DiamondRock Hospitality: The REIT That Bet on Premium Locations and Survived Every Crisis

I. Introduction & Episode Roadmap

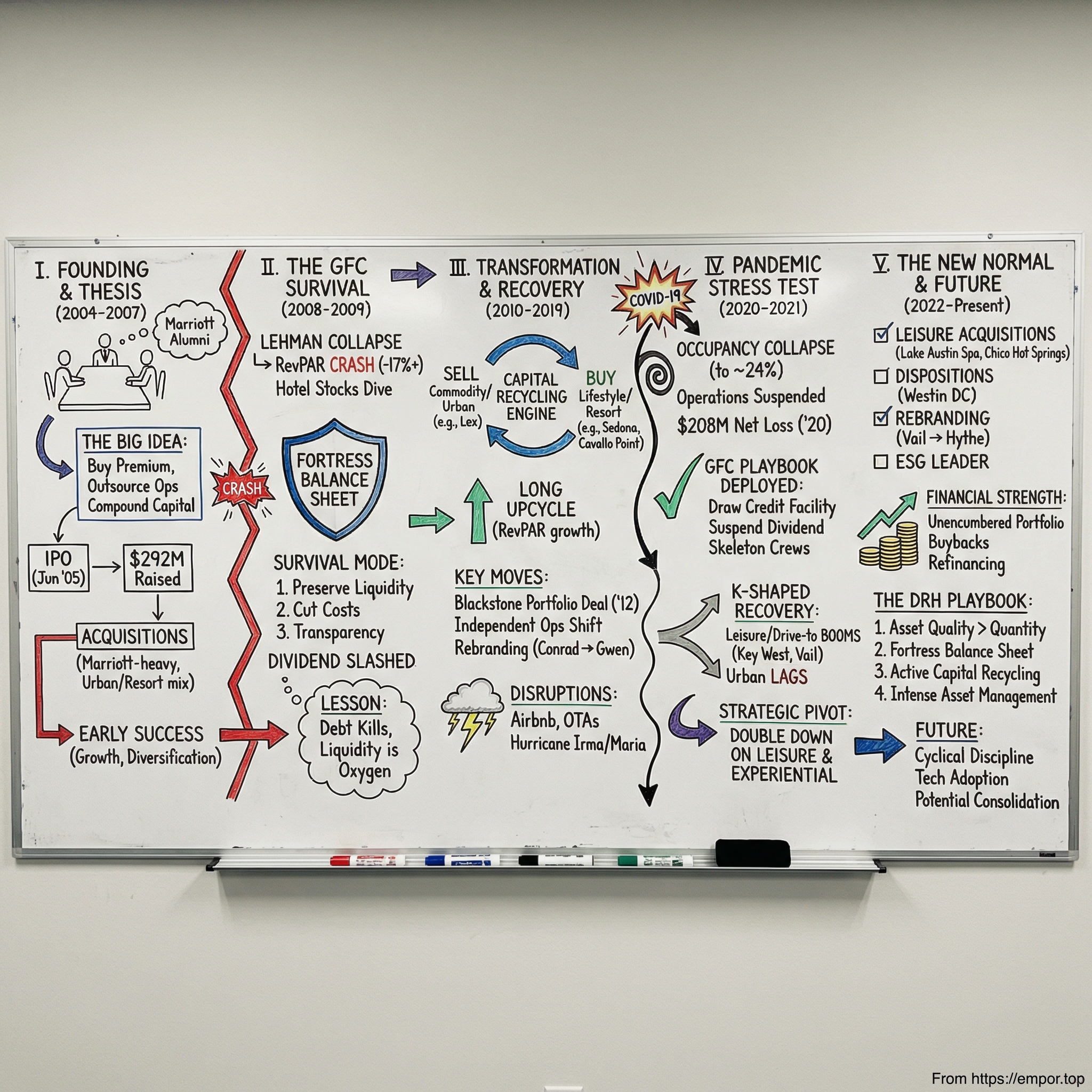

Picture a boardroom in Bethesda, Maryland, in the spring of 2004. Three former Marriott executives are sketching out a plan on a whiteboard: buy the best hotels in America's most supply-constrained markets, let someone else run them, and compound capital through cycles. The thesis sounds almost quaint in its simplicity. But over the next two decades, that thesis would be tested by the worst financial crisis since the Great Depression, a Category 5 hurricane that leveled a crown-jewel resort, and a global pandemic that pushed hotel occupancy to levels not seen since the 1930s. DiamondRock Hospitality not only survived all three. It came out the other side a leaner, smarter, and more valuable enterprise.

Today, DiamondRock trades on the Nasdaq under the ticker DRH with a market capitalization of roughly two billion dollars. The company owns thirty-five premium hotels and resorts totaling approximately 9,600 rooms scattered across the most desirable leisure and urban markets in the United States. It does not manage a single one of them. No bellhops on the payroll, no housekeeping staff, no general managers reporting to Bethesda.

DiamondRock is a pure asset ownership play — a company that makes money by owning irreplaceable real estate in places where you cannot easily build new hotels, then outsourcing operations to Marriott, Hilton, and a roster of boutique management companies.

What makes this story worth telling is not just the survival, though the survival is remarkable. It is the capital allocation playbook that emerged from each crisis. The Great Financial Crisis taught DiamondRock's leadership that a fortress balance sheet is not a luxury but a religion. COVID-19 validated that lesson and accelerated a strategic pivot toward leisure and resort properties that has fundamentally reshaped the portfolio. Along the way, the company executed one of the most disciplined buy-sell-renovate cycles in the lodging REIT universe, recycling billions of dollars of capital from commodity urban hotels into irreplaceable destination resorts.

This is the story of how a "boring" hotel REIT became a masterclass in capital allocation under fire. It is a story about REITs, hospitality cycles, the tension between hotel owners and operators, and the question every real estate investor eventually faces: when do you hold, and when do you fold? The answer, as DiamondRock's history demonstrates, depends entirely on whether you have the balance sheet to make that choice on your own terms.

II. The REIT Revolution and Lodging Real Estate Context

To understand DiamondRock, you first need to understand the strange financial architecture that makes hotel REITs possible. A Real Estate Investment Trust is essentially a tax wrapper. Congress created REITs in 1960 with the idea of democratizing real estate investing — let ordinary investors pool their money and own a piece of commercial property the way they might own a share of General Motors. The deal: if a REIT distributes at least ninety percent of its taxable income to shareholders, it pays no corporate income tax. The income gets taxed once, at the shareholder level, rather than twice. This is an enormous structural advantage.

For decades, REITs worked beautifully for asset types like office buildings, shopping malls, and apartment complexes. A landlord collects rent from a tenant, distributes the income, and everyone goes home happy. But hotels presented a peculiar problem. There are no long-term tenants in a hotel. Revenue comes from nightly guest stays — room service, restaurant tabs, spa treatments, parking fees. This is "active" business income, not passive rental income, and the IRS did not consider it REIT-qualifying.

The solution came in 1999 with the REIT Modernization Act, signed by President Clinton. The law created a new entity called the Taxable REIT Subsidiary, or TRS. Think of it like a nesting doll arrangement.

Here is how it works: the REIT owns the hotel building. The REIT leases the hotel to its own TRS. The TRS pays rent to the REIT, which recasts the hotel's operating income into REIT-qualifying rental income. But there is a critical catch — the TRS cannot operate the hotel itself. It must hire an "eligible independent contractor," a third-party management company, to run the property.

This three-layer structure — REIT owner, TRS lessee, independent operator — is unique to hotel REITs and explains why companies like DiamondRock exist in the form they do. It also explains one of the enduring tensions in the industry: the hotel owner bears all the capital risk and renovation expense, but the hotel operator controls the day-to-day guest experience and collects guaranteed fees regardless of whether the hotel makes money. Understanding this structural tension is essential to understanding DiamondRock's entire business model.

The landscape before DiamondRock's arrival was dominated by a few large players. Host Hotels and Resorts, the grandchild of the 1993 Marriott split, was the eight-hundred-pound gorilla.

When Marriott Corporation divided itself into two companies that year — Host Marriott retaining the real estate and Marriott International taking the management contracts — it created the template for the entire industry. The split was the brainchild of Stephen Bollenbach, Marriott's CFO, who recognized that the capital-heavy real estate business was dragging down the valuation of the capital-light management business. Once separated, Marriott International could grow by signing management contracts without tying up capital in bricks and mortar, while Host could pursue its own real estate strategy unburdened by the hotel management overhead. The message was clear: owning hotels and operating hotels are fundamentally different businesses with different risk profiles, different capital needs, and different return characteristics.

By the early 2000s, several hotel REITs were listed and trading: LaSalle Hotel Properties, FelCor Lodging Trust, Sunstone Hotel Investors, and others. The C-corp to REIT conversion wave was in full swing, as hotel companies realized the tax advantages of the REIT structure. But most of these companies were either very large (Host, with its portfolio of trophy assets) or focused on specific niches. There was room for a new entrant with deep industry relationships, a clear thesis, and the discipline to execute it.

It is worth pausing to explain why hospitality stands apart from other REIT sectors, because this distinction is central to everything that follows. An apartment REIT collects rent from tenants under twelve-month leases. An office REIT collects rent under five-to-ten-year leases. A hotel REIT "leases" its rooms every single night, to a different "tenant" each time, at a price that fluctuates with demand, season, day of the week, and competitive dynamics. This makes hotel revenue dramatically more volatile than any other real estate asset class. In a good year, hotels can grow revenue ten to fifteen percent. In a bad year — as DiamondRock would learn twice — revenue can fall twenty percent or more in a matter of months. The flipside of this volatility is opportunity: when the cycle turns up, hotel owners capture the upside immediately, without waiting for leases to roll over.

The capital intensity compounds the risk. Hotels are not passive assets. They require constant reinvestment — new lobbies, renovated bathrooms, upgraded HVAC systems, technology infrastructure, food and beverage concepts that keep up with changing consumer tastes. The industry standard is to reserve four to five percent of annual revenue for capital expenditures, but major renovations can cost tens of millions per property and take a hotel partially or fully offline for months. An office building can sit largely unchanged for a decade; a hotel that has not been renovated in five years starts losing rate to competitors.

The question hanging over the entire sector was a fundamental one: can you create real value just owning hotels, without running them?

The operators — Marriott, Hilton, Starwood — had the brands, the loyalty programs, the reservation systems, the operational expertise. They collected management fees of two to four percent of gross revenue plus incentive fees of five to fifteen percent of operating profit, often under contracts that lasted fifteen to thirty years. The owner took all the capital risk, bore the renovation costs, and received whatever residual cash flow was left after the operators took their cut.

It was not obvious that "pure ownership" was a great business. The operators seemed to have the better deal by a wide margin. But three men in Bethesda — with deep knowledge of exactly how that owner-operator dynamic worked, having sat on the operator side for their entire careers — thought they could prove otherwise. They knew where the value leaked, where the leverage points were, and how a sophisticated owner could extract more from the relationship. That insider knowledge would prove to be DiamondRock's founding edge.

III. Founding and the IPO

William McCarten had spent over twenty-five years at Marriott Corporation and Marriott International, rising to become President of the Services Group and then President and CEO of HMSHost Corporation, a publicly traded Marriott subsidiary that operated airport and highway concessions. He was, by all accounts, a quintessential Marriott lifer — a University of Virginia graduate who started as an accountant at Arthur Andersen before joining the Marriott machine and climbing through its ranks across three decades. When McCarten left Marriott in January 2004, he carried with him something no amount of capital could buy: an encyclopedic knowledge of hotel economics and a personal network that stretched across every major brand and ownership group in the industry.

His co-founders complemented the operational expertise with transactional firepower. Mark Brugger, a Georgetown-area lawyer with a J.D. from American University, had worked at Marriott International as a Vice President handling hotel transactions. Colleagues described him as the lead negotiator on several billion dollars of deals — the guy who understood not just the hospitality side but the real estate capital markets side, the debt structuring, the tax implications, the management contract negotiations that could make or break a deal.

John Williams, the third co-founder, brought more than thirty years of lodging industry experience and would serve as President and Chief Operating Officer, handling the day-to-day asset management that would become DiamondRock's quiet competitive advantage. If McCarten was the industry statesman and Brugger was the dealmaker, Williams was the operating hand — the person who would ensure that every hotel in the portfolio was being managed to its maximum potential, that operators were being held accountable, and that renovation dollars were being spent wisely.

The three incorporated DiamondRock Hospitality Company as a Maryland corporation on May 6, 2004. Maryland was the standard domicile for REITs, offering favorable corporate governance provisions and a well-developed body of REIT case law.

The timing was deliberate. The United States was emerging from the post-9/11 travel recession. Hotel occupancy and pricing were climbing off cycle lows. Capital markets were reopening after the dot-com bust and the Sarbanes-Oxley regulatory hangover. It was a Goldilocks moment for a hotel REIT IPO — demand was recovering, supply growth was modest, and yield-hungry investors were looking for new vehicles in real estate.

Before going public, the team moved fast on acquisitions. Using private capital, they assembled a small but strategically chosen initial portfolio: the Courtyard by Marriott Midtown East and Courtyard by Marriott Fifth Avenue in Manhattan — two New York City hotels in the heart of Midtown, the most supply-constrained hotel market in America. They added the Lodge at Sonoma in California's wine country and the Embassy Suites Bethesda, right in their backyard. These were not random picks. Each property sat in a high-barrier market where zoning restrictions, land scarcity, or community opposition made new hotel development extremely difficult.

The IPO closed on June 1, 2005, raising approximately $292 million in net proceeds. Citigroup and Friedman, Billings, Ramsey led the offering as joint book-running managers. The company elected REIT tax status effective for its 2005 fiscal year. And then the acquisitions began in earnest.

Within weeks of the IPO, DiamondRock spent $315 million on a four-hotel portfolio from Marriott-affiliated entities — a deal that would have been nearly impossible without McCarten's Marriott relationships. The package included the Marriott Los Angeles Airport, the Renaissance Worthington in Fort Worth, the Marriott Atlanta Alpharetta, and the crown jewel: Frenchman's Reef and Morning Star Marriott Beach Resort in St. Thomas, U.S. Virgin Islands — a Caribbean compound with 507 rooms perched on a bluff overlooking the turquoise waters of the Charlotte Amalie harbor.

That same summer, they added the Vail Marriott Mountain Resort for $64 million and the Oak Brook Hills Marriott outside Chicago plus a SpringHill Suites in Atlanta for another $100 million combined. The velocity of deal-making was striking. In the space of six months, DiamondRock had deployed the entire IPO proceeds and more, assembling a portfolio of ten-plus hotels across diverse markets.

By the end of 2006, DiamondRock had grown to over twenty hotels, including the 1,200-room Chicago Marriott Magnificent Mile — its largest single property — and the Conrad Chicago, acquired for $117.5 million and later repositioned as The Gwen, a Luxury Collection Hotel. The portfolio was Marriott-heavy, reflecting the founders' roots, but diversified across geographies and price points. The strategy was never to be the biggest or the cheapest. It was to target quality and location — hotels in markets where the barriers to entry were so high that the existing supply effectively constituted a scarce, irreplaceable resource.

In 2007, they sold the SpringHill Suites Atlanta Buckhead — their first-ever disposition, and a telling one. The select-service hotel did not fit the premium full-service strategy. Selling it signaled that DiamondRock's leadership was willing to admit a mistake quickly and move on. That discipline would prove essential when the world changed a year later.

IV. The Great Financial Crisis: Survival Mode

In the autumn of 2008, the American hotel industry hit a wall. Lehman Brothers collapsed on September 15, and within weeks, corporate travel budgets were slashed, convention bookings evaporated, and leisure travelers retreated to their homes. RevPAR — the industry's gold-standard metric combining both room rates and occupancy into a single number — crashed by nearly seventeen percent across the industry. Luxury and upper-upscale hotels, precisely the segment where DiamondRock had concentrated its portfolio, were hit hardest: a twenty-four percent decline. Net operating income for full-service hotels collapsed by more than a third. Lodging REIT stocks fell nearly sixty percent in 2008 alone, worse than the broader S&P 500's already catastrophic fifty-seven percent decline.

DiamondRock entered the crisis with approximately twenty-six hotels, concentrated in major cities and destination resorts. The company had been building aggressively — the Chicago Magnificent Mile, the Conrad Chicago, the Westin Boston Seaport — and carried the leverage that comes with rapid portfolio assembly.

Hotels are, by their nature, among the most cyclically sensitive assets in all of real estate. Unlike an office building with a ten-year lease that keeps paying rent through a recession, a hotel effectively re-leases every room every night. When demand drops, there is no contractual floor. Revenue falls immediately, but the fixed costs — debt service, property taxes, insurance, the minimum staffing required to keep a hotel open — remain stubbornly in place. This is operating leverage at its most punishing.

Think of it this way: if a hotel's revenue drops twenty percent but its fixed costs stay flat, the operating profit can drop forty to fifty percent. The math works beautifully in reverse during upturns — a modest revenue increase drops disproportionately to the bottom line — but in a downturn, it is devastating.

The transaction market froze. No one was buying hotels, because no one could get financing to buy hotels. This was both a curse and a blessing for DiamondRock. A curse because the company could not easily sell assets to raise cash if it needed to. A blessing because the absence of forced sellers meant that property values, while impaired on paper, were not being marked down by distressed transactions that would have established devastating new price benchmarks. The distressed buyers who circle every downturn like vultures — the opportunity funds, the private equity firms — were themselves struggling to raise capital.

What followed was a period of intense triage. The leadership team — McCarten as chairman, Brugger now as CEO after his September 2008 promotion — focused on three priorities. First, preserve liquidity. DiamondRock's property-level mortgage structure, with no corporate-level debt at the time, provided some insulation; lenders could go after individual hotels but could not force a corporate-level bankruptcy. Second, cut costs relentlessly. Hotel EBITDA margins compressed as revenue fell faster than expenses could be reduced, but every dollar saved extended the runway. Third, communicate transparently with investors and lenders. Trust was the scarcest commodity in 2008 and 2009, and management teams that hid behind optimistic projections lost credibility fast.

The leadership transition itself was notable. Brugger took over as CEO on September 1, 2008 — literally two weeks before Lehman's collapse. McCarten's decision to hand the reins to his younger co-founder at that precise moment was either spectacularly bad timing or remarkably prescient, depending on your perspective. In hindsight, it was the right call. Brugger was the transactional mind, the one who understood debt markets and capital structures. Those were precisely the skills needed to navigate a financial crisis. McCarten remained as non-executive chairman, providing the industry relationships and institutional memory, while Brugger made the hard operational and financial decisions.

The dividend was slashed. DiamondRock had been paying a quarterly dividend that represented one of the primary reasons institutional investors owned REIT shares. But with cash flows cratering, the payout was untenable. The reduction was painful — REIT investors depend on distributions, and cutting the dividend sent the stock into a tailspin. But it was the right call. Every dollar retained was a dollar that did not have to be borrowed at punitive crisis-era rates or raised through dilutive equity issuances.

Some peers fared worse. FelCor Lodging Trust, which had entered the crisis with higher leverage and a weaker portfolio concentrated in convention hotels, spent years restructuring its balance sheet and ultimately merged with RLJ Lodging Trust in 2017 at a significant discount to its pre-crisis value. Sunstone Hotel Investors was forced into emergency equity offerings. Several smaller hotel REITs were delisted or absorbed. The industry's casualty list reinforced a Darwinian lesson: in cyclical industries, the survivors are not necessarily the ones with the best assets or the smartest management — they are the ones with the most conservative capital structures.

The recovery was slow. Hotel stocks went essentially sideways for two years after the initial bounce off the March 2009 lows. RevPAR did not turn positive until early 2010, and even then, the recovery was uneven — luxury and upper-upscale lagged economy and midscale. DiamondRock survived, but the experience left permanent scars on the organization's DNA. From that point forward, the phrase "fortress balance sheet" became not a slogan but a religion. Every capital allocation decision would be viewed through the lens of: could we survive another 2008 with this debt level, this maturity profile, this liquidity cushion?

The lesson was brutal but clarifying. In the hotel business, you do not die from bad RevPAR. You die from bad balance sheets. A hotel owner with low leverage and ample liquidity can wait for the cycle to turn, can buy when others are forced to sell, can choose when to act rather than being compelled to act. A hotel owner with high leverage and looming maturities has no such luxury. The Great Financial Crisis did not just test DiamondRock's survival instincts. It forged the capital allocation philosophy that would define the next fifteen years.

V. The Long Recovery and Portfolio Transformation

When the dust settled from the financial crisis, DiamondRock's leadership did not simply rebuild the same portfolio. They rebuilt a better one. Starting in 2010, the company embarked on one of the most ambitious portfolio transformations in lodging REIT history, acquiring nearly three billion dollars of urban and resort hotels while disposing of over one billion dollars of non-core assets. The guiding principle was simple: migrate toward higher-quality assets in supply-constrained markets, exit secondary and tertiary locations where the next downturn would hit hardest, and build a portfolio that could generate superior returns through cycles, not just at the top of one.

The early moves were methodical. In 2010, DiamondRock acquired the Lindy Renaissance Charleston Hotel — 167 rooms in one of America's most tourism-dependent and supply-restricted cities — and the Hilton Garden Inn Chelsea in Manhattan.

In 2011, the pace accelerated with two Denver properties and, most significantly, The Lexington Hotel in Midtown New York. The Lexington was a 712-room full-service hotel purchased for $335 million, representing a 13.5x multiple on forecasted 2012 EBITDA. It was a bold bet on New York City at a time when many investors were still shell-shocked from the GFC. The hotel left the Radisson chain and joined Marriott's Autograph Collection, a rebranding that signaled DiamondRock's willingness to invest not just in the bricks but in the brand identity of its assets. The Autograph Collection was itself a new concept at the time — Marriott's attempt to capture the independent boutique hotel trend by offering brand distribution and loyalty program access while allowing each property to retain its individual character.

The transformational deal came in July 2012 when DiamondRock closed on a $495 million portfolio from Blackstone Real Estate Partners. Four hotels — the Hilton Boston Downtown, the Westin Washington D.C. City Center, the Hilton Burlington, and the Westin San Diego — came over in a single transaction at roughly $339,000 per key. This was DiamondRock playing the capital markets game at its highest level: Blackstone needed to exit assets from an aging fund, and DiamondRock had the balance sheet, the relationships, and the execution speed to close a half-billion-dollar deal in a market where few competitors could move that quickly.

To fund these acquisitions without over-leveraging, DiamondRock simultaneously ran a disposal program that was equally disciplined. In 2012, they sold the Renaissance Waverly in Atlanta, the Westin Atlanta North, the Griffin Gate Marriott in Lexington, Kentucky, and the Renaissance Austin. In 2013, the Torrance Marriott went. In 2014, the Los Angeles Airport Marriott and Oak Brook Hills Resort followed.

The pattern was unmistakable: out with the suburban, the secondary-market, the commodity-like hotels; in with the urban, the resort, the irreplaceable. Every hotel sold had a common profile — located in a market where new supply could easily be built, dependent on price-sensitive demand segments, and generating middling RevPAR with limited pricing power. Every hotel acquired had the opposite profile — sitting in a market with high barriers to new development, attracting premium-paying guests, and generating superior RevPAR with room to grow rates.

The later years of this transformation period brought acquisitions that foreshadowed DiamondRock's eventual leisure pivot. In 2014, the company bought the Inn at Key West for $47.5 million and the Westin Beach Resort in Fort Lauderdale for $149 million. In 2015, they added the Sheraton Suites Key West for $94 million and the Shorebreak Hotel in Huntington Beach, California, for $58.5 million. These Florida and coastal California properties were not just diversification — they were a bet on the durability of leisure travel demand in locations where you simply could not build new competition.

The "barbell strategy" was taking shape: high-quality leisure resorts on one end, urban group-oriented hotels in gateway cities on the other, and nothing in the mushy middle of secondary markets where supply could easily overwhelm demand. The results showed up in the numbers. Portfolio quality improved, EBITDA margins expanded, and RevPAR increasingly outpaced the industry average. By 2015, DiamondRock had recycled over a billion dollars of capital from lower-quality to higher-quality assets. The portfolio was unrecognizable from the Marriott-heavy collection of 2007.

The relationship management during this period was equally impressive. Negotiating management contracts and franchise terms with Marriott, Hilton, and other brands is a complex art. The brands hold significant leverage because they control the loyalty programs — Marriott Bonvoy, Hilton Honors — and the reservation systems that drive bookings. But DiamondRock, with its Marriott-alumni leadership and multi-property relationships, had the scale and credibility to negotiate favorable terms: shorter contract durations, stronger owner's priority provisions, and the flexibility to rebrand or switch operators when it made strategic sense. This was not the kind of leverage a one-hotel owner could ever hope to wield.

One crucial development during this era deserves attention: DiamondRock's deliberate decision to begin hiring independent third-party management companies rather than relying exclusively on the brand companies themselves to operate the hotels. This was a subtle but strategically important move. When Marriott both brands and manages a hotel, it controls the guest experience, the pricing, the staffing model — and it collects both a franchise fee and a management fee. When DiamondRock decoupled these functions — franchising the brand from Marriott but hiring an independent operator like Aimbridge Hospitality to manage — it gained significantly more control over day-to-day operations and costs. The independent manager reports more directly to the owner, is more responsive to cost-cutting initiatives, and can be replaced more easily. By 2015, DiamondRock had shifted a meaningful portion of its portfolio to this hybrid model, a precursor to the independent-lifestyle strategy that would define the next decade.

The cumulative effect of five years of aggressive portfolio recycling was transformative. When DiamondRock entered the GFC in 2007, it owned a Marriott-heavy collection of full-service hotels spread across primary and secondary markets. By 2015, it owned a diversified portfolio of premium urban and resort assets in high-barrier markets, operated under multiple brand flags, with an increasingly flexible management structure. The average RevPAR of the portfolio had risen substantially. The EBITDA margin profile was better. And critically, the balance sheet was in the best shape it had ever been — lower leverage, longer-dated maturities, and a growing pool of unencumbered assets that provided financial flexibility. The transformation was not glamorous. There was no single transformative deal, no bold stroke. It was grinding, methodical capital allocation — buy the right asset, sell the wrong one, repeat — executed over half a decade. But it worked.

VI. The RevPAR Game: Understanding Lodging Cycles and Operator Dynamics

To appreciate what DiamondRock does and why it matters, you need to understand how hotel economics actually work at the property level. Think of a hotel as a factory that manufactures identical products — room-nights — that expire at midnight every day. An unsold room on Tuesday night is lost revenue forever, unlike an unsold car that can sit on the lot until a buyer appears. This perishability is what makes hotel investing so different from almost every other form of real estate.

The industry tracks three core metrics. Average Daily Rate, or ADR, tells you the average price charged per occupied room — the pricing power of the asset. Occupancy tells you what percentage of available rooms were sold — the demand signal. RevPAR, or Revenue Per Available Room, multiplies the two together and captures both dimensions in a single number. When an analyst says "RevPAR grew five percent," they are saying the hotel generated five percent more revenue per available room than the prior period, whether that came from higher rates, higher occupancy, or both. DiamondRock's comparable RevPAR in 2025 was $207, up from roughly $189 in 2019 — a cumulative gain that looks modest until you remember that a pandemic happened in between.

Below RevPAR sits Gross Operating Profit, or GOP — total revenue minus direct operating expenses like labor, utilities, supplies, and maintenance. GOP margins for a well-run full-service hotel typically range from thirty to forty percent. Below GOP sits Net Operating Income, or NOI, which further deducts property-level fixed costs like taxes, insurance, and a reserve for capital expenditures (the industry standard is four percent of revenue set aside for furniture, fixtures, and equipment replacement). NOI is the number that matters most to owners because it represents the actual cash flow available to service debt, fund renovations, and return capital to investors.

Now here is where the owner-operator tension gets interesting. When you stay at a Marriott-branded hotel owned by DiamondRock, your room rate flows into a complex waterfall of fees. Think of it as a toll booth system where Marriott collects tolls at multiple points before the owner sees a dime of profit.

Marriott takes a base management fee — typically three percent of total gross revenue, paid regardless of whether the hotel makes money. If the hotel is profitable, Marriott earns an incentive fee — usually a percentage of operating profit above a certain threshold called the "owner's priority," which is essentially a preferred return hurdle that protects the owner's investment. The brand also collects franchise fees of roughly four to eight percent of room revenue, plus loyalty program assessments, plus marketing contributions.

By the time you stack up all these fees, the brand is collecting twelve to fifteen percent of the hotel's top line with essentially zero capital at risk. The brand does not own the building. It does not fund the renovations. It does not guarantee the debt. It simply collects fees for the privilege of hanging its flag on the building and plugging the hotel into its reservation system and loyalty program. It is, by any measure, one of the best business models in the American economy — which is why Marriott and Hilton trade at twenty-plus times EBITDA while hotel owners trade at single-digit multiples.

DiamondRock's response to this structural tension has been to invest in what the industry calls "asset management intensity." This means deploying a team of professionals who monitor every aspect of hotel performance — from labor productivity to energy costs to revenue management strategies — and push the third-party operators to perform better. A great asset manager can add two to three percentage points of margin through better purchasing, smarter staffing models, and more aggressive revenue management, which on a hundred-million-dollar revenue hotel translates to two or three million dollars of additional NOI flowing directly to the owner.

Consider how DiamondRock has managed its Sedona portfolio as a case study. When the company acquired L'Auberge de Sedona and the adjacent Orchards Inn in 2017 for $97 million, the two properties operated independently with separate management, separate branding, and duplicative overhead. DiamondRock spent $25 million integrating the Orchards Inn as "The Cliffs at L'Auberge," creating a unified resort experience with shared amenities, combined marketing, and streamlined operations. The result was higher ADR, better occupancy, improved margins, and a property worth substantially more than the sum of its parts. This is the kind of value creation that does not show up in a hotel brand's income statement — it accrues entirely to the owner who had the vision and the capital to execute the transformation.

The choice of markets matters enormously in this equation. DiamondRock has systematically concentrated its portfolio in what the industry calls "supply-constrained" markets — places like Key West, Sedona, Sausalito, Vail, and Huntington Beach where zoning laws, environmental regulations, land scarcity, or community opposition make it extraordinarily difficult to build new hotels. In these markets, the existing supply functions like a cornered resource: irreplaceable, scarce, and increasingly valuable as travel demand grows while the competitive set remains static.

There is one more layer to the economics that is worth understanding: Total RevPAR, or TRevPAR. Traditional RevPAR only captures room revenue, but hotels increasingly generate substantial income from food and beverage, spa services, resort fees, parking, and other ancillary sources. For DiamondRock's resort-heavy portfolio, these non-room revenues can represent thirty to forty percent of total revenue. In 2025, DiamondRock's Total RevPAR was $319, meaningfully higher than the $207 room-only RevPAR, and it grew at 1.2 percent year-over-year — faster than room RevPAR alone. This distinction matters because resort and lifestyle hotels, which command higher spending per guest on experiences, dining, and amenities, generate a richer revenue stream than commodity business hotels where the room rate is essentially the entire economic proposition. DiamondRock's strategic pivot toward experiential properties is, at its core, a bet on TRevPAR growth — the idea that guests at L'Auberge de Sedona or Lake Austin Spa Resort will spend significantly more per stay than guests at a Courtyard by Marriott, and that this incremental revenue flows to the bottom line at attractive margins.

VII. The Golden Years: 2015–2019

The period from 2015 through 2019 represented the longest sustained upcycle in the modern history of American lodging. RevPAR grew every single year. Corporate travel budgets expanded. The American consumer, buoyed by a strong labor market and rising asset prices, traveled more and spent more per trip. Convention centers across the country were booking record group business. Business transient travel — the bread and butter of urban full-service hotels — was robust. For a newly optimized portfolio like DiamondRock's, it was the payoff season — the moment when years of patient portfolio recycling and disciplined capital allocation were supposed to generate the returns that justified the pain of the GFC.

But Mark Brugger and his team were not content to ride the wave passively. The portfolio optimization continued with a series of carefully chosen acquisitions that pushed DiamondRock further toward its leisure and lifestyle thesis. In early 2017, the company acquired L'Auberge de Sedona and the Orchards Inn in an off-market transaction for $97 million — a deal that exemplified the patient, relationship-driven approach. Off-market transactions, where the buyer and seller negotiate directly without a formal auction process, typically yield better prices for the buyer but require trust, discretion, and a reputation for closing.

In 2018, the shopping continued. DiamondRock bought the Kimpton Hotel Palomar Phoenix for $80 million and The Landing Resort and Spa on Lake Tahoe for $42 million.

Then, in December 2018, came the deal that may best capture the DiamondRock strategy at its zenith: Cavallo Point, The Lodge at the Golden Gate Bridge, in Sausalito, California, for $152 million. Cavallo Point is the kind of property that makes real estate investors salivate. Picture this: a 142-room luxury lodge set within the Golden Gate National Recreation Area, housed in converted former Army officer quarters from the old Fort Baker military post. Guests wake up to views of the San Francisco skyline and the Golden Gate Bridge framed by mature eucalyptus trees. The location is not just supply-constrained; it is supply-impossible. You cannot build another hotel in a national park. No zoning variance, no political connection, no amount of capital can create a competitor.

The property was funded with a combination of cash, a new term loan, and operating partnership units issued to the seller — a creative capital structure that minimized cash outflow while aligning the seller's interests with DiamondRock's long-term performance. Cavallo Point would become one of the portfolio's strongest performers, commanding ADRs well above $500 per night and generating some of the highest margins in the entire portfolio.

Meanwhile, DiamondRock was also making strategic rebranding moves. The Conrad Chicago, acquired in 2006 for $117.5 million, was repositioned as The Gwen, a Luxury Collection Hotel — a bet that an independent, personality-driven hotel brand would outperform a legacy chain name in the evolving boutique hotel landscape. This kind of rebranding is expensive and risky, but it reflected a growing conviction that the most valuable hotel assets were not commodity chain hotels but distinctive, experiential properties that could command premium rates.

The financial results during this period were strong. The portfolio was generating healthy RevPAR growth, margins were expanding as the effects of capital recycling flowed through, and the balance sheet was in excellent shape. DiamondRock returned capital through dividends and began buying back shares when the stock traded below management's estimate of intrinsic value.

Underneath the surface, two disruptions were gaining momentum. Airbnb had grown from a quirky startup to a global platform with four million listings. The impact on traditional hotels was real but nuanced — Airbnb primarily siphoned demand from lower-tier and midscale hotels in leisure and seasonal markets. Upper-upscale branded hotels, the segment where DiamondRock operated, were relatively insulated by brand loyalty programs, consistent service standards, and the business travel segment that Airbnb could not easily penetrate. Online travel agencies like Expedia and Booking.com represented a different challenge: they drove incremental demand but extracted commissions of fifteen to twenty-five percent per booking, putting persistent pressure on margins. DiamondRock's response — investing in branded properties with strong direct booking channels — was a bet that Marriott Bonvoy and Hilton Honors would continue to drive guests to book directly rather than through OTAs.

Then Hurricane Irma struck St. Thomas on September 6, 2017, followed days later by Hurricane Maria. Frenchman's Reef and Morning Star Beach Resort, the Caribbean compound that had been a portfolio centerpiece since 2005, sustained catastrophic wind and water damage. Guests and staff were evacuated. The resort was shut down indefinitely.

The destruction was comprehensive. Roofs were torn away, interiors flooded, landscaping destroyed, and the resort's infrastructure — electrical, plumbing, mechanical systems — was rendered inoperable. DiamondRock initially estimated reconstruction costs at roughly $300 million. The company pursued a massive insurance claim that would eventually settle for $247 million, providing substantial capital recovery. But the rebuilding challenge was daunting: constructing in a remote island location during the aftermath of two Category 5 hurricanes, with supply chain disruptions, labor shortages, and eventually COVID-19 throwing additional obstacles in the path. The reconstruction timeline was repeatedly delayed — an initial 2020 reopening target slipped, then slipped again. Marriott International, the long-time operator, eventually withdrew from the project. The saga would take four more years to resolve and would permanently shape DiamondRock's view of catastrophic risk in coastal markets.

By late 2019, DiamondRock's portfolio was lean, high-quality, and increasingly tilted toward leisure destinations. More than sixty percent of the hotels were leisure-focused. Nearly ninety-five percent were independently managed, giving DiamondRock maximum flexibility in operator selection. The customer mix was roughly split into thirds: leisure travelers, group business, and business transient. It was the best positioning the company had ever achieved.

But there was an uncomfortable reality beneath the surface optimism. The lodging cycle was long in the tooth. RevPAR growth had decelerated from mid-single-digits earlier in the decade to low-single-digits by 2019. New supply was ticking up in several key markets. The industry's most sophisticated forecasters were predicting a plateau — not a collapse, just a leveling off. The consensus view was that the cycle would age gracefully, delivering modest but positive returns for another year or two before the inevitable downturn. Nobody predicted what actually happened. Nobody could have.

VIII. COVID-19: The Ultimate Stress Test

On March 11, 2020, the World Health Organization declared COVID-19 a pandemic. Within days, international borders closed, domestic travel restrictions went into effect, and corporate travel ceased entirely.

For the hotel industry, it was not a recession — it was an apocalypse. U.S. hotel occupancy, which had averaged sixty-six percent in 2019, collapsed to 24.5 percent in April 2020 — a level not seen since the Great Depression. In some urban markets, occupancy dropped to single digits. Times Square hotels, convention center hotels, airport hotels — all essentially empty. The American hotel industry would lose a collective $112 billion in room revenue over 2020 and 2021. More than 670,000 hotel operation jobs vanished, representing nearly forty percent of the industry's entire workforce.

DiamondRock moved with the speed that only a crisis-hardened management team can muster. Within days of the WHO declaration, the company suspended operations at twenty of its thirty previously operating hotels.

Mark Brugger, now in his twelfth year as CEO, drew a straight line from the GFC playbook: preserve liquidity first, cut costs second, communicate transparently third. DiamondRock fully drew down its $400 million senior unsecured credit facility, putting approximately $380 million of cash on the balance sheet. The logic was brutal but sound — in a crisis, cash is oxygen, and you do not know how long you will need to hold your breath. Dozens of hotel companies across the country drew down their credit facilities in that same week — it was as close to a bank run as the REIT industry has ever experienced.

The board suspended the quarterly common stock dividend starting with the April 2020 payment, a move estimated to preserve up to $100 million of annual capital. Every lodging REIT in America made the same decision — all eighteen public hotel REITs cut or suspended their dividends, an unprecedented blanket action that underscored the severity of the crisis. The company withdrew its 2020 financial guidance.

At the property level, the cost-cutting was surgical. Hotels that remained open operated with skeleton crews. Food and beverage outlets were closed or limited to grab-and-go. Housekeeping was reduced to upon-request only. Corporate overhead was slashed. Capital expenditure programs were deferred. The goal was not profitability — that was impossible when occupancy was in the single digits — but cash preservation. Every week of reduced burn rate was another week of runway.

The Frenchman's Reef reconstruction, already plagued by delays and cost overruns from the post-hurricane rebuild, was paused indefinitely. DiamondRock recorded a $174 million impairment loss on the property. For the full year 2020, the company reported a net loss of $208 million as comparable total revenues declined 75.2 percent from 2019.

But here is where the lessons of the GFC paid their greatest dividend. The fortress balance sheet that DiamondRock had maintained throughout the 2015–2019 expansion — low leverage, staggered maturities, ample liquidity — meant that the company was not fighting for survival the way it had in 2008. It was fighting for positioning. In June 2020, DiamondRock successfully amended its credit agreements for the $400 million revolving facility and $350 million unsecured term loan, buying time through covenant waivers that would be extended through December 2021. The lenders cooperated because DiamondRock's track record of balance sheet discipline had built trust over years, and trust is the currency that buys covenant relief.

The asset mix proved prophetic. As the pandemic ground on, a stark divergence emerged between urban hotels dependent on business and convention travel and leisure properties in drive-to destinations.

DiamondRock's Key West hotels, its Sedona resorts, its Vail property, its Sonoma lodge — these leisure-oriented assets began recovering far faster than the Chicago Marriott Magnificent Mile or the Westin Boston Seaport. The "revenge travel" phenomenon — consumers flush with stimulus checks and accumulated savings, desperate to escape their homes after months of lockdown — produced a surge of leisure demand starting in late 2020 and accelerating through 2021.

Drive-to destinations, outdoor-focused resorts, and beach properties saw occupancy and rates recover to pre-pandemic levels while urban full-service hotels limped along at a fraction of their former performance. The data was not ambiguous. Sedona was booming. Key West was booming. Vail was booming. Chicago's Magnificent Mile was a ghost town. The portfolio was effectively split in two, and management took notice.

Hotels reopened gradually: twelve in the second quarter of 2020, five more in the third quarter, and by year-end, twenty-seven of thirty were operational. But the recovery was deeply uneven, and it fundamentally shaped DiamondRock's strategic direction. Management saw what the data was screaming: leisure travel was resilient, perhaps permanently more valuable than pre-pandemic models had assumed. Business travel was structurally impaired by remote work and video conferencing. Group and convention travel would recover, but slowly.

The financial results told the story in stark terms. Full-year 2020 comparable revenue declined over seventy-five percent. The company reported a net loss of $208 million. But DiamondRock never came close to a liquidity crisis — unlike in 2008, where survival was genuinely in question, the pandemic-era balance sheet held firm. The credit facility amendments went through without drama. No assets were sold under duress. No emergency equity dilution was required. The GFC playbook had worked exactly as designed: enter a crisis with a fortress balance sheet, preserve liquidity aggressively, and emerge positioned to play offense while competitors are still playing defense.

By mid-2021, the recovery was accelerating rapidly in leisure markets. DiamondRock's Key West properties, its Sedona resorts, and its California coastal hotels were posting RevPAR numbers that exceeded 2019 levels — a remarkable achievement when urban hotels in the same portfolio were still operating at fifty to seventy percent of pre-pandemic performance. The bifurcation was not subtle. It was a chasm. And it drove what became the most consequential strategic shift in DiamondRock's history.

In May 2021, DiamondRock resolved the Frenchman's Reef situation by selling the property to an affiliate of Fortress Investment Group for $35 million in cash plus a participation right in future profits. The $35 million sale price was a fraction of the asset's pre-hurricane value, but the $247 million insurance settlement had already provided substantial capital recovery, and exiting the project freed management from a money pit of reconstruction costs that had already exceeded $400 million in total across all owners. Fortress subsequently invested an additional $311 million to complete the rebuild — reopening the resort in phases starting May 2023 under new Westin and Autograph Collection brands, at a staggering total investment approaching $1,000 per key. That number confirmed DiamondRock's decision to exit was financially rational — the reconstruction was simply too capital-intensive for a public REIT constrained by distribution requirements and investor expectations.

A month later, DiamondRock sold the 725-room Lexington Hotel in New York City for $185 million, a property purchased for $335 million in 2011. It was a loss on paper, but the Lexington represented everything DiamondRock was moving away from: a large, capital-intensive urban hotel in a market where the pandemic had cratered demand and the recovery outlook was uncertain. The sale was completed at a 5.4 percent cap rate on 2019 NOI and roughly 14x pre-COVID EBITDA — respectable pricing given the circumstances, and evidence that institutional demand for New York City hotel real estate had not entirely evaporated.

The capital recycled from these dispositions would fund the leisure acquisitions that transformed the portfolio. In the span of eighteen months, DiamondRock executed six transactions, recycling $220 million from low-yield, encumbered, capital-intensive properties into $293 million of high-quality, unencumbered, independent hotels and resorts. The math was elegant: less capital deployed, better assets acquired, and no mortgage debt attached to the new properties. It was capital recycling at its most disciplined.

IX. The New Normal: 2022 to Present

The post-COVID world handed DiamondRock's management team a thesis confirmation they could not have designed better. Leisure travel did not just recover — it surged past pre-pandemic levels. ADRs at resort properties hit records. The "bleisure" phenomenon — remote workers combining business and vacation travel into extended stays at destination hotels — created a new demand segment that favored exactly the kind of experiential, location-driven properties DiamondRock had been accumulating for years. Meanwhile, traditional business travel remained structurally below 2019 levels, and group/convention travel recovered slowly, not fully returning until 2023.

DiamondRock leaned into this reality with a purchasing spree focused almost entirely on leisure and resort assets. In 2021, the company acquired the Bourbon Orleans Hotel in New Orleans and the Henderson Park Inn in Destin, Florida, for a combined $109 million. The Henderson Park Inn — a 37-room boutique beachfront property commanding ADRs above $500 per night — was exactly the kind of irreplaceable, scarce asset that embodied the DiamondRock thesis. In December 2021, they added the Henderson Beach Resort and Spa, also in Destin, for $112.5 million in an off-market deal, giving DiamondRock a dominant position in one of the Gulf Coast's premier beach markets.

The acquisitions continued into 2022 with the Tranquility Bay Beachfront Resort in Marathon, Florida — 103 units in the Florida Keys — and Lake Austin Spa Resort, a 40-room all-inclusive luxury wellness retreat on twelve acres of private Lake Austin waterfront.

The Lake Austin deal, at $75.8 million, represented nearly $1.9 million per key — an eye-popping number that would make most hotel investors choke on their coffee. But consider the asset: it is the only short-term lodging property directly on Lake Austin, sitting on twelve acres of private waterfront in one of the most desirable zip codes in Texas. The property books months in advance, commands all-inclusive rates that start above $1,000 per night, and generates gross margins that would make a software company envious. Making it essentially impossible to replicate is the point — this is what cornered resources look like in hospitality.

In 2023, DiamondRock added Chico Hot Springs Resort in Paradise Valley, Montana, for $33 million — a 97-room resort near the northern entrance to Yellowstone National Park with natural hot spring pools, horseback riding, and the kind of authentic Western experience that no amount of new construction can recreate. The acquisition pattern was clear: unique, experiential, impossible to replicate, and commanding premium pricing from affluent travelers willing to pay for authenticity.

On the disposition side, DiamondRock sold the Westin Washington D.C. City Center in February 2025 for $92 million at a 7.5 percent cap rate and 11.2x trailing EBITDA. The Westin D.C., originally part of the 2012 Blackstone portfolio acquisition, had been a solid performer, but it represented the urban, group-dependent hotel type that DiamondRock was systematically exiting.

In November 2024, the company also acquired the AC Hotel Minneapolis Downtown, a 245-room property, for $30 million — roughly $122,000 per key, a price point that reflected the upper-midscale segment and the Minneapolis market's more modest positioning. It was a smaller deal but one that demonstrated management's willingness to be opportunistic across price points when the risk-reward was compelling.

The strategic repositioning extended beyond buy-sell transactions. DiamondRock invested heavily in rebranding and renovating existing assets to capture the experiential travel wave. The former Vail Marriott underwent an extensive renovation and relaunched in November 2021 as The Hythe, a Luxury Collection Resort — a dramatic departure from a commodity Marriott brand to a distinctive luxury identity. The Hilton Boston Downtown was rebranded as The Dagny Boston, an independent lifestyle boutique hotel, in August 2023. The Hilton Burlington became Hotel Champlain Burlington, Curio Collection by Hilton, in July 2024. Each rebranding was designed to move the property up the value chain by creating a unique guest experience that could command premium pricing.

Technology has also begun reshaping hotel operations in ways that benefit asset-intensive owners. Revenue management systems powered by machine learning now dynamically adjust room pricing hundreds of times per day based on demand signals, competitive pricing, and booking pace — an advancement that improves ADR capture rates versus the static pricing of a decade ago. Contactless check-in and mobile key technology, accelerated by COVID-era hygiene concerns, have reduced front-desk staffing needs. Energy management systems with smart thermostats and automated lighting have cut utility costs at properties across DiamondRock's portfolio. None of these innovations individually move the needle dramatically, but in aggregate, they contribute to the margin improvement that has characterized DiamondRock's recent financial performance.

On the sustainability front, DiamondRock has become an industry leader. The company earned the GRESB Listed Hotel Sector Leader designation for five consecutive years through 2024, received four Green Stars in the 2024 GRESB assessment, and was ranked first among all U.S. hotels by GRESB for environmental performance. In 2024, DiamondRock received the Nareit Leader in the Light Award recognizing leadership in sustainable REIT practices. The company has set 2030 targets to reduce portfolio energy intensity by thirty percent, carbon intensity by fifty percent, and water intensity by twenty percent. Smart thermostats, onsite solar panels, upgraded building management systems, and energy-efficient boilers have been deployed across the portfolio. Investors increasingly scrutinize ESG performance, and DiamondRock's credentials provide a modest but real competitive advantage in attracting institutional capital.

The financial and capital structure moves since 2022 have been equally transformative. In July 2025, DiamondRock completed a $1.5 billion refinancing of its senior unsecured credit facility, upsizing from the prior $1.2 billion facility and extending maturities. The company repaid all $291 million in outstanding mortgage loans during 2025, creating a fully unencumbered portfolio — meaning no individual property is pledged as collateral to any lender. This gives DiamondRock maximum financial flexibility to sell, refinance, or reposition any asset without lender consent. Total debt stands at $1.1 billion, entirely in unsecured term loans at a weighted average rate of five percent.

On December 31, 2025, DiamondRock redeemed all 4.76 million shares of its 8.25 percent Series A Cumulative Redeemable Preferred Stock for $121.5 million. Eliminating the preferred dividend creates a roughly three-cent-per-share tailwind to FFO going forward, and removing the preferred layer simplifies the capital structure. The company transferred its listing from the NYSE to the Nasdaq Global Select Market in December 2025.

The share buyback program has been a notable feature of the post-COVID capital allocation. In 2024, DiamondRock repurchased 7.9 million shares at an average price of approximately $7.97, spending $63 million. In 2025, it bought back another 4.8 million shares at $7.72 average, investing $37 million. The total share count has declined from over 213 million to approximately 205 million. Management has articulated the logic clearly: when the stock trades at an implied cap rate above nine percent — well above the cap rates at which comparable hotels transact in the private market — buying back shares is the highest-returning use of capital available. It is essentially buying hotels at a thirty percent discount to private market value. Of the $200 million buyback authorization, $137 million remains available.

The leadership also turned over in a generational transition. In April 2024, Jeffrey Donnelly was appointed CEO, succeeding co-founder Mark Brugger after twenty years of service. Donnelly came from Wall Street — he had been Managing Director of equity research at Wells Fargo Securities, where he co-founded the Real Estate and Lodging Equity Research Platform and was responsible for over $45 billion in equity transactions over twenty-two years. This was an unusual hire — most hotel REIT CEOs come from operations or real estate backgrounds, not the sell-side analyst desk. But the choice signaled DiamondRock's board belief that the next phase of value creation would come from capital allocation and capital markets strategy rather than from deal-making or property management. Briony Quinn, previously SVP and Treasurer, was promoted to EVP, CFO, and Treasurer. Justin Leonard, who had joined as EVP and COO in 2022, became President.

The new team inherited a company in strong shape. Full-year 2025 revenues came in at $1.12 billion. Adjusted FFO hit $1.08 per share — a record for the company and an increase of 3.8 percent versus 2024. Free cash flow per share reached $0.69, up twenty-two percent since 2023. The Q4 2025 earnings report, released in late February 2026, beat analyst estimates on both the top and bottom lines, with adjusted FFO of $0.27 per share topping the $0.24 consensus. The stock touched a new fifty-two-week high above $10.29 in the days following the release. The common dividend, which was reinstated at a modest $0.03 per quarter in August 2022, has been raised progressively: to $0.08 per quarter in 2025, and to $0.09 per quarter in February 2026, representing a yield of approximately 3.2 percent at recent prices. The payout ratio remains conservative at roughly thirty percent of adjusted FFO — well within the range that provides both income and balance sheet flexibility.

The 2026 guidance calls for comparable RevPAR growth of one to three percent, adjusted EBITDA of $287 to $302 million, and adjusted FFO per share of $1.09 to $1.16. Management has indicated it is "increasingly likely" that DiamondRock will be a net seller of hotels in 2026, as inbound interest for several properties has resumed. The competitive landscape continues to evolve: among lodging REITs, Host Hotels remains the sector giant at $13.7 billion market cap with eighty properties, while Apple Hospitality dominates the select-service segment with 220 hotels. Pebblebrook and Sunstone compete most directly with DiamondRock in the upper-upscale and lifestyle segments. DiamondRock's differentiation — its heavy independent hotel weighting at nearly forty percent, its leisure portfolio concentration, and its relatively conservative leverage — positions it as a distinctive option in a crowded field.

X. Playbook: Business and Capital Allocation Lessons

Twenty years of DiamondRock's history, compressed into a set of principles, reveal a remarkably consistent philosophy that was refined by crisis rather than created by it. The playbook has four pillars, and each one was stress-tested under extreme conditions.

The first pillar is asset quality over asset quantity. From the earliest days, the founders' instinct was to own fewer, better hotels in markets where the barriers to entry were high. The portfolio transformation of 2010–2015 sharpened this into an explicit strategy: exit secondary markets, concentrate in supply-constrained locations, and accept a smaller portfolio if it means a higher-quality one.

The post-COVID pivot to leisure and resort assets was the ultimate expression of this philosophy. Today, DiamondRock owns thirty-five hotels compared to over forty at its peak, but the revenue per room and the margins on each property are meaningfully higher. The portfolio generates more EBITDA from fewer rooms — the definition of quality over quantity in real estate investing.

The second pillar is balance sheet conservatism as a competitive weapon. Every lodging REIT preaches balance sheet discipline during good times. DiamondRock actually practices it.

The company's current net debt-to-EBITDA ratio of 3.7x is conservative by REIT standards. The portfolio is fully unencumbered. There are no debt maturities until 2028. There are $468 million of total liquidity. This is not just financial prudence — it is a strategic advantage.

When the next downturn comes, and in hospitality it always comes, DiamondRock will have the ability to buy when competitors are forced to sell, to hold assets when others must liquidate, and to negotiate with lenders from a position of strength rather than desperation. The company bought the $495 million Blackstone portfolio in 2012 precisely because it had the balance sheet strength that peers lacked during the GFC recovery. The pattern will repeat.

The third pillar is active capital recycling. DiamondRock does not buy hotels and hold them forever. The company continuously evaluates every asset against two questions: is this hotel earning the best risk-adjusted return available, and is the capital deployed here more valuable than the capital would be if redeployed elsewhere?

The answer drives a relentless cycle of buying, selling, renovating, and rebranding. Since 2010, DiamondRock has recycled billions of dollars through this process. The discipline shows in the numbers: in 2021 alone, the company recycled $220 million from low-yield, encumbered properties into $293 million of higher-quality, unencumbered hotels and resorts. This willingness to sell hotels — even profitable ones — when the capital can be deployed more effectively elsewhere is rarer than it sounds. Many hotel owners fall in love with their assets and hold too long. DiamondRock has demonstrated the emotional discipline to sell winners when the risk-reward no longer justifies the capital allocation.

The fourth pillar is intense asset management without operational control. DiamondRock does not employ a single hotel general manager, but it employs a team of asset management professionals who function as sophisticated overseers of the third-party operators running each property. They scrutinize labor models, energy costs, revenue management strategies, renovation scopes, and marketing plans. They negotiate with brands on franchise fees, loyalty program assessments, and contract terms. They push operators to outperform their budgets and hold them accountable when they do not. The Sedona integration — combining two separate properties into a unified resort that generated more revenue and margin than the two had independently — is a textbook example of asset management value creation.

There is a fifth, less obvious element: the willingness to rebrand and reposition. Most hotel REIT owners view brand affiliation as essentially permanent — you buy a Marriott, it stays a Marriott, end of story. DiamondRock has taken a more entrepreneurial approach, treating brand identity as another lever of value creation. The Vail Marriott became The Hythe, a Luxury Collection Resort. The Hilton Boston Downtown became The Dagny Boston. The Hilton Burlington became Hotel Champlain, Curio Collection. The Conrad Chicago became The Gwen. Each rebranding required significant capital investment, operational disruption, and the nerve to bet that a new identity would command higher rates than the legacy brand. The track record on these repositionings has been strong — ADR lifts of fifteen to thirty percent are typical when a commodity chain hotel is transformed into a distinctive lifestyle property — which validates the thesis that DiamondRock's asset management team adds value not just through cost control but through creative vision.

The REIT structure itself creates both advantages and constraints that shape every decision. The advantage is obvious: no corporate-level income tax, which means more cash flow available for distributions, reinvestment, and debt reduction. The constraint is equally significant: REITs must distribute at least ninety percent of taxable income, which limits the ability to retain earnings for reinvestment. DiamondRock has navigated this constraint by maintaining a relatively conservative dividend payout — currently about thirty percent of adjusted FFO — while relying on external capital markets for growth capital. The low payout ratio gives the company room to absorb downturns without cutting the dividend, a lesson learned the hard way during COVID. It also means that when DiamondRock does raise the dividend, as it has in each of the past three years, investors can have confidence that the increase reflects genuine improvement in sustainable cash flow rather than a stretch to meet yield expectations.

The relationships with brand partners deserve special attention. DiamondRock's founding team came from Marriott, and that heritage has been both an asset and a potential limitation. The Marriott relationship gave DiamondRock preferential access to deals, favorable franchise terms, and the institutional trust that comes from shared history. But the company wisely diversified its brand relationships over time, adding Hilton, Hyatt, IHG, and Kimpton to the portfolio mix. This brand diversification serves two purposes: it prevents over-dependence on any single franchisor, and it creates competitive tension among brands vying for DiamondRock's business. When DiamondRock decides to rebrand a hotel, Marriott, Hilton, and Hyatt are all competing to win the franchise agreement — a dynamic that gives the owner more favorable terms than a single-brand portfolio could command.

For investors evaluating DiamondRock or any lodging REIT, the lesson is that hospitality is inherently cyclical. The question is not whether the next downturn will come but whether management has the balance sheet, the discipline, and the institutional memory to turn adversity into opportunity. DiamondRock's track record across two major crises suggests it has internalized this lesson in a way that few competitors have matched.

XI. Power and Competitive Analysis

Porter's Five Forces

The threat of new entrants into DiamondRock's competitive space is a study in contradictions.

On one hand, forming a new lodging REIT and listing it on an exchange is straightforward — Pebblebrook did exactly that in 2009, raising capital during the depths of the GFC to buy distressed assets. Private equity firms and sovereign wealth funds compete aggressively for the same hotel assets. The capital is abundant; the barriers are low.

On the other hand, the individual hotel assets that DiamondRock owns sit in markets where new physical supply is extremely difficult to add. You cannot build a new hotel in Sausalito's Golden Gate National Recreation Area. You cannot replicate a beachfront resort in Key West or a lakeside property on the only stretch of accessible Lake Austin waterfront. The competitive moat exists at the asset level, not the corporate level. This is a crucial distinction — anyone can form a hotel REIT, but nobody can create the assets that DiamondRock already owns.

The bargaining power of suppliers — primarily the hotel brands and management companies — is substantial and growing. Marriott controls over 9,700 properties globally. Hilton manages more than 9,000. Their loyalty programs, Marriott Bonvoy and Hilton Honors, have hundreds of millions of members whose booking behavior is driven by points accumulation and elite status.

A hotel without brand affiliation faces severe distribution disadvantages. Franchise fees, loyalty assessments, and marketing contributions have been rising faster than room revenue, with loyalty program fees alone increasing over fifty percent in recent years. This fee creep is one of the hotel industry's most contentious issues — brand companies are effectively extracting an increasing share of hotel economics from owners.

DiamondRock's scale — thirty-five hotels, multi-brand relationships — provides some negotiating leverage, but the structural power asymmetry favors the brands. DiamondRock's strategic move toward independent hotels is, in part, an attempt to reduce this supplier power by removing the brand intermediary entirely.

The bargaining power of buyers — hotel guests — is moderate and mediated by technology. Corporate travel managers negotiate volume discounts. Leisure consumers use OTAs and metasearch engines to compare prices with unprecedented transparency. Airbnb provides an alternative for price-sensitive travelers.

But for premium branded hotels in desirable locations, the substitution options are limited. A corporate group booking a three-day conference at the Chicago Marriott Magnificent Mile does not have an Airbnb alternative. A luxury leisure traveler seeking the experience of L'Auberge de Sedona is not cross-shopping against a Holiday Inn Express. The more unique and experiential the hotel, the less price-sensitive the guest — which is precisely why DiamondRock has pivoted toward distinctive resort properties.

The threat of substitutes — primarily Airbnb and alternative accommodations — is real but segment-specific. Research indicates that Airbnb's strongest impact falls on lower-tier and midscale hotels in leisure and seasonal markets. Upper-upscale branded hotels, where DiamondRock concentrates, are relatively insulated for several reasons: business travelers require the reliability and amenities of a branded hotel; group and convention business cannot be accommodated by vacation rentals; and loyalty program members are incentivized to stay within brand ecosystems. However, the vacation rental market has permanently expanded the supply of accommodation options, particularly in resort destinations, and has reduced the pricing power that traditional hotels once enjoyed during peak demand periods. DiamondRock's pivot toward experiential, full-service resorts — where the on-site dining, spa, and activity programming constitute a major part of the value proposition — is, in part, a strategic response to the Airbnb threat. A vacation rental can replicate a hotel room; it cannot replicate a resort experience.

Competitive rivalry is the most intense force in the framework. DiamondRock competes with Host Hotels, Pebblebrook, RLJ Lodging, Apple Hospitality, Sunstone, Park Hotels, and a deep bench of private equity firms and institutional investors for the same finite pool of premium hotel assets. When a desirable property comes to market, multiple bidders with access to cheap capital drive prices up and cap rates down. Returns are compressed in hot markets. The rivalry extends to the public markets, where investors compare dividend yields, FFO multiples, and NAV discounts across the peer set with surgical precision. The lodging REIT sector is also subject to periodic waves of consolidation — Pebblebrook's hostile pursuit of LaSalle Hotel Properties in 2018, Blackstone's take-private of Extended Stay, and various private equity rollups — that reshape the competitive landscape. DiamondRock, at roughly $2 billion in market cap, is large enough to be relevant but small enough to be an acquisition target, which adds a layer of strategic optionality for shareholders.

Hamilton's Seven Powers

The most useful framework for understanding DiamondRock's competitive position is Hamilton Helmer's Seven Powers. Scale economies offer limited advantage in lodging — each hotel is a discrete operation, and corporate overhead is a small fraction of total costs. There are no network effects. Counter-positioning against integrated operators like Marriott or Hilton is modest — the pure-ownership model is different, but not defensibly so. Switching costs are asymmetric: hotel guests face high switching costs due to brand loyalty programs, but DiamondRock faces relatively low switching costs because it can change brands and operators when contracts expire.

DiamondRock has no brand power of its own. When guests book a room at the Chicago Marriott or the Westin San Diego, they are buying the Marriott or Westin brand experience. DiamondRock is invisible to the consumer. This is a structural feature of the asset-ownership model: the owner captures the residual cash flow but never builds direct consumer equity.

The two powers that DiamondRock does possess are the ones that matter most. The first is cornered resource — irreplaceable hotel locations in supply-constrained markets. Cavallo Point in a national park. Henderson Park Inn on Destin's beachfront. Lake Austin Spa Resort on the only accessible waterfront. L'Auberge in Sedona's red rock country. Chico Hot Springs at Yellowstone's doorstep. These are assets that cannot be replicated, and their scarcity value appreciates over time as travel demand grows while new competitive supply remains physically impossible.

The second is process power — a deeply embedded culture of disciplined capital allocation and intense asset management that has been refined through two existential crises. Process power is hard to measure and easy to dismiss, but it shows up in the data: DiamondRock's portfolio transformation generated measurable improvements in RevPAR, margins, and returns on invested capital over time. The ability to buy the Blackstone portfolio at the right price, to exit Frenchman's Reef at the right time, to pivot toward leisure assets before the pandemic validated the thesis — these are not lucky accidents but the outputs of a culture that consistently makes good capital allocation decisions.

The verdict: DiamondRock's moat is modest but real. In a structurally competitive industry where capital is abundant and differentiation is difficult, the combination of scarce physical assets and disciplined capital allocation is sufficient to generate excess returns over full cycles — not a wide moat, but enough to reward patient investors who understand what they own. The key insight from both frameworks is that DiamondRock's competitive advantages reside at the asset level, not the corporate level. The company itself could theoretically be replicated — but the specific hotels it owns, in the specific locations it has assembled them, cannot be. That distinction matters enormously for long-term investors.

XII. Bull vs. Bear Case and What to Watch

The Bull Case

The strongest argument for DiamondRock rests on the intersection of three forces: durable leisure travel demand, historically constrained hotel supply, and a balance sheet positioned for opportunistic action.

U.S. hotel supply growth is currently running at roughly half a percent annually, well below the long-term average of 1.3 percent, because elevated construction costs and high interest rates have made new hotel development uneconomical in many markets. For existing owners of premium properties, this is an ideal environment — demand grows, supply does not, and pricing power improves. This is the rare moment in the lodging cycle where the supply-demand dynamics favor incumbents.

DiamondRock's portfolio is specifically designed to benefit from the post-pandemic travel landscape. Over sixty percent of the portfolio is leisure-focused, skewed toward the experiential, destination-driven travel that has proven most resilient. The independent and lifestyle hotels — The Hythe in Vail, The Dagny in Boston, L'Auberge in Sedona, Cavallo Point in Sausalito — command premium rates and attract the kind of high-spending traveler least sensitive to economic cycles. The company's 2025 comparable RevPAR of $207 represents healthy pricing power, and the 2026 guidance calls for further growth.

The balance sheet is a weapon waiting to be deployed. With net debt-to-EBITDA of 3.7x, no maturities until 2028, a fully unencumbered portfolio, and $468 million of liquidity, DiamondRock has the firepower to make acquisitions when the next downturn forces weaker competitors to sell. Management has demonstrated this ability repeatedly — the 2012 Blackstone deal, the 2021–2022 leisure acquisition spree, the opportunistic share buybacks at prices management considered deeply undervalued. The share repurchase program has already retired nearly thirteen million shares at an average price well below the current stock price, boosting per-share metrics for remaining shareholders.