Element Solutions Inc: The Hidden Champion of Specialty Chemicals

I. Introduction and Episode Roadmap

Pick up your smartphone. Run your thumb across the smooth glass surface. Somewhere beneath that screen, invisible layers of copper circuitry connect processors to memory, antennas to modems, sensors to controllers. Every single one of those metallic pathways was formed using specialty chemistry—proprietary liquid formulations that deposit, etch, and plate metals at the nanometer scale.

The company that makes much of that chemistry? Element Solutions. Never heard of it? That is precisely the point.

Element Solutions Inc, trading on the NYSE under the ticker ESI, sits at the intersection of nearly every electronics device manufactured on earth. The company's formulations plate the circuit boards inside iPhones, coat the chrome trim on BMWs, protect offshore oil rigs from corrosion, and enable the advanced packaging inside Nvidia's AI chips. With roughly $2.55 billion in revenue in 2025 and a market capitalization that recently surged past $8.6 billion, Element Solutions is one of those rare businesses that touches billions of lives daily while remaining almost entirely unknown to the public.

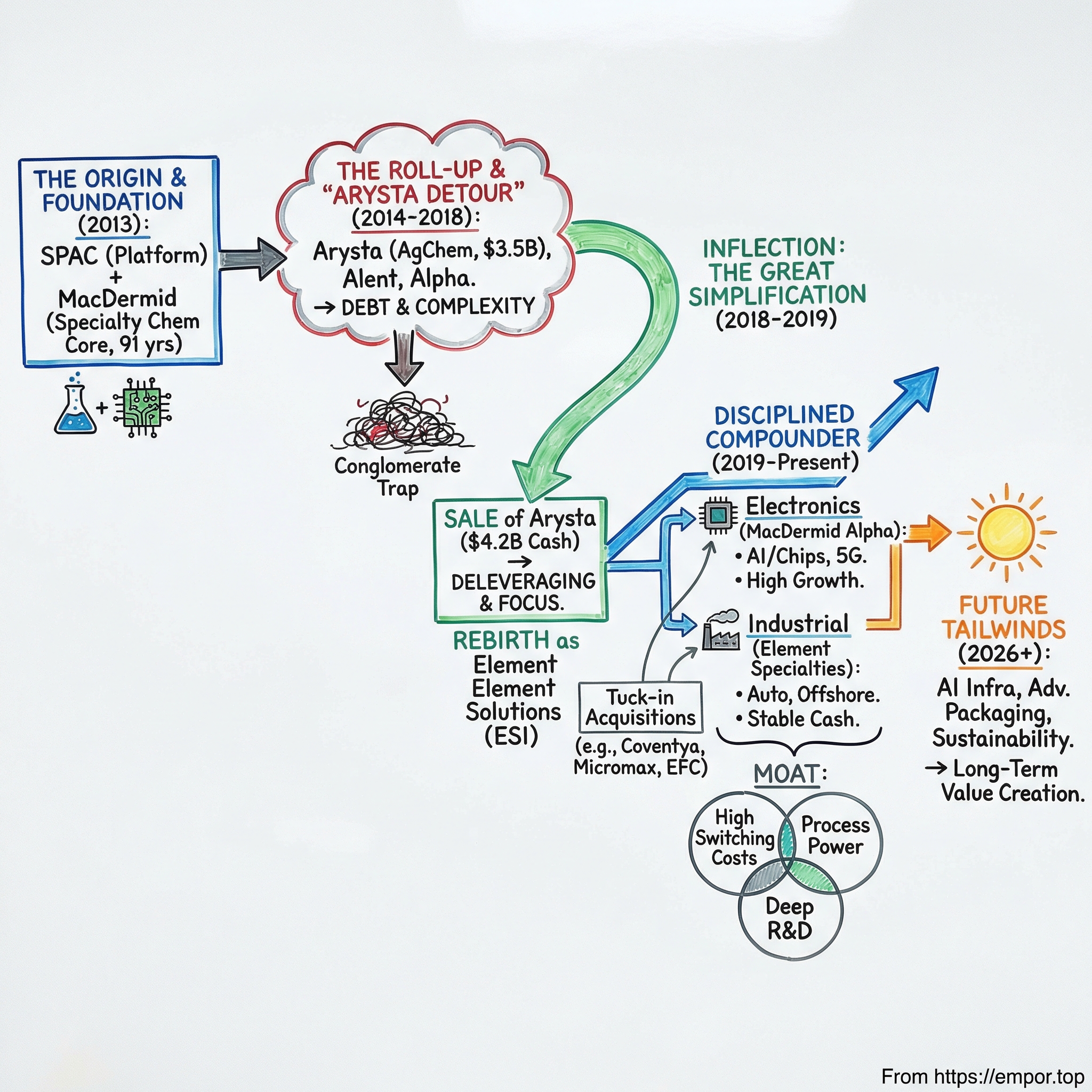

The central question of this story is both simple and extraordinary: How did a blank-check company formed in 2013—backed by two of the most aggressive capital allocators on Wall Street, Bill Ackman and Martin Franklin—transform itself from an over-levered, unfocused conglomerate into a disciplined specialty chemicals compounder?

The answer involves a hundred-year-old Scottish immigrant's metal finishing shop, a disastrous three-and-a-half-billion-dollar detour into agricultural chemicals, a $4.2 billion divestiture that changed everything, and a young CEO who rose from corporate development analyst to the corner office in just five years.

It is not the kind of story that trends on financial Twitter. There are no meme stocks here, no celebrity founders, no moonshot promises. But for investors who care about durable competitive advantages, capital-light business models, and management teams that learn from their mistakes, Element Solutions is one of the most instructive case studies in American public markets today.

This is a story about the power of subtraction—about how selling your biggest business can be the smartest strategic move you ever make. It is a story about technical moats so deep that competitors need years just to qualify as alternative suppliers. And it is a story about boring businesses that compound quietly while the market chases the next shiny object.

Think of specialty chemicals like the ingredients in a master chef's signature sauce. The raw materials—vinegar, oil, herbs—are available to anyone at any grocery store. But the precise proportions, the sequence of addition, the temperature curves, the aging process? That recipe took generations to develop, and it cannot be reverse-engineered by tasting the final product. Element Solutions sells the equivalent of those recipes to the world's most demanding manufacturers. And once a factory has calibrated its entire production line around a specific formulation, switching suppliers is about as appealing as rebuilding the kitchen from scratch.

The themes that run through this narrative are timeless: focus beats diversification, operational excellence outlasts financial engineering, and century-old customer relationships are worth more than any patent. Along the way, we will dissect the roll-up playbook that built this company, the inflection points that nearly broke it, and the competitive dynamics that make specialty chemicals one of the most attractive corners of the industrial economy.

To understand where Element Solutions is going, we need to start with the man who dreamed it into existence—and the audacious bet he made in the spring of 2013.

II. The Franklin-Ackman Origin Story and Platform's Genesis (2013-2015)

Sir Martin Franklin has a type.

The London-born dealmaker, who emigrated to the United States at fifteen and settled in Harrison, New York, built his career on a deceptively simple formula: find fragmented industries filled with small, decent businesses that generate steady cash flow, roll them up under professional management, extract operational synergies, and let compounding do the rest. By the time he turned his attention to specialty chemicals, Franklin had already executed this playbook to spectacular effect—twice.

His first major success came in the optical industry. In the early 1990s, Franklin acquired a small chain of eyecare stores and built it into Benson Eyecare through a series of acquisitions. When he sold the company in 1996, investors earned more than twenty-three times their money—an 1,800 percent return that established Franklin as one of the sharpest roll-up artists of his generation. To put that in perspective, a $100,000 investment in Benson Eyecare would have returned $2.3 million. The optical industry was fragmented, localized, and ripe for consolidation—classic Franklin territory.

But it was his second act that cemented his legend. In 2001, Franklin founded Jarden Corporation with roughly $300 million in revenue. Over the next fifteen years, he assembled a portfolio of more than 120 consumer brands—Coleman camping gear, Sunbeam appliances, Rawlings sporting goods, Marmot outdoor apparel, K2 skis—growing the company to over $10 billion in revenue and 35,000 employees. Key deals included the $845 million acquisition of American Household (which brought in Coleman and Sunbeam) in January 2005, and the $1.2 billion purchase of K2 Sports in August 2007.

When Newell Brands acquired Jarden in April 2016, Franklin's investors had earned more than 5,000 percent on their money. His acquisition philosophy was characteristically blunt: "We've made about 15 acquisitions but there are probably 300 that we could have done but didn't. We don't buy a business unless it adds to earnings up front. People use synergies as an excuse to overpay for something."

That quote tells you everything about how Franklin thinks. He is not a visionary in the Silicon Valley sense—he does not imagine futures and will products into existence. He is a value engineer. He sees existing cash flows that can be acquired, improved, and scaled. He is allergic to paying for potential.

And he has an almost preternatural discipline about walking away from deals that do not meet his criteria, even when the bankers and board members are urging him forward. At twenty-four, Franklin and his father had taken control of DRG, a company with over 13,000 employees, and were tasked with breaking up the conglomerate—early training in the art of corporate restructuring that would prove eerily relevant decades later at Platform.

In April 2013, with Jarden still in full swing, Franklin launched his next vehicle: Platform Acquisition Holdings Limited, a special purpose acquisition company incorporated in the British Virgin Islands and listed on the London Stock Exchange on May 22. The SPAC raised approximately $905 million in gross proceeds, with shares priced at $10 each. For context, this was 2013—years before the SPAC boom of 2020-2021 turned blank-check companies into a punchline. At the time, a SPAC backed by operators with Franklin's track record was a genuinely compelling proposition.

This was not Franklin's first SPAC rodeo. In April 2012, he had partnered with Bill Ackman's Pershing Square Capital Management and Nicolas Berggruen's Berggruen Holdings on Justice Holdings, a London-listed SPAC that acquired a large stake in Burger King from 3G Capital for $1.4 billion.

That deal had worked out well for everyone involved. Justice Holdings was dissolved, Pershing Square and Berggruen became investors in Burger King, and the chain was relisted on the NYSE. The gang was back together for a new hunt—this time in a very different industry.

Ackman, through Pershing Square, would eventually disclose a 30.9 percent stake in Platform—33.3 million shares—making this one of his largest concentrated bets. For Ackman, who is known for taking high-conviction positions in companies he believes are undervalued or transformable, specialty chemicals offered an attractive combination: high barriers to entry, sticky customer relationships, and fragmented market structures that rewarded consolidation.

Franklin found his target with remarkable speed. On October 10, 2013, Platform announced an agreement to acquire MacDermid, Incorporated for approximately $1.8 billion plus up to $100 million in contingent consideration. The deal closed just three weeks later, on October 31.

MacDermid was no ordinary chemical company—it was a 91-year-old institution, a global leader in specialty chemical formulations serving electronics manufacturers, graphic arts companies, oil producers, and industrial finishers. With over 2,000 employees and roughly 3,500 customers across 24 countries, MacDermid was exactly the kind of entrenched, technically complex business that Franklin believed could serve as the foundation for a much larger platform.

Court Square Capital Partners had taken MacDermid private in 2007 for about $1.2 billion, meaning Franklin was paying a meaningful premium. But he was paying for something that private equity firms rarely possess the patience to fully exploit: a business with deeply embedded customer relationships, proprietary formulations refined over nearly a century, and the kind of technical switching costs that make customer churn almost nonexistent. For a roll-up artist, this was the perfect foundation—a base of stable, recurring revenue from which to bolt on additional acquisitions.

Why specialty chemicals specifically? The answer comes down to unit economics that most investors overlook. In commodity chemicals, you sell large volumes of standardized products at thin margins, and you compete primarily on price and logistics. A commodity chemical buyer can call three suppliers, get quotes, and switch to the cheapest option within weeks. In specialty chemicals, the dynamic is completely different. You sell smaller volumes of customized formulations at fat margins, and you compete on technical performance, reliability, and service. A specialty chemical customer that wants to switch suppliers faces months of requalification testing, potential production disruptions, and the risk that the new formulation will not perform identically to the old one under the specific conditions of their manufacturing process.

Consider the economics from the customer's perspective: the specialty chemicals in a printed circuit board might cost a few cents per board, but that board goes into a smartphone that sells for $1,000. If a new plating chemistry causes even a 0.1 percent increase in defect rates, the cost of scrap and warranty claims dwarfs any savings on chemical purchases.

This asymmetry—low cost of the product, high cost of failure—creates the kind of pricing power that commodity chemical companies can only dream about. The procurement department at a major electronics manufacturer does not spend its time trying to shave pennies off the plating chemistry budget. It spends its time making sure the plating chemistry works perfectly, every time, at scale. Price is almost an afterthought.

That stickiness is what makes specialty chemicals such an attractive business model for a roll-up strategy. Acquire the business, inherit the customer relationships, and enjoy recurring revenue that is nearly as predictable as a subscription software business, but with the added protection of physical switching barriers.

Following the MacDermid acquisition, the company renamed itself Platform Specialty Products Corporation and moved its listing to the New York Stock Exchange under the ticker PAH. The SPAC structure had served its purpose as a capital-raising vehicle; now Franklin wanted the credibility and liquidity of a major U.S. exchange listing. The message to the market was unmistakable: this was no longer a blank-check vehicle waiting for a deal. This was an operating company with a world-class asset at its core and a mandate to acquire more.

But before we trace the acquisition spree that followed, it is worth pausing to appreciate just how deep the roots of these heritage businesses ran—because their histories explain the technical moats that make Element Solutions so difficult to dislodge today.

III. The Heritage Companies: Roots Going Back a Century

Waterbury, Connecticut, 1922. A young Scottish immigrant named Archie J. MacDermid opened a small metal finishing business in a factory town already famous for its brass mills and clockmaking shops. The Connecticut River Valley in the early twentieth century was America's manufacturing heartland—a dense cluster of metalworking shops, munitions factories, and precision instrument makers who all shared one common need: reliable chemical processes to coat, protect, and finish their metal products.

MacDermid's insight was practical. The existing solutions were crude and inconsistent. He began developing proprietary formulations—chemical recipes that could deposit thin, uniform layers of metal onto surfaces with precision and repeatability. What started as a local service business grew, decade by decade, into a global operation.

Each generation of MacDermid chemists built on the work of their predecessors, incrementally improving bath compositions, extending bath life, reducing waste, and adapting formulations to new substrates and applications. By the time Platform acquired the company ninety-one years later, MacDermid's formulations were embedded in manufacturing processes at thousands of factories worldwide. The chemistry had evolved from basic metal finishing into sophisticated solutions for printed circuit board fabrication, semiconductor packaging, and industrial surface treatment. But the core competitive advantage remained unchanged from Archie MacDermid's day: proprietary recipes, refined through decades of iteration, that customers could not easily replicate or replace.

Across Connecticut in New Haven, another origin story was unfolding. An auto-body shop owner, a chemist, and a lacquer salesman pooled their expertise in a small garage to develop electroplating chemistry—the science of using electrical current to deposit thin metal coatings onto surfaces.

To understand what electroplating actually involves, imagine dipping a piece of metal into a bath of dissolved metal salts and running electricity through the solution. The electrical current causes metal ions in the liquid to migrate toward the submerged part and deposit onto its surface, atom by atom, creating a thin, uniform coating. The challenge is controlling this process precisely: the coating must be uniform in thickness, adhere perfectly to the substrate, have the right crystalline structure for its intended purpose, and be deposited at a rate that makes manufacturing economically viable. Getting all of these variables right simultaneously requires extraordinarily precise chemistry—the exact concentration of metal salts, the pH of the bath, the current density, the temperature, the presence of proprietary additives that control grain structure and leveling. This is what Enthone perfected.

Their company grew from that garage into a global supplier of plating chemistry for the electronics, automotive, and industrial sectors. Enthone eventually became part of Britain's Cookson Group, which demerged its electronics division in 2012 to form Alent plc. The chemistry Enthone developed in that New Haven garage now forms the backbone of Element Solutions' semiconductor, circuitry, and industrial plating businesses.

The third lineage traces back even further. In the late nineteenth century, a metal smelting operation called I. Shonberg Inc operated out of Jersey City, New Jersey. Over time, it evolved into Alpha Metals, a pioneer in solder alloys, fluxes, and interconnect materials—the substances that physically bond electronic components to circuit boards.

Modern solder paste is a carefully engineered mixture of microscopic metal particles suspended in a flux medium—a chemical compound that cleans oxide films from surfaces and promotes wetting, ensuring the molten solder flows evenly across the contact points. The particle size distribution, the alloy composition, the flux chemistry, and the rheological properties—how the paste flows and holds its shape during printing—all determine whether the final solder joint will be reliable over decades of thermal cycling, vibration, and electrical stress. Alpha Metals industrialized this science, developing solder pastes and fluxes that enable the assembly of billions of devices every year. Like Enthone, Alpha eventually became part of Alent plc. Today, the Alpha and Kester brands are central to Element Solutions' Electronics segment.

Why does this history matter for investors evaluating the company in 2026? Because specialty chemicals are not like software or consumer goods—you cannot disrupt them with a clever algorithm or a viral marketing campaign. These formulations are the product of century-long accumulation: thousands of incremental improvements, proprietary process knowledge passed down through generations of chemists, and customer relationships built on decades of collaborative problem-solving. The DNA of specialty chemicals is complexity—multi-step processes with dozens of interdependent variables, where getting one parameter wrong can scrap an entire production batch worth millions of dollars. That complexity is the moat.

By 2015, all three of these heritage businesses—MacDermid, Enthone, and Alpha—would be united under one corporate roof. But the path to that consolidation would take a dramatic and costly detour through the agricultural chemicals industry.

IV. The Roll-Up Years and the Arysta Detour (2014-2018)

With MacDermid secured and the NYSE listing complete, Martin Franklin hit the accelerator. Platform Specialty Products was designed to be an acquisition machine, and in 2014, the dealmaking pace bordered on frenetic.

The company completed three acquisitions in quick succession that fall: Agriphar closed on October 1, Chemtura AgroSolutions on November 3, and then came the big one—Arysta LifeScience.

On October 20, 2014, Platform announced the acquisition of Arysta LifeScience Limited from Permira's funds for approximately $3.51 billion—nearly double what the company had paid for MacDermid. Arysta was a leading crop protection and life science business with roughly $1.5 billion in annual revenue, selling pesticides, herbicides, and other agricultural chemical products globally. The deal was funded through a combination of $2.91 billion in cash and $600 million of Series B convertible preferred stock. When the transaction closed on February 17, 2015, Platform had effectively doubled its size overnight—but in an entirely different industry.

Why did Franklin and Ackman pivot to agricultural chemicals? The logic, at least on paper, was seductive. AgChem shared some of the characteristics they prized: fragmented markets, technical products, recurring demand driven by the biological imperative of feeding a growing planet. And the financial engineering was appealing—Arysta's scale would allow Platform to lever up and generate enormous free cash flow to fuel further acquisitions. The Arysta deal, combined with Agriphar and Chemtura AgroSolutions, created Platform's Agricultural Solutions segment—a substantial business in its own right.

But in practice, the two businesses had almost nothing in common. Specialty chemicals for electronics manufacturing and crop protection chemicals operate on fundamentally different cycles, serve different customers, require different regulatory expertise, and demand different technical capabilities. An electronics plating chemical is sold to a factory that operates year-round with predictable demand tied to consumer electronics cycles. A crop protection chemical is sold to farmers and distributors on seasonal planting cycles that can be devastated by weather, trade disputes, government subsidies, and commodity prices. The margin structures differ, the competitive dynamics differ, the R&D timelines differ, and the customer relationships have entirely different characteristics. The synergies were a mirage.

To make matters more complex, Platform was simultaneously executing a second major deal that, unlike Arysta, was strategically brilliant. On July 13, 2015, the company announced a recommended offer for Alent plc, the London-listed specialty chemicals company that housed both Enthone and Alpha Metals. The total value was approximately $2.3 billion including net debt. The acquisition closed on December 1, 2015, bringing two of the most respected brands in electronics chemistry into the Platform fold.

That same autumn, Platform also acquired the Electronic Chemicals and Photomasks businesses from OM Group—the latter continuing today as Compugraphics, an active Element Solutions brand. Together, these transactions created MacDermid Performance Solutions—the combined entity that brought MacDermid, Enthone, Alpha, and Compugraphics under one operating umbrella.

But here was the problem: Platform now had to manage all of this simultaneously. The company was operating a global specialty electronics and industrial chemicals business, a suite of agricultural chemicals brands, and a balance sheet groaning under the weight of roughly $6 billion in acquisition debt accumulated in barely two years.

The complexity was staggering. Management bandwidth was stretched across industries that had nothing to do with each other. A chemical engineer optimizing plating bath formulations for semiconductor fabs had zero overlap with an agronomist evaluating herbicide efficacy in Brazilian soybean fields. The corporate overhead required to manage both portfolios—separate regulatory teams, separate sales organizations, separate R&D pipelines, separate supply chains—consumed resources that could have been invested in either business individually.

There was also a subtler problem that is easy to overlook: capital allocation confusion. Every dollar of free cash flow had to be allocated between two businesses with fundamentally different investment profiles. Should Platform invest in a new plating chemistry R&D lab that would deepen its moat in electronics? Or should it fund a distribution expansion for Arysta's herbicide line in Southeast Asia? These decisions require completely different analytical frameworks, different risk assessments, and different return expectations. A management team that is expert in one domain is not necessarily competent in the other. The conglomerate structure forced executives to make choices they were not equipped to make, or worse, to avoid making choices at all by spreading capital thinly across both portfolios.

The market noticed. Platform's stock, which had traded above $25 in early 2015, steadily declined as investors questioned the strategic coherence of the portfolio and worried about the debt load. Analyst coverage was confused—was this a specialty chemicals story or an agricultural chemicals story? Which peer group should it be compared to? How should the conglomerate discount be assessed? Specialty chemicals peers like Atotech and Enthone's former parent Cookson traded at premium multiples reflecting their sticky business models. Agricultural chemicals peers traded at lower multiples reflecting commodity exposure and cyclicality. Platform, stuck between two worlds, got the worst of both valuations.

The roll-up thesis that had worked so brilliantly for Franklin at Jarden was stumbling because the portfolio lacked the operational coherence that makes consolidation work. At Jarden, every brand—from Coleman to Sunbeam—served the same broad consumer products channel and could share distribution, sourcing, and back-office infrastructure. At Platform, the agricultural and specialty chemicals businesses shared nothing except a corporate parent and a pile of debt.

By 2017, it was becoming clear that something had to give. The question was not whether Platform would simplify its portfolio, but how—and whether management would have the courage to part with a business it had spent $3.5 billion to acquire barely three years earlier.

V. Inflection Point Number One: The Great Simplification — Selling Arysta (2018)

In the world of corporate strategy, the hardest decision is rarely what to buy. It is what to sell.

Executives build empires; they do not willingly dismantle them. The ego investment in a major acquisition—the board presentations, the due diligence, the integration planning, the public pronouncements about strategic rationale—makes reversal psychologically agonizing. Behavioral economists call this the endowment effect: once you own something, you value it more highly than the market does, simply because it is yours. The sunk cost fallacy compounds the problem—the billions already spent on Arysta created an almost gravitational pull against divestiture, as if selling would somehow "waste" the original investment rather than recognizing it as an irrecoverable cost.

And yet, on July 20, 2018, Platform Specialty Products announced that it had agreed to sell Arysta LifeScience to UPL Corporation Limited for $4.2 billion in cash, on a debt-free, cash-free basis.

The announcement was a thunderclap. Arysta was Platform's largest business by revenue, generating approximately $2 billion in annual operating revenue with adjusted EBITDA of roughly $424 million for the twelve months ended March 2018. The sale price represented an enterprise value of approximately 9.9 times EBITDA—a full exit at a respectable multiple that valued the business at a meaningful premium to what Platform had paid just four years earlier.

But the financial math alone does not capture the significance of this decision. Selling Arysta was an admission that the original diversification strategy had been wrong. It was Franklin and the board effectively saying: we made a mistake, and the best path forward is to undo it completely rather than continue managing a business that does not fit. In an era when corporate executives routinely cling to failed strategies for years—tweaking, restructuring, replacing management teams, doing anything to avoid admitting error—this kind of decisive reversal was remarkable. It takes a particular kind of confidence to tell your shareholders, your employees, and the market: we bought the wrong thing, and here is what we are going to do about it.

The strategic logic was compelling on multiple dimensions. Agricultural chemicals and specialty electronics chemicals are fundamentally different business models. AgChem products are closer to commodities—they compete on price, face generic competition as patents expire, and operate on agricultural planting cycles vulnerable to weather, trade disputes, and regulatory changes. Specialty electronics chemicals, by contrast, are bespoke formulations sold on technical performance, protected by switching costs and qualification requirements rather than patents, and tied to secular growth in electronics complexity. The margin profiles, growth trajectories, and capital allocation requirements were so different that managing both under one roof created more friction than synergy.

For UPL, the acquisition was transformational. The Indian agrochemical company combined Arysta with its existing business to become the fifth-largest agricultural chemicals maker in the world—a global scale player with the distribution reach, product portfolio, and geographic diversity to compete with giants like Syngenta, Bayer, and BASF. UPL could extract genuine synergies—geographic overlap, distribution leverage, formulation sharing—that Platform never could. This was a textbook case where the asset was worth more in someone else's hands.

The cash windfall was equally significant. With $4.2 billion in proceeds, Platform could dramatically deleverage its balance sheet, repurchase shares, and refocus capital allocation on the specialty chemicals businesses where it had genuine competitive advantages. The company simultaneously announced up to $750 million in share repurchase authorization—a clear signal that management believed the remaining business was undervalued by a market grown skeptical during the conglomerate years.

There were internal debates, of course. Some argued that Arysta's revenue scale and cash flow generation were valuable in their own right, and that selling at what might prove to be a cyclical trough could leave money on the table. The agricultural chemicals business was generating real cash flow—$424 million in EBITDA was not a trivial number, and there was a credible long-term thesis about rising global food demand driving structural growth in crop protection.

Others pointed out that UPL was paying a fair but not extravagant multiple, and that if Platform had more patience, it might extract a higher price from a different buyer down the road. The debate reflected a genuine tension between short-term strategic clarity and long-term financial optionality.

But the counterargument was simple and ultimately decisive: Platform was not the right owner for this business. Every dollar of management attention spent on Arysta was a dollar not spent improving the electronics and industrial chemicals portfolio. Every turn of leverage dedicated to carrying the agricultural business was a turn that could not be deployed for bolt-on acquisitions in specialty chemicals.

And the market had made its verdict clear—the conglomerate discount was destroying shareholder value. The sum of Platform's parts, valued separately, was almost certainly worth more than the whole. Selling Arysta was not just a strategic decision; it was a capital markets decision to unlock trapped value.

The Arysta sale is, in retrospect, the single most important strategic move in the company's history. It transformed a struggling, over-levered conglomerate into a focused specialty chemicals business with a clean balance sheet and a clear growth mandate.

The lesson for investors and executives alike is powerful: sometimes the most value-creating thing you can do is let go of something valuable but misaligned. Arysta was not a bad business—UPL has built it into a successful global platform. It was simply the wrong business for Platform to own.

But executing that transformation required more than just closing a deal. It required a complete reinvention of the company's identity, strategy, and leadership.

VI. Inflection Point Number Two: Rebirth as Element Solutions and the Leadership Transition (January 2019)

On January 28, 2019, Platform Specialty Products made a series of announcements that collectively amounted to a corporate rebirth.

The Arysta sale to UPL would close on January 31. The company would change its name to Element Solutions Inc and begin trading on the NYSE under the ticker ESI effective February 1. CEO Rakesh Sachdev would retire upon closing, remaining on the board but stepping away from day-to-day operations. And stepping into the chief executive role would be Benjamin Gliklich, a thirty-something executive who had risen through Platform's ranks with startling speed.

The name change alone spoke volumes. "Platform Specialty Products" carried the baggage of the SPAC era, the Arysta detour, and the over-levered conglomerate years. It sounded like what it was—a financial vehicle designed to acquire things. "Element Solutions" was something entirely different. It evoked chemistry, precision, the periodic table—a company defined by what it makes, not how it buys. The rebranding was not cosmetic. It signaled a fundamental shift in identity from acquisition machine to operating company. In the specialty chemicals world, where customers care deeply about technical credibility, having a name that sounds like a chemicals company rather than a private equity vehicle matters more than outsiders might think.

But the most consequential change was at the top.

Benjamin Gliklich's appointment as CEO was, on its surface, an unconventional choice. He was young—still in his early thirties at the time—and had joined Platform barely five years earlier without a background in chemical engineering or manufacturing.

His resume read more like that of a private equity partner than a chemical company CEO: undergraduate degree cum laude from Princeton, MBA with distinction from Columbia Business School, investment banking at Goldman Sachs, then growth equity investing at General Atlantic, one of the world's preeminent growth-oriented private equity firms. In an industry where CEOs typically rise through decades of plant management and technical leadership, appointing a financial professional in his early thirties was a bold bet.

What the resume did not capture was the extraordinary breadth of experience Gliklich had accumulated inside Platform in a remarkably compressed period.

He joined in May 2014 as Director of Corporate Development—effectively the person evaluating and executing acquisitions. Within eight months, by January 2015, he had been promoted to Vice President of Corporate Development, Finance, and Investor Relations. By October 2015—barely eighteen months after joining—he was Chief Operating Officer. By April 2016, he held the title of Executive Vice President of Operations and Strategy.

Four titles in two years. Each one represented a significant expansion of responsibility—from deal evaluation to finance oversight to operations management to full strategic leadership.

This was not a career path that happens by accident or by politics. It happens when someone demonstrates, in real time, that they can add value at each successive level of responsibility. Gliklich had been involved in every major strategic decision the company made, from the Alent acquisition to the OM Group deal to the Arysta sale deliberations. He understood the portfolio at a granular level—which businesses generated the best returns on capital, which customer relationships were stickiest, where the operational improvement opportunities lay, and which segments were worth investing in versus divesting.

The new leadership structure formalized around what the company called the "Office of the Chairman"—Martin Franklin as Executive Chairman providing strategic guidance and capital allocation oversight, Gliklich as CEO driving day-to-day operations and strategy, and Scot Benson as President and COO managing the operating businesses. This tripartite structure was deliberate: Franklin's deal experience and investor credibility, Gliklich's strategic vision and financial acumen, and Benson's operational expertise in running chemical plants and managing customer relationships. The combination ensured continuity with the Franklin era while empowering a new generation of leadership oriented toward operational excellence rather than deal volume.

The strategic restructuring went deeper than leadership. Previously, the specialty chemicals businesses had been reported as a single segment called Performance Solutions. Under the new structure, the company separated reporting into two distinct segments: Electronics (encompassing assembly solutions, circuitry solutions, and semiconductor solutions) and Industrial & Specialty (covering surface finishing, offshore fluids, and related businesses).

This was not just an accounting change—it was a statement of strategic clarity. By breaking out the Electronics segment, management was telling investors exactly where the growth engine was and inviting them to evaluate it on its own merits. Investors could now see, for the first time, that the electronics business was growing faster, carried higher margins, and had more attractive secular tailwinds than the industrial portfolio. That transparency was itself a form of value creation.

The articulated strategy was equally crisp: Element Solutions would pursue a "less levered, more nimble and more efficient business profile" focused on "organic growth and measured opportunistic acquisitions." Every word in that formulation was chosen carefully. "Less levered" was a direct repudiation of the Platform years when debt had constrained strategic flexibility. "More nimble" acknowledged that the conglomerate structure had been a drag on decision-making speed. "Organic growth" signaled that the company would no longer rely on acquisitions to hit its numbers—a crucial shift for a company whose DNA had been M&A. And "measured opportunistic acquisitions" drew a clear line between the bolt-on tuck-ins the new management favored and the transformational mega-deals that had nearly sunk the company.

The preliminary financial results disclosed alongside the transformation revealed the remaining business: approximately $2.05 billion in net revenues from continuing operations and adjusted EBITDA of about $435 million, implying a margin just above 21 percent. These were the economics of a genuinely attractive specialty chemicals business—not world-beating by specialty standards, but solid, with clear room for improvement through operational focus and portfolio optimization.

To put these numbers in context: a 21 percent EBITDA margin in specialty chemicals is respectable but not exceptional. The best-in-class specialty chemicals companies—think Ecolab, Sherwin-Williams at their peaks—can achieve margins in the mid-to-high twenties. The gap between Element Solutions' starting position and best-in-class represented a clear runway for margin improvement through operational focus, pricing discipline, and portfolio mix optimization. The fact that management articulated this gap explicitly, rather than declaring victory on day one, was itself a signal of strategic maturity.

The cultural transformation was perhaps harder to see from the outside but equally important. Under the Platform model, the organization was oriented around deals—identifying targets, negotiating terms, integrating acquisitions. The incentive structures, the organizational energy, the career paths all pointed toward M&A. Under Element Solutions, the culture shifted toward operations—improving yield rates, deepening customer relationships, accelerating new product development, expanding margins through manufacturing efficiency.

It was the difference between a company that grows by buying revenue and one that grows by earning it.

By July 2020, Gliklich's title would expand to include President alongside CEO, consolidating operational authority and signaling that the leadership transition was complete and successful. The speed of his ascent and the confidence the board placed in him spoke to something beyond mere competence—it reflected a recognition that the company's next chapter required a different kind of leader, one who could balance the financial sophistication of a private equity background with the operational intensity of running a global manufacturing business.

The question facing investors in early 2019 was straightforward: could this young CEO, this new brand, this simplified portfolio actually deliver on the promise? The answer would unfold over the next six years through a disciplined, methodical playbook that turned Element Solutions from a turnaround story into a genuine compounder.

VII. The Post-Transformation Playbook: Disciplined Growth (2019-2025)

If the Platform years were defined by transformational deals measured in billions, the Element Solutions era has been defined by tuck-in acquisitions measured in tens and hundreds of millions—each one carefully selected to extend the company's technical capabilities into adjacent markets or deepen its position in existing ones.

The shift in acquisition philosophy tells you everything about how the company changed. Under Franklin's original vision, the goal was to build a platform through large, portfolio-diversifying acquisitions. Under Gliklich, every deal had to meet a specific set of criteria: it had to be in an adjacent technology or market that management already understood, it had to be integrable into existing operations, and the synergy potential had to be identifiable and achievable. No more bets on unfamiliar industries.

The first notable deal came in July 2020, when Element Solutions acquired DMP Corporation, a premier provider of turnkey wastewater treatment and recycling solutions founded in 1971. The acquisition launched a new business called MacDermid Envio Solutions, focused on reducing the environmental impact of manufacturing processes through proprietary water treatment and metals recycling technology.

The strategic intent was revealing: as environmental regulations tighten globally and manufacturers face growing pressure to reduce water consumption and chemical waste, the demand for sophisticated treatment solutions is accelerating. By acquiring DMP, Element Solutions positioned itself to sell not just the chemicals that go into the plating bath but also the systems that clean up afterward—capturing more of the customer's total process spend and deepening the relationship at every step.

The following year brought a flurry of carefully chosen deals. In May 2021, the company acquired H.K. Wentworth Group, a UK-based manufacturer of electro-chemicals whose flagship brand, Electrolube, was a recognized name in electronic chemicals, LED manufacturing, and automotive applications. The price was approximately $60 million for a business generating about $44 million in annual revenue, with manufacturing facilities in the UK, India, and China and distribution in over 55 countries. This was a tuck-in in the purest sense—a profitable niche business with strong brand recognition that could be bolted onto the existing portfolio with minimal integration complexity.

Four months later came the largest post-transformation deal: Coventya, a global specialist in metal finishing chemical technologies serving more than 60 countries. The price was approximately EUR 420 million, or roughly $511 million including the assumption of existing debt. Coventya was generating about EUR 160 million in annual sales with adjusted EBITDA above EUR 30 million, and management expected at least EUR 13 million in annual synergies within two years. The purchase multiple of mid-teens EV/EBITDA pre-synergies dropped to approximately 10 times on a synergy-adjusted basis—well within the range specialty chemicals investors consider reasonable for a strategic acquisition.

Here is what made the Coventya deal particularly elegant: before the acquisition, Coventya was a direct competitor in metal finishing. After, its customer relationships, formulation expertise, and geographic reach were folded into Element Solutions' operations—simultaneously eliminating a rival and expanding the company's footprint in automotive, fashion, construction, and aerospace markets. It was consolidation that served the dual purpose of revenue addition and competitive neutralization.

Smaller but strategically significant deals followed. In January 2022, Element Solutions acquired HSO Herbert Schmidt, a German developer of surface finishing technology founded in 1936 in Solingen. HSO's specialization in environmentally sustainable plating-on-plastics applications—and its certification as climate-neutral in 2021—reflected the growing importance of sustainability in the company's product development strategy.

In mid-2023, the company completed a semiconductor-focused deal that, while small in dollar terms, was potentially transformative in strategic significance. The acquisition of Kuprion, Inc. for approximately $16 million net of cash brought Element Solutions a next-generation nano-copper technology called ActiveCopper.

To understand why this matters, consider the challenge facing semiconductor packaging engineers: as chips pack more transistors into smaller spaces, the interconnections between chip components generate more heat and face greater thermal stress. Traditional tin-based solder connections expand and contract at different rates than the silicon they connect, creating reliability problems over time—imagine a bridge where the steel beams and concrete deck expand differently in summer heat, eventually cracking the joints. Copper interconnects perform better—they conduct electricity and heat more efficiently and match silicon's thermal expansion characteristics more closely. But depositing copper at the nanometer scale in manufacturing-friendly processes is extraordinarily difficult. Kuprion's technology solves this problem. The upfront cost was modest, with additional milestone payments tied to product qualification and revenue through 2030, but the addressable market—advanced packaging for AI chips, electric vehicles, 5G infrastructure, and data centers—could be enormous.

Portfolio optimization was not limited to acquisitions. In September 2024, Element Solutions announced the sale of MacDermid Graphics Solutions—the flexographic printing plate business that had been part of the original MacDermid acquisition back in 2013—to XSYS. The deal closed on February 28, 2025 for net proceeds of $323 million, generating a gain of $72 million. Management deployed $200 million of those proceeds to prepay term loans, reducing outstanding principal from $1.04 billion to $836 million. The graphics business was perfectly viable but non-core. Selling it simplified the portfolio, strengthened the balance sheet, and freed management attention for higher-growth opportunities.

The transformation's success received external validation on March 24, 2025, when Element Solutions was added to the S&P SmallCap 600 Index, replacing Wabash National. Index inclusion triggers automatic buying from the hundreds of billions in assets that track the benchmark and signals institutional credibility.

Through all of this, balance sheet discipline remained a constant. By year-end 2025, net leverage had declined to just 1.8 times adjusted EBITDA—providing substantial firepower for the next phase. That phase arrived quickly: in early 2026, Element Solutions completed two significant acquisitions. On January 2, the company closed on EFC Gases & Advanced Materials for approximately $369 million—a provider of high-purity specialty gases for semiconductor manufacturing. On February 2, it completed the acquisition of Micromax from Celanese for approximately $500 million—a global supplier of advanced electronics inks and pastes.

Together, these deals were expected to contribute roughly $70 million in annual EBITDA and be over 7 percent accretive to adjusted earnings per share. Pro forma leverage ticked up to slightly above 3.0 times but was expected to decline to approximately 2.5 times by year-end 2026, funded partly by a new $450 million term loan add-on.

The pattern is unmistakable: buy adjacent technologies in known markets at reasonable multiples, integrate quickly, extract synergies, deleverage, and repeat. It is not glamorous. It does not make headlines. But it compounds.

What is most impressive about this acquisition track record is the discipline it reveals. Management had the balance sheet capacity to do larger deals throughout this period, and there was no shortage of investment bankers presenting opportunities. But Gliklich and his team resisted the temptation to swing for the fences—the very temptation that had led to the Arysta debacle. The largest post-transformation deal, Coventya, was roughly one-fifth the size of Arysta relative to the company's enterprise value. Each acquisition was digestible, fundable from existing cash flow and modest incremental debt, and integrable by teams who understood the target's market. The Arysta experience had been inoculative—the organization had learned, at great cost, the difference between a deal that creates value and one that creates complexity.

VIII. The Business Model and Competitive Positioning Today

Walk into any large-scale printed circuit board factory in Shenzhen or Taipei and you will see something that looks more like a pharmaceutical clean room than a traditional manufacturing floor. Rows of chemical baths stretch across the production line, each one filled with a precisely formulated liquid. Circuit boards move through these baths in sequence—cleaning, etching, activating, electroless plating, electrolytic plating, surface finishing—dozens of sequential steps, each requiring a specific chemistry that interacts with the specific substrate, the specific geometry, and the specific electrical requirements of that particular board design.

Think of it like a multi-course tasting menu where each dish must be prepared with exact temperatures, ingredients, and timing, and any deviation in one course ruins the entire meal. The manufacturer has spent months qualifying this exact sequence of chemistries. The technical service team has worked alongside the customer's engineers to optimize bath composition, operating parameters, and replenishment schedules.

Switching to a competitor's chemistry would mean requalifying every step—a process that takes six to eighteen months and risks production disruptions that could cost orders of magnitude more than the chemicals themselves. The chemicals might represent a tiny fraction of the product's bill of materials—perhaps one to two percent—but they are mission-critical. No manufacturer saves pennies on plating chemistry at the risk of ruining wafers worth thousands of dollars each. This is the razor-and-blade model on steroids: the product is cheap relative to its criticality, and once you are locked in, you stay locked in.

This qualification-driven stickiness is the foundation of Element Solutions' business model. The company now operates through two reporting segments, renamed in 2025 to better reflect their identities.

MacDermid Alpha Electronics Solutions generated $1.79 billion in revenue in 2025—roughly 70 percent of the total—and encompasses three interconnected verticals. Assembly Solutions provides the solder pastes, fluxes, and thermal management materials that physically attach components to circuit boards. Circuitry Solutions supplies the plating and etching chemistries that create the conductive pathways within those boards. And Semiconductor Solutions delivers increasingly sophisticated chemistries for chip assembly and advanced wafer-level packaging—a vertical that has grown at a 14 percent compound annual rate over the past five years, surpassing $300 million in revenue in 2024.

The second segment, Element Specialties, generated $765 million in 2025 revenue and serves the industrial side of the portfolio.

MacDermid Enthone provides electroless nickel, decorative chrome, and functional plating chemistries for automotive, construction, and consumer goods—when you see the shiny chrome grille on a luxury car, there is a good chance MacDermid Enthone chemistry put it there. MacDermid Offshore Solutions supplies corrosion inhibitors and drilling fluids for oil and gas production—critical chemistry that prevents multimillion-dollar offshore equipment from deteriorating in harsh saltwater environments. MacDermid Envio Solutions handles wastewater treatment and metals recycling. Electrolube provides conformal coatings and thermal management compounds for electronics protection. And Fernox sells water treatment products for building heating systems.

The global footprint supporting these businesses is substantial: approximately 60 manufacturing and R&D sites across 18 countries, direct operations in more than 30 countries, and distribution partnerships reaching over 50 countries total. The company employs over 5,500 people worldwide, with technical sales engineers positioned close to major manufacturing clusters in Asia, Europe, and the Americas.

This proximity matters enormously because specialty chemicals is fundamentally a service business masquerading as a product business. Customers are not just buying a drum of liquid—they are buying the formulation expertise, the process optimization, the troubleshooting support, and the new product development collaboration that come with it.

When a PCB manufacturer encounters a plating defect at 2 AM, Element Solutions' field engineer is the first call—and the quality of that response determines whether the relationship deepens or erodes. This is why the company maintains such a large field engineering force relative to its revenue: those engineers are not a cost center, they are the primary mechanism through which switching costs are created and reinforced.

The competitive landscape features a mix of direct rivals and larger diversified players. Atotech, historically the most direct competitor in electronics plating, was acquired by MKS Instruments in 2022 for approximately $6.5 billion—a transaction that both validated the space and created a competitor with deeper pockets but the distraction of integration into a larger conglomerate. DuPont's Electronics and Industrial division competes in electronic materials and photoresists. BASF's Chemetall unit focuses on surface treatment technologies. Japanese specialists like Uyemura and JCU Corporation hold strong positions in Asia. And in assembly materials, companies like Indium Corporation and Senju Metal Industry compete with the Alpha and Kester brands.

Element Solutions' edge lies not in dominating any single niche but in the breadth of its portfolio across the entire electronics manufacturing value chain—from semiconductor packaging to PCB fabrication to final assembly—combined with the depth of technical service at each step. A customer building a complex electronic product can source plating chemistry, solder paste, flux, conformal coating, and wastewater treatment from a single supplier ecosystem. This cross-selling capability is increasingly valuable as electronics supply chains consolidate and manufacturers seek to reduce supplier complexity.

There is also a less obvious competitive advantage at the intersection of Element Solutions' two segments: automotive electronics. Modern vehicles contain thousands of electronic components—infotainment systems, driver assistance sensors, battery management controllers—all of which require the plating, soldering, and surface finishing chemistries that Element Solutions provides. But vehicles also require decorative and functional plating on exterior trim, interior controls, and structural components—the domain of the Element Specialties segment. Very few competitors can serve an automotive OEM across both the electronic and the decorative plating requirements. This cross-segment capability creates relationship depth that single-segment competitors cannot match.

The semiconductor tailwind deserves particular attention. As chips grow more complex—with advanced packaging techniques like chiplets, fan-out wafer-level packaging, and three-dimensional stacking—the chemistry required to interconnect these components grows correspondingly more sophisticated and more valuable. Think of traditional chip packaging as putting a single item in a box. Advanced packaging is like assembling an intricate jigsaw puzzle inside that box, with each piece connected to its neighbors through microscopic copper bridges that must conduct electricity flawlessly for years. Every new generation of packaging technology requires new formulations, new processes, and new qualification cycles—a virtuous cycle for incumbents with the R&D infrastructure and customer relationships to develop qualified solutions.

IX. Porter's Five Forces and Hamilton's Seven Powers Analysis

Every investor who looks at Element Solutions' 21-plus percent EBITDA margins and thinks "that seems too good for a chemicals company" is asking the right question. Margins like that in any industry demand an explanation—what structural forces protect this profitability, and how durable are they?

Start with the threat of new entrants, which is remarkably low.

Specialty chemicals manufacturing requires not just physical infrastructure—reactors, mixing vessels, quality control laboratories, environmental compliance systems—but accumulated knowledge that cannot be purchased or replicated quickly. Element Solutions' formulations represent the output of a century of iterative refinement.

A new entrant would need to develop comparable chemistries from scratch, which means hiring experienced formulators who are in scarce supply, building application laboratories, and then spending years qualifying with customers who have zero incentive to take the risk on an unproven supplier.

The qualification cycle alone—six to eighteen months per customer, per application—creates a massive time barrier that compounds across the dozens of customers a new entrant would need to achieve viable scale. Even if you could build a competitive chemistry in a laboratory, the gap between "works in the lab" and "qualified for high-volume manufacturing" can take years to close.

And the regulatory burden adds another layer: environmental, safety, and chemical handling regulations vary by jurisdiction and require significant compliance infrastructure. The result is an industry where genuinely new competitors almost never emerge from scratch. The competitive threats come from existing players expanding into adjacent niches, not from startups disrupting from below.

Supplier power is moderate but manageable. The raw materials that go into specialty chemical formulations—base metals, acids, solvents, surfactants—are themselves largely commoditized and available from multiple sources. Element Solutions' scale as a multi-billion-dollar buyer provides meaningful negotiating leverage. More importantly, the value-add lies in the formulation, not the ingredients. A solder paste might contain tin, silver, and copper—all commodity metals—but the proprietary combination of particle sizes, flux chemistry, and rheological properties is what determines performance. This is analogous to how a great restaurant creates value through recipes and technique, not through the wholesale price of flour and butter. The chef's margin is in the transformation, not the inputs.

Buyer power is constrained by the switching costs discussed earlier. Element Solutions serves a fragmented customer base across multiple end markets—no single customer represents an outsize share of revenue. Once qualified into a manufacturing process, the customer faces significant costs and risks in switching.

The specialty nature of the products means customers are not purchasing commodities where price is the sole differentiator—they are purchasing performance, reliability, and technical support. That said, during periods of weak demand, customers can and do push back on pricing, particularly in the industrial segment where products are somewhat less differentiated than in electronics.

The threat of substitutes deserves nuanced consideration. In the near term, there are no viable substitutes for most of Element Solutions' core products—you cannot electroplate a circuit board without plating chemistry, and you cannot assemble electronic components without solder. The longer-term question is whether entirely new materials or manufacturing processes could render current chemistries obsolete. The potential shift from tin-based solder to copper interconnects in advanced semiconductor packaging is both a risk and an opportunity—Element Solutions' Kuprion nano-copper technology is specifically designed to capture this transition rather than be disrupted by it. Environmental regulations that restrict certain chemicals, like hexavalent chromium in decorative plating, force reformulation—but incumbents with deep R&D capabilities typically develop compliant alternatives faster than competitors, turning regulatory change into a competitive advantage rather than a threat.

Competitive rivalry is moderate. The specialty chemicals space is consolidated enough that destructive price competition is rare, but fragmented enough that no single player dominates.

The MKS/Atotech combination created a formidable rival, but MKS has its own integration challenges and a broader focus that dilutes management attention on any single product line. Competition occurs primarily on technical capability, service quality, and innovation rather than price—precisely the environment where incumbents with deep process knowledge and long customer relationships thrive.

The Japanese specialists—Uyemura, JCU Corporation, and others—are strong domestically but historically less aggressive in global expansion. DuPont and BASF participate in adjacent niches but treat electronics chemistry as a small piece of their massive portfolios. When your electronics plating business generates a few hundred million in revenue inside a $40 billion company, it is unlikely to receive the same strategic attention as it would inside a $2.5 billion company where it represents the core franchise.

Through the lens of Hamilton Helmer's Seven Powers framework, the company's durable advantages crystallize further. Switching costs are the most powerful force—the qualification-driven lock-in that keeps customer churn exceptionally low. Once a semiconductor manufacturer has spent twelve months qualifying a new plating chemistry into its production line, the prospect of doing that again with a competitor's product is genuinely unappealing—especially when the existing supplier's product works.

Process power ranks equally high: the multi-step, technically complex nature of chemical manufacturing and customer application creates institutional knowledge that exists only inside the organization. A plating engineer at MacDermid Enthone who has spent twenty years optimizing nickel-phosphorus bath chemistry for automotive applications possesses knowledge that cannot be hired away in a single recruitment cycle—it is embedded in teams, in documented but unpublished process notes, in the tacit understanding of how a particular bath behaves under specific conditions.

Cornered resources manifest as proprietary formulations representing decades of compounded R&D investment. Scale economies operate globally, allowing R&D amortization across a larger revenue base than smaller competitors. Counter-positioning is present: Element Solutions' focused strategy allows faster decisions and deeper investment in specialty niches than diversified giants for whom electronics plating is a rounding error. Network effects are absent in B2B chemicals. Branding is meaningful within specific technical communities but does not operate at the consumer level.

The primary moat is the combination of switching costs, process power, and cornered resources—a triple lock that explains both the margins and their durability. If you were designing a business from scratch to resist competitive disruption, you would want all three of these powers working simultaneously—and that is exactly what a century of accumulated chemistry provides.

For investors, the key question is not whether these advantages exist today—the margins confirm that they do. The question is whether the secular trends in electronics complexity, semiconductor packaging, and environmental regulation will strengthen or erode them over the coming decade. The evidence strongly suggests strengthening: as devices grow more complex and manufacturing tolerances tighten, the value of reliable, qualified specialty chemistry only increases. Each new node in semiconductor fabrication, each new packaging architecture, each new environmental regulation raises the bar for supplier qualification—widening the moat for incumbents who can clear it and raising it higher for those who cannot.

X. Bull Case vs. Bear Case

The optimistic thesis for Element Solutions rests on several mutually reinforcing pillars.

The company sits squarely in the path of some of the most powerful secular trends in the global economy. Electronics proliferation continues unabated—not just in consumer devices but in automotive, where the average vehicle's electronic content increases with every model year, in industrial automation, medical devices, and communication infrastructure.

The semiconductor industry's push toward advanced packaging creates demand for ever-more-sophisticated chemistries. The reshoring of chip manufacturing—driven by the CHIPS Act in the United States and similar initiatives in Europe and Japan—expands the geographic addressable market. And the explosive growth of AI infrastructure, with its insatiable appetite for high-performance computing hardware, creates new demand for the plating, solder, and interconnect materials that go into every server, GPU, and networking switch in every hyperscale data center being built across three continents.

The financial profile reinforces the structural story. Capital expenditure historically runs at roughly 2 percent of revenue, meaning that a very high proportion of EBITDA converts to free cash flow. In 2024, the company generated record free cash flow of $294 million on $535 million of adjusted EBITDA—a conversion rate above 50 percent that is highly attractive for an industrial business. Full-year 2025 results showed continued momentum: net sales of $2.55 billion with 6 percent organic growth, adjusted EBITDA of $548 million, and adjusted EPS of $1.49. The Electronics segment delivered $1.79 billion in revenue with 10 percent organic growth, accelerating to 13 percent in the fourth quarter driven by datacenter infrastructure and high-performance computing demand.

CEO Gliklich called 2025 a "record year." The quarterly trajectory tells the story of accelerating momentum: by the fourth quarter of 2025, total net sales reached $676 million, up 8 percent year-over-year, with the Electronics segment alone delivering $487 million on 13 percent organic growth. The industrial side stabilized as well, with Element Specialties delivering 4 percent organic growth in Q4 after multiple quarters of stagnation.

The 2026 guidance of $650 to $670 million in adjusted EBITDA implies roughly 20 percent year-over-year growth, fueled by both organic momentum and the Micromax and EFC acquisitions. Management guided for mid-to-high teens adjusted EPS growth. The balance sheet, with 100 percent of debt at fixed rates through interest rate swaps maturing in 2028-2029, provides predictability in a volatile rate environment. An October 2024 refinancing had already reduced borrowing costs by 25 basis points to SOFR plus 1.75 percent—a favorable rate reflecting the company's improved credit profile.

M&A optionality adds another dimension. The specialty chemicals industry remains fragmented, with hundreds of small, privately held companies that could be attractive tuck-in targets. Many of these are family-owned businesses with strong technical positions but limited scale—exactly the kind of acquisition targets where Element Solutions has a demonstrated ability to integrate and improve.

The company has shown disciplined integration capability and has the balance sheet capacity—even after the recent deals—to continue acquiring. If net leverage declines to 2.5 times by year-end 2026 as expected, the company would have meaningful headroom for additional bolt-ons without stressing the balance sheet.

The bear case centers on real but manageable risks.

Cyclicality is the most immediate concern. For all its specialty characteristics, Element Solutions is not immune to macro downturns. The Element Specialties segment showed organic weakness through much of 2024 and 2025 as Western industrial activity stagnated—the segment's reported revenue declined 15 percent in 2025, though much of that reflected the Graphics divestiture, with organic growth still positive at 1 percent.

A global recession that suppressed electronics manufacturing volumes would hit the company's growth rate and potentially its margins, even if the business model would prove more resilient than commodity chemicals peers. The 2022-2023 electronics downturn provided a preview: when semiconductor inventories built up and consumer electronics demand softened, even specialty chemistry volumes declined, albeit less dramatically than commodity chemical volumes.

Geographic concentration warrants monitoring. Significant revenue comes from Asia, with exposure to China, Taiwan, South Korea, and Japan—regions subject to geopolitical tensions, trade restrictions, and supply chain disruptions.

The ongoing semiconductor decoupling between the United States and China creates both risk—potential loss of Chinese customers if export controls tighten further—and opportunity, as increased demand from diversified supply chains benefits suppliers who can serve multiple geographies simultaneously. A scenario where Taiwan Strait tensions disrupted TSMC's operations would affect virtually every player in the semiconductor supply chain, Element Solutions included.

The recent acquisitions pushed pro forma leverage above 3.0 times—temporarily reintroducing the kind of balance sheet risk that the post-Arysta transformation was designed to eliminate. Management expects leverage to decline to approximately 2.5 times by year-end 2026, but integration execution and demand conditions will determine whether that target is met.

Technology disruption, while unlikely to be sudden, is a background risk. If entirely new manufacturing processes emerge that bypass current chemistry-based approaches, incumbents could find their formulation libraries less relevant. Competition from MKS Instruments, which now owns Atotech and has the resources of a larger parent, could intensify. And the "hidden champion" characteristic that makes Element Solutions attractive to knowledgeable investors also means limited sell-side coverage and investor awareness, which can constrain valuation multiples.

One accounting note warrants mention: like many serial acquirers, Element Solutions carries significant goodwill and intangible assets from its acquisition history, a legacy of the billions spent on MacDermid, Alent, Coventya, and other acquisitions. While goodwill impairment has not been a material issue to date, investors should monitor this in the context of acquisition multiples and integration outcomes, particularly as the company enters a more active M&A phase with the Micromax and EFC deals. A sustained downturn in end-market demand or competitive disruption could trigger impairment charges that, while non-cash, would signal deterioration in the long-term value of acquired businesses.

There is also a "myth versus reality" worth addressing here. The consensus narrative on Element Solutions often frames it as a "boring compounder"—steady, predictable, low-volatility. The reality is more nuanced. The Electronics segment, which now represents 70 percent of revenue, is tied to the notoriously cyclical semiconductor and consumer electronics industries. In a downturn, this segment would see meaningful volume declines, even if the specialty nature of the products would cushion the blow relative to commodity chemicals. The "boring compounder" label understates the cyclical exposure that comes with being deeply embedded in the electronics supply chain. The company's specialty characteristics provide resilience, not immunity.

For investors tracking this business over time, two KPIs stand out as the most telling indicators of fundamental health.

First: Electronics segment organic revenue growth. This metric strips out acquisitions and currency to reveal the underlying demand trajectory for the company's highest-value products. Sustained high-single-digit or better organic growth signals that Element Solutions is successfully riding the semiconductor and AI infrastructure tailwinds. A deceleration below mid-single digits for multiple quarters would warrant closer scrutiny of competitive dynamics and end-market demand.

Second: consolidated adjusted EBITDA margin. This captures pricing power, input cost management, and operational efficiency in a single number. Margins have hovered around 21 to 22 percent in recent years.

Meaningful expansion toward the mid-twenties would validate the thesis that portfolio optimization and scale are improving profitability—particularly as higher-margin Electronics revenue becomes a larger share of the total mix. Compression below 20 percent for more than a quarter or two might signal competitive pressure, integration challenges, or an inability to pass through input cost increases, and would warrant careful investigation into which segment and which end market is causing the deterioration.

XI. Epilogue: What's Next for Element Solutions

Element Solutions enters 2026 at a genuine inflection point.

The company has achieved the strategic clarity that eluded it during the Platform years. The balance sheet is healthy. The Electronics segment is growing at double-digit rates organically. The Micromax and EFC acquisitions expand capabilities into advanced inks, pastes, and high-purity gases for semiconductor manufacturing—high-growth adjacencies that deepen the moat around the core electronics franchise.

Management has guided for adjusted EBITDA of $650 to $670 million in 2026, which would represent the strongest year of earnings growth since the transformation.

The market capitalization has responded, surging past $8.6 billion and pushing the stock to all-time highs above $35 per share. The 52-week range of roughly $17 to $38 tells the story of a company whose narrative has shifted decisively from "turnaround in progress" to "compounder firing on all cylinders."

With that rerating comes a valuation that demands continued execution—the stock trades at roughly 14 to 15 times 2026 guided EBITDA, a premium to diversified chemical peers that reflects the market's growing appreciation for the quality of these businesses. The company also pays a modest quarterly dividend of approximately $0.08 per share, returning capital to shareholders while retaining the bulk of free cash flow for growth investments and acquisitions.

The AI infrastructure buildout is the most powerful near-term tailwind. Every new data center, every new GPU cluster, every new high-bandwidth memory stack requires the kinds of advanced packaging and assembly chemistries where Element Solutions has been investing most aggressively. If AI-driven capital expenditure continues at its current pace, the Semiconductor Solutions vertical could grow from its current base into a significantly larger business. The Kuprion nano-copper technology, the Micromax inks and pastes, and the EFC specialty gases all position the company to capture an increasing share of the materials content in each chip package.

Sustainability is emerging as another growth vector that few investors have fully appreciated. Manufacturers face tightening environmental regulations and growing pressure to reduce water consumption and chemical waste.

The shift away from hazardous chemicals like hexavalent chromium in decorative plating creates reformulation cycles that favor incumbents with the R&D depth to develop compliant alternatives. When a regulation forces the entire industry to switch to a new chemistry, the first company to develop and qualify a compliant formulation captures an outsized share of the transition market. MacDermid Envio Solutions' wastewater treatment capabilities become more valuable as water scarcity intensifies globally.

Geographic strategy matters increasingly. The "China plus one" diversification trend—where electronics companies establish production in Vietnam, India, Thailand, and other countries alongside Chinese operations—expands the total addressable market for technical sales and application support. When a major electronics OEM opens a new factory in Vietnam, it needs a local supplier who can provide the same plating chemistry, the same solder paste, the same technical service that it receives at its established plant in Shenzhen. Element Solutions' 60-site global footprint, expanded further by the EFC acquisition's Lehigh Valley and Mesa facilities, is built for exactly this kind of distributed manufacturing world.

The recent acquisitions also position the company for what could be a transformational decade in semiconductor materials. EFC's high-purity specialty gases serve the most demanding applications in chip fabrication—the kind of ultra-clean materials where a single impurity measured in parts per billion can render an entire wafer unusable. Micromax's advanced inks and pastes complement the existing circuitry and assembly portfolios. Together with Kuprion's nano-copper technology, these three acquisitions form a cohesive semiconductor materials strategy that did not exist three years ago.

From a leadership perspective, the management picture is stable and maturing. Martin Franklin, now sixty-one, remains Executive Chairman and continues to guide capital allocation and strategic direction. Gliklich, still in his late thirties and running the company for seven years, is firmly established as the operational and strategic leader.

The depth of the management bench, with Scot Benson as President and COO and experienced segment leaders at both MacDermid Alpha and Element Specialties, suggests continuity planning is in place. But the complementary relationship between Franklin's dealmaking instincts and Gliklich's operational rigor has been central to the company's success, and any change in that dynamic would be closely watched by long-term shareholders.

The broader lesson of the Element Solutions story transcends any single company. It is a case study in the power of strategic focus—in how selling your largest business can be the smartest move you make. The Arysta divestiture was not a failure to be explained away; it was a strategic triumph, an act of intellectual honesty that unlocked billions of dollars of shareholder value by admitting what was not working and having the courage to fix it.

It is a case study in the value of boring businesses with deep technical moats—companies that never make headlines, never trend on social media, never become household names, but that quietly compound returns because their chemistry is embedded so deeply in critical manufacturing processes that customers cannot easily walk away. In a world obsessed with disruption and innovation, Element Solutions is a reminder that some of the most durable competitive advantages come not from inventing something new but from perfecting something old so thoroughly that alternatives become unthinkable.