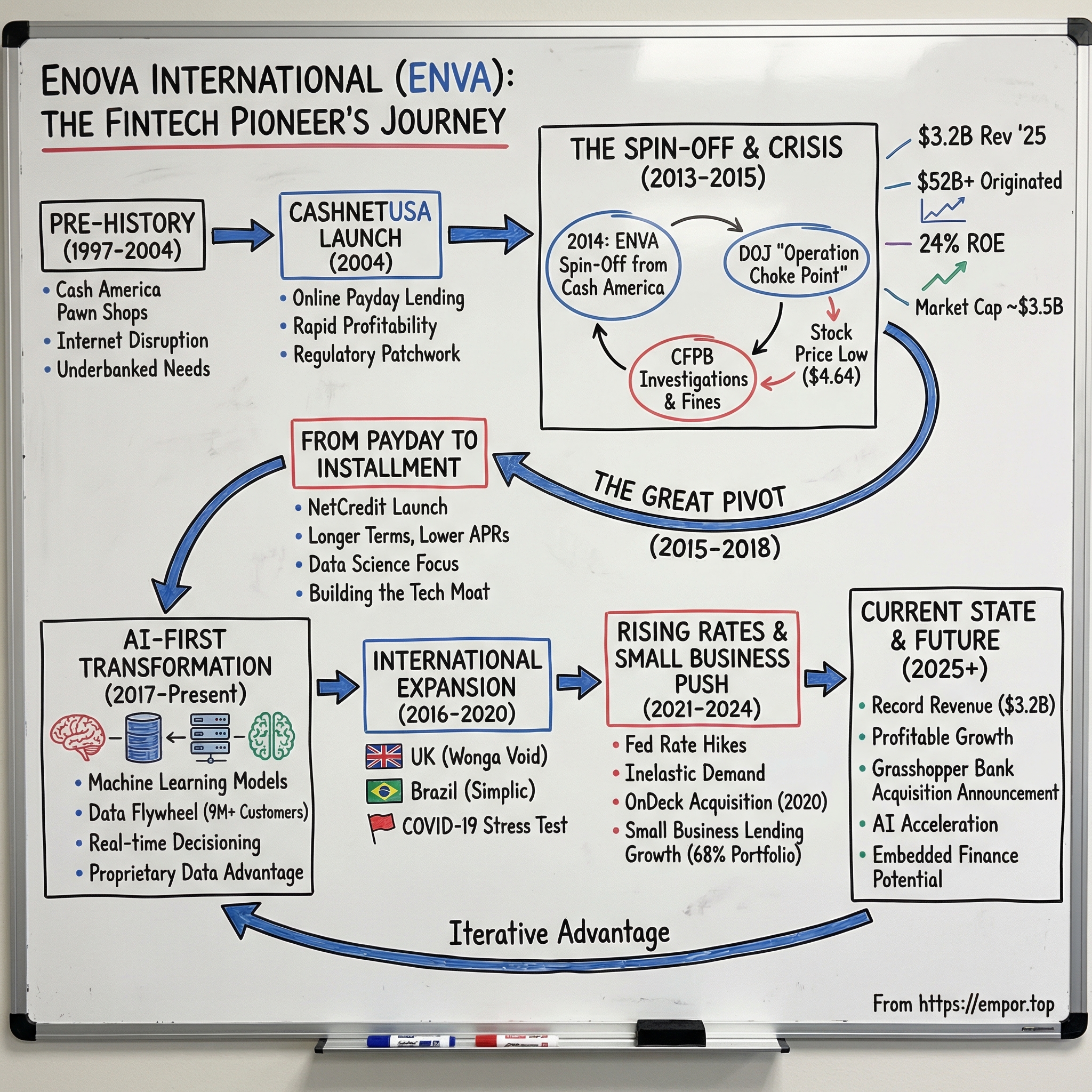

Enova International: The Fintech Pioneer You've Never Heard Of

I. Introduction & Episode Roadmap

Here is a number that should make you sit up: three point two billion dollars.

That was Enova International's revenue in 2025. Not projected, not annualized from one good quarter, but actual full-year revenue from a company most fintech enthusiasts could not name if you spotted them the first three letters.

While the Affirms and SoFis of the world burned through billions of venture capital chasing profitability, Enova quietly built a lending machine that has now served over nine million customers and originated more than fifty-two billion dollars in loans. It trades on the New York Stock Exchange under the ticker ENVA. It returned twenty-four percent on equity last year. And it has been profitable in virtually every year of its existence.

Yet if you polled a hundred investors at a fintech conference, maybe three could tell you what Enova actually does.

The central mystery of the Enova story is this: How did a subsidiary of a pawn shop operator become one of the most sophisticated AI-powered lenders in the United States? The answer involves tribal lending scandals, a Department of Justice investigation, a once-in-a-generation pandemic, and a quiet pivot from payday loans to machine-learning-driven installment credit that produced one of the best risk-adjusted track records in consumer finance.

The reason you have never heard of Enova is partly by design and partly by stigma. The company lends to subprime and near-prime borrowers at annual percentage rates that can exceed two hundred percent. That is not a typo. Consumer advocacy groups have labeled the company a repeat offender. The Consumer Financial Protection Bureau fined it fifteen million dollars in 2023. ESG-focused funds will not touch it. The business sits at the uncomfortable intersection of financial necessity and political controversy, which means that despite generating more revenue than Affirm or SoFi, Enova rarely appears on any fintech "best of" lists.

What follows is the full story: from pawn shops to artificial intelligence, from regulatory near-death to record profits, from a four-dollar stock price to a market capitalization north of three billion dollars. Along the way, we will unpack the business model that makes lending at triple-digit APRs not just viable but defensible, the technology moat that competitors have struggled to replicate, and the strategic chess moves that positioned Enova as an unlikely survivor in one of the most scrutinized corners of American finance.

The key inflection points are the CashNetUSA launch in the mid-2000s, the DOJ and CFPB confrontations that nearly killed the business, the pivot from single-payment payday loans to multi-payment installment credit, the OnDeck acquisition during COVID, the AI-first transformation of the underwriting engine, and the December 2025 announcement that Enova would acquire a bank. Each one reshaped what the company is and what it can become.

For a sense of the journey: at its January 2016 nadir, Enova's entire market capitalization was roughly one hundred and fifty million dollars. As of early 2026, the company is worth approximately three and a half billion. That is a twenty-fold increase in a decade, generated not by hype or speculation but by steady, profitable growth in a market that most Silicon Valley investors find distasteful. The Enova story is, in many ways, the anti-unicorn narrative: no celebrity founders, no splashy product launches, no viral growth, just relentless execution in a difficult market with difficult customers and difficult regulators.

To understand how they got here, we need to start not with algorithms or APRs, but with something much older: pawn shops.

II. The Classified Ads Empire: Pre-History (1997-2004)

In the late 1990s, Cash America International was the largest pawn shop operator in the United States. Founded in 1984 in Fort Worth, Texas, Cash America had grown from a single storefront into a publicly traded empire of over five hundred locations, lending money against collateral like jewelry, electronics, and firearms. It was a brick-and-mortar business in every sense: you walked in, handed over your guitar, and walked out with cash.

But Jack Daugherty, Cash America's CEO in the early 2000s, recognized something that most of his industry peers missed. The internet was not just disrupting media and retail; it was about to transform the way underbanked Americans accessed credit. Craigslist was eating newspaper classifieds. Amazon was eating bookstores. And the roughly sixty million Americans who lacked meaningful access to traditional banking were starting to go online to search for emergency loans.

The context matters here. The payday lending industry had grown from a few hundred storefronts in the early 1990s to more than twenty thousand locations by 2000. Meanwhile, mainstream banks largely refused to serve customers with credit scores below six hundred. If you were a single mother whose car broke down and you needed eight hundred dollars before your next paycheck, your options were a pawn shop, a payday lender charging fifteen dollars per hundred dollars borrowed for two weeks, or asking your family. The demand was enormous, chronic, and almost entirely unmet by the formal financial system.

Cash America saw the opportunity and acted. In 2004, they launched CashNetUSA, an online payday lending platform that allowed customers to apply for short-term loans entirely through a web browser. No storefront visit required. No collateral needed. Just an application, a bank account number, and a decision delivered in minutes.

The platform turned profitable within eleven months of launch, a speed that stunned even its creators. To put that in perspective, most fintech startups spend three to five years burning cash before reaching profitability, if they ever do. CashNetUSA did it in under a year. The product-market fit was not subtle; it was explosive. Millions of Americans needed fast cash and were willing to pay significant fees to get it. The only question was whether you could build the technology to reach them online.

Cash America consolidated full ownership, paying approximately seventy million dollars to formalize its control of the online operation.

The online business had fundamentally different economics from the pawn shop chain. The marginal cost of serving an additional online borrower was near zero, compared to the real estate, staffing, and inventory costs of a physical pawn location. Customer acquisition could be measured and optimized through digital marketing. And the data exhaust from thousands of online applications created something the pawn shops never had: a growing dataset that could be used to make better lending decisions over time.

The regulatory landscape, however, was a patchwork nightmare. Payday lending was regulated state by state, with each jurisdiction setting its own rules on maximum loan amounts, fee structures, and rollover policies. Some states banned payday lending outright. Others had few restrictions. This created an environment where operators had to maintain licenses in dozens of jurisdictions and navigate a constantly shifting set of rules.

It also created a moat, although nobody thought of it that way at the time. Getting licensed in thirty or forty states was expensive, time-consuming, and bureaucratically exhausting. Any new entrant would have to spend years and millions just to reach the same geographic footprint.

By 2012, Cash America's online lending division had grown into a significant business. But it sat awkwardly inside a company whose core identity was still physical pawn shops. The online operation wanted to invest aggressively in technology, data science, and new credit products. The pawn side wanted stability, dividends, and the slow steady cash flow of a mature business. Something had to give.

III. The Birth of Enova: The 2014 Spin-Off from Cash America

On the morning of November 13, 2014, trading screens across Wall Street displayed a new ticker symbol: ENVA. Cash America International had completed the spin-off of its online lending division into a standalone public company called Enova International. Shareholders received 0.915 shares of the new entity for every share of Cash America they held. It was a clean separation: Cash America kept its pawn shops, and Enova got the algorithms.

The thesis behind the spin-off was elegantly simple. Digital lending and pawn shops had different growth trajectories, different capital needs, different risk profiles, and critically, different investor bases. A technology-driven online lender growing at double digits deserved a different valuation multiple than a mature network of physical storefronts. Combined, the market could not properly value either business. Separated, each could pursue its own strategy and be judged on its own merits.

The man chosen to lead the newly independent company was David Fisher, who had been serving as CEO of the online lending division since January 2013 and became chairman of Enova at separation in October 2014.

Fisher's background defied the stereotype of a payday lending executive. His career had taken him through Prism Financial, the fast-casual restaurant chain Potbelly, and the online brokerage OptionsXpress, giving him a rare combination of financial services expertise and consumer-facing operational experience. He was not a pawn shop guy. He was not a traditional banker. He was an operator who understood technology, consumer behavior, and how to build scalable businesses.

The Potbelly experience is particularly revealing. Running a fast-casual chain teaches you about unit economics at the individual store level, about customer acquisition and retention, about operational consistency across hundreds of locations, and about the importance of getting the small things right every day. These are not the skills most people associate with fintech leadership, but they translate remarkably well to the discipline of running a lending operation where the difference between a profitable customer and a loss sits in the quality of individual decisions made millions of times per year.

Fisher brought one other critical quality: an engineer's instinct for measurement. From his earliest days at Enova, he pushed the organization to quantify everything, to treat every loan as an experiment, and to let data, not intuition, drive decisions. This mindset would prove essential in the years ahead.

The initial market reception was, to put it mildly, skeptical. Enova opened trading around fifteen dollars per share and immediately faced a barrage of uncomfortable questions. Was this really a technology company, or just a payday lender with a website?

The timing could not have been worse. The Obama administration was actively pursuing what became known as Operation Choke Point, pressuring banks to cut off services to industries the government considered problematic, and payday lending was near the top of that list. The CFPB, created by the Dodd-Frank Act in 2010 and led by the aggressive Richard Cordray, was drafting rules that could effectively eliminate high-cost short-term lending. Consumer advocacy groups called companies like Enova predatory.

In a world where "fintech" was starting to mean Stripe, Square, and LendingClub, Enova's brand of financial technology was decidedly unglamorous.

Fisher's positioning was deliberate: "We are a technology company that happens to do lending." It was a statement designed to reframe the narrative, but in 2014, the market was not buying it. Enova's portfolio at launch included CashNetUSA for payday and short-term loans, the emerging NetCredit brand for installment loans, and a small international operation. The company had approximately eight hundred million dollars in revenue and was profitable. And almost nobody on Wall Street wanted to own it.

The stock drifted lower throughout 2015, eventually hitting an all-time low of four dollars and sixty-four cents in January 2016. At that price, the market was essentially saying Enova was worth less than the annual revenue it generated. For investors willing to look past the headlines, this was either a value trap or the opportunity of a decade.

The answer depended entirely on whether David Fisher could navigate the company through what was about to become an existential crisis. And to understand the severity of what was coming, you need to appreciate a peculiar feature of American financial regulation: the government can effectively destroy a legal business not by banning it, but by cutting off its access to the banking system.

IV. Existential Crisis: The DOJ Settlement & CFPB Era (2013-2015)

In the summer of 2013, the Department of Justice launched Operation Choke Point. The program's stated aim was to combat fraud by pressuring banks to terminate relationships with businesses the DOJ deemed high-risk. In practice, it became a blunt instrument targeting entire industries, and payday lending was squarely in the crosshairs.

Banks began receiving informal guidance from regulators that maintaining accounts for payday lenders could attract enhanced scrutiny. One by one, financial institutions started closing the accounts of online lending companies, cutting off their ability to process payments and fund loans.

For Enova, still operating as Cash America's online division during the early phase of this campaign, the pressure was immediate and severe. The company relied on bank partnerships to originate loans in certain states and to process ACH transactions with borrowers. When those banking relationships came under threat, the operational foundation of the business was at risk.

This was not a theoretical concern: several smaller online lenders were effectively shut down when their banks abandoned them. Imagine building a restaurant and then learning overnight that your credit card processor, your food supplier, and your landlord all want to sever ties simultaneously. That is what Operation Choke Point felt like for online lenders.

The regulatory pressure only intensified. The CFPB had been building cases against online lenders, and Enova's practices came under formal investigation. The core issues centered on how the company serviced loans, communicated with borrowers, and managed collections. In 2019, the CFPB imposed a consent order requiring Enova to pay a civil money penalty of three point two million dollars over allegations of deceptive practices in loan servicing. It was the first formal regulatory mark on the newly independent company's record.

But the more existential threat came from the proposed rules themselves. The CFPB under Cordray was drafting comprehensive payday lending regulations that, in their most aggressive form, could have required lenders to verify a borrower's ability to repay before issuing a loan.

For the payday lending model, where the entire value proposition rested on speed and minimal documentation, such a requirement would have been effectively fatal. If a lender has to spend hours verifying a borrower's income, expenses, and ability to repay a three-hundred-dollar two-week loan, the economics collapse entirely.

The proposed rules also targeted the practice of rolling over loans, which is where much of the industry's profit, and much of the consumer harm, was concentrated. A borrower who takes a payday loan and rolls it over four or five times ends up paying more in fees than they originally borrowed, a pattern that consumer advocates rightly identified as destructive.

Think about what this meant for Fisher and his team. They had just been spun off into an independent company, their stock was cratering, the Department of Justice was investigating their industry, and the primary federal regulator was openly discussing rules that could kill their core product. This was not a headwind. This was an existential threat.

Fisher's response was a strategic masterclass in survival, built on three pillars. First, transparency: Enova invested heavily in compliance infrastructure, hiring lawyers, building monitoring systems, and cooperating with investigations rather than stonewalling them.

Second, product evolution: the company began systematically shifting its portfolio away from single-payment payday loans toward longer-term installment products that were easier to defend politically and better for customer outcomes.

Third, and most importantly, Fisher made a bet on data science. If Enova could prove that its underwriting technology genuinely helped customers access credit responsibly, it would have a narrative that went beyond "payday lender with a website."

The strategic decision to move upmarket, to reduce reliance on payday products, and to invest in machine learning for credit decisioning was not made from a position of strength. It was made from a position of near-desperation. The stock was in free fall. The regulatory environment was hostile. And the company's reputation was terrible.

But the pivot was exactly right. By committing to installment lending, Enova was moving toward higher-quality revenue, better unit economics, and a product that regulators found harder to attack. The payday loan could be described as a debt trap. An installment loan with a clear repayment schedule, declining balance, and the possibility of improved terms over time was something fundamentally different.

This period defined everything that followed. Companies that could not evolve were destroyed by the regulatory cycle. CURO Group, once a formidable competitor, eventually filed for Chapter 11 bankruptcy in March 2024. Elevate Credit was taken private in February 2023 for just sixty-seven million dollars, a fraction of its IPO valuation. Companies that could adapt, like Enova, emerged from the fire with better products, stronger technology, and a deeper understanding of the political landscape.

The experience gave Enova's leadership an institutional paranoia about regulatory risk that has shaped every strategic decision since: diversify products, diversify geographies, invest in compliance, and never assume that the rules of the game are fixed. In corporate strategy, there is a concept called "organizational scar tissue," the embedded memory of past crises that shapes future behavior. Enova has more scar tissue than almost any fintech in existence, and it shows in every risk management decision, every product design choice, and every regulatory engagement.

For investors, the regulatory crisis of 2013-2015 is the single most important piece of context for understanding Enova's subsequent strategic decisions. Every pivot, every investment, and every diversification move traces back to the lessons learned during those years.

V. The Great Pivot: From Payday to Installment Lending (2015-2018)

The difference between a payday loan and an installment loan might sound like a technicality, but it is actually one of the most consequential distinctions in consumer finance.

A payday loan is a single-payment product: you borrow five hundred dollars, and two weeks later, you owe five hundred plus a fee, typically around seventy-five dollars. If you cannot pay, you roll the loan over, incur another fee, and the cycle continues. The structure creates an inherent trap for borrowers living paycheck to paycheck.

An installment loan, by contrast, works like a miniature mortgage: it is amortized over months or years, with regular payments that reduce the principal balance over time. Each payment brings the borrower closer to being debt-free, and the lender has the ability to price the loan based on a much richer assessment of the borrower's capacity to repay.

For Enova, the shift from payday to installment was not merely a product change; it was a fundamental reinvention of the business model. Payday loans generated high-velocity, low-dollar revenue: small loans turning over every two weeks. Installment loans generated higher-balance, longer-duration revenue: larger loans paying down over six to thirty-six months.

Consider the math through a simple analogy. Customer acquisition cost in online lending typically runs between fifty and two hundred dollars, whether you are originating a three-hundred-dollar payday loan or a three-thousand-dollar installment loan. But the revenue from the installment loan is roughly ten times larger. One model requires a hamster wheel of constant re-acquisition. The other builds a durable asset that generates predictable cash flow over time.

The vehicle for this transformation was NetCredit, the brand Enova had launched to offer installment loans to what it called the "near-prime" borrower. These were customers with credit scores roughly in the five hundred to six hundred range: too risky for a traditional bank loan, but potentially much better credits than the typical payday borrower.

NetCredit offered unsecured personal loans with APRs that could reach nearly one hundred percent, high by mainstream standards but dramatically lower than the two-to-three-hundred-percent APRs on CashNetUSA's payday products.

The near-prime strategy was clever because it created what is essentially a credit ladder. A new customer might start with a small installment loan at a high rate. If they repaid successfully, they qualified for a larger loan at a lower rate. Over time, the best customers could graduate to terms that, while still expensive, were meaningfully better than where they started.

This created a virtuous cycle: repeat borrowers cost less to acquire, had lower default rates, and generated more lifetime revenue. The data from each repayment cycle fed Enova's underwriting models, making the next lending decision more accurate. Think of it as a gym membership model applied to credit: customers who proved their reliability earned better terms, which gave them a reason to stay.

The technology underpinning this strategy was where Enova began to genuinely differentiate itself. Traditional consumer lenders relied on FICO scores and a handful of credit bureau data points to make lending decisions. Enova's approach was fundamentally different: ingest hundreds of data variables, including traditional credit data, bank account information, employment verification signals, and behavioral data from the application process itself, then run them through machine learning models that updated continuously. The system could render a credit decision in seconds while accounting for far more nuance than a simple credit score could capture.

By 2018, the pivot was showing results. Revenue, which had dropped from approximately eight hundred million dollars at the time of the spin-off to about six hundred and fifty million in 2015 as problematic products were wound down, recovered to eight hundred and forty million. More importantly, the mix had shifted: installment loans were growing rapidly while payday volumes stabilized.

The competitive landscape during this period was brutal but clarifying. Elevate Credit was pursuing a similar near-prime strategy with its Rise and Elastic brands. CURO Group was still heavily reliant on storefronts and short-term products. World Acceptance Corporation operated primarily through a branch-based model.

Among the pure online players, Enova had the advantage of scale, technology, and a head start in data accumulation. Every loan originated was another data point in the training set. Every default pattern observed was another signal for the models. By 2018, Enova had processed millions of applications, giving it a dataset that no new entrant could replicate without years of lending history and billions of dollars in originations.

The marketing evolution during this period was equally important but less discussed. In the payday era, customer acquisition was dominated by lead generation: purchasing clicks from aggregator websites that would send borrowers to multiple lenders simultaneously. It was a commoditized, expensive, and adversarial model. With installment lending, Enova began investing in brand-building for the NetCredit product, positioning it as a more responsible alternative to traditional payday loans. The brand strategy was never going to win creative awards, but it did something more valuable: it reduced customer acquisition costs and increased the proportion of direct traffic, borrowers who came to the site on their own rather than through a paid intermediary.

The financial proof points were accumulating. Revenue was growing. The loan portfolio was getting larger and longer-duration. Charge-off rates were manageable. And the stock, which had bottomed at under five dollars, was starting to recover as the market recognized that Enova was not going to die from regulation.

With the US model proving itself, Fisher turned his attention to a bigger question: could this playbook work outside America?

VI. Going Global: The International Expansion (2016-2020)

The decision to expand internationally was driven by a combination of opportunity and insurance. The opportunity was obvious: underbanked populations existed everywhere, and the digital lending playbook that worked in the United States could theoretically be adapted to other markets. The insurance motive was more pragmatic. If the CFPB succeeded in imposing stringent federal rules on high-cost lending, having revenue streams outside the US would be existentially important.

The United Kingdom was the first major target. The UK had its own thriving high-cost lending industry, dominated by Wonga, a company that had become a cultural phenomenon with its puppet-based television commercials and APRs exceeding one thousand percent. But Wonga's aggressive growth attracted regulatory attention, and the Financial Conduct Authority imposed a price cap on high-cost short-term credit in January 2015.

Wonga staggered under the new rules, received a flood of compensation claims from past borrowers, and collapsed into administration in August 2018. The collapse created a vacuum that Enova was positioned to fill.

Through its UK subsidiary, the company offered installment loan products designed to comply with the FCA's regulatory framework. The UK market offered several advantages: a centralized regulatory system, high internet penetration, and a sophisticated consumer credit infrastructure. Enova's UK operation grew steadily and became a meaningful contributor to international revenue.

Brazil presented a different kind of opportunity and a different kind of challenge. With a population of over two hundred million, one of the largest underbanked populations in the Western hemisphere, and rapidly growing smartphone adoption, Brazil looked like a massive addressable market. Enova entered through a brand called Simplic, targeting Brazilian consumers who lacked access to traditional credit.

But Brazil's credit culture, regulatory environment, and competitive dynamics were fundamentally different from the Anglo-Saxon markets Enova knew well. Consumer credit in Brazil was dominated by large domestic banks with extensive branch networks and deep customer relationships. Breaking in as a foreign online lender proved far harder than the initial thesis suggested.

The COVID-19 pandemic in 2020 served as a stress test for every aspect of the business. Collections became more difficult as economies locked down. Government stimulus programs temporarily reduced demand for emergency credit. The uncertainty forced Enova to dramatically tighten its underwriting globally, reducing originations to protect the balance sheet.

In the UK, the response was relatively smooth because the regulatory framework was clear and the government's support programs were well-designed. In Brazil, the challenges were more acute.

The lesson from international expansion was nuanced: digital lending is not a one-size-fits-all playbook. The data advantage Enova had built over a decade in the US did not automatically transfer to markets with different credit cultures and different data availability. Capital deployed internationally earned lower returns than capital deployed domestically, and the management team acknowledged as much by maintaining a predominantly US-focused investment strategy.

International operations by 2025 contributed a meaningful but still modest share of total revenue, with the UK as the anchor market.

The discipline to recognize when a strategy is not working as expected, and to allocate capital accordingly, is a management quality that investors should note. Many growth-stage companies fall in love with their international expansion thesis and continue pouring capital into underperforming markets long past the point of diminishing returns. Fisher's willingness to keep international investment measured, and to let the US business absorb the lion's share of growth capital, demonstrates an owner-operator mentality that is increasingly rare in public company management.

There is also a counterfactual worth considering. If Enova had deployed the capital spent on international expansion into US small business lending two years earlier, the company might be significantly larger today. But that calculus assumes perfect foresight. At the time, with US regulatory risk at its peak, the decision to diversify geographically was rational and defensible. The lesson is not that international expansion was a mistake, but that the returns on domestic innovation ultimately proved far more attractive.

But the real transformation was not happening in London or Sao Paulo. It was happening inside Enova's Chicago headquarters, where a team of machine learning engineers was building something genuinely unusual.

VII. The AI-First Transformation: Building the Tech Moat (2017-Present)

To understand what Enova built, consider first what traditional lending looks like. A borrower applies for a loan. A credit officer, or an automated system mimicking one, pulls a FICO score, checks the debt-to-income ratio, looks at employment history, and makes a binary decision: approve or deny.

The process is essentially the same whether the lender is JPMorgan Chase or a storefront payday lender. The inputs are standardized, the models are well-known, and the differentiation between lenders happens mostly on price and distribution, not on the quality of the credit decision itself.

Enova's vision, articulated by Fisher and his technology team starting around 2017, was to become something fundamentally different: an AI-first lender where the quality of the credit decision was the primary competitive advantage. The idea was not just to automate the traditional process but to reimagine it from the ground up.

Think of a FICO score as a single photograph of a borrower taken from one angle. What Enova was building was more like a three-dimensional video. Instead of relying on a handful of standardized inputs, the system would ingest hundreds of data variables in real time: traditional credit bureau data, alternative data sources like bank account transaction patterns, application behavior signals such as how quickly someone fills out a form and what device they use, and publicly available information. All of this flowed into machine learning models that rendered not just a binary yes-or-no, but a nuanced risk profile.

The proprietary decisioning platform processes applications through multiple layers of models running simultaneously. The first layer handles fraud detection: is this applicant who they say they are? Online lending attracts sophisticated identity fraud, and catching it before a dollar leaves the door is worth millions.

The second layer handles credit assessment: what is the probability of default at thirty, sixty, ninety days? This is where the alternative data matters most. Traditional credit scores might give the same rating to a gig worker with volatile income and a salaried employee going through a rough patch, but their repayment behaviors are fundamentally different. Enova's models can distinguish between them.

The third layer handles pricing optimization: what APR and loan size will maximize the lifetime value of this customer while keeping charge-offs within target? The fourth handles what the industry calls "next-best action," determining whether to offer the applicant a different product, a smaller loan, or decline them entirely.

The entire process takes seconds. A borrower fills out an application at two in the morning, and by the time they finish their cup of coffee, the system has evaluated hundreds of data points, cross-referenced them against patterns from millions of prior applications, and generated a tailored offer or decline. No human touches the decision.

What makes this system genuinely defensible is the data flywheel. By 2025, Enova had processed applications from over nine million customers, observed millions of repayment patterns across different economic cycles, and accumulated a dataset representing one of the most comprehensive records of subprime and near-prime borrower behavior in existence.

Each new application, each payment made or missed, each customer interaction feeds back into the models, making them incrementally more accurate. A new entrant trying to build a competing system faces what data scientists call a cold-start problem: without historical data, their models are less accurate, leading to higher charge-offs, which makes the business less profitable, which limits their ability to acquire more customers and generate more data. It is a classic flywheel, and the gap widens with every passing year.

The talent strategy was equally intentional. Enova, headquartered in Chicago rather than San Francisco or New York, positioned itself as a place where data scientists and machine learning engineers could work on problems with immediate, measurable impact. Unlike a Big Tech research lab where a model might take years to reach production, an Enova data scientist could build a model, deploy it, and see its impact on charge-off rates within weeks.

The return on investment showed up in the numbers. The net charge-off ratio in the fourth quarter of 2025 was eight point three percent, roughly in line with historical averages despite the portfolio nearly doubling in size over the prior two years. Simultaneously, approval rates improved as the models got better at identifying creditworthy borrowers. The system was approving more loans while losing money on a smaller percentage of them, a combination that is extremely difficult to achieve without sophisticated underwriting technology.

To grasp why this matters, consider what happens when a less sophisticated lender tries to grow. They approve more loans, but because their models are less accurate, a higher proportion of those loans default. The charge-off rate spikes. Profitability drops. They tighten credit, volume shrinks, and they are back where they started. Enova broke this cycle by investing in decisioning accuracy, allowing growth and credit quality to improve simultaneously. It is the difference between a car that goes faster by pressing the accelerator harder, which also burns more fuel and wears the engine, and one that goes faster because the engine itself has become more efficient.

The AI moat is reinforced by something less quantifiable but equally important: institutional knowledge. Enova's teams have spent over fifteen years learning the seasonal patterns of borrower behavior, the macroeconomic signals that predict deterioration, the fraud vectors that evolve, and the regulatory constraints that shape product design. This knowledge is embedded not just in algorithms but in organizational processes. It cannot be acquired through a licensing deal or replicated by hiring a few data scientists.

The strategy was working. But in early 2022, the Federal Reserve began raising interest rates at the fastest pace in four decades, and the entire fintech world held its breath.

VIII. The Rising Rates Era & Small Business Push (2021-2024)

When the Federal Reserve began its rate-hiking campaign in March 2022, the fintech world braced for impact. Companies like LendingClub, Upstart, and SoFi had built their businesses in a zero-rate environment where capital was cheap and abundant. As the federal funds rate climbed from near zero to over five percent in eighteen months, origination volumes plummeted across the industry. LendingClub's share price fell more than sixty percent from early 2022 to mid-2024. Fintech stocks cratered almost across the board.

Enova's reaction was the opposite. Between early 2022 and the end of 2024, the company's stock price rose from approximately thirty-eight dollars to over one hundred and five dollars. Revenue grew from one point seven billion to two point six billion. Originations hit record after record.

How was this possible? It is one of the most counterintuitive dynamics in all of financial services.

The answer lies in the nature of Enova's customer. When you are already borrowing at one hundred to three hundred percent APR, the Federal Reserve raising rates by five percentage points is essentially irrelevant to your decision-making. Enova's borrowers are not rate-sensitive in the way a mortgage applicant or prime credit card user is. They borrow because they need cash immediately, and their willingness to pay is driven by the urgency of their situation, not by the prevailing benchmark rate. The demand is largely inelastic with respect to interest rates.

Enova did face higher funding costs as its securitization facilities and credit lines repriced. Net revenue margin compressed from about sixty-four percent in 2022 to fifty-eight percent in 2023.

But when your earning asset yields two hundred percent and your cost of funds goes from four percent to nine percent, the arithmetic still works comfortably. The spread was simply too wide for the rate hikes to meaningfully damage the business model. This is fundamentally different from a mortgage lender or a prime credit card issuer, where the spread between lending rate and funding cost might be three to five percentage points. Enova's spread is measured in hundreds of percentage points, which makes the business model remarkably insensitive to changes in benchmark rates.

The more significant strategic development during this period was the aggressive expansion into small business lending.

The seeds had been planted in October 2020, when Enova acquired OnDeck Capital in the depths of the COVID-19 pandemic. OnDeck was a pioneer in online small business lending, founded in 2007, and had gone public in 2014. But the pandemic devastated its loan portfolio, and the company's stock price collapsed.

Enova acquired OnDeck for approximately one hundred and twenty-two million dollars, a fraction of its previous market value, and recorded a one hundred and sixty-four million dollar gain on the bargain purchase, meaning the company was worth more in pieces than the price Enova paid for it. It was the kind of deal that only happens during a crisis, and Fisher seized it.

The acquisition transformed Enova's addressable market. Consumer installment lending to subprime borrowers is meaningful, but it has natural limits: loan sizes are small, competition from informal credit sources is intense, and political scrutiny is relentless. Small business lending offered larger ticket sizes, more diverse cash flows, a commercial rather than consumer regulatory framework, and borrowers who could be underwritten using business performance data.

A small business loan of fifty thousand dollars generated far more revenue per origination than a consumer loan of three thousand dollars. And the political dynamics were entirely different: nobody calls a small business loan predatory.

The growth was striking. By the fourth quarter of 2025, small business lending accounted for sixty-eight percent of Enova's total portfolio, or approximately three point three billion dollars. Small business originations in that quarter reached one point six billion, up forty-eight percent year over year, marking the eighth consecutive quarter of growth. Consumer originations, by contrast, grew just two percent.

The portfolio mix had essentially inverted: what had been a consumer-first company was now predominantly a small business lender. This is one of the most important and underappreciated aspects of the Enova story. Many investors still think of Enova as a payday lender, but the reality is that two-thirds of the loan book now consists of small business credit. The narrative has not caught up to the business, which is both a risk, in the sense that the market does not properly value the transformation, and an opportunity, in the sense that recognition of this shift could drive meaningful multiple expansion.

The competitive dynamics in small business lending were different from consumer. Instead of competing with payday lenders and near-prime consumer fintechs, Enova was now competing with Square (now Block), Shopify Capital, Amazon Lending, and traditional banks.

But Enova's technology advantage translated: the same machine learning infrastructure could assess small business risk using revenue data, bank transaction patterns, and industry-specific signals. OnDeck's brand carried credibility with small business owners who would never have considered a product from CashNetUSA.

There is an interesting strategic parallel here to Amazon's evolution. Amazon started as a bookseller and expanded into electronics, then everything, then cloud computing. Nobody calls Amazon a bookstore anymore. Similarly, Enova started as a payday lender and expanded into installment loans, then small business credit, and potentially soon into banking itself. At what point does the original identity cease to define the company? That question is central to the Enova investment thesis, because the valuation discount is largely a function of the market seeing a payday lender, while the financial statements increasingly describe a diversified lending platform.

IX. Current State & Business Model Deep Dive

As of early 2026, Enova International operates four principal business lines. NetCredit serves near-prime consumers with installment loans in thirty-seven states, typically at APRs approaching one hundred percent. CashNetUSA provides shorter-term consumer credit products including payday-style loans and lines of credit. OnDeck and Headway Capital serve small businesses with term loans and revolving lines of credit. And the international division, anchored by the UK operation and the Simplic brand in Brazil, serves consumers overseas.

The customer who borrows from Enova is not the person most fintech companies talk about. The average NetCredit borrower earns approximately thirty-nine thousand dollars per year and has a credit profile that places them firmly outside the mainstream banking system. These are people whose financial lives are characterized by income volatility, thin credit files, and limited access to traditional financial products.

They work as hourly employees, gig workers, and small business owners. They need credit for car repairs, medical bills, rent shortfalls, and business emergencies. They are willing to pay high interest rates because the alternative is far worse.

Here is the uncomfortable truth that makes Enova's business model work: for the borrower whose car breaks down and who will lose their job without transportation, an expensive loan may be vastly better than no loan at all. For the single mother facing an eviction notice, the relevant comparison is not a bank loan she cannot get but the consequences of not having the money at all. Whether triple-digit APR lending is predatory or pragmatic depends entirely on which alternative you use as the benchmark.

The unit economics work as follows. Customer acquisition cost typically runs between fifty and two hundred dollars. For an installment loan of three thousand dollars with a twelve-month term and an APR near one hundred percent, the revenue generated more than covers the acquisition cost, the expected credit losses, and the cost of capital, leaving a meaningful profit margin. When that customer returns for a second loan, the acquisition cost drops to nearly zero, and the unit economics become excellent.

The charge-off rate, the percentage of loans ultimately written off as uncollectable, ran at approximately eight to nine percent across the portfolio in 2025. That sounds alarming compared to a traditional bank's two to three percent, but Enova prices for this level of loss. The relevant metric is net revenue margin, which measures revenue after credit losses, and that figure came in at sixty percent in the fourth quarter of 2025.

Enova funds its lending through multiple securitization facilities and revolving credit lines with institutions including Jefferies, Banc of California, and Bank of Montreal. Total debt stood at approximately four and a half billion dollars at year-end 2025, against a total loan portfolio of four point nine billion. Total liquidity of approximately one point one billion provides operational flexibility and protection against market disruptions.

The full-year 2025 financial profile: three point two billion in revenue, three hundred and eight million in net income, adjusted earnings per share of nearly thirteen dollars, and a return on equity of approximately twenty-four percent. The stock, trading around one hundred and forty dollars in early 2026, values the company at roughly twelve times trailing earnings and nine times forward earnings.

That valuation discount relative to the broader fintech sector, where companies routinely trade at twenty to thirty times earnings, reflects the market's perception of regulatory risk, ESG stigma, and institutional discomfort with triple-digit APR lending. To put the valuation gap in stark terms: SoFi Technologies, which generated roughly two point one billion in revenue in 2025 with significantly lower margins and a more recent profitability track record, trades at roughly four times the price-to-earnings multiple of Enova. The market is telling you it values SoFi's brand, customer demographic, and product suite at a massive premium to Enova's, despite Enova generating more revenue and significantly higher returns on equity.

The CFPB labeled Enova a "repeat offender" in a fifteen million dollar consent order in 2023 over allegations that the company debited customer accounts without authorization and misrepresented loan terms. That order was terminated in September 2025, but the designation itself signals ongoing regulatory attention that investors must weigh carefully. It is a material legal and reputational overhang that the market prices into the stock, and rightly so.

X. Strategic Frameworks: Porter's 5 Forces & Hamilton's 7 Powers

Analyzing Enova through the lens of competitive strategy reveals a business better positioned than its valuation suggests, but with genuine vulnerabilities that justify a degree of skepticism.

Starting with Porter's framework, competitive rivalry is medium-high. The subprime lending market is fragmented, with regional players, tribal lenders, traditional banks, and fintechs all competing for borrowers. But the fragmentation tells a story: CURO Group filed for Chapter 11 in 2024, Elevate Credit was taken private at a fraction of its IPO valuation. The attrition rate among competitors has been remarkably high, suggesting that while competition is intense, few players can sustain profitability over time.

The threat of new entrants is moderated by substantial barriers. State-by-state licensing represents years of regulatory investment. The technology barrier is rising as AI-driven underwriting becomes table stakes. Companies like Dave, Brigit, and MoneyLion have entered adjacent spaces with small-dollar cash advances and financial wellness tools, but their products do not directly compete with Enova's core lending.

Supplier power is relatively low. Enova has diversified funding sources across multiple securitization facilities and revolving credit lines, reducing dependence on any single capital provider. The talent market for machine learning engineers is competitive, but Enova has built a credible data science organization in Chicago without paying peak Silicon Valley premiums. Credit bureaus and alternative data vendors are commoditized services with multiple providers, limiting their ability to extract pricing concessions.

Buyer power is structurally low, which is simultaneously the source of Enova's profitability and the root of its political vulnerability. Subprime borrowers have limited alternatives by definition. The application friction and urgency of most borrowing needs creates high switching costs in practice. Demand is largely inelastic. But this dynamic is precisely what attracts regulatory attention and consumer advocacy opposition. The low buyer power is real, but it exists within a political context that can, and periodically does, change rapidly through legislative or regulatory action.

The threat of substitutes is the most dynamic force. Buy-now-pay-later products have captured some short-term credit demand. Credit cards, when available to near-prime borrowers, offer a lower-cost alternative. Employer-based lending programs are growing. Traditional banks have slowly moved downmarket with pre-qualified digital offers. None has eliminated demand for Enova's products, but collectively they represent an expanding set of alternatives.

Turning to Hamilton Helmer's 7 Powers framework, three powers stand out as genuinely strong.

Scale economies are real and significant. The fixed costs of Enova's technology platform, compliance infrastructure, and data science team are amortized over a growing loan portfolio. The marginal cost of originating the next loan is minimal.

Larger securitization deals also command tighter spreads: a billion-dollar securitization gets better terms than a hundred-million-dollar one, creating a funding cost advantage that scales with portfolio size. This is one of the primary reasons why smaller competitors have struggled to match Enova's profitability even when they offer similar products to similar customers.

Network economics are absent. Enova is a direct lender, not a platform connecting buyers and sellers. There are no direct network effects between borrowers: one customer getting a loan does not make the product more valuable for the next customer in the way that an additional user on a social network benefits all existing users. The data flywheel discussed earlier is sometimes confused with network effects, but it is more accurately described as a learning curve advantage or data scale economy.

Counter-positioning was historically important. When Enova launched CashNetUSA, traditional banks could not and would not serve subprime borrowers online. That gave Enova years of uncontested market development. Today, the advantage has faded as banks have developed digital lending capabilities, but the head start in data accumulation remains.

Switching costs are moderate. Borrowers can apply elsewhere, but the credit ladder creates retention: repeat borrowers receive better terms. Saved payment methods and familiar interfaces add behavioral friction to leaving.

Branding is a weakness. In subprime lending, the category stigma is so pervasive that even the best-managed company struggles to build a brand customers are proud to associate with.

The two most powerful forces are cornered resources and process power. The cornered resource is the data itself: over fifteen years of lending history, millions of unique borrower observations spanning multiple economic cycles. No competitor can replicate this without spending years and billions in originations. Layered on top is the licensing portfolio: regulatory approvals across dozens of states that took years to obtain.

Process power is the AI and machine learning capability: not just the algorithms, but the organizational expertise in deploying them, the institutional knowledge of subprime borrower behavior, and the continuous improvement loops that make models better with each cycle. This is the hardest power to build because it requires the intersection of data, talent, time, and organizational commitment. It cannot be bought.

Power ranking: cornered resource first, process power second, scale economies third. These advantages should persist for seven to ten years absent a dramatic regulatory change, but they remain vulnerable to a federal rate cap or a banking industry pivot to digital subprime lending.

The Helmer framework reveals something interesting about Enova: its strongest powers, data and process, are precisely the ones that are hardest for competitors to observe, understand, and replicate. A competitor can see Enova's loan terms, can match its marketing spend, can even hire away individual data scientists. But they cannot replicate fifteen years of lending data, and they cannot replicate the organizational learning that comes from processing millions of applications across multiple credit cycles, economic environments, and regulatory regimes. That is what makes these powers durable, even if the market does not fully appreciate them.

XI. Bull vs. Bear Case & Investment Lens

The bull case begins with the size of the market. Approximately sixty million Americans are subprime or credit-invisible, roughly one in five adults. Despite decades of effort, the subprime credit gap has not meaningfully closed. The demand for Enova's products is structural and persistent.

And the market may actually be growing. The gig economy, income volatility, rising healthcare costs, and the decline of employer-sponsored benefits are all pushing more Americans into the near-prime and subprime categories. The addressable market for Enova's products is not static; it is expanding even as the broader economy grows.

The financial track record is remarkable. Enova has been profitable through the 2008 financial crisis, the regulatory assault of 2013-2015, the COVID-19 pandemic, and the rate-hiking cycle. Revenue has grown from six hundred and fifty million in 2015 to three point two billion in 2025. Adjusted earnings per share grew forty-two percent in 2025 alone.

The technology moat continues to widen. Every day that passes, Enova processes more applications and refines its models. A competitor starting today would be fifteen years behind on data. The small business expansion opens a larger, less politically sensitive market. International operations provide geographic optionality.

The most intriguing element is the Grasshopper Bank acquisition announced in December 2025 for approximately three hundred and sixty-nine million dollars. If approved, Enova would become a bank holding company with access to deposit funding, which is significantly cheaper than the institutional securitization rates it currently pays. Management projected fifteen percent or greater adjusted EPS accretion in the first year and twenty-five percent or more once synergies are fully realized.

Beyond funding costs, a bank charter would allow Enova to export interest rates nationally regardless of state-level caps, resolving one of its most persistent operational constraints. At nine times forward earnings with twenty-plus percent growth guidance, Enova trades at a significant discount to the broader fintech sector. The discount is a function of the "sin stock" stigma that follows any company lending at high APRs: similar to how tobacco and gambling companies trade at lower multiples than their financial performance would warrant, Enova carries a permanent penalty for operating in a morally contested space.

The bear case centers on regulation. The CFPB labeled Enova a repeat offender in 2023. While the order was subsequently terminated, the political winds can shift quickly. A future administration could impose federal rate caps on consumer lending, effectively eliminating a significant portion of the consumer business.

The Grasshopper acquisition has already attracted opposition from consumer advocacy groups including the National Community Reinvestment Coalition and the National Consumer Law Center, who have urged regulators to reject the deal. If the bank charter is denied or approved with restrictive conditions, the strategic value diminishes substantially.

Recession risk is a permanent shadow. Enova's borrowers are the most financially fragile segment. In a severe downturn, charge-off rates would spike, originations would need to be curtailed, and the portfolio could shrink rapidly. The company navigated COVID by tightening credit dramatically, but a longer recession would test the model more severely.

The ESG stigma has real consequences. Many institutional investors explicitly exclude high-cost lenders. Short interest of seven point four percent, well above average, reflects meaningful active skepticism. The limited institutional ownership creates a narrower buyer base and may explain some of the persistent valuation discount.

Competition from better-capitalized players is a longer-term risk. If major banks aggressively moved into digital subprime lending using their vastly cheaper deposit funding, they could undercut Enova's pricing. BNPL, employer-based advances, and government programs could erode the addressable market. And there is always the possibility of a disruptive technological shift: embedded lending within payroll systems, crypto-based credit products, or government-sponsored alternatives that fundamentally change how the underbanked access credit.

There is also the myth-versus-reality question that every prospective investor must wrestle with. The consensus narrative is that Enova is a payday lender that makes money by trapping vulnerable people in cycles of debt. The reality, as the data shows, is more complicated: Enova has evolved far beyond payday lending, two-thirds of its portfolio is small business credit, its technology genuinely improves lending decisions, and many of its customers use the products responsibly for genuine financial needs. But the consensus narrative persists because it contains a kernel of truth, the APRs are genuinely high, and because it is psychologically easier to categorize a company as "good" or "bad" than to hold the nuance that it can be both helpful and expensive simultaneously.

For investors tracking Enova's ongoing performance, three key metrics matter most.

First, the net charge-off ratio by product and vintage. This reveals whether underwriting quality is improving, stable, or deteriorating. Stable or declining charge-offs amid growing originations confirms the AI models are working. Rising charge-offs in newer vintages would be an early warning sign of credit deterioration.

Second, the portfolio mix between consumer and small business lending. This signals diversification progress away from politically vulnerable products. The shift from thirty-two percent consumer and sixty-eight percent small business at year-end 2025 toward an even more business-weighted mix would indicate continued strategic execution.

Third, the outcome of the Grasshopper Bank regulatory approval process. This will determine whether Enova can fundamentally reduce its cost of capital and expand its operating model. It is the single most important binary event on the horizon.

XII. Playbook: Lessons for Builders & Investors

The Enova story yields lessons that extend well beyond subprime lending.

Regulatory moats are real, and they compound. The state-by-state licensing that makes Enova's business operationally complex also makes it strategically defensible. Every license is a barrier to entry. Every compliance system is a fixed cost that scales with volume. Companies that invest in regulatory expertise rather than fighting against regulation often find that compliance itself becomes an advantage.

Boring can be beautiful. There is no glamour in lending money to people with bad credit scores. No magazine covers, no keynote invitations, no podcast tour of the Valley.

But Enova has generated more revenue than most celebrated fintechs and has done it profitably, year after year, through multiple economic cycles. The relationship between a business's sex appeal and its economic returns is, at best, nonexistent. Warren Buffett made his fortune in insurance, railroads, and ketchup. The Enova story reinforces this principle.

Data compounds in ways that are nearly impossible to replicate. Enova's fifteen-plus years of lending data cannot be bought, cannot be copied, and gets more valuable with each passing day.

Any company building an AI-driven business should understand that the data acquisition strategy is the technology strategy. The algorithm is the easy part. The data that trains it, and the organizational knowledge of how to interpret and deploy it, is the hard part.

Survival through crisis creates organizational resilience. Companies that navigate existential threats emerge with institutional knowledge and risk management capability that untested competitors lack. Fisher's decision to use the regulatory crisis as impetus for strategic reinvention was the defining leadership move in Enova's history.

Product evolution signals strategic sophistication. The journey from payday to installment to small business lending reflects a management team that understands the difference between defending a product and defending a capability. Enova's core capability is technology-driven lending to underserved segments. The products through which that capability is expressed can and should evolve.

Genuine AI advantages require data, talent, time, and organizational commitment. They cannot be acquired by plugging into a large language model API or hiring a handful of data scientists. The barrier to replication is not algorithmic complexity; it is the accumulated weight of experience that no shortcut can replace.

Market perception and business reality can diverge for extended periods. Enova has been a stigmatized stock since inception. For investors who can tolerate the volatility, the political risk, and the social discomfort, this disconnect between perception and reality has historically been a source of returns.

Capital allocation discipline matters. The international expansion generated lower returns than domestic deployment. The willingness to acknowledge this shows a management team prioritizing returns over empire building. The OnDeck acquisition, by contrast, demonstrated excellent capital allocation: buying a valuable asset at a distressed price and integrating it into a faster-growing platform. The contrast between the two decisions, one cautious and one opportunistic, reveals a management team that understands both the power of patience and the importance of acting decisively when circumstances demand it.

Finally, the Enova story illustrates the power of iteration. Fifteen years of lending data, continuously refined through machine learning, creates an advantage that grows wider with each passing quarter. In a world where most companies talk about AI as a future aspiration, Enova has been deploying it operationally for nearly a decade. The gap between rhetoric and reality in AI is enormous across most industries. In Enova's case, the AI is not a slide in a pitch deck; it is the engine that determines whether the company makes or loses money on every single loan it originates.

XIII. Epilogue & Future Trajectories

On January 1, 2026, David Fisher stepped back from the CEO role he had held for thirteen years, transitioning to executive chairman. Steve Cunningham, previously the chief financial officer, took the reins. Scott Cornelis became CFO. The leadership transition was orderly and planned, designed to signal continuity rather than disruption. Cunningham knew every line of the balance sheet and every nuance of the business model from his years as CFO.

The most recent results, reported on January 27, 2026, showed a business still accelerating. Full-year 2025 revenue of three point two billion represented nineteen percent growth. Adjusted earnings per share grew forty-two percent. The portfolio hit a record four point nine billion.

Management's guidance for 2026 called for fifteen percent growth in originations and revenue with at least twenty percent growth in adjusted EPS. Those are not the growth rates of a company reaching maturity. They are the growth rates of a business that has found a larger addressable market in small business lending and is executing against it with improving efficiency.

The management transition itself bears watching. Fisher's fingerprints are on every aspect of Enova's strategy, from the regulatory navigation to the AI investment to the international expansion. Whether Cunningham, as capable as he is, can maintain the same strategic vision and operational intensity will be one of the key qualitative factors in the company's next chapter.

The defining event of 2026 will be the regulatory decision on the Grasshopper Bank acquisition. Grasshopper is a digital-first commercial bank headquartered in New York, focused on small business and startup banking. If approved, Enova transforms from a specialty finance company into a bank holding company with access to deposit funding and a national charter. If denied, it must find other paths to the same strategic objectives.

The strategic logic of the acquisition extends beyond simple cost-of-capital improvement. As a bank holding company, Enova would gain the ability to offer a broader range of financial products, deepen customer relationships, and potentially attract a different class of institutional investor. It would also gain the supervisory framework of bank regulators, which paradoxically could provide a more stable and predictable regulatory environment than the current patchwork of state-level oversight and CFPB enforcement actions.

The AI acceleration presents another frontier. Rapid advancement in machine learning techniques, including deep learning and reinforcement learning for dynamic pricing, could further widen the gap between Enova's decisioning capabilities and those of competitors. The company that spent fifteen years building a proprietary data advantage is extraordinarily well-positioned to benefit from improvements in the tools used to extract value from that data.

The embedded finance opportunity is perhaps the most intriguing long-term possibility. Just as Stripe enables any company to process payments, and Shopify Capital enables merchants to access loans without applying at a bank, there is a world in which Enova's decisioning technology could power lending for platforms that want to offer credit without building underwriting capabilities from scratch.

Imagine a gig economy platform that wants to offer its workers emergency advances, or a vertical SaaS company that wants to offer its small business customers working capital. Rather than building underwriting from scratch, they could plug into Enova's decisioning engine. This would represent a fundamentally different business model, a technology-licensing stream layered on top of direct lending, and it would leverage Enova's core asset, the decisioning platform, in an entirely new way.

There is also the question of independence. As a profitable, growing fintech with sophisticated technology, Enova could be an attractive acquisition target for a bank seeking digital lending capabilities, a private equity firm seeking cash-generative assets, or a larger fintech seeking to expand downmarket. The Grasshopper acquisition, if it goes through, could actually make Enova a more attractive acquisition target by simplifying the regulatory structure and improving the cost of capital. Alternatively, it could be the foundation for Enova to become a significantly larger, more diversified financial institution in its own right.

Consider the product innovation possibilities that a bank charter would unlock. Today, Enova is a lender. With deposit-taking capability, it could offer savings products, credit-building accounts, and a fuller suite of financial services to its existing customer base. The sixty million Americans who currently come to Enova only when they need a loan could become full-time banking customers. The lifetime value of each customer relationship could increase by multiples.

The bigger question that Enova raises is about financial inclusion, inequality, and the role of private capital in serving populations the traditional financial system has abandoned.

Sixty million Americans need credit and cannot get it from a bank. That number is not shrinking. The traditional banking system has shown little appetite for serving this population at scale. And government programs, while well-intentioned, have repeatedly failed to fill the gap. Into this void steps Enova, with all of its contradictions: profitable but stigmatized, technologically sophisticated but serving unsophisticated borrowers, growing rapidly in a category that many wish did not exist.

Enova has survived everything: regulatory assaults, pandemic-induced credit crises, rate spikes, reputational attacks, and competitive attrition that bankrupted multiple rivals.

The company that traded at four dollars in January 2016 hit an all-time high of one hundred and seventy-six dollars in February 2026. Whether it can thrive in the next decade depends on the same factors that have determined its fate in every previous chapter: the quality of its technology, the wisdom of its strategic choices, and the direction of the political winds.

XIV. Further Reading & Resources

For those looking to go deeper into the Enova story and the broader landscape of alternative consumer finance, the following resources provide essential context and complementary perspectives.

Enova International's 10-K filings from 2014 to the present, available through SEC.gov, are the definitive primary source for financial history, risk factor disclosures, and management discussion of strategy. The quarterly earnings calls, archived at investor.enova.com, provide real-time insight into management thinking and strategic priorities.

Lisa Servon's "The Unbanking of America" offers a deeply reported exploration of why millions of Americans choose alternative financial services over traditional banks, essential context for understanding Enova's customer base. The CFPB's payday lending reports from 2013 through 2019 document the regulatory environment that shaped Enova's evolution.

The House Committee on Oversight's Congressional report on Operation Choke Point provides the political context for Enova's formative crisis. Karen Mills' "Fintech, Small Business & the American Dream" offers perspective on the small business lending transformation Enova has embraced through the OnDeck acquisition.

Academic research on machine learning in credit decisioning and alternative data in underwriting provides the intellectual framework for understanding Enova's technology moat. Papers from the Federal Reserve Banks on the impact of alternative data on credit access are particularly relevant.

The OCC and FDIC's guidance documents on bank partnership models from the 2000s and 2010s offer essential regulatory context for understanding both the opportunities and constraints that shaped the online lending industry's evolution.

Robert Shiller's "The Subprime Solution" provides broader context on credit access and financial innovation, while "Portfolios of the Poor" by Collins, Morduch, Rutherford, and Ruthven remains the essential text for understanding the financial lives of low-income households globally. Together, these works offer the intellectual foundation for understanding not just what Enova does, but why the demand for its products exists in the first place and why it is unlikely to disappear anytime soon.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube