Embraer: The Southern Cross of Aviation

I. Introduction & Episode Roadmap

Picture the world map of commercial aviation as most people imagine it. There are exactly two pins on it. One sits in the Pacific Northwest, in the soggy industrial sprawl of Everett and Renton, Washington, where Boeing has bent aluminum since the days of biplanes. The other sits in Toulouse, in the south of France, where Airbus assembles jets in hangars large enough to have their own weather. For half a century, that has been the story of how the world flies: a transatlantic duopoly, Seattle versus Toulouse, an industry so capital-intensive and so brutally regulated that no one else could possibly break in.

Except someone did. And they did it from a place almost no one would think to look: a mid-sized city in the interior of São Paulo state called São José dos Campos, a two-hour drive northeast of the metropolis, ringed by eucalyptus and the green hills of the Paraíba Valley. There, a company called Embraer quietly became the third-largest manufacturer of civil aircraft on the planet. Not third by aspiration — third by units in the sky, third by the only metric that matters.

Today's subject is Embraer S.A., listed in São Paulo on the B3 exchange under the ticker EMBR3.SA and in New York under ERJ. In its 2025 fiscal year, the company reported revenues of roughly US$7.58 billion — its highest annual total ever, up 18% year over year — riding a firm order backlog that closed the year at a record US$31.6 billion.1 If you have flown a short hop between two American cities in the last fifteen years — Chicago to Cincinnati, Denver to Tulsa, Newark to anywhere — there is a very good chance you did it inside an Embraer, even if the fuselage said "Delta Connection" or "United Express" on the side.

Here is the hook, the thing that makes this an Acquired-worthy story. Brazil in the 1960s did not manufacture its own automobiles at scale. It imported. It was a country wrestling with hyperinflation that would later hit four-digit percentages, a country whose industrial base was thin and whose capital markets barely existed. And yet, out of that soil, grew a company that designs and certifies clean-sheet jet aircraft — arguably the single hardest, most unforgiving engineering act in any peacetime industry. Embraer survived the collapse of a US$4.2 billion merger with Boeing that should have killed it. It stared down a global pandemic that grounded the world's airline fleet. And it emerged on the other side with an investment-grade credit rating from all three major agencies and a backlog at all-time highs.

How? That is the question this episode answers. Our roadmap runs like this. First, the strange origin — a country that built an academy before it built a factory, creating a structural cost advantage in engineering talent that no Western rival can copy. Then the near-death-and-rebirth of privatization, and the single airplane, the ERJ 145, that saved the company. We will go deep on the two commercial engines of the modern business — regional jets and private jets — and the regulatory quirk in American labor contracts that handed Embraer a near-monopoly. We will live through the Boeing tragedy in full. We will pull apart the quiet cash machine of services and the audacious bet to take on the C-130 Hercules in military transport. And then we will do what Acquired always does at the end: run the whole thing through Porter and through Hamilton Helmer's Seven Powers, weigh the bull against the bear, and name the handful of numbers that actually tell you whether this company is winning. Let us begin where Embraer began — not on an assembly line, but in a classroom.

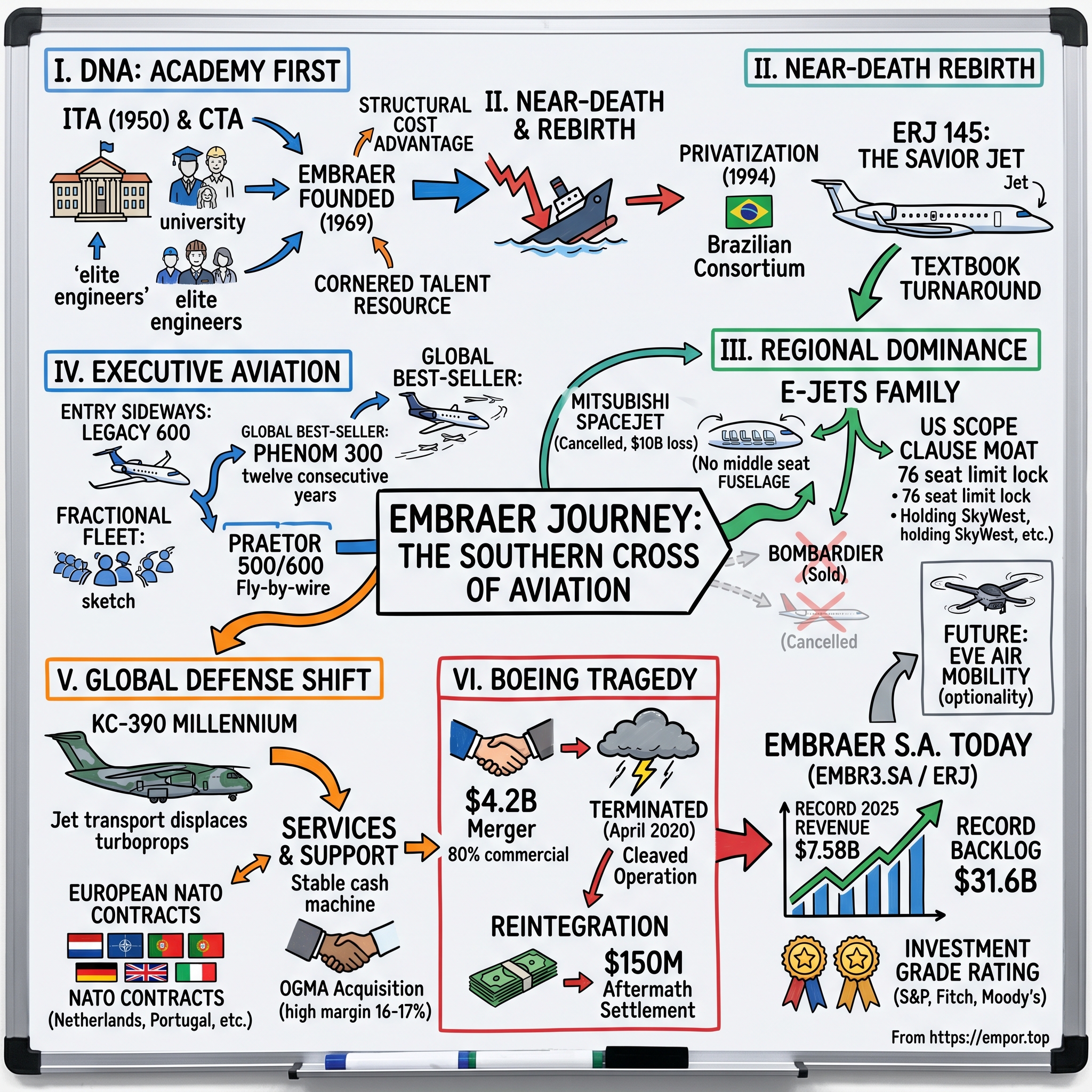

II. The DNA of Embraer: ITA, CTA, and the Brazilian Tech Cluster

The conventional way to start an aerospace industry is to build an airplane. You hire engineers, you rent a hangar, you bend metal, you fail, you try again. Brazil did something stranger and, in hindsight, far smarter. It built a university first.

The man at the center of the founding myth was an air force officer and visionary named Casimiro Montenegro Filho, who in the 1940s had flown the airmail routes over the vast, roadless interior of Brazil and understood in his bones what aviation meant for a country of continental scale. Brazil is bigger than the contiguous United States. In the 1940s, large portions of it were effectively unreachable by ground. To a generation of Brazilian military strategists, aviation was not a luxury industry — it was the literal connective tissue of national sovereignty, the only way to integrate the Amazon, the Pantanal, and the sertão into one country and to defend them.

But Montenegro and his allies had absorbed a crucial lesson from a trip to the Massachusetts Institute of Technology: you cannot import an aerospace industry. You have to grow the people. So in 1950, in São José dos Campos — chosen for its mild climate, its clear skies, and its position on the road between Rio and São Paulo — they founded the Instituto Tecnológico de Aeronáutica, the ITA, an elite aeronautical engineering school explicitly modeled on MIT, with foreign professors recruited from around the world.2 Around it grew the Centro Técnico Aeroespacial, the CTA, a cluster of military research and development institutes. The state was not trying to build a plane. It was trying to build a permanent, self-renewing supply of world-class aeronautical engineers, on Brazilian soil, paid in Brazilian currency.

It worked beyond anyone's reasonable hopes. ITA became, and remains, one of the most selective and rigorous engineering schools in all of Latin America — a place where admission is a national event and graduates are absorbed into Brazil's aerospace and technology sectors. When the government finally did spin a manufacturer out of this ecosystem in 1969 — Empresa Brasileira de Aeronáutica, Embraer, born as a state-owned enterprise — it was not starting from zero. It was harvesting two decades of accumulated human capital. The company's first head, Ozires Silva, was himself a product of this military-academic pipeline. The factory rose, quite literally, next to the schoolhouse.

Now here is why a story from 1950 belongs in a 2026 investment analysis, and why we are spending real time on it. The single most durable competitive advantage Embraer possesses today traces directly back to that founding decision. Aerospace is, at its core, an engineering-hours business. Designing and certifying an airplane consumes millions of hours of highly skilled labor — stress analysis, aerodynamics, avionics integration, systems engineering, certification paperwork that runs to the tens of thousands of pages. The dominant input cost in developing a new aircraft is not titanium or aluminum. It is the fully loaded hourly cost of an elite engineer.

And Embraer's elite engineers sit in Brazil, earning Brazilian salaries. The average hourly cost of an Embraer engineer is a fraction of what Boeing pays in the high-cost Seattle metro, what Airbus pays in Toulouse, or what Bombardier paid in Montreal — and yet, crucially, the technical output is identical or, by several measures of program execution, superior.3 This is not cheap labor in the sweatshop sense. It is the opposite: it is some of the best aeronautical talent in the world, priced against a Brazilian cost of living and a Brazilian wage scale rather than a Californian one. In Hamilton Helmer's language, which we will return to at the end, this is a cornered resource — a localized pool of elite, low-cost engineering talent that competitors cannot simply buy or relocate, because the cluster itself, with its university, its supplier base, and its decades of institutional memory, took seventy years to grow. You cannot wire that into existence with a checkbook. The lesson Embraer teaches, and we will say it again at the close, is that the country that wants a high-tech industry should not build the factory first. It should build the school. That school, however, very nearly outlived the company it created — because by the early 1990s, Embraer was almost dead.

III. Privatization and Rebirth: The ERJ 145 Savior

By 1994, the proud state enterprise was a corpse that had not yet been informed of its own death. Embraer had not delivered a meaningful new commercial program in years. Its order book was thin, its losses were staggering, and its debts had piled up to the point where the Brazilian government — itself broke, fighting the hyperinflation that would only be tamed that year by the Plano Real — could no longer fund it. The company had burned through cash for the better part of a decade. Morale was collapsing. Engineers, the cornered resource, were leaving for jobs abroad. The whisper in Brasília was liquidation: shut it down, sell the land, and end the embarrassment of a national champion that could not pay its bills.

What happened instead was one of the more consequential privatizations in Brazilian history. In December 1994, the government auctioned control of Embraer. A consortium led by the Brazilian investment bank Bozano, Simonsen, together with two large domestic pension funds — Previ, the fund for Banco do Brasil employees, and Sistel, the telecom workers' fund — took control of the company.4 The state did not vanish entirely; it retained a "golden share" giving it veto power over certain strategic and military decisions, a structure that persists to this day and that you should keep in the back of your mind as a governance feature. But operational control, and the imperative to make money, passed to private hands.

The new owners brought in management with a single, terrifying mandate: find a product that the market actually wants, and find it fast, because the cash runway is measured in months. The answer was already half-built inside the company, and it was an act of brilliant engineering frugality.

Embraer had a turboprop — the EMB 120 Brasília, a small regional propeller aircraft that had sold respectably. The team's insight was to take the hard-won knowledge embedded in that airframe, stretch the fuselage into a longer, thinner tube, and replace the propellers with two turbofan jet engines mounted on the rear of the fuselage. The result was the ERJ 145, a 50-seat regional jet. Rather than design a clean sheet from scratch — which the company could not possibly afford — they leveraged what they already knew. It was the corporate equivalent of escaping a burning building by climbing out a window you already knew was there.

The timing was, in retrospect, almost supernaturally good. In the mid-1990s, the U.S. regional airline market was on the cusp of an explosion. Major carriers were restructuring their networks around the hub-and-spoke model, feeding passengers from small cities into big hubs. The aircraft doing that feeding were aging turboprops — loud, slow, prone to bouncing in turbulence, and, fairly or not, distrusted by an American flying public that associated propellers with danger and discomfort. Passengers wanted jets. A 50-seat jet that could cruise high, fly fast, feel smooth, and connect a regional city to a hub in comfort was exactly the product the moment demanded.

The ERJ 145 family — and its smaller siblings, the ERJ 135 and 140 — became a phenomenon. Regional carriers ordered them by the hundreds. American Eagle, Continental Express, ExpressJet and others built their fleets around the type. Embraer went from a cash-bleeding ward of the state to a profitable, growing, globally relevant manufacturer in the span of a few years. The privatization that the cynics had called a fire sale instead delivered a textbook turnaround.

But the ERJ 145 also taught Embraer something profound about the shape of the market it was about to dominate. The 50-seat jet had been a derivative — clever, but compromised. The real prize would require a clean-sheet aircraft, designed from the first line on the drawing board around the specific economics and comfort demands of regional flying. That realization launched the program that would define the modern company.

IV. The Commercial Core: Capturing the Regional Skies

Walk down the aisle of a regional jet at a U.S. airport today and do a small experiment. Look at the seating. On the older 50-seaters, it is a cramped tube. But on the workhorse of the modern American regional fleet, you will notice something subtle and wonderful: every row has two seats on the left, two on the right, and an aisle in the middle. There is no middle seat. Nobody is wedged between two strangers with nowhere to put their elbows. That single design choice is worth understanding, because it is a window into how Embraer thinks, and it sits at the heart of the company's largest business — Commercial Aviation, which generated about US$2.37 billion of revenue in 2025, roughly 31% of the company total.1

Let us back up to the early 2000s. Flush with the success of the ERJ 145 but aware of its limits, Embraer made the defining bet of its modern era: a clean-sheet family of regional jets called the E-Jets — the E170, E175, E190, and E195, seating roughly 70 to 120 passengers. This was not a stretch of an old turboprop. This was a brand-new aircraft, and the company poured its accumulated engineering capital into getting the fundamentals right.

The most consequential decision was the shape of the fuselage cross-section. Most narrowbody jets — the Boeing 737, the Airbus A320 — use a single circular tube wide enough for six-abreast, 3+3 seating, which forces the dreaded middle seat. Embraer instead chose what engineers call a "double-bubble," a cross-section that is essentially two arcs joined together, producing a cabin perfectly sized for four-abreast, 2+2 seating. The genius of this was that it solved a passenger-experience problem and an airline-economics problem simultaneously. Passengers got a jet with no middle seat, wide aisles, and a feeling of spaciousness that belied the aircraft's regional size. Airlines, in turn, could market that comfort and, in many cases, charge a premium for it. Comfort became a feature you could put on a brochure. It is a beautiful example of what we will later call counter-positioning: Embraer entered a market the giants treated as an afterthought, and built something the giants' standard playbook could not easily replicate without redesigning their own airplanes.

Now to the regulatory moat, which is the single most important thing to understand about why Embraer prints money in the United States. American mainline pilots — the senior, highly paid pilots who fly for Delta, United, and American under their own brands — are represented by powerful unions. Their contracts contain provisions called scope clauses. The purpose of a scope clause is to protect mainline pilot jobs by limiting how much flying the major airline can farm out to lower-cost regional affiliates flying under names like "Delta Connection" or "United Express." And the way scope clauses draw that line is by aircraft size: regional partners are generally restricted to aircraft with no more than 76 seats and a maximum takeoff weight at or below roughly 86,000 pounds.[^5]

Sit with that for a moment, because it is the whole ballgame. The U.S. regional jet market is not bounded by physics or by passenger demand. It is bounded by a number written into labor contracts. And the Embraer E175 — the first-generation E175, to be precise — fits that box almost perfectly. It seats up to 76 passengers in a typical two-class configuration and slots in just under the weight limit. The result is that the E175-E1 became the absolute, undisputed workhorse of the U.S. regional fleet, the single most ordered scope-compliant jet, flown in vast numbers by regional operators like SkyWest, which built large fleets around the type to fly on behalf of all three major carriers.[^6]

And then Embraer's competition obligingly disappeared. For years its great rival in regional jets was Canada's Bombardier, with the CRJ family. But Bombardier, having bankrupted itself developing the larger CSeries, exited the regional jet business and sold its CRJ program to 三菱重工業 Mitsubishi Heavy Industries (MHI) of Japan. Mitsubishi had its own ambitions — a clean-sheet regional jet program originally called the MRJ and later rebranded the SpaceJet — into which it poured more than US$10 billion over roughly fifteen years. The SpaceJet was an engineering and certification catastrophe; it suffered years of delays, repeated redesigns, and an inability to clear the certification bar, and in 2023 Mitsubishi formally canceled the entire program, writing off the investment.5 When the smoke cleared, Embraer was effectively the last manufacturer standing with a modern, scope-compliant regional jet in production. It held something close to a monopoly in the segment that feeds the world's largest aviation market.

Of course, a moat built on a number in a contract is also a constraint. Embraer's next-generation E2 family — the re-engined, aerodynamically refined E190-E2 and E195-E2 — burns dramatically less fuel per seat thanks to new Pratt & Whitney geared turbofan engines and a redesigned wing. But the new technology comes with weight, and the E175-E2 ended up too heavy to fit under the U.S. scope-clause ceiling. This created a peculiar strategic split that persists today. Embraer keeps the older E175-E1 production line open specifically to serve the scope-constrained U.S. market, while marketing the larger, more efficient E2 jets globally as "crossover narrowbodies" — aircraft small enough to serve thin routes but capable enough to go head-to-head with the bottom of the mainline narrowbody market.

That is precisely where the fight gets interesting. The E2's direct competitor is the Airbus A220, an aircraft with its own dramatic backstory: it was originally Bombardier's CSeries, the very program that bankrupted Bombardier, before Airbus acquired control of it for effectively a symbolic sum and rebranded it. So Embraer now battles, in the 100-to-150-seat segment, an aircraft backed by the full marketing muscle and supply-chain scale of Airbus. Further out, the Chinese state champion 中国商飞 COMAC is building its own regional and narrowbody jets — the ARJ21 (now C909) and the larger C919 — though for now these fly almost entirely within China and for Chinese carriers. The economics of this three-way battle come down to a simple tension: Airbus can use its enormous scale to squeeze suppliers and subsidize pricing, while Embraer wins on the lower capital cost of having developed its airplane far more cheaply, and on best-in-class fuel efficiency per seat. Embraer cannot out-spend Airbus. It has to out-engineer and out-efficiency it. So far, with a regional franchise that no one else can touch, it has held its ground — and it has done so while quietly building a second business that few people associate with a Brazilian airliner company at all: private jets for the global rich.

V. The Executive Flight: From Commodity to the World's Best-Selling Light Jet

In the early 2000s, when Embraer's leadership announced they intended to enter the business-jet market, the reaction in the clubby world of private aviation ranged from polite skepticism to open laughter. The pitch sounded absurd on its face. Why would a Gulf sheikh, a Hollywood studio chief, or a Silicon Valley founder — people who buy private jets the way other people buy watches — purchase one from a company best known for building no-frills 50-seat commuter jets for regional airlines in the American Midwest? Business jets were about prestige, about the badge on the tail, about the names Gulfstream and Bombardier and Cessna. Embraer had a badge associated with the opposite of prestige: the regional puddle-jumper.

A quarter-century later, that skepticism looks spectacularly misplaced. Executive Aviation has become a co-equal pillar of the company, generating roughly US$2.2 billion in revenue in 2025 — close to 30% of the total, and growing 25% year over year, faster than the commercial side.1 How Embraer got there is a masterclass in entering a market sideways, learning, and then striking at exactly the right segment.

The first move was derivative and cautious, very much in the company's frugal DNA. Embraer took its existing regional jet airframes and converted them into large-cabin executive aircraft — the Legacy 600, essentially an ERJ 135 with a luxurious interior, extra fuel tanks for range, and the corporate name. This let Embraer dip a toe into the market without betting the company. It learned how high-net-worth buyers think, how the dealer and broker ecosystem works, how completions and interiors and customer service differ from selling fleets to airline procurement departments. It was tuition, paid cheaply.

The real bet — the clean-sheet bet — came next, and it was aimed not at the top of the market but at the bottom and middle, where the volume is. Embraer launched two purpose-built light jets, the Phenom 100 and the Phenom 300, designed from scratch for the entry-level and light-jet segments. And here Embraer found the seam in the market that would make its fortune.

The Phenom 300 turned out to be one of the great product successes in the history of business aviation. It became the best-selling light jet in the world for twelve consecutive years, a run of dominance almost unheard of in a cyclical, fashion-driven market.6 Why did it win so completely? Not because of any single headline spec, but because of a balance of them. The Phenom 300 hit a sweet spot of range, speed, cabin and baggage capacity, and — the decisive factor — exceptionally low operating costs. For the people who actually do the math on private jets, the Phenom 300 was simply the most rational airplane in its class to fly.

That last point is what made it the workhorse of the fractional-ownership operators. Companies like NetJets and Flexjet — which sell shares in aircraft and fly enormous numbers of hours — care about operating economics with a ferocity that an occasional billionaire owner does not. They are running an airline, essentially, just one with very fancy passengers. For them, a jet that costs meaningfully less per flight hour while still delivering the range and comfort customers expect is not a luxury; it is the difference between a profitable fleet and an unprofitable one. The Phenom 300 became a fractional-fleet staple, and those large, repeating fleet orders gave Embraer a volume base that prestige-only competitors struggled to match.

With the light-jet segment conquered, Embraer moved up-market into the mid-size category with the Praetor 500 and Praetor 600. And here the company executed its signature move once more: taking technology that had previously been reserved for the most expensive aircraft in the sky and pushing it down into a cheaper segment. The Praetors brought full fly-by-wire flight controls — the computerized, side-stick-controlled flight system that had long been the preserve of US$60-million-plus ultra-large-cabin jets and airliners — down into the roughly US$20-million mid-size class. For a buyer in that segment, getting airliner-grade flight control technology and intercontinental range at a mid-size price was a genuinely disruptive proposition.

The competitive set in executive aviation is a who's-who of American aerospace: General Dynamics' Gulfstream at the ultra-luxury top, Bombardier's Challenger and Global families, and Textron's Cessna Citation line, which has long dominated the light-jet volume game. Embraer does not try to out-prestige Gulfstream or out-range Bombardier's flagships. Its strategy, segment by segment, has been to deliver more capability and more technology per dollar than incumbents expect at that price point, and to back it with the operating-cost discipline that comes naturally to a company forged in the unforgiving economics of regional airlines. The same engineering cost advantage that lets Embraer win on regional jets lets it offer more airplane for the money to private buyers.

Two strong commercial businesses, both growing, both leaders in their niches. By 2017, Embraer looked like a company that had fully arrived. And it was precisely at that moment of strength that it walked to the edge of an abyss — because the biggest player in the industry came knocking with a checkbook, and what followed nearly destroyed it.

VI. The Boeing Tragedy & Triumph: The Failed $4.2B Merger and the $150M Aftermath

The chain of events that nearly broke Embraer began, as so many corporate dramas do, with a rival's move on a distant chessboard. In 2017 and into 2018, Airbus completed its takeover of Bombardier's CSeries program — the small narrowbody we met earlier, soon to be rebranded the A220. For Boeing, this was a strategic gut-punch. Airbus now had a credible, modern, fuel-efficient aircraft at the small end of the narrowbody market, a segment where Boeing's offerings were aging and weak. Boeing looked across the board, saw the one company in the world with the engineering pedigree and product line to plug that gap — Embraer — and decided to do exactly what Airbus had done. It would buy its way in.

The deal announced was breathtaking in scale by the standards of Brazilian industry. Boeing proposed to acquire an 80% stake in Embraer's commercial aviation division for US$4.2 billion, valuing that division at US$5.26 billion and creating a joint venture, to be called Boeing Brasil-Commercial. Embraer's defense and executive-jet businesses would remain separate and Brazilian. For Embraer's commercial arm, it promised the backing of the world's largest aerospace company — access to Boeing's sales force, its supply-chain heft, its global support network. On paper, it was the deal that would secure the regional franchise forever.

Executing it, however, required something agonizing and expensive: a corporate carve-out. You cannot simply hand over a "commercial division" that has spent fifty years tangled up with the rest of the company. Embraer spent the better part of two years and, by its own accounting, over US$120 million physically separating the commercial business from the defense and executive divisions — splitting IT systems, untangling shared factories and tooling, dividing personnel, redrawing the org chart of a deeply integrated enterprise, all in anticipation of a closing that everyone assumed was a formality.7 The golden share gave the Brazilian government a vote, and it gave its approval. The structure was set. The lawyers were circling the closing table.

Then the world fell apart, twice. First, Boeing's own house caught fire: the 737 MAX, its best-selling aircraft, was grounded worldwide in 2019 after two catastrophic crashes, a crisis that consumed Boeing's management attention and tens of billions of dollars in cash. Then, in early 2020, COVID-19 grounded essentially the entire global airline fleet, vaporizing demand for new aircraft and turning Boeing's balance sheet from stressed to desperate.

On April 25, 2020, Boeing terminated the agreement. It claimed Embraer had failed to satisfy certain closing conditions. Embraer's leadership saw it differently and said so bluntly — that Boeing had "wrongfully terminated" a deal it no longer wanted because it could no longer afford it, manufacturing a pretext to walk away from a Brazilian company at the worst possible moment.8 Whatever the legal truth, the human and financial truth was brutal. Embraer had been left at the altar. Its commercial business sat physically and operationally cleaved from the rest of the company. It had spent over US$120 million preparing for a wedding that never happened, it was now bleeding cash into the teeth of the worst aviation downturn in history, and it was holding the bill for a separation it now had to reverse.

This is the moment that defines the modern company, and it is why Embraer belongs in any serious conversation about corporate resilience. Faced with what could easily have been a death spiral — a fractured organization, a collapsing market, a damaged balance sheet — management refused to die. They launched a sweeping reintegration program to stitch the company back together, folding the commercial division back into the whole. They slashed costs, optimized the asset base, renegotiated with suppliers, and rebuilt liquidity airplane by airplane through the depths of the pandemic. And they took Boeing to international arbitration, refusing to let the larger company simply walk away clean.

The legal chapter closed in September 2024. Boeing agreed to pay Embraer US$150 million in gross compensation to settle all claims arising from the failed merger.[^11] Read that number against the original US$4.2 billion and it looks, at first glance, like a humiliation — three cents on the dollar of the value the deal was supposed to create. But that framing misses the point entirely. The US$4.2 billion was never going to be a cash windfall; it was the price of selling 80% of the franchise. The settlement was about a different thing: vindication and liquidity. It validated Embraer's position that it had not been the party at fault, it closed a painful and distracting chapter, and it delivered US$150 million of non-dilutive cash — money raised without selling a single new share — that the company could pour straight into paying down debt. The most important outcome of the entire Boeing saga, in the end, was not the settlement check. It was that Embraer learned it could survive being abandoned by the largest company in its industry, in the worst market in living memory, and come out the other side independent and intact. That hard-won resilience would soon be visible in the part of the business that quietly generates the company's best margins.

VII. The Quiet Cash Machine: Services & Support

Aerospace headlines are written about deliveries. The press release that gets the coverage is the one announcing a 100-aircraft order at an air show, jets rolling off the line, photographs of a new tail painted in an airline's livery. But anyone who has studied the great industrial franchises knows that the deliveries are often the loss leader, and the real money — the durable, high-margin, recession-resistant money — is made afterward, over the decades that the machine remains in service. Think of the razor and the blades, the printer and the ink. In aerospace, the blades are spare parts, maintenance, repairs, overhauls, training, and technical support. And for Embraer, this is the crown jewel of the margin profile.

The Services & Support division generated roughly US$1.93 billion in 2025, about a quarter of total revenue and growing 18% year over year.1 But the revenue is not the point. The point is the margin. While the Commercial Aviation business runs at a single-digit EBIT margin — in the neighborhood of 8 to 9%, the structurally thin economics of manufacturing airframes — Services & Support runs at roughly double that, consistently in the mid-teens, around 16% to 17% at the EBIT line.1 Every dollar of services revenue is worth far more to the bottom line than a dollar of aircraft sales. And it comes with a quality that aircraft sales conspicuously lack: predictability.

The mechanism is simple and powerful. Embraer has put a very large fleet into the sky over the past two decades — well over 2,000 E-Jets in commercial service worldwide, plus thousands of executive jets and a growing fleet of military aircraft. Every one of those airplanes is a multi-decade annuity. It needs parts. It needs scheduled maintenance. Its pilots need recurrent simulator training. Its operators need around-the-clock technical support to keep it flying. The larger the installed base grows, the larger and more predictable the services stream becomes — and crucially, much of this revenue is decoupled from the brutal cyclicality of new-aircraft orders. Airlines stop buying new jets in a downturn, but they still have to maintain the ones they own. The services business is the ballast that steadies the whole ship.

To strengthen this engine, Embraer made one of its most strategically elegant acquisitions: OGMA — Indústria Aeronáutica de Portugal. OGMA is a venerable Portuguese aircraft maintenance and manufacturing company, and Embraer took a controlling stake in partnership with the Portuguese state, which retained an interest.[^12] The logic was multi-layered. First, it gave Embraer a maintenance, repair, and overhaul hub physically located inside the European Union and inside NATO — a strategically valuable footprint as Embraer's defense ambitions grew. Second, Embraer paid a conservative price relative to the lofty multiples that aerospace MRO assets commanded globally, consistent with the company's disciplined approach to capital. And third, and most impressively, Embraer transformed the facility. OGMA became an authorized maintenance center for the Pratt & Whitney geared turbofan engines — the same GTF engines that power the A220, the A320neo, and Embraer's own E2 jets — and that engine-MRO work, riding the enormous installed base of GTF-powered narrowbodies, helped roughly triple the facility's turnover.[^13] A sleepy state-owned maintenance shop became a high-value node in the global engine-overhaul network.

This recurring, high-margin, counter-cyclical cash flow is the unglamorous foundation beneath everything else Embraer does. It is what dampens the violent swings of the aircraft-order cycle. It is what generates the predictable free cash flow that funds the next development program in Commercial and the next campaign in Defense. And it is a major reason the rating agencies grew comfortable enough to do something they had not done in years: restore Embraer to investment grade. Across 2024, S&P, Fitch, and Moody's each lifted Embraer back to investment-grade status — S&P in February, Fitch in late September, and Moody's completing the trio in December 2024 — citing the recovery in deliveries, the growing backlog, and the debt reduction driven by strong free cash flow.9 An investment-grade rating is not a vanity badge; it directly lowers the cost of capital for one of the most capital-intensive businesses on earth. The services machine, in other words, helps pay for cheaper money. And cheaper money helps fund the boldest product gamble in the company's recent history — an airplane built to dethrone a legend.

VIII. The Global Defense Shift: KC-390 Millennium Taking on the C-130

For sixty years, if a nation needed a tactical military transport — an airplane to haul troops, vehicles, and cargo into rough fields, drop paratroopers, refuel other aircraft, and fly humanitarian relief into disaster zones — it bought one airplane. The Lockheed Martin C-130 Hercules, a four-engine turboprop that first flew in the 1950s, is one of the most successful military aircraft ever built, in continuous production for longer than almost any aircraft in history, sold to dozens of air forces. It is the default. The Hercules is to military airlift what the AK-47 is to rifles: ubiquitous, rugged, and seemingly impossible to displace.

Embraer decided to displace it anyway. The C-390 Millennium — originally designated the KC-390, the "KC" denoting its aerial-refueling capability — represents the company's audacious bid to take a meaningful share of the global tactical-airlift market. And the central design decision tells you everything about Embraer's contrarian engineering instinct. Where the Hercules and its competitors use turboprops — propeller engines chosen for their fuel efficiency and short-field grit — Embraer built a jet, powering the C-390 with two high-bypass turbofan engines, the same broad family of efficient jet engines that power modern airliners.

Why does that matter? Because a jet flies faster and higher than a turboprop. The C-390 cruises faster, which means it covers more distance in less time — getting troops or relief supplies to a crisis hours sooner, and completing more missions per day. It carries a larger payload than a C-130. And, counterintuitively for a jet, Embraer engineered it for lower lifecycle costs — the all-in cost of owning and operating the aircraft over its service life — by leveraging commercial-derived systems and modern reliability engineering. Faster, bigger, cheaper to own over time: that is a genuinely disruptive value proposition in a procurement category that had grown comfortable and unchallenged.

The strategic story of the C-390 is the story of a program graduating from a domestic project into a global export machine. It began, as these programs do, funded by the home customer — the Brazilian Air Force, which needed to replace its own aging fleet. The hard part, and the impressive part, was breaking out of Brazil and into the demanding, politically wired world of Western defense procurement, where buyers want NATO-standard interoperability and where incumbent relationships run deep. Through the early 2020s, Embraer did exactly that, stringing together a remarkable run of European order wins. Portugal, the Netherlands, Austria, the Czech Republic, Hungary, and Sweden all selected the C-390, with several of these nations — NATO members replacing their own Hercules fleets — choosing the Brazilian jet over the incumbent.[^15] That is the Defense & Security segment, which generated roughly US$984 million in 2025, about 13% of revenue but growing the fastest of any business unit, up 36% year over year on the strength of these contract wins.1

The significance for the investment case is twofold. First, defense contracts are long-dated and sticky; a nation that buys a fleet of C-390s is committing to decades of associated training, parts, and support — feeding directly back into that high-margin services business we just discussed. Second, every European NATO order is a reference sale that de-risks the next campaign, building the kind of credibility that turns a challenger into an established alternative. In a world where European defense budgets are expanding sharply, Embraer has positioned a genuinely competitive product at exactly the right moment. And the company's appetite for taking on entrenched incumbents does not stop at military transports. It extends, improbably, to reinventing the very idea of urban flight.

IX. Hidden Optionality: Eve Air Mobility and eVTOL

Every great industrial company eventually faces the question of what comes after its current S-curve, and Embraer's answer carries a futuristic name: Eve Air Mobility, the company's electric-aircraft venture, which it spun out and took public on the New York Stock Exchange under the ticker EVEX via a SPAC merger in 2022.10 Eve is developing an eVTOL — an electric vertical-takeoff-and-landing aircraft, the technology popularly imagined as the "flying taxi," a quiet, electric machine that lifts off like a helicopter and cruises like a small plane, ferrying a handful of passengers across congested cities.

A word of discipline is in order here, because eVTOL is the most over-hyped corner of aerospace, and Eve must be sized appropriately. This is not a core business driver. It generates negligible revenue today, it is deeply capital-consumptive, and the entire eVTOL category faces enormous unresolved questions around certification, battery energy density, air-traffic integration, and whether the unit economics of urban air taxis will ever actually work. Eve is a speculative, future-material play. It deserves a paragraph in this story, not a chapter — and we are giving it exactly that.

But it is not nothing, and the reason it matters is the reason it is more than a moonshot. Eve is not a garage startup; it is the child of an aircraft manufacturer that has been designing and, critically, certifying aircraft for over half a century. The single hardest thing in aviation is not having a clever idea — it is shepherding a flying machine through the brutal certification gauntlet of a regulator like the FAA or Brazil's ANAC, and then manufacturing it reliably at scale and supporting it in the field. That is precisely the muscle Embraer has spent fifty years building. Against pure-play eVTOL startups like Joby Aviation and Archer Aviation — well-funded and capable, but lacking a parent with deep certification scars, a global manufacturing base, and a worldwide MRO and support footprint — Eve enjoys a real structural advantage. It can lean on the institutional knowledge of a company that knows how to turn a prototype into a certified, supportable product.

That is the right way to hold Eve in the investment case: not as a number in the model, but as genuine technological optionality — a cheap call option on urban air mobility, written on top of a real aerospace company. If the category works, Embraer is positioned to win it without having bet the company. If it does not, the downside is contained. Optionality, properly understood, is exactly that asymmetry. And managing a portfolio of bets like this — a regional cash cow, a private-jet grower, a defense disruptor, a services annuity, and a moonshot — requires a particular kind of operator at the top. So let us meet the man running the company, and examine how he is paid to do it.

X. The Playbook: Current Management, Compensation, and Operational Moats

Imagine inheriting the chief executive's office of a major aerospace company in May 2019. Within twelve months, the defining deal of the company's strategy — the Boeing merger you were brought in partly to consummate — collapses. A global pandemic grounds the entire airline industry, your customers' single source of cash. Your company sits physically dismembered from the carve-out, bleeding money, with debt to service and a market that has simply stopped buying airplanes. This was the in-tray that greeted Francisco Gomes Neto when he became CEO of Embraer.

Gomes Neto was a notable choice precisely because he was not an aerospace lifer and not a founder. His background was in the broader industrial and automotive world — he had run the bus-and-truck maker Marcopolo, and before that held senior roles in industrial multinationals — and he arrived with the mindset of an operations and manufacturing specialist rather than an aeronautical engineer or a salesman. In hindsight, that was exactly the skill set the moment demanded. Embraer in 2019 did not need a visionary to dream up a new airplane. It needed someone who could ruthlessly take cost out, stabilize a battered supply chain, and squeeze cash out of operations to survive.

That is precisely what he did, under the banner of a strategy called "Fit for Growth." It was a sweeping program of cost reduction, asset optimization, and supply-chain stabilization aimed at making Embraer leaner and more resilient. One of its most important operational components was the Production Leveling Plan — and it is worth explaining in plain terms because it speaks to how the company actually makes money. Aerospace manufacturers have a chronic, self-inflicted disease: they cram deliveries into the final weeks of each quarter to hit quarterly targets, creating a frantic, inefficient "hockey stick" of activity at the end of every period and idle capacity at the start. The Production Leveling Plan smooths that build rate across the quarter — a steadier, more even assembly pace that reduces overtime, lowers the working capital tied up in half-finished aircraft, and cuts the supply-chain whiplash that comes from lumpy demand. It is unglamorous manufacturing discipline of the kind Gomes Neto knew cold from the automotive world, and it materially improved Embraer's cash conversion. The recovery from the depths of 2020 to the record revenues and backlog of 2025 happened on his watch and bears his operational fingerprints.

Now to compensation, which is where the alignment between management and shareholders is either real or merely rhetorical — and Embraer's structure is genuinely worth examining. The company moved deliberately away from traditional stock options. Stock options, for all their popularity, have a dirty secret: when they are exercised, they create new shares, diluting existing shareholders. Embraer terminated its dilutive stock-option plans and replaced them with a Long-Term Incentive plan built on zero-exercise-price phantom shares.

Let us unpack that, because it is elegant. A "phantom share" is not a real share. It is a contractual promise that tracks the economic value of one share — when it vests, the executive is paid in cash equal to the value of the underlying stock, but no new share is ever issued. "Zero-exercise-price" means the executive does not have to pay anything to capture the value; each phantom share is economically equivalent to simply owning a share, settled in cash. The beauty of this design is twofold. It aligns management perfectly with the share price — Gomes Neto and his top team make more when EMBR3.SA on the B3 and ERJ on the NYSE rise, and less when they fall, exactly as a shareholder experiences. But because it settles in cash rather than stock, it does this without diluting the very shareholders it is meant to be aligned with. The executives' incentive moves with the stock; the share count does not.

The vesting is structured in tranches — blocks of phantom shares vesting in successive years, including blocks tied to 2027, 2028, and 2029 — and, critically, payout is not automatic with the passage of time. It is contingent on hitting strict operational targets: adjusted EBIT margins, free cash flow generation, and meeting aircraft-delivery guidance. In other words, management gets paid the full value only if it delivers the specific financial and operational results that create shareholder value in the first place — margins, cash, and the all-important deliveries that drive both. For a long-term fundamental investor, this is close to the textbook ideal of incentive design: aligned with the stock, non-dilutive, and gated on the operating metrics that actually matter. Which brings us to the deeper question every Acquired episode eventually asks — not what the company does, but why it is hard to compete with. Let us run Embraer through the frameworks.

XI. Strategy Breakdown: Porter's Five Forces & Hamilton's Seven Powers

We have been laying the pieces on the board throughout this story. Now let us assemble them into a coherent strategic picture, using the two frameworks Acquired returns to again and again: Hamilton Helmer's Seven Powers, which catalogs the genuine, durable sources of competitive advantage, and Michael Porter's Five Forces, which maps the structural attractiveness of the industry itself.

Start with Helmer's Seven Powers, of which Embraer demonstrably possesses four.

The first and most foundational is the Cornered Resource — the São José dos Campos engineering cluster. We met it in the founding story and it is worth naming precisely as a Power here: a deep, self-renewing pool of elite aeronautical engineers, trained at ITA and the surrounding institutions, available at Brazilian wage scales. This is a structural wage-to-quality arbitrage that Western competitors simply cannot replicate. Boeing cannot relocate Seattle's cost of living to São Paulo, and it cannot conjure seventy years of cluster-building overnight. The quality is world-class; the cost is not. That asymmetry sits underneath every other advantage Embraer has, because it lowers the cost of the most important input in the entire business — engineering hours.

The second is Counter-Positioning — the 2+2, no-middle-seat fuselage. Embraer entered the regional market with a clean-sheet design optimized for passenger comfort precisely when the mainline manufacturers built only 3+3 tubes and the regional incumbents offered cramped, narrow turboprop and small-jet cabins. The mainline giants could not easily follow without redesigning their own airframes and cannibalizing their existing products — the classic counter-positioning trap, where the incumbent's existing business model is the very thing that prevents it from copying the upstart.

The third is Switching Costs — fleet commonality. Once an airline commits to the E-Jet family, the cost of switching to a competitor becomes enormous. Pilots are "type-rated" on a specific aircraft, a certification that costs time and money to earn and to change. Airlines invest in flight simulators, spare-parts inventories, maintenance tooling, and trained mechanics, all specific to the fleet they fly. Switching manufacturers means writing off much of that investment and starting over. This friction secures the lifetime value of every E-Jet customer and makes the next-generation E2 the natural, low-friction upgrade path for an existing E1 operator.

The fourth is Scale Economies — within the regional niche specifically. Embraer is not bigger than Boeing or Airbus in absolute terms; it is far smaller. But scale economies are about a relevant market, and within the regional jet segment Embraer enjoys the largest backlog and the largest installed base, letting it spread the fixed costs of development, tooling, and support over more units than any rival in that category could. Smaller or failed programs — Mitsubishi's SpaceJet being the cautionary tale — never reached the volume to amortize those fixed costs, and drowned.

Now Porter's Five Forces, where two forces dominate the analysis.

The barriers to entry are extreme — arguably as high as in any industry on earth. The cautionary monument here is Mitsubishi's SpaceJet: roughly fifteen years and well over US$10 billion, spent by one of the most capable industrial conglomerates in the world, all to discover that money alone cannot buy the institutional capability to certify a clean-sheet aircraft and manufacture it at scale.5 Certification expertise is tacit, accumulated, and deeply experiential — you learn it by doing it, repeatedly, over decades. That is the moat that protects all incumbents in this industry, Embraer included, and it is precisely why COMAC's progress, though real, has been slow and confined largely to its protected home market.

The bargaining power of buyers is moderate-to-high but asymmetric by segment. Airlines are consolidated, sophisticated, and ferociously price-sensitive — in a normal market, that gives them real leverage over manufacturers. But in the U.S. regional segment, the scope clauses we examined invert the usual dynamic. When labor contracts structurally restrict carriers to aircraft of a certain size, and Embraer is the last manufacturer building a compliant, modern jet, the buyer's choice narrows dramatically. That hands Embraer unusual pricing power in its most important market — a regulatory-and-structural quirk doing the work that scale normally does.

The remaining forces round out the picture. Supplier power is real and currently painful — a small number of jet-engine makers, notably Pratt & Whitney, and specialized component suppliers hold genuine leverage, a vulnerability we will see surface in the bear case. The threat of substitutes is low for the core mission of moving people between cities by air; high-speed rail competes at the margins in some geographies but does not threaten the regional-jet franchise broadly. And competitive rivalry, while intense against the deep pockets of Airbus's A220, is muted by the simple fact that so few players can field a product at all. Put it together and you have an industry that is murderously hard to enter, with a company that has carved out structural advantages within it. The question for an investor is whether those advantages translate into a compelling forward case — and where the cracks might be.

XII. The Investment Case: Bull vs. Bear and Key KPIs

Every investment is an argument between two stories about the future. Let us steelman both, then narrow to the handful of numbers that will actually tell you which story is winning.

The bull case begins with an industry condition that has nothing to do with Embraer's own actions: the Boeing-Airbus duopoly is supply-constrained, and will be for years. Both giants have backlogs stretching into the next decade; an airline that wants narrowbody jets in the near term often simply cannot get a delivery slot. That scarcity pushes airlines to look at alternatives they might once have ignored — and Embraer's E2 family, marketed as a crossover narrowbody, is a viable, available option for carriers that need lift now and want best-in-class fuel efficiency per seat. The duopoly's bottleneck is Embraer's opening.

The bull case strengthens across the rest of the portfolio. Defense, led by the C-390, is winning the kind of NATO contracts that were unthinkable a decade ago, and European defense budgets are expanding, not contracting. Services & Support compounds at double-digit rates with high, recurring, counter-cyclical margins — the ballast that funds everything else. And the return to investment grade across all three agencies in 2024 structurally lowered the cost of capital for a business where the cost of capital is destiny.9 Record 2025 revenue and a record US$31.6 billion backlog are the evidence that the recovery is not a forecast but a fact already on the books.1 The bull's summary: a company firing on all four cylinders, with an industry tailwind it did not have to create.

The bear case is equally coherent, and a serious investor must hold it with equal conviction. The sharpest near-term risk lives inside the airplanes themselves: the Pratt & Whitney geared turbofan engines that power the E2 family have suffered industry-wide reliability and durability problems — including a fleet-wide inspection campaign affecting GTF engines across multiple aircraft types — that have grounded aircraft and frustrated airline customers across the platforms these engines power. Embraer does not build the engines, but its customers do not care whose fault it is; grounded jets sour the relationship and can chill orders. This is the supplier-power vulnerability from Porter's framework made concrete.

The second bear thread is competition with deep pockets. Airbus can subsidize the A220's pricing from the enormous cash flows of its A320 juggernaut and squeeze suppliers with scale Embraer cannot match. In a head-to-head campaign, Embraer can be out-marketed and out-financed even when its airplane is more efficient. The third thread is the supply chain itself: bottlenecks in microelectronics, castings, and forged titanium have constrained the entire industry's ability to ramp production, and Embraer's record backlog is only as valuable as its ability to actually build and deliver the aircraft in it. A backlog you cannot convert to deliveries is a promise, not a profit. And lurking beneath all of it is the irreducible cyclicality of aviation and the eVTOL cash drain at Eve, which will consume capital for years before it returns anything — if it ever does.

So how does a fundamental investor cut through the noise and actually monitor which way this is breaking? Watch three numbers, and only three.

The first is the firm order backlog in US dollars. This is the single best leading indicator of future revenue health, the visible runway of demand the company has already booked. It closed 2025 at a record US$31.6 billion; the direction and durability of that figure quarter to quarter tells you whether the demand story is intact.1

The second is the book-to-bill ratio — the ratio of new orders booked to aircraft delivered (billed) in a period. It must stay above 1.0x for the backlog to grow rather than shrink. Above 1.0x, the company is selling faster than it is delivering and the franchise is expanding; below 1.0x, it is living off its backlog and the future is quietly contracting. It is the cleanest single read on whether demand is keeping pace with production.

The third is the Services & Support EBIT margin. This is the health of the high-margin cash engine that funds everything else — the development of the next aircraft, the next defense campaign, the de-leveraging of the balance sheet. If that margin holds in the mid-teens as the installed base grows, the whole flywheel keeps turning; if it erodes, the company loses the counter-cyclical ballast that makes the rest of the strategy affordable.1 Track those three, and you are tracking the actual machine, not the headlines.

XIII. Epilogue & Key Lessons

Step back from the order books and the engine recalls and the arbitration filings, and the Embraer story resolves into a handful of lessons that outlast any single quarter.

The first is the power of academic-industrial clusters, and it is the one most relevant to any nation or company wondering how to build a hard-technology capability from scratch. Brazil did not begin with a factory. It began with a school — the ITA — and let the talent compound for two decades before it ever expected an airplane. The factory was downstream of the classroom. Seventy years later, that decision still pays dividends every single day, in the form of an engineering cost structure that the wealthiest aerospace companies on earth cannot match. The lesson for the builder is counterintuitive and durable: do not build the factory first. Build the institution that produces the people, and the rest follows.

The second lesson is about surviving the corporate divorce. Embraer was, in the most literal sense, abandoned at the altar — its commercial business carved out, separated, and prepared for a marriage to Boeing that was called off at the worst possible moment, in the worst market in living memory, with the company holding a US$120-million-plus bill and a fractured organization.7 It would have been entirely understandable for the company to spiral. Instead it reintegrated, restructured, fought for and won a settlement, and emerged independent and investment-grade. The lesson is not that the deal's collapse was good — it was genuinely devastating. The lesson is that operational resilience, the unglamorous capacity to absorb a catastrophic blow and keep building, is itself a form of competitive advantage, and one that does not show up on any spec sheet.

The third lesson is about geography, and it is perhaps the most quietly radical. The conventional wisdom held that frontier aerospace was the exclusive preserve of the rich, established industrial powers of the global North — that high-technology manufacturing of this difficulty simply could not be done competitively from the developing world. Embraer broke that assumption, not by being cheaper in the crude sense, but by being smarter about where its costs sat and bolder about its industrial design. It took the most expensive input in the business — elite engineering talent — and sourced it at a structural discount without sacrificing quality. It looked at a market the giants treated as an afterthought and built something better. A company from São José dos Campos, in the interior of Brazil, became the third force in an industry everyone assumed could only ever hold two — and it did so by leveraging exactly the advantages its critics had dismissed as handicaps.

The Southern Cross is the constellation that hangs over the Southern Hemisphere, the one that points the way for navigators below the equator and that adorns the Brazilian flag. It is a fitting emblem for a company that found its own direction by looking at the sky differently from everyone in the North. Whether Embraer's next chapter is written in crossover narrowbodies, NATO transports, or electric air taxis, the navigational logic that brought it this far — cornered talent, contrarian engineering, and the stubborn refusal to die — is the thing worth keeping an eye on.

References

-

Embraer Earnings Results — 4th Quarter and Fiscal Year 2025; see also Brazil's Embraer 2025: Record $7.6B Revenue, $31.6B Backlog — Rio Times, 2026 and Embraer reports record revenues and backlog for 2025 — TravelDailyNews, 2026 ↩↩↩↩↩↩↩↩↩

-

Embraer's Secret Weapon is its Elite Engineering Pipeline — Financial Times, 2024-05-04 ↩

-

Embraer's Secret Weapon is its Elite Engineering Pipeline — Financial Times, 2024-05-04 ↩

-

How Embraer Survived the Boeing Breakup and Built a Better Airplane — Bloomberg, 2023-06-15 ↩

-

Why the Mitsubishi SpaceJet Regional Jet Program Failed — FlightGlobal, 2023-02-07 ↩↩

-

Embraer Executive Jets Phenom 300 Milestone Deliveries — Corporate Jet Investor, 2024-02-22 ↩

-

How Embraer Survived the Boeing Breakup and Built a Better Airplane — Bloomberg, 2023-06-15 ↩↩

-

Boeing to pay Embraer $150 million over failed commercial jet deal — Reuters, 2024-09-16 ↩

-

Embraer is full Investment Grade by the 3rd main rating agency — Embraer, 2024-12; see also Embraer raised to investment grade by S&P Global Ratings — Embraer, 2024-02 ↩↩

-

Eve Air Mobility SEC Registration and SPAC Merger Prospectus — Eve Air Mobility, 2022-05-10 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube