into a more embedded position in the sales process. While the broader restructuring scaled back some of these ambitions, the underlying capability remained part of the company's toolkit as the company explored ways to capture more value per consumer interaction.

The full-year 2023 results told the story of both destruction and renewal. Revenue plunged 28.8% to $288 million, the lowest level since 2019. Variable Marketing Margin fell to $100.3 million. Net loss widened to $51.3 million, including $23.6 million in restructuring charges and the $13.2 million write-down on the health insurance assets.

The stock lingered in single-digit territory. To external observers, EverQuote looked like a value trap, a company in structural decline, losing share in a competitive market.

But beneath the surface, the restructuring was working. By stripping away the health insurance vertical, by eliminating positions that no longer aligned with the focused strategy, and by reducing non-marketing operating expenses that had bloated during the growth years, Mendal's team created a leaner, more focused organization. Headcount was ultimately reduced by nearly 50% over the full restructuring period. The remaining team was concentrated on two verticals, auto and home, where EverQuote had genuine competitive advantage and deep carrier relationships. The company's cost structure had been fundamentally reset, which meant that any recovery in carrier demand would flow through to profitability far more efficiently than it had during the growth-at-all-costs era.

There is an important myth to dispel about EverQuote's 2022-2023 downturn. The consensus narrative was that EverQuote was losing competitively, that better-funded startups and bigger platforms were eating its lunch. The reality was more nuanced. The primary driver of the revenue decline was the insurance industry's underwriting cycle. When carriers are losing money on every policy they write, they do not want more customers, they want fewer. The pullback in carrier marketing spend was an industry-wide phenomenon that affected every lead generator and marketplace, not just EverQuote. The company's decision to proactively shrink by cutting unprofitable marketing spend actually demonstrated discipline that some competitors lacked. Several well-funded rivals continued spending aggressively through the downturn, burning through venture capital without generating returns. EverQuote's approach, painful as it was for shareholders, preserved capital and competitive positioning for the recovery.

For investors, the 2020-2023 period was a masterclass in the risks of marketplace businesses in cyclical industries. When carrier budgets expand, the business booms. When they contract, there is no floor. The key learning was that EverQuote's management, under Mendal's leadership, demonstrated the willingness to make painful decisions, cutting revenue, cutting headcount, cutting verticals, in order to preserve the core business and position for recovery. Whether that recovery would materialize depended on forces largely beyond management's control: carrier profitability, consumer shopping behavior, and the competitive landscape.

IX. Current State & Future Strategy (2023-Present)

The recovery, when it came, was stunning in its speed and magnitude. Full-year 2024 revenue surged 74% to $500 million, crossing the half-billion-dollar mark for the first time. Auto insurance vertical revenue nearly doubled, rising 96% to $446 million. Adjusted EBITDA climbed to nearly $60 million. In 2025, the momentum continued. Revenue grew another 38% to $692.5 million. Auto revenue reached $630 million, up 41%. Adjusted EBITDA jumped 62% to $94.6 million. The Q4 2025 quarter alone generated $195 million in revenue, growing 32% year over year.

What drove this remarkable rebound? Two forces converged, and their timing could not have been better for EverQuote's newly streamlined business.

First, auto insurance carriers returned to profitability. After years of underwriting losses, industry combined ratios improved dramatically. The P&C industry's 2024 combined ratio was 96.5, the best since 2013. Personal auto improved to 98.4 and was projected at 92.7 for 2025. The math is simple: profitable carriers spend on marketing, unprofitable carriers cut. Progressive's advertising budget exploded to $3.5 billion in 2024, up 187% from 2023. GEICO ramped 67% to $1.4 billion after years of pullback. The aggregate marketing dollars flowing into insurance customer acquisition reached record levels, and EverQuote was a primary beneficiary.

Second, consumer shopping activity hit unprecedented levels. According to J.D. Power, 57% of U.S. auto insurance customers shopped for new coverage in 2024, the highest level in the study's nineteen-year history. The cumulative impact of three years of rate increases, totaling approximately 35% from January 2022 through end of 2024, drove even long-tenured, loyal customers into the market. Shopping among customers with ten-plus years of tenure rose 35% year over year. Auto insurance shopping in the first quarter of 2025 increased another 10% compared to the same period in 2024. EverQuote's marketplace was perfectly positioned to capture this surge in demand.

Management has set an ambitious target: $1 billion in annual revenue within the next two to three years. At the current growth trajectory, that milestone is achievable. The path involves several reinforcing strategies. First, marketplace performance improvements through continued AI and machine learning refinement, including the Smart Campaigns 3.0 platform that delivers approximately 7% efficiency improvements for carrier customers. A major national carrier named EverQuote its number-one acquisition partner, a testament to the matching quality improvements. Second, capturing a greater share of agent marketing spend through the EverQuote Pro platform, where over 35% of local agent customers now use more than one of EverQuote's four agent products, up more than 15 percentage points over the prior six months. Third, traffic expansion through the Verified Partner Network, organic channels, and emerging channels like connected TV, video, and AI-powered search where the company historically had limited presence. Fourth, faster growth in the home and renters insurance vertical, which generated $62.7 million in 2025 and represents the largest adjacent opportunity.

The financial transformation has been remarkable. The company generated $95.4 million in operating cash flow in 2025 and ended the year with $171.4 million in cash and zero debt. For a company that was posting $50 million net losses just two years earlier, the turnaround in cash generation is striking.

EverQuote achieved its first GAAP profitable year in 2024 with $32.2 million in net income, then expanded to $99.3 million in 2025. An important accounting note: the 2025 figure included a one-time $38.4 million non-cash tax benefit from the release of a valuation allowance against deferred tax assets. This is a non-cash item that reflects the company's expectation of future profitability sufficient to utilize its accumulated tax losses. Even excluding that benefit, the underlying profitability trajectory is clear and accelerating.

Management noted on the Q4 2025 earnings call that approximately 80% of their top 25 carrier partners remain below their peak spending levels, suggesting significant headroom for revenue growth even without adding new carrier relationships. This is a critical data point. If carriers continue to recover and expand their marketing budgets toward previous peaks, the demand side of EverQuote's marketplace could grow substantially without requiring proportional increases in traffic acquisition spend.

The competitive moat question remains the central debate for investors. EverQuote's defenses are real but not impregnable.

On the positive side, the company's 4.5 billion proprietary data points power matching algorithms that improve with scale. Carrier relationships built over fifteen years provide operational stickiness. The regulatory complexity of operating in fifty states creates meaningful barriers for new entrants.

On the other hand, these advantages are relative, not absolute. Credit Karma's 130-million-member platform generates organic insurance traffic at near-zero marginal cost. NerdWallet's insurance revenue grew 916% year over year in the third quarter of 2024, driven by strong SEO authority. Insurify acquired Compare.com to consolidate market share. The competitive landscape is not static.

The technology story is evolving in ways that could meaningfully affect EverQuote's competitive position. The company has integrated AI and machine learning across three critical areas. First, marketing optimization: algorithms continuously adjust bidding strategies across thousands of Google and Meta advertising campaigns, reallocating spend in real time based on which keywords, geographies, and consumer segments are generating the highest Variable Marketing Margin. Think of it as having thousands of tiny spending decisions being made every minute, each one informed by the accumulated data from billions of prior interactions.

Second, consumer matching: when a consumer completes the questionnaire, the system runs the profile against historical conversion data for every available carrier in that consumer's geography, predicting which carriers are most likely to issue a competitive policy. This matching happens in milliseconds and incorporates hundreds of variables, from obvious ones like driving record and vehicle type to subtle ones like the time of day and the consumer's behavior during the questionnaire.

Third, carrier campaign management: the Smart Campaigns 3.0 platform gives carriers visibility into how their EverQuote campaigns are performing and allows them to adjust targeting parameters, budget allocation, and lead quality thresholds in near real time. This tool has been cited as delivering approximately 7% efficiency improvements for participating carriers.

Fraud prevention is an increasingly important capability. Lead fraud, where bots or bad actors submit fake information to generate illegitimate leads, is a significant problem in the insurance marketing industry. EverQuote's fraud detection systems use behavioral analysis and pattern recognition to identify and filter out suspicious submissions before they reach carriers. These capabilities improve with scale, but they are not unique. Every serious competitor is investing in similar technology.

The FCC's proposed TCPA one-to-one consent rule, which would have required lead generators to obtain separate consumer consent for each seller rather than blanket consent, represented a potential existential threat to the shared-lead model. However, the Eleventh Circuit Court of Appeals vacated the rule in January 2025, finding the FCC had exceeded its authority. The FCC reinstated its prior standard in August 2025. This regulatory reprieve removed a significant overhang, though the possibility of future regulatory action remains.

The Q1 2026 guidance provides a window into current momentum. Management projected revenue of $175 to $185 million, Variable Marketing Dollars of $49 to $52 million, and adjusted EBITDA of $23.5 to $26.5 million. The tone was more disciplined than the aggressive growth posture of 2024, with management noting that carriers are focused on profitable policy growth rather than simply expanding volume. This discipline, if maintained, could actually benefit EverQuote's long-term economics by ensuring that carrier budgets are spent more rationally rather than in the boom-bust pattern that characterized the 2020-2023 cycle.

Looking ahead, the embedded insurance trend represents both opportunity and threat. As companies like Tesla and Carvana integrate insurance purchasing directly into the vehicle buying process, the traditional "shopping" step that drives consumers to marketplaces could diminish over time. Tesla has offered auto insurance at the point of vehicle purchase since 2019, using telematics data from vehicle sensors. Root Insurance embedded its auto coverage into Carvana's online car-buying flow, pre-filling customer information and integrating the entire quote-to-payment process into checkout. GEICO has pursued similar partnerships. The global embedded insurance market was valued at roughly $140 billion in 2024 and is projected to exceed $2 trillion by 2035.

For EverQuote, this trend is more of a five-to-ten-year structural concern than an immediate competitive threat. The near-term tailwinds from carrier profitability recovery and record consumer shopping activity overwhelm the embedded insurance risk. Most consumers still shop independently, especially at renewal time when premiums increase.

But the possibility that the addressable market for comparison shopping could shrink over time, as insurance gets bundled into vehicle purchases, home closings, and fintech platform experiences, is a factor that long-term investors must weigh.

X. Playbook: Business & Strategy Lessons

The EverQuote story yields several lessons that extend well beyond insurance distribution.

The Cold-Start Problem in Regulated Marketplaces. Two-sided marketplaces are hard enough in unregulated industries. In insurance, where every state has different rules for licensing, disclosure, and advertising, the cold-start problem is compounded by regulatory complexity. EverQuote solved it by starting narrow, one state, one product, one carrier at a time, and building outward methodically. The lesson is that regulated marketplaces reward patience and operational discipline over blitzscaling.

Performance Marketing as a Core Competency. EverQuote's business is, at its foundation, a performance marketing arbitrage: buy consumer traffic, add value through qualification and matching, and sell access to carriers at a markup. This sounds simple, but executing it profitably at scale is extraordinarily difficult. The company's Variable Marketing Margin, which has hovered around 29%, represents the accumulated result of millions of micro-optimizations in bidding strategies, landing page design, questionnaire flow, and carrier matching algorithms. Building this capability takes years. Maintaining it requires constant adaptation as platforms like Google and Facebook change their algorithms, pricing, and targeting capabilities.

Regulatory Complexity as Competitive Advantage. The fifty-state patchwork of insurance regulation is a burden, but it is also a barrier to entry. Any competitor must navigate the same maze. EverQuote has fifteen years of experience doing so, including compliance infrastructure, legal expertise, and operational processes that are difficult to replicate quickly. This is not a moat in the traditional sense, but it is genuine friction that slows competitive entry.

Pivoting Without Losing Momentum. The 2014-2016 pivot from comparison tool to performance marketing platform, and the 2023 pivot from multi-vertical growth story to focused profitability play, both demonstrate management's willingness to make difficult strategic shifts. The comparison-to-performance pivot happened quietly and set up the IPO. The 2023 restructuring was dramatic and public, involving job cuts, vertical exits, and a revenue contraction, but it preserved the core business and enabled the subsequent recovery. Both pivots required the courage to abandon a narrative that was working on the surface but deteriorating underneath.

Public Market Pressures and the Profitability Imperative. EverQuote's experience as a public company illustrates the tension between growth and profitability that defines marketplace businesses. During the 2019-2021 period, the market rewarded revenue growth. When growth stalled in 2022, the market demanded profitability. Management had to shift from a "grow at all costs" mentality to a "grow profitably" mentality in real time, while public market investors punished every misstep. The 2023 restructuring, which deliberately sacrificed revenue to improve margins, was the kind of decision that is much harder to make in a public company than a private one.

Unit Economics Obsession. In performance marketing, the difference between a profitable and unprofitable business is often a few percentage points of margin. EverQuote's key insight, that obsessing over the CAC-to-lead-value ratio at a granular level, by geography, by carrier, by traffic source, by time of day, is the only path to sustainable profitability, applies to any business built on digital customer acquisition. When the spread between acquisition cost and monetization compresses, as it did in 2022-2023, the entire business model is at risk. When it expands, as it did in 2024-2025, the business can scale rapidly.

Data as a Compounding Asset. EverQuote's 4.5 billion data points are not a static moat. They are a compounding asset that makes matching algorithms more accurate, marketing spend more efficient, and carrier relationships more sticky over time. But the value of proprietary data is only as durable as the company's ability to keep collecting it. If consumer traffic declines or competitors aggregate similar datasets, the advantage erodes. Data is a moat only if the river keeps flowing.

Strategic Positioning Matters as Much as Execution. One of the most underappreciated aspects of EverQuote's story is how the company positioned itself in the minds of investors and carriers. The S-1 filing deliberately framed EverQuote as a "technology platform" rather than a "lead generation company." This was not mere spin. The framing influenced how Wall Street valued the company, which multiples analysts applied, and how carriers perceived the relationship. A technology platform commands respect and partnership. A lead vendor gets commoditized and squeezed. EverQuote's ability to maintain the platform narrative through its product investments, data science capabilities, and carrier-facing tools has been essential to its survival in a market where perception and reality are deeply intertwined.

The Importance of Knowing What You Are Not. Perhaps the most consequential strategic lesson from EverQuote's journey is the 2023 decision to exit health insurance. Many companies would have tried to preserve the multi-vertical narrative, especially as a public company facing growth expectations. Instead, Mendal's team acknowledged that health insurance was a fundamentally different business requiring different competencies and scale, and that continuing to invest in it was diluting the company's competitive advantage in auto and home. The willingness to shrink in order to strengthen is rare, especially under public market pressure. It requires a management team that is honest about what the company does well and what it does not.

XI. Porter's Five Forces & Hamilton's Seven Powers Analysis

Porter's Five Forces

Threat of New Entrants: Moderate-High. The technical barriers to building an insurance comparison website are low. A competent engineering team can build a lead-capture form and carrier integration in months. But the operational barriers are high. Regulatory compliance across fifty states requires specialized legal infrastructure. Carrier relationships take years to build and require demonstrated volume and quality. The capital requirements for marketing are substantial, as Google insurance clicks cost $40 to $200 or more. And the data advantage of incumbents means new entrants face inferior matching algorithms until they accumulate sufficient transaction history. The net result is a market that is technically easy to enter but operationally difficult to compete in.

Bargaining Power of Suppliers (Insurance Carriers): High. Carriers control pricing, capacity, and the decision to participate. Large carriers like Progressive and GEICO, which together accounted for roughly 29% of EverQuote's revenue at the time of the IPO, can build direct digital channels and reduce reliance on marketplace intermediaries. Progressive's $3.5 billion advertising budget in 2024 demonstrates the resources carriers can deploy independently. Consolidation in the insurance industry further concentrates power. EverQuote is one of many lead sources for most carriers, which limits its negotiating leverage.

Bargaining Power of Buyers (Consumers): High. Consumers face zero switching costs between insurance marketplaces. The shopping experience is largely commoditized, the consumer types in information and receives matches or quotes. Consumer loyalty to any particular marketplace is negligible. The only consumer-side advantage EverQuote has is brand recognition and search engine presence, both of which require continuous investment to maintain.

Threat of Substitutes: High. Consumers can obtain insurance through multiple channels that bypass marketplaces entirely. Direct-to-consumer models from GEICO and Progressive's online channels serve millions of customers. Agent networks and traditional brokers remain the primary distribution channel. Embedded insurance through platforms like Carvana and Tesla offers a frictionless alternative. Other online marketplaces and comparison sites compete for the same shopping intent. Credit Karma's insurance offering, embedded within a platform of 130 million members, represents a structurally different and potentially more efficient distribution model.

Competitive Rivalry: High. Multiple well-funded competitors operate in the space. The Zebra raised $258 million and achieved a unicorn valuation. Insurify raised $154 million and acquired Compare.com. NerdWallet's insurance revenue is growing explosively. Credit Karma leverages Intuit's resources. Pressure on margins from competition is constant. Differentiation is difficult because the consumer-facing experience is similar across platforms. Jerry, the AI-powered insurance comparison app, raised $213 million at a $450 million valuation, has scaled to roughly five million U.S. customers, and represents the emerging threat of mobile-first, AI-native competitors that could reshape consumer expectations. The competitive field is not thinning; if anything, the improving economics of digital insurance distribution are drawing in more entrants, including large financial platforms that view insurance as a natural extension of their existing customer relationships.

Hamilton's Seven Powers

Scale Economies: Moderate. EverQuote benefits from fixed technology costs spread across higher volume, and marketing efficiency improves with scale as the company can test and optimize across more traffic sources and geographies. However, the marginal cost per lead does not decline dramatically because each new consumer requires a marketing dollar to acquire. This is not a software business where the marginal cost approaches zero. Scale helps, but it does not create the kind of cost advantage that makes competitors structurally uncompetitive.

Network Effects: Weak to Moderate. More consumers attract more carriers, and more carriers improve the consumer experience through better matching. But the network effects are limited. Consumers do not benefit from other consumers being on the platform in the way that users of a social network do. Marketplace liquidity helps, a consumer is more likely to find a good match if more carriers participate, but this is not a winner-take-all dynamic. Multiple marketplaces can coexist, each with sufficient carrier coverage to provide a reasonable experience.

Counter-Positioning: None. Incumbents, whether carriers, agents, or other technology platforms, can adopt digital distribution without cannibalizing their existing businesses. In fact, most have done so. Progressive sells directly online and through agents and through marketplaces simultaneously. There is no structural barrier preventing incumbents from competing, which means counter-positioning does not apply.

Switching Costs: Weak. Consumer switching costs are near zero. A consumer can switch from EverQuote to The Zebra or Insurify in the time it takes to type a new URL. Carrier switching costs are also low, as most carriers use multiple lead sources simultaneously and can shift budgets between them with minimal friction. There is some stickiness with high-performing carrier relationships, where EverQuote has demonstrated superior conversion rates, but this is performance-based loyalty rather than structural lock-in. A carrier that gets better results from a competitor will shift budget without hesitation. The relationship is purely economic, which is both EverQuote's strength, as it forces continuous improvement, and its vulnerability, as it means nothing prevents a better-performing competitor from taking share.

Branding: Weak to Moderate. EverQuote has some consumer brand recognition, but it is not a household name in the way that GEICO, Progressive, or even Credit Karma are. Trust matters in insurance, but EverQuote's brand is not strongly differentiated from competitors. The B2B brand with carriers, built on years of performance data and relationship depth, is more valuable than the consumer-facing brand, but it is not irreplaceable.

Cornered Resource: Moderate. The strongest case for EverQuote's defensibility lies here. The company's 4.5 billion proprietary data points on consumer behavior and conversion patterns, combined with machine learning models trained on years of transactions, represent a genuine asset that competitors cannot easily replicate. Carrier relationship depth at scale, built over fifteen years, provides institutional knowledge and trust. However, this resource is not truly irreplicable. Competitors accumulate their own data over time, and carriers maintain relationships with multiple lead sources.

Process Power: Moderate. EverQuote has developed operational excellence in performance marketing optimization, matching algorithms, and lead quality management that has been refined over fifteen years. The process of acquiring traffic, qualifying leads, matching them to carriers, and managing the economics at scale involves thousands of interdependent decisions and optimizations. This is difficult to replicate quickly but not impossible given sufficient time and investment.

Synthesis

EverQuote operates in a structurally challenging industry where all five of Porter's forces are moderate to high. The primary sources of strategic power come from Cornered Resource, specifically proprietary data, and Process Power, specifically operational excellence in performance marketing. Scale provides advantages but not insurmountable moats.

To compare EverQuote against its competitive set through this framework: Credit Karma has stronger Scale Economies and Cornered Resource power because its organic traffic model has near-zero marginal costs and its 130-million-member platform represents a user base that no competitor can replicate. NerdWallet has stronger Branding power because its editorial authority and SEO positioning generate organic traffic with high consumer trust. The Zebra and Insurify have similar Process Power but lack EverQuote's Scale Economies. None of the pure-play insurance marketplaces have meaningful network effects or switching costs.