eBay: The Accidental Marketplace Empire

I. Introduction & Episode Roadmap

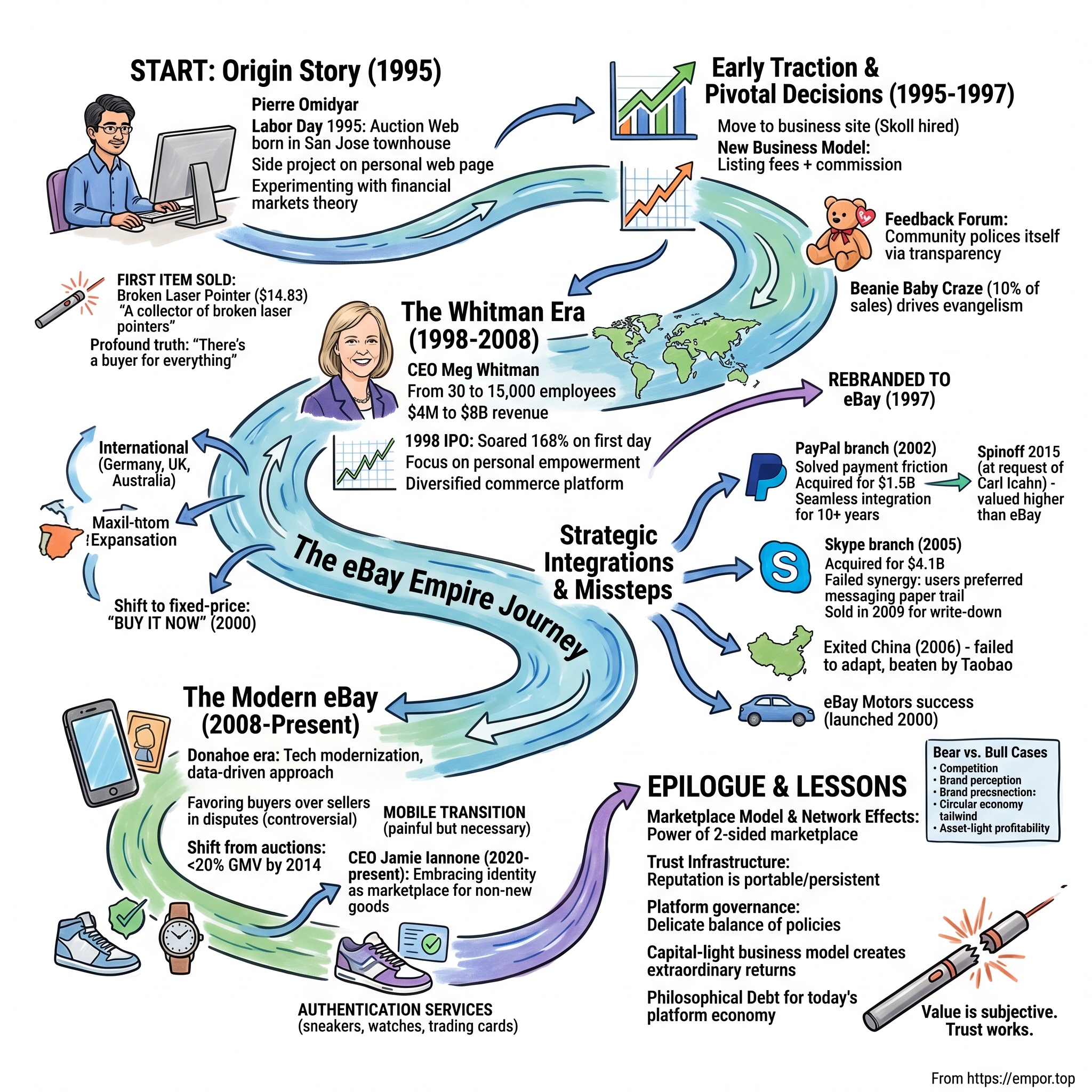

Picture this: Labor Day weekend, 1995. A 28-year-old computer programmer sits alone in his San Jose townhouse, typing code that would fundamentally reshape commerce for hundreds of millions of people. Pierre Omidyar wasn't trying to build a billion-dollar company—he was just experimenting with an idea on his personal web page. Within hours of launching what he called AuctionWeb, something extraordinary happened. Strangers began arriving at his digital experiment, not just browsing but actually transacting with each other.

The first item ever sold tells you everything you need to know about what made eBay special. Omidyar had listed a broken laser pointer on the site he created over Labor Day weekend. To his surprise, someone came forward and bought the laser pointer for $14.83. Bewildered, Omidyar contacted the buyer to make sure he understood the item was actually broken. The response came back: "I'm a collector of broken laser pointers". In that moment, Omidyar glimpsed a profound truth about human nature and markets: there's a buyer for everything, if you can just connect them with the seller.

What followed was one of the most improbable success stories in business history. A company that started as a side project would go public at a $700 million valuation just three years later, with the stock soaring 168% on its first day of trading. It would survive the dot-com crash, fend off Amazon, and create entirely new categories of entrepreneurs—from stay-at-home parents running six-figure businesses to the birth of the modern sneaker resale market.

This is the story of how a simple feedback system became more trusted than traditional retail, how a company with no inventory became one of the world's largest retailers, and how the fundamental human desire to hunt for treasure in someone else's junk drawer was transformed into a $30+ billion marketplace that processes over $70 billion in gross merchandise volume annually. It's also a cautionary tale about the challenges of platform evolution, the perils of strategic acquisitions, and what happens when you try to move away from the very thing that made you special.

II. Pierre Omidyar & The Origin Story

Pierre Morad Omidyar was born in Paris on June 21, 1967, to an Iranian family that would soon embark on a journey that epitomized the American immigrant success story. His family moved to Maryland when his father accepted a residency at Johns Hopkins University Medical Center. Growing up in the suburbs of Washington D.C., young Pierre displayed an early fascination with computers that would define his life's trajectory.

At age 14, he wrote his first computer program to catalog books for the school library—a harbinger of his future obsession with organizing and connecting information. As a precocious teen, he would regularly sneak out of physical education classes to play with his high school's computers. Rather than punish him, the principal hired him to write the catalog program at $6 per hour.

After graduating from Tufts University with a computer science degree in 1988, Omidyar's career path seemed conventional enough. He went to work for a company that developed Macintosh software, then later worked for the Apple subsidiary Claris, before helping start a software company in 1991 called Ink Development Corp. The company later changed its name to eShop and was purchased by Microsoft in 1996.

But Omidyar was restless. He saw the early web not just as a technical marvel but as a social experiment waiting to happen. In the summer of 1995, he became fascinated with the theory that in financial markets, goods will trade at fair value only when everyone has access to the same information. It was a cool theory, but the practice hit him personally when he tried to invest in an IPO for a gaming company. The company went public at $15 a share, but his broker called saying he got the stock at $24. When Omidyar asked why, the broker replied, "Well, $15 was the ideal price, not the price that people like you can get".

This moment of frustration crystallized into inspiration. What if there was a truly level playing field where anyone could buy or sell anything to anyone else, with perfect information transparency?

On Labor Day 1995, Omidyar launched the fledgling auction site which he dubbed eBay (for "electronic Bay," a reference to the San Francisco Bay area)—though that's getting ahead of ourselves. On September 4, 1995, he launched the online auction service called Auction Web. The site was remarkably primitive: gray background, basic HTML, times rendered in military format. Omidyar made no guarantees about the goods being offered, took no responsibility and settled no disputes. He simply offered a place where users could go online, interact and bid for items.

The famous story about eBay being created to help Omidyar's fiancée trade Pez dispensers? Pure fiction. The Pez story was fabricated by a PR manager in 1997. Whenever she hears about it, his wife rolls her eyes: "Tell them I'm a management consultant. Tell them I have a master's degree in molecular biology. I am not just this little Pez candy collector".

The real vision was both simpler and more profound. Omidyar wanted to help people do business with one another on the Internet. People thought it was impossible—remember this is 1995—how could they trust each other? This question would become the cornerstone of everything eBay would build.

III. Early Traction & Pivotal Decisions (1995–1997)

The broken laser pointer sale wasn't just eBay's first transaction—it was a revelation about human psychology and the long tail of commerce. Omidyar had bought the $30 laser pointer intending to use it for presentations, but ended up using it to make his cat chase the red dot. When it broke after two weeks, he decided to list it because it would be a good test for AuctionWeb and cost him nothing. In the listing, he admitted the item didn't work, even with new batteries.

Much to Omidyar's surprise, collectors of Barbie dolls, Beanie Babies and household junk seized upon eBay almost immediately. By February, the site had become so popular that it outgrew Omidyar's personal Internet account. This forced a pivotal business model decision that would define the company's economics forever.

With the help of his friend Jeff Skoll, Omidyar moved eBay to a more expensive business site and to cover his increased costs, began charging a few cents to list an item and collecting a small commission if it was sold. The small fee he collected on each sale financed the expansion of the site. The revenue soon outstripped his salary at General Magic, and Omidyar decided to dedicate his full attention to his new enterprise.

What happened next was crucial for eBay's future: the creation of the trust infrastructure. Auction Web added a Feedback Forum, allowing buyers and sellers to rate each other for honesty and reliability. This wasn't just a feature—it was a philosophical statement. Rather than eBay serving as the arbiter of disputes, the community would police itself through radical transparency.

But the real accelerant for eBay's early growth came from an unexpected source: the Beanie Baby phenomenon. The resulting scarcity from Ty's production restrictions led to a significant increase in sales, starting the trend of collecting and reselling Beanie Babies. Their popularity soon grew into a national craze in the US.

At the height of the craze, people would flip Beanies for as much as ten-fold on eBay. At their peak, Beanies made up 10% of eBay's sales. In 1997, eBay sold over $500,000 worth of the toys in a single month, with sellers averaging a profit of 500% of the retail value. The Beanie Baby collectors weren't just customers—they were evangelists, spreading the word about this new way to find rare items and complete their collections.

The growth numbers were staggering for a company with no marketing budget. In 1996, Auction Web hosted 250,000 auctions. In the first month of 1997, it hosted 2 million. By the middle of that year, eBay was hosting nearly 800,000 auctions a day.

By 1997, Omidyar knew he needed to rebrand. He changed the company's name from AuctionWeb to eBay and began advertising aggressively. The name "eBay" was actually his second choice—he originally wanted Echo Bay, the name of a recreational area near Lake Mead, Nevada, because it "sounded cool." When he learned that echobay.com was taken by a Canadian mining company, he dropped the "cho," and ebay.com was born.

The most important hire of this period wasn't a typical Silicon Valley move. In 1996, Jeff Skoll met eBay's founder Pierre Omidyar, who hired him as the company's first president and first full-time employee. While eBay was already profitable at the time Skoll joined, he wrote the business plan that eBay followed in subsequent years. eBay didn't even have a real street address—Skoll's home in Palo Alto served as its headquarters. He quit his Knight-Ridder job in 1996 to become eBay's full-time president.

Skoll brought something crucial: business discipline to complement Omidyar's technical vision. Together, they made a decision that would prove prescient—they would stay focused on being a pure marketplace, never holding inventory, never getting into the logistics business. Let the community handle everything except the platform itself.

IV. Meg Whitman Era: Professional Management (1998–2008)

When a corporate headhunter first approached Meg Whitman in 1998 to lead the online auction company eBay, she was not interested. But a visit to eBay's headquarters and the testimonies of many enthusiastic users impressed her. What she saw in that cramped San Jose office would change her life—and the trajectory of e-commerce.

She took the job as president and CEO of eBay, a company with just 30 employees, in 1998. Today, eBay has 13,000 employees and 193 million users all over the world. But the transformation wasn't smooth from day one.

Her first challenge at eBay came on her first day. The website crashed for eight hours. It was a baptism by fire that would prepare her for the scaling challenges ahead. One of Whitman's first responsibilities was to prepare the company for its initial public offering in September 1998.

The IPO itself became part of Silicon Valley lore. The initial price to the public was $18.00 per share. The final first-day closing price was $44.88—an instant validation of the marketplace model. The offering turned Omidyar and Skoll into billionaires overnight, but more importantly, it gave eBay the capital and credibility to expand aggressively.

Under Whitman's leadership, eBay transformed from a quirky collectibles site into a diversified commerce platform. She understood something fundamental: eBay wasn't really in the auction business—it was in the personal empowerment business. Many people who had been shut out of the traditional economy, such as stay-at-home mothers, disabled people, and senior citizens, had found on eBay a way to earn extra or even primary income.

The company's growth during the Whitman era was breathtaking. When she left in 2008, the company had $8 billion in revenue—up from $4 million when she started in 1998. She brought the company from having less than 50 employees to having 15,000.

But growth at this scale brought operational challenges. The most dramatic crisis came in June 1999. On June 10, 1999, the site goes down. In the middle of the night, CEO Meg Whitman rallies more than 50 engineers from eBay and Sun Microsystems to fix the problem. Less than 20 hours later since the outage began, eBay is back up and open for business.

The site experienced problems that resulted in a hard outage lasting nearly 24 hours. This was the second time in two days that they experienced this problem. The company said it expected to lose between $3 million and $5 million in second-quarter revenue due to the near 22-hour outage.

The incident forced eBay to completely rethink its infrastructure. It wasn't just about keeping the site up—it was about maintaining trust. Every minute of downtime meant thousands of auctions ending without their final bids, sellers losing sales, and buyers losing opportunities. The company implemented new policies: automatic 24-hour extensions for all affected auctions and full refunds of all fees during outages.

International expansion became a key focus under Whitman. The company launched sites in Germany, the UK, and Australia, adapting to local markets while maintaining the core marketplace model. Some markets, like Germany, became massive successes. Others, like China, would prove more challenging, eventually leading to eBay's retreat in favor of local competitors like Alibaba's Taobao.

Perhaps the most important strategic evolution during the Whitman era was the shift from pure auctions to fixed-price sales. Introducing "Buy It Now" in 2000 was controversial among purists who loved the thrill of the auction, but it opened eBay to buyers who wanted certainty and immediate gratification. By the time Whitman left, the majority of eBay's gross merchandise volume came from fixed-price sales, not auctions.

V. PayPal: The $1.5 Billion Integration

The PayPal story is perhaps the best example of eBay's complicated relationship with innovation—simultaneously recognizing brilliance and struggling to fully capitalize on it.

In the early days, payments were eBay's Achilles' heel. Buyers would send checks or money orders through the mail, adding days or weeks to each transaction. During Auction Web's early days, people would send their payments in the form of coins taped to index cards. This friction limited growth and created massive trust issues.

eBay tried to solve this with Billpoint, its own payment service launched in 1999. But a scrappy startup called PayPal, founded by Peter Thiel and Max Levchin (later joined by Elon Musk's X.com), had already captured the hearts and wallets of eBay users. PayPal's growth strategy was brilliant: they paid users $10 to sign up and $10 for each referral, creating viral growth that perfectly matched eBay's network effects.

By 2001, PayPal was processing the majority of eBay's payment volume, despite eBay's attempts to promote Billpoint. The companies were locked in an uneasy symbiosis—PayPal needed eBay's transaction volume, and eBay's users overwhelmingly preferred PayPal.

In March 1998, Meg Whitman was elected president and CEO, and she quickly recognized the strategic imperative. "PayPal had become the wallet on eBay," Whitman said. "We had to own that company". In 2002, soon after PayPal's initial public offering, it became a wholly owned subsidiary of eBay valued at $1.5 billion.

The acquisition was immediately accretive, adding a high-margin revenue stream to eBay's marketplace fees. PayPal's technology was superior to Billpoint's, and its brand had genuine user loyalty. For over a decade, the combination seemed like corporate strategy at its best—PayPal provided the payment rails for eBay's marketplace, while eBay provided the transaction volume for PayPal's growth.

But beneath the surface, tensions were building. PayPal's ambitions extended far beyond eBay. It wanted to be the payment solution for the entire internet, not just one marketplace. eBay's management, focused on marketplace dynamics, didn't fully appreciate PayPal's potential as a standalone platform business.

By 2014, these tensions had become untenable. Activist investor Carl Icahn began pushing for a spinoff, arguing that PayPal was being held back by its parent company. The numbers supported his thesis: PayPal's off-eBay volume was growing faster than its on-eBay volume. In 2015, eBay announced the separation. When PayPal went public as an independent company, it was valued at $47 billion—more than eBay itself.

Today, PayPal's market cap exceeds $60 billion while eBay's hovers around $30 billion. The student had surpassed the teacher, raising uncomfortable questions about whether eBay's management truly understood what they had owned.

VI. Scaling Challenges & Strategic Missteps

Not every big bet paid off. The Skype acquisition in 2005 stands as one of the most puzzling strategic decisions in tech history. During Whitman's tenure as CEO, eBay completed the purchase of Skype for $4.1B in cash and stock in September 2005.

The rationale seemed logical at the time: Skype could enable better communication between buyers and sellers, particularly for high-value items like cars or real estate. Whitman argued that voice communication would add trust to transactions. "The goal is to harness 'the power of three'—getting all three companies to thrive on their own but also build on each other's strengths. One area where PayPal and Skype can work together, for example, is in fraud-fighting efforts".

But the synergies never materialized. eBay users didn't want to talk to each other—the asynchronous nature of messaging was actually a feature, not a bug. It allowed buyers and sellers in different time zones to communicate without scheduling calls. More fundamentally, voice communication removed the paper trail that both parties relied on for dispute resolution.

By 2009, eBay admitted defeat, selling 65% of Skype to private equity investors at a $2.75 billion valuation—a massive write-down. Microsoft later acquired Skype for $8.5 billion, adding insult to injury. The episode revealed a crucial weakness: eBay's leadership didn't always understand the subtle dynamics that made their own platform work.

The China exit was another humbling moment. eBay entered China in 2002 by acquiring EachNet, the country's leading auction site. But they made a critical error: they tried to impose the global eBay platform and rules on the Chinese market. Meanwhile, Alibaba's Taobao launched with free listings (compared to eBay's fees) and integrated instant messaging (understanding that Chinese consumers wanted to chat and negotiate).

By 2006, eBay had effectively surrendered, shutting down its China site. Taobao had captured over 80% of the Chinese C2C market. The lesson was clear: marketplace dynamics are deeply cultural, and what works in San Jose might fail in Shanghai.

Yet not all expansions failed. eBay Motors, launched in 2000, became a massive success. The company launched eBay Motors, the online automotive marketplace. By 2006, eBay Motors sold its 2 millionth passenger vehicle. The key insight: cars were perfect for eBay's model. They were high-value items where buyers were willing to travel or arrange shipping, and the fragmented used car market benefited from national liquidity.

VII. The Marketplace Model & Network Effects

To understand eBay's resilience through multiple tech cycles, you have to understand the raw power of network effects in a two-sided marketplace. Every seller who joins makes eBay more valuable for buyers (more selection), and every buyer makes it more valuable for sellers (more demand). It's a self-reinforcing cycle that, once it reaches critical mass, becomes nearly impossible to disrupt.

The feedback system was the crucial innovation that made these network effects sustainable. By making reputation portable and persistent, eBay solved the fundamental trust problem of online commerce. A seller who spent years building a 99.9% positive feedback rating had a massive asset that was worthless anywhere else. This created switching costs that locked in supply.

The numbers tell the story of operating leverage at scale. eBay takes roughly 10% of each transaction but bears none of the inventory risk, shipping costs, or customer service burden. The sellers handle all of that. It's a capital-light model that generates extraordinary margins once fixed costs are covered.

Compare this to Amazon's evolution. While Amazon started as a marketplace, it increasingly moved toward a first-party retail model, buying inventory and managing fulfillment. This gave Amazon more control but required massive capital investment. eBay stayed pure: it would never touch the goods being sold. This philosophical difference would define both companies' trajectories.

The geographic expansion of liquidity was another key dynamic. In the early days, you might find one vintage Gibson guitar for sale in your city. On eBay, you could choose from hundreds nationwide. This density of supply and demand in niche categories created winner-take-all dynamics in collectibles, parts, and other long-tail categories.

But network effects can also work in reverse. As eBay raised fees to boost profits, some sellers defected to Amazon or started their own Shopify stores. As selection decreased in certain categories, buyers followed. The virtuous cycle can become vicious if not carefully managed.

VIII. Mobile Transition & Modern eBay (2008–Present)

Whitman resigned as CEO of eBay in November 2007, but remained on the board and served as an advisor to new CEO John Donahoe until late 2008. The Donahoe era (2008-2015) was defined by a recognition that eBay had fallen behind technologically. The site looked dated, the search function was primitive, and mobile adoption was embarrassingly slow.

Donahoe, a former Bain consultant, brought a data-driven approach to modernization. He invested heavily in technology infrastructure, improved the search algorithm, and pushed the company toward mobile. But his most controversial decision was to favor buyers over sellers in disputes, reasoning that buyer trust was essential for growth. This alienated many long-time sellers who felt eBay had abandoned them.

The shift from auctions to fixed-price listings accelerated under Donahoe. By 2014, auctions represented less than 20% of gross merchandise volume. The thrill of the hunt that defined early eBay was being replaced by the convenience of immediate purchase. Purists mourned the change, but the data was clear: buyers wanted certainty.

The mobile transition was particularly painful. eBay's desktop-centric experience didn't translate well to smartphones. Meanwhile, mobile-native competitors like Mercari and OfferUp were gaining traction in local marketplaces. eBay's mobile apps felt clunky and slow, a far cry from the delightful simplicity of the original AuctionWeb.

The 2015 PayPal spinoff marked the end of the Donahoe era. The separation was complex—the companies had to unwind years of technical integration while maintaining service for millions of active users. But it was necessary. PayPal needed independence to compete with Square and Stripe, while eBay needed to focus on its marketplace challenges.

Under current CEO Jamie Iannone (2020-present), eBay has embraced its identity as the marketplace for non-new goods. Authentication services for sneakers and watches, partnering with consignment shops for luxury goods, and investing in vertical-specific experiences for trading cards and collectibles. It's a strategy that plays to eBay's historical strengths while acknowledging that it will never out-Amazon Amazon.

The managed payments transition, completed in 2021, saw eBay finally in-house payment processing after relying on PayPal for nearly two decades. This gave eBay more control over the user experience and better economics, but it also meant taking on fraud risk and regulatory compliance that PayPal had previously handled.

IX. Investment & Business Lessons

The eBay story offers profound lessons about platform businesses, network effects, and the challenges of evolution at scale.

First, timing matters enormously. eBay launched at the perfect moment: internet penetration was reaching critical mass, but e-commerce was still nascent. Traditional retailers hadn't figured out online, and consumers were just becoming comfortable with digital payments. Five years earlier, the infrastructure didn't exist. Five years later, Amazon might have already locked up the market.

Second, capital-light business models create extraordinary returns when they work. eBay never held inventory, never operated warehouses, never employed delivery drivers. Yet it facilitated billions in commerce while maintaining software-like margins. This asset-light approach meant that revenue growth dropped almost entirely to the bottom line once fixed costs were covered.

The importance of trust in marketplaces cannot be overstated. The feedback system wasn't just a feature—it was the core innovation that enabled everything else. By making reputation quantifiable and portable, eBay created a currency more valuable than traditional advertising or brand building. A seller with 10,000 positive reviews had an asset worth real money.

Management transitions are critical inflection points. The handoff from Omidyar to Whitman worked because they had complementary skills and shared vision. Omidyar provided technical innovation and philosophical direction; Whitman brought operational excellence and scaling expertise. But later transitions were rockier, as leaders struggled to balance eBay's community roots with Wall Street's growth demands.

The acquisition track record reveals the difficulty of strategic M&A. PayPal was a massive success—until eBay failed to fully capitalize on it. Skype was a disaster that destroyed billions in value. The difference? PayPal was already integrated into eBay's ecosystem, while Skype required forcing unnatural behavior changes on users.

Platform governance is an underappreciated challenge. Every policy change—fee increases, dispute resolution rules, category restrictions—affects the delicate balance between buyers and sellers. Favor buyers too much, and sellers revolt. Favor sellers, and buyers lose trust. eBay's constant tweaking of these rules shows how difficult it is to maintain equilibrium.

The innovator's dilemma played out in real-time. eBay knew that mobile was important but couldn't move fast enough. They saw that Amazon was a threat but couldn't match its logistics investments. They understood that payment innovation was crucial but let PayPal's potential slip through their fingers. Large companies often see disruption coming but can't pivot quickly enough to address it.

X. Bear vs. Bull Case Analysis

The Bear Case:

eBay faces structural headwinds that may be insurmountable. Amazon has won the war for new goods, offering faster shipping, better prices, and superior customer service. For used goods, Facebook Marketplace provides local transaction convenience without fees. Specialized marketplaces like StockX (sneakers), Reverb (musical instruments), and The RealReal (luxury goods) are cherry-picking eBay's most profitable categories.

The brand perception problem is real and worsening. Millennials and Gen Z associate eBay with their parents' generation, a dusty attic of the internet where you might find obscure collectibles but not anything you actually need. The auction format, once eBay's differentiation, feels anachronistic in an age of instant gratification.

International market share continues to erode. After exiting China, eBay has struggled to compete with local champions in other markets. MercadoLibre dominates Latin America, Allegro owns Poland, and TradeMe rules New Zealand. The dream of a truly global marketplace has fragmented into regional fiefdoms.

The company's growth has stagnated. While gross merchandise volume inches up at low single digits, it's mostly driven by price inflation rather than unit growth. Active buyer growth has flatlined. The core marketplace is ex-growth, making eBay essentially a value stock in a growth stock's body.

The Bull Case:

eBay's moat in certain categories remains formidable. For collectibles, car parts, vintage items, and business equipment, eBay's liquidity is unmatched. Try finding a specific 1960s guitar amplifier or a discontinued automotive part on Amazon—you can't. These categories may be niche, but they're highly profitable with loyal users.

Authentication services represent a genuine innovation that competitors haven't matched. By guaranteeing authenticity for sneakers, watches, and trading cards, eBay solves a trust problem that plagues every marketplace for high-value collectibles. This service commands premium take rates and attracts younger collectors.

The asset-light model means eBay can remain highly profitable even without growth. With 40%+ EBITDA margins and minimal capital requirements, eBay generates prodigious cash flow. They've returned over $40 billion to shareholders through buybacks and dividends since 2010. For value investors, it's a cash machine trading at a reasonable multiple.

The circular economy tailwind could revitalize growth. As consumers become more environmentally conscious and economically pressured, the appeal of used goods increases. eBay is perfectly positioned for a world that values sustainability and value over newness and convenience.

Hidden asset value exists in the data and user base. With 130+ million active buyers and decades of transaction history, eBay possesses one of the richest datasets on consumer behavior and pricing dynamics. This data could be monetized through advertising (already growing rapidly) or AI-powered services that help sellers optimize pricing and inventory.

XI. Epilogue & Reflections

On Labor Day weekend in 1995, a 28-year-old Pierre Omidyar sat down at his computer to write the code for what would become eBay. Today, the San Jose, California-based company has 31,500 employees and $14 billion in revenue and has made Omidyar one of the richest people in the world.

The journey from AuctionWeb to eBay represents something larger than a business success story. It's a testament to the power of aligned incentives, the importance of trust in human commerce, and the extraordinary value that can be created by simply connecting buyers and sellers efficiently.

Pierre Omidyar's entire approach to philanthropy is rooted in what he witnessed at eBay. Everything he's done is rooted in the notion that every human being is born equally capable. What people lack is equal opportunity. His goal has been to expand opportunity to as many people as possible so they can reach their potential. That's the approach they took with eBay.

The platform economy that dominates today's tech landscape—from Uber to Airbnb to DoorDash—owes a philosophical debt to eBay. The idea that you could build a massive business by facilitating transactions rather than participating in them, that you could create trust between strangers through systematic feedback, that technology could unlock value in underutilized assets—these concepts were pioneered in that San Jose townhouse.

Yet eBay's story also serves as a warning. Network effects are powerful but not permanent. Brand relevance requires constant renewal. Strategic acquisitions must be integrated, not just owned. And perhaps most importantly, losing touch with your core user base in pursuit of growth can be fatal.

Looking forward, eBay faces an existential question: Is there room for a general-purpose, horizontal marketplace in an increasingly verticalized world? Or will eBay slowly transform into a collection of specialized marketplaces for collectibles, parts, and other non-commodity items?

The answer may lie in embracing what made eBay special in the first place—not the auction format or the fees structure, but the fundamental human behavior it enabled. People love to hunt for treasure. They love finding deals. They love the thrill of discovery and the satisfaction of selling something they no longer need to someone who values it.

"I believe that people are generally good," Omidyar said, "and I felt that we should have a community that embraces a system of values". In an age of algorithmic manipulation and surveillance capitalism, there's something refreshingly naive about this vision. But it worked. For millions of people, eBay created opportunity where none existed before.

The broken laser pointer that started it all now sits in a place of honor—a reminder that value is subjective, markets are mysterious, and sometimes the most successful businesses are the ones that trust their users to figure things out for themselves.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube