Emcor Group: From Bankruptcy to Building America's Infrastructure Empire

I. Cold Open & Episode Roadmap

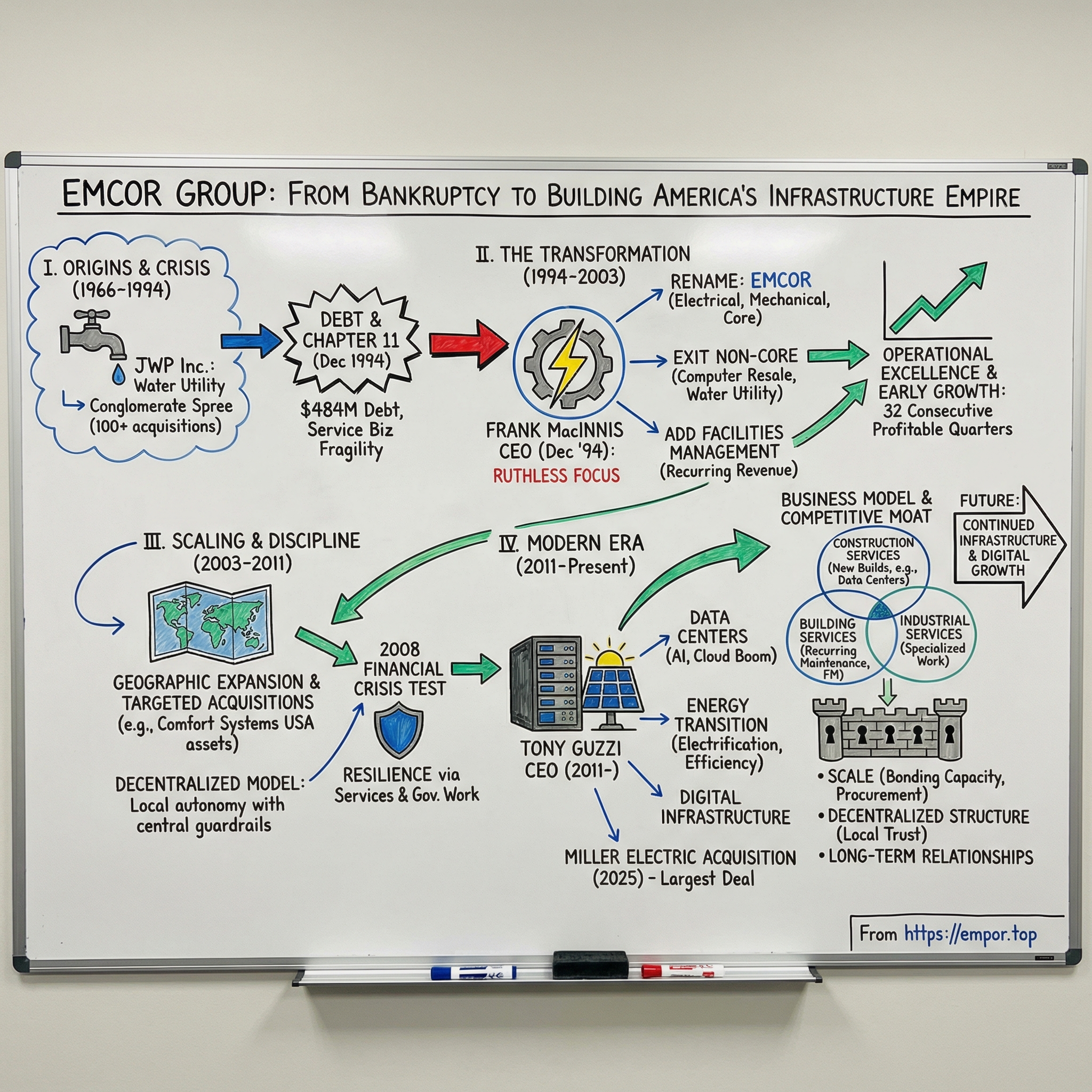

Picture this: December 15, 1994. A sprawling conglomerate with $2.8 billion in debt emerges from one of the largest Chapter 11 bankruptcies in American corporate history. The company's creditors—50 bankers, insurance companies, and equity funds—have just exchanged $484 million in debt for $180 million in new obligations and complete control of the equity. Most observers expect the firm to be carved up and sold for parts within months.

Fast forward three decades. That same company, now called Emcor Group, generates $14.6 billion in annual revenue, ranks 324th on the Fortune 500, and stands as the second-largest specialty contractor in America according to Engineering News-Record. Its stock has delivered a total return exceeding 3,000% since emerging from bankruptcy—crushing the S&P 500's performance over the same period.

The transformation reads like fiction: A water utility company that lost its way in the go-go 1980s, gorged itself on debt-fueled acquisitions including a disastrous computer reseller purchase, collapsed spectacularly, then rose from the ashes to become the backbone of America's most critical infrastructure—from data centers powering AI to energy systems driving the green transition.

How does a company go from supplying water to Long Island homeowners to installing the electrical and mechanical systems in the nation's most sophisticated semiconductor fabs? How does a firm that couldn't pay its bills in 1993 become the go-to contractor for hyperscale data centers three decades later? And perhaps most intriguingly—why has almost no one heard of a Fortune 500 company that touches nearly every aspect of modern American infrastructure?

The Emcor story offers a masterclass in corporate transformation, but it's more than that. It's a window into how America's physical infrastructure actually gets built and maintained—the unsexy but essential work of installing HVAC systems, running electrical conduits, and maintaining building controls. It's about the power of operational excellence over financial engineering, the advantage of being boring in a world obsessed with disruption, and how sometimes the best businesses are hiding in plain sight.

This is also a story about timing—how Emcor positioned itself perfectly for three successive waves of infrastructure investment: the outsourcing boom of the 1990s, the energy efficiency movement of the 2000s, and now the AI-driven data center explosion of the 2020s. Each transition could have killed the company. Instead, each one made it stronger.

At the heart of this transformation stands Frank MacInnis, a Canadian oil and gas veteran who took the CEO job just weeks after the bankruptcy filing. His first quote to analysts was sobering: "I don't know of a larger service company that's ever survived Chapter 11 reorganization." Yet survive it did—and then some.

The playbook MacInnis created—radical focus, decentralized operations with centralized control, counter-cyclical revenue streams through services, and disciplined M&A—has now been executed across three CEO tenures and multiple economic cycles. It's a playbook that turned a failed conglomerate into what might be America's most important company you've never thought about.

Today, when you walk into a modern office building, hospital, or data center, there's a good chance Emcor touched it—installing the electrical systems, maintaining the HVAC, managing the facilities, or all of the above. The company has become infrastructure-as-a-service before that was even a concept, embedding itself so deeply into America's built environment that it's become almost invisible.

The themes we'll explore—crisis-driven transformation, operational excellence as competitive advantage, and M&A as a growth engine—offer lessons far beyond construction. This is fundamentally a story about how to rebuild a broken company, create value through focus rather than financial engineering, and position for long-term secular trends while everyone else is chasing the latest fad.

II. Origins: Water, Ambition, and the Road to Disaster (1966-1993)

The company that would become Emcor began life in 1966 as Jamaica Water Supply Company, a utility serving the prosaic but essential function of delivering water to residents of Nassau County, Long Island, and parts of Queens. It was a stable, regulated business—the kind of sleepy utility that generated predictable cash flows and modest returns. For its first decade, that's exactly what it remained.

Enter the Dwyer family. Andrew T. Dwyer, who would become the architect of both the company's dramatic expansion and eventual downfall, initially seemed like the perfect leader for a new era. When he began restructuring the financially struggling water utility in 1978, the company was a modest operation with limited ambitions. Dwyer had grander visions.

The first major move came in 1971, even before Dwyer's ascension, when the company acquired Welsbach Corporation, a Philadelphia-based electrical contracting firm. This acquisition, seemingly random for a water utility, would prove prescient—electrical contracting would eventually become the core of the reborn company. But at the time, it was just the beginning of a conglomerate strategy that would spin wildly out of control.

Under Dwyer's leadership through the 1980s, Jamaica Water Supply transformed from a utility into something entirely different—a holding company using its stable cash flows to fund an acquisition binge that would make even the most aggressive private equity firms blush. The company was riding the wave of 1980s corporate excess, when conglomerates were fashionable and debt was cheap.

The transformation accelerated dramatically in 1986 when the company adopted a new name: JWP Inc. The innocuous initials masked the dramatic shift in strategy. No longer content with water and electrical contracting, Dwyer embarked on one of the most aggressive acquisition campaigns of the era. Between 1986 and 1992, JWP acquired more than 100 companies—a staggering pace of nearly one acquisition every three weeks for six straight years.

The acquisition targets revealed no coherent strategy beyond growth for growth's sake. Electrical contractors, mechanical contractors, facilities management companies—these at least had some operational logic. But then came the computer resellers, business services firms, and other ventures that had nothing to do with the company's core competencies. It was empire-building in its purest, most dangerous form.

The fatal blow came in 1991 with the acquisition of Businessland, a computer reseller that had once been a high-flying Silicon Valley success story. Businessland had pioneered the concept of computer superstores for business customers, but by 1991 it was already struggling with declining margins and fierce competition. JWP paid $210 million for a company that was hemorrhaging cash—a disastrous bet on the commoditizing computer resale business just as Dell was beginning to revolutionize the industry with its direct sales model.

The Businessland acquisition exemplified everything wrong with JWP's strategy. Here was a water utility turned construction conglomerate buying a computer retailer at the worst possible moment. The cultures couldn't have been more different—blue-collar construction workers and Silicon Valley sales teams. The business models were incompatible—project-based construction and retail sales. And the timing was catastrophic—the computer industry was about to undergo massive disruption.

By late 1992, the debt load had become crushing. JWP had borrowed heavily to fund its acquisition spree, assuming that the cash flows from its diverse portfolio would service the debt. But many of the acquired companies were underperforming, integration costs were astronomical, and the Businessland acquisition was bleeding cash at an alarming rate. The company that had started 1986 with manageable debt and a clear focus now found itself with nearly $3 billion in obligations and no coherent strategy.

The numbers told the story of the impending disaster. Revenue had grown from a few hundred million to over $4 billion, but profitability had evaporated. Debt-to-equity ratios that would make a leveraged buyout firm nervous had become the norm. The company was essentially running three different businesses—utilities, construction services, and computer reselling—none of which had any synergy with the others.

By early 1993, the situation had become untenable. Lenders were demanding payment, cash flow couldn't cover interest payments, and the company's stock had collapsed. The board finally acted, launching a major restructuring effort in mid-1993. But it was too late. The company that Andrew Dwyer had built through relentless acquisition was about to collapse under its own weight.

The irony was palpable. Jamaica Water Supply had provided an essential service to millions of New Yorkers for decades. The electrical and mechanical contracting businesses were solid, profitable operations. But these gems were now buried under the rubble of failed diversification and excessive leverage. The stage was set for one of the most dramatic corporate bankruptcies of the 1990s—and one of the most unlikely turnarounds in American business history.

III. The Crisis Years: Bankruptcy & The Search for a Savior (1993-1994)

The death spiral accelerated through the summer of 1993. JWP's bankers, who had enthusiastically funded the acquisition binge just years earlier, now circled like vultures. Daily cash management became a crisis—the company literally struggled to make payroll at some subsidiaries while others sat on trapped cash they couldn't access due to lending covenants. It was corporate chaos at its worst: a $4 billion revenue company that couldn't pay its bills.

On August 27, 1993, JWP Inc. filed for Chapter 11 bankruptcy protection in the Southern District of New York. The filing revealed the stunning scope of the disaster: $2.8 billion in total liabilities against assets that were largely intangible or rapidly depreciating. The company listed more than 100,000 creditors—everyone from major banks to small electrical supply houses that had extended trade credit.

The bankruptcy filing sent shockwaves through multiple industries. In construction, subcontractors worried about getting paid for ongoing projects. In technology, Businessland's suppliers wondered if they'd ever see their receivables. The company's 30,000 employees faced an uncertain future. Wall Street analysts, who had once praised Dwyer's "visionary" diversification strategy, now competed to deliver the most dire predictions.

The creditors' committee—a powerful group of 50 banks, insurance companies, and distressed debt funds—faced a stark choice. They could liquidate immediately, likely recovering 20-30 cents on the dollar after bankruptcy costs. Or they could attempt something virtually unprecedented: reorganize a massive service company through Chapter 11. The challenge was that service companies, unlike manufacturers with hard assets, depend entirely on their people and relationships. Both tend to evaporate quickly in bankruptcy. The creditors made a fateful decision in September 1993: they would attempt the impossible. They hired Frank MacInnis about a month after the Chapter 11 filing to lead the company through reorganization. It was an inspired choice, though few recognized it at the time.

MacInnis, then 55, was a Canada-born, 25-year veteran of the construction industry who had spent much of his career in the oil and gas end, overseeing projects in the Middle East, England and Oklahoma. Born in Camrose, Alberta, MacInnis was an unlikely savior—a lawyer by training who had transitioned into construction and developed a reputation for fixing broken companies. He had founded a company that pioneered horizontal directional drilling, which allows easier access to hard-to-reach oil reservoirs. A massive restructuring of a company in bankruptcy was the challenge MacInnis was looking for.

MacInnis's assessment of the situation was brutally honest. In his first meeting with creditors, he delivered a sobering reality check: "I don't know of a larger service company that's ever survived Chapter 11 reorganization. The financial assets of a service organization consist predominantly of their accounts receivable, and those tend to decline in quality very quickly" in a bankruptcy situation.

The challenges were staggering. Customers were fleeing—who wanted to sign a multi-year facilities management contract with a bankrupt company? Suppliers demanded cash on delivery. The best employees were being recruited away by competitors who sensed blood in the water. The Businessland operation was hemorrhaging $10 million per month. And the company's 100-plus subsidiaries were operating as independent fiefdoms, many barely aware they were part of the same organization.

But MacInnis saw something others missed. Buried beneath the wreckage of Dwyer's conglomerate were solid operating businesses—electrical contractors that had been installing power systems for decades, mechanical contractors with deep expertise in HVAC and plumbing, facilities management operations with long-term customer relationships. These weren't glamorous businesses, but they were essential. And unlike Businessland's commodity computer reselling, they required genuine expertise that created barriers to entry.

The reorganization plan that emerged was radical in its simplicity. Over the next year, MacInnis sold off dozens of companies, including the computer reseller and the parent company, JWP, itself. Every non-core asset was jettisoned. The water utility that had started it all would be sold. Businessland was shut down immediately, stopping the bleeding. Layer upon layer of corporate overhead was stripped away.

What remained would be rebuilt around a focused strategy: electrical and mechanical construction services, supplemented by facilities management to provide recurring revenue. It was back to basics with a vengeance—doing the unglamorous but essential work of building and maintaining America's infrastructure.

The financial engineering was complex but elegant. JWP's creditors—that group of 50 financial institutions—agreed to a dramatic restructuring. They exchanged $484 million in debt for just $180 million in new obligations, taking 100% of the equity in return. It was a massive haircut, but better than liquidation. The creditors were betting that MacInnis could create more value through operations than they could recover through liquidation.

On December 15, 1994 (the "Effective Date"), the Company emerged from Chapter 11. It had been just 16 months since the initial filing—lightning fast for a reorganization of this complexity. The company that emerged bore little resemblance to the sprawling conglomerate that had collapsed. It was leaner, focused, and hungry. The transformation from JWP to Emcor was about to begin.

IV. The MacInnis Transformation: Phoenix from the Ashes (1994-1995)

The company that emerged from bankruptcy on that December day in 1994 was barely recognizable. MacInnis had performed corporate surgery with a chainsaw rather than a scalpel, and the patient had survived—barely. Revenue had been slashed from over $4 billion to under $2 billion. The employee count had dropped from 30,000 to fewer than 15,000. Entire divisions had been eliminated. But what remained was alive and focused.

The first order of business was the name. JWP Inc. carried the stench of failure—every potential customer, employee, and investor associated it with the spectacular bankruptcy. By early 1995, JWP had emerged from bankruptcy under the leadership of newly elected chairman, president, and CEO Frank T. MacInnis. The company changed its name to EMCOR Group Inc. to signal its focus on key business segments related to its electrical and mechanical construction services. (EMCOR is a fusion of the words electrical, mechanical, and core.) Company headquarters were moved from Rye Brook, New York, to Norwalk, Connecticut.

The name change was more than cosmetic. It signaled a fundamental shift in identity—from a hodgepodge conglomerate to a focused specialty contractor. The move to Norwalk represented a fresh start, away from the suburban New York offices that had housed Dwyer's empire-building dreams.

MacInnis's strategic vision was deceptively simple but revolutionary for a construction company emerging from bankruptcy. He focused on electrical and mechanical construction and the design and installation of facilities like air-conditioning and fire control systems. To protect Emcor from this cyclical mix of businesses, he added facilities management to produce a continuing stream of income after the construction phase ended.

This facilities management pivot was genius. Traditional construction companies lived and died by the project cycle—feast during booms, famine during busts. By adding facilities management, MacInnis created a counter-cyclical buffer. When new construction slowed, existing buildings still needed maintenance. When construction picked up, Emcor could bid on new projects while maintaining steady service revenue. It was portfolio theory applied to construction.

The operational transformation was even more dramatic than the strategic shift. MacInnis instituted financial discipline that would have seemed draconian to the free-spending JWP era. Every subsidiary had to report weekly cash positions. Project managers who had never worried about working capital suddenly found themselves accountable for collection of receivables. Overhead was slashed to the bone—no corporate jets, no executive dining rooms, no marble lobbies.

But MacInnis wasn't just cutting. He was building a new culture from the ground up. He personally visited every major subsidiary in the first six months, meeting with local managers and front-line workers. His message was consistent: "You're not part of a bankrupt conglomerate anymore. You're part of a focused specialty contractor that's going to be the best in the business."

The decentralized operating model that MacInnis implemented became a cornerstone of Emcor's success. Each subsidiary maintained its own identity, local relationships, and entrepreneurial culture. A electrical contractor in Texas could operate differently from one in New York, adapting to local market conditions and customer needs. But they all reported to Norwalk with standardized financial metrics and operating procedures. It was coordinated autonomy—freedom within a framework.

In 1996, the firm sold its Jamaica Water Supply unit, leaving behind the company that had originally provided the backbone for the business in the 1960s. This sale was symbolically powerful—Emcor was literally selling its birthright to fund its future. The proceeds were used to pay down debt and invest in the core electrical and mechanical operations.

The early results were nothing short of miraculous. Since the Norwalk, Connecticut-based Emcor emerged from Chapter 11 in December 1994, it has reeled off 27 straight quarters in which income has exceeded that of the same quarter of the previous year. For a company that had just emerged from bankruptcy, this was unprecedented.

The numbers told the story of the transformation. Gross margins improved from mid-single digits to low double digits as Emcor focused on higher-value services. Working capital management improved dramatically—the cash conversion cycle dropped by 30 days. Most importantly, the company was generating genuine free cash flow for the first time in years.

MacInnis also began laying the groundwork for future growth through targeted acquisitions. But these weren't the debt-fueled empire-building exercises of the JWP era. Each acquisition had to meet strict criteria: accretive to earnings within 12 months, strategic fit with existing operations, and cultural compatibility with Emcor's decentralized model. The company that had nearly died from acquisition indigestion was learning to grow again—carefully and deliberately.

The transformation wasn't without casualties. Many long-time JWP employees couldn't adapt to the new reality of accountability and austerity. Some subsidiaries that couldn't meet the new performance standards were sold or shut down. The corporate staff in Norwalk was a fraction of what JWP had maintained in Rye Brook. It was cultural shock therapy, but it worked.

By the end of 1995, less than a year after emerging from bankruptcy, Emcor had established itself as a viable, focused specialty contractor. Revenue was growing, margins were expanding, and cash flow was positive. The company that investment banks had written off as dead was very much alive. But MacInnis knew that survival wasn't enough—Emcor needed to thrive. The foundation was in place for the next phase: building a true industry leader from the ashes of failure.

V. Building the Machine: Operational Excellence & Early Growth (1995-2003)

The late 1990s should have been treacherous for a newly restructured construction company. The Asian financial crisis, the Russian debt default, the dot-com boom and bust—any of these could have derailed Emcor's fragile recovery. Instead, the company delivered one of the most remarkable runs in corporate history. From 1995 to 2003, the company recorded 32 consecutive quarters of profits, a remarkable feat for any company, especially one emerging from bankruptcy protection.

How did a company that couldn't pay its bills in 1993 achieve eight straight years of profitability? The answer lay in MacInnis's obsessive focus on operational excellence rather than financial engineering. While competitors chased the latest trends—dot-com build-outs, telecom infrastructure, speculative real estate—Emcor stuck to its knitting: electrical and mechanical construction, supplemented by steady facilities management.

The numbers validated the strategy. By 2001, Emcor had grown revenue to $3.8 billion while maintaining industry-leading margins. The stock price had increased twenty-fold from its post-bankruptcy lows. But the real transformation was cultural. Emcor had evolved from a collection of acquired companies into a unified organization with a distinct identity and operating philosophy.

The UK expansion in 1999 marked Emcor's first international foray since the bankruptcy. Unlike JWP's scattershot foreign adventures, this was a calculated move into a market with similar construction practices and legal frameworks. The acquisition of Drake & Scull, a leading UK mechanical and electrical contractor, gave Emcor a foothold in Europe's facilities management market, which was more mature than the U.S. market.

But the real strategic masterstroke came in 1998 with the creation of a joint venture with CB Richard Ellis (now CBRE), the world's largest commercial real estate services firm. This wasn't just another partnership—it was Emcor's entry into the big leagues of corporate facilities management. The joint venture gave Emcor access to CBRE's massive client base while giving CBRE technical capabilities it lacked.

The partnership structure was elegant: CBRE brought the client relationships and real estate expertise, Emcor brought the technical know-how and operational capabilities. Together, they could offer integrated facilities management to Fortune 500 companies—everything from HVAC maintenance to energy management to renovation projects. It was one-stop shopping for corporate real estate departments, and it positioned Emcor at the center of the growing outsourcing trend.

EMCOR bolstered its holdings in 2002 with the purchase of 19 companies from Comfort Systems USA, which gave it a foothold in the midwestern U.S. construction and services industry. A second purchase followed in December when the firm added Virginia-based Consolidated Engineering Services Inc. to its arsenal. These acquisitions weren't random—they filled geographic gaps in Emcor's coverage map and added specialized capabilities in growth markets.

The Comfort Systems acquisition was particularly shrewd. Comfort Systems, another roll-up in the mechanical and electrical space, was struggling with integration issues and needed cash. Emcor cherry-picked their best operations in strategic markets like Chicago, Minneapolis, and Milwaukee—markets where Emcor had limited presence. The price was right, the operations were solid, and most importantly, the acquired companies fit Emcor's decentralized model. Industry recognition validated the transformation. In 2003 alone, EMCOR was named one of "America's Most Admired Companies" by Fortune magazine, ranked 37 on Barron's "Top 500 Best Performing Companies" list, and awarded the Frost & Sullivan 2003 Customer Value Enhancement Award for Building Technologies, noting that EMCOR has enjoyed phenomenal growth and garners excellent customer loyalty. For a company that had been bankrupt just nine years earlier, these accolades represented a stunning reversal of fortune.

The operational metrics during this period were extraordinary. Customer retention rates exceeded 95% in facilities management. Project completion rates hit industry highs. Safety metrics improved dramatically—lost-time incidents dropped by 60% between 1995 and 2003. These weren't just numbers on a spreadsheet; they represented a fundamental transformation in how the company operated.

MacInnis's management philosophy during this period became legendary within the industry. He instituted what he called "disciplined entrepreneurship"—giving local managers significant autonomy while holding them accountable for strict financial and operational metrics. Each subsidiary president ran their business like an owner, but with the backing of a Fortune 500 company's balance sheet and bonding capacity.

The company's approach to technology during the dot-com era exemplified its newfound discipline. While competitors rushed to create online marketplaces and digital platforms, Emcor focused on using technology to improve operations—project management systems, financial reporting tools, safety tracking databases. It was unglamorous but effective, improving margins while others chased venture capital valuations.

The facilities management business evolved from an afterthought to a strategic advantage during this period. By 2003, recurring service revenue exceeded $1 billion annually, providing a steady cash flow stream that smoothed the inherent volatility of construction. More importantly, facilities management contracts often led to construction projects as clients trusted Emcor with renovations and expansions.

Government relationships became another pillar of growth. To protect Emcor from this cyclical mix of businesses, he added facilities management to produce a continuing stream of income after the construction phase of a project ended. The company won contracts with agencies including the National Archives and Records Administration, the Federal Deposit Insurance Corporation, and the Government Accountability Office. These weren't the highest-margin projects, but they provided steady work and enhanced Emcor's credibility with private sector clients.

The company's M&A strategy during this period was surgical. Unlike the JWP era's indiscriminate buying, each acquisition had to meet specific criteria: geographic fit, cultural alignment, immediate earnings accretion, and strategic value. Between 1995 and 2003, Emcor completed over 30 acquisitions, but the total consideration was less than what JWP had spent on Businessland alone.

By 2003, Emcor had transformed from bankruptcy survivor to industry leader. Revenue approached $4 billion. The company employed 26,000 people across more than 70 subsidiaries. It had operations in 40 states and the UK. Most remarkably, it had achieved all this growth while maintaining the financial discipline that MacInnis had instituted during the crisis.

The culture that emerged during these eight years would define Emcor for decades to come. It was a culture of accountability, operational excellence, and controlled growth. Employees who had survived the bankruptcy wore it as a badge of honor—they had been through the worst and emerged stronger. New hires were indoctrinated with stories of the turnaround, creating a shared mythology that bonded the organization.

But MacInnis knew that past success guaranteed nothing. The construction industry was consolidating, competitors were getting larger, and new challenges—from technology disruption to changing workforce demographics—loomed on the horizon. Emcor had proven it could survive and even thrive. Now it needed to prove it could dominate.

VI. The Scale Game: Acquisitions & Geographic Expansion (2003-2011)

The mid-2000s presented Emcor with a strategic inflection point. The company had proven its operational model worked, but remaining a $4 billion regional player meant vulnerability to economic cycles and limited growth potential. MacInnis and his team embarked on an ambitious expansion strategy, but one fundamentally different from JWP's failed empire-building. Through its "growth through diversity" strategy—which focused on broadening company services, branching out into new geographical areas, and moving into new markets sectors—EMCOR appeared to be well positioned for future growth.

The strategy had three pillars: geographic expansion to reduce regional concentration risk, service line extensions to capture more wallet share from existing customers, and vertical market specialization to build defensible niches. Every move was calculated to strengthen the core while expanding the addressable market.

The 2005 acquisition of Poole & Kent, a major mechanical contractor in the Southeast, exemplified the new approach. Poole & Kent brought deep relationships in the pharmaceutical and biotechnology sectors—industries requiring sophisticated clean room construction and validation services. The purchase price of $140 million seemed steep, but within 18 months, Poole & Kent was generating returns exceeding Emcor's cost of capital.

What made these acquisitions work wasn't financial engineering but operational integration. Within 90 days of closing, acquired companies were converted to Emcor's financial systems. Safety programs were standardized immediately. Best practices were shared across the platform. But critically, local brands and management teams were retained, preserving the relationships that made these businesses valuable.

The housing bubble of 2004-2007 created both opportunity and temptation. While competitors gorged on residential construction and speculative commercial development, Emcor stayed disciplined. The company focused on mission-critical facilities—data centers, hospitals, pharmaceutical plants—that would need service regardless of economic conditions. This discipline would prove prescient when the financial crisis hit.

Geographic expansion accelerated through 2006 and 2007. Emcor entered new markets including Phoenix, Portland, and Salt Lake City through targeted acquisitions. Each expansion followed a playbook: acquire a strong local player, integrate their back office while preserving their market presence, then use them as a platform for additional bolt-on acquisitions. It was empire-building, but with operational discipline at its core.

The company's push into energy services during this period proved particularly prescient. As energy costs soared and sustainability became a boardroom priority, Emcor positioned itself as a one-stop shop for energy efficiency retrofits. The company could audit a facility, design improvements, implement upgrades, and guarantee energy savings—a comprehensive offering that few competitors could match.

Then came 2008. The financial crisis that destroyed countless construction companies became Emcor's opportunity to demonstrate the resilience of its model. While new construction ground to a halt, Emcor's facilities management business—now generating over $2 billion annually—provided steady cash flow. The company didn't just survive the crisis; it used it to consolidate market share.

As competitors struggled with liquidity, Emcor went shopping. The company acquired distressed assets at attractive valuations, picking up skilled teams and customer relationships at fraction of replacement cost. Between 2008 and 2010, Emcor completed 15 acquisitions, spending less than $200 million total—a fraction of what these businesses would have commanded in 2007.

The crisis also accelerated a generational transition in leadership. McInnis retired as CEO in January 2011 and as chairman in 2015. His handpicked successor, Tony Guzzi, had been with the company since 1999 and understood both the culture MacInnis had built and the need to evolve for a new era. The transition was seamless—a testament to the institutional strength MacInnis had created.

Guzzi brought a different but complementary skill set. Where MacInnis was the turnaround artist who saved the company, Guzzi was the operator who could scale it. He had run several of Emcor's largest subsidiaries and understood the business from the ground up. His appointment signaled continuity with evolution—the core values would remain, but the company would become more sophisticated in its approach to growth.

By 2011, Emcor had transformed from a domestic construction company to a international infrastructure services platform. Revenue exceeded $5.6 billion. The company operated in 45 states and multiple countries. It employed over 29,000 people. Most importantly, it had proven that its model could withstand the worst economic crisis since the Great Depression.

The geographic footprint now covered every major U.S. metropolitan area. Service capabilities spanned from traditional electrical and mechanical to sophisticated building automation and energy management. Vertical market expertise included healthcare, technology, pharmaceutical, government, and commercial real estate. It was the diversification JWP had attempted, but achieved through operational excellence rather than financial engineering.

The M&A machine MacInnis built had become self-sustaining. Emcor now had a reputation as the preferred buyer for family-owned construction businesses looking for succession solutions. Sellers knew Emcor would preserve their legacy, retain their people, and provide resources for growth. This reputation created a proprietary deal flow that gave Emcor first look at many attractive acquisitions.

Looking back, the 2003-2011 period represented Emcor's transition from recovery to dominance. The company had used disciplined expansion to build scale advantages that would be difficult for competitors to replicate. It had created a counter-cyclical business model that could prosper in any economic environment. Most importantly, it had institutionalized the operational excellence that MacInnis had instilled, ensuring the culture would survive leadership transitions.

VII. The Modern Era: Data Centers, Energy Transition & Digital Infrastructure (2011-Present)

Tony Guzzi's ascension to CEO in 2011 coincided with the early stages of a technological transformation that would redefine Emcor's growth trajectory. The cloud computing revolution was driving unprecedented demand for data center construction. The energy transition was creating massive opportunities in efficiency retrofits and renewable energy installation. And the digitization of building systems was opening new service lines around smart buildings and IoT infrastructure.

Guzzi recognized these trends early and positioned Emcor aggressively. The company's data center capabilities, which had been a modest business line in 2010, became a strategic priority. Emcor invested heavily in training, equipment, and certifications required for mission-critical facility construction. The bet paid off spectacularly.

Large projects in this division relate to data centers, data and fiber projects, and cabling, as well as semiconductor, biotech, life sciences, and pharmaceutical facilities. By 2015, Emcor had become a preferred contractor for hyperscale data centers, working with every major cloud provider. These weren't just construction projects—they were complex engineering challenges requiring coordination of electrical, mechanical, and control systems at unprecedented scale.

The numbers told the story of the transformation. Data center-related revenue grew from less than $200 million in 2011 to over $2 billion by 2020. More importantly, these projects showcased Emcor's ability to handle complexity at scale—building facilities that required 100+ megawatts of power, installing cooling systems capable of handling enormous heat loads, and ensuring 99.999% uptime reliability.

The energy transition created another growth vector. As corporations committed to net-zero targets, they needed partners who could deliver comprehensive energy solutions. Emcor's 2023 acquisition of ECM Holding Group exemplified this strategy. In 1994, Jamaica Water Properties filed for bankruptcy after making acquisitions unrelated to its core business and incurring significant debt. Frank MacInnis became CEO of the company, sold many of the businesses and renamed the remaining company as Emcor. The company also added facilities management services to provide a steady revenue stream

July 5, 2023 – EMCOR announced agreement to acquire ECM Holding Group, Inc., a leading national energy efficiency specialty services firm. ECM is a leading national provider of energy efficiency retrofit services, with specific business units dedicated to offering a variety of HVAC, lighting, water, weatherization, and airflow management solutions. With 2023 estimated revenues of $60 million, ECM brought exactly the capabilities Emcor needed to capitalize on the energy transition.

The real transformation accelerated with Emcor's electrical construction segment, which continues to benefit from surging demand in data centers, with 85% of network and communications backlog tied to this vertical. EMCOR is active across 16–17 geographies for electrical work and expanding mechanically as well, with rising demand for cooling infrastructure driven by AI data centers. The company had positioned itself perfectly for the AI revolution before most investors even understood what was coming.

Revenue for Q1 2025 came in at $3.87 billion, reflecting 12.7% year-over-year growth. The integration of Miller Electric contributed significantly to growth, while the company's adjusted operating margin expanded to 8.5%, supported by prefabrication and virtual design capabilities. The company's backlog (Remaining Performance Obligations, or RPOs) grew 28.1% year over year to $11.8 billion.

But the crown jewel acquisition came in January 2025. EMCOR Group, Inc. announced that it has entered into a definitive agreement to acquire Miller Electric Company, a leading electrical contractor serving high growth areas across the Southeastern U.S., for $865 million in cash. Headquartered in Jacksonville, Florida, Miller Electric designs, installs, maintains, upgrades, and replaces complex electrical systems and related technologies across the Southeast. Miller Electric is a trusted partner to more than 1,000 clients across a broad array of industries, with a focus on high growth sectors including data centers, manufacturing, and healthcare.

The Miller Electric acquisition was transformative. Miller Electric has a strong growth, margin, and free cash flow profile, with approximately 90% of the company's revenues currently generated from Florida and the greater Southeastern U.S., where EMCOR has limited electrical construction presence today. EMCOR expects Miller Electric to generate approximately $805 million in revenue and approximately $80 million in Adjusted EBITDA in calendar year 2024. As of November 2024, Miller Electric had $755 million in remaining performance obligations.

Tony Guzzi's assessment of the acquisition revealed his strategic vision: "The team at Miller Electric has built a legacy of delivering high-quality solutions beyond traditional electrical contracting and staying ahead of industry trends through their commitment to innovation. Their service-first mindset, long-standing reputation of excellence, and forward-thinking approach have positioned Miller Electric as a leading non-residential electrical and technology contractor in the Southeastern Uni[ted States]".

The transaction is expected to be modestly accretive to EMCOR's earnings per share in 2025, with further accretion in future years. More importantly, it positioned Emcor as the dominant electrical contractor in the fastest-growing region of the United States, just as data center construction was accelerating to unprecedented levels.

The modern Emcor had evolved far beyond MacInnis's original vision. While he had saved the company and built the foundation, Guzzi had transformed it into a technology-enabled infrastructure powerhouse. The company now offered everything from traditional electrical and mechanical construction to sophisticated building automation, energy management systems, and mission-critical facility construction.

The numbers validated the strategy. By 2024, Emcor generated $14.6 billion in revenue—nearly four times what it had been when Guzzi took over. The company ranked 324th on the Fortune 500 and 2nd by Engineering News-Record on its list of the top 600 specialty contractors. Market capitalization exceeded $30 billion, making it one of the most valuable construction companies in the world.

VIII. Business Model & Competitive Moat

Emcor's business model represents a masterclass in creating sustainable competitive advantages in what many consider a commoditized industry. The three-segment strategy—Construction services (67% of revenue), Building services (24%), and Industrial services (9%)—creates multiple revenue streams that balance cyclical exposure with recurring income.

The construction services division has evolved far beyond traditional contracting. The company's electrical and mechanical construction services division provides construction and operation services for infrastructure such as power stations, including those that provide sustainable energy such as photovoltaic systems. But it's the complexity and scale of projects that sets Emcor apart. Building a hyperscale data center requires coordinating electrical systems drawing 100+ megawatts, cooling infrastructure handling massive heat loads, and control systems ensuring five-nines reliability. Few companies have the expertise, bonding capacity, and track record to handle such projects.

The decentralized operating model remains core to Emcor's success. Over 100 operating subsidiaries and approximately 180 locations operate with significant autonomy, maintaining local relationships and market knowledge. Each subsidiary president runs their business like an entrepreneur, but with access to Emcor's balance sheet, bonding capacity, and operational best practices. This structure allows Emcor to be both large and nimble—capturing economies of scale while maintaining local market responsiveness.

Government relationships provide another competitive moat. Notable government agencies that the company provides services for include the National Archives and Records Administration, the Federal Deposit Insurance Corporation, and the Government Accountability Office. These relationships, built over decades, create high switching costs and provide steady, predictable revenue streams. Government contracts also enhance Emcor's credibility with private sector clients who value the rigorous vetting and compliance requirements.

The facilities management business has become increasingly sophisticated. What started as basic HVAC maintenance has evolved into comprehensive building optimization—using IoT sensors, predictive analytics, and energy management systems to reduce operating costs and improve building performance. This creates deep customer relationships that are difficult for competitors to displace.

Scale advantages manifest in multiple ways. Emcor's size provides superior purchasing power with equipment manufacturers and suppliers. The company's bonding capacity allows it to bid on projects that smaller competitors cannot touch. Its geographic footprint enables it to serve national clients across multiple locations with consistent service quality. And its financial strength allows it to invest in technology, training, and equipment that smaller players cannot afford.

The acquisition machine Emcor has built creates a virtuous cycle. The company's reputation as a good acquirer—one that preserves local brands, retains employees, and provides growth resources—gives it first look at many family-owned businesses seeking succession solutions. This proprietary deal flow, combined with disciplined integration processes, allows Emcor to consistently create value through M&A.

Recurring revenue from facilities management now exceeds $3 billion annually, providing cash flow stability that smooths construction volatility. These service contracts often span 3-5 years with high renewal rates, creating predictable revenue streams. More importantly, they provide continuous customer touchpoints that often lead to construction projects as clients trust Emcor with expansions and renovations.

The company's position in mission-critical facilities creates another barrier to entry. Data centers, hospitals, pharmaceutical plants, and semiconductor fabs cannot tolerate downtime. Once Emcor is embedded in these facilities—understanding their systems, maintaining their equipment, holding their trust—switching costs become prohibitive. A data center operator won't risk changing contractors to save a few percentage points when billions of dollars of computing infrastructure depend on flawless execution.

Training and workforce development represent an underappreciated competitive advantage. Emcor invests heavily in apprenticeship programs, technical training, and safety education. In an industry facing severe skilled labor shortages, Emcor's ability to develop and retain talent becomes increasingly valuable. The company's safety record—consistently outperforming industry averages—not only reduces costs but enhances its ability to win projects where safety is paramount.

The technology investments Guzzi has championed—in building information modeling, prefabrication, virtual design, and project management systems—improve productivity and margins while creating capabilities smaller competitors cannot match. These aren't flashy consumer technologies, but they fundamentally improve how buildings get built and maintained.

IX. Playbook: Lessons in Corporate Turnarounds

The Emcor transformation offers timeless lessons for corporate turnarounds that extend far beyond construction. The first and most crucial insight: crisis can be opportunity, but only with the right leadership and strategy. Frank MacInnis didn't just restructure debt and cut costs—he fundamentally reimagined what the company could become. Bankruptcy forced decisions that might have taken years in normal circumstances.

The power of focus cannot be overstated. JWP failed because it tried to be everything—water utility, construction company, computer retailer. Emcor succeeded by choosing a lane and dominating it. The discipline to say no to attractive opportunities outside the core competency proved more valuable than any single acquisition or contract win.

The M&A playbook Emcor developed should be required reading for any serial acquirer. Each acquisition must be immediately accretive, strategically logical, and culturally compatible. No empire building, no ego deals, no betting the company on transformative acquisitions. Small, disciplined deals that compound over time create more value than moonshot acquisitions.

Building a decentralized empire with centralized control represents one of the most difficult organizational challenges in business. Emcor solved it by being crystal clear about what gets centralized (financial reporting, safety standards, best practices) and what stays local (customer relationships, pricing decisions, market strategy). This balance allows the company to capture scale benefits without losing entrepreneurial energy.

Creating counter-cyclical revenue streams through services proved genius. When MacInnis added facilities management to construction, he wasn't just diversifying revenue—he was fundamentally changing the business model from transactional to relational. Service contracts create customer stickiness, provide market intelligence, and generate construction opportunities.

The importance of culture in service businesses cannot be overlooked. Emcor's culture—forged in the crucible of bankruptcy, refined through decades of execution—creates sustainable competitive advantage. Employees who understand that operational excellence isn't optional, that safety isn't negotiable, that customer service drives everything, become the company's greatest asset.

Long-term thinking in a short-term world differentiates winners from survivors. Emcor could have maximized short-term profits by cutting training, reducing safety investments, or chasing risky projects. Instead, the company consistently invested in capabilities that would pay off years later—whether in workforce development, technology, or market position.

The succession planning from MacInnis to Guzzi demonstrates another crucial lesson. Great turnaround leaders build institutions, not personal empires. MacInnis spent years developing Guzzi and other internal candidates, ensuring cultural continuity while bringing fresh perspective. The seamless transition proved that Emcor had evolved from a turnaround story to a sustainable enterprise.

The discipline to maintain financial conservatism even during boom times protected Emcor through multiple cycles. While competitors leveraged up during good times, Emcor maintained a fortress balance sheet. This allowed the company to play offense during downturns, acquiring distressed assets and gaining market share while others struggled to survive.

X. Bear vs. Bull Case & Competitive Analysis

The bull case for Emcor rests on powerful secular tailwinds that could drive growth for decades. The AI revolution is driving unprecedented data center construction, with hyperscalers planning hundreds of billions in infrastructure investment. The energy transition requires massive electrical grid upgrades and building retrofits. Aging U.S. infrastructure needs extensive renovation and replacement. These aren't short-term trends but generational investment cycles that play directly to Emcor's strengths.

Based on 7 Wall Street analysts offering 12 month price targets for EMCOR Group in the last 3 months. The average price target is $670.50 with a high forecast of $750.00 and a low forecast of $435.00. The average price target represents a 9.39% change from the last price of $612.92.

The company's proven M&A machine could accelerate growth beyond organic levels. With thousands of small contractors facing succession challenges as owners retire, Emcor has a multi-decade runway for accretive acquisitions. The Miller Electric deal proves the company can execute larger transactions while maintaining discipline. Each successful acquisition strengthens Emcor's platform and makes future deals more valuable.

Operational leverage should expand margins as revenue grows. The investments in technology, training, and systems create fixed costs that become increasingly efficient at scale. Prefabrication facilities, BIM capabilities, and project management systems don't need to be replicated for each additional dollar of revenue. This operating leverage could drive margin expansion even in competitive markets.

The bear case centers on cyclical exposure despite diversification efforts. Construction remains inherently cyclical, and even Emcor's service revenue would suffer in a severe recession. The company prospered through 2008, but past performance doesn't guarantee future results. A prolonged downturn in commercial construction could pressure both revenues and margins.

Labor challenges represent a persistent threat. The construction industry faces severe skilled labor shortages, driving wage inflation and potentially constraining growth. While Emcor's training programs provide some insulation, the company cannot fully escape industry-wide demographic challenges. Competition for skilled electricians and mechanics will likely intensify, pressuring margins.

Execution risk on large projects remains omnipresent. As projects become larger and more complex—think $1 billion data center campuses—the potential for costly mistakes increases. One major project failure could damage Emcor's reputation and financial results. The company's track record is excellent, but perfection is impossible in construction.

Technology disruption, while currently benefiting Emcor, could eventually threaten traditional construction methods. Modular construction, 3D printing, and automated building systems might reduce the need for on-site construction labor. While Emcor would likely adapt, such changes could pressure margins and require significant investment.

Competition from larger players intensifies as the market consolidates. Quanta Services (market cap ~$40 billion) dominates utility and communications infrastructure. MasTec (~$12 billion) focuses on energy and communications. Comfort Systems USA (~$15 billion) competes directly in HVAC and building services. These well-capitalized competitors can match Emcor's scale advantages and compete aggressively for large projects.

Private equity involvement in construction services creates additional competitive pressure. PE firms have been rolling up mechanical and electrical contractors, creating new scaled competitors with aggressive growth mandates. These financial buyers can overpay for acquisitions, driving up multiples and making Emcor's disciplined M&A strategy more challenging.

The consensus mark for revenues is $4.1 billion, suggesting a 11.9% year-over-year increase. For 2025, EME is expected to witness 12.7% growth in revenues and a 9.6% growth in EPS from a year ago.

The balanced view recognizes both opportunity and risk. Emcor operates in attractive markets with strong secular tailwinds, but competition is intensifying and execution challenges persist. The company's track record suggests it can navigate these challenges, but investors should monitor competitive dynamics, labor availability, and project execution closely.

XI. Epilogue: What's Next for America's Infrastructure Play

The AI and data center supercycle represents perhaps the greatest opportunity in Emcor's history. As artificial intelligence drives demand for computational infrastructure, data center construction is accelerating beyond anyone's expectations. These aren't traditional data centers but massive, complex facilities requiring sophisticated electrical and cooling systems. Emcor's position as a trusted partner to hyperscalers provides tremendous growth potential.

The energy transition creates another multi-decade opportunity. Building electrification, EV charging infrastructure, renewable energy integration, and grid modernization all require Emcor's capabilities. The Inflation Reduction Act and Infrastructure Investment and Jobs Act provide federal funding that will flow through to contractors like Emcor. The company's energy services capabilities, enhanced by acquisitions like ECM, position it to capture this spending.

Consolidation opportunities in fragmented markets remain abundant. Despite decades of M&A, the construction industry remains highly fragmented with thousands of small, family-owned businesses. As baby boomer owners retire, Emcor can continue its disciplined acquisition strategy, adding capabilities and geographic coverage while maintaining its cultural focus on operational excellence.

The lessons from Emcor's transformation apply broadly to any business facing existential crisis. The combination of decisive leadership, strategic focus, operational discipline, and cultural transformation can resurrect even the most troubled enterprises. But it requires courage to make hard decisions, discipline to stay the course, and patience to build sustainable competitive advantages.

Looking forward, Emcor appears positioned to benefit from multiple megatrends while maintaining the operational discipline that enabled its remarkable transformation. The company that emerged from bankruptcy 30 years ago has become essential infrastructure for the modern economy—building and maintaining the physical systems that enable digital transformation, energy transition, and economic growth.

The remarkable journey from Jamaica Water Supply to Fortune 500 infrastructure leader demonstrates that corporate transformation is possible but never easy. It requires leadership willing to make difficult decisions, employees committed to operational excellence, and strategies that balance growth with discipline. Emcor's story isn't just about financial engineering or lucky timing—it's about building a culture and business model that can prosper through any economic environment.

For investors, Emcor represents a unique combination of growth and stability, cyclical exposure and recurring revenue, consolidation opportunity and operational excellence. The company trades at reasonable multiples despite its strong competitive position and secular tailwinds. While risks exist—from labor shortages to execution challenges—the company's track record suggests it can navigate these obstacles while continuing to compound value.

The broader lesson for American business is that operational excellence still matters. In an era obsessed with disruption and transformation, Emcor proves that doing essential work exceptionally well creates lasting value. The company doesn't make headlines like tech unicorns or meme stocks, but it builds the infrastructure that makes modern life possible. There's profound value in that kind of essential, excellently executed work.

As America faces massive infrastructure needs—from upgrading electrical grids for renewable energy to building data centers for AI to retrofitting buildings for energy efficiency—companies like Emcor become increasingly critical. The next chapter of the Emcor story will be written by how well it executes on these opportunities while maintaining the discipline that enabled its remarkable resurrection.

The company that couldn't pay its bills in 1993 now stands as one of America's most important infrastructure companies. It's a testament to the power of crisis-driven transformation, the value of operational excellence, and the importance of building businesses that matter. In the end, Emcor's greatest achievement isn't its financial success but its evolution from failed conglomerate to essential infrastructure partner—a transformation that created value not just for shareholders but for the entire American economy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube