Entergy: Powering the Gulf South for Over a Century

I. Introduction & Episode Roadmap

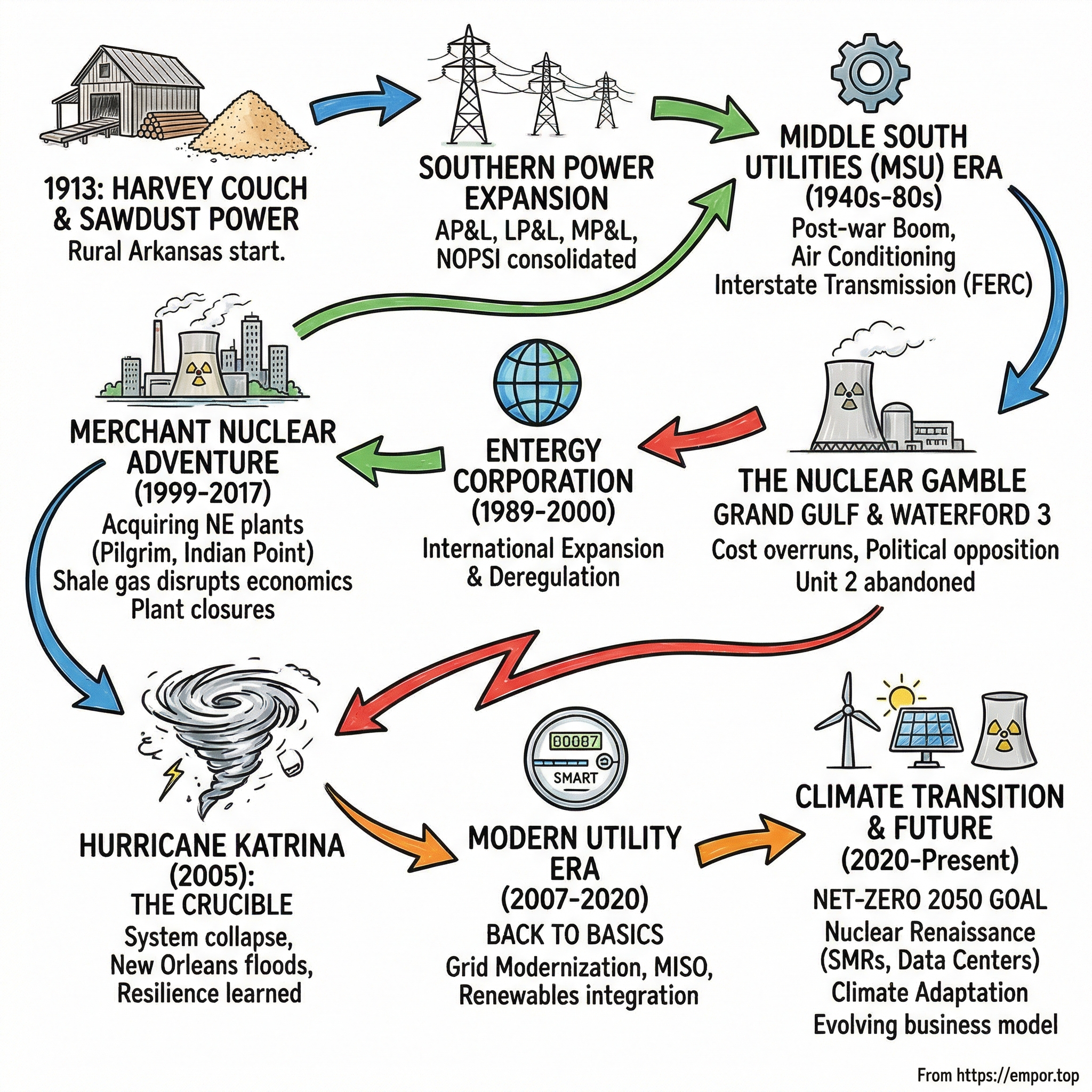

Picture this: November 1913, rural Arkansas. A young entrepreneur named Harvey Couch stands before a sawmill, watching mountains of sawdust pile up—waste material that most see as worthless. But Couch sees something different. He sees power. Literal power. Within months, he'll be burning that sawdust to generate electricity for communities that have never seen an electric light. This scrappy beginning would evolve into Entergy Corporation, today a Fortune 500 integrated energy company commanding 25,000 megawatts of generating capacity and serving 3 million customers across the Gulf South.

The central question that drives this story isn't just how a sawdust-powered startup became a regional utility giant. It's how this company survived and thrived through every major disruption of the past century: the Great Depression, World War II, the energy crisis, nuclear ambitions gone awry, catastrophic hurricanes, deregulation battles, and now the clean energy transition. Each crisis could have destroyed the company. Instead, each became a catalyst for transformation.

Today's Entergy operates across Arkansas, Louisiana, Mississippi, and Texas—a region that's both blessed with abundant energy resources and cursed with some of America's most violent weather. It's a company that bet billions on nuclear power when others fled, that rebuilt entire cities after hurricanes, and that now finds itself at the center of America's industrial renaissance as data centers and manufacturing flood into the Gulf South.

This is a story of consolidation—how hundreds of tiny local utilities became one regional powerhouse. It's about nuclear ambitions—both triumphant and tragic. It's about hurricane resilience—learning to dance with destruction. And it's about climate transition—navigating from coal to carbon-free while keeping the lights on for millions. The roadmap ahead takes us from sawdust to atoms, from Harvey Couch to Leo Denault, from rural electrification to powering the digital economy. Let's begin where all great American business stories begin: with an ambitious dreamer and an unlikely opportunity.

II. Harvey Couch & The Birth of Southern Power (1913–1940s)

Harvey Couch wasn't supposed to become a utility magnate. Born in 1877 in Calhoun, Arkansas, he started as a railroad mail clerk earning $30 a month. But Couch had something most rural Arkansans in the early 1900s lacked: he'd seen electric lights in the cities. He knew what was possible. And he knew his neighbors were living in the dark ages—literally.

The moment of transformation came on November 13, 1913. Couch had been watching the Malvern Lumber Company's operations, where massive piles of sawdust accumulated daily—a fire hazard and disposal nightmare. While others saw waste, Couch saw fuel. He convinced local investors to back his Arkansas Power Company with a radical proposition: burn the sawdust to generate electricity. The first plant, built in Malvern, Arkansas, had a capacity of just 1,850 kilowatts. To put that in perspective, a single modern wind turbine produces more power.

But Couch understood something fundamental about the utility business that remains true today: scale is everything. A single power plant serving one town is a risky proposition. A network of plants serving multiple states? That's a monopoly in the making. By 1914, he was already acquiring neighboring electric companies, rolling them into Arkansas Power & Light Company (AP&L). His pitch to local communities was simple: "Electricity will transform your town from a backwater to a beacon of progress."

The expansion was relentless and strategic. In 1923, Couch crossed state lines, acquiring Mississippi Power and Light. The company was struggling, serving just 23,000 customers across the entire state. Couch saw opportunity where others saw liability. Mississippi was agricultural, yes, but agriculture was mechanizing. Electric pumps for irrigation, refrigeration for crops, lighting for 24-hour operations—farmers would pay for power once they understood its value. Louisiana was next. In 1925, Couch formed Louisiana Power and Light, which provided power to his Mississippi customers from northern Louisiana's natural gas fields. The genius wasn't just in the acquisition—it was in the interconnection. By linking Louisiana's abundant natural gas resources with Mississippi's growing demand, Couch created the foundation for what would become an integrated regional grid. Construction of the Sterlington Station began in 1924, and it was placed into service in November 1925. Initially, Sterlington Station had two 12.5-megawatt turbogenerators, producing a total electric output of 25 megawatts. This "mighty power giant" near Monroe, Louisiana, was the first modern natural gas-fired plant in the lower Mississippi Valley—a technological leap that proved natural gas could power industrial-scale electricity generation.

But Couch's expansion came with a rival: Sidney Mitchell of Electric Bond and Share Company (EBASCO), a subsidiary of General Electric. Mitchell controlled New Orleans Public Service and had deep pockets backed by Wall Street capital. As the two men competed for territory across the South, they realized something crucial: competition would destroy value for both. The two men ultimately merged their resources. In 1925, Electric Power and Light Corporation, an EBASCO subsidiary headquartered in New Orleans, was formed with Couch as its president. It was the parent company for Arkansas Power and Light, Louisiana Power and Light, Mississippi Power and Light and New Orleans Public Service.

This merger was transformative. Couch gained access to EBASCO's capital markets expertise and financial resources. EBASCO gained Couch's operational excellence and political connections across the rural South. Together, they controlled electricity generation and distribution across four states—a monopoly that would prove remarkably durable.

The Great Depression tested everything. Banks failed. Industries collapsed. Demand for electricity plummeted as factories closed and families couldn't pay their bills. But Couch had built relationships that transcended business. When President Herbert Hoover created the Reconstruction Finance Corporation in 1932 to combat the Depression, he appointed Couch to its seven-member board. Couch moved to Washington, overseeing public works projects that kept his utilities afloat through government contracts while competitors failed.

Couch's political acumen extended beyond Washington. During the catastrophic 1927 Mississippi River flood, he served as Arkansas's flood relief director, coordinating rescue operations that saved thousands. When drought struck in 1930, he was appointed state relief chairman. These roles weren't just public service—they cemented relationships with every mayor, governor, and congressman across the region. When utilities needed favorable regulation or emergency support, Couch could call on friends who remembered his help in their darkest hours.

By the late 1930s, Couch had created not just a utility company but a regional institution. Sixteen years after starting with a 22-mile transmission line, AP&L had 3,000 miles of line serving cities and towns in sixty-three of Arkansas's seventy-five counties as well as 3,000 farmers. The company, now called Entergy, currently serves 2.4 million customers in Arkansas, Louisiana, Mississippi, and Texas. He'd also built the Remmel and Carpenter dams on the Ouachita River, creating Lakes Hamilton and Catherine—the latter named for his daughter.

Couch died on July 30, 1941, at age 63, but his vision outlived him. He'd proven that utilities weren't just about generating power—they were about building regional economies, creating political coalitions, and establishing natural monopolies that could survive any crisis. The foundation he laid would support the company through its next transformation: becoming Middle South Utilities and preparing for the post-war boom that would electrify the modern South.

III. Post-War Expansion & The Middle South Era (1940s–1980s)

The bombs had barely stopped falling on Hiroshima when American utilities began planning for a different kind of atomic age. But first, they had to navigate the immediate post-war reality: millions of returning soldiers, massive industrial conversion from military to civilian production, and pent-up consumer demand for every electric appliance imaginable. For the collection of utilities that Harvey Couch had assembled, this meant radical restructuring.

In 1949, with headquarters in New York, Middle South Utilities Inc. (MSU) was formed as a holding company for AP&L, LP&L, MP&L and NOPSI. The company's common stock began trading on the New York Stock Exchange on May 31. The name "Middle South" was deliberate—positioning the company between the industrialized North and the agricultural Deep South, suggesting a region ready for economic transformation. Moving headquarters to New York wasn't just about access to capital markets; it was a declaration that this regional utility intended to play on the national stage.

The 1950s brought explosive growth. Air conditioning, barely a luxury before the war, became essential for Southern living. Every new subdivision needed power lines. Every new factory needed industrial-grade electricity. MSU's strategy was simple but capital-intensive: build ahead of demand. If you waited for customers to request service, competitors might move in. Better to have transmission lines ready before the developers even broke ground.

The crown jewel of this expansion era was the White Bluff Plant in Arkansas. When its first coal-powered unit came online in the 1960s, it represented a crucial pivot. While Harvey Couch had built his empire on natural gas and hydroelectric power, the post-war era demanded baseload capacity that could run continuously regardless of weather or gas prices. Coal was abundant, cheap, and reliable. Environmental concerns? Those were decades away from mainstream consciousness.

Leadership transition marked this era too. Floyd Lewis had steered the company through the war years, maintaining operations despite material shortages and workforce depletion. But by the 1960s, MSU needed a different kind of leader. Enter Edwin Lupberger, an engineer by training who understood that the future of utilities lay in interstate transmission systems. Under Lupberger, MSU didn't just connect cities within states—it built high-voltage transmission lines that could move power across state boundaries, arbitraging price differences and sharing capacity during peak demand.

This interstate vision brought MSU into direct contact with federal regulation. The Federal Energy Regulatory Commission (FERC) governed interstate electricity transmission, while state utility commissions controlled retail rates. MSU had to become expert at playing a multi-dimensional regulatory game. Need to raise rates in Arkansas? Better have a compelling story for the Arkansas Public Service Commission about infrastructure investment. Want to build transmission lines across state borders? FERC needed detailed engineering studies and economic justifications.

The regulatory framework that evolved during this period was based on a grand bargain: utilities got territorial monopolies and guaranteed returns on investment, but in exchange, they had to serve everyone in their territory at regulated rates. This "regulatory compact" meant MSU could raise massive capital for infrastructure—investors knew returns were essentially guaranteed by state commissions. But it also meant every major decision required regulatory approval, turning utility executives into part-time lobbyists.

The 1970s energy crisis shattered the comfortable assumptions of the post-war era. When OPEC quadrupled oil prices in 1973, it didn't just affect gas stations—it revolutionized electricity generation economics. Suddenly, natural gas prices spiked. Coal became even more attractive, but environmental regulations were tightening. Most dramatically, nuclear power went from experimental technology to national priority almost overnight.

MSU's strategic response to the energy crisis revealed both vision and hubris. The company bet everything on nuclear power as the solution to energy independence. Oil was vulnerable to embargo. Natural gas prices were volatile. Coal faced growing environmental opposition. But nuclear? Nuclear promised abundant, cheap electricity with no carbon emissions and no dependence on foreign suppliers. Physics would provide what politics couldn't: energy security.

The commitment to nuclear wasn't just financial—it was existential. MSU's leadership believed that utilities who mastered nuclear technology would dominate the next century, while those who remained dependent on fossil fuels would become obsolete. They were half right. Nuclear would indeed become crucial to MSU's identity, but not quite in the way they imagined. The nuclear gamble would transform the company, nearly destroy it, and ultimately define its character for generations.

IV. The Nuclear Gamble: Grand Gulf & Beyond (1970s–1990s)

The meeting at MSU headquarters in 1974 must have felt like destiny. Oil prices had tripled. Natural gas allocations were being curtailed. Coal plants faced new environmental restrictions. But on the conference table sat engineering blueprints for something revolutionary: a nuclear generating station that could produce more electricity than all of Harvey Couch's original plants combined. The Grand Gulf Nuclear Station would either secure MSU's future or bankrupt it.

The site chosen—near Port Gibson, Mississippi—seemed perfect. Close to the Mississippi River for cooling water. Geologically stable. Far enough from major population centers to satisfy safety concerns, but close enough to transmission corridors to serve growing demand. The initial plan called for two units, each capable of generating over 1,200 megawatts. At full capacity, Grand Gulf would produce enough electricity to power 2.5 million homes.

Construction began in 1974 with an estimated cost of $1.4 billion and a target completion date of 1980. By 1979, the cost had ballooned to $2.8 billion. By 1984, it exceeded $3.5 billion. Every delay cascaded into more delays. New safety regulations following the Three Mile Island accident in 1979 required design changes mid-construction. Interest rates soared to 20% during the Paul Volcker Federal Reserve era, making borrowed money catastrophically expensive. Local opposition groups, initially dismissed as fringe environmentalists, gained political power and legal sophistication.

The Rex Brown Plant, named after then MP&L President Rex Brown, was completed and became the first large source of electricity generation in Mississippi. But Grand Gulf would dwarf everything that came before. When Unit 1 finally achieved commercial operation in July 1985, it was both triumph and tragedy. Triumph because MSU had actually built a functioning nuclear plant—something many utilities attempted but failed. Tragedy because the cost overruns had crippled the company's finances and poisoned relationships with regulators and customers. The 2012 upgrade makes it the largest single-unit nuclear power plant in the country and fifth largest in the world. This achievement came after decades of struggle. But Unit 2's story is pure tragedy. In December 1979, staggered by construction cost, Entergy (then called Middle South Utilities) stopped work on Unit 2. The timing was catastrophic—just months after Three Mile Island had shaken the nuclear industry to its core. Unit 2 would become the nuclear industry's most expensive ghost—a hulking concrete containment structure, 66% complete when Middle South finally abandoned it in 1990. The project was 66% complete, with billions already spent. Adjacent to the operating station today stands that unfinished structure, a monument to miscalculation. The cancellation wasn't just about cost—it was about credibility. State regulators in Arkansas and Louisiana were in open revolt, refusing to force their ratepayers to subsidize Mississippi's nuclear ambitions. The Grand Gulf disputes didn't end with construction. As recently as June 2022, the Mississippi Public Service Commission secured a $300 million settlement with Entergy Mississippi—the largest in the commission's history—over accounting and financing aspects of the plant. The settlement, the largest in the PSC's history, ends Mississippi's involvement in a multi-state dispute with Entergy. As part of the agreement, $200 million of the settlement will go towards offsetting rising natural gas costs for customers, $35 million will go towards direct payments or bill credits to Mississippi ratepayers, and the remaining $65 million will go towards savings for future mitigation costs. The fact that such disputes persisted decades after Grand Gulf's completion reveals how the nuclear gamble's financial fallout continues to reverberate.

Yet for all the controversy, Grand Gulf Unit 1 stands as a testament to persistence. It provides carbon-free baseload power that becomes more valuable each year as climate concerns intensify. The 2012 upgrade that made it America's largest single-unit nuclear plant proved that even troubled nuclear assets could be optimized. The ghost of Unit 2 may haunt the site, but Unit 1's success story—producing power at 98% capacity factor in recent years—demonstrates that the nuclear gamble, while costly, wasn't entirely misguided.

The parallel story at Waterford 3 in Louisiana followed a similar arc. Commercial operation began in September 1985, but like Grand Gulf, the second unit was scrapped. The pattern was clear: MSU could build nuclear plants, but at costs that strained every financial and political relationship the company had. The nuclear age had arrived, but it looked nothing like the utopian vision of the 1970s. It was time for a radical reimagining of what this utility could become.

V. Transformation to Entergy Corporation (1989–2000)

The boardroom at Middle South Utilities in 1989 faced a naming crisis that reflected a deeper identity crisis. "Middle South" sounded outdated, regional, limited. The company needed a name that captured ambition beyond geography. After months of deliberation, they landed on "Entergy"—a composite of "enterprise," "energy," and "synergy." Critics mocked it as corporate buzzword bingo. But the new name signaled transformation: this wouldn't be your grandfather's utility company.

The timing was perfect for reinvention. The Berlin Wall was falling. Markets were globalizing. Deregulation was sweeping through telecommunications and airlines—electricity seemed next. Under new leadership, Entergy positioned itself not as a regional utility defending territory, but as an energy company ready to compete globally. The vision was audacious: become to electricity what British Petroleum was to oil—a global brand transcending origins.

The first major move came in 1993 with the merger with Gulf States Utilities Company. GSU brought 630,000 customers across Texas and Louisiana, but more importantly, it brought River Bend Station—making it Entergy's fourth nuclear site. The merger wasn't just about scale; it was about creating a platform for national expansion. With 2.3 million customers and nuclear expertise few utilities could match, Entergy had credibility to venture beyond the Gulf South.

What followed was a five-year international expansion that would have seemed insane to Harvey Couch. Entergy acquired power plants in Australia, believing deregulation there would create opportunities for efficient operators. It built facilities in Argentina during privatization of state utilities. The company entered joint ventures in China, betting that the world's fastest-growing economy needed Western expertise. Projects sprouted in Pakistan and the United Kingdom. By 1998, Entergy operated on five continents.

The logic seemed impeccable. If electricity markets were deregulating globally, then efficient operators could arbitrage inefficiencies everywhere. Entergy's nuclear expertise and operational excellence developed through decades of running complex plants in hurricane zones should translate anywhere. The company would export American utility management to the world.

Reality proved harsher. The Australian venture hemorrhaged money when deregulation didn't materialize as expected. Political instability in Pakistan made operations impossible. The Asian Financial Crisis of 1997 destroyed currency values and power demand across emerging markets. Argentina's economy collapsed in 2001, taking Entergy's investments with it. Even the UK operations, seemingly safe in a developed market, struggled against local competitors who understood regulatory nuances Entergy missed.

By 2000, the international adventure was over. Entergy quietly unwound positions, selling assets at losses, writing off investments. The company had learned what many American corporations discovered in the 1990s: expertise doesn't always translate across borders. Running power plants in Louisiana during hurricanes was one skill; navigating Pakistani politics or Australian labor unions was entirely another.

But the international retreat coincided with domestic opportunity. Deregulation was coming to American electricity markets, particularly in the Northeast. States like Massachusetts and New York were forcing utilities to divest generation assets, creating a market for independent power producers. Entergy saw opportunity where others saw risk. If you couldn't build a global utility empire, perhaps you could roll up distressed nuclear assets in deregulating American markets.

The strategy pivot was swift and decisive. Forget building power plants in Beijing or Buenos Aires. Instead, buy nuclear plants from Northeastern utilities desperate to exit the generation business. These utilities faced political pressure to divest nuclear assets, stringent safety regulations, and public opposition following decades of cost overruns. They wanted out. Entergy wanted in.

The company created Entergy Nuclear, a subsidiary focused exclusively on acquiring and operating merchant nuclear plants—facilities that would sell power into competitive wholesale markets rather than to captive regulated customers. It was a massive bet that nuclear power, despite its troubled history, would become valuable again as natural gas prices rose and carbon concerns intensified.

The refocus on traditional strengths—operating complex power plants in challenging environments—felt like coming home. But home had changed. The Gulf South utility would now compete in deregulated Northern markets, operating nuclear plants thousands of miles from headquarters. It was still transformation, just pointed in a different direction. The company that began with sawdust in Arkansas was about to become America's second-largest nuclear operator. The merchant nuclear adventure was beginning.

VI. The Merchant Nuclear Adventure (1999–2017)

The call came in late 1998: Pilgrim Nuclear Power Station in Plymouth, Massachusetts was for sale. Boston Edison wanted out of the nuclear business. Environmental groups wanted it shut down. Local politicians wanted it gone. The asking price had dropped from $300 million to under $100 million. For Entergy's nuclear team, it was like finding a Rembrandt at a garage sale. Entergy purchased the plant in 1999 from Boston Edison for $81 million—the first U.S. company to acquire a nuclear plant through competitive bidding. The price was extraordinary. Boston Edison had spent over $1 billion building Pilgrim. Now they were practically giving it away. But Entergy saw what others missed: nuclear plants are like fine wine—they get better with age if properly maintained. The capital costs were sunk. The operating licenses extended for decades. Natural gas prices would inevitably rise. Carbon regulations would eventually come. This wasn't a distressed asset; it was an undervalued option on the future of clean energy.

The Pilgrim acquisition opened floodgates. Within months, Entergy was negotiating for Indian Point Units 2 and 3, just 35 miles from Manhattan. The politics were toxic—New York environmentalists wanted it closed yesterday. But the economics were compelling: Indian Point provided 25% of New York City's electricity. Shutting it down meant burning more fossil fuels or accepting blackouts. Entergy bet that economics would trump politics. They acquired Indian Point 3 in 2000 and Indian Point 2 in 2001, instantly becoming a major player in the Northeast power market.

Vermont Yankee came next in 2002, then James A. FitzPatrick in New York. Each acquisition followed the same pattern: distressed seller, political opposition, rock-bottom price, Entergy as the buyer of last resort. By 2007, when Entergy acquired Palisades in Michigan, the company operated 11 nuclear units outside its traditional utility territory. The Gulf South utility had become the nation's second-largest nuclear operator.

The strategy seemed brilliant—until it wasn't. The shale gas revolution that began in 2008 destroyed the economics overnight. Natural gas prices collapsed from $13 per million BTU to under $3. Suddenly, nuclear plants that needed $35/MWh to break even were competing against gas plants producing power at $25/MWh. Wholesale electricity prices plummeted. Nuclear plants that Entergy bought as cash machines became cash incinerators.

Political opposition intensified after Fukushima in 2011. Vermont wanted Vermont Yankee closed. New York's Governor Andrew Cuomo campaigned on shuttering Indian Point. Massachusetts turned against Pilgrim. The same assets Entergy acquired at distress prices were now genuinely distressed. Operating losses mounted. Capital requirements for safety upgrades soared. The merchant nuclear strategy that seemed so clever in 1999 looked catastrophic by 2013.

Enter Leo Denault, who became CEO in 2013 with a clear mandate: exit merchant nuclear. But how do you unwind a strategy that defined the company for 15 years? You can't just abandon nuclear plants—they require decades of decommissioning. You can't sell them easily—who wants money-losing nuclear plants in hostile political environments? Denault's solution was elegant: manage the exit as carefully as the entry.

Vermont Yankee closed in 2014 and was sold to NorthStar in 2019. Pilgrim shut down in May 2019 after 46 years of operation and was sold to Holtec for decommissioning. FitzPatrick was sold to Exelon in 2017. Indian Point Units 2 and 3 closed in 2020 and 2021. Palisades shut down in 2022. Each closure was negotiated, planned, and executed to minimize losses and transfer decommissioning liabilities.

The merchant nuclear adventure cost Entergy billions in losses and write-downs. But it also taught invaluable lessons: stick to your core competencies, respect political realities, and never bet against cheap natural gas. Most importantly, it convinced Entergy's leadership that the future lay not in merchant power but in returning to its roots as a regulated utility. The company that tried to become a global nuclear operator would refocus on what it did best: keeping the lights on in the Gulf South, even when nature tried its hardest to turn them off.

VII. Hurricane Katrina: The Crucible Moment (2005–2006)

August 28, 2005, 10:00 PM. Entergy's emergency operations center in Jackson, Mississippi, resembles NASA mission control. Weather monitors show a massive red spiral approaching the Gulf Coast. Hurricane Katrina, now Category 5 with 175 mph winds, aims directly at New Orleans. CEO Wayne Leonard makes the call: "Shut down Waterford 3. Evacuate all non-essential personnel. Prepare for the worst storm in company history." Nobody in that room imagined how much worse "worst" could be.

By dawn on August 29, Katrina's eye wall was demolishing Entergy's infrastructure with methodical precision. 1.1 million Entergy customers lost power—the largest outage in company history. But the numbers only hint at the devastation. One-third of Entergy's service territory was affected; 3,000 miles of transmission lines damaged or destroyed; 30,000 miles of distribution lines down; 17,400 distribution poles snapped like toothpicks. The storm didn't just damage the grid—it erased it.

At Waterford 3, the nuclear plant 25 miles west of New Orleans, operators executed a textbook emergency shutdown as winds exceeded 100 mph. The plant rode out the storm, but the transmission lines connecting it to the grid were gone. Even with a perfectly functional nuclear plant, there was nowhere to send the power. Across the region, 50 power plants were forced offline. The entire electrical backbone of the Gulf South had collapsed.

In New Orleans, the situation transcended infrastructure failure. When the levees broke, Entergy's facilities flooded with toxic water—a mixture of sewage, chemicals, and debris. The company's Canal Street headquarters, evacuated before the storm, sat in four feet of contaminated water. Substations designed to withstand hurricanes couldn't withstand being submerged. Equipment that survived the wind corroded in the flood. Nearly 2,000 New Orleans-based employees were evacuated, scattered across the country, many having lost their own homes.

The human dimension was staggering. Entergy line workers, many homeless themselves, worked 16-hour days in 95-degree heat, wading through snake-infested water to restore power. They slept in tents, ate MREs, and went weeks without seeing their families. One crew discovered an elderly couple who'd been trapped in their attic for five days, surviving on rainwater. The line workers weren't just restoring power—they were finding bodies, rescuing pets, and distributing water to survivors.

The restoration effort required military-style logistics. Entergy mobilized 11,000 workers from 23 states and Canada. Equipment poured in from across the country—poles from Arkansas, transformers from Texas, cable from Tennessee. The company established 15 staging areas, each the size of a football field, to organize materials and crews. Helicopters airlifted poles to inaccessible areas. Boats became service vehicles in flooded neighborhoods.

But Katrina wasn't finished with Entergy. Twenty-six days later, Hurricane Rita struck, affecting 800,000 Entergy customers across Texas and Louisiana. Rita was smaller than Katrina but more focused, with winds that twisted transmission towers into modern art sculptures. The same crews that had just finished 18-hour days restoring power from Katrina started over with Rita. The one-two punch was unprecedented in utility history.

The financial devastation matched the physical. Entergy New Orleans, serving America's most unique city, faced an existential crisis. With 80% of the city flooded, most customers had evacuated. No customers meant no revenue, but fixed costs continued. The utility had bonds to pay, a workforce to maintain, and massive reconstruction costs. On September 23, 2005, Entergy New Orleans filed for bankruptcy protection—the first major utility bankruptcy caused by a natural disaster.

The bankruptcy wasn't just financial restructuring—it was a fight for New Orleans' future. Without reliable power, the city couldn't rebuild. But Entergy New Orleans couldn't afford to rebuild without customers, and customers couldn't return without power. The circular trap threatened to make New Orleans America's first major city to die from a natural disaster. The solution required unprecedented cooperation between Entergy, FEMA, the state of Louisiana, and the city of New Orleans. Creditors took losses. Regulators approved emergency rate structures. Federal disaster funds flowed in ways never before contemplated.

The restoration timeline tells the story: 42 days to restore power after Katrina; 21 days after Rita. But some areas of New Orleans didn't get power back for six months. The Lower Ninth Ward, devastated by flooding, required complete infrastructure rebuilding. Entergy had to decide which neighborhoods to restore first—triage at a municipal scale. Every decision had racial, economic, and political implications. Restore wealthy areas first? Accused of discrimination. Focus on poor areas? Accused of ignoring the tax base. There were no good choices, only less bad ones.

From this catastrophe came transformation. Entergy's post-Katrina improvements read like a military after-action report. The company hardened substations, elevating critical equipment above flood levels. Transmission structures were reinforced to withstand 150 mph winds. Distribution systems were redesigned with redundancy and sectionalizing capabilities—if one section failed, others could maintain power. Emergency response protocols were revolutionized, with pre-positioned materials, mutual aid agreements, and annual hurricane drills that simulate Category 5 impacts.

The technology transformation was equally dramatic. Entergy installed automated switches that could reroute power around damaged sections. Smart meters would eventually allow remote monitoring of outages, eliminating the need for customers to call in. Predictive modeling systems could forecast damage patterns before storms hit, allowing pre-positioning of repair crews. The company that entered Katrina with 20th-century infrastructure emerged with 21st-century resilience.

Perhaps most importantly, Katrina changed Entergy's cultural DNA. The company had always dealt with hurricanes, but Katrina taught that climate change was making storms more destructive. The 100-year storm was becoming the 10-year storm. The utility couldn't just restore after disasters—it had to anticipate and adapt to increasing climate violence. This realization would drive strategy for the next two decades, influencing everything from infrastructure investment to renewable energy adoption. The company that Harvey Couch built to bring light to the South had learned to keep the lights on when nature went to war.

VIII. Modern Utility Era: Back to Basics (2007–2020)

The mahogany conference table that once hosted discussions of global expansion now bore spreadsheets focused on Mississippi pole replacements and Louisiana substation upgrades. Leo Denault, ascending to CEO in 2013 after Wayne Leonard's retirement, didn't speak of synergies or international ventures. His message was blunt: "We're a utility company. We serve Arkansas, Louisiana, Mississippi, and Texas. Everything else is a distraction."

This wasn't retreat—it was strategic focus. While Entergy had been buying nuclear plants in Vermont, Texas utilities were building massive wind farms. While Entergy wrestled with New York politics, Florida utilities were modernizing their grids. The merchant nuclear adventure had cost billions and distracted management for a decade. Denault's "back to basics" strategy meant becoming the best utility in the Gulf South, period.

The first major strategic move was joining the Midcontinent Independent System Operator (MISO) in 2013. For decades, Entergy operated as an electrical island, its own control area managing power flows across four states. Joining MISO meant surrendering some autonomy but gaining access to a market spanning from Manitoba to Louisiana. The benefits were immediate: more efficient dispatch of power plants, access to cheap wind power from the Plains, and reduced reserve requirements. MISO membership saved customers $100 million in the first year alone.

But the real transformation was happening at ground level—literally. Entergy launched one of the most ambitious grid modernization programs in America. Installing advanced meters for 3 million customers allowed for faster detection of outages and greater insight into energy usage. These weren't just digital versions of old meters. They were networked computers that could detect power quality issues, identify failing transformers before they exploded, and enable time-of-use pricing that encouraged conservation during peak periods.

The regulatory landscape had shifted dramatically since Harvey Couch's handshake deals. Entergy now operated through five retail subsidiaries—Entergy Arkansas, Louisiana, Mississippi, New Orleans, and Texas—each answering to different state commissions with different priorities. Arkansas wanted lower rates. Louisiana wanted storm resilience. Mississippi wanted economic development. Texas wanted grid reliability. Managing these competing demands while maintaining a unified system required political skills that would have impressed Machiavelli.

Rate cases became high-stakes theater. Every few years, each subsidiary would petition its state commission for rate adjustments. These weren't simple requests for inflation adjustments—they were thousand-page documents justifying every dollar of investment, every executive salary, every strategic decision. Consumer advocates scrutinized every expense. Industrial customers hired economists to argue for lower rates. Environmental groups pushed for renewable mandates. The proceedings could last years and determine billions in revenue.

The settlement with Mississippi regulators in 2022 over Grand Gulf exemplified the complexity. Decades after the plant's construction, regulators were still fighting over cost allocations and return rates. The $300 million settlement ended Mississippi's involvement in a multi-state dispute, with $200 million offsetting rising natural gas costs, $35 million in direct customer payments, and $65 million for future mitigation. Such settlements weren't victories or defeats—they were pragmatic compromises that kept the lights on while maintaining financial viability.

Infrastructure investment accelerated beyond anything Harvey Couch could have imagined. Entergy was spending $3 billion annually on capital projects—new transmission lines, distribution upgrades, generation fleet modernization. The company replaced aging infrastructure at unprecedented pace: wooden poles with steel and concrete, copper wires with advanced conductors, mechanical switches with digital controls. This wasn't glamorous work, but it was essential. Every replaced transformer meant fewer outages. Every upgraded substation meant better reliability.

The generation fleet transformation was equally dramatic. Coal plants that once formed Entergy's backbone were becoming liabilities. Environmental regulations made them expensive to operate. Natural gas made them uneconomic. Public opinion made them toxic. Entergy began systematic retirement of coal units, replacing them with efficient combined-cycle gas plants. The Lake Charles Power Station, entering commercial operation in 2020, exemplified the new model: 994 megawatts of ultra-efficient gas generation, able to ramp up quickly to support renewable intermittency.

Customer expectations had evolved far beyond simply wanting reliable power. They wanted mobile apps to track usage. They wanted solar panels on their roofs. They wanted electric vehicle chargers in their garages. They wanted their utility to fight climate change while keeping bills low. Entergy had to become a technology company that happened to deliver electricity. The company launched customer apps, online portals, and energy efficiency programs. It offered rebates for smart thermostats, LED bulbs, and efficient appliances.

The workforce transformation was perhaps most profound. Entergy's traditional workforce—line workers, plant operators, engineers—remained essential. But the company now needed data scientists to analyze smart meter data, cybersecurity experts to protect against hackers, and renewable energy specialists to integrate solar and wind. The company that once hired local farm boys to string wire now recruited from MIT and Stanford.

By 2020, Entergy had successfully completed its transformation from adventurous conglomerate back to focused utility. The merchant nuclear business was nearly unwound. International ventures were distant memories. The company generated steady returns for investors, provided reliable power to customers, and maintained strong relationships with regulators. It wasn't exciting, but it was exactly what stakeholders wanted: a boring, competent utility focused on its core mission.

Yet this "back to basics" period was actually preparing Entergy for its next transformation. The grid modernization, workforce evolution, and regulatory relationships built during this period would prove essential for the coming energy transition. The company that had learned to survive hurricanes and nuclear disasters was about to face its next existential challenge: completely reimagining electricity generation in the age of climate change.

IX. Climate Transition & The Nuclear Renaissance (2020–Present)

The announcement came in September 2020, during a virtual meeting necessitated by COVID-19. CEO Leo Denault, speaking from a nearly empty headquarters, declared Entergy would achieve net-zero carbon emissions by 2050. For a company that still operated coal plants and natural gas comprised most of its generation, this wasn't incremental change—it was revolution. The utility that began with burning sawdust would end with zero carbon.

The commitment wasn't made lightly. Entergy had already reduced carbon emissions by 35% since 2000, largely through coal plant retirements and nuclear operations. But getting to net-zero meant reimagining the entire business model. The fleet of 28 active natural gas, oil, hydroelectric, and coal facilities generating approximately 19,000 MW would need systematic transformation. The nuclear fleet producing 5,000 MW of carbon-free power suddenly became not a legacy asset but the foundation of a clean energy future.

The math was daunting. Entergy's service territory was experiencing explosive growth. Data centers were proliferating across Louisiana, drawn by cheap power and minimal natural disaster risk (hurricanes notwithstanding). Petrochemical companies were building new facilities along the Mississippi River. Electric vehicle adoption was accelerating. Demand that had been flat for a decade was suddenly growing at 2% annually. How do you decarbonize while adding thousands of megawatts of new load?

The answer was "all of the above"—but with nuclear as the backbone. Grand Gulf, once the symbol of nuclear excess, became the exemplar of clean baseload power. Operating at 98% capacity factor, producing electricity at costs competitive with natural gas, emitting zero carbon—Grand Gulf represented what nuclear could be with proper management. The plant that nearly bankrupted the company in the 1980s was now its most valuable clean energy asset.

Entergy announced 8,600 megawatts of renewable energy projects operational or announced—a stunning reversal for a company that had largely ignored wind and solar. The Sunflower Solar Station in Mississippi, Western Trail Wind in New Mexico, and dozens of other projects sprouted across the territory. But these weren't feel-good greenwashing exercises. Each project had to meet strict economic criteria, provide reliable power, and integrate with existing infrastructure.

The intermittency challenge of renewables collided with Gulf South reality. Solar panels don't generate during hurricanes. Wind turbines must shut down in extreme weather. The same climate volatility that made the region vulnerable to outages made it challenging for renewable integration. Entergy's solution was natural gas as the bridge fuel—quick-starting plants that could ramp up when renewables dropped off. The Lake Charles Power Station became the model: ultra-efficient gas generation that could partner with renewables while maintaining grid stability.

Transmission investment took on new urgency. Renewable resources were often located far from population centers—solar farms in rural Mississippi, wind projects in north Texas. Moving this power required new transmission lines, upgraded substations, and sophisticated control systems. Entergy committed $15 billion to transmission expansion over the next decade, building the electrical highways necessary for clean energy delivery.

The regulatory environment had shifted dramatically in Entergy's favor. The Inflation Reduction Act of 2022 provided unprecedented incentives for clean energy investment. Production tax credits made wind and solar economic even in the less-windy, less-sunny Gulf South. Nuclear production credits kept existing plants viable. Carbon capture incentives made natural gas plants potentially zero-emission. For the first time, federal policy aligned with Entergy's business strategy.

But the most surprising development was the nuclear renaissance. After decades of decline, nuclear power was suddenly fashionable again. Tech companies wanting 24/7 carbon-free power for data centers were willing to pay premiums for nuclear electricity. The Department of Energy was promoting small modular reactors. Even environmental groups were reconsidering their nuclear opposition in the face of climate crisis. Entergy, with decades of nuclear operating experience, was perfectly positioned for this renaissance.

The data center opportunity was particularly compelling. Northern Virginia had become "Data Center Alley," but land and power were becoming scarce. Louisiana offered abundant land, existing transmission infrastructure, and Entergy's nuclear baseload. Microsoft, Amazon, and Meta all announced major data center projects in Entergy's territory. Each facility needed 100-500 megawatts of reliable, clean power—exactly what nuclear provided.

Climate adaptation paralleled mitigation efforts. Entergy couldn't just reduce emissions; it had to prepare for worsening climate impacts. Hurricane Ida in 2021 proved that post-Katrina improvements worked but weren't sufficient. The company launched a new resilience initiative: concrete poles in critical areas, underground distribution in flood zones, and microgrids for essential facilities. The goal wasn't preventing all outages—that was impossible—but reducing restoration time from weeks to days.

The community investment strategy evolved beyond traditional corporate charity. Delivering $100+ million annually in economic benefits through philanthropy, volunteerism, and advocacy, Entergy focused on environmental justice. Low-income communities, predominantly African American in many service areas, suffered disproportionately from both climate change and energy transition. Entergy launched weatherization programs, bill assistance initiatives, and job training for clean energy careers. This wasn't just social responsibility—it was recognizing that the energy transition required everyone.

Nuclear life extensions became critical strategic decisions. Grand Gulf's license extends through 2044, but planning for the next extension must begin years in advance. Arkansas Nuclear One, River Bend, and Waterford 3 all face similar decisions. Each extension requires hundreds of millions in capital investment but provides decades of carbon-free power. The alternative—decommissioning and replacement with gas or renewables—would increase emissions and costs.

The transformation extended to the financial model. Traditional utility investors wanted steady dividends and predictable growth. But the energy transition required massive capital investment with uncertain returns. Entergy had to attract new investors—ESG funds, green bonds, sustainability-linked loans. The company that once sold bonds to local banks now accessed global capital markets with complex instruments tied to carbon reduction targets.

By 2024, Entergy's clean energy transformation was accelerating beyond initial projections. Renewable projects were coming online monthly. Nuclear plants were achieving record performance. Natural gas plants were being retrofitted for potential hydrogen or carbon capture. The company that began the decade as a traditional utility was becoming a clean energy platform. The question was no longer whether Entergy could achieve net-zero by 2050, but whether it could get there sooner—and whether the Gulf South's unique challenges would permit it.

X. Playbook: Business & Investing Lessons

The regulated utility model that Entergy perfected offers a masterclass in capitalizing on monopoly economics while navigating political constraints. The fundamental equation is elegant: regulators guarantee returns on invested capital, typically 9-11% on equity, in exchange for universal service obligations and rate regulation. This means every dollar spent on approved infrastructure generates predictable returns for decades. It's the closest thing to a perpetual bond that equity markets offer, but with growth potential that bonds lack.

Capital allocation in capital-intensive industries like utilities requires different thinking than asset-light businesses. Entergy routinely invests $3-4 billion annually—roughly 30% of revenues—in capital projects. These aren't venture bets hoping for 10x returns. They're infrastructure investments earning regulated returns for 30-40 years. The discipline required is extraordinary: every project must be justified to regulators, explained to investors, and accepted by customers who ultimately pay for it through rates.

Managing through catastrophic events has become Entergy's unique competency. While California utilities face bankruptcy from wildfire liability and Texas utilities collapsed during winter storms, Entergy has survived dozens of hurricanes, including multiple Category 4-5 storms. The secret isn't preventing damage—that's impossible. It's maintaining financial flexibility to handle $1-2 billion in restoration costs, operational capability to mobilize thousands of workers instantly, and political capital to secure regulatory recovery of storm costs. Resilience as competitive advantage sounds like consultant-speak until you've seen Entergy restore power to a million customers in six weeks.

Political and regulatory navigation across multiple states requires skills most businesses never develop. Entergy operates in four states with dramatically different political cultures: Arkansas (conservative, populist), Louisiana (oil-friendly, patronage-heavy), Mississippi (traditional Southern Democrat transitioning Republican), and Texas (business-friendly, deregulated). Each state commission has different priorities, procedures, and personalities. Success requires adapting message and method to local culture while maintaining operational consistency. It's like running four related but distinct businesses simultaneously.

Nuclear operations excellence represents perhaps the highest-stakes operational challenge in business. A single serious accident could destroy the company—financially, legally, reputationally. This creates a safety culture unlike anything in normal industry. Every procedure is documented. Every deviation is investigated. Every near-miss is treated as potential catastrophe. The paradox is that this extreme conservatism enables aggressive financial performance. Grand Gulf's 98% capacity factor doesn't happen despite the safety culture—it happens because of it.

The environmental leadership position Entergy has staked out—first utility to pledge holding greenhouse gas emissions to year 2000 levels, now targeting net-zero by 2050—isn't purely altruistic. It's recognizing that environmental leadership creates regulatory goodwill, attracts ESG investment, and positions the company for inevitable carbon pricing. Being early on climate action means influencing how rules are written rather than reacting to them. The $100+ million annual community investment similarly builds political capital that proves invaluable during rate cases or siting disputes.

The merchant nuclear misadventure offers crucial lessons about core competency and market dynamics. Entergy's nuclear expertise was real—they operated plants exceptionally well. But operating regulated nuclear plants in your home territory is fundamentally different from operating merchant plants in hostile political environments. The skills don't transfer. The relationships don't exist. The regulatory framework is different. Expanding beyond core competency isn't always wrong, but it requires honest assessment of what capabilities actually transfer.

Understanding regulatory lag and recovery mechanisms is essential for utility investing. Utilities spend capital today, file rate cases tomorrow, and recover costs years later. This creates systematic differences between accounting earnings and cash flow. During high investment periods, earnings lag cash flow. During harvest periods, the reverse. Investors who don't understand this cycle consistently misvalue utilities, seeing problems where none exist or missing real issues.

The value of optionality in long-lived assets is consistently underestimated. Grand Gulf was a disaster in 1985—billions over budget, unwanted by customers, fought by regulators. Today it's Entergy's most valuable clean energy asset. The option value of a licensed nuclear site with transmission connections and trained workforce is enormous in a carbon-constrained world. Similarly, transmission rights-of-way acquired decades ago now enable renewable integration. Patient capital in infrastructure creates options that become valuable in ways impossible to predict.

Weather risk as a permanent business factor distinguishes Gulf South utilities from peers. This isn't just about hurricanes, though those are most dramatic. It's about persistent heat driving summer demand peaks, humidity affecting equipment life, and flooding threatening infrastructure. Entergy's infrastructure must be built to different standards, maintained more frequently, and replaced more often. This shows up in higher capital intensity and O&M expenses that look excessive compared to utilities in benign climates but are essential for reliability.

The paradox of essential services is that being indispensable makes you a target. Everyone needs electricity, so everyone has opinions about how it should be provided, priced, and generated. Environmental groups attack your carbon emissions. Consumer advocates challenge your rates. Industrial customers demand special deals. Politicians grandstand during outages. The only defense is operational excellence—keeping rates reasonable, reliability high, and maintaining stakeholder trust through transparent communication and consistent execution.

Transformation within regulatory constraints requires patience and creativity. Entergy couldn't just decide to exit merchant nuclear—it took a decade of careful negotiations. They can't just build renewables everywhere—each project needs regulatory approval. They can't adjust rates dynamically—changes require lengthy proceedings. But within these constraints, massive transformation is possible. The company that was 50% coal in 2000 will be net-zero carbon by 2050. The lesson: regulated industries can transform, just not quickly or unilaterally.

XI. Analysis & Bear vs. Bull Case

Bull Case:

The essential service provider thesis remains compelling. Electricity is the oxygen of modern civilization—demand only grows more inelastic as digitalization accelerates. Entergy's monopoly across the Gulf South isn't just regulatory—it's practical. No competitor will duplicate thousands of miles of transmission lines and distribution networks. The capital barriers are insurmountable. The regulatory moat is permanent. This is as close to an unassailable business position as exists in modern capitalism.

The Gulf South industrial renaissance is real and accelerating. The Infrastructure Investment and Jobs Act is driving massive federal investment into the region. The Inflation Reduction Act incentivizes clean industrial development along the Mississippi River. Petrochemical companies are reshoring production from China. LNG export facilities are proliferating along the Louisiana coast. Each project needs reliable, affordable power—exactly what Entergy provides. The data center opportunity alone could drive 5-10% annual demand growth.

Nuclear fleet advantage becomes more valuable each year. As renewable penetration increases, the need for carbon-free baseload intensifies. Natural gas faces increasing carbon constraints. Coal is politically and economically dead. But nuclear provides 24/7 carbon-free power at predictable costs. Entergy's 5,000 MW of nuclear capacity, with licenses extending to the 2040s, represents irreplaceable clean energy infrastructure. In a world where new nuclear construction remains challenging, existing plants are golden assets.

Hurricane response capabilities, perversely, strengthen Entergy's position. Each successful restoration builds political capital and customer loyalty. The company has proven it can handle Category 5 hurricanes, restore power to millions, and maintain financial stability. Climate change makes hurricanes more frequent and severe, but Entergy has adapted faster than the storms have intensified. The expertise in extreme weather response is a competitive advantage no competitor can replicate.

The dividend story remains attractive. Entergy has paid dividends continuously since 1988, growing them at 6% annually over the past decade. The regulated utility model provides cash flow visibility that supports consistent dividend growth. With a payout ratio around 60%, there's room for continued increases. In a world of zero interest rates and volatile equity markets, a utility yielding 4% with 6% growth is compelling. The tax-advantaged nature of utility dividends (return of capital component) enhances after-tax returns.

Bear Case:

Hurricane exposure in the climate change era represents existential risk. Katrina cost $2 billion. Ida cost $3 billion. The next Category 5 direct hit on New Orleans could cost $5 billion or more. Insurance covers some damage but not all. Regulatory recovery mechanisms exist but take years. Meanwhile, the company must fund restoration immediately. A hurricane season with multiple major storms could strain even Entergy's robust balance sheet. Climate change isn't just making storms stronger—it's making them weirder, less predictable, harder to prepare for.

Regulatory lag and political uncertainties intensify as populism rises. Every rate increase faces political opposition. Social media amplifies outrage over executive compensation or storm response. Regulators, facing election pressures, may deny prudent cost recovery or mandate uneconomic investments. The regulatory compact that protected utilities for a century shows cracks. Louisiana's complex politics, Mississippi's poverty, Arkansas's populism—each creates unique regulatory risks that compound rather than diversify.

Aging infrastructure requiring massive capital investment pressures all financial metrics. Much of Entergy's system dates from the post-war boom. Wooden poles from the 1960s, transformers from the 1970s, transmission lines from the 1980s—all need replacement. The grid modernization necessary for renewable integration adds billions more. This capital intensity pressures customer rates, regulatory relationships, and credit metrics simultaneously. The investment need is accelerating faster than depreciation schedules assumed.

Renewable disruption and distributed generation threaten the fundamental utility model. Rooftop solar with battery storage allows customers to defect from the grid partially or completely. Every lost kilowatt-hour spreads fixed costs across fewer units, raising rates and encouraging more defection—the utility death spiral. Entergy's Gulf South territory has less solar potential than California or Arizona, but technology improvements and cost reductions make distributed generation increasingly viable even in less optimal locations.

Gulf South economic dependence creates concentration risk. Entergy's fortune is tied to four states that consistently rank near the bottom in education, health, and economic development metrics. Young educated workers leave for Austin, Atlanta, or Nashville. Climate change makes the region less attractive—hotter summers, stronger hurricanes, increased flooding. If the Gulf South economy stagnates while the rest of America booms, Entergy's growth stalls. Geographic concentration that provides regulatory expertise also creates economic vulnerability.

The nuclear backend liability looms larger as plants age. Decommissioning costs are estimates—actual costs always exceed estimates. Spent fuel storage remains unsolved after 60 years of nuclear power. Entergy has $2 billion in decommissioning trusts, but cleaning up five nuclear sites could cost double that. The NRC requires financial assurance, but regulations can change. The company that benefits from nuclear operations today may face massive cleanup costs tomorrow.

Natural gas bridge strategy may become stranded. Entergy is investing billions in new gas plants as "transition" resources to support renewables. But if carbon prices arrive sooner or higher than expected, these plants become stranded assets. The 30-year depreciation schedules assume gas remains viable through 2050. If social license for fossil fuels evaporates like it did for coal, Entergy faces write-downs and stranded cost battles. The bridge to clean energy might not reach the other side.

Talent acquisition and retention challenges intensify. Utilities aren't sexy employers for top engineering or technology talent. The headquarters in New Orleans, while culturally rich, doesn't attract like Austin or Seattle. The workforce is aging—average line worker is 50+. Training replacements takes years. Meanwhile, the energy transition requires new skills—data science, renewable integration, customer experience. Entergy must transform its workforce while competing against tech companies with higher pay and cooler brands.

XII. Epilogue & "If We Were CEOs"

If we were running Entergy, the strategic priorities for the next decade would begin with a radical reimagination of nuclear's role. Grand Gulf's success proves existing nuclear can thrive, but the real opportunity lies in small modular reactors (SMRs). Entergy should leverage its nuclear expertise and regulatory relationships to become America's first SMR deployer at scale. Partner with NuScale or TerraPower. Convert retiring gas plant sites to SMR installations. The first mover in next-generation nuclear captures decades of competitive advantage.

Nuclear life extensions versus new renewable investments isn't an either/or decision—it's both/and with careful sequencing. Extend every nuclear license to 80 years where technically feasible. The marginal cost of life extension is fraction of new build anything. Simultaneously, accelerate renewable deployment but focus on hybrid projects—solar plus storage, wind plus hydrogen production. Pure renewable plays are commoditizing. Integrated clean energy systems that provide reliability command premium value.

Grid resilience versus affordability tradeoffs require new thinking about risk allocation. Not every customer needs or wants hurricane-proof power. Offer reliability tiers: basic service with standard restoration times, premium service with priority restoration, and critical service with backup generation. Let customers choose their risk tolerance rather than socializing all resilience costs. This customer choice model aligns costs with benefits while maintaining universal service obligations.

The data center opportunity demands dedicated strategy. Create Entergy Digital—a subsidiary focused exclusively on hyperscale data center customers. Offer integrated packages: land, power, cooling, fiber connectivity. Partner with data center developers to create powered shells ready for rapid deployment. The Mississippi River corridor could become America's next data center hub if infrastructure is ready. Speed to market matters more than price for these customers.

Climate adaptation strategies must embrace rather than resist reality. The Gulf Coast will face more extreme weather. Rather than hardening everything—impossibly expensive—create adaptive infrastructure. Design systems that fail gracefully and restore quickly. Pre-position modular substations that can replace damaged equipment in hours not weeks. Develop floating solar that rises with floods. Build community microgrids that island during storms. Resilience through flexibility beats hardening through concrete.

Regulatory innovation could unlock enormous value. Propose performance-based rates that reward reliability and carbon reduction rather than capital investment. Create regulatory sandboxes for testing new technologies and business models. Push for regional transmission planning that enables optimal renewable resource development. The utility that helps regulators reimagine regulation shapes its own future.

The human capital transformation requires revolutionary approach. Partner with universities to create Entergy University—a degree-granting institution focused on energy transition skills. Guarantee jobs for graduates. Fund full scholarships for local students. This isn't corporate training—it's building the workforce for the entire region's energy transition. The talent pipeline becomes competitive advantage and community investment simultaneously.

Financial engineering should match operational transformation. Issue catastrophe bonds for hurricane risk transfer. Create yield vehicles for renewable assets. Develop carbon removal credits from nuclear operations. The financial innovation that funded railroad expansion and electrification can fund energy transition. Entergy's stable cash flows and essential service nature enable structures other companies can't access.

The ultimate strategic vision: Entergy as the platform enabling the Gulf South's economic renaissance through clean, reliable, affordable energy. Not just keeping lights on but powering industrial transformation. Not just serving customers but creating community prosperity. Not just surviving hurricanes but thriving through adaptation. The company that began with sawdust and entrepreneurial vision can lead America's energy transition from the region most threatened by climate change.

The next decade will determine whether Entergy remains a regional utility or becomes something more—a model for how essential infrastructure adapts to existential challenges. The pieces are in place: irreplaceable nuclear assets, hurricane-tested operations, modernizing infrastructure, supportive regulation, growing demand. The question is whether management can execute the transformation while maintaining the operational excellence that has sustained the company for 110 years.

Harvey Couch's vision of bringing power to the powerless remains relevant, just radically reimagined. Today's powerless aren't just those without electricity but those without clean electricity, reliable electricity, affordable electricity. Entergy's mission isn't complete when everyone has power—it's complete when that power enables prosperity without destroying the planet. That's a century-long project worthy of a century-old company. The next chapter of Entergy's story is being written now, in boardrooms and control rooms, in regulatory hearings and storm centers, by engineers and line workers who understand that keeping the lights on in the Gulf South isn't just a business—it's a calling.

XIII. Recent News

Fortune magazine recognized Entergy among the top utilities on its World's Most Admired Companies list for 2025. For full year 2024, the company reported earnings of $1,056 million, or $2.45 per share, on an as-reported basis, and $1,577 million, or $3.65 per share, on an adjusted basis. The company's financial performance demonstrated resilience and growth, achieving adjusted EPS in the top half of guidance for the ninth consecutive year.

Major strategic developments in 2024-2025 include significant progress on renewable energy deployment and data center customer acquisition. E-MS broke ground on the 754-megawatt Delta Blues Advanced Power Station. MISO approved 2024 MTEP that includes $1.7 billion of capital projects for Entergy utilities. CEO Drew Marsh highlighted key business milestones including: new electric service agreements with hyperscale data center customers in Mississippi and Louisiana, deployment of over 700 megawatts of solar resources, and a $153 million economic impact through corporate social responsibility initiatives.

Looking forward, Entergy initiated its 2025 adjusted earnings per share guidance range of $3.75 to $3.95. The company plans to invest $37 billion through 2028 to support growth, reliability, and resilience in the Gulf South region. This massive capital program reflects both the tremendous growth opportunities in the service territory and the ongoing need for grid modernization and climate resilience.

Regulatory developments continue to shape the business environment. Entergy Texas received approval to place $137 million of transmission investments into rates through the TCRF rider. The state of Arkansas passed legislation to allow recovery for certain generation and transmission investments outside of the formula rate plan four percent cap. These approvals demonstrate continued regulatory support for necessary infrastructure investments.

The company executed a two-for-one forward stock split effective December 13, 2024, reflecting strong stock performance and making shares more accessible to retail investors. The company also strengthened its credit metrics in 2024. The focus on financial strength positions Entergy well for the substantial capital investment program ahead while maintaining investment-grade credit ratings.

XIV. Links & Resources

Company Resources: - Investor Relations: investors.entergy.com - Annual Reports & SEC Filings: Available through EDGAR database - Sustainability Reports: Published annually as "Performance Report" - Historical Archives: Entergy corporate history documentation

Regulatory Resources: - Federal Energy Regulatory Commission (FERC): ferc.gov - Arkansas Public Service Commission - Louisiana Public Service Commission - Mississippi Public Service Commission - Public Utility Commission of Texas - Nuclear Regulatory Commission: nrc.gov

Industry Analysis: - Edison Electric Institute: Industry statistics and reports - Nuclear Energy Institute: Nuclear industry data and advocacy - Energy Information Administration: Federal energy statistics

Historical References: - "We Power Life: Entergy's First Century" by Heidi Tyline King - Harvey Couch papers at Arkansas State Archives - Middle South Utilities historical documents - Hurricane Katrina response archives

Academic Studies: - Utility regulation and rate-making principles - Nuclear power economics and safety studies - Climate change impacts on Gulf South infrastructure - Energy transition pathways for regulated utilities

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube