Essex Property Trust: Building the West Coast Apartment Empire

I. Introduction & Episode Roadmap

Picture this: A Greek immigrant boy arrives in America at age four, speaking no English, carrying nothing but his family's dreams. Fast forward seven decades, and George Marcus has built not one but two real estate empires—including Essex Property Trust, a $20 billion colossus that owns 252 apartment complexes housing over 62,000 families across America's most expensive cities. Today, Essex stands as the 11th largest apartment owner in the United States, a publicly traded REIT that has quietly become one of the most successful real estate stories you've probably never heard of.

Here's what makes Essex fascinating: While flashier tech companies dominate headlines about West Coast wealth creation, Essex has methodically built a fortress of apartments in markets where new supply is virtually impossible. They don't just own apartments—they own apartments in San Francisco, Los Angeles, San Diego, and Seattle, cities where getting permission to build a doghouse requires three environmental impact studies and a séance with the planning commission.

The central question we're exploring today isn't just how an immigrant entrepreneur built one of America's dominant apartment REITs. It's how Essex discovered, decades before it became conventional wisdom, that the secret to real estate wealth wasn't building more—it was owning what couldn't be built again. This is a story about recognizing that California's regulatory maze wasn't a bug but a feature, that NIMBYism could be a competitive moat, and that sometimes the best business strategy is letting your competitors fight over Texas while you quietly monopolize Palo Alto.

Over the next few hours, we'll trace Essex's evolution from a small private partnership in 1971 to a dividend aristocrat managing $20 billion in irreplaceable West Coast apartments. We'll explore how George Marcus simultaneously built Marcus & Millichap into the nation's largest investment brokerage while nurturing Essex on the side—a feat of parallel entrepreneurship that would make Elon Musk dizzy. We'll dive deep into the 2014 mega-merger with BRE Properties that created the only pure-play West Coast apartment REIT, a deal so strategically elegant it deserves its own business school case study.

But this isn't just a historical exercise. Understanding Essex means understanding the future of American housing. As we speak, California faces a housing shortage measured in millions of units, tech workers are paying $4,000 for one-bedrooms, and local governments are passing increasingly desperate measures to increase supply. Essex sits at the center of this storm, collecting rent checks that rise as reliably as the Pacific tide.

What you'll learn today goes beyond one company's story. We're talking about the art of identifying structural advantages, the discipline of geographic focus when everyone preaches diversification, and the counterintuitive wisdom of embracing regulatory constraints. We'll explore how a REIT structure can be a weapon, why operational excellence matters more than financial engineering, and when making a transformative acquisition is worth betting the company.

So buckle up. We're about to explore how a four-year-old Greek immigrant named George Moutsanas became George Marcus, how he turned California's housing dysfunction into a money-printing machine, and why Essex Property Trust might be the most boring, brilliant business you'll hear about all year.

II. The George Marcus Origin Story

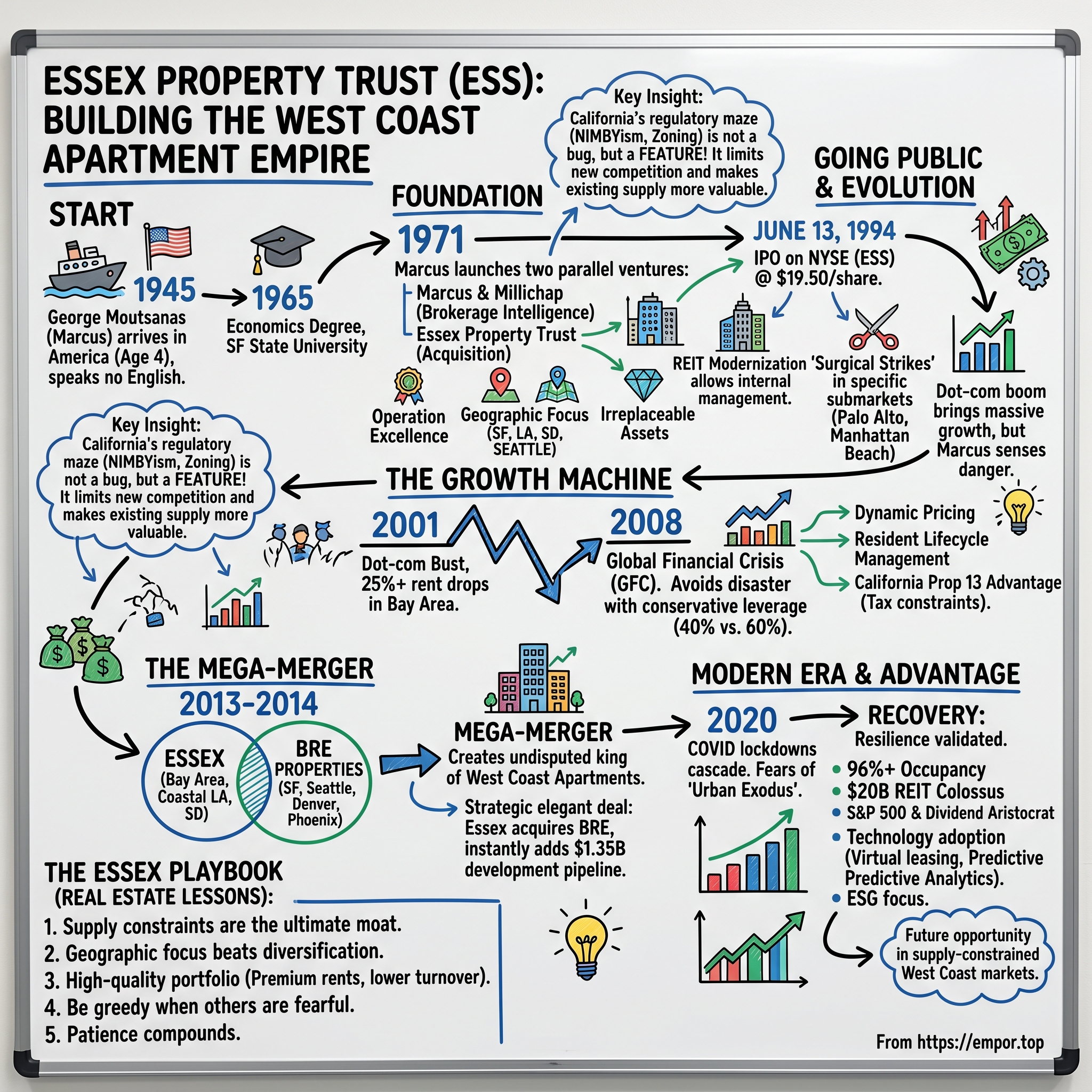

The cargo ship from Greece docked in New York Harbor in 1945, carrying among its passengers a four-year-old boy named George Moutsanas and his family, fleeing the devastation of World War II. Young George spoke no English, had no connections, and his family possessed little beyond determination. Yet this moment—this classic American immigrant arrival—would eventually reshape the West Coast real estate landscape in ways nobody could have imagined.

George's family settled in San Francisco, where the newly renamed George Marcus would grow up watching his parents struggle to establish themselves in their adopted homeland. The city in the 1950s was transforming—the war had brought massive population growth, housing was scarce, and everywhere you looked, apartment buildings were rising to meet demand. For a young immigrant kid walking the hills of San Francisco, these buildings weren't just structures; they were monuments to possibility, concrete proof that in America, you could build something from nothing.

Marcus worked his way through San Francisco State University, earning an economics degree in 1965. But unlike his classmates heading to banks or corporations, Marcus was drawn to real estate. He'd spent his college years not just studying supply and demand curves but walking neighborhoods, watching how cities grew, understanding intuitively what his textbooks called "location, location, location." He saw patterns others missed—how a new transit line could transform a sleepy district, how demographic shifts created pockets of opportunity, how California's growth wasn't just continuing but accelerating.

The real education came after graduation. Marcus spent the late 1960s learning the real estate business from the ground up—not in some executive training program, but in the trenches, evaluating properties, understanding financing, building relationships with brokers and lenders. He was particularly fascinated by apartment buildings. While others chased the glamour of office towers or the quick profits of single-family home flips, Marcus saw apartments differently. They were recession-resistant (people always need somewhere to live), they generated predictable monthly cash flow, and in supply-constrained markets, their values could only go up.

Then came 1971—a year that would define not just Marcus's career but the entire landscape of West Coast real estate. At age 30, Marcus didn't launch one company; he launched two. First, with William A. Millichap, he co-founded Marcus & Millichap, a commercial real estate brokerage focused on investment properties. The firm would eventually become the largest investment brokerage in the nation, but that's another story. What's remarkable is that in the same year, with the same entrepreneurial energy, Marcus also founded Essex Property Trust.

Think about the audacity of this moment. Here's a first-generation immigrant, just six years out of college, simultaneously launching two real estate companies. It's like starting both Uber and Lyft at the same time and running them in parallel. But Marcus saw these ventures as complementary, not competing. Marcus & Millichap would give him unparalleled market intelligence—he'd see every deal, know every seller, understand pricing dynamics in real-time. Essex would be where he'd deploy that knowledge, cherry-picking the best apartment opportunities for his own portfolio.

The name "Essex" itself was carefully chosen—sophisticated but approachable, suggesting established wealth without ostentation. Marcus wanted a brand that would appeal to both tenants and investors, something that sounded like it had been around for generations even on day one. This attention to perception would prove crucial as Essex grew.

Marcus's vision for Essex was crystalline from the start: own apartments in West Coast markets where supply was constrained. Not East Coast, despite its density. Not Sun Belt, despite its growth. The West Coast, specifically California, where even in 1971, getting approval to build anything was becoming increasingly difficult. Marcus had witnessed California's transformation from a build-anywhere frontier to a regulated, NIMBY paradise. He understood, decades before it became conventional wisdom, that the best real estate investment wasn't where you could build the most, but where others couldn't build at all.

The 1970s real estate landscape was chaotic—inflation was spiking, Nixon would soon take the dollar off the gold standard, and the oil crisis loomed. But chaos creates opportunity for those with conviction. While others hesitated, Marcus began acquiring his first properties, small apartment complexes in San Francisco and the Peninsula. Nothing flashy—20 units here, 30 units there. But each property was chosen with surgical precision: good neighborhoods, strong demographics, and most importantly, locations where adding supply would be nearly impossible.

What made Marcus different from other real estate entrepreneurs of his era wasn't just his appetite for risk or his work ethic—plenty of developers had those. It was his fundamental insight about California's future. He saw that the state's economic dynamism would continue attracting people, that its regulatory environment would only get more restrictive, and that the combination would create a permanent supply-demand imbalance. In essence, he wasn't just buying apartments; he was buying optionality on California's dysfunction.

By the mid-1970s, Essex had established its operational philosophy: buy quality properties in supply-constrained markets, manage them exceptionally well, and hold them forever. This wasn't the sexiest strategy—no grand developments, no headline-grabbing deals. But Marcus understood something his flashier competitors didn't: in real estate, boring can be beautiful, especially when boring means predictable, growing cash flows from irreplaceable assets.

The immigrant boy who arrived with nothing had discovered the perfect American business—one where patience was rewarded, where operational excellence mattered, and where the government itself (through its zoning restrictions) would protect his investments from competition. As the 1970s drew to a close, Essex was still small, still private, still unknown outside real estate circles. But the foundation was set, the strategy was proven, and George Marcus was just getting started.

III. The Private Years: Building the Foundation (1971–1994)

The morning of Black Monday, October 19, 1987, George Marcus sat in his San Francisco office watching the market crash—the Dow Jones falling 22% in a single day, the largest one-day percentage drop in history. Real estate companies were being obliterated, banks were pulling credit lines, and developers across the country were heading for bankruptcy. Marcus picked up the phone and started making calls. Not to his lawyers or bankruptcy attorneys, but to sellers. While others were selling in panic, Essex was preparing to buy.

But we're getting ahead of ourselves. To understand how Essex could be a buyer during the worst real estate crisis since the Depression, we need to understand how Marcus built the company during its private years—two decades of methodical growth that would establish Essex as the premier West Coast apartment owner before most people had even heard its name.

The early 1970s acquisitions were almost comically modest by today's standards. Essex's first property was a 24-unit complex in San Mateo, purchased for less than $500,000. Marcus would personally visit every property, often spending entire weekends walking through units, talking to tenants, understanding what made one apartment complex worth 10% more than another. He developed what he called his "three-minute rule"—within three minutes of entering a property, he could assess its true condition, its management quality, and its potential. This wasn't mysticism; it was pattern recognition born from obsessive attention to detail.

What set Essex apart even in these early days was its focus on operational excellence. While other owners treated property management as an afterthought—something to outsource to the lowest bidder—Marcus understood that in the apartment business, operations were the business. Essex developed its own property management systems, standardizing everything from maintenance schedules to tenant screening procedures. They discovered that small operational improvements—responding to maintenance requests within 24 hours instead of 72, keeping common areas immaculate, remembering tenants' names—could justify premium rents and reduce turnover.

By 1975, Essex owned eight properties with roughly 800 units, all within 50 miles of San Francisco. This geographic concentration was deliberate and controversial. Real estate investing 101 preached diversification—spread your risk across markets, property types, geographies. Marcus did the opposite. His logic was compelling: why dilute your expertise? If you truly understood the San Francisco Peninsula market, why own apartments in Phoenix or Atlanta where you had no edge? This focus allowed Essex to see opportunities others missed—a property near a planned BART station, an apartment complex in a school district about to be rezoned.

The late 1970s brought inflation and rent control battles across California. While other owners fought rent control tooth and nail, Marcus took a more nuanced view. Yes, rent control limited upside, but it also created stability and, paradoxically, made existing non-rent-controlled properties more valuable. Essex carefully mapped rent control jurisdictions, avoiding the most restrictive while positioning itself in adjacent areas that benefited from the spillover demand. It was three-dimensional chess while others were playing checkers.

Then came the savings and loan crisis of the late 1980s. The S&L industry had gone mad with real estate lending, financing speculative developments across the country. When the music stopped, the devastation was complete. The Resolution Trust Corporation was created to dispose of assets from failed S&Ls, creating a once-in-a-generation buying opportunity for those with capital and courage.

This is where Essex's conservative financial management during the good times paid off spectacularly. While competitors had leveraged themselves to the hilt during the boom, Essex had maintained modest debt levels and substantial cash reserves. Marcus had learned from studying real estate cycles that the best deals weren't made during booms but during busts, when fear dominated greed.

Between 1989 and 1992, Essex acquired twelve properties at prices that seemed impossible just years earlier. A 200-unit complex in Fremont that had sold for $15 million in 1987 was acquired for $9 million. A premier property in San Jose was purchased at a 40% discount to replacement cost. But Essex wasn't just bottom-fishing; each acquisition fit their strict criteria—supply-constrained locations, good bones, fixable problems.

The early 1990s also saw Essex expand beyond the Bay Area for the first time, but still within their West Coast thesis. They entered Southern California, focusing on Los Angeles's Westside and San Diego's coastal communities—markets that shared the Bay Area's characteristics of strong employment, limited supply, and growing demand. By 1993, Essex owned 16 multifamily communities with over 4,000 units, generating substantial cash flow and sitting on enormous unrealized gains.

The decision to go public wasn't made lightly. Marcus had built Essex as a private company for 23 years, maintaining complete control and avoiding the scrutiny and short-term pressures of public markets. But by 1994, several factors aligned to make going public compelling. First, the REIT Modernization Act of 1993 had made REITs more attractive, allowing them to provide property management services to third parties and reducing ownership restrictions. Second, the public markets were valuing apartment REITs at substantial premiums to private market values. Third, and most importantly, Marcus saw a generational opportunity to consolidate the fragmented apartment industry, and that would require the currency of public stock.

As 1994 began, Essex had assembled an institutional-quality portfolio worth over $400 million, a seasoned management team, and a 23-year track record of successful operations. They had survived multiple recessions, navigated California's regulatory maze, and built a reputation as the smartest apartment owners on the West Coast. The foundation was complete. It was time to build the empire.

The private years had taught Marcus crucial lessons that would guide Essex's public future: patience beats aggression, operations drive returns, geographic focus creates competitive advantages, and the best time to be greedy is when others are fearful. These weren't just aphorisms; they were battle-tested principles that had transformed a small private partnership into a platform ready for exponential growth. As Essex prepared its IPO documents in early 1994, one line in the prospectus stood out: "the only multifamily REIT with a diversified portfolio located in strong West Coast markets which have significant constraints on the production of housing." It was a mouthful, but it was also a moat—one that would prove nearly impossible for competitors to replicate.

IV. Going Public: The IPO and REIT Evolution (1994–2000)

June 13, 1994, 9:30 AM Eastern. The opening bell rings at the New York Stock Exchange, and Essex Property Trust begins trading under the ticker symbol "ESS" at $19.50 per share. George Marcus, standing on the exchange floor in a conservative gray suit, watches as the first trades cross. The offering raised $150 million—modest by today's standards, but enough to transform Essex from a private partnership into a public growth machine. What Marcus didn't know was that he'd just caught the perfect wave: the greatest REIT bull market in history was about to begin.

The REIT modernization of the early 1990s had fundamentally changed the game. For decades, REITs had been sleepy, dividend-focused vehicles that couldn't even manage their own properties. The new rules allowed REITs to be internally managed, to provide services, to develop properties—in short, to be real operating companies. This transformation coincided with a generational shift in how institutions viewed real estate. Pension funds and mutual funds, seeking yield in a low-rate environment, suddenly discovered REITs offered liquid exposure to real estate with professional management and regulatory oversight.

Essex's IPO roadshow had been a masterclass in positioning. While other apartment REITs pitched geographic diversification as risk mitigation, Marcus flipped the script. "Would you rather own 100 average properties scattered across America," he'd ask institutional investors, "or 50 exceptional properties in the strongest markets in the country?" He'd then pull out charts showing California's job growth, population trends, and most importantly, housing permit data that looked like a ski slope—pointing inexorably downward.

The early public days were jarring for a company accustomed to privacy. Suddenly, Essex had to report quarterly earnings, host analyst calls, and explain every decision to Wall Street. The first earnings call was particularly memorable. An analyst asked why Essex wasn't expanding to Las Vegas, where apartments were being built at record pace. Marcus's response became legendary within the company: "We don't chase growth; we chase barriers to entry. In Vegas, the barrier to entry is a pickup truck and a hammer. In San Francisco, it's an act of God."

But being public also brought unexpected advantages. The stock market in 1994-1995 was valuing apartment REITs at significant premiums to private market values—a phenomenon that seemed to defy logic but reflected the liquidity premium and professional management that REITs offered. Essex's stock, which IPO'd at $19.50, hit $25 within six months. This currency allowed Essex to be aggressive in acquisitions, using their appreciated stock as acquisition currency.

The competitive landscape was heating up. BRE Properties, founded by executives from Marcus's own Marcus & Millichap network, had also gone public and was aggressively pursuing the same West Coast strategy. Equity Residential, Sam Zell's apartment colossus, was rolling up properties nationwide. AvalonBay was dominating the East Coast. The apartment REIT sector was consolidating rapidly, and Essex needed to grow or risk being marginalized.

Essex's response was strategic rather than reactive. Instead of trying to outbid everyone everywhere, they developed what they called the "surgical strike" approach. They identified specific submarkets where they wanted to dominate—Palo Alto, West Los Angeles, Seattle's Eastside—and paid whatever it took to win in those markets. A competitor might own properties in 50 cities; Essex would own half of the institutional-quality apartments in five neighborhoods.

Then came the dot-com boom, and everything changed. Starting in 1996, the Bay Area experienced an economic explosion unlike anything since the Gold Rush. Companies with no revenue were going public for billions. Twenty-something programmers were becoming millionaires overnight. And they all needed somewhere to live. Essex's Bay Area properties, which had been generating steady 5% annual rent growth, suddenly saw 15%, 20%, even 25% increases. A two-bedroom in Palo Alto that rented for $1,500 in 1996 was getting $2,800 by 1999.

But Marcus, ever the student of cycles, saw danger in the euphoria. At the December 1999 board meeting, with Essex's stock at an all-time high of $42 and occupancy at 98%, he presented a contrarian view. "Trees don't grow to the sky," he told the board. "We need to prepare for the downturn." The response was skeptical—what downturn? The economy was booming, rents were soaring, and Essex's FFO had grown 40% in two years.

Marcus's solution was elegant: sell the bottom third of the portfolio and redeploy into the highest-quality assets available. Throughout 1999 and early 2000, Essex sold 15 properties—older complexes, secondary locations, properties that required significant capital investment. They used the proceeds to buy just five properties, but what properties they were: brand-new complexes in Santana Row, premier high-rises in Seattle, irreplaceable assets in Manhattan Beach. The average quality of the portfolio increased dramatically, even as the unit count remained flat.

The public market discipline had also forced Essex to professionalize in ways that would pay dividends for decades. They implemented sophisticated revenue management systems, copying airline yield management techniques to optimize rents. They developed centralized purchasing to reduce costs. They created training programs that turned property managers into customer service professionals. Being public meant being compared to peers every quarter, and Essex was determined to win those comparisons.

By the end of 2000, as the NASDAQ peaked and the first cracks in the tech bubble appeared, Essex had transformed from a successful private company into a public market darling. The stock had more than doubled from its IPO price. The portfolio had grown from 16 to 35 properties. Most importantly, Essex had established itself as the premium brand in West Coast apartments—the Tiffany's of multifamily REITs.

The irony wasn't lost on Marcus. The immigrant kid who'd arrived with nothing now ran a public company worth over $1 billion. But he knew the real test was coming. Anyone could look smart in a bull market. The question was whether Essex's strategy—geographic concentration, operational excellence, premium properties—would hold up when the music stopped. As 2000 turned to 2001 and the dot-com bubble began its spectacular deflation, they were about to find out.

V. The Growth Machine: Scale and Strategy (2000–2013)

Michael Schall remembers the exact moment he knew the dot-com party was over. It was March 10, 2001, and he was touring Essex's premier Palo Alto property when a tenant, a 26-year-old software engineer, handed in his keys. "Can't afford it anymore," the kid said, loading boxes into a U-Haul. "Company went under. I'm moving back with my parents in Ohio." That same day, Essex received 47 similar notices across their Bay Area portfolio. The tech apocalypse had arrived, and it was hitting Essex's core markets like a precision-guided missile.

Schall, who'd joined Essex as CFO in 1994 and would become President and CEO in 2001, had a front-row seat to one of the most dramatic boom-bust cycles in American history. Occupancy in Essex's Bay Area properties fell from 97% to 88% in eighteen months. Rents dropped 25% in some submarkets. The stock price, which had touched $45 in early 2000, crashed to $22. Wall Street analysts who'd loved Essex's Bay Area concentration suddenly questioned why they weren't more diversified.

But here's where Essex's operational discipline proved its worth. While competitors slashed services and deferred maintenance to preserve cash, Essex did the opposite. They launched "Operation Upgrade," investing $50 million in property improvements during the downturn. New fitness centers, business centers with high-speed internet (a luxury in 2002), upgraded kitchens with granite countertops. The logic was counterintuitive but brilliant: when the market recovered, Essex properties would be positioned as premium options, able to capture maximum rent growth.

They also went shopping. Between 2001 and 2003, Essex acquired $500 million of properties at prices not seen since the early 1990s. A crown jewel acquisition was the Promenade at Rio Vista in San Diego, purchased for $67 million from a distressed seller—Essex would sell it eight years later for $118 million. They bought entire portfolios from overleveraged developers, sometimes at 60 cents on the dollar. Marcus's old mantra—"be greedy when others are fearful"—was playing out in real-time.

The Essex playbook that emerged from this period would define the company for the next decade. First, strategic investments in high-growth markets—but growth defined not by population increases but by job quality and wage growth. They wanted markets attracting lawyers, doctors, and engineers, not just people. Second, acquiring properties with value-add potential—older properties in great locations that could be renovated to compete with new construction at 70% of the cost. Third, developing new properties, but only in absolutely premier locations where they could achieve premium rents.

The development strategy was particularly interesting. Unlike merchant builders who developed to sell, Essex developed to own forever. This changed the calculus entirely. They could pay more for land because they'd capture decades of appreciation. They could spend more on construction quality because they'd save on maintenance. They could include amenities that wouldn't pencil for a merchant builder but would allow Essex to charge premium rents for years.

Property management became a science. Essex implemented dynamic pricing systems that adjusted rents daily based on supply, demand, seasonality, and competitive positioning. They discovered that raising rents $50 on Monday might result in three lost leases, but raising them $30 on Friday resulted in zero losses—the kind of micro-optimization that added millions to the bottom line. They also pioneered what they called "resident lifecycle management"—tracking every interaction from initial inquiry through move-out, identifying friction points, and systematically eliminating them.

Then came 2008, and suddenly the dot-com bust looked like a gentle correction. The global financial crisis threatened to take down the entire economy. Banks stopped lending, period. Capital markets froze. Apartment values fell 30% nationally. Essex's stock crashed from $120 to $60 in six months. This time, the crisis wasn't contained to tech markets—it was everywhere.

But Essex had learned from 2001. They'd maintained conservative leverage, with debt-to-assets around 40% compared to peers at 60% or higher. They had committed credit lines, not just handshake agreements. Most importantly, they'd built a portfolio of properties that, even in the worst economy since the Depression, maintained 93% occupancy. People might lose their homes to foreclosure, but they still needed somewhere to live—and paradoxically, the housing crisis created more renters.

The financial crisis also accelerated a trend that would become central to Essex's strategy: the transformation of Americans from homeowners to renters. Millennials, scarred by watching their parents lose homes, preferred the flexibility of renting. Boomers, divorced or downsizing, discovered apartment living was easier than maintaining a house. The American homeownership rate, which peaked at 69% in 2004, began a secular decline that continues today. Essex was perfectly positioned for this demographic shift.

Michael Schall's leadership during this period deserves special mention. Unlike the stereotypical REIT CEO—usually a deal-making real estate cowboy—Schall was cerebral, analytical, almost professorial. He spoke in complete paragraphs, cited academic research, and could discuss cap rate compression with the sophistication of a Wharton professor. Under his leadership, Essex became known as the "thinking person's REIT"—sophisticated, strategic, never chasing the latest fad.

Technology adoption accelerated under Schall. Essex launched online leasing, allowing prospects to tour, apply, and sign leases entirely digitally. They implemented predictive analytics to identify residents likely to move, offering targeted incentives to retain them. They even experimented with smart home technology, though they discovered residents cared less about controlling lights with their phone than about reliable WiFi and package delivery solutions.

The California Proposition 13 advantage became increasingly valuable during this period. Prop 13, passed in 1978, limited property tax increases to 2% annually regardless of appreciation. Essex properties purchased in the 1990s for $10 million, now worth $40 million, still paid taxes based on the original purchase price. This created an enormous competitive advantage—Essex's property taxes were often one-third of what a new buyer would pay, allowing them to underprice competitors while maintaining superior margins.

By 2013, Essex had emerged from the financial crisis stronger than ever. The portfolio had grown to 226 properties with 57,000 units. The stock price hit new all-time highs. Same-store revenue growth was consistently outpacing inflation. But Schall and the board knew they needed something bigger—a transformative move that would secure Essex's position for the next generation. They found it in an unexpected place: their oldest rival, BRE Properties. The stage was set for the deal that would reshape West Coast apartments forever.

VI. The BRE Mega-Merger: Creating a West Coast Giant (2013–2014)

The phone call came on a Sunday evening in September 2013. Michael Schall was at home in Palo Alto when Constance Moore, CEO of BRE Properties, called with a simple question: "Michael, what would you think about putting our companies together?" Schall had been expecting this call for years. The apartment REIT industry was consolidating rapidly, and the two premier West Coast players circling each other was inevitable. What followed was one of the most strategically elegant mergers in REIT history—a $4.3 billion combination that would create the undisputed king of West Coast apartments.

To understand why this merger was inevitable, you need to understand the Archstone saga that preceded it. Archstone had been the nation's second-largest apartment REIT until it was taken private in 2007 in a disastrous $22 billion leveraged buyout led by Lehman Brothers. When Lehman collapsed, Archstone's assets became the prize in a complex bankruptcy proceeding. In late 2012, Equity Residential and AvalonBay partnered to acquire Archstone, splitting its massive portfolio between them. Suddenly, these East Coast giants had significant West Coast presence, threatening Essex and BRE's regional dominance.

The competitive dynamics had shifted overnight. Equity Residential, with Sam Zell's aggressive leadership and massive scale, could undercut local players on price. AvalonBay brought East Coast institutional sophistication to West Coast markets. Essex and BRE, which had competed as regional champions for two decades, suddenly looked subscale. As one analyst put it, "It's like two local restaurants discovering McDonald's and Burger King just moved to town."

But the strategic differences between Essex and BRE made them perfect merger partners. Essex's portfolio was concentrated in the Bay Area and Southern California's most expensive coastal markets—70% of their properties were in markets where median home prices exceeded $500,000. BRE's portfolio was more diverse—50% California, but with significant exposure to Seattle, Denver, and Phoenix. Essex was seen as the premium brand, commanding the highest rents in their markets. BRE was known for operational efficiency and development expertise.

The numbers were compelling. BRE's portfolio was valued at $5 billion—85% in California, 15% in Seattle, perfectly complementing Essex's footprint. But the real prize was BRE's $1.35 billion development pipeline—14 projects that would add 4,100 units in supply-constrained markets. For Essex, which had been cautious about development, acquiring BRE meant instantly becoming a major developer without taking on the execution risk from scratch.

The negotiation was delicate. Both companies had proud cultures and successful track records. The deal structure needed to be precise: 0.2971 Essex shares plus $12.33 in cash for each BRE share, valuing BRE at $56.21 per share—a 20% premium to its trading price. The exchange ratio was critical—too much cash would be dilutive to Essex's FFO, too much stock would dilute existing Essex shareholders. The final structure was engineered to be immediately accretive to Essex's FFO while giving BRE shareholders significant upside through Essex stock ownership.

The cultural integration challenge was real. Essex was known for its analytical, conservative approach—they'd joke that they measured twice, cut once, then measured again. BRE was more entrepreneurial, faster-moving, willing to take calculated risks. Essex employees wore suits; BRE was business casual. Essex's headquarters in Palo Alto was understated; BRE's San Francisco office was modern and flashy. These might seem like trivial differences, but culture clashes had killed plenty of mergers.

Schall's integration strategy was masterful. Rather than imposing Essex culture on BRE, he created a "best of both worlds" approach. Essex would adopt BRE's development expertise and property management systems. BRE properties would benefit from Essex's revenue optimization and capital allocation discipline. Key BRE executives were retained and given significant responsibilities—this wasn't a conquest but a combination of equals.

The synergy targets were aggressive but achievable: $20 million in annual cost savings within 18 months. This would come from eliminating duplicate corporate functions, centralizing procurement, and optimizing property management. But the real synergies were strategic. The combined company would have unmatched market intelligence in West Coast markets. They could better compete for acquisitions, with more capital and lower cost of funding. They could optimize the portfolio, selling non-core assets and redeploying into premier properties.

Wall Street's reaction was initially mixed. Some analysts worried about integration risk and the premium paid. Others questioned whether bigger was actually better in the apartment business. But the strategic logic was undeniable. As one analyst noted, "Essex just bought the only portfolio that perfectly fits their strategy. There's literally nothing else like BRE available."

The operational integration proceeded with military precision. Teams were formed for every function—property management, development, finance, IT. Weekly integration calls tracked hundreds of specific tasks. The companies maintained a "merger integration office" that reported directly to Schall. By March 2014, just three months after announcement, major systems were integrated and synergy capture was ahead of schedule.

The development pipeline integration was particularly successful. BRE had projects in various stages across premier West Coast markets. Essex's financial strength and lower cost of capital allowed these projects to proceed faster and with better economics. A project in Downtown Los Angeles that BRE had been developing with a joint venture partner was brought entirely in-house, saving millions in promoted interest.

The real estate operations told the story. The combined company owned 245 communities with 58,000 apartment homes, with total market capitalization of $15.4 billion. But more importantly, they'd created what Schall called "the only West Coast pure play in the public multifamily REIT space." While competitors had to manage properties across dozens of markets, Essex could focus entirely on the West Coast, achieving economies of scale and operational excellence that diversified players couldn't match.

By the end of 2014, the merger was deemed an unqualified success. Synergies exceeded targets, reaching $23 million annually. The stock price had risen 25% since announcement. Same-store revenue growth was accelerating. But perhaps most importantly, Essex had transformed from a strong regional player into a fortress—too big to be acquired, too focused to be outmaneuvered, too disciplined to make fatal mistakes.

Looking back, the BRE merger was the decisive move that secured Essex's future. In one transaction, they'd eliminated their primary competitor, achieved unprecedented scale in their core markets, and created a platform for the next phase of growth. As Schall told investors on the first post-merger earnings call, "We didn't just get bigger. We got better. And in our business, better compounds over decades."

VII. Modern Era: The Supply-Constrained Advantage (2014–Present)

The email arrived at 11:47 PM on March 16, 2020: "Effective immediately, San Francisco County is ordering all residents to shelter in place." Michael Schall, reading from his home office, felt his stomach drop. Essex's crown jewel markets—San Francisco, Los Angeles, Seattle—were implementing the nation's strictest COVID lockdowns. Within hours, similar orders cascaded across California and Washington. For a company with 100% of its properties in these markets, it was the nightmare scenario: urban exodus fears, eviction moratoriums, and work-from-home potentially permanent. Yet what followed would validate Essex's strategy in ways nobody could have predicted.

But let's rewind to 2014, when the post-BRE merger Essex began executing what they called "Essex 3.0"—a vision for dominating West Coast apartments through operational excellence, selective development, and strategic capital allocation. The first priority was portfolio optimization. Between 2014 and 2019, Essex sold $1.8 billion of properties—older assets, secondary locations, properties facing rent control threats. They redeployed this capital into $2.3 billion of acquisitions and developments in their core markets, essentially trading up the portfolio quality while maintaining similar unit counts.

The development machine that came with BRE proved transformative. Essex completed 15 major developments between 2014 and 2019, adding 4,500 units in impossibly supply-constrained markets. The jewel was MB360 in Manhattan Beach—360 luxury units where one-bedrooms rented for $4,000 monthly. The project cost $180 million to build but was valued at $250 million upon completion. This wasn't development for development's sake—it was creating irreplaceable assets in markets where getting new permits was approaching impossibility.

Essex joined the S&P 500 in 2017, a watershed moment that brought new institutional investors and index fund flows. The company also achieved Dividend Aristocrat status, having raised its dividend for 25 consecutive years—a testament to the stability of their cash flows. These milestones mattered beyond prestige; they lowered Essex's cost of capital, allowing them to compete more effectively for acquisitions.

The housing affordability crisis that exploded across the West Coast in the late 2010s was both a challenge and an opportunity. Yes, it brought political scrutiny and rent control battles. But it also validated Essex's core thesis: when supply can't meet demand, existing assets become increasingly valuable. California needed to build 180,000 units annually to meet demand; it was permitting fewer than 80,000. This wasn't a temporary imbalance—it was structural, embedded in the state's political economy.

California's regulatory environment evolved from restrictive to nearly prohibitive. CEQA (California Environmental Quality Act) lawsuits could delay projects for years. Local governments demanded increasingly expensive community benefits. Construction costs soared as labor shortages met stringent building codes. By 2019, building a new apartment in San Francisco cost $700,000 per unit. For Essex, which owned apartments acquired at $200,000 per unit, the replacement cost moat was enormous.

The technology amenity race transformed the apartment experience. Essex invested heavily in what they called "invisible amenities"—gigabit internet, package lockers, mobile app-controlled access. They discovered residents would pay $100 more monthly for reliable package delivery than for a fancy gym. Virtual tours, automated leasing, and AI-powered maintenance requests became standard. By 2019, 60% of Essex leases were signed without the resident ever visiting the leasing office.

Then came COVID-19, and every assumption about urban living was questioned. The "urban exodus" narrative dominated headlines. Tech companies announced permanent remote work. San Francisco rents fell 25% in six months. Essex's stock dropped from $330 to $180. Analysts predicted the end of cities, the death of expensive urban apartments, a permanent shift to suburban single-family homes.

But Essex's response was measured and strategic. They implemented what they called "Operation Stability"—focusing on retention over rent growth, offering flexible lease terms, accelerating unit upgrades while occupancy was lower. They avoided the mistake many landlords made of maintaining pre-COVID rents while units sat empty. Better to rent at market than hold out for yesterday's prices.

The eviction moratoriums, while challenging, revealed something interesting: Essex's resident base was remarkably stable. These weren't paycheck-to-paycheck renters but professionals with savings, stock options, and stable employment. Rent collections remained above 95% throughout the pandemic, compared to 85% for lower-tier apartments. The quality of Essex's portfolio—and its residents—proved its worth during crisis.

By mid-2021, the narrative reversed with stunning speed. Tech workers began returning to cities. The savings accumulated during lockdowns enabled move-up demand. The single-family home price explosion—up 40% in many California markets—made renting look reasonable again. Essex's occupancy recovered to 96% by year-end 2021. Rents not only recovered but exceeded pre-COVID peaks by 2022.

The 2024 performance validated the long-term strategy: FFO of $12.77 per share, 96.2% occupancy, $1.6 billion in revenue. But the numbers only tell part of the story. Essex had assembled an irreplaceable portfolio in markets where building new supply was virtually impossible. They'd survived the worst pandemic in a century with their business model intact. They'd proven that premium apartments in supply-constrained markets weren't just resilient—they were antifragile, getting stronger from stress.

ESG (Environmental, Social, and Governance) initiatives became central to Essex's strategy. They committed to reducing carbon emissions 50% by 2030, installing solar panels and efficient systems across the portfolio. They developed affordable housing—not because regulations required it, but because sustainable communities needed economic diversity. These weren't just feel-good initiatives; institutional investors increasingly demanded ESG excellence, and Essex's leadership in this area attracted capital.

Looking at Essex today, you see a company that has transcended its origins as a real estate firm to become something more complex—a platform for capturing value from the West Coast's permanent housing shortage. They don't just own apartments; they own optionality on California's continued dysfunction, demographic inevitability, and the growing preference for renting over owning. As one analyst noted, "Essex isn't really in the apartment business. They're in the scarcity business. And business is good."

VIII. The Essex Playbook: Real Estate Lessons

There's a story Michael Schall likes to tell about Warren Buffett's visit to Essex headquarters in 2018. Buffett, who generally avoids real estate investments, spent three hours with Schall discussing the business. At the end, Buffett said, "You know what I like about your model? Your competitive moat gets wider every year without you doing anything. California digs it for you." That observation captures the essence of the Essex playbook—a strategy so counterintuitive it seems like it shouldn't work, yet has created one of the most successful REITs in history.

The first lesson: supply constraints are the ultimate moat. Most businesses fear barriers—regulatory hurdles, high costs, difficult logistics. Essex realized these barriers were actually gifts if you were already inside the walls. Every new environmental review requirement, every additional affordable housing mandate, every community benefit agreement made their existing properties more valuable. They weren't trying to change California's dysfunction; they were monetizing it.

Consider the math: In Texas, you can build a new apartment for $150,000 per unit. In San Francisco, it costs $700,000—if you can get permits at all. This means Essex's San Francisco properties, acquired years ago at $300,000 per unit, have a replacement cost moat of $400,000 per unit. Multiply that by 62,000 units, and you're talking about $25 billion of embedded value that competitors simply cannot replicate. It's like owning beachfront property on an island that stopped issuing building permits.

The second lesson: geographic focus beats diversification. Every real estate textbook preaches diversification—spread risk across markets, property types, economic drivers. Essex did the opposite, concentrating entirely on West Coast apartments. This focus created information advantages (they knew every submarket intimately), operational efficiencies (regional management, centralized maintenance), and market power (in some submarkets, they owned 10% of institutional-quality apartments). As Marcus says, "We'd rather be the best at one thing than mediocre at many things."

The high-quality portfolio strategy deserves special attention. Essex discovered that the gap between premium and commodity apartments was widening. Premium properties attracted residents who paid rent reliably, treated properties well, and stayed longer. The math was compelling: a premium property might cost 30% more to acquire but commanded 40% higher rents with 50% lower turnover. Over a decade, the returns on premium properties dramatically exceeded commodity properties, even accounting for the higher initial cost.

The REIT structure itself became a weapon. REITs must distribute 90% of taxable income as dividends, which sounds like a constraint. But it forced Essex to be disciplined about capital allocation—they couldn't hoard cash for vanity projects. The structure also provided tax efficiency for investors and access to public capital markets. During downturns, when private developers couldn't access capital, Essex could tap public markets or their credit lines, allowing them to be opportunistic buyers.

Capital allocation discipline separated Essex from cowboys who dominated real estate. They had strict underwriting criteria: every acquisition needed to be accretive to FFO within 12 months, generate IRRs exceeding 7%, and fit the supply-constrained thesis. They walked away from hundreds of deals for every one they completed. This discipline meant missing some opportunities, but it also meant avoiding catastrophic mistakes. As Schall notes, "In real estate, avoiding disasters is more important than hitting home runs."

Operational excellence at scale became a massive competitive advantage. Essex discovered that the difference between 95% and 96% occupancy was $15 million in annual revenue. The difference between 24-hour and 48-hour maintenance response was 5% in renewal rates. These tiny optimizations, impossible for smaller operators to achieve, added up to enormous value at portfolio scale. They built proprietary systems, trained specialized staff, and created feedback loops that continuously improved operations.

The timing of transformative acquisitions reveals another lesson: the best deals happen during dislocations. The savings and loan crisis, the dot-com bust, the financial crisis, COVID—each crisis created opportunities for those with capital and conviction. But Essex didn't just buy during downturns; they prepared during upturns, maintaining conservative leverage and liquidity specifically to capitalize on future disruptions. This counter-cyclical thinking required resisting pressure to maximize returns during good times.

Management alignment and culture proved crucial. Essex executives were required to maintain significant stock ownership—typically 10x their annual salary. This wasn't just skin in the game; it was their entire hide. The culture emphasized long-term thinking over quarterly earnings, operational excellence over financial engineering, and team success over individual achievement. They hired locally, promoted internally, and retained key employees for decades. In an industry known for job-hopping, Essex's executive team averaged 15+ years tenure.

The development expertise acquired through BRE added a new dimension. Essex learned that developing for ownership versus sale changed everything. They could use superior materials (lowering long-term maintenance), include amenities that wouldn't pencil for merchant builders (but drove premium rents), and choose locations based on 30-year appreciation potential rather than 3-year profit margins. This patient capital approach to development created assets worth significantly more than their cost.

The technology integration strategy was pragmatic rather than revolutionary. Essex didn't try to become a tech company; they adopted proven technologies that enhanced their core business. Revenue management systems, automated leasing, predictive maintenance—boring but effective tools that improved margins. They avoided shiny objects (remember when everyone thought VR tours would revolutionize real estate?) and focused on solutions that residents actually valued.

Perhaps the most important lesson: patience compounds. Essex held properties for decades, allowing appreciation, rent growth, and operational improvements to compound. They resisted the temptation to flip properties for quick gains. This patience—anathema in today's quick-return culture—created enormous wealth. Properties acquired in the 1990s for $50 million were worth $200 million by 2020, generating cash flow the entire time.

The Essex playbook isn't easily replicable. You can't just decide to own supply-constrained West Coast apartments today—those assets are either unavailable or prohibitively expensive. The regulatory moat that protects Essex also prevents new entrants. The operational excellence took decades to build. The management culture can't be copied from a PowerPoint. In essence, Essex built a business model that gets stronger with time, harder to replicate with age, and more valuable as its markets become more dysfunctional. It's a playbook written over 50 years that would take another 50 years to duplicate—if it could be duplicated at all.

IX. Bear vs. Bull Case

The bear case against Essex writes itself—or so the skeptics would have you believe. Start with the California exodus narrative, that steady drumbeat of headlines about residents fleeing the Golden State for Texas, Florida, or Arizona. U-Haul rental data showing one-way trips out of San Francisco. Tech companies embracing permanent remote work. Population growth slowing to historic lows. For a REIT with 100% exposure to West Coast markets, these trends seem existential. Yet dig deeper, and the narrative gets complicated.

Yes, California lost population in 2020 and 2021—the first recorded declines in history. But who left? Primarily lower-income residents priced out of the housing market, not Essex's target demographic of affluent professionals. The people leaving California earn median incomes around $75,000; the people staying earn $150,000+. Essex doesn't need population growth—it needs affluent population stability. And by that measure, their markets remain robust.

The regulatory risks are real and multiplying. California's statewide rent control law, passed in 2019, caps annual increases at 5% plus inflation. Local jurisdictions are implementing stricter controls—San Francisco's infamous rent control, Los Angeles's emergency COVID protections that became permanent. The political climate grows increasingly hostile to landlords, with tenant protection laws, eviction moratoriums, and relocation payment requirements. For bears, this regulatory tightening represents a slow strangulation of returns.

But here's the paradox: every regulatory restriction that limits rent growth also limits new supply. Developers won't build if returns don't pencil. The same regulations bears cite as risks actually deepen Essex's moat. It's like complaining that a castle's walls are too high while you're safely inside. Yes, rent control limits upside, but it also ensures Essex faces minimal new competition. In markets where replacement cost exceeds $700,000 per unit, who's going to build competing products with rent control risk?

Interest rate sensitivity presents another concern. REITs are often viewed as bond proxies—when rates rise, REIT valuations typically fall. Essex's leverage, while conservative at 35% debt-to-assets, still means higher rates increase borrowing costs. The math is straightforward: every 100 basis point increase in rates costs Essex roughly $30 million annually. In a higher-for-longer rate environment, this headwind persists.

Yet Essex's rate sensitivity is overstated. Unlike bonds with fixed coupons, Essex can raise rents. Their properties have averaged 5% annual rent growth over the past decade, exceeding inflation and offsetting rate impacts. Moreover, higher rates typically slow new construction (developers can't make projects pencil), reducing supply and supporting rent growth. The correlation between rates and REIT performance is real but more complex than simple inverse relationships suggest.

The tech industry concentration risk haunts every bear thesis. The Bay Area's dependence on technology companies—and Essex's dependence on their employees—creates vulnerability. What happens when the next tech crash arrives? We saw previews in 2001 and 2020—rents falling 25%, occupancy dropping to 88%. For a company with 35% of its portfolio in the Bay Area, another tech implosion could be devastating.

But the bull case starts here: tech downturns are temporary, tech dominance is structural. Every Bay Area bust has been followed by a larger boom. The region's combination of universities, venture capital, talent networks, and entrepreneurial culture creates resilience beyond any single cycle. Even if AI displaces some tech jobs, who's better positioned to benefit from AI wealth creation than the Bay Area? Essex isn't betting on specific companies but on the region's innovation ecosystem.

The affordability crisis, paradoxically, strengthens Essex's position. Yes, paying $3,500 for a one-bedroom seems unsustainable. But unsustainable for whom? Not for the software engineer making $300,000, the doctor earning $400,000, or the dual-income couple pulling in $500,000. These are Essex's residents. The affordability crisis prices out Essex's competitors (new supply) and alternatives (homeownership) while leaving their target demographic relatively unaffected.

Competition from single-family rentals and new supply gets mentioned but misunderstands Essex's positioning. Single-family rentals appeal to families wanting yards and schools—not Essex's core demographic of young professionals and empty nesters. New supply in Essex's markets remains minimal. California needs 180,000 new units annually but permits fewer than 80,000. The "construction boom" bears cite is happening in Austin and Phoenix, not Palo Alto and Santa Monica.

The balance sheet strength that bulls celebrate is remarkable. Essex maintains investment-grade ratings from both Moody's and S&P, providing access to capital even during disruptions. Their debt maturities are well-laddered with no significant near-term refinancing needs. They have $1.2 billion in liquidity between cash and credit lines. This isn't just defensive—it's offensive, allowing opportunistic acquisitions when competitors are capital-constrained.

The irreplaceable portfolio represents the ultimate bull argument. Try to replicate Essex's portfolio today—you literally cannot. The properties don't trade (owners hold forever), the land isn't available (already developed), and the permits are impossible (regulatory constraints). Essex owns 62,000 apartments in markets where building 100 new units makes headlines. This isn't just a moat; it's an ocean.

Long-term demographic tailwinds remain powerful despite near-term noise. Millennials, the largest generation in history, are entering prime renting years. The homeownership rate continues declining, driven by affordability challenges and lifestyle preferences. Immigration, when it returns to normal, disproportionately flows to Essex's gateway markets. These aren't trends that reverse with one recession or rate cycle—they're generational shifts.

The experienced management team deserves recognition. Michael Schall has been CEO since 2001, CFO before that. The executive team averages 15+ years tenure. They've navigated the dot-com bust, financial crisis, and COVID. This isn't their first rodeo, and their track record of capital allocation, operational excellence, and cycle navigation inspires confidence. In a business where relationships and local knowledge matter, continuity is valuable.

The development expertise creates value beyond acquisition. Essex's pipeline includes 3,000 units in various stages, each creating value upon completion. In markets where new supply is constrained, the ability to actually deliver new product—navigating the regulatory maze, managing construction costs, achieving certificate of occupancy—is increasingly rare and valuable. These aren't commodity developments but premier properties in irreplaceable locations.

Technology sector resilience surprises bears but shouldn't. Despite headlines about tech layoffs and office vacancies, the fundamental drivers remain intact. AI isn't destroying tech jobs—it's creating new ones, just different ones. The venture capital ecosystem continues funding innovation. The talent wants to live in these markets despite costs. Betting against West Coast tech has been a losing proposition for 40 years; why would that change now?

The return-to-office trend, still developing, could catalyze demand. As companies mandate office presence—even hybrid schedules—proximity to work regains importance. Essex's urban and suburban locations near job centers benefit disproportionately. The "zoom town" phenomenon was real but temporary; the gravitational pull of economic clusters is reasserting itself.

Weighing both cases, the bull thesis seems stronger—not because the bear concerns are invalid, but because they're largely priced in and offset by structural advantages. Essex trades at a discount to net asset value, suggesting markets already discount the risks. Meanwhile, the supply-constrained dynamics that drive long-term value creation continue strengthening. The bear case is about cycles and sentiment; the bull case is about structure and scarcity. In that contest, structure usually wins.

X. Epilogue & "What Would We Do?"

Standing in Essex's Palo Alto headquarters, you can see Stanford University in the distance—that engine of innovation that has powered the Bay Area's growth for generations. It's a fitting view for a company that has spent 53 years betting on West Coast dynamism. But as we conclude this deep dive into Essex Property Trust, the question isn't what they've built—it's what comes next. The housing landscape is evolving, political pressures mounting, and technological disruption accelerating. If we were running Essex, what strategic moves would we make?

First, let's acknowledge what Essex has achieved. From George Marcus's immigrant beginning to today's $20 billion real estate empire, this is fundamentally a story about recognizing structural advantages before they became obvious. Essex didn't create California's housing shortage—they simply positioned themselves to benefit from it. They didn't cause the regulatory constraints—they turned them into competitive moats. This ability to see opportunity where others see obstacles defines great businesses.

The Marcus legacy extends beyond financial returns. He proved that real estate, often dismissed as a crude asset class, could be approached with sophistication and discipline. He demonstrated that geographic concentration could trump diversification if you picked the right geography. Most importantly, he built two successful companies simultaneously—Essex and Marcus & Millichap—showing that entrepreneurial ambition needn't be limited to one venture.

But succession planning looms large. George Marcus is 83. Michael Schall is nearing retirement age. The next generation of leadership faces different challenges—political hostility toward landlords, technological disruption, climate change impacts on coastal properties. The comfortable playbook of the past 50 years may not work for the next 50. New leadership needs to balance respect for what worked with recognition that the world is changing.

If we were running Essex, geographic expansion would be tempting but dangerous. The obvious move—expanding to Austin, Nashville, or Miami—dilutes everything that makes Essex special. These markets have growth but lack supply constraints. You can build apartments in Austin as fast as you can arrange financing. That's a different business—one where Essex has no particular advantage. The discipline to resist geographic diversification, even as every analyst asks why you're not in the Sun Belt, requires enormous conviction.

Asset class diversification presents more interesting possibilities. Essex's expertise in supply-constrained markets could translate to other property types. Medical office buildings in the same restricted California markets face similar dynamics. Life science properties in South San Francisco and San Diego offer exposure to biotech growth while maintaining the supply-constrained thesis. These adjacent expansions leverage existing expertise while reducing concentration risk.

Technology investments deserve careful consideration. The proptech revolution promises to transform real estate operations, but most solutions are expensive distractions. If we ran Essex, we'd focus on three areas: predictive maintenance (reducing costs), revenue optimization (the airline pricing model still has room to run), and resident experience (what actually makes people willing to pay premium rents). We'd avoid the temptation to become a technology company—Essex is a real estate company that uses technology, not the reverse.

The affordable housing opportunity is counterintuitive but compelling. California increasingly requires affordable units in new developments. Rather than viewing this as a tax, Essex could embrace it strategically. Build expertise in workforce housing—apartments for teachers, nurses, firefighters who can't afford market-rate units but earn too much for traditional affordable housing. This middle-income segment is underserved, politically popular, and economically viable with the right subsidies and tax credits.

Climate adaptation represents both risk and opportunity. Essex's coastal properties face long-term sea level rise threats. Their California portfolio faces wildfire risk. But every challenge creates opportunity for those who adapt first. Retrofitting properties for resilience—flood barriers, fire-resistant materials, backup power systems—could differentiate Essex's portfolio. Becoming the recognized leader in climate-adapted apartments could command premium rents from increasingly climate-conscious residents.

The capital allocation framework needs evolution. The traditional REIT model—90% dividend payout—made sense when REITs needed to attract income-focused investors. But today's investors increasingly value growth over current income. If regulations allowed, we'd explore structures that retained more capital for growth while maintaining REIT tax advantages. The ability to compound capital internally, rather than constantly accessing external markets, could accelerate value creation.

Strategic partnerships could unlock value. Rather than acquiring or developing alone, partner with tech companies needing employee housing, universities requiring graduate student apartments, or hospitals needing workforce accommodation. These partnerships provide guaranteed demand, potentially favorable economics, and political cover (it's harder to oppose housing for nurses than luxury apartments).

The political engagement strategy needs sophistication. The industry's traditional approach—fighting every regulation, opposing every tenant protection—has failed catastrophically. If we ran Essex, we'd engage constructively, supporting reasonable regulations while opposing counterproductive ones. We'd invest in community benefits proactively rather than reluctantly. We'd make Essex synonymous with responsible landlordship rather than exploitation. This isn't altruism—it's recognizing that political sustainability is prerequisite for business sustainability.

International expansion seems obvious but isn't. Other supply-constrained markets—London, Sydney, Vancouver—share California's dynamics. But real estate is irreducibly local. The relationships, knowledge, and operational expertise that make Essex successful don't translate internationally. The companies that successfully expanded internationally—Brookfield, Blackstone—did so through massive scale and financial engineering, not operational excellence. That's not Essex's DNA.

The innovation laboratory concept could differentiate Essex. Dedicate 5% of the portfolio to experimenting with new concepts—co-living for young professionals, senior housing for affluent retirees, micro-units for minimalists. Most experiments would fail, but successful concepts could be rolled out portfolio-wide. This systematic innovation could keep Essex ahead of changing preferences while maintaining core portfolio stability.

The vertical integration question deserves revisiting. Essex currently outsources construction, maintenance, and various services. Bringing key functions in-house could improve quality and reduce costs. Imagine Essex-employed maintenance staff who know every property, construction crews who build to Essex standards, technology teams who develop proprietary solutions. The upfront investment would be substantial, but the long-term advantages could be enormous.

Looking ahead, Essex's position in the evolving housing landscape seems secure but not guaranteed. The structural advantages—supply constraints, demographic tailwinds, operational excellence—remain intact. But new challenges—political hostility, climate change, technological disruption—require evolution. The companies that dominate the next 50 years won't be those that rest on past success but those that adapt while maintaining core strengths.

The future of West Coast real estate remains bright despite headlines suggesting otherwise. The innovation economy isn't disappearing—it's evolving. The demographic demand isn't reversing—it's shifting. The supply constraints aren't loosening—if anything, they're tightening. Essex sits at the intersection of these trends, positioned to benefit from continued scarcity, persistent demand, and operational advantages.

If we were running Essex, we'd remember George Marcus's fundamental insight: in real estate, the money isn't made in the boom times—it's made by surviving the busts and being ready for the next boom. We'd maintain financial conservatism, operational excellence, and strategic discipline. We'd resist the siren song of growth for growth's sake. We'd remember that in the apartment business, boring is beautiful, especially when boring means predictable, growing cash flows from irreplaceable assets.

The Essex story isn't ending—it's entering a new chapter. The challenge for future leadership is maintaining what works while adapting to what's changing. The supply-constrained thesis remains valid. The operational excellence remains differentiating. The portfolio remains irreplaceable. These advantages, built over 50 years, won't disappear overnight. But they need nurturing, evolution, and occasional revolution to remain relevant.

As we conclude, it's worth returning to that image of four-year-old George Marcus arriving in America with nothing but ambition. He built not just a company but a template for turning structural constraints into competitive advantages. Essex Property Trust stands as proof that in business, as in life, the obstacles often are the path. The walls that keep others out can protect those already inside. The regulations that constrain supply can guarantee value for existing assets. Sometimes the best strategy isn't to fight the system but to position yourself to benefit from its very dysfunction.

That's the Essex story—a half-century bet that California's inability to solve its housing crisis would make existing housing increasingly valuable. It's a bet that's paid off spectacularly. And as long as California remains California—innovative yet dysfunctional, wealthy yet constrained, desirable yet difficult—it's a bet that will likely keep paying off for decades to come.

XI. Recent News**

Latest Quarterly Earnings and Guidance**

Essex reported exceptional Q4 2024 results with Net Income per share reaching $4.00, up 292.2% from Q4 2023, while full-year Net Income grew 82.6% to $11.54. Core FFO per share increased by 2.3% to $3.92 in Q4 and by 3.8% to $15.60 for the full year. The company achieved same-property revenue growth of 2.6% and NOI growth of 1.7% in Q4 2024. For the full year, same-property revenues grew 3.3% and NOI increased 2.6%.

For 2025, Essex provided guidance with Core FFO projected at $15.56-$16.06 per share, and same-property revenue growth expected between 2.25% and 3.75%. Essex Property Trust Inc forecasts a 3% market rent growth for 2025, with Seattle and San Jose projected to lead the portfolio at approximately 4%. The company has over $1 billion in liquidity and ample sources of available capital, positioning it well for future opportunities.

Recent Acquisitions and Dispositions

In 2024, Essex acquired or increased ownership in 13 apartment communities for $1.4 billion and disposed of one property for $252.4 million. Notable transactions included:

- In September 2024, the company acquired a 50% common equity interest in Century Towers, a 376-unit apartment community in San Jose, CA, for $173.5 million.

- In July 2024, the company acquired a 49.9% common equity interest in Patina at Midtown, a 269-unit apartment community in San Jose, CA, for $117.0 million.

- Subsequent to Q3 2024, the company acquired a 49.9% interest in the BEX II portfolio, comprising four communities totaling 871 apartment homes, for $337.5 million. Concurrently, the company assumed $95.0 million of secured mortgages associated with the portfolio.

- Subsequent to Q3 quarter end, the company sold its 81.5% interest in Hillsdale Garden Apartments, a 697-unit apartment community in San Mateo, CA, for $252.4 million.

The company plans acquisitions of $500M-$1.5B and dispositions of $250M-$750M. The transaction activity year to date results in a reallocation towards the Northern California region with the purchase of newer communities in submarkets where Essex expects lower supply and higher rent growth over the foreseeable future. The match funded transactions are net neutral to the Company's 2025 Core FFO forecast.

Development Pipeline Updates

Essex has a development and predevelopment pipeline with incurred costs of $52.7 million, indicating a commitment to future growth through new community developments. Management sees opportunity adjacent to Oyster Point, a major biotech hub, with costs down and rents showing momentum. They're targeting a 20% spread over acquisition costs, with a projected cap rate in the mid to high 5% range, stabilizing in the high 6% range.

The Company anticipates continued growth in its core markets, with projected 2025 growth in new residential supply expected to be 1% or less of the total housing stock in its operating regions.

Market Commentary from Management

Over the long term, management sees a path for the West Coast apartment markets to continue to outperform the US average, with better job growth and wealth creation driven by centers of innovation combined with limited level of supply growth. In 2024, the West Coast experienced a meaningful uptick in volume, reaching a level close to the pre-COVID average. Although interest rates increased in the fourth quarter, there remains a deep pool of capital eager to acquire properties on the West Coast, and cap rates in the fourth quarter for high quality properties remain con

Leadership insights come from Angela Kleiman, who was appointed CEO in April 2023. She previously served as the Senior Executive Vice President and Chief Operating Officer for the Company from 2021 to 2023 and was the Company's Executive Vice President and Chief Financial Officer from 2015 to 2020.

Regulatory Developments in Key Markets

The company faces potential regulatory impacts in Los Angeles, including an eviction moratorium and rent freeze proposals, which could affect revenue growth. Management continues to monitor these developments while maintaining their long-term conviction in West Coast markets.

The company remains optimistic about immigration policy impacts. The administration's focus is on illegal immigration, which shouldn't impact Essex significantly. The administration appears pro H-1B visa, supporting foreign college students staying in the country. Historically, H-1B visa holders have been a small portion of tenants, and their exit hasn't impacted Essex significantly.

XII. Links & Resources

Essex Property Trust Investor Relations Materials - Official Investor Relations Site: investors.essexapartmenthomes.com - Quarterly Results: investors.essexapartmenthomes.com/investors/financials/quarterly-results/ - SEC Filings: sec.gov/edgar/browse/?CIK=920522

George Marcus Profiles & Interviews - Marcus & Millichap Company History: marcusmillichap.com - Essex Foundation & Leadership: essexapartmenthomes.com/about

BRE Merger Documentation - 2014 Merger Proxy Statement: SEC Archives - Transaction Press Releases: Available via Business Wire archives

West Coast Housing Market Research - California Department of Housing: hcd.ca.gov - Seattle Office of Housing: seattle.gov/housing - UCLA Anderson Forecast: anderson.ucla.edu/centers/ucla-anderson-forecast - USC Lusk Center for Real Estate: lusk.usc.edu

REIT Industry Reports & Analysis - NAREIT (National Association of REITs): reit.com - Green Street Advisors: greenstreet.com - Cohen & Steers Research: cohenandsteers.com - REIT.com Industry Data: reit.com/data-research

Books on Real Estate Investing & REITs - "The Intelligent REIT Investor" by Stephanie Krewson-Kelly and R. Brad Thomas - "Investing in REITs" by Ralph L. Block - "Real Estate Investment Trusts: Structure, Performance, and Investment Opportunities" by Su Han Chan, et al.

Academic Papers on Supply Constraints & Housing - "The Impact of Building Restrictions on Housing Affordability" - Edward Glaeser & Joseph Gyourko - "Regulation and the Rise of Housing Prices in Greater Boston" - Glaeser, Schuetz, and Ward - "Housing Supply and Affordability: Evidence from Rents, Housing Consumption and Household Location" - Baum-Snow and Han

Historical Documents on California Real Estate - California Association of Realtors Historical Data: car.org - Federal Reserve Economic Data (FRED): fred.stlouisfed.org - Census Bureau Housing Statistics: census.gov/topics/housing

Related Podcast Episodes - The Real Estate Guys Radio Show episodes on West Coast markets - BiggerPockets Podcast episodes on apartment investing - Walker & Dunlop's "Walker Webcast" featuring REIT CEOs

Industry Association Resources - National Multifamily Housing Council (NMHC): nmhc.org - California Apartment Association: caanet.org - Apartment List Research: apartmentlist.com/research - Urban Land Institute (ULI): uli.org

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube