Equity Residential: The REIT That Reinvented American Apartment Living

I. Introduction & Episode Setup

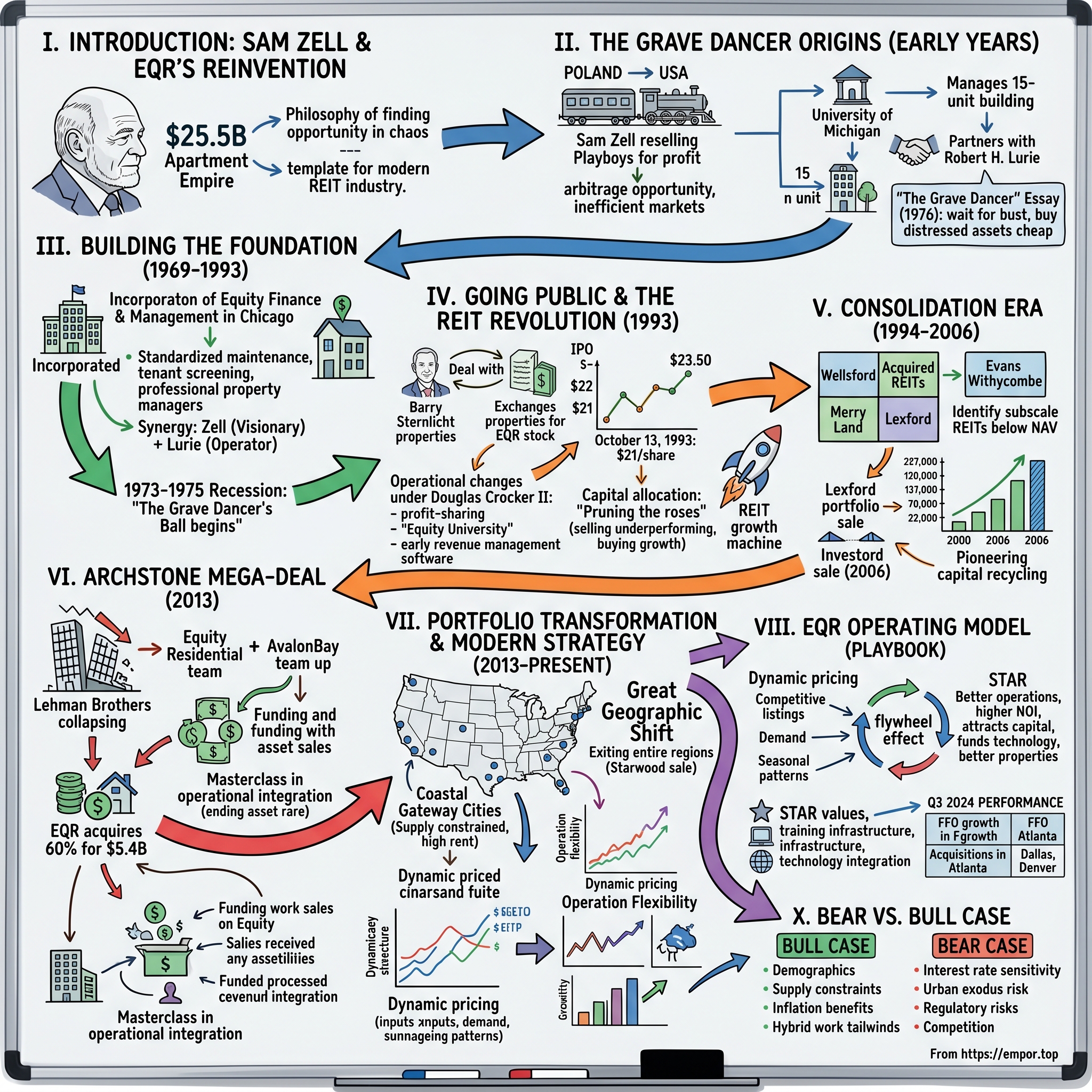

Picture this: It's 1973, and the American real estate market is in freefall. Office buildings sit empty, apartment complexes slide into bankruptcy, and developers who were kings just months earlier are now begging banks for mercy. In a modest Chicago office, a 32-year-old lawyer-turned-investor named Sam Zell is making phone calls, but not the kind you'd expect. While others are selling in panic, he's buying—not just buying, but dancing. Dancing on the graves of failed real estate empires, as he would later famously put it.

That contrarian dance would eventually create Equity Residential, today a $25.5 billion apartment empire that fundamentally transformed how Americans think about renting. This isn't just a story about real estate—it's about how one man's philosophy of finding opportunity in chaos created the template for the modern REIT industry, now worth over $4 trillion globally.

What makes Equity Residential fascinating isn't just its scale—though owning 86,000+ apartments across America's most expensive cities is impressive. It's how Sam Zell and his successors built a machine that treats apartment buildings not as static assets but as dynamic businesses, constantly evolving with demographic shifts, technology disruptions, and economic cycles. They pioneered the idea that owning apartments could be as sophisticated as running a Fortune 500 company.

We'll explore how a Polish immigrant's son who sold Playboy magazines to Hebrew school classmates built America's first truly institutional apartment landlord. We'll dive into the game-changing 1993 IPO that created the modern REIT playbook, the audacious $9 billion Archstone acquisition that nearly doubled the company overnight, and the radical portfolio transformation that saw EQR exit entire regions to double down on coastal gateway cities.

Along the way, we'll unpack the operational excellence that maintains 96% occupancy across tens of thousands of units, the financial engineering that allows REITs to compound value while paying out most of their income, and the strategic decisions that separate winners from also-rans in the brutal world of real estate cycles. This is the Equity Residential story—grab your hard hat, we're going in.

II. The Grave Dancer Origins: Sam Zell's Early Years

The story begins not in boardrooms but in the cramped cabin of a train heading from Poland to the United States in 1941. Bernard and Rochelle Zielonka—later Americanized to Zell—were among the last Jews to escape Poland before the Holocaust consumed their homeland. Rochelle was four months pregnant. That child, born September 28, 1941, in Chicago, would become Samuel Zell, though no one could have imagined the empire he would build from such desperate beginnings.

Young Sam inherited more than just his parents' survival instinct—he absorbed their entrepreneurial DNA. At age 12, while his classmates collected baseball cards, Sam spotted an arbitrage opportunity that would preview his entire career. He'd take the train downtown to buy Playboy magazines for 50 cents, then resell them to his Hebrew school classmates for $1.50. The 200% markup wasn't just about profit—it was about understanding inefficient markets and human desire, lessons that would serve him well in real estate.

But the real transformation came during his undergraduate years at the University of Michigan. Picture a 20-year-old Sam in 1961, standing in front of a dilapidated 15-unit apartment building in Ann Arbor. The owner, exhausted by tenant complaints and maintenance headaches, made him an offer: manage the property in exchange for free room and board. Sam didn't just accept—he revolutionized the building's operations, implementing systematic maintenance schedules and tenant screening processes that were unheard of in student housing. By the time he graduated, he'd parlayed that experience into managing multiple properties, netting $150,000—roughly $1.5 million in today's dollars.

The crucial partnership that would define the next three decades began in that same fraternity house. Robert H. Lurie, a fraternity brother with complementary skills—where Sam was bold and visionary, Bob was methodical and operational—became his business partner. Together, they formed a syndicate that acquired and managed apartment buildings around Ann Arbor. By the time they graduated from law school in 1966, they controlled over 4,000 apartment units, generating cash flows that dwarfed what their lawyer classmates would earn for years.

Sam's brief flirtation with traditional employment lasted exactly one week. In 1966, he joined a Chicago law firm, sat in his office, reviewed contracts, and realized something profound: he was already wealthier than the senior partners, and he was building something far more interesting than legal briefs. He walked out after five days, telling Lurie, "I'm not meant to work for other people."

What emerged from these experiences was a philosophy Sam would later codify in his famous 1976 essay, "The Grave Dancer." The premise was counterintuitive yet brilliant: while everyone else focused on development and new construction during boom times, Sam would wait for the inevitable bust, then acquire distressed properties for pennies on the dollar. He noticed something others missed—real estate development volume correlated more strongly with availability of financing than with actual demand. When credit was loose, developers would overbuild. When credit tightened, they'd go bankrupt. And that's when Sam would dance.

This wasn't vulture capitalism—it was pattern recognition at its finest. Sam understood that real estate moves in cycles as predictable as seasons, but most players have memories shorter than the cycles themselves. While others saw failure and wrote off properties as worthless, Sam saw temporarily impaired assets that would recover with better management and patience. He was buying optionality at distressed prices, a strategy that would make him and his investors billions over the coming decades.

The foundation was set. A Polish immigrant's son who understood scarcity, a natural trader who recognized inefficiency, and a contrarian who thrived on chaos—Sam Zell was ready to build something unprecedented in American real estate. But first, he would need to survive the brutal recession that was about to hit.

III. Building the Foundation: 1969-1993

The year 1969 marked a quiet revolution. While America watched Neil Armstrong walk on the moon, Sam Zell and Bob Lurie incorporated Equity Finance and Management Company in a small Chicago office. No press releases, no fanfare—just two guys in their late twenties with a radical idea: they would build a real estate empire by acquiring and professionally managing apartments when everyone else was obsessed with development.

The timing seemed terrible. The go-go sixties had created a real estate bubble of epic proportions. REITs—a new structure created by Congress in 1960—had gone wild, leveraging themselves to the hilt to build office towers and shopping centers. Money was everywhere, and everyone was a genius. Sam watched from the sidelines, accumulating cash and waiting. He didn't have to wait long.

The 1973-1975 recession hit real estate like a sledgehammer. Oil prices quadrupled, inflation soared, and suddenly all those highly leveraged REITs couldn't service their debt. Properties that had been valued at millions were being foreclosed and sat empty. Banks, desperate to get non-performing loans off their books, would practically give properties away to anyone who could close quickly with cash. This was Sam's moment—the grave dancer's ball had begun.

One deal from this era captures the Zell magic perfectly. A 200-unit apartment complex in Toledo, built for $8 million just three years earlier, had gone into foreclosure. The bank had already written it off as a total loss. Sam offered $1 million cash, as-is, close in 30 days. The bank, shocked anyone would take the "worthless" property, accepted immediately. Sam spent $200,000 on deferred maintenance, adjusted rents to market, and within 18 months the property was cash-flowing $400,000 annually. He'd eventually sell it for $4.5 million. Multiply this by dozens of similar deals, and you understand how Equity was built.

But it wasn't just about buying cheap. Sam and Bob pioneered professional property management at scale. They hired college graduates—unheard of for property managers in the 1970s—and paid them well with profit-sharing arrangements. They standardized everything: maintenance schedules, tenant screening, rent collection, even the paint colors used in units. They treated apartment management like manufacturing, bringing quality control and systematic processes to an industry that had operated on gut feel and relationships.

The partnership with Lurie was the secret weapon. While Sam was the visionary and dealmaker, constantly flying around the country looking for opportunities, Bob was the operator, ensuring their growing portfolio ran like clockwork. They had a rule: any acquisition had to be approved by both. This check-and-balance system prevented the empire-building ego trips that destroyed so many real estate partnerships.

By the mid-1980s, Equity had quietly become one of the largest apartment owners in America, with over 30,000 units. But Sam saw something bigger coming. The Tax Reform Act of 1986 had destroyed many of the tax shelters that made real estate attractive to individual investors. Suddenly, properties were being valued on cash flow rather than tax benefits. Prices crashed again. And once again, Sam was ready to dance.

In 1987, he convinced Merrill Lynch to back what he called "vulture funds"—opportunity funds that would acquire distressed real estate. The timing was perfect. The savings and loan crisis was about to create the largest real estate fire sale in American history. Between 1987 and 1993, Sam's funds would acquire over $1 billion in properties, often at 20-30 cents on the dollar.

Then tragedy struck. In 1990, Bob Lurie, Sam's partner of 25 years, died of cancer at age 48. Sam lost not just a business partner but his closest friend and the operational genius who kept their empire running. At the memorial service, Sam broke down crying—one of the few times colleagues had seen him vulnerable. The loss came at the worst possible time. The early 1990s recession was brutal, commercial real estate values were collapsing, and banks were calling loans.

What happened next became Wall Street legend. With properties hemorrhaging cash and banks circling, Sam personally guaranteed $600 million in loans to keep Equity afloat. He worked 80-hour weeks, flying from city to city, negotiating with banks, restructuring loans, selling properties, doing whatever it took to survive. At one point, he was so leveraged that a colleague asked what would happen if things went south. Sam's response: "I'll be teaching real estate at the University of Chicago for the rest of my life."

But Sam didn't just survive—he thrived. By being one of the few players with credibility and cash during the darkest days of the recession, he could extract extraordinary terms from desperate sellers. He was acquiring trophy properties in major markets for prices that would never be seen again. And crucially, he was thinking about the next evolution: how to access permanent capital at scale.

The answer was revolutionary for its simplicity: take Equity public as a REIT. The tax-advantaged structure, combined with public market liquidity, would create a permanent capital vehicle that could grow through any cycle. Sam spent 1992 preparing, hiring investment bankers, cleaning up the portfolio, and creating institutional-grade reporting. The grave dancer was about to dance on the biggest stage of all—Wall Street.

IV. Going Public & The REIT Revolution (1993)

March 1993. Sam Zell sat across from Barry Sternlicht, the 32-year-old wunderkind who'd built Starwood Capital into a powerhouse by acquiring distressed properties from the Resolution Trust Corporation. Sternlicht had a problem: he owned 15,000 apartments but needed liquidity for his investors. Sam had a vision: he wanted to create the first truly institutional apartment REIT. Over coffee that would go cold as negotiations intensified, they hammered out a deal that would transform American real estate.

The agreement was elegant in its ambition: Equity would acquire Starwood's entire apartment portfolio in exchange for a 20% stake in the newly formed Equity Residential Properties Trust. No cash would change hands—just paper for properties. Sternlicht's investors would get liquidity through publicly traded shares, while Sam would instantly vault Equity into the big leagues with 22,000 apartments. But the real genius was timing: they would close the deal just weeks before taking the combined entity public.

The IPO roadshow that summer was unlike anything Wall Street had seen. Here was Sam Zell, the infamous grave dancer, pitching not distressed assets but a growth story. His pitch was compelling: apartments were essential housing, recession-resistant, and generated predictable cash flows. Unlike office or retail properties that could sit empty for years, apartments rarely had vacancy rates above 5-10%. And demographics were on their side—baby boomers were downsizing, young professionals were delaying homeownership, and immigration was driving urban growth. But the real drama came on pricing day. Investment bankers had suggested an IPO price of $18-19 per share, conservative given the uncertain market for REITs. Sam pushed for $21, arguing that institutional investors needed to see confidence. The bankers reluctantly agreed, and on October 13, 1993, Equity Residential went public at $21 per share. By the end of the first trading day, shares had climbed to $23.50. The grave dancer had pulled off his greatest trick yet—transforming a collection of apartments into a liquid, institutional-grade investment vehicle.

What made the IPO revolutionary wasn't just the structure but the operational philosophy Sam brought to the public markets. He hired Douglas Crocker II, a former manufacturing executive with no real estate experience, to run day-to-day operations. The choice was deliberate—Sam wanted someone who thought about apartments as a business, not just as buildings. Crocker spent his first six months visiting all 30 cities where Equity owned properties, analyzing everything from demographic trends to local employment patterns to rental regulations.

The changes Crocker implemented would become the playbook for modern REITs. He instituted profit-sharing for all employees—from property managers to maintenance staff—tying compensation directly to property performance. Regional managers received stock options, aligning their interests with shareholders. He created "Equity University," a training program that taught property managers not just maintenance and leasing but finance, marketing, and customer service. The message was clear: you're not janitors and rent collectors; you're running a business.

The technology investments were equally radical for 1993. While competitors kept records on paper and collected rent by check, Equity was building centralized databases, implementing electronic payments, and using early revenue management software to optimize pricing. They could tell you the occupancy rate, average rent, and maintenance costs for any property in real-time—data that took competitors weeks to compile.

But perhaps the most important innovation was how Sam thought about capital allocation as a public company. Unlike traditional real estate developers who fell in love with their properties, Sam treated apartments as financial instruments. If a property in Phoenix could be sold at a 5% cap rate and similar quality apartments in Seattle purchased at a 7% cap rate, the decision was automatic—sell Phoenix, buy Seattle. This constant portfolio optimization, what Sam called "pruning the roses," would generate billions in value over the coming decades.

The REIT structure itself was genius in its simplicity. By distributing 90% of taxable income as dividends, REITs avoided corporate taxation, essentially passing through rental income directly to shareholders. For investors, it meant predictable, tax-advantaged income. For Equity, it meant access to permanent capital at lower costs than traditional real estate companies. The model was so successful that within five years, dozens of competitors would follow Equity's lead, transforming REITs from a backwater of the capital markets into a trillion-dollar industry.

By 2001, the company's extraordinary growth earned it inclusion in the S&P 500 Index, a validation of Sam's vision that apartment ownership could be as institutional and liquid as owning shares in IBM or GE. The grave dancer had not just survived—he had fundamentally transformed American real estate finance. But the real growth was just beginning.

V. The Growth Machine: Consolidation Era (1994-2006)

The acquisition machine kicked into high gear on a gray February morning in 1997. David Neithercut, then head of acquisitions, stood in a Phoenix conference room staring at a map covered in colored pins—each representing an apartment complex owned by Wellsford Residential Trust. Wellsford was bleeding cash, its stock trading at a 40% discount to net asset value. Sam Zell saw opportunity where others saw distress. Within 72 hours, they'd negotiated a $620 million all-stock deal. No cash, no debt assumption—just paper for properties. It was financial engineering at its finest.

That same year, before the Wellsford ink was dry, Equity struck again. Evans Withycombe Residential, another struggling REIT with properties scattered across the West Coast, agreed to a $625 million merger. In less than six months, Equity had added 15,000 apartments to its portfolio without spending a dollar in cash. The consolidation playbook was simple but ruthless: identify subscale REITs trading below NAV, offer a premium to their depressed stock price (but still below true asset value), and integrate the properties into Equity's superior operating platform.

The real test of this strategy came in 1998 with the Merry Land acquisition. This wasn't a distressed seller but a thriving private company owned by the Merry family, with 34,990 apartments concentrated in the Southeast. The negotiation took six months and nearly fell apart three times. The sticking point wasn't price—$1.17 billion in stock plus assumption of $656 million in debt—but control. The Merry family wanted board seats and operational input. Sam's response was classic: "You can have board seats or you can have our stock price, not both." They chose the stock price, and it proved wise—Equity shares would double over the next three years.

But the boldest move came in 1999 with Lexford Residential Trust. Lexford specialized in affordable housing—Section 8 properties in inner cities that most institutional investors wouldn't touch. The properties required intensive management, dealt with challenging demographics, and operated under complex government regulations. Sam saw what others missed: these properties had virtually no competition, enjoyed government-subsidized rents, and had occupancy rates near 100%. The $203 million stock deal, plus $530 million in debt assumption, added a completely different revenue stream to Equity's portfolio. It was contrarian investing at its finest.

The integration of these acquisitions showcased Equity's operational superiority. Each acquired portfolio saw immediate improvements: occupancy rates typically jumped 2-3% within six months, operating expenses dropped 10-15% through centralized purchasing and standardized procedures, and revenue increased through professional management and targeted renovations. The secret wasn't complex—it was disciplined execution at scale.

Douglas Crocker II, the CEO who'd joined in 1993, had built a machine that could digest massive acquisitions without missing a beat. By 2002, Equity owned 227,000 apartments—a ten-fold increase from the IPO. But Crocker, exhausted from a decade of hypergrowth, announced his retirement in January 2003. His parting statistic was staggering: during his tenure, Equity had generated a 380% total return to shareholders, crushing the S&P 500's 90% return over the same period.

The transition to David Neithercut as CEO in 2006 marked a philosophical shift. Neithercut, who'd been with Equity since 1994, had witnessed every deal, every integration, every market cycle. He understood that the era of easy consolidation was ending—most weak REITs had already been absorbed, and private equity firms were driving up prices. The new strategy would be about focus, not just growth.

The decision to sell the Lexford affordable housing portfolio in 2006 signaled this new direction. The 27,115 units sold for $1.09 billion—a massive profit on the 1999 acquisition price. But it wasn't just about the money. Neithercut believed Equity needed to concentrate on what it did best: high-quality apartments in supply-constrained coastal markets where demographics and job growth supported premium rents. The affordable housing experiment, while profitable, was a distraction from this core mission.

This period also saw Equity pioneer new forms of capital recycling. Instead of just buying and holding, they constantly evaluated every property through a simple question: "Would we buy this asset today at its current market value?" If the answer was no, they sold—regardless of sentiment or history. This discipline led to some controversial decisions, like exiting Las Vegas entirely in 2005, just before the market peaked. Competitors mocked the move—Vegas was booming! But when the financial crisis hit two years later, those same competitors were desperately trying to unload Vegas properties at 50 cents on the dollar.

The management culture that emerged during this era became Equity's enduring competitive advantage. They promoted from within religiously—90% of senior executives had been with the company for over a decade. They paid well but demanded excellence—property managers who hit performance targets could earn six figures, unheard of in the industry. And they invested heavily in training—Equity University had evolved from a simple orientation program into a comprehensive real estate MBA, with courses on everything from fair housing law to Excel modeling.

By 2006, Equity Residential had transformed from a scrappy opportunist into the institutional gold standard of apartment REITs. They owned properties worth over $20 billion, operated with investment-grade credit ratings, and had delivered consistent returns through multiple cycles. But the biggest test—and opportunity—was still ahead. The financial crisis would create distress not seen since the 1970s, and once again, the grave dancer's protégés would be ready to dance.

VI. The Archstone Mega-Deal: Peak Empire Building (2013)

The opportunity began with catastrophe. September 15, 2008: Lehman Brothers collapsed, sending shockwaves through global finance. Among Lehman's assets was something unusual for an investment bank—a 47% stake in Archstone, one of America's premier apartment companies. Just a year earlier, in October 2007, Lehman had partnered with Tishman Speyer to acquire Archstone for $22.2 billion in one of the largest real estate deals in history. Now Lehman was bankrupt, Tishman Speyer was hemorrhaging cash, and Archstone—despite owning some of the best apartments in America—was trapped in a financial nightmare.

David Neithercut watched from Equity's Chicago headquarters as the drama unfolded. Archstone wasn't just any portfolio—it was the crown jewel of American multifamily real estate. The company owned 71 premier properties with over 20,000 units in exactly the markets Equity coveted: Manhattan, Washington D.C., San Francisco, Los Angeles, Seattle. The average monthly rent exceeded $2,600, the properties were nearly new, and the locations were irreplaceable. This was the kind of portfolio that came available once in a generation—if that.

For six years, Neithercut played a chess match with Lehman's bankruptcy estate. The first offer came in 2009—$2.5 billion for select properties. Rejected. Another bid in 2010—$4 billion for half the portfolio. Rejected again. Lehman's estate, managed by court-appointed trustees, believed Archstone would be worth more as markets recovered. They were both right and wrong—the properties did increase in value, but the complexity of unwinding the ownership structure meant years of legal battles and mounting costs.

The breakthrough came in late 2012. Lehman's estate, eager to finally liquidate and distribute proceeds to creditors, agreed to negotiate exclusively with Equity and its rival AvalonBay Communities. The partnership was unusual—two fierce competitors joining forces—but necessary. Neither company alone could digest a $9 billion acquisition without dangerous leverage. Together, they could split the portfolio strategically, with each taking properties that fit their geographic focus.

The negotiation that November was a marathon. Teams of lawyers, bankers, and executives worked around the clock in Lehman's midtown Manhattan offices—the same building where Lehman traders had once ruled Wall Street. The complexity was mind-bending: unwinding joint venture agreements, assuming or refinancing $5 billion in property-level debt, obtaining consent from dozens of lenders, and structuring tax-efficient transfers. At one point, a disagreement over a single property's valuation nearly killed the entire deal.

On February 27, 2013, at 9:00 AM Eastern, the deal closed. The numbers were staggering: Equity Residential acquired 60% of Archstone's assets for approximately $5.4 billion, while AvalonBay took 40% for $3.6 billion. But here's what made it brilliant—Equity funded its portion entirely through asset sales, not new debt or equity dilution. In the months leading up to the acquisition, they'd quietly sold $4 billion of non-core properties, accumulating a war chest precisely sized for this moment.

The integration was a masterclass in operational excellence. Within minutes of closing—literally minutes—all Archstone apartments appeared on Equity's website, available for leasing. The IT teams had been preparing for months, building shadow systems that could flip live instantly. Marketing materials were pre-printed with spaces for the date. Maintenance staff were hired and trained before they knew which properties they'd manage. When residents woke up on February 28, their apartments had new ownership, but their rent checks went to the same address, their maintenance requests used the same portal—the transition was seamless.

But the real genius was in the portfolio transformation that followed. Equity didn't just absorb Archstone—they reimagined it. Within six months, they'd sold 43 properties comprising 11,588 units for $1.68 billion, achieving a 6.1% cap rate that validated their underwriting. These weren't the crown jewels—they were good properties in secondary locations that didn't fit Equity's laser focus on gateway cities. The sales proceeds were immediately recycled into property improvements, technology upgrades, and debt reduction.

The Archstone acquisition also marked a strategic inflection point. In 2013, Equity executed another massive disposition, selling 8,010 units to a joint venture between Goldman Sachs and Greystar for $1.5 billion. The message was clear: size for size's sake was over. Equity would own fewer, better properties in the absolute best locations, even if it meant shrinking the overall portfolio.

This philosophy reached its apex in 2016 when Equity made a shocking announcement: they were selling 23,262 apartments to Starwood Capital Group for $5.365 billion. The portfolio comprised their entire position in markets like Denver, Orlando, and inland California. Wall Street was stunned—why would a REIT sell a quarter of its assets in one shot? The answer revealed Neithercut's conviction: coastal gateway markets were becoming winner-take-all economies where supply constraints and job growth would drive outsized rent growth. Everything else was a distraction.

The financial engineering behind these moves was sophisticated. By selling properties at cap rates around 5.5% and redeploying capital into coastal markets at similar or slightly higher cap rates, Equity was betting on superior rent growth rather than initial yield. It was a quality-over-quantity strategy that required confidence and patience—exactly the traits Sam Zell had embedded in the company's DNA.

The Archstone deal's legacy extends beyond financial returns. It demonstrated that REITs could execute transformational M&A with the sophistication of any Fortune 500 company. It proved that disciplined capital recycling could create more value than empire building. And it established Equity Residential as the undisputed leader in institutional apartment ownership, a position they maintain today.

VII. Portfolio Transformation & Modern Strategy (2013-Present)

The morning after the Starwood sale closed in 2016, David Neithercut stood before a map of the United States in Equity's boardroom. Entire regions were now blank—no pins in Texas, Florida, Arizona, Colorado. The Sunbelt, where America's population was booming, had been abandoned. To most observers, it looked like retreat. To Neithercut, it was the culmination of a radical thesis: in the age of tech-driven inequality, only a handful of cities would capture outsized economic gains, and Equity would own apartments in every one of them.

The great geographic shift had actually begun years earlier with a simple observation. Equity's data scientists noticed that rent growth in San Francisco and Manhattan consistently outpaced Phoenix and Atlanta, even during downturns. The reason wasn't just tech jobs—it was the confluence of supply constraints, network effects, and what economists call agglomeration advantages. These cities attracted the best talent, which attracted the best companies, which attracted more talent, creating a virtuous cycle that pushed rents ever higher.

The numbers validated the strategy. Between 2013 and 2019, Equity's same-store revenue growth averaged 3.8% annually—seemingly modest until you realized this was on a base of already-premium rents. A typical Equity apartment in San Francisco rented for $3,800 per month in 2019, up from $2,900 in 2013. Similar apartments in Dallas, which Equity had exited, saw rents grow from $1,100 to $1,400—impressive in percentage terms but generating far less absolute dollar growth.

But the transformation wasn't just geographic—it was technological. Equity launched what they called "Revenue 3.0," a dynamic pricing system that adjusted rents daily based on supply, demand, seasonal patterns, and competitive dynamics. Think airline pricing but for apartments. The system was so sophisticated it could predict optimal renewal rates months in advance, adjusting offers to retain high-quality residents while maximizing revenue from those likely to leave anyway.

The resident experience underwent its own revolution. The company introduced "YieldStar," an AI-powered leasing system that could tour prospects virtually, answer questions 24/7, and even negotiate lease terms within preset parameters. Maintenance requests were handled through an app that used image recognition to diagnose problems and automatically dispatch technicians. Smart home features—keyless entry, programmable thermostats, USB outlets—became standard, allowing Equity to charge premium rents while actually reducing operating costs.

The pandemic of 2020 tested every assumption. Urban exodus headlines dominated the news. San Francisco and Manhattan saw rents plummet 20-30% as residents fled to suburbs. Equity's concentrated coastal strategy suddenly looked like a catastrophic mistake. The company's stock fell from $88 in February 2020 to $36 in March—a 59% collapse that wiped out $20 billion in market value.

But Neithercut and his team held their nerve. They implemented what they called "Operation Flexibility"—short-term lease options, furnished units for remote workers, concessions targeted at retention rather than acquisition. Most importantly, they didn't panic-sell properties. The thesis remained intact: knowledge workers would eventually return to cities because that's where opportunities clustered. The only question was when.

The recovery, when it came, was violent. By mid-2021, urban rents were not just recovering but exploding. Equity's San Francisco properties, which had seen occupancy drop to 87%, roared back to 96% occupancy with rents 10% above pre-pandemic peaks. The phenomenon was repeated in every coastal market. The company that looked foolish for concentrating in expensive cities suddenly looked prescient. The stock hit an all-time high of $90 in early 2022.

Capital allocation during this period was surgical. While competitors rushed to build new properties in hot markets, Equity focused on renovation and repositioning. They invested $1.5 billion between 2017 and 2023 in property improvements—not cosmetic upgrades but fundamental reimagining of spaces. Unused retail spaces became co-working areas. Parking garages were converted to bike storage and package centers. Rooftops became amenity decks with outdoor kitchens and yoga studios.

The ESG (Environmental, Social, Governance) initiatives weren't just virtue signaling—they were business strategy. Equity committed to reducing carbon emissions by 30% by 2030, but the real motivation was economics. Energy-efficient buildings commanded premium rents, attracted quality residents, and qualified for tax credits. Solar panels, LED lighting, and efficient HVAC systems had payback periods under five years. Green building certifications became a marketing tool that justified rent premiums.

The company's approach to development also evolved. Rather than ground-up construction—expensive and risky—Equity focused on joint ventures and preferred equity investments. They'd provide capital to local developers who understood permitting and construction, then purchase the completed property at a pre-negotiated price. This asset-light model generated returns without the brain damage of development.

Current portfolio composition tells the story. As of today, Equity owns or has investments in 312 properties consisting of 84,648 apartment units, with an established presence in Boston, New York, Washington, D.C., Seattle, San Francisco and Southern California, and an expanding presence in Denver, Atlanta, Dallas/Ft. Worth noting. Each market was chosen through rigorous analysis of job growth, supply constraints, demographic trends, and regulatory environment.

The modern Equity Residential is barely recognizable from the opportunistic acquirer of distressed properties that Sam Zell built. It's now a technology-enabled, data-driven operating company that happens to own real estate. The transformation required selling 72,000 apartments, investing billions in technology and renovations, and maintaining conviction through the worst pandemic in a century. But the result is a focused, defensible portfolio in America's most dynamic cities—exactly where you'd want to own apartments for the next generation.

VIII. Playbook: The EQR Operating Model

Walk into any Equity Residential property at 8 AM on a Tuesday, and you'll witness something remarkable: a morning huddle that looks more like a tech startup standup than traditional property management. The maintenance supervisor pulls up real-time dashboards on an iPad showing unit turnover schedules, predictive maintenance alerts, and even weather forecasts that might impact operations. The leasing manager reviews AI-generated pricing recommendations for every available unit, adjusted overnight based on competitive listings, seasonal patterns, and prospect traffic. This is apartment management reimagined as data science.

The REIT structure itself is the foundation of Equity's financial engineering. Congress created REITs in 1960 to democratize real estate investment, but Sam Zell recognized their true power: tax-efficient cash flow pass-through vehicles that could scale infinitely. By distributing 90% of taxable income as dividends, REITs avoid corporate taxes entirely. For Equity, this means every dollar of rental income flows directly to shareholders without the double taxation that handicaps traditional corporations. It's a structural advantage worth billions over time.

But the real magic happens in revenue management. Equity's pricing algorithm processes over 20 variables for each unit: historical seasonal patterns, competitive supply within a half-mile radius, prospect traffic trends, economic indicators, even social media sentiment about the neighborhood. The system can predict with 94% accuracy whether a prospect who tours will sign a lease, allowing real-time pricing adjustments. One example: in Seattle, the algorithm noticed prospects who toured on Sundays were 20% more likely to sign at full price. Weekend pricing immediately adjusted upward, generating an extra $2 million annually from that market alone.

The operational excellence extends to every corner of the business. Maintenance requests are triaged by AI that can identify urgent issues through keyword analysis and image recognition. A resident complaining about "water" and "ceiling" triggers immediate response; "squeaky door" gets scheduled for regular hours. The system learns from every interaction, becoming more accurate over time. Response times have dropped 40% while resident satisfaction scores have increased—efficiency and service quality moving in tandem.

The company's brand philosophy, "creating communities where people thrive," isn't just marketing speak—it's embedded in operations. Community managers are trained in event planning, creating monthly calendars of resident gatherings that build stickiness. Wine tastings, yoga classes, pet meetups—these aren't random activities but carefully orchestrated retention tools. Data shows residents who attend two or more events annually renew leases at 15% higher rates.

The STAR values—Service, Teamwork, Accountability, and Respect—cascade through the organization via systematic reinforcement. Every employee, from porters to regional managers, has quarterly reviews tied to these principles. But it's not corporate bureaucracy—it's practical. Service means responding to maintenance requests within two hours. Teamwork means properties share best practices through a company-wide Slack channel. Accountability means every property's performance is transparent, posted weekly for all to see.

Capital allocation follows a disciplined framework that would make Warren Buffett proud. Every investment decision—whether acquiring a property, renovating units, or building amenities—must clear three hurdles: generate returns exceeding the cost of capital plus 200 basis points, improve portfolio quality metrics, and be defensible against technological disruption. This discipline has led to some counterintuitive decisions, like refusing to build new properties in hot markets where construction costs made returns impossible.

The build versus buy versus renovate decision matrix is particularly sophisticated. Equity maintains a database of construction costs, acquisition cap rates, and renovation ROIs updated weekly across all markets. When Seattle construction costs hit $400,000 per unit in 2018, Equity stopped all development and pivoted to acquisitions. When San Francisco cap rates compressed to 3.5%, they focused on renovations generating 15% returns. This dynamic allocation generates superior returns while competitors blindly follow single strategies.

Property management at scale creates competitive moats that individual owners can't replicate. Centralized purchasing generates 20-30% discounts on everything from appliances to insurance. Shared services—accounting, HR, legal—spread costs across thousands of units. The company's size allows dedicated specialists: they employ full-time acoustical engineers to minimize noise complaints, energy managers who optimize utility costs, and even behavioral economists who design lease renewal communications.

The training infrastructure rivals major corporations. Equity University isn't just orientation—it's a two-year program covering everything from fair housing law to Excel modeling to conflict resolution. Maintenance technicians get certified in HVAC, plumbing, and electrical work, with the company paying for training and providing career paths to property management. The average property manager has been with Equity for eight years; the average regional manager, fifteen. This continuity creates institutional knowledge that no competitor can quickly replicate.

Physical occupancy averaging 96.1% through 2024 isn't luck—it's the result of systematic excellence. The company measures and manages dozens of operational metrics: tour-to-lease conversion rates, renewal notice timing optimization, maintenance response satisfaction scores, even the optimal number of photos per online listing (twelve, if you're wondering). Each metric has benchmarks, improvement plans, and accountability structures.

Technology integration continues accelerating. The company is testing facial recognition for building access, predictive maintenance sensors that identify HVAC problems before they occur, and even virtual reality tours that let prospects "walk through" apartments from anywhere. But technology isn't pursued for its own sake—every implementation must demonstrate clear ROI through reduced costs, increased revenue, or improved retention.

The sophistication of Equity's operating model creates a flywheel effect. Better operations generate higher NOI, which attracts capital at lower costs, which funds better properties and technology, which improves operations further. It's a virtuous cycle that's taken decades to build and would take competitors years to replicate—if they could at all. This is the moat that protects Equity's castle, built not of stone but of systems, data, and human capital.

IX. Competition & Market Dynamics

The multifamily REIT sector resembles an oligopoly more than a free market. Three giants—Equity Residential, AvalonBay Communities, and Essex Property Trust—control the institutional apartment landscape in America's gateway cities. Together, they own over 400,000 units worth $150+ billion. But while they compete fiercely for acquisitions and residents, they've also created an informal cartel of operational excellence that keeps smaller players perpetually disadvantaged.

AvalonBay, Equity's closest rival, mirrors its strategy with eerie precision. Founded in 1978, AvalonBay owns 281 properties with 86,000 apartments concentrated in the same coastal markets. The companies are so similar that employees regularly jump between them, creating a cross-pollination of best practices. Where they differ is philosophy: AvalonBay emphasizes ground-up development, building 3,000-4,000 units annually, while Equity focuses on acquisitions and renovations. It's build versus buy, and both strategies have merit depending on the cycle.

Essex Property Trust, the West Coast specialist, demonstrates the power of geographic focus. With 62,000 apartments concentrated in California and Seattle, Essex achieves operating margins exceeding 70%—the highest in the sector. Their secret? Density. By clustering properties in specific submarkets, they dominate local leasing, achieve unprecedented maintenance efficiency, and exercise pricing power that scattered operators can't match. Essex proves you don't need national scale if you have local dominance.

The rise of single-family rental REITs represents a new competitive threat. Invitation Homes and American Homes 4 Rent, both formed after the financial crisis, now collectively own over 150,000 single-family houses. Their pitch to residents is compelling: the space and privacy of a house with the convenience of renting. For families with children and pets—traditionally apartment dwellers by necessity, not choice—these companies offer an attractive alternative. Equity has responded by emphasizing urban locations where single-family rentals are physically impossible.

Private equity's entrance has fundamentally altered market dynamics. Blackstone, Starwood Capital, and Greystar collectively control over 500,000 apartments, dwarfing even the public REITs. These firms operate with different objectives—typically holding properties for 5-7 years before selling—which creates both opportunity and disruption. They'll overpay for acquisitions to deploy capital, driving up prices, then dump properties simultaneously, creating volatility. Public REITs like Equity must navigate these waves while maintaining steady operations.

The technology disruption in property management is accelerating. Companies like RealPage and Yardi provide software that allows small operators to achieve near-institutional efficiency. Dynamic pricing, automated marketing, predictive maintenance—capabilities once exclusive to large REITs are now available off-the-shelf. This democratization of technology erodes some of Equity's operational advantages, forcing constant innovation to stay ahead.

PropTech startups are reimagining every aspect of the rental experience. Latch provides smart access systems that eliminate keys. Flex enables residents to split rent into bi-weekly payments. Zillow and Apartments.com have aggregated demand online, reducing the power of individual property brands. These innovations force Equity to constantly evaluate build-versus-partner decisions, balancing the desire for control against the need for cutting-edge capabilities.

Regulatory challenges multiply with each passing year. Rent control, once limited to New York and San Francisco, now threatens expansion to Seattle, Denver, even Austin. California's statewide rent control law, enacted in 2019, limits annual increases to 5% plus inflation—devastating for operators counting on market-rate resets. Eviction moratoriums during COVID set precedents that politicians now invoke regularly. Equity must price these regulatory risks into every investment decision, avoiding markets where populist politics threaten property rights.

The demographic tailwinds that powered apartment demand for decades are shifting. Millennials, despite stereotypes, aspire to homeownership—surveys show 90% want to buy eventually. As this massive generation ages into prime homebuying years, apartment demand could soften. Generation Z displays different preferences: they value experiences over space, prefer urban to suburban, and show less attachment to ownership. Equity must navigate this generational transition while adapting properties to evolving preferences.

Climate change introduces new competitive dynamics. Coastal properties—Equity's specialty—face rising insurance costs and potential physical risks. Miami, where Equity has minimal exposure, sees regular flooding. San Francisco confronts wildfire smoke that makes outdoor amenities unusable for weeks. Companies with inland portfolios suddenly tout climate resilience as a competitive advantage. Equity has responded by investing heavily in building resilience and partnering with climate scientists to model long-term risks.

The institutionalization of single-family rentals creates a new competitive paradigm. Build-to-rent communities—entire subdivisions of rental houses—combine the benefits of single-family living with professional management. These properties compete directly with garden-style apartments for families. Equity's urban focus provides some insulation, but the trend forces constant evaluation of suburban exposure.

International capital adds another layer of complexity. Sovereign wealth funds, Canadian pension plans, and European institutions view American multifamily as a safe haven. They'll accept lower returns for stability, driving cap rates to levels that make acquisitions challenging for public REITs requiring immediate accretion. Equity must compete against cost-of-capital advantages while maintaining return discipline.

The competitive landscape reveals a fundamental truth: scale alone no longer guarantees success. Operational excellence, technological sophistication, and strategic focus matter more than raw unit count. Equity's response has been to double down on what differentiates them: gateway city expertise, institutional operations, and long-term ownership mentality. In a market where everyone claims to be "best in class," Equity must constantly prove it through superior returns—the ultimate scorecard in the ruthless game of real estate.

X. Bear vs. Bull Case & Future Outlook

The Bull Case: A Generational Setup for Apartment REITs

Demographics alone could power Equity Residential for the next decade. The numbers are staggering: 4.7 million Americans turn 30 annually through 2030—prime apartment-renting age. Meanwhile, homeownership has become mathematically impossible for many. With median home prices at $400,000 and mortgage rates above 7%, the typical monthly payment exceeds $3,500. Equity's average rent of $2,800 suddenly looks like a bargain, especially when you factor in maintenance, taxes, and flexibility.

The supply constraints in Equity's chosen markets border on absolute. San Francisco hasn't permitted significant new apartment construction in years. Manhattan's development costs exceed $1,000 per square foot. Seattle and Boston face similar dynamics: massive demand meeting immovable supply constraints. This isn't a temporary phenomenon—it's structural, embedded in zoning laws, NIMBY politics, and geographic limitations. Equity owns irreplaceable assets in markets where new supply is effectively illegal.

Inflation, counterintuitively, benefits Equity's model. Apartment leases reset annually, allowing rapid rent adjustments that track or exceed inflation. Operating costs—mostly labor and utilities—comprise just 35% of revenue, providing significant operating leverage. Meanwhile, Equity's debt is largely fixed-rate, creating a beautiful mismatch: inflating revenues servicing static debt costs. The 1970s, America's last inflationary period, saw apartment REITs generate spectacular real returns.

The work-from-home revolution, initially seen as threatening cities, has evolved into a powerful tailwind. Knowledge workers no longer need to live near offices five days a week—but they still cluster in dynamic cities for cultural amenities, dating pools, and optional office access. This flexibility actually increases demand for quality urban apartments. Equity's properties, with their co-working spaces and high-speed internet infrastructure, are perfectly positioned for the hybrid future.

Technological leverage amplifies returns beyond what traditional real estate could achieve. Equity's revenue management systems generate 2-3% annual pricing gains above market. Predictive maintenance reduces operating costs by 10-15%. Virtual leasing eliminates the need for weekend staff. Each innovation compounds, creating returns that wouldn't exist without scale and sophistication. Smaller operators simply can't match this technological arms race.

The Bear Case: Storm Clouds Gathering

Interest rate sensitivity could devastate REITs broadly and Equity specifically. REITs trade like bonds with growth kickers—when rates rise, valuations compress. A return to 1980s-style rates would crater property values and make Equity's dividend yield uncompetitive with risk-free Treasuries. The company's significant floating-rate debt exposure amplifies this risk. Every 100 basis point increase in rates costs Equity approximately $50 million in annual interest expense.

The urban exodus narrative, while currently paused, could resume with vengeance. Crime, homelessness, and quality-of-life deterioration in cities like San Francisco and Seattle are real issues. Remote work technology continues improving, making urban proximity less necessary. If knowledge workers decisively choose suburbs over cities, Equity's concentrated coastal strategy becomes a concentrated coastal disaster.

Regulatory risks multiply by the day. Rent control expansion seems inevitable in blue states where Equity concentrates. Good cause eviction laws make removing problem tenants nearly impossible. Transfer taxes, vacancy taxes, and wealth taxes targeting real estate owners proliferate. California's recent legislation requiring solar panels and EV charging adds millions in retrofit costs. Each regulation individually seems manageable; collectively, they threaten the business model.

Millennial homeownership aspirations remain powerful. Surveys consistently show 85-90% want to own homes eventually. As this generation accumulates wealth and starts families, the exodus from apartments could accelerate. The pandemic proved that when pushed, Americans choose space over location. Equity's premium urban apartments might be a waystation, not a destination.

New supply, while currently constrained, could surge unexpectedly. Zoning reforms in California and Oregon aim to dramatically increase housing production. Office-to-residential conversions could add thousands of units in urban cores. Modular construction and 3D printing promise to slash building costs. If any of these trends accelerate, Equity's supply-constrained thesis collapses.

The Future Outlook: Navigating Uncertainty

Climate change represents both existential risk and competitive opportunity. Equity's coastal concentration exposes it to hurricanes, flooding, and earthquakes—risks that insurance markets are beginning to price prohibitively. But the company's resources allow adaptation investments smaller operators can't afford: flood barriers, backup power systems, earthquake retrofits. Climate resilience could become a differentiator that justifies premium rents.

The evolution toward micro-units and co-living challenges traditional apartment models. Young urbanites increasingly accept smaller private spaces in exchange for elaborate shared amenities. Companies like Common and WeLive (despite WeWork's struggles) demonstrate demand for community-oriented housing. Equity must decide whether to compete, acquire, or ignore this trend that could fundamentally reshape urban living.

Mixed-use development represents the next frontier. Equity's properties sit on valuable land that could support retail, office, or even medical facilities. Adding complementary uses creates value, diversifies income, and builds community amenities that increase retention. But it also adds complexity, regulatory challenges, and capital requirements. The company must balance focus with opportunity.

Artificial intelligence will revolutionize property operations within five years. Imagine AI assistants that handle all resident communications, predictive systems that prevent maintenance issues before they occur, and pricing algorithms that optimize to the penny. Equity's scale provides the data necessary to train these systems. But it also requires massive technology investments and cultural changes that old-line real estate companies traditionally resist.

The path forward requires threading multiple needles simultaneously. Equity must maintain operational excellence while transforming technology infrastructure. They must generate current returns while investing for an uncertain future. They must satisfy shareholders demanding dividends while retaining capital for growth. It's a balancing act that would challenge any management team.

XI. Legacy & Lessons

Sam Zell died on May 18, 2023, at age 81, leaving behind more than just a real estate empire—he left a philosophy that fundamentally changed how Americans think about property, risk, and opportunity. The boy who fled Poland in his mother's womb had built a $4 trillion industry, created thousands of millionaires, and housed millions of Americans. But his greatest legacy might be the mindset he embedded in the organizations he built: contrarian thinking, operational excellence, and the courage to dance when others flee.

The institutionalization of apartment ownership represents a profound shift in American capitalism. Before Equity Residential and its peers, apartments were owned by local families, small partnerships, and occasional insurance companies. Professional management meant a live-in super with a toolbox. Today, institutional investors own millions of apartments, managed with the sophistication of Fortune 500 companies. This transformation improved living standards, stabilized communities, and created investable assets for pension funds and 401(k)s.

Zell's impact extends far beyond Equity Residential. He created the modern REIT industry through advocacy, education, and example. The company was founded by Robert H. Lurie and Sam Zell in March 1993, but Sam's vision extended decades earlier. His speeches at industry conferences became legendary—provocative, profane, and invariably prescient. He pushed REITs to think like operators, not just landlords. His book, "Am I Being Too Subtle?"—the title itself a perfect Zellism—became required reading for real estate professionals.

The grave dancer philosophy—finding opportunity in distress—influenced a generation of investors. But people misunderstand the metaphor. Sam wasn't celebrating failure; he was recognizing cycles. Every boom contains the seeds of its bust. Every bust creates opportunities for the next boom. The key is maintaining liquidity and courage when others lose both. This thinking now permeates investment firms worldwide, from Oaktree to Apollo to Blackstone.

Leadership transitions test organizational culture, and Equity has passed remarkably well. David Neithercut, who succeeded Zell as chairman, embodies continuity with evolution. He maintains the contrarian discipline while embracing technology and ESG initiatives Sam might have mocked. Mark Parrell, the current CEO, rose through the ranks over 20 years, ensuring cultural continuity. The company remains promoted-from-within, long-term focused, and refreshingly candid—rare qualities in corporate America.

The lessons for investors are timeless. First, specialized knowledge creates edges. Equity doesn't just own apartments; they understand demographics, psychology, and urban dynamics at granular levels. Second, operational excellence matters more than financial engineering. Anyone can buy properties with leverage; few can operate them at 96% occupancy while maintaining pricing power. Third, concentration can be strength if you pick the right areas to concentrate. Equity's coastal focus looked risky but generated superior returns.

Creating shareholder value through cycles requires different skills than riding a single wave. Equity has navigated the dot-com bubble, 9/11, the financial crisis, and COVID-19 while maintaining its dividend and investment-grade rating. This isn't luck—it's systematic risk management, conservative leverage, and the discipline to sell assets when prices are high, not when capital is needed. The company has returned over 2,000% to shareholders since its IPO, crushing broader market indices.

What would Sam Zell do today? He'd probably be looking where others aren't. While everyone focuses on AI and technology, he'd be buying trailer parks and self-storage facilities. While others chase growth, he'd be accumulating cash for the next downturn. He'd certainly be skeptical of current valuations, warning about excessive leverage and tourist investors who've never seen a real bear market. But he'd also recognize opportunity in disruption, possibly building the Airbnb of apartments or the Amazon of property management.

The cultural preservation at Equity deserves study by business schools. How does a company maintain entrepreneurial spirit while operating at institutional scale? How does it preserve founder DNA through multiple leadership transitions? The answer lies in systematic culture transmission: hiring for values fit, promoting from within, maintaining high ownership mentality through equity compensation, and telling stories that reinforce core principles. Every Equity employee knows the grave dancer story, understands capital allocation, and thinks like an owner.

The broader lessons for American capitalism are profound. REITs democratized real estate investment, allowing small investors to own institutional-quality properties. They professionalized property management, improving living conditions for millions. They created liquidity in an illiquid asset class, enabling efficient capital allocation. And they proved that tax-efficient structures could align public and private interests. Sam Zell didn't just build a company—he built an industry that reshapes how Americans live, invest, and build wealth.

The transformation from Sam Zell's opportunistic partnership to today's sophisticated institution represents American capitalism at its best: innovation, adaptation, and value creation through multiple cycles. Equity Residential stands as testament that contrarian thinking, operational excellence, and long-term focus can build enduring enterprises. The grave dancer may be gone, but the dance continues—and for those who understand the rhythm, the music has just begun.

XII. Recent News### **

Q3 2024 Earnings and Operational Performance**

Equity Residential reported results for the quarter and nine months ended September 30, 2024, demonstrating solid operational performance despite mixed financial metrics. The company reported an earnings per share (EPS) of $0.38 for Q3 2024, falling short of the analyst estimate of $0.43, representing a 15.6% decrease from the $0.45 EPS reported in the same quarter of 2023. However, the underlying business showed strength with Funds from Operations (FFO) per share of $0.99, up 3.1% from $0.96 in the prior year.

The operational metrics painted a picture of disciplined execution. Same store revenue increased 2.7% for the third quarter of 2024 compared to the third quarter of 2023, driven by good demand and modest supply across most of the Company's markets. Same store expense increased 3.2% with low growth in the primary expense categories. This resulted in Same store Net Operating Income (NOI) increased 2.5%.

CEO Mark Parrell emphasized the company's resilience: "Our business continues to benefit from high employment levels among our well-earning resident base, wage growth across the economy, and limited home ownership and rental options in most of our markets, making our well-located apartment properties an appealing choice". The company maintained exceptional occupancy rates, with 96.1% during the third quarter, demonstrating the continued demand for quality apartments in gateway cities.

Strategic Acquisitions and Portfolio Expansion

The third quarter marked a significant acceleration in Equity's expansion market strategy. During the third quarter of 2024, the Company acquired fourteen properties, consisting of 4,418 apartment units, for an aggregate acquisition price of approximately $1.26 billion at a weighted average Acquisition Cap Rate of 5.1%. These assets are located in the Company's Expansion Markets of Atlanta, Dallas/Ft. Worth and Denver.

The marquee transaction was the acquisition of 11 apartment properties from Blackstone Real Estate strategies for approximately $964 million, expected to close in the third quarter of 2024. The properties total 3,572 apartment units and are on average eight years old, representing high-quality, institutional-grade assets that align perfectly with Equity's target demographic.

CIO Alec Brackenridge highlighted the strategic rationale: "We are pleased to add these high-quality, well-located properties to our growing portfolios in Atlanta, Dallas/Ft. Worth and Denver at pricing that is attractive compared to replacement costs. This transaction is a significant step in our goal of generating a higher percentage of our annual net operating income from these strong growth expansion markets".

The financial engineering behind these acquisitions demonstrated sophisticated capital management. The unlevered IRR for the Blackstone portfolio is about 8%, which was in excess of our weighted average cost of capital at the time. To fund these acquisitions, the Company issued $600.0 million of unsecured 10-year notes at a coupon rate of 4.65%, the lowest 10-year coupon rate issued by a REIT since 2022, and an all-in effective yield of 4.9%. Proceeds from this issuance were used to partially fund the acquisitions.

2025 Outlook and Market Positioning

Looking ahead to 2025, management expressed cautious optimism. "We think 2025 should produce solid same-store revenue results for Equity Residential. Seattle and San Francisco, particularly our uniquely urban portfolios in those markets should generate better same-store revenue results, which, along with the continued strength in the Northeast, and the favorable 2025 supply picture across almost all of our established markets should more than offset continued supply-driven weakness in our expansion markets. In later years, the supply wanes in our expansion markets, those markets will be more of a same-store rev growth engine for our company".

The company is also exploring operational improvements through technology. Equity Residential is leveraging AI technology to handle resident inquiries, aiming to improve operational efficiencies and reduce costs. Additionally, management identified opportunities in ancillary revenue streams, with CFO Robert Garechana noting: "We expect to end 2024 with bad debt around 1% of revenue, with normal pre-pandemic levels at about 50 basis points. The opportunity is the delta between these figures. For other income, particularly from the bulk WiFi program, contributions will be more meaningful in the fourth quarter and into 2025".

Regulatory Developments and Market Challenges

The regulatory landscape continues to evolve, particularly in Equity's key markets. Washington State recently enacted significant rent control legislation. "Washington landlords can no longer raise rents by more than 10% per year under landmark legislation Gov. Bob Ferguson signed into law Wednesday. Effective immediately, House Bill 1217 caps residential rent hikes during a 12-month period at 7% plus inflation, or 10%, whichever is lower. The limit will last 15 years".

In Seattle specifically, As of May 7, 2025, maximum rent increase of 7% plus the consumer price index (CPI) up to a maximum of 10% per year, with all housing cost increase notices must provide a minimum of 180 days' advance written notice. These regulations create both challenges and opportunities—while limiting pricing power, they also create barriers to entry for less sophisticated operators who cannot navigate the complex regulatory environment.

Denver and Colorado present a different regulatory environment. "Currently, Colorado doesn't implement rent control regulations at a state-wide level. Moreover, the state prohibits cities and counties from implementing rent control measures. In essence, enforcing rent control laws in Colorado isn't allowed". This regulatory freedom in expansion markets provides Equity with pricing flexibility that partially offsets constraints in coastal markets.

Development Pipeline and Capital Allocation

As of September 30, 2024, the Company has 42 properties (including those under development) located in its Expansion Markets of Atlanta, Austin, Dallas/Ft. Worth and Denver, which constitutes approximately 10% of total portfolio NOI. This represents substantial progress toward management's goal of geographic diversification while maintaining the company's core strength in coastal gateway cities.

The company continues to demonstrate disciplined capital allocation, as evidenced by recent market commentary from management. The focus remains on acquiring properties at attractive prices relative to replacement cost while maintaining a strong balance sheet. The successful debt issuance at historically low spreads demonstrates continued access to capital markets at favorable terms, providing dry powder for future opportunistic acquisitions.

XIII. Links & Resources

Company Resources

- Equity Residential Investor Relations: investors.equityapartments.com

- Annual Reports and 10-K Filings: SEC EDGAR Database

- Q3 2024 Earnings Presentation and Transcript

- Corporate Responsibility Reports

Sam Zell Legacy Materials

- "Am I Being Too Subtle?: Straight Talk From a Business Rebel" by Sam Zell (2017)

- "The Grave Dancer" Essay (1976) - Real Estate Review

- Zell/Lurie Real Estate Center at Wharton

Industry Research

- National Multifamily Housing Council (NMHC) Research

- Urban Land Institute (ULI) Multifamily Reports

- REIT Industry Analysis - NAREIT

- CoStar Multifamily Market Reports

- Green Street Advisors REIT Analytics

Academic Studies

- "The Economics of REITs" - Journal of Real Estate Finance and Economics

- "Multifamily Housing Trends" - MIT Center for Real Estate

- "REIT Performance Through Market Cycles" - Real Estate Economics Journal

Regulatory Resources

- Washington State Rental Laws and Rent Control Updates

- Seattle Department of Construction & Inspections Rental Regulations

- Colorado Landlord-Tenant Law Resources

- Federal Fair Housing Act Guidelines

Competitive Analysis

- AvalonBay Communities Investor Relations

- Essex Property Trust Investor Materials

- Camden Property Trust Financial Reports

- Blackstone Real Estate Investment Trust (BREIT) Updates

Historical Context

- "The REIT Revolution: How REITs Changed Real Estate" - NAREIT Historical Archive

- Resolution Trust Corporation Historical Database

- Federal Reserve Economic Data (FRED) - Real Estate Metrics

Technology and Innovation

- RealPage Revenue Management Systems

- Yardi Property Management Software

- PropTech Industry Reports - MetaProp Analytics

- AI in Real Estate - McKinsey & Company Research

Market Data and Analytics

- Census Bureau Housing Statistics

- Bureau of Labor Statistics Rental Market Data

- Moody's Analytics Multifamily Forecasts

- Zillow Rental Market Reports

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube