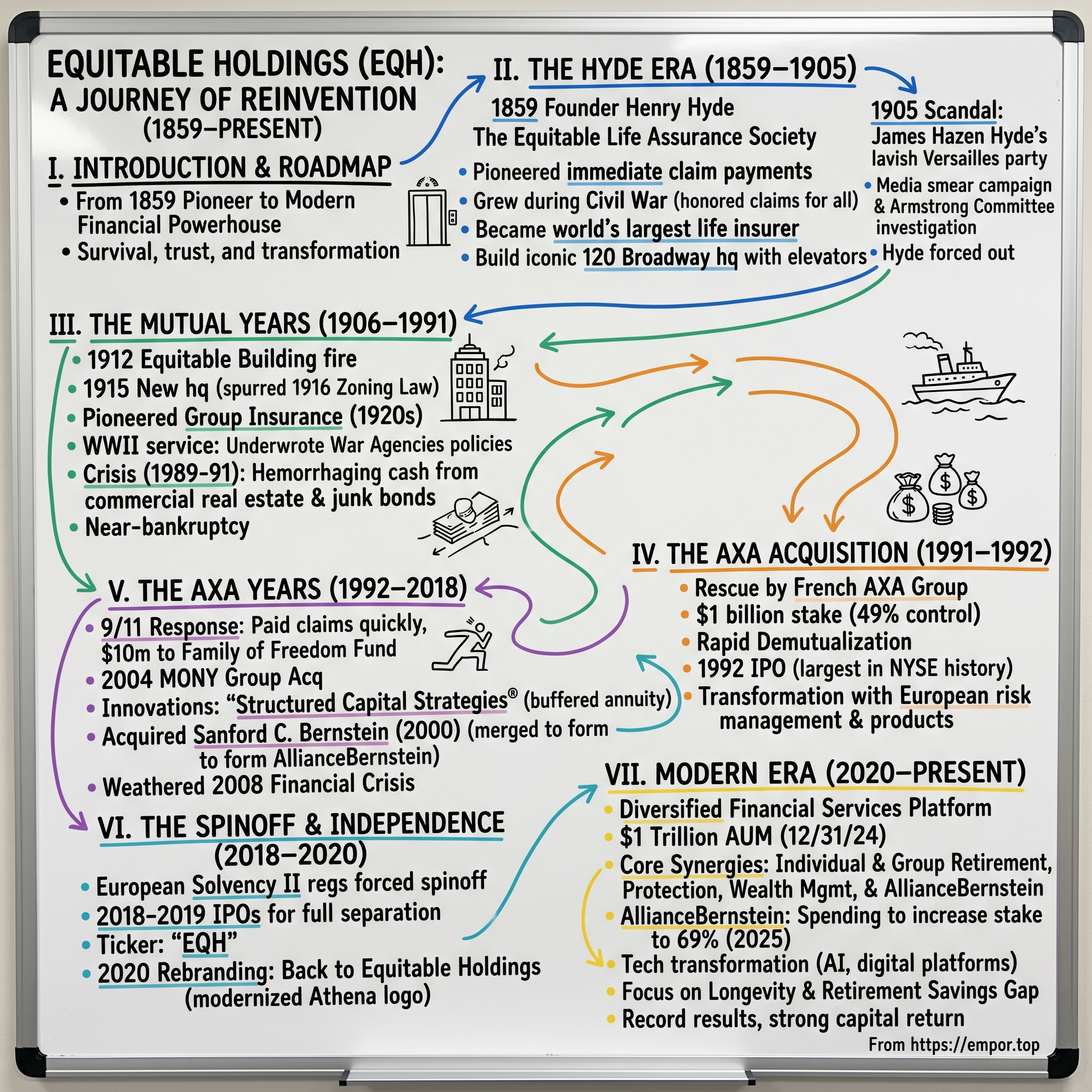

Equitable Holdings: From 1859 Pioneer to Modern Financial Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's July 18, 1991, and Equitable Life—one of America's oldest and most prestigious insurers—is hemorrhaging cash. Commercial real estate loans have gone sour. Junk bonds are imploding. The company that once towered over Manhattan from its iconic headquarters is now weeks away from potential bankruptcy. Then, like cavalry arriving at dawn, a French insurance company named AXA appears with a $1 billion check. This rescue would transform not just Equitable, but reshape the entire landscape of American financial services.

Today, Equitable Holdings manages over $1 trillion in assets—a staggering sum that represents the retirement dreams and financial security of millions of Americans. The company that Henry Baldwin Hyde founded in a modest New York office in 1859 with $100,000 in capital now operates as one of America's leading financial services companies, touching everything from individual retirement accounts to sophisticated asset management through AllianceBernstein.

But here's the central question that makes this story so compelling: How did a 19th-century life insurance mutual survive the Civil War, the Great Depression, near-bankruptcy in 1991, French ownership for nearly three decades, and emerge as an independent powerhouse in 2020? The answer involves scandal at Versailles-themed parties, innovation born from wartime necessity, and financial engineering that would make Wall Street's sharpest minds take notice.

This isn't just a story about insurance—though insurance is where it begins. It's about survival, reinvention, and the art of building trust over 165 years. It's about how a company can lose its way, find salvation from an unlikely source, and ultimately rediscover its identity. From post-Civil War insurance innovation to today's diversified financial services leader, Equitable's journey offers profound lessons about crisis management, patient capital, and the power of strategic transformation.

We'll trace this epic arc through distinct eras: the Hyde family's ambitious empire-building, the mutual years that brought both glory and near-death, the AXA rescue and transformation, and finally, the company's rebirth as an independent entity. Along the way, we'll uncover how Equitable pioneered the buffered annuity, why European solvency laws triggered its independence, and what its future holds in an America where 10,000 people turn 65 every single day.

II. The Hyde Era: Building an Insurance Empire (1859–1905)

The summer of 1859 was sweltering in New York City when 25-year-old Henry Baldwin Hyde walked into a small office at 98 Broadway with an audacious plan. The son of a successful merchant, Hyde had spent years studying the insurance business, and he'd identified a critical flaw: when breadwinners died, their families often waited months—sometimes years—for death benefit payments. Hyde's radical idea? Pay claims immediately, within days of receiving proof of death. In an era when widows could lose their homes while waiting for insurance payouts, this was revolutionary.

Hyde founded The Equitable Life Assurance Society of the United States with William C. Alexander as its first president and a stated capital of $100,000. But Hyde was the driving force—a relentless salesman who understood that life insurance wasn't really about death; it was about dignity, security, and keeping promises to families. He recruited agents with evangelical fervor, training them to sell not just policies but peace of mind. "Life assurance," Hyde would tell his agents, "is the greatest invention of modern times for the benefit of the human race. "The Civil War erupted just two years after Equitable's founding, and while other insurers hesitated, Hyde saw opportunity in tragedy. He instructed his agents to continue writing policies for soldiers—both Union and Confederate—and honored every death claim promptly, regardless of which side the policyholder fought for. This decision, controversial at the time, established Equitable's reputation for putting policyholders above politics. By 1865, the company had paid out hundreds of thousands in war claims, yet its assets had grown to over $2 million.

After William C. Alexander's death in 1874, Hyde assumed the presidency and led the company through an extraordinary period of expansion. He was a marketing genius who understood that insurance needed to be sold, not bought. Hyde pioneered the use of aggressive advertising, plastering Equitable's name on billboards, newspapers, and even the sides of buildings. He recruited agents with the fervor of a religious revival, offering them generous commissions and elaborate sales contests. Winners received gold watches, European trips, and public recognition at grand banquets.

The numbers tell a stunning story of growth. In 1886, Equitable surpassed Mutual to become the largest life insurance company in the world, selling $111.5 million worth of policies that year and maintaining $411.8 million of coverage in force. Hyde had built the Equitable Life Assurance Building in 1870, installing the first passenger elevators in what was then the tallest office building in the United States—a statement of ambition that New Yorkers couldn't ignore.

During these boom years, the firm could boast of having among its directors Ulysses S. Grant and financier John Jacob Astor. Hyde cultivated relationships with America's power elite, understanding that insurance was as much about trust and prestige as it was about actuarial science. He was also a founding member of the Jekyll Island Club, known as The Millionaires Club, where America's financial titans gathered to shape the country's economic future.

But Hyde's greatest innovation might have been his succession planning—or rather, his catastrophic failure at it. Hyde sought to guarantee that his son James Hazen Hyde would continue the family's control of the company after his death. The younger Hyde was appointed a vice president at 22 and was 23 when he inherited a majority interest in the company. This nepotistic arrangement would plant the seeds for one of Wall Street's first great scandals.

When Henry Baldwin Hyde died on May 2, 1899, The Equitable was the largest life insurance company in the world. He had transformed a $100,000 startup into a global colossus in just forty years. But he had also created a time bomb. His son James Hazen Hyde, brilliant but flamboyant, inherited control of this empire at an age when most men were just starting their careers.

The stage was set for catastrophe. On January 31, 1905, James Hazen Hyde threw what would become the most infamous party in American business history. Hyde was falsely accused through a media smear campaign initiated by company president James Waddell Alexander and board directors E. H. Harriman, Henry Clay Frick and J.P. Morgan of charging a fabulous $200,000 Versailles-themed affair to the company. The party, held at Sherry's restaurant in New York, featured guests dressed as members of the court of Louis XVI, with Hyde himself appearing as the Sun King's brother. The evening included performances by the Metropolitan Opera stars and a midnight supper served on gold plates.

Whether Hyde actually charged the party to the company remains disputed—modern historians largely agree he paid for it personally—but the perception was devastating. The press seized on the story of corporate excess, painting Hyde as a symbol of Gilded Age corruption. The repercussions rocked Wall Street and resulted in an investigation of the entire insurance industry by the New York State Legislature. The Armstrong Committee hearings that followed exposed widespread corruption across the insurance industry, leading to sweeping reforms that still shape insurance regulation today.

Hyde, facing a coordinated assault from board members who wanted control of the company, was forced to sell his shares to financier Thomas Fortune Ryan for $2.5 million and fled to France, where he would remain for decades. The Hyde era had ended not with a whimper but with a scandal that defined an epoch.

III. The Mutual Years: Growth and Near-Death (1906–1991)

The morning of January 9, 1912, started like any other winter day in lower Manhattan. By noon, the original Equitable Building at 120 Broadway was engulfed in flames. Six people died, and the fire raged so intensely that ice formed on firefighters' coats as they battled the blaze in sub-freezing temperatures. The building that Henry Hyde had erected as a monument to American capitalism was reduced to frozen rubble. But from these ashes, Equitable would build something even more audacious—and controversial.

The new Equitable Building, completed in 1915, rose 38 stories straight up from the sidewalk, without any setbacks. Its 1.2 million square feet of office space could house 16,000 workers, casting a shadow that plunged seven acres of lower Manhattan into permanent twilight. The public outcry was so intense that New York City passed the 1916 Zoning Resolution—America's first citywide zoning law—specifically to prevent another Equitable Building. The company had literally changed the shape of American cities.

But while Equitable was reshaping skylines, it was also quietly revolutionizing insurance. The 1920s brought group insurance to the forefront, and Equitable led the charge, convincing corporations that employee benefits were not just perks but essential tools for attracting and retaining talent. By 1925, the company was providing group life insurance to major corporations across America, establishing relationships that would endure for decades. World War II would test Equitable in ways no one could have imagined. In 1943, at the request of President Franklin D. Roosevelt and Treasury Secretary Henry Morgenthau Jr., Equitable stepped forward when other insurers hesitated. The Equitable Life Assurance Society was selected to underwrite policies for the War Agencies Employees Protective Association, providing group life insurance to U.S. Government employees working in or around war zones. Through WAEPA, Equitable sold policies to employees of 40 U.S. agencies, including individuals from the Offices of Strategic Services and War Information, which often sent their men behind enemy lines, and also included air-traveling statesmen and Congressmen.

The risk was enormous—these were people parachuting behind Nazi lines, conducting espionage in occupied territory, flying over active combat zones. Yet Equitable's actuaries had calculated the risks with such precision that by May 1945 only 24 death claims had been filed, allowing the insurer to return roughly 30% of the premiums to WAEPA. This wasn't just good business; it was patriotic service that cemented Equitable's reputation as America's insurer.

The post-war boom years saw Equitable riding high. The company expanded aggressively into group insurance, retirement planning, and real estate. The 1950s and 1960s were golden years—America was prosperous, corporations were expanding benefits, and Equitable was there to provide them. By 1959, the company's centennial year, it had nearly $10 billion in assets and $34.4 billion of insurance in force.

But success bred complacency, and complacency bred risk-taking. Through the 1970s and early 1980s, Equitable began chasing higher yields to compete with newer, more aggressive players. The company loaded up on commercial real estate loans, believing that property values only went up. It invested heavily in junk bonds, seduced by their high interest rates. Most dangerously, it sold guaranteed investment contracts (GICs) that promised fixed returns regardless of market conditions.

In 1985, the Equitable Life Assurance Society of the United States, then the third largest life insurance company in the country, formed Equitable Real Estate Investment Management, a subsidiary used by Equitable Life to develop and finance new real estate projects and manage the US$20 billion worth of real estate under Equitable's control. This move into real estate would prove to be both ambitious and ultimately dangerous.

By 1989, the warning signs were everywhere. The commercial real estate market was beginning to crack. The junk bond market, inflated by Michael Milken's empire at Drexel Burnham Lambert, was collapsing. Equitable's GIC obligations were coming due just as its investment returns were plummeting. The company that had survived the Civil War, two World Wars, and the Great Depression was now facing its gravest crisis.

In December 1990, Equitable announced its decision to demutualize under New York's liberalizing laws. This was intended to enable Equitable to increase and diversify its asset base. But this was more than a strategic shift—it was a desperate attempt to raise capital before disaster struck.

The company's real estate portfolio was hemorrhaging value. Office buildings in Houston stood empty. Shopping centers in Phoenix couldn't find tenants. The junk bonds were being marked down daily. By early 1991, Wall Street was buzzing with a terrifying rumor: There had been rumors that Equitable was nearing a bankruptcy filing prior to the AXA Group infusion of capital.

Equitable Life, the company that had defined American insurance for 132 years, was weeks away from potential collapse. The mutual structure that had served it since 1905 now trapped it—unable to raise capital quickly, unable to sell assets fast enough, unable to stop the bleeding. Something dramatic had to happen, or one of America's most storied financial institutions would cease to exist.

IV. The AXA Acquisition: French Rescue & Transformation (1991–1992)

Claude Bébéar sat in his Paris office on a gray March morning in 1991, studying a confidential report about The Equitable Life Assurance Society of the United States. The chairman of AXA, France's ambitious insurance conglomerate, saw something others missed. Where American executives saw a dying giant bleeding cash, Bébéar saw the keys to global dominance. "The Americans think only in quarters," he told his lieutenants. "We French, we think in decades."

AXA had been aggressively expanding since the 1980s, but it lacked what Equitable possessed: a massive American distribution network, a prestigious brand dating to 1859, and relationships with corporate America's elite. Bébéar knew that Equitable's crisis was AXA's opportunity. He dispatched a team to New York with instructions: negotiate hard, but get the deal done.

On July 18, 1991, AXA Group bought a $1 billion stake for 49% of the business. This enabled Equitable to set aside $500 million for losses in its real estate and junk bond portfolios. The deal was structured brilliantly—AXA got effective control without triggering regulatory complications that would come with majority ownership, while Equitable got the capital infusion it desperately needed to avoid bankruptcy.

But the real genius was what came next. AXA and Equitable's management team, led by CEO Richard Jenrette, embarked on one of the fastest demutualizations in insurance history. What typically took three to five years, they accomplished in just 19 months. The IPO process was a masterclass in financial engineering and organizational transformation.

The demutualization required converting 3.5 million policyholders into shareholders, restructuring billions in liabilities, and convincing skeptical regulators that this radical transformation would protect, not harm, policyholders' interests. Teams worked around the clock, with French executives flying back and forth across the Atlantic weekly. The cultural clash was intense—American managers accustomed to quarterly earnings met French strategists thinking in decade-long arcs.

On July 20, 1992, Equitable went public in what was then the largest IPO in New York Stock Exchange history. The offering raised $450 million through 50 million shares priced at $9 each, with AXA's $1 billion commitment locked in. The total capital raised exceeded $1.45 billion. Trading opened at $9.50 and closed the first day at $10.25—a 14% gain that signaled market confidence in the French-American alliance.

The investment by AXA Group significantly altered the trajectory of both companies. For Equitable, it meant survival and access to global markets. For AXA, it was the cornerstone of becoming a global insurance powerhouse. Bébéar would later call it "the deal that made AXA."

The transformation under AXA was swift and comprehensive. French executives brought European-style product innovation, particularly in investment-linked insurance products. They introduced sophisticated risk management techniques developed in volatile European markets. Most importantly, they brought patient capital—the willingness to invest for long-term growth rather than quarterly earnings.

The cultural integration was fascinating to observe. AXA instituted wine at business lunches (shocking to American insurance executives), while Americans introduced casual Fridays (equally shocking to the French). The head office featured both an excellent cafeteria with French cuisine and an American-style gym. Meetings began to feature simultaneous translation, and executives on both sides began learning each other's languages.

By 1993, just two years after near-bankruptcy, Equitable was profitable again. The real estate losses had been absorbed, the junk bond portfolio restructured, and new products were flying off the shelves. By 1997, the assets of the U.S. operation, the Equitable Insurance Group, had reached nearly a quarter of a trillion dollars, and by 2003, AXA Equitable Insurance Company was the leading carrier in the world with more than 50 million clients, in more than 50 countries, and with nearly a trillion dollars in client assets.

In 2004, the company officially changed its name to AXA Equitable Life Insurance Company. The rebranding represented more than a name change—it was the final integration of American ambition and French sophistication. The company that Henry Hyde had built from a single New York office was now part of a global empire, yet somehow still quintessentially American in its core business.

The AXA acquisition would go down as one of the most successful cross-border insurance deals in history. It saved an American icon from collapse, gave a French company its crucial American foothold, and created a template for international insurance consolidation that others would follow for decades. But this was just the beginning of a 27-year journey that would see even more dramatic transformations ahead.

V. The AXA Years: Global Integration & Innovation (1992–2018)

The morning of September 11, 2001, began like any other at AXA Equitable's offices in Manhattan. Then American Airlines Flight 11 struck the North Tower of the World Trade Center at 8:46 AM. The company's disaster response team, trained but never truly tested, suddenly faced the unimaginable. Within hours, CEO Mark Pearson made a decision that would define the company's character: AXA Equitable would pay every claim immediately, waive all waiting periods, and provide emergency funds to affected families without requiring documentation.

The company pledged over $10 million as a founding donor to the Families of Freedom Scholarship Fund, supporting education for children who lost parents in the attacks. Claims processors worked 24-hour shifts, grief counselors were stationed in every office, and the company set up emergency assistance centers throughout the New York area. When final numbers came in, AXA Equitable had lost 17 employees and would pay out over $80 million in death benefits. The French parent company sent a delegation led by Chairman Henri de Castries, who stood at Ground Zero and promised: "AXA will never abandon New York."

This response to 9/11 exemplified how AXA Equitable had evolved—combining American resilience with European solidarity. The company emerged from the tragedy with its reputation enhanced and its purpose clarified. It was no longer just selling insurance; it was providing security in an increasingly uncertain world. The 2004 acquisition of MONY Group for $1.5 billion represented a strategic masterstroke. AXA Financial, AXA's U.S. financial services unit, acquired 100 percent of MONY, bringing with it not just 560,000 policies but more importantly, a distribution network and product expertise that filled critical gaps in AXA Equitable's capabilities. The MONY Group Inc. was formed and went public in 1998 as part of the demutualization of the Mutual Life Insurance Company of New York, a mutual life insurance company founded in 1842. This wasn't just buying market share—it was acquiring 162 years of American insurance heritage and relationships. But the real innovation came with product development. Equitable introduced Structured Capital Strategies®, the first registered index-linked, or buffered, annuity in 2010. This revolutionary product offered investors something unprecedented: the ability to participate in market upside while having a buffer against the first 10-20% of market losses. It was insurance meets investment, a hybrid that only a company with Equitable's actuarial expertise and AXA's risk management sophistication could have created.

The product was so successful that competitors scrambled to copy it, but Equitable maintained its first-mover advantage through continuous innovation. By 2020, the company was launching enhanced versions with features like "Dual Direction" segments that could make money whether markets went up or down, and "Loss Limiter" options that guaranteed investors could never lose more than 5% or 10% of their investment at maturity. Meanwhile, the asset management side of the business was flourishing. In October 2000, Alliance Capital acquired Sanford C. Bernstein. Alliance Capital's growth equity and corporate fixed-income investing, and its family of retail mutual funds, accompanied Bernstein's value equity and tax-exempt fixed-income management and its private-client business. This combination created AllianceBernstein, merging growth and value investing philosophies under one roof—a rare achievement in an industry often divided by investment theology.

The integration wasn't without challenges. Bernstein's analysts, famous for their contrarian research and refusal to chase investment banking business, initially clashed with Alliance's more traditional approach. But AXA's management wisely kept the cultures separate where it mattered—research independence—while combining back-office operations for efficiency. The result was a powerhouse that could serve everyone from pension funds to ultra-high-net-worth individuals.

Group retirement became another growth engine. AXA Equitable methodically built relationships with America's corporations, becoming the retirement plan provider for thousands of companies. By focusing on mid-market firms often ignored by larger competitors, the company found a profitable niche. The technology investments made during this period—automated enrollment, mobile apps for participants, sophisticated modeling tools for plan sponsors—positioned the company as an innovator in a traditionally stodgy market.

The financial crisis of 2008 tested these innovations. While competitors collapsed or required government bailouts, AXA Equitable remained stable, supported by its French parent's strong balance sheet and the diversification strategy implemented over the previous decade. The company actually gained market share during the crisis, as customers fled weaker competitors for the perceived safety of AXA's global backing.

By 2017, AXA Equitable had become a juggernaut. By 2003, AXA Equitable Insurance Company was the leading carrier in the world with more than 50 million clients, in more than 50 countries, and with nearly a trillion dollars in client assets. The company had successfully navigated the transition from traditional life insurance to modern financial services, from American mutual to global subsidiary. But change was coming again—this time from Europe, where new solvency regulations would force AXA to make a choice that would reshape Equitable's destiny once more.

VI. The Spinoff: Independence at Last (2018–2020)

Thomas Buberl, AXA's CEO, stood before investors in Paris on November 28, 2017, and dropped a bombshell. "We are announcing our intention to IPO our U.S. operations," he said, his measured tone belying the magnitude of the decision. The room erupted in questions. Why would AXA divest its crown jewel American operation after 27 years of investment?

The answer lay in the arcane world of European insurance regulation. Solvency II, the EU's regulatory framework implemented in 2016, required insurers to hold significantly more capital against long-term guarantees and market risks—exactly the kind of products that dominated AXA Equitable's portfolio. By 2018, AXA, facing tougher European solvency laws, decided to re-balance its operations from life and annuities and towards property and casualty – from financial risks to insurance risks.

For AXA's European regulators, American variable annuities with their long-term guarantees looked dangerously capital-intensive. Every dollar of premium sold in New York required euros of capital held in Paris. Buberl faced a stark choice: either dramatically shrink the U.S. life and annuity business or spin it off. He chose independence for Equitable.

The IPO process was a masterclass in financial engineering. In May 2018, AXA announced the successful completion of the IPO of AXA Equitable Holdings, raising $2.75 billion on the sale of 24.5% of the outstanding shares. Additionally, the company announced an issuance of $750 million of bonds mandatorily exchangeable into shares of AXA Equitable Holdings stock. And finally, $502 million of options were exercised, bringing the total to $4.02 billion in proceeds to AXA.

Mark Pearson, who had led AXA Equitable since 2011, faced the challenge of his career. He had to convince investors that a company that had been French-owned for nearly three decades could thrive as an independent American entity. His pitch was compelling: Equitable would be nimble, focused on the U.S. market, and free to pursue strategies that might not align with a European parent's priorities.

The roadshow was grueling. Pearson and his team visited over 100 institutional investors in two weeks, flying from New York to Boston to London to Frankfurt and back. They faced skeptical questions: Could Equitable maintain its credit rating without AXA's backing? Would distribution partners remain loyal? How would the company fund growth without access to AXA's balance sheet?

Trading began on May 10, 2018, under the ticker symbol "EQH." The stock opened at $20 per share, exactly at the IPO price—neither a pop nor a flop, but a validation of the bankers' pricing. AXA retained 59.5% ownership after the IPO, but the path to full independence was set.

On March 25, 2019, AXA announced the successful completion of a secondary common stock offering of 40 million shares of AXA Equitable Holdings, Inc. This secondary offering reduced AXA's stake to 48.3%, crossing the crucial 50% threshold that gave Equitable true operational independence.

The final act came swiftly. On November 7, 2019, AXA announced the sale of its remaining stake in AXA Equitable Holdings (EQH), selling 144 million shares of common stock to Goldman Sachs, which was the sole underwriter for the public offering of the shares. The expected close date was stated by the company at the time as November 13, 2019. This brought to a close a long and largely successful chapter in Equitable's history – the end of the AXA Group ownership of the company.

Goldman Sachs executed the block trade brilliantly, placing the shares with institutional investors overnight at $22.50 per share, a modest discount to the closing price. By morning, AXA's 28-year ownership of Equitable was over. The French had made a spectacular return on their 1991 rescue investment, and Equitable was free to chart its own course.

But freedom required a new identity. The AXA brand, which had defined the company for 15 years, would have to go. On January 14, 2020, Equitable unveiled its new branding. The company dropped "AXA" from its name, becoming simply Equitable Holdings, Inc. The logo returned to a modernized version of the classical imagery that had defined the company since 1859—the goddess Athena, symbol of wisdom and strategy.

The rebranding was more than cosmetic. It was a declaration of independence and a return to American roots. Employee surveys showed overwhelming support for the change. "We're not the French subsidiary anymore," one veteran executive said. "We're Equitable again—the company that Henry Hyde founded."

The timing of independence proved fortuitous. Just two months after the rebrand, COVID-19 struck. As an independent company, Equitable could respond quickly without seeking approval from Paris. The company shifted to remote work in 48 hours, accelerated digital initiatives, and provided emergency support to policyholders affected by the pandemic.

The spinoff had transformed Equitable from a subsidiary constrained by European regulations into an agile, independent American financial services leader. The company that had nearly collapsed in 1991, been rescued by the French, and spent 28 years as part of a global conglomerate had come full circle. It was American-owned again, publicly traded, and free to pursue its destiny. The only question now was: what would Equitable do with its newfound freedom?

VII. Modern Era: The Diversified Financial Services Platform (2020–Present)

The executive team gathered in Equitable's Jersey City headquarters on a crisp September morning in 2023. CEO Mark Pearson looked out at the Manhattan skyline—the same view Henry Hyde might have seen 164 years earlier—and laid out a bold vision: "We're not just an insurance company anymore. We're America's premier retirement security platform."

The numbers backed his ambition. Equitable Holdings had evolved into a sophisticated financial services ecosystem with five distinct but synergistic business lines: Individual Retirement, Group Retirement, Protection Solutions, Wealth Management, and crucially, a 65% ownership stake in AllianceBernstein that generated consistent fee income and provided captive asset management capabilities. In 2024, Equitable made a strategic move to deepen this relationship: spending $761 million to increase AllianceBernstein stake to 68.6%. The purchase, completed through a tender offer at $38.50 per unit, represented approximately 17.9% of AllianceBernstein's outstanding units. This wasn't just financial engineering—it was a statement about Equitable's commitment to the asset management business and its belief in the synergies between insurance and investment management. AllianceBernstein itself had been transforming under Equitable's ownership. In 2022, AllianceBernstein's acquisition of CarVal Investors for $750 million brought $14.3 billion in AUM focused on opportunistic and distressed credit, renewable energy infrastructure, specialty finance and transportation investments. This pushed AB's private markets platform to $50 billion in AUM, creating new fee streams and diversifying revenue sources. The deal exemplified the synergies between Equitable and AllianceBernstein—Equitable committed to deploy $10 billion from its General Account toward AB's Private Alternatives platform, with $750 million allocated to CarVal strategies.

The modern Equitable operates with a sophistication that would astonish Henry Hyde. The Individual Retirement business leverages behavioral economics and digital tools to help Americans save. The Protection Solutions division uses AI-powered underwriting to provide life insurance in minutes, not weeks. The Wealth Management arm serves ultra-high-net-worth clients with strategies that blend insurance, investments, and estate planning.

Technology transformation accelerated post-independence. The company launched digital platforms that allowed customers to buy annuities entirely online—unthinkable just a decade ago. Machine learning algorithms now predict which customers are most likely to lapse their policies, enabling proactive intervention. Virtual reality training programs prepare financial advisors for complex client conversations. The financial performance validates this multi-pronged strategy. Operating earnings consistently exceeded $600 million per quarter in 2024, with full year Non-GAAP operating earnings of $2.0 billion, or $5.93 per share. The company generated $1.5 billion in cash in 2024, with expectations to increase to $1.6-1.7 billion in 2025. Record assets under management and administration of $1.0 trillion, up 20% year-over-year, demonstrate the power of the integrated model.

But perhaps the most impressive achievement is the cultural transformation. The company that was once a traditional life insurer, then a French subsidiary, has become a uniquely American financial services innovator. Employees describe a culture that combines startup agility with institutional gravitas. The Jersey City headquarters buzzes with energy that feels more Silicon Valley than Wall Street.

The retirement opportunity ahead is massive. With 10,000 Americans turning 65 every day through 2030, the addressable market for Equitable's products expands daily. The company estimates the U.S. retirement savings gap at $4 trillion—a problem that represents both a societal challenge and a business opportunity.

Digital transformation continues at breakneck pace. The company is experimenting with blockchain for policy administration, testing robo-advisors for retirement planning, and using natural language processing to improve customer service. Yet it maintains the human touch through its network of financial professionals who provide the empathy and judgment that algorithms cannot.

The competitive landscape has intensified. Traditional insurers like MetLife and Prudential are reinventing themselves. Tech giants eye the financial services space hungrily. New fintech startups promise to disrupt everything. But Equitable's unique combination of heritage, scale, product innovation, and distribution gives it advantages that are hard to replicate.

Risk management, learned through centuries of experience and recent near-death encounters, remains paramount. The company maintains disciplined underwriting, sophisticated hedging strategies, and a diversified business model that can weather various economic scenarios. The Legacy segment—old policies with challenging economics—continues to wind down systematically, freeing capital for growth investments.

As 2025 unfolds, Equitable Holdings stands at an inflection point. It has the freedom to chart its own course, the financial strength to invest in growth, and the market opportunity of a generation. The company that Henry Hyde founded with $100,000 now manages over $1 trillion, but in many ways, its story is just beginning.

VIII. Business Model & Strategic Playbook

In the bowels of Equitable's Jersey City headquarters, there's a room that few outsiders ever see. It's called the "War Room," though officially it's the Strategic Planning Center. Giant screens display real-time data: interest rate curves, competitor pricing, demographic heat maps, distribution metrics. This is where Equitable's three-pillar strategy—Protection, Retirement, and Asset Management—comes to life through thousands of daily decisions that collectively determine the company's fate.

"Most people think insurance is about selling policies," explains the head of strategy, a former McKinsey partner who joined after the spinoff. "That's like saying Amazon is about shipping boxes. What we really do is financial engineering at massive scale."

The Protection pillar isn't your grandfather's life insurance business. Modern protection products blend insurance with wealth transfer, tax optimization, and estate planning. A typical Equitable client might buy a variable universal life policy not primarily for the death benefit, but as a tax-advantaged investment vehicle that can fund retirement, provide liquidity for estate taxes, and transfer wealth across generations. The margins are attractive—often 15-20% returns on capital—and the relationships are sticky, lasting decades.

The Retirement pillar represents the company's growth engine. Here, Equitable leverages its pioneering position in buffered annuities to capture market share in the massive retirement wave. The brilliance of the buffered annuity model lies in its risk transfer mechanism. Customers accept capped upside in exchange for downside protection—say, they'll participate in market gains up to 10% but are protected from the first 10-20% of losses. This allows Equitable to hedge efficiently using options strategies, generating consistent spreads regardless of market direction.

But the real magic happens in the Asset Management pillar through AllianceBernstein. This isn't just about the 68.6% ownership stake generating dividend income. It's about the symbiotic relationship where AB manages assets for Equitable's insurance portfolios, Equitable provides seed capital for new AB strategies, and both entities cross-sell to each other's clients. When an Equitable annuity customer's assets grow, AB's fees increase. When AB launches a new private credit fund, Equitable's General Account provides anchor investment.

The capital-light transformation deserves special attention. Traditional life insurance requires massive capital reserves—every dollar of premium might require 10-15 cents of capital support. But Equitable has systematically shifted toward fee-based products. Investment-only variable annuities, asset management fees, advisory services—these generate returns on capital exceeding 30% with minimal capital requirements.

The Legacy segment wind-down is a masterclass in financial engineering. These are old policies—some dating to the 1980s—with guaranteed rates that seemed reasonable then but are underwater now. Rather than letting them drain capital indefinitely, Equitable actively manages this block: offering buyouts to policyholders, reinsuring blocks to specialty insurers, and using sophisticated hedging to minimize economic volatility. The segment shrinks by roughly 8-10% annually, freeing $200-300 million in capital each year for redeployment.

Distribution strategy reflects modern consumer behavior. The multi-channel approach includes: (1) Equitable Advisors, the proprietary channel with 4,600 financial professionals who know the products intimately; (2) third-party channels including wirehouses, independent broker-dealers, and banks that provide scale; (3) digital direct-to-consumer platforms for simple products; and (4) workplace benefits channels accessing 40 million American workers.

Each channel requires different economics and support models. Proprietary advisors receive higher compensation but deliver better persistency and cross-sell rates. Third-party channels provide volume but require competitive pricing. Digital channels have low acquisition costs but higher lapse rates. The art lies in optimizing the mix.

Risk management philosophy permeates everything. Unlike 1991 when concentrated real estate bets nearly killed the company, today's Equitable maintains strict limits: no single asset class exceeds 15% of the General Account, no single counterparty exposure exceeds $500 million, and stress testing assumes 2008-style market dislocations happening simultaneously across all asset classes.

The hedging program alone employs 50 quantitative analysts who manage $150 billion in notional derivatives exposure. They don't try to predict markets; they systematically hedge tail risks. When markets crashed in March 2020, Equitable's hedges performed exactly as designed, generating $2 billion in gains that offset portfolio losses.

Capital allocation follows a clear hierarchy: (1) maintain AA- financial strength ratings requiring roughly $11 billion in capital; (2) fund organic growth in Retirement and Protection where returns exceed 15%; (3) pursue bolt-on acquisitions in asset management and distribution; (4) return excess capital to shareholders through dividends and buybacks. This discipline means saying no to exciting but marginal opportunities—a cultural shift from the go-go years that preceded the 1991 crisis.

The technology stack powering all this is surprisingly modern for a 165-year-old company. Core systems run on cloud infrastructure allowing real-time scaling. APIs connect to hundreds of distribution partners. Machine learning models continuously optimize pricing, underwriting, and customer service. Yet legacy systems dating to the 1970s still process certain policy blocks—a reminder that in insurance, the past is never truly past.

Competitive advantages compound over time. Brand trust built over 165 years can't be replicated by a startup. Actuarial data covering millions of lives over decades provides underwriting insights competitors lack. Distribution relationships cultivated over generations create switching costs. The AllianceBernstein engine generates capital for growth while competitors must access expensive external funding.

The strategic playbook isn't static. Management constantly tests new models: partnering with insurtechs for digital distribution, exploring embedded insurance through major retailers, experimenting with parametric products that pay automatically when triggering events occur. Some will fail—that's expected. But the winners will define the next chapter of growth.

As one board member observed: "Insurance looks boring from the outside—premiums come in, claims go out. But inside, it's one of the most complex businesses on Earth. You're simultaneously running a hedge fund, a tech company, a distribution network, and a risk management operation. Getting all those pieces to work together—that's the art."

IX. Financial Analysis & Investment Case

The investment case for Equitable Holdings reads like a financial engineer's dream: a company trading at 7-8x forward earnings despite generating 15%+ returns on equity, with massive secular tailwinds and multiple expansion potential. Yet the stock languishes, misunderstood by a market that still sees "insurance" and reflexively assigns a conglomerate discount.

Let's start with valuation. As of late 2024, Equitable trades at approximately 0.7x book value excluding AOCI, compared to peers like Prudential at 0.9x and MetLife at 1.1x. On a P/E basis, Equitable's 7-8x multiple compares to the S&P 500 at 20x and financial services peers at 12-15x. The discount partially reflects the Legacy block overhang, but even adjusting for this, the valuation appears compelling.

The company's earnings power is undeniable. Operating earnings consistently exceeded $600 million per quarter in 2024. Cash generation of $1.5 billion annually provides ample firepower for growth investment and shareholder returns. The 60-70% payout ratio balances growth reinvestment with returning capital to shareholders who've been patient through the transformation.

The bull case rests on several pillars. First, demographics are destiny. With 4.1 million Americans turning 65 annually and the retirement savings gap at $4 trillion, demand for Equitable's products will grow regardless of economic cycles. Second, the buffered annuity market where Equitable pioneered and maintains leadership is growing 20%+ annually as advisors discover these products solve the sequence-of-returns risk that terrifies near-retirees.

Third, AllianceBernstein's transformation is underappreciated. Active management has been declared dead repeatedly, yet AB's assets under management grew to $740 billion with improving margins. The private alternatives platform, bolstered by the CarVal acquisition, positions AB to capture allocations as institutions shift from public to private markets. If AB were standalone, it might trade at 15x earnings; Equitable's 68.6% stake is worth $8-10 billion alone.

Fourth, capital efficiency continues improving. The shift from capital-intensive guaranteed products to capital-light fee businesses means each dollar of earnings requires less capital support, enabling higher returns and more cash generation. As the Legacy block runs off—declining from $50 billion to potentially $20 billion by 2030—billions in trapped capital will be released.

The bear case has merit too. Interest rate sensitivity remains real despite hedging. A Japan-style scenario of prolonged zero rates would pressure spread income and require product repricing. The Federal Reserve's actions ripple through every aspect of the business from investment yields to policyholder behavior.

Regulatory risk looms large. The Department of Labor's fiduciary rule variations create compliance complexity and could limit distribution. State insurance regulators increasingly scrutinize product features and illustrations. Federal proposals for retirement security could help (mandatory auto-enrollment) or hurt (government-provided annuities) depending on implementation.

Competition intensifies from every angle. Traditional insurers like Prudential and MetLife have awoken from their slumber. Private equity-backed insurers like Athene compete aggressively on price. Technology companies eye the trillion-dollar retirement market hungrily. Even Vanguard and Fidelity, traditionally focused on accumulation, now offer retirement income solutions.

Legacy block exposure, while declining, remains substantial. These policies with guaranteed minimum benefits from the 1990s and 2000s are essentially short options positions—fine in normal markets but potentially explosive in tail scenarios. Management has hedged aggressively, but hedges can fail when correlations break down, as Long-Term Capital Management learned fatally.

The ESG angle cuts both ways. Positively, Equitable's products enable retirement security—a social good. The company's commitment to sustainable investing through AllianceBernstein attracts ESG-focused allocators. Diversity initiatives have made Equitable a employer of choice. But life insurance faces ESG headwinds: climate change increases mortality volatility, social inflation drives claim costs, and governance scrutiny intensifies around executive compensation and product suitability.

Relative to peers, Equitable offers a unique profile. MetLife provides more international diversification but lower growth. Prudential has a strong brand but challenged business mix. Principal Financial offers pure-play retirement exposure but lacks Equitable's asset management engine. Lincoln National trades cheaper but faces capital constraints. Only Equitable combines growth, capital generation, and strategic flexibility.

The investment case ultimately depends on time horizon. Short-term traders face a complex story with quarterly volatility from markets, hedging, and actuarial adjustments. But long-term investors see a transformation story: a company shedding its past constraints, capitalizing on secular growth trends, and compounding capital at attractive returns.

One astute analyst summarized: "The market treats Equitable like a melting ice cube—a legacy insurer managing decline. But look closer and you see a growth company hidden in plain sight. The retirement wave isn't a forecast; it's happening now. The only question is whether Equitable or someone else captures the opportunity."

Wall Street coverage reflects this dichotomy. Bulls see 50%+ upside as the market recognizes Equitable's transformation. Bears worry about the next financial crisis exposing hidden risks. The consensus sits uncomfortably in between—acknowledging the opportunity but uncertain about execution.

For fundamental investors, Equitable offers an asymmetric proposition: downside protected by book value and cash generation, upside driven by multiple expansion as the transformation becomes undeniable. It's not without risk—no financial services investment is—but for those willing to dig deeper than surface metrics, the risk/reward appears compelling.

X. Lessons & Legacy

Standing in the lobby of Equitable's headquarters, you're confronted by a bronze statue of Henry Baldwin Hyde, the company's founder. His stern gaze seems to ask each passing employee: "What have you built that will last 165 years?" It's a question that captures the central tension of Equitable's story—how to honor permanence while embracing change.

The art of corporate reinvention might be Equitable's greatest lesson. Most companies die rather than transform. Kodak couldn't pivot from film to digital. Blockbuster couldn't evolve from stores to streaming. But Equitable has reinvented itself repeatedly: from mutual to stock company, from American to French-owned and back, from traditional insurer to diversified financial services. Each transformation required abandoning comfortable identities for uncertain futures.

The 1991 crisis teaches the perils of concentration risk. Equitable nearly died because it made a simple bet—that real estate would keep rising—with complex instruments. The guaranteed investment contracts that seemed so clever in the 1980s became poison when property values collapsed. Today's risk managers at Equitable study that period obsessively, knowing that the next crisis will come from wherever they're not looking.

The value of patient capital emerges clearly from AXA's 28-year ownership. American capitalism often demands quarterly results, but building enduring value requires decade-long perspectives. AXA invested $1 billion in 1991 and extracted perhaps $10 billion in value by 2019—not through financial engineering but through steady building. They provided capital when Equitable needed it, expertise when markets evolved, and patience when transformation took longer than expected.

Building trust over 165 years creates a moat that no amount of venture capital can replicate. When a widow receives a death benefit check within 48 hours of her husband's passing—as Equitable promises—she tells her children. When those children need retirement planning decades later, they remember. This trust compounds across generations, creating customer acquisition costs that approach zero for certain segments.

The insurance industry offers broader lessons about innovation. Insurance seems stodgy—actuaries calculating mortality tables—but it's actually been radically innovative. Life insurance enabled the industrial revolution by allowing entrepreneurs to leverage human capital. Annuities are solving the retirement crisis by converting assets into income. The next innovations might involve longevity risk, climate adaptation, or risks we can't yet imagine.

Crisis management lessons from Equitable's history could fill business school cases. In 1905, James Hazen Hyde faced a coordinated boardroom coup and survived through tactical brilliance before ultimately accepting defeat. In 1991, management swallowed pride and accepted French ownership rather than risk policyholder security. In 2008, disciplined risk management meant Equitable avoided the disasters that befell AIG. Each crisis required different responses, but all demanded choosing long-term survival over short-term face-saving.

The importance of culture during transformation cannot be overstated. When AXA acquired Equitable, two proud cultures could have clashed destructively. Instead, leadership fostered mutual respect—Americans learned French precision, French learned American entrepreneurialism. When independence came in 2020, employees felt liberated rather than abandoned because cultural identity had been preserved through the transition.

Equitable's journey illuminates the evolution of American capitalism. The company Henry Hyde founded served individual families protecting against premature death. Today's Equitable serves institutional investors, provides retirement security for millions, and manages assets for sovereign wealth funds. This isn't mission creep—it's capitalism responding to society's evolving needs.

The demographic megatrend driving Equitable's future—population aging—offers lessons beyond insurance. Every industry must grapple with changing demographics: healthcare systems treating chronic diseases rather than acute injuries, real estate developers building senior housing rather than starter homes, technology companies designing for accessibility rather than just innovation. Equitable's strategic positioning for the silver tsunami provides a template.

Technology disruption in financial services follows patterns Equitable has navigated before. When computers arrived in the 1960s, Equitable was among the first insurers to digitize policy administration. When the internet emerged in the 1990s, Equitable launched online services while competitors hesitated. Today's AI revolution finds Equitable again at the forefront, using machine learning for underwriting and robo-advisors for wealth management. The lesson: embrace technology early or become its victim.

Regulatory adaptation showcases another eternal truth: financial services is ultimately a permission-based business. You need licenses to operate, approval for products, and consent for transactions. Equitable has survived by working with regulators rather than against them—even when regulations like Solvency II forced painful strategic changes. Companies that fight regulators typically lose; those that adapt typically survive.

The interplay between Main Street and Wall Street reveals itself through Equitable's story. The company raises capital from Wall Street (institutional investors buying stocks and bonds) to serve Main Street (families buying insurance and annuities). When this circular flow works, both prosper. When it breaks—as in 1991 or 2008—both suffer. Equitable's role as intermediary between these worlds carries both privilege and responsibility.

Leadership transitions offer their own lessons. From Hyde to his son to professional managers to French executives and back to American leadership, Equitable has experienced every permutation. The successful transitions shared common elements: respect for heritage while embracing change, clear strategic vision, and patience during adjustment periods. Failed transitions—like the 1905 scandal—featured ego, impatience, and disrespect for stakeholders.

Finally, Equitable's story teaches that corporate longevity requires constant reinvention within unchanging principles. The principle—helping people achieve financial security—hasn't changed since 1859. But everything else has: products, distribution, technology, ownership, regulation. Companies that confuse means with ends, tactics with strategy, die. Those that remain faithful to purpose while radically adapting methods endure.

As one longtime employee reflected while retiring after 40 years: "I worked for the same company my entire career, but it was actually five different companies. That's the secret—staying the same by constantly changing."

XI. Epilogue & Forward Look

The conference room on the 30th floor of Equitable's headquarters offers a panoramic view of Manhattan—you can see from the Statue of Liberty to the George Washington Bridge. It's here, in early 2025, that the executive team gathers monthly to discuss what they call "Project Longevity"—not a single initiative but a comprehensive vision for Equitable's next chapter.

"By 2030, there will be more Americans over 65 than under 18 for the first time in history," the Chief Strategy Officer begins, clicking through slides that would terrify most but energize this room. "This isn't a demographic trend—it's a complete societal reorganization."

The numbers are staggering. Ten thousand Americans turn 65 daily, a pace that continues through 2030. Life expectancy at 65 has increased by five years since Equitable was founded. A 65-year-old today has a 50% chance of living to 85, a 25% chance of reaching 92. The traditional three-stage life—education, work, retirement—is dissolving into something more fluid. People are working longer, retiring gradually, and facing 30-year retirements that their parents' 10-year retirements never contemplated.

For Equitable, this represents the opportunity of the century. The company's actuaries estimate Americans need $50 trillion in retirement assets to maintain their living standards—they have $30 trillion. That $20 trillion gap isn't just a statistic; it represents millions of individual anxieties about outliving savings, paying for healthcare, leaving legacies.

Technology disruption accelerates these changes. Artificial intelligence is already transforming underwriting—what once took weeks now takes minutes. Equitable's AI models analyze thousands of variables from credit scores to exercise patterns, enabling personalized pricing that wasn't possible even five years ago. But the real revolution comes from behavioral AI that can predict when customers might lapse policies, need service, or be receptive to new products.

Blockchain technology, still experimental, could revolutionize policy administration. Imagine smart contracts that automatically pay claims when triggering conditions are met—no paperwork, no delays, no disputes. Equitable is running pilots with three blockchain platforms, preparing for a future where insurance becomes embedded and invisible.

Climate change represents both risk and opportunity. As physical risks increase—floods, fires, hurricanes—traditional property insurance becomes untenable in certain geographies. But this creates demand for new products: parametric insurance that pays automatically when wind speeds exceed thresholds, resilience bonds that fund adaptation, migration insurance for climate refugees. Equitable's innovation lab is designing products for risks that didn't exist a decade ago.

The competitive landscape will look radically different by 2030. Technology giants like Apple and Google have the customer relationships and data to enter financial services at scale. Chinese insurers like Ping An demonstrate what's possible when technology-first thinking meets insurance. Private equity-backed insurgents continue rolling up smaller players and competing aggressively on price.

But Equitable's leadership sees opportunity in disruption. "Every new entrant validates the market opportunity," the CEO argues. "And most underestimate the complexity of insurance. It's not just about having an app or offering low prices. It's about being there, reliably, for decades."

The next acquisition targets are already being evaluated. Small technology companies that could accelerate digital transformation. Boutique asset managers that add capabilities to AllianceBernstein. Distribution firms that provide access to new customer segments. The company has $2 billion in excess capital and the discipline to wait for the right opportunities.

Strategic priorities for the next five years are clear. First, become the premier provider of protected retirement solutions, capturing disproportionate share of the retirement wave. Second, transform AllianceBernstein into a $1 trillion asset manager through organic growth and acquisitions. Third, digitize the entire customer experience while maintaining human advisors for complex needs. Fourth, build new businesses in adjacent spaces like long-term care, longevity insurance, and retirement communities.

Regulatory changes could accelerate or impede these plans. Proposed federal legislation mandating auto-enrollment in retirement plans would add millions of customers. Social Security reform might increase demand for private solutions. But aggressive regulation of fees, products, or distribution could constrain growth. Equitable maintains a 20-person government affairs team in Washington, knowing that policy shapes possibility.

Management changes loom as well. CEO Mark Pearson, who led the company through the AXA spinoff and independence, approaches traditional retirement age. The board has begun succession planning, seeking leaders who combine insurance expertise with technology fluency and growth mindset. Internal candidates are being groomed, but external searches haven't been ruled out.

The cultural evolution continues. Equitable is hiring engineers from Silicon Valley, data scientists from universities, designers from creative agencies. The average age of employees has dropped by five years since 2020. The headquarters, once formal and hierarchical, now features open workspaces, meditation rooms, and a startup-style cafeteria. Yet the company maintains deep reservoirs of institutional knowledge—actuaries with 30-year tenures who've seen every market cycle.

International expansion, dormant since the AXA era, is being reconsidered. Not through acquisitions or subsidiaries, but through partnerships and technology licensing. Equitable's buffered annuity technology could be licensed to insurers in Europe and Asia facing similar retirement challenges. AllianceBernstein already operates globally, providing a platform for coordinated expansion.

Environmental and social considerations increasingly shape strategy. Equitable has committed to net-zero emissions by 2050, requiring fundamental changes in investment portfolios and operations. Diversity initiatives aim for 50% female and 30% minority leadership by 2030. Products are being designed for underserved communities that traditional insurance has ignored.

The vision is ambitious but achievable: By 2035, Equitable aims to serve 10 million Americans directly, manage $2 trillion in assets, and generate $3 billion in annual earnings. This would make it one of the five largest financial services companies in America, a remarkable achievement for a company that nearly died in 1991.

But perhaps the most profound change is philosophical. Equitable no longer sees itself as just an insurance company that happens to offer investments and advice. It's positioning as a longevity company—helping people not just live longer but live better. This means products that adapt as lives evolve, services that anticipate needs, and relationships that span generations.

As the strategy session concludes, the CEO offers a final thought: "Henry Hyde founded this company to solve the problems of his era—premature death leaving families destitute. We're solving the problems of our era—extended life requiring financial security for decades. The mission hasn't changed, just the methods."

Looking out at Manhattan's skyline, where Equitable has operated for 165 years, the future seems both uncertain and exciting. Challenges abound—technological disruption, regulatory scrutiny, competitive pressure, demographic shifts. But so do opportunities—trillions in retirement assets seeking homes, millions of Americans needing guidance, and technologies enabling solutions previously impossible.

The story of Equitable Holdings is far from over. In many ways, it's just beginning.

XII. Recent News

The latest developments at Equitable Holdings paint a picture of sustained momentum and strategic execution. Full year 2024 results showed robust growth with record net inflows of $7.1 billion in Retirement, $4.0 billion in Wealth Management and active net inflows of $4.3 billion in Asset Management. Net income reached $1.3 billion, or $3.78 per share for the full year, with fourth quarter net income of $899 million, or $2.76 per share.

Cash generation of $1.5 billion in 2024 is expected to increase to $1.6-1.7 billion in 2025. The company returned $1.3 billion to shareholders during the year, maintaining its 60-70% payout ratio target. Full year Non-GAAP operating earnings per share of $5.93 increased 29% from 2023.

Looking ahead, the company is on track to close its life reinsurance transaction with RGA mid-2025, which will free over $2 billion in capital. In April 2025, Equitable increased its ownership in AllianceBernstein to 69% through a $760 million unit purchase. The company plans an additional $500 million share repurchase post-RGA transaction closure.

Leadership changes continue to strengthen the organization. Jim Kais was appointed as the Head of Group Retirement business, effective April 1, 2024, reporting to Nick Lane, President of Equitable, and joining the company's Operating Committee. Kais succeeds Jessica Baehr, who was recently named President of Equitable Investment Management.

The wealth management business continues attracting top talent, with multiple teams of experienced financial advisors joining Equitable Advisors throughout 2024, bringing decades of experience and established client relationships from major wirehouses and independent firms.

In a notable development, Octane, a fintech company specializing in recreational purchases financing, secured a $700 million forward-flow facility with three major insurance partners: New York Life ($350 million), MetLife Investment Management ($200 million), and Equitable ($150 million). The agreement will fund fixed-rate installment powersports loans originated by Octane's in-house lender, following Octane's strong performance in 2024 with 36% year-over-year growth in originations.

Equitable Holdings now has $1 trillion in assets under management and administration (as of 12/31/2024) and more than 5 million client relationships globally. Founded in 1859, Equitable provides retirement and protection strategies to individuals, families and small businesses. AllianceBernstein is a global investment management firm that offers diversified investment services to institutional investors, individuals and private wealth clients. Equitable Advisors has 4,600 duly registered and licensed financial professionals that provide financial planning, wealth management, retirement planning, protection and risk management services to clients across the country.

Management's confidence in the business is evident in their 2027 financial targets, which remain on track. The company continues to benefit from favorable demographic trends, with strong demand for retirement and protection products driving organic growth across all business segments.

XIII. Links & Resources

For those seeking to dive deeper into Equitable Holdings' story and current operations, the following resources provide valuable information:

Company Resources: - Investor Relations: ir.equitableholdings.com - Annual Reports and SEC Filings: Available through the investor relations portal - Quarterly Earnings Presentations: Updated following each earnings release - Corporate Website: equitable.com - AllianceBernstein: alliancebernstein.com

Historical Archives: - Baker Library Historical Collections at Harvard Business School maintains extensive Equitable Life Assurance Society records from 1782-1919 - The Museum of American Finance features exhibits on early American insurance including Equitable artifacts - New York Historical Society archives contain materials related to the 1905 Hyde Ball scandal

Regulatory Filings: - SEC EDGAR Database: All public filings including 10-K, 10-Q, and proxy statements - New York State Department of Financial Services: Insurance company regulatory filings - NAIC (National Association of Insurance Commissioners): Industry-wide data and company reports

Industry Research: - LIMRA: Life insurance industry research and benchmarking data - Insurance Information Institute: Industry statistics and trend analysis - A.M. Best: Credit ratings and insurance industry analysis - Society of Actuaries: Research on mortality, longevity, and retirement trends

Books on Insurance History: - "The Equitable Life Assurance Society of the United States: 1859-1964" by R. Carlyle Buley - "After the Ball: Gilded Age Secrets, Boardroom Betrayals, and the Party That Ignited the Great Wall Street Scandal of 1905" by Patricia Beard - "Tontines: From the Reign of Louis XIV to the French Revolutionary Era" by Robert M. Jennings and Andrew P. Trout

Academic Research: - NBER Working Papers on insurance markets and retirement security - Wharton Pension Research Council publications - Journal of Risk and Insurance archives

Investment Research: - Sell-side analyst reports (available through brokerage platforms) - Morningstar analysis and ratings - Value Line Investment Survey coverage

Industry Associations: - American Council of Life Insurers (ACLI) - Insured Retirement Institute (IRI) - National Association of Insurance and Financial Advisors (NAIFA)

These resources offer multiple perspectives on Equitable Holdings—from its historical roots to current strategic positioning—enabling investors, researchers, and industry observers to develop a comprehensive understanding of this remarkable company's evolution and future prospects.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube