Domo Inc.: The Business Intelligence Bet That Went Public

I. Introduction & Episode Roadmap

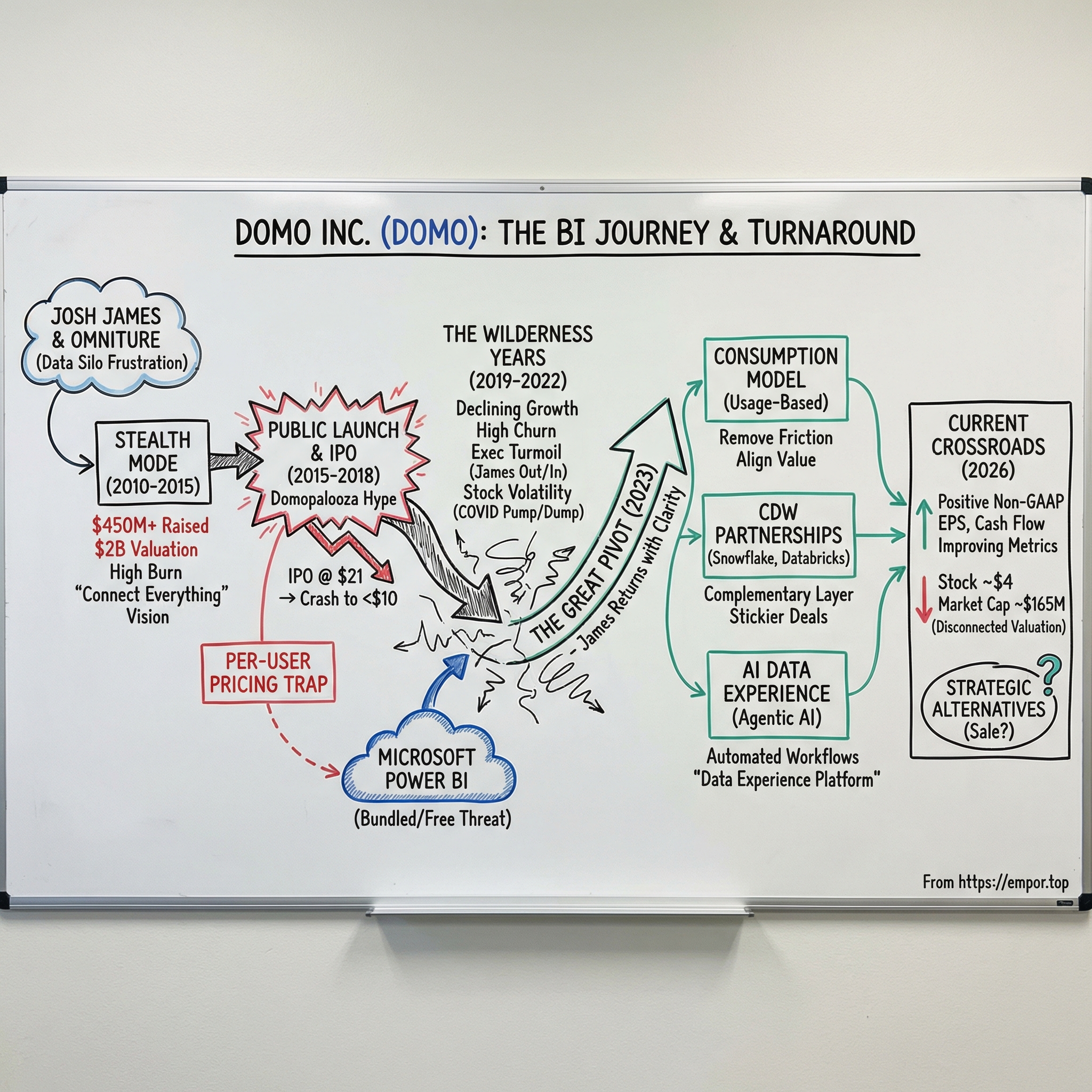

Picture this: it is 2015, and in the middle of Utah's Silicon Slopes, a company nobody outside the tech world has heard of is quietly burning through hundreds of millions of dollars. Its founder, a man who had already sold a company to Adobe for nearly two billion dollars, is telling investors that he is building the future of how every business on earth will interact with its data. The company is called Domo. The valuation has just hit two billion dollars. And it has not yet launched a single product publicly.

Fast forward to today, and Domo trades on the NASDAQ at roughly four dollars per share, with a market capitalization of about a hundred and sixty-five million dollars, less than a quarter of the venture capital that was poured into it. The company just announced it is exploring "strategic alternatives," which in corporate-speak means the board is open to selling the company. How did one of the most heavily funded SaaS startups in history, led by a proven entrepreneur, end up here?

The Domo story is not a simple tale of failure. It is something more nuanced and arguably more instructive: the story of a genuinely ambitious product vision colliding with a market that became savagely competitive, a business model that created the wrong incentives, and a public offering that came at precisely the wrong moment. It is also, in its latest chapters, a story of reinvention. Because after years of stagnation and a stock price that fell ninety percent from its highs, Domo executed one of the most aggressive business model pivots in enterprise software history, switching from per-user licensing to consumption-based pricing while simultaneously rebuilding its go-to-market engine around cloud data warehouse partnerships.

This episode covers the full arc: Josh James's Omniture origin story and the frustration that birthed Domo, the audacious stealth-mode strategy that consumed a quarter billion dollars before anyone knew the product existed, the public launch into an increasingly crowded BI market, the IPO that priced below expectations and then cratered, the wilderness years of declining growth and existential doubt, the consumption model gamble, and finally, the recent turnaround signals that have brought Domo to its current crossroads. The board hired Jefferies in February 2026 to explore a sale. Whether this story ends in acquisition, a standalone comeback, or something else entirely remains to be written. But the journey to this point is a masterclass in the brutality of enterprise software markets and the thin line between visionary and overextended.

II. Founding Context & Josh James's Origin Story

The Omniture Foundation (1996-2009)

To understand Domo, you have to understand Josh James, and to understand Josh James, you have to go back to a dorm room at Brigham Young University in the mid-1990s. James was a classic entrepreneurial archetype: restless, ambitious, and utterly convinced that the internet was going to change everything about business. In 1996, while still in college, he co-founded a company called Omniture, which would become one of the defining web analytics platforms of its era.

The timing was both perfect and terrible. Perfect because the internet was exploding, and every company suddenly needed to understand what was happening on its website. Terrible because the dot-com bubble was inflating, and when it burst in 2000-2001, it nearly wiped out every internet-adjacent company in existence. Omniture survived, which in itself was a remarkable accomplishment. Most of its competitors did not. James navigated the company through the bust, kept the lights on, and emerged on the other side with a product that was becoming essential infrastructure for online businesses.

By the mid-2000s, Omniture was the dominant player in web analytics. It went public in 2006, becoming the second-best-performing technology IPO of that year, and earned the distinction of being the number one returning venture investment out of over a thousand venture capital investments in 2004. James himself earned a distinction he would carry with him: he became one of the youngest CEOs of a public company listed on NASDAQ or the New York Stock Exchange. He was brash, competitive, and deeply product-oriented. He built Omniture into a platform that companies simply could not run their digital businesses without.

Then, in 2009, Adobe came calling. The acquisition price was $1.8 billion, a number that validated everything James had built over thirteen years. At the time, it was one of the largest SaaS acquisitions ever. James could have stayed at Adobe, collected his payout, and settled into the comfortable life of a successful tech executive. He did not. The "entrepreneur's itch" was too strong, and more importantly, he had identified a problem during his years running Omniture that he believed was far bigger than web analytics.

The Genesis of Domo (2010)

The frustration was simple but profound. As CEO of Omniture, James had access to every web analytics metric imaginable. But when he wanted to see how that data connected to sales numbers, HR metrics, financial performance, or supply chain data, he hit a wall. The information existed, but it lived in dozens of different systems, managed by different teams, accessible only through different tools. Getting a unified view of his own business required waiting days or weeks for IT to pull reports together.

"Why couldn't I see all my data in one place in real-time?" became the founding question of Domo. James believed that business intelligence, as it existed in 2010, was fundamentally broken. The tools were too complex, requiring specialized training and SQL knowledge. They were too slow, delivering reports that were already stale by the time they arrived. And they were too IT-dependent, creating bottlenecks where business users had to submit requests and wait for analysts to fulfill them.

The mechanics of the founding were characteristically unorthodox. In October 2010, James incorporated a company called Shacho, Inc. Two months later, Shacho acquired Corda Technologies, a Lindon, Utah-based data visualization firm that gave the new venture an immediate technical foundation and engineering team. James then renamed the entity to Domo, Inc. The Corda acquisition was a shrewd move: rather than building visualization capabilities from scratch, James acquired a team that already knew how to render data beautifully, then layered on the data integration and cloud infrastructure that would differentiate the platform.

His vision for Domo was radical in its ambition: build a cloud-native, mobile-first business intelligence platform that could connect to every data source a company used, visualize that data in real-time, and put it directly into the hands of every employee, not just analysts and executives. This was 2010, when enterprise mobile was still deeply controversial. The idea that a CEO would make strategic decisions by looking at a dashboard on an iPhone struck many enterprise veterans as absurd. The cloud infrastructure to support such a platform was just barely mature enough to make it technically feasible.

But James had the conviction of someone who had lived the problem, and more importantly, he had the track record to convince investors that he could solve it. The timing was not accidental. Cloud computing was maturing rapidly thanks to Amazon Web Services, mobile adoption was exploding with the iPhone and iPad, and the concept of "big data" was transitioning from academic buzzword to corporate obsession. The ingredients were all there. James just needed capital, time, and secrecy.

III. The Stealth Years & Building in Secret (2010-2015)

The Unusual Strategy

What Josh James did next was almost unprecedented in the SaaS world: he took the company completely dark. Domo operated in stealth mode for nearly five years, from its founding in late 2010 until April 2015. During that period, it raised hundreds of millions of dollars, hired hundreds of engineers, accumulated over a thousand clients, and generated more than $100 million in annual revenue, all while revealing almost nothing publicly. In an industry where startups typically crave attention, launch with minimum viable products, and iterate publicly, Domo's silence was deafening.

The strategy was deliberate and rooted in hard-won experience. At Omniture, James had watched competitors study his product roadmap and copy features before he could bring them to market. He was determined not to repeat that mistake. By staying in stealth, Domo could build its connector library, perfect its mobile experience, and develop its platform architecture without giving Tableau, Microsoft, or anyone else a playbook to follow.

The luxury of this approach came down to one thing: Josh James's credibility. Having delivered a $1.8 billion exit, he had the kind of track record that opens checkbooks without PowerPoint presentations. When he told investors he was building the next great enterprise platform, they believed him, even when he would not show them the product in detail.

Building the War Chest

The fundraising during the stealth years was staggering and meticulously staged. A $33 million Series A from Benchmark Capital in July 2011 signaled serious intent. A $60 million Series B followed, bringing in GGV Capital and Greylock Partners. Then came the Series C in February 2014: $125 million from TPG Growth, T. Rowe Price, and Viking Global Investors, valuing the company at $825 million. By the time Domo finally emerged from stealth in April 2015 with a $200 million Series D led by BlackRock, the total capital raised stood at roughly $450 million, and the valuation hit $2 billion. The investor roster read like a who's who of Silicon Valley and Wall Street: Benchmark, IVP, Andreessen Horowitz, GGV Capital, Greylock Partners, BlackRock, Capital Group, and Glynn Capital, thirty-nine investors in total, thirty-six of them institutional.

The hot SaaS market of the early 2010s combined with James's pedigree created a perfect storm of investor appetite. But even at the time, the burn rate raised eyebrows among those who knew about it. Building a platform with hundreds of pre-built data connectors, a mobile-first interface, cloud-native architecture, and enterprise-grade security was extraordinarily expensive. Domo was not building a simple dashboarding tool. It was building an entire data platform from scratch, and every connector required engineering work to build, test, and maintain. The question of whether this spending was an investment in a massive future opportunity or an unsustainable burn rate would not be answered for years.

Product Philosophy & Technical Bets

The product vision that emerged from the stealth years was genuinely ambitious. Domo conceived of itself as an "app store for business," a concept that was ahead of its time. The idea was that on top of the core data platform, you could build and share purpose-built data applications: a marketing dashboard, a supply chain tracker, an HR analytics suite. Each would be a self-contained "app" that connected to the relevant data sources and presented information in a domain-specific way.

The cloud-native architecture was another bold bet. In 2010, many enterprise software companies were still offering on-premises or hybrid deployment options, hedging their bets on whether CIOs would trust the cloud with their most sensitive data. Domo went all-in on cloud, which meant it did not have to deal with the complexity of supporting multiple deployment models but also limited its addressable market to companies willing to put their data in the cloud.

The mobile-first approach was perhaps the most controversial decision. Enterprise software in 2010 was designed for desktop browsers and large monitors. The idea that a CFO would pull up a financial dashboard on an iPhone during a board meeting was, to put it mildly, not the consensus view. But James was convinced that mobile was where the world was heading, and he wanted Domo to be there first. Building what would eventually grow to over a thousand pre-built connectors, covering everything from Salesforce to SAP to Google Analytics to obscure industry-specific databases, was the most engineering-intensive part of the vision. Each connector had to be built, maintained, and updated as the underlying APIs changed. To appreciate the scale of this undertaking, consider that each connector is essentially a small software application that must authenticate with an external system, understand its data schema, handle rate limits and API changes, transform the data into a standardized format, and maintain reliability over time. Multiplied by a thousand, this is the kind of engineering investment that creates a genuine technical moat, but also one that consumes an enormous amount of capital.

The hiring spree that accompanied all of this drew heavily on Omniture alumni, people who had built and scaled enterprise software with James before and trusted his vision. The company's Utah base became both an advantage and a constraint: it could hire talented engineers at lower costs than San Francisco, but the talent pool for enterprise SaaS experience was smaller.

The Competitive Landscape They Were Entering

While Domo built in secret, the business intelligence market was undergoing its own transformation. Tableau had gone public in 2013 to enormous fanfare, proving that there was massive demand for self-service data visualization. Tableau's approach was different from Domo's: it was desktop-first, designed for analysts and power users, and focused primarily on visualization rather than data integration. But its IPO success sent a clear signal that the BI market was hot.

The old guard, SAP BusinessObjects, Oracle BI, and IBM Cognos, was expensive, complex, and deeply entrenched in large enterprises. These were the incumbents that Domo hoped to displace, but they had the advantage of existing relationships and the inertia of enterprise IT decisions.

More ominously, new competitors were emerging. Looker was gaining traction with its modern approach to data modeling. Qlik had a loyal following. And in a development that would prove fateful for Domo, Microsoft was quietly developing what would become Power BI, a tool that would eventually be offered for free or nearly free as part of the Office 365 bundle that most enterprises already paid for. The question hanging over Domo's stealth period was whether there was room for another full-platform player, or whether the market was already becoming too crowded for a latecomer with a premium price tag.

IV. The Public Launch & Rapid Scaling (2015-2017)

Coming Out of Stealth (April 2015)

When Domo finally pulled back the curtain in April 2015, it did so with characteristic Josh James showmanship. The coming-out party coincided with the $200 million Series D fundraise and a $2 billion valuation, numbers designed to generate headlines and signal that this was not another small startup hoping to be noticed. The company launched with a massive customer showcase and the inaugural Domopalooza conference, an annual event that would become the company's tentpole marketing moment. The name itself, a playful riff on Lollapalooza, signaled that Domo wanted to be the cool kid in a category full of stodgy enterprise vendors. This was not your father's business intelligence tool.

The initial customer traction was more advanced than most observers expected. By the time of the public launch, Domo already had over a thousand clients, a figure that stunned industry watchers who had assumed the company was still in early pilot stages. The use cases ranged from marketing analytics to executive dashboarding to operational monitoring, and the company was already generating more than $100 million in annual revenue. These were not typical stealth-mode numbers.

But the market reception was decidedly mixed. Analysts and journalists were excited about the vision, the breadth of the platform, and the energy behind it. At the same time, the skepticism about the burn rate was immediate and vocal. Even with a thousand customers and meaningful revenue, the company had consumed vastly more capital than it had generated in sales, entering a market where Tableau was already dominant and Microsoft was circling. The bulls saw a platform that could transform how companies used data. The bears saw a cash incinerator entering a knife fight.

The Growth-at-All-Costs Era

From 2014 through 2016, Domo executed the playbook that defined the era: grow revenue as fast as humanly possible, worry about profitability later. Sales and marketing spend went through the roof as Domo built out an enterprise sales force capable of competing for large deals against Tableau, SAP, and Oracle. The company hired aggressively, poaching talent from Salesforce, Workday, and other enterprise SaaS leaders.

Domopalooza became an annual spectacle, growing each year and serving as both a customer engagement tool and a marketing statement. The conference attracted thousands of attendees and generated significant buzz in the data analytics community. Product development continued at a rapid pace, with Domo adding Buzz (a collaboration layer that allowed users to discuss data within the platform), workflow capabilities, and a social layer designed to make data consumption a collaborative rather than solitary activity.

The unicorn valuation arrived on schedule. By 2015, Domo was valued at more than two billion dollars, making it one of the most valuable private SaaS companies in the world. For James, this was validation that his vision was resonating. For investors, it meant their early bets were generating impressive paper returns. For employees, it meant their equity packages looked enormously valuable.

Key Strategic Decisions & Their Implications

Several strategic choices made during this period would have lasting consequences. The most significant was the upmarket push: Domo targeted large enterprises rather than small and medium businesses. This meant higher annual contract values but longer sales cycles, more complex implementation requirements, and a customer base that demanded enterprise-grade features like security, governance, and integration capabilities.

The pricing strategy was aggressively premium. Domo positioned itself as a high-end platform, with per-user licensing that could make deals expensive as organizations tried to roll out the platform broadly. This created an awkward tension at the heart of the business model: Domo's value proposition was "data at everyone's fingertips," but the pricing model penalized companies for putting it in everyone's hands. The more users you added, the more you paid, which created natural resistance to the kind of viral, bottom-up adoption that was driving growth at other SaaS companies.

The partner ecosystem was nascent, and geographic expansion into Europe and other international markets began but remained a secondary priority behind domestic growth. These were reasonable decisions at the time, but they left Domo without the distribution advantages that partner channels would later prove essential.

In hindsight, the per-user pricing trap was the most consequential decision of this era. Consider the math: if a Fortune 500 company wanted to give five thousand employees access to Domo dashboards, the cost could run into seven figures annually. That same company could give those five thousand employees Power BI access for a fraction of the cost, or nothing at all if they already had Office 365 licenses. The pricing model that funded Domo's growth was simultaneously capping its market opportunity.

The BI Market Heats Up (2015-2016)

The event that would most shape Domo's future happened not in American Fork, Utah, but in Redmond, Washington. In 2015, Microsoft launched Power BI with an aggressively low price point and, critically, bundled it with Office 365, the productivity suite that most enterprises already owned. Suddenly, the marginal cost of adding basic business intelligence for many companies dropped to essentially zero.

This was a seismic shift. Tableau continued to dominate among analysts and data professionals, but Power BI's near-free price point and integration with Excel, a tool that every business user already knew, created a powerful gravitational pull. Looker was gaining momentum among companies embracing the "modern data stack" narrative. Amazon launched QuickSight. Google was building what would become Data Studio. The BI market, which had seemed wide open when Domo began its stealth period, was becoming one of the most competitive categories in enterprise software.

For Domo, the realization was sobering. Mobile-first design and an integrated platform were genuine differentiators, but were they enough to justify a significant price premium over tools that were free or nearly free? The company's "connect to everything" vision was powerful, but competitors were rapidly building their own connector libraries. The question of defensibility, which had been easy to wave away when the product was still in stealth and the market was less crowded, was becoming unavoidable.

V. The IPO Decision & Public Market Reality (2017-2018)

The Road to IPO

By the time Domo began seriously preparing for its IPO, the company had raised more than $700 million in total venture capital across eleven funding rounds. A $131 million Series D extension in March 2016 and an additional roughly $200 million round in April 2017, again led by BlackRock, had pushed the peak private valuation to $2.3 billion and the total capital raised past the $700 million mark, making it one of the most heavily funded private SaaS companies in history. That number alone tells a story. At some point, private investors need liquidity. The late-stage investors who had written nine-figure checks at the two billion dollar valuation needed an exit, and the most straightforward path was a public offering.

The market timing window appeared favorable. SaaS companies were commanding premium multiples in the public markets. Investors had an appetite for high-growth, recurring-revenue businesses. And Domo's revenue growth, while decelerating, was still north of thirty percent annually. The pressure from investors, combined with the need for employee equity liquidity and the competitive dynamics of operating in a market where Tableau was already public, made the IPO feel inevitable.

Then came the S-1 filing, and for the first time, the outside world got an unfiltered look at Domo's financials. The picture was sobering. Revenue growth was strong but the losses were massive. The company was burning through cash at an alarming rate, with sales and marketing expenses consuming a disproportionate share of revenue. The S-1 also revealed a dual-class share structure that would give Josh James effective control of the company regardless of public shareholder sentiment, a structure that had become fashionable in tech but that governance-minded investors viewed skeptically.

The initial market cap at IPO was roughly $511 million, a staggering discount from the $2 billion-plus private valuation. For late-stage investors, this was effectively a down round conducted in public, a painful outcome that eroded trust and signaled that the private market valuation had been inflated.

IPO Day & Immediate Aftermath (June 2018)

Domo priced its IPO at twenty-one dollars per share on June 28, 2018, offering 9.2 million shares of Class B common stock and raising $193 million. The pricing was below the initial target range, an early sign that institutional investors were not as enthusiastic as the company had hoped. On the first day of trading, June 29, shares opened at $23.80 and closed at $27.30, a 30 percent gain that briefly generated optimism. Josh James rang the NASDAQ bell. At the time, the company reported fiscal year 2018 revenue (ended January 2018) of $108.5 million, with net losses of $176.6 million, a staggering loss-to-revenue ratio that underscored just how much the company was spending to grow.

But the first-day pop proved fleeting, and the slide began almost immediately.

Within months, the stock had fallen below fifteen dollars, then below ten. The valuation reset was brutal: from more than two billion dollars in private markets to sub-eight hundred million, then sub-five hundred million in public markets. Analysts zeroed in on the fundamental question that had always lurked beneath the surface: what was the moat? What made Domo defensible against Microsoft, which could give Power BI away for free, or Tableau, which had a massive installed base and devoted user community?

The public market reception exposed every weakness that private market dynamics had allowed to remain hidden. Customer acquisition costs were too high relative to lifetime value. Product differentiation against Tableau and Power BI was not clear enough to justify the premium pricing. The per-user licensing model limited expansion within existing accounts. And the "Rule of 40" metric that SaaS investors use to evaluate companies, which sums revenue growth rate and profit margin, was deeply negative.

What Went Wrong: The Honest Post-Mortem

The timing was arguably the most significant factor. Domo went public in June 2018, just as the market narrative around unprofitable growth companies was beginning to shift. The era of "growth at all costs" was not quite over, but cracks were forming. Investors were starting to ask harder questions about paths to profitability and unit economics.

But timing alone does not explain what happened. The competitive moat question was real and damaging. Microsoft's decision to bundle Power BI with Office 365 was an existential threat to every standalone BI vendor, but it was particularly acute for Domo because Domo's pricing model made it expensive at scale. If a Fortune 500 company could get "good enough" business intelligence for free through a Microsoft license it already owned, the burden of proof for spending millions on Domo was enormous.

The S-1 also revealed related party transactions that, while not illegal, did not inspire confidence. Domo had paid $1.8 million to JJ Spud, an aircraft leasing company controlled by Josh James, for private plane usage between 2016 and 2018. The company spent approximately $300,000 per year on catering from Cubby's Chicago Beef, a restaurant owned by James and his brother. And roughly $200,000 went to Alice Lane Home Collection, an interior design firm connected to another James family member. The total was about $2.6 million, not a material sum relative to the company's spending, but the optics were terrible for a company asking public investors to trust its fiscal discipline.

Market Context

The broader BI market was sending mixed signals. Tableau was doing well as a public company, but in June 2019, Salesforce acquired it for $15.7 billion, a deal that simultaneously validated the category's value and signaled that consolidation was coming. The acquisition price was remarkable: roughly twelve times trailing revenue, reflecting Tableau's position as the category leader with strong growth and a devoted user community. For Domo investors, the Tableau acquisition was bittersweet. It proved that BI companies could command enormous valuations, but only if they had established clear market leadership. The message was clear: in a market dominated by massive platform companies like Microsoft and Salesforce, the window for independent BI players to build standalone businesses was narrowing. Domo was left as one of the few independent pure-play BI companies, and the stock market was not rewarding independence.

VI. The Wilderness Years: Struggling for Traction (2019-2023)

Facing Reality

The years following the IPO were grueling and, in one brief interlude, surreal. Domo's stock price drifted steadily downward through 2019 and into 2020, from the low teens to single digits. Each quarterly earnings report brought the same dispiriting pattern: revenue growth decelerated, losses persisted, and the competitive environment intensified.

Then came the pandemic. In 2020 and 2021, as remote work accelerated digital transformation and investors poured money into every SaaS company with a pulse, Domo's stock caught the wave. In a period of irrational exuberance for cloud software, the stock briefly touched $97.70 on August 26, 2021, an all-time high that valued the company at over $3 billion. For a few intoxicating months, it appeared that the market had come around to Domo's vision. Investors who had been underwater since the IPO were suddenly in the money. Employees saw their equity packages explode in value.

But the pandemic rally masked the underlying business dynamics. Revenue growth was healthy but not exceptional by SaaS standards, and the valuation was being driven by multiple expansion across the entire software sector, not by Domo-specific improvements. When the tech bubble deflated in 2022, Domo's stock collapsed even faster than it had risen, eventually giving back all of the pandemic gains and then some. The crash was brutal: from nearly $98 to single digits in the space of eighteen months.

Underneath the stock price volatility, the customer retention numbers told the most important story. Net retention rates, the metric that measures whether existing customers are spending more or less over time, were declining. This meant that even as Domo signed new customers, existing customers were either churning or reducing their spend. For a SaaS company, declining net retention is a death spiral indicator: it means the business is a leaky bucket, and you have to acquire ever more new customers just to stay in place.

The competitive losses were accelerating. CIOs facing budget pressure found it increasingly difficult to justify Domo's premium pricing when Power BI was essentially free with their Microsoft licenses. Salesforce customers migrated their BI needs to Tableau, which now sat within the same ecosystem as their CRM. Companies building modern data stacks chose Looker for its integration with Google Cloud. Even the smallest competitors were eating into Domo's addressable market: ThoughtSpot offered a search-first analytics experience, Sisense targeted embedded analytics, and open-source tools like Metabase and Apache Superset provided basic BI capabilities for free. With an estimated market share of under one percent in the broader BI sector, Domo was a small player in an increasingly consolidated market. The differentiation that James had spent years building, the breadth, the mobile capabilities, the connector library, was real but insufficient to overcome the pricing and ecosystem advantages of larger competitors.

CEO Transition Chaos (2022-2023)

In March 2022, Josh James stepped down as CEO, and John Mellor, who had served as Domo's Chief Strategy Officer since 2019, was promoted to the top job. James had recruited Mellor three years earlier, and the transition was positioned as a planned evolution rather than a crisis response. Mellor was a seasoned enterprise executive with the kind of operational discipline that Wall Street tends to reward.

Mellor's mandate was clear: fix the operations, find a path to profitability, stop the bleeding. He launched cost-cutting initiatives and began restructuring the sales organization. But the fundamental problem was not operational execution; it was strategic positioning. Cutting costs while growth continued to slow felt like managing decline rather than creating a new trajectory. The internal disruption of a leadership change, combined with the uncertainty it created among customers and employees, arguably made things worse in the short term.

In March 2023, barely a year later, Mellor stepped down as both CEO and board director. Josh James was reinstated as CEO, bringing David Jolley as the new CFO and Jeff Skousen as Chief Revenue Officer. Board Chair Dana Clark stated the board was "pleased to welcome Josh back at the helm," noting his "true entrepreneurial spirit." The diplomatic language could not disguise the underlying message: the professional-manager approach had not worked, and the company needed its founder's urgency and conviction.

Josh Returns with Clarity

The circumstances of James's return were not triumphant. The stock was trading in single digits, down more than ninety percent from its post-IPO highs. Market capitalization had fallen below the total amount of venture capital raised, a humbling benchmark that meant the company had destroyed value in aggregate for its investors. Employee morale was fragile. Customer churn was increasing.

But James came back with something he had not had before: clarity about what needed to change. The years of struggling had stripped away the ambiguity. The data was unambiguous on two points. First, customers who fully embraced the Domo platform, who connected multiple data sources, built numerous dashboards, and integrated it into their daily workflows, loved it and stayed. Second, the per-user licensing model was the single biggest barrier to customers reaching that level of engagement.

If a company paid per user, there was always a gatekeeper counting heads, always someone deciding who "needed" access and who did not. This was the opposite of the "data at everyone's fingertips" vision. The pricing model was actively undermining the product's value proposition.

The Strategic Review: What Must Change?

James and his team conducted a deep analysis of win/loss data, customer satisfaction surveys, and churn patterns. The conclusions pointed in one direction: Domo needed to eliminate the friction of per-user pricing and adopt a consumption-based model, where customers paid based on how much data they processed and how actively they used the platform, not how many people had access.

This was not a minor tweak. It meant rebuilding the company's revenue model, retraining the entire sales force, redesigning customer contracts, and accepting that near-term billings would be disrupted during the transition. For a company already struggling, deliberately making things worse before they got better required significant courage and board-level conviction.

The competitive analysis reinforced the conclusion. Companies were not just choosing Power BI because it was cheaper; they were choosing it because Microsoft had eliminated the friction of user-by-user procurement decisions. When a CIO could roll out Power BI to ten thousand employees with a single checkbox in their Microsoft admin console, asking those same CIOs to negotiate individual user licenses with Domo felt like asking someone to take a horse and buggy when a highway was available. Domo needed to compete on the same terms: make it easy to start, let value drive expansion, and charge based on usage rather than seat counts.

VII. The Great Pivot: Consumption Model Transformation (2023-2024)

The Consumption Model Decision (Fall 2023)

In the fall of 2023, Josh James made the call. Domo would migrate to a consumption-based pricing model, and it would do so fast. Not a gradual multi-year transition, but an aggressive push to move the majority of annual recurring revenue to the new model within a year. When James presented the plan to the board, the directive came back unequivocal: "Move as fast as you possibly can."

The strategic rationale was elegant in its simplicity. Under the old per-user model, a customer buying Domo for five hundred people was making a six-figure commitment before anyone had logged in. Under consumption pricing, the same company could start with unlimited users, pay nothing upfront, and only incur costs as people actually used the platform. This aligned Domo's revenue with the value customers received, reduced the friction of initial adoption, and removed the artificial ceiling that per-user pricing created on platform engagement.

Think of it this way: the old model was like selling gym memberships where you paid for each family member separately. The new model was like paying based on how many classes you actually attended. The first model discourages broad adoption; the second rewards engagement.

What Changed Operationally

The execution was remarkably fast for an enterprise software company. By the third quarter of fiscal year 2024, one hundred percent of new customer deals were on the consumption model, and fifty-five percent of existing annual recurring revenue had already been transitioned. In the fall of 2023, Domo launched a freemium tier, offering unlimited access to the platform with no time limit, letting potential customers connect their data and explore the product before committing any dollars. Within four months of the freemium launch, the number of users actively connecting data and exploring Domo had more than doubled.

The internal changes were just as sweeping. The entire compensation structure for sales representatives and customer success managers was overhauled to incentivize consumption-model transitions. A new customer adoption team was created with the specific mandate of expanding platform usage within existing accounts. The selling motion shifted from convincing a procurement committee to sign a large upfront contract to demonstrating value and letting usage grow organically.

Why This Was Radical and Risky

The near-term financial impact was significant and predictable. Multi-year, prepaid contracts under the old model provided predictable revenue and favorable cash flow dynamics. Consumption-based contracts, by nature, meant that revenue recognition shifted to follow actual usage, and billings became more variable. During the transition period, Domo's reported billings metrics would look worse even if underlying customer health was improving.

The sales cycle disruption was equally challenging. Enterprise sales representatives who had spent their careers selling traditional SaaS contracts had to learn an entirely new motion. Some adapted; others did not. The competitive vulnerability was real: during any business model transition, a company appears uncertain, and competitors exploit uncertainty. And there was always the "J-curve" risk: the possibility that performance would deteriorate significantly before the benefits materialized, potentially pushing the company past a point of no return.

The Cloud Data Warehouse Partnership Strategy

Simultaneously with the consumption model transition, Domo made another strategic pivot that would prove equally important. Rather than competing with cloud data warehouses like Snowflake, Databricks, Google BigQuery, and Oracle, Domo repositioned itself as their complement.

The logic was straightforward. Many large enterprises had invested heavily in cloud data warehouses, centralizing their data in platforms like Snowflake. But those warehouses were storage and processing engines, not visualization and analysis tools. Those companies still needed something to make the data actionable for business users. Domo's "Cloud Amplifier" feature allowed organizations to leverage their existing data warehouse investment while using Domo for the "last mile" of data consumption: dashboards, alerts, automated workflows, and embedded analytics.

The partnership strategy bore fruit faster than almost anyone expected. Year-to-date in 2024, the joint pipeline with cloud data warehouse partners went from zero deals to sixty. Partner-sourced deals closed at five to seven times the rate of internally generated leads, and the sales cycles were two to three times faster. By the time of the Q3 fiscal 2026 earnings call, more than 350 accounts were using Cloud Amplifier across nine different cloud data warehouses, a figure that had more than doubled year over year, with unique users on Cloud Amplifier up 450 percent.

The reason this worked was simple: CIOs wanted consolidated data strategy conversations. When a Snowflake or Databricks representative brought Domo to the table as a visualization and analytics layer, it simplified the CIO's decision-making. Domo went from being one of many BI tools competing for budget to being the recommended analytics layer within an existing strategic relationship. As James described it, these partner-led deals were "stickier" because they "involved CIOs and multiple vendors," creating a deeper, more strategic commitment than a standalone BI purchase.

The company added twenty-six new channel partners during this period, building a distribution network that had been notably absent during Domo's earlier years. Lead generation from strategic partners increased over twenty-five percent in Q3 fiscal 2026 compared to Q2, and more than doubled compared to Q1, showing accelerating momentum rather than one-time gains.

VIII. The Turnaround Emerges (2024-2025)

The First Positive Signal (August 2025)

For years, the quarterly earnings calls had been exercises in managing expectations downward. Then, in August 2025, something changed. Domo reported its second quarter of fiscal year 2026, and buried in the numbers was a milestone that had eluded the company for its entire public life: the first-ever positive non-GAAP earnings per share, at two cents.

The number was tiny in absolute terms but enormous in symbolic significance. After burning through more than $700 million in venture capital and accumulating hundreds of millions in operating losses, Domo had demonstrated, even if narrowly, that the business could make money. The stock surged nine percent, reaching near its fifty-two-week high. Adjusted free cash flow was positive at $1.4 million. CFO Todd Crane called it a milestone "that demonstrates the strength and momentum of our business."

Fiscal 2025 Full Year Results

The full fiscal year 2025 results, reported in early 2025, told a more complete story. Revenue was $317 million, essentially flat year over year, reflecting the billing disruption of the consumption model transition. But beneath that flat headline, the leading indicators were encouraging. Subscription remaining performance obligations grew fourteen percent year over year, reaching $403.6 million. More notably, the long-term portion of that RPO, commitments extending beyond twelve months, was up thirty-eight percent. Customers were not just renewing; they were signing longer contracts, a strong signal of increasing platform stickiness.

Operating cash flow turned positive at $8.9 million, a sixty-four percent improvement. Adjusted free cash flow was $6 million, up a hundred and five percent. The path to sustainable profitability, which had seemed like a fantasy during the wilderness years, was becoming visible.

The Breakthrough Quarter: Q3 Fiscal 2026 (October 2025)

The third quarter of fiscal 2026, reported in December 2025, delivered the clearest evidence yet that the turnaround was real. Non-GAAP operating margin reached positive seven percent, the highest in company history, representing a four percentage point improvement year over year. Non-GAAP earnings per share came in at one cent, beating analyst expectations of negative nineteen cents by a staggering margin, a hundred and five percent earnings surprise. Adjusted free cash flow was $2.1 million, a $15.8 million improvement from the year-ago quarter.

Revenue of $79.4 million came in near the high end of guidance. Subscription RPO reached $405.9 million, up fifteen percent. Eighty percent of annual recurring revenue was now on consumption contracts, up from negligible levels just two years earlier, with the company targeting eighty-five percent or higher by year-end.

The one blemish was billings of $73.2 million, which came in below guidance. James attributed this to longer-than-expected sales cycles in partner-led deals, not lost deals. "We didn't lose any deals, just timing shifted," he told analysts. The Q4 guidance called for billings of $107.5 million to $109.5 million, which would represent six percent year-over-year growth, what James characterized as "the fastest billings growth we've seen in over three years."

What Is Working Now

The consumption model has fundamentally changed the customer dynamic. By removing per-user friction, Domo enabled broader platform adoption within accounts, which in turn created more engagement, more data integrations, and higher switching costs. Net revenue retention for consumption-first customers reached 108 percent, meaning those customers were expanding their usage and spending faster than overall attrition. Overall gross retention improved to 86 percent from 83 percent a year earlier, with management guiding toward 87 percent in Q4, the highest in six quarters.

The AI features adoption surge has been another bright spot. Unique AI feature users more than doubled year over year, and Domo was ranked the number one vendor in Dresner Advisory Services' inaugural 2025 Wisdom of Crowds Agentic AI report, the fifth Dresner distinction the company earned that year.

Cost discipline finally took hold without gutting innovation investment. The company was simultaneously improving margins and investing in product development, a combination that had proved elusive for years. The gross margin held at approximately 75 percent, with subscription gross margins above 80 percent on a non-GAAP basis, demonstrating that the underlying business had strong economics once the cost structure was right-sized.

The debt situation was stabilized through a critical refinancing in August 2024: the term loan with BlackRock, approximately $100 million, was extended to mature in August 2028, with reduced interest rates and lower annual cash interest costs. The amendment provided the financial runway Domo needed to continue the consumption model transition and invest in the CDW partnership strategy without facing an imminent debt maturity cliff. Monthly active users across the customer base increased over ten percent year over year, a metric that validated the consumption model's core premise: remove friction, and people use the platform more.

The Strategic Alternatives Announcement

Then came February 19, 2026. Domo announced that its board of directors had initiated a formal process to explore strategic alternatives aimed at maximizing shareholder value. The options under consideration included a strategic investment, outright sale, business combination, or other transaction. Jefferies was retained as financial advisor, and Goodwin Procter as legal counsel.

The timing was telling. The company reaffirmed its fiscal 2026 revenue guidance of $317.5 million to $318.5 million and its non-GAAP net loss per share guidance of seven to eleven cents. The business was not in distress. Rather, the board appeared to be recognizing a disconnect: a company generating over $300 million in recurring revenue, with improving margins and positive free cash flow, was trading at roughly half its annual revenue. The market capitalization of approximately $165 million represented a fraction of the capital invested in the business.

James himself framed the decision thoughtfully: "Domo has made significant progress in strengthening our product platform and expanding our AI capabilities, and we believe this is an appropriate time to evaluate opportunities that may further drive our growth strategy and maximize shareholder value." He added that the company remains "focused on serving our customers who rely on Domo every day, supporting our employees, and growing our business." The dual message was clear: this is not a fire sale, but the board recognizes that the current market valuation does not reflect what has been built.

Whether this announcement leads to an acquisition, a take-private transaction, or simply serves as a catalyst for the stock price to better reflect the business's improving trajectory remains an open question. As of late February 2026, the stock traded around four dollars, having touched an all-time low of $3.45 on February 24. Analyst price targets ranged from $3.50 to $22, with an average target of $12.92 and six analysts covering the stock (three Strong Buy, two Hold, one Sell). The gap between the current price and the consensus view of value is unusually wide, suggesting either that analysts are wrong or that the market is pricing in a significant probability of a negative outcome.

IX. Product Evolution & AI Integration

From BI Platform to "Data Experience Platform"

Domo's product has evolved substantially from its original vision of a dashboarding tool. The current platform is better described as a data experience platform, a term the company has adopted to differentiate itself from traditional BI tools. The distinction is meaningful: traditional BI is about looking at charts and tables. A "data experience" encompasses the entire workflow from data ingestion through transformation, analysis, action, and automation.

Think of traditional BI tools as a newspaper: you read it, absorb the information, and then go do something with what you learned. Domo aims to be more like a cockpit: the instruments are connected to the controls, so seeing that fuel is low triggers an automated response, not just an awareness. This shift from passive reporting to active automation is where much of Domo's recent product investment has been directed.

Domo Everywhere, the company's embedded analytics offering, allows B2B SaaS companies and other businesses to white-label Domo's visualization and analytics capabilities within their own products. Rather than building analytics from scratch, a software company can embed Domo dashboards, alerts, and data experiences directly into its application, providing its customers with analytics capabilities powered by Domo's platform without those customers ever knowing Domo is involved. Domo was named a Leader in the Nucleus Research 2024 Embedded Analytics Technology Value Matrix, with customers reporting 10 to 35 percent time savings for analytics teams, 55 to 70 percent faster data request fulfillment, and a 300 percent increase in upsell adoption rates. This represents both a revenue opportunity and a strategic shift: instead of only competing for direct BI budget, Domo can become invisible infrastructure powering analytics across thousands of applications.

The multi-cloud data strategy represents another evolution. Rather than insisting that customers move all their data into Domo, the platform now works seamlessly with data wherever it resides, in Snowflake, Databricks, BigQuery, Oracle, or Domo's own storage layer. This flexibility reduced a key objection that enterprise buyers had raised: "We've already invested millions in our data warehouse, and we don't want to move our data again."

The AI Wave and Domo's Response

Like every software company, Domo has leaned heavily into artificial intelligence. But its approach has a distinctive angle that plays to the platform's strengths. The company launched Domo.AI, an integrated suite of AI capabilities, and followed it with Agent Catalyst at Domopalooza 2025, a framework for building autonomous AI agents within the Domo environment.

The core argument is that AI is only as good as the data it has access to, and Domo's platform, with its 500-plus connectors, built-in data transformation capabilities (ETL), governance controls, and visualization layer, provides the kind of governed data foundation that AI agents need to be useful and trustworthy in a business context. One customer reported that an agentic AI workflow built on Domo completed in two and a half minutes an analysis that previously took four weeks of manual work.

Agent Catalyst allows users to build AI agents through a four-step process: select a language model (Domo supports multiple LLMs through its DomoGPT framework, its own hosted language model that serves as the configurable "brain" of each agent), provide instructions in natural language, connect knowledge sources including unstructured data like PDFs, images, audio files, and PowerPoint presentations through a new capability called FileSets that uses retrieval-augmented generation, and assign tools that the agent can use to take actions. The result is an autonomous agent that can monitor data, identify anomalies, generate analyses, and trigger workflows without human intervention. A new Text Generation Tile in Magic ETL enables no-code AI processing, democratizing access to AI capabilities for business users who cannot write code.

The adoption metrics are encouraging: accounts using AI features increased sixty percent year over year, and unique AI users more than doubled. Josh James has been blunt about the strategic importance: "We're definitely playing offense" with AI, and "BI as a simple dashboard concept is dead, but the spending environment for infrastructure and services to capitalize on the promise of AI is very healthy."

The Dresner number one ranking in agentic AI validates that the product is resonating with at least a segment of the market. But the bigger question for investors is whether AI becomes the differentiator that justifies Domo's existence as a standalone platform, or whether the large cloud and productivity vendors, Microsoft, Google, and Salesforce, incorporate similar AI capabilities into their own analytics offerings and once again compress Domo's competitive space.

Where Domo Wins Today

Domo's sweet spot has narrowed from its original "everything for everyone" vision, but the focused positioning may ultimately prove more defensible. The platform wins in scenarios involving multi-source data integration, where organizations need to combine data from many systems into unified views. It wins in embedded analytics, where B2B companies want to add analytics to their own products without building from scratch. It wins with organizations using multiple cloud data warehouses, where Domo's ability to work across clouds is genuinely differentiated. And it wins in use cases requiring both IT governance and business user empowerment, the intersection where many competitors are weaker.

Typical deal sizes range from $100,000 to $500,000 or more in annual contract value, positioning Domo squarely in the mid-market to enterprise segment. The customer base of over 2,600 organizations is modest relative to competitors but represents a meaningful installed base of committed users. Importantly, 74 percent of customers by dollar value are on multi-year contracts, providing revenue visibility and reducing the risk of sudden churn spikes. The upcoming Domopalooza 2026, scheduled for March 24-26 in Salt Lake City, is expected to showcase the next wave of AI-driven capabilities, continuing the tradition of using the annual conference as a product launch vehicle and customer engagement platform that has run for over a decade.

X. Porter's Five Forces Analysis

Threat of New Entrants: Medium-High. Building a basic dashboarding tool is relatively easy with modern development frameworks. Any team with decent engineering talent can create attractive visualizations. However, building the kind of enterprise-grade platform that Domo offers, with 500-plus data connectors, robust security, governance, and compliance capabilities, is a multi-year, multi-hundred-million-dollar undertaking. The real threat comes not from startups but from cloud data warehouses that could forward-integrate into analytics. Snowflake and Databricks have both made moves in this direction, though neither has yet built a comprehensive visualization and workflow layer comparable to Domo's. AI is simultaneously lowering the barrier to entry for basic analytics while raising the quality bar for what constitutes a competitive product.

Bargaining Power of Suppliers: Low. Domo runs on AWS and standard cloud infrastructure that is essentially commoditized. Engineering talent is competitive but available, particularly with the company's Utah base offering favorable cost dynamics relative to San Francisco or New York. Data sources do not have pricing power over Domo; it is Domo that builds and maintains the connectors, not the other way around.

Bargaining Power of Buyers: Medium-High. Enterprise buyers have numerous alternatives and increasingly demand consolidation. The consumption model actually works in Domo's favor here by reducing upfront commitment and letting customers prove value before scaling spend. However, the availability of free or low-cost alternatives like Power BI gives buyers significant leverage in negotiations. Once deeply integrated, switching costs are substantial, but many customers never reach that level of integration.

Threat of Substitutes: High. This is Domo's most challenging force. Microsoft Power BI is free or near-free with Office 365, an offering that covers the needs of a significant portion of the market. Tableau backed by Salesforce has a massive user base and deep ecosystem. Looker is the preferred choice for Google Cloud environments. Technical teams increasingly build custom analytics solutions using Python, Jupyter notebooks, and open-source tools. And cloud data warehouses are steadily improving their native analytics capabilities, potentially making dedicated BI tools redundant for some use cases. Even Excel, the original business intelligence tool, remains dominant for many everyday analytics tasks.

Competitive Rivalry: Very High. The BI and analytics market is fragmented, fiercely competitive, and increasingly characterized by price compression. Microsoft's decision to offer Power BI essentially for free set an expectation that basic BI capabilities should be included with broader platform subscriptions. Feature parity across competitors is increasing, making differentiation difficult on core capabilities like dashboarding, charting, and basic data transformation. Consolidation has already claimed Tableau (acquired by Salesforce for $15.7 billion in 2019) and Looker (acquired by Google), leaving Domo as one of the few remaining independent, publicly traded pure-play BI companies. Qlik went private through a Thoma Bravo acquisition. Many smaller competitors have been acquired or shut down. The rivalry is not just about features; it is about ecosystem positioning, and Domo lacks the kind of platform gravity that Microsoft, Salesforce, or Google can generate. The remaining independent players must find defensible niches or risk being marginalized by bundled offerings from tech giants.

Overall Assessment. The structural forces in the BI market are generally unfavorable for an independent, mid-scale player. The threat of substitutes and competitive rivalry are particularly intense, creating persistent pricing pressure and making customer acquisition expensive relative to the available budget.

Domo's survival and potential success depend on execution excellence in specific niches, particularly embedded analytics, multi-cloud environments, and AI-driven automation, rather than on broad structural advantages. The consumption model and cloud data warehouse partnerships represent a strategic attempt to change the game by aligning with powerful market trends rather than fighting against them. Whether these moves are sufficient to overcome the structural headwinds is the central question facing the company and any potential acquirer evaluating the strategic alternatives process.

XI. Hamilton's Seven Powers Framework Analysis

Scale Economies: Weak. Software inherently has strong unit economics once built, with near-zero marginal costs for each additional user. But Domo's enterprise sales motion still requires expensive sales representatives, and customer support costs scale with the complexity of implementations. More critically, Domo is significantly smaller than its key competitors. Microsoft, Salesforce, and Google can spread their BI development costs across vastly larger revenue bases and customer ecosystems. Domo's scale is a disadvantage, not an advantage.

Network Effects: Minimal. There are no meaningful network effects between Domo customers. One company's use of Domo does not make the platform more valuable for another company. The Domo Everywhere embedded analytics strategy could theoretically create ecosystem effects, as more ISV partners embedding Domo increase the platform's reach and create familiarity, but this is early and unproven. The connector library has modest network effects: the more customers use a connector, the more investment Domo makes in maintaining it. But these effects are too weak to constitute a meaningful competitive advantage.

Counter-Positioning: Moderate, and Evolving. The consumption model represents genuine counter-positioning against legacy per-user licensing. Competitors like Tableau and some traditional BI vendors are locked into seat-based pricing models that their existing revenue bases depend on. Switching to consumption would cannibalize their existing revenue, creating the classic innovator's dilemma. Domo, with its smaller revenue base, could make this transition more aggressively. The cloud-native architecture was powerful counter-positioning in 2010 but has since become table stakes. The AI-driven automation capabilities could represent new counter-positioning if Domo can demonstrate meaningfully different AI experiences than what competitors offer. However, Microsoft has the resources to copy any successful strategy relatively quickly, which limits the durability of counter-positioning.

Switching Costs: Moderate-High (When Activated). This is Domo's strongest power, but it comes with a critical caveat. For deeply embedded customers, those who have built dozens of dashboards, integrated multiple data sources, trained their teams, and woven Domo into daily workflows, switching costs are substantial. Migrating that infrastructure to another platform would take months and significant expense. But many customers never reach deep embedding. The consumption model, somewhat paradoxically, lowers the initial switching costs by making it easy to start with Domo, while potentially increasing long-term switching costs by encouraging broader platform adoption.

Branding: Weak. Domo is not a household name, even within the enterprise technology community. Among data professionals, Tableau has iconic brand recognition. Power BI benefits from the Microsoft halo. Looker is associated with the modern data stack movement. Domo's brand is strongest in the Dresner analyst community and among its existing customer base, but it lacks the broader brand equity that drives inbound demand. Josh James has a personal brand in Utah's Silicon Slopes community, but this does not translate into meaningful commercial advantage at scale.

Cornered Resource: Not Applicable. Domo does not possess a unique resource, whether intellectual property, regulatory advantage, or exclusive data, that competitors cannot replicate. The over one thousand pre-built connectors represent significant accumulated engineering work, but individual connectors can be built by competitors with sufficient investment. There is no patent thicket or regulatory moat protecting the business.

Process Power: Emerging. If Domo's consumption model transition and cloud data warehouse partnership strategy continue to produce improving results, the organizational muscle and institutional knowledge built during this transformation could constitute a form of process power. The ability to drive consumption-based growth, manage CDW partner relationships, and deliver AI-powered data experiences is a learned capability that takes time to develop.

Consider that few enterprise software companies have successfully executed a mid-flight business model transition of this magnitude. If Domo's processes for managing consumption-based customers, optimizing usage-driven revenue, and scaling through partner channels become institutionalized, they could represent a genuine organizational advantage. But this power is nascent and has not yet been proven at the scale needed to constitute a durable advantage.

Overall Assessment. Domo's power portfolio is thin. The strongest potential sources of competitive advantage are switching costs (for deeply embedded customers) and the emerging counter-positioning of the consumption model. The company lacks the scale, network effects, and brand strength that characterize the most defensible enterprise software businesses. The strategic alternatives process makes sense through this lens: Domo's platform may be more valuable as part of a larger ecosystem, whether acquired by a cloud data warehouse vendor, a private equity firm, or a strategic buyer, than as an independent public company fighting structural headwinds.

XII. The KPIs That Matter

For investors tracking Domo's ongoing performance, three metrics matter above all others.

Consumption-Model ARR Percentage and Growth. The single most important metric is the percentage of annual recurring revenue on consumption contracts and the growth rate of consumption-based revenue specifically. This metric captures the success of the fundamental business model transformation that underpins Domo's turnaround thesis. The current figure stands at roughly eighty percent. If this metric continues climbing toward ninety percent or higher while consumption revenue per customer grows, it validates the entire strategic pivot. If it stalls or if per-customer consumption revenue stagnates, the pivot may prove insufficient.

Gross Retention Rate. Gross retention measures the percentage of existing customer revenue retained before any expansion. It is the purest measure of whether customers find the product valuable enough to keep paying for it. Domo's gross retention has improved from 83 percent to 86 percent and is guided toward 87 percent, but best-in-class enterprise SaaS companies typically achieve 90 percent or higher. Crossing the 90 percent threshold would signal that the consumption model and product improvements have fundamentally changed the customer value proposition. Staying below 85 percent would suggest that churn remains a structural problem.

Billings Growth Rate. Revenue growth is important but is distorted by the consumption model transition, which shifts timing of revenue recognition. Billings, which measure the total cash invoiced in a period, provide a more real-time view of commercial momentum. Think of billings as a leading indicator: it captures contracts signed and invoiced today, which will flow into revenue over the coming quarters.

Domo has guided for its fastest billings growth in over three years in Q4, and has set a target of exiting fiscal 2027 with ten percent billings growth. Tracking whether the company meets or exceeds this trajectory is the most direct measure of whether the growth engine is restarting after years of stagnation. For a company in the midst of a business model transition, billings growth is the earliest signal of whether the new model is generating commercial traction.

XIII. The Bull Case and the Bear Case

The Bull Case

The bull case for Domo rests on three pillars. First, the consumption model transformation is working and is still in early innings. With eighty percent of ARR converted and leading indicators like net revenue retention of 108 percent for consumption customers, the model is demonstrating that it aligns Domo's revenue with customer value. As more customers transition and freemium users convert, the revenue growth rate should reaccelerate beyond the current flat trajectory.

Second, the cloud data warehouse partnership strategy has created a genuinely new distribution channel. Partner-led deals close at five to seven times the rate of internal leads. As Snowflake, Databricks, and others continue to grow their installed bases, Domo's addressable market grows with them, without Domo having to pay for the customer acquisition. This is a scalable, capital-efficient growth strategy that did not exist eighteen months ago.

Third, the AI opportunity represents a potential step-function improvement in Domo's value proposition. If AI agents need governed, connected data to be useful, and if Domo's platform provides that foundation better than point solutions, then the AI wave could make Domo's integrated platform more valuable, not less. The Dresner number one ranking in agentic AI is early evidence that this thesis has merit.

The strategic alternatives process adds an asymmetric risk-reward element. At roughly half times revenue with improving fundamentals, Domo would be an attractive acquisition target for a cloud data warehouse vendor seeking a visualization layer, a private equity firm seeing operating leverage potential, or a strategic acquirer looking for AI-enhanced data capabilities. A take-private at even a modest premium to the current price could deliver significant returns.

The Bear Case

The bear case is equally compelling. The fundamental competitive dynamics have not changed: Microsoft can give away BI for free, Salesforce owns Tableau, Google owns Looker, and the cloud data warehouses are building their own analytics layers. Domo's roughly $318 million in revenue, while meaningful, is tiny relative to these competitors. The consumption model may be improving engagement, but it has not yet restarted revenue growth, and there is no guarantee it will.

The financial profile remains concerning. Even with the recent profitability milestones, the company is still modestly unprofitable on a GAAP basis, carries debt with BlackRock, and has limited financial flexibility for major investments. The stock price decline from twenty-one dollars to four dollars reflects a market judgment that the business, in its current form, may not be viable as an independent entity.

The AI thesis is unproven at scale. Every software company is claiming AI capabilities, and the large platforms have vastly more resources to invest in AI features. If AI-powered analytics become a commodity feature bundled into existing platforms, Domo's AI differentiation evaporates.

Finally, the strategic alternatives process itself carries risk. If no buyer emerges at a price the board considers acceptable, the announcement could be seen as a signal of distress rather than strength, potentially accelerating customer churn as organizations worry about the platform's long-term viability.

Myth vs. Reality

Myth: Domo failed because the product was bad. Reality: Domo's product, by most user accounts and analyst assessments, is genuinely capable. The failure was in business model design (per-user pricing), market timing (IPO during peak multiple expansion), and competitive positioning (trying to be a premium standalone product in a market trending toward bundled, free alternatives). The product itself consistently ranked well in analyst reports and earned strong customer satisfaction scores.

Myth: The consumption model pivot is just re-arranging deck chairs. Reality: The consumption model has produced measurable improvements in customer engagement, retention, and unit economics. Net revenue retention of 108 percent for consumption customers versus declining retention under the old model is meaningful evidence of structural improvement, not cosmetic accounting.

Myth: At four dollars per share, the stock is cheap. Reality: Cheapness depends entirely on whether the turnaround trajectory continues and whether the strategic alternatives process produces an outcome. At roughly half times revenue with flat growth and modest profitability, the stock could be a bargain or a value trap, depending on execution over the next twelve to eighteen months. The market capitalization of roughly $165 million for a company generating over $317 million in annual recurring revenue seems optically cheap, but that valuation also reflects the market's assessment of the competitive risks, the limited growth trajectory, and the debt on the balance sheet. Context matters: Salesforce paid roughly twelve times revenue for Tableau, but Tableau was the market leader growing at thirty percent. Domo's valuation reflects a very different competitive position.

XIV. Where the Story Goes From Here

Domo stands at a genuine crossroads, and unlike many inflection points in its history, this one was chosen rather than forced. The board's decision to explore strategic alternatives came not from desperation but from a recognition that the company's improving fundamentals were not being reflected in its market valuation. Josh James stated that "this is an appropriate time to evaluate opportunities that may further drive our growth strategy and maximize shareholder value."

The company has set a target of exiting fiscal 2027 with ten percent billings growth and ten percent non-GAAP operating margin, a "Rule of 20" that, while modest by SaaS standards, would represent a dramatic improvement from the recent years of stagnation and losses. Domopalooza 2026 is scheduled for March 24-26 in Salt Lake City, where the company is expected to showcase the next generation of its AI-driven capabilities. The freemium pipeline continues to build. The CDW partnerships continue to mature.

Whether Domo's story ends with an acquisition, a take-private, or a standalone turnaround, the sixteen-year journey from Josh James's frustration with siloed data to this moment encapsulates many of the defining tensions of modern enterprise software: the trade-off between vision and viability, the brutal consequences of pricing model missteps, the power of platform bundling to reshape competitive dynamics, and the potential for business model transformation to revive even the most challenged companies.

In the end, Domo is a case study in the difference between building a great product and building a great business. Few who have used the platform deeply would dispute its technical capabilities. But in enterprise software, product quality alone does not guarantee survival. Distribution, pricing, timing, and competitive positioning matter just as much, sometimes more. The next chapter will determine whether Domo's considerable technology and loyal customer base find a home where they can thrive, or whether the structural forces that have compressed the stock for eight years ultimately prove insurmountable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube