Enterprise Products Partners: The $70 Billion Pipeline Empire That America Runs On

I. Introduction & Opening Story

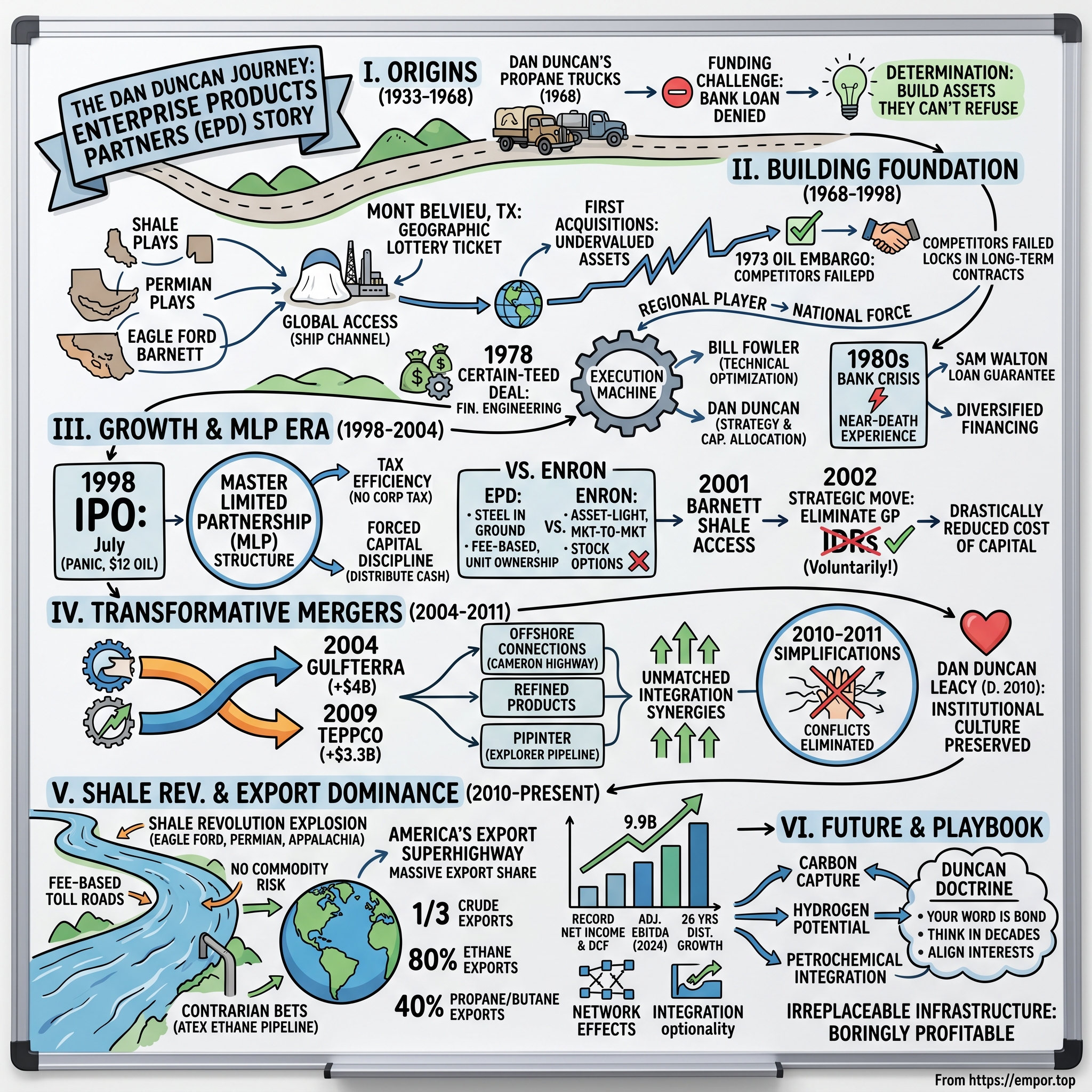

Picture this: March 1968, Houston, Texas. A 35-year-old Dan Duncan sits across from his wife in their modest kitchen, two propane delivery trucks parked outside—his entire net worth on wheels. He's just quit his executive position at Wanda Petroleum with $10,000 in savings and a radical idea: build an asset-based midstream company when everyone else is just trading commodities. His friends think he's lost his mind. The oil majors dominate energy infrastructure. Independent operators are getting crushed left and right.

Fast forward to today: Enterprise Products Partners commands a $70 billion market capitalization, operates 50,000 miles of pipelines—enough to circle the Earth twice—and generates over $2 billion in quarterly distributable cash flow. The company moves one-third of America's crude oil exports, 80% of its ethane exports, and touches virtually every molecule of natural gas liquids that powers American industry. It's the invisible giant that keeps America's energy economy humming, yet most investors have never heard Dan Duncan's name.

How did two propane trucks become the backbone of American energy infrastructure? How did a company founded on delivering fuel to rural Texas farms end up controlling the commanding heights of U.S. energy exports? And perhaps most intriguingly—how did Duncan build a business model so resilient that it thrives whether oil is at $30 or $130 a barrel?

This is the story of Enterprise Products Partners—a masterclass in compound value creation, strategic positioning, and the power of owning irreplaceable infrastructure. It's about building when others are selling, integrating when others are specializing, and most importantly, understanding that in the energy business, the real money isn't in finding oil—it's in moving it.

The story unfolds across three distinct eras: First, the bootstrap years where Duncan built the foundation at Mont Belvieu, establishing what would become America's NGL pricing hub. Second, the financial engineering phase where Enterprise pioneered the MLP structure and executed transformative mergers that created today's integrated giant. And third, the shale revolution where Enterprise's strategic positioning paid off spectacularly, transforming America from energy importer to dominant exporter.

Along the way, we'll uncover the playbook Duncan created—one that his successors have executed flawlessly even after his death in 2010. It's a playbook about patient capital deployment, relationship-driven dealmaking, and the compound advantages of vertical integration in a fragmented industry. We'll see how Enterprise consistently stayed one step ahead of the market: eliminating IDRs before peers, pivoting to exports before the shale boom, and building infrastructure based on actual demand rather than speculation.

But this isn't just a historical exercise. As America grapples with energy transition, infrastructure investment, and geopolitical realignment, Enterprise's story offers crucial lessons. Can a fossil fuel infrastructure company adapt to a changing world? What happens when the molecules flowing through these pipes change from hydrocarbons to hydrogen? And is Enterprise's dominance a moat or a melting ice cube?

Buckle up. We're about to trace the path from two propane trucks to the pipeline empire that America literally runs on.

II. Origins: Dan Duncan's American Dream (1933-1968)

The office was sparse—a metal desk, two folding chairs, and a map of Texas pinned to fake wood paneling. Dan Duncan had been in business exactly three weeks when the bank called. They'd reviewed his loan application for expanding beyond those two propane trucks. The answer was no. Duncan hung up the phone, looked at that map, and made a decision that would define Enterprise forever: if banks wouldn't lend against promises, he'd build assets they couldn't refuse.

To understand that moment, you need to understand Duncan's childhood—a succession of losses that would crush most people but somehow forged titanium-strength determination. Born in 1933 in rural Shelby County, Texas, Duncan's early years read like a Steinbeck novel. His mother died of tuberculosis when he was seven. His brother died the same year. His father, struggling to raise two remaining sons alone while working as a farmer, succumbed to leukemia when Duncan was seventeen. By the time he graduated high school, Duncan was essentially alone in the world with nothing but a fierce work ethic and an equally fierce desire never to be vulnerable again.

Duncan did what tough Texas kids did in 1951—he became a roughneck, working the oil fields around Kilgore. The work was brutal: twelve-hour shifts in hundred-degree heat, handling drill pipe that could kill you if you looked away for a second. But Duncan noticed something. The real money wasn't in drilling holes—it was in what happened after oil came up. The midstream players—those moving, processing, and storing hydrocarbons—had steadier cash flows and better margins than either the wildcatters finding oil or the refiners turning it into gasoline.

After two years of saving every penny, Duncan enlisted in the Army, not out of patriotism but pragmatism—the G.I. Bill would pay for college. Posted to Korea during the war's aftermath, he spent nights in frozen bunkers reading business textbooks by flashlight. His squad mates thought he was crazy. Duncan was mapping out his future.

The G.I. Bill took him to Massey Business College in Houston, where he studied accounting—not because he loved numbers but because he understood that in business, "you can't manage what you can't measure." He graduated in 1957 and immediately joined Wanda Petroleum, a midstream company focused on natural gas liquids. This was where Duncan's real education began.

Wanda Petroleum was run by two brothers who treated business like a poker game—all bluff and leverage. They'd buy propane low, store it, and sell high. Pure trading. Duncan, starting as a trader, quickly rose to executive vice president by spotting opportunities others missed. While his bosses focused on price arbitrage, Duncan studied infrastructure. He mapped every pipeline, every storage cavern, every fractionation plant in Texas. He realized the real competitive advantage wasn't predicting prices—it was controlling the bottlenecks.

By 1967, Duncan was effectively running Wanda's operations, but he and the owners had fundamentally different visions. They wanted to trade paper; Duncan wanted to pour concrete. The breaking point came during a management meeting when Duncan proposed building a fractionation facility at Mont Belvieu. The owners killed it immediately—too capital intensive, too risky. Duncan saw it differently. Mont Belvieu sat atop massive underground salt domes perfect for hydrocarbon storage, connected to refineries on the Houston Ship Channel, with pipeline access to every major market. It was destiny disguised as geography.

The conversation that night with his wife Barbara was brief. "I'm starting my own company," Duncan said. "We'll mortgage everything." Barbara, who'd been with him since the roughneck days, simply asked, "When do we start?"

Duncan's departure from Wanda was professional but cold. He took no employees, no customers, no assets—just knowledge and relationships. His non-compete prevented him from trading NGLs for two years, so he'd start with retail propane delivery. It wasn't glamorous, but it generated cash flow. More importantly, it connected him directly with end users—farmers, rural businesses, small towns—who needed reliable supply more than cheap prices.

The company's founding philosophy came from Duncan's father, who despite limited education had unlimited wisdom: "Do the best you can every day." Duncan translated this into three business principles that would guide Enterprise forever: First, always tell the truth—your word is your bond. Second, treat people fairly—suppliers, customers, employees, everyone. Third, think long-term—build for decades, not quarters.

Enterprise Products Company incorporated in February 1968 with those two trucks, one employee (Duncan), and a radical idea: while competitors fought over trading margins, Duncan would build the infrastructure everyone else needed. He couldn't compete with majors on scale or traders on sophistication. But he could out-execute everyone on reliability.

The name "Enterprise" wasn't accidental. Duncan had served on the USS Enterprise during a naval reserve stint. But more than that, the word captured his vision—this would be an enterprise in the truest sense, a bold undertaking requiring courage, persistence, and systematic execution. As he told his first employee, hired three months after founding: "We're not building a company. We're building an institution."

Within weeks of starting, Duncan had identified his first target: a small propane storage facility near Mont Belvieu that was underutilized and undervalued. The owner wanted $75,000. Duncan had $10,000. The negotiation would test everything he believed about business—and set the template for every Enterprise deal to come.

III. Building the Foundation: Mont Belvieu & Early Growth (1968-1998)

The seller's office reeked of cigarette smoke and disappointment. Jim Bradley had inherited the propane storage facility from his father but had no interest in the energy business—he wanted to open a marina on Lake Conroe. Duncan sat across from him with $10,000 in the bank and a storage facility priced at $75,000 staring back at him. "I'll give you $15,000 down," Duncan said, "and the rest over seven years. But here's what I need—you finance it yourself, and I'll pay you prime plus two." Bradley laughed. "Son, why would I do that?" Duncan's response would become Enterprise lore: "Because in seven years, you'll wish you'd kept a piece of this."

Bradley took the deal. Within eleven months, Duncan had not only made every payment early but had expanded the facility's capacity by 40%. The Mont Belvieu complex—that geographic lottery ticket Duncan had identified at Wanda—was about to explode in strategic importance. Phillips Petroleum was building a massive NGL fractionation plant nearby. Exxon was expanding its chemical complex. Every major pipeline company was drawing routes that converged on this salt dome geography east of Houston. Duncan owned one of the few independent storage facilities in the middle of it all.

Mont Belvieu wasn't just a location—it was destiny manifesting as infrastructure. The salt domes, formed millions of years ago, created perfect underground storage caverns. You could solution-mine them—pump in water, dissolve salt, pump out brine—and create massive storage chambers that were essentially free once you paid for the drilling. The site connected to the Houston Ship Channel, giving access to global markets. It sat at the intersection of major pipeline systems from Eagle Ford, Permian, and Barnett shale formations (though shale's importance wouldn't be recognized for decades). Duncan saw what others missed: whoever controlled storage and processing at Mont Belvieu would effectively control NGL pricing for the entire Gulf Coast.

By 1970, Enterprise had grown from two trucks to a fleet of twenty, from one employee to thirty. But Duncan wasn't interested in building a trucking company. Every dollar of profit went into infrastructure. He bought depleted salt caverns when natural gas prices were low. He acquired struggling propane retailers and kept their storage assets while selling their trucks. He partnered with chemical companies to build dedicated pipelines, taking minority stakes that gave Enterprise exclusive operating rights.

The 1973 Arab oil embargo changed everything. Energy prices quadrupled overnight. Companies that had treated Duncan like a small-time operator suddenly needed his storage capacity and transportation network. But while competitors raised prices to capture windfall profits, Duncan did something counterintuitive—he locked in long-term contracts at moderate rates. "Pigs get fat, hogs get slaughtered," he told his management team. The strategy paid off magnificently. When prices collapsed in 1974, Enterprise's competitors went bankrupt while Duncan's stable cash flows allowed him to buy their assets for pennies on the dollar.

The acquisition that transformed Enterprise from regional player to national force came in 1978. Certain-Teed Corporation, a building materials company, had inherited a propane distribution business it didn't understand and didn't want. The business included storage facilities across Texas, Louisiana, and Mississippi, plus long-term supply contracts with major producers. Certain-Teed wanted $30 million cash. Duncan had perhaps $3 million in liquidity.

The negotiation took six months. Duncan flew to Certain-Teed's Pennsylvania headquarters seventeen times, each time refining the deal structure. The final agreement was financial engineering at its finest: $5 million cash at closing, $10 million seller financing over five years, and $15 million paid from the acquired business's own cash flows over seven years. Duncan also negotiated a crucial provision—if Enterprise hit certain performance metrics, the seller financing would convert to equity, giving Certain-Teed upside while reducing Enterprise's debt burden.

The Certain-Teed acquisition brought something more valuable than assets—it brought Bill Fowler, who would become Duncan's right hand for the next three decades. Fowler, a chemical engineer by training, understood the technical aspects of midstream operations in ways Duncan, the businessman, didn't. Their partnership embodied Enterprise's culture: Duncan handled strategy and capital allocation while Fowler optimized operations and engineering. They communicated in half-sentences and shared looks, building an execution machine that could integrate acquisitions in weeks rather than months.

By 1983, Enterprise took its next evolutionary leap—from land to water. Duncan built the company's first marine terminal on the Houston Ship Channel, capable of loading propane and butane onto oceangoing vessels. The timing seemed bizarre. Global energy markets were in chaos. Continental Illinois Bank had just collapsed. Paul Volcker's interest rates made capital impossibly expensive. But Duncan saw opportunity in chaos. Asian petrochemical demand was exploding. U.S. Gulf Coast production was abundant. Someone had to connect supply and demand across the Pacific.

The marine terminal's first year was a disaster. Ships arrived late. Loading equipment malfunctioned. Hurricane Alicia nearly destroyed the entire facility. Enterprise lost $2 million—devastating for a company doing $50 million in annual revenue. Duncan's response revealed his character. Instead of retreating, he doubled down, hiring the best marine engineers from Exxon and Shell, rebuilding the terminal with redundant systems, and creating operating procedures that became industry standards. By 1985, the terminal was profitable. By 1990, it was the most efficient NGL export facility on the Gulf Coast.

The 1980s Texas banking crisis should have killed Enterprise. Between 1980 and 1989, over 500 Texas banks failed. Enterprise's lead bank, First City Bancorporation, collapsed in 1988. Duncan owed them $300 million—more than Enterprise's entire asset value. The FDIC seizure meant all loans were immediately callable. Duncan had thirty days to find new financing or lose everything.

What happened next became midstream industry legend. Duncan called every major customer and supplier, explaining the situation with brutal honesty. Within two weeks, he had commitment letters from chemical companies, refiners, and producers—companies that needed Enterprise's infrastructure—collectively guaranteeing $200 million in new bank financing. The remaining $100 million came from an unlikely source: Sam Walton. The Walmart founder, who knew Duncan from propane supply deals to rural Walmart stores, personally guaranteed a loan from Arvest Bank. "Dan Duncan's word is worth more than most people's contracts," Walton told his bankers.

The near-death experience transformed Duncan's thinking about capital structure. Never again would Enterprise depend on a single financing source. He established relationships with twenty different banks, issued public bonds, and most importantly, began exploring a new financial structure gaining popularity in the energy sector—master limited partnerships. The MLP structure would allow Enterprise to access public capital markets while maintaining tax efficiency. It would also solve Duncan's biggest challenge: how to build billion-dollar infrastructure without diluting his control.

By 1990, Enterprise had evolved from a propane truck company to an integrated midstream operator. The company owned 4,000 miles of pipelines, 20 million barrels of storage capacity, and processing facilities across the Gulf Coast. Annual revenues exceeded $1 billion. But Duncan knew this was just the foundation. The real growth would come from accessing public markets and executing transformative acquisitions.

The 1990s brought new challenges and opportunities. Natural gas deregulation created massive price volatility. Environmental regulations required expensive infrastructure upgrades. International competition intensified as Middle Eastern producers built their own export facilities. But Enterprise's integrated model—owning the entire value chain from wellhead to water—provided resilience. When processing margins collapsed, storage revenues increased. When storage was oversupplied, transportation demand spiked. The portfolio effect smoothed earnings in ways pure-play competitors couldn't match.

As 1998 approached, Duncan made the decision that would transform Enterprise from private company to public giant. The IPO process would test every relationship Duncan had built over thirty years. Investment bankers insisted Enterprise needed to restructure, bring in professional management, and adopt Wall Street-friendly practices. Duncan's response was vintage: "We'll go public on our terms or not at all." The roadshow pitch was simple: Enterprise owned irreplaceable infrastructure, generated stable cash flows, and would grow through disciplined capital allocation. Either investors understood that value proposition or they didn't.

The IPO would price in July 1998, in the middle of the Asian financial crisis, with oil prices collapsing and Russia defaulting on sovereign debt. The timing couldn't have been worse. Or could it?

IV. Going Public & The MLP Revolution (1998-2004)

The Lehman Brothers conference room on July 28, 1998, felt like a funeral parlor. Asian markets were in freefall. Russia would default on its debt within three weeks. Oil had crashed to $12 a barrel. The investment bankers recommended pulling the IPO—market conditions were "impossible." Duncan stood up, walked to the window overlooking Manhattan, and turned back to face the room. "Gentlemen, I've been building this company for thirty years. We're not traders timing markets. We're infrastructure owners. If investors can't see value when everyone's panicking, they don't deserve to own Enterprise." The IPO would proceed as planned. The pricing was brutal. Enterprise offered 11.5 million common units at $22 per unit on July 28, 1998, raising approximately $253 million—less than hoped but enough. The structure was revolutionary for its simplicity. Unlike other MLPs with complex incentive distribution rights (IDRs) that could take 50% of incremental cash flow, Enterprise capped its general partner's take at 25%. Duncan retained control through Enterprise Products Company, which owned the 2% general partner interest plus substantial limited partner units.

The MLP structure itself was financial engineering at its finest. Created by Apache Oil in 1981 and refined through the 1980s, MLPs allowed companies to avoid corporate taxation—all cash flow passed through to unitholders who paid individual taxes. For capital-intensive businesses like pipelines, this was transformative. Every dollar saved in taxes could be reinvested in growth. The structure also created a virtuous cycle: more assets generated more distributable cash flow, which supported higher unit prices, which made acquisitions cheaper, which created more cash flow.

But Duncan understood something his investment bankers didn't—the real value wasn't tax efficiency but forced discipline. MLPs must distribute most of their cash flow to unitholders. There's no retained earnings cushion, no rainy-day fund. Every growth investment must earn its cost of capital immediately or the distribution gets cut and units crater. This brutally efficient capital allocation framework meant only the best projects got built.

The first acquisition as a public company tested Enterprise's credibility. In 1999, Shell Oil was divesting non-core midstream assets—a hodgepodge of pipelines, storage facilities, and processing plants scattered across Texas and Louisiana. Shell wanted $350 million cash. Enterprise had maybe $50 million in liquidity post-IPO. The investment bankers proposed a complex structure involving preferred units, convertible debt, and contingent payments. Duncan killed it immediately. "If we can't explain the deal to a pipeline operator in two sentences, we shouldn't do it."

The solution was elegant: Enterprise issued $300 million in common units directly to Shell at a 5% premium to market price, plus $50 million cash. Shell became Enterprise's largest unitholder, aligning their interests perfectly. But the masterstroke was the commercial agreement—Shell committed to minimum volume throughput on the acquired assets for ten years. Enterprise got assets plus guaranteed cash flows. Shell got liquidity plus upside exposure. Wall Street called it transformative. Duncan called it common sense.

The 2001 dot-com crash created unexpected opportunity. Energy was out of favor. Enron's collapse destroyed confidence in energy trading and complex financial structures. MLPs traded at historic discounts. While others retreated, Enterprise deployed $1.1 billion acquiring Tejas Energy from Shell—doubling its pipeline network overnight. The price was 7x EBITDA when recent deals had been 10-12x. But more importantly, Tejas brought something invaluable: access to the Barnett Shale, where a wildcatter named George Mitchell was perfecting something called hydraulic fracturing.

The year 2002 marked Enterprise's most important strategic decision—one that wouldn't be fully appreciated for years. Under Duncan's leadership, Enterprise embarked on an aggressive growth strategy through both organic development projects and strategic acquisitions, but the key move was structural. Enterprise eliminated its 50% IDRs voluntarily, years before peers were forced to by activist investors. The decision cost Duncan personally—he gave up hundreds of millions in future distributions. But it reduced Enterprise's cost of capital dramatically, making growth accretive at lower returns.

The board meeting where Duncan proposed eliminating IDRs was contentious. Several directors, including major unitholders, opposed it. "You're giving away the crown jewels," one argued. Duncan's response captured his philosophy: "Gentlemen, you can own 50% of a shrinking pie or 25% of a growing one. I know which I'd choose." The vote was unanimous once he put it that way.

The IDR elimination had second-order effects Duncan anticipated but didn't advertise. Without the GP's disproportionate take, Enterprise could retain more cash flow for growth. This self-funding capability meant less dilution, less debt, more flexibility. While competitors paid 15% of incremental cash flow to sponsors, Enterprise reinvested it. Over the next decade, this advantage would compound into billions of value creation.

By 2003, Enterprise had evolved from pure-play NGL processor to integrated midstream operator. The company owned 19,000 miles of pipelines, 140 million barrels of storage, and processing capacity of 6 billion cubic feet per day. But the real transformation was philosophical. While Enron had tried to be an asset-light trading house, Enterprise doubled down on steel in the ground. While Williams Companies levered up for telecom ventures, Enterprise stayed focused on molecules. While El Paso chased international expansion, Enterprise built deeper roots in Texas and Louisiana.

The contrast with Enron was particularly stark. Both companies were Houston-based, both were in energy, both had charismatic leaders. But where Jeff Skilling preached intellectual capital and virtual integration, Duncan built physical assets and actual integration. Where Enron used mark-to-market accounting to manufacture earnings, Enterprise used fee-based contracts to generate cash. Where Enron's executives cashed out stock options, Enterprise's management increased their unit ownership. By 2002, Enron was bankrupt. Enterprise was buying its assets.

The cultural difference manifested in small details. Enron's headquarters had original art and marble lobbies. Enterprise operated from a non-descript office park. Enron executives flew private jets. Duncan drove a ten-year-old pickup truck. Enron sponsored stadium naming rights. Enterprise sponsored engineering scholarships. These weren't just aesthetic choices—they reflected fundamentally different business philosophies about value creation versus value extraction.

As 2004 approached, Enterprise faced a strategic inflection point. The company had grown organically as far as possible. To achieve the next level of scale, transformative acquisitions were necessary. The target was obvious: GulfTerra, El Paso's crown jewel midstream subsidiary. The negotiation would be Duncan's masterpiece—a $4 billion deal that would create America's largest pipeline company. But first, he had to convince El Paso's CEO that selling to Enterprise was better than any alternative.

V. The Transformative Mergers Era (2004-2011)

The phone call came at 2 AM. El Paso's CEO was desperate. Natural gas prices had collapsed, their debt was trading at distressed levels, and Moody's was threatening a downgrade to junk. "Dan, I need to sell GulfTerra. Goldman has five bidders. You've got 48 hours to make your best offer." Duncan hung up, walked to his home office, and pulled out a map of GulfTerra's assets he'd been studying for three years. By sunrise, he had the deal structure sketched out—not just what to pay, but how to integrate two companies with combined revenues exceeding Exxon's downstream division.

The GulfTerra acquisition in September 2004 was transformative on multiple dimensions. The enterprise value reached $4 billion, but the structure was innovative: Enterprise paid $500 million cash to El Paso and issued 13.8 million partnership units, while GulfTerra unitholders received 1.81 Enterprise units for each GulfTerra unit. This wasn't just financial engineering—it was strategic architecture. GulfTerra brought 10,000 miles of pipelines, including the critical Cameron Highway system in the deepwater Gulf of Mexico, plus the massive Stingray pipeline connecting offshore production to onshore processing.

The synergies Duncan promised seemed impossible: $40 million in annual G&A savings, $45 million in reduced interest costs, and $100 million in commercial optimization. Wall Street was skeptical. How could Enterprise find $185 million in synergies from a $4 billion deal? The answer revealed Duncan's operational genius. Within six months, Enterprise had eliminated duplicate functions, renegotiated supplier contracts using combined scale, and most importantly, optimized flow patterns across the combined network. GulfTerra's offshore pipelines fed Enterprise's onshore processing. Enterprise's NGL production supplied GulfTerra's fractionation capacity. The whole became exponentially greater than the sum.

But the real masterstroke was timing. Hurricane Katrina struck eleven months after closing. While competitors' standalone assets were damaged and offline, Enterprise's integrated network could reroute flows, share processing capacity, and maintain customer deliveries. Enterprise emerged from Katrina stronger while competitors struggled to restart operations. Duncan's integration strategy had created resilience that no disaster planning could have anticipated.

The TEPPCO acquisition in 2009 happened against the backdrop of global financial meltdown. Lehman had collapsed, credit markets were frozen, and energy demand was crashing. TEPPCO—Texas Eastern Products Pipeline Company—was a storied franchise with 12,000 miles of refined products and crude pipelines, including the critical Explorer pipeline delivering gasoline from the Gulf Coast to Chicago. But TEPPCO's sponsors needed liquidity desperately.

The negotiation took place in TEPPCO's Houston boardroom in February 2009. Duncan faced off against TEPPCO's CEO and a room full of investment bankers. They wanted $35 per unit—a 25% premium. Duncan offered $28. The bankers erupted, calling it insulting. Duncan stood up to leave. "Gentlemen, in this market, I'm the only buyer who can close without financing contingencies. You can take my offer or explain to your unitholders why you're gambling on better conditions that may never come." He walked out. Three hours later, they called back. Deal.

The $3.3 billion acquisition created the largest publicly traded energy partnership in America with $30 billion in enterprise value. The 1.24 exchange ratio meant TEPPCO unitholders became Enterprise owners, aligning interests perfectly. But the FTC raised concerns—the combined company would control too much Gulf Coast refining logistics. The solution was surgical: Enterprise divested select terminals to satisfy regulators while keeping the strategic assets that created network value.

Integration was flawless. Within 100 days, Enterprise had consolidated operations, captured $75 million in annual synergies, and improved TEPPCO's capacity utilization from 65% to 85%. The secret was Enterprise's integration playbook, refined over dozens of acquisitions: Day 1, ensure safety and environmental compliance. Week 1, meet with major customers to ensure continuity. Month 1, integrate IT systems and commercial contracts. Month 3, optimize operations and eliminate redundancies. Month 6, full integration complete.

The 2010-2011 simplification transactions were Duncan's final strategic masterwork before his death. Enterprise GP Holdings and Duncan Energy Partners had been created years earlier as funding vehicles, but their complex structures with multiple classes of units and IDRs created conflicts of interest. Duncan, despite owning substantial GP interests that benefited from the complexity, pushed for simplification.

The $9 billion merger with Enterprise GP Holdings eliminated the general partner's 2% interest and remaining IDRs completely. Duncan personally gave up over $500 million in future distributions. When asked why, his answer was prescient: "Complex structures create friction. Friction destroys value. Simple structures aligned around cash flow generation create permanent value." The Duncan Energy Partners merger followed similar logic, collapsing multiple entities into a single, simplified Enterprise.

The timing of these simplifications—completed just months after Duncan's death in March 2010—revealed remarkable succession planning. Duncan had been diagnosed with brain cancer in late 2009 but kept it private. He spent his final months ensuring Enterprise could thrive without him. The simplification transactions removed any potential governance disputes. The management succession to co-CEOs Michael Creel and Jim Teague was seamless. The family's commitment to hold their units for decades was documented.

Duncan died with a net worth exceeding $9 billion, making him America's richest person never to appear on the Forbes 400 (he actively avoided publicity). But his true legacy was institutional. While other energy entrepreneurs built companies around their personalities—T. Boone Pickens at Mesa, Aubrey McClendon at Chesapeake—Duncan built Enterprise to outlast any individual. The culture, strategy, and capital allocation framework were embedded in the organization's DNA.

The post-Duncan era began with Enterprise perfectly positioned for America's energy renaissance. The Permian Basin was beginning its ascent to become the world's most prolific oil field. The Marcellus and Utica shales were transforming Appalachia into a gas powerhouse. The Gulf Coast's refineries and chemical plants were retooling for domestic production abundance. Enterprise owned the critical infrastructure connecting all these pieces—pipelines from every major basin, processing plants at key junctions, export terminals on the Gulf Coast.

But the real strategic advantage was cultural. While competitors celebrated engineering complexity and financial innovation, Enterprise remained boringly focused on operational excellence. While others chased headlines with mega-projects, Enterprise built dozens of smaller, high-return debottlenecking projects. While peers levered up to boost returns, Enterprise maintained conservative balance sheet metrics. This operational discipline would prove invaluable as the shale revolution accelerated beyond anyone's imagination.

VI. The Shale Revolution & Export Dominance (2010-Present)

The conference room at MD Anderson Cancer Center was silent except for the hum of medical equipment. Dan Duncan, Enterprise's founder, had hours to live. His son Scott and co-CEOs Michael Creel and Jim Teague stood beside his bed. Duncan's final words to them weren't about family or legacy—they were about business: "The shale revolution is just beginning. Build for export. Asia will need everything we can ship." He passed away on March 29, 2010. Within five years, his prediction would prove staggeringly prescient as Enterprise became America's export superhighway.

Duncan's death could have destabilized Enterprise. He owned 25% of the units, controlled the general partner, and was the company's strategic visionary. But the succession was flawless—a testament to decade-long preparation. The family, led by Duncan's four children, committed to hold their units long-term rather than liquidate for estate taxes. Management, owning 33% of units collectively, aligned perfectly with public unitholders. The culture Duncan built—patient, operational, focused on cash flow—continued seamlessly.

The timing was extraordinary. In 2010, the Eagle Ford shale was producing 50,000 barrels per day. By 2015, it would exceed 1.7 million barrels. The Permian, America's historic oil giant, was being reborn through horizontal drilling and hydraulic fracturing. The Marcellus shale was transforming America from gas importer to potential exporter. Enterprise owned strategic infrastructure in all these plays, but more importantly, it owned the Gulf Coast's processing and export capacity where all this production needed to go.

The first major post-Duncan decision revealed the management team had internalized his strategic thinking. In 2011, while oil was trading above $100 and everyone was building crude pipelines, Enterprise made a contrarian bet on natural gas liquids. They announced the ATEX pipeline—a $1.3 billion project to deliver ethane from the Marcellus shale to the Gulf Coast. Wall Street was skeptical. Natural gas was at historic lows. Ethane was being rejected into gas streams because it had no value. Why build expensive infrastructure for a worthless commodity?

Jim Teague's explanation to analysts was pure Duncan doctrine: "We don't trade commodities, we move them. Chemical companies on the Gulf Coast need ethane feedstock. Marcellus producers need takeaway capacity. ATEX connects supply and demand with a fee-based toll road. Whether ethane is $0.20 or $0.60 per gallon, we make our return." By 2014, ATEX was fully subscribed with 20-year contracts. Enterprise's early move locked up the Marcellus-to-Gulf Coast corridor before competitors realized its strategic value.

The export infrastructure buildout from 2012-2020 was Enterprise's moonshot—except it actually worked. The company spent $20 billion on export terminals, pipelines, and processing facilities, creating America's energy export backbone. The scale was staggering: Enterprise now handles one-third of U.S. crude exports, 80% of ethane exports, and 40% of propane and butane exports. No single company in history has controlled such a large percentage of a nation's energy exports.

The propane export story exemplified Enterprise's strategic positioning. In 2010, America imported propane. Winter heating demand exceeded domestic supply, requiring expensive imports from Algeria and Norway. Enterprise's management made a bold prediction: shale production would create massive propane surplus, global demand (especially from Asia) would explode, and America would flip from importer to world's largest exporter.

Enterprise built accordingly. The company constructed the world's largest propane export terminal on the Houston Ship Channel, capable of loading 16 million barrels per month. Competitors thought Enterprise was overbuilding. By 2015, the terminal was running at capacity. Enterprise expanded it twice more. Today, Enterprise Products Partners L.P. (NYSE: EPD) is one of the largest publicly traded partnerships and a leading North American provider of midstream energy services, dominating propane exports with volumes that exceed most countries' total production.

The crude oil export revolution following the 2015 lifting of America's 40-year export ban created another windfall. Enterprise had anticipated this possibility years earlier, building crude storage and terminal capacity at its Echo facility. When the ban lifted, Enterprise could immediately load VLCCs (Very Large Crude Carriers) while competitors scrambled to build infrastructure. First-mover advantage translated into long-term contracts with trading houses and Asian refiners desperate for American light sweet crude.

But the masterstroke was ethane exports—a market that literally didn't exist until Enterprise created it. Ethane, the lightest NGL, was historically consumed domestically by chemical plants making ethylene. Enterprise recognized that new petrochemical capacity in China and India would create massive ethane demand but these countries had no domestic supply. The solution: build specialized, refrigerated ethane export terminals and develop a global ethane shipping market.

The technical challenges were immense. Ethane must be refrigerated to -127°F for shipping. Specialized vessels cost $400 million each. No infrastructure existed at receiving ports. Enterprise solved each problem methodically, working with ship owners, Asian petrochemical companies, and port authorities to create an entirely new global supply chain. By 2016, Enterprise was loading the world's first ethane export cargo. Today, the company controls 80% of U.S. ethane exports—a market Enterprise essentially invented. The operational achievements during this period were staggering. Total NGL pipeline transportation volumes were a record 4.8 million BPD in the fourth quarter of 2024, a 12 percent increase over the fourth quarter of 2023. Total NGL marine terminal volumes increased 9 percent to a record 1.0 million BPD for the fourth quarter of 2024. Enterprise reported record volumes across its midstream system for 2024. Natural gas processing inlet volumes reached 7.4 billion cubic feet per day (Bcf/d), a 10% increase from 2023. Total equivalent pipeline volumes were 12.9 million barrels per day (BPD), a 6% increase compared to the previous year. NGL fractionation volumes were 1.6 million BPD, a 3% increase, and marine terminal volumes were 2.2 million BPD, a 6% increase from 2023.

The integration of shale production with export infrastructure created a virtuous cycle. Producers needed reliable takeaway capacity to justify drilling investments. Chemical companies needed secure feedstock supply to justify facility expansions. Trading houses needed flexible logistics to arbitrage global price differences. Enterprise sat at the nexus, collecting fees from everyone while taking no commodity risk.

Consider the Permian Basin transformation. In 2010, the region produced 900,000 barrels per day. By 2024, production exceeded 6 million barrels daily. Enterprise built or expanded twelve major pipeline systems connecting the Permian to Mont Belvieu and the Gulf Coast. The company's Midland-to-Echo pipeline system alone moves 540,000 barrels per day—more than many countries' total production. Each barrel generates fee income regardless of oil prices.

The strategic foresight extended to seemingly minor investments that became major profit centers. In 2014, Enterprise built specialized rail terminals to move crude when pipeline capacity was constrained. Critics called it a temporary band-aid. But when pipeline disruptions occurred—Colonial Pipeline hack, Hurricane Ida, Texas freeze—Enterprise's rail flexibility commanded premium rates. The terminals, built for $200 million, generated that much in EBITDA during crisis periods alone.

Enterprise's dominance created network effects competitors couldn't replicate. Refiners preferred Enterprise because its integrated system could deliver multiple products—crude, natural gas, NGLs—from a single counterparty. Producers preferred Enterprise because its downstream assets ensured reliable demand. International buyers preferred Enterprise because its scale provided supply security. Each additional connection made the network more valuable, creating a gravitational pull that attracted more volumes.

The financial performance validated the strategy. For the full year 2024, Enterprise achieved record net income attributable to common unitholders of $5.9 billion, or $2.69 per common unit on a fully diluted basis, a 7% increase from 2023. DCF for the year was a record $7.8 billion, compared to $7.6 billion in 2023. Adjusted EBITDA for 2024 was $9.9 billion, up from $9.3 billion in the previous year. These weren't cyclical windfalls but structural earnings from irreplaceable infrastructure.

The succession to co-CEOs Jim Teague and Randy Fowler (who succeeded Michael Creel) proved Duncan's leadership development. Both had spent decades at Enterprise, understood its culture, and most importantly, owned substantial equity stakes that aligned their interests with unitholders. Their strategy wasn't revolutionary—it was evolutionary, executing Duncan's playbook with incremental improvements.

The 2020s brought new challenges—ESG pressure, renewable competition, capital market volatility. Enterprise's response was pragmatic rather than ideological. The company invested in carbon capture infrastructure, not because management believed in net-zero but because industrial customers would pay for CO2 transport. They explored hydrogen pipelines, not as green virtue signaling but because existing pipes could be repurposed if economics justified it. Every decision filtered through Duncan's framework: does it generate sustainable cash flow?

2024 marked Enterprise's 26th consecutive year of distribution growth. This wasn't financial engineering—it was operational excellence compounding over decades. While tech companies celebrated user growth and biotech promised future breakthroughs, Enterprise quietly delivered cash to unitholders every quarter for over two decades. Boring? Perhaps. Profitable? Absolutely.

Looking forward, Enterprise's position seems unassailable. The Permian Basin has decades of remaining inventory. Asian petrochemical demand continues growing. American energy dominance has bipartisan support. The infrastructure Enterprise built can't be replicated without decades and tens of billions in capital. As management noted in their latest earnings call, they expect "continuing net income and cash flow per unit growth" supported by "$6 billion of major organic growth projects in 2025, including two natural gas processing plants in the Permian Basin, the Bahia NGL pipeline, Fractionator 14, and expansions of the company's ethane and ethylene marine terminals."

VII. The Business Model & Financial Architecture

Randy Fowler pulled up a slide that looked like spaghetti—hundreds of lines connecting boxes labeled with cryptic abbreviations. "This is our asset map," he told the JPMorgan energy conference audience. "Competitors show simple diagrams. We show this mess because the mess is our moat. Every line is a pipeline, every box is a facility, every connection is a commercial relationship. Good luck replicating thirty years of infrastructure development." The audience laughed nervously. Fowler wasn't joking.

Enterprise operates through four business segments, each contributing to an integrated whole that's exponentially more valuable than its parts:

NGL Pipelines & Services (45% of gross margin): This segment is Enterprise's crown jewel, encompassing the entire NGL value chain from wellhead to water. The company operates 19,000+ miles of NGL pipelines, 31 natural gas processing plants with 14.1 billion cubic feet per day of capacity, 25 NGL fractionators producing 2.3 million barrels per day, and storage capacity exceeding 160 million barrels. The Mont Belvieu complex alone—with its massive underground storage caverns, fractionation facilities, and pipeline interconnections—generates over $1 billion in annual EBITDA.

Crude Oil Pipelines & Services (25% of gross margin): With 8,800 miles of crude pipelines and 95 million barrels of storage, Enterprise moves oil from every major U.S. basin to Gulf Coast refineries and export terminals. The flagship asset is the Seaway Pipeline, reversed in 2012 to flow from Cushing, Oklahoma to the Gulf Coast, eliminating the WTI-Brent pricing disconnect and generating hundreds of millions in value. The Echo terminal near Houston can load two million barrel VLCCs, capturing Asian demand for U.S. light sweet crude.

Natural Gas Pipelines & Services (15% of gross margin): Operating 20,000 miles of natural gas pipelines and 14 billion cubic feet of storage, this segment provides the foundation for America's power generation and industrial consumption. The Texas Intrastate system alone moves 7 trillion BTUs daily. While less sexy than liquids, natural gas infrastructure generates rock-solid fee income with minimal capital requirements.

Petrochemical & Refined Products Services (15% of gross margin): This segment includes propylene production facilities, ethylene pipelines and export terminals, refined products pipelines, and octane enhancement units. The integration with upstream NGL production creates unique optimization opportunities—when propane is cheap, Enterprise's PDH units convert it to propylene. When ethane is abundant, ethylene exports surge. This optionality is worth billions but doesn't appear on any financial statement.

The genius of Enterprise's model is its fee-based structure. Approximately 85% of gross margin comes from fee-based services—fixed tolls for moving, storing, or processing hydrocarbons. Enterprise doesn't care if oil is $30 or $130; they make the same fee per barrel transported. This transforms a cyclical commodity business into a stable infrastructure play. During the 2020 oil price collapse when WTI went negative, Enterprise's cash flow barely budged.

But the model isn't purely fee-based—and that's intentional. The remaining 15% of margin comes from commodity-sensitive activities, primarily NGL marketing and optimization. This provides upside during favorable market conditions while the fee base provides downside protection. It's having your cake and eating it too, executed through sophisticated hedging strategies that lock in margins months in advance.

The capital allocation framework is deceptively simple but ruthlessly disciplined. Every growth project must meet three criteria: minimum 15% unlevered returns, supported by long-term contracts or fee structures, and strategic fit within the integrated network. Projects that meet all three criteria get funded. Those that don't get killed, regardless of how exciting they sound. This discipline has led Enterprise to walk away from headline-grabbing projects like LNG export terminals (too capital intensive), offshore production (too risky), and renewable fuels (too dependent on subsidies).

The MLP structure remains central to Enterprise's financial architecture despite tax reform reducing some advantages. By avoiding corporate taxation, Enterprise saves approximately $1.5 billion annually versus a C-corp structure—capital that gets reinvested or distributed rather than sent to the Treasury. The requirement to distribute most taxable income creates capital allocation discipline. Management can't hoard cash for empire building; every retained dollar must earn its keep.

Enterprise's balance sheet strength differentiates it from leveraged peers. With debt-to-EBITDA of 3.0x and coverage ratios exceeding 2.0x, the company maintains investment-grade ratings from all major agencies. This isn't conservatism for its own sake—it's strategic. During market dislocations, Enterprise can access capital when competitors can't. This advantage has enabled opportunistic acquisitions at distressed valuations repeatedly over decades.

The distribution strategy balances growth and current income. Enterprise targets 60% of distributable cash flow for distributions, retaining 40% for growth investment. This self-funding model reduces reliance on capital markets and dilution from equity issuance. Since 2010, Enterprise has retained over $25 billion in cash flow—enough to build the equivalent of a Fortune 500 company without issuing a single new unit.

The financial engineering extends to seemingly mundane decisions that create enormous value. Enterprise times maintenance capex for market downturns when contractor rates are cheap. They issue debt when rates are low, not when they need capital. They hedge commodity exposure when volatility is low, not when prices move against them. These decisions, compounded over decades, have created billions in value.

Consider the 2016 debt refinancing. With interest rates at historic lows, Enterprise issued $2.5 billion in 30-year bonds at 4.2%. Competitors thought they were crazy—why lock in long-term debt when short-term rates were under 2%? By 2023, with rates above 5%, those bonds were trading at 70 cents on the dollar, effectively creating $750 million in value from a Treasury management decision.

The unit repurchase program, initiated in 2019, represents another layer of capital allocation sophistication. When units trade below intrinsic value, Enterprise buys them back. When units are fairly valued, buybacks cease. This countercyclical approach has retired 5% of units outstanding at an average price 20% below current trading levels—creating $2 billion in value for remaining unitholders.

But the real financial magic happens in the optimization activities invisible to most investors. Enterprise's integrated network allows countless arbitrage opportunities. When Conway propane trades at a discount to Mont Belvieu, Enterprise moves volumes between markets. When ethane is rejected in the Marcellus but needed on the Gulf Coast, Enterprise captures the spread. When international propane prices spike, Enterprise redirects volumes from domestic to export markets. Each optimization might generate just pennies per gallon, but across billions of gallons, it adds up to hundreds of millions in annual gross margin.

The commercial strategy leverages Enterprise's market position to extract favorable terms. Minimum volume commitments protect against demand downturns. Take-or-pay contracts ensure payment regardless of usage. Escalation clauses pass through inflation. Dedication agreements lock in volumes for decades. These provisions, negotiated from a position of strength, create contractual moats around cash flows.

Partnership agreements with producers reveal another competitive advantage. Enterprise often provides gathering and processing services in exchange for percentage-of-proceeds contracts, aligning interests while sharing risks. When commodity prices are high, both parties win. When prices are low, Enterprise's fee-based revenue provides stability. This structure has enabled Enterprise to build processing infrastructure in emerging basins before competitors, capturing first-mover advantages worth billions.

The financial architecture creates resilience that's been tested repeatedly. During the 2008 financial crisis, Enterprise's distribution coverage never fell below 1.0x. During the 2014-2016 oil collapse, cash flow actually increased as volumes grew despite price declines. During the 2020 pandemic, Enterprise maintained its distribution while peers cut or suspended payments. This isn't luck—it's the result of a financial model designed for survival in any environment.

VIII. Competitive Dynamics & Market Position

The question came from a hedge fund analyst during Enterprise's investor day: "Who's your biggest competitor?" Jim Teague paused, looked at his co-CEO Randy Fowler, and responded: "Honestly? We compete against different companies in different basins for different products. But systemwide? Nobody does what we do at our scale. Our biggest competitor is probably ourselves—the risk of becoming complacent." The analyst pressed: "But surely Kinder Morgan or Energy Transfer..." Teague cut him off: "They're good companies. But show me another midstream company that handles one-third of America's crude exports, 80% of ethane exports, and processes 7.5 billion cubic feet of gas daily. I'll wait."

The midstream sector appears fragmented with dozens of public and private players, but true competition for Enterprise is remarkably limited. Kinder Morgan, with its 70,000 miles of pipelines, seems like an obvious rival. But Kinder focuses on natural gas transportation and CO2 for enhanced oil recovery—different products, different markets. Their footprints overlap in Texas, but Kinder lacks Enterprise's NGL processing and fractionation capacity, marine terminals, and petrochemical integration. When Asian buyers need propane, they call Enterprise, not Kinder.

Energy Transfer, created through Kelcy Warren's aggressive roll-up strategy, operates 90,000 miles of pipelines. But Energy Transfer's network is a collection of acquired assets lacking Enterprise's integration. Their crude pipelines don't connect seamlessly to NGL processing. Their gas gathering doesn't feed proprietary fractionation. They're playing checkers—moving pieces independently. Enterprise plays chess—every asset reinforces others in coordinated strategy.

Plains All American focuses almost exclusively on crude oil, operating 18,000 miles of pipelines and 140 million barrels of storage. In Permian crude gathering, Plains is formidable. But crude is commoditizing—pipelines are pipelines. Enterprise's advantage comes from handling everything else producers need: gas processing, NGL takeaway, water disposal. Producers prefer one-stop shopping. Plains offers a single service; Enterprise offers solutions.

ONEOK presents interesting competition in NGL gathering and processing, particularly in the Bakken and Mid-Continent regions. But ONEOK's 2023 acquisition of Magellan Midstream for $18.8 billion reveals the challenge—they paid 15x EBITDA to acquire assets Enterprise could have built for 6x. This isn't criticism of ONEOK's strategy; it's recognition that Enterprise's first-mover advantages force competitors to overpay for catch-up acquisitions.

The private equity-backed midstream companies—Brazos Midstream, Diamondback's Rattler Midstream, Mach Resources—compete aggressively for gathering systems in specific basins. They'll often outbid Enterprise for acreage dedications. But gathering is the lowest-margin, highest-risk part of the value chain. Enterprise is happy to let others fight over gathering while it controls downstream processing, fractionation, and export infrastructure where margins are higher and risks lower.

The competitive dynamics vary dramatically by product and geography. In Permian natural gas processing, Enterprise competes with Targa Resources, DCP Midstream, and others for producer volumes. But competition isn't just about price—it's about reliability, downstream connectivity, and balance sheet strength. When producers evaluate midstream partners for 20-year infrastructure commitments, Enterprise's track record matters more than saving pennies on processing fees.

The Mont Belvieu advantage deserves special attention. Enterprise controls approximately 40% of fractionation capacity and 50% of storage capacity at Mont Belvieu—the pricing hub for all U.S. NGLs. Competitors must connect to Mont Belvieu because that's where price discovery happens. But Enterprise controls many of the connections. It's like owning prime real estate in Manhattan—others can build tall buildings, but location remains everything.

International competition is virtually non-existent for U.S. hydrocarbon exports. Middle Eastern producers have massive reserves but lack infrastructure to process and export NGLs at Enterprise's scale. Russian companies face sanctions. Canadian midstream players focus on oil sands and domestic markets. Chinese companies are buyers, not competitors. Enterprise's export terminals face more competition from geology—the U.S. shale resource base—than rival companies.

The barriers to entry are almost insurmountable for new competitors. Building Enterprise's infrastructure today would cost over $100 billion—assuming you could get permits, which post-Dakota Access Pipeline is nearly impossible for greenfield interstate pipelines. The regulatory environment has shifted from accommodation to hostility. Enterprise built much of its system when permitting meant dealing with local counties. Today, any major pipeline faces federal review, environmental lawsuits, and activist opposition. Enterprise's existing infrastructure is grandfathered—an irreplaceable advantage.

Beyond regulatory barriers, the commercial barriers are equally daunting. Producers won't sign 20-year commitments with unproven operators. Chemical companies won't depend on startup midstream companies for critical feedstocks. Banks won't finance speculative infrastructure without contracted cash flows. It's a chicken-and-egg problem: you need contracts to build infrastructure, but you need infrastructure to get contracts. Enterprise solved this paradox over decades. New entrants can't.

The technological barriers are underappreciated. Processing natural gas into NGLs, fractionating NGLs into purity products, and maintaining product quality during transportation requires sophisticated engineering. Enterprise has spent decades perfecting processes, developing proprietary technologies, and training specialized workforces. Competitors can buy equipment; they can't buy institutional knowledge.

Network effects create compounding competitive advantages. Every new connection makes Enterprise's system more valuable to existing customers. A producer with gas processing needs also needs NGL takeaway. A refiner buying crude also needs natural gas for power. A chemical company importing ethane also exports polyethylene. Enterprise can bundle services, optimize across products, and provide integrated solutions competitors can't match.

The capital markets advantage is self-reinforcing. Enterprise's investment-grade rating, 26-year distribution growth record, and $70 billion market cap provide access to capital at rates 200-300 basis points below smaller competitors. This cost of capital advantage means Enterprise can bid lower on projects while still achieving target returns. Over time, this leads to market share gains that further strengthen the balance sheet—a virtuous cycle competitors can't break.

Customer relationships built over decades create switching costs beyond economics. When plant managers have Jim Teague's cell phone number, when supply contracts have been renewed multiple times without dispute, when operational issues get resolved with phone calls instead of lawyers, relationships become competitive moats. Energy Transfer might offer lower rates, but can they guarantee the CEO will answer during a crisis?

The competitive response to Enterprise's dominance has been consolidation. Competitors merge hoping scale creates advantages. But consolidation without integration just creates bigger problems. When Energy Transfer bought Enable Midstream, they got assets, not synergies. When ONEOK bought Magellan, they got pipelines, not Enterprise's integrated value chain. Mergers driven by investment bankers rarely create operational advantages that threaten Enterprise's position.

The sustainability of Enterprise's competitive advantages seems secure for the foreseeable future. Shale production will continue for decades. Asian demand for hydrocarbons is growing, not shrinking. The infrastructure Enterprise built can't be replicated. The relationships took generations to establish. The operational expertise compounds daily. Short of nationalization or technological disruption that eliminates hydrocarbon demand entirely, Enterprise's competitive position appears unassailable.

IX. Playbook: Lessons for Builders & Investors

The scene was a Harvard Business School case study discussion in 2019. The professor asked: "What's Enterprise's secret sauce?" A former investment banker raised his hand: "Financial engineering—the MLP structure, IDR elimination, sophisticated hedging." A McKinsey consultant countered: "Operational excellence—best-in-class assets, technical expertise, integration synergies." Then a student who'd actually worked at Enterprise spoke up: "You're both wrong. It's culture. Everything else follows from how they think about business." The room fell silent. She was right.

The Duncan Doctrine, though never formally written, permeates every decision at Enterprise. First principle: your word is your bond. In an industry infamous for sharp practices, Enterprise's handshake deals stick. When Hurricane Harvey flooded Houston, Enterprise honored contracted rates despite force majeure clauses that legally freed them from obligations. Competitors invoked force majeure immediately. Guess who got the next round of contracts?

Second principle: think in decades, not quarters. Wall Street analysts constantly push for higher distributions, leverage for buybacks, or aggressive growth targets. Enterprise ignores them. The company models projects over 30-year lifecycles. They'll accept lower year-one returns for higher terminal value. They'll sacrifice near-term earnings for long-term positioning. This long-term orientation enables contrarian decisions that look stupid initially but brilliant eventually.

Third principle: align interests obsessively. Management owns 33% of units—their wealth is tied to unit price, not salary or bonuses. Major decisions require skin in the game. When Enterprise eliminated IDRs, Duncan personally gave up hundreds of millions. When they buy assets, sellers often take units as payment, aligning their interests with Enterprise's success. Even contractors on major projects sometimes take partial payment in units. Everyone rows in the same direction.

The talent strategy is radically different from peers who recruit from investment banks and consultancies. Enterprise hires engineers from Texas A&M and UT, trains them for decades, and promotes from within. Jim Teague started as an engineer. Randy Fowler began in operations. They understand pipelines viscerally, not theoretically. This technical depth enables better capital allocation—executives who've actually operated assets make better investment decisions than those who've only modeled them in Excel.

The cultural elements seem soft but create hard advantages. Enterprise's Houston headquarters is deliberately unglamorous—no marble lobbies or executive floors. Executives fly commercial, drive their own cars, and eat in the company cafeteria. This isn't performative frugality; it's cultural DNA. Every dollar saved on corporate overhead is a dollar invested in infrastructure. Employees see executives living these values daily, reinforcing the culture.

Capital discipline in a capital-intensive industry separates winners from bankruptcies. Enterprise's hurdle rates are simple: 15% unlevered returns minimum, 20% preferred. No exceptions for strategic projects, market share gains, or competitive responses. If a project doesn't clear the hurdle, it doesn't get built. This discipline has led Enterprise to walk away from billions in potential projects. The projects they didn't do are as important as those they did.

The acquisition strategy follows a repeatable playbook. Target assets that are subscale for sellers but strategic for Enterprise. Pay fair prices, not auction premiums. Structure deals with seller financing or unit consideration to align interests. Integrate rapidly—within 100 days, not years. Optimize operations before seeking synergies. This systematic approach has enabled Enterprise to complete over 50 acquisitions without a major failure.

When to eliminate IDRs is the trillion-dollar question for MLP investors. Most sponsors cling to IDRs until forced to eliminate them by activist pressure or capital needs. Enterprise eliminated IDRs voluntarily in 2002, years before peers. The timing was crucial—early enough to capture growth benefits but late enough that the business was established. This decision alone created tens of billions in value by reducing cost of capital during the shale boom.

The M&A integration philosophy is "boring is beautiful." No rebranding, no culture transformation, no strategic pivots. Enterprise keeps what works, fixes what's broken, and optimizes everything else. Acquired employees keep their jobs if they perform. Acquired customers keep their contracts. Acquired assets keep operating. This stability enables rapid integration and immediate synergy capture.

Building for demand versus speculation might be Enterprise's most important lesson. Competitors build pipelines hoping production will come. Enterprise builds after producers sign contracts. Competitors construct export terminals anticipating Asian demand. Enterprise builds after buyers commit volumes. This demand-pull versus supply-push approach means lower utilization initially but higher returns over time.

The power of vertical integration in midstream contradicts modern business theory about focus and specialization. Enterprise owns gathering, processing, fractionation, storage, pipelines, and terminals. Academics say this creates complexity. Enterprise says it creates optionality. When one part of the chain struggles, another thrives. When markets dislocate, integration enables optimization. The whole really is greater than the sum.

Risk management philosophy starts with the recognition that Enterprise is already in a risky business—commodity infrastructure in a cyclical industry. Therefore, everything else should reduce risk. Conservative balance sheet. Long-term contracts. Geographic diversification. Product diversification. Multiple financing sources. This belt-and-suspenders approach seems excessive until crisis hits—then it seems prescient.

The partnership with customers goes beyond typical vendor relationships. Enterprise invests in understanding customers' businesses, strategies, and challenges. When a chemical company needs feedstock security for a new plant, Enterprise might build dedicated infrastructure. When a producer needs processing capacity for a new field, Enterprise might construct facilities on speculation. These customer-centric investments create dependencies that last decades.

Operational excellence sounds generic but manifests specifically. Enterprise's pipeline capacity factors exceed 95%—industry-leading utilization. Their fractionation yields exceed 99%—minimal product loss. Their safety metrics beat industry averages by 50%. Their environmental compliance is perfect—zero major violations in the past decade. These operational metrics translate directly to financial performance.

The financing strategy leverages multiple sources to maintain flexibility. Bank revolvers for short-term needs. Public bonds for long-term financing. Convertible preferreds for growth capital. Asset-backed securities for specific projects. Private placements for quick execution. This diversification means Enterprise is never dependent on a single capital source—crucial during market disruptions.

The technology adoption philosophy is pragmatic, not progressive. Enterprise doesn't chase digital transformation or AI buzzwords. But they'll implement proven technologies that improve operations. Automated pipeline monitoring reduces leaks. Predictive maintenance prevents failures. Optimization software improves scheduling. Technology serves operations, not vice versa.

Succession planning started decades before needed. Duncan identified successors, developed them systematically, and tested them with increasing responsibility. The transition from founder to professional management was seamless because it was planned. This contrasts with peers where founder departures created chaos, strategic pivots, or cultural collapse.

The stakeholder management extends beyond unitholders to communities, regulators, and employees. Enterprise invests in local communities where they operate—schools, hospitals, infrastructure. They maintain relationships with regulators through compliance and transparency. They treat employees as partners, not costs—no layoffs during downturns, profit-sharing during upturns. This stakeholder capitalism isn't altruism; it's pragmatic. Community support enables expansion. Regulatory relationships expedite permitting. Employee loyalty reduces turnover.

For investors, the Enterprise playbook offers clear lessons. Look for businesses with irreplaceable assets, not replicable strategies. Value operational excellence over financial engineering. Prefer proven execution over promised transformation. Seek aligned management with skin in the game. Embrace boring businesses with exciting economics. Most importantly, think like owners, not traders—Enterprise has created enormous wealth for patient investors while destroying impatient capital.

X. Analysis: Bull vs. Bear Case

The debate at the Sohn Conference was heating up. The hedge fund manager presenting the short case pulled up a slide: "Enterprise is a melting ice cube. Renewable energy will destroy hydrocarbon demand. Stranded assets everywhere. The MLP structure is tax arbitrage that Congress will eliminate. Management is old and stuck in the past." The audience nodded. Then the long-only manager took the stage: "Enterprise owns the pipes that connect America's geology to global demand. The assets are irreplaceable. The cash flows are contracted. The distribution has grown for 26 years. You're betting against physics and chemistry." The audience nodded again. Both arguments sounded compelling. Who was right?

The Bull Case: Irreplaceable Infrastructure for Inevitable Demand

The bull case starts with physical reality: Enterprise's infrastructure cannot be replicated. The 50,000 miles of pipelines, 260 million barrels of storage, and marine terminals handling 2+ million barrels daily would cost over $100 billion to rebuild—assuming you could get permits, which you can't. The Dakota Access Pipeline controversy killed greenfield pipeline development. Enterprise's existing infrastructure is grandfathered, creating a permanent moat.

The export dominance is mathematically staggering. Enterprise handles one-third of U.S. crude exports, approaching 2 million barrels per day. They control 80% of ethane exports, a market they essentially created. 40% of propane and butane exports flow through Enterprise terminals. This isn't market share that can be competed away—it's physical infrastructure that took decades to build and cannot be replicated.

The fee-based model provides recession-resistant cash flows. 85% of gross margin comes from fees unrelated to commodity prices. Take-or-pay contracts guarantee payment regardless of volumes. Minimum volume commitments protect against demand destruction. Cost escalators pass through inflation. This isn't a commodity business; it's an infrastructure utility with better economics than regulated utilities.

Balance sheet strength enables opportunistic capital allocation. With investment-grade ratings and conservative leverage, Enterprise can access capital when competitors can't. During the 2020 pandemic, while peers cut distributions and canceled projects, Enterprise continued investing. This countercyclical capability has enabled acquisitions at distressed valuations repeatedly—GulfTerra during the 2004 gas collapse, TEPPCO during the financial crisis, multiple assets during the 2014-2016 oil crash.

The Asian demand story is just beginning. China's petrochemical capacity is growing 5-7% annually. India's energy consumption per capita is one-tenth of developed countries with massive growth ahead. Southeast Asian economies are industrializing rapidly. These countries need hydrocarbons for plastics, fertilizers, and chemicals—not just fuel. Enterprise's export infrastructure is the bridge between U.S. abundance and Asian demand.

Shale geology provides decades of supply. The Permian Basin alone has 75 billion barrels of recoverable oil and 300 trillion cubic feet of natural gas—decades of production at current rates. The Marcellus/Utica contains 500 trillion cubic feet of gas. These aren't speculative resources; they're proven reserves accessible with existing technology. Enterprise's infrastructure is perfectly positioned to handle this production.

Management alignment is extraordinary. Insiders own 33% of units worth over $20 billion. They're not paid in options that encourage risk-taking but in units that encourage long-term value creation. No golden parachutes, no change-of-control provisions, no poison pills. Management wins only if unitholders win. This alignment has driven disciplined capital allocation for decades.

The hidden option value in the infrastructure is massive. Pipelines built for natural gas can transport hydrogen with modifications. Storage caverns holding NGLs can store ammonia or CO2. Marine terminals exporting hydrocarbons can handle any liquid. As energy transition occurs, Enterprise's infrastructure can adapt. The molecules might change; the need for infrastructure won't.

Financial performance validates the thesis. 26 consecutive years of distribution growth through multiple recessions, oil crashes, and pandemics. Returns on invested capital consistently exceeding 12%. Distributable cash flow growing at 8% annually. These aren't promises; they're proven results. Enterprise has compounded wealth for decades and shows no signs of slowing.

The Bear Case: Structural Decline in a Dying Industry

The bear case begins with energy transition inevitability. Electric vehicles are destroying oil demand—every Tesla sold is 400 gallons of annual gasoline demand gone forever. Renewable electricity is killing natural gas power generation. Bioplastics are replacing petrochemicals. Enterprise's infrastructure might be irreplaceable, but it's also unnecessary in a decarbonizing world.

Regulatory and environmental pressures are intensifying. The Inflation Reduction Act subsidizes everything competing with hydrocarbons. The SEC's climate disclosure rules will reveal Enterprise's massive carbon footprint. Environmental lawsuits are proliferating. Banking regulations increasingly prevent financing for fossil fuel infrastructure. Enterprise might own grandfathered assets, but they can't grow in this environment.

Growth limitations are mathematical. Enterprise already handles one-third of U.S. crude exports—how much higher can that go? They process 7.5 billion cubic feet of gas daily in a country producing 100 billion—growth requires taking share from established competitors. The easy infrastructure has been built. Remaining opportunities are marginal, expensive, and risky.

Commodity cycle exposure persists despite fee rhetoric. When oil crashed in 2020, Enterprise's units fell 50%. If 85% of revenue is fee-based and immune to commodity prices, why such volatility? The answer: perceived risk matters more than actual risk. In the next downturn, investors will shoot first and ask questions later.

Technological disruption could strand assets overnight. Fusion energy could make natural gas obsolete. Synthetic biology could produce chemicals without hydrocarbons. Direct air capture could make CO2 pipelines worthless. Quantum computing could optimize logistics, eliminating Enterprise's advantages. These might seem like science fiction, but so did shale technology twenty years ago.

Capital allocation risks are rising. Enterprise is spending $4-5 billion annually on growth projects. If energy transition accelerates, these investments become stranded assets. The Permian processing plants built today might be worthless in a decade. The export terminals constructed for Asian demand might find no buyers. Management is fighting the last war while the battlefield changes.

MLP structure disadvantages are mounting. Tax reform eliminated many MLP benefits. K-1 tax forms complicate ownership for institutions. Index exclusion limits passive investor demand. Governance concerns persist with no voting rights for limited partners. The structure that enabled growth might now constrain it.

Demographic challenges loom. Enterprise's workforce is aging—average employee age exceeds 50. Younger workers don't want fossil fuel careers. Engineering programs are pivoting to renewable energy. In ten years, who will operate these assets? The institutional knowledge built over decades could evaporate with retirements.

Customer concentration creates vulnerability. Top ten customers represent 40% of revenues. If a major chemical company switches to bio-feedstocks or a key producer goes bankrupt, the impact would be severe. Customer diversification sounds good, but physical infrastructure creates natural concentration.

Alternative capital competition is intensifying. Infrastructure funds have raised $500 billion for energy transition. That capital needs deployment. They'll compete for any attractive return, driving down margins. Enterprise's 15% return hurdles will become 10%, then 8%, then utility-like 6%. Competition for returns is more dangerous than competition for assets.

The Verdict: Synthesis and Probability Weighting