Energy Recovery Inc.: The Story of an Industrial Dark Horse

I. Introduction & Episode Roadmap

There is a company headquartered in a modest office park in San Leandro, California, that holds a near-monopoly over one of the most critical processes in modern civilization: making seawater drinkable. Energy Recovery Inc., trading under the ticker ERII on the Nasdaq, commands a market capitalization of roughly half a billion dollars. Most investors have never heard of it. Most people who drink desalinated water every day have never heard of it. And yet, without this company's technology, the cost of desalination around the world would be dramatically higher, and hundreds of millions of people in the Middle East, North Africa, and Asia would face a far more precarious water future.

The puzzle of Energy Recovery is this: how did a small company, founded by a Norwegian inventor in 1992, build a device called the PX Pressure Exchanger that captured over ninety percent of the global desalination energy recovery market? How does a company that makes industrial hardware consistently generate gross margins above sixty-five percent, territory typically reserved for software businesses? And how, after dominating its niche so completely that growth became constrained, did it attempt the treacherous leap into entirely new industries?

This is a story about deep technology, the kind that takes a decade or more to commercialize. It is about the patience required to sell into industries that move at geological speed, about the financial discipline needed to survive revenue volatility that would break most small companies, and about the strategic challenge of reinvention when your core market matures. Energy Recovery's journey from a single-product desalination company to an aspiring multi-industry platform illustrates every tension between focus and diversification, between the comfort of a monopoly and the hunger for growth.

The narrative arc follows three major inflections: the moment desalination plants around the world adopted the PX as the de facto standard, the ambitious but troubled pivot into oil and gas through a technology called VorTeq, and the more recent transformation into a multi-product industrial technology company now navigating project delays, a CO2 business wind-down, and a stock price that has fallen more than thirty percent from its highs.

There is also a founder's story as dramatic as any in technology: a Norwegian inventor held as a prisoner of war in Baghdad, a bitter patent dispute that nearly tore the company apart, and a succession of CEOs each tasked with answering the same impossible question: what do you do after you've already won?

Along the way, there are lessons about what makes a business truly defensible, why boring industries produce extraordinary investment opportunities, and what happens when patience runs out.

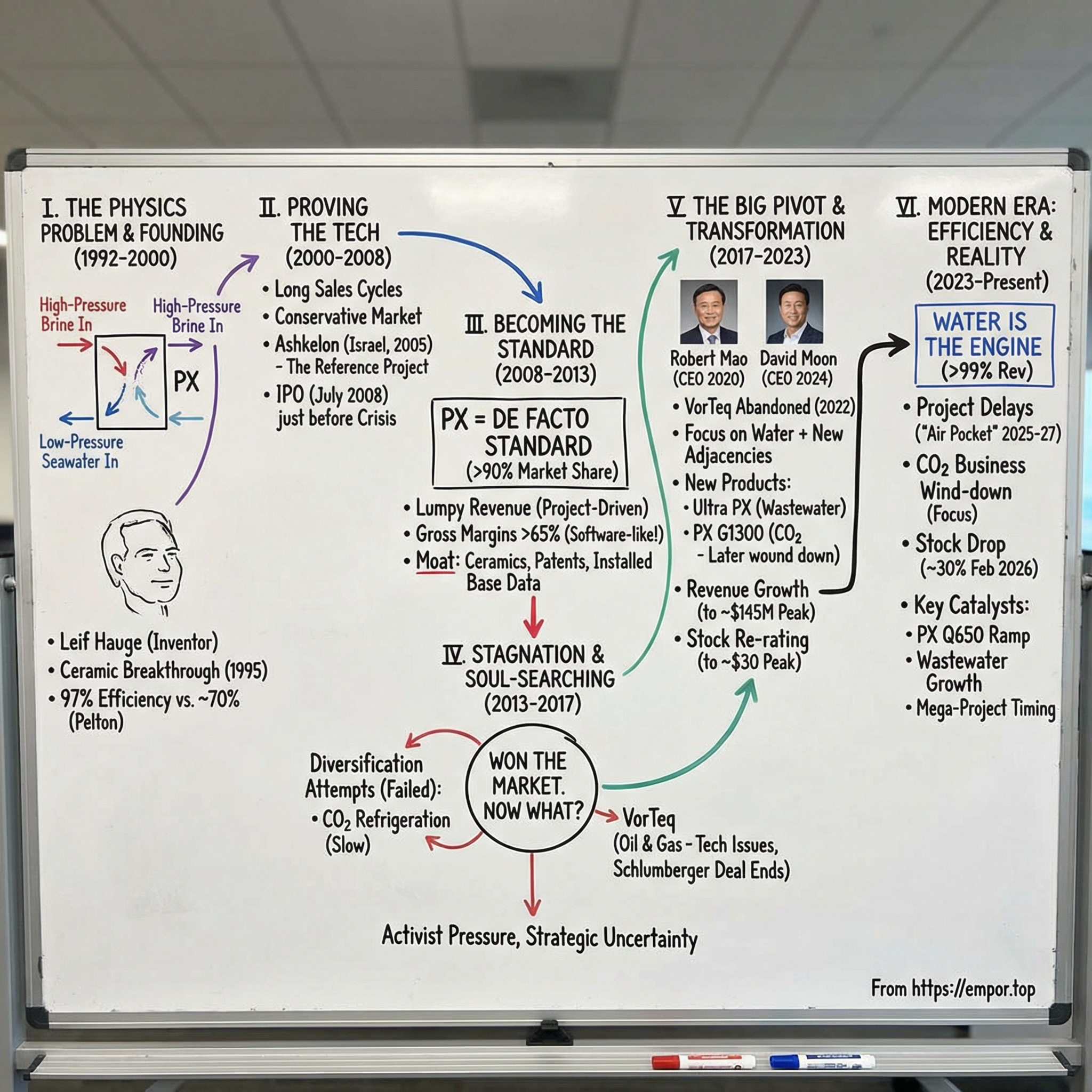

II. The Physics Problem & Founding Vision (1992-2000)

Picture a fjord in western Norway, steep granite walls plunging into cold, dark water. A young engineer named Leif Hauge is visiting his brother's vegetable farm, perched on a hillside above the fjord. The farm needs water pumped up from below, and Hauge, who had worked as a carpenter before turning to invention, becomes fascinated by the problem of moving water efficiently against pressure. It is a simple observation, the kind that lodges in an inventor's mind and refuses to leave.

The path from that Norwegian fjord to founding a company would take a detour through one of the most dramatic episodes in modern geopolitical history. In the late 1980s, Hauge was working at the Kuwait Institute of Scientific Research, developing pressure exchanger concepts for desalination. When Saddam Hussein's forces invaded Kuwait in August 1990, Iraqi soldiers targeted KISR seeking advanced technology. Researchers at the facility destroyed key documents to prevent the technology from falling into enemy hands. Hauge was abducted by Iraqi forces and held as a prisoner of war in Baghdad, reportedly used as a human shield. Critically, Saddam never got the plans or the device.

After the Gulf War ended and Hauge was repatriated to the United States, he carried with him the knowledge that would birth an industry.

To understand what Hauge eventually built, you need to understand why desalination is so expensive. The dominant technology for turning seawater into drinking water is called reverse osmosis. Think of it this way: if you take a semi-permeable membrane, essentially a very fine filter, and push saltwater against it at extremely high pressure, pure water molecules squeeze through while salt and other dissolved solids stay behind. The problem is that "extremely high pressure" part. Seawater reverse osmosis plants operate at pressures of fifty-five to seventy bars, roughly fifty to seventy times atmospheric pressure. Generating that kind of pressure requires enormous amounts of electricity, and in the 1990s, energy represented more than half the total operating cost of a desalination plant.

Here is the critical insight: after the freshwater passes through the membrane, you are left with a concentrated brine stream that is still at very high pressure. Only about thirty-five to forty-five percent of the incoming seawater is converted to freshwater. The remaining fifty-five to sixty-five percent exits as high-pressure brine still carrying most of the applied energy. In early desalination plants, that high-pressure brine was simply dumped, and all the energy that had been used to pressurize it was wasted. It was like heating your house with the windows open. In the 1970s, desalination required roughly twenty kilowatt-hours per cubic meter of freshwater. Even by the 1990s, with better membranes and pumps, energy remained the dominant cost.

Hauge's breakthrough was conceptually elegant. He designed a device called a pressure exchanger that would take the high-pressure energy from the outgoing brine stream and transfer it directly to the incoming feedwater. Picture a ceramic cylinder, about the size of a large thermos, with a rotor inside containing longitudinal channels. The rotor spins at roughly twelve hundred revolutions per minute, completing about twenty full rotations per second. At any given moment, half of the rotor's channels are exposed to the high-pressure brine stream and half to the low-pressure feedwater. As the rotor turns, high-pressure brine enters one end of a channel and acts as a liquid piston, pushing the low-pressure seawater out the other end at high pressure. The energy transfer happens in a fraction of a second per channel cycle, with minimal mixing between the two streams. The rotor is the only moving part. No motors, no valves, no complex electronics. The device requires no electricity at all, driven entirely by the fluid flows themselves. The physics are simple, but the engineering is extraordinarily difficult.

In April 1992, Hauge and his wife Marissa formally incorporated Energy Recovery Inc. in the state of Virginia. For the first three years, he attempted to build the pressure exchanger from stainless steel, titanium, and other high-grade alloys. Every attempt failed. Seawater, it turns out, is a terrible lubricant. The metal components would gall and seize, grinding against each other until the device locked up.

By 1995, Hauge made a pivotal decision: he abandoned metal entirely and turned to advanced ceramics. This was counterintuitive. Ceramics are brittle, difficult to machine to tight tolerances, and not traditionally associated with high-pressure industrial equipment. But ceramics have three properties that made them ideal for this application: they are extremely resistant to saltwater corrosion, they can be manufactured to tolerances of a few thousandths of an inch, and their surface hardness prevents the galling and seizing that destroyed every metallic prototype.

The choice of ceramics would become one of the company's most enduring competitive advantages. It takes years of trial and error to develop reliable ceramic manufacturing processes for pressure exchange applications, and the resulting know-how cannot be easily replicated through reverse engineering or patent study. By 1997, Hauge had developed several commercial ceramic devices that were saving energy in medium-sized desalination plants in the Canary Islands, providing the first proof that the concept could work in real-world industrial conditions.

This was not obvious technology. The graveyard of failed energy recovery attempts in desalination was already crowded by the 1990s. Pelton wheels, a kind of water turbine that converts the high-pressure brine stream into rotational energy that drives a generator or pump, had been used since the 1980s. They were simple and reliable but captured only fifty to seventy percent of the available energy. Turbochargers and other centrifugal devices were incrementally better, pushing into the low eighties, but still left enormous amounts of energy on the table.

The fundamental problem with all centrifugal approaches is the double energy conversion: hydraulic energy becomes mechanical rotational energy, which then becomes hydraulic energy again. Each conversion loses efficiency. Hauge's isobaric approach eliminated both conversions entirely, transferring pressure directly from one liquid stream to another. The result was net transfer efficiencies of up to ninety-seven percent.

That gap between seventy-something percent and ninety-seven percent may sound small in percentage terms, but in absolute terms it translated into millions of dollars in annual energy savings for every large desalination plant. For a plant producing two hundred thousand cubic meters per day, the difference between an eighty percent efficient device and a ninety-seven percent efficient device could mean two to three million dollars per year in reduced electricity costs. Over a thirty-year plant life, that difference compounds to sixty to ninety million dollars, enough to justify almost any premium on the initial equipment purchase.

But as the dot-com boom consumed investor attention and Silicon Valley capital in the late 1990s, a small company in Virginia making ceramic cylinders for water plants attracted little notice. By 1999, dozens of PX devices were installed globally, and by 2002, nearly five hundred were in the field. But the company's founder would not be there to see what came next.

Hauge departed Energy Recovery in 2000 under contentious circumstances. In a dramatic turn, he registered all pressure exchanger patents with the U.S. Patent and Trademark Office and assigned the rights to a new entity, Energy Recovery International. He notified two hundred of the company's customers that patent rights had been transferred and informed shareholders he was suing ERI for patent infringement.

The company fought back with a three-count complaint in federal court, and the dispute was resolved through a settlement agreement in March 2001. Hauge went on to found Isobaric Strategies Inc., but the technology he had originated remained with Energy Recovery. The messy divorce was a reminder that even the most elegant inventions come wrapped in human drama.

III. The Long Slog: Proving the Technology (2000-2008)

Two figures would prove essential to Energy Recovery's survival and growth during the long proving years. Hans Peter Michelet had joined the board of directors in 1995, drawn by the promise of a technology that could reshape the global water industry. A Norwegian-born investor and entrepreneur with a finance degree from the University of Oregon, Michelet had spent his career founding and developing multinational organizations. He recognized something that most investors missed: the desalination market was not a niche. It was an inevitability. Michelet became chairman of the board in 2004 and would eventually serve as executive chairman starting in 2008, providing the strategic continuity that the company desperately needed.

The second critical figure was G.G. Pique, who became president and CEO in 2002. Pique brought more than thirty-five years of water industry experience and was recognized as an expert in reverse osmosis. He would later describe the company he inherited as "a one-and-a-half-million-dollar-a-year garage operation." What Pique built over the next decade was something entirely different.

The challenge of selling pressure exchangers to the desalination industry was a masterclass in the difficulty of deep technology commercialization. Desalination plants are massive infrastructure projects, typically costing hundreds of millions of dollars and taking three to five years to design and build. They are constructed by engineering, procurement, and construction firms like Veolia, IDE Technologies, Doosan, and Acciona on behalf of government utilities and sovereign water authorities.

The decision-making process involves multiple layers of bureaucracy, conservative engineering cultures that default to proven technologies, and sales cycles that stretch from three to five years. An engineer specifying equipment for a new plant is not going to risk a hundred million dollar project on unproven technology, no matter how impressive the laboratory data. A single decision to specify Energy Recovery's PX devices in a plant design might take half a decade from initial introduction to purchase order. For a small company burning cash, that timeline felt like eternity.

Also in 2002, the company hired Richard Stover as chief technology officer, a chemical engineer with a PhD from UC Berkeley whose dissertation on bubble dynamics in electrolytic gas evolution hinted at the kind of mind that thrived on fluid physics problems. Stover's task was to develop the next generation of pressure exchangers that could compete at the scale of the world's largest desalination projects. He led the development of the PX-220, which would become the leading energy recovery device in the industry. His work was recognized in 2006 when he shared the European Desalination Society's Sidney Loeb award for outstanding innovation.

The breakthrough contract came in 2003, when Energy Recovery's isobaric devices were specified for the Ashkelon seawater reverse osmosis plant in Israel. Built by a consortium led by IDE Technologies and Veolia, Ashkelon was designed to be the world's largest seawater reverse osmosis plant. When it began operations in August 2005, it was producing 100,000 cubic meters of freshwater per day, enough to supply roughly fifteen percent of Israel's domestic water consumption, at a cost of just over fifty cents per cubic meter.

That price stunned the industry. Previous large desalination plants had produced water at costs well above a dollar per cubic meter. Ashkelon demonstrated that reverse osmosis with efficient energy recovery could produce freshwater at prices competitive with traditional water sources. The PX devices were a key reason the plant could achieve such low operating costs, and Ashkelon became the reference installation that every subsequent project would be measured against. For Energy Recovery, it was the equivalent of getting your product installed in the most prestigious building in the city: every architect in the world would take note.

Revenue told the story of a company beginning to find its footing. In 2005, Energy Recovery generated just under eleven million dollars in sales. The following year, revenue nearly doubled to twenty million. In 2007, it jumped again to thirty-five million, a seventy-seven percent increase. The growth was lumpy and unpredictable, driven by the timing of mega-projects that could swing revenue dramatically from quarter to quarter. But the trajectory was unmistakable.

The company's operating margins were also improving rapidly, climbing from roughly ten percent in 2005 to over twenty-six percent by 2007. This margin expansion reflected the inherent operating leverage of the business: each additional unit sold carried high gross margins, and the fixed cost base did not need to grow proportionally. It was a financial model that, if the revenue growth continued, could produce exceptional returns on invested capital. The question was whether the growth would continue, or whether the company was simply benefiting from a handful of well-timed projects.

Under Pique's leadership, the company had transformed from Hauge's garage invention into the dominant player in desalination energy recovery, commanding roughly seventy percent of the market by 2008. The company had survived on approximately twenty-four million dollars in total private investment over its fifteen-year pre-IPO development period, a remarkably frugal history for a company developing breakthrough industrial technology.

On July 2, 2008, Energy Recovery went public on the Nasdaq, ending what had been a two-month drought of successful IPOs in the market. Citi and Credit Suisse served as joint bookrunning managers. The offering comprised nearly fourteen million shares at eight dollars and fifty cents each, raising approximately sixty-nine million dollars in gross proceeds. The stock opened at eleven dollars, twenty-nine percent above the offering price, before settling to close at nine dollars and eighty-three cents.

The timing, however, was spectacularly unfortunate. The IPO came just weeks before the global financial system began its catastrophic unraveling. Lehman Brothers would collapse in September. Credit markets would freeze. Infrastructure projects around the world would be delayed or cancelled.

Energy Recovery had just raised the capital it needed to scale, but the market it was selling into was about to seize up.

Full-year 2008 revenue reached fifty-two million dollars, the company's best year yet, reflecting orders placed before the crisis hit. The company was profitable, with the IPO proceeds providing a financial cushion that would prove essential. But the pipeline of new projects was already thinning as governments and developers paused infrastructure spending worldwide.

In a cruel twist, the company had finally achieved the scale and public market access it needed to capitalize on the global desalination boom, just as that boom hit pause. The next several years would test whether Energy Recovery's technology advantage was strong enough to survive a brutal economic downturn, or whether the company would become another casualty of unfortunate timing.

IV. The Inflection Point: Becoming the Standard (2008-2013)

The years following the IPO were defined by a paradox: Energy Recovery was winning the technology war but losing the revenue battle. The PX Pressure Exchanger was becoming the de facto standard for new desalination plants globally. Every major engineering firm studying energy recovery options for reverse osmosis reached the same conclusion: the PX's ninety-seven percent efficiency was so far superior to competing technologies that specifying anything else was almost indefensible on an engineering basis. The installed base grew steadily, creating a powerful feedback loop. More installations meant more operating data, which meant better products, which meant more wins.

But the global recession of 2008-2009 slowed new desalination project approvals to a crawl. Revenue dipped from fifty-two million in 2008 to forty-seven million in 2009 and forty-six million in 2010. Then came 2011, when revenue collapsed to twenty-eight million dollars, a thirty-nine percent decline that shook investor confidence. The stock price followed revenue downward, eventually touching one dollar and ninety-five cents in April 2012.

The culprit was not competition or technology failure. It was the lumpy, project-driven nature of the desalination market. When a handful of mega-projects are delayed by a year, the revenue impact on a small, concentrated supplier is devastating. This pattern of project-driven volatility would repeat throughout the company's history, becoming perhaps the single most important characteristic for investors to understand. Energy Recovery's revenue in any given year is determined far less by its competitive position, which remains dominant, than by the timing of a handful of large orders.

What sustained the company through this volatility was the growing recognition that the PX had no real substitute. Competing energy recovery devices, primarily the centrifugal devices made by companies like Flowserve and Danfoss, operated at significantly lower efficiencies. For a large desalination plant processing hundreds of thousands of cubic meters per day, the difference between seventy-five percent and ninety-seven percent energy recovery efficiency translated into millions of dollars in annual electricity savings. Once a plant operator experienced the PX's economics, there was no going back.

Why didn't competitors catch up? The answer lies in the intersection of physics and manufacturing. The isobaric approach, transferring pressure through direct liquid-to-liquid contact, is fundamentally more efficient than the centrifugal approach used by Pelton wheels and turbochargers, which convert hydraulic energy to rotational mechanical energy and then back to hydraulic energy, losing efficiency at each conversion step. It would be like converting dollars to euros to yen and back to dollars, losing a few percent at each exchange, versus directly swapping equal amounts. The PX eliminated the intermediate conversions entirely.

But knowing the physics was not enough. Building a device that could maintain the required tolerances, with gaps of just a few thousandths of an inch between the ceramic rotor and its housing, while handling corrosive seawater at seventy bars of pressure, required manufacturing know-how that took years to develop. Flowserve, which acquired Calder Energy Recovery Systems in the mid-2000s, attempted to compete with its own isobaric device, the DWEER (Dual Work Exchange Energy Recovery), but struggled to match the PX's reliability and efficiency in the field. Danfoss marketed its iSave device, an integrated motor and pump system, but it was better suited for smaller brackish water applications than the massive seawater plants where Energy Recovery dominated.

The intellectual property moat deepened year by year. Energy Recovery accumulated more than two hundred patents and trade secrets covering the design, manufacturing, and application of its pressure exchange technology. The ceramic manufacturing process itself represented a form of process power: replicating the tight tolerances and material science required to build a PX device was not something a new entrant could accomplish quickly, even with significant capital investment. The company's manufacturing facility in San Leandro, California, became a kind of temple of precision ceramics, where quality control processes were refined over thousands of production runs.

The validation came from the Middle East, where water scarcity was not a future risk but a present reality. Saudi Arabia, which produces over twenty percent of the world's desalinated water, launched massive capacity expansion programs. The Saline Water Conversion Corporation, the kingdom's state-owned desalination authority, began specifying PX devices as standard in new reverse osmosis plants. A thirty-three million dollar contract from Saudi Arabia, one of the largest in the company's history at that point, demonstrated the scale of the opportunity.

The United Arab Emirates followed with a five million dollar award, and as word spread through the tight-knit community of desalination engineers and EPC firms, a powerful network effect took hold. IDE Technologies, Doosan, Acciona, and other major desalination contractors standardized their designs around the PX. Israel expanded its desalination capacity with PX devices at Hadera and Palmachim, building on the Ashkelon reference. Singapore, Australia, and Spain all commissioned major reverse osmosis plants featuring Energy Recovery's technology.

The geographic spread was itself a form of competitive moat. With reference installations operating successfully across dozens of countries and climates, from the extreme heat of the Arabian Peninsula to the temperate waters of the Mediterranean, the PX had accumulated a body of real-world performance data that no competitor could match.

By 2012, revenue rebounded sharply to forty-three million dollars, and 2013 held roughly steady at the same level. The company was profitable, generating positive operating cash flow, and the PX's market share in new desalination installations had climbed above ninety percent. Energy Recovery had crossed the adoption chasm that Geoffrey Moore famously described in his book of the same name. The technology was no longer novel or risky. It was the standard.

To put the impact in perspective, Energy Recovery's technology had helped drive the cost of desalinated water from roughly ten dollars per cubic meter in the 1960s down to under fifty cents per cubic meter by the late 2000s. The PX was not solely responsible for this decline, improvements in membrane technology and pump efficiency played major roles, but the step-change in energy recovery efficiency from seventy percent to ninety-seven percent was one of the most significant contributors. The theoretical minimum energy required for reverse osmosis is approximately one kilowatt-hour per cubic meter. With PX devices, plants could operate at specific energy consumption as low as 0.8 kilowatt-hours per cubic meter, remarkably close to the thermodynamic limit.

The financial transformation was meaningful: the company demonstrated that it could maintain gross margins in the sixty-five percent range even during revenue downturns, a testament to the pricing power that comes with a near-monopoly position in a mission-critical application. The PX's impact was now measured in planetary terms: the installed base of devices was helping to produce millions of cubic meters of freshwater daily across more than a hundred countries, and the company estimated the technology was avoiding over twenty-six terawatt-hours of energy consumption annually, equivalent to removing more than two and a half million passenger vehicles from the road.

But market dominance brought its own challenge. When you already own ninety percent of the market, where does growth come from?

V. The Stagnation & Soul-Searching (2013-2017)

G.G. Pique retired as CEO in February 2011, handing the reins to Tom Rooney, who brought nearly thirty years of executive experience including a stint as CEO of SPG Solar. Rooney's mandate was clear: reduce costs, improve manufacturing efficiency, and find new markets. He achieved a notable success in recovering Energy Recovery's desalination market share from roughly fifty percent back to ninety percent within two years, a testament to the PX's fundamental superiority. But the broader strategic challenge of growth remained unsolved.

In December 2009, the company had acquired Pump Engineering LLC of New Boston, Michigan, for approximately twenty million dollars in cash plus one million shares of stock. Pump Engineering manufactured the very type of centrifugal energy recovery devices, turbochargers and hydraulic turbines, that the PX was displacing. The acquisition added these legacy products to Energy Recovery's lineup, enabling the company to offer packaged solutions that included both isobaric and centrifugal devices for different plant sizes and configurations.

The strategic logic was sound: by owning the competing technology, Energy Recovery could control the transition pace and offer customers a full spectrum of options while steering them toward the higher-efficiency PX. But the acquisition did not fundamentally change the growth trajectory. The centrifugal products were a declining business as the PX gained share, and the integration required management attention during a period when the core technology was still establishing itself as the industry standard.

When Rooney resigned in early 2015, Joel Gay stepped into the role. Gay had joined Energy Recovery as chief financial officer in 2012 and was formally appointed CEO in April 2015. At the time, he was noted as one of the youngest Black CEOs of a publicly traded company, and Fortune magazine would name him to its 40 Under 40 list in 2016. He inherited a company that was profitable, cash-rich, technologically dominant, and frustratingly stagnant.

The numbers told the story of a company trapped in an uncomfortable middle ground. Revenue in 2013 was forty-three million dollars. In 2014, it dropped to thirty million, a twenty-nine percent decline driven by the timing of Middle Eastern mega-projects. In 2015, it recovered to forty-four million. In 2016, it climbed to fifty million. In 2017, it reached fifty-eight million.

The overall trajectory was upward, but the year-to-year volatility and the slow pace of growth relative to the company's market position left investors restless. The stock had touched an all-time low of one dollar and ninety-five cents in April 2012, and while it had recovered to the five-to-eight dollar range by mid-decade, the market was telling Energy Recovery that it was valued as a mature, low-growth industrial company. For a business with ninety percent market share and sixty-five percent gross margins, that valuation felt like an insult to long-term shareholders who understood the quality of the franchise.

The strategic question was existential: what do you do when your core market is growing at single digits and you already own virtually all of it? The desalination industry was expanding globally, driven by water scarcity in the Middle East, Asia, and increasingly the American Southwest. But Energy Recovery's share of that market was so dominant that the company's growth was essentially capped at the growth rate of new desalination capacity additions. That rate was meaningful, perhaps five to eight percent annually, but it was not enough to excite growth investors or justify a premium valuation multiple.

The company faced a variant of what Clayton Christensen called the "innovator's dilemma," though from the opposite direction. Most companies face disruption from below, as cheaper technologies erode their market. Energy Recovery faced the dilemma of having disrupted so completely that there was nobody left to displace. The market was won. Now what?

Management explored several diversification paths, each guided by a seemingly logical extension of the company's core expertise in pressure exchange. The most technically adjacent bet was CO2 refrigeration. Supermarkets and grocery stores are among the largest commercial energy consumers, and their refrigeration systems represent a significant share of that consumption. The industry was beginning to transition from traditional hydrofluorocarbon refrigerants to carbon dioxide, which is more environmentally friendly but operates at much higher pressures. Energy Recovery saw an opportunity to apply its pressure exchange technology to reduce the energy consumption of transcritical CO2 refrigeration systems.

The technical concept was sound: a pressure exchanger could recover energy from the high-pressure supercritical CO2 stream and transfer it to the low-pressure side, reducing compressor work by fifteen to twenty-five percent. But the commercial reality proved challenging on every dimension. The grocery industry operated with razor-thin margins and notoriously long procurement cycles. Store managers and facilities engineers were skeptical of any technology that might risk refrigeration failures, which could spoil millions of dollars worth of perishable inventory. The sales motion bore no resemblance to desalination: instead of selling to a dozen mega-project EPC firms, the CO2 business required convincing thousands of individual grocery chains, one store at a time. The unit economics were orders of magnitude smaller, with each installation worth tens of thousands rather than millions.

The more ambitious bet was oil and gas. Energy Recovery launched VorTeq in December 2014, a technology that applied pressure exchange principles to hydraulic fracturing. In fracking, enormous volumes of fluid mixed with abrasive proppant are pumped at extremely high pressure into wellbores to crack open rock formations. The pumps used in this process are among the most abused pieces of equipment in all of industry, and replacing them is one of the largest recurring costs in well completion. VorTeq was designed to re-route the abrasive proppant-laden fluid away from the high-pressure pumps, so they would only process clean water. The system used tungsten carbide components and could handle up to a hundred and ten barrels per minute at fifteen thousand pounds per square inch. If it worked, it could more than double pump life and reduce fracking break-even costs by five to ten dollars per barrel.

Field trials began with Liberty Oilfield Services in the Bakken Formation in 2015, and in October of that year, Energy Recovery signed a headline-grabbing fifteen-year exclusive license with Schlumberger. The deal structure was dramatic: Schlumberger paid a seventy-five million dollar exclusivity fee upfront and agreed to two additional milestone payments of twenty-five million dollars each, contingent on VorTeq meeting certain key performance indicators expected to be achieved in 2016.

But the milestones were not met. The VorTeq encountered serious vibration and reliability issues that required a significant redesign. The harsh realities of the oilfield, with its extreme temperatures, abrasive proppants, and punishing operating conditions, proved far more difficult to master than desalination's relatively benign seawater environment. Year after year, management guided toward progress that failed to materialize. The two twenty-five million dollar milestone payments never came. By 2017, VorTeq had become a symbol of over-promising and under-delivering, and investors filed class action lawsuits accusing the company of misleading shareholders about the technology's readiness.

Activist investors took notice. For a company sitting on substantial cash reserves and generating consistent if unspectacular profits, the temptation to pressure management was strong. The critique was pointed: Energy Recovery risked becoming a "lifestyle business," comfortable in its desalination monopoly, burning cash on speculative adjacencies, and failing to return capital to shareholders.

The activist argument had some merit. Energy Recovery had accumulated cash that was earning negligible returns on the balance sheet while simultaneously investing in technologies that had yet to produce revenue. The company's return on equity during this period was underwhelming given its monopoly position, and the stock was trading at a fraction of its post-IPO highs. From a pure capital allocation standpoint, the activists had a point: either invest the cash in projects with clear return profiles, return it to shareholders through buybacks or dividends, or pursue strategic alternatives including a potential sale of the company.

Board pressure intensified, and the company entered a period of genuine strategic uncertainty about its identity and direction.

Was Energy Recovery a desalination company that should maximize cash returns from its monopoly? Or was it a technology platform with broader ambitions that justified continued investment in unproven markets? The answer would define the next decade.

VI. The Big Pivot: Oil & Gas Awakening (2017-2020)

The Schlumberger partnership, for all its disappointments, taught Energy Recovery something invaluable: pressure exchange technology had genuine applicability beyond desalination, but commercializing it in a new industry was an order of magnitude harder than anyone had anticipated. The well completion market represented a potential addressable opportunity worth billions, but the engineering challenges of handling abrasive proppant slurries at extreme pressures had been profoundly underestimated.

The leadership changes continued, reflecting the difficulty of finding the right executive to navigate the company's strategic crossroads. Joel Gay resigned in 2018. Chris Gannon, a veteran of the water and wastewater industry, stepped in as interim president and CEO.

Then came Robert Yu Lang Mao, perhaps the most improbable CEO in the company's history. Mao had served as chairman and CEO of 3Com Corporation, the networking equipment company, and as chairman for the China region at Hewlett-Packard. He joined Energy Recovery's board in 2010, became chairman in 2019, and was formally named president and CEO in May 2020. His background in technology hardware and global operations brought a different lens to the company's challenges. Where previous leaders had come from the water industry, Mao thought in terms of platform technology, global supply chains, and manufacturing scale. His appointment signaled that the board was looking beyond desalination for the company's future.

Revenue continued its slow but steady climb from the desalination base: fifty-eight million in 2017, sixty-one million in 2018, and seventy-three million in 2019. Each year's growth was modest in isolation, but the cumulative effect was significant. From a trough of twenty-eight million in 2011, the water business had more than doubled in eight years.

The aftermarket business was becoming increasingly important during this period. As the global installed base of PX devices grew, the recurring revenue from replacement parts and maintenance created a more predictable income stream that partially offset the lumpiness of new project orders. A desalination plant that installed PX devices in 2005 would need replacement rotors, end covers, and bearings at regular intervals over its thirty-year life. With thousands of devices now operating worldwide, this annuity-like revenue was quietly becoming the foundation of the business.

The company also opened a Commercial Development Center near Houston in 2019, signaling continued commitment to oilfield technology development even as the Schlumberger milestones remained unmet. The Houston facility gave the company proximity to the Permian Basin operators who would ultimately determine whether pressure exchange technology could find a home in the oilfield.

Then 2020 happened. The COVID-19 pandemic and the simultaneous oil price collapse created a double stress test. Oil prices briefly went negative in April 2020, crushing the economics of every oilfield technology investment. In June 2020, the Schlumberger exclusive licensing agreement was terminated. Energy Recovery recognized approximately twenty-four million dollars in previously deferred Schlumberger revenue upon termination, which helped boost full-year 2020 revenue to ninety-two million dollars. The headline number was strong, but the underlying message was clear: the VorTeq bet, as originally structured, had failed.

The forced austerity of the pandemic had a clarifying effect. Under Mao's leadership, the company tightened operations, reduced costs, and emerged with a sharper understanding of where its resources should be deployed.

The desalination business proved remarkably resilient through the pandemic and its aftermath. Water infrastructure spending continued even as other capital expenditures were cut, because governments could not simply stop providing water to their populations. If anything, the pandemic reinforced the strategic importance of water security, as countries recognized the vulnerability of their critical infrastructure systems.

VorTeq was officially abandoned in 2022, after approximately eight years of development and tens of millions of dollars in cumulative investment. The technology never achieved the reliability needed for commercial deployment, and the Schlumberger exclusivity had already been terminated. Investors, somewhat paradoxically, cheered the decision to stop the bleeding. The stock rose on the announcement, as the market rewarded the discipline of acknowledging failure over the stubbornness of continuing to pour capital into a project with diminishing prospects. It was a painful but necessary chapter in the company's evolution.

VII. The Transformation: Becoming a Multi-Product Company (2020-2023)

The revenue trajectory from 2020 through 2023 told a story of accelerating growth: ninety-two million, one hundred four million, one hundred twenty-six million, one hundred twenty-eight million. Energy Recovery was no longer the forty-to-fifty-million-dollar company that had frustrated investors during the stagnation years. The water segment was the engine, and the company was investing in a broader portfolio of products designed to apply pressure exchange technology across multiple industries.

Under Mao's leadership, the product portfolio expanded along several vectors simultaneously. The Ultra PX was developed specifically for ultra-high-pressure reverse osmosis applications in industrial wastewater treatment. The global wastewater treatment market was valued at nearly forty-nine billion dollars in 2024 and projected to double by 2034. The Ultra PX could recover up to sixty percent of wasted energy in these applications, and the business quickly established itself with ten to twelve million dollars in annual revenue at gross margins in the mid-to-high sixties.

The company also pursued gas processing applications, a technically adjacent market where high-pressure gas streams carry significant recoverable energy. IsoBoost and IsoGen technologies, designed to recover energy from gas processing operations, were deployed at Saudi Aramco installations and attracted interest from other Middle Eastern national oil companies. A licensing deal with Alderley, a UK-based process technology firm, provided additional distribution capabilities and industry credibility in the gas processing sector.

In 2022, the PX G1300 was launched for CO2 refrigeration in supermarket applications, with a pilot installation in southern Europe. This was the culmination of years of research into adapting pressure exchange for the transcritical CO2 cycle, a market that, as subsequent events would demonstrate, proved commercially unviable for the company.

The thesis underlying all of these initiatives was that pressure exchange was not just a desalination technology but a horizontal platform with applications wherever energy was being wasted in pressurized fluid systems. It was an intellectually compelling argument: the fundamental physics of transferring pressure between fluid streams applies across many industrial processes. But as the company would learn, the distance between physical applicability and commercial viability can be vast.

Financially, the transformation was evident in the margin profile. Gross margins consistently exceeded sixty-five percent, a figure that bears repeating because it is so anomalous for a hardware company. To put that in context, the S&P 500 Industrials sector averages gross margins in the low thirties. Even high-quality industrial companies like Danaher or Roper Technologies typically achieve gross margins in the mid-fifties. Energy Recovery's margin profile looked more like a medical device company or a specialty software firm, reflecting the combination of dominant market position, mission-critical application, and limited competition that defined its business.

The revenue mix was shifting in a healthy direction. Aftermarket parts and service revenue, which carried high margins and provided recurring income, was becoming a more meaningful share of total sales. For investors, this was perhaps the most important development: as the installed base grew, the predictable portion of revenue grew with it, gradually reducing the company's dependence on lumpy mega-project timing.

The stock market began to take notice. ERII shares climbed steadily from the single digits, where they had languished during the stagnation years, to reach an all-time high of thirty dollars and seventy-six cents in July 2023. The re-rating was dramatic: from a market cap of roughly one hundred fifty million in 2020 to well over one and a half billion at the peak, a tenfold increase in three years. Wall Street coverage expanded from a handful of boutique analysts to include major firms. The "boring alpha" thesis, the idea that unsexy industrial companies in growing end markets could generate outsized returns, gained currency among institutional investors who had never heard of a pressure exchanger.

But the re-rating also raised the stakes. At a thirty-dollar stock price, the market was pricing in continued execution across multiple fronts. The company's enterprise value to revenue multiple had expanded from roughly two times to over ten times. Any stumble would be punished severely. Energy Recovery had gone from being an undiscovered gem to a company that needed to justify elevated expectations.

VIII. The Modern Era: Industrial Efficiency & Decarbonization Tailwinds (2023-Present)

In July 2023, the board appointed David Moon as a director, and by October he was named interim president and CEO, with the appointment made permanent in January 2024. The rapid progression from board member to CEO suggested the board had identified Moon as the right leader well before the formal transition.

Moon brought a different profile than his predecessors. Where Pique had been a water industry veteran, Gay a young finance-trained executive, and Mao a technology hardware leader, Moon came from the commercial refrigeration and HVAC world. His twenty-five years of leadership included stints as president and chief operating officer of Heatcraft Worldwide Refrigeration, a division of Lennox International, where he oversaw operations from 2006 to 2017, and as president of Carrier Commercial Refrigeration at Carrier Global. He understood manufacturing operations, supply chain optimization, and the challenge of scaling industrial products across multiple markets and geographies. Perhaps most importantly, he had experience managing businesses through product transitions and cost restructurings, exactly the challenges facing Energy Recovery.

Moon inherited a company at a crossroads. The water business was strong, with revenue of one hundred forty-five million dollars in 2024, the best year in company history. The water segment alone contributed over ninety-nine percent of that total, while the emerging technologies segment generated a negligible three hundred thousand dollars. The portfolio of growth bets, CO2 refrigeration, gas processing, residual oil and gas ambitions, was collectively producing almost nothing.

But the macro backdrop for the core business had never been more favorable. The global desalination equipment market was valued at roughly eighteen billion dollars in 2024 and projected to reach over thirty billion by 2030, growing at nearly ten percent annually. Reverse osmosis technology held a sixty-nine percent share of that market, which meant virtually every major new plant represented an opportunity for Energy Recovery's PX devices.

The regional dynamics were compelling. The Middle East and North Africa, which accounted for roughly half of global desalination capacity and well over sixty percent of Energy Recovery's revenue, was investing aggressively. Saudi Arabia's Vision 2030 initiative included massive water infrastructure commitments, with mega-projects like Neom, Jubail 3B, and Rabigh 4 representing billions of dollars in construction spending. The UAE continued to expand its desalination capacity. India was emerging as a significant new market, with Chennai, Mumbai, and Gujarat all pursuing large-scale reverse osmosis projects. In the American Southwest, cities were confronting the reality that the Colorado River could no longer reliably support population growth without desalination and water reuse.

The fundamental numbers on water scarcity were stark. Available freshwater per capita had declined to just forty-eight hundred cubic meters globally, and the trajectory was worsening every year as population grew and climate patterns shifted.

Half of the Middle East's twenty-nine countries fell below five hundred cubic meters per person per year, the threshold for absolute water scarcity. India, home to nearly a fifth of the world's population, was approaching severe water stress in several major regions. These were not cyclical trends. They were structural and irreversible. No amount of conservation, efficiency improvement, or rainfall could close the gap between supply and demand. Desalination was not optional. It was existential.

But near-term execution proved challenging. In the fourth quarter of 2025, Energy Recovery reported revenue of sixty-seven million dollars, essentially flat year over year, and full-year 2025 revenue came in at one hundred thirty-five million, a seven percent decline from 2024's record. The culprit was familiar: project timing. Several large desalination mega-projects experienced delays, pushing expected revenue recognition into future periods. Management confirmed that three specific projects would slip into 2027, creating what CEO Moon characterized as an "air pocket" in the near-term outlook.

More consequentially, Moon announced the decision to wind down the CO2 retail grocery business entirely. After years of investment dating back to the mid-2010s, the company concluded that the CO2 refrigeration opportunity would require substantial additional capital to commercialize and did not justify the continued burn. The PX G1300 device for transcritical CO2 systems had been deployed in a handful of European supermarkets, but the adoption rate was glacial. The grocery retail channel simply moved too slowly, required too many individual sales touchpoints, and generated too little revenue per installation to justify the ongoing R&D and commercialization expense.

The wind-down would eliminate approximately twenty positions, roughly ten percent of the workforce, and generate seven million dollars in annualized operating expense savings. Moon framed it as a strategic refocusing: resources would be redirected toward the water business, including both core desalination and the growing wastewater opportunity. It was a painful admission that not every application of pressure exchange technology would succeed commercially, but it also demonstrated a CEO willing to make difficult capital allocation decisions rather than allowing underperforming businesses to linger indefinitely. Given the VorTeq experience, where management arguably held on too long, the faster decision on CO2 was welcomed by many investors as a sign of improved capital discipline.

The February 2026 earnings announcement sent the stock reeling. ERII shares dropped more than thirty percent in a single session, falling from over sixteen dollars to roughly eleven dollars, setting a new fifty-two week low. For context, the stock had peaked above thirty dollars just two and a half years earlier. From that all-time high, the decline exceeded sixty-five percent, erasing roughly a billion dollars of shareholder value.

The 2026 guidance was sobering: revenue of one hundred fifteen to one hundred forty million dollars and earnings per share of fifty to seventy cents, well below consensus expectations. The wide guidance range, spanning twenty-two percent from bottom to top, underscored the inherent unpredictability of project-driven revenue. The market's reaction reflected not just the near-term disappointment but a broader recalibration: investors were repricing the stock from a growth narrative back toward a value narrative, acknowledging that the multi-product platform thesis had not yet been validated and that the core business, while excellent, was subject to the same lumpy project dynamics it had always faced.

Yet beneath the negative headlines, several developments warranted attention. The new PX Q650, a larger and more efficient pressure exchanger, was expected to begin manufacturing in the second half of 2026 and promised higher average selling prices per unit while reducing the number of units required per plant. The wastewater business had generated ten to twelve million dollars in revenue with gross margins in the mid-to-high sixties, establishing a genuine second product line. And the company's cash position remained robust at eighty-three million dollars with minimal debt, providing ample runway to weather the project delay cycle.

There are also legal and regulatory items that investors should monitor. The intellectual property lawsuit against Flowserve, filed in 2025, remains in its early stages. If Energy Recovery prevails, it could further entrench its patent position and potentially generate licensing revenue. If it loses, it could embolden competitors. Separately, the class action lawsuits filed by investors during the VorTeq era, alleging that management misled shareholders about the technology's readiness, were a material legal overhang. The resolution of those cases, while the specific financial terms were not widely disclosed, removed a cloud that had hung over the stock for years.

From an accounting perspective, the mega-project revenue recognition model deserves scrutiny. Because large desalination orders are recognized when equipment ships and passes acceptance testing, the timing of revenue is inherently lumpy. This is not aggressive accounting; it is standard practice for industrial equipment companies. But it means that investors should focus on trailing twelve-month or multi-year revenue trends rather than any single quarter's results.

Moon's message to investors was direct: "This isn't that people don't need water." The underlying demand for desalination was not weakening. The air pocket was a timing issue, not a demand issue. Whether the market would be patient enough to wait for that thesis to play out remained the central question.

IX. Business Model Deep Dive & Unit Economics

To understand why Energy Recovery commands software-like margins from a hardware business, you need to understand the economics at the plant level. A typical large seawater reverse osmosis plant might cost five hundred million to a billion dollars to build. The PX Pressure Exchanger devices in that plant represent a small fraction of the total capital cost, perhaps one to three percent. But those devices determine the plant's energy consumption, which is the single largest operating expense over the facility's thirty-year lifespan. Energy Recovery estimates that its installed base saves customers approximately two and a half billion dollars annually in energy costs.

This dynamic creates extraordinary pricing power. When your product costs a few hundred thousand dollars but saves millions per year, the buyer's willingness to pay is very high relative to your manufacturing cost. Think of it as selling a device that costs one dollar but saves the customer a hundred dollars every year for thirty years. How much would you charge for that device? A lot more than one dollar. That is essentially Energy Recovery's business in a nutshell.

Gross margins have consistently exceeded sixty-five percent, reaching sixty-seven percent in the fourth quarter of 2025. For context, the median gross margin for industrial equipment companies is typically in the thirty to forty percent range. Only companies with exceptional differentiation and limited competition achieve margins this high. The comparison set is not other pump or valve manufacturers, but rather medical device companies like Intuitive Surgical or specialty software firms like Veeva Systems.

The business model has a razor-and-razorblade element that is worth unpacking. The initial equipment sale brings the customer into the Energy Recovery ecosystem, but the real long-term value lies in the aftermarket. A PX device has a rotor that spins twenty times per second, twelve hundred revolutions per minute, through corrosive seawater at extreme pressures. Even with the durability of advanced ceramics, these components wear over time. Rotors need replacement, end covers need servicing, and the overall system requires periodic commissioning and optimization.

In 2025, aftermarket revenue reached twenty million dollars, growing twelve percent year over year, and representing roughly fifteen percent of total sales. As the global installed base of PX devices continues to expand, with more than thirty thousand devices now deployed, this recurring revenue stream becomes an increasingly important and predictable component of total sales. The aftermarket business carries even higher margins than new equipment sales, because the parts are proprietary, the service requires trained technicians, and the customer has no practical alternative once the PX is installed.

Revenue is recognized through three primary channels. Mega-project sales represent the largest and most volatile category, contributing roughly eighty-three million dollars in 2025, or about sixty-one percent of total water revenue. These are the massive desalination plants commissioned by governments and sovereign utilities in Saudi Arabia, the UAE, Israel, and increasingly India. A single mega-project can represent ten million dollars or more in PX equipment, and the timing of a handful of these orders can swing annual revenue by twenty to thirty percent. Original equipment manufacturer sales, at roughly thirty-two million in 2025, flow through major desalination system builders who integrate PX devices into their packaged systems. This channel is somewhat more stable but still project-driven. The aftermarket channel, at twenty million and growing twelve percent year over year, provides replacement parts, repair services, field commissioning, and technical support to the installed base. In the fourth quarter of 2025, aftermarket revenue surged fifty-four percent, suggesting the installed base is reaching sufficient scale to generate meaningful recurring income.

The revenue concentration creates a strategic vulnerability that management is actively working to address. Building reference installations in India, South America, the United States, and Europe is designed to diversify the geographic mix beyond the Middle East over time. But for now, the MENA region remains the center of gravity.

The balance sheet reflects a company that generates far more cash than it needs to sustain operations. At the end of 2025, Energy Recovery held eighty-three million dollars in cash and investments against just nine million in total debt. The net cash position of sixty-six million represented roughly twelve percent of the company's market capitalization. The company has no dividend but maintains an active share repurchase program. The completed fifty million dollar buyback and newly authorized thirty million dollar program represent meaningful capital returns for a company this size. At the current stock price, the buyback yield exceeds six percent, suggesting management views the shares as attractively valued and prefers share repurchases to dividends as the return mechanism, a sensible approach for a company with volatile earnings that wants to maintain balance sheet flexibility.

Operating leverage is the key to understanding Energy Recovery's profit potential, and the fourth quarter of 2025 provided a vivid illustration. The company's fixed cost base, including research and development, sales and marketing, and general and administrative expenses, does not scale linearly with revenue. Those costs run at roughly sixty to sixty-five million dollars per year regardless of whether revenue is a hundred million or a hundred forty million.

When mega-project revenue arrives in concentrated bursts, the incremental revenue drops almost entirely to the bottom line. In the fourth quarter of 2025, when revenue hit sixty-seven million, the GAAP operating margin expanded to a stunning forty-seven percent. That is a level of profitability that most industrial companies never see. Conversely, when revenue dips during project delay periods, those same fixed costs compress margins dramatically: full-year 2025 operating margin was just eighteen percent on the GAAP basis.

This operating leverage works in both directions, and investors need to understand the mechanics to avoid overreacting to any single quarter's results. The 2026 guidance, with its wide revenue range of one hundred fifteen to one hundred forty million and the overhead reduction from the CO2 exit, suggests management is actively positioning the cost structure to deliver acceptable margins even in the lower revenue scenario.

Capital expenditure has historically been modest, typically well under five million dollars annually, reflecting the asset-light nature of the business. The company's San Leandro manufacturing facility has served as the sole production center for its entire history, a remarkable concentration of manufacturing in a single location.

However, the 2026 guidance calls for three to six million in capex to support an international manufacturing facility buildout beginning in early 2027. This signals a new phase of investment in production capacity and geographic diversification. The international facility, with site selection expected by mid-2026, would reduce shipping costs to Middle Eastern and Asian customers, provide a hedge against supply chain disruptions, and potentially improve cost structure. It is the most significant capital investment decision the company has made in years, and its execution will be closely watched by investors as a test of management's ability to scale operations beyond the San Leandro hub.

X. Playbook: Business & Strategic Lessons

Energy Recovery's three-decade journey offers a compressed case study in the challenges of deep technology commercialization. The first lesson is about time horizons. Leif Hauge founded the company in 1992. The first meaningful commercial revenues did not arrive until the early 2000s. The technology did not become the industry standard until roughly 2010. From founding to market dominance took nearly two decades.

This timeline is not unusual for deep technology companies. SpaceX took twelve years from founding to its first profitable year. Tesla took seventeen years from founding to its first full year of profitability. In the industrial space, companies developing breakthrough materials, manufacturing processes, or precision devices routinely require a decade or more to move from laboratory to commercial viability. The difference is that deep tech companies rarely attract the patient capital required to survive this journey. Most venture capital fund structures have a ten-year life. Most public market investors measure performance in quarters. Energy Recovery survived because it had a small group of believers, Hans Peter Michelet chief among them, who understood the timeline and were willing to wait.

The second lesson concerns selling to industries that change slowly. Water utilities, EPC firms, and government infrastructure agencies are among the most conservative buyers in the world. They do not adopt new technologies based on a pitch deck or a pilot program. They require years of field data, reference installations at scale, and the endorsement of their peer networks before they will commit.

This conservatism creates a paradox: the very characteristics that make these markets frustrating to enter are what make them so attractive once you have established yourself. Energy Recovery's sales cycles of three to five years are not a bug; they are a feature of the market. They serve as a moat against new entrants just as effectively as patents do. Any company entering this space must be capitalized to survive long enough for those cycles to complete, and most startups or corporate diversification initiatives simply cannot sustain the cash burn required to wait three to five years for their first meaningful orders. The same dynamic that made Energy Recovery's early years so painful now protects its market position.

The third lesson is about the second act. Energy Recovery's desalination monopoly was both its greatest strength and its most constraining limitation. When your market share approaches saturation, you face a choice: accept low single-digit growth that mirrors your end market, or attempt to apply your technology to new applications.

The VorTeq experience with oil and gas illustrates how treacherous this path can be. The technology that works brilliantly in seawater may require fundamental redesign to function in abrasive hydraulic fracturing fluids. The sales motion that succeeds with government utilities may fail entirely with oilfield services companies. Different industries mean different everything: customer psychology, procurement processes, competitive dynamics, and risk tolerance.

The lesson is not that diversification is wrong, but that adjacent markets must be chosen with extreme care. The most successful adjacencies for Energy Recovery have been those closest to the core: wastewater treatment uses the same membrane technology, the same type of customers, and the same ROI-driven selling process as desalination. The further the company ventured from its core competence, the more money it lost. CO2 refrigeration and oil and gas fracking were technically related but commercially alien, and both failed.

The fourth lesson is about platform thinking. The most valuable industrial technology companies are those that develop a core capability and then successfully apply it across multiple markets. Danaher built a manufacturing empire on the Danaher Business System. Illinois Tool Works created value through a decentralized model of applying engineering expertise to hundreds of niche applications. Even within the water technology space, Xylem has demonstrated how a portfolio of water-related technologies can create a diversified growth platform. Energy Recovery's aspiration to become a "pressure exchange platform" serving desalination, wastewater, chemical processing, and potentially lithium extraction follows this playbook. The wastewater business, with its mid-to-high-sixties gross margins and growing revenue, suggests the platform thesis may have legs. The CO2 failure and VorTeq abandonment suggest it does not work every time. The key insight is that platform adjacencies must share the same economic DNA as the core business: mission-critical applications where the product's cost is small relative to the savings it delivers.

The fifth lesson is perhaps the most important: customer economics trump everything. Energy Recovery's success in desalination was not built on brand, relationships, or sales execution, though all played a role. It was built on the incontrovertible math that a PX device pays for itself in energy savings within months of installation. When you can present a customer with an ROI that is essentially infinite, selling becomes a matter of education and patience rather than persuasion. The challenge for Energy Recovery's new product lines is replicating that kind of economic no-brainer in different contexts.

There is a sixth lesson embedded in the story, one that is easy to overlook: the value of a boring moat. Energy Recovery does not benefit from network effects, platform dynamics, or viral adoption, the competitive advantages that dominate Silicon Valley discourse. Its moat is constructed from ceramics, patents, and the institutional knowledge of how to manufacture and sell complex industrial equipment to conservative buyers over multi-year sales cycles. It is a moat that takes decades to build and is nearly impossible to replicate through capital alone. For investors accustomed to evaluating software-style competitive advantages, Energy Recovery is a reminder that the most durable businesses are often the ones that nobody talks about at dinner parties.

XI. Hamilton's 7 Powers & Porter's 5 Forces Analysis

Hamilton's 7 Powers

The framework developed by Hamilton Helmer identifies seven sources of persistent competitive advantage. Applied to Energy Recovery, the picture reveals a company with two dominant powers and several supporting ones.

Switching Costs represent Energy Recovery's most potent power. Once a desalination plant is designed around PX Pressure Exchanger devices, switching to a different energy recovery technology requires redesigning the plant's hydraulic system, requalifying the equipment, and accepting performance risk. Given that desalination plants operate for thirty years or more, the installed base creates a deeply entrenched position. Even for new plants, the engineering specifications that call for PX devices create institutional switching costs: EPC firms have standardized their designs around the technology, and changing would require revalidation.

Cornered Resource is the second major power. Energy Recovery's patent portfolio of approximately sixty-five patent families, combined with proprietary manufacturing know-how in advanced ceramics, creates a resource advantage that competitors cannot easily replicate. The company has demonstrated willingness to enforce its IP, having previously obtained a federal injunction against its own founder Leif Hauge when he attempted to manufacture competing devices through Isobaric Strategies. The ceramic manufacturing process represents decades of accumulated learning that cannot be transferred through patent filings alone. Trade secrets around tolerances, material formulations, and quality control processes compound this advantage.

Process Power operates at a moderate level. The company's expertise in managing multi-year sales cycles with conservative industrial buyers, its deep application engineering capabilities, and its institutional relationships with major EPC firms represent accumulated organizational knowledge that new entrants would need years to develop.

Scale Economics are present but limited. Energy Recovery benefits from manufacturing scale efficiencies and from spreading R&D costs over a larger revenue base, but the company is small enough that these advantages are not overwhelming. At one hundred thirty-five million in revenue, it remains a small industrial company by most measures, and a well-capitalized new entrant could potentially achieve competitive manufacturing scale within a few years.

The installed base does create a network effect of sorts, though it is more accurately described as a data advantage. More installations generate more performance data across different water chemistries, temperatures, and operating conditions. This data enables continuous product improvement and allows Energy Recovery's application engineers to provide precise performance guarantees for new installations. A competitor without this operating history database would struggle to offer the same level of confidence to risk-averse utility buyers.

Counter-Positioning applied historically when Energy Recovery disrupted the established Pelton wheel and turbocharger technologies. Incumbents like Flowserve were reluctant to cannibalize their existing energy recovery device businesses by adopting isobaric technology, giving Energy Recovery time to establish dominance. This power has largely been exercised and is no longer the primary driver of advantage.

Branding is moderate in desalination, where Energy Recovery is the known quantity, but still developing in newer markets like wastewater treatment. Network Effects are limited in the traditional sense but manifest through the installed base dynamics described above.

Porter's 5 Forces

Competitive Rivalry (Low): Energy Recovery operates as a near-monopoly in desalination energy recovery, with more than thirty thousand PX devices installed in over one hundred countries. Competitors exist on the periphery, primarily Flowserve, Danfoss, FEDCO, and Sulzer, offering centrifugal devices and alternative energy recovery technologies for smaller installations, but no company has successfully challenged the PX's dominance in large-scale reverse osmosis plants. Notably, Energy Recovery filed an intellectual property lawsuit against Flowserve in 2025, currently in its early phases, signaling a willingness to aggressively defend its patent position. In wastewater, the competitive landscape is more fragmented, but Energy Recovery's technology advantage appears meaningful.

Threat of New Entrants (Low to Medium): The barriers to entry are substantial and multi-layered. First, the patent portfolio of approximately sixty-five families creates legal barriers that require either licensing or designing around. Second, the ceramic manufacturing expertise took decades to develop and cannot be replicated through capital expenditure alone. Third, the installed base of more than thirty thousand devices generates performance data that enables continuous product improvement, a data advantage that new entrants cannot shortcut. Fourth, the qualification cycles with conservative desalination EPC firms and utilities can take three to five years, meaning a new entrant must sustain years of investment before generating meaningful revenue.

However, well-funded industrial conglomerates with adjacent capabilities could potentially enter if the market opportunity became large enough to justify the patient investment. Chinese competitors represent a particularly notable long-term threat, given the Chinese government's track record of supporting domestic industrial technology development and the country's rapidly growing desalination market.

Supplier Power (Low): Energy Recovery's inputs are standard industrial materials and components, including alumina ceramics, stainless steel housings, and standard machined parts. The company's competitive advantage resides entirely in its design, engineering, and manufacturing processes, specifically the proprietary methods for shaping and finishing ceramic rotors to ultra-precise tolerances. No single supplier has meaningful leverage over the company, and materials could be sourced from multiple vendors in different geographies if needed.

Buyer Power (Medium): Large desalination project buyers, including government utilities, EPC firms like Veolia and IDE Technologies, and sovereign wealth fund-backed developers like ACWA Power, have significant negotiating leverage due to their scale and the size of individual orders. A single mega-project buyer might represent five to ten percent of Energy Recovery's annual revenue, creating meaningful concentration risk.

Long sales cycles give buyers time to evaluate alternatives, and government procurement processes in the Middle East often include competitive bidding requirements. However, the switching costs and ROI advantages of the PX significantly mitigate buyer power. Once a buyer has experienced the economics of PX technology, the incentive to switch is minimal. The buyer power dynamic is best understood as moderate at the initial sale but declining sharply over the life of the relationship.

Threat of Substitutes (Low to Medium): In desalination, no alternative energy recovery technology approaches the PX's efficiency. The centrifugal devices made by Flowserve, Danfoss, and others operate at meaningfully lower efficiencies, making them uncompetitive for large-scale plants. Theoretical substitutes like forward osmosis or capacitive deionization remain far from commercial viability at scale.

The deeper substitution risk is not a better energy recovery device but an entirely different desalination technology that does not require energy recovery at all. Forward osmosis, membrane distillation, and electrochemical desalination are all areas of active research. However, none of these technologies is close to matching reverse osmosis in cost, efficiency, or scalability. The International Desalination Association projects that reverse osmosis will remain the dominant technology for at least the next two decades. For investors, this means the substitution risk is real in theory but remote in practice.

Key KPIs to Watch

For investors monitoring Energy Recovery's ongoing performance, two metrics matter above all others:

Water Segment Aftermarket Revenue Growth: This is the single most important metric for assessing the long-term health of Energy Recovery's business. Aftermarket revenue is higher-margin, more predictable, and less dependent on mega-project timing. It represents the compounding value of the installed base: each new PX device sold today generates a stream of aftermarket revenue over the next thirty years. Consistent growth here indicates that the installed base is expanding and that existing customers remain engaged. The twelve percent growth in 2025 was a positive signal even as overall revenue declined. If aftermarket revenue continues to grow at double-digit rates while the installed base expands, the business is fundamentally healthy regardless of quarterly mega-project timing.

Mega-Project Backlog and Revenue Conversion Rate: Given the lumpy nature of project-driven revenue, tracking the backlog of committed orders and the rate at which they convert to recognized revenue provides the best leading indicator of near-term financial performance. The current air pocket, with three projects slipping into 2027, illustrates why this metric matters: the demand exists, but the timing of revenue recognition determines whether any given year meets or misses expectations. Investors should track the number and size of mega-projects in the global pipeline, the rate at which Energy Recovery wins these orders, and the historical conversion rate from order to revenue recognition. A healthy pipeline with delayed conversion is very different from a shrinking pipeline, and the distinction matters enormously for forward estimates.

XII. Bull vs. Bear Case & Investment Considerations

The Bull Case

The foundational bull argument rests on water scarcity as a secular, irreversible megatrend. Unlike energy transition, artificial intelligence, or other popular investment themes, water scarcity is not subject to technological disruption or political reversal. Humans need freshwater. The planet has a fixed supply. Population and industrial demand continue to grow. The math is implacable.