EHang: The Flight of the Autonomous Dragon

I. Introduction & The "Blade Runner" Vision

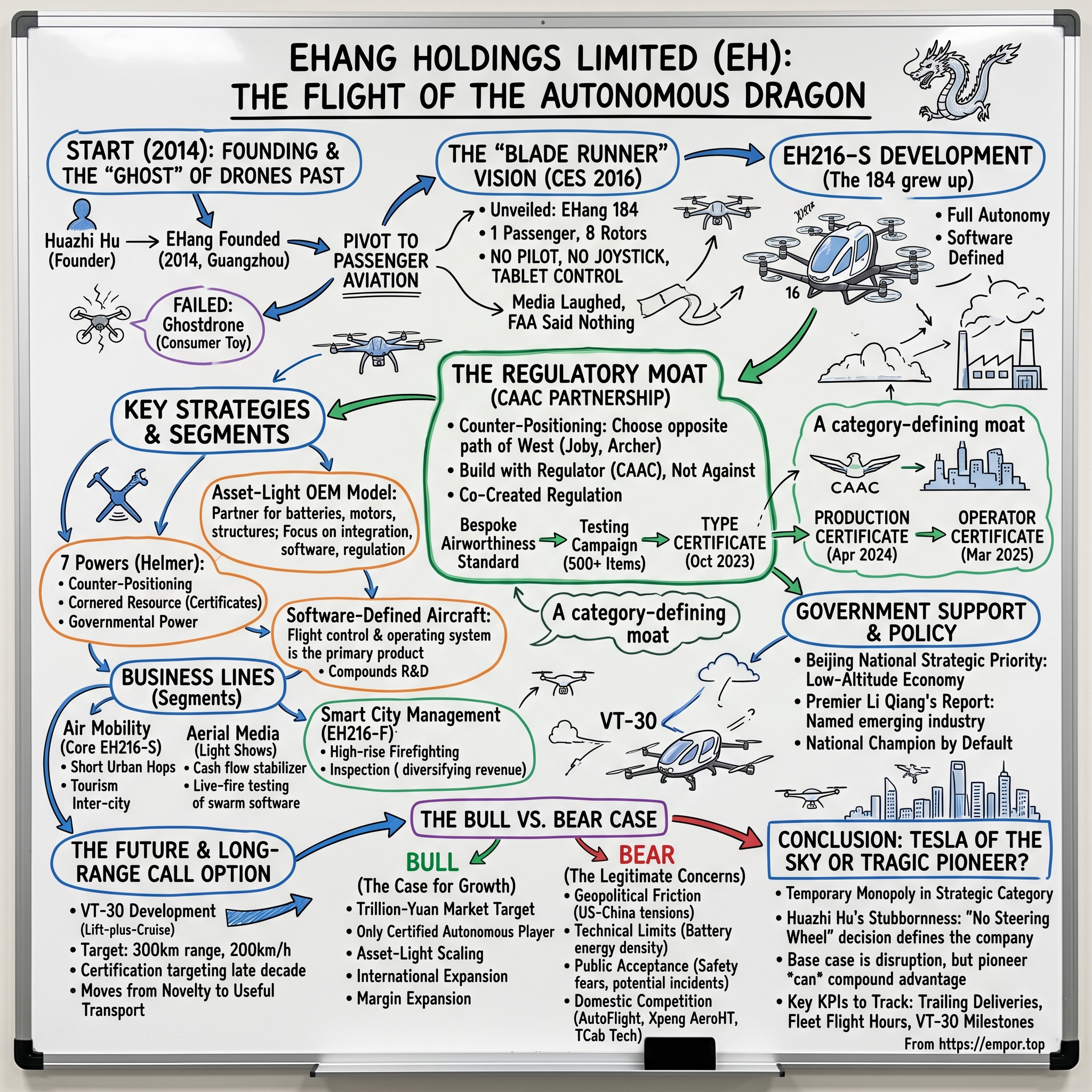

Las Vegas, January 2016. The Consumer Electronics Show was the usual circus of 4K televisions, IoT refrigerators, and VR headsets that would be forgotten by March. But in a corner of the Las Vegas Convention Center, a small Chinese company with a name few Americans could pronounce had wheeled in something that looked like it had been stolen from the set of a Ridley Scott film. It was matte white, roughly the size of a small car, with eight propellers arranged on four arms, and a single-seat cockpit with a tablet where the yoke should have been. They called it the EHang 184. One passenger. Eight rotors. Four arms. Zero pilots.

The press release claimed this thing could carry a human being through the sky, autonomously, at 100 kilometers per hour, for roughly 23 minutes on a single charge. No license required. No joystick. Just punch in a destination on the tablet and lean back. The American aviation press laughed. The Chinese aviation press was cautiously intrigued. The FAA said nothing, because from the FAA's perspective, what EHang had shown was not an aircraft at all—it was a large drone that had no business carrying a human.

And yet, ten years later, almost to the day, that same company now holds the only Type Certificate in the world for a pilotless passenger-carrying electric vertical take-off and landing aircraft. The 184 grew up. It became the EH216-S. It earned its airworthiness papers from the Civil Aviation Administration of China in October 2023, its Production Certificate in April 2024, and its first commercial operator certificates for air taxi service in March 2025. By the time this story is being told in the spring of 2026, EHang has delivered hundreds of these vehicles, its factory in Yunfu is scaling toward thousands of annual units, and Chinese municipalities from Hefei to Guangzhou are competing to be designated "low-altitude economy" pilot zones.

So here is the question this article wants to chew on. Is EHang merely a drone company that got lucky with a regulatory tailwind? Or are they something stranger and more interesting—the first real architect of a new layer of infrastructure called the Low-Altitude Economy, a category that Beijing has declared a trillion-yuan growth frontier and which, by definition, cannot be built by Western competitors while the current geopolitical lines hold?

The roadmap ahead traces a company that began with a failed consumer toy, pivoted into a product so audacious that most of the aerospace establishment dismissed it as marketing vapor, quietly accumulated a regulatory moat while Silicon Valley rivals raised billions of dollars to chase piloted designs, and today sits at the strange intersection of consumer electronics economics and aviation-grade certification discipline. It is a story about counter-positioning, about building with the regulator rather than against it, and about a founder named Huazhi Hu who looked at the skies above Chinese cities and refused, stubbornly and famously, to put a steering wheel in his aircraft.

II. Founding & The "Ghost" of Drones Past

Huazhi Hu was born in 1975 in Linchuan, a city in Jiangxi province more famous for the Ming Dynasty playwright Tang Xianzu than for any technological output. As a child, his bedroom ceiling was allegedly decorated with dangling balsa-wood model aircraft that he built from kits, then from scratch once the kits ran out. By the time he reached the University of Chinese Academy of Sciences for his doctoral work in pattern recognition and intelligent systems, he had essentially fused two obsessions: the machine-learning problem of getting computers to recognize patterns in noisy data, and the childhood problem of getting things to fly without falling out of the sky. Both problems, as it turned out, share a common underlying discipline: control theory in the presence of uncertainty.

Before EHang, Hu had already built one company, a mobile navigation firm called Billion Spring, which gave him his first taste of what it was like to be a founder in Guangzhou's hyper-competitive Pearl River Delta tech scene. Guangzhou is often overshadowed in Western accounts of Chinese tech by Shenzhen to the south and Beijing to the north, but for hardware-adjacent businesses it has long been the real crucible. You can cross the bridge to Dongguan for injection molding by lunchtime and be back in Guangzhou for dinner. That proximity to the manufacturing belt would matter later.

EHang was founded in 2014, initially with a very different business model than the one the company has today. The first product was the Ghostdrone, a consumer aerial photography quadcopter aimed at the same market that DJI was rapidly annexing. There is a version of history where EHang went head to head with DJI and simply lost. That is approximately what happened. DJI's Phantom line was already in its second generation, the company had Shenzhen's component ecosystem wrapped around it, and its unit economics were brutal for any challenger. Ghostdrone reviews in 2015 and 2016 were polite but pointed: the app was buggy, the gimbal was not as smooth as the competition, and the price was not low enough to be a true value play.

For most companies, this would have been a quiet death. You pivot to enterprise drones, or you pivot to agricultural spraying, or you are acquired by a larger player for your engineering team. Hu's response was the opposite of quiet. If EHang could not win in a market where DJI had already established dominance, then it would simply invent a new market where no one else was playing yet. And the market Hu chose, with the kind of almost reckless ambition that separates memorable founders from forgettable ones, was passenger aviation.

The EHang 184—one passenger, eight rotors, four arms—was revealed at CES 2016. The name was both literal and a little bit cheeky. The timeline from the internal decision to pivot into human-carrying autonomous flight to the CES reveal was, according to later interviews with Hu, something on the order of a year. That is an absurd cadence for an aircraft program, and the resulting vehicle was, by any honest assessment, closer to a functioning prototype than a certifiable production aircraft. Batteries were off-the-shelf lithium-polymer packs. The structure borrowed heavily from composite fabrication techniques already mature in drone racing. The flight computer was, in Hu's own framing, a scaled-up version of the redundant controllers EHang had built for consumer drones.

What the 184 had, and what almost no other aerial vehicle in the world had in 2016, was a coherent commitment to full autonomy. There was no pilot. There was no fallback stick. There was a tablet, a vertical take-off phase, a cruise phase, and a vertical landing phase. Everything else was software. That was the bet. And in retrospect, it was the single most consequential strategic decision in the company's history, because it defined the regulatory path, the R&D budget, the competitive positioning, and ultimately the moat that EHang would spend the next decade building.

III. The Regulatory Moat: The CAAC Partnership

The usual way to tell the eVTOL regulatory story in the West is to focus on the FAA's Part 23 framework, the subsequent G-1 issue papers, and the slow, painful, deeply bureaucratic dance that companies like Joby Aviation and Archer Aviation have been performing since roughly 2019. Joby, founded in 2009 and publicly listed via SPAC in 2021, has for years been telling investors that its type certification is months away; the goalposts have moved enough times that watching them has become its own spectator sport. Archer, which went public in 2021 as well, has been running a parallel version of the same race. Both companies have chosen piloted architectures, partly because the FAA's existing rulebooks have a very clear concept of what a pilot is, and partly because the insurance and public-acceptance math, in their view, required a human in the cockpit for the first generation.

EHang looked at this landscape, in or around 2018, and chose the exact opposite path. There would be no pilot. The aircraft would be certified as an unmanned aerial vehicle with passenger-carrying capability, under a regulatory framework that, at the time EHang started pushing for it, did not actually exist in any aviation authority in the world.

The negotiating partner was the Civil Aviation Administration of China, the CAAC. In the abstract, asking a national aviation regulator to invent a new certification category for your specific product is the kind of ask that usually ends a company's credibility. But the CAAC, under pressure from Beijing's broader industrial policy agenda, was genuinely looking for a demonstration case. China's "low-altitude economy" concept, which would later be elevated to a national strategic priority in 2024, was already being discussed internally as a potential growth vector. The CAAC needed a company willing to be the test case. EHang needed a regulator willing to build the rulebook in parallel with the product.

The process that followed is not documented in public fidelity, but the shape is clear from the certification record. The CAAC issued a Special Conditions framework for the EH216-S in early 2022. This was, effectively, a bespoke airworthiness standard written specifically for an autonomous, pilotless, multi-rotor passenger aircraft. Then came the testing campaign, which EHang later disclosed involved more than 500 discrete test items across structural, environmental, electromagnetic, software, and operational categories. The Type Certificate arrived on October 13, 2023, and was the first of its kind globally. The Standard Airworthiness Certificate, which allows a specific production unit to fly commercially, followed in December 2023. The Production Certificate, which allows mass manufacturing under an approved quality system, came through on April 7, 2024. And the Operator Certificate, which allows commercial air taxi operations in designated airspace, was granted to EHang's subsidiaries in Hefei and Guangzhou in March 2025.

Each of these is, in isolation, a meaningful regulatory document. Together, they represent something closer to a category-defining moat. A new entrant wanting to replicate this cannot simply copy EHang's aircraft and file paperwork. The CAAC's Special Conditions were written specifically against the architectural choices in the EH216-S—the eight-rotor configuration, the redundant flight control architecture, the specific battery chemistry, the ground control station design, the communication links. A competitor with a different architecture would need its own Special Conditions negotiation, which is a multi-year process. And meanwhile, EHang continues to accumulate flight hours and incident-free operations, which continually reinforce the regulator's comfort with the specific design.

This is what strategists call co-created regulation, and it is one of the most durable competitive advantages in existence when it works. The frame to keep in mind is that EHang has not merely received a permit. It has become, in the specific domain of autonomous passenger eVTOL, the national champion by default. When Beijing launched the formal Low-Altitude Economy policy initiative in 2024, and when Premier Li Qiang's government work report in March 2024 explicitly named the low-altitude economy as a strategic emerging industry, there was only one company in China with a certified product to anchor that policy. For an investor, this is the thing to really sit with, because it explains why a company with revenues still measured in the low hundreds of millions of renminbi commands a market capitalization that makes it one of the more expensive industrial stocks on NASDAQ: the market is not pricing the current P&L, it is pricing the option value of being the anointed infrastructure provider for a category that Beijing has declared strategic.

Which leads, naturally, to the question of what exactly the company sells today, and how much of the current revenue base looks like hype versus genuine operating business.

IV. Hidden Businesses & Segment Dynamics

The temptation when discussing EHang is to talk only about the air taxi. It is the photogenic product. It is the product that makes investors dream in CNBC-ready sound bites about the Jetsons becoming real. But the actual revenue mix of the company over the past several years tells a more complicated and, in some ways, more interesting story.

The core product, the one that grounds the entire franchise, is the EH216-S. This is the air mobility segment, and it is the direct descendant of the 184 prototype from 2016. Two seats, 16 rotors arranged in a counter-rotating coaxial configuration on eight arms, roughly 30 kilometers of usable range, cruise speed around 100 kilometers per hour, and a maximum payload around 220 kilograms. The 216-S is not a regional aircraft and it was never designed to be one. It is designed for short urban hops—tourism routes, point-to-point inner-city shuttles, scenic area flights. Think of it as the vehicle that proves the category, not the vehicle that will eventually own it. List price for the 216-S has been disclosed at roughly 2.39 million yuan per unit for commercial deliveries, though actual ASPs vary based on configuration and volume terms with municipal customers.

The second business line, and the one that tends to get underweighted in analyst coverage, is aerial media—specifically, drone light shows. These are the massive synchronized drone swarms that have become a staple of Chinese civic celebrations, Olympic opening ceremonies, tourism events, and increasingly corporate branding activations worldwide. EHang is one of the global leaders in this market, competing primarily against Shenzhen-based players like Damoda and High Great. A single light show can involve hundreds to low thousands of drones flying in precise formation, rendering three-dimensional logos and animations across a city skyline. The drones themselves are relatively low-margin commodity hardware, but the software stack—the swarm choreography engine, the real-time collision avoidance, the synchronized telemetry—is genuine intellectual property. More interestingly from a strategic perspective, every large-scale light show is effectively a live-fire test of EHang's swarm software, its communication protocols, and its operational procedures in uncontrolled outdoor environments. The aerial media business is, in this sense, a training ground that happens to be profitable.

The third segment, often overlooked, is smart city management. The EH216-F is a variant of the core airframe adapted for high-rise firefighting, capable of delivering foam or water at altitudes that traditional fire trucks cannot reach. There are also inspection variants for forest monitoring, power line surveillance, and agricultural applications. These products sell in lower volumes than the passenger aircraft but they are meaningful both because they diversify the revenue base and because they embed EHang hardware into municipal procurement cycles. Once a fire department has trained on an EH216-F, the switching costs to a competitor's platform are non-trivial.

The fourth and most forward-looking initiative is the VT-30. This is a completely different aircraft from the 216 family. It is a lift-plus-cruise configuration, meaning it has rotors for vertical take-off and landing and separate forward-thrust propulsion with fixed wings for horizontal cruise. The target design parameters were disclosed as approximately 300 kilometers of range and a top speed around 200 kilometers per hour, which moves the product out of the intra-city hop category and into genuine inter-city point-to-point transport. The VT-30 has been under development since 2021 and was still in the certification process as of early 2026, with EHang targeting CAAC Type Certification in the latter part of this decade. If the 216-S is the iPhone 1, the VT-30 is the iPhone 4—the version where the product category becomes genuinely useful for everyday consumers rather than a novelty for enthusiasts.

The way to think about the segment mix, for investors trying to build a mental model, is this: air mobility is the optionality, aerial media is the cash flow stabilizer, smart city is the government account penetration, and the VT-30 is the long-duration call option that justifies the valuation multiple. That framing also explains why EHang's revenue has been volatile quarter to quarter. When municipal deliveries are recognized in lumpy batches, it dominates the income statement. When aerial media wins a major festival contract, it dominates. And underneath all of it, the R&D line keeps marching forward, because the company that wins this category in 2035 will be the one that has the broadest certified product family, not the one that optimized for 2026 quarterly earnings.

V. Management Analysis: The Visionary and the Operators

Every founder story has a mythology, and Huazhi Hu's mythology is particularly well-curated. He is almost always photographed in a crisp dark blazer, rarely smiles in official portraits, and in interviews tends to speak in careful, deliberate sentences that translate cleanly from Mandarin into English. The persona he projects is something between an aerospace engineer and a state-enterprise executive—a contrast to the slightly more manic energy that characterized Chinese consumer tech founders of his generation like Lei Jun at Xiaomi or William Wang at iFlytek.

Hu's shareholding structure is the kind of thing that matters enormously to long-term investors and is often glossed over in sell-side notes. Through his Class B super-voting shares and related holdings, Hu controls the majority of the voting power at EHang, even while his economic ownership is a smaller percentage. The practical effect is that the company is, and will remain for the foreseeable future, founder-led in a strict sense. Activist campaigns, hostile takeovers, and near-term-oriented shareholder pressure are all structurally impossible. For a business whose fundamental value proposition is a multi-decade infrastructure bet tied to a national industrial policy, this governance structure is a feature, not a bug. The flip side, which diligent investors should underwrite honestly, is that the founder's judgment is the single largest concentrated risk in the capital structure. If Hu is wrong about autonomy, or wrong about the long-range inter-city segment, or wrong about the pace of Chinese low-altitude buildout, there is no internal counterweight that will course-correct.

The incentive architecture beneath Hu tells you something about how the company actually runs. Public filings describe an equity compensation structure that is heavily weighted toward certification milestones and flight-hour targets rather than traditional financial metrics like revenue or EBITDA. That is a rare and telling design choice. It implies that the company is still in the mode of a capital-intensive science project rather than an operating business to be optimized quarter over quarter. An executive at EHang who delivered record revenue but slipped a CAAC certification timeline would, under the current framework, be considered to have failed. That is the correct framing for this stage of the business, but it does require investors to accept that the traditional tools of management scrutiny—return on invested capital, free cash flow yield, incremental margin expansion—are not yet the right lens.

The second key figure in the current management constellation is Conor Yang, the long-serving Chief Financial Officer who joined EHang in 2019 and has been the public face of the company in Western capital markets. Yang's background in investment banking and his comfort with English-language investor audiences have made him, effectively, the translator of Hu's technical vision into the language of public markets. The third figure, and the one most operationally relevant at the current stage of the company, is the Chief Operating Officer responsible for the transition from prototype-scale assembly in Guangzhou to industrial-scale production in the Yunfu factory. The move to Yunfu, a smaller city in Guangdong province, was driven by a combination of municipal incentives, available industrial land, and proximity to the supplier ecosystem—the kind of location choice that reveals how Chinese industrial policy actually works on the ground.

The deeper cultural shift happening inside EHang, and one that rarely gets discussed in quarterly reports, is the transition from a scrappy consumer-drone startup mindset to a certified aircraft OEM mindset. These are not the same kind of company. A consumer drone company iterates fast, ships firmware updates over the air, and treats user feedback as the primary quality signal. A certified aircraft OEM documents everything, change-controls everything, maintains a quality management system that passes audit by the aviation regulator, and treats deviation from specification as a compliance event rather than a feature. The cultural muscle memory required for these two modes is almost opposite. Watching EHang build that muscle, hire the right people from Chinese aerospace state-owned enterprises, and retire the cowboy instincts of its earliest engineers has been a quiet, invisible transformation—one of the things most likely to determine whether the company can scale safely or whether an eventual incident will set the category back.

The transition matters because the category does not get a second chance at first impressions. One fatal incident involving a certified EH216-S would not only affect EHang's stock; it would affect the entire global narrative around autonomous passenger flight. Hu understands this, which is why the pace of commercial deployment has been noticeably conservative even after certification—tourism routes over controlled scenic areas first, then short point-to-point urban routes in designated low-altitude zones, with full urban mobility operations still some years away.

VI. M&A, Capital Deployment, & The "Asset-Light" Model

If you line up the balance sheets of EHang and its Western peers side by side, the most striking number is not revenue or gross margin. It is cumulative capital raised and R&D spent. Joby Aviation, by the time of its SPAC listing in August 2021, had raised roughly 1.6 billion dollars; subsequent raises and a Toyota partnership have pushed total committed capital well above 2 billion dollars. Archer Aviation has raised, by similar reckoning, over 1 billion dollars including its SPAC proceeds in 2021. Lilium, the German jet-powered eVTOL company that eventually filed for insolvency protection in late 2024, burned through more than 1.5 billion dollars of committed capital before running out of runway.

EHang, across its entire corporate history since 2014, has raised a cumulative amount that is a small fraction of any of those figures. The initial venture rounds from GGV Capital, GP Capital, and ZhenFund, the Series B and C rounds, the pre-IPO GreenTree capital, and eventually the December 2019 NASDAQ IPO at 12.50 dollars per share together brought in somewhere in the range of a few hundred million dollars of cumulative equity capital. A subsequent convertible notes issuance and various strategic investments have added more, but the total capital deployed to build a certified passenger aircraft company is shockingly small by Western standards.

How is this possible? The answer is a combination of deliberate strategic choices and Chinese cost structure realities. On the strategic side, EHang has pursued what is best described as an asset-light OEM model. The company owns the flight control system, the overall airframe design, the swarm management software, and the certification dossier. It partners for almost everything else. Battery cells are sourced from Chinese lithium-ion leaders rather than developed in-house. Motors and electronic speed controllers come from established drone component manufacturers. Composite structures are produced by contract manufacturers specializing in aerospace-grade carbon fiber. Final assembly happens in EHang's Yunfu facility, but the facility is modest compared to the multi-hundred-million-dollar factories that Joby and Archer have built in the United States.

The philosophical framing here is that EHang decided very early that it was a flight systems company, not a vertically integrated aircraft company. The analogy is not Boeing or Airbus. The analogy is closer to Apple in the early iPhone era, where the value is concentrated in the integration layer, the software stack, and the regulatory relationships, while the commodity component supply chain is orchestrated through trusted partners. Whether this asset-light model holds as the company scales to thousands of units per year is one of the genuinely open strategic questions, because certified aerospace supply chains tend to gradually force more vertical integration as production volumes grow and single-source supplier risk becomes intolerable.

On the M&A and partnership side, EHang's deal-making has been characterized more by small strategic investments than by transformative acquisitions. The partnership with Incepto Capital Management, a Japanese investment firm, brought capital and Japanese market access. Joint ventures with the Hefei municipal government and with Wuhan's high-tech development zone brought not only capital but also committed order books for initial fleet deliveries and preferred access to designated low-altitude test corridors. These are not glamorous deals in the way that Joby's Toyota partnership or Archer's Stellantis tie-up are glamorous, but they are arguably better structured for the actual business EHang is trying to build, because they lock in operating demand rather than just supplying capital.

A question sometimes raised by skeptical analysts is whether EHang's low R&D spend reflects prudence or under-investment. The honest answer is that it probably reflects both. A certified aircraft program in China, with Chinese engineering salaries and Chinese test pilot costs, is genuinely cheaper to execute than the equivalent program in California. But at some point, the true test of whether EHang has built an efficient program or a thin program is the operational performance of the fleet over tens of thousands of cumulative flight hours. The 500-plus test items in the CAAC certification campaign are a strong signal. The absence of a fatal incident across years of test flights and early commercial operations is a stronger signal. But the ultimate verdict requires more operational data than currently exists. Which brings the conversation directly to the question of competitive moats and whether the advantages EHang has accumulated are truly durable.

VII. The 7 Powers & Porter's Five Forces

Hamilton Helmer's 7 Powers framework, which has become the de facto strategic analysis lens for serious long-term investors, maps onto EHang with unusual clarity. Three of the seven powers apply with real force, one applies partially, and the remaining three are either absent or aspirational.

The first and most distinctive power at work is counter-positioning. EHang's decision to pursue full autonomy while Joby, Archer, Lilium, Volocopter, and Vertical Aerospace all pursued piloted configurations was, at the time it was made around 2017 and 2018, considered eccentric at best and reckless at worst. It was a classic counter-positioning move: the dominant incumbents in the emerging eVTOL space could not easily follow without cannibalizing their existing certification campaigns, their existing investor narratives around pilot-based operations, and their existing FAA relationships. Even today, with the benefit of hindsight, a Western competitor looking at the Chinese autonomous regulatory framework cannot simply pivot; the FAA does not yet have an equivalent framework, the public acceptance work has not been done, and the company's own certification program is committed to piloted operations. EHang is alone in its category not because competitors have not noticed, but because competitors structurally cannot follow.

The second and most mechanical power is cornered resource. The Type Certificate, the Production Certificate, the Standard Airworthiness Certificate, and the Operator Certificates together constitute a cornered resource in the sense that Helmer defines it: a preferential access to a coveted asset on attractive terms. You cannot buy these certificates. You cannot copy them. You cannot work around them. You have to earn them through a multi-year testing campaign that is expensive, technically demanding, and subject to regulatory discretion. And the CAAC, having been burned by approval dynamics in other industries, is under no pressure to accelerate approvals for EHang's competitors. A new entrant starting today would be several years behind even under the most generous assumptions.

The third power is governmental power, which overlaps with but is distinct from cornered resource. Beijing has formally designated the low-altitude economy as a strategic emerging industry. The Central Economic Work Conference of December 2023 named it explicitly. The 2024 Government Work Report named it explicitly. The 14th Five-Year Plan for Civil Aviation Development incorporated eVTOL as a development priority. When a national government decides that a category is strategic, the ecosystem that forms around the chosen champion—in this case, EHang—becomes substantially easier to build. Municipalities compete to host demonstration zones. State-owned enterprises become customers. Insurance frameworks get created. Air traffic management protocols get rewritten. All of this accrues disproportionately to the only company with a certified product.

Branding and network effects, two of the remaining 7 Powers, are partially present but not yet load-bearing. The EHang brand has genuine recognition in Chinese aerial media circles and is becoming recognized globally, but it does not yet command premium pricing in the way that a true brand power would imply. Network effects may eventually emerge around EHang's urban air mobility operating system and the air traffic management infrastructure that connects cities, but those effects are potential rather than actual in 2026.

Turning to Porter's Five Forces, the picture is equally unusual. The threat of new entrants is extremely low, for the reasons just described around regulatory moats and the cumulative decade of flight data. The bargaining power of buyers is, counterintuitively, not as high as it might first appear; while municipal governments and tourism operators are relatively concentrated buyers, they do not have competitive alternatives, because there is only one certified autonomous passenger eVTOL on the market. The bargaining power of suppliers is moderate—battery cells and composite structures are commodified, but certain avionics components have a narrower supply base. The threat of substitutes is real in the long run, once Western piloted eVTOLs reach certification, though the piloted versus autonomous distinction means they are not direct substitutes so much as adjacent products. Competitive rivalry within the specific segment of certified autonomous passenger eVTOL is, today, essentially zero, which is the strange and telling fact that investors keep returning to.

The frame that best captures this is that EHang has built, through patience and counter-positioning, a temporary monopoly in a category that Beijing has declared strategically important. The word "temporary" matters, because no monopoly lasts forever, and Chinese industrial champions have a history of being joined rapidly by domestic competitors once a category is proven. But "temporary" can still be measured in years, and the value captured during the window is often disproportionate to the eventual equilibrium state.

VIII. The Playbook: Lessons for Founders

Every company worth a long-form treatment leaves behind a playbook, and EHang's is unusually legible because the strategic choices are few but each one is consequential. Three lessons in particular stand out for founders building in regulated, frontier categories.

The first lesson is regulation as a product. Most Silicon Valley founders, trained in the Uber playbook of the 2010s, think about regulation as an obstacle to be disrupted, worked around, or petitioned against after the product is already deployed. That approach works in categories where consumer demand can create political pressure faster than regulators can mobilize. It does not work in aviation, where a single incident can justify years of restrictive rule-making. EHang chose instead to treat the regulator as a co-creator. The company's engineering team spent as much time in Beijing briefing CAAC officials on the technical details of the flight control redundancy architecture as it spent in the factory building prototypes. The resulting Special Conditions framework was not imposed on EHang; it was co-developed with EHang. That is a wildly different posture from the adversarial stance that Joby and Archer have periodically taken with the FAA, and it explains a great deal about why EHang is where it is today.

The second lesson is the minimum viable aircraft. There is a strong temptation in aerospace to go immediately for the product that actually solves the user's problem, which in the case of urban air mobility is an inter-city, long-range, high-speed, efficient aircraft capable of carrying multiple passengers with compelling economics. That is the VT-30 target. But starting with the VT-30 would have been a disaster, because the certification pathway for a lift-plus-cruise aircraft with fixed wings is substantially more complex than the pathway for a pure multi-rotor design. By starting with the 216-S, which is essentially a scaled-up drone architecture, EHang was able to concentrate its regulatory negotiation on the minimum possible set of novel elements: autonomy, passenger carriage, and multi-rotor airworthiness. Everything else about the aircraft was as boring as possible. This is the aerospace equivalent of shipping the MVP. The VT-30 can now follow, with most of the hardest regulatory work already done and the CAAC already comfortable with EHang as an operator.

The third lesson is the software-defined aircraft. Traditional aviation has always treated the airframe as the primary product and the software as a component of the airframe. EHang inverted this, treating the flight control system and the operating software as the primary product and the airframe as the package that wraps around it. The practical consequence is that the 216-S and the VT-30 share a surprising amount of software stack, even though the airframes are completely different. The development cost of the second aircraft is therefore a fraction of what it would have been if each aircraft were treated as a fresh clean-sheet program. This is the same insight that Tesla applied to the Model 3 after the Model S, that Apple applied to the iPad after the iPhone, and that SpaceX has applied to Starship after Falcon. Software-defined hardware compounds its R&D investments across product generations in a way that traditional hardware companies simply cannot match.

There is a fourth, softer lesson worth naming, which is about founder stubbornness. Every decision that made EHang distinctive was, at the moment it was made, unpopular. Full autonomy in 2016 was considered reckless. Partnering with the CAAC instead of trying to enter the U.S. market first was considered narrow. Keeping R&D spend low when every competitor was raising billions was considered under-investment. In each case, Hu held the line. That kind of conviction in the face of consensus disagreement is rare and is, arguably, the single trait that distinguishes category-defining founders from merely successful ones. It is also a trait that is impossible to evaluate in advance, because it looks exactly like stubbornness that happens to be wrong until the moment it turns out to be stubbornness that happened to be right.

IX. The Bull vs. Bear Case

The bull case for EHang, in its most expansive form, goes roughly as follows. China has declared the low-altitude economy a strategic industry and set an explicit target of a trillion-yuan market size by the early 2030s. EHang is the only company with a full set of CAAC certifications for autonomous passenger flight, meaning that for a meaningful portion of that market, competitive alternatives simply do not exist in the near term. The company's asset-light, software-defined architecture allows it to scale production with substantially less capital than Western peers. The VT-30 long-range platform, once certified, unlocks inter-city transport economics that are multiples more attractive than the current short-hop tourism use cases. International expansion into Southeast Asia, the Middle East, and Latin America, where regulatory frameworks are more willing to follow CAAC precedent than FAA precedent, provides additional optionality. And the eventual transition from selling aircraft at low volumes to operating fleets at high volumes—the same transition that allowed the ride-hailing industry to expand its margin profile dramatically—represents a significant structural margin expansion opportunity. Applied to the current revenue base, even conservative assumptions about penetration rates produce valuation mathematics that justify the current multiple on an out-year basis.

The bear case, which deserves equal weight in a serious investment process, is built on several legitimate concerns. The first is geopolitical friction. As U.S.-China tensions continue to evolve, the ability of Chinese aerospace companies to operate in Western markets has been progressively constrained. EHang has been the subject of various regulatory inquiries in the United States, including a short-seller report from Wolfpack Research in February 2021 that raised questions about the company's disclosures and customer relationships, and SEC-related disclosure obligations that remain open questions for any U.S.-listed Chinese issuer. The ongoing HFCAA audit requirements add another layer of uncertainty. These are not existential risks, but they do compress the addressable market meaningfully and complicate the international expansion narrative.

The second bear argument is technical. Battery energy density remains the binding constraint on eVTOL range and payload. The 216-S's 30-kilometer practical range is useful for tourism hops but insufficient for genuine urban commuting. The VT-30's target of 300 kilometers depends on battery chemistry advances that may or may not arrive on the assumed timeline. If battery improvements stagnate, the entire category may end up stuck in a narrower use case than current projections assume.

The third bear argument is about public acceptance. Autonomous passenger flight is a genuinely novel proposition. Even in China, where public tolerance for technological novelty tends to be higher than in the West, it is not obvious that sustained consumer demand for pilotless flights will materialize quickly enough to justify aggressive fleet deployment. A single high-profile incident, particularly early in the commercial deployment phase, could set the category back by years.

The fourth bear argument is about competition. Once the CAAC has established a precedent with EHang, the regulatory pathway for Chinese competitors becomes meaningfully clearer. AutoFlight, Xpeng AeroHT, TCab Tech, and several other well-capitalized Chinese entrants are already in various stages of development. The first-mover advantage is real but not permanent, and Chinese industrial categories historically tend toward fragmentation rather than sustained monopoly.

For investors trying to track the company's ongoing performance, three KPIs stand out as the most important. The first is unit deliveries of the EH216-S family on a trailing basis, because this is the most direct signal of whether the certified product is translating into actual commercial adoption. The second is cumulative fleet flight hours without a reportable incident, because this is the operational safety record that underpins the regulatory moat and the category's broader social license. The third is the VT-30 certification milestones, because this is the single largest swing factor for long-term valuation and represents the transition from a niche tourism aircraft provider to a genuine urban-and-intercity mobility platform. Everything else—quarterly revenue, gross margin, aerial media mix—is secondary to these three.

A second-layer diligence note worth flagging: the auditor situation for U.S.-listed Chinese issuers has been in flux since the HFCAA amendments, and EHang's audit arrangements should be monitored alongside the broader cohort. Insider transactions and share issuance activity should also be watched, because any meaningful change in Hu's equity position would be a material governance signal given the company's founder-led structure.

X. Epilogue & Final Reflections

In the spring of 2026, the Yunfu factory is running. Commercial flights are operating in Hefei's designated air taxi corridor and in Guangzhou's Baiyun district. The EH216-S fleet has accumulated tens of thousands of autonomous flight hours, both in testing and in early commercial service. The first international deliveries have reached customers in the United Arab Emirates, Indonesia, and Brazil. The VT-30 is in flight testing. The aerial media business continues to generate stable cash flow that cushions the lumpy aircraft delivery revenue. The stock has been volatile, swinging on every certification update and every short-seller report, but the underlying operational trajectory has been one of steady, if unspectacular, compounding.

The question the industry will be asking over the next five years is whether EHang turns out to be the Tesla of the sky—an early, unlikely, vertically integrated company that actually delivered on the promise that everyone else was merely discussing—or whether it turns out to be something more modest and perhaps more tragic, a pioneer that opened a category for others to eventually dominate. The honest answer is that it is almost certainly too early to know. The base rate for category-creating companies is that they get disrupted, either by scaled competitors who show up later with better unit economics or by technological pivots that invalidate the original bet. But the base rate also includes cases—Tesla being the obvious example, but also cases like Illumina in genomics or TSMC in foundries—where the pioneer builds a structural advantage that compounds faster than competitors can erode it.

What is clear is that Huazhi Hu has done something that very few founders in the history of aerospace have managed to do. He has taken a product category that did not exist, negotiated a regulatory framework that did not exist to approve it, delivered a certified aircraft under that framework, and begun commercial operations—all on a capital budget that would barely cover the marketing spend of a single Western competitor. That is not a small achievement. Whether it turns out to be a generationally important one depends on what happens next, on execution, on geopolitics, on battery chemistry, and on the slow accumulation of the kind of operational trust that only comes with time.

The image to hold in mind, as the story stands at this moment, is the one Hu himself returns to in interviews. He was asked, in a 2019 conversation with a Chinese aviation magazine, why he had been so insistent on removing the pilot from the aircraft when every other company in the category had chosen to keep one. His answer was characteristically unadorned. If you put a steering wheel in a self-driving car, he said, then what you have built is still fundamentally a car with a driver. If you want to build something genuinely new, you have to refuse the option of the fallback. You have to commit. He refused to put a steering wheel in his aircraft. Whether history vindicates that refusal or not, it is the decision that defines the company.

XI. Outro & Further Reading

The key primary source documents for anyone wanting to go deeper on EHang include the CAAC's Type Certification announcement from October 2023, which contains the substantive Special Conditions framework and is available in Chinese from the CAAC's official website. The company's annual reports on Form 20-F filed with the SEC provide the most detailed financial and operational disclosures, including the R&D pipeline descriptions, segment reporting, and risk factor discussions. EHang's Urban Air Mobility white paper, published in 2020 and updated periodically, lays out the company's own framing of the market and its strategic positioning. Historical footage of the EHang 184 unveiling at CES 2016 is available in various archived news segments and remains a useful artifact for appreciating how improbable the current trajectory once appeared.

For broader context on the Chinese low-altitude economy policy environment, the 2024 State Council work reports and the 14th Five-Year Plan's civil aviation chapter provide the official framing. Research reports from Chinese brokerages including CICC and Huatai Securities have been the most informative third-party sources on the industrial policy dimension, though they should be read alongside skeptical Western analysis to get a balanced view. The Wolfpack Research short report from February 2021 remains worth reading specifically because understanding the bear case articulated by sophisticated short sellers is a discipline that tends to strengthen any investment thesis. And for the broader eVTOL landscape comparison, Joby Aviation's, Archer Aviation's, and the now-insolvent Lilium's public disclosures offer instructive contrasts in strategy, capital allocation, and regulatory approach.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube