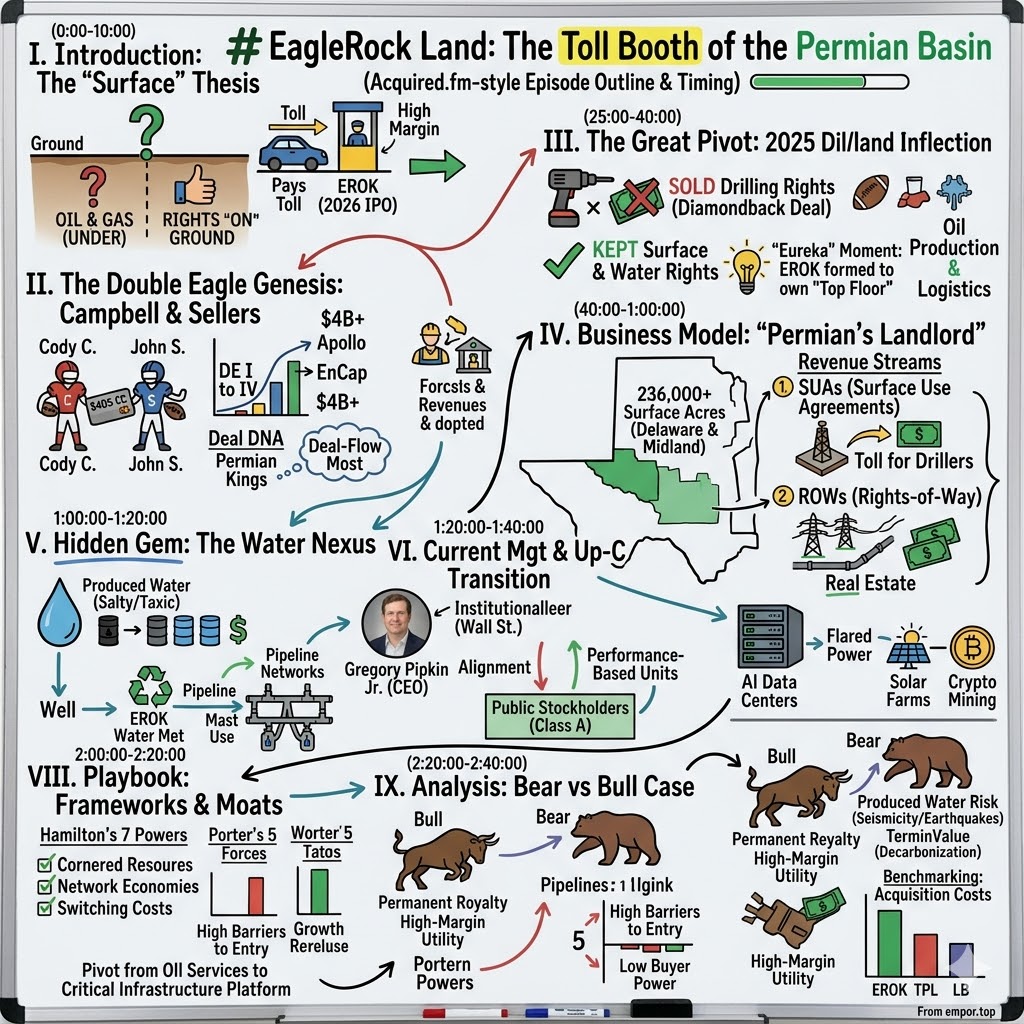

EagleRock Land: The Toll Booth of the Permian Basin

I. Introduction & The "Surface" Thesis

Drive west from Midland, Texas, on State Highway 158, and you enter a landscape that, from a thousand feet up, looks less like a desert than a circuit board. Pump jacks bob in metronomic rhythm. Service roads cut perfect rectangles through the scrub. Tanker trucks hauling brine queue at injection sites the way airliners queue at LaGuardia. Somewhere under the caliche dirt, a Pioneer or a Diamondback or an Exxon rig is punching another lateral two miles sideways through the Wolfcamp shale, and somewhere above the rock, a flare burns natural gas that no one has yet bothered to pipe out.

For a hundred years, the entire story of the Permian Basin has been told from below the ground. Whose mineral rights? Whose hydrocarbon column? Whose lease, whose unit, whose royalty? The folklore of West Texas — the wildcatters, the gushers, the H.L. Hunts and the George Mitchells — was always a folklore of what lay beneath. The dirt itself was something you scraped a road across to get to the real prize.

But the joke of the 2020s, and the thesis behind one of the most unusual energy IPOs in recent memory, is that the dirt itself was the prize all along.

On May 13, 2026, EagleRock Land LLC priced its initial public offering on the New York Stock Exchange at $18.50 per Class A share, the top of its marketed range, raising gross proceeds north of $740 million.1 The ticker, almost too on-the-nose, was EROK. Within two trading sessions the stock opened above $22, and a company that, eighteen months earlier, had been a footnote in a Diamondback Energy press release was suddenly worth several billion dollars.1

EagleRock does not drill wells. It does not own rigs. It does not pump oil, and it does not pay royalties on hydrocarbons it produces, because it does not produce any. Instead, it owns the surface — 236,000-plus contiguous acres sitting on top of the most productive oil-and-gas real estate on the planet — and it charges everyone else for the right to operate up there.2 Every pad. Every road. Every pipeline right-of-way. Every saltwater disposal well. Every freshwater pond. Every potential solar array or data-center foundation slab. It is, in the most literal sense possible, a toll booth.

This is the story of how two former Texas Tech offensive linemen turned a $40,000 credit-card limit into a multi-billion-dollar deal-making machine, sold the underground rights to the world's biggest Permian pure-play, kept the surface rights for themselves, and then did what every great private equity outcome eventually does: took it public.3

It is also a story about a quiet shift in the economics of American energy. As the Permian matures, the binding constraint is no longer geology. It is logistics. Water in. Water out. Power. Pads. Pipelines. The geology has been derisked by a million horizontal wells. What remains scarce is the right to stand on top of the rock — and the operational density to monetize that right at scale. EagleRock is what happens when somebody finally builds a public-market vehicle around that observation.

Over the next two hours of reading, the story will move from the Texas Tech weight room to the executive floor of Barclays to a 2026 prospectus tucked into the EDGAR archive. It will pass through Apollo and EnCap and Diamondback, and it will end, somewhat improbably, with a discussion of AI data centers, flared methane, and earthquakes near Pecos. The through-line is simple: in a maturing basin, the landlord wins.

II. The Double Eagle Genesis: Campbell & Sellers

The most useful biographical detail about Cody Campbell and John Sellers is also the easiest to overlook: they played offensive line together at Texas Tech in the early 2000s. Offensive linemen are, almost by job description, the people on a football team who are paid to absorb impact, coordinate movement, and never get the credit. They learn early that the value they create is invisible to the box score. That instinct — to do the unglamorous work that makes someone else's touchdown possible — would, twenty years later, turn out to be a remarkably good description of the surface-rights business.4

The two graduated, drifted into the post-football half-life of all minor college athletes, and eventually started buying mineral leases together in their late twenties. The often-repeated origin myth involves a $40,000 credit-card line and a leased pickup truck. The substance behind the myth is that, in the late 2000s and early 2010s, the Permian Basin was being re-rated by horizontal drilling and hydraulic fracturing, and large swaths of West Texas mineral acreage — particularly the awkward, fragmented, "pigeonhole" parcels that majors did not bother to chase — were sitting in the hands of ranchers, heirs, and probate estates that had no idea what they were about to be worth.4

Campbell and Sellers built a business model around being the people willing to do that work. Door to door. County courthouse to county courthouse. Stitching ten-acre tracts into thousand-acre packages, and thousand-acre packages into fifty-thousand-acre packages, until the resulting block was big enough that an EnCap-backed E&P or a public independent had to sit down and write a check.

That was Double Eagle I. They then did it again, with more capital, as Double Eagle II. Then again, with EnCap Investments as anchor financial sponsor, as Double Eagle III. The exits compounded. By the time the third vehicle was wound down, Campbell and Sellers had built one of the most efficient land-aggregation machines in the basin's history, and they had done it without ever owning a drilling rig.

The cultural DNA that emerged from this period is worth pausing on, because it explains a great deal about EROK. The Double Eagle playbook is not a geology playbook. It is a Rolodex playbook. It rewards the people who can pick up a phone and reach a county judge, a third-generation rancher, an EnCap principal in Houston, and a Goldman energy banker in the same afternoon. The moat is reputational. If a private operator wants to sell a 12,000-acre block quickly and discreetly, there is a short list of buyers who can write the check and close in cash. Campbell and Sellers spent fifteen years making sure they were on the top of that list.4

By the early 2020s, the duo were sometimes described — half-jokingly, half-reverently — as the Kings of the Permian, a title that captured both their dealmaking volume and a certain bigger-than-life Texan persona. Cody Campbell took a turn into political and civic life, including involvement in collegiate athletics and West Texas philanthropy. John Sellers stayed closer to the deal desk. Together, they ran a machine that, between roughly 2012 and 2024, deployed and recycled billions of dollars of energy capital. EnCap, the Houston-based energy private-equity firm, was the constant. Apollo Global Management financed a chunk. The public majors and large independents were, almost without exception, the eventual exit buyers.4

What matters for the EROK story is not the count of deals or the precise IRR on Double Eagle III. It is the realization that, somewhere along the way, the two of them stopped thinking of land as a thing you flipped and started thinking of land as a thing you held. The drilling cycle is volatile; the surface beneath it is not. The basin will be developed, redeveloped, infilled, refracked, and then someday repurposed. Through all of that, somebody owns the dirt. Campbell and Sellers, by the early 2020s, had quietly decided that somebody should be them.

That decision set up the most important pivot in this entire story — the one that takes a private dealmaking partnership and turns it into a public landlord with a permanent capital base.

III. The Great Pivot: The 2025 Diamondback Inflection

Diamondback Energy, ticker FANG, is a $30-billion-plus public Permian pure-play headquartered in Midland. By 2024, it was on a tear of consolidation, having already absorbed several smaller operators and announced its blockbuster $26 billion all-stock merger with Endeavor Energy Resources. Diamondback's strategy was straightforward and ruthlessly executed: own as much of the best Midland Basin acreage as possible, drill it efficiently, and return cash to shareholders.

On February 12, 2024, Diamondback announced that it would acquire Double Eagle IV, the latest Campbell-Sellers vehicle, for a deal valued at roughly $4 billion in cash and stock.5 At face value, this was another tidy exit on top of an already extraordinary track record. The Double Eagle assets — tens of thousands of net acres in the Midland Basin, contiguous with Diamondback's core inventory — slotted neatly into the buyer's drilling schedule. Diamondback got more years of premium inventory at a price its analysts could justify against strip pricing.

The strategically interesting move was not the sale. It was the carve-out.

Buried in the transaction was a structural decision that, in hindsight, looks like the entire EagleRock thesis crystallizing in legalese. Campbell and Sellers sold the mineral and leasehold interests — the actual right to drill and produce oil and gas — but retained a separate book of surface acreage and water-management infrastructure overlaying the same footprint and adjacent territory.5 Diamondback got the right to drill. The sellers got the right to charge for everything that has to happen on top of the dirt in order to drill.

To appreciate why this was such a clever piece of financial engineering, you have to understand how the Permian had changed. In 2013, a typical horizontal well consumed modest amounts of water and a modest physical footprint. By 2024, a single multi-well pad could occupy ten or fifteen acres, host a dozen lateral wellbores, consume tens of thousands of barrels of freshwater per stage, and produce four to five barrels of saltwater for every barrel of oil over its lifetime. The "infrastructure intensity" of a Permian well — pads, roads, water lines, gas takeaway, power drops, sand-handling — had multiplied severalfold. And the cost of all that infrastructure, plus the access rights it required, had migrated from being a rounding error in an E&P AFE to being a meaningful line in the well economics.

Translation: the surface was no longer free.

That recognition is what separates EagleRock from a generic land company. Campbell and Sellers did not just want to be paid once when the land changed hands. They wanted to be paid every time a barrel of oil moved across the land, every time a foot of pipe was laid under it, every time an electron crossed it on a transmission line. They wanted a recurring, contractual, inflation-linked stream of cash flows tied to the operational intensity of the basin — and they wanted it on a balance sheet that was capital-light enough to throw off most of its operating income as distributable cash.

The vehicle for that idea, formally organized in 2025 and brought to market in May 2026, was EagleRock Land LLC. The S-1 made the framing explicit: this was not an E&P company, not an oilfield-services company, and not a midstream company in the conventional pipe-and-processing sense. It was, in management's own preferred phrase, a "surface infrastructure" company.2

Diamondback's willingness to do the deal this way is, if anything, the more remarkable half of the story. Most acquirers would have insisted on taking surface and mineral together, because surface rights look like an obscure liability hiding inside the cap stack until you really stare at them. Diamondback, run by operators who actually understood what their wells cost to put in the ground, evidently decided that paying surface fees to a friendly counterparty was a tolerable price for getting the underground rights cleanly. The hidden subtext is that Campbell and Sellers, by virtue of fifteen years of relationship-building, had become a counterparty Diamondback could live with as a long-term landlord — and that mattered more than any single line in the spreadsheet.

From the moment that deal closed, the trajectory toward a public IPO was effectively set. The only remaining questions were when, at what size, and with whom in the CEO chair.

IV. The Business Model: "The Permian's Landlord"

There is an old joke in real estate that the three most important things are location, location, and location. EagleRock's pitch to public-market investors is essentially that joke, told with a straight face and a map of the Delaware and Midland Basins.

The company controls 236,000-plus surface acres concentrated in the western Delaware Basin and the southern Midland Basin — two of the highest-rate, lowest-breakeven shale fairways in North America.2 The acreage is not random. It tracks, almost parcel by parcel, the same Wolfcamp and Spraberry sweet spots that the Double Eagle vehicles spent more than a decade aggregating from underneath. That overlap is not an accident. It is the entire moat.

The revenue model breaks down into a handful of contractual streams, all of which share a single elegant property: somebody else pays the capital expenditure, and EagleRock collects the rent.2

Surface Use Agreements. Every time an operator wants to build a well pad on EagleRock land, lay a flowline, cut a service road, install a tank battery, or place a frac spread, they sign a surface use agreement. The SUA specifies a one-time payment for the disturbance, an ongoing annual rental, and a damage schedule that compensates EagleRock for caliche, vegetation, livestock, and reclamation obligations. The bigger the pad and the longer the operations, the bigger the payment. Multiplied across hundreds of pads on a 200,000-acre block, the result is a stream of contracted, predictable, geographically locked-in cash flows.

Rights-of-Way. Pipelines, gathering systems, electric distribution lines, and fiber routes all need to cross the surface. Each crossing is a separately negotiated easement, sometimes paid as a per-rod or per-foot charge, sometimes as a lump sum plus annual rental. As the basin densifies, the number of these crossings has gone up by an order of magnitude relative to a decade ago. Every new piece of midstream infrastructure built on EagleRock land is, in effect, a perpetual rent contract paid by somebody whose balance sheet is much larger than EagleRock's own.

Sand and Caliche Royalties. Drilling pads and roads need fill material; frac jobs need proppant. Where EagleRock owns suitable in-situ sand or caliche reserves, it can lease those out to mining operators on a tonnage basis.

Water Sales and Disposal Fees. This stream is large enough to deserve its own section, which it will get next.

What makes the model unusual, and what management leans into in every slide of the IPO roadshow, is what is missing from the cost side.2 EagleRock does not drill. It does not own rigs, frac fleets, or completion crews. It does not buy or sell hydrocarbons. It does not take commodity price risk in the traditional sense. Its operating expense is dominated by a small headcount of land managers, water-operations staff, and corporate overhead. The capital intensity that defines an E&P balance sheet — billions of dollars of producing-property PP&E, depreciating against a relentless decline curve — is simply absent.

The result is a financial profile that looks, on a per-share basis, less like an oil company and more like a triple-net REIT with optionality. Margins are high. Free cash conversion is high. Maintenance capex is low. The growth driver is not commodity price; it is operational activity by the company's tenants. As long as somebody is drilling, completing, producing, and piping in the basin, EagleRock gets paid.

There is a subtle but important corollary. Because so much of the cost is fixed, the incremental margin on every new SUA or ROW is extraordinary. The fifteenth pipeline that crosses a given section adds nearly the same easement income as the first — but at almost zero incremental cost to the landlord. This is what management means when they describe the business as one with "operational densification" as the key tailwind. The more crowded the basin gets, the more rent flows up to the surface owner. The asset gets more valuable not because the land grew but because the operations on top of it got more intense.

The right historical analogy is not really to a mineral-rights royalty trust, even though that comparison gets made constantly. A royalty trust is exposed directly to commodity price and to a specific decline curve. EagleRock is exposed to activity — a far more durable and far more diversified variable. The closer analogy is to a port operator that charges a fee per container regardless of the price of the goods inside the container, or to a tollway operator whose revenue scales with vehicle counts and not with the price of gasoline. In a basin where drilling activity has been remarkably resilient through commodity cycles, that distinction matters.

For an investor, the upshot is that the most important question to ask about EagleRock is not "where will WTI trade?" It is "how many surface disturbances per acre per year will the basin generate over the next decade?" Those are very different questions, with very different answers, and the second one is far more favorable to the landlord.

V. Hidden Gem: The Water Nexus

Stand on a pad in Reeves County during a hot August afternoon and the dominant sound is not the rig itself. It is the slow, mechanical thrum of pumps. Two of every five barrels of fluid moving across the Permian on a given day is not oil. It is salty, mineral-laden, often radioactive brine — the unloved byproduct of fracking and production known throughout the industry as produced water. For every barrel of oil that a mature Permian well brings to the surface, it brings up roughly four to five barrels of this brine.6 In aggregate, the basin produces north of twenty million barrels of produced water per day. That is a flow rate larger than several of the world's biggest crude pipelines.

For an E&P operator, this water is, in a word, a problem. It cannot be released to surface streams. It cannot, in most cases, be cheaply desalinated to a useful standard. It must be either reinjected back into the subsurface through disposal wells or recycled and reused as frac fluid on the next completion job. Both options require an enormous network of pipes, pumps, tanks, ponds, and disposal wells. And every single one of those pieces has to be built on top of somebody's dirt.

This is the second, less obvious leg of the EagleRock thesis, and it may, over time, prove to be the more valuable one.6

EagleRock operates a water-management business that does three things at once. First, it sells freshwater and brackish water out of its own onsite sources to operators that need it for completions. Second, it gathers produced water from third-party operators on a per-barrel fee basis, much the way a midstream company would gather gas. Third, where the economics work, it recycles produced water into reusable frac-grade fluid that can be sold back into the next completion cycle, displacing freshwater demand entirely.6

The structural reason this is so attractive has nothing to do with the per-barrel margin on water disposal, which on its own is modest. It has to do with the layout of the network. Because EagleRock owns the surface, it can build its produced-water pipeline grid along the most efficient corridors across its acreage, and it can require third-party operators on its land to tie into the system as part of their surface use agreement. The cost to a competitor of replicating that network is not high — it is essentially infinite, because you cannot build a competing pipeline across a piece of dirt whose owner has already given exclusivity to somebody else. The right-of-way is, by definition, a single-occupancy asset.

In moat terms, this is a textbook switching cost layered on top of a textbook cornered resource. Once an operator's wells are tied into EagleRock's gathering system, the cost to switch — to redrill flowlines, recommission another disposal node, reroute capacity — is prohibitive for the remaining life of the wells. And the wells, even on a steep Permian decline curve, last fifteen to twenty years.

There is also a regulatory tailwind that almost nobody on the IPO roadshow mentioned explicitly but that hangs over the entire produced-water economy. The Texas Railroad Commission, the state agency that regulates oil and gas, has been gradually tightening rules around saltwater disposal in response to the now well-documented link between high-volume injection into the shallow Delaware-Mountain Group formations and induced seismicity. A 2026 commission report logged hundreds of induced events of magnitude 2.0 or greater across the basin in the prior twelve months, with clusters around Pecos and Culberson counties.[^7] The commission's response has been to designate seismic response areas in which disposal volumes are throttled and, in some cases, suspended outright.

The net effect of all of this is that disposal capacity has gone from being abundant and cheap to being constrained and increasingly expensive. Operators who once paid a few cents a barrel to inject brine are now negotiating much richer per-barrel rates and longer-dated contracts. Recycling, which used to be a marginal sustainability story, is increasingly the cheapest molecule of water available. And the entity sitting in the middle of that shift — owning the surface, the pipelines, the disposal wells, and the recycling facilities — captures the value that flows through.

Put bluntly: as a regulatory matter, the Permian is being slowly weaned off its decades-old habit of free or near-free saltwater disposal, and as a physical matter, the basin is producing more water relative to oil every year as wells age. Both vectors are favorable to a vertically integrated water-management business that already owns the dirt.

That is why one industry observer described the dynamic at the end of 2025 as "water becoming the new oil" in the Permian — not because anyone is going to drink it, but because the right to move it, store it, and recycle it has become a commercial chokepoint.6

VI. Current Management & The Up-C Transition

Cody Campbell and John Sellers are dealmakers. They built Double Eagle on relationships, not on quarterly earnings calls. Running a public company is a different sport — one that involves SEC filings, sell-side analysts, an audit committee with actual teeth, and the daily indignity of having an investor relations team email you about consensus estimates. So in 2025, as the path to public markets crystallized, the duo did the smart thing. They hired somebody else to be the public-company CEO.

That person was Gregory Pipkin Jr.

Pipkin is in some ways the un-Campbell-and-Sellers. Where the founders are West Texas dealmaking through and through — backslapping, instinctive, comfortable in a hangar in Midland — Pipkin is a former Barclays banker who spent years in the energy investment-banking practice working with public independents on capital-markets and M&A transactions. After Barclays, he moved into operating roles, including a stint at Infinity Natural Resources, before being recruited to lead what would become EagleRock Land into the public markets.7 On paper, he is the institutionalizer: the person whose job is to take a private dealmaking machine and translate it into a quarterly-cadence, GAAP-compliant, equity-research-friendly public entity.

His Form 3 initial statement of beneficial ownership, filed on the day the IPO priced, shows a meaningful personal stake in the company alongside performance-vesting equity that ramps over a multi-year schedule tied to growth in distributable surface earnings.7 That alignment is not just decorative. The deal Pipkin made when he took the seat was, in effect, that he would be compensated based on how successfully he could grow the underlying yield of the surface portfolio — not on how successfully he could grow earnings per share through buybacks or financial engineering. Whether that incentive structure holds up under public-market pressure is one of the more interesting questions hanging over the next three to five years.

Underneath the CEO sits a leadership team drawn largely from the Double Eagle bench, plus a CFO with a public-company background and a general counsel imported to manage what is, in regulatory terms, a quite complicated structure. The structural complication is worth its own paragraph or three, because it is the single most important thing for a public-equity investor to understand about EROK.

EagleRock came public via what corporate lawyers call an "Up-C" structure.8 In an Up-C, the operating business sits in a partnership at the bottom of the capital stack — in EROK's case, an LLC that, for tax purposes, is treated as a partnership. Above that partnership sits a publicly traded C-corporation, which is what the IPO investors actually buy shares in. The C-corp owns a managing-member interest in the LLC. The original owners — Campbell, Sellers, EnCap, and a handful of other private holders — keep their economic ownership down at the LLC level, in the form of LLC units, and they hold a separate class of voting stock (Class B) in the C-corp that carries voting power without economic claims.

In EROK's specific case, after the IPO, those existing owners retained roughly 72.8 percent of the combined voting power of the public company through their Class B shares.2 Public Class A shareholders, despite providing the new capital, hold the minority of the votes. The economic split between Class A and the LLC-unit holders looks more balanced, because LLC units are eventually exchangeable, one-for-one, into Class A shares — but the timing and tax consequences of those exchanges sit firmly in the hands of the pre-IPO owners.

There are several reasons sophisticated energy issuers like the Up-C. The biggest is tax: existing owners get to defer the gain on their built-up basis until they actually exchange units, and a tax receivable agreement typically lets them capture a share of the step-up benefits the C-corp realizes when exchanges happen. The next-biggest is governance: founders and anchor private-equity sponsors keep effective control of the strategic direction of the business through their voting majority, even after capital has been raised from public markets.8

For a public-market investor, the Up-C structure cuts two ways. On the bright side, it aligns the long-term interests of the founders and the financial sponsor with the underlying performance of the LLC, because most of their wealth still sits inside the operating business rather than in liquid Class A shares. On the dimmer side, it means public Class A shareholders are minority voters in a controlled company, with limited ability to influence governance, board composition, or major M&A. Anyone who buys EROK is, in essence, buying a passive interest alongside Campbell, Sellers, and EnCap, on terms set by those same people.

That is not necessarily a bad bargain — these are people whose multi-decade track record in the basin is among the best in the industry. But it is a bargain that needs to be entered with eyes open, and it puts the question of management quality and incentive alignment at the very center of the EROK thesis.

VII. The "Next Act": Data Centers & Power Generation

The most surreal sight in the Permian today is not a flare or a frac spread. It is a converted shipping container, painted matte gray, sitting next to a wellhead in Loving County, humming with the sound of cooling fans. Inside the container, racks of GPUs are training, or at least inferring, on artificial intelligence workloads — powered by stranded natural gas that, six months earlier, would have been burned off into the desert sky as a regulatory liability.9

This is the seam that EagleRock is moving into, and it is the part of the EROK story that most squarely transforms the company from "oilfield landlord" into "critical infrastructure platform."

Three macro trends collide in the Permian Basin to make this work.9

First, the basin produces enormous volumes of associated natural gas as a byproduct of oil production — far more than can be moved out via existing pipelines. For years, the excess has been flared, vented, or trapped behind pipeline constraints, depressing local Waha hub gas prices and creating an ongoing emissions problem that operators would gladly solve if they could.

Second, the United States has stumbled into a genuine power crisis driven by AI workloads. Major hyperscalers have spent the past three years scrambling for any combination of land, power, and water that can host the next generation of training clusters. Traditional data-center markets like Northern Virginia are increasingly capacity-constrained. New markets are emerging in places that, twenty-four months ago, would have seemed exotic — including, very much, West Texas.

Third, the Permian has land. Lots and lots of flat, cheap, sparsely populated, weather-tolerant land, much of it sitting on top of grid interconnects and adjacent to pipeline infrastructure. It also has, courtesy of EagleRock and a handful of competitors, an emerging class of consolidated surface landlords who can underwrite the kind of long-dated, large-footprint master leases that hyperscalers prefer.

EagleRock's stated strategy is to use a portion of its surface acreage to host data-center campuses powered, in part, by behind-the-meter natural gas generation fueled by associated gas that operators on its acreage would otherwise flare.9 In effect, the company is monetizing two stranded assets simultaneously: the dirt and the gas. Neither asset, on its own, has obvious value. Combined and converted into electrons fed into a GPU cluster, they have very obvious value indeed.

The company has also discussed solar development opportunities on portions of its acreage where surface use is not yet committed to active oil and gas operations, and there is some indication of bitcoin mining pilots that test the economics of using stranded gas to power compute when grid prices spike. None of these are at this stage core revenue lines. They are options.

That word — options — is key to the EagleRock story. The acreage portfolio is not just a static collection of rent-paying parcels. It is a long-dated call on multiple secular trends that have very little to do with oil prices: AI infrastructure demand, the decarbonization of compute, the regulatory pressure to monetize rather than flare associated gas, and the gradual conversion of the Permian from an oil basin into a hybrid energy basin that exports both molecules and electrons.

A skeptic will rightly point out that, as of the IPO, almost none of this contributes to current cash flow. Data centers and solar farms in the Permian are early. The hyperscaler contracts are still being negotiated. The behind-the-meter power generation business model has obvious technical and commercial risks. Anybody buying EagleRock for its data-center thesis today is paying for an option whose strike is years away.

But that is also the point. EagleRock is the rare energy IPO where the optionality is genuinely interesting rather than vaporware. Its lowest case is "we collect rent from drillers and water customers for the next twenty years and pay out most of it as cash distributions." Its higher cases involve becoming one of the principal landlords of one of the principal AI compute regions in North America. That is an unusually attractive return distribution for a company whose lowest case is already a perfectly respectable yield investment.

The transition from "Permian's landlord" to "critical infrastructure platform" is going to take a decade to play out, and most of the heavy lifting will be done by partners willing to spend their own capital on top of EagleRock dirt. But the trajectory is set. EROK is no longer just an oilfield surface-rights story. It is, increasingly, a story about who owns the land underneath the next generation of American industrial buildout.

VIII. Playbook: Frameworks & Moats

When you strip away the West Texas color and the IPO mechanics, what is EagleRock really? In Hamilton Helmer's Seven Powers taxonomy — the lens through which long-horizon investors increasingly evaluate competitive position — EagleRock displays an unusually clean stack of mutually reinforcing advantages.

Cornered Resource. This is the strongest of the seven, and the one most directly applicable here. EagleRock owns surface acreage above some of the highest-rate, lowest-breakeven shale on the planet. That acreage is, by definition, non-replicable: the geology under it cannot be moved, and the surface above any given section can be owned by exactly one entity. Once the basin's surface acreage has been aggregated by a small set of holders — EagleRock, Texas Pacific Land Corporation, LandBridge, and a handful of family ranches — there is no greenfield opportunity for a newcomer. The window has closed.10

Switching Costs. Once an operator's pads, flowlines, freshwater ponds, and produced-water gathering systems are physically located on EagleRock land, the cost of moving them is effectively infinite for the remaining life of the development. The capital has already been sunk in a specific geographic spot, and that spot is fixed.

Network Economies. The water gathering and recycling system gets more valuable as more operators tie into it. Each additional tie-in reduces the unit cost of operating the network and increases the depth of optionality on routing, blending, and storage. The same logic, in a smaller way, applies to internal road and gathering networks.

Scale Economies. A 236,000-acre contiguous block is administered with materially lower per-acre overhead than ten 23,600-acre blocks held by ten separate owners. Negotiations with operators are centralized. Legal, regulatory, and surveying costs spread over a larger denominator. The result is a structurally lower operating cost per dollar of revenue than smaller surface owners can achieve.

Counter-Positioning. This is more subtle. The Up-C structure, the deep alignment with EnCap and the founders, and the willingness to operate as a friendly long-term landlord rather than as an extractive monopolist all make EagleRock easier to deal with for the major operators than a pure-play, public surface-rights aggregator focused only on near-term rent maximization might be. In a small, repeat-game market like the Permian, that softer style is itself a competitive moat.

Now run the same exercise through Porter's Five Forces, with a sharper investor's lens.

Threat of New Entrants. Effectively zero in the Delaware and Midland Basins. The land has been aggregated. The remaining unowned, unfragmented surface tracts in the sweet spots are a vanishingly small share of the basin. Capital alone cannot create a new EagleRock; you would need ten years and a willingness to overpay every existing holder simultaneously.

Bargaining Power of Buyers. The "buyers" of EagleRock's services are the operators that drill on the acreage. Their bargaining power is constrained by the simple fact that their inventory is geographically locked. If you are Diamondback or Pioneer or ConocoPhillips drilling a section bounded on three sides by EagleRock land, you do not have the option to drill the same well in Pennsylvania. You sign the SUA and move on.

Bargaining Power of Suppliers. EagleRock's true "supplier" is the basin itself — the geological endowment that determines how many wells get drilled and at what rate. The basin is mature but enormous, with several decades of inventory at current activity levels. The supply of drillable rock is, for practical purposes, abundant.

Threat of Substitutes. This is the most interesting force, and the bear-case anchor. The substitutes are not other landlords — those are competitors, not substitutes. The substitute is the entire question of whether the basin matters in twenty or thirty years. If global demand for oil declines materially or domestic policy shifts dramatically, drilling activity drops, and the surface rent stream shrinks. EagleRock does not require commodity prices to be high. It requires drilling activity to continue. Substitutes for that activity — at the level of the entire energy economy — are the long-term existential variable.

Industry Rivalry. Among surface-rights holders, rivalry is more cooperative than cutthroat. Texas Pacific Land Corp, LandBridge, and EagleRock largely own different parts of the basin and compete only at the margin for new acquisitions and incremental SUAs with operators that happen to cross multiple jurisdictions. The bigger competitive variable is each landlord's relationship quality with the operators on its block.

Put all of that together and the resulting picture is unusually rare in commodity-adjacent businesses: a portfolio of contractually durable cash flows, sitting on top of a non-replicable asset, with multiple compounding moats, and meaningful long-dated optionality on top. The bull case essentially writes itself. The bear case, equally, is concentrated in a small handful of well-defined risks — which is where the next section goes.

IX. Analysis: Bear vs. Bull Case

Every IPO comes with a roadshow deck full of bull-case narrative. The serious work is to translate that narrative into a clear-eyed list of what has to go right and what could go wrong.

The Bull Case. The cleanest articulation of the bull case is that EagleRock is a permanent royalty on the operational intensity of the most strategically important hydrocarbon basin in the United States. It is structurally inflation-protected, because rents and fees can be reset or escalated and because surface use volume rises with activity. It is capital-light, because tenants pay the capex. It is operationally light, because the headcount required to administer a static block of land does not scale linearly with the cash flows it produces. It is increasingly diversified, with the water nexus already material and the data-center optionality genuinely live. And its largest holders — Campbell, Sellers, and EnCap — have skin, scar tissue, and reputation tied up in its long-term performance.10

The investor who buys EROK on this view is essentially saying: I want a high-margin, free-cash-generative landlord with a once-in-a-basin asset position, run by the most respected dealmakers in West Texas, with a real chance of being a critical piece of the next decade's data infrastructure on top of being a critical piece of the current decade's oil infrastructure. That is, on its face, a perfectly defensible thesis for a long-duration investor.

The Bear Case. There are three concentrated risk vectors worth taking seriously, none of which is fully resolved by anything in the prospectus.

The first is regulatory. The Texas Railroad Commission's response to induced seismicity is still evolving. If disposal restrictions tighten further, operators on EagleRock acreage face higher water-handling costs, which they will try to push back into the SUA negotiation. Recycling absorbs some but not all of the pressure. In a worst case, a coordinated reduction in disposal volumes across the Delaware Basin could constrain overall drilling activity for a period of quarters or years, which would dent the volume side of EagleRock's revenue equation even if the per-unit pricing held.[^7]

The second is terminal value. The Permian basin matters enormously in 2026. It matters less, eventually, in a world that has electrified light-duty transportation and decarbonized substantial portions of heavy industry. EagleRock's response to that long-arc risk is its optionality on power, data, and renewables, and that response is plausible — but it is also unproven. The data-center revenue line is, at the IPO, a sliver. Whether it can grow to be a meaningful counterweight to a structurally declining oil business in a 2045 scenario is the kind of question that gets resolved by the next two decades of capital allocation, not by anything visible today.

The third is valuation. EagleRock did not come public cheap. Comparing the implied multiples to Texas Pacific Land Corp (TPL), the original surface-rights story, and to LandBridge (LB), the more recent, faster-growing comparable, the IPO priced at a premium that anticipates a great deal of execution. TPL has a multi-decade track record, an ungeared balance sheet, and a long history of returning cash. LandBridge has a younger asset base but a more aggressive growth profile. EagleRock sits in between, and its acreage quality arguably justifies the premium — but the margin for disappointment is narrower than it would have been at, say, a 20 percent lower price.10 The Financial Times noted as much in an April 2026 piece comparing the three: investors are increasingly being asked to choose between three flavors of essentially the same idea, and the willingness to pay up for EagleRock specifically rests on the acreage quality and management track record.10

There are also smaller, second-order risks worth keeping on the watch list. The Up-C governance structure means public shareholders have limited recourse if the controlling shareholders pursue a strategy public investors dislike. The tax receivable agreement is a real, ongoing cash flow to insiders that reduces what is available to Class A holders over time. Insider lockups will eventually roll off, which means a future supply-demand imbalance on the equity. And the recently announced Double Eagle V fund, with $2.5 billion of fresh EnCap backing, is a reminder that the founders' attention is divided across more than just the public company.[^12]

Benchmarking. The cleanest peer is TPL, a longtime stalwart of the West Texas surface-rights world, whose story has, over decades, validated essentially the same thesis that EROK is now selling at IPO. LandBridge is closer in vintage and asset profile, but smaller. The Financial Times' surface-wars piece in April 2026 framed the trio as "the three flavors of the Permian landlord," with TPL the conservative incumbent, LandBridge the aggressive new entrant, and EagleRock the well-credentialed middle ground.10 An investor's choice among the three is, in many respects, a choice about how to weight track record against growth against acreage quality.

KPIs to Track. For an investor focused on whether the EagleRock thesis is actually playing out quarter by quarter, three numbers matter more than the rest.

The first is rig count on EagleRock acreage — the simplest leading indicator of upcoming SUA, ROW, and water-related revenue. The second is barrels of produced water handled per day, with a particular eye on the mix between disposal and recycled water, since the latter has structurally better unit economics and is also a hedge against further regulatory tightening. The third is committed long-term contracts with non-oil-and-gas counterparties — hyperscalers, power developers, solar operators — because that is the clearest signal that the "next act" is graduating from optionality to recurring revenue. Everything else, including reported EBITDA and headline distributable cash flow, is downstream of these three.

Together, they form a clean, falsifiable dashboard. If activity stays elevated, water volumes grow, and non-hydrocarbon contracts start to appear in the operating commentary, the bull thesis is on track. If any one of them stalls for an extended period, the cleanly compounded story starts to look more complicated.

X. Epilogue & Final Reflections

There is a particular kind of business model that, once you see it, you start seeing everywhere. The owner of the asset on top of which other people invest their capital. The toll booth on the road that the trucks have to use. The landlord whose tenants pay both the rent and the property tax. The middleman who never touches the inventory.

EagleRock Land is one of the cleanest examples of that pattern in the public market. It does not produce oil. It does not refine gas. It does not own a single drilling rig. What it owns is the dirt, the right to charge people for stepping on the dirt, and the pipelines and ponds and pads they have to install in order to do anything useful on top of the dirt. In the Permian Basin of the late 2020s — a basin that has gone from frontier to factory to constrained industrial complex — that is an extraordinary asset position.

The thread that runs from a $40,000 credit-card limit in the late 2000s to a $740-million-plus IPO in 2026 is, at its core, a thread about recognizing where the binding constraint really lives. In the early days of the shale revolution, the constraint was geology — and the people who profited were the people who could find the rock. As the rock got commoditized, the constraint shifted to capital — and the people who profited were the people who could raise and recycle private equity at scale. By the mid-2020s, the constraint had shifted again, to the surface — and the people best positioned to profit, almost in retrospect, were the people who had been quietly buying that surface all along.

Campbell and Sellers did not invent the idea. Texas Pacific Land Corporation has owned dirt in West Texas since the nineteenth century. But Campbell and Sellers did invent a particular institutional playbook for it: aggregate aggressively, structure thoughtfully, retain the right rights at the right moment, and bring a public-company executive in to translate the result into something a buy-side analyst can model. EROK is the formalization of that playbook, packaged into common stock.

Whether the stock is a buy at the current price is not the question this piece is going to answer. It is the kind of question that depends on time horizon, on commodity outlook, on regulatory trajectory, on what the data-center optionality actually turns out to be worth, and on how much trust one is willing to extend to a controlling shareholder block that, by design, holds the steering wheel of the company.

What is clearly true is that EagleRock represents a particular thesis about American energy that is worth understanding regardless of one's view on the stock. The thesis is this: the most valuable real estate in the Permian Basin is not the rock two miles down. It is the caliche under your boots.

The Earth's surface, in the only place in North America where it really matters this decade, is what they are not making more of. Everything else — the oil, the gas, the water, the electrons, the GPUs, the carbon credits — flows through it. EagleRock is the company built around that observation.

What happens next depends on whether Greg Pipkin and his team can run the public-company playbook with the same discipline that Cody Campbell and John Sellers ran the private one. The early signal — a top-of-range IPO pricing, a deep institutional sponsor base, a fully aligned founding group with most of their wealth still tied to the operating LLC — is encouraging. The longer-arc signals will arrive one rig count, one water barrel, and one hyperscaler contract at a time, and those are the data points that should drive the long-term view rather than the noise of any particular quarter.

For now, EROK sits on the exchange as one of those rare IPOs where the underlying business model is genuinely worth pausing on, regardless of whether one ever takes a position. It is a reminder that the most durable franchises in any cyclical industry are often the ones standing slightly to the side of the cycle — collecting rent while everyone else takes the risk.

In the basin they call the Permian, that side, as it turns out, is the top.

References

-

SEC Form S-1 Registration Statement — EagleRock Land, LLC ↩↩↩↩↩↩

-

The Permian Kings: Cody Campbell and John Sellers Profile — Bloomberg Businessweek, 2025-01-15 ↩↩↩↩

-

Diamondback Energy to Acquire Double Eagle IV for $4B — Reuters, 2024-02-12 ↩↩

-

Water is the New Oil in the Permian Basin — Houston Chronicle, 2025-11-10 ↩↩↩↩

-

Gregory Pipkin Jr. Form 3 Initial Statement of Beneficial Ownership — SEC, 2026-05-13 ↩↩

-

The Up-C Structure Explained for Energy IPOs — Skadden, Arps, Slate, Meagher & Flom LLP, 2025-12-01 ↩↩

-

Data Centers in the Desert: The Permian's New Power Play — The Economist, 2026-03-05 ↩↩↩

-

Texas Pacific Land vs. LandBridge vs. EagleRock: The Surface Wars — Financial Times, 2026-04-20 ↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube