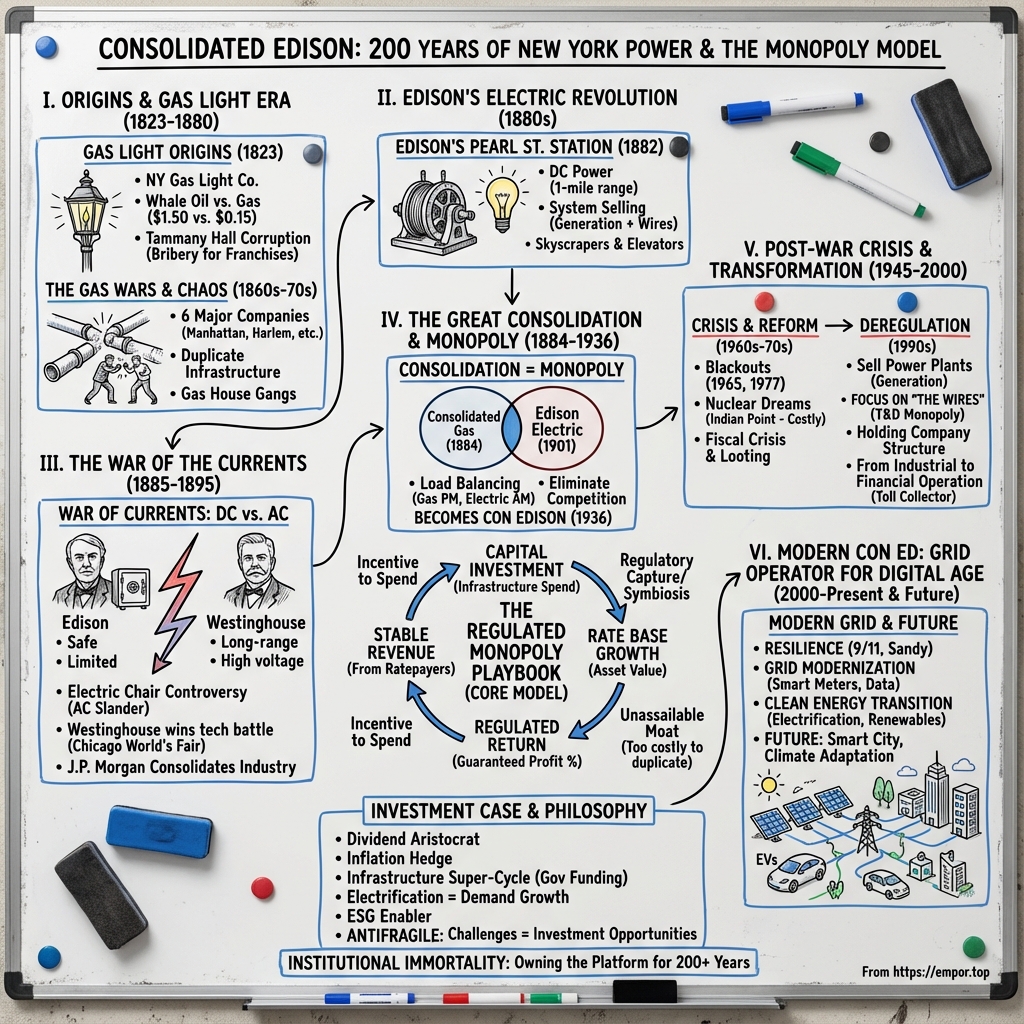

Consolidated Edison: Powering New York for Two Centuries

I. Introduction & Episode Roadmap

Picture this: Deep beneath the streets of Manhattan, in a maze of tunnels older than the Brooklyn Bridge, steam hisses through 105 miles of pipes at 350 degrees Fahrenheit. Above ground, 36,000 miles of underground electric cables—enough to circle the Earth one and a half times—power everything from the New York Stock Exchange to the neon lights of Times Square. This is Consolidated Edison's empire, hidden in plain sight, the invisible foundation upon which the world's financial capital operates every single day.

Con Edison isn't just another utility company. With a market cap of $38.64 billion and annual revenues of $16.15 billion, it's the longest continuously traded stock on the NYSE—listed without interruption since 1824, before railroads crossed America, before the Civil War, before electricity itself was commercialized. Think about that: this company has been publicly traded longer than Procter & Gamble, longer than any bank, longer than any industrial giant you can name.

But here's what's truly remarkable: Con Edison started as a gas lamp company in 1823, when New York's population was just 123,000 people clustered around the southern tip of Manhattan. The company that began by lighting street lamps with whale oil derivatives would eventually power the elevators that made skyscrapers possible, the subway system that moves millions daily, and the data centers that process trillions in financial transactions. It's a story of how infrastructure shapes destiny—how the pipes and wires beneath our feet determine what's possible above ground.

The questions we're exploring today go beyond corporate history. How does a company maintain a monopoly for two centuries in America's most competitive city? What happens when technological disruption—from gas to electricity, from centralized to distributed generation—threatens your entire business model, yet you can't be displaced? And perhaps most intriguingly: in an era of tech monopolies under antitrust scrutiny, why does nobody question Con Edison's dominance over New York's energy supply?

This is fundamentally a story about three things: the economics of natural monopolies, the symbiotic relationship between infrastructure and urban growth, and how regulatory capture can be a feature, not a bug, of modern capitalism. It's about understanding why Warren Buffett loves utilities, why private equity can't disrupt them, and why, despite all the talk of solar panels and battery storage, Con Edison's moat might be wider today than it was a century ago.

II. Gas Light Origins: Pre-Edison Era (1823-1880)

The gaslight flickered to life on Broadway for the first time in 1825, and New Yorkers gathered in wonder. Just two years after the New-York Gas Light Company's incorporation on March 23, 1823, by the 46th New York State Legislature, the miracle of artificial illumination had arrived. But not everyone was celebrating—whale oil merchants watched their monopoly evaporate, and property owners worried these new gas pipes would explode and burn their buildings to the ground.

The founding directors tell you everything about early American capitalism. Samuel Leggett wasn't just a banker; he controlled significant shipping interests and understood that extending business hours past sunset could double warehouse productivity. Henry Eckford, the Scottish-born naval architect who designed warships for the War of 1812, owned vast tracts of undeveloped Manhattan real estate that would quintuple in value once gas lines arrived. These weren't visionaries pursuing some abstract future—they were pragmatists who understood that controlling light meant controlling commerce.

Gas illumination technology had only arrived in America in 1816, when Baltimore became the first city to install gas streetlights. The resistance in New York was fierce and visceral. Newspapers published accounts of gas explosions in London. Insurance companies threatened to cancel policies on buildings with gas fixtures. The city's powerful whale oil lobby funded pamphlets warning that "manufactured gas" would poison the air and cause mysterious diseases. One prominent physician claimed gas light would damage people's eyesight, leading to an "epidemic of blindness."

But economics always wins. A whale oil street lamp cost $1.50 per night to operate. Gas? Fifteen cents. For a city with ambitions of overtaking Philadelphia as America's commercial capital, the math was irresistible. By 1830, New-York Gas Light had installed 2,000 street lamps and was serving 600 private customers, including Astor House, the city's premier hotel, where gaslight in the ballroom became a tourist attraction.

Then came the necessary corruption. The Board of Aldermen controlled franchise rights for laying pipes under city streets, and the Board of Aldermen was controlled by Tammany Hall. This wasn't subtle—aldermen literally held auctions for their votes. When New-York Gas Light wanted to expand north of Canal Street in 1833, the cost wasn't just pipe and labor; it was $50,000 in "fees" to various aldermen, documented in company ledgers as "municipal relations expenses."

The Tammany machine's grip tightened under William M. "Boss" Tweed in the 1860s. By then, franchise approval had shifted to the County Board of Supervisors, which Tweed controlled absolutely. Tweed became a board member of the Harlem Gas Light Company, strategically positioning himself to profit from the gas industry's expansion. The price for a gas franchise wasn't measured in application fees—it was calculated in bribes, kickbacks, and political favors that would make modern lobbyists blush.

By the 1870s, competition had created chaos. Six major gas companies operated in Manhattan—New York Gas Light, Manhattan, Metropolitan, Municipal, Knickerbocker, and Harlem—each with its own network of pipes, its own territories, and its own "gas house gangs." These weren't metaphorical gangs. When Manhattan Gas wanted to expand into New York Gas Light's territory, they'd send crews at night to dig up the competitor's pipes. The response? Armed guards protecting excavation sites. Police were useless—each company had purchased its own precinct captains.

The city streets became a battlefield of competing infrastructure. Property owners might find three different companies' pipes running under their buildings, each claiming exclusive rights. One contemporary observer noted that "Broadway has been excavated so frequently that the street level has dropped three feet in five years." The inefficiency was staggering—by 1882, Manhattan had enough duplicate gas infrastructure to serve a city three times its size.

This wasteful competition set the stage for what would become the great consolidation. The companies were bleeding money on redundant infrastructure and protection rackets. Meanwhile, a new threat loomed on the horizon—something called electricity that a certain inventor named Edison was tinkering with downtown. The gas monopolies that had seemed invincible were about to face their first existential crisis.

III. The Great Consolidation & Gas Monopoly (1884-1900)

The meeting took place at 2 AM in the backroom of Delmonico's restaurant on November 10, 1884. Six men, representing the six competing gas companies of Manhattan, sat around a mahogany table with a single document—articles of incorporation for something called "The Consolidated Gas Company of New York." The lawyer present later recalled that more guns than pens were visible at the signing. By dawn on November 11, 1884, New York's gas wars were officially over.

The consolidation wasn't driven by vision or efficiency—it was pure exhaustion. The six companies—New York, Manhattan, Metropolitan, Municipal, Knickerbocker, and Harlem—had spent the previous decade in a destructive competition that enriched only the politicians and lawyers. By the mid 1860s, the Tweed Ring openly bought votes, encouraged judicial corruption, and extracted millions from city contracts, with gas franchises being particularly lucrative targets. After Tweed's fall in 1871, the corruption continued but became more sophisticated—less outright bribery, more regulatory capture.

The newly formed Consolidated Gas immediately controlled 80% of Manhattan's gas supply. The monopoly was so complete that the company didn't even pretend to compete. They divided Manhattan into districts, shut down redundant plants, and raised prices 30% within six months. When customers complained, the company's president famously responded: "They can burn candles if they prefer."

But Consolidated Gas faced a more sophisticated challenge than angry customers—regulatory pushback that would reshape American capitalism. In 1886, New York State created the first public utilities commission with rate-setting authority. Consolidated Gas fought back, arguing that government-mandated rates violated the Fourteenth Amendment's protection against property seizure without due process. The case went all the way to the Supreme Court.

The 1894 Supreme Court decision in Consolidated Gas Co. v. New York became a landmark in regulatory law. The Court ruled that while governments could regulate utilities, they couldn't set rates so low as to prevent a "reasonable rate of return on investment." The Court estimated Consolidated Gas's asset value at $56 million, establishing the principle of rate-base regulation that still governs utilities today. This was genius—Consolidated Gas had effectively gotten the Supreme Court to guarantee its profitability.

The "gas house gangs" didn't disappear—they were institutionalized. Former street fighters became "customer service representatives." The protection rackets became "connection fees." The bribes to politicians became "regulatory compliance costs" that could be passed on to ratepayers. Consolidated Gas had discovered something profound: in a regulated monopoly, every cost, including corruption, becomes part of the rate base that customers must pay.

By 1900, Consolidated Gas was the most powerful corporation in New York, more influential than the railroads, more essential than the banks. The company employed 10,000 people and had a market capitalization exceeding $100 million (roughly $3.5 billion today). Its board of directors read like a who's who of Gilded Age capitalism: Astors, Vanderbilts, and Morgans.

But the company's executives weren't resting easy. Down on Pearl Street, in a small building near the financial district, Thomas Edison's electric company was running an experiment that would threaten everything Consolidated Gas had built. The age of gas was about to collide with the age of electricity.

IV. Edison's Revolution: Pearl Street Station & Electric Dawn (1880-1901)

Thomas Edison stood in the basement of 255-257 Pearl Street on September 4, 1882, his hand on a switch that would change the world. Above him, J.P. Morgan sat in his Wall Street office, waiting. At exactly 3 PM, Edison threw the switch. In Morgan's office, 106 electric bulbs blazed to life. The banker reportedly stood up, applauded alone in his office, and immediately bought another thousand shares of Edison Electric Light Company stock.

Edison had formed the Edison Electric Light Company in 1878 with several financiers, including J.P. Morgan, Spencer Trask, and members of the Vanderbilt family. On December 17, 1880, he founded the Edison Illuminating Company, and during the 1880s, he patented a system for electricity distribution. The Pearl Street Station consumed coal for fuel and began with six 100 kW dynamos, serving an initial load of 400 lamps to 82 customers.

The Pearl Street Station was an engineering marvel hidden in plain sight. Edison had deliberately chosen the location in the heart of New York's financial district, knowing that if he could convert Wall Street, the rest of the world would follow. The station's six dynamos, each the size of a small building, were nicknamed "Jumbos" after P.T. Barnum's famous elephant. They roared so loudly that workers communicated through hand signals.

By the end of the month, they had 59 customers. By the next year, they had 513. By 1884, Pearl Street Station was serving 508 customers with 10,164 lamps. But these numbers don't capture the psychological revolution. For the first time in human history, night could be turned into day at the flip of a switch. The New York Times building installed electric lights and immediately doubled its printing hours. The Stock Exchange extended trading. Restaurants stayed open past midnight.

Edison's genius wasn't just technical—it was financial. He didn't just sell light bulbs; he sold an entire system. Customers paid for the dynamos, the wiring, the meters, and a monthly service fee. He created the blueprint for every infrastructure business that would follow: huge upfront capital costs, recurring revenue, and customer lock-in. Once you wired a building for electricity, switching back to gas was unthinkable.

The established gas companies initially dismissed electricity as a novelty for the rich. Gas was 40% cheaper per unit of light, and gas infrastructure already reached 90% of Manhattan buildings. But they missed the crucial point: electricity wasn't just about light. It was about power—for elevators, for machinery, for ventilation systems. The first electric elevator was installed in 1889, and suddenly buildings could rise beyond the five-story walk-up limit. The skyscraper age had begun, and it ran on electricity.

The station burned down in 1890, destroying all but one dynamo that is now kept in the Greenfield Village Museum in Dearborn, Michigan. The fire, likely caused by overloaded equipment struggling to meet exploding demand, should have been a disaster. Instead, Edison used it as an opportunity. The rebuilt station, operational by 1895, had triple the capacity and incorporated every lesson learned from the first decade of operation.

But Edison had a problem that would define the next phase of electrical development: his direct current (DC) system could only transmit power about a mile from the generating station. This meant building a power plant every few blocks—economically impossible for citywide coverage. Meanwhile, a Pittsburgh entrepreneur named George Westinghouse had acquired patents for alternating current (AC) systems that could transmit power hundreds of miles. The stage was set for one of American business history's most vicious competitive battles.

V. War of the Currents & The Edison-Westinghouse Battle (1885-1895)

The body of William Kemmler twitched and convulsed for eight minutes as 1,000 volts of alternating current surged through the first electric chair on August 6, 1890, at Auburn Prison in New York. The execution was supposed to be quick and humane. Instead, witnesses vomited and fled the chamber as the smell of burning flesh filled the air. George Westinghouse, whose AC generators powered the execution, telegrammed the press: "They would have done better with an axe." Edison's response was colder: "The criminal died instantly. The experiment was a complete success."

This grotesque spectacle was just one battle in the War of the Currents, a corporate conflict that began in 1886 when George Westinghouse's company introduced an alternating current system that used transformers to step down from high voltage for indoor lighting. Edison had built his empire on direct current (DC), which was safe but limited—power could only travel about a mile from the generator. Westinghouse's AC could travel hundreds of miles, making citywide and eventually nationwide electrification economically feasible.

Edison understood the existential threat immediately. If AC became the standard, his entire infrastructure—every generator, every meter, every foot of copper wire installed under Manhattan's streets—would become obsolete. His response was a masterclass in corporate warfare disguised as public safety advocacy. Edison secretly funded Harold P. Brown, who conducted public demonstrations electrocuting dogs, cats, and eventually an elephant named Topsy (though this occurred later, in 1903) to prove AC was a deadly menace.

Edison decided to use spectacle to slander AC, including arranging for Topsy the elephant to be fed carrots laced with potassium cyanide and electrocuted with AC current, causing the elephant to die in less than a minute.

The electric chair controversy was Edison's most cynical maneuver. He colluded with Thomson-Houston Electric Company, Westinghouse's chief AC rival, to ensure the first electric chair used a Westinghouse AC generator. Edison's team secretly purchased the generators through third parties when Westinghouse refused to sell them directly. The goal was linguistic—Edison wanted execution by electricity to be called "Westinghousing," forever associating his rival's technology with death.

But technology has its own logic. AC's economics were irresistible. Where Edison needed a power station every square mile, Westinghouse could serve an entire city from a single plant. When Westinghouse won the contract to light the 1893 World's Columbian Exposition in Chicago—underbidding Edison by half—the war was effectively over. The exposition's 100,000 incandescent lights, powered by Westinghouse AC generators, dazzled 27 million visitors. It was the largest electrical installation in history, and it worked flawlessly.

The financial toll on Edison was devastating. By 1889, his investors, led by J.P. Morgan, forced him to merge his companies into Edison General Electric, reducing his role to a figurehead. In 1892, Morgan engineered another merger with Thomson-Houston, dropping Edison's name entirely. The company became simply General Electric. Edison reportedly said, "I've come out of it all right, but it's hard to be thrown out of your own shop."

By the early 1890s, the war was winding down. Further deaths from AC lines in New York forced companies to implement safety measures—insulated wires, proper grounding, professional installation standards. The technology that Edison claimed would kill children in their sleep became the backbone of modern civilization. Even Edison's own power stations eventually converted to AC.

The real victor wasn't Westinghouse or Edison—it was J.P. Morgan, who ended up controlling both General Electric and, through various financial maneuvers, significant stakes in Westinghouse Electric. Morgan understood something both inventors missed: in infrastructure businesses, consolidation is destiny. The war of the currents didn't end with one technology defeating another; it ended with finance capital subordinating both technologies to the logic of monopoly returns.

VI. The Merger: Gas Meets Electricity (1901-1936)

The deal that created modern Con Edison was negotiated in a private dining room at the University Club on Fifth Avenue over the course of three dinners in December 1900. Anthony N. Brady, who controlled Consolidated Gas, and Henry Villard, who ran Edison's electric interests, initially despised each other. Brady called electricity "a rich man's toy." Villard considered gas "a dying technology for slum tenements." J.P. Morgan, who held stakes in both companies, locked them in the room with a simple message: "Gentlemen, you will not leave until you've agreed to terms."

In 1901, Consolidated Gas Company bought Edison Illuminating Company, which had been founded by Thomas Edison in 1880. The merger made brutal economic sense. Gas and electric companies were literally destroying each other's infrastructure—when electric companies laid conduits, they "accidentally" ruptured gas mains. When gas companies did repairs, they "inadvertently" cut electric cables. The city had recorded 1,700 such "accidents" in 1899 alone.

But the real driver was load balancing. Gas demand peaked in the evening for lighting. Electricity peaked during the day for industrial motors and elevators. Combined, the companies could run their generators more efficiently, spreading fixed costs over more hours of production. It was the same logic that would later drive every utility merger: infrastructure has massive fixed costs and marginal variable costs, so utilization is everything.

By 1920, after absorbing more than 30 smaller companies, New York Edison (the electric subsidiary of Consolidated Gas) had become the undisputed electricity leader in New York. The consolidation process was methodical and ruthless. When Yonkers Electric Light refused to sell in 1919, New York Edison built transmission lines that completely surrounded their service territory, then offered electricity at half Yonkers' rates to any customer just outside their franchise area. Yonkers Electric sold within six months.

The transformation of the company's identity was gradual but inevitable. By 1932, Consolidated Gas was the largest electrical utility in the world, yet its name suggested it was still primarily a gas company. The irony was stark—the company supplied electricity to the Empire State Building (completed in 1931), the Chrysler Building (1930), and Rockefeller Center (1933), the very symbols of electrical modernity, yet operated under a 19th-century gas company name.

On February 18, 1936, an annual report revealed that roughly 75% of gross operating revenue came from electricity, leading to discussion about changing the company's name to better reflect its nature. The board meeting where the name change was debated lasted seven hours. Old-guard directors argued that "Consolidated Gas" had a century of brand equity. Younger members pointed out that customers literally didn't know the company sold electricity. The compromise was genius in its simplicity: Consolidated Edison Company of New York—keeping the consolidation theme while adding Edison's name, even though Edison himself had been forced out of the electricity business forty years earlier.

The newly christened Con Edison of 1936 was a behemoth: 40,000 employees, $1.2 billion in assets (roughly $25 billion today), serving 3.2 million customers. It operated 17 generating stations, 85 substations, and maintained 62,000 miles of underground cable. The company didn't just power New York—it was New York, as essential to the city's function as its water supply or streets.

The merger created the template for modern utility operations: massive scale, regulatory capture disguised as compliance, and the transformation of a competitive market into a regulated monopoly that guaranteed returns. It was capitalism perfected—competition was eliminated not through victory but through consolidation, and profits were guaranteed not by market success but by regulatory fiat.

VII. Post-War Era: Nuclear Dreams & Urban Crisis (1945-1980)

The lights went out at 5:27 PM on November 9, 1965. Within minutes, 30 million people across eight states were in darkness. In New York City, 800,000 people were trapped in subway cars. At the Waldorf-Astoria, guests formed human chains to navigate pitch-black corridors. The New York Stock Exchange, caught mid-transaction, wouldn't know for three days whether certain trades had cleared. Con Edison's CEO, Charles Luce, was at the opera when an aide whispered the news. His response: "That's impossible. Check again."

The Great Northeast Blackout of 1965 wasn't supposed to happen. Post-war Con Edison had built what engineers called "the most reliable grid in human history." The company had invested $2 billion between 1945 and 1965 expanding capacity for a booming metropolis. New York's population had swelled to 8 million. Air conditioning, adopted by 40% of households by 1965, had transformed summer peak loads. The subway system, fully electrified, moved 2 billion riders annually. Con Edison powered it all.

Con Edison acquired land on the Hudson River in Buchanan, NY, in 1954 for the Indian Point nuclear power plant, with the first reactor beginning generation on September 16, 1962. Nuclear power was supposed to be the ultimate solution—endless, clean electricity "too cheap to meter," as Atomic Energy Commission Chairman Lewis Strauss famously predicted. Indian Point represented a massive bet: $150 million for the first reactor (roughly $1.4 billion today), more than Con Edison had spent on infrastructure in any single year of its history.

The nuclear dream quickly became a nightmare. The reactor was shut down on October 31, 1974, because the emergency core cooling system did not meet regulatory requirements. Cost overruns were spectacular—Indian Point 2, originally budgeted at $120 million, cost $460 million. Indian Point 3 ballooned from $200 million to $620 million. Environmental groups, led by the Hudson River Fishermen's Association, sued over thermal pollution killing millions of fish. By 1975, Con Edison was spending more on lawyers than on coal.

Then came July 13, 1977—the night New York went insane. Lightning strikes caused a blackout of all New York City except the Rockaways, which received power from the Long Island Lighting Company. But this wasn't the almost festive atmosphere of 1965. This was New York in fiscal crisis, with 300,000 jobs lost since 1970, the South Bronx literally burning, and crime at historic highs. The looting started within an hour. By dawn, 1,616 stores had been ransacked, 1,037 fires set, 3,776 people arrested. Damage exceeded $300 million. In Bushwick, Brooklyn, entire blocks burned to the ground.

The 1977 blackout exposed a utility in crisis. Con Edison hadn't built a new power plant since 1974. Maintenance had been deferred for years—the company later admitted that critical equipment at the Ravenswood generating station hadn't been properly serviced since 1969. The transmission system was held together with what one engineer called "prayer and duct tape."

Enter Charles Luce, the CEO who saved Con Edison from itself. A former Undersecretary of the Interior, Luce understood that Con Edison's problem wasn't technical—it was political and managerial. The company was organized like a medieval fiefdom, with separate duchies for Manhattan, Brooklyn, Queens, each with its own management structure, incompatible equipment, and bitter rivalries. Brooklyn managers literally wouldn't share spare parts with Queens during emergencies.

Luce's reforms were radical. He reorganized operations by function rather than geography—one department for generation, another for transmission, a third for distribution. He hired the first woman executive in the company's history, the first Black senior managers, and instituted what he called "customer service"—a concept so foreign that employees needed training on how to answer phones politely. The company's previous customer service philosophy was summed up by a sign in the Bronx service center: "We're the only game in town. Take it or leave it."

The turnaround was measurable. Customer complaints dropped 70% between 1978 and 1980. System reliability improved from 99.96% to 99.98%—seemingly tiny, but representing millions of customer-hours of avoided outages. Luce negotiated the sale of Indian Point 3 to the New York Power Authority for $387 million, removing a massive capital burden. He settled environmental lawsuits by agreeing to install fish-protection systems that, while costing $40 million, ended a decade of legal warfare.

But Luce's greatest achievement was psychological. He convinced New Yorkers that Con Edison was competent again. When asked how he did it, he said: "I stopped treating customers like hostages and started treating them like the owners—which, through their rates, they essentially are."

VIII. Deregulation & Transformation (1980-2000)

The meeting that would revolutionize New York's energy market took place in Albany on March 19, 1996. Governor George Pataki, flanked by utility executives and consumer advocates, announced the unthinkable: New York would deregulate its electricity market. Con Edison's century-old monopoly on power generation was ending. "Competition," Pataki declared, "will do for electricity what it did for telecommunications—lower prices and improve service."

Con Edison's executives had seen this coming. California had begun deregulation proceedings in 1994. Pennsylvania and Massachusetts were moving forward. The logic seemed irresistible: why should a regulated monopoly own both the power plants and the wires? It would be like letting AT&T own both the phone lines and the only phones you could buy. CEO Eugene McGrath knew resistance was futile, but he also saw opportunity—Con Edison could shed its aging, expensive generation assets and focus on what couldn't be replicated: the distribution network.

On January 1, 1998, following deregulation, a holding company, Consolidated Edison, Inc., was formed. This wasn't just a corporate restructuring—it was an admission that the integrated utility model Edison and Insull had created was obsolete. The holding company structure allowed Con Ed to separate its regulated utility operations from new, unregulated ventures. Wall Street loved it. The stock jumped 15% on the announcement.

The asset sales were breathtaking in scope. Northern States Power, KeySpan, and Orion Power paid a total of $1.65 billion for Con Edison's generation facilities. The Indian Point nuclear plants went for $967 million. The Ravenswood generating station in Queens—3,000 megawatts of oil and gas-fired capacity—sold for $597 million. In eighteen months, Con Edison divested 7,800 megawatts of generation, roughly 70% of New York City's power supply.

Con Ed then announced plans to buy Orange and Rockland Utilities for $790 million, completed in 1999, which helped protect it from acquisition. This was defensive strategy at its finest. Throughout the late 1990s, utilities were consolidating nationally. Duke Energy, American Electric Power, and Dominion Resources were all hunting for acquisitions. By buying Orange and Rockland, Con Edison made itself 30% larger and much more expensive to acquire. It also gained a foothold in New Jersey and Pennsylvania, markets with different regulatory structures that provided diversification.

The failed Northeast Utilities merger of 1999-2001 revealed the limits of Con Edison's expansion ambitions. The $3.8 billion deal would have created the nation's largest utility, serving from Maryland to Maine. But 9/11 changed everything. The destruction of Con Edison's substations under the World Trade Center, the billion-dollar rebuilding cost, and regulatory concerns about a distracted management team killed the merger. Con Edison paid a $1.2 billion breakup fee—the largest in utility history.

But here's what's remarkable: deregulation didn't weaken Con Edison—it made it stronger. Without the capital burden of power plants, Con Edison could focus on its true monopoly: the wires, pipes, and infrastructure that nobody could duplicate. The company's return on equity improved from 8.5% in 1997 to 11.2% by 2000. Operating margins expanded. The stock price doubled.

The transformation also changed how Con Edison made money. Before deregulation, profits came from the spread between the cost of generating electricity and the regulated price. After deregulation, profits came from transmission and distribution charges—basically, toll collection on electron highways. Every kilowatt-hour that moved through Con Edison's wires, regardless of who generated it, paid a fee. It was like owning every bridge and tunnel into Manhattan—pure monopoly rents.

McGrath understood something his critics missed: in infrastructure, ownership of the network is more valuable than ownership of what flows through it. Generators could compete, prices could fluctuate, new technologies could emerge, but everyone still needed Con Edison's wires to reach customers. As he told investors in 2000: "We're not in the electricity business anymore. We're in the delivery business. And nobody delivers to New York except us."

The numbers validated the strategy. By 2000, Con Edison's regulated rate base had grown to $12 billion, generating guaranteed returns of nearly $1.3 billion annually. The company had transformed from an industrial operation—burning fuel to make power—into a financial operation—collecting fees for use of irreplaceable assets. It was the perfect business model for the 21st century: capital-intensive, competition-proof, and absolutely essential.

IX. Modern Con Ed: Grid Operator for the Digital Age (2000-Present)

The smoke hadn't cleared from Ground Zero when Con Edison crews descended into the ruins. Seven World Trade Center had collapsed directly onto Con Edison's primary lower Manhattan substation, crushing transformers the size of school buses. Two million gallons of oil from the station's cooling systems had leaked into the debris. The lights in the Financial District—in buildings that survived—stayed on only because Con Edison engineers had manually rerouted power through century-old cables never designed for such loads, some dating back to Edison's era.

Rebuilding lower Manhattan's electrical infrastructure after 9/11 cost Con Edison $400 million, but the company learned something invaluable: its grid was both more fragile and more resilient than anyone imagined. Fragile because a single building collapse could black out 20 square blocks. Resilient because engineers could reroute power through alternate pathways, some installed during the Great Depression. This paradox would define Con Edison's next chapter—modernizing ancient infrastructure while maintaining perfect reliability in an increasingly digital city.

Hurricane Sandy in October 2012 provided the ultimate stress test. The storm surge reached 14 feet in lower Manhattan, flooding five Con Edison substations and leaving 800,000 customers without power. The images were apocalyptic: cars floating down Avenue C, water cascading into subway tunnels, the lower half of Manhattan dark while midtown blazed with light. But Con Edison had made a calculated decision—they preemptively shut down power to flood zones, preventing the kind of electrical fires and explosions that destroyed much of post-Katrina New Orleans.

The post-Sandy transformation has been extraordinary. Con Edison has invested $1 billion specifically in storm hardening: submarine cables to connect Manhattan and Brooklyn, flood walls around critical substations, submersible transformers that can operate underwater. The company redesigned its entire network topology, creating "microgrids" that can isolate and self-power critical facilities like hospitals even when the broader grid fails.

Con Edison operates the largest commercial steam system in the world, providing steam service to nearly 1,600 commercial and residential establishments in Manhattan from Battery Park to 96th Street. This steam system, often forgotten, reveals Con Edison's hidden value. The 105-mile network heats the Empire State Building, the United Nations, and most major Manhattan hospitals. It's irreplaceable—the cost to duplicate it would exceed $20 billion. During COVID-19, when buildings emptied, steam demand dropped 30%, but Con Edison still collected minimum charges from every connected building. It's the perfect monopoly—customers can't disconnect without spending millions on new boiler systems.

Consolidated Edison Company of New York, Inc., provides electric, gas, and steam service to more than 3 million customers in New York City and Westchester County, an area of 660 square miles with a population of nearly 9 million. These numbers underscore an operational complexity that's hard to fathom. On a typical August afternoon, Con Edison manages 13,000 megawatts of peak demand—enough to power entire countries. The company processes 62 billion cubic feet of natural gas annually. Every day, 370 million gallons of water flow through the steam system.

The clean energy transition presents both an existential challenge and a massive opportunity. New York State's Climate Leadership and Community Protection Act mandates 70% renewable electricity by 2030. For Con Edison, this means completely reimagining a grid built for one-way power flow from large plants to consumers. Now, solar panels on Brooklyn brownstones feed power back into the grid. Battery systems in Queens charge at night and discharge during peak hours. The grid must become bidirectional, smart, and infinitely more complex.

Con Edison's response has been to position itself as the essential enabler of clean energy. The company is investing $4 billion in grid modernization through 2025—smart meters that provide real-time usage data, sensors that can detect and isolate problems before they cause outages, and software that can manage millions of distributed energy resources. As CEO Tim Cawley puts it: "We're becoming a technology company that happens to own wires."

In 2024, Consolidated Edison's revenue was $15.26 billion, up 4.04% from $14.66 billion, though earnings fell 27.75% to $1.82 billion. The earnings decline reflects the massive capital investments required for grid modernization—spending that will eventually be recovered through rates but pressures near-term profitability. This is the utility paradox: the more they invest, the larger their rate base grows, generating higher future returns, but the immediate impact is margin compression.

The most fascinating development is Con Edison's transformation into a data company. The utility now collects 250 million meter readings daily, tracking not just how much energy customers use but when, creating patterns that reveal everything from economic activity to public health trends. During COVID lockdowns, Con Edison could track the return to office by watching midtown Manhattan's electricity demand. They knew restaurants were recovering before sales tax data showed it. This data is invaluable—and Con Edison owns it all.

Looking forward, Con Edison faces three megatrends that will define its next decade. First, building electrification: New York City has banned natural gas connections in new buildings starting in 2024. Every new building must be all-electric, dramatically increasing electricity demand. Second, transportation electrification: the MTA's plan to convert its entire bus fleet to electric by 2040 will require charging infrastructure equivalent to adding a small city to the grid. Third, climate adaptation: Con Edison now models for Category 3 hurricanes hitting New York, scenarios that would have seemed absurd in 2000.

X. Playbook: The Regulated Monopoly Model

Here's the beautiful paradox of Con Edison's business model: the more money they spend, the more money they make. This isn't corporate inefficiency—it's the mathematical logic of rate-base regulation, a system so perfectly designed to generate returns that it makes Silicon Valley's winner-take-all dynamics look amateur.

The formula is deceptively simple. Con Edison's allowed revenue equals its operating costs plus a return on its "rate base"—the depreciated value of its capital investments. If Con Edison has a $20 billion rate base and regulators allow a 9% return, that's $1.8 billion in guaranteed profit, regardless of economic conditions, competitive threats, or technological disruption. The only way to grow profits is to grow the rate base, which means spending more on infrastructure. It's a perpetual motion machine powered by capital expenditure.

This creates perverse incentives that would horrify any MBA student. Why would Con Edison want to make its grid more efficient if efficiency means less capital investment? Why pursue cost-saving technologies when costs get passed through to customers anyway? The answer is they wouldn't—except that regulators require it. This dance between utility and regulator—each pretending to oppose the other while actually collaborating to grow the rate base—is what economists call "regulatory capture," though in utilities it's more like regulatory symbiosis.

The infrastructure moat is absolute. You cannot compete with Con Edison in New York City. It's not illegal—it's physically impossible. The right-of-way under Manhattan's streets is fully utilized. There's no room for competing cables. Even if there were, the cost to duplicate Con Edison's infrastructure would exceed $100 billion. The payback period, assuming you could somehow steal all their customers, would be 40 years. No rational investor would attempt it. This isn't a moat—it's an ocean.

But the real genius is the political economy. Con Edison employs 14,000 unionized workers in New York—voters who reliably support politicians who support Con Edison. The company pays $2.8 billion annually in property taxes—9% of New York City's property tax revenue. Every city councilmember knows that antagonizing Con Edison means explaining to constituents why their taxes went up or why their nephew lost his union job. It's mutual assured destruction, ensuring political stability.

The tax collection function is particularly elegant. Con Edison doesn't just pay taxes—it collects them. Look at your utility bill: delivery charges, system benefit charges, renewable energy charges, temporary state assessment surcharges. These aren't Con Edison fees—they're government taxes and programs that Con Edison collects on behalf of various agencies. The company is essentially a tax collector with better credit ratings than most governments. This makes Con Edison indispensable to government finance, creating another layer of protection.

Capital allocation in this environment follows different rules than in competitive markets. Con Edison doesn't maximize return on invested capital—it maximizes invested capital subject to regulatory approval. Every dollar spent on infrastructure earns that guaranteed 9% forever. This is why Con Edison will spend $500 million on grid modernization that might save customers $100 million—the savings don't matter; the $500 million added to the rate base does.

Managing regulatory relationships is the core competency. Con Edison maintains a full-time staff of 200 people whose only job is regulatory affairs. They don't just respond to regulations—they shape them. When New York considered retail electricity competition in 2016, Con Edison's regulatory team crafted the proposal that was ultimately adopted, ensuring that regardless of who sold the electricity, Con Edison would still own the delivery infrastructure. They wrote the rules of their own game.

The contrast with tech monopolies is instructive. Google or Facebook face constant antitrust scrutiny, consumer backlash, and competitive threats. Their monopolies depend on network effects that could theoretically reverse. Con Edison faces none of this. Nobody questions why one company controls all of New York's electricity distribution because the alternative—competing infrastructure—would be insane. Imagine three sets of power lines on every street, three gas pipeline networks, three steam systems. The monopoly isn't a market failure—it's the only rational market structure.

For investors, utilities like Con Edison offer something unique: predictable, inflation-protected returns with virtually no disruption risk. Warren Buffett owns $90 billion in utility assets precisely because he understands this dynamic. As he wrote to shareholders: "Society will forever need massive investments in both transportation and energy. It is in the self-interest of governments to treat capital providers in a manner that will ensure the continued flow of funds to essential projects. And it is in our self-interest to conduct our operations in a manner that earns the approval of our regulators and the people they represent."

This is why private equity can't disrupt utilities. You can't financially engineer a better return when returns are regulated. You can't cut costs when costs are passed through. You can't create value through multiple expansion when multiples are determined by allowed returns. The utility model is immune to modern financial capitalism's favorite tricks.

The lesson for infrastructure investors is profound: in essential services with natural monopoly characteristics, the regulatory framework is more important than the business operations. Con Edison doesn't win by being efficient or innovative—it wins by being necessary. In a world obsessed with disruption, there's enormous value in being undisruptable.

XI. Analysis & Investment Case

The bull case for Con Edison writes itself in an era of electrification everything. New York City's building electrification mandate means every skyscraper converting from gas to electric heating—adding 3,000 megawatts of demand by 2040, a 25% increase. The MTA's electric bus conversion adds another 500 megawatts. Uber and Lyft electrifying their fleets by 2030? Another 300 megawatts. Every climate policy is a demand driver for Con Edison's monopoly product.

The infrastructure super-cycle is even more compelling. The Infrastructure Investment and Jobs Act provides $65 billion for grid modernization, with New York getting $2.5 billion. But here's the kicker—utilities must match federal funds, meaning Con Edison will add $5 billion to its rate base with only $2.5 billion of shareholder capital. It's leveraged rate base growth with taxpayer subsidy. The company projects its rate base growing from $36 billion today to $51 billion by 2028—a 42% increase that translates directly to profit growth.

Regulatory certainty in New York is remarkable. The Public Service Commission just approved Con Edison's request for 9.2% allowed return on equity through 2025, above the national average of 8.8%. More importantly, they approved automatic recovery mechanisms for storm costs, bad debt, and property taxes—removing major earnings volatility. New York needs Con Edison to finance the energy transition. Antagonistic regulation would be economic suicide for the state.

The dividend aristocrat status matters more than most realize. Con Edison has paid dividends for 49 consecutive years, making it one of only 65 companies in the S&P 500 with such consistency. At the current $3.60 annual dividend and $111 stock price, that's a 3.2% yield—not spectacular, but with 4% annual dividend growth, total returns approach 7-8% with minimal risk. For pension funds and retirees, Con Edison is a bond substitute with inflation protection.

But the bear case has teeth. Capital intensity is crushing—Con Edison will spend $20 billion over the next five years just to maintain and moderately grow its system. That's $4 billion annually in a business generating $16 billion in revenue. Free cash flow after dividends is consistently negative, meaning Con Edison must constantly access capital markets. Rising interest rates directly impact profitability since utilities are essentially leveraged plays on the spread between allowed returns and borrowing costs.

Climate risks are existential and accelerating. Category 3 hurricanes, once considered impossible in New York, are now planned for. Sea level rise threatens $10 billion of Con Edison's infrastructure below the flood plain. The company spent $2 billion on Hurricane Sandy recovery—the next major storm could cost double. Insurance is becoming problematic; Con Edison increasingly self-insures, adding volatility to earnings.

The distributed generation threat is real but overstated. Yes, rooftop solar reduces demand, but it increases grid complexity, requiring more investment in smart grid technology. Battery storage could theoretically allow buildings to disconnect from the grid, but the economics don't work—a Manhattan office building would need $50 million in batteries to go off-grid, versus paying Con Edison $500,000 annually. The grid isn't disappearing; it's becoming more valuable as the platform enabling distributed resources.

With a market cap of $38.64 billion and the stock trading at $111.44 per share, representing 346,711,639 outstanding shares, Con Edison trades at compelling valuations. At 2.5x book value and 18x forward earnings, it's neither cheap nor expensive—it's fairly valued for a regulated utility with 5-7% rate base growth. The EV/EBITDA multiple of 11x reflects the capital intensity but also the earnings stability.

The competitive positioning is unassailable. National Grid operates in parts of New York but focuses on gas distribution. Public Service Enterprise Group operates in New Jersey but can't enter Con Edison's territory. The only theoretical competitor is municipalization—New York City taking over the utility—but the $50+ billion acquisition cost makes this political fantasy. Con Edison's monopoly is more secure than any tech platform's dominance.

ESG considerations are transformative. Con Edison is the enabler of New York's net-zero ambitions. Every electric vehicle charged, every heat pump installed, every distributed solar panel connected—all require Con Edison's grid. The company has committed to net-zero by 2040, investing $8 billion in renewable interconnection. For ESG-focused investors, Con Edison is a climate solution, not a climate problem.

The energy transition investment case is the most compelling long-term driver. Electrification of everything—transport, heating, cooking, industrial processes—means electricity growing from 20% of total energy consumption to potentially 50% by 2050. In New York, where Con Edison has monopoly distribution rights, this is pure demand growth flowing directly to the bottom line through rate base expansion.

For fundamental investors, Con Edison offers something rare: a business model that actually benefits from the problems it faces. Climate change requires grid hardening—rate base growth. Distributed generation requires grid modernization—rate base growth. Electrification requires capacity expansion—rate base growth. Every challenge becomes an investment opportunity that generates regulated returns. It's antifragile by design.

XII. Epilogue: The Future of Urban Infrastructure

Standing in Con Edison's control room in Queens, watching operators manage 13,000 megawatts of power flow across five boroughs in real-time, you're witnessing something remarkable: a 200-year-old company operating at the technological frontier. Every smart meter, every grid sensor, every predictive algorithm is layered atop infrastructure dating back to the Gilded Age. It's archaeology and artificial intelligence occupying the same space.

The grid of 2050 will be unrecognizable from today's, yet Con Edison will still own it. Imagine buildings as batteries, storing power when cheap and selling it back when expensive. Vehicle-to-grid technology turning every parked electric car into a distributed power plant. Artificial intelligence predicting and preventing outages before they occur. Quantum computing optimizing power flow in ways current mathematics can't conceive. All of it will flow through Con Edison's wires, generating those guaranteed returns.

Climate adaptation will reshape everything. Con Edison is already planning for 2100 scenarios: summer temperatures reaching 115°F, creating unprecedented cooling demand; winter polar vortexes dropping to -20°F, stressing heating systems never designed for such extremes; hurricanes arriving annually rather than generationally. The company is designing infrastructure for a climate that doesn't yet exist—a remarkable act of faith in both engineering and capitalism.

The smart city revolution makes Con Edison more essential, not less. Every IoT sensor, every connected streetlight, every automated building system requires reliable power. The data centers supporting urban artificial intelligence consume massive amounts of electricity—Manhattan alone has 400 megawatts of data center demand, growing 20% annually. The digital city is an electric city, and Con Edison owns the electrons.

Distributed energy resources seem disruptive but actually entrench Con Edison's position. Managing millions of solar panels, batteries, and smart appliances requires a orchestration platform—the grid itself. Con Edison becomes not just a utility but a system operator, a market maker, a technology platform. It's the App Store for energy, taking a cut of every transaction while others do the innovation.

But the real future is about resilience, not just reliability. Cities are recognizing that infrastructure is destiny—that economic competitiveness depends on power reliability, climate resilience, and energy affordability. Con Edison's ability to deliver all three makes it indispensable to New York's future. The company that started by lighting gas lamps will end up powering whatever comes next.

The philosophical implications are profound. Con Edison represents a different model of capitalism—one where returns come not from innovation or efficiency but from stewardship of essential infrastructure. It's almost medieval in its stability: a hereditary monopoly passing from generation to generation, collecting rents from an unchanging territory. Yet it's also radically modern, constantly rebuilding itself while maintaining perfect continuity of service.

What does the next 200 years look like? Con Edison will still be here, that much is certain. The company has survived two world wars, the Great Depression, the 1970s fiscal crisis, 9/11, Hurricane Sandy, and COVID-19. It has transitioned from whale oil to gas to electricity and will transition again to whatever energy form the 22nd century demands. The infrastructure will evolve, the technology will transform, but the monopoly will endure.

There's a plaque at 257 Pearl Street, where Edison's first power station stood. It reads: "Here began the electric age." But that's only half right. The electric age didn't begin with generation—it began with distribution, with the wires and systems that made electricity useful. Con Edison owns those wires, and in owning them, owns a piece of civilization itself. As long as New York needs power, Con Edison will deliver it, collecting its regulated return, indifferent to disruption, essential to everything.

The company that began in 1823 lighting streets with gas will likely still exist in 2223, powering technologies we can't imagine through infrastructure we're building today. That's not just a business model—it's a form of institutional immortality. In a world where the average S&P 500 company lasts 20 years, Con Edison has lasted 200 and is planning for 200 more. It's the ultimate infrastructure play: betting on the permanence of New York City and the perpetual human need for power.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube