Elevance Health: The Blueprint for America's Health Insurance Giant

I. Introduction & Episode Roadmap

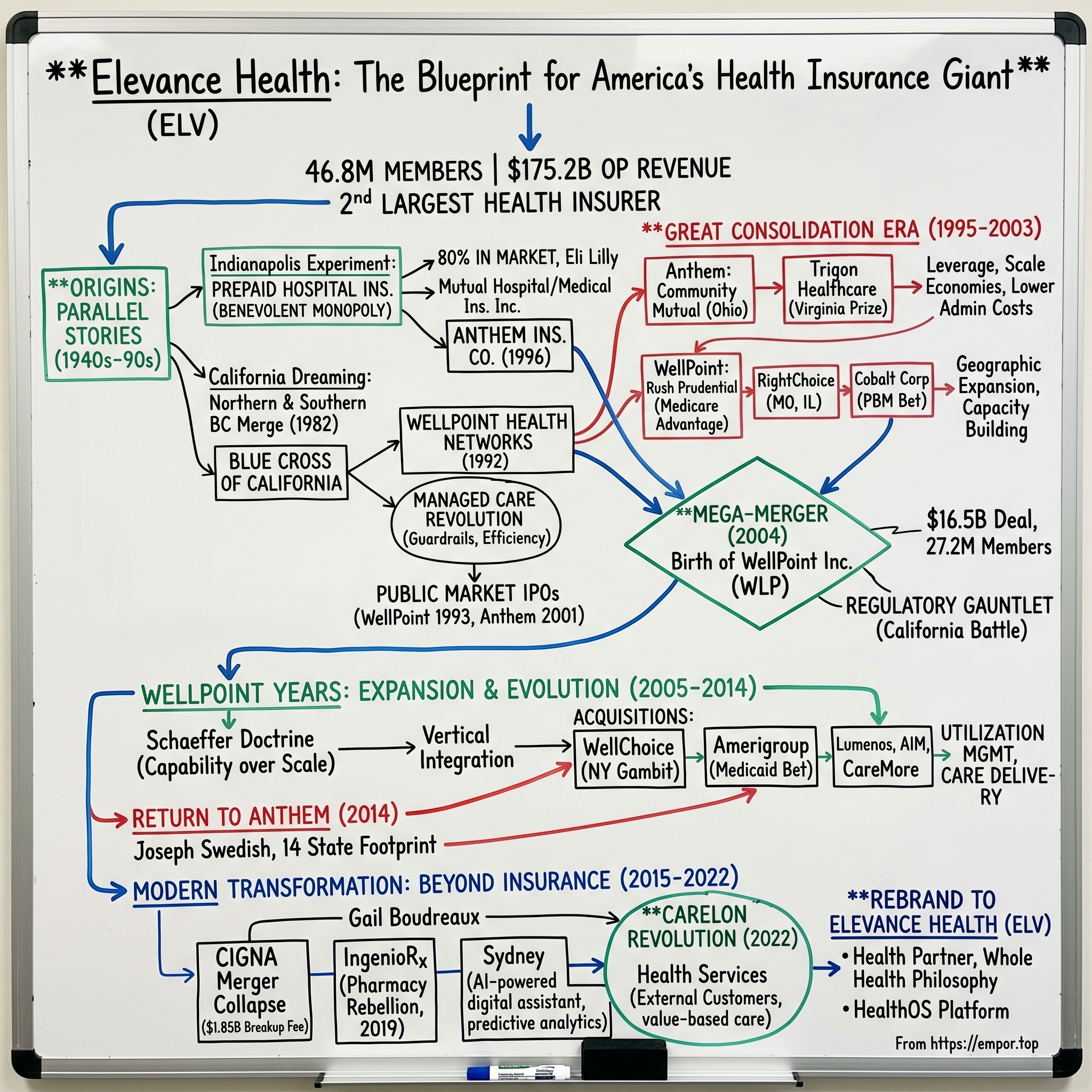

Picture this: It's 2024, and somewhere in America right now, 46.8 million people—roughly one in seven Americans—are carrying a health insurance card with some variation of the Elevance Health name on it. The company processes $175.2 billion in operating revenue annually, making it the second-largest health insurer in the United States. Yet most Americans have never heard the name "Elevance Health."

That's because until June 2022, this insurance behemoth operated under a different name: Anthem. And before that? WellPoint. And before that? A constellation of regional Blue Cross Blue Shield affiliates scattered across the American heartland, each with its own origin story stretching back to the Great Depression.

How did a collection of nonprofit hospital insurance cooperatives, founded to help Americans afford medical care during the 1930s and 1940s, transform into one of the most powerful for-profit corporations in American healthcare? How did regional insurers serving Indiana factory workers and California fruit pickers merge, acquire, and consolidate their way to controlling the health benefits of nearly 50 million Americans?

The answer involves one of the most aggressive consolidation plays in American corporate history, a strategic chess match with regulators across multiple states, and a fundamental reimagining of what a health insurance company can be. It's a story of network effects at massive scale, of turning administrative efficiency into competitive advantage, and of navigating the treacherous waters where capitalism meets healthcare.

This is also a story about transformation—from traditional insurance to integrated health services, from regional operators to national powerhouse, from passive payer to active participant in care delivery. Today's Elevance Health isn't just processing claims; it's running its own pharmacy benefit manager, operating behavioral health clinics, managing provider networks, and increasingly betting that the future of health insurance looks nothing like its past.

We'll trace this journey from those Depression-era mutual aid societies through the managed care revolution of the 1990s, the consolidation frenzy of the 2000s, the Affordable Care Act upheaval, and into today's world of vertical integration and value-based care. Along the way, we'll unpack the economics of health insurance, examine the strategic rationale behind dozens of acquisitions, and explore what happens when you try to build a healthcare giant in America's uniquely complex and politically charged system.

So buckle up. This is the story of how Elevance Health became the blueprint for America's modern health insurance industry—and why its next chapter might look radically different from everything that came before.

II. The Origins: Two Parallel Stories (1940s–1990s)

The Indianapolis Experiment

In 1946, post-war Indianapolis was booming. Factories hummed with peacetime production, veterans returned home to start families, and employers scrambled to attract workers in a tight labor market. Into this environment stepped two entrepreneurs with a radical idea: What if employers could offer prepaid hospital insurance as a benefit to their workers?

Mutual Hospital Insurance Inc. and its sister company Mutual Medical Insurance Inc. weren't the first to try this model—Blue Cross plans had been sprouting across America since the 1930s. But the Indianapolis entities had something special: aggressive local marketing, tight relationships with major employers like Eli Lilly and the Indiana Farm Bureau, and a willingness to innovate on plan design. By the 1970s, these twin companies controlled an astounding 80% of Indiana's medical insurance market.

The dominance was so complete that when federal investigators looked into the Indiana health insurance market in the late 1960s, they found what amounted to a benevolent monopoly. Mutual Hospital and Mutual Medical had achieved the network effects that would later define the entire industry: more members meant better negotiating power with hospitals, which meant lower premiums, which attracted more members. It was a virtuous cycle that competitors couldn't break.

California Dreaming

Three thousand miles west, a different story was unfolding. Blue Cross of California had emerged from two separate entities—one serving Northern California (established 1937) and another serving Southern California (established 1936). These organizations had grown up serving agricultural workers in the Central Valley, defense contractors in Los Angeles, and the emerging tech industry in Silicon Valley.

The California market was different from Indiana—more diverse, more competitive, more regulated. By 1982, facing pressure from commercial insurers and struggling with inefficiencies from their bifurcated structure, the Northern and Southern California Blue Cross entities merged into a single Blue Cross of California. This consolidation was defensive, a response to market pressures rather than a growth strategy.

But the real innovation came a decade later. In 1992, Blue Cross of California's leadership made a decision that would reshape American healthcare: they created WellPoint Health Networks as a for-profit subsidiary focused entirely on managed care. This wasn't just a new product line—it was a fundamental rethinking of the insurance model.

The Managed Care Revolution

To understand why WellPoint was revolutionary, you need to understand what health insurance looked like before managed care. Traditional indemnity insurance was simple: you got sick, you saw any doctor you wanted, the insurance company paid most of the bill. There was no network, no prior authorization, no primary care gatekeeper. It was freedom—and it was unsustainably expensive.

By the late 1980s, healthcare costs were spiraling out of control. Employers who had happily offered generous health benefits in the 1960s and 1970s were watching their healthcare expenses grow faster than their revenues. Something had to give.

Enter managed care. The concept was elegantly simple: instead of paying for whatever care providers decided to deliver, insurers would actively manage that care. Primary care physicians would coordinate treatment. Specialists would require referrals. Networks would be limited to efficient providers. Prior authorization would prevent unnecessary procedures. It was healthcare with guardrails.

WellPoint embraced this model with unprecedented sophistication. They didn't just build networks; they analyzed provider efficiency down to the procedure level. They didn't just require referrals; they created algorithms to predict which patients would need specialty care. They turned health insurance from a passive payment mechanism into an active management system.

The Public Market Beckons

In 1993, Blue Cross of California made another pivotal decision: they spun off WellPoint Health Networks as an independent, publicly traded company. The IPO raised $494 million and valued WellPoint at $1.9 billion. For the first time, a Blue Cross affiliate had gone fully commercial, answering to shareholders rather than members.

The reaction from the nonprofit Blue Cross Blue Shield Association was swift and negative. This violated everything the Blues stood for—community service, nonprofit status, putting members before profits. But California didn't care. WellPoint's leadership saw that the future of healthcare required massive capital investments in technology, data analytics, and network development. The public markets could provide that capital in ways that nonprofit status never could.

Meanwhile, back in Indiana, a parallel transformation was occurring. The Associated Group, which had emerged from those original Mutual companies, was watching WellPoint's success with interest. In 1996, they rebranded as Anthem Insurance Company, signaling their ambition to become more than a regional player. And in 2001, they followed WellPoint's lead, launching their own IPO that raised $2.2 billion.

By the turn of the millennium, two former Blue Cross affiliates—one from California, one from Indiana—had transformed themselves into publicly traded, for-profit managed care companies. They were about to embark on one of the most aggressive consolidation campaigns in American corporate history. The stage was set for the creation of a healthcare giant.

III. The Great Consolidation Era (1995–2003)

The Ohio Gambit

Larry Glasscock had only been CEO of Anthem for three months when he made his first big move. In late 1995, he announced Anthem would acquire Community Mutual Insurance and its 1.9 million Ohio policyholders for $85.5 million. The Ohio insurance commissioner called it "predatory." Consumer advocates warned about monopoly power. But Glasscock saw something others didn't: the future of health insurance would be won by scale.

"We're not buying customers," Glasscock told his board. "We're buying leverage." Every additional million members meant better rates from pharmaceutical companies, stronger negotiating positions with hospital systems, and lower per-member administrative costs. In an industry where margins were measured in single digits, these efficiencies were the difference between thriving and dying.

The Community Mutual acquisition was a masterclass in integration. Anthem didn't just absorb the company; they rebuilt it. They standardized claims processing systems, consolidated provider contracts, and eliminated duplicate administrative functions. Within 18 months, they had reduced Community Mutual's administrative expense ratio from 18% to 12%. That 6% improvement, multiplied across nearly 2 million members, translated to over $200 million in annual savings.

The Virginia Prize

But Ohio was just the appetizer. In 2002, Anthem set its sights on Trigon Healthcare, Virginia's dominant Blue Cross Blue Shield licensee with 2.2 million members. The $4.04 billion price tag was astronomical—nearly double Anthem's own market capitalization at the time. Wall Street analysts called it "insanely aggressive." The Virginia attorney general threatened to block it.

The political battle was fierce. Virginia's governor opposed the deal. Consumer groups held rallies. Local newspapers ran editorials warning about out-of-state corporate raiders. Anthem's response was surgical: they committed $175 million to Virginia community health programs, guaranteed no Virginia job losses for three years, and promised to maintain Trigon's Richmond headquarters as a major operations center.

The real genius of the Trigon deal wasn't just the 2.2 million members—it was the Blue Cross Blue Shield license for Virginia. These licenses were like broadcast spectrum in the 1990s: finite, valuable, and impossible to replicate. Once Anthem owned Virginia's license, no competitor could use the Blue Cross Blue Shield brand in the state. It was a permanent competitive moat.

WellPoint's Western Empire

While Anthem was consolidating the Midwest and Southeast, WellPoint was building its own empire in the West. Their 2001 acquisition of Rush Prudential Health Plans for $204 million seemed modest, but it gave WellPoint something invaluable: a foothold in the rapidly growing Medicare Advantage market. Rush Prudential had cracked the code on serving seniors profitably, with sophisticated risk adjustment models and efficient care management programs.

The 2002 acquisition of RightChoice for $1.5 billion was different—this was about geographic expansion. RightChoice brought 2.4 million members across Missouri and Illinois, along with the Blue Cross Blue Shield licenses for both states. WellPoint CEO Leonard Schaeffer called it "the missing piece of our Midwest strategy."

But the most intriguing WellPoint acquisition of this period was barely noticed: In 2003, they bought Cobalt Corporation, a small Wisconsin-based company that specialized in pharmacy benefit management. The purchase price was just $240 million, but Cobalt represented WellPoint's first serious move into the pharmacy supply chain. It was a bet that controlling drug costs would become central to health insurance profitability—a bet that would pay off spectacularly in the decades to come.

The Network Effect Accelerates

By 2003, both Anthem and WellPoint had discovered the same fundamental truth: in health insurance, scale compounds. Every acquisition made the next one more valuable. More members meant better provider rates, which meant more competitive premiums, which made future acquisitions easier to win. It was a flywheel that, once spinning, was almost impossible to stop.

Consider the mathematics: When Anthem acquired Community Mutual's 1.9 million members, they negotiated a 7% reduction in hospital rates across Ohio. When they later acquired Trigon's 2.2 million Virginia members, their combined 11.9 million member base allowed them to renegotiate pharmaceutical contracts nationally, achieving 12% better pricing than either company had achieved alone. These savings dropped straight to the bottom line.

The administrative efficiencies were equally powerful. Anthem's cost per member for claims processing dropped from $38 in 1995 to $19 by 2003. Multiply that $19 savings by 11.9 million members, and you're talking about $226 million in annual cost advantages versus subscale competitors.

The Inevitable Conclusion

By late 2003, the logic was inescapable. Anthem controlled 11.9 million members across the Midwest and Southeast. WellPoint had 15.3 million members concentrated in California and the West. Both had Blue Cross Blue Shield licenses in key states. Both had achieved massive scale efficiencies. Both were bumping up against the limits of what they could acquire without triggering antitrust concerns.

There was only one move left that made sense: merge with each other. The rumors started in September 2003, with whispers from investment bankers about "Project Titan." By October, the whispers had become roars. The two giants of health insurance consolidation were about to become one. The era of regional health insurers was ending, and the age of the national healthcare behemoth was about to begin.

IV. The Mega-Merger: Creating WellPoint Inc. (2004)

The Secret Summit

On a crisp October morning in 2003, Leonard Schaeffer landed his private jet at a small airport outside Chicago. The WellPoint CEO had told his executive team he was visiting his daughter. Larry Glasscock, Anthem's chief, had told his board he was attending a industry conference. In reality, they were both headed to the same place: a nondescript Marriott conference room where the future of American healthcare would be decided.

The two men had been circling each other for years. They'd competed for acquisitions, poached each other's executives, and publicly dismissed merger speculation. But privately, both understood the inevitable logic. Schaeffer opened with characteristic bluntness: "Larry, we can keep fighting for scraps, or we can own the whole damn table."

The numbers were staggering. Combined, they would have 27.2 million members—larger than the population of Texas. Annual revenues would exceed $45 billion. They would hold Blue Cross Blue Shield licenses in 14 states. The merged entity would be the largest health insurer in America.

The $16.5 Billion Handshake

On October 27, 2003, the companies announced the deal: Anthem would acquire WellPoint for $16.5 billion. The structure was elegant—WellPoint shareholders would receive $23.80 in cash plus one share of Anthem stock for each WellPoint share. It was the largest merger in health insurance history.

Wall Street's reaction was volcanic. Anthem's stock jumped 8% in minutes. WellPoint soared 15%. Healthcare stocks across the board surged on speculation about defensive consolidation. Investment bankers started updating their league tables—the fees on this deal alone would exceed $200 million.

But the real action was in corporate boardrooms across America. UnitedHealth's CEO called an emergency meeting. Aetna's board convened via conference call. Every health insurer in America suddenly faced an existential question: How do you compete with a behemoth that has 27 million members?

The Regulatory Gauntlet

If the executives thought announcing the deal was hard, getting it approved was Herculean. The merger required approval from insurance commissioners in 14 states, the Department of Justice, the Federal Trade Commission, and various state attorneys general. Each regulator had their own concerns, their own politics, their own demands.

California was the biggest battle. Insurance Commissioner John Garamendi opposed the deal outright, calling it "a disaster for California consumers." The California Medical Association warned about "unprecedented market concentration." Consumer advocates organized protests outside WellPoint's headquarters.

Anthem and WellPoint's response was a textbook in regulatory management. They hired 47 different lobbying firms. They commissioned economic studies showing consumer benefits. Most importantly, they made concessions—big ones.

The California commitments alone were extraordinary: $100 million for health programs in underserved communities, $50 million for community clinics, $15 million for nursing education, and a guarantee to maintain 21,000 California jobs for at least three years. They agreed to caps on administrative expenses and mandatory investments in health IT systems.

The Integration Marathon

Even as regulators deliberated, integration planning proceeded in secret. Two companies with completely different cultures, systems, and approaches had to become one. Anthem was hierarchical, Midwestern, conservative. WellPoint was entrepreneurial, Californian, aggressive. The cultural clash was immediate and intense.

The technology integration alone was a nightmare. Anthem ran on mainframe systems dating to the 1980s. WellPoint had invested heavily in modern distributed systems. They had different claims processing platforms, different provider databases, different member portals. The integration team identified 847 different IT systems that needed to be consolidated or connected.

The human integration was equally complex. Who would run which divisions? Whose strategy would prevail? Which headquarters would dominate? The companies created 47 integration teams, each focused on a specific functional area. They held 2,000 integration meetings in six months. The consulting fees alone exceeded $75 million.

November 30, 2004: Birth of a Giant

After 13 months of regulatory review, political maneuvering, and integration planning, the deal closed on November 30, 2004. In a symbolic gesture, the combined company took the WellPoint name but kept Anthem's Indianapolis headquarters. Leonard Schaeffer became chairman, Larry Glasscock became CEO. The stock would trade under the symbol WLP.

The first day of combined operations was choreographed like a military operation. At 6 AM Eastern, 79,000 employees across 14 states logged into their computers to find new email addresses, new organizational charts, and a video message from Glasscock: "Today, we stop being two companies trying to become one. Today, we are WellPoint."

The Immediate Aftermath

The synergies came faster than anyone expected. Within six months, WellPoint had renegotiated pharmaceutical contracts that saved $340 million annually—double the original projections. Administrative costs per member dropped 15% in the first year. The stock price rose 32% in the first six months post-merger.

But there were casualties. Despite promises about job security, 4,800 positions were eliminated in the first year—mostly middle management and duplicate administrative roles. Dozens of senior executives from both companies departed, unable to find their place in the new hierarchy. The California Medical Association filed three separate lawsuits challenging various aspects of the merger.

The deeper challenge was strategic. WellPoint was now too big to grow through major acquisitions—antitrust concerns would block anything significant. They needed a new playbook, one focused on capabilities rather than scale, on vertical integration rather than horizontal expansion. The age of consolidation was ending. The age of transformation was about to begin.

V. The WellPoint Years: Expansion & Evolution (2005–2014)

The Schaeffer Doctrine

Leonard Schaeffer's final strategic planning session as CEO took place in March 2006, three months before his retirement. Standing before WellPoint's top 100 executives in a Phoenix resort, he laid out what would become known as the "Schaeffer Doctrine": "We've won the scale game. Now we need to win the capability game."

The doctrine was simple but revolutionary for a health insurer: WellPoint wouldn't just pay for healthcare; it would actively shape how healthcare was delivered. This meant acquiring companies that did things, not just companies that had members. It was a fundamental shift from horizontal to vertical integration.

The first major move under this strategy was the $185 million acquisition of Lumenos in 2005. Lumenos wasn't an insurer—it was a consumer-directed health plan administrator, specializing in health savings accounts and high-deductible plans. The price seemed high for a company with just 60,000 members, but Schaeffer saw something others missed: Lumenos had built technology that let consumers shop for healthcare like they shopped for anything else, with price transparency and quality ratings.

The Empire State Gambit

Angela Braly had been CEO for barely six months when she made her biggest bet. In December 2005, WellPoint announced it would acquire WellChoice—parent of Empire Blue Cross Blue Shield of New York—for $6.5 billion. Wall Street was stunned. New York was the most regulated, most expensive, most complex health insurance market in America. It was where health insurance companies went to die.

But Braly saw opportunity in the chaos. New York's individual market was imploding, with only 30,000 people buying coverage directly. Small businesses were dropping coverage at record rates. The state was desperate for a solution. WellPoint had the scale to negotiate with New York's powerful hospital systems and the operational expertise to navigate its Byzantine regulations.

The WellChoice integration was a case study in surgical precision. WellPoint identified $195 million in annual synergies before the deal closed. They achieved $230 million within 18 months. They consolidated 14 different IT systems into three. They renegotiated every major provider contract in the state, achieving average rate reductions of 8%.

More importantly, New York made WellPoint truly national. They now had Blue Cross Blue Shield licenses from California to New York, covering 14 states with 34 million members. No other insurer had comparable geographic reach with the Blue brand.

Building the Care Management Machine

The acquisition spree of 2007-2009 looked random to outsiders but followed a precise logic. American Imaging Management ($292 million) brought capabilities in radiology benefit management. Resolution Health ($300 million) added chronic disease management programs. DeCare Dental ($435 million) provided dental benefit expertise.

Each acquisition added a specific capability that WellPoint could deploy across its entire membership base. American Imaging's prior authorization programs, initially covering 2 million lives, were rolled out to 25 million WellPoint members within two years, saving $450 million annually in unnecessary imaging costs.

The 2012 acquisition of CareMore for $800 million was particularly strategic. CareMore operated 26 care centers for Medicare Advantage members, providing everything from primary care to urgent care to chronic disease management. It was WellPoint's first serious move into actually delivering care rather than just paying for it.

The Medicaid Bet

The biggest acquisition of the Braly era was also the most controversial. In July 2012, WellPoint announced it would buy Amerigroup for $4.9 billion. Amerigroup was a pure-play Medicaid managed care company with 2.7 million members across 13 states.

The timing seemed insane. The Supreme Court had just upheld the Affordable Care Act but made Medicaid expansion optional for states. Nobody knew how many states would expand, when they would expand, or what the economics would look like. WellPoint was betting billions on political decisions that hadn't been made yet.

But Braly and her team had done the math. Even if only half the states expanded Medicaid, it would add 10-15 million newly insured Americans. These would be younger, healthier members on average—exactly the kind of members insurers wanted. And Medicaid managed care was growing regardless of expansion, as cash-strapped states sought to control costs.

The Amerigroup deal also brought something invaluable: expertise in serving low-income populations. This wasn't just about processing claims differently; it was about understanding that a Medicaid member might not have reliable transportation to doctor appointments, might not have a stable address for mail, might need help navigating social services as well as healthcare.

The Return to Anthem

By 2014, WellPoint faced an identity crisis. The company operated under dozens of different brand names: Anthem Blue Cross Blue Shield in 14 states, Empire in New York, UniCare, Amerigroup, CareMore. Employees didn't know what company they worked for. Customers were confused. The stock ticker "WLP" meant nothing to anyone.

New CEO Joseph Swedish, who had taken over in 2013, made a bold decision: rebrand everything as Anthem. It was a return to the company's roots, but also a recognition that in healthcare, brand trust matters. The Blue Cross Blue Shield brand consistently ranked as the most trusted in health insurance. Why hide it behind a corporate name nobody recognized?

The rebrand cost $87 million but Swedish considered it a bargain. Internal surveys showed employee engagement increased 12 percentage points after the change. Brand recognition scores jumped 30%. The stock responded too—rising 15% in the six months after the rebrand announcement.

Navigating the ACA Storm

The October 2013 launch of Healthcare.gov was a disaster. The federal exchange website crashed repeatedly. Enrollment was a fraction of projections. Media coverage was relentlessly negative. Every health insurer in America was scrambling to figure out how to operate in this new world.

But WellPoint—now Anthem—was uniquely positioned. They operated in 14 of the 36 states using the federal exchange. They had the scale to absorb the adverse selection that everyone knew was coming. Most importantly, they had built the operational capabilities through a decade of acquisitions to actually manage the care of millions of new members.

The first year was brutal. The members who signed up were sicker than expected. Medical loss ratios spiked above 90%. Anthem lost $175 million on exchange business in 2014. But Swedish didn't panic. He knew this was a long game. As he told investors: "The first people to buy fire insurance are the ones whose houses are already on fire. But eventually, everyone needs coverage."

By the end of 2014, Anthem had transformed from a traditional health insurer into something more complex: a health benefits company with care delivery capabilities, technology platforms, and the scale to shape American healthcare. The foundation was set for an even more dramatic transformation in the years to come.

VI. The Modern Transformation: Beyond Insurance (2015–2022)

The $54 Billion That Got Away

Joseph Swedish was pacing in Anthem's Indianapolis boardroom on July 23, 2015, when he made the call that would define his legacy. On the line was David Cordani, CEO of Cigna. Swedish's offer was simple and staggering: $54 billion for Cigna, creating a health insurance colossus with 53 million members and $115 billion in annual revenues.

The strategic logic was impeccable. Cigna brought international operations, a sophisticated pharmacy benefit management operation, and deep relationships with large employers. Combined with Anthem's Blue Cross Blue Shield licenses and Medicaid footprint, it would create an unassailable competitive position.

But the deal was doomed from the start. Cordani wanted to be CEO of the combined company; Swedish refused to step aside. Cigna's board wanted more cash; Anthem insisted on stock. The Delaware Court of Chancery would later call it "one of the most dysfunctional corporate courtships in modern business history."

The Department of Justice delivered the death blow in July 2016, suing to block the merger on antitrust grounds. The government's case was devastating: the combined company would control over 50% of the national employer market and face no meaningful competition in dozens of local markets. Federal judge Amy Berman Jackson agreed, writing that the merger would cause "irreparable harm to competition."

The collapse wasn't just expensive—Anthem paid Cigna a $1.85 billion breakup fee—it was strategically catastrophic. While Anthem spent two years fighting regulators and Cigna in court, UnitedHealth quietly built its Optum division into a $100 billion revenue juggernaut. CVS acquired Aetna for $69 billion. The industry transformed while Anthem stood still.

The Pharmacy Rebellion

Swedish's next move was born of necessity but executed with precision. In 2019, Anthem announced it would not renew its pharmacy benefit management contract with Express Scripts, instead launching its own PBM called IngenioRx. It was a declaration of independence that shocked the industry.

Express Scripts had managed pharmacy benefits for Anthem's 40 million members, generating over $20 billion in annual drug spending. Walking away from that partnership meant building pharmacy networks from scratch, negotiating with drug manufacturers directly, and convincing members to switch pharmacies—all while ensuring no disruption in medication access.

The execution was flawless. Anthem partnered with CVS Health for pharmacy network access, ensuring members could fill prescriptions at 68,000 locations nationwide. They poached dozens of Express Scripts' top executives, acquiring instant expertise. Most audaciously, they guaranteed clients $4 billion in savings over four years—a promise that essentially forced them to succeed.

By 2021, IngenioRx was managing $22 billion in annual drug spending and generating $500 million in annual profits. But the real value wasn't the profits—it was the control. Anthem could now see real-time prescription data, intervene when members weren't taking medications, and coordinate pharmacy with medical benefits. It was the kind of integration that Swedish had pursued with Cigna, achieved through building rather than buying.

The Carelon Revolution

Gail Boudreaux took over as CEO in November 2017 with a radical vision: transform Anthem from a health insurer into a "health partner." The vehicle for this transformation would be Carelon, a collection of healthcare services businesses that Boudreaux would build into Anthem's second growth engine.

The name Carelon was unveiled in March 2022, consolidating what had been a confusing array of subsidiary brands. But this was more than a rebranding exercise. Carelon represented Anthem's bet that the future of healthcare wasn't in risk-bearing insurance but in actually delivering and managing care.

Carelon's portfolio was impressive: behavioral health services covering 95 million Americans, care management programs for complex conditions, post-acute care coordination, payment integrity services that identified billions in improper payments, and even palliative care programs. By 2022, Carelon was generating $35 billion in revenues, with 40% coming from external customers—competing health plans that needed Anthem's capabilities.

The strategic beauty of Carelon was its dual nature. Internally, it gave Anthem capabilities that improved medical management and reduced costs. Externally, it was a high-margin services business selling to competitors. It was having your cake and eating it too—using your scale to build capabilities, then monetizing those capabilities across the entire industry.

The Digital Transformation

While building Carelon, Boudreaux was quietly orchestrating another transformation: turning Anthem into a technology company that happened to sell health insurance. The centerpiece was Sydney, an AI-powered digital assistant that could answer member questions, find doctors, explain benefits, and even predict health issues before they became critical.

Sydney wasn't just a chatbot. It was connected to Anthem's clinical data, claims history, and pharmacy records. It could notice that a diabetic member hadn't refilled insulin and proactively reach out. It could identify members at risk for hospital readmission and trigger care management interventions. By 2022, Sydney was handling 35 million interactions annually, with customer satisfaction scores higher than human call centers.

The deeper digital transformation was in clinical operations. Anthem built predictive models that could identify high-risk pregnancies weeks before complications arose. They created algorithms that detected fraud in real-time, saving hundreds of millions annually. They developed provider scorecards that measured quality and efficiency at the individual physician level.

The Rebrand to Elevance

On June 28, 2022, Anthem ceased to exist. In its place stood Elevance Health, a name that meant nothing to anyone but signaled everything about Boudreaux's ambitions. The company would still use Anthem Blue Cross Blue Shield for health plans, but the corporate entity would be something bigger.

The rebrand cost $127 million and generated widespread mockery. "Elevance" sounded like a pharmaceutical drug or a consulting firm. The stock ticker changed from ANTM to ELV, breaking decades of brand equity. Critics called it corporate vanity.

But Boudreaux had solid strategic reasoning. Carelon was increasingly selling to Anthem's competitors, who were uncomfortable buying from a company that competed with them in insurance markets. International expansion opportunities were limited by the Anthem brand's association with American health insurance. Most importantly, Elevance signaled that this wasn't just a health insurer anymore—it was a health solutions company that happened to have an insurance arm.

The market eventually agreed. By the end of 2022, Elevance was trading at 15 times earnings, a premium to pure-play insurers like Centene or Humana. The transformation from regional insurer to national healthcare platform was complete. The question now was what to do with all that power.

VII. The Business Model: How Elevance Makes Money

The Four-Headed Hydra

To understand how Elevance generates $175 billion in annual revenue, imagine a four-headed hydra where each head feeds the others. The first head, Health Benefits, is the traditional insurance business—collecting premiums, paying claims, and hoping the former exceeds the latter. This division serves 46.8 million members across Commercial, Medicare, and Medicaid markets, generating roughly $150 billion in annual revenues.

The second head, CarelonRx (formerly IngenioRx), manages pharmacy benefits. This isn't just about negotiating drug prices; it's about formulary management, rebate administration, specialty pharmacy services, and mail-order fulfillment. CarelonRx touches $24 billion in annual drug spending, capturing margins at every step of the pharmaceutical supply chain.

The third head, Carelon Services, is the capabilities platform—behavioral health, utilization management, care coordination, payment integrity, and provider services. This division generates $35 billion in revenues, with 40% coming from external customers. It's the fastest-growing segment, with operating margins approaching 8%, double the company average.

The fourth head, Corporate & Other, includes the Medicaid management business in certain states, life and disability insurance, and various investment operations. It's the smallest segment but includes some of Elevance's most profitable niches.

The Premium Pyramid

The commercial business—employer-sponsored insurance—remains Elevance's profit engine. Large employers pay average annual premiums of $7,600 per employee for single coverage and $21,700 for family coverage. Elevance keeps roughly 15% for administrative costs and profit, with the rest paid out in medical claims.

The economics are beautiful at scale. Once you've built the provider network, added incremental members costs almost nothing. The same contracts, same systems, same call centers serve 100,000 members as easily as 90,000. This operating leverage means that every additional commercial member drops roughly $1,140 in gross profit to the bottom line.

Medicare Advantage is the growth story. Elevance receives approximately $12,000 per member per year from the federal government to provide Medicare benefits. The key is risk adjustment—sicker members generate higher payments. Elevance has become exceptionally sophisticated at documenting member health conditions, ensuring they're paid appropriately for the risk they're assuming. Stars ratings add another layer: five-star plans receive 5% bonus payments, worth hundreds of millions annually.

Medicaid is the volume play. Payments average just $4,500 per member annually, with medical loss ratios often exceeding 90%. But Medicaid members are sticky—they rarely switch plans—and the administrative costs are lower because benefits are standardized. It's a low-margin, high-volume business that generates steady cash flow.

The Pharmacy Profit Machine

CarelonRx's business model is deceptively complex. Start with formulary management: Elevance decides which drugs are covered and at what tier. Pharmaceutical companies pay billions in rebates to secure favorable placement. CarelonRx keeps a portion of these rebates—typically 10-20%—as profit.

Specialty pharmacy is where the real money lies. These drugs for complex conditions like cancer or rheumatoid arthritis can cost $10,000+ per month. CarelonRx buys them at wholesale prices, dispenses them through its own specialty pharmacies, and captures the entire margin between wholesale and retail—often 15-20%.

Mail-order pharmacy adds another profit stream. By requiring 90-day supplies for maintenance medications, CarelonRx reduces dispensing costs and captures higher margins than retail pharmacies. The mail-order business generates operating margins above 10%, versus 3-4% for traditional retail pharmacy.

The genius is the integration. When CarelonRx identifies a member not taking their diabetes medication, Carelon Services can intervene with care management. When claims data shows a member needs a specialty drug, CarelonRx can steer them to its own specialty pharmacy. Every division feeds the others.

The Services Gold Mine

Carelon Services is Elevance's bet on the future. Behavioral health management alone generates $4 billion in annual revenues, serving 95 million Americans through contracts with competing health plans, employers, and government programs. Operating margins approach 12%—exceptional for healthcare services.

Payment integrity services use AI to identify improper payments, duplicate claims, and fraud. Carelon recovers $3 billion annually for clients, keeping 15-20% as fees. It's essentially free money—using technology to find errors in the $4 trillion Americans spend on healthcare annually.

Utilization management is equally lucrative. Carelon reviews prior authorization requests, ensures medical necessity, and coordinates care across settings. Health plans pay millions for these services because effective utilization management can reduce medical costs by 5-10%.

The Network Effect in Numbers

The magic of Elevance's model is how scale creates competitive advantages. With 46.8 million members, Elevance negotiates hospital rates that average 40% below charged amounts. A competitor with 5 million members might only achieve 25% discounts. That 15 percentage point difference is pure competitive advantage.

Administrative costs tell the same story. Elevance spends roughly $420 per member annually on administration. Smaller plans spend $600 or more. That $180 difference, multiplied by millions of members, creates billions in cost advantages.

Technology investments amplify these advantages. Elevance spends $2 billion annually on technology—impossible for smaller competitors to match. But spread across 47 million members, it's just $43 per member per year. The resulting capabilities—predictive analytics, digital engagement, automated processing—create advantages that compound over time.

The Margin Reality

Despite these advantages, Elevance's net margin is just 4.1%. For every dollar in premiums, 85 cents goes to medical costs, 11 cents to administration, and 4 cents to profit. It's a brutal business where success is measured in basis points.

But at Elevance's scale, basis points matter. A 10 basis point improvement in medical loss ratio—from 85.0% to 84.9%—generates $175 million in additional profit. A 1% reduction in administrative costs adds $300 million to the bottom line. This is why scale matters: tiny improvements in efficiency generate massive absolute returns.

The future is about expanding margins through vertical integration. Every service Elevance provides directly—every prescription filled by CarelonRx, every behavioral health session delivered by Carelon—captures margin that would otherwise go to suppliers. It's a slow transformation from low-margin insurance to higher-margin healthcare services, using the insurance business as the customer acquisition engine.

VIII. Financial Performance & Challenges (2023–2024)

The Numbers Tell a Story

On paper, Elevance's financial trajectory from 2022 to 2024 looks like a triumph of American capitalism. Revenues grew from $156.6 billion to $177.0 billion—a 13% climb that added more than $20 billion to the top line. The company generated $6.8 billion in operating cash flow in 2024. The stock price hit all-time highs. By any traditional measure, Elevance was winning.

But CEO Gail Boudreaux knew better. Speaking to analysts in January 2025, her tone was uncharacteristically defensive: "We are navigating unprecedented challenges in our Medicaid business while simultaneously positioning for sustainable long-term growth." Translation: We're getting killed in Medicaid and hoping Medicare Advantage saves us.

The benefit expense ratio—the percentage of premiums paid out in medical claims—told the real story. It had crept up from 87.0% in 2022 to 88.5% in 2024, a 150 basis point deterioration that translated to $2.6 billion in reduced profitability. For a business where success is measured in basis points, this was a crisis.

The Medicaid Meltdown

The Medicaid disaster of 2024 was a perfect storm of regulatory failure, actuarial miscalculation, and political dysfunction. During the COVID-19 pandemic, states had suspended Medicaid eligibility redeterminations, keeping millions enrolled who might otherwise have lost coverage. When redeterminations resumed in 2023, everyone expected the Medicaid rolls to shrink and the remaining population to be healthier.

Everyone was wrong. The members who left Medicaid were the healthiest—those who had gotten jobs with employer coverage or aged into Medicare. The members who remained were sicker, poorer, and more expensive than anyone anticipated. Medical costs in Medicaid spiked 8% year-over-year, while state reimbursement rates increased just 2%.

The timing mismatch was brutal. States set Medicaid rates annually based on historical data. By the time 2024 rates were set in late 2023, the data didn't yet reflect the post-redetermination reality. Elevance was locked into contracts that assumed a healthier population, paying for a sicker one.

California was the worst disaster. Elevance's Medi-Cal business lost $450 million in 2024 as utilization spiked beyond any reasonable projection. Emergency room visits increased 15%. Behavioral health costs exploded 22%. Prescription drug utilization in certain categories jumped 30%. The state's response? "Wait until the 2025 rate cycle."

The Medicare Advantage Bright Spot

While Medicaid burned, Medicare Advantage thrived. Elevance added 750,000 Medicare Advantage members in 2024, growth of 12% that exceeded every projection. The demographics were irresistible: 11,000 Americans turn 65 every day, and increasingly they're choosing Medicare Advantage over traditional Medicare.

The profitability was even better than the growth. Elevance's Medicare Advantage medical loss ratio improved to 84.5%, generating margins above 6%. The secret was clinical integration—using Carelon's capabilities to manage chronic conditions, prevent hospital readmissions, and steer members to efficient providers.

The Stars program added another layer of profitability. Elevance improved its average Star rating to 4.3 out of 5.0 in 2024, with 85% of members in 4-star or higher plans. This triggered hundreds of millions in bonus payments from CMS, pure profit that dropped straight to the bottom line.

Looking forward to 2025, Elevance projected 7-9% Medicare Advantage membership growth, adding another 500,000-600,000 members. With the Medicare-eligible population growing 2.5% annually and Medicare Advantage penetration still below 50%, this growth runway extended for years.

Commercial Resilience

The commercial business—employer-sponsored insurance—proved surprisingly resilient in 2024. Despite predictions of employer coverage erosion, Elevance retained 97% of its national accounts and actually grew membership slightly. The secret was benefit design innovation and cost management that kept premium increases below 5%.

The risk-based commercial business was particularly strong. Large self-insured employers increasingly turned to Elevance not just for administrative services but for stop-loss coverage, care management, and pharmacy benefits. These fee-based services generated stable margins regardless of medical cost trends.

Small group commercial was tougher. Competition from new entrants like Oscar Health and Friday Health Plans pressured margins. But Elevance's Blue Cross Blue Shield brand remained powerful with small employers who valued network breadth and brand recognition over digital bells and whistles.

Capital Allocation Discipline

Faced with Medicaid headwinds, Boudreaux doubled down on capital discipline. The company announced $2.3 billion in share repurchases for 2025, retiring roughly 4% of shares outstanding. The dividend increased 10% to $1.75 per share quarterly, maintaining Elevance's 15-year streak of dividend growth.

But the real capital story was investment in capabilities. Elevance committed $2.5 billion to technology investments in 2025, focused on generative AI for prior authorization, advanced analytics for risk prediction, and digital tools for member engagement. These weren't just efficiency plays—they were survival requirements in an industry where United's Optum and CVS's Aetna were setting new standards for tech-enabled care management.

The acquisition pipeline remained active but selective. Elevance walked away from several potential deals in 2024 when prices exceeded strategic value. As CFO Mark Kaye explained: "In this environment, the best acquisition might be our own shares."

The 2025 Outlook

Elevance's 2025 guidance reflected both optimism and caution. Revenue was projected at $185-188 billion, with adjusted EPS of $37.50-38.50. The embedded assumptions were telling: Medicaid margins would remain pressured through at least mid-year, Medicare Advantage would drive growth, and commercial would stay stable.

The wildcard was pharmacy. CarelonRx was projected to grow revenues 15% in 2025, driven by biosimilar adoption and expansion into specialty pharmacy. But drug pricing reform remained a constant threat. The Inflation Reduction Act's Medicare drug negotiation provisions would begin impacting prices in 2026. Every percentage point reduction in drug prices flowed through to CarelonRx's bottom line.

The deeper question was strategic. Elevance had built massive scale and capabilities, but medical cost inflation was accelerating. The company's ability to manage those costs—through clinical integration, utilization management, and vertical integration—would determine whether 2024's challenges were a blip or the beginning of a structural shift in industry profitability.

IX. Strategic Vision & The Future of Healthcare

"Improving the Health of Humanity"

When Gail Boudreaux unveiled Elevance's new mission statement in 2022—"Improving the health of humanity"—cynics scoffed. How does a for-profit insurance company that denies claims and restricts access improve humanity's health? But Boudreaux's vision was more sophisticated than corporate platitudes. She was betting that Elevance could make money by keeping people healthy rather than just processing claims when they got sick.

The math was compelling. A diabetic who takes their medication costs $4,000 annually. A diabetic who doesn't, ends up in the emergency room, and develops complications costs $40,000. Every prevented heart attack saves $100,000. Every avoided premature birth saves $500,000. If Elevance could crack the code on prevention and intervention, it could simultaneously improve health outcomes and profitability.

This wasn't theoretical. Carelon's chronic disease management programs had already demonstrated 20% reductions in hospital admissions for enrolled members. The behavioral health integration programs showed 30% improvements in depression scores and 25% reductions in total medical costs. The data proved that coordinated, proactive care management worked.

The Whole Health Philosophy

Elevance's "whole health" approach recognized what traditional insurance had long ignored: health is determined more by social factors than medical care. A diabetic who can't afford healthy food won't improve regardless of medication quality. A depressed person without stable housing won't benefit from therapy alone.

The company's social determinant programs were remarkably sophisticated. In Indianapolis, Elevance partnered with food banks to provide healthy meal delivery to diabetic members. In California, they funded transitional housing for homeless members with chronic conditions. In Georgia, they provided transportation vouchers for prenatal appointments.

The ROI was extraordinary. Every dollar spent on food assistance for diabetic members generated $2.50 in medical cost savings. Housing support for homeless members with behavioral health conditions reduced emergency room visits by 70%. Transportation assistance improved medication adherence by 40%.

But scaling these programs was murderously complex. Each required local partnerships, customized interventions, and sophisticated data analytics to identify eligible members. It was easier to just deny claims and manage utilization. The fact that Elevance was investing billions in these programs suggested they saw something others didn't.

HealthOS: The Platform Play

The most ambitious element of Elevance's strategy was HealthOS, a technology platform designed to connect every aspect of healthcare delivery. Think of it as an operating system for healthcare—standardizing data exchange, enabling interoperability, and creating a common foundation for innovation.

HealthOS wasn't just internal technology. Elevance was opening it to partners, providers, even competitors. The vision was to become the AWS of healthcare—the infrastructure layer that everyone else built upon. Provider groups could use HealthOS for population health management. Digital health startups could integrate for patient data. Pharmaceutical companies could leverage it for real-world evidence.

The early results were promising. By 2024, over 200 provider organizations were using HealthOS capabilities, generating $150 million in high-margin platform revenues. But the real value was strategic: every provider using HealthOS became more integrated with Elevance's ecosystem, creating switching costs and competitive moats.

Value-Based Care at Scale

Elevance's push into value-based care arrangements represented a fundamental reimagining of the payer-provider relationship. Instead of fee-for-service contracts that incentivized volume, Elevance was signing deals that paid providers for keeping populations healthy.

By 2024, Elevance had 25% of members in some form of value-based arrangement, ranging from simple quality bonuses to full-risk capitation. The most sophisticated were the "payvider" partnerships, where Elevance and provider systems essentially merged their economics, sharing savings from improved outcomes.

The partnership with Advocate Health in the Carolinas was the exemplar. Elevance and Advocate created a clinically integrated network covering 2 million members, with shared governance, integrated data systems, and aligned incentives. Medical costs for members in this network were 12% lower than traditional arrangements, with quality scores significantly higher.

The Optum Obsession

Every strategic discussion at Elevance eventually came back to Optum. UnitedHealth's services division had grown from nothing to $226 billion in revenues in just 15 years. It employed 115,000 physicians, operated thousands of surgical centers, and generated operating margins double United's insurance business.

Elevance's Carelon was explicitly designed as the "Optum killer," but the gap remained massive. Optum's revenues were six times Carelon's. Optum employed physicians directly; Carelon partnered with them. Optum had spent two decades building capabilities; Carelon had existed for two years.

But Elevance had advantages. The Blue Cross Blue Shield brand carried trust that United lacked. Carelon could sell to Blue plans nationwide, a market Optum couldn't access. Most importantly, Elevance's state-level market density allowed for deeper provider partnerships than United's more dispersed footprint.

The Amazon/Google/Apple Question

The tech giants' healthcare ambitions loomed over every strategic discussion. Amazon's acquisition of One Medical, Google's health data initiatives, and Apple's health tracking ecosystem suggested that Big Tech saw opportunity in healthcare's $4 trillion of inefficiency.

Elevance's response was nuanced. Rather than viewing tech companies as existential threats, they saw them as potential partners or acquisition targets. Elevance had what tech companies lacked: regulatory expertise, provider relationships, and risk-bearing capabilities. Tech companies had what Elevance needed: consumer engagement, data analytics, and digital innovation.

The partnership with Amazon Pharmacy was instructive. Rather than competing with Amazon's pharmacy ambitions, CarelonRx integrated with them, allowing members to fill prescriptions through Amazon while Elevance managed the benefits. It was cooperation rather than competition, leveraging each company's strengths.

The Tension at the Heart

The fundamental tension in Elevance's strategy was between its mission and its margins. Every intervention that improved health—preventive care, social services, care coordination—cost money upfront with uncertain payback. Wall Street wanted predictable earnings growth; improving humanity's health required long-term investment with volatile returns.

Boudreaux's solution was portfolio balance. The commercial business generated steady profits that funded innovation. Medicare Advantage provided growth. Carelon created optionality. The combination allowed Elevance to invest in transformation while delivering quarterly earnings.

But the deeper question remained: Could a for-profit company truly optimize for health outcomes when those outcomes sometimes conflicted with profitability? Or would market forces ultimately push Elevance toward the same utilization management and claim denial practices that made health insurers so universally despised? The next decade would provide the answer.

X. Playbook: Business & Investing Lessons

The Consolidation Masterclass

If you want to understand how to consolidate a fragmented industry, study Elevance's 1995-2004 playbook. The pattern was elegant: start with small, financially distressed targets to prove integration capabilities. Use the cost savings to fund larger acquisitions. Leverage increased scale for better terms on the next deal. Rinse and repeat until you're too big for anyone to compete with.

The genius was in the sequencing. Anthem didn't go straight for the giants—they built credibility with the $85 million Community Mutual deal, proved they could integrate successfully, then leveraged that track record for the $4 billion Trigon acquisition. Each deal made the next one easier to finance, easier to integrate, and easier to justify to regulators.

The Blue Cross Blue Shield licenses were the strategic masterstroke. These weren't just brands; they were exclusive territorial franchises. Once Anthem owned Virginia's Blue license, no competitor could use the Blue brand in that state—ever. It was like buying broadcast spectrum in the 1990s or domain names in the early internet. The scarcity value was permanent.

For modern entrepreneurs, the lesson is clear: in fragmented industries, whoever consolidates first often wins permanently. The operational synergies create cost advantages. The scale creates negotiating leverage. The market power creates pricing discipline. But you have to move fast—once consolidation starts, windows close quickly.

Network Effects in Unlikely Places

Healthcare insurance seems like the last place you'd find network effects, but Elevance proved otherwise. Every additional member made their provider networks more valuable to hospitals. Every additional hospital made their networks more valuable to members. Every additional percentage point of market share made their data more valuable for population health management.

The network effects were particularly powerful in local markets. In Indiana, where Elevance has 45% market share, hospitals essentially have to accept their rates. Employers have to offer their plans. This density creates a virtuous cycle: market power leads to better rates, which leads to competitive premiums, which leads to more members, which increases market power.

The modern application extends beyond insurance. Any business that sits between fragmented suppliers and fragmented customers can create similar dynamics. The key is reaching critical mass in defined geographic or vertical markets before trying to expand everywhere.

Vertical Integration as Defense and Offense

Elevance's move into pharmacy benefit management and healthcare services wasn't just about growth—it was about survival. When your biggest supplier (healthcare providers) and your biggest cost center (pharmacy) are consolidating and gaining pricing power, you have two choices: accept margin compression or vertically integrate.

The creation of IngenioRx was defensive—protecting against Express Scripts' margin extraction. But it became offensive once Elevance realized they could serve other health plans. The same pattern repeated with Carelon: built to manage Elevance's medical costs, then sold to competitors as a high-margin service.

The lesson for other industries: vertical integration works when you can achieve minimum efficient scale internally and then sell excess capacity externally. But it fails when you're subscale or when the capability isn't core to your business model. Elevance could justify building a PBM because they had 40 million members. A 2-million-member plan couldn't.

Regulatory Complexity as Moat

Healthcare is regulated at federal, state, and local levels, with different rules for different products in different markets. Most see this as a burden. Elevance turned it into a competitive advantage. Their regulatory affairs team of 500+ professionals could navigate approval processes that would bankrupt smaller competitors.

Consider Medicare Advantage: succeeding requires mastering CMS regulations, achieving Star ratings, managing risk adjustment, and coordinating with dozens of state Medicaid programs. The regulatory knowledge required is so complex that new entrants typically fail or achieve subeconomic returns for years.

The investing insight: in highly regulated industries, look for companies that have turned compliance into a core competency. They often trade at discounts due to regulatory "overhangs" but actually have more durable competitive positions than companies in unregulated markets.

Capital Allocation in Mature Industries

Elevance faces the classic mature industry dilemma: organic growth is limited, acquisitions face antitrust scrutiny, but cash generation is massive. Their capital allocation strategy is instructive: buy back shares when valuations are reasonable, pay growing dividends for income investors, and make selective capability acquisitions that won't trigger regulatory concern.

The $2.3 billion in planned 2025 buybacks seems boring but is brilliant financial engineering. At 12x earnings, each dollar of buyback is accretive to EPS. The 4% annual share count reduction means existing shareholders own more of the company each year without additional investment.

The discipline to walk away from overpriced acquisitions is equally important. Healthcare services companies were trading at 20x+ EBITDA in 2024. Elevance refused to overpay, instead building capabilities organically or buying their own undervalued shares. As Buffett says: "Price is what you pay, value is what you get."

Brand Value in Commoditized Markets

Health insurance is essentially commoditized—everyone covers the same services under the same regulations. Yet Blue Cross Blue Shield consistently commands 3-5% premium pricing over competitors. Why? Brand trust in healthcare is literally life and death. When choosing health insurance, consumers overwhelmingly prefer known brands.

Elevance's return to the Anthem brand in 2014 and retention of Blue Cross Blue Shield for health plans showed sophisticated brand portfolio management. Use the trusted consumer brand where it matters (health plans), but create a separate corporate brand (Elevance) for B2B services where trust comes from capabilities, not consumer recognition.

The Platform Business Hidden in Plain Sight

Most investors see Elevance as a health insurer, but Carelon is really a platform business. It provides services to 115 million Americans, including 68 million who aren't Elevance insurance members. The capital-light, high-margin, subscription-like revenue model looks more like software than insurance.

Platform businesses are valuable because they exhibit economies of scale, network effects, and switching costs. Carelon has all three: spreading development costs across more customers, creating data network effects, and embedding deeply into customer operations. The 40% of revenues from external customers validates that these capabilities have value beyond internal use.

The lesson: look for traditional companies building platform businesses within their four walls. They often trade at traditional multiples while building assets that deserve technology valuations. The market eventually recognizes this value, but patient investors can buy transformation at mature company prices.

XI. Analysis & Bear vs. Bull Case

The Bull Case: Scale Wins in the End

The optimistic view of Elevance starts with an indisputable fact: American healthcare is broken, and someone has to fix it. Healthcare costs are approaching 20% of GDP. Chronic disease rates are exploding. The population is aging rapidly. These aren't problems that get solved by startups or disrupted by apps. They require massive scale, deep expertise, and regulatory know-how—exactly what Elevance has spent 80 years building.

Start with demographics. The Medicare-eligible population is growing 2.5% annually and will for the next two decades as Baby Boomers age. Medicare Advantage penetration is still below 50%, providing years of runway for growth. Elevance's 7-9% annual MA membership growth could continue for a decade, adding 5-7 million high-margin members.

The Medicaid challenges of 2024 are temporary. States will eventually adjust rates to reflect actual acuity. They have no choice—if Medicaid managed care plans fail, states have to manage these populations directly, which they're neither equipped nor willing to do. The $450 million California lost in 2024 will be recouped through rate adjustments in 2025-2026.

Carelon is the hidden gem. Growing at 15% annually with expanding margins, it could be worth $50-75 billion as a standalone company. The comparison to Optum is instructive but incomplete—Carelon doesn't need to own providers to capture value. By remaining asset-light and partnership-focused, Carelon can achieve Optum-like margins without Optum-like capital intensity.

The vertical integration strategy is working. IngenioRx is generating $500 million in annual profits while saving members billions in drug costs. The clinical integration programs are reducing medical costs by 10-15% for engaged populations. Every percentage point improvement in medical loss ratio drops $1.7 billion to the bottom line.

Trading at just 12x forward earnings versus 16x for UnitedHealth, Elevance is priced for problems, not potential. If they execute on Medicare Advantage growth, stabilize Medicaid margins, and scale Carelon to $50 billion in revenues, the stock could double from current levels.

The Bear Case: Structural Headwinds Accelerating

The pessimistic view sees Elevance as a melting ice cube in a warming world. The fundamental business model—taking a percentage of healthcare spending—only works if healthcare spending grows faster than medical costs. That spread is compressing and may invert.

Start with competition. UnitedHealth's Optum is six times Carelon's size and growing faster. CVS Health owns the largest pharmacy chain, giving them consumer touchpoints Elevance lacks. Amazon is entering healthcare with unlimited capital and no legacy constraints. Even Walmart is building health clinics. Elevance is fighting on multiple fronts with structural disadvantages.

The regulatory environment is increasingly hostile. The Inflation Reduction Act's drug pricing provisions will compress pharmacy margins. Proposed regulations on prior authorization and claim denials will increase medical costs. Medicare Advantage rate updates consistently fall below medical trend. The political consensus—rare bipartisan agreement—is that health insurers make too much money.

The Medicaid disaster of 2024 might not be temporary. States are broke, facing massive budget deficits as federal COVID funding ends. They can't afford actuarially sound Medicaid rates. The choice between raising taxes or underpaying managed care plans is politically obvious. Elevance could face years of Medicaid margin pressure.

Technology disruption is accelerating. Telemedicine companies like Teladoc provide primary care at 80% lower cost than traditional visits. Digital therapeutics replace expensive medications. AI-powered diagnosis could eliminate specialist referrals. Every technological improvement that makes healthcare more efficient reduces the pool of money Elevance can take a percentage of.

The social license to operate is eroding. Public opinion of health insurers is at all-time lows. The assassination of UnitedHealth's CEO in December 2024 led to widespread social media celebration. Political candidates from both parties run against health insurers. This social hostility eventually manifests as regulatory restriction, taxation, or disruption.

United vs. Elevance: The Heavyweight Battle

Comparing Elevance to UnitedHealth is inevitable but reveals uncomfortable truths. United is simply bigger, better, and more diversified. With $371 billion in revenues versus Elevance's $177 billion, United has scale advantages in every dimension. Their medical loss ratios are 50 basis points better. Their operating margins are 200 basis points higher.

Optum is the real differentiator. While Elevance talks about Carelon, Optum generates $226 billion in revenues, employs 90,000 physicians, and operates the largest health services platform in America. Optum's operating margins of 7.5% are double United's insurance margins. It's a better business model, and United got there first.

But Elevance has unique advantages. The Blue Cross Blue Shield brand remains more trusted than United. Elevance's state-level density allows deeper provider partnerships. Their Medicaid expertise positions them for potential single-payer scenarios. If healthcare becomes a regulated utility, regional density might matter more than national scale.

The Disruption Scenarios

Three disruption scenarios keep Elevance executives awake at night. First is government single-payer. If Medicare for All ever passes, private insurers become administrators, not risk-bearers. Margins would compress from 4% to 1-2%. The stock would fall 70%.

Second is technology platform disruption. If Amazon, Google, or Apple figure out how to aggregate consumer demand and bypass traditional insurance, Elevance becomes a regulated utility processing claims for tech platforms. They'd survive but never grow.

Third is provider integration. If large hospital systems like Kaiser Permanente or Intermountain Healthcare can replicate their integrated models nationally, they cut out the insurance middleman entirely. Elevance would be left with the worst risks that integrated systems don't want.

The Probabilistic View

Weighing the scenarios, Elevance faces a 60% probability of muddling through—growing slowly, managing margins carefully, returning cash to shareholders. There's a 25% chance of upside surprise if Carelon becomes a true Optum competitor and Medicare Advantage growth exceeds expectations. There's a 15% chance of disruption that permanently impairs the business model.

At 12x earnings with a 1.5% dividend yield, the risk-reward is balanced but uninspiring. Elevance is neither cheap enough to be a value play nor growing fast enough to be a growth story. It's a mature company in a challenging industry with excellent execution but limited optionality.

For investors, Elevance represents a bet on American healthcare dysfunction continuing indefinitely—profitable but ethically uncomfortable. The company will likely compound at high single digits with occasional volatility from regulatory changes. Whether that's adequate return for the regulatory, political, and disruption risks is the $200 billion question.

XII. Epilogue & "If We Were CEOs"

The View from the Corner Office

Imagine walking into Elevance's Indianapolis headquarters tomorrow as the new CEO. You inherit 47 million members, $177 billion in revenues, and one of the most complex businesses in America. You also inherit the accumulated hatred of millions of Americans who blame you for their medical bankruptcies, denied claims, and unaffordable premiums. What do you do?

The first priority would be radical transparency. The health insurance industry operates in deliberate opacity—nobody understands how claims are adjudicated, how prices are set, or where the money goes. Publish it all. Show that 85 cents of every premium dollar goes to medical care. Reveal that hospital systems, not insurers, are driving cost inflation. Make prior authorization criteria public and algorithmic. Transparency wouldn't solve everything, but it would shift the conversation from conspiracy theories to facts.

The second move would be aggressive provider partnership restructuring. The current adversarial relationship between insurers and providers is destructive for everyone. Create true risk-sharing partnerships where Elevance and health systems win or lose together. Start with the 20 largest health systems, offering them 50/50 splits on any savings achieved through care coordination. Make providers true partners, not vendors.

The third initiative would be a massive simplification of benefits. The current system where every employer has a different plan design with different copays, deductibles, and coverage rules is insane. Create three standardized plan designs—Basic, Standard, Premium—and refuse to deviate. The operational savings would be enormous, and members might actually understand their benefits.

The Technology Transformation

The technology strategy would be complete platform unbundling. Instead of building monolithic systems, create modular, API-first services that anyone can use. Make Elevance the AWS of healthcare—the infrastructure layer that powers thousands of health tech startups. Open source the prior authorization engine. License the provider directory. Sell the claims processing platform.

This isn't charity—it's strategy. Every startup using Elevance infrastructure becomes dependent on it. Every competitor licensing Elevance services funds R&D. Every open-sourced component becomes an industry standard that Elevance controls. It's the difference between defending a castle and owning the entire valley.

AI would be deployed aggressively but transparently. Not for denying claims—that's both unethical and counterproductive—but for identifying members who need intervention. Build models that predict which diabetics will have complications, which pregnant women will deliver prematurely, which seniors will fall. Then intervene proactively with services, not restrictions.

The Consumer Revolution

The biggest missed opportunity in health insurance is consumer experience. Members interact with their health insurer at the worst moments of their lives—when they're sick, stressed, and scared. Yet the experience is typically awful: hours on hold, incomprehensible explanations, arbitrary denials.

Create a consumer experience that would make Apple jealous. One-tap prior authorization from a smartphone. Video calls with nurses who actually know your medical history. Proactive outreach when you miss medications. Price transparency before procedures, not surprise bills after. Make health insurance feel like a service, not a tax.

The brand strategy would acknowledge reality: nobody loves their health insurer, but they might respect one that's honest. Launch a campaign called "We Know You Hate Us" that acknowledges the industry's failures while showing concrete steps toward improvement. It would be shocking, controversial, and potentially transformative.

The Political Navigation

Healthcare is becoming increasingly political, and Elevance needs a strategy beyond lobbying for the status quo. Propose a grand bargain: insurers accept rate regulation and standardized benefits in exchange for universal coverage mandates and stable funding. It's better to shape regulation than be subjected to it.

Internationally, explore opportunities in markets where American-style managed care could improve outcomes. Brazil, India, and Indonesia are building modern healthcare systems and need expertise in population health management. Elevance's capabilities could be valuable exports, diversifying beyond the U.S. regulatory minefield.

The Capital Allocation Revolution

The current strategy of buybacks and dividends is safe but uninspiring. Instead, make a massive bet on value-based care by acquiring provider groups—not to run them, but to create demonstration projects. Buy 10 mid-sized physician practices and show that integrated care can reduce costs by 20% while improving outcomes. Use these as laboratories for innovation and blueprints for partnership.

Simultaneously, invest aggressively in preventive care infrastructure. Build or acquire a national network of urgent care clinics focused on keeping people out of hospitals. Create the largest telehealth platform in America. Fund community health workers in underserved areas. These investments might not generate immediate returns, but they position Elevance for a future where healthcare happens outside hospitals.

The Ultimate Question

The fundamental challenge facing any Elevance CEO is philosophical: Can a for-profit company truly optimize for health outcomes when those outcomes sometimes conflict with profitability? The honest answer is probably not completely. But the current system—where insurers profit from denying care—is clearly broken.

The solution might be reconceptualizing the business model entirely. Instead of taking a percentage of healthcare spending, charge flat per-member fees for health maintenance. Instead of managing sickness, manage wellness. Instead of being a payer, become a health partner. It would require restructuring every contract, retaining every employee, and reimagining every process.

It would also require convincing Wall Street that long-term value creation matters more than quarterly earnings. That improving health outcomes is ultimately more profitable than managing decline. That building trust is more valuable than extracting margins.

The Legacy Play

If we were CEO, the ultimate goal would be making Elevance unnecessary. Build systems and incentives that keep people so healthy they rarely need expensive medical care. Create price transparency that eliminates inefficiency. Develop care models that prevent rather than treat disease. Success would mean shrinking the total addressable market—anathema to Wall Street but transformative for society.

This isn't utopian thinking—it's long-term strategy. The current American healthcare system is unsustainable. It will either transform gradually through innovation or suddenly through crisis. By leading transformation, Elevance could control its destiny rather than having change forced upon it.

The legacy wouldn't be building America's largest health insurer—that's already done. It would be building America's last health insurer—the one that made the rest unnecessary. That's a mission worth pursuing, even if it takes decades to achieve.

XIII. Recent News### **

Fourth Quarter 2024: Navigating Unprecedented Headwinds**