Everest Group, Ltd. (NYSE: EG): The Bermuda Engine and the Casualty Trap

I. Introduction & The Everest Paradox

Picture a trading floor in Hamilton, Bermuda, on a January morning. Outside, the Atlantic is calm and turquoise. Inside, a small team of underwriters is deciding, in a matter of hours, how many billions of dollars of hurricane, earthquake, and wildfire risk the firm will carry into the coming year. There are no branch offices to visit, no armies of retail agents to manage—just a fortress balance sheet, a set of catastrophe models, and the nerve to say yes or no at a scale that would terrify almost any other financial institution. This is Everest at its best: quiet, lean, and astonishingly efficient at renting out its capital to insure the world against its worst days.

Now hold that serene image next to a very different one. In early February 2025, the same company disclosed that it had torn a hole in its own balance sheet—not from a hurricane, not from an earthquake, but from lawyers. Everest booked a net loss of $593 million for the fourth quarter of 2024, driven by roughly $1.7 billion of reserve strengthening, most of it in unglamorous US casualty lines it had been writing to reduce volatility.1 Weeks earlier its chief executive had resigned.2 The property-catastrophe machine that could earn 20%-plus returns in a hard market had nearly given back years of accumulated equity by wandering into the invisible, slow-fuse world of American liability litigation.

That is the Everest paradox, and it is the spine of this story. How does a business celebrated for underwriting discipline in the most violent, headline-grabbing risks on earth end up humbled by the boring stuff—commercial auto, general liability, excess casualty—where the losses don't arrive in a single terrible week but ooze out over a decade?

The deeper irony is that Everest walked into the casualty trap in pursuit of safety. Property catastrophe is thrilling and terrifying: a single hurricane can wipe out a quarter's earnings, and public-market investors, who reward predictability, had grown weary of a company whose results swung with the weather. Casualty insurance was supposed to be the calm harbor—steady premiums, no correlation to storms, the ballast that would smooth the ride and win a higher valuation. Instead, the calm harbor turned out to be mined. The very quest to reduce visible volatility imported a slower, deeper, and far more destructive kind. That is not just a story about one insurer's reserving miss; it is a parable about the seductions of diversification, and about how the risks that destroy you are usually the ones you cannot see coming because they haven't happened yet.

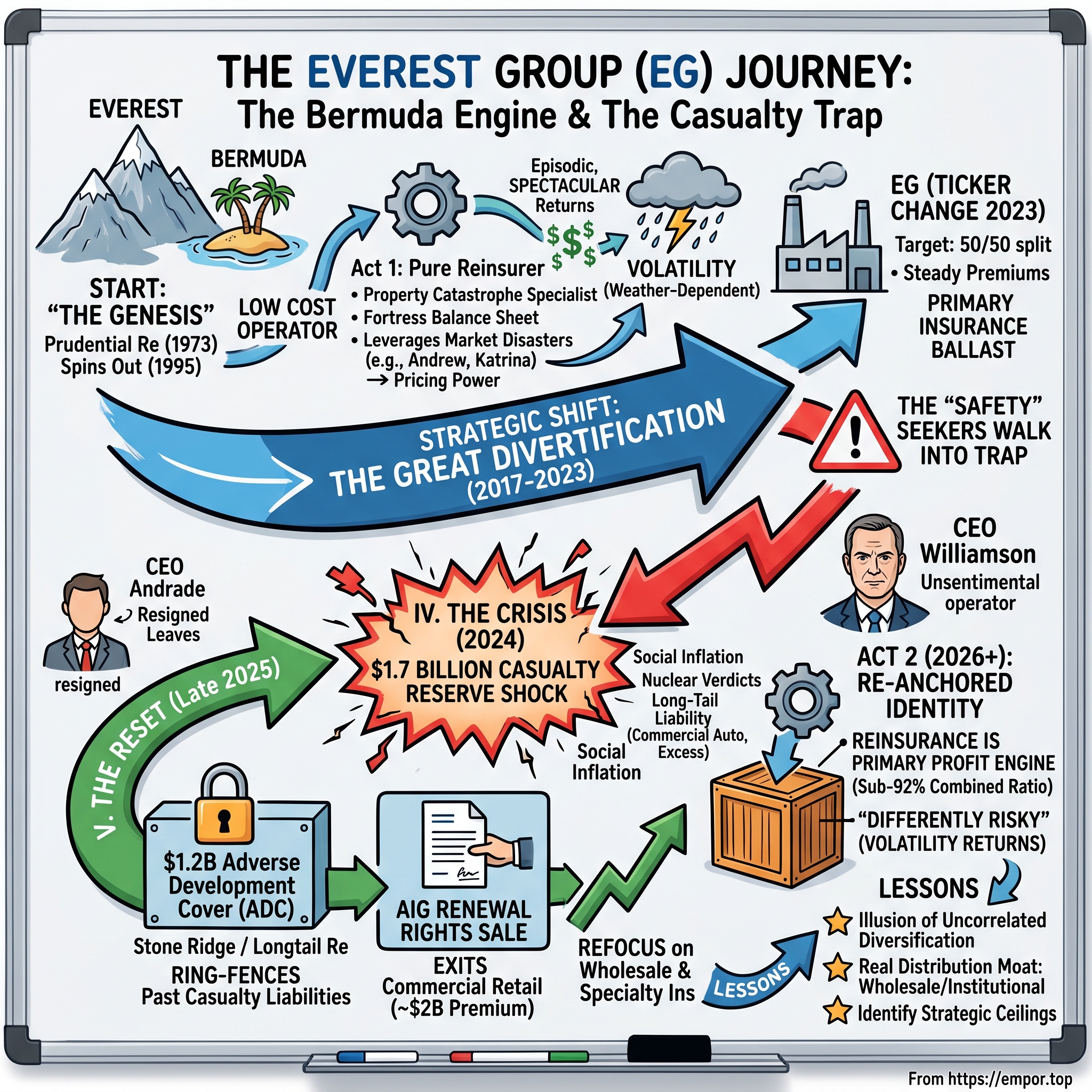

Here is the roadmap. The Genesis: a 1973 Prudential subsidiary that spun out, went public, and redomiciled to Bermuda to become one of the world's leanest reinsurers. The Great Pivot: the July 2023 rebrand from Everest Re (ticker RE) to Everest Group (EG), a public declaration that it was no longer just a reinsurer but a diversified insurer chasing a 50/50 split between reinsurance and primary business.3 The Crisis: the casualty reserve shock of 2024 that cost CEO Juan Andrade his job. The Reset: the defensive campaign that Jim Williamson ran through late 2025—buying a $1.2 billion adverse development cover backed by Stone Ridge's Longtail Re, and selling the renewal rights to its ~$2 billion global commercial retail book to AIG—to shrink Everest back toward what it actually does well.[^4]4

A word on posture before we begin. This is not a victory lap for management, nor an indictment. Everest's leaders have made confident claims about being "a more focused, higher-return enterprise."5 Our job is to ask what evidence supports those claims, what would falsify them, and where the story is genuinely unresolved. The interesting question is not whether Everest is good at reinsurance—it is—but whether the events of 2024 and 2025 reveal a one-time misadventure or a deeper truth about how hard it is to diversify a volatility business. Let's start at the beginning, with a mountain and a name.

II. The Genesis: Prudential Re, IPO, and the Bermuda Moat

Every good origin story needs a parent that underestimates the child. Everest's parent was one of the largest financial institutions in America. Incorporated in Delaware in June 1973 and run out of Newark, New Jersey, Prudential Reinsurance Company was built as a captive muscle inside Prudential Financial—a place to write large, high-capacity risks that the insurance giant wanted on its books.6 For two decades it was a subsidiary, not a franchise: competent, well-capitalized, and largely invisible.

The transformation came in the mid-1990s, when Prudential decided reinsurance was not core and chose to set the business free. On October 6, 1995, the company listed on the New York Stock Exchange, with Joseph Taranto—a hard-nosed underwriter who would define the firm's culture for the next fifteen years—as chairman and CEO.6 The chosen name was pure branding theater and pure strategy at once: Everest, the highest point on earth, a metaphor for permanence, altitude, and the one thing a reinsurer sells above all else—the credible promise that it will still be standing after the disaster. In a business where a customer buys a balance sheet's ability to pay a claim years or decades later, projecting immovable solidity is not marketing fluff. It is the product.

Then came the move that shaped Everest's economics for a generation. In 2000, the company completed a corporate reorganization that placed a newly created Bermuda holding company—Everest Re Group, Ltd.—atop the structure as the ultimate parent.6 To understand why a New Jersey reinsurer sailed for Hamilton, you have to understand three simultaneous advantages that Bermuda offered around the turn of the millennium.

The first was tax. Bermuda levied no corporate income tax, so a holding company domiciled there could compound underwriting profits and investment income without the drag that burdened US-domiciled peers—capital that could then be recycled into more underwriting. The second was regulatory. The Bermuda Monetary Authority built a supervisory regime that was rigorous on solvency but fast and flexible on capital deployment, letting reinsurers stand up and stand down enormous amounts of capacity as the cycle turned.7 The third was gravitational: Bermuda had become the physical and intellectual capital of the global catastrophe-reinsurance market, a few square miles where the brokers, the modelers, and the money all sat within walking distance. Domiciling there put Everest inside the room where the world's disaster risk gets priced.

It is worth being clear-eyed that this maneuver—an American company relocating its holding-company parent to a zero-tax island—was a species of what would later be politically branded a corporate "inversion," and it drew its share of scrutiny over the following two decades as Washington periodically debated whether offshore reinsurers were unfairly advantaged. For a long stretch, the arbitrage held and compounded. But an advantage born of a specific tax and regulatory gap is only as durable as the gap itself, and the global tax reforms of the 2020s—chiefly the international push toward a minimum corporate tax—have been steadily narrowing exactly the edge that made Bermuda so attractive in 2000. That erosion is a slow-moving fact worth holding in mind as we assess how much of Everest's structural moat is permanent versus borrowed from a policy environment that is changing.

Out of these ingredients Everest built the moat that mattered most in its first act: it became a ferociously low-cost operator. Where the European titans carried the overhead of sprawling global bureaucracies, Everest ran lean, keeping its expense ratio structurally below the likes of Swiss Re and Munich Re. In reinsurance—a commodity-adjacent business where everyone is ultimately renting out capital against the same catastrophe models—being the low-cost provider is a durable edge. It means you can accept the same premium as a rival and keep more of it, or undercut a rival and still make money. That structural thriftiness, more than any single clever trade, is the quiet engine beneath everything that follows.

There is a broader piece of context worth planting here, because it explains why Bermuda—and Everest with it—came to matter so much. The modern Bermuda reinsurance market was, in large part, forged by disaster. After Hurricane Andrew flattened South Florida in 1992, and again after the September 11 attacks in 2001, and once more after Hurricane Katrina in 2005, waves of fresh capital rushed to the island to stand up new reinsurers—the industry literally nicknamed these cohorts the "Class of 2001" and the "Class of 2005." Each catastrophe destroyed capacity, spiked prices, and drew billions in opportunistic capital to Hamilton to write the newly expensive risk. Everest, already established, was perfectly positioned to ride each of these hard markets without having to raise money from scratch. It had the balance sheet, the ratings, and the low cost base to lean in when others were still incorporating.

The company's leadership through this era reinforced the underwriting-first culture. Joseph Taranto ran the firm as a disciplined risk-taker into the early 2010s; Dominic Addesso, a finance executive who had risen through the organization, took the CEO seat in 2013 and pushed Everest to modernize how it sourced capital.6 The signal innovation of the Addesso years was Mt. Logan Re, launched in 2013—a vehicle that let outside investors, from pension funds to specialist asset managers, put their own money directly behind Everest's catastrophe book in exchange for a share of the returns.6 This was Everest quietly joining the insurance-linked securities revolution, effectively turning its underwriting franchise into an asset-management platform that could deploy other people's capital against catastrophe risk and earn fees for the privilege. It was a smart, capital-light way to grow the top line without straining Everest's own balance sheet. Two years later, in 2015, the company formalized its primary-insurance ambitions under the Everest Insurance brand—the seed of the diversification story that would later flower and then wither.6 And in 2017 Everest was admitted to the S&P 500, the establishment's stamp on a company that had grown from a Newark subsidiary into a global top-ten reinsurer.6

That structural thriftiness and capital flexibility, more than any single clever trade, is the quiet engine beneath everything that follows. And to see why it mattered so much, we need to open up the machine itself.

III. Reinsurance 101: Inside the Property Catastrophe Engine

Start with a homeowner in Florida. She pays State Farm or Allstate a premium, and in return the insurer promises to rebuild her house if a hurricane flattens it. That's insurance. Now zoom out: the insurer has written hundreds of thousands of those promises across a single stretch of coastline. One bad storm could bankrupt it, because all those individual risks are secretly the same risk—they all depend on where the hurricane makes landfall. So the insurer does what the homeowner did. It buys insurance on its insurance. That is reinsurance, and the company selling it—taking on the concentrated, correlated, catastrophic tail—is a reinsurer like Everest.

The magic and the menace of this business is that the reinsurer is deliberately holding the risks that cannot be diversified away at the primary level. A reinsurer's whole art is assembling enough geographically and structurally uncorrelated catastrophes—a Japanese earthquake here, a Gulf hurricane there, a European windstorm, a US tornado outbreak—that its overall book is survivable even though every individual piece is terrifying. It is diversification by portfolio construction, priced with catastrophe models that estimate, for a given book of exposures, how much loss a "1-in-100-year" or "1-in-250-year" event would inflict.

Now the part that makes this an investment story rather than a science lesson: the pricing is savagely cyclical. Reinsurance breathes in and out on a rhythm the industry calls the soft market and the hard market. In a soft market, capital is abundant, everyone is chasing the same deals, prices grind lower, contract terms get looser, and returns sink toward or below the cost of capital. Then something breaks. A cluster of megacatastrophes—the textbook example is the 2017 hurricane trio of Harvey, Irma, and Maria—burns through the industry's capital, sometimes compounded by a bout of macro inflation that raises the cost of every rebuild. Capacity evaporates. Suddenly the reinsurers, not the buyers, hold the whip. In a hard market, renewal rates can leap 30% to 50%, reinsurers push their "attachment points" higher so cedents absorb more of the smaller losses themselves, and terms tighten across the board. The years that follow a capital-destroying catastrophe are, paradoxically, the most profitable years to be a reinsurer—if you kept enough capital to still be underwriting when the price finally turned.

That single sentence explains most of the strategic behavior in this industry, including Everest's. The prize goes to the disciplined balance sheet that has dry powder precisely when frightened competitors are pulling back.

Two more mechanics complete the picture, and both matter for understanding Everest. The first is retrocession—reinsurance for reinsurers. Just as a primary insurer offloads its concentration to a reinsurer, a reinsurer can offload its peak concentrations to yet another layer of the market. This is the same principle that would later underpin the adverse development cover Everest bought in 2025; retroactive reinsurance is simply retrocession pointed backward in time, at losses that have already been incurred but not yet fully paid. The second mechanic is the rise of alternative capital, and it has quietly reshaped the whole industry over the past fifteen years. Pension funds, sovereign wealth funds, and specialist hedge funds discovered that catastrophe risk—being uncorrelated with stocks and bonds—was an attractive thing to own, and they found ways to own it directly through instruments like catastrophe bonds and insurance-linked securities (ILS). A cat bond, in plain terms, is a bond that pays a fat coupon but wipes out the investor's principal if a specified catastrophe occurs; the sponsor gets reinsurance-like protection, and the investor gets a high yield in exchange for taking hurricane or earthquake risk. This flood of third-party capital—the same pool Everest tapped through Mt. Logan Re—has become a structural force that dampens how hard the hard markets can get, because when reinsurance prices spike, ILS money rushes in to arbitrage the opportunity. Any bull case that assumes catastrophe pricing stays elevated forever has to reckon with this ever-ready wall of alternative capital waiting to compete it back down.

The prize, then, goes to the disciplined balance sheet with dry powder—but the size of the prize is capped by how quickly outside capital can flood the trade.

The 2017 season is the cleanest illustration of how this cycle actually turns, and it is worth living inside it for a moment. In the span of a few weeks that autumn, Hurricane Harvey drowned Houston, Irma raked Florida, and Maria devastated Puerto Rico, while wildfires burned through California wine country. The industry absorbed one of its costliest catastrophe years on record, and reinsurers' capital was visibly dented. For a company like Everest, a year like that is a paradox: the immediate hit to earnings is painful, but the aftermath is where the money is made, because the capital destruction pushes the next January's renewal prices sharply higher and lets disciplined survivors re-underwrite the same risks at far better rates. The reinsurers who kept their balance sheets intact through the storm got to reprice the world afterward. This is precisely why balance-sheet strength and a low cost base are not merely defensive virtues in reinsurance—they are the mechanism by which a firm converts other people's catastrophe losses into its own future profits. Understanding that dynamic is essential to reading everything Everest did next, including its fateful decision that surviving the property cycle was not enough and that it needed a steadier second engine.

Who is in the ring? At the top sit the balance-sheet titans—Munich Re, Swiss Re, Hannover Re, and Berkshire Hathaway's reinsurance operation—firms whose sheer scale lets them absorb losses that would cripple a smaller player. A tier down sit the specialty and Bermuda peers: RenaissanceRe, which vaulted up the league tables after acquiring Validus from AIG in 2023; Arch Capital; and PartnerRe. Everest lives in the top ten globally, carrying an A+ financial-strength rating from A.M. Best that it has reaffirmed even through the recent turmoil.8 Its calling card in this crowd has always been speed and capacity: the ability to put down a very large, thoughtfully priced line on a big property-catastrophe program faster than most rivals, precisely because it is lean enough and well-capitalized enough to move.

For an investor, the takeaway is that a pure property-catastrophe reinsurer is a machine for converting balance-sheet strength and underwriting nerve into episodic, sometimes spectacular, returns—punctuated by years where a bad catastrophe season simply eats the profit. Which raises an obvious and fateful question, one that Everest's leadership asked out loud in the early 2020s: what if you could smooth out those violent swings? What if you could bolt a steadier, less catastrophe-exposed business onto the side of the engine? The answer to that question is where the trouble begins.

IV. The Great Diversification: The Siren Song of Primary Insurance

Between roughly 2017 and 2021, something unsettling happened to the reinsurance business, and it happened in a form the models were slow to catch. The headline megacatastrophes—the giant hurricanes and earthquakes—were manageable. It was the secondary perils that kept spoiling the year: wildfires ripping through California, winter storms freezing Texas, and above all the relentless drumbeat of severe convective storms—hail, straight-line winds, tornadoes—that individually look small but collectively pile up into billions of dollars of losses. Year after year, these "attritional" catastrophes dented Everest's property-reinsurance earnings, and public-market investors, who prize predictability, grew visibly impatient with a company whose quarterly results swung with the weather.

Enter Juan Andrade. Everest brought him in—first as head of the insurance business, then as group CEO in 2020—from Chubb, the gold standard of disciplined commercial insurance. That pedigree is central to the story's irony. Andrade arrived carrying the aura of the industry's most respected underwriting culture, precisely the credential that made his primary-insurance build-out credible to Everest's board and to Wall Street. Who better to construct a world-class commercial-casualty franchise than a lieutenant from the house that Evan Greenberg built? His mandate was explicitly to build a counterweight. If reinsurance earnings were a rollercoaster, the theory went, then a large, diversified primary insurance arm—Everest Insurance—could act as ballast: writing commercial casualty and specialty coverage whose premium streams were steadier and, crucially, uncorrelated with the hurricanes and earthquakes that whipsawed the reinsurance book. Diversify the risk, smooth the earnings, and the market would reward the stock with a higher, more stable multiple. It is a seductive logic, and it was the consensus wisdom of the moment—the very playbook that peers like Arch and RenaissanceRe were pursuing in their own ways.

Andrade's Everest grew the insurance segment aggressively. Over his tenure the company pushed the insurance arm from a modest fraction of the whole toward a genuine second pillar, hiring underwriting teams, opening distribution, and stacking on premium at a pace that looked, from the outside, like disciplined expansion into a hardening commercial market. The growth was real, and for a few years it flattered the diversification narrative. The problem, invisible at the time, was in the composition of that growth: a great deal of it was concentrated in exactly the long-tail US casualty lines whose true cost would not reveal itself for years.

The strategy reached its symbolic climax in July 2023, when the company retired the name that had carried it since the 1990s. Everest Re Group became Everest Group, Ltd., and the ticker changed from RE to EG.3 This was not cosmetic. Dropping the "Re" was a deliberate signal to Wall Street that the company no longer wished to be valued as a mere reinsurer; it was a diversified global insurance platform, publicly targeting something close to a 50/50 balance between its reinsurance and insurance segments. Management was, in effect, asking the market to re-rate the business on the promise of smoother, more balanced earnings.

There is a subtle governance hazard buried in a target like "50/50," and it is worth flagging because it helps explain what went wrong. Once a company publicly commits to rebalancing toward a segment, the target itself becomes a source of pressure: growing the smaller side becomes a strategic imperative, and strategic imperatives have a way of overriding underwriting caution. If the mandate is to build a primary insurance business large enough to balance the reinsurance book, the fastest way to hit that number is to write more premium—and the fastest way to write more premium in a competitive market is to be a little less picky about price and terms than the most disciplined competitor. Growth targets and underwriting discipline are natural adversaries, because discipline sometimes means walking away from business, which is the opposite of hitting a growth number. Whether Everest's actuaries were pressured, or merely wrong, is not something an outsider can prove; but the structural incentive to grow into casualty at exactly the wrong price was undeniably present, baked into the very ambition management was celebrating.

The segment economics tell you what each side was supposed to contribute. Reinsurance had long been the profit engine, historically generating the lion's share of underwriting income—but with the volatility we've described. Insurance came with a heavier cost structure: primary insurance means paying brokers, staffing regional offices, and handling far more individual policies, all of which loads the expense ratio. The bargain was that you accepted that operating drag in exchange for premium that was supposed to be steady and diversifying. On paper, adding a low-correlation earnings stream to a volatile one is textbook portfolio theory. You reduce total volatility without necessarily sacrificing return.

But here is where an independent eye has to interrupt the tidy narrative. The specific flavor of primary insurance Everest leaned into to build that ballast was US casualty—long-tail liability lines. And long-tail casualty carries a form of risk that is fundamentally different from a hailstorm. A hailstorm's loss is knowable within days. A casualty policy's true cost may not be known for a decade, because it depends on how American courts, juries, and plaintiffs' lawyers behave years after the policy was written. Everest was trying to cure the visible volatility of property by importing the invisible volatility of casualty—and invisible volatility is the most dangerous kind, because you can convince yourself it isn't there right up until it detonates. That detonation is the next section.

V. The Casualty Trap & The $1.7 Billion Shock

To understand what went wrong, you first have to understand a phrase that has quietly become one of the most expensive in American finance: social inflation. It is not the inflation of consumer prices. It is the inflation of legal costs—the steady, compounding rise in the size of jury awards and legal settlements, running well ahead of general economic inflation. Three forces feed it. First, litigation funding: hedge funds and specialized investors now bankroll plaintiffs' lawsuits as an asset class, giving trial lawyers the staying power to push cases toward ever-larger payouts. Second, "nuclear verdicts"—jury awards of tens or hundreds of millions of dollars that would have been unthinkable a generation ago, as juries grow more willing to punish corporate defendants. Third, medical inflation, which raises the cost of the injury claims sitting at the heart of most liability cases. Together they mean that a policy written in, say, 2019 to cover a trucking company's liability can end up costing the insurer far more than the models assumed when the premium was set.

Now layer on Everest's specific behavior. To hit the aggressive premium-growth targets that the diversification strategy demanded, Everest's insurance arm wrote a great deal of North American high-limit excess casualty, general liability, and commercial auto through roughly 2019 to 2023. In the rush to build scale, it appears to have systematically underestimated how fast historical loss trends were compounding—pricing the tail as if the old actuarial patterns still held while social inflation was quietly bending the curve upward. This is the underwriting blind spot at the center of the whole affair.

It is worth pausing on why commercial auto and excess casualty in particular became such traps, because the specifics illuminate the whole industry's blind spot. Commercial auto—covering the trucks, delivery fleets, and commercial vehicles crisscrossing America—sits directly in the path of the nuclear-verdict phenomenon: a fatal highway accident involving a corporate trucking defendant is the exact fact pattern that plaintiffs' attorneys, armed with litigation financing and "reptile theory" courtroom tactics, have learned to convert into eight- and nine-figure awards. Excess casualty is even more insidious, because it sits on top of primary liability layers: the excess writer only pays when a loss is catastrophically large, which means its entire book is a leveraged bet on the severity tail—precisely the part of the distribution that social inflation is stretching. When average verdict sizes creep up, primary layers get exhausted more often, and losses that used to stop below the excess attachment now punch straight through into the excess writer's pocket. A modest-looking rise in verdict severity thus translates into a wildly outsized increase in excess-casualty losses. Everest, chasing premium growth, had loaded up on exactly this leverage without pricing for the trend that would detonate it.

The mechanism that turned a pricing error into a balance-sheet event is called the reserving lag, and it is worth dwelling on because it is the single most important technical concept in the story. When a reinsurer takes a hurricane loss, it knows within weeks roughly what the bill will be. But casualty claims settle slowly—lawsuits take years to wind through discovery, negotiation, and trial. An insurer must therefore estimate today what it will eventually pay, and book that estimate as a liability called a "reserve." If the early estimates were too low—because the underwriter mispriced the tail—the shortfall surfaces gradually, years later, as the claims mature and the true numbers come in higher than booked. Actuaries call this prior-year development: adjustments to reserves for policies written in earlier "accident years." When those adjustments are unfavorable and large, they hit current earnings even though the underwriting mistake was made years ago. It is a delayed-detonation charge, and the fuse can run a decade.

The reckoning came in the fourth quarter of 2024. Everest strengthened its reserves by roughly $1.7 billion for the full year, the bulk of it targeting US casualty lines and concentrated in accident years 2019 and later.1 Under the hood, the damage was spread across the company: reinsurance casualty reserves were strengthened by hundreds of millions, the insurance segment took the largest share, and even legacy "other" exposures—sports and leisure business, plus old asbestos and environmental liabilities—contributed.9 The quarter closed with a net loss of $593 million, or $13.96 per diluted share.1 Years of the diversification thesis, which had promised smoother earnings, had instead produced one of the ugliest quarters in the company's public history.

How management framed all this on the Q4 2024 earnings call is itself revealing. The language leaned heavily on words like "prudent" and "decisive," positioning the giant charge as a proactive clearing of the decks rather than a belated confession—Everest even pushed its loss picks for the most recent accident year higher, signaling it wanted to be seen as getting ahead of the trend. An independent listener has to weigh that framing skeptically, because "we are being conservative" is precisely what every management team says the first time it strengthens reserves, and it is only credible in hindsight if the reserves then hold. Everest's did not hold for even a year, which is why the tone of that call reads very differently in retrospect than it did in the moment.

The human consequence followed almost immediately. On January 8, 2025, Everest announced that Juan Andrade was leaving to become president and CEO of USAA, and that Group Chief Operating Officer Jim Williamson—a coldly analytical operator who had joined in 2020 and risen to run both the reinsurance and insurance businesses—would step in as acting CEO.2 The timing is hard to read as coincidence: the architect of the casualty build-out departed for the top job at another institution in the same week the bill for that build-out landed. Whether Andrade jumped or was pushed is a matter the two companies framed politely, and USAA's willingness to hire him suggests his reputation survived intact—but the optics for Everest shareholders, watching the CEO exit as a $1.7 billion charge printed, were unavoidably jarring. Williamson was confirmed as permanent president and CEO on January 22, 2025, inheriting a balance sheet that needed to be made believable again and a shareholder base that had stopped trusting the reserves.[^11] How he chose to rebuild that trust is a case study in defensive capital management.

VI. Jim Williamson's Restructuring: Ring-Fencing and Retrenchment

Here is the moment that separates a one-time stumble from a chronic problem. If the $1.7 billion charge in early 2025 had truly cauterized the wound, the reserves would have held. They did not. In the third quarter of 2025, Williamson had to go back to the well, booking roughly $478 million of net unfavorable prior-year reserve development, of which about $361 million was fresh US casualty strengthening—this time concentrated in accident years 2022 through 2024, driven by continued elevated losses in excess casualty and US liability lines, with a further chunk coming from the legacy sports-and-leisure book in the "other" segment.510 The combined ratio for the group spiked to 103.4% for the quarter—meaning Everest paid out more in claims and expenses than it collected in premium—while net income fell to $255 million from $509 million a year earlier.10

The significance of that second charge cannot be overstated, and an independent analyst has to say it plainly: it undercut the credibility of the first one. When a company tells the market it has "fixed" its reserves and then has to strengthen them again three quarters later—now reaching into accident years as recent as 2024—the natural inference is that management still does not have a confident handle on the ultimate cost of its casualty book. Social inflation, it turned out, was not a discrete event to be absorbed but a moving target that kept outrunning the estimates.

Williamson himself is worth a closer look, because his temperament shaped the response. Where Andrade carried the polish of a Chubb underwriter-diplomat, Williamson had built his Everest reputation as an operator and a numbers man—he had come in as group COO in 2020, taken over the reinsurance division in 2021, and been handed both reinsurance and insurance in early 2024, meaning he had a front-row seat to the casualty book before the reckoning. That is a double-edged biographical fact. On one hand, it made him credible as the person who understood the problem intimately; on the other, it complicates any narrative that casts him purely as the clean-up outsider, since he was a senior member of the very leadership team that ran the book into trouble. His public posture from the moment he took over was relentlessly analytical and unsentimental: fix the balance sheet first, worry about growth later, and be willing to shrink the company to shrink the risk.

So Williamson stopped trying to out-estimate the problem and instead tried to wall it off. In late 2025 he executed two tightly engineered transactions, announced together on October 27, that together amount to a strategic retreat dressed as capital discipline.

The first was the $1.2 billion Adverse Development Cover (ADC), effective October 1, 2025. In plain terms, an ADC is retroactive reinsurance: Everest paid another party to absorb future deterioration on past liabilities. The cover, supported by Stone Ridge's Longtail Re, provides $1.2 billion of gross protection against further adverse development on substantially all of Everest Insurance's North American business for accident years 2024 and prior, sitting in two layers on top of the roughly $5.4 billion of subject reserves.[^4]11 The structure was intricate—Everest transferred well over a billion dollars of in-the-money reserves into the first layer, paid roughly $122 million in additional consideration for the second (booked as a Q4 2025 loss), and retained a $100 million co-participation in each layer plus full control of claims handling.11 Strip away the machinery and the purpose is simple: buy a hard ceiling on legacy casualty reserve creep, and buy back the confidence of rating agencies and equity investors who had stopped believing the numbers. It is expensive certainty. Whether it is cheap certainty depends entirely on whether the losses ultimately breach the cover.

The second maneuver was the renewal-rights sale to AIG. Everest agreed to hand AIG the rights to renew its US, UK, European, and Asia-Pacific commercial retail insurance business—roughly $2 billion of aggregate gross written premium—thereby exiting global commercial retail almost entirely.4 Critically, Everest kept the liabilities on the business it had already written and continued to administer those claims; it sold the future, not the past. AIG expected to begin renewing most of those clients from January 1, 2026. A few months later, in March 2026, Everest tidied up the remaining edges by selling its Canadian commercial retail portfolio to Wawanesa.[^14]

The strategic logic knits the two deals together. Retail commercial insurance—the business of selling coverage to ordinary companies through ordinary brokers—had proven to be exactly the wrong place for Everest: high operating cost, and stuffed with the long-tail casualty exposure that had just detonated. So Williamson refocused Everest Insurance into a pure-play Global Wholesale & Specialty insurer, distributing through specialty wholesale brokers such as Amwins and RT Specialty.

It is worth being precise about why wholesale-and-specialty is a genuinely different animal from the retail book Everest was fleeing, because the distinction is the whole bet. The wholesale specialty market—often called the excess-and-surplus (E&S) lines market—handles risks that standard "admitted" insurers won't touch at standard rates: unusual, hard-to-place, or fast-changing exposures. Crucially, E&S carriers enjoy freedom from the rate-and-form regulation that binds admitted retail insurers, meaning they can reprice quickly as loss trends move—exactly the flexibility Everest lacked when social inflation ran ahead of its filed retail rates. Specialty lines also tend to be shorter-tail and more technically underwritten, and the wholesale broker acts as a filter that channels only the risks that need specialist pricing. In theory, this is a market where underwriting skill is rewarded and where a nimble carrier can outrun a deteriorating trend rather than being locked into it. Whether Everest actually possesses a durable edge here—as opposed to simply being present—is the open question, since E&S is also fiercely competitive and currently attracting capacity from every carrier that, like Everest, is fleeing commoditized retail.

To run it, Williamson hired Jason Keen, appointing him CEO of Global Wholesale & Specialty Insurance in November 2025.12 The message to investors was unambiguous: Everest was retreating to the two things it could defend—big-ticket global reinsurance and specialty wholesale—and abandoning the retail-diversification dream that had defined the prior regime. The question left hanging is whether this is genuine strategic clarity or an expensive admission that the entire post-2020 pivot was a mistake. The 2026 financials are where we can start to test it.

VII. Current Operations & Segment Economics (2026 Status)

Walk into Everest as it stands in 2026 and the first thing you notice is how much has been swept off the table. The company that spent the early 2020s adding businesses spent 2025 subtracting them, and the resulting entity is deliberately smaller and simpler. Gross written premium for full-year 2025 came in at $17.7 billion, down about 3% year over year—a decline management frames not as weakness but as pruning, the visible result of shedding retail commercial lines and pulling back from underpriced casualty.13 For the full year, the group posted net income of about $1.6 billion and a return on equity of roughly 10.5%, a rebound from the loss-scarred prior year but still well short of the 15%-to-20% the franchise aspires to in a good cycle.13

The two-segment story underneath that number is where the real information lives. Global Reinsurance remains the engine, and in 2025 it did exactly what it is supposed to do. It produced a combined ratio of 91.7% for the full year—comfortably profitable—while the group as a whole limped in at 98.6%, dragged down by the insurance side's 114.6%.13 In other words, the healthy business subsidized the sick one. Reinsurance is operating in one of the firmest property-catastrophe markets in decades, and a relatively benign 2025 catastrophe experience helped: third-quarter catastrophe losses, for instance, ran at just $45 million versus $239 million a year earlier.5 The reinsurance segment now accounts for the clear majority of premium and the overwhelming majority of profit—the outline's framing of roughly three-quarters of premium and something like 85% of profit is consistent with a company whose earnings are, once again, riding on the catastrophe cycle.

Global Wholesale & Specialty Insurance is the rebuilt survivor of the old insurance ambition—drastically simplified, carrying zero commercial retail exposure going forward, and with its most dangerous legacy North American casualty liabilities now sitting behind the $1.2 billion ADC. The intent is a cleaner, shorter-tail, higher-margin book. But an honest reading of the 2025 combined ratio says the healing is not finished: an insurance segment running north of 114% is still losing money on an underwriting basis, weighed down by the reserve charges that punctuated the year. The thesis that wholesale specialty will deliver attractive, lower-volatility margins is a forward promise, not yet a demonstrated result.

One structural tailwind sits underneath both segments and deserves mention, because it flatters the reported numbers in a way that has nothing to do with underwriting: investment income. A reinsurer collects premiums today and pays claims later—sometimes much later, in the case of casualty—and it invests the "float" in between. After the sharp rise in interest rates that began in 2022, the yield on that enormous bond portfolio climbed materially, so Everest, like every insurer, has been earning far more on its investments than it did in the zero-rate 2010s. This is a real and durable benefit, but an analyst should hold it apart from underwriting quality: a company can post respectable net income on the strength of investment income even while its underwriting is mediocre, and the casualty debacle is a reminder that float earned on long-tail business is not free money—it is the offsetting reward for holding liabilities whose ultimate cost you may have badly underestimated. The float that funds the investment income is the very same casualty float that blew up.

The third-party capital story also continues quietly in the background through Mt. Logan Re and related vehicles, which let Everest earn fee income by managing outside investors' catastrophe exposure alongside its own—an increasingly important, capital-light complement to the balance-sheet reinsurance business, and one that aligns Everest with the same alternative-capital wave that pressures pricing.

On capital allocation, Williamson's record deserves a genuinely balanced verdict. On the positive side, he did the hard, unglamorous things: exited volatile and mispriced lines, avoided the temptation to paper over the casualty problem with a splashy, dilutive acquisition at a market peak (a discipline several peers did not show), and kept returning capital through buybacks and dividends. The most instructive prior data point is the May 2023 equity raise, when Everest sold 3.6 million shares at $360 apiece—about $1.5 billion including the greenshoe—and pushed the proceeds straight into hard-market reinsurance lines just as pricing was peaking.14 Raising equity at a premium to deploy into the best pricing in years is capital allocation at its most opportunistic and correct.

But the same executive team also presided over—and in Williamson's case, as a senior operator, helped run—the casualty build-out that required $1.7 billion of reserve strengthening, a second charge of nearly half a billion, and a $1.2 billion insurance policy to contain. Good defense after a self-inflicted wound is still commendable, but it is not the same as never taking the wound. The fair conclusion is that Everest's capital discipline is real but recently tested, and that the 2026 balance sheet is cleaner precisely because management spent heavily to clean it.

The shape of the full-year 2025 result reinforces the point. The $1.6 billion of net income and ~10.5% ROE for the year masked a sharp split between a bruising third quarter, dominated by the reserve charge and restructuring, and a stronger fourth quarter as the cleanup landed and the reinsurance engine kept earning.13 Management leaned on that Q4 turn to argue that the go-forward business is healthier than the full-year averages suggest—a fair point, but also exactly the kind of "look past the messy year" framing that investors should accept only once it is corroborated by clean reserves in subsequent quarters. Everest continued returning capital to shareholders through dividends and buybacks even while absorbing the charges, a signal of confidence in its underlying capital position; a skeptic, though, would note that buying back stock in the same year you pay a counterparty to insure your own reserves is a statement of priorities worth scrutinizing, since both compete for the same capital. Which sets up the broader lessons the whole saga offers.

VIII. Playbook: Key Strategy & Business Lessons

Step back from the quarter-by-quarter drama and four durable lessons emerge, each of them useful well beyond insurance.

The first is the illusion of uncorrelated diversification. The entire intellectual case for building Everest Insurance rested on a portfolio-theory intuition: bolt a low-correlation earnings stream onto a volatile one and you reduce total volatility. The flaw was not the math but the hidden nature of the second stream. Property-catastrophe risk is volatile but fast and visible—you know within weeks whether you were right. Long-tail casualty risk is the opposite: it looks placid for years and then reveals, all at once, that you were wrong for a decade. Swapping short-tail visible volatility for long-tail invisible volatility does not diversify your risk so much as hide it, and hidden risk compounds silently until it is far larger than the volatility you were trying to escape. For any business tempted to diversify into an adjacent line because it "smooths earnings," the Everest lesson is to ask whether the new line's risks are simply slower to show up—because slow-to-show-up is not the same as small.

The second lesson is the power of structural ceilings. When a company is buried under legacy liabilities that it can no longer credibly estimate, the market stops trusting every number on the balance sheet, not just the bad ones. In that situation, paying a steep transactional price to a third party to cap the downside—as Everest did with the $1.2 billion ADC—can be the cheapest available way to buy back credibility, even though it looks expensive in isolation. The ADC does not make Everest money; it makes Everest believable, and for a company whose entire product is the credibility of its promise to pay, believability has hard economic value. The caveat, which a skeptic must keep in view, is that a ceiling only works if the losses stay beneath it.

The third lesson is about reading management credibility through behavior, not words. Everest's leadership said all the right things throughout the pivot—discipline, prudence, diversification, conservatism—and the words were indistinguishable from those of a company doing everything correctly. What separated rhetoric from reality was only visible in the sequence of actions: aggressive growth in a line where the company had no edge, loss picks that proved too optimistic, a first reserve charge described as conservative, and then a second charge that exposed the first as insufficient. For an investor, the durable technique is to treat every "we are being prudent" as an unproven claim until the reserves hold across multiple periods, and to weight a management team's track record against its prior promises far more heavily than its current characterization of events. The tell in the Everest saga was not any single statement but the gap between the confident language of 2024 and the corrective action of 2025. Narrative consistency across calls and filings is a real diligence signal, and Everest's narrative bent under the weight of its own reserves.

The fourth lesson is the most humbling: identify your real distribution moat. For years Everest told itself, and the market, that it could be a diversified global insurer with a broad commercial retail footprint. The retreat to wholesale and specialty is, at bottom, an admission that its genuine competitive advantage was never retail distribution. Everest's edge is underwriting large, wholesale, institutional capacity—putting down big lines fast, backed by a lean, fortress balance sheet. Building a global retail sales machine to compete with the Chubbs and AIGs of the world played against that edge, layering on cost and long-tail exposure while adding no distinctive advantage. Knowing what you are not is as valuable as knowing what you are, and it took a multi-billion-dollar detour for Everest to relearn it. With those lessons in hand, we can test how defensible the refocused business actually is.

IX. Strategic Analysis: Five Forces & Helmer's 7 Powers

War-game the refocused Everest against the classic frameworks and a nuanced picture emerges—strong where it competes on balance-sheet scale, weaker where it competes on price.

Start with Porter's Five Forces. Barriers to entry are high, and this is Everest's structural friend. You cannot simply decide to become a major property-catastrophe reinsurer: you need billions in capital, an A-range financial-strength rating from A.M. Best (which cedents and brokers effectively require before they will trade with you), and the accumulated modeling expertise to price global catastrophe accumulations without blowing yourself up.8 Those requirements keep the competitive set small and known. Buyer power is medium-to-high, and this is the subtler force. Reinsurance is intermediated by a handful of giant brokers—Aon, Marsh McLennan's Guy Carpenter, and Gallagher—who concentrate the buying and can squeeze reinsurer margins in soft markets. But the power oscillates with the cycle: when catastrophes destroy capacity and capital gets scarce, pricing power swings hard back to underwriters like Everest, who can suddenly dictate terms. Rivalry is high but disciplined—the competitors are sophisticated, but they are all bound by the same reinsurance cycle and the same global cost of capital, which tends to prevent the kind of suicidal price war you see in less capital-intensive industries. The recent casualty debacle, notably, was not a Porter's-forces failure at all; it was an underwriting failure inside a line where the discipline broke down.

A direct comparison with the closest peers sharpens where Everest sits. RenaissanceRe made the opposite bet at almost the same moment: rather than diversifying into primary casualty, it doubled down on reinsurance by acquiring Validus from AIG in 2023, becoming an even more concentrated property-and-casualty reinsurance specialist. Arch Capital, meanwhile, built a genuinely diversified model spanning insurance, reinsurance, and mortgage insurance, and has been widely admired for underwriting discipline through the cycle—the outcome Everest was reaching for and missed. Berkshire Hathaway's reinsurance operation plays a different game entirely, using a permanent, low-cost capital base and a willingness to sit out soft markets that few public companies can match. Everest's distinctiveness in this set was always its lean, fast, large-line property-catastrophe capability—and the casualty episode, viewed against peers, looks less like an industry-wide accident and more like a company-specific overreach, since the peers who stuck closer to reinsurance or underwrote casualty more cautiously did not blow the same hole in their balance sheets. That is an uncomfortable but important comparative fact: this was, to a meaningful degree, a self-inflicted wound rather than a storm that hit everyone equally.

Now Hamilton Helmer's 7 Powers, where three apply with real force. Scale economies: a large, diversified reinsurance balance sheet lets Everest spread its capital across uncorrelated zones and perils, which lowers the amount of capital it must hold per dollar of risk underwritten—a genuine cost-of-capital edge over a smaller or more concentrated rival. Cornered asset: the Bermuda domicile, with its tax efficiency and regulatory agility, is a structural advantage, though an eroding one—global tax reform is steadily narrowing the Bermuda arbitrage that was so potent in 2000, and an honest analysis should treat this power as weakening rather than permanent. Process power: decades of proprietary catastrophe modeling and accumulated underwriting judgment about how risks pile up geographically constitute real, hard-to-copy know-how in property-cat.

But here is the war-game's most important finding, and it is a critical one for anyone tempted to over-rate Everest's moat: none of these powers protected it from the casualty trap, because none of them operate in long-tail casualty. Scale economics, catastrophe process power, and the Bermuda cornered asset are all advantages in the reinsurance and property-catastrophe world. In US excess casualty, Everest had no discernible edge—no proprietary insight into how juries and litigation funders would behave, no cost advantage that mattered, no process power in reserving that its rivals lacked. It was, in that line, an ordinary competitor exposed to an extraordinary trend. The strategic frameworks thus confirm the playbook lesson: Everest's powers are real but bounded, concentrated in the arena it is now retreating back toward. That boundedness is exactly what the bull and bear cases fight over.

X. Valuation, Bull vs. Bear Case, and KPIs

Rather than chase a target price—which is not the purpose here—the more useful exercise is to isolate what actually moves the needle and then honestly weigh the two sides of the argument.

The three KPIs that matter most. First, the combined ratio, both consolidated and by segment—the single cleanest gauge of underwriting profitability, where anything under 100% means the underwriting itself makes money before investment income. The numbers to watch are whether the group stays below roughly 95%, with reinsurance holding its sub-92% form and, crucially, the specialty insurance segment finally dragging its attritional (ex-catastrophe, ex-reserve-charge) ratio down toward the mid-90s. In 2025 the insurance segment was nowhere near that, so this is the metric where the recovery thesis will be proven or broken.13 Second, book value per share growth, the ultimate scoreboard for a compounding balance-sheet business; reserve charges destroy it and disciplined underwriting rebuilds it, which makes it the honest long-run referee of whether the whole enterprise is creating value. Third, return on equity, where the franchise aspires to 15%-to-20% in a hard market but delivered only about 10.5% in 2025—the gap between those figures is a direct measure of how much the casualty cleanup is still costing.13 A useful way to hold these three together: the combined ratio tells you whether the underwriting is healthy quarter to quarter, book value per share tells you whether that health is actually compounding into shareholder wealth over years, and ROE tells you how efficiently the capital is working relative to what the franchise is capable of. Think of book value per share as the odometer of the whole enterprise—an insurer is, at bottom, a machine for growing the pool of capital behind its promises, and every reserve surprise is a stretch of the journey driven in reverse. The reason the casualty saga was so damaging is precisely that it ran the odometer backward for the better part of two years; the reason the reinsurance engine matters so much is that it is the thing now driving it forward again. An investor does not need to compute these figures—Everest reports them every quarter—only to watch whether the trajectory of book value resumes its climb and whether the insurance segment's combined ratio finally crosses back below the line where underwriting makes money. Track these three and you are tracking Everest; almost everything else is commentary.

Myth versus reality. Before the bull and bear cases, it is worth puncturing two consensus narratives. The first myth is that the ADC "solved" the casualty problem. The reality is narrower: the ADC caps disclosed, North American, accident-year-2024-and-prior reserves up to a limit, with Everest retaining co-participations and continuing to handle the claims. It does nothing for casualty written in 2025 and beyond, nothing for reinsurance-segment casualty, and nothing if losses exceed the cover. It bought a ceiling on one specific room of the house, not a new house. The second myth is that Everest is now a "de-risked" company. The reality is that it has re-concentrated into property catastrophe—the very volatility it spent five years trying to diversify away from. A company whose profits again ride overwhelmingly on the reinsurance segment is not low-risk; it is differently risky, exposed once more to the single bad hurricane season that started this whole story. De-risking the casualty tail by leaning harder into the catastrophe tail is a trade, not an elimination of risk.

The bull case runs as follows. The legacy casualty reserves are now insulated behind the $1.2 billion ADC, so the market can finally stop fearing a fresh reserve grenade and re-rate the stock on go-forward earnings. Property-catastrophe pricing remains historically firm, driven by climate volatility and the relentless rise in the value of insured assets, which keeps the reinsurance engine—the true profit center—running hot. And the simplified wholesale-and-specialty insurance model, shorn of retail cost and long-tail exposure, should eventually deliver the attractive, lower-volatility margins that the old diversification strategy only promised. In this telling, 2024–2025 was a painful but bounded cleanup, and what remains is a leaner, higher-return underwriter trading at a discount born of recent trauma.

The bear case—and an activist skeptic would press every point—is equally coherent. Start with the reserves: the second charge in Q3 2025, reaching into accident years as recent as 2024, is evidence that social inflation keeps outrunning management's estimates, and there is no law of nature that says it stops politely at $1.2 billion. If casualty deterioration blows through the ADC ceiling, Everest is back to taking dilutive charges, and the credibility purchased in 2025 evaporates. Next, the cycle: the reinsurance profits that make the whole story work depend on hard property-catastrophe pricing, and that market can soften fast when alternative capital—catastrophe bonds and other insurance-linked securities—floods back in chasing high returns, as it periodically does. A bull's "hard market indefinitely" is a bear's "peak of the cycle." And finally the tail that no strategy can ring-fence: a genuine mega-catastrophe—a Category 5 hurricane driving straight into Miami, or a great Tokyo earthquake—could impair Everest's capital base directly, because concentrating catastrophe risk is, after all, the business. The activist would add a governance jab: the same leadership that is now praised for the cleanup is the leadership that built the mess, and a $1.2 billion insurance policy on your own past underwriting is not a trophy—it is a receipt.

A full activist stress test would push on several additional pressure points beyond the reserves and the cycle. On governance and accountability, a skeptic would ask why the same senior team that oversaw the build-out is the team now trusted to run the retreat, and whether the board moved fast enough as casualty warning signs accumulated through 2023 and 2024. On disclosure, the two-charge sequence invites questions about the reserving process itself—how a company this sophisticated could be surprised twice in three quarters, and whether the actuarial assumptions were genuinely independent of the growth targets management was chasing. On capital allocation, the very act of paying roughly $122 million of hard cash and transferring more than a billion dollars of reserves into an ADC is a transfer of shareholder value to a counterparty in exchange for certainty—defensible, but only if the alternative (continued reserve surprises) was truly worse, which is unprovable in advance. And on portfolio complexity, while the 2025 simplification cuts the right way, an activist would want assurance that the "other" and legacy books—sports and leisure, asbestos, environmental—hold no further surprises of their own, since those lines contributed to both charges. None of this makes the bear case correct; it makes the bull case conditional. The burden of proof, after two reserve charges, sits squarely with management.

The honest synthesis is that both cases are live, and which one wins is genuinely unresolved as of mid-2026. The bull case is a bet that the casualty wound is cauterized and the reinsurance engine keeps humming; the bear case is a bet that long-tail losses are still leaking and the cycle is closer to its top than its bottom. The evidence to settle it will show up, quarter by quarter, in exactly those three KPIs. That is the state of play as the story reaches the present.

XI. Epilogue & Conclusion

Return, one last time, to that calm Bermuda trading floor. The company sitting there in 2026 is, in a strange way, closer to the one that redomiciled in 2000 than to the ambitious diversified platform that rebranded itself in 2023. It has walked out of retail commercial insurance, ring-fenced its most dangerous legacy liabilities, narrowed its insurance arm to specialty wholesale, and re-anchored its identity in the two things it can actually defend: large-scale global reinsurance and a fortress balance sheet. The arc is almost novelistic—from quiet Bermuda reinsurer, to overreaching diversifier, to casualty cautionary tale, and finally to chastened, ring-fenced pure-play.

There is a final tension the refocused Everest carries into its next chapter, and it is worth naming clearly. In retreating to what it does best, the company has re-embraced the very cyclicality it once found unbearable. Its fortunes now ride, more than they have in years, on the property-catastrophe cycle staying hard and on the great storms staying away long enough for the reinsurance engine to rebuild the equity that casualty destroyed. If the cycle softens—if alternative capital floods back, if a quiet catastrophe stretch tempts rivals to cut prices—the earnings power that underwrites the whole recovery narrative will thin. And if the casualty reserves prove, a third time, to be short, the credibility so expensively repurchased in 2025 will have to be bought again. The company has bought itself focus and a ceiling on its worst legacy exposure; it has not bought itself immunity from the ocean or the courts.

What makes the story worth an investor's attention is not the drama of a single bad quarter but the clarity of the lesson underneath it. Everest did not get into trouble by being reckless with the risks it understood—the hurricanes and earthquakes it has priced for half a century. It got into trouble by seeking safety in a line of business where it had no pricing edge, mistaking the slow, invisible volatility of American casualty litigation for the ballast it craved. The deepest form of underwriting discipline, this saga suggests, is not the courage to take on frightening risks; a good reinsurer does that every January. It is the harder, humbler wisdom to recognize the risks where you hold no advantage—and to have the discipline to walk away before they find you. Whether Everest has truly internalized that lesson, or merely survived its first hard reminder of it, is the question its next several years will answer.

References

-

Everest Reports Fourth Quarter and Full Year 2024 Results — Everest Group, Ltd., 2025-02-05 ↩↩↩

-

Everest Group Announces Leadership Transition — Everest Group / Business Wire, 2025-01-08 ↩↩

-

Everest Re Group, Ltd. Announces Name Change to Everest Group, Ltd. — Everest Group, Ltd., 2023-07-10 ↩↩

-

Everest Announces Agreement to Sell Retail Commercial Insurance Renewal Rights to AIG — Everest Group / Business Wire, 2025-10-27 ↩↩

-

Everest Reports Third Quarter 2025 Results — Everest Group, Ltd., 2025-10-27 ↩↩↩

-

Everest Re Group, Ltd. Form 10-K (corporate history and organization) — U.S. Securities and Exchange Commission / EDGAR (CIK 0001095073) ↩↩↩↩↩↩↩

-

Bermuda Monetary Authority — Insurance & Reinsurance Supervision — Bermuda Monetary Authority ↩

-

A.M. Best Affirms Credit Ratings of Everest Group, Ltd. and its Subsidiaries — A.M. Best, 2025-11-12 ↩↩

-

Everest reports total reserve strengthening of $1.7bn for 2024 — Reinsurance News, 2025-02-04 ↩

-

Everest Group reports Q3 2025 results and adverse casualty reserve development — Reinsurance News, 2025-10-29 ↩↩

-

Everest Secures $1.2 Billion Adverse Development Cover — Everest Group / Business Wire, 2025-10-27 ↩↩

-

Everest Group Appoints Jason Keen as CEO of Global Wholesale & Specialty Insurance — Reinsurance News, 2025-11-12 ↩

-

Everest Reports Fourth Quarter and Full-Year 2025 Results — Everest Group, Ltd., 2026-02 ↩↩↩↩↩↩

-

Everest Re Group, Ltd. Announces Pricing of Public Offering of 3,600,000 Common Shares — Everest Group, Ltd., 2023-05 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube