EastGroup Properties: The Quiet Sunbelt Compounder

How a Sleepy Mississippi REIT Became the Dominant Force in Last-Mile Industrial Real Estate

I. Introduction: The $9 Billion Company You've Never Heard Of

On a crisp October morning in 2025, CEO Marshall Loeb stepped up to the podium for EastGroup Properties' third-quarter earnings call and delivered a message that encapsulated decades of disciplined strategy: "I'm proud of the quarterly results the team created this quarter as well as year-to-date. These results are a testament to our team, our properties and our markets, in that order."

The numbers backed him up. EastGroup's operating portfolio was 96.7% leased, with rental rates on new and renewal leases increasing an average of 35.9% on a straight-line basis. The company declared its 183rd consecutive quarterly dividend—raised 10.7% to $1.55 per share. Not bad for a company that once operated "in near obscurity" from Jackson, Mississippi.

EastGroup Properties, Inc. (NYSE: EGP), a member of the S&P Mid-Cap 400 and Russell 2000 Indexes, is a self-administered equity real estate investment trust focused on the development, acquisition and operation of industrial properties in high-growth markets throughout the United States with an emphasis in the states of Texas, Florida, California, Arizona and North Carolina.

But what makes EastGroup remarkable isn't just its current success—it's the journey. How did a company that started investing in northeastern real estate in 1969, nearly collapsed during the REIT crash of the mid-1970s, and languished for two decades suddenly become the quiet compounder dominating Sunbelt industrial real estate?

The Company's portfolio, including development projects and value-add acquisitions in lease-up and under construction, currently includes approximately 63.9 million square feet. That's up from roughly 16 million square feet at the turn of the millennium, and less than 10 million square feet in the early 1990s. The growth didn't come from aggressive leverage or high-risk bets. It came from what Piper Sandler analyst Alex Goldfarb calls "Their secret sauce is down pat."

This is the story of that secret sauce—a blend of geographic foresight, development discipline, tenant diversification, and a management philosophy that prioritizes "not blowing up" over spectacular short-term gains. Along the way, EastGroup became a case study in how small, well-run REITs can outperform their larger peers by picking the right battles in the right markets at the right time.

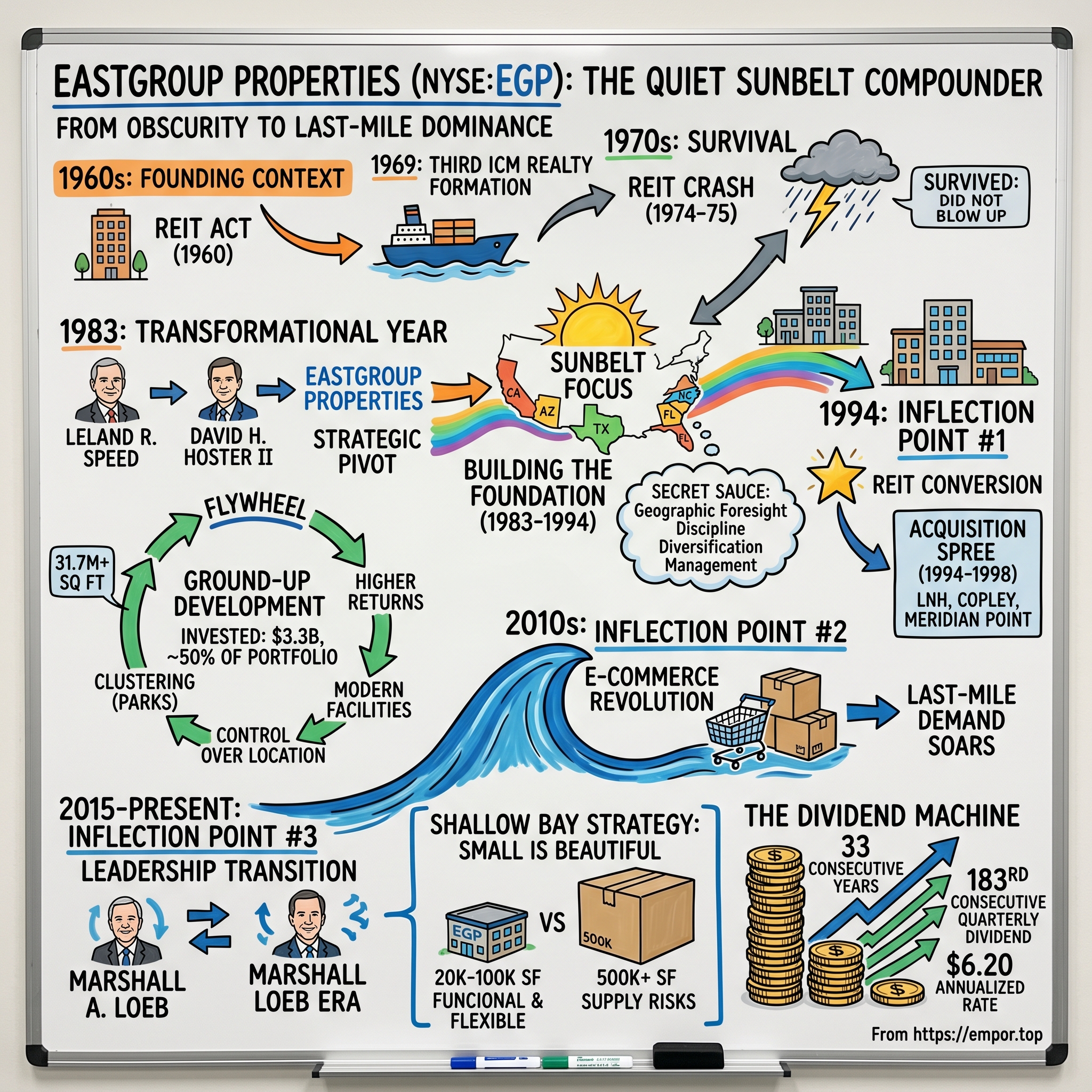

II. The REIT Revolution & Founding Context (1960s–1969)

To understand EastGroup, we must first understand the vehicle that made it possible. U.S. REITs were established by Congress in 1960 to give all investors, especially small investors, access to income-producing real estate. Since then, the U.S. REIT approach has flourished and served as the model for around 40 countries around the world.

REITs are created when President Dwight D. Eisenhower signs the REIT Act title law contained in the Cigar Excise Tax Extension of 1960. The legislation was revolutionary in its simplicity: allow ordinary investors to pool capital and invest in diversified portfolios of income-producing real estate, just as mutual funds allowed them to invest in diversified portfolios of stocks.

The birth of EastGroup followed not long after REITs were encouraged to be formed by the Real Estate Investment Trust Act of 1960. The law sought to stimulate investment in real estate by granting special tax concessions to companies, trusts, or associations that qualified as REITs. The qualification standards were numerous, but as a general rule REITs were exempt from federal income taxation provided they distributed nearly all of their taxable income as dividends to shareholders and held at least 75 percent of their assets in real property.

Against this backdrop, EastGroup's predecessor was formed in July 1969 as Third ICM Realty, commencing operations several months later in December 1969. The company was a creature of its time—part of a wave of new REITs capitalizing on the favorable tax structure Congress had created nearly a decade earlier.

Around the time of their creation in 1960, the first REITs primarily consisted of mortgage companies. The industry expanded significantly in the late 1960s and early 1970s.

ICM Realty invested in real estate projects in the northeastern United States, developing its portfolio in markets far removed from the company's geographic focus in later years. The company completed its initial public offering in 1971, the same year it dropped "Third" from its corporate title.

There was nothing special about ICM Realty at this stage. It was one of dozens of small REITs formed in the late 1960s, riding the wave of enthusiasm for the new investment vehicle. Most of its peers would not survive the decade.

III. Surviving the REIT Crash & Two Decades of Obscurity (1970s–1982)

The early 1970s brought a reckoning for the young REIT industry. What had seemed like a foolproof formula—raise capital from public markets, invest in real estate development—turned into a disaster.

The industry, particularly those REITs involved in development projects, suffered as it entered the mid-1970s, experiencing a general downturn that was exacerbated by recessive economic conditions between 1974 and 1975. Numerous real estate projects failed during the period, prompting a series of amendments to the provisions governing REITs.

The combination of recession, rising interest rates, and over-leveraged real estate projects proved fatal for many REITs. Construction lenders called in loans, development projects stood half-finished, and investors who had poured money into the sector saw their holdings collapse.

ICM Realty withstood the downturn, enduring the grim conditions that beset the industry early in the company's development. ICM Realty survived, giving it a chance to some day make its mark on the national scene—a day, as it happened, that was years away.

The lesson of survival is often underappreciated in business narratives. We celebrate the bold bets, the aggressive growth stories, the companies that scaled rapidly. But EastGroup's early history teaches a different lesson: sometimes the most important thing a company does is simply not blow up.

For more than two decades, ICM Realty operated in near obscurity. The company wasn't growing dramatically. It wasn't making headlines. It was simply existing—managing its small portfolio, paying dividends to shareholders, and waiting for its moment.

That moment came in 1983.

IV. The 1983 Transformation: New Management, New Name, New Strategy

The company's path towards prominence did not begin until it gained the management team that would lead it into the 21st century. In 1983, the year the company adopted the name EastGroup Properties, the two most influential individuals in the company's history arrived.

Leland R. Speed, who earned a B.S. in industrial management from Georgia Institute of Technology and an M.B.A. from Harvard Business School, became EastGroup's chief strategist. Before joining the company, Speed was involved in the general securities and real estate development business.

Speed was a product of Jackson, Mississippi—the son of Leland Speed Sr., a former mayor of Jackson. After graduate school, Leland moved back to Jackson, joining his father, former mayor of Jackson, Leland Speed Sr. (aka "Pappy"), in the securities business. The two Speeds also worked in the real estate business, developing the Eastover subdivision in northeast Jackson.

The name "EastGroup" itself appears to be derived from the Eastover subdivision that Speed had helped develop—a connection between the family's local real estate roots and the company's new national ambitions.

In 1983, Speed was joined by David H. Hoster II, who received a B.A. in history from Princeton University and an M.B.A. from Stanford University. Before joining EastGroup, Hoster spent eight years in Washington, D.C., serving as president of Riviere Realty Trust.

Speed and Hoster brought complementary skills: Speed the vision and local relationships, Hoster the operational rigor and capital markets experience. Together, they would transform a sleepy northeastern REIT into a Sunbelt industrial powerhouse.

EastGroup, as led by Speed and Hoster, focused on acquiring and developing industrial properties, particularly distribution centers located near transportation hubs. EastGroup positioned itself as an industrial REIT with a particular focus on distribution centers near transportation hubs, although the company occasionally acquired office space that did not meet its principal strategic criteria. Speed applied EastGroup's strategy to the Sunbelt, concentrating much of his efforts in Florida, Texas, Arizona, and California.

The strategic pivot to the Sunbelt was prescient. In 1983, the conventional wisdom favored established markets in the Northeast and Midwest—the industrial heartland of America. Speed saw something different. He recognized that demographic shifts, business-friendly state policies, lower taxes, and a more favorable cost structure would drive economic growth to the South and Southwest for decades to come.

Early concentration on the fast-growing Sunbelt region proved visionary. Focusing exclusively on industrial properties, primarily distribution facilities, in states like Florida, Texas, Arizona, and California positioned the company to capitalize on demographic shifts and supply chain evolution. This strategic clarity has been a key driver of its success.

The investment thesis was simple: go where the people are going, where businesses want to be, and where the economics of real estate development favor patient capital over speculative froth.

V. Building the Foundation: Slow and Steady Growth (1983–1994)

For more than a decade after Speed and Hoster arrived, EastGroup grew at a measured pace. The company's revenue volume edged passed $13 million in 1992, beginning a measured march upwards.

With Speed in the lead and Hoster at his side, EastGroup Properties gradually developed into a REIT of note. It took more than a decade after the pair's arrival before the company began its rise, however.

This patience is worth emphasizing. In an era obsessed with hockey-stick growth curves and disruptive innovation, EastGroup's founders chose a different path. They built slowly, deliberately, focusing on acquiring the right properties in the right locations rather than scaling for scale's sake.

The company's investment philosophy crystallized during this period: "Our investment approach reflects these recurring specific themes: being where location sensitive tenants want to be; competing on location rather than rent; clustering of multi-tenant properties; distribution—not storage; focus on transportation features; submarket driven."

Each element of this philosophy addressed a specific source of risk or competitive advantage:

"Being where location-sensitive tenants want to be" meant prioritizing access to consumers, transportation networks, and labor pools. This wasn't about finding the cheapest land—it was about finding the most valuable land for the tenants who would pay premium rents.

"Competing on location rather than rent" inverted the typical landlord-tenant dynamic. Instead of winning tenants by offering below-market rents, EastGroup aimed to own properties so well-located that tenants would pay market or above-market rents to secure them.

"Clustering of multi-tenant properties" created operational efficiencies and customer stickiness. A tenant expanding from one building could easily move to an adjacent building in the same park, staying within EastGroup's portfolio rather than leaving for a competitor.

"Distribution—not storage" reflected a bet on the velocity of goods movement rather than static warehousing. Distribution centers serve customers who need quick access to inventory; storage facilities serve customers who need cheap space. The former is much more valuable.

"Focus on transportation features" and "submarket driven" together ensured that EastGroup's properties were positioned where they mattered most—near airports, highways, and intermodal facilities in specific submarkets with favorable supply-demand dynamics.

EastGroup, despite the implication in its name and its region of origin, created its identity in the southern and southwestern United States, in the region commonly referred to as the Sunbelt. The company made its mark not as a Maryland-based company but as a Jackson, Mississippi-based company, one that started to exhibit impressive growth during the 1990s.

VI. Inflection Point #1: The 1994 REIT Conversion & Acquisition Spree (1994–1998)

The mid-1990s marked EastGroup's transformation from a small regional player into a company with genuine scale and national ambitions.

The entity that became EastGroup Properties, Inc. underwent a significant transformation, converting to a Real Estate Investment Trust (REIT) structure and adopting the name EastGroup Properties, Inc. in 1994, coinciding with its initial public offering. Jackson, Mississippi served as the original base and remains the corporate headquarters today.

The REIT conversion was transformational: The 1994 decision to become a REIT was foundational. It provided a tax-efficient structure attractive to investors and aligned the company with public market standards, fueling its subsequent expansion.

With access to public capital markets, EastGroup embarked on an aggressive acquisition strategy. Growth came as Speed expanded the company's portfolio of property holdings, with sharp increases realized by acquiring other industrial REITs. Speed assumed an acquisitive posture as his company exited the mid-1990s, when EastGroup was generating roughly $30 million in revenue.

Four public REITs have been merged into or acquired by EastGroup—Eastover Corporation in 1994, LNH REIT, Inc. and Copley Properties, Inc. in 1996 and Meridian Point Realty Trust VIII in 1998.

Between 1996 and 1998, the company acquired three publicly held REITs, beginning with the May 1996 purchase of LNH REIT, Inc. LNH, with approximately $2.5 million in 1995 revenues, had $6.2 million worth of real estate properties in its portfolio.

A much larger acquisition followed the next month, when EastGroup purchased Copley Properties, Inc. in a $166 million transaction. Formed in 1985, Copley owned and operated 15 properties with more than 2.5 million square feet of leasable space, possessing more than $80 million in assets. Copley's properties, primarily located in Arizona and California, bolstered EastGroup's presence in the Sunbelt.

In June 1998, the company completed another acquisition on the scale of the Copley purchase, acquiring Meridian Trust VIII Co.

The results were dramatic: The acquisition of REITs and the expansion of the company's own portfolio through internal means greatly accelerated EastGroup's growth during the late 1990s. By the end of 1999, the company was a $74-million-in-revenues REIT, having increased its revenue volume nearly fivefold in five years.

The company maintained the intensified pace in 1999, completing 13 acquisitions in five states that added more than 1.6 million square feet of leasable space. By this point, Hoster had assumed day-to-day control over the company, becoming EastGroup's chief executive officer in September 1997. Speed presided as chairman. Under Hoster's leadership, EastGroup entered the 21st century with roughly 16 million square feet of leasable space.

The acquisition spree established a pattern that continues to this day: strategic bolt-on acquisitions in markets where EastGroup already has presence, rather than diversifying into new geographies or property types.

VII. The Development Flywheel: Building vs. Buying

One of EastGroup's most distinctive characteristics is its commitment to ground-up development. While many REITs focus primarily on acquiring existing properties, EastGroup has built roughly half of its portfolio from scratch.

EastGroup has built half of its portfolio from the ground up. It has invested $3.3 billion to develop 271 properties with 31.7 million square feet since 1996. It builds in park-like settings. This strategy drives increased returns with less risk.

Building a significant portion of its assets through its own development program became a core competency. This approach allows for the creation of modern, high-quality facilities in desirable locations, often yielding higher returns compared to acquiring existing properties and ensuring the portfolio remains state-of-the-art.

The company's development history is impressive, with 261 properties developed since 1996, representing 29.8 million square feet and $3.0 billion in investment. This development activity now accounts for approximately 50% of EastGroup's portfolio, demonstrating the success of its build-to-core strategy.

The development strategy serves multiple purposes:

Higher returns: Developing a property costs less than buying a comparable existing property at market prices. The difference—often called the "developer's margin"—flows directly to shareholders.

Modern facilities: Developed properties incorporate the latest design features, clearances, and amenities that tenants demand. Older properties require capital expenditures to remain competitive.

Control over location: By acquiring land and developing, EastGroup can target specific infill submarkets where existing inventory is scarce.

Clustering: Development allows EastGroup to create entire business parks rather than owning scattered individual buildings.

CEO Marshall Loeb explains the approach: "EastGroup's properties are more akin to attractive office parks than typical warehouse space, and instead of focusing on a handful of prominent tenants, the REIT rents to a wide variety of businesses that may need just 15,000 or so square feet. 'Our customers typically serve a local, growing metro area,' says Marshall Loeb, EastGroup's president and CEO. 'As a result, our last-mile locations are often irreplaceable as cities grow and our customer pool continues to grow and diversify.'"

The park-style approach creates a "sense of place" that differentiates EastGroup's properties from typical warehouse stock. Tenants value the landscaping, architectural consistency, and overall environment—and they pay for it.

Perhaps most importantly, the development strategy is demand-responsive rather than supply-driven. Management explicitly states that they prefer to let market demand "pull" supply rather than pushing new supply into the market: they build incrementally within parks, starting one or two buildings and adding more only as those lease up. This discipline prevents the overbuilding that has historically plagued industrial real estate.

VIII. Inflection Point #2: The E-Commerce Revolution (2010s)

If the 1994 REIT conversion was EastGroup's first major inflection point, the rise of e-commerce was its second. The company's strategy—Sunbelt-focused, last-mile oriented, multi-tenant industrial—proved almost perfectly suited to the demands of online retail.

Digital sales soared in 2020 amid the pandemic and grew by 14.6% in 2021, equating to $870.8 billion being spent online. In 2020, a record 97.5 million square feet were leased directly by e-commerce occupiers, while another 77.1 million square feet were transacted throughout 2021.

E-commerce companies had accounted for 28.2% of all industrial absorption from 2016 through 2019, and that number increased even more to approximately 40% from 2020 through 2021 as COVID-19 shifted consumer shopping patterns to more frequent online purchasing.

According to U.S. Census Bureau data, e-commerce accounted for 16 percent of U.S. retail sales in the third quarter of 2024. That's up from 6 percent a decade ago and just 2 percent 20 years earlier. The fast-growing consumer demand for online shopping forced a rapid evolution of supply chains and logistics practices to handle the growing volume of direct-to-consumer sales.

The shift fundamentally changed what industrial tenants needed. E-commerce fulfillment requires intense use of logistics space, often demanding three to four times the logistics space of traditional brick-and-mortar retail replenishment.

For EastGroup, the e-commerce boom validated decades of strategic choices:

Sunbelt markets: Population growth in Texas, Florida, Arizona, and the Carolinas meant more consumers demanding faster delivery.

Last-mile locations: E-commerce requires facilities close to end consumers for same-day and next-day delivery.

Multi-tenant buildings: Third-party logistics providers and regional distributors—key players in e-commerce fulfillment—often need smaller, more flexible spaces.

Shallow bay facilities: The 20,000-100,000 square foot buildings EastGroup specializes in are ideal for last-mile distribution operations.

The company's strategy has resonated with investors, as EastGroup's market capitalization has soared from $2.8 billion in early 2016 to roughly $6.8 billion today. Meanwhile, the dividend has been increased or maintained for 28 consecutive years, with increases in each of the last nine, according to the company.

The e-commerce tailwind accelerated EastGroup's growth, but it didn't change the company's fundamental approach. Management continued the same disciplined strategy they had followed for decades—they simply benefited from having positioned the company on the right side of a massive secular trend.

IX. Inflection Point #3: Leadership Transition & The Marshall Loeb Era (2015–Present)

Leadership transitions are always pivotal moments for long-term investors. When founder-led companies pass to the next generation of management, there's always risk that the new team will lack the vision, discipline, or cultural continuity that drove earlier success.

EastGroup handled this transition with characteristic thoughtfulness. Marshall A. Loeb rejoined the Company as President and Chief Operating Officer in March 2015 and was named Chief Executive Officer and a director in January 2016. He served as President and Chief Operating Officer of Glimcher Realty Trust, a retail REIT, from 2005 to 2015, when it was acquired by Washington Prime Group. From 2000 to 2005, he served as Chief Financial Officer of Parkway Properties, an office REIT. Mr. Loeb was previously employed by the Company from 1991 to 2000, beginning as an asset manager and rising to senior vice president after having a variety of responsibilities with the Company.

The "prodigal son" narrative is compelling. Loeb didn't come in as an outside hire unfamiliar with EastGroup's culture—he had spent nearly a decade at the company before leaving to gain broader experience. Mr. Loeb has over 30 years of experience with publicly held REITs and brings real estate industry, finance, operations, development, and executive leadership expertise to the Board.

Leland Speed, chairman emeritus of EastGroup's board of directors and a director of the company, died in January at the age of 88. Speed was the company's founder and served as CEO until 1997. His service as a director began in 1978; he served as the chairman of the board from 1983 to 2015 and then as chairman emeritus until the time of his death.

Speed was awarded Nareit's Industry Leadership Award in 2008 in recognition of his "significant and lasting contribution to the growth and betterment of the industry."

Speed was a REIT pioneer, beginning his career in 1978 when the industry was composed primarily of mortgage REITs. He built an enterprise through the acquisitions of a series of mortgage REITs through the 1980s and was an early champion of the potential for publicly traded equity REITs in the 1990s.

When Speed passed away in January 2021, Marshall Loeb, President and CEO, stated, "Mr. Speed's contributions to EastGroup are tremendous. His real estate knowledge and expertise were instrumental to the growth of the Company. His leadership and 'healthy, wealthy, wise' philosophy were the capstone for our positive culture. From my internship to today, he made EastGroup feel like family, and he could often be found in conversations with employees about a variety of topics, from Company history to personal wellbeing and ways to make positive impacts in our communities."

Under Loeb's leadership, EastGroup has accelerated its growth while maintaining the strategic discipline that Speed established. The company's FFO per share, portfolio size, and dividend have all grown substantially since 2016.

Loeb's management style emphasizes operational excellence and market responsiveness. In recent earnings calls, he articulated the company's flexible approach: "We're pleased with our mid-year results." He emphasized the company's strong balance sheet, saying, "Our balance sheet positions us well during volatile moments." Loeb also highlighted the strategic approach to market conditions: "We'll go fast or slow and it's really listening to what the market will tell you."

X. The Shallow Bay Strategy: Small Is Beautiful

When it comes to industrial real estate, EastGroup Properties (NYSE: EGP) has operated under a simple mantra in its 30 years as a public company: bigger isn't always better. The REIT has honed its strategy in favor of smaller warehouse buildings located closer to consumers in markets across the Sun Belt.

The Company's goal is to maximize shareholder value by being a leading provider in its markets of functional, flexible and quality business distribution space for location sensitive customers (primarily in the 20,000 to 100,000 square foot range).

This "shallow bay" strategy differentiates EastGroup from larger industrial REITs like Prologis, which focus on massive distribution centers often exceeding 500,000 square feet. The distinction matters enormously.

A key differentiator in EastGroup's strategy is its focus on shallow bay industrial properties (20,000 to 140,000 square feet), which have historically demonstrated lower vacancy rates compared to larger box facilities. The company's presentation highlights this advantage with data showing consistently lower vacancy and availability rates for shallow bay properties over time. As illustrated in the following chart, shallow bay properties have maintained lower vacancy rates than larger box properties, with shallow bay vacancy at 3.9% compared to 12.8% for larger box properties as of 2023.

Why do shallow bay properties outperform? Several structural reasons:

Tenant diversification: Multi-tenant buildings spread risk across dozens of companies rather than concentrating it in one or two anchor tenants. As of December 31, 2024, EastGroup's operating portfolio was 97.1% leased to tenants in approximately 1,600 leases, with no single tenant accounting for more than approximately 1.6% of the Company's annualized based rent.

Supply constraints: It's relatively easy to build a large distribution center on cheap land in the exurbs. It's much harder to build small multi-tenant facilities in infill locations where land is scarce and zoning is difficult.

Demand breadth: The universe of tenants needing 20,000-70,000 square feet is far larger than the universe needing 500,000+ square feet. This creates a deeper pool of potential occupants.

Tenant stickiness: Small tenants are often more rooted in local economies and less likely to relocate. Large e-commerce fulfillment centers can and do move based on network optimization models.

The niche of "last mile, shallow bay distribution" uniquely positions EastGroup among its peers. The majority of our institutional industrial ownership peers develop large, big box (500,000 square feet and above) properties, with few in-fill projects.

Portfolio of 63.1M+ SF. Shallow bay buildings — Average size 96K SF. Multi-tenant — Average tenant size 35K SF. High-growth, infill locations. Clustered assets in park settings. Typically, rear load buildings.

XI. The Modern Era: COVID Acceleration & Supply Chain Reshoring (2020–Present)

The COVID-19 pandemic and its aftermath created both headwinds and tailwinds for industrial real estate. EastGroup navigated the period with characteristic balance.

The pandemic initially supercharged e-commerce demand, accelerating the trends that had been favorable to EastGroup's strategy. But the subsequent normalization—combined with rising interest rates and economic uncertainty—created more challenging conditions.

CEO Loeb has articulated management's view on the emerging reshoring/nearshoring trend: "That new source of demand is, I think, through our portfolio and especially kind of our markets, we are seeing the manufacturing companies and the relocations a lot into Texas. We have a number of Tesla suppliers in Austin and in San Antonio. The new chip plant with Intel's building in Phoenix, we have Intel related to construction there, a supplier to Intel."

EastGroup's focus on industrial real estate—a sector experiencing structural tailwinds—positions it to capitalize on long-term trends. The REIT's recent $61 million acquisition of two properties in Raleigh, North Carolina, near the Research Triangle Park, exemplifies its strategy to expand in supply-constrained logistics hubs. These markets are driven by nearshoring, e-commerce growth, and population migration, all of which are expected to sustain demand for industrial space.

Recent financial performance reflects both the tailwinds and EastGroup's execution:

Average Occupancy of Operating Portfolio was 96.8% for 2024 as Compared to 98.0% for 2023. Rental Rates on New and Renewal Leases Increased an Average of 53.0% on a Straight-Line Basis. Acquired Six Operating Properties Containing 2,474,000 Square Feet and 61.1 Acres of Development Land for Approximately $404 Million. Started Construction of 10 Development Projects Totaling 1,585,000 Square Feet with Projected Total Costs of Approximately $230 Million. Transferred Seven Development Projects Containing 1,519,000 Square Feet to the Operating Portfolio.

With Funds From Operations (FFO) per share experiencing robust growth, reaching $8.06 for the full year 2024, a 9.1% increase over 2023.

The company maintains a conservative capital structure: Debt-to-total market capitalization was 15.4% at December 31, 2024. The Company's interest and fixed charge coverage ratio was 12.77x and 11.48x for the three and twelve months ended December 31, 2024, respectively.

The Company's ratio of debt to earnings before interest, taxes, depreciation and amortization for real estate ("EBITDAre") was 3.20x and 3.36x for the three and twelve months ended December 31, 2024, respectively.

Most recently, On November 19, 2025, EastGroup Properties, Inc. and its subsidiary entered into a $250 million Term Loan Agreement with PNC Bank and other financial institutions, divided into two tranches with maturity dates in 2030 and 2031.

XII. Portfolio Deep Dive: Geography & Assets

As of December 31, 2024, EastGroup owned 536 industrial properties in 12 states. As of that same date, the Company's portfolio, including development projects and value-add properties in lease-up and under construction, included approximately 63.1 million square feet consisting of 497 business distribution properties containing 57.8 million square feet, 17 bulk distribution properties containing 4.4 million square feet, and 22 business service properties containing 900,000 square feet.

The geographic concentration is deliberate: The company's property net operating income remains well-diversified across its Sunbelt footprint, with Texas contributing 34%, Florida 25%, California 17%, Arizona 7%, North Carolina 6%, and other markets 11%.

EastGroup's property management teams are located in San Antonio, Austin, Miami, Jacksonville, San Francisco, Charlotte, Las Vegas and Greenville. These locations allow the Company to provide property management services to 87% of the Company's operating portfolio on a square foot basis.

Recent acquisitions demonstrate continued expansion: In November, EastGroup acquired Riverpoint Industrial Park, which contains three industrial buildings totaling 779,000 square feet in Atlanta, for approximately $88,000,000. This property was developed in 2020 and is 100% leased.

The company is also expanding into new markets strategically: In May, EastGroup acquired a 275,000 square foot newly constructed industrial property in Raleigh for approximately $54,000,000. This property, which is 100% leased to three tenants, represents the Company's entry into the Raleigh-Durham market, which has been a target market for EastGroup for several years due to its population growth, diversified economic base.

As of December 31, 2024, EastGroup had 101 full-time employees. This remarkably lean organization manages over 63 million square feet of property—a testament to operational efficiency and the benefits of a self-administered structure.

XIII. The Dividend Machine

Perhaps no aspect of EastGroup's history better illustrates its commitment to shareholders than its dividend record.

EastGroup Properties, Inc. (NYSE: EGP) announced that its Board of Directors approved a 10.7% increase in its quarterly dividend, raising it to $1.55 per share from $1.40 per share. The dividend is payable on October 15, 2025, to shareholders of record of Common Stock on September 30, 2025. This dividend is the 183rd consecutive quarterly cash distribution to EastGroup's shareholders and represents an annualized dividend rate of $6.20 per share. EastGroup has increased or maintained its dividend for 33 consecutive years. The Company has increased it 30 years over that period, including increases in each of the last 14 years.

The Company has increased or maintained its dividend for 32 consecutive years and has increased it 29 years over that period, including increases in each of the last 13 years.

The Company has increased or maintained its dividend for 33 consecutive years and has increased it 30 years over that period, including increases in each of the last 14 years. The annualized dividend rate of $6.20 per share represents a dividend yield of 3.4% based on the closing stock price of $180.67 on October 22, 2025.

This consistency is rare among REITs, which are required to distribute at least 90% of taxable income but often cut dividends during economic downturns. EastGroup maintained its dividend through the Global Financial Crisis, through COVID-19, and through rising interest rate environments.

The dividend growth reflects underlying business performance: The company's revenue CAGR over the past five years stands at 14%, demonstrating consistent long-term performance.

The REIT has raised its dividend in 30 of those years, including 14 consecutive annual increases up to 2025. The most recent hike, a 10.7% increase to $1.55 per share in August 2025, marks the 183rd consecutive quarterly payout.

For income-oriented investors, this track record represents exactly what they seek: reliable, growing distributions backed by a conservatively managed balance sheet and a portfolio of essential real estate assets.

XIV. Playbook: Business & Investing Lessons

EastGroup's five-decade journey offers several lessons applicable beyond industrial real estate:

Lesson 1: Geographic Focus Pays Off

Speed's decision to concentrate on the Sunbelt in 1983—decades before the consensus recognized these markets as growth engines—demonstrates the power of contrarian geographic positioning. The company didn't try to be everywhere; it tried to be in the right places.

Lesson 2: Development as a Core Competency

EastGroup has built half of its portfolio from the ground up. It has invested $3.3 billion to develop 271 properties with 31.7 million square feet since 1996. This strategy drives increased returns with less risk.

Building properties requires different skills than buying them. EastGroup invested in those skills over decades, creating a sustainable competitive advantage.

Lesson 3: Small and Multi-Tenant Beats Big and Single-Tenant

Risk diversification at the property level protects against tenant-specific problems. With 1,600 leases and no single tenant exceeding 1.6% of rent, EastGroup can absorb individual tenant failures without material impact.

Lesson 4: Clustering Creates Value

By developing entire business parks rather than scattered buildings, EastGroup creates operational efficiencies and growth options for tenants. "Their secret sauce is down pat," says Alex Goldfarb, REIT analyst with Piper Sandler. "They've just become phenomenal at it."

Lesson 5: Internal Management Matters

EastGroup is self-administered—its management works directly for shareholders rather than an external advisor. This alignment eliminates conflicts that have plagued externally managed REITs.

Lesson 6: Capital Discipline Through Cycles

EastGroup continues to maintain a strong and flexible balance sheet. Debt-to-total market capitalization was 14.1% at September 30, 2025. The Company's interest and fixed charge coverage ratio was 16.8x and 15.9x for the three and nine months ended September 30, 2025, respectively.

Lesson 7: Demand-Pull Development

Rather than building speculatively and hoping to lease up, EastGroup develops in response to demonstrated demand. This discipline prevents the overbuilding that has historically led to boom-bust cycles in real estate.

XV. Competitive Positioning & Strategic Analysis

Porter's Five Forces Analysis

Threat of New Entrants: MODERATE

Industrial real estate development requires significant capital, local expertise, and tenant relationships. However, new competitors can enter specific markets, and large institutional players have been increasing their industrial allocations. EastGroup's focus on infill shallow bay properties creates some natural barriers—it's easier to build big boxes on greenfield sites than small multi-tenant buildings in established submarkets.

Bargaining Power of Suppliers: LOW

The "suppliers" in real estate development are construction contractors, land sellers, and capital providers. Construction costs have been a headwind, but EastGroup's scale provides some leverage. Land acquisition is competitive in desirable markets but fragmented enough that no single supplier has undue power. Capital markets access has historically been favorable for investment-grade REITs.

Bargaining Power of Buyers (Tenants): MODERATE

EastGroup's tenant base is highly diversified, with no single tenant exceeding 1.6% of rent. This limits individual tenant leverage. However, in weaker economic environments, tenants across the portfolio may have increased negotiating power on renewals. The shallow bay focus somewhat mitigates this—as noted, shallow bay vacancy at 3.9% compared to 12.8% for larger box properties—indicating tighter supply-demand dynamics.

Threat of Substitutes: LOW

For location-sensitive distribution, there are few substitutes for well-located industrial real estate. Remote work has crushed office demand; e-commerce has hurt retail; but nothing has emerged to substitute for physical distribution facilities. The growth of same-day delivery has if anything increased the value of last-mile locations.

Industry Rivalry: HIGH

Competition for acquisitions and development sites is intense. Prologis is by far the largest industrial REIT with $122.54 billion market cap, while EastGroup at $8.5 billion is substantially smaller. Other competitors include Rexford Industrial, First Industrial Realty Trust, and STAG Industrial. EastGroup competes on local market expertise and a differentiated product (shallow bay) rather than scale.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Limited. Industrial real estate doesn't exhibit strong scale economies—a 60 million square foot portfolio isn't dramatically cheaper to operate per square foot than a 30 million square foot portfolio.

Network Effects: Absent. No meaningful network effects in industrial real estate.

Counter-Positioning: STRONG. EastGroup's shallow bay focus represents classic counter-positioning versus Prologis and other large industrial REITs focused on big boxes. Incumbents like Prologis would cannibalize their own business model by shifting heavily to small multi-tenant properties. This creates durable strategic space.

Switching Costs: Moderate. Tenants face some costs in relocating—moving equipment, updating customer addresses, training employees on new locations—but these aren't prohibitive. EastGroup's clustering strategy helps create switching costs by offering growth options within their parks.

Cornered Resource: LIMITED. While EastGroup has accumulated valuable infill land positions over decades, they don't have exclusive access to critical resources.

Process Power: MODERATE TO STRONG. Decades of development experience have created organizational knowledge about how to acquire sites, navigate entitlements, build efficiently, and lease up properties. This institutional knowledge is difficult to replicate quickly.

Branding: Limited relevance in B2B industrial real estate.

Competitive Comparison

| Metric | EastGroup (EGP) | Prologis (PLD) |

|---|---|---|

| Market Cap | ~$9B | ~$120B |

| Portfolio Size | ~64M sq ft | ~1.3B sq ft |

| Geographic Focus | Sunbelt USA | Global |

| Property Type | Shallow bay / Multi-tenant | Big box / Single-tenant |

| Development | ~50% of portfolio | Significant but smaller % |

| Typical Tenant Size | 20,000-100,000 sq ft | Often 500,000+ sq ft |

| Top 10 Tenants | <10% of rent | More concentrated |

EastGroup isn't trying to be Prologis. It's built a differentiated position in a specific niche where its smaller scale is actually advantageous—it can pursue infill opportunities that are too small to move the needle for a $120 billion company.

XVI. Bull Case & Bear Case

The Bull Case

-

Structural demand drivers remain intact: E-commerce penetration continues to grow, nearshoring/reshoring is accelerating, and Sunbelt population growth shows no signs of reversing.

-

Supply constraints favor incumbents: CEO Marshall Loeb noted increased activity for vacant spaces and expressed optimism about market opportunities arising from declining industrial construction pipeline and improving tenant demand. New shallow bay development in infill locations is inherently limited.

-

Rent upside remains substantial: At 35-55% releasing spreads, in-place rents remain significantly below market, providing embedded growth even without expansion.

-

Balance sheet provides flexibility: With debt-to-EBITDA around 3x and interest coverage above 15x, EastGroup can navigate economic volatility and pursue opportunistic acquisitions.

-

Management continuity and culture: The leadership transition to Marshall Loeb has been seamless, and the company's disciplined culture appears intact.

-

Dividend growth is sustainable: 14 consecutive years of increases backed by growing FFO provides income investors confidence in long-term distributions.

The Bear Case

-

E-commerce growth is normalizing: After pandemic acceleration, online retail growth has slowed. If e-commerce penetration stabilizes or declines, industrial demand could weaken.

-

Interest rate sensitivity: Higher rates increase financing costs and compress valuations for all real estate. While EastGroup's balance sheet is conservative, it's not immune to this headwind.

-

Sunbelt supply risks: Texas, Arizona, and Florida have seen significant industrial development. If supply catches up with demand in these markets, rent growth could stall.

-

Economic recession risk: Industrial real estate is cyclical. A severe recession would reduce tenant demand, increase vacancies, and compress rents.

-

Tariff uncertainty: While thought with the tariffs cap rates might go up, but they really those have been sticky. Prolonged trade policy uncertainty could freeze tenant decision-making.

-

Premium valuation: EastGroup typically trades at a premium to NAV and to industrial REIT peers, reflecting high expectations that must be met.

XVII. Key Metrics to Watch

For investors tracking EastGroup's ongoing performance, three metrics deserve primary focus:

1. Same-Property NOI Growth (Cash Basis)

This measures the organic growth of the existing portfolio, excluding acquisitions and developments. It reflects both occupancy trends and rent growth on renewals. EastGroup has consistently delivered mid-single-digit same-property growth, and deviations from this trend would signal either outperformance or emerging problems.

2. Leasing Spreads on New/Renewal Leases

The gap between expiring rents and new rents provides visibility into embedded portfolio growth. EastGroup reported 35-55% spreads recently. As this gap narrows toward historical norms of 10-20%, the growth runway shortens. Conversely, persistently high spreads indicate sustained pricing power.

3. Development Lease-Up Velocity

EastGroup's development pipeline represents future growth. The speed at which newly completed buildings lease up indicates demand strength. If lease-up slows, development economics deteriorate—and management may need to pull back starts.

XVIII. Myth vs. Reality

Myth: EastGroup is just a smaller version of Prologis.

Reality: The companies pursue fundamentally different strategies. EastGroup focuses on small multi-tenant buildings in infill locations; Prologis builds large single-tenant distribution centers in logistics corridors. Most new property developments are large single-tenant industrial properties like Amazon or Walmart such as those owned by PLD. On the other hand, there are relatively few smaller multi-tenant properties being built in urban, high-barriers-to-entry markets and that's what EGP owns for the most part.

Myth: Small industrial REITs can't compete with larger peers.

Reality: EastGroup's size is actually an advantage in its niche. Deals too small for Prologis to pursue are meaningful for EastGroup. Local relationships and market knowledge matter more in fragmented shallow bay markets than in institutional big box markets.

Myth: The dividend payout ratio above 100% of GAAP earnings is unsustainable.

Reality: REITs should be evaluated on FFO, not GAAP earnings. GAAP earnings include depreciation, which overstates economic costs for well-maintained real estate. EastGroup's FFO payout ratio is approximately 65%, which is sustainable and allows for dividend growth.

XIX. Risks & Considerations

Regulatory/Legal Overhang: No material legal or regulatory issues have been disclosed. As a REIT, EastGroup must comply with various requirements regarding income distribution, asset composition, and tenant concentration. The company has maintained REIT qualification continuously.

Accounting Considerations: Real estate accounting involves significant estimates around depreciation useful lives and impairment assessments. Investors should note that reported depreciation may not match economic depreciation for well-located industrial properties, which often appreciate rather than depreciate over time.

Environmental Liabilities: The company has disclosed environmental liabilities, including costs, fines or penalties that may be incurred due to necessary remediation of contamination of properties presently owned or previously owned. This is standard disclosure for industrial real estate owners.

XX. Conclusion: The Compounding Machine from Mississippi

EastGroup Properties represents something rare in modern markets: a company that has followed the same basic strategy for four decades, refined its execution continuously, and compounded value through cycles without succumbing to the temptations of leverage, diversification, or empire-building.

From its origins as Third ICM Realty in 1969, through near-death in the mid-1970s, through two decades of obscurity, through the 1983 transformation under Leland Speed, through the 1990s acquisition spree, through the e-commerce revolution, and through COVID—EastGroup has maintained its focus on Sunbelt industrial real estate, shallow bay facilities, multi-tenant buildings, clustered development, and conservative capital management.

CEO Loeb expressed this continuity in the October 2025 earnings call: "With limited supply and ever growing demand, we are excited about our pathway. Looking beyond this environment, I remain bullish on the continuing external trends benefitting our shallow bay, last mile, high-growth market portfolio."

For long-term fundamental investors, EastGroup offers a case study in how disciplined strategy execution, thoughtful capital allocation, and conservative balance sheet management can compound wealth over decades. The company will never be the largest industrial REIT. It doesn't need to be. It has found its niche, mastered it, and continues to compound.

The secret sauce, as Piper Sandler's Goldfarb noted, is down pat. Whether that sauce continues to deliver depends on the same factors that have always mattered: demographic trends, e-commerce penetration, supply discipline in target markets, and management's continued commitment to the principles that have guided the company for forty years.

In an era of disruption and innovation, sometimes the most valuable skill is knowing exactly what you are, doing it exceptionally well, and having the patience to let compounding do its work.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube