Devon Energy: From Oklahoma Wildcatters to Shale Pioneers

I. Introduction & Cold Open

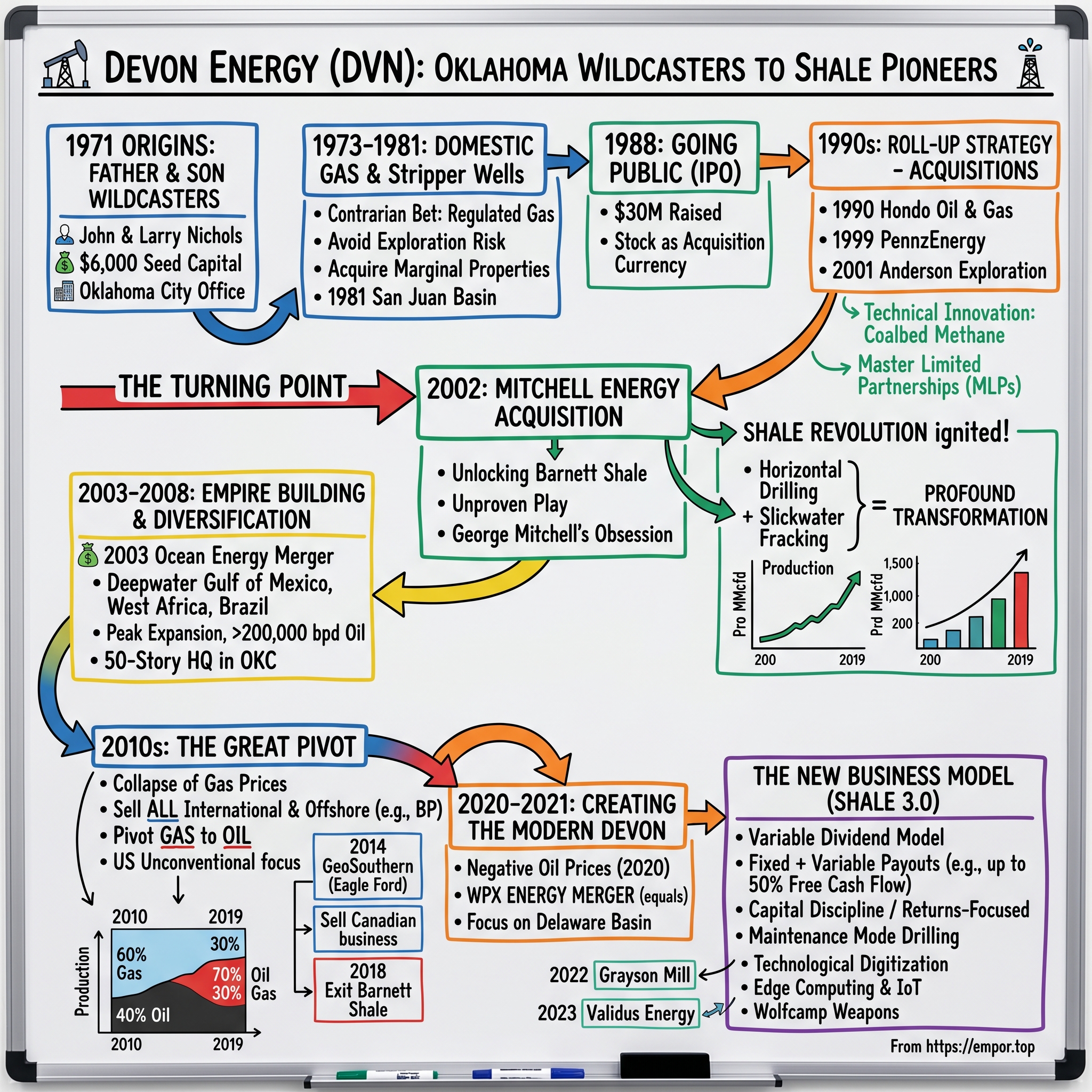

Picture this: A father and son sitting in a cramped Oklahoma City office in 1971, pooling together $6,000 to start an oil company. The majors are chasing elephants in the North Sea and Middle East. Natural gas is practically worthless—a nuisance byproduct you flare off at wellheads. Yet John Nichols, a 57-year-old veteran of the Oklahoma oil patch, and his son Larry, a reluctant lawyer who'd rather be in Washington, decide this is their moment.

Fast forward fifty years. That $6,000 seed capital has multiplied into a company worth over $40 billion. Devon Energy didn't just ride the American shale revolution—they helped ignite it. When they bought Mitchell Energy in 2002, they acquired more than assets; they inherited George Mitchell's two-decade obsession with cracking the code of the Barnett Shale. Within months, Devon's engineers combined Mitchell's fracturing techniques with horizontal drilling, unlocking trillions of cubic feet of natural gas that had been trapped in rock for millions of years.

The $12 billion question isn't just how a father-son team from Oklahoma built one of America's largest independent oil and gas producers. It's how they repeatedly zigged when the industry zagged—buying gas assets when everyone wanted oil, pioneering unconventional drilling when others stuck to conventional plays, and most recently, revolutionizing shareholder returns with their variable dividend model when peers chased growth at any cost.

This is a story about contrarian bets, technological innovation, and exquisite timing. It's about how a company named after a street in Oklahoma City (Devon Avenue, where their first office stood) became the catalyst for American energy independence. More than that, it's a masterclass in capital allocation through commodity cycles—a half-century journey through booms, busts, and everything in between.

The themes that emerge from Devon's story read like an energy industry playbook: the power of buying distressed assets and applying new technology, the importance of financial innovation in a capital-intensive business, and the delicate balance between growth and returns. But perhaps most importantly, it's about recognizing inflection points—those moments when conventional wisdom is about to be proven wrong.

II. Origins: The Nichols Dynasty & Early Years (1971–1988)

John Nichols had been knocking around the Oklahoma oil patch since the 1930s, a classic wildcatter who'd seen fortunes made and lost on the turn of a drill bit. By 1971, at age 57, he'd accumulated enough wisdom—and scars—to know that the next generation of oil and gas wealth wouldn't come from competing with the majors on their turf. His son Larry, meanwhile, had just spent several years as a young attorney in Washington D.C., working at the Justice Department and rubbing shoulders with future power brokers. He'd married Mary Nichols (no relation), whose father happened to be a prominent Oklahoma oilman, and the pull of family and opportunity drew him back to Oklahoma City.

The timing of Devon's founding was either terrible or brilliant, depending on your perspective. The 1970s energy crisis was brewing, OPEC was flexing its muscles, and the major oil companies were pouring billions into international mega-projects. For a tiny independent with $6,000 in capital, competing for prime acreage seemed impossible. But the Nicholses saw opportunity in what others ignored: domestic natural gas properties that the majors considered too small and gas itself, which was regulated, price-controlled, and trading at rock-bottom prices.

Larry Nichols brought more than a law degree to the partnership. His Washington years had given him a keen sense of regulatory trends and political winds. He suspected—correctly, as it turned out—that natural gas deregulation was coming, and when it did, gas prices would soar. While his father worked the geology and operations, Larry structured deals, navigated regulations, and built relationships with banks willing to finance their acquisitions.

By 1973, just two years after founding, Larry had become executive vice president and general counsel, essentially running the business side while his father handled technical operations. The early strategy was elegantly simple: acquire producing properties in proven North American basins, particularly in Oklahoma and Texas, where they understood the geology and had relationships. They avoided exploration risk, preferring to buy assets with established production that could be optimized with better management and modest capital investment.

The company's early moves were decidedly unglamorous. While headlines celebrated major discoveries in Alaska and the North Sea, Devon was buying stripper wells in Oklahoma—marginal properties producing 10-15 barrels per day that larger companies couldn't be bothered to operate. But these assets generated steady cash flow, and more importantly, they came with something invaluable: acreage positions in basins that would later prove to be sleeping giants.

In 1976, Larry became president, taking operational control as his father transitioned toward retirement. By 1980, at just 38 years old, Larry assumed the CEO role, inheriting a company that had grown from two employees to nearly 30, with production scattered across Oklahoma, Texas, and New Mexico. The company was generating about $10 million in annual revenue—respectable for a small independent, but Larry had bigger ambitions.

The real strategic insight came in 1981 when Devon acquired its first interest in the San Juan Basin of New Mexico. At the time, the San Juan was known for conventional gas production, but Devon's geologists noticed something interesting: massive coal seams that seemed to be releasing methane. This coalbed methane was considered a hazard in coal mining, but the Nicholses wondered if it could be commercially produced. They were about to pioneer an entirely new type of natural gas production.

Throughout the early 1980s, while oil prices gyrated wildly and many independents went bankrupt, Devon stayed disciplined. They focused on natural gas when it was deeply out of favor, believing that the supply-demand dynamics would eventually shift. They were right—natural gas deregulation came in stages throughout the decade, and prices began their slow climb from under $2 per thousand cubic feet (MCF) toward more economic levels.

The decision to go public in 1988 represented a crucial inflection point. Devon had reached the limits of what it could accomplish with private capital and bank debt. The initial public offering raised $30 million—not a huge sum, but enough to pursue more aggressive acquisition strategies. More importantly, having publicly traded stock would give Devon a currency for future deals, setting the stage for the roll-up strategy that would define its next phase of growth.

By the end of 1988, Devon Energy was producing about 50 million cubic feet of gas equivalent per day, had proven reserves of approximately 200 billion cubic feet equivalent, and employed 100 people. The company that started with $6,000 was now worth over $100 million. But Larry Nichols was just getting started—he'd spent the 1980s learning how to operate in the energy business; the 1990s would be about learning how to consolidate it.

III. The Roll-Up Strategy: Building Through Acquisitions (1989–2001)

The late 1980s oil price collapse created a buyer's market that Larry Nichols had been preparing for his entire career. While others saw distress, Devon saw opportunity. The company's first major move came in 1990 with the $122 million acquisition of Hondo Oil & Gas, a deal that doubled Devon's production overnight and established a template for future acquisitions: buy quality assets from distressed sellers, apply better operational practices, and integrate quickly.

But the real innovation wasn't just buying assets—it was how Devon financed these purchases. In 1985, even before going public, the company had pioneered the use of Master Limited Partnerships (MLPs) in the energy sector, creating tax-efficient vehicles that could raise capital from retail investors seeking yield. This financial engineering gave Devon access to capital markets that many competitors couldn't tap, providing crucial flexibility during downturns.

The San Juan Basin, where Devon had established a foothold in 1981, became the proving ground for their technical innovation. By the early 1990s, Devon had become the leading producer of coalbed methane in the basin, essentially creating an industry from scratch. The technology was deceptively complex—you had to dewater coal seams slowly and carefully to release the methane without damaging the formation. Devon's engineers developed proprietary techniques for drilling, completing, and producing these wells, achieving success rates that competitors couldn't match.

The coalbed methane success story illustrated Devon's approach perfectly: find an overlooked resource, develop the technology to extract it economically, then scale aggressively. By 1995, the San Juan Basin was producing over 100 million cubic feet per day for Devon, generating cash flows that funded further expansion.

The late 1990s saw Devon shift into acquisition overdrive. The 1998 purchase of Northstar Energy for $340 million gave Devon its first international foothold in Canada. But the transformative deal came in 1999 with the $2.5 billion acquisition of PennzEnergy. This wasn't just Devon's largest deal to date—it was a bet-the-company transaction that tripled the size of the firm and expanded its footprint into the Permian Basin, offshore Gulf of Mexico, and international markets including Egypt and Venezuela.

Wall Street was skeptical. How could a company with a market cap of $1.5 billion successfully integrate a company nearly twice its size? The answer lay in Devon's decentralized operating model and Larry Nichols' meticulous integration planning. Rather than impose a top-down structure, Devon maintained regional offices and kept key technical teams intact, focusing instead on financial controls and best-practice sharing.

The integration worked better than anyone expected. Within 18 months, Devon had achieved $100 million in annual cost synergies while maintaining production growth. The company's proved reserves jumped from 500 million barrels of oil equivalent (BOE) to over 1.5 billion BOE. Devon was no longer a small independent—it had joined the ranks of large-cap energy companies.

The year 2000 brought another significant milestone: Devon's stock joined the S&P 500 index, providing access to a whole new class of institutional investors. Larry Nichols, now 58 and at the height of his deal-making powers, wasn't satisfied. He'd built Devon into a major player through North American acquisitions, but he knew the next phase of growth would require international scale.

The $4.6 billion acquisition of Anderson Exploration in 2001 delivered exactly that. Anderson was one of Canada's premier natural gas producers, with significant positions in both conventional gas fields and emerging unconventional plays. The deal made Devon the third-largest independent gas producer in Canada and pushed total company production above 1 billion cubic feet equivalent per day—a psychological and operational milestone.

By the end of 2001, Devon had completed over 20 acquisitions totaling more than $10 billion in transaction value. The company that had started the decade with 100 employees and $100 million in market value now employed 3,500 people and was worth over $15 billion. Production had grown from 50 million cubic feet equivalent per day to over 1 billion—a twenty-fold increase achieved primarily through acquisitions.

The roll-up strategy had worked brilliantly, but it had also created a sprawling, complex organization with assets scattered across North America and beyond. Devon needed a new catalyst—something that would focus its technical capabilities and provide the next leg of growth. That catalyst would come from an unlikely source: an 83-year-old wildcatter in Fort Worth who'd spent two decades trying to crack the code of the Barnett Shale. The philosophy that had guided Devon through the 1990s—buy when others are selling, apply technology to mature fields—was about to pay its biggest dividend yet.

IV. The Mitchell Energy Acquisition: Unlocking the Shale Revolution (2002)

George Mitchell was either a visionary or a fool, depending on who you asked in Fort Worth circa 2000. For nearly two decades, the Greek-American wildcatter had been pouring money into the Barnett Shale, a dense rock formation north of Fort Worth that conventional wisdom said could never be commercially produced. Mitchell had already spent over $250 million trying to prove the experts wrong, drilling hundreds of wells with marginal results. His board wanted him to stop. His investors thought he was wasting money. But Mitchell, then 81 years old, kept drilling.

The Barnett Shale wasn't supposed to work. Shale rock is like concrete—so tight that hydrocarbons can't flow through it naturally. Mitchell's team had been experimenting with different fracturing techniques since the early 1980s, pumping various fluids and proppants into the formation to create artificial fractures. By the late 1990s, they'd developed a technique called "light sand fracking"—using water-based fluids with minimal additives that could create a network of fractures in the shale.

The breakthrough came gradually, then suddenly. Wells that had been producing 200-300 thousand cubic feet per day jumped to 1-2 million cubic feet per day. The Barnett Shale wasn't just productive—it was prolific. But there was a problem: Mitchell Energy, despite its technical success, was running out of money and management depth. George Mitchell was 83, his health was declining, and the company needed capital to develop thousands of drilling locations across the Barnett.

Larry Nichols had been watching Mitchell's progress closely. Devon's technical teams had evaluated the Barnett data and reached a startling conclusion: Mitchell had unlocked something revolutionary, but they were only scratching the surface. Devon's engineers believed that combining Mitchell's fracturing techniques with horizontal drilling—a technology Devon had perfected in other basins—could increase production by 3-4 times while accessing far more rock volume per well.

The negotiations played out over several months in 2001. Mitchell wanted to ensure his 3,500 employees would be treated fairly and his Fort Worth operations would remain intact. Nichols wanted the Barnett acreage and technical team but didn't need Mitchell's conventional assets or corporate overhead. The final deal, announced in late 2001 and closed in January 2002, was structured at $3.1 billion in cash and stock—a price that many observers thought was too high for an unproven play.

What happened next changed the energy world forever. Within four months of closing, Devon had permitted its first horizontal wells in the Barnett. The results were stunning: horizontal wells produced 3-4 times more gas than vertical wells while accessing 3,000-4,000 feet of lateral formation compared to just 200-300 feet in a vertical well. The economics weren't just improved—they were transformed.

Devon's engineers didn't stop there. They refined Mitchell's fracturing techniques, developing what became known as "slickwater" fracking—high-volume, high-pressure water treatments that could create extensive fracture networks throughout the shale. They optimized the number of fracture stages, the proppant concentrations, and the well spacing. Within 18 months, Devon was drilling Barnett wells that produced 5-6 million cubic feet per day—10 times what Mitchell's early wells had achieved.

The numbers tell the story of transformation. When Devon acquired Mitchell, the Barnett was producing about 200 million cubic feet per day from 1,800 wells. By 2005, Devon alone was producing over 1 billion cubic feet per day from 3,000 wells. By 2007, Devon had drilled over 5,000 Barnett wells and was producing 1.5 billion cubic feet per day—making the Barnett the largest gas field in the United States.

But the real revolution wasn't just about production volumes. Devon had proved that shale resources—previously considered source rocks that generated hydrocarbons but couldn't produce them—could be commercially developed. The implications were staggering. The United States had hundreds of thousands of square miles of shale formations: the Marcellus in Appalachia, the Haynesville in Louisiana, the Eagle Ford in Texas, the Bakken in North Dakota. If these could be developed like the Barnett, America's energy equation would fundamentally change.

Devon became the master class for the industry. The company hosted hundreds of visits from other operators, showing them the horizontal drilling techniques, the fracturing designs, and the production data. Some saw this openness as naive, but Larry Nichols understood something deeper: Devon couldn't develop all of America's shale resources alone. By teaching others the techniques, Devon was creating an industry that would drive service costs down, improve technology faster, and create political support for domestic energy development.

The financial returns from the Mitchell acquisition exceeded all expectations. Devon recovered its entire $3.1 billion purchase price in less than three years through cash flow from the Barnett. By 2010, Devon had generated over $15 billion in revenue from Barnett production. The acquisition multiple, which seemed expensive at 6x cash flow in 2002, looked brilliant in retrospect as production grew and gas prices rose.

More importantly, the Barnett had transformed Devon from an acquirer of conventional assets into a technology leader in unconventional resources. The expertise developed in the Barnett—horizontal drilling, multi-stage fracturing, pad drilling, real-time data analytics—became the foundation for Devon's expansion into other shale plays. The company that had bought its way to growth in the 1990s now had organic growth opportunities that would last decades. The shale revolution had begun, and Devon held the playbook.

V. Empire Building: Ocean Energy & Peak Expansion (2003–2008)

Fresh off the Barnett success, Larry Nichols faced a classic growth company dilemma in 2003: Devon had mastered shale gas, but natural gas prices were volatile and the company needed diversification. The answer came in the form of Ocean Energy, a Houston-based producer with significant oil assets in the Gulf of Mexico deepwater, West Africa, and Brazil. The $5.3 billion merger, announced in April 2003, would create the largest U.S.-based independent oil and gas producer—a behemoth with production across every major basin type on multiple continents.

Ocean Energy brought assets that Devon couldn't have accessed organically. The crown jewel was the Gulf of Mexico deepwater portfolio, including interests in major fields like Constitution, Magnolia, and Ticonderoga. These projects required $100 million-plus investments and technical expertise in subsea engineering that Devon had never developed. Ocean also brought international positions in Equatorial Guinea and Brazil—frontier markets with massive potential but significant political risk.

The cultural integration proved more challenging than any previous Devon acquisition. Ocean's Houston headquarters housed 1,200 employees accustomed to the big-company culture of deepwater development—long planning cycles, huge capital commitments, and engineering-driven decision-making. Devon's Oklahoma City culture was more entrepreneurial, focused on quick decisions and rapid drilling programs. The two organizations eyed each other warily across the Texas-Oklahoma divide.

But the timing was perfect from a market perspective. Oil prices were beginning their historic run from $30 per barrel toward $100, driven by Chinese demand growth and supply constraints. Devon's expanded oil production—now over 200,000 barrels per day—generated massive cash flows. The company declared a two-for-one stock split in 2004 and moved its listing from the American Stock Exchange to the New York Stock Exchange, symbolically joining the energy establishment.

The mid-2000s became Devon's imperial phase. In 2006, the company doubled down on the Barnett with the $2.2 billion acquisition of Chief Oil & Gas's acreage, adding 180,000 net acres adjacent to Devon's existing position. That same year, Devon began construction on a new headquarters that would reshape Oklahoma City's skyline—a 50-story tower that would become the tallest building in the state when completed in 2012.

International expansion accelerated. Devon entered Azerbaijan through a partnership with BP, taking a stake in the massive ACG field in the Caspian Sea. In Brazil, the company acquired deepwater blocks in the Campos Basin, betting that Brazilian pre-salt geology would yield elephant-sized discoveries. By 2007, Devon was operating on six continents with over 5,000 employees worldwide.

The numbers from this period remain staggering. Total production reached 600,000 barrels of oil equivalent per day. Proved reserves exceeded 3 billion barrels of oil equivalent. The company was drilling over 2,000 wells per year, from 15,000-foot horizontal shale wells in Texas to 30,000-foot deepwater wells in the Gulf of Mexico. Devon's market capitalization peaked at over $40 billion in 2008, making it one of the 100 largest companies in America.

Yet beneath the surface, cracks were forming. The complexity of managing assets across multiple continents and basin types was straining the organization. International projects were consuming massive capital with long payback periods—the Brazil deepwater program alone required $500 million in exploration spending before seeing any production. Meanwhile, the Barnett Shale and other North American unconventional plays were generating immediate cash flows with much lower political risk.

The 2008 financial crisis brought these tensions to a head. Oil prices crashed from $147 to $35 per barrel in six months. Natural gas prices, inflated by the pre-crisis commodity bubble, began a decline that would last a decade as shale gas production soared. Devon's stock fell 60% from its peak, and the company faced the harsh reality that its empire-building phase had created an unwieldy conglomerate.

Larry Nichols, now 66 and having led Devon for nearly 30 years, began contemplating succession. The company needed fresh leadership to navigate the post-crisis world—someone who could rationalize the portfolio, focus on capital efficiency, and adapt to a new era where U.S. shale would dominate global energy markets. The imperial phase was ending, and Devon would need to transform once again.

The Ocean Energy merger had achieved its goal of diversification and scale, but it had also pulled Devon away from its core competency: North American unconventional resources. The technical expertise developed in the Barnett was being diluted across too many projects. Capital was being allocated based on size rather than returns. The company that had built its reputation on disciplined acquisitions and focused operations had become exactly what it used to acquire: a bloated major with assets scattered across the globe, struggling to generate acceptable returns on capital.

VI. The Great Pivot: From Gas to Oil, International to Domestic (2010–2019)

The boardroom atmosphere at Devon's Oklahoma City headquarters in early 2010 was tense. Natural gas prices had collapsed to under $4 per MCF and showed no signs of recovering. The very success of the shale revolution that Devon had pioneered was now its biggest problem—America was drowning in natural gas. Meanwhile, oil prices had recovered to $80 per barrel and were climbing. Larry Nichols made the call that would define Devon's next decade: sell everything international and offshore, pivot from gas to oil, and focus exclusively on North American unconventional resources.

The asset sales began with a shocking announcement in March 2010. Devon would sell its entire international and offshore portfolio to BP for $7 billion—the Brazil deepwater blocks, the Azerbaijan position, the Gulf of Mexico deepwater assets, everything outside North America. The timing seemed terrible. BP desperately needed cash after the Deepwater Horizon disaster, and Devon was selling prized assets to a distressed buyer. Critics called it a fire sale.

But Nichols and his team saw it differently. Those international assets were consuming $2 billion in annual capital expenditure with development timelines stretching to 2020 and beyond. Meanwhile, Devon's engineers had identified a new opportunity that could deliver immediate returns: tight oil. The same horizontal drilling and fracturing techniques that had unlocked shale gas could also produce oil from formations like the Eagle Ford in South Texas and the Permian Basin in West Texas.

The pivot accelerated through a series of transformative acquisitions. In 2014, Devon purchased GeoSouthern Energy for $6.1 billion, acquiring 82,000 net acres in the liquids-rich window of the Eagle Ford Shale. The price tag raised eyebrows—over $70,000 per acre in some areas—but Devon's technical team believed they could drill 1,200 wells generating 30-40% rates of return even at $60 oil.

The organizational transformation was equally dramatic. In 2015, Larry Nichols stepped down as CEO after 35 years at the helm, though he remained executive chairman. His successor, Dave Hager, came from a different mold—a Presbyterian elder with a degree in petroleum engineering who spoke about "stewardship" and "capital discipline" rather than growth and empire building. Hager inherited a company in transition: still too exposed to natural gas, carrying too much debt from acquisitions, and struggling with activist investors demanding better returns.

Hager's remedy was radical simplification. Devon would become a pure-play U.S. unconventional oil producer, period. No more international ventures, no more offshore drilling, no more conventional assets. Every property would be evaluated on a simple metric: could it generate free cash flow at $50 oil? If not, it would be sold.

The divestiture program was relentless. In 2017, Devon sold its Canadian business to Canadian Natural Resources for $2.8 billion, exiting a country where it had operated for nearly 20 years. Most symbolically, in December 2018, Devon announced the sale of its Barnett Shale assets for $770 million—divesting the very properties that had launched the shale revolution. The Barnett, now mature and generating declining production, no longer met Devon's return thresholds.

The numbers tell the story of transformation. In 2010, Devon produced 60% natural gas and 40% oil and liquids. By 2019, that ratio had completely reversed—70% oil and liquids, 30% gas. International and offshore production went from 30% of total output to zero. The employee count fell from 5,000 to 1,800. Devon had become a fundamentally different company.

But the real revolution was in capital allocation philosophy. The old Devon, like most independents, had pursued growth at almost any cost, measuring success by production increases and reserve additions. The new Devon focused on returns on capital employed, free cash flow generation, and capital efficiency. Instead of drilling 2,000 wells per year across dozens of plays, Devon drilled 300 highly optimized wells in a handful of core positions.

The Delaware Basin in New Mexico became Devon's crown jewel. Through a series of bolt-on acquisitions and acreage trades, Devon assembled 400,000 net acres in the heart of the play. The Delaware's stacked geology—multiple oil-bearing formations from 5,000 to 12,000 feet deep—allowed Devon to drill multiple wells from single pad sites, dramatically reducing surface impact and costs. Wells that cost $15 million in 2014 were being drilled for $7 million by 2019, while production per well had doubled.

Technology evolution accelerated under Hager's leadership. Devon implemented real-time drilling optimization using cloud computing and machine learning. Fracturing designs were customized for each formation using microseismic monitoring and production history matching. The company even experimented with "wine rack" well configurations—complex 3D well paths that maximized reservoir contact while minimizing interference.

By 2019, Devon had completed one of the most successful corporate transformations in energy history. The sprawling conglomerate with assets on six continents had become a focused operator in five core U.S. basins. Debt had been reduced from $10 billion to $4 billion. The company was generating free cash flow even at $45 oil prices. But the ultimate test was about to come—a global pandemic that would send oil prices negative and force yet another reinvention.

VII. The WPX Merger: Creating the Modern Devon (2020–2021)

April 20, 2020, will forever be remembered as the day oil prices went negative. West Texas Intermediate crude futures settled at minus $37.63 per barrel—traders were literally paying people to take oil off their hands. For Devon Energy, trading at $7 per share with a market cap under $3 billion, it felt like an existential moment. The company that had survived every oil crash since 1971 was facing something unprecedented: a world that suddenly didn't want hydrocarbons.

Dave Hager and his team huddled virtually—COVID-19 had sent everyone home—to devise a survival strategy. Devon immediately cut its capital budget by 45%, reduced its dividend by 50%, and shut in 35,000 barrels per day of production. But Hager knew that defensive moves alone wouldn't be enough. Devon needed to fundamentally reimagine itself for a post-COVID world where investors would demand returns, not growth.

The opportunity came from an unexpected source. Rick Muncrief, CEO of WPX Energy and a former Devon executive who'd worked on the Mitchell Energy acquisition, reached out in May 2020. WPX, based in Tulsa, had fantastic Delaware Basin assets but was struggling with debt and scale. Muncrief proposed something radical: a true merger of equals that would create a Delaware Basin powerhouse while fundamentally restructuring how the combined company would operate.

The negotiations, conducted entirely over Zoom, focused less on price and more on philosophy. Both management teams agreed that the old E&P business model was broken. Instead of pursuing growth, the new company would target sustainable free cash flow. Instead of fixed dividends that forced companies to borrow during downturns, they would implement a variable dividend that flexed with commodity prices. Instead of empire building, they would focus ruthlessly on their best assets.

The deal, announced in September 2020, was elegantly structured. Devon shareholders would own 57% of the combined company, WPX shareholders 43%. No premium was paid—both stocks were so beaten down that arguing over percentages seemed pointless. Dave Hager would become executive chairman, providing continuity, while Rick Muncrief would serve as CEO, bringing fresh energy and deep Delaware Basin expertise.

But the real innovation was the new business model announced simultaneously with the merger. Devon would implement the industry's first fixed-plus-variable dividend framework. A small fixed dividend (initially $0.11 per quarter) would provide baseline income, while a variable dividend would distribute up to 50% of excess free cash flow each quarter. When oil prices were high, shareholders would receive large payouts. When prices fell, the dividend would automatically adjust without requiring board drama or credit rating downgrades.

The merger closed on January 7, 2021, just as oil prices began recovering from pandemic lows. The integration was remarkably smooth—both companies used similar drilling techniques, had adjacent acreage positions, and shared cultural DNA from Devon's earlier years. The promised $575 million in annual synergies were achieved within six months, primarily through reducing duplicate operations and optimizing drilling programs.

The transformation was immediately visible in operations. The combined company's Delaware Basin position totaled 400,000 net acres in the economic core of the play. Devon could now conduct manufacturing-mode drilling—multiple rigs drilling identical wells using standardized designs. Well costs fell to $6 million while initial production rates exceeded 3,000 barrels of oil equivalent per day. These weren't just good wells; they were among the best wells ever drilled in North America.

The variable dividend framework proved transformative for investor sentiment. In the second quarter of 2021, with oil prices recovering to $70 per barrel, Devon paid a variable dividend of $0.49 per share—a 10% annualized yield. Suddenly, Devon wasn't just another E&P company promising jam tomorrow; it was generating immediate cash returns comparable to mature industrials or utilities.

Rick Muncrief brought a different leadership style from Dave Hager's thoughtful stewardship. An Alabama native with an engineering background and a gift for plain speaking, Muncrief communicated in football metaphors and factory-floor analogies. He talked about "manufacturing" oil and gas, not exploring for it. He focused employee attention on "execution velocity" and "capital efficiency" rather than reserve growth or production targets.

The cultural integration revealed interesting dynamics. WPX employees, coming from a smaller, more entrepreneurial company, initially worried about being absorbed into Devon's larger bureaucracy. Devon employees wondered if WPX's aggressive drilling style would compromise Devon's technical rigor. But both cultures shared something crucial: a focus on unconventional resource development and a belief that technology and operational excellence could drive superior returns.

By the end of 2021, the merger's success was undeniable. The combined company generated $3.9 billion in free cash flow, returned $1.9 billion to shareholders through dividends and buybacks, and reduced debt to under $8 billion. Devon's stock price had risen from $7 to over $40 per share. The company that had seemed on death's door 18 months earlier was now the poster child for E&P transformation.

The WPX merger represented more than just successful M&A execution. It marked the final evolution of Devon from a growth-oriented acquirer to a returns-focused operator. The company that Larry Nichols had built through aggressive expansion had been completely reimagined for a new era. The question now was whether this model could survive the next inevitable cycle.

VIII. The New Business Model: Variable Dividends & Capital Discipline (2021–Present)

The quarterly earnings call in February 2021 sounded different from any Devon had conducted in its 50-year history. Rick Muncrief didn't lead with production growth figures or drilling statistics. Instead, he opened with cash returns: "We generated $500 million in free cash flow this quarter and we're returning 50% of it to shareholders through our variable dividend." Wall Street analysts, accustomed to E&P companies hoarding cash for drilling programs, were stunned. Devon was actually doing what it promised—prioritizing shareholders over growth.

The variable dividend framework, initially met with skepticism, began proving its elegance through commodity cycles. When oil prices surged above $100 per barrel in 2022 following Russia's invasion of Ukraine, Devon's quarterly variable dividend reached $1.55 per share—an annualized yield exceeding 12%. When prices moderated to $75 in 2023, the dividend automatically adjusted to $0.70 without any board meetings or investor drama. The mechanism was working exactly as designed.

But capital discipline meant more than just dividends. Devon implemented what Muncrief called "maintenance mode" capital allocation. The company would only drill enough wells to maintain flat production—about 250-300 wells annually. Every dollar of capital above that threshold had to compete against returning cash to shareholders. In practice, this meant Devon left hundreds of prime drilling locations undeveloped even when oil prices exceeded $90 per barrel—heresy in the traditional E&P playbook.

The operational philosophy evolved to match the financial model. Devon organized its Delaware Basin development into what it called "Wolfcamp Weapons"—standardized drilling and completion designs that could be replicated across hundreds of wells. A Wolfcamp well in Lea County, New Mexico, used the same casing design, fracturing recipe, and production equipment as one in Reeves County, Texas, 100 miles away. This manufacturing approach drove costs down to $550 per lateral foot, among the lowest in the industry.

Technology adoption accelerated under the new model. Devon deployed automated drilling rigs that could operate with minimal human intervention, reducing safety incidents and improving consistency. Fracturing operations used real-time microseismic monitoring to optimize stage placement and proppant volumes. Production operations implemented edge computing and IoT sensors to detect and respond to issues before they impacted output. The company that had pioneered shale drilling was now pioneering shale digitization.

The discipline extended to M&A activity. In October 2022, Devon announced the $5 billion acquisition of Grayson Mill Energy's Williston Basin assets, adding 165,000 net acres in the Bakken formation. The market initially punished the stock, viewing it as a return to the old empire-building ways. But the details revealed the discipline: Devon would fund the acquisition entirely from cash flow, maintain its dividend framework, and divest non-core Williston acreage to focus on the best rock.

The Grayson Mill integration showcased the new Devon's operational excellence. Within six months, Devon had reduced Bakken well costs by 15% while increasing initial production rates by 20%. The company applied its Delaware Basin learnings—longer laterals, more fracturing stages, better proppant placement—to rejuvenate a basin many considered mature. The Williston assets, initially producing 80,000 barrels per day, were optimized to 100,000 barrels per day without increasing the rig count.

In November 2023, Devon struck again with the $1.8 billion acquisition of Validus Energy's Eagle Ford assets. This wasn't about entering a new basin—Devon already had an Eagle Ford position—but about achieving critical mass for development efficiency. The combined 65,000 net acres could support multi-well pad drilling that reduced costs by 20% compared to single-well programs.

The succession from Dave Hager to Rick Muncrief and then to Clay Gaspar in 2024 demonstrated organizational depth. Gaspar, elevated from Chief Operating Officer to CEO, represented continuity rather than change. An engineer who'd spent his entire career in unconventionals, Gaspar spoke the language of capital efficiency and shareholder returns fluently. His first act as CEO was to reaffirm the variable dividend framework and announce a $2 billion share buyback authorization.

The financial results validated the model. In 2023, Devon generated $3.8 billion in free cash flow on $17 billion in revenue—a 22% free cash flow margin that rivaled technology companies. The company returned $2.8 billion to shareholders through dividends and buybacks while reducing gross debt to $6.2 billion. Return on capital employed exceeded 25%, placing Devon in the top quartile of S&P 500 companies, not just energy peers.

But challenges emerged. Investor fatigue with energy stocks, despite strong cash returns, kept valuations depressed. Devon traded at just 4-5 times free cash flow, implying the market expected either permanent multiple compression or imminent collapse in oil prices. ESG pressures intensified, with some institutional investors excluding all fossil fuel companies regardless of financial performance. The variable dividend, while successful, created quarterly volatility that some income-focused investors couldn't tolerate.

The "shale 3.0" playbook that Devon pioneered—capital discipline, variable returns, manufacturing-mode development—was being copied across the industry. EOG Resources, Pioneer Natural Resources (before its Exxon acquisition), and ConocoPhillips all adopted similar frameworks. Devon's first-mover advantage was eroding as the entire sector converged on the same model.

By 2024, Devon had transformed from a growth-at-any-cost driller into something unprecedented in energy history: a mature, cash-generative manufacturer of hydrocarbons. The company that had helped launch the shale revolution was now showing how shale companies could generate consistent returns through commodity cycles. The question was whether this model represented the final evolution of independent E&P companies or merely another waystation in the industry's constant transformation.

IX. Playbook: Lessons in Energy & Capital Allocation

The Devon story, stripped to its essence, is about timing—not just being early, but being contrarian at precisely the right moment. When John and Larry Nichols bought natural gas assets in the 1970s, gas was trading at regulated prices under $2 per MCF. When Devon acquired Mitchell Energy in 2002, the Barnett Shale had been losing money for 20 years. When the company pivoted to oil in 2010, gas prices were collapsing from oversupply. Each move looked questionable at the time but brilliant in retrospect.

The pattern reveals a deeper insight: in cyclical commodities, the best assets are usually available when nobody wants them. Devon's greatest acquisitions—Mitchell Energy, GeoSouthern, WPX—all occurred during periods of distress when sellers needed liquidity and buyers had fled the market. This contrarian timing wasn't luck; it was discipline. Larry Nichols and his successors maintained strong balance sheets during booms specifically to have capital available during busts.

But timing alone doesn't explain Devon's success. The company exhibited a rare combination of technical innovation and fast-follower advantage. Devon didn't invent horizontal drilling (that was done in the Austin Chalk in the 1990s) or hydraulic fracturing (Halliburton developed it in the 1940s). But Devon was the first to combine these technologies at scale in shale formations. Similarly, Devon didn't create the variable dividend concept, but it was the first E&P company to implement it systematically.

This fast-follower approach extended to technology adoption. Devon let service companies like Schlumberger and Halliburton develop new tools, then became their first major customer. When other operators proved new techniques—like zipper fracking or extreme limited-entry completions—Devon would quickly adopt and scale them. The company spent enough on R&D to stay current but not so much as to subsidize the industry's learning curve.

The roll-up economics that defined Devon's growth from 1990-2010 offer a masterclass in value creation through consolidation. The formula was consistent: acquire subscale operators with good assets but operational challenges, apply Devon's technical expertise and capital access, achieve cost synergies through scale, then redeploy cash flow into the next acquisition. The cumulative effect was powerful—Devon created over $30 billion in equity value through acquisitions while spending roughly $25 billion on purchases.

The variable dividend innovation deserves special attention as a solution to the E&P industry's perpetual challenge: how to maintain financial flexibility through commodity cycles while providing attractive returns to shareholders. Traditional fixed dividends forced companies to cut payouts during downturns, destroying investor confidence. Pure buyback strategies provided flexibility but no current income. Devon's fixed-plus-variable framework elegantly solved both problems.

The cultural evolution from wildcatters to corporate to entrepreneurial tracks broader industry trends. The first generation (John Nichols) were classic wildcatters—intuitive, relationship-driven, comfortable with enormous risk. The second generation (Larry Nichols) professionalized the business—adding systems, processes, and financial sophistication. The third generation (Hager, Muncrief, Gaspar) combined entrepreneurial agility with corporate discipline, creating what might be called "institutional entrepreneurs."

Capital discipline in a boom-bust industry requires almost superhuman organizational restraint. When oil prices exceed $100 per barrel, every instinct pushes toward growth—drill more wells, acquire more acreage, build more infrastructure. Devon's ability to maintain flat production and return excess cash to shareholders during the 2022 price spike demonstrated rare organizational maturity. The key was aligning management compensation with returns on capital rather than production growth.

The management of commodity cycles reveals another pattern: successful energy companies don't predict prices, they prepare for volatility. Devon's stress-testing at $40 oil, maintaining debt below 2x EBITDA, and keeping 40% of production unhedged provided flexibility to survive downturns and capitalize on upturns. The company's 50-year survival through at least seven major oil price cycles proves the strategy's durability.

The lesson about culture mattering extends beyond corporate platitudes. Devon's Oklahoma City headquarters, physically distant from Houston's energy establishment, fostered independent thinking. The company's promotion from within—Clay Gaspar was the 12th consecutive internal CEO appointment—created institutional memory and organizational loyalty. The willingness to maintain field offices in Midland, Calgary, and Oklahoma City rather than centralizing everything demonstrated respect for local expertise.

The technology adoption pattern—fast follower rather than pioneer—suggests a broader principle about innovation in capital-intensive industries. The first mover bears the cost of failure; the fast follower captures most of the value. Devon let George Mitchell spend 20 years proving the Barnett could work, then scaled his innovation across America. This approach required humility (acknowledging others' innovations) and agility (moving quickly once concepts were proven).

The ultimate lesson from Devon's playbook might be about corporate evolution. Very few companies successfully transform themselves multiple times—from wildcatter to acquirer to technology leader to capital allocator. Each transformation required different skills, metrics, and culture. Devon's ability to evolve while maintaining continuity (the Nichols family still owns significant stock) represents a rare achievement in corporate adaptation. The playbook isn't just about energy; it's about how organizations can repeatedly reinvent themselves while honoring their history.

X. Bear vs. Bull Case & Competitive Analysis

The Bull Case: Devon represents the apex predator of Shale 3.0—a company that has shed its empire-building past to become a ruthlessly efficient hydrocarbon manufacturer. Bulls point to the company's premier acreage position in the Delaware Basin, where 400,000 net acres in the core of the play provide 10+ years of drilling inventory at current activity levels. These aren't marginal locations; Devon's average Delaware well generates 30%+ returns at $60 oil, creating a wide margin of safety.

The financial framework is equally compelling. Devon's variable dividend policy has proven its worth through multiple cycles, automatically adjusting payouts without drama or credit stress. The company generates 20%+ free cash flow yields at $75 oil—valuation metrics typically associated with declining businesses, not one with a decade of visible production. With debt-to-EBITDA below 1.0x and $2 billion in liquidity, Devon has the balance sheet strength to weather any conceivable downturn.

Execution consistency adds another layer of confidence. Devon has beaten quarterly production guidance for 12 consecutive quarters while reducing per-unit costs each year. Well productivity continues improving through technical innovation—2024 wells produce 15% more oil than 2022 wells despite being drilled in similar geology. This operational excellence translates directly to capital efficiency, with Devon generating the highest returns on capital employed among large-cap E&P companies.

The consolidation opportunity provides additional upside. With over 100 small E&P companies struggling to access capital, Devon can acquire assets at distressed valuations, apply its operational expertise, and generate immediate synergies. The Grayson Mill and Validus acquisitions proved this playbook still works. As the industry consolidates toward 10-15 major players, Devon's scale, technical expertise, and capital access position it as a natural acquirer.

The Bear Case: Critics see Devon as a melting ice cube dressed up with financial engineering. The fundamental bear argument rests on decline curves—shale wells decline 70% in their first year, forcing companies onto a treadmill of constant drilling just to maintain production. Devon must spend $2.5-3 billion annually to keep production flat. This capital intensity means the company is really just converting depleting assets into dividends, not creating long-term value.

The commodity exposure creates unavoidable volatility. Despite hedging programs and capital discipline, Devon's cash flow swings wildly with oil prices. A return to $40 oil—entirely possible in a recession—would eliminate free cash flow and force dividend cuts. The variable dividend framework, while theoretically sound, simply institutionalizes this volatility rather than solving it.

ESG pressures pose an existential threat that no amount of operational excellence can address. Major institutional investors are excluding fossil fuel companies from portfolios regardless of financial performance. European pension funds, sovereign wealth funds, and increasingly U.S. institutions are implementing blanket divestment policies. This shrinking investor base creates permanent multiple compression—Devon trades at 5x free cash flow while consumer staples companies trade at 20x despite lower growth and returns.

The peak shale thesis suggests Devon's best days are behind it. The core of the Delaware Basin has been largely delineated and drilled. While Devon has thousands of remaining locations, the best rock has been developed. Future wells will inevitably deliver lower returns as the company moves toward tier-2 and tier-3 acreage. The manufacturing-mode drilling that enabled recent efficiency gains has reached diminishing returns—you can only drill wells so fast or fracture rock so intensively.

Competitive Positioning: Against peers, Devon occupies an interesting middle ground. EOG Resources, the acknowledged operational leader, generates slightly higher well productivity but at higher costs. ConocoPhillips offers more international diversification and downstream integration but lower capital efficiency. Diamondback Energy, Devon's closest Delaware Basin peer, achieves similar well results but lacks Devon's scale advantages.

The recent consolidation wave has reshuffled competitive dynamics. ExxonMobil's $60 billion acquisition of Pioneer Natural Resources created a Permian behemoth that could outspend and out-tech smaller players. Chevron's purchase of PDC Energy and Hess signals the majors are serious about unconventionals. Occidental's acquisition of CrownRock continues the trend. In this consolidating landscape, Devon must decide whether to be predator or prey.

The technology race adds another competitive dimension. EOG's proprietary completion designs, Pioneer's (now Exxon's) data analytics platform, and ConocoPhillips's low-carbon initiatives all represent different bets on competitive advantage. Devon's approach—fast following rather than pioneering—may become a liability if transformative technologies emerge that require first-mover investment.

The Energy Transition Question: Can Devon evolve beyond hydrocarbons? The company has made token investments in carbon capture and renewable natural gas but nothing approaching a real energy transition strategy. Management's position—that oil and gas will remain essential for decades—may be correct but doesn't address the valuation discount imposed by ESG-focused investors.

Some bears argue Devon should liquidate—stop drilling, harvest existing production, and return 100% of cash flow to shareholders. Under this scenario, the company could distribute $30-40 per share over 8-10 years, well above the current $40 stock price. But management shows no inclination toward liquidation, believing the business can generate attractive returns indefinitely.

Valuation Framework: Traditional E&P valuation metrics—EV/EBITDA, price-to-book, PEG ratios—fail to capture Devon's transformation. The company should be valued on free cash flow yield and return on capital employed, metrics that highlight its manufacturing-like characteristics. At current strip prices, Devon trades at 8x free cash flow versus 15-20x for industrial companies with similar capital intensity and returns. This discount reflects either massive market inefficiency or an implicit assumption that oil prices will collapse permanently.

XI. Epilogue: What Would We Do?

Standing at Devon's 50-year mark, the strategic choices facing Clay Gaspar and his team echo those that confronted Larry Nichols in 2010 or Rick Muncrief in 2020: how to position for the next decade when the only certainty is change. The energy landscape of 2034 will likely be as different from today as today is from 2014, when oil traded above $100 and shale was still called "unconventional."

The Next Decade: Consolidation Endgame or Reinvention? The independent E&P sector stands at a crossroads. One path leads toward further consolidation into 5-10 super-independents, each with sufficient scale to compete with the majors on technology and capital access. The other path involves transformation beyond traditional E&P—perhaps into energy infrastructure, carbon management, or even electricity generation. Devon's choice will define its next chapter.

The consolidation endgame seems most probable. Devon could merge with another large independent—perhaps Diamondback to dominate the Delaware, or Marathon to diversify into the Bakken and Eagle Ford. A merger of equals creating a $70-80 billion enterprise would achieve massive synergies while maintaining operational focus. Alternatively, Devon could become the consolidator, rolling up smaller players at distressed valuations during the next downturn.

Technology Frontiers: The next wave of innovation won't come from drilling or fracturing—those technologies are approaching theoretical limits. Instead, artificial intelligence promises to revolutionize how companies find, develop, and produce hydrocarbons. AI-powered reservoir modeling could identify bypassed pay zones in mature fields. Machine learning algorithms could optimize production in real-time across thousands of wells. Automated drilling rigs could reduce well costs by another 30-40%.

Carbon capture and storage represents another frontier. Devon's depleted reservoirs could become carbon storage sites, generating credits worth $50-100 per ton. The infrastructure Devon built to produce hydrocarbons—wells, pipelines, processing plants—could be reversed to sequester CO2. This wouldn't replace oil and gas revenue but could provide a sustainable cash flow stream as production naturally declines.

Enhanced oil recovery techniques using CO2, chemicals, or microbiology could unlock another 10-20% of original oil in place from Devon's mature fields. The Permian Basin alone contains 100+ billion barrels of residual oil that conventional techniques can't extract. If Devon could recover even 5% of this resource economically, it would double the company's reserves.

Capital Allocation Priorities: The tension between growth, dividends, and buybacks will intensify as Devon's core inventory depletes. Our view: Devon should accelerate shareholder returns while it can. The company should target returning 75% of free cash flow through dividends and buybacks, up from the current 50%. Growth capital should be limited to the absolute best projects—those generating 50%+ returns at conservative price assumptions.

The variable dividend framework should evolve to include a larger fixed component as production matures and becomes more predictable. A $1 per share quarterly fixed dividend (versus $0.20 currently) with a smaller variable component would appeal to income investors while maintaining flexibility. This would position Devon more like a utility—steady, predictable, boring—which might actually expand the investor base.

Share buybacks should accelerate when the stock trades below 6x free cash flow. At current valuations, every share retired is massively accretive to remaining shareholders. Devon could reduce its share count by 50% over five years while maintaining the dividend—creating enormous per-share value even with flat production.

The Succession Question: Clay Gaspar, at 52, could lead Devon for another decade, but the company needs to develop the next generation of leadership. The industry's talent crisis—young professionals aren't entering petroleum engineering—means Devon must compete fiercely for technical expertise. The company should consider recruiting leaders from adjacent industries—technology, manufacturing, finance—who can bring fresh perspectives.

The board composition needs evolution too. Devon's board remains dominated by industry veterans who made their careers during the growth era. Adding directors with technology, ESG, and capital markets expertise would provide valuable perspective for navigating the energy transition. A board that combines industry knowledge with outside insight could help Devon avoid the insularity that doomed previous energy giants.

Final Reflections: Devon's 50-year journey from a two-person startup to a $40 billion enterprise mirrors America's energy evolution. The company that began buying conventional gas wells in Oklahoma helped unlock unconventional resources that transformed global energy markets. Along the way, Devon pioneered technologies, financial innovations, and business models that redefined what an energy company could be.

The next 50 years—if there are another 50 years for hydrocarbon companies—will require similar adaptation. The energy transition isn't a distant threat; it's a current reality that's already reshaping capital allocation, government policy, and social acceptance of fossil fuels. Devon must navigate this transition while generating returns for shareholders who've suffered through a decade of underperformance.

What would we do? Accept reality: Devon is a mature company in a mature industry producing a commodity that, while essential today, faces long-term decline. Maximize cash extraction while the assets retain value. Return substantially all free cash flow to shareholders. Resist the temptation to diversify into renewable energy or other industries where Devon has no competitive advantage. Run the business for cash, not growth.

But also prepare for surprises. Energy transitions take longer than expected—coal still generates 20% of global electricity 50 years after its "inevitable" decline began. Oil demand could surprise to the upside from Indian and African growth. Carbon capture could transform Devon's liabilities into assets. AI could unlock resources nobody imagines today.

The ultimate lesson from Devon's history is that energy is never just about energy—it's about human ingenuity, economic development, and societal needs. The company that John and Larry Nichols founded with $6,000 helped America achieve energy independence, created thousands of jobs, and generated hundreds of billions in economic value. Whatever comes next, that legacy is secure.

XII. Recent News**

Q3 2024 Earnings and Production Updates**

Devon reported record Q3 2024 production of 728,000 barrels of oil equivalent per day, including 335,000 barrels of oil per day. The company generated $786 million in free cash flow during the third quarter. Core earnings reached $683 million, or $1.10 per share, with EBITDA of $1.9 billion.

For the quarter ended September 2024, Devon posted revenues of $4.02 billion, surpassing consensus estimates by 7.20%. Looking ahead to 2025, Devon forecasts production of around 800,000 BOEs per day, with oil volumes averaging around 380,000 barrels per day, and capital spending expected between $4 and $4.2 billion.

The company elected not to pay a variable dividend in Q3, focusing instead on fixed dividends and share repurchases. Devon maintained a strong balance sheet with a net debt to EBITDA ratio of just over one times.

Recent Acquisition Activity

In July 2024, Devon announced a definitive agreement to acquire the Williston Basin business of Grayson Mill Energy for $5 billion, consisting of $3.25 billion in cash and $1.75 billion in stock. The acquisition was completed in September 2024.

The transaction transformed Devon's Williston Basin business, adding 307,000 net acres, 500 undrilled gross locations and 300 high-quality refrac candidates. Due to the accretive nature of this transaction, Devon's board expanded its share-repurchase authorization by 67 percent to $5 billion through mid-year 2026.

In February 2025, incoming CEO Clay Gaspar indicated Devon would prioritize organic growth over acquisitions, stating his team's main focus "is just making Devon a heck-of-a-lot-better Devon".

Commodity Price Impacts

As of August 22, 2025, crude oil rose to $63.77 USD/Bbl. The EIA forecasts Brent crude oil prices to decline from $71 per barrel in July to $58/b in Q4 2025 and around $50/b in early 2026, with the forecast average of $51/b for 2026.

The price decline is driven largely by expectations of more oil inventory builds following OPEC+ members' decision to accelerate production increases, with global oil inventory builds expected to average more than 2 million barrels per day in Q4 2025 and Q1 2026.

The White House has indicated a strong preference for reducing crude prices to $50/bbl or lower, though analysts don't anticipate intervention unless crude falls below $50 WTI, where shale production starts to decline.

Regulatory and Policy Developments

In July 2024, Devon published its 2023 ESG performance report, with CEO Rick Muncrief noting pride in the company's environmental, social and governance accomplishments. In 2022, Devon set its first standalone emissions reduction goal in response to stakeholder requests to tie compensation directly to environmental targets.

In 2023 and early 2024, Devon made strategic investments totaling $100 million in Fervo Energy, a leader in next-generation geothermal technology. A major 2023 accomplishment was implementing an internally developed carbon accounting platform that improves emissions data precision and reporting methodologies, better preparing Devon for advanced emissions modeling and evolving regulatory disclosure programs.

Devon took an active role with federal trade associations to respond to proposed EPA methane rules, while also engaging independently with EPA personnel on technical issues, with advocacy around methane regulations continuing in 2024 in parallel with operational efforts to achieve meaningful reductions in methane emissions.

As of June 2024, Devon's board included four women (36%) and one racially diverse (9%) director, demonstrating the company's commitment to board diversity and governance best practices.

XIII. Links & Resources

Company Investor Presentations - Devon Energy Investor Relations: investors.devonenergy.com - Quarterly Earnings Materials: investors.devonenergy.com/investors/quarterly-results - 2024 Sustainability Report: devonenergy.com/sustainability - Corporate Governance Documents: devonenergy.com/sustainability/governance

Industry Reports and Analysis - U.S. Energy Information Administration Short-Term Energy Outlook: eia.gov/outlooks/steo - American Exploration & Production Council: axpc.us - International Energy Agency Reports: iea.org - CME Group Energy Markets: cmegroup.com/markets/energy

Books on Shale Revolution and Energy Markets - "The Frackers" by Gregory Zuckerman - "The Quest" by Daniel Yergin - "Crude Volatility" by Robert McNally - "Saudi America" by Bethany McLean

Relevant SEC Filings and Transcripts - Devon Energy SEC Filings: sec.gov/edgar/browse/?CIK=1090012 - Annual Reports (10-K) and Quarterly Reports (10-Q) - Proxy Statements (DEF 14A) - Current Reports (8-K)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube