DexCom: The Revolution in Continuous Glucose Monitoring

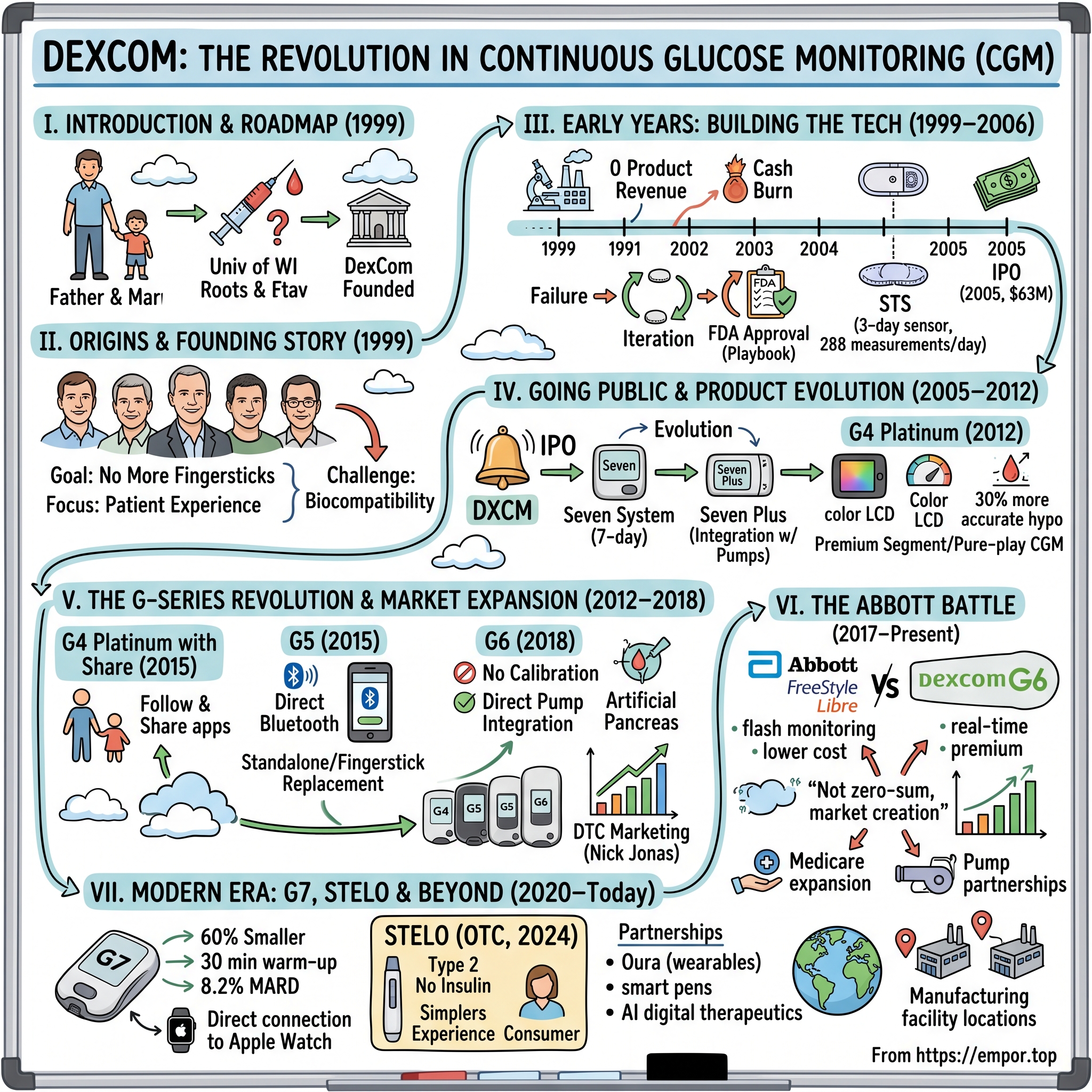

I. Introduction & Episode Roadmap

Picture a father in 1999 San Diego, watching his diabetic child endure yet another fingerstick—the seventh that day. The pain, the inconvenience, the constant interruption of childhood. Now imagine that same father thinking: "There has to be a better way." That moment of parental frustration would spark a revolution that transformed diabetes management forever.

DexCom was founded in 1999 by Scott Glenn, John Burd, Lauren Otsuki, Ellen Preston and Bret Megargel, emerging from a simple yet audacious premise: what if diabetics could know their blood sugar levels continuously, without the painful ritual of fingersticks? The company's roots stem from the pioneering 1967 research on implanted glucose sensors at the University of Wisconsin—three decades of academic promise waiting for the right team to commercialize it.

Today, DexCom stands as a $33.26 billion market cap juggernaut, having eliminated billions of fingersticks and fundamentally altered how millions manage their diabetes. Chicago-based Abbott Laboratories and San Diego-based Dexcom are the top two sellers of continuous glucose monitors, locked in a fascinating duopoly that has both companies winning as the market explodes.

But how did a San Diego startup take on medical device giants like Johnson & Johnson and Medtronic? How did they navigate seven years of regulatory hell before selling their first product? And why are they now partnering with smart ring makers and launching over-the-counter sensors for people who don't even have diabetes?

This is the story of relentless innovation in the face of skepticism, of building trust fingerstick by fingerstick, and of creating a market that is expected to reach US$ 32.97 billion by 2031 from US$ 12.63 billion in 2024, at a CAGR of 12.6%. It's a story that matters because 29.7 million people of all ages—or 8.9% of the U.S. population—had diagnosed diabetes in 2021, with diabetes being the direct cause of 1.6 million deaths globally that same year.

We'll trace DexCom's journey from university research through IPO struggles, product evolution, and the current battle for continuous glucose monitoring supremacy. Along the way, we'll uncover the strategic decisions that separated winners from losers, the partnerships that mattered, and what the future holds as biosensing moves beyond diabetes into the mainstream of preventive health.

II. Origins & Founding Story

The conference room at the University of Wisconsin hummed with possibility in 1967. Researchers had just demonstrated something remarkable: an implanted glucose sensor that could survive inside the human body. For the first time, continuous monitoring seemed theoretically possible. Yet for three decades, this breakthrough languished in academic journals, waiting for someone with the vision—and personal motivation—to bring it to market.

Enter Scott Glenn in 1999, a serial entrepreneur with a track record in life sciences. One of Scott's significant roles was as Chairman and Founder of Dexcom, a leader in Continuous Glucose Monitoring (CGM) technology that has transformed diabetes management for patients worldwide. But Glenn wasn't motivated solely by market opportunity. The founders saw a significant problem in diabetes care. They aimed to create a better way for people with diabetes to monitor their blood sugar levels, moving beyond the limitations of fingerstick tests.

The founding team read like a who's who of biomedical entrepreneurship. John Burd brought deep technical expertise in sensor technology. Lauren Otsuki understood the regulatory labyrinth they'd need to navigate. Ellen Preston brought operational excellence. Bret Megargel rounded out the team with business development acumen. A group including John F. Burd, Scott R. Pancoast, Bret Megargel, Lauren Otsuki, and Ellen Preston spearheaded the company's formation.

Their vision was deceptively simple yet technically audacious: create an implantable sensor that could measure glucose continuously and transmit that data wirelessly. No more fingersticks. No more guessing between measurements. Real-time data that could prevent the dangerous highs and devastating lows that define life with diabetes.

The early days were marked by a fundamental technical challenge: biocompatibility. The human body has an impressive ability to reject foreign objects, encasing them in scar tissue that would render any sensor useless within days. Previous attempts by larger companies had failed precisely at this hurdle. DexCom's founders believed they could crack the code by combining new materials science with innovative sensor chemistry.

DexCom secured early-stage venture capital funding shortly after its founding to develop its core continuous glucose monitoring technology. The pitch to investors was compelling but required patient capital—this wouldn't be a quick flip. They were honest about the timeline: years of R&D, extensive clinical trials, and a regulatory approval process that could stretch beyond a decade.

What set DexCom apart from the beginning was their focus on the patient experience. While competitors were building for clinicians and hospitals, DexCom designed for the 10-year-old who wanted to play soccer without mom hovering with a glucose meter. They designed for the executive who needed discrete monitoring during board meetings. They designed for real life.

The founding philosophy was clear: perfect was the enemy of good. They didn't need to eliminate all fingersticks on day one. They just needed to dramatically reduce them while providing trend data that fingersticks could never offer. This pragmatic approach would prove crucial in navigating FDA approval and gaining physician acceptance.

By late 1999, with initial funding secured and a clear technical roadmap, DexCom set up shop in San Diego—a biotech hub with access to talent from UCSD and proximity to the thriving medical device ecosystem of Southern California. The location would prove strategic, allowing them to recruit top engineering talent while maintaining lower costs than Silicon Valley.

The founders knew they were embarking on a marathon, not a sprint. They structured the company accordingly, with patient investors who understood the medical device timeline and a culture that celebrated incremental progress toward a revolutionary goal. This long-term thinking would be tested repeatedly over the next seven years as they burned through cash with no product to sell—but it would ultimately prove to be their greatest strategic asset.

III. Early Years: Building the Technology (1999–2006)

Seven years. That's how long DexCom operated without a single dollar of product revenue. In Silicon Valley terms, this was an eternity. In medical device reality, it was actually quite fast. The journey from founding to first FDA approval would test every assumption about patience, persistence, and the power of believing in a technology that could change millions of lives.

The money came in waves. The company raised a total of $52.7 million through 8 rounds. The latest funding round was a Post IPO round. This round raised $1.05 billion on April 11, 2020. But in those early years, every dollar was precious. Warburg Pincus, Canaan Partners, and Black Diamond Ventures saw something special—not just the technology, but the market opportunity as diabetes rates climbed inexorably upward.

The technical challenges were staggering. The sensor needed to survive in the hostile environment of human interstitial fluid for days, maintain accuracy despite the body's attempts to wall it off, and transmit data wirelessly without draining batteries every few hours. Each problem spawned a dozen more. The adhesive that held the sensor to skin couldn't cause reactions. The insertion mechanism needed to be painless enough for a child to tolerate. The algorithm interpreting sensor data had to account for lag time between interstitial fluid and blood glucose.

Inside DexCom's labs, failure was a daily occurrence. Sensors that worked perfectly on the bench would fail within hours in clinical trials. The team would gather around failed units like detectives at a crime scene, methodically working backward to identify the point of failure. Was it the membrane? The enzyme? The electronics? Each iteration brought incremental improvements, but progress was measured in months, not weeks.

The FDA approval process loomed like Everest. The agency had never approved a continuous glucose monitor for home use. There was no clear regulatory pathway, no precedent to follow. DexCom had to essentially write the playbook while following it, working with FDA officials to establish what safety and efficacy standards should even look like for this new category of device.

Clinical trials revealed uncomfortable truths. Patients loved the concept but struggled with the reality. Early prototypes were bulky, uncomfortable, and still required regular fingerstick calibrations. Accuracy in the hypoglycemic range—where precision mattered most—was inconsistent. The team faced a crucial decision: push for approval with a flawed but functional product, or delay further to improve performance.

They chose to push forward with what would become the STS (Short-Term Sensor) system. It wasn't perfect. In 2006, Dexcom received U.S. Food and Drug Administration (FDA) approval and launched the Dexcom STS Continuous Glucose Monitoring System, which is a three-day sensor that provides up to 288 glucose measurements for every 24 hours. Three days of wear seemed almost insulting compared to their original vision of implantable sensors lasting months. But it was a start.

The market education challenge was perhaps even greater than the technical one. Endocrinologists were skeptical. Why would patients want to wear a device 24/7 when fingersticks took seconds? Insurance companies balked at the cost. Who would pay hundreds of dollars monthly for data when test strips cost pennies per reading? Even patients—desperate for better solutions—hesitated at the commitment of continuous wear.

The company went public via an IPO in April 2005, raising approximately $63 million to fuel further development and commercialization. Going public before having a product in market was unusual but necessary. The capital requirements for manufacturing scale-up, clinical trials, and market development were enormous. Since April 14, 2005, DexCom's market cap has increased from $312.50M to $33.26B, an increase of 10,542.74%. That is a compound annual growth rate of 25.90%.

The first STS units shipped in 2006 to a mix of excitement and trepidation. Early adopters—often parents of children with Type 1 diabetes—were willing to tolerate the limitations for the peace of mind that came from continuous data. Every success story was amplified within the tight-knit diabetes community. Every failure was scrutinized and shared.

DexCom's strategy during these early years was brilliantly focused: win over the Type 1 community first. These patients, dealing with the most severe form of diabetes, had the most to gain from continuous monitoring. They were motivated, engaged, and vocal. If DexCom could prove value here, expansion to the much larger Type 2 market would follow.

By the end of 2006, DexCom had achieved what many thought impossible: FDA approval for a wearable continuous glucose monitor. But the real work was just beginning. They had proven the technology could work. Now they had to prove it was worth the cost, the hassle, and the learning curve. The next phase would require not just better technology, but a fundamental shift in how the medical establishment thought about diabetes management.

IV. Going Public & Product Evolution (2005–2012)

The NASDAQ bell rang on April 14, 2005, marking a peculiar moment in medical device history. DexCom went public without a product, without revenue, and with years of losses ahead. CEO Terry Gregg stood at the podium, knowing they were selling a promise, not performance. The ticker symbol DXCM appeared on screens, valued at just over $300 million—a bet on technology that wouldn't reach patients for another year.

Wall Street was confused. Analysts accustomed to evaluating price-to-earnings ratios found themselves staring at spreadsheets full of red ink. The investor calls were exercises in education. "Imagine knowing your blood sugar every five minutes," Gregg would explain. "Imagine preventing seizures before they happen. Imagine giving parents peace of mind while their diabetic child sleeps." Some got it immediately. Others remained skeptical until they met their first CGM user.

The capital from going public proved essential. Manufacturing continuous glucose monitors wasn't like making pills or even traditional medical devices. Each sensor contained precious metals, sophisticated electronics, and biocompatible membranes that required clean room production. Quality control meant testing every single unit. A single contaminated batch could destroy patient trust that would take years to rebuild.

2007 brought a crucial evolution with the Seven System, extending wear time from three to seven days. This wasn't just a 133% improvement in duration—it fundamentally changed the user experience. Weekly sensor changes felt manageable. The adhesive technology improved. The insertion process became less intimidating. But most importantly, the accuracy improved, especially in the critical hypoglycemic range where parents feared their children might slip into comas during sleep.

In 2008, Dexcom announced two consumer development agreements with Insulet Corporation and Animas Corporation. During February 2009, Dexcom received approval for the Seven Plus Continuous Glucose Monitor. These partnerships revealed DexCom's strategic thinking: they didn't need to build everything themselves. By integrating with insulin pump makers, they could create closed-loop systems—artificial pancreases that would automatically adjust insulin based on glucose readings.

The Seven Plus represented more than incremental improvement. It was DexCom's statement that they were serious about accuracy, usability, and integration. The device could communicate with insulin pumps, turning reactive diabetes management into proactive care. For the first time, patients could see not just where their glucose was, but where it was heading.

But 2008 also brought the financial crisis. Suddenly, expensive medical devices seemed like luxuries. Insurance companies tightened coverage. Patients delayed upgrades. DexCom's stock plummeted from $20 to under $3. Board meetings turned tense. Should they cut R&D to preserve cash? Reduce marketing? Delay the next generation?

Leadership made a contrarian bet: accelerate innovation. While competitors pulled back, DexCom pushed forward with the G4 Platinum development. They reasoned that when the economy recovered, they needed to have the best product in market, not just a surviving company. This decision would define DexCom's trajectory for the next decade.

Dexcom's first G-series CGM, the G4 Platinum, received a CE mark and FDA approval in 2012 for adults ages 18 and over. This device improved hypoglycemic accuracy by 30%. It also offered a longer range of transmission between the sensor and receiver, as well as a color LCD. The G4 wasn't just better—it was beautiful. The receiver looked like a consumer device, not medical equipment. This might seem trivial, but it mattered enormously to users who wore these devices every day.

The G-series naming convention itself was strategic. Like Apple's iPhone or BMW's series, it promised regular innovation and gave users something to anticipate. Each generation would be better, smaller, more accurate. The roadmap was clear even if the technical challenges remained daunting.

Distribution strategy during this period was crucial. DexCom couldn't rely solely on endocrinologists—there weren't enough of them, and many remained skeptical. They needed to reach primary care physicians who saw the vast majority of diabetes patients. This meant simplified training, clear value propositions, and most importantly, patient success stories that doctors couldn't ignore.

The sales force became educators as much as sellers. They didn't just demo products; they explained the psychology of diabetes management, the burden of constant decision-making, the fear parents felt every night. They brought patients to medical conferences, letting them tell their stories directly. "This saved my daughter's life" was more powerful than any clinical trial data.

Competition during this period was fierce but fragmented. Medtronic had sensor technology but bundled it with their pumps, limiting their addressable market. Abbott was developing what would become the FreeStyle Libre but hadn't yet figured out the form factor. Traditional glucose meter companies like LifeScan and Roche dismissed CGM as too expensive and complex for mainstream adoption.

By 2012, DexCom had established itself as the pure-play CGM company. They weren't distracted by pumps, strips, or other diabetes products. Every engineer, every dollar of R&D, every marketing message focused on one thing: making continuous glucose monitoring better, cheaper, and more accessible. This focus would prove invaluable as the market inflected from early adopters to mainstream acceptance.

V. The G-Series Revolution & Market Expansion (2012–2018)

The auditorium at the 2014 American Diabetes Association conference fell silent. On stage, a 7-year-old girl named Emma stood next to her mother. "Before G4," her mother said, "we checked Emma's blood sugar 15 times a day. We hadn't slept through the night in three years." She paused, composing herself. "Last month, Emma's sensor alerted us to a low at 2 AM. Without it..." She didn't need to finish. Everyone understood. This was why DexCom existed.

The G4 Platinum was approved by the FDA for use in patients ages 2–17 in February 2014. Pediatric approval wasn't just another market segment—it was validation of accuracy and safety at the highest level. Parents of diabetic children are the most demanding customers imaginable, requiring absolute reliability when their child's life literally depends on the device.

But the real revolution came with connectivity. Dexcom received FDA approval in January 2015 for the G4 Platinum with Share, which enabled the sharing of CGM data with up to five other people using the "Share" and "Follow" smartphone apps. Suddenly, a parent could be at work and see their child's glucose levels at school. Grandparents could babysit without fear. Teenagers could have independence while parents maintained peace of mind.

The psychological impact was profound. Diabetes management had always been isolating—a personal burden carried alone. Share technology made it communal. Support networks could actually provide support, seeing data in real-time rather than hearing about it after the fact. Marriage tensions eased when both partners could see the same information. The invisible became visible.

The Dexcom G5 was approved in August 2015 by the FDA for use as a standalone device, the G5 has Bluetooth integrated into its transmitter, enabling it to send data to a mobile device. This allows for use of the device without the standalone receiver. This eliminated the need for a separate receiver—users could see their glucose directly on their phones. It seems obvious in retrospect, but it required years of FDA negotiation to prove a consumer device could be trusted with medical data.

The smartphone integration triggered a cascade of possibilities. Third-party developers could build apps that integrated glucose data with food logs, exercise tracking, and insulin dosing. Apple Watch compatibility meant discrete glucose checking during meetings. The medical device had become a consumer technology product, and with it came consumer expectations for design, usability, and seamless integration.

Kevin Sayer, who became CEO in 2015, brought a different energy to DexCom. Where previous leadership focused on survival and regulatory approval, Sayer thought like a tech CEO. He talked about user experience, platform strategies, and network effects. He wore jeans to investor meetings and quoted Steve Jobs. Wall Street initially didn't know what to make of him, but the results spoke for themselves.

The Clarity platform launched in 2016, turning raw glucose data into actionable insights. Patterns emerged that no amount of fingerstick testing could reveal. Dawn phenomenon became visible. Post-meal spikes could be correlated with specific foods. The overnight basal rate adjustments that had bedeviled pump users for decades could finally be optimized. Big data had come to diabetes.

The G5 was approved in 2016 by the FDA for use as a standalone device, meaning for the first time, patients could dose insulin based solely on CGM readings without confirming with a fingerstick. This was the holy grail—complete fingerstick replacement. The regulatory approval required years of clinical data proving CGM accuracy matched or exceeded blood glucose meters.

But the masterstroke came with the G6. The G6 gained approval in 2018 with two game-changing features: no calibration required and direct integration with insulin pumps. The no-calibration feature eliminated the last regular fingersticks, while pump integration enabled the first true closed-loop systems. The artificial pancreas, dreamed of since the discovery of insulin, was finally becoming reality.

The more affordable FreeStyle Libre system (Baird senior research analyst Jeff Johnson estimates its average cost per day is about $4, compared to G6's $7 or $8) had launched and was gaining traction, especially internationally. But DexCom's response was strategic: they wouldn't compete on price alone. They would focus on accuracy, features, and outcomes. Let Abbott have the price-sensitive customers; DexCom would own the premium segment and work to expand insurance coverage.

Marketing shifted dramatically during this period. Direct-to-consumer advertising appeared during prime time. Nick Jonas, the pop star with Type 1 diabetes, became a spokesperson. The message evolved from "manage your diabetes" to "live your life." CGM wasn't about the disease anymore; it was about freedom from the disease's constraints.

The numbers told the story. Revenue grew from $257 million in 2014 to $1.03 billion in 2018. The installed base expanded from 65,000 to over 350,000 users. But more importantly, retention rates exceeded 80%. Once patients tried CGM, they rarely went back to fingersticks. The technology had crossed the chasm from early adopters to mainstream medical practice.

By 2018, DexCom had achieved something remarkable: they had made continuous glucose monitoring normal. Endocrinologists expected their Type 1 patients to use CGM. Insurance coverage was expanding. The technology that had seemed impossibly futuristic in 1999 was now standard of care. But the biggest battles—and opportunities—lay ahead.

VI. The Abbott Battle & Competitive Dynamics (2017–Present)

The war room at DexCom headquarters in late 2017 was tense. On the screens: Abbott's FreeStyle Libre marketing materials. "Flash Glucose Monitoring—Not CGM!" the tagline read. The price point: roughly half of DexCom's G6. Abbott CEO Miles White had just declared war, and he had a $20 billion medical device giant's resources behind him.

Abbott's strategy was brilliant in its simplicity. By calling it "flash" monitoring instead of continuous, they sidestepped years of regulatory requirements. Users had to scan the sensor with a reader to get glucose values—it didn't continuously transmit like DexCom. This one compromise allowed Abbott to slash costs and accelerate approval. With more than 1.3 million users worldwide, Libre anchors Abbott's diabetes device business, which posted 37 percent sales growth to $1.9 billion in 2018. Diabetes care is the fastest-growing product line at Abbott, which saw total revenue rise 11.6 percent to $30.6 billion last year.

Kevin Sayer's response in investor calls was measured but pointed. "Many international payers have recognized that flash-based systems are not equivalent to real-time CGM and have created different reimbursement categories for each. Early signs in the US suggest that payers feel the same way. We also know that many of our new international patients have transitioned from Libre to Dexcom because of these important differences".

The battlefield quickly became clear: DexCom would own Type 1 diabetes with superior accuracy and real-time alerts. Abbott would dominate Type 2 with lower cost and simplicity. Dexcom is widely considered to have more convenient design and premium technology for children with Type 1, for example, who are at greater risk of having a potentially deadly hypoglycemic episode while asleep. But both companies understood the real prize: the massive, underpenetrated Type 2 market.

"We're firm believers that both Dexcom and Abbott can be winners at the same time – the global CGM opportunity is large enough that success isn't mutually exclusive," wrote JP Morgan analyst Robbie Marcus. This wasn't zero-sum competition—it was market creation. Every Abbott user who experienced the benefits of glucose monitoring was a potential future DexCom customer as their disease progressed.

The marketing wars intensified. DexCom launched its first Super Bowl commercial in 2021 featuring Nick Jonas. Abbott responded with aggressive direct-to-consumer campaigns emphasizing affordability. Both companies began targeting primary care physicians, knowing that endocrinologists alone couldn't drive the volume needed for mass adoption.

Where there might just be 8,000 or 9,000 endocrinologists in the U.S., there are more than 200,000 primary care physicians, Kaczor said. In the past, Dexcom's marketing messages were largely directed at endocrinologists. "We realized this technology was bigger than that, and we needed to get to the user," CEO Kevin Sayer said. "We started directing media more toward the end user rather than the prescriber as a customer".

Medicare expansion in 2023 changed everything. The CGM market could expand to $10 billion in 2025, assuming more people with Type 2 diabetes who take daily injections of long-acting basal insulin or who don't take insulin at all start wearing the devices. Suddenly, millions of Type 2 patients had coverage for CGM. The land grab was on.

But competition wasn't just about stealing customers—it was about expanding the pie. Continuous glucose monitoring product manufacturers holding majority of the market share include Dexcom, Inc., Abbott Laboratories, and Medtronic plc. Medtronic, despite having integrated pump-sensor systems, struggled to compete with standalone CGM offerings. Their closed ecosystem strategy that had worked in pumps proved a liability in sensors.

The international dynamics were particularly fascinating. In Europe, where government health systems made purchasing decisions, price mattered more. Abbott gained significant share. But in markets like Germany and the UK, where accuracy standards were stricter, DexCom maintained leadership. Each country became a chess match of regulatory strategy, pricing, and clinical evidence.

"I think those two are going to be a duopoly here over the next five years," predicted analyst Ryan Blicker. The economics supported this view. CGM manufacturing required massive scale for profitability. The regulatory barriers for new entrants were enormous. Patent thickets protected key technologies. Network effects from data platforms and ecosystem partnerships created additional moats.

Innovation acceleration became the new battlefield. Product cycles compressed from years to months. Dexcom plans to quadruple its G6 production capacity to meet demand. Abbott pushed Libre 3 with even smaller sensors. Both companies raced to add features: predictive alerts, medication tracking, food logging, exercise correlation.

The partnership strategies diverged notably. DexCom pursued deep integration with insulin pump makers like Tandem and Insulet, enabling closed-loop systems. Abbott went broad, partnering with digital health platforms and pharmaceutical companies. Abbott has deals with Danish drugmaker Novo Nordisk, medical technology companies Livongo and Bigfoot Biomedical and online nutrition service Nutrino. Dexcom also has a partnership with Novo Nordisk, which is developing a smart insulin pen, as well as drugmaker Eli Lilly and insulin pump maker Tandem Diabetes Care.

Pricing pressure intensified but didn't become the race to the bottom many feared. Both companies learned that outcomes data, not just price, drove coverage decisions. Real-world evidence showing A1C reductions, decreased hospitalizations, and improved quality of life justified premium pricing. The conversation shifted from "cost per sensor" to "value per patient outcome."

By 2024, the competitive landscape had stabilized into a sophisticated dance. Abbott and DexCom pushed each other to innovate faster while carefully avoiding price wars that would destroy margins. They competed fiercely for new customers while respecting each other's core markets. Most importantly, their rivalry had grown the entire category from a niche medical device to a mainstream health technology. Together, they had made CGM not just acceptable but expected for diabetes management.

VII. Modern Era: G7, Stelo & Market Expansion (2020–Today)

The December 2022 FDA approval letter for the G7 arrived at DexCom headquarters like a Christmas gift. But CEO Kevin Sayer wasn't celebrating—he was already thinking three moves ahead. "We haven't had anything new to push in the United States for quite a while," he told investors. The G7 wasn't just an iteration; it was a statement of intent to dominate the next decade of diabetes technology.

The next generation Dexcom G7 continuous glucose monitor (CGM) got the green light from the FDA, boasting a smaller, more accurate, and easier-to-use system than its predecessor, the Dexcom G6. At 60% smaller than the G6, the combined sensor-transmitter unit looked like something Apple might design. The sensor warmup time is only 30 minutes (the G6 is two hours)—a seemingly small detail that eliminated a major friction point for users.

The accuracy improvements were remarkable. The MARD for the G7 is 8.2% for sensors placed on the upper arm. That means the reading from the Dexcom is, on average, 8.2% different than the reading on the glucometer. This is an improvement over the G6's 9% MARD. In the hypoglycemic range—where accuracy could mean the difference between life and death—the G7 performed even better.

But the real revolution came in March 2024 with Stelo. The Dexcom Stelo Glucose Biosensor System is an integrated CGM (iCGM) intended for anyone 18 years and older who does not use insulin, such as individuals with diabetes treating their condition with oral medications, or those without diabetes who want to better understand how diet and exercise may impact blood sugar levels. This wasn't just market expansion—it was market creation.

There are more than 25 million Type 2 diabetes patients in the U.S. that do not use insulin, and suddenly, they could access CGM without a prescription. The over-the-counter approval was unprecedented. For the first time, continuous glucose monitoring escaped the confines of medical practice and entered the consumer wellness space.

The Stelo launch strategy was masterful. Instead of competing with Abbott's Libre on price in the prescription market, DexCom created an entirely new category. The platform will be tailored to the needs of these Type 2 patients, which means it will not include many of the alerts and notifications meant for diabetes patients at risk of experiencing more serious emergencies. "It's designed to be a simpler experience," Jake Leach said.

International expansion accelerated dramatically. Manufacturing facilities sprouted across the globe—Mesa, Arizona; Batu Kawan, Malaysia; and Athenry, Ireland. Each facility represented not just production capacity but regulatory strategy, allowing local manufacturing for faster approval and better reimbursement terms in key markets.

Medicare expanded coverage of the devices for more people with Type 2 diabetes, representing "the largest single expansion of access to CGM" in 2023. This wasn't just about reimbursement—it was validation that CGM had become standard of care, not experimental technology. Private insurers quickly followed, understanding that CGM coverage reduced long-term costs through better outcomes.

The venture capital arm launched in early 2021 marked DexCom's ambition beyond glucose. Investments in digital therapeutics, AI-driven coaching platforms, and predictive analytics companies created an ecosystem play. DexCom wasn't just selling sensors anymore—they were building a metabolic health platform.

Direct-to-consumer marketing exploded. The 2024 Super Bowl featured not one but two DexCom commercials. Social media influencers with diabetes became brand ambassadors, showing real-life CGM data to millions of followers. The message had evolved from "manage your diabetes" to "optimize your health"—a subtle but crucial shift that expanded the addressable market exponentially.

Manufacturing scale became a strategic weapon. "We've been pushed to our limits on capacity the entire year because our growth has been so dramatic," CEO Kevin Sayer noted. "When it comes to building thousands, and tens of thousands, and hundreds of thousands, the challenges of these manufacturing materials and these processes becomes very real". Each production line represented millions in capital investment but enabled cost reductions that made broader coverage viable.

TIME named Stelo as the best Over-The-Counter Glucose Monitor on its list of the most groundbreaking inventions of the year in 2024. The recognition wasn't just about the technology—it was acknowledgment that DexCom had successfully repositioned CGM from medical device to consumer health product.

The G7 ecosystem expanded rapidly. In June, Dexcom announced it expanded its diabetes-management capabilities by offering direct connectivity to the Apple Watch for its G7 continuous glucose monitoring system via a dedicated Bluetooth connection. Integration with Tandem's t:slim X2 pump created a true artificial pancreas. Partnerships with digital health platforms meant glucose data could inform everything from meal planning to exercise optimization.

Competition evolved from hardware to software and services. The sensors themselves were becoming commoditized—the real value lay in the algorithms interpreting the data, the coaching provided through apps, and the ecosystem connections that made glucose data actionable. DexCom's investment in AI and machine learning capabilities suggested they understood this shift.

By late 2024, DexCom's transformation was complete. From a medical device company selling to hospitals and clinicians, they had become a consumer health technology company with FDA approval. The TAM had expanded from millions of insulin-dependent diabetics to potentially anyone interested in metabolic health. The question was no longer whether CGM would become mainstream, but how quickly and how completely it would reshape our understanding of health itself.

VIII. Business Model & Unit Economics

The spreadsheet on the CFO's screen told a beautiful story. Customer acquisition cost: $800. Lifetime value: $12,000. Gross margins: 65% and climbing. The razor-and-blade model that Gillette pioneered had found its perfect expression in continuous glucose monitoring—but with a twist that would make even the savviest investor jealous.

Each DexCom user needs a new sensor every 10 days (or 15 days with the latest G7 version). At roughly $70 per sensor, that's $210-280 monthly in recurring revenue. The transmitter, lasting three months, adds another $30 monthly. But here's the genius: unlike razors, where customers might switch brands for a sale, CGM users rarely churn. Switching means learning new software, risking insurance coverage gaps, and potentially breaking integration with insulin pumps or other devices.

The manufacturing economics are equally compelling. A CGM sensor contains perhaps $10 worth of materials—platinum electrodes, biocompatible membranes, medical-grade adhesives, and a tiny circuit board. The real costs lie in the clean room manufacturing, quality control, and regulatory compliance. But once production lines are optimized and running at scale, each additional sensor is nearly pure profit.

In the last 12 months, operating cash flow was $964.10 million and capital expenditures -$388.90 million, giving a free cash flow of $575.20 million. This cash generation funds a virtuous cycle: more R&D leads to better products, which command premium pricing, which funds more R&D. It's the same playbook that built Intel, but applied to medical devices.

The channel strategy reveals sophisticated thinking about healthcare economics. DexCom sells through two primary channels: pharmacy benefit (like getting prescriptions filled at CVS) and durable medical equipment (DME, delivered directly to patients). The pharmacy channel offers convenience and faster payment but lower margins. DME provides higher margins but requires more customer service. The mix has shifted toward pharmacy as CGM has mainstreamed—a strategic trade-off of margin for volume and market penetration.

Insurance dynamics create both moat and frustration. Getting on formulary with major insurers takes years of outcomes data, economic modeling, and relationship building. Once achieved, this coverage becomes a massive competitive advantage. New entrants can't simply undercut on price—they need to navigate the same labyrinthine approval process. But this also means DexCom must constantly prove value through real-world evidence and health economic studies.

The international model differs dramatically from the U.S. In single-payer systems like the UK's NHS, DexCom negotiates with governments, not insurers. Price pressure is intense, but volumes are guaranteed. In emerging markets, they've experimented with different models—subscription services, pay-per-insight rather than pay-per-sensor, and partnerships with local manufacturers to reduce costs.

The patent portfolio represents billions in hidden value. DexCom holds over 500 patents covering everything from sensor chemistry to insertion mechanisms to data algorithms. Each patent extends the moat, but more importantly, the interconnected nature of the technology makes design-arounds nearly impossible. Competitors can't just copy one element—they'd need to reinvent the entire system.

Partnerships have become profit multipliers. Dexcom entered a non-exclusive agreement with Tandem Diabetes Care, Inc. in 2015 to allow the integration of its new G5 and G6 continuous glucose monitoring systems into Tandem's insulin pumps. Each pump integration creates switching costs for users and opens new distribution channels. Pump companies handle the selling; DexCom just provides sensors. It's found revenue with zero customer acquisition cost.

The software platform strategy is still emerging but potentially transformative. Clarity, DexCom's analytics platform, aggregates billions of glucose readings. This data has immense value for pharmaceutical companies developing new diabetes drugs, researchers studying disease progression, and AI companies building predictive models. DexCom hasn't fully monetized this yet, but the potential is enormous.

R&D spending tells the strategic story. At 12-15% of revenue, DexCom invests more in R&D than most medical device companies but less than pure tech companies. This reflects their hybrid nature—they need breakthrough innovation but within the constraints of regulatory approval. Every R&D dollar must balance moonshot research with incremental improvements that maintain market leadership.

The Stelo launch revealed new unit economics possibilities. According to DexCom, the Stelo glucose biosensor will be available for purchase online in the summer of 2024. Because it will be an OTC product, consumers will not need a prescription. Direct-to-consumer sales eliminate insurance complexity and potentially double margins. Even at lower price points, the economics could be superior to prescription CGM.

Gross margin is 59.43%, with operating and profit margins of 15.25% and 12.90%. These margins have expanded steadily as manufacturing has scaled, but they're still below pure software companies. The question is whether DexCom can transition more value to software and services, where margins approach 80-90%.

Competition has created price pressure but hasn't destroyed the model. Both DexCom and Abbott have learned that racing to the bottom on price destroys value for everyone. Instead, they compete on features, accuracy, and ecosystem integration. The result is a stable duopoly with rational pricing—the best possible outcome for shareholders.

Looking forward, the unit economics only improve. Manufacturing automation reduces costs. Longer-lasting sensors amortize fixed costs over more days. Software features command premium pricing without additional COGS. The subscription model ensures predictable revenue. It's a business model that would make any SaaS founder envious—recurring revenue with switching costs, wrapped in regulatory protection and delivered through established healthcare channels.

IX. Playbook: Lessons for Founders & Investors

The conference room at Andreessen Horowitz was packed with founders, all leaning forward as Kevin Sayer concluded his talk. "Everyone asks me about the seven years without revenue," he said. "But that wasn't the hard part. The hard part was staying focused when everyone—investors, employees, even patients—wanted us to be something else." This discipline would define DexCom's playbook for building a medical device unicorn.

Lesson 1: Patient Capital is Not Optional

DexCom secured early-stage venture capital funding shortly after its founding to develop its core continuous glucose monitoring technology. The company went public via an IPO in April 2005, raising approximately $63 million to fuel further development and commercialization—still without a product in market. This wasn't irrational exuberance; it was recognition that medical devices operate on different timescales than software. Founders must set these expectations early and find investors who truly understand the timeline.

The key is staging risk intelligently. DexCom didn't try to solve every problem before raising money. They proved technical feasibility, then raised for clinical trials. Proved clinical efficacy, then raised for regulatory approval. Proved regulatory pathway, then raised for commercialization. Each round de-risked a specific element, justifying higher valuations despite no revenue.

Lesson 2: Regulatory Strategy as Competitive Moat

DexCom's masterstroke wasn't just getting FDA approval—it was helping define the entire regulatory category for continuous glucose monitors. By working collaboratively with FDA to establish iCGM standards, they created a pathway that they understood better than any competitor. This wasn't regulatory capture; it was regulatory partnership.

The playbook: engage regulators early and often. Treat them as stakeholders, not adversaries. Help them understand the technology and its benefits. Most importantly, never surprise them. DexCom's transparency with FDA built trust that paid dividends when they needed expedited approvals for next-generation products.

Lesson 3: Start with the Desperate, Scale to the Mainstream

Type 1 diabetics represented less than 10% of the diabetes market, but DexCom focused there exclusively for the first decade. Why? Because these patients were desperate for solutions. Parents would pay anything to know their child was safe at night. This desperation created word-of-mouth marketing that no advertising could match.

The strategy: find the segment with the highest pain and willingness to pay. Solve their problem completely, even if the market seems small. These early adopters become your evangelists, your clinical evidence, and your proof points for expansion. DexCom's Type 1 success made Type 2 expansion inevitable.

Lesson 4: Platform Thinking in Hardware

Most medical device companies think in products. DexCom thought in platforms from day one. The sensor was just the beginning—the real value would come from data, algorithms, and ecosystem connections. This thinking drove seemingly irrational decisions, like open APIs when competitors kept systems closed.

Dexcom entered a non-exclusive agreement with Tandem Diabetes Care, Inc. in 2015 precisely because they understood that openness would create more value than capture. Every pump integration, every app connection, every data partnership increased switching costs and expanded their moat. The lesson: in connected devices, the network effects matter more than the hardware margins.

Lesson 5: Direct-to-Consumer in Regulated Markets

Traditional medical device marketing focused on physicians. DexCom went directly to patients, a heretical approach in 2015. "We realized this technology was bigger than that, and we needed to get to the user," CEO Kevin Sayer said. "We started directing media more toward the end user rather than the prescriber as a customer".

This wasn't just marketing innovation—it was recognition that patients had become healthcare consumers. They researched conditions online, joined Facebook groups, and increasingly advocated for their own care. By empowering patients with information, DexCom created pull-through demand that physicians couldn't ignore.

Lesson 6: Real-World Evidence Trumps Clinical Trials

Clinical trials prove safety and efficacy. Real-world evidence proves value. DexCom invested heavily in outcomes studies, registry data, and health economics research. They could show insurers exactly how much CGM reduced hospitalizations, improved A1C levels, and increased quality-adjusted life years.

The playbook: instrument everything. Track not just clinical outcomes but economic ones. Build partnerships with health systems to gather data. Publish relentlessly. Make the economic case so overwhelming that coverage becomes inevitable. This evidence-based approach turned CGM from "nice to have" to "standard of care."

Lesson 7: Competition Can Expand Markets

When Abbott entered with FreeStyle Libre, DexCom's stock initially crashed. But Sayer's response was counterintuitive: this was good for DexCom. "We're firm believers that both Dexcom and Abbott can be winners at the same time – the global CGM opportunity is large enough".

Abbott's lower price point brought new users into CGM who would never have tried DexCom's premium product. Many eventually upgraded to DexCom for better features. More importantly, Abbott's marketing dollars educated the market, reducing DexCom's customer acquisition costs. The lesson: in nascent markets, competition often grows the pie rather than dividing it.

Lesson 8: Hardware Margins, Software Multiples

Wall Street values software companies at 10-20x revenue but medical device companies at 3-5x. DexCom has systematically shifted value from hardware to software—through subscription models, data analytics, and AI-driven insights—pushing their multiple higher. The Clarity platform, coaching services, and predictive algorithms transform them from device manufacturer to digital health company.

The playbook for founders: start with hardware to solve the immediate problem, but architect for software from day one. Every hardware decision should enable future software capabilities. The hardware gets you in the door; the software keeps you there and expands wallet share.

This playbook isn't just about building a medical device company. It's about recognizing that in healthcare, patience isn't just a virtue—it's a strategy. That regulatory barriers can become competitive moats. That desperate customers become your best marketers. And that sometimes, the best response to competition is gratitude for growing your market. DexCom didn't just build a better glucose monitor; they built a better way to build medical device companies.

X. Analysis & Investment Case

The analyst day presentation in November 2024 was vintage Kevin Sayer—equal parts victory lap and battle cry. DexCom had just announced its Oura partnership, launched Stelo, and delivered another quarter of 20%+ growth. Yet Sayer spent most of the time talking about what they hadn't achieved yet. "We're 1% penetrated in Type 2 diabetes," he said. "One percent. We're just getting started."

The Market Opportunity: Bigger Than Anyone Imagined

The global market for continuous glucose monitoring devices projected to reach $16.5 billion by 2031, expanding at a double-digit CAGR of 17.8%. But this understates the true opportunity. These projections assume current diagnostic rates and treatment paradigms. They don't account for CGM becoming a preventive health tool, for pre-diabetics monitoring glucose, or for the worried well optimizing their metabolic health.

The numbers are staggering. More than 38 million Americans have diabetes (about 1 in 10), and about 90% to 95% of them have type 2 diabetes. Globally, approximately 462 million individuals were affected by type 2 diabetes corresponding to 6.28% of the world's population in 2017. Yet CGM penetration remains below 10% in Type 2 diabetes, the largest segment.

Competitive Positioning: The Moat Widens

Continuous glucose monitoring product manufacturers holding majority of the market share include Dexcom, Inc., Abbott Laboratories, and Medtronic plc. But market share doesn't tell the full story. DexCom has systematically built advantages that compound over time:

-

Accuracy Leadership: The G7's 8.2% MARD sets the industry standard. In closed-loop systems where insulin dosing depends on CGM readings, this accuracy advantage becomes insurmountable.

-

Ecosystem Control: Every pump integration, every app partnership, every data connection increases switching costs. A Tandem pump user with DexCom can't easily switch to Abbott—they'd have to change their entire diabetes management system.

-

Regulatory Expertise: Being first to market with new categories (pediatric, iCGM, OTC) provides 6-12 month advantages that competitors can't overcome.

Abbott remains formidable, but the competition has evolved from price war to market segmentation. Dexcom is widely considered to have premium technology for children with Type 1, while the more affordable FreeStyle Libre system targets adults with Type 2 diabetes. This rational competition maintains margins while expanding the total market.

Technology Roadmap: Beyond Glucose

The Oura partnership reveals DexCom's ambition. The partnership will enable two-way data flow between Dexcom glucose biosensors and Oura Ring, providing a first-of-its-kind metabolic health management experience. Combining Dexcom glucose data with the biometrics collected by Oura Ring will provide users of both products with a more complete picture of overall health.

This isn't just about glucose anymore. DexCom is positioning for the future of multi-analyte sensing—ketones, lactate, alcohol, hormones. The same technology platform that measures glucose can be adapted for other molecules. The installed base, regulatory expertise, and manufacturing scale provide advantages no startup can match.

The GLP-1 Question: Threat or Opportunity?

The elephant in the room is GLP-1 agonists like Ozempic. If these drugs cure diabetes, does anyone need CGM? The bear case writes itself: fewer diabetics means fewer CGM users. But the reality is more nuanced.

GLP-1 users need to titrate dosing, monitor effectiveness, and watch for hypoglycemia. CGM provides the feedback loop that optimizes treatment. Moreover, as these drugs expand beyond diabetes to weight management, they create new CGM users who want to understand their metabolic response. The threat might actually be an opportunity.

Financial Trajectory: The Path to $10 Billion

Revenue growth remains robust at 20%+ annually, but the composition is changing. Stelo and other direct-to-consumer products carry higher margins. International expansion, particularly in underpenetrated markets like China and India, provides runway for decades. The subscription model ensures recurring revenue with improving unit economics as manufacturing scales.

Operating cash flow of $964.10 million and gross margins of 59.43% demonstrate the model's profitability. But margins should expand further as software becomes a larger component of revenue and manufacturing automation reduces costs.

Risk Factors: What Could Go Wrong?

-

Commoditization: If CGM becomes a commodity, price becomes the only differentiator. DexCom's premium pricing depends on maintaining technical superiority.

-

New Technologies: Non-invasive glucose monitoring has been promised for decades. If someone cracks it, the entire CGM market could evaporate. But physics suggests this remains unlikely in the near term.

-

Regulatory Changes: Adverse FDA decisions or reimbursement cuts could dramatically impact growth. The regulatory moat protects but also constrains.

-

Integration Risk: As DexCom expands through acquisition and partnership, execution becomes more complex. Cultural integration, technology compatibility, and maintaining innovation speed become critical.

The Investment Case: Compounding at Scale

DexCom represents a rare combination: a growth company with defensive characteristics. The recurring revenue model, high switching costs, and regulatory moats provide downside protection. The massive underpenetrated market, expansion into wellness, and platform opportunities offer upside potential.

At current valuations, the market is pricing in successful Type 2 penetration but not wellness market expansion. If Stelo succeeds in making CGM a consumer product, if the Oura partnership opens new distribution channels, if multi-analyte sensing becomes reality—the current $33 billion market cap could look quaint in retrospect.

The bear case—that competition and GLP-1 drugs destroy the market—seems increasingly unlikely. The bull case—that CGM becomes as common as fitness trackers—seems increasingly possible. For long-term investors, DexCom offers exposure to the megatrend of preventive, personalized health with the safety of proven execution and profitable growth.

XI. Epilogue & Future Vision

The Oura ring on Kevin Sayer's finger glinted as he gestured during the November 2024 partnership announcement. "Twenty-five years ago, we dreamed of eliminating fingersticks," he said. "Today, we're dreaming bigger. What if everyone could understand their metabolic health? What if we could prevent diabetes, not just manage it?"

Dexcom is making a $75 million strategic investment in ŌURA Series D funding, with ŌURA now valued at more than $5 billion. This wasn't just an investment—it was a declaration that the future of health monitoring would be ambient, continuous, and integrated. The person of 2034 won't wear a CGM and a fitness tracker and a sleep monitor. They'll wear one or two devices that do everything, seamlessly sharing data to create a complete picture of health.

The vision extends beyond diabetes into the massive worried well market. Imagine 100 million Americans wearing glucose sensors not because they have diabetes, but because they want to optimize their health. Every meal becomes an experiment. Every workout's effectiveness becomes measurable. The quantified self movement, which started with step counters, culminates in real-time metabolic awareness.

AI will transform this data into action. Today's CGM tells you your glucose is 180 mg/dL. Tomorrow's will predict you'll hit 180 in 30 minutes based on what you just ate, your stress levels from your Oura ring, and your historical patterns. It will suggest a 10-minute walk to blunt the spike or remind you that this meal always causes problems when you're sleep-deprived.

The international opportunity dwarfs the U.S. market. In 2017, approximately 462 million individuals were affected by type 2 diabetes. The gender distribution is equal, and the incidence peaks at around 55 years of age. As CGM costs decrease and smartphone penetration increases in developing markets, billions of people could gain access to technology that was recently available only to wealthy diabetics in developed countries.

Manufacturing will evolve from medical device production to something resembling semiconductor fabs. Sensors will be printed, not assembled. Costs will plummet from dollars to cents. The expensive part won't be the hardware but the AI interpreting the data, the coaching provided through apps, and the integration with the healthcare system.

The regulatory landscape will shift from barrier to enabler. As real-world evidence accumulates showing CGM prevents complications, reduces healthcare costs, and improves outcomes, coverage will become universal. The question won't be whether insurance covers CGM, but whether not using CGM constitutes substandard care.

Partnerships will reshape the competitive landscape. The partnership means the two companies will enable data flow between Dexcom and ŌURA products. The first app integration is expected to roll out in the first half of 2025. But this is just the beginning. Imagine partnerships with Apple for integrated health monitoring, with Epic for EMR integration, with Teladoc for remote patient monitoring. The platform, not the product, becomes the moat.

New entrants will emerge, but not where expected. The threat isn't another medical device company but Apple, Google, or Amazon deciding glucose monitoring is strategic. Yet even here, DexCom's regulatory expertise, clinical evidence, and manufacturing scale provide protection. More likely, tech giants partner with rather than compete against established players.

The science will advance beyond glucose. Multi-analyte sensors measuring ketones, lactate, cortisol, and other biomarkers will provide a complete metabolic picture. Implantable sensors lasting months or years will eliminate the hassle of frequent replacement. Non-invasive monitoring—the holy grail—might finally become reality through advances in spectroscopy or other technologies.

But perhaps the biggest change will be cultural. Today, wearing a CGM marks you as diabetic. Tomorrow, not monitoring your glucose will seem as outdated as not knowing your step count. The stigma will invert—continuous health monitoring will signal health consciousness, not illness.

Success in 10 years looks like CGM disappearing into the background of daily life. Your morning routine includes checking your metabolic dashboard like you check weather or email. Your food delivery app integrates with your CGM to suggest meals that won't spike your glucose. Your doctor reviews months of continuous data, not a single fasting glucose test. Diabetes becomes preventable for millions who can see their progression from normal to pre-diabetic and intervene before crossing the threshold.

DexCom's journey from a San Diego startup to a global health technology leader mirrors the transformation of diabetes care from reactive to proactive, from episodic to continuous, from one-size-fits-all to personalized. The next chapter won't be written in regulatory approvals or market share battles, but in lives extended, complications prevented, and human potential unlocked through better understanding of our own biology.

The revolution in continuous glucose monitoring isn't ending—it's just beginning. And for investors, entrepreneurs, and anyone interested in the future of health, DexCom's story provides both inspiration and blueprint for what's possible when patient capital meets patient care, when regulation becomes innovation catalyst rather than inhibitor, and when a simple idea—knowing your glucose continuously—transforms into a platform for understanding human health itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube