Enanta Pharmaceuticals: The Science of Viral Disruption

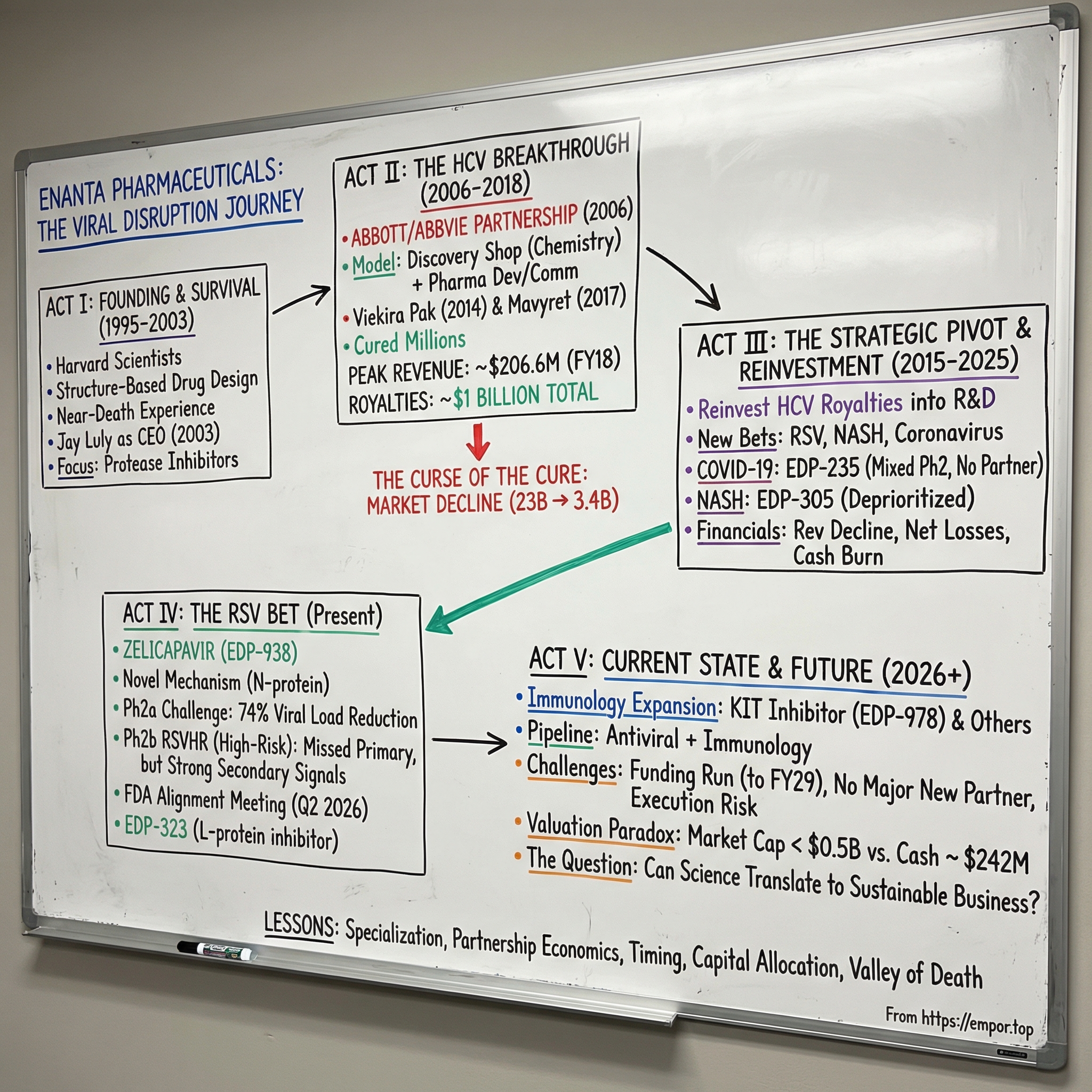

I. Introduction and Episode Roadmap

On a quiet stretch of Arsenal Street in Watertown, Massachusetts — just across the Charles River from Boston's glittering biotech corridor — sits a company with one of the strangest resumes in drug development history. Walk past the modest office park entrance and you would never guess that the molecules designed inside helped cure one of the deadliest viral diseases of the twentieth century. Enanta Pharmaceuticals helped cure Hepatitis C — a disease that infected 170 million people worldwide and killed hundreds of thousands annually. The protease inhibitors discovered in its labs became core components of drugs that have cured over a million patients. Nearly a billion dollars in royalties have flowed through its doors.

And yet, as of early 2026, the company trades at a market capitalization under half a billion dollars.

That paradox is the heart of the Enanta story. How does a company discover billion-dollar molecules, collect nearly a billion in non-dilutive financing, and still find itself navigating existential questions about its future? The answer involves the peculiar economics of curing diseases rather than treating them, the treacherous passage between one blockbuster product and the next, and a CEO who has been steering the ship for over two decades through one of the wildest rides in biotech.

This is a story about protease inhibitors — the molecular scissors that cut viral proteins and, in the right hands, can cut apart entire disease categories. It is about what happens when a research shop model meets the realities of pharmaceutical commercialization. It is about the race to find the next franchise after the first one starts to fade. And increasingly, it is about whether Enanta's deep scientific expertise in antiviral chemistry can translate into new chapters in respiratory disease and immunology.

The themes run deep: drug discovery economics, the power and limits of Big Pharma partnerships, the curse of the cure, and the question every small biotech must eventually face — what comes next?

The structure of this story follows Enanta through five distinct acts: the founding science and near-death experience; the HCV breakthrough and its extraordinary economics; the strategic pivot as royalties began their inevitable decline; the COVID moment that proved the platform's versatility; and the current state — a company in transition, placing new bets on RSV and immunology while racing against its own shrinking financial cushion. Along the way, there are lessons about drug discovery economics that apply far beyond any single company — lessons about what happens when scientific brilliance meets commercial reality, and whether the two can coexist sustainably.

II. Founding Context and the Biotech Revolution

To understand Enanta, you have to understand Cambridge and Boston in the mid-1990s. This was the golden age of rational drug design, a period when structural biology was transforming from an academic curiosity into a commercial weapon. Scientists could finally see the three-dimensional shapes of proteins and design molecules that fit into them like keys into locks. The human genome was being sequenced. The tools of molecular biology were becoming precise enough to target specific viral enzymes rather than carpet-bombing the body with toxic drugs and hoping for the best.

In this ecosystem, Vertex Pharmaceuticals was already making headlines, pioneering protease inhibitors for HIV under the leadership of Joshua Boger. Vertex's work demonstrated that understanding the three-dimensional structure of a viral protease — the enzyme a virus uses to chop up its own proteins during replication — could lead to drugs of extraordinary potency and specificity. The concept was elegant: if you could block the scissors, you could stop the virus from assembling itself.

Enanta Pharmaceuticals was incorporated in 1995, founded not by Vertex alumni as sometimes reported, but by a group of Harvard University scientists led by Gregory Verdine, the Erving Professor of Chemistry. Verdine was a pioneer in chemical biology, and the founding team brought deep expertise in structural biology and synthetic chemistry. Their thesis was ambitious: apply the emerging tools of structure-based drug design to untapped viral diseases, focusing on chemistry-driven approaches to hit targets that others considered too difficult.

The company's early years were rocky. Enanta burned through its venture capital funding, accumulated debt, and saw its original platform technology fail. By 2003, with roughly 80 employees and a depleted treasury, the company faced a binary outcome: restructure or shut down. Oxford Bioscience Partners, a Boston-based venture firm, brought in Jay Luly as an Entrepreneur in Residence to evaluate the situation.

Luly's background was tailor-made for the challenge. He had spent fifteen years at Abbott Laboratories in senior drug discovery positions, followed by stints at LeukoSite — a scrappy 30-person biotech startup — and then Millennium Pharmaceuticals after LeukoSite's merger. He understood both the science of drug discovery and the business of making it work. When he looked at Enanta's remaining assets and talent, he saw something worth saving.

The board presented Luly with a choice: recommend shutdown or propose a turnaround. He chose the latter, but with a condition — he needed approximately ten million dollars in seed capital to execute the plan. The board agreed, with its own condition: Luly had to become CEO. In July 2003, he took the helm.

That decision proved to be one of the most consequential in Enanta's history. More than two decades later, Luly still leads the company. Under his direction, Enanta would pivot toward protease inhibitors for Hepatitis C, strike a partnership that would generate nearly a billion dollars in non-dilutive financing, and build a pipeline that now spans respiratory viruses and immunology. But in the summer of 2003, all of that was still hypothetical. The immediate challenge was survival.

What made protease inhibition such a compelling drug target? The biology is surprisingly intuitive. Viruses are molecular parasites — they hijack a host cell's machinery to make copies of themselves. Many viruses, including HCV and coronaviruses, produce their proteins as one long chain called a polyprotein. Think of it as a string of sausages that need to be cut apart before each one can function. The protease is the knife. Block the knife, and the virus cannot assemble the individual proteins it needs to replicate. No replication means no infection.

The beauty of this approach is specificity. Because viral proteases have unique structures distinct from human enzymes, drugs designed to fit the viral protease's active site can be highly selective — potent against the virus while leaving human proteins alone.

This is the foundation of rational drug design: see the target, understand its shape, build a molecule that fits. Think of it like designing a key for a very specific lock. The viral protease has a particular three-dimensional shape at its active site — the pocket where it grabs and cuts proteins. If you can design a small molecule that nestles perfectly into that pocket, you can jam the lock shut. The virus's scissors stop working. But you need the molecule to fit the viral lock without accidentally jamming any human locks — that is where the art of medicinal chemistry meets the science of structural biology.

Enanta's scientific team, armed with expertise in both disciplines, was perfectly positioned to exploit this approach. They just needed the right target.

III. The Hepatitis C Context: A Silent Epidemic

In the late 1990s and early 2000s, Hepatitis C was one of the great unresolved crises in global health. An estimated 130 million people had been infected cumulatively, with roughly 170 million chronically carrying the virus at its peak prevalence. In the United States alone, HCV killed more people than HIV by the mid-2000s. Yet most of those infected did not know it — HCV earned the grim nickname "the silent epidemic" because acute infections were frequently asymptomatic. A person could carry the virus for twenty or thirty years, the virus quietly scarring the liver through progressive fibrosis, before symptoms appeared. By then, the damage was often irreversible: cirrhosis, liver failure, liver cancer.

The standard of care was brutal. Treatment consisted of weekly injections of pegylated interferon-alpha combined with daily oral ribavirin, sustained for six to twelve months depending on the viral genotype. Interferon worked not by targeting the virus directly, but by broadly stimulating the patient's immune system — an approach with devastating collateral damage.

The side effects read like a medical horror catalogue: debilitating flu-like symptoms, severe anemia, depression so profound that psychiatric screening was required before starting treatment, hair loss, skin rashes, and in some cases suicidal ideation. Patients described the experience as months of feeling like they had the worst flu of their lives, every single day.

After enduring nearly a year of this regimen, patients with the most common genotype — genotype 1, prevalent in the United States and Europe — had roughly a coin-flip chance of being cured. Approximately 40 to 50 percent achieved sustained virologic response, the clinical term for cure. For many patients, the treatment was simply not worth the suffering.

Why was HCV so hard to treat? Several factors conspired against easy solutions. The virus replicated with extraordinary speed and high error rates, generating enormous genetic diversity within a single patient. This "quasispecies" phenomenon meant the virus could rapidly evolve resistance to any single drug. HCV also had a tropism for the liver — it preferentially infected hepatocytes, making it difficult to reach with systemic therapies. And unlike HIV, which could be studied in cell culture relatively easily, HCV was notoriously difficult to grow in the laboratory, slowing basic research for years.

By the early 2000s, a race was underway. Multiple pharmaceutical companies — Vertex, Gilead, Bristol-Myers Squibb, Merck, and others — were pursuing direct-acting antivirals that would target the virus's own replication machinery rather than relying on the blunt instrument of interferon. Protease inhibitors were the first class to reach the clinic. The potential market was enormous: with hundreds of millions of infected patients worldwide and inadequate existing treatments, analysts projected multi-billion dollar annual revenues for the first effective oral therapies. The question was not whether there was demand, but who would get there first — and with what approach.

Enanta's competitive positioning was unusual. Unlike Gilead or Vertex, which had the resources and infrastructure to develop and commercialize drugs independently, Enanta was a research-focused company. It had scientific firepower but limited capital and no commercial capabilities. This constraint would shape its entire strategy: discover the molecules, then find a larger partner to shoulder the enormous costs of clinical development and global commercialization. It was a bet on brains over balance sheets.

The geographic concentration of HCV also shaped the opportunity. Egypt had the highest prevalence in the world — roughly 30 percent of its population was infected, a devastating legacy of contaminated injection campaigns during schistosomiasis eradication efforts in the mid-twentieth century. High prevalence also existed in India, Pakistan, China, and Indonesia. In the United States, two distinct epidemics overlapped: the Baby Boomer generation, many of whom had been infected through blood transfusions before universal screening began in 1992, and a newer wave driven by the opioid crisis, as needle sharing among intravenous drug users created fresh transmission chains. The disease was everywhere, largely invisible, and almost universally undertreated. For a drug developer with the right molecule, the opportunity was once-in-a-generation.

IV. The Abbott/AbbVie Partnership: A Defining Relationship

In November 2006, Enanta signed the deal that would define its next two decades. The partner was Abbott Laboratories, then one of the world's largest diversified healthcare companies. The agreement granted Abbott an exclusive license to identify, develop, and commercialize HCV NS3 and NS3/4A protease inhibitor compounds discovered through the collaboration. Enanta would do what it did best — the chemistry, the drug discovery, the molecular design. Abbott would handle the expensive, risky, and logistically complex work of clinical trials, regulatory filings, manufacturing, and global sales.

The structure was elegant in its simplicity. Abbott brought deep pockets, clinical development expertise, and a global commercial infrastructure. Enanta brought world-class medicinal chemistry and a growing portfolio of protease inhibitor candidates. The economics reflected this division of labor: Enanta would receive milestone payments as compounds advanced through development, plus tiered royalties on eventual sales. The royalty structure was notably generous — blended rates ranging from the low double digits up to the high teens on worldwide net sales, with allocation formulas based on the proportion of sales attributable to Enanta-discovered compounds.

Why did this model make sense for Enanta? Consider the economics of drug development. Taking a compound from discovery through Phase 3 clinical trials to FDA approval typically costs between one and two billion dollars and takes a decade or more. For a small company with limited capital, attempting this independently would require massive equity financing, diluting existing shareholders into oblivion. The partnership model allowed Enanta to participate in the upside — through milestones and royalties — without bearing the full cost and risk of development. It was capital efficiency taken to its logical extreme.

For Abbott, the deal was equally logical. Large pharmaceutical companies are perpetually hungry for innovative molecules to feed their development pipelines. Internal R&D at scale is expensive and often less productive per dollar than collaboration with focused discovery shops. By partnering with Enanta, Abbott gained access to cutting-edge protease inhibitor chemistry without having to build that capability internally from scratch.

The collaboration produced two critical molecules. The first was paritaprevir, designated ABT-450, an NS3/4A protease inhibitor that would become the centerpiece of Viekira Pak. The second, developed later, was glecaprevir (ABT-493), which would anchor AbbVie's next-generation regimen Mavyret. Together, these two compounds would cure over a million Hepatitis C patients worldwide.

Clinical development was neither quick nor straightforward. Paritaprevir needed to be combined with other agents — ritonavir as a pharmacokinetic booster (to keep drug levels high enough in the body), ombitasvir as an NS5A inhibitor, and dasabuvir as a polymerase inhibitor — to achieve the high cure rates necessary for regulatory approval.

Why did you need all these drugs combined? The answer goes back to HCV's biological trickery. The virus mutated so quickly that targeting any single step in its replication cycle would lead to resistance within days. But targeting multiple steps simultaneously — the protease, the polymerase, and the NS5A protein — made it nearly impossible for the virus to escape. Think of it like sealing every possible exit from a building simultaneously. The virus had nowhere to go.

Designing, testing, and optimizing this multi-drug combination required years of clinical trials involving thousands of patients across multiple countries and genotypes.

In January 2013, Abbott spun off its research-based pharmaceuticals business into a new company called AbbVie. The Enanta collaboration was assigned to AbbVie as part of the separation. This was more than a corporate housekeeping detail — it meant Enanta's commercial partner was now a focused pharmaceutical company rather than a diversified healthcare conglomerate. AbbVie, under CEO Richard Gonzalez, was aggressively building its position in specialty pharmaceuticals, and the HCV franchise was a key piece of its early strategy.

The milestone payments to Enanta accumulated steadily as the program advanced. By the time of FDA approval, Enanta had received over 160 million dollars in development and regulatory milestones, with additional payments of 75 million upon U.S. approval and 50 million upon European authorization. Total milestone receipts exceeded 235 million dollars. But the real prize was the royalty stream that would begin flowing once the drug reached the market.

That same year, 2013, Enanta went public. The company priced its IPO at fourteen dollars per share on March 21, 2013, selling four million shares on the NASDAQ Global Select Market and raising 56 million dollars in gross proceeds. It was a modest debut for a company that would soon find itself at the center of one of the largest pharmaceutical market opportunities in history.

The partnership also produced a brief side venture. In February 2012, Enanta signed an exclusive collaboration with Novartis for the development of EDP-239, an NS5A HCV inhibitor (a different drug class from the protease inhibitors developed with Abbott). Novartis paid 34 million dollars upfront, with the deal potentially worth up to 440 million. But the collaboration did not survive the rapidly evolving HCV competitive landscape. Novartis eventually terminated the agreement and returned rights to EDP-239. The episode underscored a recurring theme in Enanta's history: partnerships can generate value, but they can also evaporate when the strategic calculus shifts at the larger partner.

V. The Breakthrough: Viekira Pak and the HCV Cure

On December 19, 2014, the FDA approved Viekira Pak — a combination of ombitasvir, paritaprevir boosted with ritonavir, and dasabuvir — for the treatment of chronic genotype 1 Hepatitis C. In clinical trials, the regimen achieved cure rates of 95 to 100 percent, with less than 2 percent experiencing virological failure. In certain patient populations, including genotype 1b patients with cirrhosis, cure rates hit a perfect 100 percent. An oral therapy, taken for just 12 weeks, that could essentially eradicate a chronic viral infection that had plagued patients for decades. The era of curing Hepatitis C had arrived.

The approval capped years of painstaking clinical development, but it landed in a market that was already white-hot. Gilead Sciences had beaten everyone to the punch. Sovaldi, its nucleotide polymerase inhibitor sofosbuvir, received FDA approval in December 2013 — a full year before Viekira Pak — at a sticker price of 84,000 dollars for a 12-week course, or roughly a thousand dollars per pill. Harvoni, Gilead's combination of sofosbuvir with the NS5A inhibitor ledipasvir, followed in October 2014. By the time Viekira Pak arrived, Gilead had already generated billions in HCV revenue and commanded roughly 90 percent of the market.

AbbVie attacked the pricing problem head-on. Viekira Pak launched at approximately 83,319 dollars for a full course — a deliberate 12 percent undercut to Harvoni's 94,500 dollar list price. But the real competitive weapon was not the list price; it was formulary exclusivity. In a move that sent shockwaves through the pharmaceutical industry, AbbVie struck an exclusive deal with Express Scripts, the largest pharmacy benefit manager in the United States. Express Scripts agreed to favor Viekira Pak over Harvoni for most of its covered patients, in exchange for substantial discounts. Gilead responded with its own exclusive arrangement with CVS. For the first time, two branded specialty drugs were engaged in open price warfare for formulary position — a dynamic more commonly seen in generic competition.

Despite this aggressive positioning, Viekira Pak struggled against the Gilead juggernaut. Harvoni had the advantage of being a single-tablet, once-daily regimen — a meaningful convenience factor for both patients and prescribers. Viekira Pak required multiple pills. More damaging, the FDA later issued a safety warning about serious liver injury risk with the AbbVie regimen. At least 26 cases of hepatic injury were reported post-marketing, including 10 cases of liver failure resulting in transplant or death. AbbVie eventually pulled Viekira Pak from the European market.

But for Enanta, the commercial competition between AbbVie and Gilead was somewhat academic. What mattered was that drugs were being sold, and royalties were flowing. Under the collaboration agreement, Enanta received tiered, double-digit royalties calculated on a formula that allocated 30 percent of three-drug regimen sales (Viekira Pak) and 45 percent of two-drug regimen sales to the Enanta-discovered paritaprevir component. The quarterly royalty checks began arriving in 2015.

The successor product proved even more important. In August 2017, the FDA approved Mavyret (glecaprevir/pibrentasvir), AbbVie's next-generation HCV regimen featuring another Enanta-discovered protease inhibitor, glecaprevir. Mavyret was pan-genotypic — effective across all major HCV genotypes — with a shorter eight-week treatment duration for most patients and a dramatically lower price of approximately 26,400 dollars per course. It captured roughly 50 percent of new HCV prescriptions and became AbbVie's dominant HCV product. For Enanta, Mavyret quickly superseded Viekira Pak as the primary royalty driver.

The peak years were extraordinary. Enanta's annual revenue reached 206.6 million dollars in fiscal year 2018, almost entirely from HCV royalties and milestones. For a company that had nearly been shut down fifteen years earlier, the transformation was remarkable.

Consider the math: a company that raised 21 million in venture capital and 56 million in its IPO eventually collected close to a billion dollars in milestone payments and royalties from a single partnership. That is a return on invested capital that would make any venture capitalist weep with joy. Jay Luly's turnaround bet had paid off spectacularly.

But the mathematics of curing a disease contain a cruel irony. Every patient cured is a patient who will never need treatment again. Unlike chronic conditions such as diabetes or hypertension — where patients take medication for life, generating recurring revenue indefinitely — a curative therapy systematically destroys its own market.

The global HCV drug market peaked at approximately 23 billion dollars in 2015 and began a relentless decline. By 2022, it had shrunk to roughly 3.4 billion — a decline of more than 85 percent in seven years. Gilead's HCV franchise alone fell from 19.1 billion at peak to less than four billion within three years. No other therapeutic category in pharmaceutical history has experienced value destruction of this magnitude, this quickly. It was the market equivalent of a controlled demolition — and every company in the space felt the blast.

For Enanta, the message was unmistakable. The royalty stream that had transformed the company from a struggling startup into a profitable enterprise would not last forever. The HCV franchise was a wasting asset — enormously valuable, but with a finite and shrinking lifespan. What Enanta chose to do with those royalties while they lasted would determine whether the company had a future beyond Hepatitis C.

The HCV experience contained one more lesson that would prove relevant to everything Enanta did next. The first generation of protease inhibitors — Vertex's telaprevir (Incivek) and Merck's boceprevir (Victrelis), both approved in 2011 — had demonstrated that targeting HCV's replication machinery directly could dramatically improve cure rates. But they still required the interferon backbone, limiting their appeal. Telaprevir had earned the title of fastest drug launch in history, yet sales cratered 96 percent within three years once interferon-free regimens arrived. Vertex discontinued the drug entirely in October 2014. The speed of that collapse — from blockbuster to discontinued in three years — was a powerful reminder that in drug development, being first matters less than being best. Enanta's compounds, arriving as part of the interferon-free generation, benefited from being later but better. That timing lesson would recur, with different implications, when the company attempted to develop a COVID antiviral.

VI. The Inflection Point: Post-HCV Strategy

The period between 2015 and 2018 presented Enanta's management with one of the classic strategic dilemmas in biotech: what do you do after your major product starts declining? The temptation to simply ride the royalty stream and return cash to shareholders was real. But Luly and his team made a different choice — they would reinvest the HCV royalties into building a diversified pipeline, using the cash flow to self-fund research and development without resorting to heavy dilution.

Three strategic bets emerged. The first and most natural was respiratory syncytial virus, or RSV. This was an enormous unmet medical need — RSV caused approximately 177,000 hospitalizations and 14,000 deaths annually among older adults in the United States alone, plus 58,000 to 80,000 pediatric hospitalizations, with no approved antiviral treatment. The second bet was NASH, or non-alcoholic steatohepatitis, the next liver disease epidemic driven by the global obesity crisis. The third, and in retrospect the most prescient, was coronaviruses — a focus that Enanta initiated years before anyone had heard of SARS-CoV-2.

The underlying philosophy was disciplined: stick to what you know. Enanta's competitive advantage lay in protease inhibitor chemistry and antiviral expertise. Rather than chasing fashionable therapeutic areas where it had no edge, the company would apply its core capabilities to new viral targets. The RSV program leveraged the team's deep understanding of viral replication biology. The coronavirus work exploited similar protease inhibitor expertise. Even the NASH program, which represented a departure into metabolic liver disease, stayed within the liver — the organ Enanta's scientists understood best from years of HCV work.

Building clinical capabilities required investment. Enanta hired experienced drug developers, built out its clinical operations infrastructure, and expanded its medicinal chemistry teams. The Cambridge biotech ecosystem provided a deep talent pool, though competing for top scientists against larger companies like Vertex, Moderna, and the academic institutions was a constant challenge. The company's reputation for scientific rigor and the opportunity to work on first-in-class programs helped attract researchers who valued intellectual freedom over corporate scale.

Financially, the strategy was elegant. While HCV royalties remained robust — fiscal year 2018 revenues hit 206 million dollars — Enanta could fund its pipeline programs internally. R&D spending ramped up progressively, reaching over 130 million dollars annually at peak. The beauty of royalty-funded R&D was that it avoided the dilution cycle that plagues most small biotechs: raise equity, spend on R&D, run out of cash, raise more equity at a lower price, repeat. Enanta's shareholders were getting pipeline development largely for free, funded by the HCV franchise.

But the clock was ticking. Every quarter, the HCV market shrank a little more. The question was whether any of the new programs could mature before the royalty stream dried up completely. It was, in essence, a race between pipeline advancement and revenue decline — the biotech equivalent of building a bridge while standing on a melting iceberg.

The financial dynamics revealed the challenge in stark terms. Enanta's revenue peaked at 206.6 million in fiscal 2018, then declined approximately 45 percent over the following year as the HCV market compressed. By fiscal 2021, revenues had stabilized somewhat, but the trajectory was relentlessly downward. Meanwhile, R&D spending was increasing as the new programs advanced through clinical development. The company was running a deliberate deficit — consuming its cash reserves and royalty income to fund the pipeline. The strategy was intellectually sound but financially precarious. Each year the gap between revenue and R&D spending persisted, the runway shortened.

VII. RSV Program: Betting on Respiratory Disease

Picture a packed emergency room in January. Beds are full of elderly patients struggling to breathe, children wheezing with labored respiration, immunocompromised patients deteriorating rapidly. The culprit is not influenza, not COVID, but a virus that most people outside of medicine have barely heard of: respiratory syncytial virus, or RSV. Despite causing more hospitalizations among infants than any other pathogen and killing thousands of older adults annually in the United States alone, RSV had no approved antiviral treatment. Vaccines began arriving in 2023 — GSK's Arexvy and Pfizer's Abrysvo — but vaccines prevent infection; they do not treat patients who are already sick. The treatment gap remained wide open.

Enanta's approach to RSV was characteristically scientific. Rather than developing another fusion inhibitor — the mechanism most competitors pursued — the company targeted the RSV N-protein (nucleoprotein), a critical component of the viral replication complex. The lead compound, zelicapavir (EDP-938), was designed to jam the virus's replication machinery through a novel mechanism that no other approved or late-stage drug employed. This differentiation mattered enormously: in a field where multiple approaches might fail, having a unique mechanism provided both scientific and commercial optionality.

The early clinical data was genuinely impressive. In a Phase 2a human challenge study — where healthy volunteers are deliberately infected with RSV in a controlled setting — zelicapavir demonstrated a 74 percent reduction in viral load compared to placebo, achieving high statistical significance. The results were published in The New England Journal of Medicine, lending scientific credibility to the program. The FDA granted Fast Track designation, signaling regulatory recognition of the unmet need.

Translating challenge study success into real-world efficacy proved more complex. A Phase 2b study in low-risk adults with naturally acquired RSV infection missed its primary endpoint — reduction in total symptom score. This was disappointing but perhaps not surprising: in healthy adults, RSV is typically a mild, self-resolving illness. The drug worked against the virus (statistically significant viral clearance), but the patients got better on their own regardless.

The pivotal data came from the RSVHR study in high-risk adults — the population where RSV is most dangerous. Results announced in September 2025 told a nuanced story. The formal primary endpoint, time to resolution of four lower respiratory tract disease symptoms, was missed by a slim margin — only a half-day improvement. But the secondary endpoints revealed clinically meaningful benefits. Among the highest-risk patients — those with congestive heart failure, chronic obstructive pulmonary disease, or aged 75 and older, comprising 81 percent of the efficacy population — zelicapavir delivered a 6.7-day improvement in time to complete symptom resolution. Hospitalization rates were 1.7 percent on zelicapavir versus 5.0 percent on placebo. Viral clearance was four to five days faster.

Enanta also generated first-in-pediatrics data. A Phase 2 study in children aged 28 days to 36 months showed a meaningful 1.4 log decline in viral load at Day 5. No other RSV antiviral had demonstrated efficacy in this population.

Meanwhile, Enanta developed a second RSV compound with a completely different mechanism. EDP-323 inhibits the RSV L-protein (polymerase), making it mechanistically complementary to zelicapavir. In a Phase 2a challenge study, EDP-323 showed 85 to 87 percent reductions in viral load and rapid symptom improvement. Remarkably, data presented at IDWeek 2025 suggested EDP-323 could prevent RSV infection when initiated up to five days after exposure — a post-exposure prophylaxis application that could be transformative in institutional settings like nursing homes.

The competitive landscape for RSV antivirals remains favorable — and here it is worth pausing to explain why this matters so much. While vaccines from GSK, Pfizer, and Moderna address prevention, no oral antiviral treatment exists for patients who develop symptomatic RSV. Zero options. A doctor treating a hospitalized elderly patient with RSV has essentially nothing to prescribe except supportive care — fluids, oxygen, rest. This is analogous to the state of COVID treatment before Paxlovid arrived. The unmet need is enormous.

Pfizer discontinued its antiviral candidate sisunatovir, removing a competitor. Shionogi's S-337395 showed Phase 2 efficacy, representing the most direct competitive threat. But Enanta's dual-mechanism portfolio — with the option of combination therapy using both zelicapavir and EDP-323 — remains the broadest RSV antiviral program in development.

The critical near-term catalyst is a planned FDA alignment meeting in the second quarter of 2026 to discuss Phase 3 trial design for zelicapavir. The outcome of that meeting will shape Enanta's trajectory for years: it will determine whether the company pursues Phase 3 independently (requiring substantial capital), seeks a development partner, or potentially restructures the program around the higher-risk patient subgroup where efficacy was most pronounced.

The RSV opportunity, if it materializes, could be transformative in scale. The RSV treatment market is projected to reach multiple billions of dollars annually, driven by an aging global population, increasing awareness of RSV's burden in adults, and the fact that vaccines — while helpful for prevention — do not address patients who become symptomatic despite vaccination or who are unvaccinated. With RSV vaccine uptake still below expectations (GSK's Arexvy and Pfizer's Abrysvo saw sales decline more than 50 percent from their launch year highs as adoption normalized), the residual treatment-eligible population remains enormous. For Enanta, the prize justifies the risk — but only if the clinical and regulatory stars align.

VIII. The COVID Pivot: Opportunity Knocks Again

When SARS-CoV-2 emerged in early 2020 and shut down the world, most of the pharmaceutical industry was caught flat-footed. Enanta was not. In one of those instances where scientific curiosity pays unexpected dividends, the company had been working on coronavirus protease inhibitors since 2015 — five years before anyone outside of epidemiology circles was worried about a coronavirus pandemic. The work was not driven by pandemic preparedness planning; it was driven by scientific logic. Coronaviruses, like HCV, rely on proteases to process their polyproteins. Enanta's expertise in protease inhibition was directly applicable.

When the pandemic hit, Enanta moved quickly. The company leveraged its existing coronavirus chemistry to develop EDP-235, an oral, once-daily 3CL protease inhibitor designed specifically for SARS-CoV-2. The 3CL protease (also called Mpro, for main protease) is the primary enzyme SARS-CoV-2 uses to cleave its polyprotein into functional components. Blocking it shuts down viral replication — the same conceptual approach that had worked against HCV, now applied to a different virus.

The competitive landscape for COVID antivirals was ferocious. Pfizer was developing nirmatrelvir (branded as Paxlovid in combination with ritonavir), another 3CL protease inhibitor. Merck had molnupiravir, a nucleoside analog with a different mechanism. Dozens of other companies were racing to develop oral treatments. Pfizer's resources, speed, and clinical execution were formidable — Paxlovid received Emergency Use Authorization in December 2021, less than two years after the pandemic began.

EDP-235's Phase 1 results were encouraging, showing favorable pharmacokinetic properties and safety. The Phase 2 SPRINT trial enrolled 231 subjects and was designed to evaluate both safety and preliminary efficacy. Results reported in May 2023 were mixed: the drug was safe and well-tolerated, and a dose-dependent improvement in symptoms was observed, achieving statistical significance in the 400 milligram group starting as early as Day 1. However, EDP-235 did not reduce viral load or time to overall symptom improvement in the full study population.

The COVID program also gave rise to one of Enanta's most intriguing strategic plays: patent litigation against Pfizer. In June 2022, Enanta filed suit in U.S. District Court alleging that Paxlovid infringed Enanta's patent covering coronavirus 3CL protease inhibitor compounds. The patent, based on a provisional application filed in July 2020, covered chemical structures that Enanta argued encompassed nirmatrelvir. Enanta sought monetary damages, not an injunction — the company made clear it was not trying to block Paxlovid distribution during a pandemic, but rather seeking fair compensation for its intellectual property.

In December 2024, a federal judge granted summary judgment in Pfizer's favor, ruling the patent invalid. Enanta is appealing the decision to the Court of Appeals for the Federal Circuit. Additionally, the company filed a parallel patent infringement suit in the European Union's Unified Patent Court in August 2025. The Pfizer litigation remains a potential source of significant value, though the U.S. setback dimmed near-term expectations.

Following the mixed Phase 2 results, Enanta made the pragmatic decision not to advance EDP-235 further on its own. The company described the compound as "Phase 3 ready" but indicated it would only continue development with a partner. No such partner had materialized as of early 2026. In an endemic COVID landscape where vaccines have dramatically reduced severe disease and Paxlovid has established itself as the standard of care, the commercial opportunity for a late-entering oral antiviral has narrowed considerably.

The COVID experience illustrates a recurring tension in drug development: being scientifically early does not guarantee being commercially early. Enanta had been working on coronavirus chemistry since 2015, yet Pfizer — starting much later but with vastly greater resources — reached the market first. For a small company operating on constrained timelines and budgets, speed-to-market in a competitive race against well-capitalized rivals remains a fundamental challenge.

The COVID antiviral market itself continues to evolve. Pfizer is developing ibuzatrelvir, a next-generation oral COVID antiviral designed to be taken without ritonavir — addressing one of Paxlovid's key drawbacks. Shionogi's ensitrelvir offers a lower pill burden. The market is projected to grow substantially as COVID becomes an endemic seasonal virus, but the window for a new entrant like EDP-235 has narrowed considerably. Unless a partner with deep pockets and regulatory sophistication steps forward, Enanta's COVID program is likely to remain on the shelf — a scientifically impressive compound that arrived at the wrong time.

IX. NASH and the Liver Franchise

The story of Enanta's foray into NASH — non-alcoholic steatohepatitis — is a cautionary tale about the allure of large market opportunities and the difficulty of therapeutic diversification. NASH represents the severe, inflammatory form of fatty liver disease, driven primarily by obesity and metabolic dysfunction. With an estimated 20 million Americans affected and no approved pharmacological treatments for most of Enanta's development period, the addressable market was projected in the tens of billions. Every major pharmaceutical company wanted a piece of it.

Enanta's approach leveraged its liver expertise from the HCV franchise but employed a different scientific mechanism: FXR agonism. The farnesoid X receptor is a nuclear receptor in liver cells that regulates bile acid metabolism, lipid homeostasis, and inflammation. Activating FXR with a small-molecule agonist could, in theory, reduce liver inflammation and fibrosis in NASH patients. Enanta developed EDP-305, a highly selective FXR agonist, and advanced it through clinical trials.

The Phase 2a ARGON-1 study produced genuinely encouraging results. EDP-305 demonstrated statistically significant reductions in ALT (a marker of liver inflammation) and meaningful reductions in liver fat content at 12 weeks — differentiating it from other FXR agonists that showed less impact on hepatic steatosis. A Phase 2b study, ARGON-2, was initiated, and EDP-305 was eventually dosed in nearly 600 patients.

But NASH proved to be a graveyard for drug developers. Clinical endpoints were difficult to achieve, safety signals emerged across the class (pruritus, or itching, was a near-universal side effect of FXR agonists), and the long treatment durations required for liver fibrosis improvement made trials expensive and slow. Enanta ultimately decided to prioritize combination approaches through out-licensing rather than continuing monotherapy development. A follow-on candidate, EDP-297, was also positioned for out-licensing.

The broader NASH landscape validated the decision to deprioritize. Madrigal Pharmaceuticals eventually achieved the first FDA approval for a NASH therapy with resmetirom in 2024, but the path was long, costly, and required enormous capital commitment. For a company of Enanta's size, competing in NASH against better-funded players would have been a dangerous distraction from its core antiviral strengths.

The NASH experience reinforced a lesson that Luly had articulated from the beginning: stay in your lane. Enanta's competitive advantage was in antiviral chemistry and protease inhibition. Metabolic liver disease, while intellectually adjacent, required different clinical expertise, longer development timelines, and larger patient populations than the company was equipped to handle independently. The resources freed up from scaling back NASH were redirected toward the RSV and, eventually, immunology programs.

It is worth noting the irony: Enanta's expertise in liver biology, hard-won through years of HCV work, was precisely what made NASH seem like a natural extension. The FXR agonist mechanism was scientifically sound, and the early clinical data was competitive. But in drug development, sound science is necessary but not sufficient. You also need the capital to run large, long trials, the patience to wait years for histological endpoints, and the commercial infrastructure to market to a different set of physicians (hepatologists and endocrinologists rather than infectious disease specialists). Enanta had the science but lacked the other ingredients. The decision to deprioritize NASH was painful but correct — an example of strategic discipline that many biotechs fail to exercise until it is too late.

X. Business Model Deep Dive: The Discovery Shop Strategy

Think about this for a moment: Enanta Pharmaceuticals has generated nearly a billion dollars in non-dilutive financing without ever selling a drug directly to a patient. Not one prescription. Not one sales call. Not one relationship with a pharmacy benefit manager. The company has no sales force, no manufacturing facilities, no distribution network. What it has is a collection of laboratories in Watertown, Massachusetts, staffed by world-class medicinal chemists who are exceptionally good at one very specific thing: designing small molecules that fit into viral protease active sites.

This is the discovery shop model in its purest form — a company that exists to do the hardest intellectual work in pharmaceutical development and then hands off everything else to a partner with the infrastructure to bring drugs to market. It is the biotech equivalent of an architecture firm that designs magnificent buildings but never swings a hammer.

The discovery shop model has both elegance and fragility.

The elegance lies in capital efficiency. By partnering with larger companies for development and commercialization, Enanta captures a meaningful share of the economic value — through milestones and royalties — while spending a fraction of what it would cost to build an integrated pharmaceutical company. The AbbVie partnership alone generated over 950 million dollars in cumulative royalties through September 2025, plus hundreds of millions in milestone payments. For a company that raised just 21 million in pre-IPO venture capital and 56 million in its IPO, those are extraordinary returns on invested capital.

The fragility lies in dependency.

Enanta's entire revenue stream flows through a single partnership with a single company for a single therapeutic area. When the HCV market contracts — as it inevitably does when you cure a disease — the royalty stream contracts with it. Annual revenue declined from the peak of 206.6 million dollars in fiscal 2018 to 65.3 million in fiscal 2025. The company went from profitability to losses, with net losses of 81.9 million in fiscal 2025. Cash burn has necessitated equity offerings that dilute existing shareholders — a painful irony for a company that had prided itself on non-dilutive financing.

In April 2023, Enanta executed a creative financial maneuver to shore up its balance sheet. The company sold 54.5 percent of its future Mavyret royalties to OMERS Life Sciences, one of Canada's largest pension funds, for 200 million dollars upfront. OMERS would receive the majority of royalty payments through June 2032, with total payments capped at 1.42 times the purchase price (284 million dollars). Once the cap was reached, all royalties would revert to Enanta. The transaction provided immediate capital while preserving long-term optionality — a form of royalty monetization that has become increasingly common in biotech.

The talent model is central to Enanta's value proposition. Structure-based drug design is not something that can be bought off the shelf. It requires years of accumulated expertise in medicinal chemistry, computational chemistry, structural biology, and pharmacology — and critically, it requires scientists who have done it before, who have the intuition to know which modifications to a molecular scaffold will improve potency, selectivity, and drug-like properties. Enanta has built a team with deep experience in protease inhibitor design, creating a form of institutional knowledge that is difficult for competitors to replicate quickly.

Whether this constitutes a durable competitive advantage is a key debate. The techniques of structure-based drug design are well-understood in principle; what Enanta possesses is execution excellence in practice. The analogy might be to a master craftsman versus a textbook reader — both understand the theory, but only one can consistently produce exceptional work. In Hamilton Helmer's framework, this is a combination of Cornered Resource (the scientific talent and proprietary compound libraries) and Process Power (the methodology and institutional knowledge of drug discovery).

The strategic question that has defined the post-HCV era is when to partner and when to retain rights. For the RSV program, Enanta has thus far chosen to retain full ownership — a departure from the HCV model. This decision reflects both ambition and necessity. Ambition because an independently commercialized product would generate far more value than a royalty stream. Necessity because no pharma partner has yet offered terms attractive enough to justify giving up control. Whether Enanta can afford to self-fund a Phase 3 RSV program, or whether economics will force a partnership, is one of the defining questions for the company's near-term future.

The comparison to other discovery-focused biotechs is instructive. Arena Pharmaceuticals built a discovery engine around GPCR targets and was eventually acquired by Pfizer for 6.7 billion dollars. Pharmacyclics discovered ibrutinib and was acquired by AbbVie for 21 billion. In both cases, the discovery shop model ultimately led to an acquisition rather than independent commercialization. The pattern suggests that discovery-focused biotechs either find a partner early (as Enanta did with HCV), build commercial capabilities themselves (as Vertex successfully did), or get acquired. Enanta has done the first, has not yet attempted the second, and remains a candidate for the third. The path it ultimately takes will depend on which pipeline programs succeed and what partnership opportunities emerge in the coming years.

XI. Recent Inflection Points and Current State

The years from 2020 through 2026 have been a crucible for Enanta, compressing multiple strategic challenges into a compressed timeframe. Royalty revenues declined faster than the most optimistic pipeline programs advanced. The COVID bet produced scientific validation but no commercial product. The RSV program showed genuine promise but missed its formal primary endpoint in the pivotal high-risk study. And in September 2025, the company lost its longtime CFO Paul Mellett, who passed away after serving alongside Luly since 2003 — a deeply personal blow to the leadership team that removed one of the few constants in Enanta's executive suite.

The broader biotech funding environment amplified every challenge. The speculative biotech boom of 2021 — when loss-making companies with preclinical programs could raise hundreds of millions at sky-high valuations — briefly lifted Enanta's stock. But the severe correction that followed in 2022 and 2023, as interest rates rose and investors retreated from risky assets, hit small-cap biotechs disproportionately hard. Companies without near-term revenue, including Enanta, saw their valuations compressed to levels that made raising capital increasingly punishing. The XBI biotech ETF fell roughly 60 percent from its 2021 highs, and Enanta's stock tracked that decline — and then some.

The financial trajectory tells a stark story. From peak revenue of 206.6 million in fiscal 2018, annual revenue fell to 65.3 million in fiscal 2025. Meanwhile, R&D spending remained elevated as the company invested in advancing its pipeline — 131.5 million in fiscal 2024, 106.7 million in fiscal 2025. The result was persistent net losses, reaching 116 million in fiscal 2024 and 81.9 million in fiscal 2025. Cash reserves, once robust, required replenishment.

In October 2025, Enanta executed an upsized public offering, selling 7.475 million shares at 10.00 dollars per share for gross proceeds of approximately 74.75 million dollars. At ten dollars, the offering price represented a roughly 90 percent discount to the stock's all-time high. The dilution was significant — approximately 35 percent expansion of shares outstanding. But the capital was necessary: combined with existing reserves and ongoing royalty income, management estimated the company was now funded into fiscal year 2029.

The stock price journey captures the emotional arc of the entire story. From the 14-dollar IPO in 2013, shares rose steadily as HCV royalties swelled, reaching an all-time high of 127.77 dollars intraday in July 2018 at the peak of Mavyret revenue. The subsequent decline mirrored the HCV market contraction and pipeline uncertainty. By April 2025, shares touched an all-time low of 4.09 dollars. The October 2025 offering at 10 dollars and subsequent positive RSV data drove a partial recovery to approximately 14 dollars by early 2026 — coincidentally almost exactly the IPO price. Thirteen years of extraordinary value creation and destruction, returning to where it started.

In a strategic pivot that surprised some observers, Enanta announced in late 2025 and early 2026 an expansion into immunology. Three new programs — a KIT inhibitor (EDP-978) for chronic spontaneous urticaria, a STAT6 inhibitor (EPS-3903) for atopic dermatitis, and an MRGPRX2 inhibitor for type 2 immune diseases — represent Enanta's first major departure from antiviral chemistry. The KIT inhibitor was selected as a clinical candidate in November 2025, with an IND filing expected in the first quarter of 2026 and Phase 1 data targeted for the fourth quarter. The shift reflects a recognition that Enanta's core competency — designing small molecules to fit specific protein targets — is transferable beyond virology.

Analyst coverage reflects cautious optimism. Eight analysts track the stock, with an average Outperform rating and a consensus price target around 19 dollars. J.P. Morgan initiated coverage at Overweight with a 17-dollar target in November 2025. Jefferies upgraded from Hold to Buy. But the range is wide — from 11 to 28 dollars — reflecting deep uncertainty about whether the RSV program can clear the regulatory bar and whether the immunology expansion will bear fruit.

The absence of a major partnership remains the most conspicuous gap in Enanta's strategy. The AbbVie collaboration demonstrated the company's ability to create transformative value through partnership. Yet despite years of pipeline advancement, no comparable deal has materialized for the RSV or COVID programs. Whether this reflects market conditions, the stage of the programs, or strategic patience by management is debated among investors. The forthcoming FDA alignment meeting on zelicapavir Phase 3 design may catalyze partnership discussions, as potential partners would want to understand the regulatory pathway before committing capital.

There is also the matter of accounting judgment worth flagging. Enanta's revenue recognition depends entirely on royalty estimates from AbbVie, with true-ups occurring quarterly. The OMERS royalty sale introduced additional complexity — the 200 million dollar upfront payment was recorded as deferred revenue, being recognized over the life of the agreement. Meanwhile, the company's R&D expenses include significant non-cash stock compensation, meaning the cash burn rate is lower than reported net losses suggest. For fiscal 2025, the net loss was 81.9 million, but operating cash consumption was closer to 60 million after adjusting for non-cash items. These nuances matter for assessing the true runway and cash trajectory.

The most recent quarterly results, for the three months ending December 2025, showed modest stabilization. Revenue came in at 18.6 million dollars — roughly flat with the year-ago period — while R&D spending declined to 20.9 million from 27.7 million, reflecting the timing gap between completed Phase 2 studies and the planned Phase 3. Net loss narrowed to 11.9 million. With 241.9 million in cash, the quarterly burn rate suggests the company has meaningful breathing room — but not infinite patience.

XII. Playbook: Business and Investing Lessons

The Enanta story is a masterclass in several recurring themes of biotech investing, each carrying implications far beyond this single company.

The power of specialization. Enanta built its entire value proposition around one thing: designing protease inhibitors with structure-based drug design. That narrow focus produced two blockbuster drug components, generated nearly a billion dollars in royalties, and created institutional expertise that proved applicable to multiple viral families. The lesson for other biotechs — and companies in any industry — is that being the best in the world at one specific skill, even a very narrow one, can generate enormous value if the skill is applied to the right problems.

Partnership economics and the control-for-capital trade-off. The AbbVie deal was spectacularly successful by the numbers, but it also meant Enanta never built the commercial capabilities to sell drugs independently. When the royalty stream began declining, the company had no alternative revenue source. The lesson is that partnerships optimize for capital efficiency but create dependency. The challenge Enanta now faces — building clinical and potentially commercial capabilities from scratch — is the deferred cost of having outsourced those functions for two decades.

The curse of the cure. No company illustrates this pharmaceutical paradox more vividly than Enanta. Helping cure Hepatitis C was a monumental scientific and humanitarian achievement. It also systematically destroyed the market that generated Enanta's revenue. The HCV drug market shrank from 23 billion to roughly 3.4 billion in seven years. For investors, the lesson is brutally simple: curative therapies have finite commercial lifespans. Valuing them requires modeling not just peak sales but the rate of market erosion — and having a clear view of what comes next.

Timing in drug development. Enanta was working on coronavirus protease inhibitors in 2015, years before COVID-19 existed. That prescience led to a viable drug candidate. But Pfizer, starting later with far greater resources, reached the market first. Being scientifically early and commercially late is a recurring risk for small biotechs. The advantage of having the right science matters only if you can convert it into an approved product before the window closes.

Capital allocation after a windfall. Management's decision to reinvest HCV royalties into pipeline development rather than returning cash to shareholders was bold. It preserved the company's scientific identity and created multiple shots on goal. But it also committed hundreds of millions to programs with uncertain outcomes, and the transition from profitability to sustained losses tested shareholder patience. The reinvestment decision is defensible — what else should a drug discovery company do with its earnings if not discover more drugs? — but the execution has been imperfect.

Navigating the valley of death. The period between one major product and the next is the most dangerous time for a biotech company. Revenue declines, costs remain high, and the market punishes uncertainty with a declining stock price, which raises the cost of capital, which accelerates the cycle. Enanta is deep in this valley. The company's survival depends on converting pipeline programs into approved products — or finding partners willing to pay for the opportunity to do so.

Scientific platform value versus commercial execution. Perhaps the deepest lesson from Enanta is the distinction between creating scientific value and capturing economic value. The company's scientists have created molecules worth billions of dollars to the healthcare system — medications that have cured over a million people of a deadly chronic disease. The platform has demonstrated its applicability across HCV, RSV, coronaviruses, and now immunological targets. Yet the economic value captured by Enanta and its shareholders has been a fraction of the value created, because the company lacks the commercial infrastructure to monetize its discoveries independently. The platform is real. The question is whether the economics of the platform can sustain an independent public company.

The myth versus the reality. The consensus narrative about Enanta often frames it as a "one-hit wonder" — a company that got lucky with HCV and has been struggling ever since. The reality is more nuanced. The RSV portfolio is the most advanced antiviral program for a disease with no approved treatment. The immunology expansion, while early, is scientifically grounded. The challenge is not the absence of good science; it is the gap between promising clinical data and the definitive proof required for approval and commercialization. That gap — the space between "this looks promising" and "this works" — is where biotech fortunes are made and lost.

XIII. Strategic Frameworks Analysis

Porter's Five Forces

The competitive dynamics surrounding Enanta reveal an industry where scientific barriers to entry are high but capital barriers are surmountable, creating a landscape of intense rivalry among well-funded competitors.

Threat of new entrants is paradoxically both high and low. The expertise required to design effective protease inhibitors — years of medicinal chemistry experience, sophisticated computational tools, institutional knowledge — creates substantial barriers. However, the broader biotech ecosystem is awash in venture capital and academic talent, and new companies regularly emerge with novel approaches to the same viral targets. The barrier is not capital but capability, and that capability is increasingly distributed across the biotech ecosystem.

Bargaining power of suppliers is moderate. Enanta relies on contract research organizations for certain clinical trial functions and specialized equipment for drug discovery. These inputs are available from multiple providers, preventing any single supplier from exerting significant leverage. However, the market for top-tier medicinal chemists is tight, and talent acquisition costs have risen as the Boston biotech ecosystem has expanded.

Bargaining power of buyers is high and increasing. The end customers for pharmaceutical products — insurance companies, pharmacy benefit managers, government payers — have become increasingly aggressive in negotiating drug prices. The HCV pricing war between Gilead and AbbVie demonstrated that even breakthrough therapies face intense downward pressure once competition emerges. For Enanta's future products, the pricing environment will likely be more challenging than the one that greeted Viekira Pak.

Threat of substitutes is very high. This is perhaps the most critical force shaping Enanta's competitive position. For RSV, vaccines from GSK, Pfizer, and Moderna address prevention, potentially reducing the treatment-eligible population. For COVID, multiple antivirals, monoclonal antibodies, and vaccines already exist. In any therapeutic area Enanta enters, it faces not just direct competitors with similar mechanisms but entirely different modalities — vaccines, biologics, gene therapies — that could address the same unmet need through different approaches.

Competitive rivalry is intense across all of Enanta's target markets. In RSV antivirals, Shionogi and others are advancing programs. In immunology, the company faces well-capitalized competitors with decades of experience. The fundamental challenge is that Enanta competes against companies ten to a hundred times its size, with proportionally larger R&D budgets, commercial infrastructure, and financial resilience.

Hamilton's Seven Powers

Evaluating Enanta through Hamilton Helmer's framework reveals a company whose primary source of durable advantage is narrower than investors might hope.

Scale Economics are limited. Drug discovery R&D does not benefit significantly from scale until commercialization, where larger companies can spread fixed costs across wider product portfolios and geographies. Enanta has no scale advantages in its current configuration.

Network Effects are nonexistent. Drug efficacy does not improve with more users. There is no demand-side scale advantage in pharmaceuticals.

Counter-Positioning is moderate. Enanta's discovery shop model differs from integrated pharma in ways that are difficult for large companies to replicate internally — but not impossible. The model is more of a strategic choice than a structural advantage.

Switching Costs are high once a drug achieves formulary placement, but achieving that placement is the challenge. For physicians and payers, switching between therapeutically equivalent options is relatively frictionless.

Branding is weak. Enanta is a B2B partner and pipeline company, not a consumer brand. Its reputation matters in the scientific community and with potential partners, but it confers no pricing power with end customers.

Cornered Resource is strong, and this is Enanta's primary power. The company's scientific talent, proprietary compound libraries, and accumulated expertise in protease inhibitor design represent resources that competitors cannot easily acquire or replicate. Jay Luly's two decades of leadership and the institutional knowledge embedded in the organization are genuinely difficult to reproduce.

Process Power is also strong. Enanta's structure-based drug design methodology, refined over decades, enables the company to identify and optimize drug candidates with greater efficiency than competitors operating with less specialized approaches. The ability to consistently design molecules that fit specific protein targets is a form of process excellence.

The primary competitive positioning, then, rests on Cornered Resource combined with Process Power — the talent and the methodology. Whether this is sufficient to generate sustained returns depends on whether the company can convert that scientific excellence into approved, revenue-generating products.

Competitive Positioning

Against Gilead Sciences, Enanta is outmatched on every dimension except pure discovery chemistry. Gilead has commercial scale, manufacturing capabilities, and diversified therapeutic franchises. Against Vertex Pharmaceuticals — a company with similar discovery DNA but much greater size and diversification — Enanta is a smaller, more focused, and consequently more fragile operation. Against peer-sized antiviral biotechs like Atea Pharmaceuticals, Enanta has a deeper track record and more advanced pipeline, but similar capital constraints.

The niche Enanta occupies is best described as "best-in-class protease inhibitor discovery for specific viral targets." Whether that niche is large enough to support a standalone public company is the central investment question.

The immunology expansion, if successful, would broaden this niche considerably. But for now, the company's identity — and its value — remains rooted in antiviral chemistry. The immunology programs are bets on transferability: can the same scientific team that designs world-class antiviral protease inhibitors also design world-class kinase inhibitors and transcription factor modulators for immune diseases? The answer is not yet known.

XIV. Bear versus Bull Case

The Bull Case

The optimistic thesis starts with RSV. If zelicapavir can navigate the regulatory pathway — potentially using the high-risk subgroup data to define a Phase 3 population — the addressable market is substantial. No approved oral RSV antiviral exists anywhere in the world. With RSV vaccines covering only a portion of the at-risk population and waning in efficacy over time, the treatment opportunity could be worth multiple billions of dollars annually. Enanta's dual-mechanism portfolio (zelicapavir plus EDP-323) creates the possibility of combination therapy — the same playbook that made HCV treatment so successful. And the pediatric data adds another dimension: treating RSV in infants and young children, where the disease burden is heaviest and the emotional urgency greatest.

The immunology expansion represents a new vector of growth into markets far larger than respiratory antivirals. If Enanta's core competency in small-molecule design translates to immunological targets — and early preclinical data on the KIT inhibitor EDP-978 shows potent nanomolar activity — the company could diversify beyond virology into a field where Dupixent alone generates over 13 billion dollars annually. Chronic spontaneous urticaria, atopic dermatitis, and related type 2 immune diseases collectively represent tens of billions in addressable market opportunity.

Partnership optionality provides asymmetric upside. A single large partnership — structured like the AbbVie deal, with upfront payments, milestones, and royalties — could transform the company's financial position overnight. With RSV Phase 3 design coming into focus, the window for such a deal may be approaching. In the current pharma environment, where large companies are desperate for innovative assets to fill late-stage pipeline gaps, a company with two Fast Track-designated RSV programs and a novel immunology portfolio has negotiating leverage — if the data holds up.

The Pfizer patent litigation, particularly the EU case filed in August 2025, represents a free option. If Enanta prevails on any claim, the financial windfall could be substantial given Paxlovid's multi-billion dollar cumulative sales history. Patent litigation outcomes are inherently binary and unpredictable, but the magnitude of the potential award makes it a material consideration.

Finally, the valuation provides a margin of safety. With cash of 241.9 million dollars representing a large fraction of the company's market capitalization, investors are paying a modest premium for the pipeline. If any single program succeeds, the current valuation could prove deeply discounted.

The Bear Case

The pessimistic thesis centers on execution risk and competitive dynamics. Zelicapavir missed its primary endpoint in the RSVHR study. The FDA has historically been skeptical of regulatory pathways built primarily on subgroup analyses — even when those subgroups represent the majority of the efficacy population. The agency may require a large, expensive Phase 3 trial with a primary endpoint that the drug has not yet convincingly met. And the company may lack the resources to run it independently. A partnership would dilute the economic upside. If the Phase 3 fails, Enanta's most advanced program would be effectively dead.

The royalty decline continues to erode the financial foundation. With OMERS receiving 54.5 percent of Mavyret royalties through 2032, Enanta's retained royalty income is modest — perhaps 30 million dollars annually — against R&D spending that has been running above 100 million. The math requires either additional equity raises (more dilution), successful partnerships (not yet secured), or dramatic cost cuts (which would impair the pipeline). There is no scenario where the current trajectory is sustainable indefinitely.

The "one-hit wonder" risk is real. Enanta's entire commercial track record consists of a single collaboration in a single therapeutic area. Everything else is preclinical or clinical-stage. The company has never independently developed, manufactured, or commercialized a drug. The immunology expansion, while intellectually exciting, is at the earliest stages — discovery and IND-enabling — and years from generating any revenue. The history of biotech is littered with companies that announced exciting new therapeutic area expansions that never panned out.

Competitive dynamics could overwhelm Enanta's scientific advantages. In RSV, Shionogi and potentially other players are advancing rival antivirals. In immunology, the company faces entrenched competitors with decades of experience and billions in annual R&D budgets. The risk of being outspent and outpaced by larger, better-funded companies — the same dynamic that played out in COVID — applies to every program in the pipeline.

The stock's journey from 127 to 4 to 14 dollars reflects market uncertainty about whether the company can successfully navigate the transition from HCV royalty recipient to multi-franchise drug developer. Until a program produces late-stage clinical validation and a clear path to commercial revenue, that uncertainty will persist.

Key Metrics to Monitor

For investors tracking Enanta's trajectory, three metrics matter most.

First, quarterly royalty revenue from AbbVie. This is the company's only recurring revenue source and funds a portion of ongoing operations. The trend — and particularly the rate of decline — determines how long Enanta can sustain R&D investment before needing additional capital.

Second, cash position and projected runway. With 241.9 million dollars as of December 2025 and management guidance of funding into fiscal 2029, any acceleration or deceleration in burn rate directly impacts the company's negotiating leverage with potential partners and its ability to advance programs independently.

Third, clinical milestone achievement — specifically the outcome of the Q2 2026 FDA alignment meeting for zelicapavir and the progression of immunology candidates into clinical trials. Each positive milestone reduces risk and potentially unlocks partnership value; each delay or setback compounds the bear case.

XV. The Path Forward

Enanta Pharmaceuticals stands at a crossroads that will feel familiar to students of biotech history. The company possesses genuine scientific excellence, a proven track record of discovering billion-dollar molecules, and a pipeline spanning virology and immunology. It also faces the uncomfortable reality of declining royalty revenue, no approved products of its own, and clinical programs that have shown promise but not yet delivered the definitive proof of efficacy that regulators and partners require.

The next twelve to twenty-four months will be decisive. The FDA alignment meeting on zelicapavir Phase 3 design, expected in the second quarter of 2026, represents the most important near-term catalyst. If the FDA agrees to a trial design focused on the high-risk population where zelicapavir showed its strongest signal, the path to approval becomes clearer — and more fundable. If the agency requires a broader study with a more stringent primary endpoint, the cost and risk increase substantially.

The immunology expansion adds a new dimension to the story. EDP-978, the KIT inhibitor for chronic spontaneous urticaria, is expected to enter clinical trials in 2026, with Phase 1 data targeted for the fourth quarter. If the company can demonstrate that its drug design capabilities translate beyond virology, it could open up therapeutic markets that dwarf the RSV opportunity.

What would success look like? In the near term: a clear regulatory path for zelicapavir, a partnership that validates the RSV franchise, and positive early clinical data in immunology. Over the longer term: multiple approved products generating sustainable revenue, reducing dependence on declining HCV royalties. The ultimate measure is whether Enanta can convert its scientific platform — the chemists, the compound libraries, the protease inhibitor expertise — into a durably profitable pharmaceutical company.

The bigger picture extends beyond Enanta's financial statements. The company's work on antiviral protease inhibitors has contributed directly to pandemic preparedness. The RSV antiviral program, if successful, would address a disease that kills tens of thousands annually and for which no treatment exists. The scientific platform that Enanta has built over three decades represents a national asset in the fight against infectious disease — even if the stock market has not always valued it accordingly.

For other biotechs, Enanta's story offers both inspiration and caution. The discovery shop model can generate extraordinary value when paired with the right partner and the right disease. But it also creates structural vulnerabilities — dependency on a single revenue source, limited control over commercialization, and the ever-present challenge of funding the next program before the current one runs out. The tension between scientific excellence and commercial viability is not unique to Enanta, but few companies have lived it so vividly.

There is also the acquisition question. At a market capitalization under 300 million dollars, with 242 million in cash, investors are effectively valuing Enanta's entire pipeline and scientific platform at a modest premium to its bank account. For a larger pharmaceutical company seeking to acquire antiviral expertise, RSV treatment candidates, or an immunology entry point, Enanta represents a potential acquisition target at a valuation that might look attractive relative to the cost of building similar capabilities internally. Whether management would entertain an acquisition, and at what premium, is an open question — but the possibility provides a floor of sorts for the stock.

The Enanta story is far from over. Whether the next chapter is one of resurgence — fueled by RSV approval and immunology diversification — or a more difficult narrative of continued struggle, the fundamental question remains the same one Jay Luly confronted when he walked into a nearly bankrupt company in the summer of 2003: is the science good enough, and can we find a way to make it matter?

XVI. Further Reading

Top 10 Resources for Deep Dive:

- Enanta's 10-K annual filings (2014-2025) — detailed partnership economics, royalty structures, and strategic evolution

- "The Hepatitis C Wars" article series in Nature Reviews Drug Discovery — essential context on the HCV drug development revolution

- Abbott/AbbVie collaboration press releases and SEC filings (2006-2025) — deal structure evolution and milestone tracking

- ClinicalTrials.gov registry entries for zelicapavir, EDP-323, and EDP-235 — trial design and enrollment details

- Bruce Booth's Atlas Venture blog on biotech valuation frameworks — intellectual context for evaluating discovery-stage companies

- FDA Antiviral Advisory Committee meeting transcripts — regulatory thinking on antiviral development pathways

- RSVHR and RSVPEDs trial publications and conference presentations — primary clinical efficacy data

- Senate Finance Committee Wyden-Grassley investigation into HCV drug pricing — the pricing war in granular detail

- Life Science Leader profiles of Jay Luly — "From Failure to Formidable" — founding narrative and leadership philosophy

- Academic literature on structure-based drug design — the methodology underlying Enanta's core competency

Book References:

- The Billion Dollar Molecule by Barry Werth — the Vertex founding story that contextualizes the Cambridge drug discovery ecosystem from which Enanta emerged

- Biotech Valuation by Boris Bogdan — frameworks for understanding small-cap biotech economics and the discovery-stage investment thesis

- The Antiviral Agents (multiple editions) — technical grounding in the mechanisms of action that underpin Enanta's entire pipeline

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube