EOG Resources: From Enron Spinoff to Shale Revolution Pioneer

I. Introduction & Episode Roadmap

Picture this: It's 2007, and Mark Papa, CEO of a mid-sized energy company, sits in his Houston office staring at production data that would change American energy forever. His team had just cracked the code on extracting oil from rock formations so tight that geologists once considered them worthless. Within a decade, his company would help transform the United States from the world's largest oil importer to its largest producer. This is the story of EOG Resources—the company that engineered America's shale revolution.

They call EOG the "Apple of Oil," and for good reason. While Apple revolutionized consumer technology through relentless innovation and disciplined execution, EOG did the same for energy extraction. Both companies share an obsession with in-house R&D, vertical integration of critical capabilities, and a willingness to bet against conventional wisdom. Where Steve Jobs saw opportunity in combining existing technologies into revolutionary products, Mark Papa saw opportunity in combining horizontal drilling with hydraulic fracturing to unlock trillions of dollars of previously inaccessible oil.

The journey from Enron subsidiary to $70 billion shale powerhouse reads like a business school case study in contrarian thinking. Born from the ashes of one of history's most spectacular corporate frauds, EOG somehow emerged not just unscathed but positioned to lead the most significant energy transformation since the discovery of Saudi Arabia's Ghawar field. How did a company that started life as a sleepy natural gas driller inside Enron's sprawling empire become the architect of American energy independence?

This isn't just a story about drilling techniques or geological formations. It's about how disciplined capital allocation, technological innovation, and contrarian thinking can create extraordinary value even in commodity businesses. It's about leaders who zigged when the industry zagged, who invested when others retreated, and who built a culture of innovation in an industry notorious for boom-bust cycles and me-too strategies.

The themes that emerge from EOG's story—the power of focused R&D, the importance of capital discipline, the value of contrarian positioning—offer lessons far beyond the oil patch. In an era when investors chase the latest AI startup or crypto protocol, EOG proves that extraordinary returns can still be found in "old economy" industries for those willing to think differently and execute flawlessly.

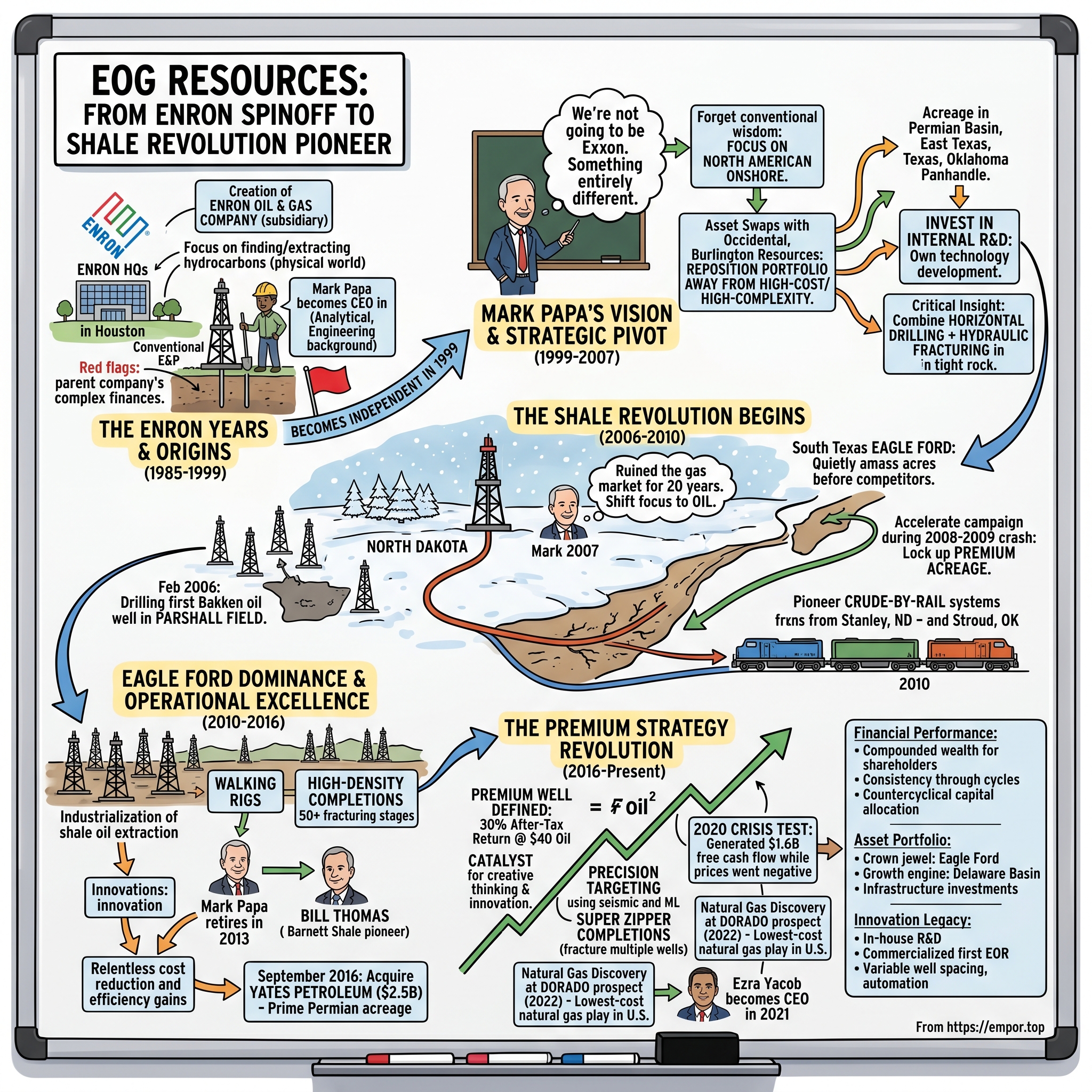

II. The Enron Years & Origins (1985-1999)

The conference room at Enron headquarters in 1985 buzzed with the kind of energy that would later become synonymous with the company's culture—aggressive, ambitious, borderline reckless. Ken Lay had just orchestrated the merger of Houston Natural Gas and InterNorth, creating what would become Enron. But buried in the deal structures and subsidiary formations was a decision that would outlive the parent company by decades: the creation of Enron Oil & Gas Company, a traditional exploration and production subsidiary focused on actually finding and extracting hydrocarbons rather than trading them.

The irony is delicious in hindsight. While Enron would become infamous for mark-to-market accounting, off-balance-sheet vehicles, and phantom profits, its oil and gas subsidiary operated in the physical world where you either found oil or you didn't. There were no "weather derivatives" or "bandwidth trading" schemes here—just the ancient business of punching holes in the earth and hoping hydrocarbons flowed out.

In those early years, Enron Oil & Gas operated like any conventional E&P company. They drilled vertical wells in proven fields, acquired producing properties when prices dipped, and slowly built a portfolio centered on natural gas assets in Texas, Oklahoma, and the Gulf of Mexico. The subsidiary contributed steady if unspectacular cash flows to Enron's increasingly complex financial empire. Annual reports from the early 1990s show a competent but unremarkable operator, generating returns in line with industry averages. Everything changed in 1998 when Mark G. Papa was named chairman and chief executive officer. Papa graduated from the University of Pittsburgh, where he received a bachelor's degree in Petroleum Engineering in 1968. He went on to receive a master's degree in Business Administration from the University of Houston. In 1981, he joined Belco Petroleum which, after several mergers, was one of the predecessor companies to Enron Oil & Gas Company. He served as EOG's Senior Vice President, Operations from 1984 to 1993 and President, North America Operations from 1994 to 1996.

Papa was not your typical oil executive. While many industry leaders came from geology or finance backgrounds, Papa combined petroleum engineering expertise with business acumen. His colleagues described him as intensely analytical, someone who could discuss decline curves and net present values with equal fluency. But what set him apart was his willingness to challenge conventional wisdom—a trait that would prove invaluable as Enron's house of cards began to wobble.

By 1999, the writing was on the wall for anyone paying attention. Enron's stock price soared on promises of revolutionary business models and exponential growth, but Papa saw something different from his perch atop the oil and gas subsidiary. The parent company's increasingly complex financial structures and aggressive accounting raised red flags. While Enron executives celebrated mark-to-market accounting that allowed them to book future profits immediately, Papa dealt with the reality of dry holes and depleting wells.

The separation came in August 1999, executed with the precision of a special operations extraction. In 1999, the company became independent from Enron and changed its name to EOG Resources, Inc. The mechanics were straightforward: Enron distributed its shares in the subsidiary to Enron shareholders, creating an independent public company. EOG Resources—the initials a subtle nod to its origins—was born with approximately $1 billion in annual revenues and a market capitalization around $2 billion.

The timing couldn't have been more fortuitous. Within two years, Enron would implode in one of the most spectacular corporate frauds in history, taking down Arthur Andersen and destroying billions in shareholder value. But EOG, safely separated from the wreckage, was free to chart its own course. Papa later reflected that the separation was "the best thing that ever happened to us," though at the time it felt more like abandonment than liberation.

What EOG inherited from its Enron years was a solid if unspectacular asset base: natural gas properties across Texas and the Gulf Coast, a competent technical team, and most importantly, a culture of engineering excellence that had somehow survived within Enron's trading-obsessed environment. What it lacked was a clear strategic vision beyond being a reliable natural gas producer in an increasingly commoditized market. That was about to change dramatically under Papa's leadership.

III. Mark Papa's Vision & Strategic Pivot (1999-2007)

The boardroom at EOG's Houston headquarters in early 2000 felt like a startup despite the company's 15-year history. Papa stood before his leadership team with a simple but radical proposition: forget everything you know about how an E&P company should operate. "We're not going to be Exxon," he declared. "We're not even going to try to be Apache. We're going to be something entirely different."

In the 14 years Papa headed up EOG, the company's market cap grew from $2 billion to $54 billion, and the stock value increased 2,200%. But that extraordinary value creation began with a series of strategic moves that seemed counterintuitive at the time. While competitors chased international mega-projects and deepwater drilling programs, Papa focused on North American onshore assets that others considered second-tier. The first major strategic moves came through asset swaps that reshaped EOG's portfolio. In 2000, the company swapped properties with Occidental Petroleum. EOG received properties in East Texas and the Oklahoma Panhandle in exchange for properties in California and the Gulf of Mexico. In February 2000, the company also swapped properties with Burlington Resources. EOG received properties in West Texas and the New Mexico, specifically in the Permian Basin, in exchange for properties in Texas and Oklahoma.

These weren't random trades. Papa was systematically repositioning EOG away from high-cost, high-complexity assets toward onshore properties with running room for drilling programs. The California assets EOG gave up required dealing with complex environmental regulations and mature fields. The Gulf of Mexico properties came with hurricane risk and expensive offshore infrastructure. In exchange, EOG acquired acreage in regions that would become the epicenter of America's shale revolution.

Papa said, "The properties in east Texas and Oklahoma complement our assets in each of these divisions and provide significant upside potential for our drilling program in 2000 and beyond in each area. Overall this transaction is expected to increase both earnings and cash flow." But even Papa couldn't have imagined just how prescient these moves would prove to be.

The international expansion that followed might seem contradictory to this North American focus, but it served a different purpose. Trinidad offered stable, long-term natural gas contracts with government-backed buyers—essentially a cash flow hedge against volatile North American gas prices. The China ventures provided a window into international operations and potential future growth markets. The UK North Sea assets came with tax advantages and technological learning opportunities. But these were sideshows to the main event unfolding in Texas and Oklahoma.

The company acquired properties in Canada from Husky Energy for $320 million in 2003. This Canadian acquisition brought EOG into the Western Canadian Sedimentary Basin, adding natural gas reserves and production that would provide stable cash flows during the transition period ahead. More importantly, it gave EOG exposure to some of the early horizontal drilling experiments happening in Canada's tight gas formations.

By 2004, EOG had quietly assembled one of the most significant land positions in what would become ground zero for the shale revolution. By 2004, EOG had nearly 400,000 acres under lease in the Barnett Shale, the Fort Worth-area formation where George Mitchell's company had been experimenting with hydraulic fracturing since the 1980s. But while Mitchell Energy focused on natural gas in vertical wells, Papa's team was thinking differently.

The critical insight came from combining two existing technologies in a new way. Horizontal drilling had been around since the 1920s, though it remained expensive and technically challenging. Hydraulic fracturing dated back to the 1940s. But nobody had successfully combined them at scale in tight rock formations. Papa's engineering background told him this combination could unlock resources previously considered uneconomical. His business training told him the economics could be revolutionary.

What made Papa different from other CEOs was his willingness to invest in internal R&D rather than relying on service companies. "It wasn't the service companies that provided the advances in shale technology," Papa would later say with characteristic bluntness. While Halliburton and Schlumberger marketed their fracturing services, EOG's engineers were developing proprietary completion techniques, testing different proppant mixtures, and optimizing well spacing through trial and error.

This period from 1999 to 2007 would later be recognized as EOG's transformation from a conventional natural gas company to a technology-driven oil producer. But at the time, Wall Street was skeptical. Natural gas prices were volatile, the company's international ventures seemed scattered, and the heavy investment in unproven shale acreage looked risky. EOG's stock underperformed peers who were riding high on conventional production and international mega-projects.

Papa didn't care about quarterly earnings calls or sell-side analyst reports. He was playing a longer game, positioning EOG for a revolution he could see coming but couldn't yet fully articulate. The company's engineers were reporting increasingly positive results from horizontal wells in the Barnett. The economics were improving with each iteration. And most importantly, the techniques they were developing could be applied to oil-bearing formations, not just natural gas.

The seeds of the shale revolution had been planted. All that remained was to harvest them.

IV. The Shale Revolution Begins (2006-2010)

The winter wind cut across the North Dakota plains like a blade, temperatures plunging to minus thirty degrees Fahrenheit. It was February 2006, and EOG Resources executive vice president Kurt Doerr stood on a drilling pad fifty miles west of Minot, watching his crew punch through frozen earth toward a geological formation that would redefine American energy. The timing seemed odd given that EOG's core business—drilling for natural gas, not oil—was absolutely booming, and if Doerr had any doubts about his boss's strategy, they were put to rest in May 2006 when EOG drilled its first major North Dakota oil well in Parshall.

The company made what still stands as the most prolific discovery in the play when it explored the Parshall Field in Mountrail County, ND, in 2006. The Parshall oil well was drilled horizontally, with Doerr's crew drilling to a depth of 9,100 feet, then curving out laterally to target a 40-foot-wide layer of porous, oily rock. Their goal was to drill horizontally 5,000 feet, but they only got out 1,800 because of all the oil and gas encountered. To Doerr's amazement, the well immediately produced 450 to 500 barrels a day.

But the Bakken discovery was just the opening act. The real epiphany came a year later, in 2007, when Papa made a statement that would prove prophetic for the entire industry. In 2007, Papa stated that so much shale gas had been discovered that "we had probably ruined the market for 20 years". This wasn't just hyperbole from a frustrated executive—it was a fundamental insight into how horizontal drilling and hydraulic fracturing had permanently altered the supply dynamics of North American natural gas.

The numbers told the story. Natural gas prices, which had spiked above $13 per thousand cubic feet in 2005 and 2008, would never sustainably recover. The Barnett Shale alone was producing more gas than entire states had produced just years earlier. EOG's own success in natural gas had helped create a glut that would persist for decades. Papa saw what others missed: the same technology that had crashed natural gas prices could revolutionize oil production.

Papa intended to shift EOG's focus from natural gas toward oil. Even more surprising: Papa intended to drill for oil not in hot spots like Canada, Africa, or the deep water of the Gulf of Mexico, but in the continental U.S. This wasn't a gradual pivot—it was a complete strategic reversal executed with military precision.

The shift required more than just moving rigs from gas fields to oil fields. EOG had to reinvent its entire technical approach. Natural gas molecules are tiny and mobile; they flow relatively easily through rock formations once fractures are created. Oil is viscous and stubborn, requiring different fracturing techniques, proppant mixtures, and completion designs. EOG's engineers became obsessed with fluid dynamics, testing different gel compositions and sand concentrations in their fracturing fluids. While EOG was perfecting its Bakken operations, another opportunity emerged 1,500 miles south. In 2008, Petrohawk Energy successfully drilled the exploratory well "STS #241-1H" in La Salle County, Texas, proving the Eagle Ford Shale could produce oil. But EOG had already been quietly accumulating acreage in the region, betting that the geological characteristics that made the Barnett Shale productive would translate to this Cretaceous-age formation.

In South Texas, EOG has accumulated acreage across six counties in the Eagle Ford Play where it has drilled 16 delineation wells over a 120 mile trend. The company's approach to the Eagle Ford exemplified Papa's philosophy: move fast, move quietly, and lock up the best acreage before competitors realize what's happening. EOG Resources led the push into the oil window of the Eagle Ford Shale oil play. The company began leasing in the oil window before many thought producing liquids from the formation would yield economic wells.

The technical challenges in the Eagle Ford differed from the Bakken. The formation was deeper, hotter, and more geologically complex. EOG's engineers had to develop new drilling fluids that could withstand temperatures exceeding 300 degrees Fahrenheit. They experimented with different proppant sizes and concentrations, eventually pioneering what they called "high-density completions" that packed more fracturing stages into each horizontal wellbore.

The financial crisis of 2008-2009 created an unexpected opportunity. While other companies pulled back on drilling programs and cancelled leases, EOG accelerated its Eagle Ford campaign. Oil prices had crashed from $147 per barrel in July 2008 to $34 by December, but Papa saw this as a chance to lock up premium acreage at fire-sale prices. The company has since amassed a position of almost 650,000 acres that stretches from Gonzales County down to La Salle and Webb counties.

By 2010, the transformation was complete. We announce the South Texas Eagle Ford oil play, our more than half a million-net acre position there, and for the first year in EOG's history, we generate more revenues from crude oil, condensate and natural gas liquids production than from natural gas production. This wasn't just a strategic shift—it was a complete metamorphosis. The company that had helped crash natural gas prices through oversupply was now positioned to lead America's oil renaissance.

The infrastructure innovations that accompanied this drilling revolution were equally impressive. The first train to transport crude oil for EOG Resources arrives in Stroud, Oklahoma on January 3, 2010. The first train to transport crude oil for EOG Resources departed Stanley, North Dakota on December 31, 2009. While pipelines remained the preferred method of oil transportation, EOG recognized that the shale boom was producing oil faster than pipeline infrastructure could be built. The company pioneered crude-by-rail systems that would move Bakken oil to refineries on the East and Gulf Coasts.

Papa's vision had materialized. In just four years, EOG had transformed from a natural gas company facing a commodity glut to an oil producer at the forefront of America's most significant energy development since the Alaska pipeline. The techniques developed in the Barnett had been successfully applied to oil-bearing rocks. The land accumulated during the downturn was now among the most valuable real estate in North America. And most importantly, EOG had proven that American innovation could unlock resources everyone thought were impossible to extract economically.

V. Eagle Ford Dominance & Operational Excellence (2010-2016)

The drilling rig count at dawn in Gonzales County, Texas, told the story: twenty-two rigs operating simultaneously across EOG's Eagle Ford acreage, each one a $20 million bet on the future of American oil. It was 2012, and EOG had become a drilling machine, perfecting the industrialization of shale oil extraction with assembly-line efficiency and Silicon Valley-style innovation.

We became the largest producer of oil in the lower 48 states, reaching 300,000 barrels of oil per day of gross operated production in 2014. This wasn't just incremental growth—it was a complete transformation of American energy production. EOG's Eagle Ford operations alone were producing more oil than entire countries. The company that had helped crash natural gas prices was now reshaping global oil markets.

The operational innovations during this period read like a manufacturing revolution applied to oil extraction. EOG pioneered what they called "walking rigs"—massive drilling platforms that could move from well to well without being disassembled, cutting days off drilling times. They developed proprietary drilling fluids that reduced friction by 40%, allowing them to drill laterals extending 10,000 feet horizontally. Most impressively, they created an in-house sand processing facility in Wisconsin, vertically integrating their supply chain for proppant—the sand pumped into fractures to keep them open.

The numbers from individual wells defied belief. In the South Texas Eagle Ford, EOG drilled its best well to date. The Boothe Unit #10H in Gonzales County began initial production at 4,820 barrels of oil per day (Bopd) while an offset well, the Boothe Unit #9H, had an initial production rate of 3,708 Bopd. These weren't anomalies—they were becoming the norm as EOG refined its completion techniques.

The logistics revolution was equally impressive. In July, we marked another milestone with the departure of our 500th crude oil unit train from our Stanley, North Dakota, rail terminal, which opened in December 2009. While pipelines remained the preferred transportation method, EOG's crude-by-rail system provided crucial flexibility, allowing the company to chase the best prices across multiple markets.

But the real magic happened underground, in the completion designs that EOG kept as closely guarded secrets. The company developed what it called "high-density completions," packing 50 or more fracturing stages into a single horizontal wellbore. Each stage was precisely engineered, with different proppant mixtures and fluid volumes calculated by proprietary algorithms. Competitors would drill similar wells in adjacent acreage and get half the production—the difference was EOG's completion technology.

The financial performance reflected this operational excellence. Year-over-year non-GAAP earnings per share grew 50% and crude oil production grew 39%, driven by strong performance from the South Texas Eagle Ford and North Dakota Bakken. But Papa wasn't satisfied with just strong returns. He wanted to build something that would endure beyond the next boom-bust cycle. The leadership transition that began in 2011 represented a critical test for EOG's culture. The Board also confirmed that Bill Thomas and Gary Thomas will continue to report to Mark G. Papa, Chairman and Chief Executive Officer until June 2013, when Papa will retire and be succeeded by Bill Thomas. Papa's announcement wasn't sudden—it was carefully orchestrated over two years to ensure continuity.

"Although I will continue in my role as day-to-day hands-on Chairman and CEO through 2012, I plan to gradually turn over my responsibilities to Bill Thomas six months before I retire," Papa said. This wasn't just succession planning; it was cultural preservation. Bill was the primary driving force behind EOG's and the industry's first large-scale successful horizontal shale gas activities in the Johnson County Barnett Shale Play in 2004.

Under Bill Thomas's leadership from 2013 onward, EOG didn't just maintain Papa's vision—it amplified it. The company continued to push the boundaries of what was possible in shale extraction. Well productivity in the Eagle Ford increased by 30% through enhanced completion designs. Drilling times fell from 20 days to 12 days per well. Most impressively, EOG maintained its discipline even as oil prices recovered from their 2014-2015 crash.

The capstone of this period came in September 2016 with a deal that surprised the industry. EOG Resources and Yates Agree to Combine in Transaction Valued at $2.5 Billion. Under the terms of the agreements, EOG will issue 26.06 million shares of common stock valued at $2.3 billion and pay $37 million in cash. The acquisition increased the company's holdings by 176,000 net acres in the Delaware Basin, 200,000 net acres in the Powder River Basin, and 138,000 net acres on the Northwest Shelf in New Mexico.

This wasn't just any acquisition. Yates Petroleum was a 93-year-old company with prime acreage in the heart of the Permian Basin's Delaware sub-basin. The timing was perfect—oil prices had crashed from over $100 per barrel in 2014 to under $30 in early 2016, creating a buyer's market for quality assets. "This deal really isn't about getting bigger. It's about getting better," Thomas told investors.

Yates immediately adds an estimated 1,740 net premium drilling locations in the Delaware Basin and Powder River Basin to EOG's growing inventory of premium drilling locations, a 40 percent increase. But the real value wasn't just in the acreage—it was in how EOG could apply its completion technology to Yates' underdeveloped assets.

The operational excellence that defined this period went beyond just drilling and completing wells. EOG built an entire ecosystem of innovation. They developed proprietary seismic interpretation software that could identify "sweet spots" within shale formations. They created automated drilling systems that adjusted in real-time to geological conditions. They even pioneered new sand mining and processing techniques that reduced proppant costs by 40%.

By 2016, EOG had achieved something remarkable: consistent profitability in a commodity business. While competitors lurched between boom and bust, EOG generated positive returns even when oil prices crashed. The secret was their relentless focus on cost reduction and efficiency gains. Every dollar saved on drilling was a dollar that went straight to the bottom line.

The culture Papa had built—one of engineering excellence, capital discipline, and contrarian thinking—had not only survived the leadership transition but thrived under it. EOG wasn't just another oil company anymore. It had become the template for how to build a sustainable energy business in the 21st century.

VI. The Premium Strategy Revolution (2016-Present)

The whiteboard in EOG's Houston conference room in early 2017 contained a simple equation that would revolutionize the oil industry: 30% after-tax return at $40 oil = Premium Well. For an industry accustomed to chasing production growth at any cost, this was heresy. But for EOG, it was the beginning of their most audacious strategy yet.

"Premium" is born. EOG establishes a new standard for capital allocation: the premium well, delivering a minimum 30% direct after-tax rate of return at $40 crude oil and $2.50 natural gas. We identified 6,000 premium net drilling locations. The concept was deceptively simple but operationally revolutionary. Instead of drilling every available location when oil prices rose, EOG would only drill wells that met this stringent threshold.

He established our "premium well" standard, one of the most strict investment hurdle rates in the industry, which became an incredible catalyst that tapped the EOG culture of creative thinking and innovation. This wasn't just financial engineering—it required a complete reimagination of how oil companies operate. Every aspect of the drilling and completion process had to be optimized to meet these returns. The implementation was ruthless in its efficiency. EOG's engineers developed what they called "precision targeting"—using advanced seismic data and machine learning algorithms to place horizontal wellbores within six-inch tolerances in formations 10,000 feet underground. They pioneered "Super Zipper" completions that allowed multiple wells to be fractured simultaneously, cutting completion times by 40%. Most remarkably, they achieved these efficiency gains while actually improving well productivity.

The 2020 crisis became the ultimate test of the premium strategy. At the start of the year, EOG doubled the internal hurdle rate for capital allocation from a minimum of 30% to 60% direct after-tax rate of return at $40 crude oil and $2.50 natural gas. This wasn't just raising the bar—it was launching it into the stratosphere. When the pandemic hit and oil prices briefly went negative, EOG's discipline paid off spectacularly.

EOG generated $1.6 billion of free cash flow which both paid the dividend and further shored up what was already an industry-leading balance sheet, all while WTI oil prices averaged less than $40 per barrel. While competitors hemorrhaged cash and slashed dividends, EOG actually increased its dividend by 30%. The premium strategy had proven its worth in the crucible of the worst oil market in modern history.

The technological innovations during this period read like science fiction. By leveraging the company's decentralized structure, EOG offset persistent inflationary pressure to limit well cost increases to just 7%. They increased the number of completed lateral feet per day by approximately 14% in 2023 through continuous pumping operations. They developed iSense®, a continuous methane leak detection system that could identify emissions invisible to the human eye.

But perhaps the most impressive achievement was what EOG didn't do. While competitors rushed to grow production when oil prices recovered above $100 per barrel in 2022, EOG maintained discipline. "There's no reason to consider growth until the market rebalances," Thomas said. This restraint allowed EOG to generate massive free cash flows while others chased growth at any cost. The discovery of new frontiers continued even as EOG perfected its existing operations. EOG has made a large natural gas resource play discovery on its Dorado prospect located in Webb County, Texas. A total of 21 trillion cubic feet (Tcf) of estimated net resource potential is contained in 700 feet of stacked pay in the Austin Chalk and Eagle Ford Shale formations. This wasn't just another gas discovery—it was potentially the lowest-cost natural gas play in America.

"We believe this prolific new discovery represents the lowest cost natural gas play in the U.S., which will be both operationally efficient and have a small environmental footprint," Thomas said. With a breakeven cost of less than $1.25 per Mcf, Dorado could compete with renewable energy on cost while providing the reliability that wind and solar couldn't match.

The leadership transition to Ezra Yacob in 2021 brought fresh energy to the premium strategy. Ezra Y. Yacob has 21 years of industry experience and 16 years of service with EOG. He established our "premium well" standard, one of the most strict investment hurdle rates in the industry. Under his leadership, EOG continues to push the boundaries of what's possible in shale development.

The technology stack EOG has built over this period reads like a Silicon Valley startup's pitch deck. Machine learning algorithms optimize drilling parameters in real-time. Automated drilling rigs adjust their trajectory based on geological data streaming from downhole sensors. Completion designs are customized for each well using proprietary software that simulates fracture propagation through different rock types.

But what truly sets EOG apart in this era is its financial discipline. While the industry celebrated $100+ oil prices in 2022-2023, EOG maintained its premium hurdle rates. The company generated massive free cash flows, returning 98% of 2024 free cash flow to shareholders—well in excess of their commitment to return a minimum of 70%.

The premium strategy has transformed EOG from a commodity producer into something closer to a technology company that happens to produce oil. Every well is a data point, every completion an experiment, every quarter an opportunity to optimize further. The result is a company that can generate superior returns at $40 oil while competitors need $60 or $70 to break even.

As we look at EOG today, the premium revolution continues to evolve. The company has moved beyond just drilling the best wells to creating an integrated system of production, processing, and marketing that maximizes value at every step. It's no longer just about finding oil—it's about finding oil that can be extracted profitably regardless of commodity prices, processed efficiently through proprietary infrastructure, and sold at premium prices through advantaged marketing arrangements.

VII. Financial Performance & Capital Allocation

The numbers tell a story that would make any Wall Street analyst reach for their calculator in disbelief. In the 14 years Papa headed up EOG, the company's market cap grew from $2 billion to $54 billion, and the stock value increased 2,200%. This wasn't a tech startup riding a wave of speculation—this was an oil company, in a commodity business, generating returns that would make Silicon Valley jealous.

The transformation becomes even more remarkable when you zoom out to see the full picture. From its separation from Enron in 1999 at around $2 billion market capitalization, EOG has grown to exceed $70 billion at various peaks, creating more than $68 billion in shareholder value. During a period when many energy companies destroyed capital, EOG compounded wealth at rates typically reserved for technology monopolies.

What makes EOG's financial performance exceptional isn't just the absolute returns—it's the consistency through cycles. During the 2014-2016 oil crash, when prices fell from $107 to $26 per barrel, EOG remained profitable while peers bled billions. In 2020, when oil prices briefly went negative, EOG generated $1.6 billion of free cash flow. This isn't luck; it's the result of systematic improvements in capital efficiency.

The secret sauce lies in EOG's countercyclical capital allocation. When oil prices crashed in 2008-2009, EOG accelerated its Eagle Ford leasing program, locking up 650,000 acres at rock-bottom prices. When prices crashed again in 2014-2016, EOG acquired Yates Petroleum's premium Permian acreage for $2.3 billion—assets that would be worth multiples of that price just a few years later. While others retreated, EOG advanced.

The dividend story exemplifies EOG's balanced approach to capital allocation. For the third year in a row, EOG increased the dividend at least 30% in 2020—during a pandemic and oil price collapse. Since 2000, EOG has raised its dividend 22 times, growing it from $0.09 per share annually to $3.90 per share in 2024, a compound annual growth rate exceeding 16%.

But dividends are just part of the shareholder return equation. EOG's share buyback program has been equally impressive, retiring over $10 billion in stock since 2021. The company doesn't just buy back shares mechanically—it accelerates purchases during market weakness and pulls back during exuberance. In 2024 alone, the company repurchased 25.8 million shares for $3.2 billion at an average price of $123 per share.

The balance sheet strength enables this flexibility. At December 31, 2019, EOG's total debt outstanding was $5.2 billion for a debt-to-total capitalization ratio of 19 percent. Considering $2.0 billion of cash on the balance sheet, EOG's net debt-to-total capitalization ratio was 13 percent. Many "investment grade" companies would kill for such metrics.

The working capital management deserves its own Harvard Business School case study. EOG pioneered "just-in-time" drilling, where rigs move seamlessly from one location to the next without downtime. They negotiate master service agreements with suppliers that lock in costs but allow volume flexibility. They even time completions to coincide with seasonal price strength in natural gas markets.

Return on capital employed (ROCE) tells the efficiency story. In the four years since COVID, we have earned an average 28% ROCE—a staggering number for a capital-intensive industry. For context, ExxonMobil, considered best-in-class among integrated oils, averaged about 10% ROCE over the same period. EOG generates nearly three times the return per dollar invested.

The free cash flow generation has been extraordinary. From 2020 to 2024, EOG generated over $25 billion in free cash flow while investing more than $20 billion back into the business. This dual achievement—massive cash generation while maintaining production growth—is virtually unprecedented in the energy sector.

Finding and development costs paint perhaps the clearest picture of EOG's operational excellence. Finding and development cost, excluding price revisions, decreased in 2024 to $6.68 per Boe. The industry average hovers around $15-20 per BOE. EOG finds and develops reserves at one-third the cost of peers, a sustainable competitive advantage that compounds over time.

The market has rewarded this performance. EOG's stock has outperformed the S&P 500 over virtually every time period since 2000. A $10,000 investment at the time of separation from Enron would be worth over $350,000 today, assuming dividend reinvestment. The same investment in the S&P 500 would be worth about $65,000.

But perhaps the most impressive financial metric is one that doesn't appear on any income statement: optionality value. EOG's 11,500 premium drilling locations represent decades of high-return investment opportunities. At current commodity prices and using EOG's hurdle rates, these locations have a net present value exceeding $100 billion—well above EOG's enterprise value.

The capital allocation framework EOG has developed—premium returns, countercyclical investment, balanced shareholder returns—has become the template for the industry. Competitors now tout their own "premium" inventories and return frameworks, though few can match EOG's execution.

As CFO Tim Driggers noted in a recent call, since the shift to premium, EOG has retired bond maturities totaling about $2 billion. The company's plans are to retire another $1.25 billion in 2023 when the bond matures. This systematic deleveraging during good times ensures EOG has dry powder when opportunities emerge during downturns.

The financial discipline extends to hedging strategy. Unlike peers who hedge mechanically, EOG hedges opportunistically, locking in prices when markets offer attractive premiums but maintaining exposure to upside. This balanced approach has added billions in value over the years while providing downside protection during crashes.

VIII. Operational Footprint & Asset Portfolio

Stand on a platform above EOG's operations center in Houston, and you're looking at the nerve center of American energy production. Giant screens display real-time data from thousands of wells scattered across the continent—each dot representing millions of dollars of investment, billions of cubic feet of reserves, and decades of engineering innovation. The portfolio EOG has assembled isn't just large; it's strategically positioned in every major U.S. shale play that matters.

As of December 31, 2020, the company had 3.219 billion barrels of oil equivalent of estimated proved reserves, of which 98% was in the United States. The reserves were 51% petroleum, 22% natural gas liquids, and 27% natural gas. This balanced commodity mix provides natural hedging—when oil prices fall, NGL and gas often provide support, and vice versa.

The crown jewel remains the Eagle Ford in South Texas. As of December 31, 2020, EOG was the largest petroleum producer in the Eagle Ford Group. With 565,000 net acres after recent bolt-on acquisitions, EOG's Eagle Ford position generates over 170,000 barrels of oil equivalent per day. The company has drilled over 5,000 wells in the play, yet still has thousands of premium locations remaining.

The Delaware Basin represents EOG's growth engine. Following the Yates acquisition, EOG holds 424,000 net acres in the core of the Delaware, with stacked pay targets including the Wolfcamp, Bone Spring, and Leonard formations. Production from the Delaware now exceeds 200,000 BOE per day and continues growing as EOG shifts capital to this lower-cost basin.

The Bakken remains a cash flow machine despite being EOG's oldest shale play. The company holds 600,000 net acres in North Dakota, with production averaging 25,000 BOE per day. While EOG has reduced activity here in favor of higher-return opportunities elsewhere, the Bakken assets generate substantial free cash flow with minimal capital investment.

The Powder River Basin in Wyoming emerged as a surprise winner. What started as a tag-along in the Yates deal has become a core asset, with 400,000 net acres prospective for the Turner, Parkman, and Niobrara formations. The geology here is simpler than the Permian, leading to more consistent well results and lower drilling costs.

The DJ Basin in Colorado rounds out the Rockies portfolio with 35,000 BOE per day of production. Despite regulatory challenges in Colorado, EOG's operational excellence allows it to generate strong returns while exceeding the nation's most stringent environmental standards.

But the real strategic masterstroke is EOG's infrastructure investments. The Verde Pipeline, a 36-inch natural gas pipeline from the Dorado field to Agua Dulce hub, provides EOG with advantaged market access. Rather than selling gas at the wellhead for whatever local prices offer, EOG can access premium markets along the Gulf Coast. The infrastructure story extends beyond pipelines. Pecan Pipeline Company's Verde Pipeline can move up to 1.0 Bcf/d of producer EOG Resources' natural gas production from Webb County, Texas, in the Eagle Ford producing region to the Agua Dulce hub in southern Texas. We also progressed two strategic infrastructure projects last year: the 36 inch Verde pipeline which runs from our Dorado natural gas asset to Agua Dulce and provides access to Gulf Coast market centers and the Janus natural gas processing plant in the Delaware Basin.

The international footprint, while smaller, provides strategic value. Trinidad operations generate stable cash flows through long-term contracts with government-backed buyers. The production there—about 25,000 BOE per day—might seem insignificant compared to U.S. operations, but the stability and premium pricing make these assets valuable portfolio diversifiers.

The geographic diversification provides natural hedging against regional issues. When winter storms shut down Texas production in February 2021, EOG's Rockies and Bakken assets continued operating. When Colorado imposed stringent drilling regulations, EOG shifted capital to Texas and New Mexico. This flexibility is a luxury few competitors possess.

But what truly distinguishes EOG's portfolio is the quality gradient. Not all acres are created equal, and EOG has systematically high-graded its position through trades, sales, and selective development. The company divested the rest of its "noncore, sub-premium" Marcellus Shale position in the third quarter for proceeds of about $130 million. Meanwhile, it continues accumulating tier-one acreage through bolt-on acquisitions that rarely make headlines but consistently add value.

The data infrastructure overlaying these physical assets is equally impressive. EOG operates one of the energy industry's most sophisticated data analytics platforms, processing terabytes of geological, production, and operational data daily. This isn't just about tracking production—it's about optimizing every aspect of the operation in real-time.

The logistics network EOG has built deserves special mention. Beyond pipelines, the company operates rail terminals, truck loading facilities, and even owns railcars. This multi-modal transportation capability allows EOG to chase the best prices across multiple markets, adding dollars per barrel to realized prices.

Water management, often overlooked, has become a competitive advantage. EOG operates sophisticated water recycling facilities that can process millions of gallons daily, reducing both costs and environmental impact. In water-scarce regions like the Permian, this capability is worth billions in avoided costs and operational flexibility.

The land position itself tells a story of strategic foresight. EOG holds approximately 7,200 total net well locations in the Eagle Ford alone, with about 6,000 wells still remaining to be drilled. At current drilling rates, this represents decades of inventory. But it's not just about quantity—these are predominantly held-by-production acres in the sweet spots of each formation.

Looking at EOG's portfolio today, you see an energy company built for any price environment. High oil prices? The premium inventory generates massive cash flows. Low prices? The lowest-cost assets remain profitable while high-cost competitors struggle. Natural gas rally? Dorado provides exposure. This isn't luck—it's the result of two decades of strategic positioning.

IX. Technology & Innovation Legacy

Walk into EOG's technology center in Houston, and you might mistake it for a Silicon Valley startup. Engineers huddle around screens displaying 3D seismic data that looks like abstract art. Data scientists debate machine learning algorithms. Geologists manipulate holographic representations of rock formations 10,000 feet underground. This is where EOG's competitive advantage is forged—not on drilling rigs, but in laboratories and server rooms.

EOG pioneered horizontal drilling and hydraulic fracturing techniques that became industry standard. But saying EOG "pioneered" these technologies understates their achievement. They didn't just adopt existing techniques—they fundamentally reimagined how oil could be extracted from rock. The company developed new drilling fluids and proppants that could withstand extreme pressures and temperatures. They applied data analytics and AI for automation before "digital transformation" became a corporate buzzword.

The evolution of EOG's completion designs illustrates this innovation trajectory. In 2010, a typical EOG well might have 20 fracturing stages along a 5,000-foot lateral. By 2015, that had evolved to 40 stages along a 7,500-foot lateral. Today, EOG regularly completes wells with 60+ stages along 10,000-foot laterals, with each stage optimized using real-time data analytics.

The company commercialized the first enhanced oil recovery process, or EOR, in shale. This wasn't just incremental improvement—it was questioning fundamental assumptions about how oil moves through rock. While the industry assumed shale was too tight for EOR, EOG's engineers proved that injecting gas into fractured shale could increase recovery rates by 30-50%.

The proprietary technologies EOG has developed read like a patent portfolio from multiple companies. iSense®, their continuous methane leak detection system, can identify emissions invisible to traditional monitoring. Their "Super Zipper" completion technique allows multiple wells to be fractured simultaneously, cutting completion times in half. Their drilling fluids reduce torque and drag by 40%, allowing longer laterals to be drilled faster.

But perhaps EOG's greatest innovation is organizational rather than technical. While competitors rely on service companies like Halliburton and Schlumberger for critical technologies, EOG develops most innovations in-house. This vertical integration of R&D provides multiple advantages: faster iteration cycles, proprietary knowledge that competitors can't access, and the ability to customize solutions for specific geological challenges.

The data analytics capabilities EOG has built deserve special attention. Every well generates millions of data points—pressure readings, flow rates, chemical compositions, seismic signatures. EOG's systems process this data in real-time, using machine learning algorithms to optimize everything from drill bit rotation speed to fracturing fluid viscosity. One EOG engineer described it as "playing three-dimensional chess where the board changes every move."

The company's approach to spacing optimization exemplifies this data-driven innovation. Early shale development used geometric spacing—wells placed on regular grids regardless of geology. EOG pioneered variable spacing based on rock properties, stress fields, and production data. The result: 30% more oil from the same acreage.

Continuous improvement has reduced spacing from 130-acre to 65-acre units in the Eagle Ford while maintaining well productivity. This isn't just drilling more wells—it's understanding subsurface drainage patterns with precision that would have seemed impossible a decade ago.

The automation systems EOG has deployed are years ahead of competitors. Drilling rigs adjust parameters automatically based on real-time data. Completion operations run 24/7 with minimal human intervention. Production facilities self-optimize, adjusting pressures and flow rates to maximize output while minimizing costs.

EOG's innovation extends to seemingly mundane areas that have massive economic impact. They developed new proppants—the sand pumped into fractures to keep them open—that increase conductivity by 50%. They pioneered new chemical tracers that allow engineers to understand which fracture stages are contributing to production. They even innovated in logistics, developing systems to move millions of pounds of sand and millions of gallons of water with military precision.

The knowledge management systems EOG has built ensure innovations spread rapidly across the organization. A breakthrough in the Permian Basin is immediately shared with teams in the Eagle Ford and Bakken. Best practices are codified into standard operating procedures updated weekly. The company operates more like a technology platform than a traditional oil company.

The talent strategy supporting this innovation is equally sophisticated. EOG recruits petroleum engineers, but also data scientists, software developers, and materials scientists. The company's internship program is as competitive as those at Google or Goldman Sachs. Once hired, employees enter a culture that rewards experimentation and tolerates intelligent failure.

The R&D budget, while not publicly disclosed in detail, is estimated at hundreds of millions annually—multiples of what similar-sized E&Ps spend. But the return on this investment is evident in EOG's industry-leading metrics: lowest finding and development costs, highest well productivity, best capital efficiency.

Looking forward, EOG's innovation pipeline includes technologies that sound like science fiction. They're experimenting with autonomous drilling rigs that can operate without human intervention. They're developing new completion fluids that change viscosity based on temperature and pressure. They're even exploring quantum computing applications for seismic processing.

The cumulative effect of two decades of innovation is a technological moat that competitors can't easily cross. Even if a competitor acquired EOG's current technology stack, they'd lack the organizational knowledge to implement it effectively. The innovations are embedded in processes, encoded in software, and embodied in a culture that views every problem as an opportunity for improvement.

X. Challenges & Controversies

Not everything in EOG's story gleams with success. Behind the impressive returns and technological achievements lie challenges that threaten the company's future and controversies that tarnish its reputation. Understanding these headwinds is crucial for assessing whether EOG's premium strategy can endure.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube