Washington REIT to Elme Communities: The Rise, Reinvention, and Final Act of D.C.'s Oldest REIT

I. Introduction & Episode Roadmap

Picture a boardroom in suburban Rockville, Maryland, sometime in 2016. A group of real estate executives is staring at a chart showing D.C.-area office vacancy rates climbing steadily higher, quarter after quarter. Across the table, another slide shows apartment rents in Arlington, Alexandria, and Bethesda doing exactly the opposite—climbing, climbing, climbing. Somewhere in that room, the leadership team of Washington Real Estate Investment Trust, one of the oldest publicly traded REITs in American history, is confronting a question that would define the next decade of corporate life: Do we keep riding the horse that got us here, or do we get on a completely different one?

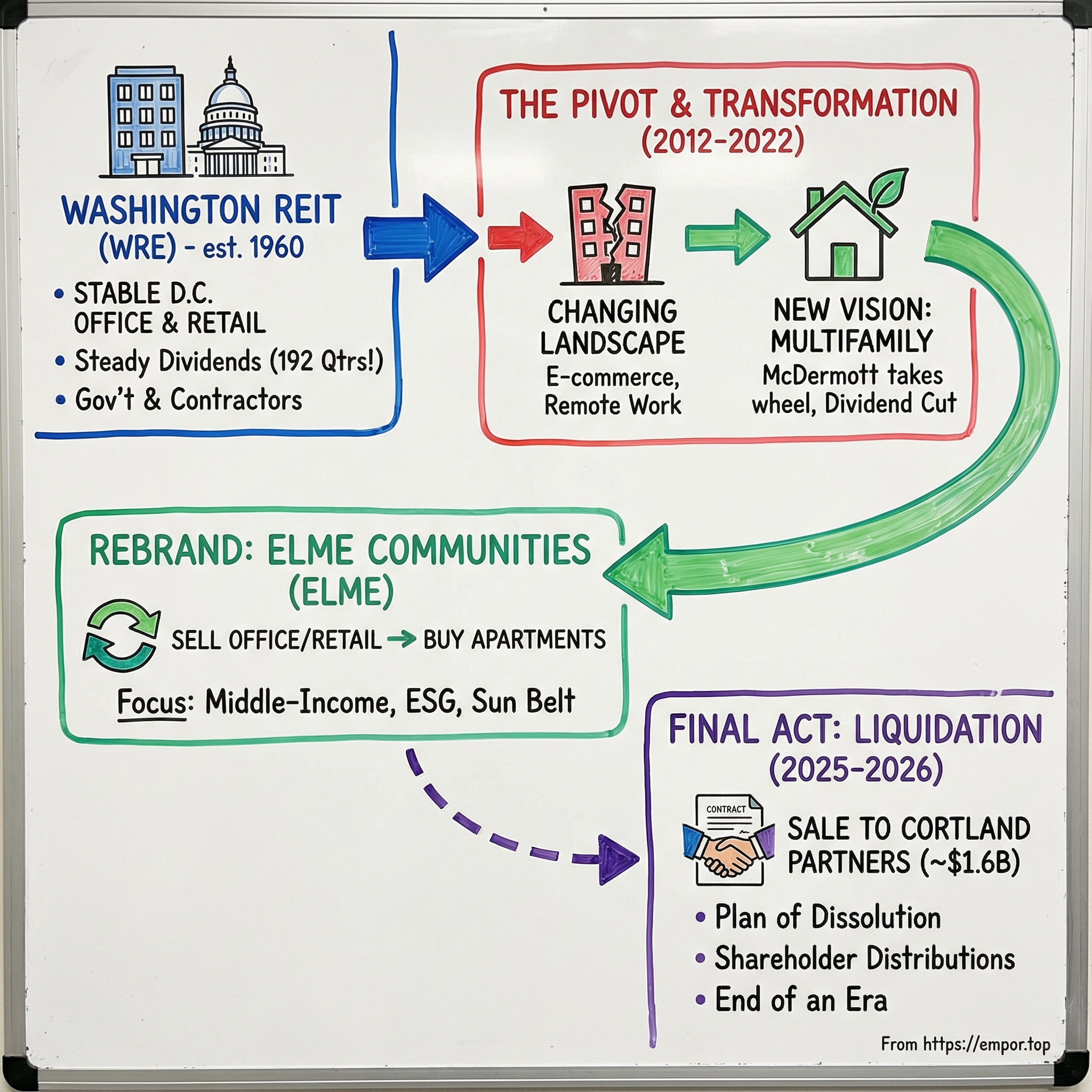

That question—and how it got answered—is the story of Elme Communities, formerly Washington REIT. Founded in 1960, the same year President Eisenhower signed the legislation that created REITs as a vehicle for ordinary Americans to invest in real estate, Washington REIT spent more than half a century as the quintessential boring, predictable, dividend-paying landlord. Its tenants were government contractors, lobbying firms, and federal agencies. Its buildings were the Class B office parks and strip malls that ring the Capital Beltway. Its shareholders were retirees who cashed quarterly dividend checks like clockwork—192 consecutive quarters of equal or increasing payouts at one point, a streak that stretched back to the early 1960s.

Then the world changed. Millennials didn't want to work in suburban office parks. The federal government started tightening budgets. E-commerce hollowed out shopping centers. Remote work went from a perk to a pandemic necessity. And Washington REIT—a company older than most of its competitors—made a bet that would have been unthinkable a decade earlier: it would sell nearly a billion dollars of office and retail properties, rebrand itself entirely, and become a residential apartment company.

This is a masterclass in strategic pivoting, capital allocation under duress, stakeholder management, and the brutal economics of real estate cycles. It is also, as events would reveal, a story with a twist ending that nobody in that Rockville boardroom could have predicted. The transformation succeeded on its own terms—the portfolio was repositioned, the brand was remade, the operations were retooled—and then the market delivered its own verdict. By late 2025, Elme Communities would conclude a strategic review and sell its entire multifamily portfolio to Cortland Partners for approximately $1.6 billion, entering a plan of liquidation and dissolution.

The arc from founding to liquidation covers sixty-five years of American real estate history. Along the way, it teaches lessons about the REIT structure, demographic shifts, the courage required to abandon a legacy business, and the sometimes-painful reality that transformation does not always guarantee survival as an independent company. For investors, it raises a question that applies far beyond one mid-cap REIT: When is the right time to pivot, and can you ever pivot fast enough?

II. The Birth of REITs & Washington REIT's Founding

On September 14, 1960, President Dwight Eisenhower signed the Real Estate Investment Trust Act into law. The concept was elegant and democratic: just as mutual funds allowed small investors to own diversified portfolios of stocks, REITs would allow ordinary Americans to pool capital and invest in income-producing real estate—office buildings, shopping centers, apartment complexes—without needing the millions of dollars required to buy properties outright. In exchange for passing through at least 90% of taxable income to shareholders as dividends, REITs would pay no corporate income tax. It was a grand bargain: the government gave up tax revenue, investors got access, and capital flowed into real estate development.

Washington REIT was among the very first companies to take advantage of this new structure. Founded in 1960, it was organized as a trust by a group of local D.C.-area investors who saw something that seems obvious in retrospect but was genuinely prescient at the time: Washington, D.C. was going to keep growing, and it would need buildings. The federal government was the ultimate anchor tenant—not just the agencies themselves, but the vast ecosystem of contractors, consultants, lobbyists, trade associations, and law firms that orbited the Capitol like moons around a planet. These tenants didn't go bankrupt during recessions. They didn't move to cheaper cities. They signed leases, paid rent, and renewed year after year with the predictability of cherry blossoms in April.

The original portfolio was modest: a handful of suburban office buildings and small shopping centers in Northern Virginia and suburban Maryland, the kind of low-rise, garden-style commercial real estate that was sprouting across the Beltway corridor as the federal workforce expanded. Think brick-and-glass office parks near the Dulles Toll Road, strip malls anchored by a grocery store and a dry cleaner in Silver Spring. Nothing glamorous. But the genius was in the consistency. Government-adjacent tenants meant government-adjacent stability.

To understand why this mattered, consider how the REIT structure actually works in practice. A REIT collects rent from tenants, pays its operating expenses—maintenance, property taxes, insurance, management—and what remains is Net Operating Income, or NOI. Think of NOI as the fundamental heartbeat of a real estate business: it measures how much cash the properties themselves generate before debt service and corporate overhead. From NOI, the company pays interest on its mortgages and loans, covers corporate expenses, and distributes the vast majority of what remains as dividends. Because REITs must distribute at least 90% of taxable income, they cannot hoard cash the way a tech company might. Every dollar of profit is spoken for. This creates an iron discipline: management must either generate enough internal cash flow to maintain and grow the portfolio or tap external capital markets—issuing new shares or taking on new debt—to fund acquisitions and development.

For Washington REIT, the implied social contract was straightforward: own stable buildings in the D.C. metro, collect predictable rents, pay generous dividends, and don't take unnecessary risks. For decades, that contract held. The company went public, began trading on the American Stock Exchange (later moving to the NYSE), and built a reputation as the kind of stock a financial advisor would recommend to a retired federal employee looking for steady income. It was not exciting. It was not supposed to be.

The "Washington advantage" was real and durable—at least for a while. Federal spending grew under every administration, regardless of party. The national security apparatus expanded after every geopolitical crisis. And all of that spending created jobs, which created demand for office space, which created demand for the shopping centers and restaurants that served the office workers. Washington REIT sat at the nexus of this self-reinforcing cycle, collecting rent from tenants whose ultimate funding source was the United States Treasury.

But embedded in that stability was a hidden fragility. When your entire business model depends on one metropolitan area and one dominant economic driver, you're making an enormous concentration bet. It just doesn't feel like a bet when the driver is the federal government. The question was never whether D.C. would keep growing—it was whether the kind of growth would keep favoring the kind of buildings Washington REIT owned.

III. The Glory Years: Riding D.C.'s Suburban Office Boom (1960s–2000s)

Drive the Capital Beltway—Interstate 495—on a weekday morning, and you'll pass through the economic geography that made Washington REIT possible. Starting from the Pentagon in Arlington, sweep north through Tysons Corner, where glass office towers house Booz Allen Hamilton, SAIC, and a constellation of defense contractors. Continue into Bethesda, where the National Institutes of Health anchors a biomedical corridor. Cross into Silver Spring and the Maryland suburbs, where NOAA and the FDA draw their own orbits of consultants and suppliers. Every exit ramp leads to another cluster of office parks, every cluster filled with tenants whose business cards feature abbreviations like DARPA, NSA, and DOD.

This was Washington REIT's hunting ground for four decades. The strategy was deliberately unglamorous: own Class B and B+ office buildings and neighborhood retail centers in the suburban ring around D.C. Not trophy towers downtown, not cutting-edge research campuses, but the solid, functional space where mid-tier government contractors housed their proposal-writing teams, where small law firms drafted regulatory filings, where trade associations held their board meetings. The buildings were never going to make an architecture magazine, but they were going to be full.

The competitive landscape was formidable. JBG Companies (later JBG Smith) was the dominant local developer-operator, known for mixed-use projects and an aggressive development pipeline. Boston Properties, one of the largest office REITs nationally, held major trophy assets in D.C. proper. The Carr Companies, Vornado Realty Trust, and Brandywine Realty all competed for tenants in the same submarkets. Washington REIT differentiated not by building the flashiest buildings but by being the steadiest operator—conservative leverage, local relationships, and an intimate knowledge of which submarkets were tightening and which had surplus space.

The dividend story was the real siren song. Washington REIT paid its first quarterly dividend shortly after its founding and then proceeded to either maintain or increase that dividend for an extraordinary 192 consecutive quarters—a streak that spanned roughly from the early 1960s through the early 2010s. To put that in context, that is nearly fifty years of unbroken, non-declining quarterly cash payments to shareholders. For income investors, this was the gold standard. Financial advisors in the D.C. metro area recommended Washington REIT stock the way they recommended Treasury bonds: not for excitement, but for reliability.

The management philosophy reinforced this identity. Leadership teams through the decades shared a common creed: we know our market, we stay conservative, and we don't chase growth for its own sake. Washington REIT never tried to become a national REIT. It never made a splashy acquisition in Dallas or Miami. It stuck to the 50-mile radius around the Capitol dome and tried to own the best B+ assets in that radius. In an industry prone to empire-building and overleveraging, this modesty was genuinely distinctive.

And it worked, for a long time. Government spending rose under Kennedy, Johnson, Nixon, Reagan, Clinton, and both Bushes. Each defense buildup, each new agency, each expansion of the regulatory state added tenants to the Beltway economy and demand for the kind of space Washington REIT owned. The company wasn't trying to catch lightning in a bottle. It was trying to collect rain in a very reliable basin.

But real estate is a physical business, and physical assets age. By the early 2000s, some of Washington REIT's office buildings were thirty or forty years old. The tenants they were built for—small to mid-size firms that needed 5,000 to 20,000 square feet—were beginning to rethink what they wanted. Younger workers, even in government contracting, were starting to prefer locations near Metro stations, not buildings surrounded by parking lots. The retail centers, too, were showing their age as big-box stores and e-commerce began pulling shoppers away from neighborhood strip malls. The rain was still falling, but the basin was starting to crack.

IV. Cracks in the Foundation: The 2008 Crisis & Changing Tides

The 2008 financial crisis didn't destroy Washington REIT, but it exposed vulnerabilities that had been accumulating quietly for years. As credit markets froze and the broader economy contracted, office demand in the D.C. suburbs softened meaningfully for the first time in a generation. Government contractors, who had been expanding relentlessly through the post-9/11 defense buildup, suddenly faced a new fiscal reality: the wars in Iraq and Afghanistan were winding down, deficit hawks were gaining political power, and the era of automatic budget growth was ending.

The sequestration crisis of 2013 put an exclamation point on this shift. Automatic across-the-board spending cuts, triggered by Congress's failure to reach a deficit-reduction deal, slashed discretionary spending by roughly $85 billion in a single year. Defense contractors cut headcount. Consulting firms shrank their D.C. footprints. Agencies consolidated into fewer, more efficient buildings—often newer ones with better amenities, LEED certifications, and open floor plans. The tenants that had been Washington REIT's bread and butter for fifty years were suddenly economizing, and the Class B office park in Fairfax County was the first thing to go.

Simultaneously, the retail portfolio was under assault from a different direction. Amazon—headquartered three thousand miles away in Seattle—was systematically destroying the economics of neighborhood shopping centers. The strip mall anchored by a Borders bookstore and a RadioShack looked increasingly obsolete when those tenants went bankrupt. The "retail apocalypse" was not yet in full swing, but the early warning signs were unmistakable: foot traffic declining, renewal rates softening, and the gap between Class A retail (experiential, high-foot-traffic) and Class B retail (commodity, convenience-driven) widening into a chasm.

Perhaps the most consequential shift was demographic. The millennial generation—the largest cohort in American history—was entering the workforce and making housing and location choices that were fundamentally different from those of their parents. These young workers didn't want to commute from a single-family home in Centreville to a cubicle in a Tysons Corner office park. They wanted to live in walkable neighborhoods near Metro stations, preferably in buildings with amenities like rooftop decks, fitness centers, and coworking spaces. They wanted urban. And they were willing to pay for it.

The Amazon HQ2 saga crystallized these dynamics. When Amazon announced in 2017 that it was searching for a location for a second headquarters that would employ up to 50,000 people, cities across North America fell over themselves to compete. Washington, D.C. was a finalist, but the ultimate winner—announced in November 2018—was Crystal City in Arlington, Virginia, rebranded as "National Landing." The irony was rich: D.C. "lost" the competition to a submarket that was technically within Washington REIT's portfolio area. But the deeper signal was what Amazon wanted: transit access, walkability, urban density, and a deep pool of young, educated workers who preferred apartments to houses.

For Washington REIT, HQ2 was both validation and warning. It validated the D.C. metro as a growth market—Amazon was betting tens of billions of dollars on the region's talent pool and quality of life. But it warned that the growth was concentrating in precisely the asset types Washington REIT didn't own: high-rise residential towers, transit-oriented mixed-use developments, and Class A office space with cutting-edge amenities. The suburban office parks and strip malls that made up the bulk of Washington REIT's portfolio were on the wrong side of every trend HQ2 represented.

The existential question was now impossible to ignore. Washington REIT's leadership had to confront a reality that many legacy companies in many industries have faced: the business that built us is the business that will bury us if we don't change. The question was not whether to change, but how fast, how radically, and whether the company could survive the financial and organizational pain of transformation.

V. The Inflection Point: Paul McDermott Takes the Wheel (2012–2018)

Paul Thomas McDermott was not the obvious choice to lead a revolution. A Washington, D.C. native with a business degree from Shepherd University and an MBA in finance from American University, he had spent his entire career—more than two decades by the time he became CEO—in D.C.-area real estate finance. His resume read like a tour of the institutional plumbing behind commercial real estate: Lend Lease Real Estate Investments, where he ran the D.C. region; Freddie Mac, where he served as chief credit officer of the multifamily division; PNC Realty Investors; and Rockefeller Group Investment Management, a subsidiary of Japan's Mitsubishi Estate.

What made McDermott different was his Freddie Mac years. From 2002 to 2006, he had been immersed in the economics of multifamily housing—not office buildings, not shopping centers, but apartments. He understood the credit characteristics of rental housing, the demographics driving demand, and the policy environment that shaped supply. When he arrived at Washington REIT in 2013 as President and CEO—elevated to Chairman in 2018—he brought a mental model that was distinct from the office-centric worldview that had governed the company for fifty years.

His first moves, however, were conventional. McDermott initially tried to reposition the existing portfolio: upgrading office properties, investing in tenant improvements, pursuing higher-quality retail tenants. The logic was sensible—improve what you own, push rents higher, and capture more value from the D.C. market's underlying growth. But the results were mixed. The fundamental challenge was that improving a Class B office park in Herndon, Virginia, could only do so much when the tenants themselves were migrating to different kinds of space in different locations.

One of McDermott's early tough calls came in July 2012, when the board cut the quarterly dividend from $0.43375 to $0.30 per share—a 31% reduction that broke the legendary streak of 192 consecutive quarters of equal or increasing payouts. For a company whose identity was built on dividend reliability, this was a watershed. Income investors who had held the stock for decades felt betrayed. But the cut freed up capital that management argued was necessary for repositioning. It was the first signal that the old Washington REIT was yielding to something new, even if nobody yet knew exactly what.

The real intellectual breakthrough came in the mid-2010s, as McDermott and his team studied the data on what was actually happening in the D.C. metro economy. The region was still growing—adding jobs, attracting immigrants, drawing young professionals—but the growth was manifesting as demand for housing, not office space. Northern Virginia's population was expanding. Millennials were forming households but renting rather than buying, pushed by student debt, urban preferences, and sky-high home prices. The D.C. metro's housing stock was chronically undersupplied, constrained by restrictive zoning, NIMBY opposition, and the natural geographic limits of building in a region carved up by rivers, parks, and federal land.

This was the demographic insight that changed everything. McDermott's team saw that the same economic engine that had powered Washington REIT's office portfolio for decades—federal spending, defense contractors, a stable white-collar workforce—was now generating even stronger demand for apartments. Amazon's arrival would only accelerate this. HQ2 alone promised 25,000 high-income jobs in a submarket where housing was already scarce. The tech sector was expanding in the D.C. area. Government agencies were adopting hybrid work models that reduced demand for office space but did nothing to reduce demand for housing near transit and amenities.

The strategic question was stark: Should a fifty-plus-year-old office REIT become a multifamily player? The internal debate was fierce. Board members with decades of office experience questioned whether the management team had the operational expertise to run apartments. Shareholders who had bought the stock for its office-backed dividends wondered why they should trust the same leadership to operate in a completely different asset class. Analysts pointed out that selling office properties in a weak market to buy apartments in a strong market meant selling low and buying high—the cardinal sin of capital allocation.

McDermott's counterargument was existential: the office market isn't cyclically weak, it's structurally impaired. Suburban Class B office space is not coming back. Waiting for a recovery that may never arrive is a worse gamble than executing a pivot with imperfect timing. In effect, he was asking the board and shareholders to accept a near-term value destruction in exchange for a long-term repositioning toward growth. It was the kind of argument that gets a CEO fired if it goes wrong.

The pivot began modestly in 2017 and 2018, with small multifamily acquisitions that tested the operational capabilities and gave the team experience managing apartments. These early deals were deliberate: not trophy assets, but solid, well-located workforce housing communities that would prove the concept. If Washington REIT could acquire, operate, and lease up apartment communities at competitive returns, the full-scale transformation would follow. If not, the bet could be unwound before it became fatal.

The multifamily thesis had powerful structural tailwinds. Apartment buildings generate higher revenue growth than office when demand exceeds supply, which it clearly did in the D.C. metro. Tenant turnover in multifamily is manageable and predictable—leases are annual, not five-to-ten-year commitments, which means rents can be marked to market faster. The ESG narrative favored residential over office. And perhaps most importantly, the capital markets loved multifamily: apartment REITs traded at higher valuation multiples than office REITs, which meant that every dollar of NOI generated by apartments was worth more in the stock market than a dollar of NOI from an office building. The same company, with the same management team, could be worth significantly more simply by changing the composition of its portfolio.

VI. The Great Transformation: Office to Residential (2018–2022)

If the period from 2012 to 2018 was about diagnosis and debate, the years from 2019 through 2022 were about surgery. Washington REIT embarked on one of the most aggressive portfolio transformations in REIT history—a complete asset-class pivot executed in the span of roughly three years, accelerated by a global pandemic that no one saw coming.

The first phase, in 2019 and early 2020, involved selective dispositions of office assets and targeted multifamily acquisitions. Management sold two office properties in December 2020 for $106.5 million, using the proceeds to fund apartment purchases in the D.C. metro and, notably, in the Atlanta metro area—a geographic expansion that signaled ambitions beyond the traditional Washington footprint. The pace was deliberate: sell one or two buildings, buy one or two communities, prove the model, repeat.

Then COVID-19 arrived in March 2020, and the transformation went from deliberate to urgent. The pandemic didn't cause the office-to-residential pivot—the strategic logic predated COVID by several years—but it provided the most powerful possible validation. Overnight, tens of millions of American office workers began working from home. Corporate tenants discovered that they could function without physical offices, or at least with far less space. Office vacancy rates spiked nationally, and in the D.C. metro, the impact was amplified by the federal government's embrace of telework. Agencies that had been slow to adopt remote work suddenly had no choice, and many discovered they liked it.

Multifamily, by contrast, proved remarkably resilient. People still needed to live somewhere, and in fact, the pandemic increased housing demand as households sought more space, roommates separated, and workers no longer tethered to an office chose neighborhoods based on lifestyle rather than commute times. Apartment occupancy held steady. Rent growth, after a brief pandemic dip, roared back. Washington REIT's multifamily assets outperformed its office portfolio by every meaningful metric.

This divergence gave McDermott the ammunition to accelerate. In 2021, Washington REIT executed two landmark transactions that fundamentally remade the company. First, in June 2021, it sold its entire remaining office portfolio—twelve properties totaling 2.37 million square feet across Northern Virginia and Washington, D.C.—to Brookfield Asset Management for $766 million. Then, in September 2021, it sold all eight retail assets, totaling nearly 700,000 square feet, to Rosenthal Properties for $168.3 million. Combined, these two dispositions generated nearly $934 million in proceeds—close to a billion dollars—and eliminated the company's exposure to the two asset classes that had defined it for sixty years.

The sole exception was Watergate 600, a roughly 300,000-square-foot Class A office building at 600 New Hampshire Avenue in Washington, D.C., adjacent to the Kennedy Center and the Potomac River. Part of the internationally recognized Watergate Complex, this property had been acquired for $135 million in 2017 and was retained through the transformation, likely because its iconic location and prestige-tenant profile made it a different animal from the suburban office parks that were sold. It would prove to be the last commercial holdout, the final vestige of the old Washington REIT.

The proceeds from the office and retail sales were redeployed into multifamily acquisitions—apartment communities in the D.C. metro, Atlanta, and other southeastern markets—and into debt repayment. The capital allocation was aggressive: management was simultaneously selling a depressed asset class and buying into an asset class trading at or near peak valuations. Critics called it selling low and buying high. Management's response was that pricing reflected long-term fundamentals, not temporary dislocations—office was cheap because it deserved to be cheap, and apartments were expensive because the demand was real and sustainable.

In October 2022, the transformation received its symbolic capstone: Washington REIT officially rebranded as Elme Communities, changing its NYSE ticker from WRE to ELME. The name "Elme" was derived from "elm," evoking the tree-lined streets of the D.C. neighborhoods where the company operated. It was a deliberate break with the past—shedding "Washington" and "Real Estate Investment Trust" in favor of a softer, lifestyle-oriented brand that signaled community, livability, and modernity. The old name had suggested a conservative, institutional landlord. The new name was designed to appeal to residents, not just investors.

The third critical dimension of the transformation was talent. Running apartment communities requires a fundamentally different skill set than managing office buildings. Office landlords negotiate complex, multi-year leases with corporate tenants represented by real estate brokers. Apartment operators manage thousands of individual leases, handle maintenance requests, run amenity programs, and compete for residents through marketing and customer service. McDermott brought in experienced multifamily operators, leasing specialists, and development professionals—essentially rebuilding the company's human capital from scratch while executing the largest portfolio restructuring in its history.

By the end of 2022, the transformation was substantially complete. Elme Communities owned approximately 9,400 apartment homes, concentrated in the D.C. metro with a growing presence in Atlanta. Its same-store multifamily NOI had grown 8.8% in 2022, with blended lease rate growth of 9.4%. Occupancy hovered around 95.6%. These were strong operating metrics by any standard, and they appeared to vindicate the pivot.

The dividend, however, told a more complicated story. In the third quarter of 2021, management cut the quarterly payout again—from $0.30 to $0.17 per share, a 43% reduction. The rationale was that the transformation required capital, and aligning the dividend to post-transformation taxable income was necessary to fund growth. For long-term shareholders who had held Washington REIT for its dividend reliability, this was a second painful cut in less than a decade. The stock price reflected the tension: after briefly recovering to about $25 at the end of 2021, shares fell to roughly $17.57 by late 2022 as rising interest rates hammered REIT valuations across the board.

VII. The New Elme: Vision, Portfolio, and the Unexpected Finale (2022–2026)

By early 2023, Elme Communities was operating as a fundamentally different company from the Washington REIT of even five years earlier. The portfolio was over 90% multifamily, with Watergate 600 as the lone remaining office asset. The target tenant was the middle-income renter—not the luxury apartment dweller served by AvalonBay or Equity Residential, but the workforce renter earning enough to afford market-rate housing but priced out of homeownership. This was a deliberate niche: middle-income renters had lower vacancy rates and more stable occupancy than luxury tenants, and the D.C. metro's housing shortage was most acute in this segment.

Riverside Apartments in Alexandria, Virginia—the portfolio's largest community at 1,222 units—exemplified the strategy. Located near Cameron Run, it offered solid workforce housing with convenient access to the region's transit network and employment centers. Other communities in McLean, Bethesda, Germantown, and Washington, D.C. proper rounded out a portfolio oriented toward transit accessibility and suburban walkability.

The ESG program was substantive, not performative. Elme set ten-year targets for a 20% reduction in energy intensity, a 50% reduction in greenhouse gas emissions, and a 15% reduction in water usage. Its GRESB score climbed from 45 in 2014 to 76-77, and it earned a Public Disclosure rating of "A" for three consecutive years. A $350 million Green Bond issued in 2021 funded environmentally certified building projects. By 2023, 69% of the portfolio held at least one sustainability certification, EV charging stations had expanded from 5% to 42% of communities, and solar installations at two D.C. communities generated approximately 600,000 kilowatt-hours of clean energy annually.

But macroeconomic headwinds were intensifying. The Federal Reserve's rate-hiking cycle, which began in March 2022 and ultimately took the federal funds rate from near zero to 5.25-5.50% by mid-2023, was devastating for REIT equities. Higher rates increased borrowing costs, compressed valuation multiples, and made dividend yields less competitive relative to risk-free Treasury bonds. REIT share prices fell more than 21% from January 2022 through late 2023, with valuation multiples declining over 30%—worse than any other S&P 500 sector.

Elme was caught in this vise. Despite solid operating performance—same-store NOI grew 8.3% in 2023, occupancy remained in the mid-95% range, and Core FFO reached $0.97 per share—the stock price languished. The market was not rewarding execution; it was punishing the entire sector for interest rate sensitivity. The company that had successfully transformed itself from a declining office REIT into a growing apartment company found that the stock market didn't much care about the distinction when the ten-year Treasury yield was approaching 5%.

The deceleration in 2024 compounded the problem. Same-store NOI growth slowed to 1.4%, reflecting broader D.C. market supply absorption as approximately 14,187 new apartment units came online in the metro area—a surge that temporarily diluted pricing power. Core FFO dipped to $0.93 per share. Occupancy edged down to the mid-94% range. None of these metrics were alarming in isolation, but for a company that had promised investors a growth story to justify the pain of transformation, the slowdown was poorly timed.

Then came the announcement that nobody expected. In 2025, Elme's board initiated a strategic alternatives review—corporate-speak for "we're exploring whether to sell the company." The review concluded with a definitive agreement: Cortland Partners would acquire nineteen of Elme's multifamily communities for approximately $1.6 billion. The transaction closed in November 2025. Elme's board approved a plan of liquidation and dissolution, and in January 2026, the company paid a special liquidating distribution of $14.67 per share to shareholders. Additional liquidating distributions of $2.90 to $3.50 per share were expected from the sale of remaining assets, primarily Watergate 600, which was being marketed for a first-half 2026 closing.

The stock, which had started 2024 around $17.40, dropped to approximately $2.14-$2.23 by early 2026—reflecting the fact that most of the company's value had already been distributed to shareholders in cash. The total anticipated return from the liquidation was approximately $17.58 to $18.50 per share, which means shareholders who held through the process received roughly the pre-announcement stock price in cash, plus or minus a few percent. It was neither a windfall nor a disaster—it was, in a sense, the market telling Elme that its transformation had created value, but not enough to sustain an independent public company.

The question of why Elme's board chose liquidation rather than continued independence is crucial. Several factors converged. The company's small scale—roughly 9,400 units against competitors with 60,000 to 100,000—created a persistent cost-of-capital disadvantage. Larger REITs could issue debt and equity at lower rates, spread corporate overhead across more properties, and attract a broader investor base. Elme's regional concentration in D.C., while providing deep market knowledge, limited its growth runway compared to diversified or Sun Belt-focused competitors. And the interest-rate environment, even as the Fed began cutting rates in September 2024, had reset investor expectations for REIT valuations in ways that made it difficult for a small, single-region apartment REIT to trade at a premium.

VIII. The REIT Business Model & Capital Structure Deep Dive

To understand why Elme's story ended the way it did, it helps to understand the mechanics of how REITs actually work—and why the structure that makes them so attractive to income investors also constrains them in ways that most operating companies never face.

Start with how REITs make money. The core financial metric is not earnings per share, as it would be for a normal corporation, but Funds from Operations, or FFO. Why the difference? Because traditional earnings include depreciation—a non-cash accounting charge that reduces reported profits as buildings "age" on paper. But real estate, unlike a manufacturing plant or a piece of software, often appreciates in value over time, especially in strong markets. Depreciation understates the true economic performance of a well-maintained building. FFO adds back depreciation and amortization to net income, providing a clearer picture of the cash a REIT actually generates. Think of it as the real estate equivalent of free cash flow.

A further refinement is Adjusted FFO, or AFFO, which takes FFO and subtracts the capital expenditures that are actually necessary to maintain the properties—replacing roofs, upgrading HVAC systems, renovating kitchens. AFFO is the truest measure of sustainable, distributable cash flow, and it is what savvy REIT investors watch most closely.

Below these corporate-level metrics sits the property-level engine: Net Operating Income. NOI equals rental revenue minus operating expenses at the property level—before corporate overhead, interest expense, or capital expenditures. Same-store NOI growth—how much NOI increases at properties the company has owned for at least a year—is the single most important indicator of whether a REIT's core business is getting better or worse. It strips out the effect of acquisitions and dispositions and reveals the organic health of the portfolio.

The dividend imperative is what makes the REIT structure both a gift and a straitjacket. By distributing at least 90% of taxable income, REITs avoid corporate taxation—a massive advantage that effectively gives shareholders access to pre-tax real estate returns. But it also means REITs cannot retain significant earnings to fund growth. A tech company can reinvest profits into R&D and expansion. A REIT must go to the capital markets—issuing new shares (diluting existing shareholders), taking on new debt (increasing leverage), or selling existing properties (shrinking the portfolio)—to fund acquisitions or development.

This creates a permanent dependence on external capital that makes REITs exquisitely sensitive to financial market conditions. When interest rates are low and capital is abundant, REITs can issue cheap debt, sell shares at high prices, and fund growth aggressively. When rates spike—as they did in 2022-2023—the equation reverses: debt becomes expensive, share prices fall (making equity issuance dilutive), and development projects that penciled at 4% cap rates no longer work at 6%. This is not a flaw in particular companies' strategies; it is a structural feature of the REIT model that affects every company in the sector.

During Elme's transformation, this structural constraint was acutely felt. The company sold nearly a billion dollars of office and retail assets to fund multifamily acquisitions, essentially self-financing the pivot through dispositions rather than relying on capital markets that were increasingly hostile. The approach was clever—using the proceeds of one asset class to buy another—but it meant the pace and scale of transformation were limited by what the company could sell. And because the office market was depressed while the apartment market was elevated, every transaction involved a painful spread between sale prices and purchase prices.

Elme's balance sheet management during this period was a high-wire act. The company needed to maintain investment-grade credit ratings, comply with debt covenants, and preserve financial flexibility even as it was executing the largest portfolio restructuring in its history. Leverage ratios—the amount of debt relative to the value of the assets or to EBITDA—had to stay within bounds acceptable to lenders and rating agencies. The $350 million Green Bond issued in 2021 was a creative tool: it raised capital at favorable rates while signaling ESG commitment, effectively killing two birds with one stone.

For investors, the key takeaway about REIT capital structure is that growth in this sector is always capital-intensive and externally funded. A REIT that grows too aggressively risks overleveraging. One that grows too cautiously risks falling behind competitors who are building and acquiring. The balancing act is permanent, and management's skill at navigating it—timing equity raises, locking in favorable debt terms, managing development pipelines—is arguably more important than any individual property decision.

IX. Competitive Landscape & Market Position

Elme Communities operated in one of the most competitive multifamily markets in the United States, facing rivals that ranged from national giants with ten times its scale to nimble local operators with deep neighborhood-level knowledge. Understanding where Elme fit in this competitive landscape—and why its position was both distinctive and precarious—is essential to understanding the liquidation decision.

At the national level, the apartment REIT sector is dominated by a handful of mega-cap companies. AvalonBay Communities, with a market capitalization in the range of $27-29 billion, owns approximately 98,700 apartment homes across the coastal United States, including a meaningful D.C. presence that accounted for roughly 12-15% of its portfolio. Equity Residential, at about $26 billion, operates over 80,000 units with D.C. as one of its six core markets. UDR, Mid-America Apartment Communities, and Camden Property Trust round out the major public competitors, each with portfolios ranging from 58,000 to over 100,000 units.

Against these behemoths, Elme's roughly 9,400 units looked almost boutique. The scale differential was not just a vanity metric—it had concrete financial implications. Larger REITs can issue bonds and commercial paper at lower interest rates because their diversification and size reduce perceived credit risk. They can spread corporate overhead—executive compensation, legal and accounting costs, investor relations—across more properties, resulting in lower per-unit costs. They attract broader analyst coverage and a deeper investor base, which generally supports higher trading multiples. In short, scale in the REIT world translates directly into a lower cost of capital, which is the single most important competitive advantage in a capital-intensive business.

Locally, Elme's closest geographic peer was JBG Smith Properties, another D.C.-focused REIT with approximately 6,164 multifamily units and a market cap of $1.1-1.3 billion. JBG Smith was hyperconcentrated in National Landing—the Arlington submarket anchored by Amazon's HQ2—with roughly 75% of its portfolio in that single neighborhood. On the private side, Bozzuto, a family-owned development and management company, was one of the most active apartment operators in the D.C. region, managing communities that competed directly with Elme's for tenants.

Elme's advantages were real but narrow. Decades of operating in the D.C. metro had given the company intimate knowledge of local market dynamics—which submarkets were tightening, where permitting processes were most favorable, which transit corridors were attracting investment. McDermott's Freddie Mac background gave the company sophisticated insight into multifamily credit and financing structures. Relationships with local governments, built over sixty years, provided advantages in navigating the zoning and permitting processes that could make or break development projects.

The D.C. market itself had distinctive dynamics that shaped competitive positioning. Supply constraints were significant: NIMBYism, restrictive zoning, and the natural geography of the region (rivers, federal parks, the District's height limits) limited new construction in many desirable neighborhoods. Demand drivers were diverse—the federal government, defense contractors, the tech sector (accelerated by Amazon), major universities, and international immigration all contributed to housing demand. Inside the Beltway, effective rents reached an all-time high of approximately $2,173 per month in 2024, and vacancy rates for Class B properties—Elme's primary niche—were lower than for luxury Class A properties.

The Amazon effect deserves special attention. When Amazon selected National Landing for HQ2 in 2018, it promised 25,000 jobs. The reality, as of 2024-2025, was more modest—approximately 8,000 employees had been hired, and Phase 2 of the campus (called PenPlace, including the iconic Helix building) was indefinitely paused as Amazon dealt with tech-sector headwinds and its own layoffs. But the announcement had already catalyzed enormous investment in the Arlington-Alexandria corridor, with rents in core areas near National Landing rising 12-18% annually in the years following the announcement. The ripple effect extended well beyond Arlington itself, expanding demand across the broader metro as Amazon workers chose to live in Bethesda, Alexandria, and other neighborhoods served by transit.

Looking at the supply pipeline, the competitive outlook was actually improving as Elme entered its final year. After the surge of roughly 14,200 new units delivered in 2024, the pipeline was dropping sharply to about 6,100 units expected in 2025 and only about 4,000 in 2026. This supply correction meant improving pricing power for existing landlords—a tailwind that Elme's successor owner, Cortland Partners, would likely benefit from.

X. Porter's Five Forces & Hamilton's Seven Powers

Porter's Five Forces Analysis

The multifamily REIT industry in the Washington, D.C. metro can be dissected through Michael Porter's framework to reveal the structural forces that shaped Elme's competitive environment and ultimately influenced its decision to pursue a sale.

The threat of new entrants is moderate. Building apartment communities requires enormous capital—tens of millions for a single project, hundreds of millions for a meaningful portfolio. Local knowledge, relationships with municipal governments, and experience navigating the D.C. region's complex permitting landscape create significant barriers. But these barriers are not impregnable. Private equity firms, sovereign wealth funds, and institutional investors like pension funds can deploy capital at scale and hire local expertise. Cortland Partners, the company that ultimately purchased Elme's portfolio, exemplified this: a well-capitalized private operator that could enter the D.C. market by acquiring an established platform rather than building from scratch.

Supplier bargaining power is medium to high, and it was a persistent headwind during Elme's transformation. "Suppliers" in real estate means construction labor, building materials, and land sellers. In the hot D.C. market, all three had significant pricing power. Construction costs escalated steadily throughout the 2020s, driven by labor shortages, supply chain disruptions, and rising material prices. Land in transit-oriented locations—the parcels Elme specifically targeted—was scarce and expensive. These cost pressures squeezed development margins and made the build-versus-buy decision more complicated.

Tenant bargaining power is moderate, tempered by the D.C. housing shortage. In a market where demand outstrips supply, landlords have pricing power. Elme's middle-income renter niche was particularly well-positioned: these renters had fewer alternatives than luxury tenants (who might trade down) or subsidized tenants (who had government-supported options). But renters are not captive. Annual leases mean turnover is constant, and tenants can and do comparison-shop among competing communities. Corporate relocations and government policy changes can shift demand patterns rapidly.

The threat of substitutes is moderate and evolving. For-sale housing is the primary substitute for renting, but sky-high D.C.-area home prices and elevated mortgage rates through 2023-2024 kept many would-be buyers in the rental market—a tailwind for multifamily landlords. Single-family rental homes, an asset class that expanded dramatically in the 2020s, represented a growing alternative. And remote work introduced a location substitution threat: if a federal contractor can work from home, they might choose to rent in a cheaper metro area entirely.

Industry rivalry is high—the most intense of the five forces. The D.C. multifamily market featured national REIT giants with superior capital access, aggressive local developers, and deep-pocketed private operators all competing for the same tenants and the same development sites. Differentiation among apartment communities is genuinely difficult: buildings offer similar floor plans, similar amenities, and similar locations within the same submarkets. Competition ultimately comes down to pricing, service quality, and the specific location advantages of individual properties.

Hamilton's Seven Powers Analysis

Hamilton Helmer's framework asks a different question: not what are the competitive forces, but what sustainable competitive advantages—"powers"—does a company possess? For Elme, the analysis is revealing and somewhat sobering.

Scale economies worked against Elme. With roughly 9,400 units against AvalonBay's 98,700 or Equity Residential's 80,000-plus, Elme could not spread corporate costs as efficiently, could not access capital markets as cheaply, and could not negotiate vendor contracts with the same leverage. In a capital-intensive, low-margin business like apartments, scale economies are one of the most important structural advantages—and Elme was on the wrong side of the equation.

Network effects are largely absent in real estate. Unlike a technology platform where each additional user makes the service more valuable, each additional apartment building does not inherently make the other buildings more valuable. There are minor community and reputation effects—a well-managed portfolio builds word-of-mouth referrals—but nothing approaching the structural network effects that power tech companies.

Counter-positioning was Elme's most compelling power, and it was the intellectual core of the transformation story. By pivoting from office to multifamily before the market consensus recognized that suburban office was structurally impaired, Elme positioned itself against legacy office REITs that were slower to adapt. The problem was that counter-positioning is a transitional advantage—once the market recognizes the shift (as it did during and after COVID), the positioning edge erodes and execution must carry the day.

Switching costs are low in multifamily. Tenants sign annual leases and can move relatively easily. However, the friction of moving—packing, logistics, disruption—creates some stickiness, and communities that build genuine neighborhood identity and social connections can retain residents at modestly above-market rents. Elme's rebranding to "Elme Communities" was partly an attempt to build this kind of community loyalty, though the evidence of its success was still nascent.

Branding power was limited. "Elme Communities" was a young brand in a market where tenant decisions are driven primarily by location, price, and amenities rather than brand loyalty. Unlike a luxury goods company where the brand itself commands a premium, an apartment company's "brand" is largely local and functional.

Cornered resources represented a genuine, if narrow, power. Elme held land and entitled development sites in transit-oriented D.C.-area locations that were difficult to replicate. The relationships with local governments, built over sixty years, provided advantages in navigating zoning and permitting. These are valuable assets, though they are transferable—as Cortland Partners effectively demonstrated by acquiring the entire portfolio.

Process power was emerging but unproven. Multifamily operations require specific expertise in leasing, maintenance, resident services, and community management. Elme was building these capabilities post-transformation, but had only a few years of operating history as a pure-play multifamily company—not long enough to demonstrate the kind of distinctive operational excellence that would constitute a durable competitive advantage.

The Key Insight: Elme's story ultimately illustrates a harsh reality about competitive advantage. The company successfully executed a strategic counter-positioning move that was genuinely prescient. But counter-positioning without scale economies is a transitional advantage, not a permanent one. Once the market recognized the superiority of multifamily over office (which COVID accelerated), Elme found itself competing as a small player in a space dominated by giants with structural cost advantages. The transformation was strategically correct but insufficient to overcome the scale disadvantage. Cortland Partners' acquisition was, in a sense, the market's way of saying: these are good assets, but they need a larger platform to reach their full potential.

XI. Business & Investing Lessons — The Playbook

Elme's sixty-five-year arc from founding to liquidation offers an unusually rich set of lessons for investors and business operators alike—lessons that extend far beyond real estate.

The first and most fundamental lesson concerns strategic pivoting: when to abandon a legacy business versus trying to optimize it. Washington REIT could have continued attempting to reposition its office and retail portfolio—upgrading buildings, chasing higher-quality tenants, investing in amenities. Many office REITs took exactly this approach, and most of them suffered worse outcomes. McDermott and his team recognized something that most incumbents struggle to accept: incremental improvement of a structurally declining asset class is a losing strategy. The gap between "cyclically weak" and "structurally impaired" is the most important distinction in business strategy, and Washington REIT got it right.

The second lesson is about timing and conviction. McDermott saw the office-to-residential trend early—arguably three to five years before the market consensus. But seeing a trend early is only valuable if you have the courage to act on it. Acting meant selling assets at depressed prices, buying into an expensive asset class, cutting a beloved dividend, and convincing skeptical shareholders that a sixty-year-old company should become something entirely new. Each of these decisions carried career risk for McDermott and financial risk for the company. The fact that the transformation was ultimately validated—operationally, if not in terms of sustained public-company independence—is a testament to the quality of the strategic thinking.

The third lesson is the most nuanced and perhaps the most valuable: transformation does not guarantee survival as an independent entity. Elme executed the strategic pivot successfully. The portfolio was repositioned. The brand was remade. Operating metrics improved. Same-store NOI grew at healthy rates. Occupancy was strong. The team delivered. And yet the company was ultimately sold and liquidated, because the competitive landscape favored larger platforms with cheaper capital access. This is a lesson that applies across industries: being right about strategic direction is necessary but not sufficient. Execution matters, but so does scale, timing relative to capital market conditions, and the competitive structure of the industry you're pivoting into.

The REIT structure itself creates a paradox that Elme's story illuminates. The forced dividend distribution enforces discipline—management cannot waste cash on vanity projects or empire-building. But it also starves companies of the retained earnings that might fund transformative investments. A tech company can reinvest profits for years to build a new business line. A REIT must distribute virtually every dollar of profit, then go hat in hand to the capital markets to fund growth. This structural constraint makes large-scale pivots extraordinarily difficult for REITs, which is one reason Elme's transformation was so unusual—and why it required asset dispositions rather than retained earnings to fund.

The talent dimension deserves emphasis. Transforming from an office REIT to a multifamily REIT meant hiring an entirely new operational skill set. The people who negotiate ten-year office leases with corporate tenants are not the people who manage annual lease renewals with thousands of individual residents. The marketing strategies are different. The maintenance requirements are different. The customer service expectations are different. Elme had to rebuild its human capital while simultaneously restructuring its asset base—a dual transformation that is extraordinarily difficult to execute.

Stakeholder management was perhaps McDermott's most underappreciated achievement. Convincing the board of directors to approve a wholesale business model change at a sixty-year-old company required extraordinary persuasion. Convincing shareholders to accept two dividend cuts in less than a decade required credibility and a compelling narrative. Convincing analysts to cover and recommend a company in transition—neither pure office nor pure multifamily, with uncertain earnings trajectory—required patience and transparency. The rebranding to "Elme Communities" was not cosmetic; it was a signal to capital markets that the old identity was gone and a new investment thesis applied.

The regional concentration trade-off runs through the entire story. Deep local expertise was Washington REIT's founding advantage and remained Elme's differentiator: decades of relationships, granular market knowledge, and reputational capital in a single metro area. But concentration also meant vulnerability to D.C.-specific risks—federal budget cuts, government reorganizations, local policy changes—and limited the company's growth runway compared to diversified competitors operating in multiple markets. The Atlanta expansion was an attempt to address this, but it was too small and too late to meaningfully change the risk profile.

Finally, there is the lesson about narrative and identity in capital markets. When Washington REIT rebranded as Elme Communities, it was attempting something that many companies try and few succeed at: changing how investors categorize and value the company. A name change alone accomplishes nothing, but when backed by genuine portfolio transformation, it can shift analyst coverage, attract new institutional investors, and break free from the valuation anchors of the old business. Elme made significant progress on this front—it was increasingly covered as a multifamily REIT rather than a diversified REIT—but the small scale and regional concentration ultimately limited the rerating potential.

XII. Bull vs. Bear Case, Key Metrics, and What to Watch

Although Elme Communities has entered a plan of liquidation and dissolution, the strategic and analytical framework of its story remains instructive for investors evaluating similar transformation narratives in the REIT sector and beyond. And for those holding ELME shares through the liquidation process, the remaining questions are practical: How much will the final distributions total? What will Watergate 600 sell for? Here is how to think about the bull and bear cases, reframed for a company in its final chapter.

The Bull Case for the Transformation Thesis (Validated)

The D.C. region's fundamental demand drivers proved durable. Federal government employment remained stable, Amazon HQ2 brought thousands of high-income jobs (even if fewer than the 25,000 originally promised), immigration added population, and the chronic housing shortage persisted. The supply pipeline, after surging in 2024, was declining sharply—to roughly 6,100 units expected in 2025 and about 4,000 in 2026—which implied improving pricing power for existing landlords. Same-store NOI growth, which had decelerated to 1.4% in 2024, was already re-accelerating to 5.5% in the first quarter of 2025 before the liquidation process took hold.

Management's decision to target middle-income renters proved prescient. This segment experienced lower vacancy rates (around 6.4% for Class B properties versus 10.6% for Class A luxury) and more stable occupancy because tenants had fewer alternatives. The ESG program was substantive and externally validated, with GRESB scores roughly doubling over a decade. The interest rate environment was improving, with the Fed beginning to cut rates in September 2024, which historically benefited REIT valuations.

The Cortland Partners acquisition at approximately $1.6 billion for nineteen communities represented meaningful validation that the assets themselves were attractive to sophisticated buyers. Cortland—a well-capitalized private multifamily operator—was paying a price that suggested confidence in the D.C. metro's long-term multifamily fundamentals.

The Bear Case (Also Validated)

The scale disadvantage was ultimately decisive. At roughly 9,400 units, Elme simply could not compete on cost of capital against AvalonBay (98,700 units), Equity Residential (80,000+ units), or even Camden Property Trust (58,000+ units). In a business where the cost of debt and equity directly determines which development projects are feasible and which acquisition prices are competitive, a persistent cost-of-capital gap is almost impossible to overcome through operational excellence alone.

Regional concentration limited the growth runway. While D.C. is a strong multifamily market, it is not growing as fast as Sun Belt markets like Dallas, Phoenix, Charlotte, and Tampa, where many larger competitors were deploying capital aggressively. The Atlanta expansion was a step toward diversification, but it was too small to meaningfully change the geographic risk profile before the liquidation decision was made.

The interest-rate environment, even after the Fed began cutting, had reset expectations. The pre-2022 world of near-zero rates and compressed cap rates was gone. REIT investors were recalibrating what they would pay for apartment NOI, and the recalibration disproportionately hurt smaller, less liquid names like Elme.

Development execution risk was real. The transformation required not just acquiring existing apartments but building new communities and mixed-use developments—projects that carried construction cost, permitting, and lease-up risks. Rising construction costs through the early 2020s squeezed prospective development margins and made it harder to generate attractive returns on invested capital.

The KPIs That Mattered Most

For Elme during its operating life—and for investors evaluating similar multifamily REITs—three key performance indicators stood above all others:

Same-Store NOI Growth: This single metric captures the organic health of the portfolio, stripping out the effects of acquisitions and dispositions. When Elme's same-store NOI was growing 8-9% annually (as in 2022-2023), the transformation thesis looked compelling. When growth slowed to 1.4% (as in 2024), concerns about the competitive environment and pricing power came to the fore. For any multifamily REIT, same-store NOI growth above the rate of inflation signals genuine value creation; growth below inflation signals margin compression.

Occupancy Rate: For a company targeting middle-income renters, occupancy is the canary in the coal mine. Elme maintained occupancy in the 94.5-95.6% range throughout the transformation—a healthy level that suggested demand was robust. A sustained decline below 94% would have signaled oversupply or tenant migration. For multifamily REITs generally, the 95% level is often considered the equilibrium: above it, landlords have strong pricing power; below it, concessions and incentives begin eroding effective rents.

Leverage Ratio (Net Debt to EBITDA): In a capital-intensive, interest-rate-sensitive business, balance sheet health determines whether management has the flexibility to pursue opportunities or is trapped servicing debt. For REITs, net debt to EBITDA ratios above 7x are generally considered elevated; below 6x provides meaningful financial flexibility. Elme's management of this ratio during the transformation—using asset sale proceeds to fund acquisitions while maintaining investment-grade credit—was one of the most critical dimensions of execution.

XIII. Epilogue & Reflections

The final chapter of Elme Communities is still being written as Watergate 600—that last, iconic office building at 600 New Hampshire Avenue, adjacent to the Kennedy Center—awaits a buyer. When it sells, likely in the first half of 2026, the remaining proceeds will be distributed to shareholders, the corporate entity will be dissolved, and sixty-five years of continuous public-market existence will come to an end. Washington REIT, the company that was among the very first to bring the REIT concept to life in 1960, will become a case study rather than a going concern.

But what a case study it is. The Washington REIT-to-Elme transformation stands as one of the most dramatic strategic pivots in REIT history—a complete asset-class metamorphosis executed in roughly three years, under the pressure of a global pandemic, rising interest rates, and intense skepticism from the investment community. That the company ultimately chose liquidation rather than continued independence does not invalidate the strategic logic of the transformation. It does, however, add an important coda: strategic correctness is necessary but not sufficient for long-term survival. Scale, capital access, and competitive positioning in the target industry matter just as much as the quality of the pivot itself.

The broader story is about how companies survive—or don't survive—disruption. Across the American office REIT sector, the 2020s have been an existential reckoning. Remote and hybrid work permanently reduced demand for office space, particularly the Class B suburban space that was Washington REIT's historical bread and butter. Some office REITs have adapted by upgrading to trophy-quality properties in prime urban locations. Others have attempted conversions to residential or mixed-use. Many have simply watched their portfolios decline in value as vacancies climbed. Washington REIT chose the most radical option—total portfolio replacement—and executed it with remarkable speed and competence. That the end result was a sale to a private operator, rather than a flourishing independent public company, speaks more to the structural dynamics of the apartment REIT market (where scale is king) than to any failure of execution.

For the D.C. region itself, the story reflects a metropolis in transition. The federal government remains the anchor of the economy, but its role is evolving. Hybrid work has permanently changed the spatial dynamics of how and where government employees and contractors operate. Amazon's HQ2, even at reduced scale, has catalyzed investment in the Arlington-Alexandria corridor. Immigration, university research, and the growing life sciences sector are diversifying the economic base. The chronic housing shortage that drove Elme's transformation thesis persists, and the declining supply pipeline suggests it will worsen before it improves. Whoever owns those 9,400 apartment homes in the years ahead—whether Cortland Partners or a successor—will likely benefit from the same demographic and supply dynamics that McDermott identified a decade ago.

The lessons for founders, operators, and investors are both timeless and specific. Know when to pivot, but understand that pivoting is only the beginning—you must also have the scale and capital structure to compete in your new market. Transformation requires not just new assets but new skills, new talent, and a new organizational identity. The REIT structure, for all its advantages, imposes constraints that make large-scale transformation extraordinarily difficult, because you cannot retain the earnings needed to self-fund the change. And perhaps most importantly: the market does not reward effort or intentions. It rewards results, measured in the cold arithmetic of funds from operations, occupancy rates, and returns on invested capital.

Paul McDermott and his team saw the future of the D.C. real estate market more clearly than most. They had the courage to act on that vision when the conventional wisdom was to stay the course. They executed a transformation that, by any operational measure, succeeded. And in the end, they made the disciplined decision to return capital to shareholders when the public-market structure no longer served the company's assets and strategy. There is a particular kind of integrity in that final act—knowing when the story of an independent company has been told, and letting the next chapter be written by someone else.

XIV. Further Reading & Resources

-

Elme Communities Investor Presentations (2019-2025) — Track the transformation in real time through quarterly decks, earnings call transcripts, and supplemental data packages available on the company's investor relations page.

-

Green Street REIT Research — The preeminent independent research firm covering the REIT sector provides detailed company-level analysis, valuation frameworks, and comparative metrics for apartment REITs including Elme's historical coverage.

-

Nareit (National Association of Real Estate Investment Trusts) — Industry data, policy analysis, and educational resources on REIT structure, tax treatment, and sector performance metrics.

-

"The Color of Law" by Richard Rothstein — Essential context for understanding D.C.'s housing dynamics, including the zoning policies, racial segregation, and land-use decisions that shaped the metro area's residential development patterns.

-

Washington Business Journal Archives — Local business journalism covering D.C. real estate market transactions, development projects, and the competitive dynamics among the region's major landlords and developers.

-

Urban Land Institute (ULI) Case Studies — Research on mixed-use development, transit-oriented communities, and the planning frameworks that shaped projects in Elme's target submarkets.

-

Paul McDermott Earnings Call Transcripts — Available through the company's investor relations page and third-party providers, these transcripts reveal the CEO's strategic thinking, his framing of the transformation rationale, and his responses to analyst skepticism over multiple years.

-

"The REIT Way" by Ralph Block — A comprehensive guide to REIT investing, valuation methodologies, and the mechanics of the REIT structure, providing essential context for evaluating companies like Elme.

-

CoStar and Real Capital Analytics — Commercial real estate data platforms providing D.C. metro market fundamentals, transaction data, rent trends, and supply pipeline information.

-

Cortland Partners Investor Materials — As the acquirer of Elme's multifamily portfolio, Cortland's public statements and market communications provide insight into how a sophisticated private operator valued and plans to manage the assets going forward.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube