Darden Restaurants: The Full-Service Dining Empire

I. Introduction & Episode Overview

Picture this: It's a Thursday evening in suburban America. Families stream into an Olive Garden, greeted by the familiar aroma of garlic breadsticks. Down the street, business executives seal deals over ribeyes at Capital Grille. Meanwhile, a couple celebrates their anniversary at Eddie V's, savoring oysters flown in that morning. These aren't random restaurants—they're all pieces of a $12 billion empire that most Americans interact with but few truly understand.

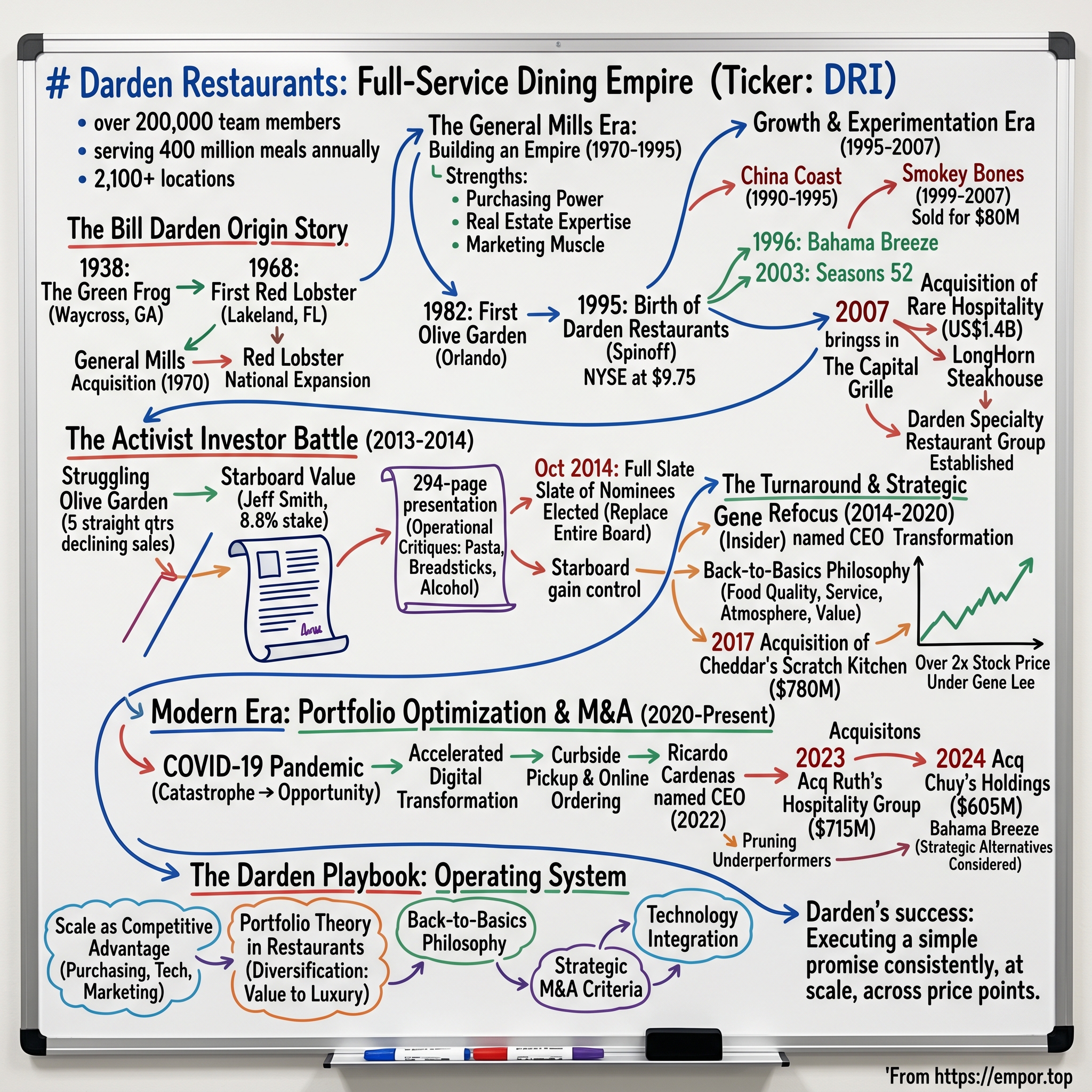

Welcome to Darden Restaurants, the world's largest full-service restaurant company. With over 200,000 team members serving 400 million meals annually across 2,100+ locations, Darden has mastered something that seems almost impossible in the notoriously difficult restaurant business: consistent, profitable growth at massive scale. Think about that for a moment—when 60% of restaurants fail within their first year and 80% don't make it past five years, Darden has built a portfolio of chains that have thrived for decades.

But here's the fascinating question: How did a General Mills spinoff—yes, the cereal company—become the most successful operator of casual dining chains in America? The answer isn't just about good food or clever marketing. It's a story of operational excellence, strategic portfolio management, and understanding a fundamental truth about American dining culture that others missed.

This journey takes us from Bill Darden's first diner in Depression-era Georgia to today's sophisticated restaurant conglomerate that generates over $1 billion in annual profit. Along the way, we'll explore the strategic brilliance of bringing affordable seafood to landlocked America, witness one of the most dramatic activist investor battles in corporate history (complete with a 294-page presentation about breadsticks), and understand how a company written off as a relic of suburban sprawl engineered one of the great turnarounds in restaurant history.

Three themes will emerge throughout this story. First, the extraordinary power of scale in an industry where most operators stay small. Second, the delicate balance between standardization and brand differentiation—how do you run Olive Garden and Capital Grille under the same roof? And third, the portfolio approach to restaurants, where diversification isn't just about risk management but about capturing different occasions, demographics, and price points in American dining.

II. The Bill Darden Origin Story & Red Lobster Foundation

The year was 1938. America was still clawing its way out of the Great Depression when a 19-year-old named William "Bill" Darden scraped together $1,500—a fortune at the time—to open a 25-seat luncheonette called The Green Frog in Waycross, Georgia. The name came from the building's previous life as a nightclub, but young Bill saw opportunity where others saw a failed business. He served simple fare—burgers, fries, milkshakes—but with an obsessive attention to quality and service that would define his entire career.

Darden wasn't content with one restaurant. By the 1960s, he'd built a small empire of family restaurants across the Southeast, but he saw something others didn't: Americans were becoming more adventurous eaters. Travel was democratizing taste. The interstate highway system was connecting communities. And here was his radical insight—people in landlocked states craved seafood just as much as coastal dwellers, but had no access to it.

In 1968, at age 49, Bill Darden opened the first Red Lobster in Lakeland, Florida. The location choice was deliberate and brilliant—Lakeland sat dead center in Florida, about as far from the ocean as you could get in the Sunshine State. If he could make a seafood restaurant work there, he reasoned, he could make it work anywhere in America. The restaurant featured something revolutionary: fresh seafood flown in daily, served at prices middle-class families could afford, in an atmosphere that felt special but not intimidating. The response was electric. Within days, that first Red Lobster in Lakeland became a near-instant success, with lines of diners eager to try something they'd never experienced—quality seafood at reasonable prices. Lobster was considered exotic at the time, and the restaurant had a mystique about it—dark, fancy, creating an atmosphere that made middle America feel sophisticated without intimidation.

The numbers tell the story: By 1970, just two years after opening, Red Lobster had expanded to three locations in Florida with two more under construction. But Darden faced a classic entrepreneur's dilemma. The concept was proven, the demand was obvious, but expansion required capital he didn't have. In a decision that would shape the entire casual dining industry, Red Lobster was acquired by General Mills in 1970, giving the chain the backing to expand across the country—growing to almost 400 restaurants by 1985.

Bill Darden stayed on as company manager, watching his vision spread across America until his death in 1994 at age 75. But his legacy wasn't just Red Lobster—it was proving that Americans everywhere, not just in coastal cities, would pay for quality dining experiences. He'd created not just a restaurant but a new category: affordable casual dining with a specific culinary focus. That blueprint would be copied thousands of times over the next five decades.

III. The General Mills Era: Building an Empire (1970–1995)

General Mills in 1970 wasn't the focused CPG company we know today. This was the era of conglomerate thinking, when food companies believed they could leverage their operational expertise across multiple categories. For General Mills, acquiring Red Lobster wasn't about seafood—it was about applying industrial-scale management to the fragmented restaurant industry.

The transformation was immediate and profound. General Mills brought three superpowers to Red Lobster that no independent operator could match. First, purchasing power: suddenly Red Lobster could negotiate seafood contracts at national scale, driving down costs while maintaining quality. Second, real estate expertise: General Mills had the capital and knowledge to identify prime locations and negotiate favorable leases. Third, marketing muscle: national advertising campaigns made Red Lobster a household name from coast to coast.

But the real genius move came in 1982. General Mills opened the first Olive Garden in Orlando, and by 1989 had expanded to over 145 restaurants, making it the fastest-growing unit in the company's restaurant holdings. The insight was brilliant: apply the Red Lobster playbook—affordable, approachable versions of "exotic" cuisine—to Italian food. While Olive Garden didn't win critical acclaim, it was wildly popular, with per-restaurant sales soon matching Red Lobster's, eventually becoming the largest chain of Italian-themed full-service restaurants in the United States.

Not every experiment worked. In 1990, General Mills launched China Coast, attempting to create a national casual dining chain featuring American Chinese cuisine. The chain expanded to 50 restaurants but lost an estimated $20 million before shuttering by the end of 1995. The failure taught valuable lessons: not every cuisine translated to the casual dining model, and operational excellence couldn't overcome a flawed concept.

By the mid-1990s, General Mills faced pressure from Wall Street to focus on its core packaged goods business. Running restaurants required different skills than selling cereal. The capital requirements were enormous, the labor issues complex, and the business cyclical in ways that frustrated investors accustomed to the steady growth of consumer staples. The solution? Spin off the restaurant division and let it sink or swim on its own. The restaurants had grown too large to kill but had become too distracting to keep.

IV. The 1995 Spinoff: Birth of Darden Restaurants

May 9, 1995 marked a watershed moment in casual dining history. Darden Restaurants was spun off from General Mills beginning on May 9, 1995, when it began trading on the when-issued basis at $9.75 a share. The company became a fully separate entity on May 31, 1995, when its shares went on sale on the NYSE. The spinoff wasn't just a financial transaction—it was a cultural declaration of independence.

The naming itself carried deep symbolism. Joe Lee, who had managed the first Red Lobster in Lakeland and risen to become president, chose to honor his mentor. In a tribute to Red Lobster founder William Darden, General Mills Restaurant Group will become Darden Restaurants Inc. when it spins off from General Mills Co. in May. President Joe Lee said the name was the "emotional favorite" among 500 considered. The announcement came on the one-year anniversary of Bill Darden's death, adding poignancy to the moment.

But Wall Street's reaction was brutal. Investors failed to rally around Darden Restaurants, whose stock ended its first day of trading on the New York Stock Exchange below the $12 to $13 a share expected by analysts. One securities analyst said that the restaurants had been accounting for only one-quarter of General Mills' operating profits while absorbing half of the company's capital spending for expansion and renovation. The market saw restaurants as capital-intensive, cyclical businesses with thin margins—everything that packaged goods weren't.

Yet Darden's executives saw opportunity where investors saw risk. Casual dining, according to the company, was the fastest-growing segment of the full-service restaurant market, with sales increasing at more than twice the overall market's rate since 1988 and representing, in 1995, 32 percent of full-service restaurant sales, or $29 billion. The trend toward casual dining, it argued, was reflected in the less formal dress code in the workplace and would continue in years to come. Moreover, the company noted that 40- to 60-year-olds were the most frequent visitors to casual dining restaurants, and that the population aged 45 and older was expected to grow by 40 million through 2010.

The new company was massive from day one. At the end of fiscal 1995, Darden Restaurants was operating 1,250 restaurants in every state except Alaska. A total of 73 were in Canada. It instantly became the world's largest full-service restaurant company, a position it would never relinquish. But size alone wouldn't guarantee success—Darden needed new concepts to drive growth beyond Red Lobster and Olive Garden.

V. The Growth & Experimentation Era (1995–2007)

The freedom from General Mills unleashed an explosion of experimentation at Darden. In March 1996, just months after independence, the company launched Bahama Breeze Caribbean Grille in Orlando, featuring food and drinks from the Caribbean islands. The concept represented a bold bet: Americans were ready for more adventurous ethnic cuisines beyond Italian and seafood. By the early 2000s, Bahama Breeze had expanded to 21 locations, riding the wave of casual dining's golden age.

But Darden's most ambitious experiment came in late 1999 with Smokey Bones BBQ Sports Bar. The restaurant featured barbecue and related foodstuffs in an Appalachian mountain-lodge setting, targeting the sports bar demographic that chains like Buffalo Wild Wings were capturing. Darden opened the first location at a former Red Lobster site near its Orlando headquarters—a symbolic passing of the torch from old to new. By 2007, Smokey Bones had mushroomed to 129 locations.

Markets were oversaturated with restaurants in 1997, forcing Darden to close 48 poorly performing locations and lose $91 million due to the restructuring. This brutal awakening taught Darden a critical lesson: growth for growth's sake was a recipe for disaster. The company pivoted to a more disciplined approach, focusing on same-store sales growth and operational excellence rather than pure expansion.

In 2003, Seasons 52 was under development with the idea of "provide guests the opportunity to indulge while still eating well." This concept represented Darden's recognition of changing consumer preferences—health-conscious but unwilling to sacrifice flavor. With every item under 595 calories and a seasonally rotating menu, Seasons 52 was ahead of its time, anticipating the farm-to-table movement by years.

Yet not every experiment succeeded. Otis said, "We have concluded that it is not a meaningful growth vehicle for Darden. As a result, we've decided to exit the Smokey Bones business and offer it and the related assets for sale." In December 2007, Darden sold Smokey Bones to Barbeque Integrated Inc., a subsidiary of Sun Capital, for approximately $80 million—a fraction of what it had invested. The failure revealed a harsh truth: Darden's operational excellence couldn't overcome a flawed concept or saturated market.

The crown jewel acquisition came in August 2007. Darden acquired rival Atlanta-based restaurant holder Rare Hospitality for US$1.4 billion, gaining Rare's two chains, The Capital Grille and LongHorn Steakhouse. This wasn't just about adding restaurants—it was about portfolio theory applied to dining. LongHorn gave Darden a mid-priced steakhouse to compete with Outback and Texas Roadhouse. Capital Grille provided entry into fine dining, with average checks double those of Olive Garden. As part of the Rare acquisition, Darden set up its Specialty Restaurant Group to include Capital Grille, Bahama Breeze, and Seasons 52. Suddenly, Darden could capture every dining occasion from Tuesday night family dinner to Saturday night anniversary celebrations.

VI. The Activist Investor Battle & Transformation (2013–2014)

By 2013, Darden was stumbling. Same-store sales at Olive Garden had declined for five straight quarters. The company's stock languished at $45, barely above where it had traded a decade earlier. Management seemed paralyzed, caught between maintaining the status quo and acknowledging fundamental problems with their business model. Into this vacuum stepped one of the most formidable activist investors in America.

Starboard Value late Monday pressed ahead with its proxy contest to take control of Darden Restaurants' board despite the restaurant chain's offer of concessions and move to axe its CEO - Clarence Otis. Led by Jeff Smith, Starboard had quietly accumulated an 8.8% stake in Darden, making them the second-largest shareholder. But this wasn't going to be a typical activist campaign of demanding buybacks or board seats. Smith had something far more audacious in mind: complete control.

The opening salvo came in December 2013 when Darden announced plans to sell or spin off Red Lobster, citing pressure from investors. Starboard will tell Darden shareholders that because of the tax-inefficent way the deal was structured, Darden netted only $100 million from the sale of the Red Lobster business after taking into account $1.5 billion it believed could have been realized from the tax-efficient sale of real estate. Smith called the Red Lobster sale "value destructive," arguing management was giving away an iconic American brand for effectively nothing.

But the masterstroke came in September 2014. Starboard, which is the second-largest investor in Darden with a 8.8% stake, last month issued a very-detailed nearly 300-page slide presentation that gave details of a potential turnaround plan for Darden's Olive Garden chain, where it claimed customers had "fond memories, but where we believe execution has recently failed to live up to the brand image." Some of the top complaints focused on the company's all-you-can-eat breadsticks, which Darden said were too plentiful and lacked flavor, as well as low alcohol sales compared to rival casual-dining chains and salads that were overfilled and dressed with too much dressing.

The presentation became legendary on Wall Street. Page after page of granular operational critiques: Olive Garden wasn't salting its pasta water (to extend pot warranty periods). Breadsticks sat too long before serving. Servers didn't push alcohol sales. Tables weren't turned fast enough. It was simultaneously absurd and brilliant—an activist investor telling a restaurant company how to cook pasta. But the details proved Smith wasn't just a financial engineer; he understood the restaurant business at an operational level that embarrassed incumbent management.

The investor's strategy resonated with two of the world's largest proxy firms — Glass Lewis & Co. and Institutional Shareholder Services (ISS)–backed Starboard's full slate of nominees ahead of the meeting. The endorsements were devastating for Darden's board. When the votes were counted on October 10, 2014, the result was unprecedented: Darden Restaurants Inc., owner of the Olive Garden, lost a more than nine-month battle against Starboard Value LP, which persuaded investors to replace the company's entire board at its shareholder meeting today. Investors voted for the 12 directors at Darden's annual meeting in Orlando, Florida, where the company is based, according to a statement.

While owning less than 10% of the firm, Smith replaced the entire board and became Darden's chairman. By doing so, wrote Cohan, Smith "fired a shot over the bows of directors everywhere," informing them that shareholders were now in the ascendant, and "managers ignore them at their peril." According to Cohan, "the scope of Smith's triumph with Darden has left jaws hanging open across Wall Street and beyond. Only in a handful of times in the past few years has an activist managed to replace an entire board of directors, and never at a company the size of Darden."

VII. The Turnaround & Strategic Refocus (2014–2020)

The new board's first crucial decision would define Darden's future: who should lead the turnaround? In a move that surprised Wall Street, they turned to an insider—Gene Lee, a company veteran who had joined Darden in 2007 with the Rare Hospitality acquisition. Lee, who started his storied career as a busboy, was named CEO in February 2015. The choice signaled that Starboard believed Darden's problems weren't about strategy but execution.

Lee immediately implemented what he called the "Back-to-Basics Operating Philosophy." No more chasing trends or complicated menu innovations. Instead, focus relentlessly on four things: food quality, service, atmosphere, and value. The simplicity was radical in an industry obsessed with the next big thing. Make the restaurants run well. Simplify operations. Focus on takeout and what consumers want.

The transformation at Olive Garden was immediate and dramatic. Lee added online ordering, which led to a rise in its takeout business. He also added lower-calorie dishes to the menu and was credited with speeding up the lunch service. Tables were turned faster. Alcohol sales increased. Even the breadsticks improved—served warmer, with better seasoning. The eight-concept casual dining operator's stock price has more than doubled since Lee was given the permanent CEO title in February 2015, providing a story of consistent sales performance that almost defies explanation.

But the real genius was in portfolio management. Instead of treating all brands equally, Darden began managing each concept based on its specific market position and growth potential. Olive Garden and LongHorn received the bulk of capital investment, recognized as the growth engines. Capital Grille and Eddie V's were positioned as jewels to be polished, not expanded rapidly. Struggling concepts were fixed or divested without sentiment. Strategic acquisitions accelerated the turnaround. On March 27, 2017, Darden announced its intent to acquire Cheddar's Scratch Kitchen for $780 million from shareholders such as L Catterton and Oak Investment Partners. The acquisition was completed on April 24, 2017. Cheddar's, with 165 locations across 28 states and average annual restaurant volumes of $4.4 million, brought something Darden desperately needed: a value-oriented concept that could compete in the lower price tiers of casual dining. As Lee said, "Cheddar's is an undisputed casual dining value leader with broad appeal and strong average restaurant volumes."

The integration of Cheddar's demonstrated how much Darden had learned from past failures. Instead of forcing rapid changes, they took a measured approach—transitioning systems, training teams, maintaining the brand's scratch-cooking identity while leveraging Darden's scale advantages in purchasing and marketing. The patience paid off: Cheddar's would eventually become one of Darden's strongest performers.

After Starboard took over Darden, its stock went up by almost 60%. By 2020, During his tenure at Darden, he drove revenue growth of over $2 billion and nearly tripled market capitalization to $20 billion. The activist campaign that began with mockery of breadsticks had delivered one of the most successful turnarounds in restaurant history. What seemed like micromanagement—salting pasta water, timing breadstick service—turned out to be exactly what Darden needed: attention to operational details that directly impacted guest experience.

VIII. Modern Era: Portfolio Optimization & Strategic M&A (2020–Present)

The COVID-19 pandemic should have devastated Darden. In March 2020, Darden's stock price fell to $34.16 a share during the coronavirus pandemic. At the time, most restaurants in America had to shut down due to public-health restrictions enacted to control the spread of the coronavirus. Yet what could have been a catastrophe became an opportunity to accelerate digital transformation and operational improvements that might have taken years under normal circumstances.

During the pandemic, Darden streamlined its business with smaller menus and a pullback on marketing. It has also invested in technology and training to make its staff more productive. The crisis forced innovation: curbside pickup, enhanced delivery partnerships, ghost kitchens for off-premise orders. What started as emergency measures became permanent competitive advantages. By the time restaurants fully reopened, Darden had fundamentally transformed its operating model while competitors struggled to survive.

The recovery was spectacular. Ricardo Cardenas, who succeeded Gene Lee as CEO in May 2022 after rising from an hourly team member in 1984, continued the strategic playbook while adding his own touches. Under new leadership, Darden doubled down on what worked: operational excellence, strategic acquisitions, and portfolio optimization.

On May 3, 2023, Darden announced it was acquiring Ruth's Hospitality Group Inc. for $21.50 per share in an all-cash transaction, with an equity value of approximately $715 million. Ruth's Hospitality is the owner and operator of the Ruth's Chris Steak House chain. The acquisition was completed on June 14. Ruth's Chris, with 155 locations worldwide and average unit volumes of $6.2 million, filled a crucial gap in Darden's portfolio—a nationally recognized steakhouse brand with room to grow. The deals kept coming. In July 2024, Darden agreed to acquire Chuy's Holdings for $37.50 per share, in an all-cash transaction with an enterprise value of approximately $605 million. The acquisition was completed on October 11, 2024. Chuy's, with 101 restaurants in 15 states and average annual restaurant volumes of $4.5 million, gave Darden entry into the fast-growing Tex-Mex category—a glaring gap in their portfolio. As Cardenas said, "Based on our criteria for adding a brand to the Darden portfolio, we believe Chuy's is an excellent fit that supports our winning strategy."

The company said Thursday that adding the 155-unit steakhouse chain to its portfolio will unlock $35 million in run rate synergies and savings annually, which is $15 million more than Darden was initially expecting. This wasn't just about cost-cutting—it was about leveraging Darden's scale in purchasing, marketing, and technology across an increasingly diverse portfolio. The numbers tell a remarkable story of recovery and growth. Olive Garden reported $5.2 billion in sales for fiscal 2025, a 2.8% increase from the previous year, while LongHorn's sales grew by 7.8% to $3.03 billion. Overall, Darden achieved nearly $12.08 billion in sales with net earnings of $1.05 billion, highlighting the robust performance of its brands amid challenging economic conditions. For the full fiscal 2026, Darden gave a forecast for revenue growth of 7% to 8%, expecting adjusted earnings to be in a range of $10.50 to $10.70 per share.

But not every brand thrived equally. During the earnings call, the company also revealed it was looking at "strategic alternatives" for its 28-location Bahama Breeze chain. "Consequently, we will be considering strategic alternatives for Bahama Breeze, including a potential sale of the brand or converting restaurants to other Darden brands." The willingness to prune underperformers demonstrated that the activist-driven discipline remained embedded in Darden's DNA.

IX. Playbook: The Darden Operating System

What makes Darden work? After decades of evolution, crisis, and transformation, a clear operating playbook has emerged—one that turns the challenges of full-service dining into competitive advantages.

Scale as Competitive Advantage: With over 2,100 restaurants, Darden negotiates purchasing contracts that independent operators can only dream of. A single basis point improvement in food costs across the portfolio translates to millions in profit. But scale goes beyond purchasing—it's about shared services, technology platforms, and marketing efficiency. When Darden develops a new point-of-sale system or loyalty program, the cost is spread across thousands of locations.

Portfolio Theory in Restaurants: Darden isn't really in the restaurant business—it's in the portfolio management business. Each brand serves a specific purpose: Olive Garden for volume and cash generation, LongHorn for steady growth, Capital Grille for prestige and margins, Cheddar's for value positioning. This diversification isn't just about risk management; it's about capturing every dining occasion, price point, and demographic.

The "Back-to-Basics" Philosophy: Post-Starboard, Darden's operational philosophy can be summed up in four words: food, service, atmosphere, value. Every decision is filtered through this lens. Does a menu innovation improve food quality? Does a technology investment enhance service? The discipline to say no to complexity has been as important as the courage to say yes to opportunity.

Strategic M&A Criteria: Darden's acquisition strategy follows strict criteria: the brand must be differentiated, have proven unit economics, offer growth potential, and fit culturally. Ruth's Chris and Chuy's weren't just bought for their revenues—they filled specific gaps in the portfolio while bringing operational practices Darden could learn from and scale.

Real Estate Strategy: Unlike many competitors who lease everything, Darden owns a significant portion of its real estate. This provides stability, control over locations, and an asset base that can be leveraged for financing. The owned real estate also provides optionality—underperforming brands can be converted to stronger concepts without lease complications.

Technology Integration: From kitchen display systems that optimize cooking times to sophisticated labor management tools that match staffing to demand, technology at Darden isn't about being cutting-edge—it's about operational efficiency. The company was late to delivery partnerships but entered on its own terms, maintaining control over the customer relationship.

X. Analysis & Investment Case

The Bull Case rests on four pillars. First, unmatched scale advantages in a fragmented industry where most operators lack the resources to compete effectively. Second, proven turnaround ability—Darden has shown it can fix broken concepts and optimize performing ones. Third, a strategic portfolio that spans from value (Cheddar's at $15 per person) to luxury (Capital Grille at $75+), capturing wallet share across income levels. Fourth, strong cash flow generation supporting consistent dividend growth and opportunistic buybacks.

The financial metrics support the optimism. Operating margins consistently exceed industry averages by 200-300 basis points. Return on invested capital hovers around 15%, exceptional for a capital-intensive business. Same-store sales growth, while modest, has been positive and consistent—a feat in an industry plagued by volatility.

The Bear Case can't be ignored. Labor costs continue to rise, with many states pushing minimum wages toward $20/hour. The math is brutal: labor represents roughly 30% of sales, and every dollar increase in hourly wages cuts directly into margins. Changing consumer preferences pose another threat—younger diners gravitate toward fast-casual concepts that offer perceived better value and convenience. Darden's average customer skews older, raising questions about long-term relevance.

High exposure to discretionary spending makes Darden vulnerable to economic downturns. When budgets tighten, dining out is often the first expense cut. Integration risks from acquisitions remain real—Ruth's Chris and Chuy's must be successfully integrated without losing their unique identities that made them attractive in the first place.

Competitive Analysis reveals Darden's unique position. Versus Brinker (Chili's, Maggiano's), Darden has superior scale and operational discipline. Against Bloomin' Brands (Outback, Carrabba's), Darden's portfolio is more diverse and margins consistently higher. Independent operators simply can't match Darden's purchasing power or marketing reach. The real competition might be from outside traditional dining—meal kits, ghost kitchens, and grocery prepared foods all compete for the same stomach share.

XI. Epilogue & Future Vision

The evolution of full-service dining post-pandemic has accelerated trends that were already in motion. Off-premise dining, once an afterthought, now represents 20-30% of sales at many Darden concepts. The company that once resisted third-party delivery has embraced it strategically, using it to reach new customers while maintaining direct relationships through proprietary channels.

Technology's role continues to evolve. Darden is experimenting with automation in kitchens—not to replace workers but to handle repetitive tasks, freeing staff for guest interaction. Digital ordering, payment at table, and AI-driven scheduling are becoming standard. Yet the human element remains central—Darden understands that hospitality, not just food, drives loyalty in full-service dining.

Portfolio strategy going forward will likely focus on optimization over expansion. The days of launching new concepts from scratch appear over. Instead, expect strategic acquisitions of proven brands that fill portfolio gaps, continued pruning of underperformers, and investment in winner brands. The Bahama Breeze decision signals this discipline—sentiment won't save struggling brands.

What Darden's success says about American dining culture is profound. Despite predictions of full-service dining's demise, Americans still crave the experience of being served, of celebrating milestones over tablecloths, of escaping kitchen duties for an evening. Darden has proven that executing this simple promise—consistently, at scale, across price points—remains a powerful business model.

The key lessons for operators and investors are clear. First, operational excellence beats conceptual brilliance—better to run a good concept excellently than a great concept poorly. Second, scale matters more than ever in an industry with rising costs and complexity. Third, portfolio diversification provides resilience that single-concept operators lack. Fourth, listening to activists might be painful but can drive necessary change. Finally, in an industry obsessed with the new, there's tremendous value in making the familiar consistently excellent.

Darden's journey from Bill Darden's Green Frog to today's $12 billion empire isn't just a business success story. It's a reflection of how Americans eat, gather, and celebrate. Through boom and bust, changing tastes and economic cycles, the company has adapted while staying true to a simple principle: give people a place to connect over good food at fair prices. In a world of algorithmic everything, that human need remains remarkably constant. And remarkably profitable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube