Brinker International: From Casual Dining Pioneer to Digital Transformation Leader

I. Introduction & Episode Roadmap

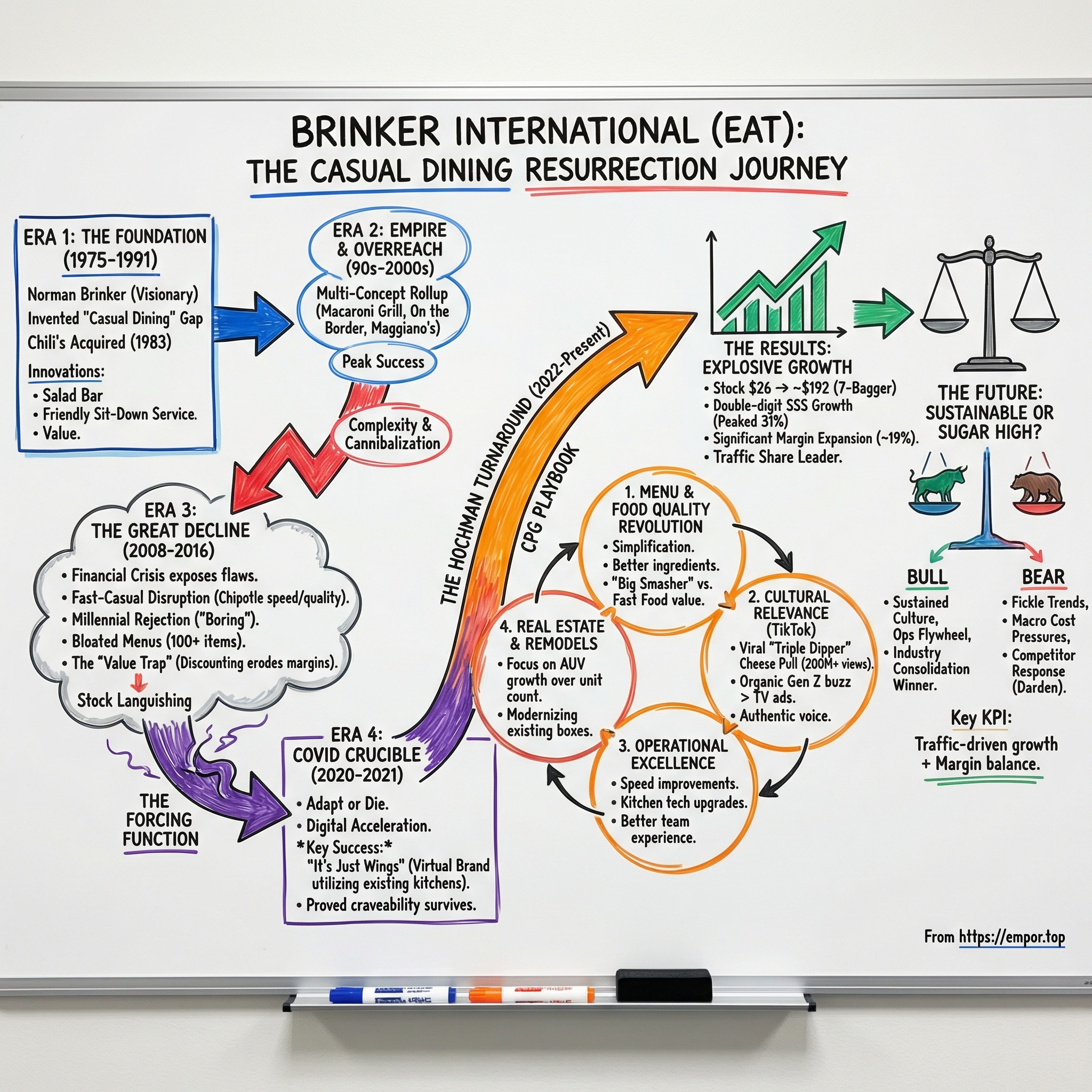

Picture this: a fifty-year-old restaurant chain, written off by Wall Street and mocked by millennials as a relic of suburban mediocrity, suddenly becomes the hottest brand on TikTok. A cheese pull video from a nine-dollar appetizer platter goes viral, racking up two hundred million views. A ten-dollar burger meal becomes a Gen Z status symbol, cheaper than a fast-food combo and served with bottomless chips and salsa. The stock, languishing around twenty-six dollars when the new CEO arrived, rockets past one hundred and ninety dollars in less than three years, a seven-bagger that made believers out of skeptics and case studies out of business school professors.

This is the story of Brinker International, parent company of Chili's Grill & Bar and Maggiano's Little Italy, and it is one of the most remarkable corporate turnarounds in American restaurant history.

Brinker International, trading under the ticker EAT on the New York Stock Exchange, operates and franchises more than 1,600 restaurants across 28 countries. In fiscal year 2025, ending June 2025, the company generated $5.4 billion in revenue, a staggering twenty-two percent increase over the prior year. But the numbers only tell part of the story. The real narrative is about how a company named after the godfather of casual dining nearly died alongside the category he created, only to be resurrected by a consumer packaged goods executive who understood something his predecessors didn't: the future of restaurants isn't about food quality versus speed versus price. It's about cultural relevance.

The central question of this deep dive is deceptively simple: how did a single Dallas steakhouse concept become the casual dining bellwether that's thriving while peers crumble? To answer it, we need to trace an arc that spans five decades, from the invention of the salad bar to the invention of the Nashville Hot Mozz. We need to understand category creation, rollup strategy, near-death experiences, and viral resurrection. We need to examine the unit economics of a business where three percent net margins are considered acceptable and a single bad quarter can destroy years of brand equity.

Along the way, we'll meet Norman Brinker, the polo-playing Olympic equestrian who literally invented casual dining, a man whose competitive fire was so intense that he survived a traumatic polo accident in 1993 that left him in a coma for two weeks and returned to running his company within months. We'll watch his empire expand through acquisitions, contract through divestitures, and nearly collapse under the weight of fast-casual disruption and COVID-19. And then we'll meet Kevin Hochman, the Procter & Gamble alumnus who turned around KFC before arriving at Chili's with a contrarian thesis: that Gen Z, the generation everyone said would never eat at chain restaurants, was actually the key to saving them.

This is the story of an American institution that refused to die. And embedded within it are lessons about brand building, category positioning, operational leverage, and the difference between a fad and a franchise that apply far beyond the restaurant industry.

II. The Casual Dining Revolution & Founding Context (1975-1991)

To understand where Brinker International stands today, you have to understand where it came from. And that means going back to a time when the American restaurant landscape looked nothing like it does now.

Before Norman Brinker, dining in America was binary. On one side, you had white-tablecloth restaurants where a steak dinner cost a day's wages, reservations were required weeks in advance, and the maitre d' judged your jacket before deciding whether to seat you. On the other, you had McDonald's, where you could feed a family of four for five dollars but ate standing up in a plastic booth or in your car in a parking lot. There was nothing in between. No place where a middle-class family could sit down, be served by a waiter who introduced themselves by name, and enjoy a decent meal with a margarita for ten or fifteen dollars per person. That gap wasn't just an oversight. It was a category waiting to be invented, and Norman Brinker was the man who invented it.

Norman Eugene Brinker was born in 1931 in Denver, Colorado, and raised on a ten-acre farm in Roswell, New Mexico. He was, by every account, a man of relentless energy and audacious ambition. As a child, he ran a rabbit farm at age ten, managed a paper route, and bought and sold horses. He competed on the U.S. Olympic Equestrian team at the 1952 Helsinki Games, then rode in the 1954 pentathlon world championships in Budapest. The competitive instinct never left him. It simply found a new arena.

After graduating from San Diego State College in 1957, Brinker joined Jack in the Box, then a tiny fast-food chain with fewer than ten locations in Southern California. Within two years, he was elevated to president and had accumulated a twenty percent stake in the company. He learned the mechanics of scaling a restaurant brand, the discipline of operational consistency, the mathematics of throughput and ticket averages. But he also saw the limitations of fast food. The margins were thin, the customer loyalty was nonexistent, and the experience was transactional. Brinker wanted to build something with soul.

In 1966, he founded Steak and Ale in Dallas, putting up every dollar he had. The concept was revolutionary in ways that seem obvious in hindsight but were genuinely radical at the time. Brinker created dimly lit Tudor-style dining rooms with exposed brick and warm wood paneling that offered an upscale steak experience at accessible prices. A customer could get a quality steak dinner for under five dollars at a time when comparable meals at fine dining establishments cost three or four times as much. He invented the restaurant salad bar, a concept so novel that customers literally didn't know what to do with it at first. They would leave their tables to serve themselves from a communal buffet of greens, croutons, and dressings, creating a sense of participation in their own meal that felt liberating compared to the rigid formality of traditional steakhouses. He introduced the practice of servers greeting tables by name and introducing themselves personally, a move so successful it became an industry standard within a decade. Steak and Ale proved that Americans would pay a premium over fast food for atmosphere, service, and the feeling of being treated like a guest rather than a customer.

The concept grew rapidly, reaching more than one hundred locations by the mid-1970s. Every restaurant was a gathering place, a democratic space where a family of four could enjoy the trappings of fine dining without the intimidation or the expense. Brinker was not just building restaurants. He was building a new category of American life.

Brinker sold Steak and Ale to Pillsbury in 1976 for approximately $100 million, then rose to become president of Pillsbury's entire restaurant operations division. While there, he created Bennigan's, which pioneered the "fern bar" concept, restaurants designed to attract young singles in the era of disco and yuppie culture. Fern bars became a phenomenon. TGI Friday's, Ruby Tuesday, Houlihan's, and Applebee's all followed the template Brinker established.

But the concept that would define his legacy was already taking shape in Dallas. In March 1975, a restaurateur named Larry Lavine had opened the first Chili's Grill & Bar in a converted postal station on Greenville Avenue. The concept was simple: Southwestern flair, affordable hamburgers, cold beer, and a fun, casual atmosphere. By the early 1980s, Lavine had grown the chain to twenty-three locations, but he was running out of capital and operational expertise to scale further. The restaurants had less than one million dollars in equity and were carrying $8.5 million in debt.

In 1983, Norman Brinker acquired the Chili's chain. It was the partnership of visionary operator and proven concept. Within a year, those twenty-three restaurants were generating $40 million in sales. Brinker took the company public on January 9, 1984, trading under the ticker EAT at a split-adjusted price of two dollars per share. The IPO was oversubscribed, buoyed by Brinker's reputation and the obvious demand for what he was building.

The insight that drove everything was deceptively simple: Americans wanted sit-down service without the formality or the price tag. They wanted a place where they could bring the kids on Tuesday night, take a date on Friday, and meet colleagues for a business lunch on Wednesday. They wanted burgers and ribs and margaritas served by friendly people in a room with personality. Casual dining filled a void that millions of Americans didn't even know existed until Brinker gave it to them.

Through the mid-1980s, Chili's expanded aggressively, perfecting its real estate playbook, franchising strategy, and restaurant prototype. The real estate strategy was particularly shrewd: Brinker's team identified suburban intersections with high traffic counts and strong demographics, then clustered multiple locations within a market to maximize advertising efficiency. A television ad in Dallas didn't help if you only had one restaurant in the metro area. But if you had fifteen, that same ad drove traffic to all of them. This clustering strategy created local scale advantages that were difficult for competitors to match.

The franchising model provided capital-light expansion while maintaining brand control. Franchisees brought local market knowledge and entrepreneurial energy. Brinker provided the brand, the training, the supply chain, and the operational playbook. It was a partnership that worked beautifully when the brand was hot and became strained when same-store sales declined, but in the 1980s and early 1990s, it was pure rocket fuel. Each new unit generated strong returns, attracting more franchisees, which funded more growth.

By 1991, the company had grown so far beyond its original Chili's identity that a rebranding was warranted. Chili's Inc. became Brinker International, a name that honored the man who had built it and signaled ambitions that extended well beyond a single concept.

The timing was perfect. TGI Friday's, Applebee's, Olive Garden, and Red Lobster were all expanding simultaneously, and casual dining was becoming the defining American dining experience of the 1990s. Think about what these restaurants represented to the American middle class. They were the place where suburban families celebrated report cards and Little League victories. They were where couples went on date nights when a babysitter was too expensive for fine dining. They were where traveling salespeople ate dinner in every mid-sized city from Portland to Pensacola. Casual dining wasn't just a category. It was a cultural institution, and Brinker International was positioned not just as a participant in this revolution, but as its standard-bearer.

III. The Rollup Era: Building an Empire (1991-2000)

The renaming of the company wasn't merely cosmetic. It reflected a strategic pivot from single-brand operator to multi-concept restaurant conglomerate. Norman Brinker's thesis was elegant in its logic: different dining occasions call for different brands. A family celebrating a birthday wants something different from a couple on date night, and both want something different from a group of colleagues grabbing a quick lunch. If you could own brands that covered multiple occasions, you could capture a larger share of the consumer's dining dollar while leveraging shared infrastructure behind the scenes.

The acquisition spree began before the rebrand. In November 1989, Brinker acquired the franchise rights to Romano's Macaroni Grill, a concept created by the flamboyant Dallas restaurateur Philip J. Romano. Romano had founded the restaurant in April 1988 in Leon Springs, a district of San Antonio, based on the idea of communal Italian family-style dining. The atmosphere was boisterous and theatrical: bottles of wine left on tables for customers to pour themselves on the honor system, opera-singing waiters, open kitchens where you could watch the cooks work. Brinker paid $41 million from a stock sale for the rights and immediately began scaling the concept. By the end of 1990, Brinker was operating three Macaroni Grill locations alongside 240 Chili's outlets. The Italian concept would eventually grow to more than 200 restaurants.

In February 1994, Brinker acquired On the Border Mexican Grill & Cantina, a twenty-one-unit chain that targeted the booming Tex-Mex market. The Tex-Mex category was growing rapidly as Americans discovered that Mexican-inspired food could be more than a taco stand, and On the Border gave Brinker a foothold in a cuisine category that Chili's Southwestern menu only partially addressed.

A year later, in August 1995, Brinker struck a deal with Chicago's legendary Lettuce Entertain You Enterprises to acquire two concepts simultaneously. Maggiano's Little Italy was a family-style Italian restaurant designed for celebrations and large parties, the kind of place where a table of twelve could share platters of chicken parmesan and baked ziti while someone's grandmother held court at the head of the table. Corner Bakery Cafe was a fast-casual bakery concept that would prove ahead of its time. The Lettuce deal also included Big Bowl Asian Kitchen, a pan-Asian concept that rounded out the portfolio with flavors from Thailand, China, and Vietnam.

Throughout the mid-1990s, Brinker developed additional concepts internally, including Cozymel's Coastal Mexican Grill, which opened its first location in May 1994. At its peak, the Brinker empire encompassed half a dozen distinct brands, each targeting a different customer occasion and price point. The logic was compelling on paper: diversify consumer occasions, own multiple real estate categories, and leverage shared infrastructure in purchasing, technology, human resources, and supply chain.

Norman Brinker's leadership philosophy was as distinctive as his strategy. He was a hands-on operator who believed in empowerment over micromanagement, hospitality over transactionalism, and innovation over complacency. Executives who worked under him describe a man who could walk into any restaurant, spot the three things that needed fixing, and deliver the feedback in a way that left the general manager feeling energized rather than criticized. He attracted talent with an almost magnetic force. Many of the most successful restaurant CEOs of the next generation, including the leaders who would build Outback Steakhouse, Cracker Barrel, and dozens of other chains, started their careers working for Norman Brinker.

The late 1990s represented the zenith of both Brinker International and the casual dining category. Families, couples, and business groups flocked to these restaurants. The economics worked beautifully at scale: commodity purchasing power kept food costs down, national advertising created brand awareness, and real estate clustering strategies ensured that Brinker's restaurants were always the most convenient option in their trade area.

But the multi-concept strategy, while intellectually appealing, contained the seeds of its own complexity. Managing half a dozen brands, each with different menus, supply chains, kitchen equipment, and marketing strategies, stretched the organization's attention and resources. For every Maggiano's that thrived in its niche, there was a Cozymel's that struggled to differentiate itself. There's an analogy to conglomerates in other industries: General Electric under Jack Welch could make jet engines, light bulbs, and television shows, but that breadth eventually became a liability when each division needed world-class management and capital simultaneously. Restaurant conglomerates face the same challenge, except that the pace of consumer preference shifts in dining is even faster than in industrial markets.

The question was whether Brinker could sustain this breadth of ambition, or whether the empire would eventually need to contract. The late 1990s looked like vindication. But as any student of business history knows, peak performance often precedes peak complacency.

IV. Peak Casual Dining & Cracks in the Model (2000-2008)

The early 2000s felt like a golden age for Brinker International. The company operated multiple brands across a nationwide footprint with strong margins and a playbook that seemed endlessly repeatable: find a good real estate location, build a restaurant, hire a capable general manager, and watch the cash flow in. The formula had been refined over two decades, and the execution was disciplined. Real estate teams clustered locations to maximize advertising efficiency and brand visibility. Local marketing created community ties. Franchisee relationships provided capital-light growth in secondary and tertiary markets.

But underneath the surface, pressure was building. In 2004, Norman Brinker stepped down from active management, passing the torch to Doug Brooks, a Brinker veteran who had risen through the operational ranks. Norman retained the title of Chairman Emeritus, but his daily presence, the intuitive feel for the customer that had guided the company for two decades, was no longer at the helm. The transition was smooth operationally, but it marked the beginning of an era where Brinker International would be managed rather than led.

The challenges emerged gradually, then all at once. Overexpansion was the first problem. With six concepts competing for management attention, capital allocation became a zero-sum game. Every dollar invested in a Macaroni Grill remodel was a dollar not spent on a Chili's kitchen upgrade. Cannibalization crept in as different Brinker brands competed for the same customers in the same trade areas. A family driving to dinner had a choice between Chili's, On the Border, and Macaroni Grill, all owned by the same parent company, all competing for the same discretionary dining dollar. Meanwhile, the competitive landscape was intensifying. Applebee's, which had grown to become the largest casual dining chain in America with more than two thousand locations, was fighting aggressively for market share. Outback Steakhouse was expanding rapidly. Darden's Olive Garden was perfecting its never-ending pasta bowls and breadstick strategy. The casual dining sector was beginning to feel overcrowded, with too many seats chasing too few diners.

Same-store sales pressure, the metric that matters most in restaurant economics, began to emerge. When you're adding new units, total revenue can grow even if existing locations are flat or declining. But same-store sales growth is the canary in the coal mine. It tells you whether the core business is gaining or losing relevance with customers. And by the mid-2000s, Brinker's core business was showing signs of fatigue.

The company responded with financial engineering. Share buybacks returned capital to shareholders and propped up earnings per share, but they also increased the debt load on the balance sheet. It was a classic case of prioritizing financial metrics over operational fundamentals, a pattern that would become all too common in the casual dining industry.

More ominously, consumer preferences were beginning to shift in ways that casual dining was slow to recognize. Health consciousness was rising, and the perception of casual dining as calorie-bomb territory was hardening. Ethnic cuisines, from Thai to Indian to Vietnamese, were becoming mainstream, making the standard American grill menu feel stale. And in the background, a new category was emerging that would threaten casual dining's entire value proposition.

In 1993, a former classically trained chef named Steve Ells had opened a small burrito shop in Denver called Chipotle. By the mid-2000s, Chipotle had proven that customers would pay near-casual-dining prices for food that was prepared in front of them, served in minutes rather than half an hour, and made with ingredients that sounded better on a label. Panera Bread, Five Guys, and others followed. Fast-casual dining offered quality without wait times, freshness without formality, and value without the overhead of a full-service restaurant. It was the most significant disruption to the restaurant industry since Norman Brinker invented casual dining itself.

Norman Brinker died on June 9, 2009, at the age of seventy-eight, while vacationing in Colorado Springs. He passed from pneumonia complications after inhaling a piece of food the week prior. The timing was cruelly symbolic. The man who had created casual dining left the world just as the category he built was entering its darkest period. He retained the title of Chairman Emeritus until his death, and the company that bears his name mourned the loss of not just a founder but a mentor who had shaped thousands of careers across the restaurant industry. The industry he created was about to face an existential reckoning that would have tested even Norman Brinker's legendary resilience.

V. The Great Casual Dining Decline (2008-2016)

The 2008 financial crisis didn't create the structural problems facing casual dining, but it exposed them with brutal clarity. When American families suddenly had to choose between a sixty-dollar dinner out and a thirty-dollar trip to the grocery store, casual dining lost. Traffic collapsed. Same-store sales turned sharply negative. And the industry entered a period of decline that would last the better part of a decade.

The headwinds were structural, not cyclical. Fast-casual disruption was the most obvious threat. Chipotle, Panera, and Five Guys offered food that tasted better than casual dining's assembly-line output, delivered in half the time, at comparable or lower prices. These concepts also carried a patina of authenticity that chain casual dining lacked. The ingredients lists were shorter. The kitchens were visible. The experience felt honest in a way that a laminated menu at a suburban Applebee's simply didn't.

Millennial preferences amplified the damage. This generation, which should have been casual dining's core growth demographic as they entered their earning years, largely rejected the category. They valued authenticity over chain predictability, Instagram-worthy presentation over quantity, and unique experiences over familiar formula. The rise of food trucks, pop-up restaurants, and farm-to-table concepts made casual dining feel like the musical equivalent of easy listening: competent, inoffensive, and utterly forgettable. A millennial food blogger would sooner post about a hole-in-the-wall taqueria than a plate of Chili's fajitas, and in the age of social media, that visibility gap translated directly into foot traffic.

Smartphone culture changed the dining occasion itself. A family of four sitting at a Chili's table with every member staring at a phone screen didn't need to go to a restaurant for that experience. They could do it at home with DoorDash. The social component of dining out, the conversation and connection that justified the premium over eating at home, was eroding as screen time consumed attention. The very technology that would later save Chili's was, in the early 2010s, contributing to its decline.

Delivery technology was changing consumer behavior in ways the industry struggled to understand. GrubHub, founded in 2004, and Seamless, which merged with GrubHub in 2013, were teaching Americans that they could eat restaurant food without leaving their couch. The idea of ordering delivery from a sit-down restaurant, something that would have seemed absurd in Norman Brinker's era, was becoming normalized. This was devastating for casual dining, whose entire value proposition was the dine-in experience. The ambiance, the waiter, the social occasion, none of these traveled in a brown paper bag.

Fast-casual and fast-food concepts adapted to delivery more easily because their food traveled better and their margins could absorb the thirty percent commission that delivery platforms charged. A burrito bowl from Chipotle arrives looking and tasting nearly identical to what you'd eat in the restaurant. A Chili's Baby Back Ribs platter that took thirty-five minutes to prepare, cost fifteen dollars, and lost thirty percent of its quality in a Styrofoam container during a twenty-minute delivery ride was an economic impossibility. The casual dining industry was caught in a bind: if it embraced delivery, it destroyed its margins and degraded its food quality. If it ignored delivery, it ceded an entire consumption occasion to competitors. Neither option was attractive.

Brinker's response during this period was reactive rather than strategic. Menu innovation became an exercise in throwing spaghetti at the wall. Discounting wars escalated as chains competed for a shrinking pool of customers with ever-more-aggressive promotions. Two-for-twenty-dollar deals, endless appetizer specials, and loyalty discounts drove traffic but destroyed margins. The company became trapped in what industry observers called the "value trap": discounting so aggressively that customers came to expect promotional pricing, making it impossible to raise prices without losing volume.

The asset rationalization began in earnest. Brinker sold Corner Bakery Cafe to CBC Restaurant Corp. in 2005 for $70 million, when it was a ninety-two-unit concept. Cozymel's was sold during fiscal 2004 after Brinker took a $15.1 million asset impairment charge. Big Bowl was sold back to its original creator, Lettuce Entertain You Enterprises, in 2004-2005. Romano's Macaroni Grill was sold to Golden Gate Capital in December 2008 for $131.5 million. On the Border followed in June 2010, also to a Golden Gate Capital affiliate.

The divestitures were painful but necessary. Each sale represented the unwinding of Norman Brinker's multi-concept vision, an acknowledgment that the company lacked the bandwidth to operate multiple brands while its flagship was struggling. The Macaroni Grill story was particularly telling: Brinker sold it to Golden Gate Capital in 2008, then watched the new owner struggle before eventually seeing the brand change hands again in 2013 when Mac Acquisitions took over. The lesson was that some restaurant concepts, no matter how charming, simply don't scale the way investors hope. A concept that works beautifully at twenty locations can be mediocre at two hundred.

By the time the fire sale was complete, Brinker International had been simplified to two brands: Chili's and Maggiano's. The multi-concept conglomerate that Norman Brinker had envisioned was now, for better or worse, a single-concept company with a niche companion brand. Paradoxically, this simplification would prove to be a strength. With management's full attention focused on one flagship brand, the quality of strategic thinking and operational execution could improve dramatically. The same lesson that would later be applied to Chili's menu, less is more, first applied to Brinker's portfolio.

Leadership churn compounded the problems. Multiple CEOs cycled through, each bringing a different strategy that was abandoned before it could be fully executed. The "death of casual dining" narrative hardened in business media, with article after article documenting traffic declines, store closures, and the relentless march of fast-casual alternatives. Activist investors circled, pressuring management to optimize short-term returns at the expense of long-term brand building.

The numbers told a stark story. Casual dining chains made less money than any other restaurant category in ten out of twelve months during 2016. The segment experienced eight consecutive quarters of negative sales growth before finally turning positive in the fourth quarter of 2017. Traffic declines became structural rather than cyclical, meaning that customers weren't just waiting for the economy to improve before returning. They were leaving and not coming back.

The math was unforgiving. In the restaurant industry, there's a concept called "share of stomach." Unlike technology, where market expansion creates new demand, the total number of meals Americans eat is essentially fixed. Every customer that Chipotle gained was a customer that someone else lost. And casual dining was losing across the board, not to a single competitor but to an entire ecosystem of alternatives. The grocery store, the food truck, the Uber Eats scroll, the TikTok recipe, the meal kit on the doorstep, all of these were competing for the same discretionary food dollar that used to flow automatically to the local Chili's or Applebee's.

For investors watching this unfold, the critical question wasn't whether casual dining would survive. It was whether any individual chain could break free from the category's gravitational pull. The answer, as it turned out, would take another six years and a global pandemic to reveal.

VI. The Existential Crisis & False Starts (2016-2020)

By 2016, Chili's had hit bottom. Same-store sales had been declining for years. The menu had bloated to over one hundred items, creating kitchen complexity that made consistency impossible and speed laughably slow. Every item on the menu competed for grill space, prep time, and storage, turning what should have been a streamlined operation into a chaotic scramble. A guest could order Nashville-spiced chicken tenders, a Southwestern egg roll, a classic burger, fish tacos, or shrimp linguine, all from the same kitchen. The cooks couldn't be experts at anything because they had to be adequate at everything.

The competition was closing in from every direction. Fast-casual chains were stealing the quality-conscious customer. Delivery apps were stealing the convenience customer. Ghost kitchens and virtual brands were eroding the notion that a physical restaurant was even necessary. And within casual dining itself, stronger competitors like Texas Roadhouse and Olive Garden were outperforming by staying focused on their core identity while Chili's drifted. Texas Roadhouse, in particular, had built a cult following by doing things that seemed impossibly old-fashioned: hand-cutting steaks in each restaurant, baking rolls from scratch, and creating a raucous atmosphere with line dancing employees. While Chili's tried to be everything, Texas Roadhouse knew exactly what it was.

The "value" trap had become a vicious cycle, and understanding it is critical because it's the single biggest pitfall in the restaurant industry. Years of discounting had trained Chili's customers to expect deals. When every visit was prompted by a coupon or a two-for-one special, the customer relationship was built on price rather than product. This eroded average ticket prices, which compressed margins, which left less money for food quality improvements, which gave customers fewer reasons to visit without a discount. The brand was trapped in a race to the bottom with no clear exit. It's the restaurant equivalent of a drug addiction: the short-term hit of promotional traffic feels good, but the long-term damage to brand equity and margin structure is devastating.

Leadership attempted various interventions with mixed results. Menu simplification efforts started but were executed inconsistently. Kitchen equipment upgrades were planned but rolled out slowly. Digital and mobile ordering investments began, laying groundwork that would prove critical later, but the execution was halting and the messaging was unclear. The company knew it needed to change but couldn't decide what to change into.

In 2018, Wyman Roberts was promoted to CEO. A Brinker veteran who had risen through the operations side of the business, Roberts had been serving as President of Chili's since 2013 and understood the brand's problems from the inside. He inherited a company that needed surgery, not aspirin. His early moves were bold by Brinker standards. He ordered a radical menu reduction, cutting roughly forty percent of items. This was heresy in an industry that equated menu breadth with customer choice. The conventional wisdom held that if you remove a customer's favorite dish, they'll never come back. Roberts bet that the opposite was true: that a smaller, better-executed menu would bring more customers back more often. He launched the "3 for $10" value platform, an attempt to own the affordability positioning with a clear, memorable price point that customers could remember without consulting a menu. Kitchen reengineering commenced with the replacement of conveyor belt ovens with faster, more versatile Turbochef ovens, which could cook items more evenly and at higher speeds, reducing the average ticket time and improving food quality simultaneously.

Roberts also invested in early digital infrastructure, including mobile ordering capabilities and a loyalty program called My Chili's Rewards, which used Ziosk tablets at tables and a mobile app to create a fully digital enrollment and redemption experience. These investments seemed incremental at the time but would prove prescient.

Initial progress was real but modest. Same-store sales stabilized. Operational metrics improved. The bleeding was slowing. And then, in March 2020, the world shut down. The pandemic would test every assumption casual dining had ever made about its business model.

VII. COVID Crucible & Digital Acceleration (2020-2021)

When Ohio Governor Mike DeWine ordered all bars and restaurants to close dining rooms on March 15, 2020, the first major state action of the pandemic, it felt like a temporary disruption. Within a week, it was clear the industry was facing something far worse. Twenty-five states ordered restaurants to cease dine-in service. By March 22, thirty-eight states had mandated closures. Industry experts estimated that nearly half of the restaurant industry's fifteen million workers were laid off within days. The food services industry would lose $130 billion in sales between March and October 2020. Casual dining revenues declined by as much as eighty-five percent. Fine dining was even worse, with sales dropping more than ninety percent. The last three weeks of March 2020 alone saw a 46.3 percent decline for casual dining brands.

For Brinker International, the crisis demanded a choice: adapt or die. The company chose to adapt with a speed and creativity that surprised even its own management team. The most audacious move was the launch of "It's Just Wings," a virtual brand that existed only on delivery platforms. The concept had been quietly tested at several California locations since November 2019, but the pandemic accelerated the rollout from experiment to national launch in a matter of weeks.

In late June 2020, It's Just Wings went live across all Chili's and Maggiano's locations simultaneously, more than a thousand restaurants in a single day, through an exclusive DoorDash partnership. The menu was deliberately simple: eight-count bone-in or eleven-count boneless wings with curly fries and ranch, starting at eight dollars. The genius was in the economics. The brand used existing kitchens, existing cooks, existing supply chains, and existing real estate. The incremental investment was essentially zero. The incremental revenue was pure margin enhancement.

The results exceeded all expectations. It's Just Wings generated three million dollars in weekly sales almost immediately and surpassed its target of $150 million in annualized sales within its first year, ultimately reaching approximately $170 million when franchise partner sales were included. Perhaps most impressively, seventy percent of first-month orders came from DoorDash customers who had never ordered from Chili's, demonstrating that the virtual brand was genuinely incremental rather than cannibalistic.

Meanwhile, Brinker's earlier digital investments paid dividends under the most extreme possible stress test. Mobile ordering, online infrastructure, and the loyalty program, all of which had seemed like nice-to-haves before the pandemic, became essential survival tools. Digital sales exploded from roughly ten percent of total sales to more than thirty percent. The loyalty program gained millions of members as customers shifted to digital channels.

The operational learnings were equally valuable and would shape Brinker's strategy for years to come. Leaner menus worked better than bloated ones. Speed mattered more than variety. Technology could reduce labor requirements without degrading the customer experience. Perhaps most importantly, the pandemic revealed that Chili's core menu items, the burgers, the ribs, the chicken crispers, were genuinely craveable. When customers could order from any restaurant in their city through a delivery app, a meaningful number chose Chili's. That was a data point that contradicted the "death of casual dining" narrative and suggested that the problem hadn't been the food itself but the overall experience and value equation surrounding it.

But the pandemic also reinforced the bears' thesis about casual dining's structural challenges. Customer return to dining rooms was slow and uneven. Labor shortages made staffing a nightmare, with seven in ten full-service restaurants reporting insufficient employees. Food costs surged as supply chains fractured. And the industry narrative hardened further: casual dining might never fully recover to pre-pandemic norms.

Brinker also experimented with a "Maggiano's Italian Classics" virtual brand, mirroring the It's Just Wings model with Italian fare. However, the company later pulled the plug on that concept, having learned that not every virtual brand works. The wings concept succeeded because it was simple, craveable, and perfectly suited to delivery. Italian pastas and entrées lost too much quality in transit. The lesson was important: virtual brands work when the food travels well, the operations are simple, and the brand identity is distinct from the parent concept.

Brinker emerged from the COVID crucible relatively healthy compared to peers. Bennigan's and Steak & Ale had already filed for bankruptcy in 2008. Ruby Tuesday filed for Chapter 11 in 2020. The weakest players were being culled. But "relatively healthy" and "thriving" were very different things, and Brinker's stock reflected the uncertainty. What the company needed was not incremental improvement but a fundamental reimagining of what Chili's could be. That reimagining would arrive in the form of a consumer packaged goods executive with a radical idea about TikTok.

VIII. The Kevin Hochman Turnaround & TikTok Renaissance (2022-2024)

The Crisis Deepens

In the spring of 2022, the mood inside Brinker International's Dallas headquarters was grim. The stock had cratered from its post-pandemic highs. The recovery that management had promised investors was stalling out. Inflation was spiking across every cost category that mattered: beef, chicken, cooking oil, wages, and utilities. The labor market was the tightest in decades, with restaurants competing against Amazon warehouses, gig economy platforms, and retail chains for the same pool of hourly workers. DoorDash and Uber Eats were taking thirty percent of every delivery order, making off-premise sales a margin trap.

Wyman Roberts, who had steadied the ship through the pandemic's worst days with operational grit and the It's Just Wings innovation, recognized that the next phase of Brinker's evolution needed a different kind of leader. He announced his retirement, and the board began searching for a new CEO. What they found was someone with almost no casual dining experience but a track record of transforming legacy brands that had been given up for dead.

Enter Kevin Hochman

Kevin Hochman's resume read like it belonged to a different industry. He held a Bachelor of Science in Economics from The Wharton School and a Bachelor of Arts from the Annenberg School for Communication at the University of Pennsylvania. He spent eighteen years at Procter & Gamble in finance, brand management, and marketing roles, including a stint as North America Cosmetics Business Leader. At P&G, he played a key role in the legendary Old Spice rebranding of 2010, the viral campaign with Wieden + Kennedy that repositioned a sleepy deodorant brand as a cultural phenomenon for younger consumers. That experience, transforming a legacy brand by meeting a new generation where they lived, would prove eerily relevant.

From P&G, Hochman moved to Yum! Brands in 2014, where he served as U.S. KFC President for more than five years while simultaneously leading Pizza Hut as President from 2020 to 2022. His connection to the restaurant world came through Brian Niccol, a fellow P&G alumnus, who introduced him to David Novak at Yum. At KFC, Hochman oversaw a digital transformation that modernized the brand without losing its heritage. He understood how to take a legacy brand, strip away what wasn't working, amplify what was, and use modern marketing channels to reach consumers who had never considered the brand relevant to their lives.

When Hochman took the CEO role at Brinker in June 2022, EAT stock was trading in the mid-twenties. His diagnosis was devastating in its simplicity: Chili's had lost its identity. It wasn't the value leader. It wasn't the quality leader. It wasn't the speed leader. It wasn't the social media leader. It was trying to be everything and succeeding at nothing. The brand occupied a no-man's-land between fast-casual quality and full-service pricing, satisfying neither the value-conscious customer nor the experience-seeking one.

Hochman's first move was to listen. He spent his initial weeks visiting Chili's restaurants across the country, eating in the dining rooms, talking to servers and line cooks, watching how customers interacted with the brand. What he found confirmed his hypothesis: the food was decent but uninspiring, the marketing was invisible to anyone under thirty-five, the operations were inconsistent, and the brand had no clear answer to the question "why should I eat at Chili's instead of anywhere else?" The answer, he decided, would be: because Chili's gives you more for less, and it's actually fun to be here.

The Transformation Playbook

Hochman's turnaround rested on four interconnected pillars, each informed by his CPG background of understanding consumer behavior, brand positioning, and the power of cultural relevance.

Pillar One: Menu & Food Quality Revolution. Hochman doubled down on Chili's core items, the dishes that customers actually craved: burgers, chicken crispers, fajitas, and ribs. He continued Roberts' menu simplification, cutting thirteen more items and twelve SKUs, reducing kitchen complexity further. But the critical move was investing in food quality. Ingredient upgrades included better beef and fresher produce. Portion sizes were benchmarked not against other casual dining chains but against fast-casual competitors, ensuring that a Chili's meal offered visibly more food for less money.

The signature launch was the Big Smasher, a half-pound hand-smashed burger introduced in April 2024 as Chili's first burger innovation in three years. It was offered as part of the "3 for Me" value platform at $10.99, including the burger, a bottomless drink, and bottomless chips and salsa with fries. The marketing message was deliberately provocative: this burger was cheaper than a fast-food meal from McDonald's or Wendy's, and it was objectively larger and arguably better. The comparison was audacious and effective.

Pillar Two: Social Media & Cultural Relevance. This is where Hochman's Old Spice experience proved transformative. He recognized that traditional advertising, television commercials and print campaigns that cost millions and reached an aging demographic, was a depreciating asset. Social media virality, by contrast, was a compounding one. Every share, every duet, every reaction video created more awareness at zero marginal cost.

Chili's tripled its marketing budget over three years, from $32 million in 2022 to $137 million in 2025, an incremental $105 million in three years. But the spending shifted dramatically from traditional channels to social media, particularly TikTok. The strategy wasn't to create polished corporate content. It was to create conditions for organic virality and then amplify what caught fire.

The breakout moment came with the Triple Dipper, Chili's customizable appetizer platter of three dippable items with sauces. In April 2024, a video of the thick, stretchy cheese pull from Chili's fried mozzarella sticks went viral, eventually accumulating over 200 million views on TikTok. The visual was perfect for the platform: satisfying, shareable, and viscerally appealing. The Triple Dipper went from a menu item to a cultural moment. By fiscal year 2025, Chili's had sold 41 million Triple Dippers, and the item accounted for fifteen percent of total sales.

Employee TikToks were encouraged, trading corporate polish for authenticity. Memes were embraced. The brand leaned into participatory culture, the kind of unscripted, slightly chaotic engagement that Gen Z trusts precisely because it doesn't feel manufactured. As Hochman told reporters: "What's happening is young people come in after seeing us on TikTok, and realize the experience is really good, making us part of their rotation."

The marketing team, led by George Felix, who was promoted to EVP and Chief Marketing Officer effective March 2, 2026, proved adept at nurturing viral moments without smothering them. When the Nashville Hot Mozz emerged as a fan-created hack, a Chili's team member had suggested tossing fried mozzarella sticks in Nashville Hot sauce, the company turned it into an official secret menu item rather than shutting down the organic buzz. Customers had to ask for it by name, creating a sense of insider knowledge that drove further social media sharing.

Approximately sixty percent of the traffic increase was attributed to paid advertising, while about forty percent came from organic TikTok buzz. This ratio represented extraordinary marketing efficiency. No television campaign in casual dining history had generated anything close to that level of organic amplification.

Pillar Three: Operational Excellence. Hochman understood that viral marketing was worthless if the restaurant experience disappointed. A Gen Z customer who showed up because of TikTok and encountered slow service, cold food, or a dirty restaurant would post a very different kind of video. Kitchen speed metrics were tightened. The Turbochef oven upgrades that Roberts had initiated were accelerated. Labor scheduling was optimized. Digital integration, from seamless mobile ordering to contactless payment to loyalty program enrollment, was streamlined to reduce friction at every touchpoint.

The results showed up in the data. Even as traffic surged, Chili's "guests with a problem" score fell to 2.9 percent from 3.5 percent year-over-year. Delivering better customer satisfaction at higher volumes is the operational equivalent of squaring the circle, and Chili's managed it. Hochman instituted what he called "back-to-basics" operational discipline, where restaurant managers were evaluated not just on financial performance but on customer satisfaction scores, food quality audits, and speed of service metrics. The philosophy was borrowed from his KFC days: you can market a restaurant into a single visit, but only operational excellence creates a repeat customer.

Pillar Four: Real Estate & Remodeling. Rather than pursuing reflexive expansion, Hochman focused on making existing locations more productive. Selective remodels with modern aesthetics refreshed the brand's physical presence without the capital intensity of new unit development. Underperforming locations were closed. Technology investments, from tablets to QR codes to streamlined kitchen displays, modernized in-restaurant operations. The goal was to increase average unit volumes rather than unit counts, a capital-efficient strategy that pleased both operators and shareholders. Each dollar spent on improving an existing restaurant generated higher returns than building a new one from scratch, because the customer base and real estate were already in place.

The Results

The transformation showed up in the numbers with breathtaking speed. By the fiscal second quarter of 2025, ending December 2024, Chili's same-store sales had surged 31.4 percent, with three consecutive quarters of double-digit growth. Traffic growth, the metric that casual dining hadn't seen in years, was explosive. Chili's became the leader in casual dining traffic share according to Circana Crest data. Average unit volumes climbed from $3.6 million to $4.2 million, a $600,000 improvement per restaurant.

Restaurant operating margins expanded to 19.1 percent in that quarter, up six full percentage points from 13.1 percent a year earlier. The math is simple but staggering: more customers coming through the door, spending on higher-margin items, served by a more efficient operation. Every element of the flywheel was spinning in the right direction simultaneously.

The stock price told the ultimate story. From the mid-twenties when Hochman arrived in June 2022, EAT shares climbed relentlessly, reaching an all-time high of $192.22 on February 4, 2025. An investor who bought the stock on Hochman's first day as CEO and held through the peak would have seen a return of more than six hundred percent in less than three years. The market capitalization grew from approximately $1.3 billion to over $7 billion at its peak. It was the kind of performance that turns a turnaround story into a legend.

Hochman was named Restaurant Business's 2025 Restaurant Leader of the Year. The industry narrative flipped completely: instead of asking whether casual dining could survive, analysts were asking whether Chili's had invented a new playbook. Business publications that had written casual dining's obituary now penned breathless accounts of the resurrection. Harvard Business School and Wharton would inevitably case-study the transformation. The question shifted from "can Chili's survive?" to "how long can this last?"

Most recently, in the second quarter of fiscal 2026, ending late December 2025, Brinker reported revenue of $1.44 billion, up 6.9 percent year-over-year, with adjusted diluted EPS of $2.87, beating the consensus estimate of $2.57. Chili's same-store sales were up 8.6 percent, marking the nineteenth consecutive quarter of same-store sales growth and outperforming the casual dining industry by 680 basis points. The two-year comparable sales stack stood at an extraordinary forty-three percent. Management raised fiscal 2026 revenue guidance to $5.76 billion to $5.83 billion and EPS guidance to $10.45 to $10.85.

The deceleration from 31 percent same-store sales growth to 8.6 percent inevitably raised questions about sustainability. Was the turnaround peaking? Hochman's response was characteristically direct: the company was now comping against its own record-setting quarters, making year-over-year comparisons artificially difficult. An 8.6 percent comp on top of a 31 percent comp represents genuinely extraordinary two-year growth. The more important signal was that traffic remained positive, meaning customers were still coming through the door in greater numbers, not just spending more per visit. Multiple analyst firms responded by raising price targets, with JPMorgan moving to $187 and Piper Sandler to $166.

IX. The Business Model Deep Dive

Strip away the narrative of turnarounds and TikTok, and Brinker International is fundamentally an operating business that makes money by serving meals to customers in physical restaurants. Understanding the mechanics of how that business works, the unit economics, the cost structure, the capital allocation, is essential for any investor trying to assess whether the current momentum translates into durable shareholder value.

Unit Economics & Franchising

Understanding Brinker's economics requires understanding the unusual structure of its portfolio. Unlike many restaurant companies that are primarily franchisors, collecting royalties while franchisees bear the operational risk, Brinker is predominantly a company-owned operator. Of approximately 1,628 total restaurants at the end of fiscal 2025, 1,162 were company-owned and 466 were franchised, with the franchise operations concentrated in international markets across twenty-eight countries and two U.S. territories.

This ownership-heavy model means Brinker captures the full economics of each restaurant, both the upside and the downside. When same-store sales are growing at double-digit rates, as they have been under Hochman, the operating leverage is enormous. Fixed costs like rent, insurance, and base labor are spread across a larger revenue base, and every incremental dollar of sales drops to the bottom line at a much higher rate than the average dollar. But the reverse is also true: in a downturn, those fixed costs become anchors.

Restaurant-level margins in casual dining typically follow the "rule of thirds": roughly one-third of revenue goes to food costs, one-third to labor, and the remainder must cover occupancy, utilities, marketing, and corporate overhead, leaving net margins of three to five percent. To put this in perspective, a technology company might enjoy net margins of twenty to thirty percent. A pharmaceutical company might see forty percent. Casual dining operates in a world where a three-cent increase in the price of lettuce or a fifty-cent increase in the minimum wage can erase an entire quarter's profit improvement. The margin of error is razor-thin, which is why operational consistency matters so much. A single badly managed restaurant can lose money for months before the corporate office notices.

Brinker's recent performance has stretched above these norms, with restaurant operating margins hitting 19.1 percent in the fiscal second quarter of 2025 under the dual tailwinds of higher traffic and better operational efficiency. This represents the power of operating leverage in a high-fixed-cost business: once you've paid for the building, the equipment, the manager, and the base kitchen staff, incremental customers flow through at significantly higher margins. It's the same principle that makes software businesses so profitable at scale, except in restaurants, the incremental cost of each additional customer isn't zero. It's the food on their plate and the fraction of labor needed to prepare and serve it. Still, the leverage is substantial, and it explains why traffic growth is far more valuable than price increases for a casual dining operator.

The company's real estate strategy has evolved from aggressive expansion to selective optimization. Average annual net sales per company-owned Chili's reached $4.5 million in fiscal 2025, with an average revenue per meal of $21.90. These unit volumes are strong by casual dining standards and approaching levels that make new-unit economics attractive for selective growth.

In recent years, Brinker has moved to acquire franchised restaurants back into company ownership, purchasing 103 franchised Chili's restaurants in 2015 for $106.5 million, 116 Midwestern locations in 2019, and 23 more in 2021. This consolidation strategy increases company control over the brand experience and captures the full margin rather than just a royalty fee.

The Digital Flywheel

Brinker's digital infrastructure has evolved from a crisis response tool during COVID to a genuine competitive advantage. The My Chili's Rewards loyalty program creates a first-party data asset that enables personalized marketing, reducing dependence on expensive third-party advertising. Mobile ordering reduces labor requirements at the point of sale while often generating higher ticket averages, since digital orders tend to include more add-ons than verbal orders at a hostess stand.

The delivery channel remains a strategic tension that every restaurant executive wrestles with. Third-party platforms like DoorDash charge commissions ranging from fifteen to thirty percent depending on the service tier. For a business with three to five percent net margins, paying thirty percent commission on delivery orders is mathematically devastating unless those orders are genuinely incremental. Consider the math: a $20 meal delivered through DoorDash at a thirty percent commission rate nets the restaurant $14 in revenue against roughly $7 in food costs and $4 in labor, leaving $3 before any overhead. Compare that to the same $20 meal eaten in the restaurant, where the full $20 is revenue and the margin is dramatically better. Delivery is a necessary evil for most casual dining chains, not a profit center.

Brinker has navigated this tension more shrewdly than most. The It's Just Wings virtual brand generates delivery revenue from customers who might never visit a Chili's, while the core Chili's brand pushes dine-in and pickup orders through its own digital channels where commissions don't apply. The strategy is essentially: use third-party platforms for incremental customer acquisition through virtual brands, but drive your core customers to first-party channels where you control the economics and the data.

Maggiano's: The Stable Companion

Maggiano's Little Italy operates in a fundamentally different market than Chili's. Its fifty-two locations, including three franchised units, target a higher-end customer for celebrations, corporate events, and large family gatherings. Average annual net sales per Maggiano's are $9.9 million, more than double a Chili's, with average revenue per guest of $39.06. The banquet and catering business generates high-margin event revenue that provides stability and predictability.

The brand has seen modest same-store sales growth, including 1.8 percent in the fiscal second quarter of 2025, compared to Chili's 31.4 percent. In August 2025, following the departure of Maggiano's President Dominique Bertolone, Hochman assumed interim leadership and began applying elements of the Chili's turnaround playbook, including a "Back to Maggiano's" focus on food, service, and atmosphere. The appointment of Michelin-starred Chef Anthony Amoroso as Vice President of Innovation and Growth signaled an intent to elevate the culinary experience. Maggiano's represents an interesting optionality for Brinker: if the Chili's playbook of food quality improvements, digital integration, and cultural marketing can be adapted for an older, higher-spending demographic, the brand could become a meaningful second growth engine rather than just a stable companion.

Supply Chain & Purchasing

Brinker's scale, purchasing for more than 1,600 restaurants, provides meaningful leverage with commodity suppliers. The company's simplified menu, the result of years of item reductions, concentrates purchasing volume on fewer ingredients, which strengthens negotiating power and reduces waste. Menu engineering has become a science, balancing food cost percentages against customer appeal and kitchen efficiency. The "3 for Me" platform, for example, is engineered so that the $10.99 price point delivers value perception to the customer while maintaining acceptable margins for the company. It represents roughly nine percent of tickets but less than five percent of sales, functioning more as a traffic driver than a profit center.

The company's fiscal discipline has improved dramatically. Long-term debt and finance leases were reduced from $786.3 million to $426.0 million during fiscal 2025, and the board authorized an additional $400 million in share repurchase capacity. The combination of revenue growth, margin expansion, and debt reduction has created meaningful financial flexibility for the first time in years. For a company that once faced questions about its viability as a going concern, the transformation in the balance sheet is nearly as impressive as the transformation in same-store sales.

Myth vs. Reality: Fact-Checking the Consensus Narratives

Myth: Chili's turnaround is entirely driven by TikTok virality. Reality: While social media has been transformative for brand awareness, the operational improvements are arguably more important. Menu simplification, kitchen speed improvements, food quality upgrades, and the value-focused "3 for Me" platform were all in motion before the first viral TikTok moment. Social media amplified a better product, but it didn't create it. A viral video of mediocre food in a slow restaurant would have been a disaster, not a turnaround.

Myth: Casual dining is a dying category. Reality: The category is consolidating, not dying. Total industry revenue has stabilized, and the strongest players, Chili's, Texas Roadhouse, and Olive Garden, are growing. What died was the weakest quartile of operators: the TGI Fridays, the Ruby Tuesdays, the Hooters. The survivors are capturing the freed-up market share and building stronger competitive positions. Consolidation often looks like death when viewed from the outside, but for the survivors, it's an enormous opportunity.

Myth: Gen Z doesn't eat at sit-down restaurants. Reality: Gen Z is eating at Chili's in record numbers. They want value, they want social experiences, and they want to participate in cultural moments. The Triple Dipper phenomenon proves that Gen Z isn't anti-restaurant. They're anti-boring. Give them something shareable, affordable, and genuine, and they'll show up in droves.

X. Competitive Analysis: Porter's Five Forces & Hamilton's Seven Powers

The story of Brinker International is compelling on its own terms, but great investors don't just evaluate companies in isolation. They evaluate them within the context of the industry structure and competitive dynamics that determine how much value a company can capture. Two frameworks are particularly useful here.

Porter's Five Forces

Understanding the structural forces that shape Brinker's competitive environment requires moving beyond the company-specific narrative to examine the industry architecture itself. Porter's framework reveals why the restaurant industry is inherently difficult and why only the most disciplined operators thrive.

Competitive Rivalry: Very High. The restaurant industry is among the most competitive in the American economy, with over one million restaurant locations in the United States alone. Brinker doesn't just compete with other casual dining chains like Applebee's, Olive Garden, and Texas Roadhouse. It competes with fast-casual (Chipotle, Cava, Sweetgreen), quick-service (McDonald's, Wendy's), fine dining, food trucks, grocery prepared meals, meal kits, and the consumer's own kitchen. The total addressable market, what the industry calls "share of stomach," is essentially fixed. Every meal eaten at Chili's is a meal not eaten somewhere else. There's no Moore's Law in restaurants, no exponential growth in the number of times Americans eat per day. Price wars, promotional dependency, and marketing arms races are endemic. The result is persistent margin compression for all but the strongest operators.

The recent wave of competitor distress has thinned the herd but intensified competition among survivors. TGI Fridays filed for Chapter 11 in November 2024 with only about eighty-five locations remaining from a peak of several hundred. Red Lobster emerged from Chapter 11 in September 2024 at a $375 million valuation, a fraction of its former worth. Hooters' parent company filed for bankruptcy in March 2025. Denny's announced plans to close 150 restaurants. Nearly 350 full-service chain restaurants closed amid bankruptcy in 2024 alone. These closures free up real estate and customers, but the surviving competitors, Darden, Texas Roadhouse, and Brinker, are all strong operators who will fight hard for the spoils.

Threat of New Entrants: Moderate to High. Ghost kitchens and virtual brands lowered the barriers to entering the restaurant business during and after COVID. A new concept can launch on DoorDash with minimal capital. Social media enables grassroots brand building without television advertising budgets. However, scaling from a single location or virtual brand to a national chain with 1,600 restaurants requires capital, operational expertise, real estate relationships, and supply chain infrastructure that take decades to build. The threat is real at the local and regional level but limited at national scale.

Bargaining Power of Suppliers: Moderate. Most food inputs are commoditized with multiple suppliers. However, volatility is a constant challenge. Beef prices were fifteen percent higher in January 2026 than a year earlier, and the USDA predicts beef will increase an average of 9.4 percent in 2026 due to tight cattle supplies. Brinker's scale provides some negotiating leverage, but no restaurant chain is immune to commodity swings. Labor, arguably the most critical "supplier," commands very high bargaining power in the current environment. Twenty-two states are implementing minimum wage increases in 2026, and labor now accounts for nearly thirty-five percent of total operating costs, up from thirty percent two years ago.

Bargaining Power of Buyers: High. Consumers have infinite choice and essentially zero switching costs. Opening a delivery app presents dozens of options within a five-mile radius. Price transparency through social media and review platforms means that any gap between price and value is quickly punished. Loyalty programs create some stickiness, but no one is locked into dining at Chili's the way they might be locked into an iPhone ecosystem. The customer holds significant power, and brands must earn every visit.

Threat of Substitutes: Very High. This is arguably the most dangerous force in the restaurant industry. Grocery stores sell meal kits and prepared foods that replicate restaurant quality. Delivery platforms make every restaurant in a metro area accessible from a couch. Home cooking experienced a renaissance during COVID that hasn't fully reversed. Convenience stores like Wawa and Sheetz now offer hot food that rivals fast-food quality. Even entertainment spending competes for the same discretionary dollar. Every year, the question "should we eat out tonight?" has more alternatives on the "no" side.

Hamilton's Seven Powers

If Porter's framework explains why an industry is hard, Hamilton Helmer's Seven Powers framework explains what makes individual companies within that industry durably successful. The Seven Powers are the sources of persistent differential returns, the reasons why some companies earn outsized profits while competitors in the same industry earn normal or below-normal returns. Applying this lens to Brinker reveals both the strengths and vulnerabilities of its current position.

Scale Economies: Moderate. Brinker enjoys purchasing power with suppliers, marketing efficiency from national campaigns, and technology development costs spread across 1,600 units. But regional competitors can achieve local scale, and fast-casual chains like Chipotle have comparable or superior unit economics. Scale is a real advantage but not an unassailable one.

Network Effects: Weak to Moderate. The My Chili's Rewards loyalty program creates mild data network effects: more customers generate better data, which enables better personalization, which drives higher frequency. Social media virality also exhibits network dynamics, where each viral moment brings new customers who create more shareable content. But Chili's is not a marketplace or a platform. The network effects are emerging but not structural.

Counter-Positioning: Strong (Currently). This is Brinker's most interesting strategic asset. Hochman's TikTok-native marketing strategy puts competitors in a genuine bind. Applebee's and Olive Garden, with their older brand positioning and customer demographics, cannot authentically pivot to Gen Z culture without alienating their core base. Fast-casual brands positioned on "better ingredients" and premium pricing cannot match Chili's aggressive value positioning without undermining their own brand promise. The combination of full-service dining, fast-casual speed, and value pricing at a culturally relevant brand is genuinely unique in the market right now. The critical caveat: counter-positioning is inherently temporary. Competitors will adapt. Darden, with its deep resources and operational expertise, has already signaled its intent to learn from Chili's playbook.

Switching Costs: Weak. There are minimal customer switching costs in restaurants. Loyalty points create minor friction, and habit and convenience matter, but customers are not locked in. This is a structural feature of the industry, not a Brinker-specific weakness.

Branding: Moderate. Chili's has fifty years of brand equity, and the recent revival has strengthened brand perception among Gen Z consumers significantly. But casual dining brands carry less power than fast-food brands like McDonald's, which benefit from childhood associations and global ubiquity, or luxury brands that command price premiums. Maggiano's has strong brand recognition within its niche. Chili's brand power is real but not commanding.

Cornered Resource: Weak. There are no proprietary ingredients, and recipes can be replicated. Real estate locations matter but are not exclusive. Kevin Hochman himself could be considered a cornered resource, his specific combination of CPG marketing instincts, restaurant operating experience, and cultural sensibility is rare, but key-man dependence is a risk factor, not a durable competitive advantage.

Process Power: Moderate to Strong. This may be Brinker's most underrated strength. Decades of operational refinement have produced kitchen systems, training programs, and franchisee playbooks that are difficult to replicate quickly. The recent integration of digital tools, AI-assisted labor scheduling, and streamlined kitchen operations represents process innovation that compounds over time. Managing 1,600 restaurants with consistent quality while driving 31 percent same-store sales growth is an extraordinary operational achievement. Process power is Brinker's emerging moat.

The overall assessment: Brinker's current advantage rests on counter-positioning plus process power. The combination of Gen Z cultural relevance with operational scale at value pricing creates a temporary but real moat. The critical question is whether Hochman can convert these tactical advantages into durable structural power, either through brand entrenchment or scale advantages, over the next three to five years. In Hamilton Helmer's framework, the most enduring businesses eventually develop either scale economies that make competition uneconomical or brand power that commands premium pricing. Brinker has neither in its final form yet, but the ingredients are assembling. The next chapter of the story will determine whether a turnaround becomes a dynasty.

XI. The Competitive Landscape & Strategic Positioning

If the Porter and Hamilton frameworks provide the theoretical architecture, the competitive landscape provides the ground truth. The casual dining industry has bifurcated into winners and losers, with very little middle ground. The gap between the top performers and the bottom has never been wider, and the consequences of being on the wrong side of that divide have never been more severe. Understanding where Brinker sits in this landscape requires mapping the key competitors and their relative trajectories.

Darden Restaurants is the industry's eight-hundred-pound gorilla. With fiscal 2025 revenue of $12.1 billion across brands including Olive Garden, LongHorn Steakhouse, and the recently acquired Chuy's (103 restaurants, completed October 2024), Darden has the deepest resources and the most diversified portfolio. Olive Garden generated $5.2 billion in fiscal 2025 sales with moderate same-store growth of around two to six percent depending on the quarter. LongHorn Steakhouse has been a quiet juggernaut, posting 7.5 percent same-store sales growth with strong traffic. Darden's advantage is consistency and operational discipline. Its vulnerability is an older customer demographic and a brand portfolio that hasn't achieved the cultural relevance that Chili's has found with younger consumers.

Texas Roadhouse may be the most consistently excellent operator in casual dining. The chain posted $5.4 billion in 2024 revenue, surpassing Olive Garden as the largest casual dining chain by U.S. systemwide sales. Same-store sales have been positive for sixty consecutive quarters excluding the pandemic, a streak dating to 2010. Traffic growth of 4.9 percent in 2024 demonstrates genuine customer acquisition, not just price increases. The company broke the 800-store mark in 2025 and plans to open 35 more in 2026. Texas Roadhouse's advantage is a cult-like customer following built on visible food quality, the hand-cut steaks and from-scratch rolls are prepared in full view of guests, combined with a fun, high-energy atmosphere. Its limitation is a narrower menu positioning that makes it less adaptable to changing food trends.

Bloomin' Brands (Outback Steakhouse) is the turnaround candidate that hasn't turned around yet. After CEO Michael Spanos replaced David Deno in September 2024, the company announced a $75 million turnaround plan focused on improving steaks, redesigning menus, upgrading service, and increasing marketing. By late 2025, Outback posted its first positive traffic quarter since 2021, a modest 0.9 percent gain. But fiscal 2026 guidance of 0.5 to 2.5 percent same-store sales growth highlights how far behind Bloomin' Brands remains relative to Chili's, Texas Roadhouse, and Darden.

Dine Brands (Applebee's/IHOP) has stabilized after years of decline. Applebee's posted 1.3 percent same-store sales growth for full-year 2025, a significant improvement from the negative 4.2 percent decline in 2024. The chain's "two for $25" deal helped end the multi-year sales slide, and the dual-branded Applebee's/IHOP locations, which achieve 1.5 to 2.5 times the revenue of single-brand units, represent an innovative approach to real estate efficiency. But Applebee's remains well behind Chili's in cultural relevance and traffic momentum.

Brinker's Strategic Position. Chili's has leapt over Applebee's into the number-three position in casual dining, behind Texas Roadhouse and Olive Garden, powered by fifteen percent sales growth. The three winners in casual dining, Chili's, Texas Roadhouse, and Olive Garden, share a common thread: they kept prices lower than rivals, invested heavily in labor and restaurant improvements, and maintained clear brand identities. The losers, Cracker Barrel, Bloomin' Brands, Denny's, and the bankrupt chains, shared the opposite traits: confused positioning, underinvestment, and a failure to adapt to changing consumer preferences.

The pattern is instructive: in a brutally competitive industry, the winners aren't necessarily the most innovative or the most aggressive. They're the most disciplined. Texas Roadhouse doesn't try to be trendy. Olive Garden doesn't chase Gen Z. But both execute their respective strategies with extraordinary consistency. Chili's, uniquely, has managed to add cultural relevance on top of operational discipline, which is why its growth has outpaced even these formidable competitors. The question is whether it can sustain both simultaneously.

Against fast-casual competitors, Brinker has executed an unusual counter-positioning. Chipotle and similar chains positioned themselves as premium alternatives to fast food and casual dining, charging more for better ingredients and a faster experience. A typical Chipotle burrito bowl now costs thirteen to fifteen dollars, and a meal with drink and chips can easily exceed twenty dollars. Chili's has flipped the script by offering full-service dining at fast-casual prices, essentially arguing that you can have it all: a sit-down meal with waiter service, larger portions, and a social atmosphere, all for less than a Chipotle bowl.

This positioning created what might be the most potent value proposition in the restaurant industry right now. The Big Smasher burger, served with bottomless chips, salsa, and a drink for $10.99, offers more food and more experience than anything available in fast-casual at a comparable price. The marketing team made this comparison explicit, running ads and social media content that directly compared Chili's prices and portion sizes against McDonald's, Wendy's, and Chipotle. It was a strategy that would have been unthinkable five years earlier, when Chili's was too embarrassed about its own quality to draw direct comparisons. Under Hochman, the brand had the confidence, and the product quality, to go on offense.

Whether this positioning is sustainable as food and labor costs rise is a key question for investors. The $10.99 price point has to absorb increasing costs of beef, labor, and rent. At some point, the math may force a price increase that tests whether the value perception, and the customer relationship, can survive it.

XII. Bull vs. Bear Case

The investment thesis for Brinker International hinges on a fundamental question: is the Hochman turnaround a sustainable transformation or a spectacular but temporary sugar high? The answer depends on which side of several key debates an investor falls. Let's steelman both cases.

The Bull Case

Sustained Cultural Relevance. The bear assumption that Gen Z engagement is inherently fickle may be wrong. Chili's isn't just riding a single viral moment. It has created an ongoing relationship with a generation of consumers through consistent social media engagement, authentic brand voice, and a value proposition that resonates in an era of food price inflation. The Triple Dipper, the Big Smasher, and the Nashville Hot Mozz are not one-time gimmicks. They are menu items that customers order repeatedly, and each one generates fresh social media content as new customers discover them. The $105 million marketing reinvestment, growing from $32 million to $137 million over three years, isn't a one-time stunt. It's a structural commitment to meeting customers where they are. If Chili's can maintain its cultural relevance, the demographic tailwind could last a decade as Gen Z enters its peak earning and dining-out years.