eGain Corporation: The Unsung AI Pioneer of Customer Engagement

I. Introduction: A Twenty-Seven-Year Survivor in Silicon Valley

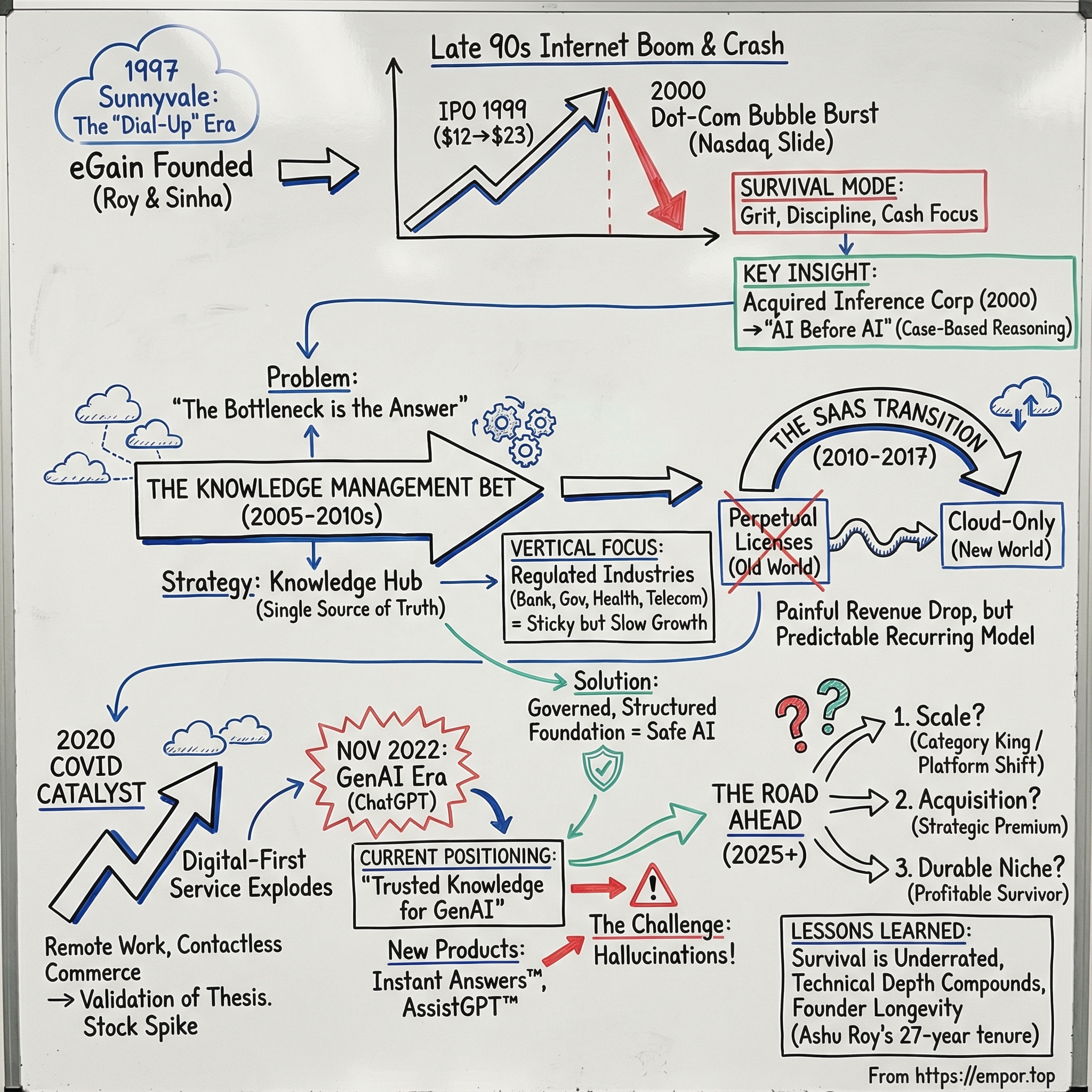

Picture a software company in Sunnyvale that’s been around long enough to watch the commercial internet arrive, explode, crash, and reinvent itself—again and again. While startups all around it either vaporized in the dot-com fallout, stumbled during the move to SaaS, or got absorbed by bigger platforms, this one stayed standing. And it did so under the same leader the whole time. Ashutosh Roy, eGain’s co-founder, has served as CEO and Chairman since 1997—an almost unheard-of streak in enterprise tech, spanning four distinct eras without handing over the keys.

eGain Corporation is a publicly traded software company that builds customer service and support applications. Founded in 1997 and headquartered in Sunnyvale, California, it trades on NASDAQ under the ticker EGAN. With roughly a $150 million market cap and about $90 million in annual revenue, eGain sits in a strange middle ground: too small to bully the market, but too established—and too stubbornly viable—to fade away. It’s also been doing “AI-powered customer service” since long before that phrase became a staple of earnings calls.

That sets up the central mystery: how does a company born in the internet boom survive the dot-com crash, make it through the SaaS transition, and come out the other side still independent? eGain’s answer is part grit, part unusually early conviction about knowledge and automation, and part a founder’s belief that the biggest mistake would be selling right before the world finally catches up.

This story follows eGain’s evolution from an email-management upstart to a knowledge-first customer engagement platform, and it looks at what kept the company alive, what kept it from scaling the way some rivals did, and whether the generative AI era finally creates the breakout moment eGain has been waiting for.

II. Founding Context: The Late 90s Internet Boom

In 1997, the commercial internet wasn’t a utility yet. It was a land grab. Netscape’s blockbuster 1995 IPO had taught the market a new lesson: a software company could go from unknown to wildly valuable in a blink. At the same time, email was becoming mainstream—and businesses suddenly found themselves with a brand-new customer support channel and absolutely no playbook for how to run it. Inboxes filled up. Customers expected answers. And companies had no systems, no workflows, and no staffing model built for the flood.

That’s the problem eGain was born to solve.

eGain Corporation started life as eGain Communications Corporation, founded in late 1997 by Ashutosh Roy and Gunjan Sinha. At the time, both were part of WhoWhere?, an internet search company they had founded that would be acquired by Lycos in 1998. Roy wasn’t just catching the dot-com wave; he was building companies inside it—and he had a resume that mixed hard engineering with business instincts. From 1988 through 1992, he worked in software engineering roles at Digital Equipment Corp. He earned a BS in Computer Science from the Indian Institute of Technology, New Delhi, a master’s in Computer Science from Johns Hopkins, and later an MBA from Stanford.

That mix mattered. Roy understood systems, operations, and enterprise buying—rare all in one person at the time. And he’d already spent time close to the customer service world. From 1993 to 1995, he co-founded Parsec Technologies, a call center software company based in India. So he’d seen how support worked in the pre-internet era: phones, scripts, queues, and armies of agents. What he saw next was obvious in hindsight and contrarian at the time. The center of gravity was shifting. Customer service wasn’t going to stay trapped in the call center—it was going online.

The founding insight was simple: if customers were going to email companies, companies would need purpose-built software to manage it. Not just an inbox, but routing, tracking, reporting, and eventually web-based self-service—and, over time, the ability to handle multiple digital channels in one place. eGain set up in Sunnyvale, right in the middle of Silicon Valley’s late-90s acceleration, and raised venture funding in its early days to build product and get to market.

Then the market opened a door that, in 1999, seemed to open for almost anyone with an internet story.

eGain filed for an initial public offering with the SEC in July 1999. At the time, the company had 114 employees and planned to trade on NASDAQ. By September, it was public. The stock debuted at $12 per share and quickly traded up to $23 within its first few days—nearly doubling in the afterglow of dot-com euphoria.

eGain had timed its public debut almost perfectly. But the bigger story is that, underneath the hype, it was selling into a real, growing pain.

Early customers—especially in financial services and telecommunications—were getting crushed by customer email volume. Call centers weren’t designed for it. Agents weren’t trained for it. And the tools were primitive. eGain’s email management software wasn’t a nice-to-have; it was a way to keep up with customers who had suddenly learned they could hit “send” instead of waiting on hold. eGain positioned itself as the infrastructure for this new world of digital customer engagement—right as the internet convinced everyone it was the future.

III. Surviving the Dot-Com Nuclear Winter (2000-2004)

The dot-com bubble burst in March 2000. The NASDAQ Composite, stuffed with tech’s most overhyped names, peaked on March 10—and then began a long, ugly slide. By late 2002 it had lost most of its value, and trillions of dollars of market cap had vanished along with it.

For enterprise software companies like eGain, the crash wasn’t some abstract market event. It was an extinction-level shift. IPOs stopped. Venture money dried up. Big customers froze budgets and delayed projects. Companies that had looked unstoppable a year earlier were suddenly fighting to make payroll.

eGain survived by doing something profoundly uncool for that era: it turned its attention from growth at any cost to staying alive. That meant tighter spending, sharper focus, and doubling down on enterprise value instead of hype. The mindset that formed here—discipline first, durability always—would carry through every tech cycle that followed.

And in the middle of that chaos, eGain made a move that looks almost insane in hindsight: it bought an AI company.

In March 2000, right as the crash was getting underway, eGain acquired Inference Corporation. Inference wasn’t a dot-com. It was a much older kind of Silicon Valley company—founded in 1979 and known for building artificial intelligence systems long before “AI” became a marketing term.

One of Inference’s notable achievements in the 1990s was a case-based system for Compaq that could help troubleshoot problems—like a printer producing blurry, smeared pages—without a call to the help desk. The point wasn’t that troubleshooting software was new. The point was that Inference had made it practical: small, deployable, and useful.

Strategically, the pitch was straightforward. eGain had strength in web-based, multi-channel customer communications. Inference brought customer profiling and contact center support technology. Together, eGain said, they could extend their leadership in building customer-centric “interactive enterprises” for large global companies.

The deal was valued at approximately $78.6 million, based on eGain’s stock price at the time. But the real value wasn’t the headline number—it was what Inference added to the product DNA. Inference brought genuine AI capability, especially case-based reasoning technology that could power knowledge management: finding the right answer, guiding a customer or agent to it, and doing it consistently. This was AI before the buzzwords—reasoning engines, early semantic search concepts, and intent-style matching that would later become table stakes.

Meanwhile, the market around eGain was thinning. The customer service software space was crowded with companies that would eventually disappear or get absorbed: Kana Communications, eShare Technologies, and others fought for the same enterprise budgets. RightNow Technologies—also founded in 1997—made it through the crash too. But while both survived, their trajectories would diverge in ways that would define the next decade.

Inside eGain, the dot-com collapse forged what you might call the cockroach playbook: protect gross margins, keep R&D focused, and take obsessive care of the enterprise customers who were already in the tent. Rather than chasing growth that depended on ever-more capital, eGain prioritized cash generation and stability—serving large customers who could provide steady revenue even when the broader market was in free fall.

This period set the default operating system for the company: frugal execution, tight founder control, and a willingness to trade speed for survival. In a decade where so many software companies died young, eGain learned how to endure—and that durability became its most underrated product.

IV. The Knowledge Management Bet (2005-2010)

By the mid-2000s, eGain’s leadership had landed on a hard truth about customer service: routing the question to the right person wasn’t the real bottleneck. The bottleneck was the answer. Could your agents give the same correct response every time, across every channel, without reinventing the wheel?

The Inference acquisition had quietly set eGain up for this moment. Inference’s case-based reasoning technology—built for troubleshooting and guided support—gave eGain something more durable than another communications channel. It gave them a way to capture expertise, structure it, and reuse it. That capability became the foundation for what eGain would later call its Knowledge Hub: a system designed to help agents (and customers) find the best answer quickly and consistently.

This was “AI” in its original, pre-hype form. Not neural nets and GPU clusters, but software that could reason through a problem, narrow down what the user meant, and guide them toward a resolution. eGain’s Guided Help application, for example, used the eGain Inference Reasoning Engine to turn “search” into an interactive Q&A flow. Instead of forcing customers to guess the right keywords, the system could interpret everyday language, ask clarifying questions, and drive toward the right fix.

Strategically, this was eGain’s bet—and its counter-positioning. While giants like Salesforce and Oracle were building customer service inside broader CRM suites—records, cases, workflows, and dashboards—eGain argued that knowledge was the missing layer. Great service wasn’t just about tracking the interaction; it was about delivering the right answer, reliably, at scale.

The market around them kept getting more intense. Salesforce was building out Service Cloud. SAP and Oracle pushed their enterprise CRM suites deeper into large accounts. And RightNow—another survivor from the late-90s customer service wave—became the clearest signal of where the industry was headed. Oracle announced in October 2011 that it intended to acquire RightNow, a deal completed in January 2012. The message to everyone else in the category was unmistakable: the platforms were coming, and independence was going to get harder.

That put Ashu Roy in the familiar position eGain seemed to revisit every few years: sell to a giant, or keep going alone. Roy stayed. He remained CEO, kept control of product direction, and protected the company’s engineering-driven culture—at the cost of passing on the kind of outcome RightNow’s shareholders ultimately got.

Under the hood, the business still ran on the old enterprise software model. eGain primarily sold perpetual licenses paired with maintenance and professional services: big upfront installs, followed by ongoing support and consulting. It generated cash, but it also carried a lurking risk. The industry was slowly, inevitably moving toward subscription-based SaaS, and the companies built around upfront license deals would eventually have to pay the transition toll.

One more strategic shape formed in this era, too: eGain’s vertical focus. Roy has said that roughly 90% of the customer base sits in five top industries: banking, financial services, and insurance; government; healthcare; telecommunications; and retail. That concentration became both a strength and a constraint. Regulated customers like banks and insurers valued security, compliance, and reliability—areas where eGain had real depth. But those customers also moved slowly, and selling into them rarely produced the kind of breakout growth that flashier, faster-moving markets could deliver.

V. The Existential SaaS Transition (2010-2016)

If the dot-com crash was an extinction event, the shift from perpetual licenses to SaaS was a slow-moving ice age—and for enterprise software companies built on big upfront deals, it was just as threatening.

By the early 2010s, the market had picked a direction. Salesforce had proven that cloud-delivered software could win serious enterprise accounts, and born-in-the-cloud upstarts like Zendesk and Freshworks were coming in from below with products that were simpler, cheaper, and easier to adopt. Meanwhile, eGain was still operating in the old world: perpetual licenses, maintenance, and a lot of professional services.

Then came the hardest part: deciding to actually cross over.

In fiscal 2017, eGain completed its shift from a mixed license-and-SaaS business to one focused exclusively on cloud-based offerings. That kind of change isn’t just a technical migration. It forces you to rebuild how the company sells, bills, forecasts, and even thinks about success. You’re not closing “a license deal” anymore. You’re building a recurring relationship and hoping it compounds.

The financial hit was exactly what you’d expect—and still painful. Total revenue fell to $58.2 million in fiscal 2017, down from $69.4 million in fiscal 2016. The main reason was the intentional collapse of perpetual license revenue, which dropped from $14.5 million to $4.6 million as eGain finished moving to a recurring model.

This is the SaaS transition toll in its purest form. Under the old model, a customer might generate a huge first-year payment, and the income statement would light up immediately. In SaaS, that same value gets spread out over time. The business can become healthier, more predictable, and more valuable—but during the crossover, the headline numbers look like you’re shrinking.

To make it work, eGain had to rewire the go-to-market machine too. The company introduced Try+Buy, a pilot program offering customers a cost-free trial of its products, and said about 75% of participants converted into full-time clients. It also appointed a new head of sales who pushed a land-and-expand approach and reorganized the function: one team for direct marketing, another for channel partnerships, and another dedicated to expanding within existing accounts.

But none of this happened in a vacuum. The stock languished through this stretch, and it’s not hard to see why. Critics looked at the bigger market and asked why eGain wasn’t riding the same wave. From calendar year 2007 to 2017, eGain’s total revenue grew at a much slower pace than the SaaS giants—Salesforce, in particular, was growing dramatically faster over the same period.

Still, there’s a real accomplishment buried inside those uninspiring charts: eGain made it across the bridge. It successfully shifted from a hybrid license-cloud provider to a cloud-only business, while also executing significant cost reductions and fully delevering the company.

And crucially, eGain didn’t abandon the customers that made it durable in the first place. The decision to keep on-premise options for regulated industries ended up being strategically sound. Many banks and government agencies couldn’t move everything to public cloud infrastructure overnight because of compliance requirements. eGain’s hybrid approach—cloud-native architecture that could be delivered as SaaS or deployed on-premise—helped preserve those sticky relationships while the rest of the industry rushed ahead.

The competitive pressure, though, kept rising. Zendesk was scaling fast with a developer-friendly, lower-cost approach and a broad set of customer communication channels—telephony, chat, email, messaging, social, communities, and help centers. Salesforce Service Cloud was bundling service into the gravitational pull of the world’s dominant CRM. And Oracle, after absorbing RightNow, was folding modern customer service capabilities into its enterprise stack.

So why didn’t eGain get acquired during this vulnerable window—when many companies either sold or got squeezed out?

A few reasons stand out. eGain remained profitable even through the transition, generating cash instead of burning it. Ashu Roy, still founder-CEO, controlled the board and wasn’t eager to sell. And that vertical depth—especially in financial services, where compliance, integration, and knowledge migration create real switching costs—gave eGain enough defensibility to stay independent, even when the market seemed designed to punish companies its size.

VI. Doubling Down on AI & Knowledge (2016-2019)

By 2016, artificial intelligence was finally crossing from research labs into budget lines. Deep learning breakthroughs—AlexNet in 2012, then rapid gains in image recognition and natural language processing—were starting to show up in real products. And suddenly, eGain’s long, unglamorous obsession with knowledge management and reasoning engines didn’t look old-fashioned. It looked early.

So eGain leaned into the moment. The company began framing itself as an AI-native customer engagement platform—one that had been building “intelligent automation” long before the current wave made it fashionable. eGain Cloud™ was positioned as a cloud customer engagement software suite built before cloud became the default. And the core architecture—structured knowledge, reasoning, and semantic understanding—mapped cleanly to what enterprises actually needed from AI: answers they could trust.

At the center of that story was eGain Knowledge Hub™. Powered by AI reasoning, machine learning, natural language processing, and analytics, it was sold as a one-stop system of record for contact center knowledge—built for a world where service was increasingly digital and, more and more, remote.

The pitch sharpened into something simple and sticky: eGain wasn’t trying to be just another customer service application. It wanted to be the “brain” behind chatbots and virtual agents. The company focused on creating, capturing, and optimizing the knowledge of how to help customers—then putting a conversational AI layer in front of that knowledge so it could be delivered consistently, whether the “agent” was a person or a bot. As enterprises rushed to deploy virtual assistants, they ran into an uncomfortable truth: AI without accurate, governed knowledge produces confident nonsense. eGain positioned Knowledge Hub as the structured foundation that kept automation from going off the rails.

To make that foundation easier to adopt, eGain pushed deeper into the ecosystems customers were already using. Embedded in the Salesforce Service Cloud agent desktop, eGain Knowledge Hub™ for Salesforce was designed to proactively surface trusted answers and personalized guidance for agents. The company also highlighted AssistGPT™, a capability aimed at automating knowledge management tasks. And beyond Salesforce, integrations with platforms like Microsoft Dynamics, IBM Watson, and Google DialogFlow broadened how and where eGain could fit.

The customer profile stayed consistent with what had kept the company alive for decades: big enterprises, big contact centers, big compliance requirements. About 80% of eGain’s business came from the contact center, and the industry mix was heavily weighted toward regulated and high-stakes environments. Roy has said roughly 90% of the customer base sits in five industries: banking, financial services, and insurance; government; healthcare; telecommunications; and retail. It wasn’t the fastest path to growth—but it was exactly the kind of customer base that values reliability, governance, and institutional knowledge.

And eGain pointed to the accumulated proof. The product baked in best practices from knowledge management deployments across more than 300 enterprises globally, and the company claimed it had helped hundreds of organizations save millions while improving customer experience.

Financially, the shift toward recurring revenue was becoming clearer. In Q2 2017, SaaS revenue reached $7.7 million, up 24% year over year. Recurring revenue was $12.6 million, up 14% year over year, and made up 82% of total revenue. The ugly optics of the SaaS transition were starting to fade, and the underlying engine—knowledge management sold as a durable, renewable relationship—was easier to see.

The market, meanwhile, was getting noisier. Point solutions for chatbot building, sentiment analysis, and conversation analytics were multiplying fast, each promising a quicker path to “AI-powered service.” eGain’s argument was the opposite: that you didn’t win with a pile of disconnected tools, you won with integrated knowledge management across every channel. Whether the market would ultimately reward that integrated thesis—or keep drifting toward easier, cheaper point products—was still an open question.

VII. The COVID Catalyst & Digital Acceleration (2020-2021)

The COVID-19 pandemic forced an immediate, global experiment in digital-first customer service. Physical call centers shut down. Customers who might have tolerated long hold times suddenly expected help through chat, messaging, and self-service. And enterprises that had mapped out three-year transformation plans found themselves shopping for solutions they could stand up in weeks.

For eGain, this was the kind of moment its entire product thesis had been built around.

In its fiscal 2020 fourth quarter and full year ended June 30, 2020, eGain reported what CEO Ashu Roy described as “strong financial performance across the board.” The key signal was in SaaS: fourth-quarter SaaS revenue grew 34% year over year, reaching $15.5 million. Roy acknowledged the uncertainty of the economic outlook, but argued the company had a tailwind anyway—accelerating demand for digital customer engagement.

That acceleration carried into fiscal 2021. eGain reported SaaS revenue of $16 million, up 29% year over year. Management pointed to profitability and cash generation too: $5.8 million of operating cash in the quarter, a 31% operating margin, and a cash balance of $53 million with no debt.

The stock market noticed. From March 2020 to November 2020, EGAN climbed from $5.81 to $18.33—more than tripling as investors repriced anything tied to remote work and digital service.

On the ground, the new use cases arrived fast. Healthcare organizations rolled out virtual agents for COVID screening. Government agencies automated benefits inquiries as unemployment claims surged. Retailers, suddenly without foot traffic, shifted support volume into digital channels. After years of telling the market that customer engagement would move online, eGain watched that future show up all at once.

Roy framed it as a structural shift, not a temporary spike: enterprises were automating engagement to support contactless commerce and remote work models, and eGain expected its “digital-first platform” to help it grow share.

The company also leaned into the moment with new capabilities and offers designed to reduce friction for adoption, and it talked up early momentum. Executives highlighted “new logo momentum” and said they were confident it could continue.

Meanwhile, the industry around eGain was consolidating and financializing. NICE had already acquired inContact to build a contact center powerhouse. Five9 went public. Private equity interest across customer service tech surged. This was the kind of environment where a subscale public company often gets taken out.

eGain didn’t. It stayed independent—again. But the pandemic boost came with a catch: the stock’s run-up didn’t just validate the strategy. It raised expectations. And expectations are harder to manage when the world stops behaving like an emergency.

Still, in the thick of it, eGain had real momentum to point to. The company said its SaaS logo wins were up 100% year over year for the second quarter in a row, highlighted new-logo wins with partner Cisco, and noted that during the quarter it added its first Avaya CcaaS customers.

VIII. Generative AI Era & Current Positioning (2022-Present)

The launch of ChatGPT in November 2022 changed everything—and, for eGain, almost nothing. Generative AI made the whole world care about automated answers overnight, which validated the knowledge-management thesis eGain had been pushing for years. But it also flooded the market with new competitors and reset expectations for what “AI-powered” customer service should look like.

eGain moved quickly to productize this new wave. The company announced the general availability of eGain Instant Answers™, positioning it as a simple way for users to pull relevant answer snippets from enterprise knowledge bases using generative AI. The idea was straightforward: instead of forcing customers or agents to guess the right keywords, the system could use large language models tuned to enterprise content to surface an answer in context—even if it was buried inside a long document.

Ashu Roy framed the moment as an opening, not a threat. “Generative AI technologies like ChatGPT™ open up exciting automation possibilities in knowledge management and conversational engagement,” he said.

Then, in September 2023 at its Solve™ 23 conference in London, eGain launched eGain AssistGPT™. Built as part of eGain Knowledge Hub and powered by generative AI “out of the box,” AssistGPT was positioned as a comprehensive, zero-code approach to knowledge automation. One of the clearest promises: tasks like drafting knowledge content—work that used to take weeks—could now be done in minutes.

But eGain’s real enterprise pitch wasn’t “we have GenAI.” It was “we can make GenAI safe.”

Hallucinations are a feature of raw LLMs, not a bug—and in customer service, wrong answers aren’t just embarrassing. For regulated enterprises—banks with compliance obligations, healthcare systems with patient-safety concerns, government agencies with public accountability—confidently incorrect answers can be catastrophic. eGain’s argument was that its structured, governed knowledge foundation is what turns generative AI from a risky demo into something you can actually deploy at scale with “trusted answers.”

As Roy put it: “Given that Gen AI needs a solid knowledge foundation to deliver that value, as Gartner points out, not surprising that we are seeing more and more businesses looking to centralize and modernize the knowledge platform. So as we've been saying for a few quarters, we are doubling down on this AI Knowledge market opportunity.”

That story got a credibility boost in December 2024, when eGain said it was named a Visionary in the Gartner Magic Quadrant for the CRM Customer Engagement Center. The report evaluated 12 vendors across 15 criteria. eGain pointed to the pace of its AI-centric product additions, including an AI assistant, GenAI analytics for managers, an AI tool library for knowledge automation, and GenAI reasoning functionality for customers.

Still, the GenAI era hasn’t been a straight line up for the business.

The financial reality has been choppier than the narrative. eGain’s stock fell sharply amid revenue declines tied to the loss of two large customers, which spooked investors. On an earnings call, management said total revenue for the second quarter was $22.4 million—within guidance, but down 6% year over year—primarily because of those two prior-year client losses: one a Conversation Hub customer, the other an Analytics customer.

For fiscal year 2025, total revenue was $88.4 million, down 5% year over year. But profitability held up, and the company highlighted bookings momentum—including what Roy described as one of the largest deals eGain had ever signed. “We are pleased to close fiscal 2025 with solid bookings and strong profitability,” he said. “With one of our largest deals ever signed this quarter and healthy demand in the pipeline, we are well-positioned to capture the compelling opportunity in AI CX automation powered by trusted knowledge.”

eGain also returned capital to shareholders through buybacks, repurchasing about 630,000 shares at an average price of $5.97 per share, for a total of $3.8 million. Cash and cash equivalents were $62.9 million as of June 30, 2025, compared to $70.0 million a year earlier.

And the customer base still looked like classic eGain: regulated, operationally complex, and knowledge-heavy. Oregon Community Credit Union selected the eGain AI Knowledge Hub and AI Agent software to improve service delivery and member experience. OCCU cited eGain’s open architecture and unified platform strategy, and planned to support more than 700 users—contact center representatives using AI Agent for Contact Center for Genesys, plus enterprise users accessing portals customized for corporate and branch needs.

IX. The Founder's Journey & Company Culture

Ashu Roy has remained eGain’s CEO throughout its history. That one fact explains more about the company than any product launch ever could. Twenty-seven years at the helm means he steered eGain through the dot-com crash, the long slog of the SaaS transition, multiple recessions, and several waves of “the next big thing” in AI. In an industry where CEOs turn over fast, Roy’s tenure is the exception—and it’s a big part of why eGain feels so consistent, for better and for worse.

Roy’s career has always sat at the intersection of customer service and software. From 1988 through 1992, he worked in software engineering roles at Digital Equipment Corp. From 1993 to 1995, he co-founded Parsec Technologies, an international call center software company based in India. Long before “customer experience” became a boardroom buzzword, Roy was already building for the messy, operational reality of support teams and contact centers.

Co-founder Gunjan Sinha took a different path—but stayed connected. Sinha served as eGain’s President from 1998 to 2003 and remains on the board. Outside of eGain, he became Chairman of MetricStream, a provider of enterprise Governance, Risk, Compliance (GRC), and Quality Management software. So while Roy continued to run eGain day-to-day, Sinha provided continuity with the founding vision while focusing his operating energy elsewhere.

Roy’s leadership philosophy comes through in the shape of the business. eGain repeatedly chose durability over hypergrowth. It pushed through the SaaS transition without leaning on large, dilutive capital raises. And it kept investing in technical depth—especially knowledge management—even as competitors chased broader platform stories.

That leads to the question that’s hovered over eGain for decades: why didn’t it sell? RightNow Technologies, founded the same year, sold to Oracle for $1.5 billion. Other competitors exited too, at various points and at various prices. eGain stayed independent.

The best explanation is conviction—Roy’s belief that the company’s knowledge-centric approach to customer engagement would be more valuable over the long arc than any near-term acquisition premium. The generative AI era arguably strengthens that case, because “trusted answers” and governed knowledge suddenly matter more than ever. But the unresolved part is scale: being right about the future doesn’t automatically mean you win it.

Inside the company, the culture mirrors the founder: engineering-driven, operationally frugal, and customer-intimate. eGain serves more than 350 customers across multiple sectors, primarily enterprises with more than $500 million in revenue, and generates about half of its revenue internationally. The company employs roughly 470 professionals, about half based in India, with headquarters in Sunnyvale and offices across EMEA and APAC.

That footprint isn’t accidental. It supports a cost structure built for staying profitable at sub-$100 million revenue, especially compared to venture-backed competitors willing to burn cash to buy growth. Whether that’s disciplined stewardship or an under-investment in scale depends on what you think matters more: surviving every cycle, or swinging hard enough to dominate one.

X. Business Model Deep Dive

eGain makes money in three main ways: SaaS subscriptions, maintenance from legacy deployments, and professional services. In practice, it’s now overwhelmingly a subscription business. The company sells its software through cloud subscriptions, typically on three-year contracts, with pricing tied to things like agent seats or customer sessions. And today, the majority of revenue comes from SaaS.

That shift shows up clearly in the mix: SaaS revenue made up 93% of total revenue. Even with overall revenue under pressure, eGain still posted a non-GAAP net income of $1.3 million, or $0.05 per basic share, backed by a 29% operating cash flow margin. It’s a reminder of the company’s defining trait: it may not be growing fast, but it’s built to stay on its feet.

The gross margin tells the same story. eGain ran at a gross profit margin of nearly 70%. That’s strong software economics, but it’s not “pure SaaS” territory, because professional services pull it down. Implementation and ongoing consulting are essential for big enterprise deployments—but they’re structurally lower margin than recurring subscriptions.

Underneath the income statement, the customer economics are both eGain’s moat and its speed limit. Enterprise deployments are sticky for reasons that are hard to overstate: knowledge bases can represent years of accumulated content, workflows become embedded in day-to-day contact center operations, and compliance and security certifications can take months to earn. But the very things that make customers hard to lose also make new customers hard to win. Sales cycles stretch across quarters and sometimes years, especially in regulated industries like financial services.

That’s why the most important growth signal isn’t just “SaaS,” it’s what’s growing inside SaaS. As the company put it: "As a result, our annual recurring revenue from AI Knowledge Hub customers grew by 17% year over year and 5% sequentially." In other words, AI Knowledge Hub is outpacing the broader business—evidence that eGain’s “trusted knowledge for GenAI” positioning is landing, even if the rest of the portfolio is moving more slowly.

Management also framed how central that shift has become: "Currently, half of our revenue comes from AI Knowledge offerings." That’s a meaningful identity change. eGain increasingly looks less like a broad customer engagement suite and more like a knowledge management company—with AI as the delivery engine.

Financially, eGain kept generating cash. Cash provided by operations for fiscal 2024 was $12.5 million, or a 13% operating cash flow margin. Total cash and cash equivalents were $70.0 million as of June 30, 2024, down from $73.2 million the year before. And the company continued buying back shares: approximately 2,752,000 shares repurchased at an average price of $6.28, totaling $17.3 million.

That capital allocation choice is telling. eGain has leaned toward returning cash via buybacks instead of making aggressive acquisitions or initiating dividends. It preserves optionality and signals discipline—but it also means the company isn’t using its balance sheet to force a new growth chapter.

eGain Announces Increase to Stock Repurchase Program of $20 Million. The expansion suggests management views the shares as undervalued. It can also be read as a quieter admission: there may not be many obvious, high-confidence places to deploy cash that would materially accelerate growth.

Which brings us to the big question: scale. Revenue has hovered around the $90–$100 million range for years. To break through to $200 million or $500 million, eGain would likely need a step-change—higher sales productivity, a credible expansion into adjacent markets, or strategic M&A. Based on current trends, none of those accelerants looks imminent.

XI. Competitive Dynamics: Porter's Five Forces

Competitive Rivalry: HIGH

This is a brutal market to play in: crowded, noisy, and dominated by giants. eGain goes up against platform players like Salesforce Service Cloud and Microsoft Dynamics, contact center heavyweights like NICE and Genesys, and a long tail of specialists—ServiceNow, LivePerson, Verint Systems, BEKO Holding, and dozens more—who all want a slice of the same enterprise service budgets.

On paper, eGain can hold its own. It scores well in customer satisfaction, with a 4.7-star rating across 95 reviews, versus Oracle’s 4.2 stars across 216 reviews. In practice, though, buying decisions at the enterprise level are often less about who has the better rating and more about who’s already embedded, who can bundle, and who feels “safe.” And that’s where eGain runs into the reality of its size: it doesn’t have the reach, brand, or default-vendor status of the big suites.

Competition also comes from below. Point solutions keep popping up with cheaper, narrower promises—one for bots, one for analytics, one for agent assist. That creates constant price pressure and a kind of buyer whiplash: should a company standardize on an integrated platform, or assemble a best-of-breed stack from a dozen vendors?

eGain’s answer has been consistent: knowledge is the differentiator. It’s trying to win on depth—especially with the pace of its AI-centric product additions, including an AI assistant, GenAI analytics for managers, an AI tool library for knowledge automation, and GenAI reasoning functionality for customers. The risk is obvious, though. As AI features become table stakes, differentiation gets harder, faster, and more expensive.

Threat of New Entrants: HIGH

The barrier to entry has collapsed. With cloud infrastructure everywhere and AI tooling increasingly off-the-shelf, a small team with OpenAI APIs can ship a chatbot in weeks. That doesn’t mean they can land a major bank—but it does mean the market fills up with “good enough” options that keep pressuring incumbents on price, messaging, and attention.

eGain does have defenses: long enterprise relationships, compliance certifications, and the integration work that makes big deployments stick. But those moats aren’t as wide as they used to be. Five years ago, building credible AI required more proprietary tech and more time; today, the raw capabilities are easier to rent.

Bargaining Power of Buyers: MEDIUM-HIGH

eGain sells to sophisticated enterprises with procurement teams whose job is to create leverage. And they have plenty of alternatives.

Ecosystems matter here. Zendesk, for example, offers over 1,500 apps and integrations via the Zendesk Marketplace. eGain offers fewer than 30 integrations. That gap doesn’t automatically mean eGain loses deals—but it does mean buyers can push harder on “why you” and “why now,” especially when they’re comparing against platforms that plug into everything.

Switching costs still exist—moving knowledge, retraining agents, redoing workflows—but modern APIs and integration tooling are slowly chipping away at the friction.

Where eGain can push back is in vertical specialization. In regulated industries, details matter: financial services knowledge models, compliance frameworks, and domain expertise that horizontal platforms often struggle to replicate. For certain buyers, that specificity is worth paying for.

Bargaining Power of Suppliers: LOW

On the supplier side, eGain is in a better spot. Cloud infrastructure is largely commoditized across AWS, Azure, and Google Cloud. Many AI and ML tools are open source, and no single vendor controls eGain’s fate. Talent is competitive, but eGain’s development footprint in India helps keep costs manageable. Overall, suppliers don’t have much leverage here.

Threat of Substitutes: MEDIUM-HIGH

The biggest substitute isn’t a rival product—it’s “we’ll build it ourselves.”

Enterprises can increasingly stitch together customer service automation by combining OpenAI APIs, vector databases, and open-source frameworks. And on the other end of the spectrum, Microsoft and Salesforce keep bundling more AI into their platforms, making it tempting for customers to standardize and reduce vendor sprawl.

eGain’s counter-argument is that the hard part isn’t generating language—it’s governing knowledge. A specialized knowledge architecture, built for accuracy and compliance, is tougher to replicate than a generic LLM wrapper. But the market is still working through a fundamental question: does generative AI make structured knowledge management more important, because it needs grounding—or less important, because it can “just read the docs”?

XII. Hamilton's Seven Powers Analysis

Scale Economies: ❌ WEAK

eGain doesn’t get the benefits of scale that the giants do. When you’re competing with Salesforce or Microsoft, you’re up against companies that can spread massive fixed costs across huge revenue bases. eGain’s SaaS model does create some operating leverage, but at its current size it doesn’t translate into the kind of per-unit cost advantage that changes the game.

Network Effects: ❌ NOT APPLICABLE

There’s no flywheel here. Customer engagement software doesn’t really get stronger because more companies use it. Each deployment is its own enterprise project, with its own knowledge base, workflows, and integrations. eGain wins or loses on the direct value it delivers, not on network-driven pull.

Counter-Positioning: ⚠️ HISTORICAL, FADING

For years, eGain had a clear contrarian stance: knowledge-first beats CRM-first. In the 2000s and 2010s, incumbents treated structured knowledge management as extra complexity. eGain insisted it was the foundation.

That bet paid off. But now it’s no longer contrarian—everyone agrees knowledge is critical, especially in an AI world. That means the advantage shifts from being early to being better. Execution matters more than insight.

Switching Costs: ✅ MODERATE-STRONG

Once eGain is embedded, it’s hard to rip out. Migrating a knowledge base isn’t like swapping a chat widget. It means moving content libraries and taxonomies, rebuilding integrations, retraining agents, and revalidating compliance and security requirements. In financial services, that stickiness gets even stronger because the bar for change is higher.

Still, the moat isn’t permanent. Modern APIs and more standardized tooling are slowly making it easier to switch. The friction is real, but it may be declining over time.

Branding: ❌ WEAK

eGain is still not a default name in enterprise tech. Compared to companies like Zendesk, it has fewer public reviews and fewer widely recognized proof points, which matters when buyers are making shortlist decisions. eGain does have a strong reputation in certain verticals—especially banking and government—but that credibility doesn’t automatically carry into broader awareness or easier new-customer acquisition.

Cornered Resource: ⚠️ PARTIAL

eGain has accumulated real domain expertise in knowledge management, plus deep experience in regulated industries like financial services. Roy’s long tenure adds continuity, and decades of customer deployments generate practical insight competitors don’t get from a slide deck.

But it’s not an unassailable resource. There’s no single exclusive dataset, dominant patent wall, or irreplaceable asset that prevents a well-funded competitor from narrowing the gap—especially if parts of the advantage are tied closely to key people.

Process Power: ✅ MODERATE

This may be eGain’s most underrated strength: the muscle memory of running complex enterprise deployments for decades. The company positions this as a repeatable playbook in the eGain AI Knowledge Method™, aimed at delivering business value quickly from AI and knowledge.

That kind of process discipline shows up in the numbers too: eGain has managed to stay profitable at a scale where many competitors would be tempted to burn cash. And in regulated industries, compliance expertise—FINRA, HIPAA, and similar frameworks—compounds into a practical edge over time.

Summary: eGain’s strongest powers are Switching Costs and Process Power. It doesn’t have the Scale Economies or Branding that produce category dominance, and its counter-positioning edge has largely expired now that “knowledge + AI” is table stakes. To stay durable—and maybe finally break out—eGain needs to deepen the integration between AI and governed knowledge, and keep expanding where its vertical depth is hardest to copy.

XIII. Bear vs. Bull Case

🐻 Bear Case

Too Small to Matter: At roughly a $150 million market cap and about $90 million in annual revenue, eGain is playing a game dominated by companies like Microsoft, Salesforce, and Zendesk—players with effectively bottomless R&D and go-to-market budgets. Even if eGain’s product is strong, the platforms can outspend, out-market, and out-bundle.

GenAI Disruption: Large language models could make structured knowledge management feel optional. If companies can point an LLM at messy internal documents and still get reliable answers, the need to curate and govern a formal knowledge base shrinks. If the “garbage in, garbage out” problem gets solved at the model layer, eGain’s core value proposition gets squeezed.

Growth Stagnation: Revenue has hovered around the $90–$100 million range for years, which suggests the company has struggled to break into a higher growth gear. And concentration risk is real at this scale: management said total revenue for the first quarter fell 10% year over year, primarily due to losing two large customers in the conversation and analytics business.

Founder Risk: A 27-year CEO tenure is a testament to consistency—but it also raises the succession question. Roy has been the strategy, the product instincts, and the operating discipline for decades. Any eventual transition introduces real uncertainty.

Commoditization: Customer service AI is quickly becoming table stakes. Every CRM suite, contact center platform, and CX vendor now ships “AI features,” and that trend makes differentiation harder and price pressure more intense. When everyone sounds the same, margins usually suffer.

Acquisition Risk: eGain could be an attractive takeout for private equity at a modest multiple. Shareholders might get a near-term premium, but the company could be absorbed before any longer-term upside from an AI-led breakout materializes.

🐂 Bull Case

AI Renaissance: Generative AI may create more need for knowledge grounding, not less. As Roy has put it: "Given that Gen AI needs a solid knowledge foundation to deliver that value, as Gartner points out, not surprising that we are seeing more and more businesses looking to centralize and modernize the knowledge platform."

Enterprise Trust: In banking, healthcare, and government, hallucinations aren’t a funny demo failure—they’re a compliance and reputational nightmare. eGain’s pitch is that explainable, auditable knowledge models are exactly what regulated enterprises need to deploy AI without losing control.

Profitable & Durable: eGain has survived for 27 years by staying profitable and cautious. It ended fiscal 2025 with what it described as “solid bookings and strong profitability,” and it had about $63 million in cash. The company isn’t dependent on capital markets to keep operating.

Undervalued: eGain trades at lower revenue multiples than many SaaS peers, and a re-rating is possible if growth returns. The bull view is simple: if AI Knowledge keeps growing while overall revenue stabilizes, investor perception can change faster than the business itself.

Vertical Depth: eGain’s strength in regulated industries creates defensibility—and a path to expand further in areas like healthcare and government, where compliance and governance are central requirements, not checkboxes.

Platform Play: In the best case, eGain becomes the trusted knowledge layer behind many AI agents—less a flashy front-end and more foundational infrastructure. The thesis is that in enterprise AI, knowledge governance becomes the scarce asset, and eGain is already built around it.

M&A Upside: A strategic acquisition by Salesforce, NICE, Genesys, or Microsoft remains plausible at a premium to today’s valuation. For a platform company, buying credibility in knowledge management—plus the customer base and deployments that come with it—could be an efficient shortcut versus building it all from scratch.

XIV. What Would Need to Be True for eGain to 10x?

For eGain to go up ten-fold from here, it would need to become roughly a $1.5 billion company. That doesn’t happen by accident. It would take some combination of a real growth surge, a market that suddenly values eGain’s kind of business much more highly, or a buyer willing to pay a premium for what eGain has built.

Scenario 1: Category King

eGain becomes the enterprise knowledge platform for AI agents, owning 40%+ share in the verticals where it already has credibility. That would mean: - A meaningful step up in sales and marketing investment to create more pipeline - Faster product velocity so “knowledge + AI” doesn’t get commoditized out from under them - Brand building beyond the industries where eGain is already known - Expanding deeper into healthcare, government, and adjacent regulated industries where trust and compliance are non-negotiable

Scenario 2: Acquisition Premium

A strategic acquirer buys eGain at a premium—paying something like 5–8x revenue—to instantly add knowledge management and governed AI capabilities. Think Salesforce, Microsoft, NICE, or Genesys looking to close a gap rather than build it themselves. For this to happen, eGain would likely need: - Continued profitability plus enough growth to make the story feel “strategic,” not distressed - Clear proof that eGain’s knowledge layer materially improves AI outcomes in the real world - The kind of competitive tension that creates an auction, not a single-bid outcome

Scenario 3: Accelerated Growth

eGain breaks out of the $90–$100 million revenue gravity and pushes past $200 million in ARR, with improving unit economics, and the market re-rates it like a real SaaS grower again. That would require: - AI Knowledge products sustaining 30%+ growth and becoming the obvious center of gravity - A successful expansion of sales capacity that actually translates into new logos - Holding onto the large, sticky base while layering in new customers fast enough to change the growth profile

Scenario 4: Platform Shift

Generative AI makes knowledge management feel like critical enterprise infrastructure—like data platforms in the big data era—and eGain gets positioned more like “Snowflake for customer knowledge.” For that to be true, you’d need: - Broad market recognition that knowledge governance is foundational to enterprise AI, not optional - Technical leadership in the unglamorous but decisive work: knowledge graphs, LLM integration, and safety controls - A partner ecosystem that builds on top of eGain’s platform instead of treating it as a standalone tool

XV. Lessons for Founders & Investors

For Founders:

Survival is underrated. eGain outlasted dozens of competitors by staying disciplined when the market rewarded chaos. When cycles turn, cash flow and cost control matter more than whatever the hype cycle is selling.

Product-market fit evolves. The thing customers paid for in 1997 (email management) wasn’t the thing they needed most in 2010 (knowledge management), and it isn’t the thing they’re desperate for now (a governed, GenAI-ready knowledge platform). The companies that make it across decades don’t “pivot” once—they keep translating their core strengths into whatever the next interface becomes.

Staying independent has costs. Control versus resources is a real trade. Roy chose control, protected product direction, and kept the company from being absorbed too early. The price was obvious: less capital, less go-to-market muscle, and less room to force growth the way venture-backed competitors can.

Technical depth compounds. Twenty-seven years of domain knowledge in customer engagement and applied AI is hard to fake and hard to rebuild. In enterprise software, deep expertise in a narrow, painful problem can beat broad capability—especially when customers are regulated, risk-averse, and tired of “generic” solutions.

Founder-CEO longevity cuts both ways. A long-running founder vision creates coherence—product decisions stack on top of each other instead of getting rewritten every few years. But it can also reduce outside perspective. The same conviction that avoids a premature exit can also limit the appetite for strategic risk.

For Investors:

Value traps versus hidden gems. Is eGain a durable niche player that stays small forever, or a coiled spring that finally gets revalued in a world where AI needs trusted knowledge? The answer hinges on a single question: does knowledge governance become more valuable as LLMs spread, or does it get bypassed?

Small-cap software risks. Limited liquidity, light analyst coverage, and fewer natural buyers can keep a stock mispriced for a long time. If you want the upside, you also have to tolerate the waiting.

Enterprise stickiness masks growth challenges. Low churn is great for cash generation—and it can still coexist with a new-logo problem. Retention tells you the product is embedded; new business velocity tells you whether the story is expanding.

AI hype cycles. eGain has lived through multiple “AI moments.” The current GenAI wave could turn into real demand—or it could stay stuck at pilots and demos. Don’t confuse excitement about the category with proof of acceleration in the business.

Public comps mispricing. Markets often overlook profitable, cash-generating software companies in unsexy categories. Sometimes that’s a mistake; sometimes it’s a warning. The difference is whether the company can translate durability into growth, not just survival.

Key Performance Indicators to Monitor:

-

AI Knowledge Hub ARR Growth Rate: The cleanest signal of whether eGain’s “trusted knowledge for GenAI” positioning is turning into real momentum. Management has pointed to 17% year-over-year growth here, which is exactly the kind of line you’d want to see keep moving up and to the right.

-

Net Revenue Retention: In enterprise SaaS, expansion is the difference between a stable base and a compounding business. If eGain can consistently upsell AI Knowledge capabilities into its installed base, revenue can re-accelerate without needing a dramatic spike in new logos.

XVI. Epilogue: The Road Ahead

As 2025 draws to a close, eGain sits at a familiar crossroads: proven enough to matter, too small to relax.

In its fiscal 2025 fourth quarter and full-year results (year ended June 30, 2025), the company leaned on the same message it’s leaned on through multiple cycles: bookings held up, profitability held up, and the strategy is still intact. “We are pleased to close fiscal 2025 with solid bookings and strong profitability,” CEO Ashu Roy said.

One item in those results was unusually large, and unusually telling: a tax benefit of approximately $29.0 million from releasing a majority of the company’s valuation allowance in Q4 2025. It’s accounting, yes—but it’s also a signal. Companies don’t release valuation allowances unless they believe future profitability is more likely than not. In plain terms, management was saying: we think the business has enough earnings power ahead to use these tax assets.

Capital allocation told a similar story. The company expanded its stock repurchase program by $20 million. That’s a vote of confidence in the value of the shares—and a clue about posture. eGain is choosing to return cash and stay disciplined, rather than swing big with aggressive expansion.

Outside the walls of Sunnyvale, the market is moving again. Contact center consolidation keeps pushing enterprises toward unified platforms. Agentic AI is emerging as the next leap—from bots that answer questions to systems that complete tasks end-to-end. And voice is back on the agenda as speech recognition and natural language understanding keep improving.

All of that is opportunity. It’s also pressure.

Salesforce and Microsoft are embedding AI deeper into their service stacks. Contact center giants keep expanding the surface area of what they bundle. And an endless stream of startups is shipping “AI customer service” features at startup speed. The result is a category that’s both crowded and confusing: point solutions everywhere, platforms trying to swallow them all, and buyers trying to decide what’s real versus what’s a demo.

That’s where eGain’s differentiation either becomes decisive—or gets drowned out. Deep knowledge management, vertical expertise, and enterprise trust matter most in the places eGain already knows well: regulated industries where accuracy is not a nice-to-have, and where the cost of a wrong answer is measured in compliance risk, customer harm, or brand damage.

So the existential question doesn’t really change, even as the technology does: in 2030, is eGain a billion-dollar company, or a footnote in the history of customer service software?

The answer hinges on the bet eGain has been placing, in one form or another, since the beginning: that the “knowledge layer” is the infrastructure layer. That enterprises won’t trust pure generative approaches without governed, structured knowledge underneath—and that the vendors who own that layer will own the outcomes.

eGain’s story, in the end, is about endurance and the difficulty of scaling in enterprise software when you don’t have platform gravity on your side. Roy’s original thesis—that customer engagement would go digital, and that knowledge would be the key to getting answers right—looks more relevant than ever. The remaining question is whether relevance finally turns into scale.

And that’s the real lesson here. In enterprise software, surviving isn’t just about being early. It’s about evolving the product, staying financially disciplined, and having the patience to let bets play out over decades. eGain has done the first two. The GenAI era will decide the third.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube