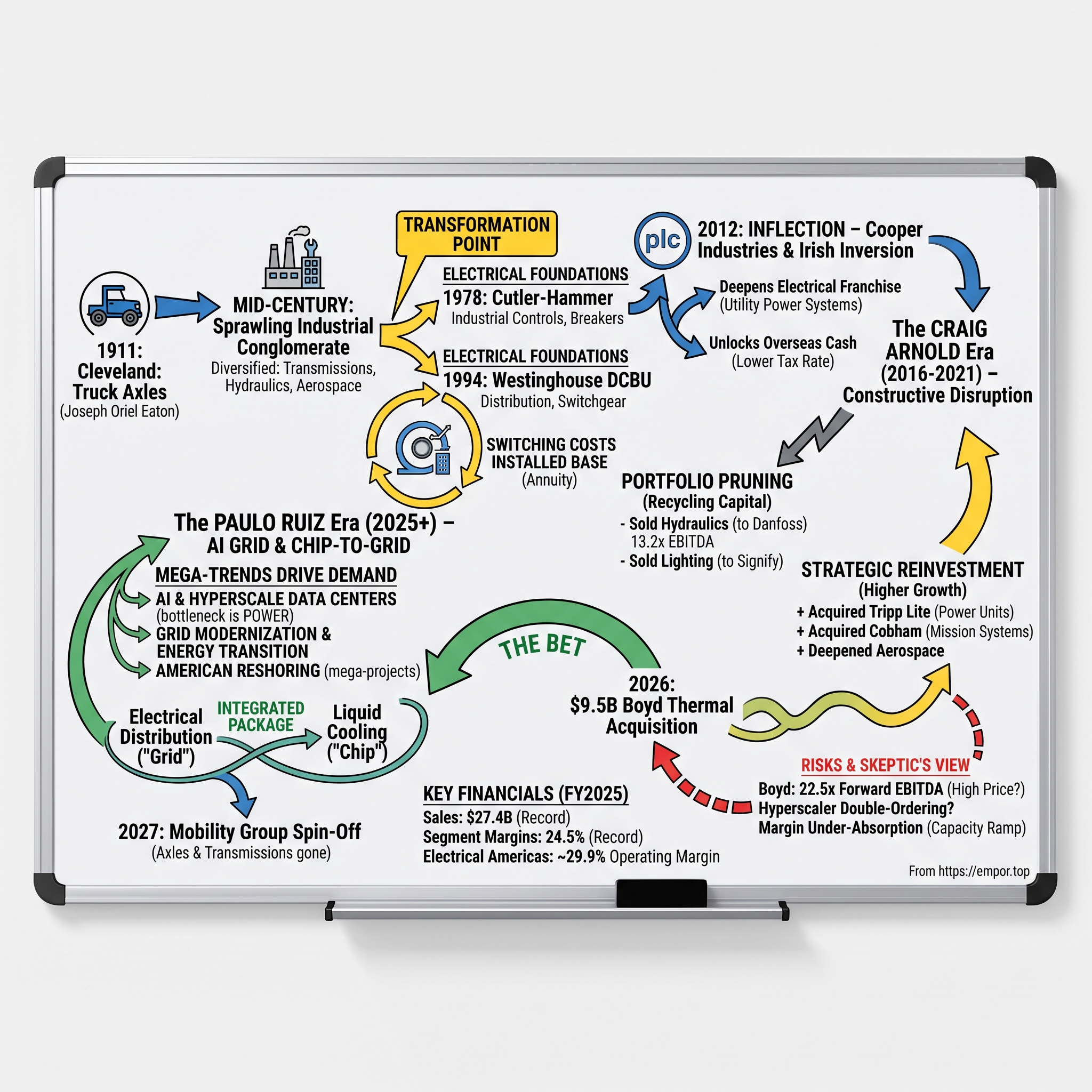

Eaton Corporation: From Cleveland Axles to the Spine of the AI Grid

There is a particular kind of company that hides in plain sight. It doesn't make the chip everyone talks about, or the model that writes the poetry, or the app on your phone.

It makes the unglamorous stuff in between — the breakers, the busways, the switchgear, the transformers — the plumbing through which electrons must physically travel before an artificial-intelligence cluster can do anything at all. For most of the last century, this was a sleepy, cyclical, low-multiple corner of the industrial economy.

And then, almost overnight, the world discovered that the single hardest thing about building an AI data center is not the silicon. It is getting enough power to the silicon, and getting the heat back out.

That realization turned a 115-year-old truck-axle maker from Ohio into one of the most important "picks-and-shovels" suppliers of the AI era. This is the story of how Eaton Corporation plc got there — and, just as importantly, an independent look at whether the story holds up under pressure.

I. Introduction & Episode Roadmap

Picture the boardroom framing of the pitch. How did a company founded in 1911 to make heavy axles for the first generation of American trucks — a business as physical and old-economy as it gets — quietly reposition itself as a critical supplier behind the largest capital-investment cycle of the twenty-first century?

The short answer is that Eaton spent a hundred years learning how to bend metal profitably, and the last fifteen deliberately re-pointing that capability at electricity instead of horsepower.

Today Eaton is not an industrial afterthought.

It reported record full-year 2025 sales of $27.4 billion, up 10% over 2024, with record segment margins of 24.5%.[^1] Its largest business, Electrical Americas, earned a roughly 29.9% operating margin for the full year — the kind of profitability that software investors associate with subscriptions, not with steel enclosures full of copper.[^1]

The market has re-rated the stock accordingly, pushing Eaton's equity value well into the hundreds of billions and placing it in the same conversation as the semiconductor names it quietly supplies.

The central theme of this episode is not "AI winner." It is capital allocation as a competitive weapon. Eaton's real edge over the last decade has been a willingness to sell perfectly good, cash-generative legacy businesses at the top of their multiple and recycle the proceeds into higher-growth, higher-margin electrical franchises — a philosophy management came to call "constructive disruption."

The most vivid recent examples bookend the transformation: the disciplined 2021 sale of the legacy Hydraulics business to Denmark's Danfoss at 13.2 times trailing EBITDA,[^4] and the far more aggressive $9.5 billion purchase of liquid-cooling specialist Boyd Thermal in March 2026 at roughly 22.5 times forward EBITDA.[^2]

One was selling low-growth cyclicality dear; the other was buying secular growth expensive. Whether that second trade proves as smart as the first is one of the open questions this piece will test rather than assume.

Why should a long-term investor care about a maker of breakers and busways rather than the AI companies themselves?

The picks-and-shovels logic is old but sound: during a gold rush, the miners face brutal competition and uncertain odds, while the person selling every miner their shovel does fine regardless of who strikes it rich.

The AI application layer is fiercely contested and its winners are unknowable; the electrical infrastructure underneath is supplied by a handful of entrenched players who get paid whether the AI models turn out to be revolutionary or merely useful. There is even a version of this argument in which the supplier is safer than the customer — because a data center must be powered and cooled before it can run a single model, the electrical spend comes first in the sequence and is harder to defer than the software bets it enables.

That is the seductive core of the Eaton thesis, and like all seductive theses it deserves to be tested rather than swallowed, which is what the back half of this piece will do.

The neutral posture matters here. This is not a shareholder letter, and Eaton's management, however capable, is not a neutral narrator of its own story. When the company says it will win, the useful question is always the same: what evidence supports that, and what would prove it wrong?

Order books can be padded, cycles can turn, and the most dangerous moment for any company is the one when the market has fully embraced its story — which is roughly where Eaton sits today.

Here is the roadmap. First, the Cleveland roots — truck axles, engine valves, and a mid-century conglomerate that could easily have died the slow death that killed General Electric's mystique. Second, the two bedrock electrical acquisitions, Cutler-Hammer in 1978 and Westinghouse's distribution unit in 1994, that gave Eaton its installed base.

Third, the 2012 Cooper Industries deal and the Irish tax inversion that reshaped the company structurally. Fourth, the Craig Arnold era and the pruning of the portfolio. Fifth, the "chip-to-grid" thesis and the secular tailwinds now driving the electrical business. Sixth, the segment-level financial reality and the Boyd Thermal bet.

Then the moat analysis, the playbook, the bull-and-bear stress test, and a close.

One housekeeping note that matters for how you read everything that follows: the man most associated with this transformation, Craig Arnold, is no longer running the company. He reached Eaton's mandatory retirement age of 65 and handed the CEO role to Paulo Ruiz on June 1, 2025.8

So this is also a story about succession — about whether a transformation built on one executive's discipline survives his departure, right at the moment the stakes have never been higher. Let's begin where Eaton began: with axles.

II. Century-Long Roots: Truck Axles to Electrical Foundations (1911–2011)

In 1911, a Detroit-born entrepreneur named Joseph Oriel Eaton bet that the internal-combustion truck was going to replace the horse-drawn wagon, and that whoever supplied the drivetrain guts of those trucks would ride the wave. He co-founded the Torbensen Gear and Axle Company, licensing an internal-gear rear axle that let heavy trucks carry more load, and moved the operation to Cleveland to be near the burgeoning auto industry.7

It was a classic first-principles supplier bet: don't build the vehicle, build the indispensable component every vehicle maker needs and few can make well.

That instinct — sell the shovels, not the gold — would echo across the next hundred years.

For most of the twentieth century Eaton grew into exactly the kind of company business-school professors would later warn against: a sprawling, multi-divisional industrial conglomerate.

Truck transmissions and clutches. Engine valves. Superchargers. Hydraulics. Aerospace fluid systems. By the 1970s it was a respectable, diversified maker of mechanical things, deeply cyclical, tied to the fortunes of Detroit and the broader capital-goods economy.

In another timeline, that Eaton becomes a slow-motion casualty of the same forces that hollowed out the American industrial conglomerate — the model that made GE a colossus and then, decades later, made its breakup a cautionary tale.

What saved Eaton was an early and, in hindsight, prescient pivot into electrical power. The first bedrock move came in 1978, when Eaton acquired Cutler-Hammer, a storied maker of industrial controls, circuit breakers, and electrical distribution equipment.7 Overnight, a company that mostly knew torque and gears owned a real foothold in the business of controlling and distributing electricity inside factories and buildings.

It was a different kind of metal-bending — enclosures, contacts, breakers — but it came with something axles never had: an installed base that needed servicing, upgrading, and replacing for decades.

The second and more consequential move came in 1994, when Eaton paid roughly $1.1 billion for Westinghouse Electric's Distribution and Control Business Unit — the DCBU.7 This is the moment a careful observer would circle as the true origin of modern Eaton. Westinghouse was one of the founding names of American electrification, and its distribution business meant breakers, panelboards, switchgear, and motor controls physically embedded in commercial buildings, utilities, and industrial sites across North America.

By folding Westinghouse's distribution franchise together with Cutler-Hammer, Eaton assembled something that is far harder to build than any single product: a continent-spanning installed base of electrical equipment that owners would keep buying parts and upgrades for, year after year.

Here is why that mattered strategically, and it is a point worth dwelling on because it explains the economics of the company to this day. In electrical distribution, the equipment is spec'd into a building's design and then lives in that building for twenty, thirty, sometimes forty years.

When a breaker fails or a panel needs expansion, the facility manager does not run a fresh competitive bake-off — they buy the part that fits the existing gear, from the brand already installed.

Eaton spent the following years consolidating the Cutler-Hammer and Westinghouse names under the single Eaton brand while preserving that replacement-part compatibility.7 The effect was a quiet, durable annuity: an installed base that generates recurring, high-margin aftermarket demand and locks customers into the ecosystem without a single line of software. It is switching cost in its most physical, least fashionable form.

What Eaton was actually selling

It is worth pausing to translate what "electrical distribution equipment" means in physical terms, because the whole investment case rests on it and the jargon obscures a simple idea. When power arrives at a building or a factory from the utility, it cannot be used as delivered — it is too high a voltage and it needs to be split, controlled, and protected. Switchgear is the heavy metal cabinet, full of circuit breakers, that acts as the traffic cop for all that electricity, routing it to different parts of the facility and cutting it off instantly if something goes wrong.

A busway is essentially a rigid metal highway for electrons — an enclosed bar of copper or aluminum that carries large currents along a ceiling or wall far more efficiently than bundles of cable.

Panelboards and breakers are the smaller subdivisions of the same idea, the descendants of the fuse box in a home basement scaled up to industrial loads.

None of this is glamorous, and that is precisely the point. This equipment is engineered to a building's specific requirements, installed once, and expected to run for decades in the background, invisible until it fails. It is a business of trust and reliability, not novelty — the customer is buying the confidence that the lights and the machines will never go dark.

That is why brand and installed base matter so much more here than in a commodity product, and why the Cutler-Hammer and Westinghouse names carried value long after the companies behind them had been absorbed. When you have wired the country's buildings for a century, you own something a new entrant cannot conjure: the default choice.

By the end of the 2000s, Eaton was a genuinely diversified industrial with a large and growing electrical franchise sitting alongside its legacy vehicle, hydraulics, and aerospace businesses. It had survived the century that killed off many of its peers. But it was still, in the market's eyes, a "diversified industrial" — a conglomerate discount waiting to happen, valued on the cyclical earnings of its weakest divisions rather than the annuity economics of its best.

Fixing that perception would require both a structural change and a change of heart about what Eaton wanted to be. The structural change came first, in 2012, and it was as much about tax law as it was about electricity.

III. The Inversion Inflection: Cooper Industries & The Tax Gamble (2012)

To understand the boldest deal in Eaton's modern history, you have to understand how badly the U.S. tax code of the early 2010s punished an American multinational. In 2012, Eaton was domiciled in the United States, facing a headline federal corporate rate near 35% and, worse, a system that taxed foreign profits again when brought home — a double-taxation drag that left billions of dollars of overseas cash effectively trapped, unable to be repatriated and reinvested without a punishing toll.1

European rivals like Schneider Electric and ABB operated under far friendlier regimes. For a company that wanted to go acquire its way into a bigger electrical future, that structural disadvantage was a millstone.

Enter Cooper Industries. Cooper was a highly complementary electrical-equipment company, home to a roster of blue-chip brands — Crouse-Hinds explosion-proof fittings, Bussmann fuses, B-Line support systems, and a utility-facing power-systems portfolio of transformers and switchgear.1 Crucially for the mechanics that follow, Cooper had already reincorporated in Ireland years earlier. It was, in other words, the perfect target: it deepened Eaton's electrical franchise on the product side and, by virtue of its Irish domicile, it offered a path out of the U.S. tax trap.

The deal, announced in May 2012 and completed on November 30, 2012, was a cash-and-stock transaction valued at roughly $13.2 billion.1

Cooper shareholders received $39.15 in cash plus 0.77479 Eaton shares for each Cooper share.1 The combined company was reincorporated in Ireland as Eaton Corporation plc — the "plc" that has trailed the name ever since. This was a corporate tax inversion in the textbook sense: a U.S. company using a foreign acquisition to move its legal domicile abroad and shed the burdens of the American worldwide-taxation system.

Management was refreshingly candid about the arithmetic. Eaton's leadership acknowledged that the transaction would not have been economically feasible without the tax structure the Irish domicile enabled.1 Read that plainly.

A meaningful chunk of the deal's value creation came not from synergies or growth but from tax geography.

The inversion slashed Eaton's global effective tax rate and, just as importantly, freed up offshore cash that could now be deployed into acquisitions and buybacks without the repatriation penalty.

For a company whose entire future strategy would hinge on recycling capital from old businesses into new ones, unlocking that trapped cash was foundational.

Did Eaton overpay? The deal carried roughly a 15–20% premium in a market where Cooper had other suitors, so it was not a steal.1 But the strategic verdict, with the benefit of more than a decade of hindsight, is that this was a home run — and the tax angle is only half the reason. The deeper prize was Cooper's utility-side electrical portfolio: the transformers, fuses, and grid-level switchgear that plug into the power grid itself, not just into buildings.

That utility franchise would become extraordinarily valuable a decade later, when grid modernization and data-center power demand collided into one of the biggest infrastructure spending waves in American history. Eaton bought the shovel years before anyone knew where the gold rush would be.

Myth versus reality: was Eaton just a tax dodge?

It is worth confronting the cynical version of this story head-on, because it circulated widely at the time and still colors how some investors view the company. The myth is that Eaton is fundamentally a tax-arbitrage vehicle — an American company that fled to Ireland to shave its tax bill, dressed up in the language of strategy.

The reality is more nuanced and, on balance, more favorable to Eaton. Yes, the Irish domicile was essential to the deal's math, and management said so plainly.1 But the Cooper acquisition also brought a genuinely valuable operating business — the utility-facing transformers, fuses, and grid switchgear that would prove central to the grid-modernization wave a decade later. A pure tax play buys the cheapest possible shell with the friendliest domicile; Eaton bought a strategic asset that happened to carry the domicile it needed.

The tax structure was the enabler, not the thesis.

The distinction matters because it predicts behavior. A company built on financial engineering keeps reaching for the next clever structure; a company built on operating assets compounds by improving and extending those assets. Everything Eaton did in the following decade — the pruning, the reinvestment, the operating discipline — points to the latter. The inversion looks, in retrospect, less like the whole plan and more like the key that unlocked the door.

There is a fair skeptic's footnote here worth flagging, because it speaks to management's willingness to be judged by results. Tax inversions were politically radioactive in the mid-2010s, drawing Treasury Department crackdowns and public criticism of companies that "renounced" their U.S. citizenship for tax savings.

Eaton absorbed that reputational cost, and the subsequent 2017 U.S. tax reform narrowed some of the inversion's relative advantage. But the domicile stuck, the cash was freed, and the electrical portfolio was in the building. What Eaton did with that combination over the following decade is where the story really turns — and it required a new CEO with a very specific philosophy about what to keep and what to sell.

IV. The Craig Arnold Era & "Constructive Disruption" (2016–2021)

When Craig Arnold became Eaton's chairman and CEO in June 2016, he inherited a company that was structurally global, financially sound, and strategically unfocused.8 Arnold was not a typical machine-tools lifer. He had spent years at General Electric — that famous finishing school for American operating executives — before joining Eaton and running its Electrical sector, the crown jewel he understood better than anyone.3

He brought two things to the top job: a disciplined, continuous-improvement operating religion codified as the "Eaton Business System," and a conviction that the conglomerate model his generation had inherited was a value trap.

Arnold's central insight, which he articulated as "constructive disruption," was that diversification for its own sake had become a liability, not a strength.3 He watched GE — his old employer — dismantle itself under the weight of its own sprawl, and he watched Japan's Toshiba unravel. His conclusion was that staying "diversified and cyclical" was a slow path to a permanent conglomerate discount.

Eaton, he decided, should stop trying to be a little of everything and instead concentrate ruthlessly on becoming a focused, high-margin, secularly growing "intelligent power management" company. The word "intelligent" was doing real work: the future Arnold saw was electrical, digital, and structurally growing, not mechanical, analog, and cyclical.

The Eaton Business System

Before Arnold could reshape the portfolio, he leaned on an operating discipline that most outsiders never hear about but that quietly underpins the company's margins: the Eaton Business System, or EBS. In plain terms, EBS is Eaton's version of the continuous-improvement methodologies that companies like Toyota and Danaher made famous — a standardized set of processes for running factories, developing products, managing quality, and holding managers accountable to targets across a globally sprawling operation.

The value of such a system is not any single trick; it is consistency.

A company that operates dozens of plants on four continents needs a common language for how work gets done, or it fragments into a federation of fiefdoms, which is exactly the disease that hollows out conglomerates.

The reason EBS matters to an investor is that it is the mechanism behind a genuinely surprising fact: Eaton extracts software-like margins from a hardware business.

Bending metal, winding copper, and assembling breakers is not inherently a 30%-margin activity. Getting there requires relentless cost discipline, pricing rigor, and the ability to push productivity gains through the system year after year.

EBS is the closest thing Eaton has to a repeatable process advantage, and it is the reason Arnold could credibly promise that a more focused portfolio would also be a more profitable one. Skeptics rightly note that operating systems can be copied; the counter is that culture and execution discipline built over decades are far harder to replicate than a slide deck describing them.

The philosophy only means something if you act on it, and Arnold acted. Between 2020 and 2021, Eaton pruned two businesses that had been part of its identity for decades. In 2020, it sold its Lighting business to the Dutch company Signify for $1.4 billion — a high-volume operation that had been thoroughly commoditized by low-cost LED manufacturing, where competing on price against Asian producers was a race to the bottom.3

Getting out was an admission that scale and heritage do not save you in a commoditizing market; better to exit while the business still commanded a price.

The bigger and more symbolically loaded move came in 2021: the sale of the Hydraulics business to Denmark's Danfoss for $3.3 billion in cash.[^4] Hydraulics was old Eaton — a legacy core that traced back to the company's mechanical roots. But it was cyclical, capital-intensive, and lower-margin, and by Arnold's logic it no longer belonged.

What made the divestiture a case study in discipline was the price. Eaton sold Hydraulics at roughly 13.2 times its 2019 EBITDA — around $250 million of EBITDA on $2.2 billion of sales — a rich multiple for a cyclical industrial business.[^4]

The buyer, Danfoss, completed the deal in August 2021 to build scale in fluid power.2 For Eaton, the effect was twofold: it permanently lifted corporate margins by removing a lower-margin division, and it stripped a capital-hungry, highly cyclical asset off the balance sheet.

This is the clearest single illustration of the constructive-disruption trade — sell cyclicality dear, and free the capital.

That freed capital went straight back to work in businesses Arnold believed had secular wind behind them. In 2021, Eaton acquired Tripp Lite for $1.65 billion, buying its way into single-phase uninterruptible power supplies, power distribution units, and edge-computing power gear — precisely the equipment that keeps servers and small data closets running when the grid hiccups.[^5]

It was an early, if under-appreciated, down payment on the data-center thesis. The same year, Eaton paid $2.83 billion for Cobham Mission Systems, adding high-margin, defense-critical capabilities like air-to-air refueling systems to its Aerospace segment — a business riding both civil-aviation recovery and rising defense budgets.[^6]

Step back and the pattern is unmistakable. Sell Lighting and Hydraulics — commoditized and cyclical. Buy Tripp Lite and Cobham — secular and defensible.

Recycle low-multiple cash cows into higher-multiple growth franchises, and let the blended margin and growth profile of the whole company drift steadily upward. It is portfolio management as a discipline rather than a slogan, and for a stretch of years the market rewarded it with a re-rating from "industrial" toward "electrical growth compounder." The question Arnold could not have fully answered in 2021 was how large the tailwind he was leaning into would become. The answer arrived with the AI boom — and it was bigger than almost anyone forecast.

V. The "Chip-to-Grid" Masterclass: Riding the Secular Megatrends of the 2020s

For years, the knock on grid-and-electrical suppliers was that they sold into a mature, GDP-plus market — steady, dull, low-single-digit growth. Then three enormous spending waves arrived at roughly the same time and broke over the same set of products. Understanding why they converged is the key to understanding Eaton's re-rating, so it is worth taking each in turn, in plain language.

The first and loudest is AI and hyperscale data centers. Training and running large AI models requires racks of power-hungry chips packed together at densities the industry has never seen. A traditional data-center rack might draw a handful of kilowatts; an AI rack full of accelerators can draw ten or twenty times that. All that power has to be delivered, stepped down, distributed, protected, and metered — which means vastly more breakers, busways, switchgear, and power-distribution units per building.

The bottleneck for building AI capacity, executives across the industry now concede, has shifted from land and even from chips to raw electrical power availability.

On Eaton's own calls, management has described a data-center backlog measured not in dollars but in years of work: by the first quarter of 2026, roughly 228 gigawatts of data-center backlog, equivalent to about twelve years of construction at 2025 build rates.10 Whatever one thinks of the durability of the AI boom, the near-term demand signal for the physical power equipment is extraordinary.

To make the data-center opportunity concrete, it helps to walk through where Eaton's equipment physically lives inside one of these buildings, because "AI needs power" is too vague to be useful. Utility power enters the site at high voltage and hits Eaton's medium-voltage switchgear and transformers, which step it down and distribute it.

From there it flows through uninterruptible power supply systems — the big battery-backed units that bridge the gap during a grid outage so servers never lose power for even the fraction of a second that would crash a training run. That power then travels along busways and into rack-level power distribution units, the strips that feed individual servers. Industry insiders divide the building into "gray space," the electrical and mechanical rooms where the power and cooling gear sits, and "white space," the raised floors where the servers live.

Eaton sells into both, and into the utility substation feeding the site as well. Owning content at every one of those layers is what lets management talk about capturing millions of dollars of equipment per megawatt of capacity rather than winning a single box.

The reason AI specifically supercharges this is density. Because AI accelerators pack so much computing — and therefore so much power draw — into each rack, the electrical infrastructure per square foot of building goes up dramatically compared with a traditional cloud data center. More power per rack means more copper, more breakers, more UPS capacity, and more cooling, which is why the same physical footprint now carries several times the electrical content it did a decade ago. That is the mechanism turning a GDP-plus market into a structural growth market, and it is why a company that spent a century in slow-growth end-markets suddenly finds itself with a backlog measured in years.

The second wave is grid modernization and the energy transition. The North American electrical grid is old, and it was designed for a world of steady, one-directional power flow from big central plants. Now it has to absorb volatile, intermittent solar and wind, handle two-way flows from rooftop panels and batteries, cope with more extreme weather, and serve surging demand from electrification and — again — data centers.

That requires enormous investment in smart switchgear, substation transformers, protective relays, and digital power meters. This is precisely the utility-facing portfolio Eaton acquired with Cooper Industries a decade earlier, now sitting in exactly the right place at exactly the right time.

The third wave is the reshoring of American manufacturing. Government programs like the CHIPS Act and the Inflation Reduction Act, along with a broader corporate rethink of supply-chain resilience, have triggered a wave of multi-billion-dollar "mega-projects" on North American soil: semiconductor fabs, EV battery gigafactories, and large-scale industrial plants.

The Financial Times has chronicled a mega-project pipeline running into the trillions of dollars.6 Every one of those factories is, from Eaton's perspective, an enormous electrical order — and these are greenfield sites where a supplier can win the entire electrical specification rather than fight over replacement parts.

Now to the crown jewel that captures all three waves: Electrical Americas. In 2025 this single segment generated net sales of $13,276 million — nearly half of Eaton's total corporate revenue — and produced a segment operating profit of $3,972 million, a record margin of roughly 29.9%.[^1]

Let that margin sink in. This is a business that manufactures heavy physical equipment — steel, copper, enclosures — and yet earns a margin that would make many software companies content. That is not normal for metal-bending, and it tells you something important: Eaton is not a price-taking commodity manufacturer here. It is capturing genuine pricing power and structurally advantaged economics.

Where does that advantage come from? The single most important concept is what one might call the specification moat. Long before a data center or a semiconductor fab is ever built, the electrical design engineers on the project specify the physical form factors, breaker ratings, busway layouts, and control systems of the electrical supplier.

Once Eaton's equipment is written into the drawings and the building is engineered around it, swapping it out is not a simple procurement decision — it means re-engineering, re-permitting, and risking months of costly commissioning delays on a project where every week of delay is enormously expensive. Getting spec'd in early converts a one-time sale into multi-year visibility and pricing leverage, because by the time the customer might want to shop around, the cost of switching has become prohibitive.

There is a digital layer on top of all this hardware that deserves its own mention, because it is where the "intelligent" in intelligent power management is supposed to live. Eaton's Brightlayer software platform sits over the physical equipment and lets operators monitor, analyze, and manage their power infrastructure — think of it as the dashboard and nervous system for a facility's electrical guts, tracking loads, predicting failures, and optimizing energy use. The strategic point of a software layer is stickiness: once a data-center or utility operator runs its operations on Brightlayer, the switching cost is no longer just the physical pain of swapping breakers but the operational pain of retraining people and re-integrating systems.

It is worth being appropriately skeptical here, though. Every major electrical player — Schneider with EcoStruxure most prominently — is racing to build the same kind of platform, and industrial software has a long history of being announced more impressively than it is adopted.

Brightlayer strengthens the moat at the margin; it is not yet proven to be the decisive advantage the marketing implies.

Of course, Eaton does not have this field to itself. The competitive landscape is a genuine oligopoly of formidable players. Schneider Electric, the French champion, is arguably the global leader by breadth, with an estimated low-double-digit share of the global market and a powerful EcoStruxure digital platform layered on top of its hardware. ABB, the Swiss-Swedish giant, is dominant in medium-voltage utility connections and global industrial applications. Siemens and Legrand compete hard in building automation and low-voltage distribution.

It is worth sizing these rivals honestly rather than waving at them, because the "monopoly" framing that gets attached to Eaton in bullish commentary is an overstatement. Schneider Electric is larger than Eaton in total revenue and has spent years building EcoStruxure into one of the most widely deployed industrial-software platforms in the world; it is not a laggard Eaton is out-innovating, but a peer running the same playbook with comparable resources.

ABB brings deep strength in the medium-voltage and utility layer and a global installed base of its own. Siemens carries the weight of one of the most respected engineering brands on earth into building automation and low-voltage distribution. And in the specific data-center-cooling fight that the Boyd deal was meant to win, Vertiv is a focused, fast-growing pure-play that many customers already know well. Eaton competes credibly against all of them, and in North American electrical it may well be the strongest single player — but "strongest in a rational oligopoly" is a very different claim from "monopoly," and conflating the two is how investors talk themselves into paying too much.

This is not a monopoly, and any honest analysis has to reckon with the fact that Eaton's most valuable market is contested by well-capitalized, technically excellent rivals. What tilts the field in Eaton's favor in North America specifically is the combination of its installed base, its manufacturing footprint on the continent, and the switching costs baked in once its switchgear and its Brightlayer control software are architected into a mission-critical facility. The moat is real, but it is a moat against a handful of equally serious castle-builders, not against open country. That competitive reality — and the price Eaton was willing to pay to widen the moat — sets up the most controversial capital-allocation decision of the new era.

VI. Financial Mechanics: Segment Realities & The $9.5B Boyd Thermal Bet

Before dissecting the headline-grabbing acquisition, it helps to see the whole company as it actually is, because narrative and materiality can drift apart. Eaton reports in five segments, and their economic weights are wildly different — a fact worth internalizing so that the exciting small businesses do not distort the picture.

Electrical Americas, already discussed, is the giant: $13,276 million of 2025 sales and $3,972 million of profit at that ~29.9% margin.[^1] Electrical Global is the next largest at $6,815 million of sales and $1,323 million of profit, a roughly 19.4% margin — the grid, utility, and commercial-project business outside the Americas, structurally lower-margin because of geographic and project mix but still a healthy franchise.[^1]

Aerospace contributed $4,249 million of sales and $1,013 million of profit at about 23.8%, riding civil-aviation backlogs and elevated defense spending.[^1]

This is an underappreciated jewel in the portfolio and deserves more than a passing mention. Aerospace electrical, hydraulic, and fluid systems sit on commercial jets and military platforms that fly for decades, and — much like the electrical installed base — they generate high-margin aftermarket revenue every time a part is serviced or replaced.

The Cobham Mission Systems acquisition deepened Eaton's position in defense-critical niches such as air-to-air refueling, a business insulated from consumer cycles and buoyed by rising global defense budgets.

With the commercial-aviation recovery driving record aircraft backlogs at Boeing and Airbus and defense spending elevated by geopolitical tension, Aerospace has become a quietly durable, second growth engine that will loom larger in the remaining company once the lower-margin Mobility businesses are gone.

Then come the two businesses that reveal where Eaton is heading. Vehicle — the direct descendant of that 1911 axle company — generated $2,505 million of sales and $419 million of profit at roughly 16.7%, down from $2.79 billion of sales in 2024.[^1] It is cash-generative but structurally shrinking, tied to the ongoing decline of internal-combustion transmissions and engine valves.

And eMobility, the speculative EV-powertrain-components business, produced just $604 million of sales — about 2.2% of the company — and an operating loss of $14 million.[^1] It is important to size eMobility honestly: it is a small, unprofitable option on an electrified-vehicle future, not a pillar of the investment case, and any analysis that lets its exciting label crowd out the segments that actually pay the bills is telling you a story rather than reading the financials.

Management appears to agree, and that led to a strategically clarifying decision that the earlier framing of Eaton's portfolio did not anticipate. On January 26, 2026, Eaton announced it would spin off its Vehicle and eMobility segments — together branded the "Mobility Group" — into an independent, publicly traded company, with completion targeted by the end of the first quarter of 2027.9 CEO Paulo Ruiz framed it as advancing Eaton's "bold new 2030 growth strategy to lead, invest and execute for growth," giving Mobility its own capital and focus, while leaving the remaining Eaton concentrated on electrical and aerospace.9

Read through the corporate language, this is constructive disruption applied to the founder's own business: Eaton is preparing to jettison the axle-and-transmission heritage that started it all in order to become an almost pure-play electrical-and-aerospace company. That is a remarkable act of institutional self-editing, and it removes a cyclical, lower-margin, slower-growth drag from the story — while also, fairly, removing a source of diversification and steady cash.

There is something almost poetic about the decision, and it is worth sitting with for a moment because it captures the whole ethos of the company. The Vehicle business is not a random appendage; it is the lineal descendant of the 1911 axle company, the thing Joseph Eaton actually founded.

For a company to spin off its own origin — to say, in effect, that the business that gave us our name no longer fits the future we are building — requires a kind of unsentimental clarity that most organizations never achieve.

Sentiment is exactly what traps conglomerates: managers protect legacy divisions because of what they once meant rather than what they now earn. Eaton's willingness to cut the cord on its founding business is the strongest possible signal that the constructive-disruption philosophy is genuine rather than a slogan. The bear's rejoinder is that shedding steady, cash-generative, counter-cyclical businesses to concentrate everything on a single hot end-market is precisely how a company maximizes both its upside and its fragility — a more focused Eaton is a more powerful Eaton in a boom and a more exposed one in a bust. Focus cuts both ways, and the spin-off makes the bet on electrical demand less hedged, not more.

Why liquid cooling suddenly matters

To appreciate the Boyd bet, you have to understand why the cooling problem became existential almost overnight. For most of computing history, data centers were cooled with air — big fans and chillers pushing cold air across the servers, the same idea as the fan in a laptop, just industrialized. Air works fine up to a point. But AI accelerators concentrate so much power into such a small area that they generate more heat than moving air can carry away; past a certain density, an air-cooled rack simply cooks itself.

The solution the industry has converged on is liquid cooling — running coolant directly to the hottest components through cold plates and manifolds, because liquid absorbs and transports heat far more effectively than air, it is the same reason a car engine uses coolant rather than a fan alone.

This is not a nice-to-have accessory; for the highest-density AI hardware it is a gating requirement, which means the company that supplies the cooling is no longer a peripheral vendor but a co-equal to the company supplying the power. That reframing is the entire strategic logic of Boyd. Historically, an electrical company sold the power side and a separate specialist sold the thermal side, and the data-center operator stitched them together. By owning both, Eaton can offer an integrated package and, more importantly, make it harder for a rival to win the whole job.

Which brings us to the deal that dominates the current debate. On March 12, 2026, Eaton completed the acquisition of Boyd Thermal from Goldman Sachs Asset Management for $9.5 billion in cash — about $9.55 billion net of cash acquired.[^2]4 The strategic logic is elegant and follows directly from the power-density problem. Those AI chips that demand so much electricity also generate enormous heat, and air cooling can no longer keep up; the industry is moving to liquid cooling, piping coolant directly to the chips. Boyd is a leader in exactly that technology, with an estimated $1.7 billion of 2026 revenue and nearly 90% of it tied to liquid cooling.[^2]

By owning both the electrical distribution ("grid") and the liquid cooling ("chip"), Eaton can now sell an integrated "chip-to-grid" package, and management estimates its content per megawatt of data-center capacity approaches $3 million post-acquisition.[^2]

The deal folded Boyd into the Electrical Global segment.

Now the uncomfortable question every serious investor should ask: did Eaton overpay? At roughly 22.5 times estimated 2026 adjusted EBITDA, this was not a bolt-on bargain.[^2] It was a full, growth-priced number.

There are two ways to read the multiple. The bullish read is peer comparison: the pure-play liquid-cooling and data-center-infrastructure specialist Vertiv has traded at a forward EV/EBITDA in the mid-30s to low-50s in 2026, and nVent in the mid-teens to mid-20s — against which 22.5x for a market leader in a scarce, fast-growing capability looks defensible, even cheap relative to the highest-flying comp.

The bearish read is that Eaton paid a private-equity seller a top-of-cycle price for a business whose growth assumes the AI capex wave continues unabated, and did so with debt, at the precise moment margins were already under pressure from other investments.

Both reads contain truth, and it is worth naming what the deal reveals about management rather than adjudicating it prematurely. Boyd is a clear break from Craig Arnold's prior narrative of strictly disciplined, conservative bolt-on M&A. It is a large, debt-funded, aggressively priced bet made by a new CEO in his first year, at a cyclical high, in a category where the acquirer had limited prior presence.

That does not make it wrong — the strategic fit in liquid cooling is genuine, and controlling the thermal layer meaningfully raises the barrier for Vertiv and Schneider to offer a fully integrated solution. But it does mean Boyd should be judged on execution and returns, not on the strategic story alone. The best acquisitions and the worst both come wrapped in compelling narratives; the difference shows up years later in the numbers. That distinction — story versus proof — is exactly what the moat analysis has to grapple with next.

VII. Competitive Moats: Moat Analysis (7 Powers & 5 Forces)

Strip away the AI excitement and ask the durable question: what actually protects Eaton's economics from competition over a full cycle? Two frameworks help structure the answer — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — and the honest conclusion is that Eaton holds several real powers — but not all seven, and not without vulnerabilities.

Start with the strongest of Helmer's powers in Eaton's case: switching costs. As discussed, once Eaton's switchgear and its Brightlayer control software are engineered into a utility grid or a high-reliability data center, changing vendors is genuinely painful — it risks re-engineering, re-certification, and commissioning delays measured in months.

This is not marketing switching cost; it is physical and regulatory switching cost, the hardest kind to dislodge.

It is the same annuity dynamic that the Cutler-Hammer and Westinghouse installed base created — now supercharged by mission-critical facilities where even brief downtime is catastrophic.

The second power is scale economies. Eaton operates one of the broadest physical manufacturing networks in North America, which lets it secure supply chains, minimize shipping lead times, and localize capacity in ways that matter enormously when customers are desperate for equipment and delivery speed is a competitive weapon. In a market where lead times can stretch to a year or more, being able to deliver sooner is worth real pricing power. The third power is process power — the Eaton Business System, the continuous-improvement operating discipline that helps the company squeeze roughly 30% margins out of physical manufacturing.

Process power is the most fragile of the three to claim, because operating systems can be imitated over time, but the sustained margin record suggests it is real rather than rhetorical.

What Eaton does not clearly have is worth stating too, because a neutral analysis names the gaps. It does not have a decisive branding power of the consumer-luxury kind, nor a cornered resource, nor — critically — meaningful network effects.

Its competitors are not fringe players it can out-network; they are Schneider, ABB, and Siemens, each with their own scale and process advantages.

So the moat is best understood as a bundle of switching costs plus regional scale plus operating excellence, defended against a small number of peers — durable, but not impregnable.

Now the Five Forces, which sharpen the same picture. The threat of new entrants is extremely low: breaking into utility and data-center electrical equipment requires decades of distributor relationships (through the likes of Graybar and Wesco), grueling regulatory and utility field certifications, and — again — an installed base you cannot buy off the shelf.

The bargaining power of buyers is currently low-to-moderate and unusually favorable to Eaton — hyperscalers need power equipment urgently to bring AI capacity online, and with backlogs at record levels, Eaton holds real pricing leverage it would not enjoy in a slack market.

The important caveat is the phrase "currently": buyer power is cyclical, and a demand air-pocket would swing it back toward the customer.

The bargaining power of suppliers is moderate, driven by exposure to commodity inflation in copper and specialty steel; Eaton has largely offset this through structured price-escalation clauses that pass input costs down the chain, though that mechanism works better when demand is strong than when it is weak.

The threat of substitutes is low — there is no alternative to physically delivering high-capacity electricity and actively managing the heat it produces. And competitive rivalry is best described as a rational oligopoly: the major players compete on backlog lead times, engineering customization, and integrated solutions rather than on destructive price-cutting, which is why the whole industry earns attractive margins.

That rationality is itself an asset, but it depends on continued discipline; oligopolies that over-invest in capacity during a boom can turn rational pricing into a price war when demand cools — a risk that connects directly to the capacity buildout worrying analysts today. The lesson management would draw from all this leads naturally into the playbook.

VIII. Playbook: Business, Investing, and Capital Allocation Lessons

Every good business story leaves behind transferable lessons, and Eaton's transformation offers three worth extracting for any long-term investor — with the caveat that lessons drawn at the top of a cycle should be held with appropriate humility.

The first lesson is active portfolio stewardship. The most important thing the last decade of Eaton teaches is that you do not have to let a low-margin legacy business die a slow, value-destroying death inside a conglomerate. You can sell it — ideally at a rich multiple to a strategic buyer who values it more than the market values it inside your holding company — and recycle the proceeds into higher-growth franchises.

Selling Hydraulics at 13.2 times EBITDA to fund secular electrical growth, and now spinning off the Mobility Group entirely, is the disciplined version of this idea.[^4]9 The honest counterpoint is that the same logic was used to justify buying Boyd at 22.5 times: recycling into growth is only value-creating if you do not overpay for it, and the market will not know for years whether the buy side of this playbook was as disciplined as the sell side.[^2]

The second lesson is the power of getting "spec'd in." In business-to-business industrial investing, the companies worth the most are the ones that get written into a customer's design early, before the purchase decision is even made, because that converts a transactional sale into a multi-year, high-visibility, pricing-advantaged relationship.

The specification moat is why Eaton's electrical margins look nothing like a commodity manufacturer's. When you evaluate any industrial supplier, the question to ask is: does this company get spec'd in, or does it fight for every order in an open bid? The answer largely determines the quality of the business.

The third lesson is the tax-arbitrage flywheel. The 2012 Irish inversion was not just a one-time savings; it structurally lowered Eaton's effective tax rate and freed offshore capital to be redeployed into growth without repatriation leakage.1

Structural advantages in where and how a company is taxed compound quietly over decades. The lesson comes with a warning, though: tax structures that look brilliant in one political era can become liabilities in the next, and depend on regulatory arrangements outside management's control. A durable business should not need a tax gimmick to work — and to Eaton's credit, the electrical franchise it bought with the inversion would be valuable under any tax regime. With the playbook in hand, the fair thing to do is turn it against the company itself and ask what a skeptic would attack.

IX. The Bull vs. Bear Case & Analyst Stress Test

Every compelling growth story attracts a chorus of believers, so the more useful exercise is to sit in the skeptic's chair and interrogate the case. Start with management credibility, because leadership just changed hands. Paulo Ruiz, who became CEO on June 1, 2025, is not an outsider parachuted in; he ran Eaton's Industrial Sector and served as president and chief operating officer before taking the top job, so there is real continuity of operating philosophy.8

But he is being tested immediately and hard: his first year has featured the largest and most aggressively priced acquisition in company history and the decision to spin off the founding business. Those are not caretaker moves. They are conviction bets, and they mean Ruiz will own the outcome of Boyd in a way he cannot delegate to his predecessor's reputation. Executive compensation is structured around relative total shareholder return, adjusted EPS, and operating cash flow, which at least aligns incentives with the metrics investors care about — though bull markets have a way of making incentive alignment look better than it is.

The way to judge a management team is not by the promises it makes but by the pattern of its behavior over time — target-setting, guidance discipline, the willingness to explain misses in specifics rather than platitudes, and consistency of narrative across calls.

On the demand side, Eaton's recent track record scores well: the company has repeatedly raised guidance through 2025 and into 2026 as orders accelerated, lifting its full-year 2026 organic-growth outlook by 200 basis points to a 10% midpoint and its adjusted-EPS midpoint to $13.28 on the first-quarter call.10 Raising numbers is easier than cutting them, of course, and a rising tide flatters any operator; the harder test comes when demand turns, and that test is still ahead. On the margin side, management has been unusually specific about the drag — quantifying the capacity-ramp headwind and committing to a numeric 2030 target — which is the kind of falsifiable promise that at least lets investors keep score. The concern is not evasiveness; it is that the specificity is all on the recovery, and the recovery has not yet happened.

Now the analyst stress test, drawn from what management was actually pressed on during recent earnings calls. The first and sharpest challenge is the margin-pressure conundrum. Electrical Americas — the crown jewel — saw its operating margin compress to 29.8% in the fourth quarter of 2025, down 180 basis points year over year, and then dip further to 25.6% in the first quarter of 2026.10 The cause, management explained, is "under-absorption": Eaton is spending heavily to build out roughly $1.5 billion of new capacity to serve data-center demand, and those new factories carry startup costs before they run at full volume.

On the fourth-quarter call, CFO Olivier Leonetti quantified the ramp headwind at around 130 basis points for 2026, concentrated in the first half, and management reiterated a target of returning to 32% margins by 2030.11 The bull hears "temporary investment for durable growth." The bear hears a legitimate question: what if the company is overbuilding capacity into a demand peak, and the margins never fully recover to the old highs? Analysts have pushed precisely on when margins will inflect, and management's answer — sequential improvement through the year with exit rates above 30% in the second half — is a promise that will be checked, quarter by quarter.10

The second challenge is M&A pricing and leverage. Paying $9.5 billion at 22.5 times EBITDA for Boyd, largely with debt, is a sharp deviation from the conservative, disciplined capital allocation that defined the prior era.[^2] A skeptical long-short investor or activist would zero in on the balance sheet: elevated leverage taken on at a cyclical high, integration risk in a business Eaton did not previously operate, and the uncomfortable optics of buying from a private-equity seller who presumably sold because the price was good.

The strategic fit is real, but the financial risk is also real, and the two do not cancel out.

There is an activist's angle worth voicing here too, even though Eaton is far too large and too well-run to be a conventional activist target. A skeptical investor would note that the Boyd deal, coming immediately after years of management preaching capital discipline, is exactly the kind of narrative reversal that invites scrutiny: the company that sold Hydraulics at a disciplined multiple and lectured about not overpaying then turned around and paid a growth-stock multiple for a business it did not previously operate. An activist would ask whether the board pushed back hard enough on price, whether the leverage taken on is prudent this late in a cycle, and whether the eagerness to own the "chip-to-grid" story overrode the discipline that made the company valuable in the first place. The Mobility spin-off, by contrast, is the kind of shareholder-friendly simplification an activist would applaud — so the governance picture is genuinely mixed rather than uniformly reassuring. The fair conclusion is that Eaton has earned trust on execution and portfolio focus while opening a real question about M&A discipline, and both things can be true at once.

The third and most fundamental challenge is the sustainability of hyperscaler capex. Data-center orders surged roughly 200% in the fourth quarter of 2025 and 240% in the first quarter of 2026 — numbers so large they invite suspicion.[^1]10

The bear's specific worry is "double-ordering": in a supply-constrained environment, customers place orders at multiple suppliers and pad their numbers to secure delivery slots, which can inflate backlog beyond true underlying demand. When the initial wave of AI data centers is built and capacity catches up, orders could pause abruptly, leaving Eaton with expensive new factories and a backlog that shrinks faster than expected.

Management counters that orders now being taken are for delivery twelve to eighteen months out and that the demand is broadening across AI and conventional cloud workloads.11 But the honest position is that no one — not management, not the analysts, not the bears — actually knows how durable the AI capex cycle is, and Eaton has leveraged its balance sheet and its capacity plans to a bet that it lasts.

The current risk radar rounds this out. Leverage and cost of capital are elevated post-Boyd. Execution risk runs through the multi-year factory expansions that must be delivered on time and on budget through late 2026 and beyond.

And there is a subtler bottleneck that could bite even if AI demand holds: grid-connection backlogs. As the Wall Street Journal has reported, utilities cannot connect new data centers to the grid fast enough, and those interconnection queues can stall the very commissioning timelines Eaton depends on to convert backlog into revenue.5

A booming order book means little if the projects it represents cannot get plugged in.

So where does the "why win / why not" spine actually land? Eaton wins from here if the specification moat and switching costs hold, if the capacity investments convert into the promised margin recovery toward 32%, and if the AI-and-grid capex wave proves to be a multi-year structural build rather than a two-year spike — in which case Boyd looks prescient and the re-rating is justified by durable earnings growth.

The case breaks if hyperscaler orders were inflated by double-ordering and roll over, if the capacity buildout leaves the industry with excess supply that erodes the rational-oligopoly pricing discipline, or if Boyd's price proves to have front-loaded years of future returns into a single top-of-cycle check. The evidence today genuinely supports the bull spine on the demand side — the order and backlog figures are real and independently corroborated across quarters — while the bear spine rests on the still-unprovable durability of that demand, and the price paid to chase it.

That leaves the discipline of watching, and here the KPIs matter more than any narrative. Three numbers cut through the noise.

The first is Electrical Americas backlog growth — the record backlog reported for the segment, and the 48% year-over-year growth in the broader electrical backlog reported for the first quarter of 2026, are the leading indicator of everything downstream; watch whether that growth decelerates.10 The second is the book-to-bill ratio in the data-center and utility verticals — a rolling figure above roughly 1.2 signals that new orders are still outrunning shipments and that structural growth is intact, while a slip below 1.0 would be the first hard evidence of the demand rollover bears fear.10 The third is operating-margin inflection in Electrical Americas — the recovery from the low-to-mid-twenties back toward the 30%-plus and eventually 32% target, which will confirm or refute management's core claim that today's margin pressure is a temporary investment cost rather than permanent competitive erosion.

Track those three, and you will know how the story is actually unfolding long before the headlines do.

X. Epilogue & Outro

Zoom out, and the arc is almost improbable. A company that began in 1911 selling gear-and-axle assemblies to the first American truck fleets — a business so physical and so old-economy it is hard to imagine anything further from artificial intelligence — has become one of the essential, invisible suppliers of the AI build-out, the maker of the electrical spine and, now, the liquid-cooling veins through which the data-center revolution must physically run.

It got there not by inventing a breakthrough product but by making a long series of deliberate choices about what to own: buying Cutler-Hammer and Westinghouse to build an installed base, inverting into Ireland to free its capital, pruning Hydraulics and Lighting to sharpen its focus, and finally spinning off the very axle business that gave it its name.

There is a human dimension to how this ends, too. The transformation was built on the discipline of one operator, Craig Arnold, whose whole philosophy was restraint — sell dear, buy cheap, never confuse a good story with a good price. He has now handed the company to Paulo Ruiz, whose opening moves have been anything but restrained: the largest and most expensive acquisition in Eaton's history and the spin-off of its founding business, both inside twelve months.89 That is not a criticism so much as an observation about inflection points. Successions are where corporate cultures are tested, and Ruiz has chosen to test his in public — at the top of a cycle, with the balance sheet leaned into the bet. If it works, he will be remembered as the leader who saw the chip-to-grid future clearly and moved before rivals could. If the cycle turns against him, he will be the executive who broke a decade of discipline in his first year. Both outcomes are live, and the coming quarters will begin to sort them.

The deeper lesson is that capital allocation, practiced patiently over decades, can outlast even the most storied incumbents. While General Electric — the finishing school where Craig Arnold learned his trade — dismantled itself under the weight of a conglomerate model it could not manage, Eaton quietly did the opposite: it edited itself, sold its weakest links dear, and concentrated its capital where the secular winds were strongest.

That is why a Cleveland gear maker outlasted an icon.

But an independent telling has to end where it began: with the tension between story and proof. Eaton has earned its transformation on the sell side — the discipline of its divestitures is a matter of record. The buy side, embodied by a $9.5 billion, top-of-cycle bet on liquid cooling made in a new CEO's first year, is a story whose ending has not been written. The demand is real today; the durability of that demand, and the wisdom of the price paid to capture it, will be revealed only in the numbers over the next several years.

For a company that spent a century learning to bend metal profitably, the final test is whether it can bend a booming market's capital to its advantage without, this time, bending too far.

References

-

Eaton to Buy Cooper Industries; Retrospective on the Irish Inversion — Reuters, 2012-05-21 ↩↩↩↩↩↩↩↩

-

Danfoss Completes Acquisition of Eaton Hydraulics — Danfoss, 2021-08-02 ↩

-

Eaton's Craig Arnold on Portfolio Transformation and Intelligent Power — S&P Global, 2024-05-14 ↩↩↩

-

Goldman Sachs Asset Management Sells Boyd Thermal to Eaton for $9.5 Billion — Bloomberg, 2025-11-03 ↩

-

The Grid-Connection Bottleneck Stalling the AI Boom — Wall Street Journal, 2025-09-18 ↩

-

American Reshoring and the Mega-Project Wave — Financial Times, 2025-12-10 ↩

-

Eaton Corporation plc — SEC Filings and Form 10-K Archive (company history and business description) ↩↩↩↩

-

Eaton Sets CEO Transition: Paulo Ruiz to Succeed Craig Arnold on June 1, 2025 — Crain's Cleveland Business, 2024-08-12 ↩↩↩↩

-

Eaton to Spin Off Vehicle and eMobility Segments (Mobility Group) — IndustryWeek, 2026-01-26 ↩↩↩↩

-

Eaton Q1 2026 Earnings: Record $7.5B Revenue, Data Center Orders Up 240%, Guidance Raised — BigGo Finance, 2026-05-05 ↩↩↩↩↩↩↩

-

Eaton (ETN) Q4 2025 Earnings Call Transcript — The Motley Fool, 2026-02-03 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube