Electronic Arts: The Empire of Digital Entertainment

I. Introduction & Gaming Industry Context

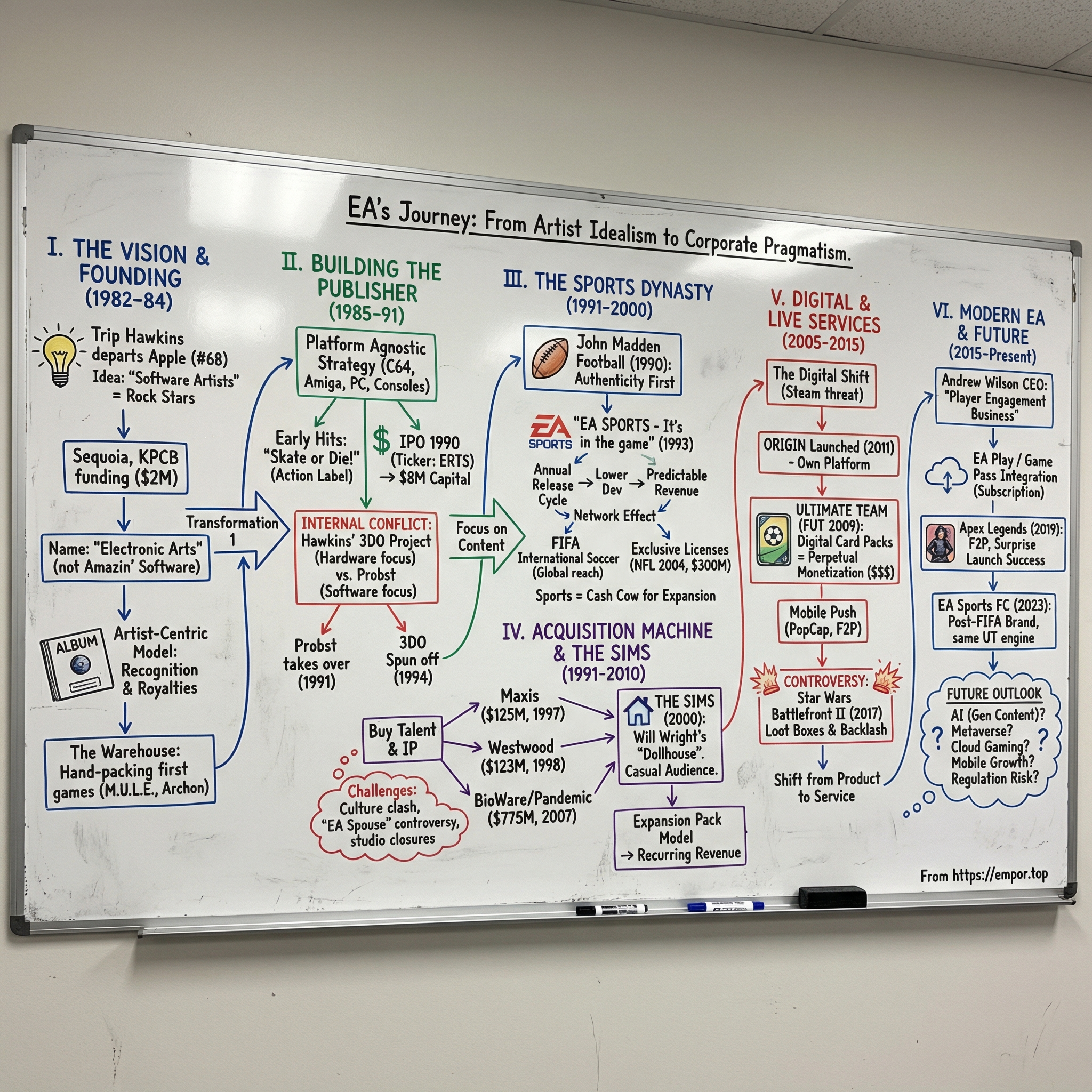

The year is 1982. Silicon Valley is still finding its rhythm, Apple has just gone public two years earlier, and the video game industry—still reeling from Atari's dominance—is about to experience its first major crash. Into this chaos steps Trip Hawkins, Apple employee #68, with a radical idea: what if game developers were treated like rock stars?

This wasn't just another software company launch. When Hawkins walked away from his Apple stock options to start Electronic Arts, he carried with him a vision that would fundamentally reshape how we think about interactive entertainment. The company that began by putting developers' names on game boxes—treating them as "software artists" rather than anonymous coders—would eventually become the very embodiment of corporate gaming that many of those same artists would rail against.

Today, Electronic Arts stands as a $40 billion colossus, commanding an empire that stretches from the virtual soccer pitches of EA Sports FC to the suburban landscapes of The Sims, from the battlefields of Apex Legends to the gridirons of Madden NFL. In fiscal year 2024, EA posted GAAP net revenue of approximately $7.6 billion—a figure that would have seemed fantastical to the dozen employees who gathered in a South San Francisco warehouse forty years ago to hand-pack their first game shipments.

But here's the fascinating paradox at the heart of the EA story: How did a company founded on the principle of creative empowerment—one that literally pioneered the concept of celebrity game designers—transform into what critics often characterize as the ultimate corporate machine, famous for acquiring studios and franchises, annualizing beloved series, and pioneering controversial monetization strategies?

The answer lies not in a single pivot or decision, but in a series of calculated transformations, each responding to seismic shifts in technology, consumer behavior, and business models. From the early days of floppy disks sold in record album-style packaging to today's live service games generating billions through microtransactions, EA's journey mirrors the evolution of the entire gaming industry—except EA didn't just adapt to these changes; it often drove them. The modern EA, with a market cap of approximately $43 billion as of August 2025, bears little resemblance to that scrappy startup that challenged industry conventions. Yet understanding how we got here—from artist-centric idealism to corporate pragmatism, from physical media to digital dominance, from single-player experiences to live service empires—reveals not just the story of one company, but the blueprint for how the entire $200 billion gaming industry operates today.

What makes EA's trajectory particularly instructive for investors and industry observers is its uncanny ability to identify and exploit each major platform shift and business model innovation before competitors fully grasped their implications. Whether it was recognizing the power of sports licenses in the early 1990s, understanding the acquisition arbitrage opportunity in independent studios, or pivoting aggressively toward digital distribution and live services ahead of the curve, EA has consistently demonstrated a strategic prescience that has kept it at the industry's apex even as countless competitors have fallen by the wayside.

This is the story of how Electronic Arts built its empire—through vision and acquisition, innovation and imitation, artistry and analytics. It's a tale of transformation that asks fundamental questions about creativity versus commerce, independence versus scale, and ultimately, what it means to succeed in an industry where technology, art, and business collide with unprecedented force.

II. The Trip Hawkins Vision & Founding Story (1982-1984)

Picture the scene: It's late 1981, and Trip Hawkins is sitting in his Cupertino office at Apple Computer, employee badge #68 pinned to his shirt, staring at spreadsheets that show the company's valuation soaring toward the stratosphere. He's been there since 1978, helped launch the Apple II, and his stock options are worth a small fortune. By any measure, the 28-year-old Harvard MBA has already won Silicon Valley's lottery.

But Hawkins can't shake an idea that's been percolating since his days at Stanford, where he'd created one of the world's first college courses on strategy games. While the rest of Apple focused on productivity software and hardware innovation, Hawkins saw something else entirely: a future where interactive entertainment would rival Hollywood, where game creators would be celebrated like film directors, and where software would become the primary form of cultural expression for an entire generation.

The catalyst for his departure came during a strategy meeting where Apple's leadership dismissed gaming as a trivial market. "They saw games as something to demonstrate the computer's capabilities, not as a business unto itself," Hawkins would later recall. That fundamental misunderstanding of gaming's potential—shared by virtually every major tech company at the time—created the opening Hawkins needed.

In May 1982, Hawkins made his move. Walking away from Apple options that would have made him wealthy beyond imagination (Apple's stock would increase 50-fold over the next decade), he set out to raise capital for his new venture. His pitch to investors was audacious: he wanted to create the world's first "software artist" company, where game developers would be promoted like rock stars, complete with album-style packaging and their photos on game boxes.

The venture capital community was intrigued but skeptical. Video games meant Atari, and Atari was beginning to show cracks. But Hawkins had done his homework. Armed with detailed market analysis and a vision for platform-agnostic publishing (a revolutionary concept when most game companies were tied to specific hardware), he managed to secure approximately $2 million from Sequoia Capital, Kleiner Perkins Caufield & Byers, and other prominent Silicon Valley firms.

The company's first identity crisis came immediately. Hawkins had fallen in love with the name "Amazin' Software"—a playful nod to the wonder he hoped games would inspire. His early employees, however, universally despised it. Don Valentine from Sequoia reportedly told Hawkins it was "the worst company name he'd ever heard." After weeks of heated debate and brainstorming sessions that consumed entire weekends, the team landed on "Electronic Arts" in November 1982. The name was perfect: it positioned games as an art form while acknowledging their technological foundation.

But a name was just the beginning. Hawkins' true innovation lay in completely reimagining the relationship between publisher, developer, and consumer. At Atari and other game companies, programmers were anonymous wage workers, forbidden from taking credit for their creations. Hawkins flipped this model entirely. EA's first advertisements, designed to look like album covers, featured game developers in dramatic black-and-white portraits above the tagline "Can a Computer Make You Cry?"

This wasn't just marketing fluff. Hawkins structured EA's contracts to give developers unprecedented creative control and profit participation. While Atari kept its programmers hidden (leading to the famous revolt that created Activision), EA made them the main attraction. Early EA developers like Bill Budge, who created Pinball Construction Set, and Dan Bunten, who designed M.U.L.E., became industry celebrities—exactly as Hawkins had envisioned.

The company's approach to production was equally revolutionary. Rather than maintaining a large internal development team, EA pioneered the "affiliated label" model—essentially becoming the gaming industry's first true publisher. Independent developers would create games, and EA would handle manufacturing, distribution, and marketing. This asset-light model allowed EA to scale rapidly without the overhead that was crushing competitors.

On May 20, 1983, came the moment of truth. EA's first batch of games was ready to ship. The entire company—at that point just a few dozen people—gathered in a warehouse in South San Francisco. There were no automated systems, no fulfillment centers. Every employee, from Hawkins to the newest hire, spent the day packing boxes, affixing labels, and loading UPS trucks by hand. The scene was both humbling and exhilarating: here was a company that had raised millions and talked about transforming entertainment, literally hand-packing boxes like a garage startup.

The initial lineup showcased EA's diverse ambitions: Hard Hat Mack (a platform game), Archon (a chess-like strategy game), Pinball Construction Set (a creativity tool), M.U.L.E. (a multiplayer economic simulation), Worms? (an artillery game), and Axis Assassin (an action game). None were massive hits, but collectively they established EA as a publisher willing to take creative risks.

More importantly, the artist-centric model was working. The gaming press ate up the story of developers as artists. Retailers appreciated the sophisticated packaging that made games feel like premium products rather than toys. And while sales were modest, EA was building something more valuable than immediate revenue: a reputation as the thinking person's game company.

By 1984, EA had published nearly 20 titles and was generating meaningful revenue. But Hawkins was already looking ahead to the next challenge. The home computer market was fragmenting—Commodore 64, Apple II, IBM PC, and others all required different versions. The console market, dominated by Nintendo in Japan, was beginning to recover from the 1983 crash. And Hawkins had a secret project that he believed would revolutionize everything: a new gaming hardware platform that would make current computers look like toys.

The artistic idealism of early EA would soon collide with harsh business realities. The company that started by asking "Can a Computer Make You Cry?" would eventually need to answer a different question: "Can artistic integrity survive the demands of a public market?" But in those early days, with the team hand-packing games in a warehouse, anything seemed possible.

III. Building the Publishing Powerhouse (1985-1991)

By 1985, Electronic Arts had survived its scrappy startup phase, but Trip Hawkins knew that survival wasn't enough. The gaming industry was consolidating rapidly—Atari had collapsed, taking dozens of smaller publishers with it, while Nintendo was quietly building a console empire that would soon dominate the global market. EA needed to evolve from boutique publisher to industry powerhouse, and fast.

The transformation began with a strategic insight that seems obvious in retrospect but was revolutionary at the time: while competitors fought over hardware platforms, EA would become platform-agnostic, porting games to every viable system. This meant maintaining separate development teams for Commodore 64, Apple II, IBM PC, Amiga, and eventually Nintendo and Sega consoles. The overhead was substantial, but the market reach was unprecedented.

The affiliated label model that had served EA well was evolving too. Rather than just publishing external developers' games, EA began acquiring strategic stakes in successful studios, creating a hybrid model that balanced creative independence with corporate control. This approach would become the template for EA's future acquisition strategy—buy the talent, integrate the technology, preserve the brand.

One early success story that validated this model was Skate or Die!, released in 1987. Developed by Stephen Landrum and published under EA's new "action" label, the game captured the skateboarding craze sweeping America. It sold over 250,000 copies—massive numbers for the time—and proved that EA could compete in the lucrative action game market previously dominated by Japanese publishers.

But the real breakthrough came from an unexpected source: celebrity endorsements in sports games. While competitors saw sports games as niche products for statistics obsessives, EA recognized their mainstream potential. The key was authenticity, and authenticity meant licenses—real teams, real players, real stadiums. This insight would fundamentally reshape not just EA, but the entire sports gaming sector.

The path to going public began in 1989, as Hawkins and the board recognized that competing globally required capital scales that venture funding couldn't provide. The IPO process was grueling—Wall Street didn't understand video games, constantly comparing EA to toy companies rather than media enterprises. Hawkins spent months educating investment bankers about the software entertainment business, essentially creating the framework that investors still use to evaluate gaming companies today.

On March 26, 1990, Electronic Arts filed for its initial public offering on the NASDAQ exchange. The company went public under the ticker symbol "ERTS" at a split-adjusted price of $0.52 per share. The IPO raised approximately $8 million—modest by today's standards but transformational for EA. For the first time, the company had the war chest to compete with anyone.

Yet even as EA celebrated its public market debut, internal tensions were mounting. Hawkins had become increasingly obsessed with a new venture—the 3DO Interactive Multiplayer, a gaming console he believed would unite the fragmented market. He was spending more time on 3DO than on EA, effectively running a startup within a public company. The board was not amused.

The 3DO project embodied both Hawkins' visionary genius and his fundamental weakness as a corporate leader. The technology was revolutionary—a 32-bit CD-ROM-based system that far exceeded anything on the market. But at $700, it was priced like a high-end computer rather than a gaming console. Hawkins insisted that consumers would pay premium prices for premium experiences. The market disagreed.

Meanwhile, Larry Probst, EA's President and COO since 1991, was quietly building support for a different vision. Where Hawkins saw EA as a technology innovator that happened to publish games, Probst saw it as a content company that should stay out of the hardware business. Where Hawkins romanticized developers as artists, Probst understood that sustainable success required process, discipline, and scale.

The boardroom showdown came in 1991. After months of increasingly acrimonious debates about strategic direction, Hawkins agreed to step down as CEO while remaining chairman. Probst took the helm, inheriting a company at a crossroads. EA had gone public, had strong franchises emerging, but was still losing money on the 3DO venture and faced intensifying competition from larger players.

Probst's first major decision set the tone for his entire tenure: EA would exit the hardware business entirely and double down on software. The 3DO project was spun off as a separate company (with Hawkins departing to run it full-time in 1994), freeing EA to focus on what it did best—publishing games across every available platform.

The strategic clarity was immediately apparent in EA's financial performance. Without the 3DO albatross, margins improved dramatically. The company's platform-agnostic approach meant it could capitalize on the explosive growth of both Sega Genesis and Super Nintendo. And most importantly, Probst had identified the division that would define EA's next chapter: EA Sports.

Looking back, the period from 1985 to 1991 represented EA's adolescence—that turbulent phase where founding ideals clash with market realities. The company that emerged under Probst's leadership was more corporate, less romantic about the "software artist" concept, but also more focused and financially disciplined. The question was whether this new EA could maintain the creative spark that Hawkins had ignited while building the operational excellence that public markets demanded.

The answer would come from an unlikely source: a former NFL coach turned broadcaster named John Madden, who was about to teach EA that sometimes the best art is the kind that sells millions of copies every single year.

IV. The Sports Dynasty: EA Sports Brand Creation (1991-2000)

The meeting that would reshape sports gaming forever almost didn't happen. It was 1988, and EA producer Rich Hilleman was sitting in a train dining car with John Madden, the legendary NFL coach turned broadcaster. Madden, terrified of flying after a near-miss experience years earlier, traveled exclusively by train—his famous Madden Cruiser bus would come later. Hilleman had been pursuing Madden for months to lend his name to EA's football game, but Madden kept refusing. He didn't just want his name on a box; he wanted the game to be real football—11 players on each side, authentic plays, genuine strategy.

"If it's not real football, I'm not putting my name on it," Madden insisted, sketching plays on a napkin as the train rolled through the Midwest. The technical challenge was immense. Most football games of the era featured six or seven players per side due to hardware limitations. But Hilleman made a promise that would cost EA millions in development: they would wait for technology to catch up to Madden's vision.

That decision—to prioritize authenticity over expedience—would become the cornerstone of EA Sports' philosophy. When John Madden Football finally launched in 1990 for the Sega Genesis, it wasn't just a game; it was a simulation. Real plays from Madden's own playbook. Commentary that taught football strategy. Graphics that showed all 22 players on the field. The game sold 400,000 copies in its first year—phenomenal for a sports title.

But Larry Probst saw something bigger than a single successful game. In 1991, he made a decision that would transform EA's trajectory: create a dedicated sports division with its own brand identity. The original name was "Electronic Arts Sports Network," deliberately echoing ESPN to convey legitimacy and broadcast quality. A trademark dispute forced a change, but the shortened "EA Sports" proved even more powerful—simple, memorable, and endlessly marketable.

The masterstroke was the tagline, delivered in a voice that would become one of gaming's most recognizable audio signatures: "EA Sports—It's in the game." That phrase, introduced in 1993, perfectly captured the division's promise: not just sports games, but authentic sports experiences. Every real stadium, every actual player, every genuine team—it was all in the game.

The business model innovation was equally revolutionary. Rather than treating sports games as one-off products, EA Sports pioneered the annual release cycle. New version every year, timed to coincide with each sport's season, incorporating updated rosters, new features, and incremental improvements. Critics derided it as glorified roster updates, but consumers didn't care. Buying the new Madden became as much a fall tradition as watching NFL games themselves.

The genius of the model lay in its economics. Development costs for annual iterations were far lower than creating new games from scratch—maybe 30-40% of the original development cost for 80-90% of the revenue. The predictable revenue stream allowed EA to plan investments years in advance. And the annual cycle created a powerful network effect: as more people bought each year's version, the multiplayer community remained vibrant, encouraging holdouts to upgrade.

By 1993, EA Sports had expanded beyond Madden to include NHL Hockey, PGA Tour Golf, and FIFA International Soccer. Each followed the same playbook: secure authentic licenses, partner with a credible spokesperson, prioritize simulation over arcade action, and release annually. The formula was so successful that competitors began copying it wholesale, but EA had first-mover advantage and the capital to outbid rivals for exclusive licenses.

The FIFA franchise deserves special attention. When EA launched FIFA International Soccer in 1993, soccer games were popular in Europe but niche in America. EA's insight was that soccer was becoming increasingly global, and a truly international sports franchise could dwarf even Madden's success. They were right. By 2000, FIFA was generating more revenue than any other EA Sports title, with particularly strong sales in Europe, Latin America, and Asia.

The exclusive licensing strategy reached its apex in 2004 when EA signed a five-year exclusive deal with the NFL and NFLPA for a reported $300 million. The move was controversial—competitors like 2K Sports were locked out of making NFL games entirely—but strategically brilliant. With exclusive NFL rights, Madden became not just the best football game but the only football game with real teams and players. Sales exploded, crossing 5 million copies annually. The financial validation of the sports strategy was undeniable. In 2011, Forbes ranked EA Sports eighth on their list of most valuable sports brands, with a value of $625 million—remarkable for a video game division competing against actual sports leagues and equipment manufacturers. By the late 1990s, EA Sports titles were consistently among the best-selling games every year, generating predictable, high-margin revenue that funded EA's expansion into other genres.

The cultural impact went beyond sales figures. EA Sports didn't just make sports games; it shaped how fans experienced sports. The detailed player ratings in Madden became so influential that NFL players would complain publicly about their virtual attributes. FIFA introduced millions of Americans to international soccer. Tiger Woods PGA Tour made golf cool for a generation that had never picked up a club.

Perhaps most importantly, EA Sports proved that gaming could be a mass market phenomenon, not just a niche hobby. When Monday Night Football ran commercials for Madden, when NBA stars appeared at EA Sports launch events, when FIFA tournaments filled stadiums—it validated gaming as mainstream entertainment. The division that began with a train conversation between a producer and a coach had become one of the most powerful brands in all of sports, virtual or otherwise.

But success bred scrutiny. Critics argued that exclusive licenses stifled innovation, that annual releases were cynical cash grabs, that EA was prioritizing profits over gameplay. These tensions would only intensify as EA embarked on its next phase: acquiring the industry's most creative studios and attempting to integrate them into an increasingly corporate machine.

V. The Acquisition Machine: Studios & IP Consolidation (1991-2010)

The conference room at EA's Redwood Shores headquarters had seen many acquisition discussions, but the one in October 2007 was different. John Riccitiello, who had returned as CEO earlier that year after a stint running a private equity firm, was orchestrating EA's largest deal ever: the simultaneous acquisition of BioWare and Pandemic Studios for $775 million. As he later revealed, BioWare would not have lasted much longer, as the studio had "essentially run out of money"—a stunning admission about one of gaming's most celebrated RPG developers.

This deal epitomized EA's acquisition philosophy during its empire-building phase: identify struggling but talented studios, acquire them with a combination of cash and promises of creative freedom, then gradually integrate them into the EA machine. It was a strategy that would make EA one of gaming's most prolific acquirers, but also one of its most controversial. The story begins much earlier, with the shift from external publishing to internal development through strategic acquisitions. In 1991, EA acquired Distinctive Software, transforming it into EA Canada—a studio that would become the crown jewel of the EA Sports empire. This wasn't just an acquisition; it was a blueprint for how EA would grow: buy talented teams, give them resources, but ultimately mold them to EA's vision.

According to data from Pitch Book via VentureBeat, the company has spent about $2.9 Billion on its 10 biggest acquisitions since 1992. This figure only tells part of the story—it doesn't capture the dozens of smaller acquisitions, the cultural transformations, or the studios that didn't survive the integration.

The June 1997 acquisition of Maxis for $125 million seemed expensive at the time for a company known primarily for SimCity. But Will Wright had a new concept brewing—a "people simulator" that many at EA initially dismissed as too weird for mainstream success. Wright's vision for The Sims faced internal skepticism; focus groups hated it, and marketing didn't know how to position it. But EA, to its credit, gave Wright the resources and time to realize his vision. When The Sims launched in 2000, it didn't just succeed—it redefined what a video game could be, eventually selling over 200 million copies across all versions and becoming EA's most valuable non-sports franchise.

EA's purchase of Las Vegas-based Westwood Studios in 1998 for $123 million brought the company Westwood pioneered real-time strategy games such as Dune 2 and Command & Conquer. Westwood represented a different acquisition philosophy—buying established franchises rather than just talent. Command & Conquer was already a phenomenon, and EA wanted to own the RTS genre. But the cultural clash was immediate. Westwood's freewheeling Vegas culture collided with EA's increasingly corporate structure. By 2003, Westwood was shuttered, its teams dispersed, and Command & Conquer became just another EA franchise—competently produced but lacking the innovative spark that made it special.

The pattern was becoming clear: EA could successfully acquire companies and franchises, but maintaining their creative culture was another matter entirely. Studios complained about excessive oversight, rigid production schedules, and pressure to annualize franchises. The term "EA Spouse" entered gaming lexicon in 2004 when an anonymous blog post detailed the crushing work conditions at EA studios, sparking industry-wide discussions about crunch culture and work-life balance.

Then came Bullfrog Productions, acquired in 1995, home to Peter Molyneux and innovative titles like Populous and Theme Park. Molyneux lasted until 1997 before departing to found Lionhead Studios, citing creative differences. Origin Systems, creators of Ultima and Wing Commander, acquired in 1992—closed by 2004. The list grew longer: studios acquired, talent departed, franchises continued under new management but often lacking their original magic.

EA's BioWare/Pandemic deal in October 2007 for US$775 million represented the apex of this acquisition strategy. BioWare brought Mass Effect and Dragon Age, while Pandemic had Mercenaries and was developing what would become a highly anticipated Star Wars game. The timing seemed perfect—both studios were at creative peaks but needed capital for increasingly expensive AAA development.

The revelation that BioWare had "essentially run out of money" explains why so many independent studios eventually sold to publishers. The economics of AAA development had become brutal: budgets reaching $50-100 million, development cycles stretching to 3-4 years, and one failure potentially bankrupting a studio. EA offered stability, resources, and global distribution—but at the cost of independence.

Pandemic's fate illustrated the risks. Despite the promises of autonomy, EA shuttered Pandemic in 2009, just two years after acquisition. BioWare fared better, continuing to produce successful titles, but even they faced challenges. The rushed development of Dragon Age 2, the controversial ending of Mass Effect 3, and the troubled launch of Anthem all suggested that even EA's most successful acquisitions struggled under corporate pressure.

By 2010, EA had assembled an impressive portfolio of studios and IP through acquisitions. The company owned some of gaming's most valuable franchises: The Sims, Command & Conquer, Battlefield, Mass Effect, Dragon Age, and dozens more. But critics argued that EA had become where good studios went to die—a corporate machine that excelled at extracting value from creative teams but struggled to nurture the innovation that made those teams special in the first place.

The financial results, however, told a different story. Many of these acquisitions, particularly Maxis and BioWare, generated billions in revenue. The key insight was that EA wasn't really buying studios—it was buying IP, technology, and talent that could be integrated into its increasingly efficient production machine. Whether that machine preserved or destroyed creative culture was, from a purely financial perspective, almost beside the point.

VI. The Sims & Casual Gaming Revolution (1997-2010)

Will Wright stood before the EA executives in 1997, trying to explain his latest obsession. After the success of SimCity, everyone expected another city builder. Instead, Wright was pitching something bizarre: a game about managing the daily lives of suburban families. No winning condition. No combat. Just virtual people living virtual lives, going to virtual bathrooms, and forming virtual relationships. The executives exchanged skeptical glances. This was their big acquisition's next project?

The genesis of The Sims actually traced back to 1991, when Wright's home burned down in the Oakland firestorm. Rebuilding his life from scratch, he became fascinated with the psychology of acquiring possessions and constructing domestic spaces. He envisioned a game that was part dollhouse, part social experiment, part consumer satire. For years, the project—codenamed "Project X" and later "Jefferson"—languished in development hell at Maxis. Even after EA's acquisition, the game faced constant threats of cancellation.

Focus groups were disastrous. Male players, who constituted the vast majority of PC gamers, showed little interest in managing virtual households. EA's marketing department had no idea how to position it. Was it a game? A toy? A simulation? The Maxis team internally called it "the toilet game" because of its emphasis on mundane activities like bathroom management. Wright later admitted that without a few key champions within EA who believed in the vision, The Sims would never have shipped.

When The Sims finally launched on February 4, 2000, initial sales were modest. Then something unexpected happened. Word of mouth exploded, particularly among demographics that traditional games ignored. Women, who made up less than 20% of typical PC game buyers, constituted nearly 60% of The Sims' audience. Casual players who had never bought a PC game were suddenly frequenting gaming stores. Within two years, The Sims had sold over 6.3 million copies, becoming the best-selling PC game of all time.

But the real revolution wasn't just the base game—it was the expansion model that followed. Rather than rushing a sequel, EA and Maxis released seven expansion packs over three years: Livin' Large, House Party, Hot Date, Vacation, Unleashed, Superstar, and Makin' Magic. Each added new content for $20-30, and remarkably, attachment rates exceeded 50%. Players who bought The Sims typically bought three or four expansions. The math was staggering: a single customer might generate $150-200 in revenue over the game's lifecycle.

This expansion strategy redefined how EA thought about game monetization. Traditional games saw revenue decline sharply after launch. The Sims maintained steady revenue for years through expansions, creating the industry's first true "games as a service" model for single-player content. The Sims 2, launched in 2004, perfected this approach with 18 expansions and "stuff packs"—smaller content additions that further extracted value from the engaged player base.

The cultural impact transcended sales figures. The Sims introduced millions to gaming who had never considered themselves "gamers." It sparked academic discussions about identity, consumer culture, and human behavior simulation. Players created elaborate stories, shared families online, and built thriving mod communities. The game's same-sex relationship options, included without fanfare, made it an unexpected touchstone for LGBTQ representation in gaming.

EA's handling of The Sims franchise demonstrated both the company's strengths and weaknesses. On one hand, they provided resources that Maxis alone could never have mustered, supported Wright's vision despite skepticism, and expertly marketed to non-traditional demographics. The franchise generated over $5 billion in revenue by 2010, validating the acquisition many times over.

On the other hand, the pressure to monetize led to decisions that frustrated fans. The Sims 3 (2009) introduced a controversial online store selling individual items for real money—a chair for $2, a car for $5. The Sims 4 (2014) launched with features stripped from previous versions, only to sell them back as expansions. Will Wright himself departed EA in 2009, citing a desire to work on smaller, more experimental projects—a diplomatic way of expressing creative differences with EA's increasingly commercial approach.

The Sims' success had broader implications for EA's strategy. It proved that the gaming market extended far beyond young males, that casual games could generate hardcore revenue, and that the right IP could sustain monetization for decades. These lessons would directly influence EA's later moves into mobile gaming, free-to-play models, and live services.

By 2010, The Sims had sold over 125 million copies across all versions, making it one of the best-selling game franchises ever. But more importantly, it had transformed EA's understanding of its audience and business model. The company that had built its reputation on sports simulations and action games now understood that the future might lie not in epic battles or athletic competitions, but in the mundane magic of everyday life—as long as players were willing to pay $20 for a new set of virtual furniture.

The transition from The Sims' expansion packs to modern live services was already beginning. The question was whether EA could apply these lessons to its entire portfolio without alienating the core gamers who had sustained the company for decades.

VII. Digital Transformation & Live Services (2005-2015)

The meeting at EA's Redwood Shores headquarters in 2008 was tense. Valve's Steam platform was eating into PC game sales, consumers were increasingly downloading games instead of buying discs, and EA was hemorrhaging revenue to digital distribution platforms that took 30% of every sale. CEO John Riccitiello had a radical proposal: EA needed its own digital platform. The room was skeptical—competing with Steam seemed impossible. But Riccitiello saw no alternative: "Either we control our own destiny, or we become sharecroppers on someone else's platform."

The digital revolution had been creeping up on EA for years. In 2005, digital game sales represented less than 5% of EA's revenue. By 2010, that figure had grown to 20%. The writing was on the wall: physical media was dying, and whoever controlled digital distribution would control gaming's future. EA's response—Origin, launched in June 2011—was both necessary and controversial.

Origin faced immediate backlash. PC gamers, comfortable with Steam's near-monopoly, resented being forced to use another platform. When EA made Battlefield 3 an Origin exclusive, pulling it from Steam, the gaming community erupted. Forums filled with complaints about another launcher, another account, another friends list to manage. But EA held firm. The 30% platform tax was simply too expensive for a company operating on 20-25% margins.

While Origin struggled to win hearts and minds on PC, a quieter revolution was happening in EA's sports division. In March 2009, EA launched FIFA 09 Ultimate Team as downloadable content—a fantasy football mode where players built teams by opening digital card packs. The mode was free, but the card packs cost real money. It seemed like a minor addition, a niche mode for hardcore fans. Nobody at EA anticipated it would fundamentally transform the company's business model.

Ultimate Team's genius lay in its psychology. Players weren't just buying advantages; they were buying hope—the possibility that the next pack might contain Messi or Ronaldo. It perfectly married the collecting compulsion of trading cards with the competitive nature of sports gaming. Revenue started modestly but grew exponentially. By 2012, Ultimate Team modes across FIFA, Madden, and NHL were generating $200 million annually. By 2015, that number exceeded $650 million.

The success caught even EA off guard. Andrew Wilson, who ran EA Sports before becoming CEO in 2013, later admitted they didn't initially understand what they'd created. Ultimate Team wasn't just a game mode; it was a platform for perpetual monetization. Players who bought FIFA every year for $60 were now spending hundreds, sometimes thousands, on card packs. The lifetime value of a customer exploded from $60 to potentially $500 or more.

This period also saw EA's aggressive push into mobile gaming. The 2012 acquisition of PopCap for up to $1.3 billion was meant to position EA as a casual gaming powerhouse. Plants vs. Zombies 2, released as free-to-play in 2013, generated over $100 million in its first year through microtransactions. But the mobile market proved more challenging than expected. Competition from companies like Supercell and King meant that even successful games struggled to maintain relevance beyond a few months.

The free-to-play model extended beyond mobile. In 2011, EA launched Star Wars: The Old Republic, a massively multiplayer game with a $200 million development budget—one of the most expensive games ever made. Initially subscription-based, it struggled to compete with World of Warcraft and went free-to-play within a year. The transition was painful but successful, with the game eventually generating over $1 billion in lifetime revenue through microtransactions.

But the aggressive monetization strategies began generating backlash. Parents complained about children spending hundreds on Ultimate Team packs. Governments started investigating whether card packs constituted gambling. Gaming media criticized EA for prioritizing monetization over gameplay. The company's reputation, already damaged by studio closures and franchise annualization, deteriorated further.

The nadir came with Star Wars Battlefront II in November 2017. EA implemented a loot box system that made iconic characters like Darth Vader effectively locked behind either 40 hours of grinding or immediate payment. The backlash was unprecedented. EA's Reddit comment defending the system became the most downvoted comment in Reddit history. Disney, protective of the Star Wars brand, reportedly called EA CEO Andrew Wilson directly to express concern. Multiple governments launched investigations into loot boxes as gambling.

Within days, EA suspended all microtransactions in Battlefront II—a shocking reversal for a core monetization strategy. The game's sales disappointed, and EA's stock dropped 8% in a month. More importantly, the controversy crystallized public sentiment against aggressive monetization. Belgium and the Netherlands banned loot boxes entirely. Other countries considered similar legislation.

Yet despite the controversies, the financial results were undeniable. By 2015, digital revenue exceeded 60% of EA's total. Ultimate Team alone was generating over $800 million annually—more than many entire game franchises. Live services had transformed EA from a product company to a service company. Games were no longer one-time purchases but ongoing relationships, platforms for continuous monetization.

The shift fundamentally changed how EA developed games. Every major release now needed a live service component, a roadmap for post-launch content, and monetization mechanics that could sustain revenue for years. Single-player experiences without ongoing revenue potential received less investment. Studios were evaluated not just on game quality but on "recurrent user spending" metrics.

Looking back, the 2005-2015 period marked EA's most dramatic transformation since going public. The company that Trip Hawkins founded to celebrate software artists had become a data-driven service provider, optimizing for engagement metrics and lifetime value. Whether this evolution was inevitable or a betrayal of gaming's artistic potential remained hotly debated. But one thing was clear: the financial model worked, even if it came at the cost of consumer goodwill.

VIII. Modern EA: Platform Wars & Service Games (2015-Present)

Andrew Wilson's first all-hands meeting as CEO in September 2013 set a new tone. The former EA Sports executive, who had witnessed Ultimate Team's transformation of sports gaming, had a simple message: "We're not in the product business anymore. We're in the player engagement business." This philosophy would define modern EA—for better and worse—as the company navigated an industry increasingly dominated by free-to-play giants like Fortnite and platform shifts that threatened traditional publishers.

Wilson inherited a company at a crossroads. The disastrous launch of SimCity in 2013, which required an always-online connection that servers couldn't support, had damaged EA's reputation further. The company had been voted "Worst Company in America" by Consumerist readers two years running—a dubious honor for a video game publisher competing against banks and oil companies. But Wilson saw opportunity in the chaos. If EA could pivot from selling games to delivering services, it could escape the boom-bust cycle of retail releases.

The strategy crystallized around three pillars: expanding live services beyond sports, embracing new platforms and business models, and building direct relationships with players. Live service games became EA's largest money-maker by a wide margin, accounting for 74% of the company's revenue in 2024. This wasn't just Ultimate Team anymore—it was a fundamental reimagining of how games generated value.

The surprise hit that validated Wilson's vision came from an unexpected source. In February 2019, EA shadow-dropped Apex Legends, a free-to-play battle royale game set in the Titanfall universe. No marketing campaign, no hype cycle—just a coordinated influencer push and a polished game that immediately challenged Fortnite's dominance. Within 72 hours, Apex Legends had 10 million players. Within a month, 50 million.

Apex represented everything EA had learned about live services. Free to enter, reducing friction to zero. Seasonal content updates every three months, maintaining engagement. Cosmetic-only monetization that avoided pay-to-win criticism. Character-based gameplay that enabled continuous additions. The game generated over $600 million in its first year, proving EA could compete with anyone in the live service arena.

But the biggest strategic shock came in 2023 with EA's decision to end its 30-year partnership with FIFA. The FIFA license reportedly cost EA $150 million annually, and FIFA was demanding a doubling of that fee for renewal. Wilson made a calculation that would have been unthinkable a decade earlier: the FIFA brand was worth less than EA's own football platform. EA Sports FC launched in 2023 without the FIFA name but with all other licenses intact—teams, players, leagues.

The gamble paid off spectacularly. EA Sports FC continued the franchise's momentum in fiscal year 2024, with the company delivering record fiscal year cash flow. Players didn't care about the FIFA branding; they cared about Ultimate Team, gameplay, and licenses. The move saved EA hundreds of millions while proving the strength of its own brands.

The subscription model represented another strategic evolution. EA Play (originally EA Access), launched in 2014, offered a Netflix-style catalog of EA games for a monthly fee. By 2020, it had been integrated into Xbox Game Pass, exposing EA's catalog to millions of subscribers. The economics were compelling: predictable revenue, extended game lifecycles, and a direct relationship with players that bypassed traditional retail.

Battlefield's struggles illustrated the challenges of this new era. Battlefield V (2018) attempted to add live service elements to the franchise's traditional multiplayer formula but launched incomplete, with promised features arriving months late. Battlefield 2042 (2021) was even more disastrous—bugs, missing features, and design decisions that alienated core fans led to player counts dropping 90% within months. The failure cost EA hundreds of millions and demonstrated that live service wasn't a magic formula; execution still mattered.

Meanwhile, EA's sports franchises continued printing money. Madden NFL and EA Sports FC generated billions annually, with Ultimate Team modes driving the majority of profits. The annual release cycle that critics derided as roster updates had evolved into something more sophisticated: each year's game was essentially a platform update for an ongoing service. Players migrated their engagement, if not their specific teams, from year to year. The financial performance validated Wilson's strategy. For FY24, net cash provided by operating activities was a fiscal year record $2.315 billion, up 49% year-over-year. EA's FY24 was highlighted by record cash flow and strong earnings growth driven by EA SPORTS FC and Madden NFL. The company's transformation from product sales to ongoing services had fundamentally changed its economics.

The company's latest strategic evolution involves embracing platform partnerships rather than fighting them. EA Play's integration with Game Pass, once unthinkable for a company that tried to compete with Steam, acknowledged that distribution battles were less important than maximizing audience reach. Similarly, EA's return to Steam in 2019 after an eight-year absence showed pragmatic flexibility.

College Football's return in 2024 after an 11-year hiatus demonstrated EA's ability to resurrect dormant franchises when conditions aligned. The game launched to massive success, proving that EA's sports dominance extended beyond its annual franchises. The combination of nostalgia, pent-up demand, and modern live service mechanics created another billion-dollar franchise overnight.

Looking at modern EA, the transformation from Trip Hawkins' artist-centric vision is complete. The company that once asked "Can a Computer Make You Cry?" now asks "How can we maximize player lifetime value?" It's a less romantic question but a more profitable one. EA in 2024 is a live service company that happens to make games, not a game company exploring services. Whether this represents maturation or corruption depends entirely on perspective—and perhaps on whether you're a player or a shareholder.

IX. Business Model & Financial Architecture

The conference room display showed three simple circles: Sports, Action, and Casual. "This is our entire business," Andrew Wilson told investors during EA's 2024 Investor Day. "Everything else is just execution." The simplicity was deceptive. Behind those three circles lay one of gaming's most sophisticated financial machines—a business model engineered to extract maximum value from every player interaction while maintaining the illusion of simple entertainment.

The transformation of EA's revenue model over the past decade represents a masterclass in financial engineering. In 2014, roughly 60% of revenue came from full game sales—the traditional model of selling a $60 disc. By 2024, live service games accounted for 74% of the company's revenue. This wasn't just a shift in product mix; it was a fundamental reimagining of what a video game company could be.

The economics of live services are compelling to the point of being transformative. A traditional game follows a predictable revenue curve: massive spike at launch, rapid decline over 3-6 months, long tail of minimal sales. Marketing costs are front-loaded, development costs are sunk, and success depends entirely on that crucial launch window. Live services invert this model. Revenue starts modestly but grows over time. Marketing becomes an ongoing investment. Development continues post-launch. The game becomes a platform, not a product.

Take FIFA Ultimate Team—now EA Sports FC Ultimate Team—as the exemplar. The mode generates over $1.6 billion annually, more than many entire game publishers. The gross margins are staggering: once the platform is built, selling digital card packs costs essentially nothing. No manufacturing, no distribution, no retail markup. Pure profit at scale. A player spending $100 on packs generates perhaps $95 in gross margin. Multiply that by millions of players, and you understand why EA's executives speak of Ultimate Team in almost reverential tones. The development cost structure reveals the challenges beneath the attractive margins. A AAA game now costs $100-200 million to develop over 3-5 years. Marketing can add another $50-100 million. But a successful live service game can generate that entire investment back in a single quarter. The math is seductive but brutal: one Apex Legends funds five failed experiments. One Ultimate Team justifies an entire sports division.

Platform holder relationships add another layer of complexity. Sony, Microsoft, and Nintendo take 30% of digital sales on their platforms—a tax that EA has fought but ultimately accepted as the cost of access. This platform tax is why EA pushed Origin so hard on PC and why cloud gaming represents both opportunity and threat. If gaming moves to the cloud, who owns the customer relationship? Who takes the 30%? These questions keep EA executives awake at night.

The geographic revenue mix tells its own story. North America generates approximately 40% of revenue, Europe 35%, and Asia-Pacific the remainder. But the growth rates diverge dramatically. Asian markets, particularly mobile-first countries, grow at 15-20% annually. Traditional console markets in the US and Europe grow at 3-5%. This geographic shift explains EA's aggressive mobile acquisitions and free-to-play experiments—the future of gaming's growth lies in markets that never owned consoles.

For FY24, net cash provided by operating activities was a fiscal year record $2.315 billion, up 49% year-over-year. This cash generation enables EA's shareholder-friendly capital allocation: During FY24, EA returned $1.505 billion to stockholders through stock repurchases and dividends. The board has authorized a new stock repurchase program of $5 billion over three years. This isn't a company betting everything on growth; it's a mature business returning cash while selectively investing.

The subscription model adds another dimension. EA Play generates hundreds of millions in high-margin recurring revenue. Players pay $5-15 monthly for access to EA's catalog—revenue that requires no incremental development cost. It's the holy grail of software economics: turning one-time purchases into ongoing relationships. The integration with Xbox Game Pass extends this reach to millions more players, though at lower margins.

But the real innovation in EA's financial architecture isn't any single model—it's the portfolio approach that combines them all. Sports games provide predictable annual revenue. Live services generate high-margin ongoing income. Subscription services create baseline recurring revenue. Single-player games, though less emphasized, still provide sporadic hits that justify their development costs. Each model hedges the others' weaknesses.

The risk management implicit in this structure is sophisticated. If live service engagement drops, subscription revenue provides cushion. If a major game fails, Ultimate Team keeps printing money. If regulations ban loot boxes, cosmetic sales and battle passes fill the gap. EA has engineered redundancy into its business model—multiple ways to monetize the same player, multiple revenue streams from the same content.

The marketing efficiency gained from this model is often overlooked. When EA launches a new game, it's marketing to an audience it already owns—millions of EA Play subscribers, Ultimate Team players, and engaged community members. Customer acquisition cost, the bane of mobile gaming, becomes almost negligible when you already have the customer's credit card on file.

Looking at the numbers holistically, EA has transformed from a hits-driven product company to a diversified service provider with multiple monetization vectors. The company that once lived or died by Christmas sales now generates steady cash flow year-round. It's a transformation that would make any CFO proud, even if it makes some gamers nostalgic for simpler times when you bought a game once and owned it forever.

X. The EA Playbook: Lessons & Strategy

In the executive conference room at EA's Redwood Shores headquarters, there's reportedly a whiteboard that hasn't been erased in years. On it, someone long ago wrote three questions: "Does it ship annually? Can we monetize it post-launch? Does it have franchise potential?" These questions, whether apocryphal or real, encapsulate the EA playbook—a strategic framework that has guided the company through four decades of technological disruption and market evolution.

The portfolio theory that underpins EA's strategy treats game development like venture capital. The assumption is brutal but realistic: most games will fail to meet expectations. In a hits-driven business where 10% of titles generate 90% of profits, diversification isn't just smart—it's existential. EA's response has been to maintain a portfolio broad enough to absorb failures but focused enough to capitalize on successes.

This philosophy manifests in the three-pillar structure: Sports provides stability, Action offers growth potential, and Casual captures emerging demographics. Within each pillar, multiple franchises ensure that no single failure can cripple the division. It's why EA maintains franchises like Need for Speed despite inconsistent performance—portfolio insurance against concentration risk.

The power dynamics between owned IP and licensed properties reveals another strategic tension. FIFA—now EA Sports FC—demonstrates both sides. The FIFA license provided instant global credibility and marketing power, worth hundreds of millions in implied value. But when FIFA demanded doubled fees, EA walked away, betting that its own platform power exceeded the license value. The successful transition validated a core thesis: after decades of investment, EA's game mechanics and online infrastructure matter more than the name on the box.

The contrast with Star Wars illuminates the opposite dynamic. EA paid handsomely for exclusive Star Wars rights from 2013-2023, seeing the license as a gateway to new audiences and guaranteed marketing attention. But the restrictions that came with the license—Disney's approval processes, canon requirements, brand guidelines—constrained creativity and slowed development. The Battlefront II controversy partly stemmed from trying to force EA's monetization model into Disney's family-friendly framework.

Studio management philosophy has evolved through painful trial and error. The early approach—acquire studios, impose EA's processes, integrate aggressively—led to an exodus of talent and shuttered studios. BioWare's struggles with Anthem exemplified the problem: forcing a studio known for single-player RPGs to create a live service game predictably ended in disaster.

The modern approach attempts more nuance. Respawn Entertainment, acquired in 2017, maintained relative autonomy and delivered Apex Legends—a billion-dollar success. The lesson seemed clear: preserve studio culture, provide resources, but don't impose rigid frameworks. Yet even this approach shows strain. Respawn's founders have departed, and the studio increasingly resembles any other EA division.

The innovation versus iteration debate plays out most visibly in sports franchises. Critics deride annual sports releases as roster updates, but EA has turned this perceived weakness into strategic strength. Iteration allows for predictable development costs, reduced technical risk, and accumulated improvements over time. Revolutionary changes would actually be strategically dangerous—why risk alienating millions of satisfied customers?

Instead, EA innovates through modes and monetization. Ultimate Team was a revolutionary innovation hidden inside an iterative product. The franchise looks the same, plays similarly, but generates revenue in entirely new ways. It's innovation that doesn't disrupt the core product—perhaps the most difficult kind to execute.

Marketing muscle represents another competitive advantage often underestimated by competitors. EA spends over $1 billion annually on marketing—more than many publishers' entire revenue. This creates a flywheel effect: marketing spend drives awareness, awareness drives sales, sales justify more marketing spend. Smaller publishers simply can't compete at this scale, regardless of game quality.

The network effects in multiplayer gaming add another moat. Apex Legends succeeded not just because it was free-to-play and well-designed, but because EA could instantly put it in front of millions of players through its marketing channels. The game reached 50 million players in a month—impossible without EA's scale. These players then recruited friends, creating organic growth that no amount of marketing spend could replicate.

The subscription future positions EA for the next platform shift. If gaming follows video (Netflix) and music (Spotify) toward subscription models, EA Play provides the foundation. The challenge is managing the transition without cannibalizing high-margin traditional sales. It's why EA Play includes older games and limited-time trials rather than day-one releases—testing the model without betting the company.

Cloud gaming positioning remains cautiously optimistic. EA partners with every major cloud platform—Google Stadia (before its shutdown), Amazon Luna, Xbox Cloud Gaming—without committing exclusively to any. It's a hedge against platform shift while maintaining flexibility. If cloud gaming explodes, EA is positioned to benefit. If it remains niche, EA hasn't overinvested.

The EA playbook, ultimately, is about risk management through diversification, scale advantages through marketing and infrastructure, and strategic flexibility through portfolio breadth. It's not a playbook for creating the most innovative or beloved games—it's a playbook for building a sustainable, profitable business in an inherently volatile industry.

Critics argue this approach prioritizes commerce over art, and they're not wrong. But EA would counter that commercial success enables artistic investment, that scale allows for experimentation, and that sustainability serves players better than brilliant failure. Whether you agree depends on whether you see games primarily as cultural artifacts or commercial products. EA made its choice long ago.

XI. Bull & Bear Case Analysis

The investment case for Electronic Arts splits sharply depending on your time horizon and beliefs about gaming's future. Like analyzing a consumer products company that happens to make interactive entertainment, or a technology platform masquerading as a game publisher, EA defies simple categorization. The bull and bear cases reflect this fundamental tension.

The Bull Case: Dominance at Scale

Bulls see EA as one of the few gaming companies with truly defensible moats. Start with sports gaming, where EA's position approaches monopolistic. The exclusive NFL license through Madden, the soccer supremacy of EA Sports FC, the NHL and PGA dominance—these aren't just successful franchises but regulatory-capture-level market positions. Competitors literally cannot make NFL games. That's not a competitive advantage; it's a legal monopoly.

The financial characteristics of these franchises boggle the mind. Madden generates over $600 million annually with 75%+ operating margins on incremental revenue. Development costs are largely fixed—the game engine evolves gradually, rosters update automatically through data feeds, and marketing campaigns recycle established formats. It's essentially an annuity stream disguised as a video game business.

The successful transition to digital and live services proves EA's adaptability. Remember, this company thrived through every platform shift: PC to console, cartridge to CD, offline to online, physical to digital, product to service. Each transition created opportunities for disruption, yet EA emerged stronger. For FY24, net cash provided by operating activities was a fiscal year record $2.315 billion, up 49% year-over-year, demonstrating the model's cash-generating power.

The portfolio diversification provides unusual stability for a gaming company. When Battlefield fails, FIFA compensates. When mobile disappoints, console thrives. This isn't a Zynga or Rovio dependent on a single franchise or platform. EA's breadth means it can weather failures that would cripple smaller publishers.

Bulls also point to shareholder-friendly capital allocation. During FY24, EA returned $1.505 billion to stockholders through stock repurchases and dividends, with the board has authorized a new stock repurchase program of $5 billion over three years. This isn't a growth-at-all-costs tech company burning cash on moonshots. It's a mature business returning excess capital while maintaining strategic flexibility.

The emerging platforms story adds optionality. Cloud gaming, VR/AR, subscription services—EA doesn't need to pick winners. Its scale allows participation across all platforms. When the next computing paradigm emerges, EA will already be there with content and infrastructure.

The Bear Case: Disruption from Below

Bears see existential threats lurking beneath apparent strength. Start with the platform shifts that EA supposedly navigated successfully. Yes, EA survived, but at what cost? The company that pioneered artist-centric development became the poster child for corporate gaming. The innovator became the incumbent. History suggests incumbents eventually fall.

The free-to-play competition represents a clear and present danger. Fortnite generates more revenue than EA's entire sports division while giving the game away free. Genshin Impact, a mobile game from a Chinese studio, generates billions annually. These aren't traditional competitors playing by EA's rules—they're rewriting the rules entirely.

The talent retention crisis deepens annually. EA's reputation among developers has never recovered from the "EA Spouse" era and studio closure spree. Top talent increasingly flows to independent studios or platform holders with better reputations. Respawn's founders left. BioWare's leaders departed. When your key asset walks out the door every evening, reputation matters.

Rising development costs threaten the economic model. AAA games now cost $200+ million to develop. One failure can erase years of profits. The live service model that generates such attractive margins also requires constant content updates, ongoing server costs, and community management. The economics aren't as attractive as they appear when fully loaded.

Platform holder power represents another threat. Apple and Google's 30% tax on mobile, console makers' licensing fees, potential regulation of digital stores—EA doesn't control its distribution destiny. If platform holders squeeze publishers harder, margins evaporate quickly.

Regulatory risks around monetization loom larger each year. Belgium and Netherlands banned loot boxes. UK Parliament investigated gaming addiction. US senators propose legislation around "pay-to-win" mechanics. Ultimate Team's billion-dollar revenue stream exists at regulatory sufferance. One major market banning card packs could devastate EA's most profitable division.

The demographic shift away from traditional gaming poses long-term challenges. Younger players gravitate toward free-to-play, social, mobile-first experiences. They watch gaming content on Twitch rather than playing themselves. The $70 AAA game might be aging out with its audience.

Competition from unexpected quarters intensifies. Netflix enters gaming. Apple invests billions in Apple Arcade. Amazon builds gaming studios. These tech giants have resources that dwarf EA's, and gaming represents a strategic priority for platform control.

The Verdict: Persistent but not Invincible

The reality likely lies between these extremes. EA's sports monopoly provides a cash cushion that funds experimentation and mistakes. The live service transformation, while controversial, aligns with industry economics. The company generates prodigious cash flow and returns it to shareholders responsibly.

But the threats are real. Free-to-play competitors don't need to kill EA—just erode its growth and margins. Regulatory intervention could arrive suddenly and devastatingly. Platform shifts could strand EA's competencies in obsolete paradigms.

EA resembles a successful industrial company more than a tech growth story. It extracts value from established franchises, optimizes operations for efficiency, and returns cash to shareholders. That's a perfectly valid investment thesis—just not an exciting one.

The fundamental question isn't whether EA survives—its financial strength ensures that. The question is whether it thrives or gradually transforms into gaming's equivalent of a tobacco company: profitable but shrinking, cash-generative but uninspiring, persistent but no longer vital.

For investors, the calculation depends on time horizon and risk tolerance. EA offers stability, dividends, and predictable cash flows in an unpredictable industry. It won't go to zero, but it might not go to the moon either. In a portfolio, it's the ballast, not the sail.

XII. Looking Forward: The Next Chapter

Andrew Wilson stood before investors at EA's September 2024 Investor Day with unusual confidence. Behind him, slides showed hockey-stick growth projections and margin expansion targets. "We're not just participating in the future of entertainment," he declared, "we're creating it." The statement would have seemed hyperbolic from most CEOs, but EA's position at the intersection of gaming, AI, and platform evolution gives it unusual optionality for whatever comes next.

The artificial intelligence revolution presents EA with opportunities that smaller publishers can't match. Training AI requires data—billions of player interactions, millions of hours of gameplay telemetry, decades of design decisions. EA possesses one of gaming's largest data repositories. Every FIFA match, every Apex Legends battle, every Sims interaction feeds algorithms that could fundamentally transform game development.

Consider procedural content generation. EA spends hundreds of millions annually creating content—new levels, characters, storylines, items. AI could generate this content at fractional cost. Not replacing human creativity but augmenting it. A designer creates the template; AI produces infinite variations. Ultimate Team could offer genuinely unique cards. The Sims could generate personalized storylines. Battlefield maps could adapt to player behavior in real-time.

The technology extends beyond content to core development. AI-assisted programming could reduce development time from years to months. Automated testing could eliminate bugs before players encounter them. Dynamic difficulty adjustment could keep every player in the optimal challenge zone. These aren't theoretical possibilities—EA's research labs are actively developing these capabilities.

The metaverse question, though tarnished by crypto association and Meta's struggles, represents another frontier. EA doesn't use the M-word publicly, but its actions speak louder. The Sims already approximates a social metaverse. EA Sports FC's Ultimate Team creates persistent digital identity across seasons. Apex Legends builds social graphs that transcend individual matches.

The convergence seems inevitable: persistent worlds where players maintain identity across games, where virtual goods have real value, where social interaction becomes primary and gameplay secondary. EA's portfolio positions it perfectly—sports for competition, The Sims for social interaction, Battlefield for action. It's not building a metaverse; it's building multiple metaverses that could eventually interconnect.

Subscription gaming's end state remains unclear, but EA's positioning seems optimal regardless of outcome. If subscriptions dominate, EA Play provides the foundation. If hybrid models emerge, EA's diverse portfolio supports multiple monetization strategies. If traditional sales persist, EA maintains that capability. It's strategic optionality at its finest.

The mobile gaming evolution continues accelerating. Mobile hardware now rivals consoles. 5G enables cloud streaming to phones. Generation Z treats phones as primary gaming devices. EA's mobile revenue, while growing, remains subscale relative to opportunity. The acquisition strategy signals recognition—buying Glu Mobile, Playdemic, and others positions EA for mobile's next phase.

But the real mobile opportunity might be convergence rather than separation. Games that seamlessly transition from console to mobile, maintaining progress and social connections. EA Sports FC already synchronizes Ultimate Team across platforms. Expanding this to all franchises could unlock enormous value.

Emerging markets represent the clearest growth vector. India, Southeast Asia, Africa—billions of potential players entering the global middle class. These markets won't follow Western gaming evolution. They'll leapfrog straight to mobile, free-to-play, and cloud streaming. EA's challenge is creating products for markets with different payment methods, cultural preferences, and infrastructure limitations.

Success in five years would look like transformation without abandoning core strengths. Sports franchises still dominate but through games-as-a-service rather than annual releases. Live services generate 80%+ of revenue but through cosmetics and convenience rather than pay-to-win. EA originals compete with anyone while licensed IP provides stability. The company remains profitable but also innovative, corporate but also creative.

The technical infrastructure investments suggest EA understands the stakes. The Frostbite engine, despite criticism, provides technological consistency across franchises. Cloud computing partnerships ensure scalability. Data analytics capabilities rival tech companies. These aren't sexy investments, but they're essential for competing at scale.

The wildcard remains regulation. Government intervention could arrive suddenly and severely. Loot box bans could spread globally. Privacy regulations could limit data collection. Antitrust action could force divestiture of sports licenses. EA's lobbying efforts and industry associations provide some protection, but regulatory risk remains the sword of Damocles hanging over the entire model.

Cultural relevance represents another challenge. Gaming increasingly means watching streams, sharing clips, and creating content—not just playing. EA's games generate billions in revenue but modest cultural impact compared to Minecraft, Roblox, or Fortnite. The company needs hits that transcend gaming into broader culture.

Looking forward, EA faces a fundamental choice: embrace radical transformation or optimize incremental evolution. The safe path—steady improvements, careful expansion, reliable returns—ensures survival but not leadership. The bold path—platform shifts, business model innovation, creative risk-taking—could establish EA for another generation or trigger expensive failures.

History suggests EA will choose carefully managed evolution with selective bold bets. It's not in the company's DNA to bet everything on unproven concepts. But it's also shown remarkable ability to recognize and exploit platform shifts others miss.

The next chapter of EA's story won't be written in boardrooms or development studios but in the behavioral patterns of billions of global players. Whether they choose subscriptions or purchases, mobile or console, competitive or casual, realistic or fantastical—these choices will determine EA's trajectory more than any strategic plan.

What seems certain is that EA will remain central to gaming's future, even if that future looks nothing like gaming's past. The company that began by asking "Can a Computer Make You Cry?" might eventually ask "Can an AI Make You Dream?" The answer, as always with EA, will depend on whether someone's willing to pay for it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube