Healthpeak Properties: The Architecture of Healthcare Discovery and Delivery

I. Introduction & Episode Roadmap

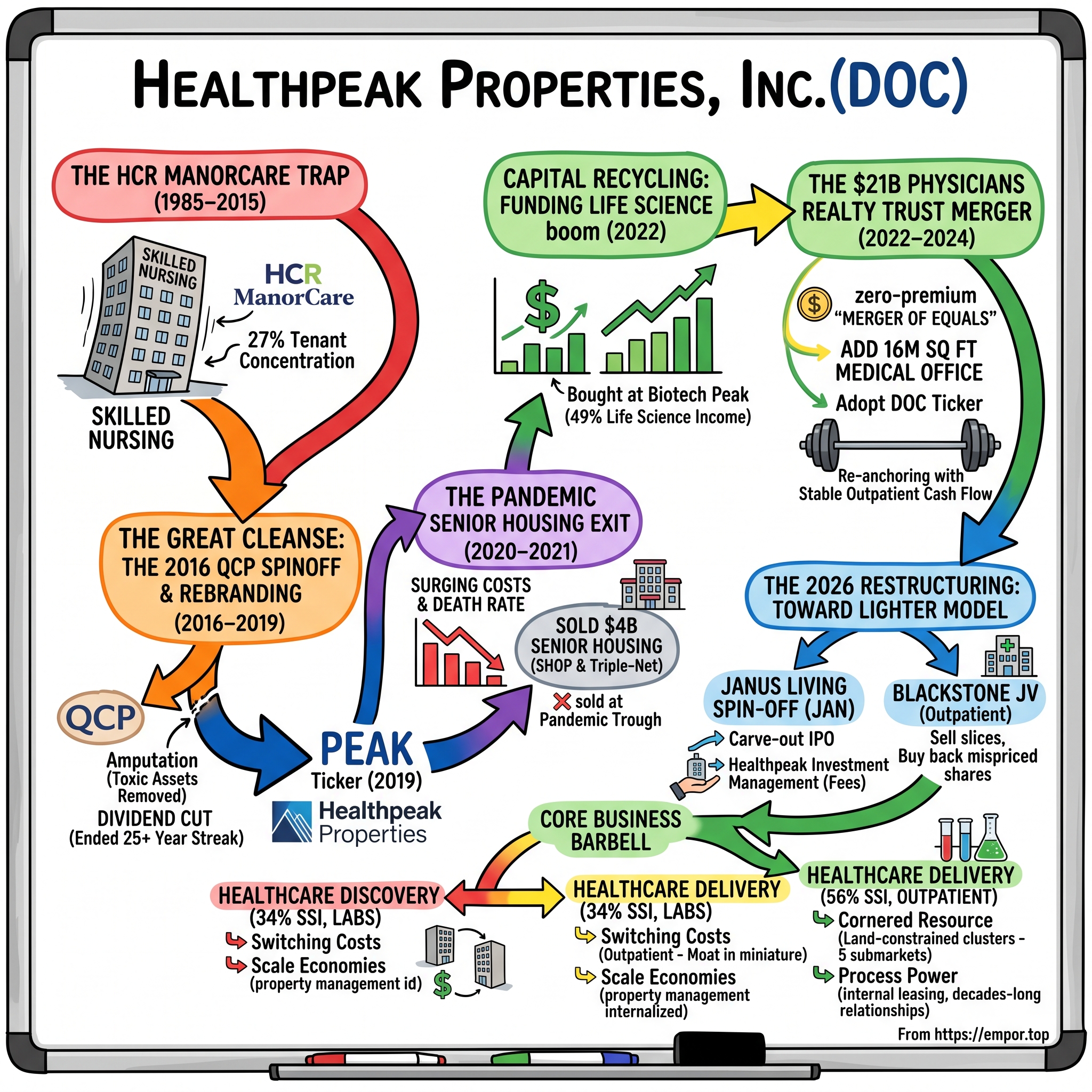

Here is a question that ought to be impossible. How does a company get to the brink of losing its investment-grade credit rating, cut a dividend it had raised for a quarter-century, hand its shareholders stock in a doomed skilled-nursing spin-off, panic-sell billions of dollars of senior housing at the worst possible moment, plow the proceeds into laboratory buildings just as that market fell off a cliff — and still, a decade later, be a roughly $20 billion healthcare real estate powerhouse trading on the New York Stock Exchange under one of the cleverest ticker symbols in the business: DOC?

That is the story of Healthpeak Properties, Inc. It is not a story of a company that got everything right. It is a story of a company that made several very large, very public mistakes, learned to survive its own concentration, and rebuilt itself around a barbell: on one end, the volatile, high-beta world of life-science real estate — the wet labs where drugs are discovered — and on the other, the boring, defensive, cash-gushing world of outpatient medical buildings — the clinics where care gets delivered. Management brands these two engines "Healthcare Discovery" and "Healthcare Delivery," and the ticker itself, DOC, is meant to stand for "Discovery and Outpatient Care."27 It is good marketing. Whether it is good business is the question this piece exists to test.

The arc runs through five acts. First, the concentration trap: HCP, Inc. bet the balance sheet on a single skilled-nursing tenant, HCR ManorCare, and nearly went down with it. Second, the great cleanse: the 2016 decision to jettison the toxic assets into a separate public company and, in 2019, to bury the HCP name entirely and re-emerge as Healthpeak. Third, the capital-recycling gamble: selling roughly $4 billion of senior housing into the teeth of the pandemic to fund a late-cycle life-science building boom that soured almost immediately. Fourth, the re-anchoring merger: the 2024 zero-premium "merger of equals" with Physicians Realty Trust that handed Healthpeak both a stable outpatient cash-flow engine and its new ticker. And fifth, the 2026 restructuring: the carve-out IPO of its senior housing arm as Janus Living, Inc. (NYSE: JAN), and a joint venture with Blackstone, both designed to turn Healthpeak into something lighter — a manager of other people's capital as much as an owner of buildings.

One consensus myth is worth puncturing at the outset, because it colors how the company is discussed. The popular framing is that Healthpeak is a "life-science REIT" that got caught in the lab downturn — a high-beta bet on biotech real estate. The reality, after the 2024 merger, is closer to the opposite: the largest slice of its income comes from humble outpatient medical buildings, and the lab exposure, while the loudest part of the story, is the minority. Much of the bear commentary aimed at Healthpeak is really commentary about the lab market that would apply in full only to a pure-play like Alexandria. Getting the weighting right is the difference between analyzing this company and analyzing a caricature of it.

Throughout, keep one tension in mind. Management tells a clean story of discipline rewarded: it cut off life-science spending before the crash, absorbed the downturn without cutting the dividend, and is now buying distressed assets nobody else can afford. The skeptic tells a messier one: the same team that "recycled" capital sold low and bought high, and the 2026 financial engineering may be dressing up slowing organic growth. Both stories use the same facts. Let's start where the trap was set.

II. The Consolidated Conglomerate & The HCR ManorCare Trap (1985–2015)

In March 1985, a new real estate investment trust called Health Care Property Investors, Inc. listed on the New York Stock Exchange with a portfolio you could count on two hands: two acute-care hospitals and twenty-two skilled nursing facilities.1 Its founding operating chief, Kenneth Roath, spent the next two decades turning that starter kit into one of the pioneers of an entirely new asset class — real estate whose rent checks were underwritten not by retailers or office tenants but by the American healthcare system. By 2008 it had become the first healthcare REIT admitted to the S&P 500.1 The model was seductive in its simplicity: buy the buildings, lease them back to the operators who run the hospitals and nursing homes, collect a rising rent, and let someone else worry about the messy business of actually caring for patients.

The seduction had a flaw, and its name was the triple-net lease. Under a triple-net structure, the tenant pays rent plus taxes, insurance, and maintenance — the landlord is a pure toll-taker. It feels bulletproof, because the rent is contractual and the escalators are automatic. But a triple-net lease is only as strong as the tenant standing behind it, and if that tenant's own business model breaks, the "guaranteed" rent becomes a fiction and the landlord is left holding specialized buildings that are worth a great deal less without their operator. A shuttered nursing home is not an office you can re-lease to a law firm; it is a purpose-built structure whose value is almost entirely a function of the license and the operator inside it.

To understand why HCP walked into that flaw, you have to understand the competitive arms race it was running inside. By the 2000s the healthcare-REIT universe had crystallized into a handful of scaled players — HCP, Welltower (then Health Care REIT), and Ventas — all chasing the same demographic thesis and all measured against one another on the size and growth of their portfolios. Scale was not merely a vanity metric; it lowered the cost of capital, which for a REIT is the entire game. A company that can borrow and issue equity more cheaply can outbid rivals for assets and still clear its return hurdle. That dynamic rewarded boldness and punished patience, and it set the stage for a landlord to convince itself that a single enormous, high-yielding acquisition was prudent diversification rather than a concentrated bet.

Under CEO Jay Flaherty, who ran the company from 2003 to 2013, HCP decided to press that bet to its limit. It had built up debt and mezzanine exposure to HCR ManorCare — one of the nation's largest post-acute and skilled-nursing operators — in the late 2000s, and in December 2010 it agreed to buy essentially all of ManorCare's real estate outright for $6.1 billion, closing the deal on April 7, 2011.23 The structure tells you how big the swing was: roughly $3.5 billion in cash, about $1.7 billion from converting HCP's existing ManorCare loans into equity in the bricks, and the rest in stock, all wrapped in a long-term triple-net master lease with a first-year rent of $472.5 million escalating 3.5% a year.2 (Note the date: the outline's shorthand of "2006" marks when HCP first waded into ManorCare's debt; the company did not own the real estate until 2011.)

The asset on the other side of the table had its own baggage. HCR ManorCare had been taken private by the Carlyle Group in a 2007 leveraged buyout, and by 2010 its private-equity owner was a motivated seller of the real estate underneath the operations — a classic sale-leaseback in which the operator monetizes its buildings and stays on as tenant.2 For HCP, buying at the top of a credit cycle from a sophisticated PE seller should have been a yellow flag; instead the sheer scale and the double-digit initial rent yield were treated as the attraction. This is a recurring pattern worth internalizing: the deals that look most accretive on day-one yield are often the ones where the seller knows something about the durability of that yield that the buyer is choosing not to price.

The problem was not the price so much as the dose. By the end of 2011, the post-acute and skilled-nursing segment threw off roughly 29% of HCP's total revenue, with HCR ManorCare alone accounting for about 27%.3 More than a quarter of the entire company's income now depended on one operator whose own revenue depended, in turn, on Medicare and Medicaid reimbursement — the most politically exposed dollar in American healthcare. HCP had taken a diversified REIT and quietly turned it into a leveraged bet on federal reimbursement policy for nursing-home rehab.

Then the bet went wrong on two fronts at once. Post-financial-crisis, Washington tightened Medicare reimbursement for skilled nursing, compressing ManorCare's operating margins from the top down. And on April 21, 2015, the Department of Justice intervened in a set of whistleblower suits and filed a consolidated False Claims Act complaint alleging that ManorCare — then running about 281 skilled nursing facilities across 30 states — had systematically billed Medicare and Tricare for rehabilitation therapy that was not medically necessary, pressuring its own therapists to hit revenue targets.4 The government's own exhibit was damning in its arc: ManorCare's data showed the share of therapy days billed at the top "Ultra High" reimbursement tier climbing from 38.8% in October 2006 to 80.3% by November 2009.4

It is worth being clear about why government-reimbursed healthcare real estate is structurally more dangerous than the private-pay kind, because this distinction becomes the organizing principle of everything Healthpeak does afterward. A skilled-nursing operator's revenue is set, in large part, not by supply and demand but by Medicare and Medicaid fee schedules — administered prices that Washington can cut with the stroke of a rule-making pen, and that come wrapped in dense compliance requirements whose violation invites exactly the kind of False Claims Act exposure ManorCare walked into. A landlord standing behind such an operator is therefore exposed to two compounding risks at once: reimbursement policy that can compress the tenant's margins from above, and regulatory enforcement that can blow a hole in the tenant's balance sheet from the side. Private-pay assets — luxury senior housing, labs funded by venture capital, clinics whose rent is ultimately backed by commercial-insurance economics — are cyclical and can be volatile, but they are not one adverse CMS rule away from insolvency. When Healthpeak later declared itself a private-pay company, it was not marketing; it was drawing the exact boundary this episode taught it to fear.

For HCP, the tenant's operational distress detonated inside the triple-net structure exactly as theory warned it would. As ManorCare's coverage of its rent deteriorated, HCP took a roughly $478 million impairment on its ManorCare investment in early 2015, followed by an $817 million write-down at year-end, and ultimately cut the lease's annual rent from about $541 million to $473 million to keep the operator alive.1 The landlord that thought it had bought a contractual annuity had in fact bought a call option on a fraud investigation. (In a final irony, the DOJ later moved to dismiss the ManorCare case in 2017 after its expert testimony was struck — but by then the damage to HCP was long done.4) The lesson HCP was about to learn the hard way: when one tenant is a quarter of your income, its problems are your problems, and no lease clause can change that.

III. The Great Cleanse: The 2016 QCP Spinoff and Rebranding (2016–2019)

By 2016, HCP's board faced a choice that every over-concentrated lender eventually faces: keep pretending the impaired asset will recover, or amputate. The company chose amputation, and it did so through a piece of financial surgery that was elegant on paper and painful in practice — a spin-off.

The mechanism was clean. On October 31, 2016, HCP completed the separation of its ManorCare real estate — together with certain other post-acute, skilled-nursing, and memory-care assets — into a brand-new, independently traded REIT called Quality Care Properties, Inc.56 HCP shareholders received one QCP share for every five HCP shares they held, as of an October 24 record date.5 In a stroke, the toxic exposure was walled off in its own corporate entity, with its own balance sheet and its own management, no longer able to drag down the parent's credit or valuation. What was left inside HCP — senior housing, life science, and medical office — was the "private-pay" portfolio, the assets whose rents came from wealthy retirees and hospital systems rather than from Washington.

Why spin the assets off rather than simply sell them? Because there was no clean buyer. A distressed skilled-nursing portfolio anchored by a tenant under federal investigation is not something you sell into a strong bid; you would be forced to accept a fire-sale price that crystallized the loss. A spin-off sidesteps the market entirely: instead of finding one buyer, you distribute the asset to your existing shareholders and let the public market price it over time. It also, critically, protected HCP's credit rating. The company was staring at the real possibility of a downgrade toward junk, which for a REIT is close to a death sentence because it raises borrowing costs across the entire balance sheet, not just on the troubled assets. Walling ManorCare off in QCP severed that contagion.

The elegance came with a bill. To preserve cash and right-size a balance sheet that had been leaning on ManorCare rent, HCP cut its quarterly dividend by roughly 36%, from $0.575 to $0.37 a share — its first dividend reduction in more than 25 years, which ended its cherished status as a dividend aristocrat.1 For a REIT, whose entire investor base is built on the promise of a reliable and rising payout, that is close to an admission of failure. Income investors do not merely dislike a dividend cut; many of them are structurally forced to sell, because their mandates require a rising or at least stable payout. The cut therefore did double damage — it signaled distress and it flushed out a chunk of the shareholder base. It was the price of having concentrated in the first place.

QCP's afterlife proved the point emphatically. Cut loose from HCP's diversification, the spin-off had no cushion when ManorCare's operations kept deteriorating; ManorCare filed for Chapter 11 bankruptcy in March 2018. Within weeks, Welltower agreed to acquire QCP outright at $20.75 a share in cash and to fold the real estate into an 80/20 joint venture with the not-for-profit health system ProMedica, which simultaneously took over ManorCare's operations.7 The whole package closed in July 2018 for about $4.4 billion.8 The structural verdict was unambiguous: the only way to save the parent had been to sever the tenant entirely, and even then the severed assets needed a deep-pocketed operator and a bankruptcy court to be rescued. Isolation, not cleverness, was what worked.

With the anchor gone, HCP set about erasing the memory of it. On October 30, 2019, the company announced it would change its name to Healthpeak Properties, Inc. and adopt a new ticker, PEAK, which began trading on November 5.9 CEO Tom Herzog framed it as "the culmination of efforts to reposition our strategy, team, portfolio and balance sheet," and the same release promoted a rising executive named Scott Brinker to President alongside his role as chief investment officer.9 A rebrand is, in one sense, cheap theater — new logo, new website, same buildings. But it also functioned as a public commitment device: Healthpeak was declaring that it would live in the high-barrier, private-pay corner of healthcare real estate and stay out of the government-reimbursement swamp that had nearly killed it. The declaration was sincere. The timing of what came next would test whether discipline and good luck are the same thing.

IV. The Pandemic Senior Housing Exit & Capital Recycling Dilemma (2020–2021)

In the spring of 2020, the private-pay sanctuary Healthpeak had built for itself turned out to have a trapdoor. Senior housing — the assisted-living and independent-living communities that were supposed to be the safe, demographic-tailwind heart of the portfolio — became, almost overnight, the single most dangerous place to own real estate in America. COVID-19 tore through congregate elderly settings. National senior housing occupancy, which had stood at 87.2% in March 2020, collapsed toward a record low of 78.8% by the first quarter of 2021 and bottomed near 77.9% that June — the steepest, fastest occupancy decline the sector had ever recorded.1314 Behind those numbers were surging costs for personal protective equipment, an acute labor shortage as frontline caregivers fled, and a mortality shock: an independent study for the National Investment Center found that in 2020 the adjusted COVID death rate ran to 59.6 per 1,000 residents in skilled nursing and 19.3 in assisted living, versus 5.9 in independent living.15

Faced with this, Healthpeak's leadership under Tom Herzog made a decisive, and deeply controversial, call: get out. Not trim — exit. In late 2020 the company announced a plan to sell roughly $4 billion of senior housing, spanning both its operating (SHOP) portfolio and its triple-net leased communities.10 By the end of 2020 it had already closed about $2.5 billion of that, including 70 operating assets sold at a blended trailing cap rate of roughly 3.1% — a rich-sounding yield that in fact reflected pandemic-depressed income, meaning buyers were paying for a recovery Healthpeak was choosing not to wait for.10 Through the first half of 2021 the rest went out the door in a rapid series of deals: a 32-property Sunrise operating portfolio for $664 million, a 24-property triple-net portfolio leased to Brookdale for $510 million, and a long tail of smaller sales.11 In September 2021, the company closed the final tranche and declared the exit complete — about $4 billion of dispositions since July 2020, with leverage brought down to a comfortable 5.0x net-debt-to-EBITDA.12

It is worth pausing on the operational nightmare that drove the decision, because it explains the fear without excusing the timing. A senior housing operating portfolio — the "SHOP" structure — is not a passive rent stream; under RIDEA the owner participates directly in the community's profit and loss, which means Healthpeak was exposed to every dollar of surging labor and PPE cost and every point of lost occupancy in real time. When a community cannot admit new residents because of a lockdown, and existing residents are dying faster than they can be replaced, the operating margin does not just compress — it can invert. Management was staring at an asset class that had transformed overnight from a demographic sure-thing into an uninsurable operating liability. Selling was psychologically understandable.

The other half of the mistake was the destination, and here the boom mechanics matter. The 2020–2021 biotech bubble was one of the great capital-formation manias of the era: a wide-open IPO window, a flood of SPAC mergers, and record venture funding meant that hundreds of drug-development startups were raised, each needing specialized lab space, each willing to sign a lease at almost any rent to secure it. Landlords like Healthpeak and Alexandria watched their lab rents spike and their development pipelines pre-lease before the concrete was poured — the 98.9% occupancy and 78%-pre-leased pipeline of 2022 were the visible symptoms of that mania.19 Buying into it felt not like speculation but like riding an obvious secular trend. That is exactly how tops feel.

Here is where the story splits into two irreconcilable readings, and an honest analysis has to hold both. Management's version: it de-risked a volatile, operationally intensive business at a moment of existential uncertainty and freed up capital to redeploy into higher-conviction assets. The skeptic's version is harsher, and the calendar is not kind to management. Senior housing occupancy and rents staged a powerful recovery from mid-2021 onward — precisely the upside Healthpeak had sold away at trough pricing. Selling operating communities at a 3% cap rate on depressed income is, almost by definition, selling at the bottom.

Worse was where the money went. Healthpeak recycled the senior-housing proceeds straight into life science, and it did so at the top of a historic biotech boom. By 2022, life science had swollen to 49.1% of the company's portfolio income, up from just 14% a decade earlier, and the development machine was running hot: a nearly $900 million active life-science pipeline that was 78% pre-leased, portfolio occupancy at an almost unreal 98.9%.19 The flagship was Vantage, a ground-up campus in South San Francisco announced in late 2021 — an initial 343,000 square feet with room to grow to 1.7 million, ultimately anchored by a lease with Japan's アステラス Astellas Pharma.161718 It all looked brilliant in 2021. The trouble, as the next chapters show, is that Healthpeak was buying the trendiest asset class in commercial real estate at the exact moment its cycle was about to turn — the mirror image of the senior housing it had just dumped. Whether that was "capital recycling" or "selling low to buy high" is the case the skeptics would spend the next three years pressing.

V. The Scott Brinker Era: Re-anchoring with the $21B Physicians Realty Trust Merger (2022–2024)

The man who inherited that mismatch had spent his whole career underwriting healthcare real estate. On October 6, 2022, Healthpeak's board named Scott Brinker — its president and chief investment officer since 2020 — as chief executive, with Tom Herzog stepping down.24 It is worth correcting a common misconception here, because it speaks to Brinker's pedigree: he did not come from Ventas. Brinker joined Healthpeak in 2018 after roughly fifteen years at Welltower, where he had risen to executive vice president and chief investment officer.24 In other words, Healthpeak handed the top job to a lifelong investor from the disciplined school of healthcare REIT capital allocation — someone whose instinct was to underwrite deals rather than to build empires.

Brinker's temperament matters to the story because it is the antithesis of the empire-building instinct that produced the ManorCare disaster. Colleagues and analysts describe him as an underwriter's underwriter — a leader who talks in terms of basis points, cost of capital, and downside cases rather than vision and scale. On earnings calls he is notably willing to say unfashionable things: that he shut off life-science spending years before the crash while rivals kept building, that concentration in a few dominant submarkets reduces rather than increases risk, and — as we will see — that the industry's favorite growth metric is one he would rather ignore. Whether that self-image survives contact with the record is the crux of the credibility question later in this piece, but the style itself is real and it shaped every move that followed.

Brinker inherited a barbell that was badly out of balance. Life science, now nearly half the company, was heading into a brutal downturn: biotech venture funding was contracting hard off its 2021 peak, and a wave of speculative lab construction was hitting the market just as demand evaporated. Vacancy in the premier clusters, which had been near zero, began marching into the teens. His answer was not to double down on labs, but to build a counterweight — and to do it through the largest deal in the company's history.

On October 30, 2023, Healthpeak and Physicians Realty Trust announced an all-stock "merger of equals" valued at roughly $21 billion.25 Physicians Realty was a self-managed REIT built almost entirely around medical office buildings — the outpatient clinics, cancer centers, and surgery centers that cluster on and around hospital campuses. Under the terms, each Physicians Realty share converted into 0.674 of a Healthpeak share, a structure with essentially no premium; this was a combination pitched on strategic logic and synergies, not on one side paying up for the other.25 The partner deserves a proper introduction, because Physicians Realty Trust was itself a purpose-built machine. It had gone public in 2013 under John T. Thomas — "JT" to the industry — a healthcare-real-estate specialist who had previously helped build the medical-office platform at Health Care REIT before striking out to assemble his own. His thesis was narrow and disciplined: own the outpatient buildings physically attached to strong hospital systems, lease them to physician groups, and collect boring, escalating rent. By the time of the merger, that focus had produced a portfolio of roughly 16 million square feet of outpatient medical real estate across hundreds of buildings, overwhelmingly on-campus or affiliated with health systems. In the combined company, Thomas took the role of Vice Chair, staying on to shepherd the health-system relationships that are the real asset in outpatient real estate.[^26] Healthpeak was not just buying buildings; it was buying a relationship network and the operator who had built it.

The deal closed on March 1, 2024, and — in the branding masterstroke that gives this whole story its title — the combined company kept the Healthpeak name but adopted Physicians Realty's ticker, DOC, which began trading on March 4.[^26]26 The mechanics of integration were substantial: Healthpeak's board expanded from eight directors to thirteen to absorb five former Physicians Realty trustees, and the combined company set about knitting together two enterprise systems and two leasing organizations into one.[^26]

The strategic rationale was a hedge dressed as a growth story. By bolting on Physicians Realty's roughly 52 million square feet of medical office and life-science real estate, Brinker deliberately re-weighted the portfolio away from the burning life-science segment and toward stable outpatient medical.25 Outpatient rent behaves nothing like lab rent: it is diversified across thousands of physician tenants, contractually escalated, and remarkably sticky, which makes it exactly the kind of cash flow that can cover a dividend while the lab segment works through its hangover. There is also a powerful secular current running beneath it. American healthcare has been migrating steadily out of expensive inpatient hospital settings and into lower-cost outpatient ones — procedures that once required an overnight stay are increasingly done in a surgery center and sent home the same day, a shift actively encouraged by Medicare reimbursement policy that keeps expanding the list of surgeries payable in outpatient settings. That trend structurally grows demand for exactly the buildings Physicians Realty specialized in, while the high cost of new construction keeps new supply scarce — a rare combination of rising demand and constrained supply that underwrites landlord pricing power. The deal also promised hard cost savings — an initial target of $40 million of synergies in 2024 with $20 million more by the end of 2025 — and, less obviously but more durably, the scale to bring property management in-house across the whole combined footprint.25 On the Q1 2026 call, management would point to that internalization as a structural edge, noting it did half its outpatient renewals in-house in a single quarter and saved millions in leasing commissions in the process.31

For investors, the merger reframed the entire company. It converted Healthpeak from a wounded life-science pure-play back into a diversified healthcare REIT whose largest, most defensive segment could carry the payout through the cycle. That is a genuine improvement in resilience. But it is worth being precise about what a zero-premium merger of equals actually is: it is not value creation out of thin air, it is two companies agreeing that together they are worth more than apart, and pledging synergies to prove it. The proof would come in the execution — and, as the next act shows, Brinker was only getting started on the financial engineering.

VI. The Janus Living Carve-out & The External Fee Model (2026)

There was still one loose end from the pre-pandemic company: senior housing. Healthpeak had never fully exited it — it kept a portfolio of continuing-care retirement communities and had even been quietly acquiring more high-quality communities as the sector recovered. By late 2025 those assets were performing spectacularly, with same-store growth around 17% in the fourth quarter — and yet, buried inside a $20 billion diversified REIT, they were being valued at Healthpeak's own modest multiple rather than the premium the market was assigning to pure-play senior housing. Brinker's team saw an arbitrage, and in early 2026 it executed one of the more creative structures the REIT sector had seen in years.

In March 2026, Healthpeak carved its senior housing business out into a separate, publicly traded, pure-play REIT: Janus Living, Inc., listed on the NYSE as JAN.28 The IPO priced at $20 a share and was upsized to $840 million, with net proceeds of roughly $878 million once the over-allotment was exercised.2829 Crucially, Healthpeak did not sell out — it sold down. It retained about 81.6% of the economics of Janus, keeping full exposure to the senior-housing recovery it had once fled, while shifting the operational drag and the public-company optics onto a separate entity.29 The initial Janus portfolio comprised 34 senior-living communities and 10,422 units across ten states, all structured under RIDEA — the operating-participation model that, unlike a triple-net lease, lets the owner share directly in the community's profits rather than collect a fixed rent.32 On the first-quarter call, Brinker described the multiple arbitrage bluntly: the roughly $240 million of current-year cash flow from that portfolio was suddenly being valued at a multiple some 20 turns higher than Healthpeak's own.31

It is worth slowing down on RIDEA, because it is the structural hinge of this entire chapter and it explains why Healthpeak could leave and return to senior housing on its own terms. Under a traditional triple-net lease, the landlord collects a fixed rent and the operator keeps whatever profit — or absorbs whatever loss — is left over. RIDEA, a structure enabled by the 2008 REIT Investment Diversification and Empowerment Act, lets a REIT own the operating business itself through a taxable subsidiary and share directly in the community's net operating income. The trade-off is symmetrical: in good times the owner captures the full upside of rising rents and occupancy rather than a capped rent check, but in bad times — a pandemic, say — it eats the labor inflation and the empty rooms. That is precisely why Healthpeak fled the operating model when COVID made the downside unbearable, and precisely why it wanted back in through Janus once the upside re-emerged. The lesson is not that one structure is superior; it is that the ability to toggle between them is itself a competitive advantage.

The genuinely novel piece is the fee stream. Janus Living is externally managed by a Healthpeak subsidiary, Healthpeak Investment Management, LLC.32 That converts a slice of Healthpeak into something it had never been: an asset-light manager collecting recurring fees on capital it does not fully own, a model that — if it scales — lifts return on equity because the fees require almost no incremental balance sheet. Management's pitch is that Janus already enjoys a lower cost of capital than Healthpeak, so acquisitions Janus makes are accretive to Healthpeak as its majority owner; Brinker put the run-rate benefit at roughly $0.04 per share once the IPO proceeds are fully deployed.31

Alongside the carve-out came a second, smaller move in the same asset-light spirit. In March 2026, Healthpeak formed a joint venture with Blackstone, contributing a fully occupied, six-property outpatient portfolio of about 418,000 square feet valued at $212 million at a 6.1% cash cap rate. Blackstone took 80%, Healthpeak kept 20% and continued to manage the buildings for a fee, and the deal raised about $170 million of gross proceeds that Healthpeak steered into stock buybacks and debt paydown.27 Brinker was explicit that this was a template, not a one-off, telling analysts the company was working on additional transactions with Blackstone that could generate $700 million or more of proceeds at cap rates well inside where its own stock was trading.31 The strategic logic is coherent: if the private market values your buildings more richly than the public market values your shares, sell slices to the private market and buy back the mispriced shares. Whether it is a durable value-creation engine or a clever way to paper over slowing organic growth is precisely the question the skeptics raise — and it deserves a fair hearing, which the bear case below gives it.

VII. Core Business Deep Dive: Discovery (Lab) vs. Delivery (Outpatient) Economics

Strip away the corporate history and Healthpeak today is two very different businesses stapled together. Understanding why they behave so differently is the key to the whole investment.

Segment one is Healthcare Discovery — the lab and life-science portfolio, about 34% of same-store income.27 Think of a wet lab not as an office but as a highly specialized factory: reinforced floors to hold heavy equipment, massive ventilation and exhaust systems, backup power, and plumbing for gases and chemicals. You cannot conjure one of these clusters into existence, and that is the moat. Life-science ecosystems form only where three things coincide — elite research universities, deep venture-capital money, and a critical mass of scientific talent — which is why they concentrate in a handful of submarkets: South San Francisco near Stanford and Berkeley, Cambridge near MIT and Harvard, and San Diego. Healthpeak has leaned into that concentration hard. As Brinker told analysts, the company's entire lab footprint sits in roughly five submarkets, and in South San Francisco it controls around 210 acres — about a third of the entire submarket — with some 6.5 million square feet of space.31

Why can't these clusters simply be replicated somewhere cheaper? Because a life-science hub is an agglomeration economy, not a collection of buildings. The value comes from density: a founding scientist who can walk from her lab to her former university department, recruit post-docs who don't want to move their families, meet three venture investors before lunch, and share a specialized contract-manufacturing vendor with the startup next door. Each additional lab in the cluster makes every other lab slightly more valuable, which is why the same three or four metros have dominated for decades and why a gleaming new lab park in a low-cost city struggles to fill. This is the real barrier to entry — and it is also why Healthpeak's deliberate concentration in five submarkets is a coherent strategy rather than a failure to diversify. Brinker made the point directly on the first-quarter call: in life science, concentration in dominant local markets reduces risk, because it makes you the landlord tenants and brokers must call, gives you the flexibility to move a growing tenant across your own buildings, and lets you dominate the broker network in a way a scattered portfolio never can.31

The catch is that a moat around your land does not protect you from the cycle inside it. The 2021 biotech boom triggered a building frenzy, and by the time the venture money dried up the market was drowning in speculative lab space. Greater Boston lab vacancy climbed from near nothing to 11.7% by late 2023 and kept going, reaching roughly 25% by early 2025; even San Diego, the tightest of the three clusters, saw vacancy back up from a record-low 2.7% to 5.6% within a single quarter of 2023 as the tide went out everywhere at once.202122 Nationally, lab vacancy hit about 23.2% by the first quarter of 2026, with more than half of everything delivered between 2020 and 2025 sitting empty.23 Healthpeak's own lab occupancy sat at 77.7% in the first quarter of 2026 — an honest reflection of a market still clearing.31 Its contrarian bet is the Gateway campus in South San Francisco: 1.4 million square feet, bought for $600 million in early 2026 at a steep discount to replacement cost, roughly 60% leased, with the vacant half representing pure lease-up optionality.2730 Brinker called it a "once-in-a-decade buying opportunity," and by May reported it was already running ahead of underwriting with 62,000 square feet signed or under letter of intent and another 113,000 in active proposals.31 The contrast with the category's king, Alexandria Real Estate Equities, sharpens the read. Alexandria essentially invented the pure-play life-science REIT and remains the largest and most concentrated bet on the sector — which cut both ways in the downturn, forcing it into a sharp dividend reduction as vacancy and concessions bit. Healthpeak's structural answer is different: it never let life science become the whole company again after the merger, so the lab segment can bleed without threatening the payout. A skeptic would counter that Healthpeak's caution was partly luck of timing and partly the forced consequence of a balance sheet that could not afford to keep building; a defender would point out that the outcome — a diversified REIT that kept its dividend intact through the worst lab market in a generation — is what actually matters to shareholders. On the evidence, the diversification did its job, but it is the outpatient engine, not any brilliance in the labs, that deserves the credit.

The analytical read: this is a genuine distressed-buying opportunity if the biotech cycle inflects, and a value trap if oversupply lingers to 2029. The evidence is mixed but tilting positive — management noted April 2026 was the strongest month for biotech equity issuance since early 2021 — but occupancy, not optimism, is what pays the rent.31

Segment two is Healthcare Delivery — outpatient medical, about 56% of same-store income and the ballast of the entire company.27 The moat here is the opposite of the lab's: not scarcity of land, but the physics of a hospital campus. More than 80% of Healthpeak's outpatient buildings sit on or adjacent to dominant health-system campuses, and physicians almost never leave them. Why? Because an on-campus practice lives on referrals from the hospital, needs proximity to operating rooms, and has sunk enormous cost into installing specialized, often immovable equipment. Relocating means severing the referral pipeline and re-plumbing a clinic — so tenants renew, and they renew at rents that rise with contractual 3% escalators. The numbers management reported for the first quarter of 2026 tell the story of a business that simply works: 91% occupancy, 79% tenant retention, cash re-leasing spreads of 5.4% on renewals, and — the detail that reveals the real edge — leasing costs of only about 10% of annual rent, far below peers, because the company negotiates directly with health systems it has known for decades.31 Its showcase was renewing an entire 458,000-square-foot Baylor cancer campus in Dallas at leasing costs of barely $1 per square foot per year — a deal management stressed was done through direct negotiation with Baylor Scott & White and McKesson, leveraging decades-long relationships rather than paying brokers to run a competitive process.31 That detail is the whole moat in miniature. The tenants that anchor these buildings are not anonymous small businesses but the dominant health systems of their regions — the HCA Healthcares, the Baylors, the Norton Healthcares — and the relationships that let Healthpeak renew a cancer campus over coffee are the accumulated product of years of being the reliable landlord on a health system's campus. A new entrant cannot buy that relationship; it has to earn it one building at a time, which is exactly why the outpatient business compounds quietly while attracting far less attention than the volatile labs next door. That is what a defensive, inflation-indexed cash flow engine looks like — and it is why the dividend gets covered even while the labs sit half-empty.

VIII. The Strategic Moat: Helmer's 7 Powers & Porter's 5 Forces Applied

Frameworks are only useful if they force you to be precise about why an advantage is durable — or admit that it isn't. Run Healthpeak through Hamilton Helmer's 7 Powers and Michael Porter's Five Forces and the two engines light up different boxes, which is itself the point.

Start with Helmer's Switching Costs, which is the strongest genuine power in the portfolio and lives almost entirely in outpatient delivery. The lock-in described above — referrals, operating-room proximity, immovable equipment, and the reputational cost to a physician of moving patients across town — is a textbook switching-cost moat, and it shows up quantitatively in that 79% retention rate and the ability to push rent with minimal tenant-improvement spend.31 This is not management rhetoric; it is visible in the leasing economics.

Next, Cornered Resource, which is the strongest power on the lab side. Owning roughly a third of a land-constrained submarket like South San Francisco, protected by zoning and geography, is close to a literal cornered resource — you cannot build another Oyster Point.31 But note the asymmetry with switching costs: a cornered resource in land protects the value of the location over decades, yet it does nothing to protect this year's rent when 23% of the market sits vacant. The lab moat is real and long-dated; it is simply not a cyclical shield.

Then Scale Economies, a moderate power unlocked by the Physicians Realty merger. National scale lets Healthpeak internalize property management, negotiate directly with health systems, and spread G&A across a bigger base — the source of those below-peer leasing costs.31 It is real but replicable; a Healthcare Realty or a Welltower can build the same. Adjacent to it sits a modest Process Power: the in-house leasing and asset-management engine that renews millions of square feet a year at low cost is a capability built up over time, not a switch a rival flips overnight. But process advantages erode as competitors copy the playbook, so this is a lead, not a fortress.

Where Healthpeak is conspicuously weak on the Helmer map is just as instructive. It has essentially no Branding power in the consumer sense — no physician chooses a clinic because Healthpeak owns the building, and no biotech pays a premium for the Healthpeak name the way a shopper pays for a luxury label. It has no Network Economies in the classic sense and no Counter-Positioning — it is not doing something incumbents are structurally unable to copy; the Janus external-management and Blackstone-JV structures are clever, but any well-capitalized REIT could pursue them. Recognizing the absent powers matters because it tells you where the durable edge is not: this is not a business protected by brand or by a business model rivals cannot imitate. Its real moats are switching costs in outpatient and cornered land in labs — full stop.

Now Porter. Threat of new entrants is low in outpatient — you cannot muscle onto a hospital campus without the health system's blessing — but the 2021–2024 lab glut proved it is dangerously high in life science, where any office developer could pour money into speculative wet labs. Bargaining power of buyers is currently inverted between the two: biotech tenants hold the whip hand in lease negotiations today because vacancy is high, while outpatient physicians have almost no alternative space near their campuses. Threat of substitutes deserves a note the outline does not force but the analysis demands: in labs, the substitute is brutally live — a glut of newly built space that tenants can walk to instead, plus the option for landlords to convert failed lab buildings back to office or other uses, which quietly drains supply from the market over time. In outpatient, the substitute threat is thin, because there is no good alternative to a suite physically attached to the operating rooms a surgeon uses. And competitive rivalry is intense and specific: Healthpeak fights Alexandria Real Estate Equities head-to-head in labs — a rival that cut its dividend sharply in the downturn — and Healthcare Realty Trust in outpatient medical, alongside the diversified giants Welltower and Ventas, both of which have leaned hard into the senior-housing recovery that Healthpeak is now re-entering through Janus. The rivalry is not a price war so much as a competition for relationships and cost of capital: whoever can borrow cheapest and knows the health systems best wins the next building. The honest synthesis: Healthpeak's most durable, evidence-backed advantage is the switching-cost moat in outpatient delivery, which is exactly the segment the market treats as boring. The lab segment offers a long-dated cornered resource wrapped around a painful cyclical problem. A portfolio built on the durable engine covering the volatile one is defensible — but only if the volatile one eventually turns.

IX. Bear vs. Bull: Skeptic Stress Test & Current Risk Radar

Put an activist short-seller in the room and the bear case writes itself, because it is built from Healthpeak's own history. The capital-destruction narrative is the sharpest blade: this management team, broadly speaking, sold roughly $4 billion of senior housing at pandemic-trough pricing in 2021 and recycled it into life science at the cycle's peak — then watched lab vacancy blow out to the twenties.1123 Selling low and buying high is the single worst thing a capital allocator can do, and Healthpeak did a version of it in plain sight. Any bull case has to reckon with the fact that the people now asking for trust in their "disciplined" contrarian buying are the same people who mistimed the last great rotation.

The second prong is the re-syndication question. Are the 2026 Janus Living IPO and Blackstone joint venture brilliant unlocks of trapped value, or complex financial engineering designed to mask thin organic growth? The skeptic notes that same-store cash NOI guidance for 2026 straddles zero — a range of roughly negative 1% to positive 1% — which is not the profile of a company compounding organically; it is a company leaning on transactions.27 When Brinker told analysts that same-store NOI is "really a terrible metric" that the company would "prefer to just ignore entirely," a charitable read is that he was defending a holistic view of total-portfolio value; a skeptical read is that a CEO dismissing the industry's standard organic-growth yardstick, in a year that yardstick is flat, is exactly what you would expect.31 Both readings are legitimate, and an investor should hold the tension rather than resolve it prematurely.

Push the activist lens further and the sharpest attack is on complexity and governance rather than on any single number. After the 2026 restructuring, an investor buying Healthpeak stock is buying a genuinely tangled thing: a REIT that consolidates an 82%-owned public subsidiary onto its own financial statements (so the reported revenue and NOI include a business it does not fully own, with a large minority-interest deduction below the line), that collects fees from that same subsidiary through a captive external manager (a textbook related-party arrangement that boards and proxy advisors scrutinize precisely because the incentives of manager and owner can diverge), and that has sold economic slices of its best outpatient assets to a private-equity partner. Each piece is defensible on its own. Together they make the consolidated financials harder to read, create multiple layers at which value can leak to minority partners or to fees, and hand management a menu of levers — buybacks funded by asset sales, accretion "once fully deployed and stabilized," IPO-multiple arbitrage — that can flatter per-share optics without underlying organic growth. None of this is evidence of wrongdoing. It is evidence that the burden of proof has shifted onto management to show, over several years, that the machine produces real per-share cash-flow growth rather than merely the appearance of it.

A brief second-layer note belongs here, on the balance sheet itself. Leverage sits in a reasonable band for the sector, but a REIT's health is ultimately a credit story: its investment-grade rating is what gives it the cheap, reliable access to debt that the whole model depends on, and that rating in turn depends on keeping leverage contained and coverage healthy as low-cost pre-pandemic debt rolls off into a higher-rate world. That is the quiet variable underneath every growth narrative — and it is why the refinancing schedule, not the investor-day slides, is where the real risk lives.

On management credibility, the ledger is genuinely mixed rather than damning. In the merger's favor: the outpatient business has, by management's own account, exceeded the expectations set at announcement, and the synergy and internalization promises appear to be landing.31 The decision to cut off life-science capital deployment before the 2022 crash — which Brinker cites repeatedly — is a real, verifiable instance of discipline that distinguished Healthpeak from peers who kept building into the glut. Against it: the senior-housing timing was poor, and the 2026 structures add balance-sheet and governance complexity (a consolidated 82%-owned subsidiary, an external-management related party, a private-equity JV partner) that makes the reported numbers harder for outsiders to parse.

The current risk radar has three items that actually matter, mechanism-first. Oversupply-duration risk: if the lab glut takes until 2029–2030 to absorb, the lease-up assumptions underwriting Gateway and the rest of the vacant lab space slip years to the right, and the "inflection" never quite arrives. Refinancing and cost-of-capital risk: as a REIT, Healthpeak lives and dies by its spread between asset yields and borrowing costs; management flagged that $650 million of ~3.5% senior notes had to be refinanced in mid-2026 at much higher rates, a direct headwind to FFO, and net debt sat around 5.4x EBITDA.31 Tenant-credit risk: many lab tenants are pre-revenue biotechs, and when one fails, Healthpeak eats the unamortized tenant improvements it fronted to win the lease.

And the bull case, stated fairly, is not flimsy. The demographic tailwind is real and long: an aging population drives structurally rising demand for both outpatient care and the drugs the labs exist to discover. The defensive outpatient engine demonstrably covers the dividend through the lab trough, which buys time for the cycle to turn. And the fee-and-JV model, if it scales, genuinely raises returns on capital. The clearest statement of the bull view is management's own action: Healthpeak bought back $100 million of its stock in April 2026 at an implied FFO yield above 10%, a bet by insiders that their own shares were mispriced against intrinsic value.31 There is a mechanism under the bull case worth naming precisely, because it is what would make the 2026 restructuring more than financial theater. If the private market persistently values healthcare real estate — outpatient buildings at low-6% cap rates, senior housing at premium multiples — more richly than the public market values Healthpeak's shares, then a management team willing to sell assets into the private bid and buy back its own undervalued stock is running a genuine value-creation loop, not a shell game. The April 2026 buyback at a double-digit FFO yield, the Blackstone recap at a 6.1% cap rate, and the Janus multiple arbitrage are all expressions of the same trade, and each is accretive so long as that public-private valuation gap persists.2731 The catch is that the gap is not permanent: if Healthpeak's own share price re-rates upward, the arbitrage closes and the company is back to needing old-fashioned organic growth. So the bull case is really two bets stacked — that the valuation gap stays open long enough to harvest, and that the underlying labs eventually inflect so the company does not need the arbitrage forever.

The bull needs the lab cycle to turn and the fee model to prove durable; the bear needs neither to happen. The next few years of occupancy data will settle it.

X. Playbook: Key Durable Business & Investing Lessons

Healthpeak's forty-year arc is unusually rich in transferable lessons, precisely because so many of them were learned the expensive way.

Beware the concentration trap. The ManorCare episode is the cleanest cautionary tale in the modern REIT canon: a triple-net lease is only as strong as the tenant's operating model, and when a single tenant becomes a quarter of your income, you have stopped being a diversified landlord and started being an unhedged credit bet on that tenant's business.34 Contractual rent is not the same as safe rent.

Capital recycling is a double-edged sword. "Recycling capital" sounds like prudent gardening, but executing macro surgery under duress usually means selling the frightened asset at the bottom and buying the fashionable one at the top. Healthpeak's 2021 senior-housing-for-life-science swap is a live example of how a sound-sounding process can destroy value when the timing is dictated by fear rather than by price.

Structural neutrality is a survival tool. The ability to toggle between the triple-net model (fixed rent, tenant bears the operations) and the RIDEA model (the owner shares in operating upside and downside) is what let Healthpeak both flee senior housing when operations were terrifying and re-embrace its economics through Janus when they recovered.32 A REIT that can only own one lease structure is a REIT that cannot adapt to the cycle.

Cost of capital is the REIT's real product. Underneath every episode in this story — the ManorCare overreach, the near-downgrade that forced the spin-off, the buybacks funded by asset sales — sits a single variable: the spread between what a REIT earns on its buildings and what it pays for the money to own them. A healthcare REIT does not really sell real estate; it sells access to cheap, patient capital that operators and health systems cannot raise as efficiently themselves. When that cost of capital is low, the company can outbid rivals and compound; when a credit scare or a share-price collapse raises it, the same company is forced to sell assets and shrink. Everything else — the leases, the segments, the clever structures — is downstream of that spread. An investor who watches only NOI and misses the cost of capital is watching the wrong dial.

And the subtle one: a ticker can be a brand. Adopting DOC in the Physicians Realty merger instantly aligned the corporate identity with the company's most defensive, most valuable cash-flow asset class — outpatient medical — and quietly signposted the strategic pivot to every investor who typed the symbol.[^26] It costs nothing and it frames everything. The deeper lesson underneath all four: in a business where the assets are commodities — anyone can own a building — the durable edge comes from tenant relationships, structural flexibility, and capital-allocation discipline, not from the bricks themselves.

XI. Epilogue & What to Watch

By the middle of 2026, Healthpeak has, on paper, completed the transformation it began under duress a decade earlier. The toxic skilled-nursing exposure is long gone, spun off and then buried inside a health system. The volatile senior-housing operations are ring-fenced inside Janus Living, retained for their upside but removed from the core's optics. What remains is the barbell Brinker built deliberately: a defensive outpatient engine throwing off inflation-indexed cash flow, and a lab portfolio that is either a coiled spring or a cautionary tale, depending on when — and whether — the biotech cycle turns.

For an investor trying to judge which it is, three metrics cut through the noise. First, same-store cash NOI growth, read by segment. The single most important question is whether lab NOI inflects from flat-to-negative toward positive while outpatient holds above roughly 3% — that combination is what would prove the barbell is compounding rather than just balancing.27 Second, life-science occupancy and lease-up, especially the trajectory in South San Francisco and Boston and the fill rate at Gateway; occupancy is the leading, un-spinnable indicator of whether the lab bet is working.31 Third, the FFO/AFFO payout coverage ratio, which answers the question that matters most to a REIT shareholder: is the dividend being paid out of durable, recurring cash flow, or is it being propped up by one-time transaction proceeds from IPOs and JV sales? Guidance for 2026 puts FFO as adjusted at $1.71 to $1.75 a share against an annualized dividend near $1.22, which looks comfortably covered — but the coverage should be judged on organic cash flow, not on the proceeds of financial engineering.27 These three are the right dials precisely because they are the hardest to spin: occupancy is a physical fact, segment same-store NOI strips out the acquisitions and dispositions that flatter headline growth, and payout coverage read against recurring cash flow reveals whether a dividend is earned or financed. Headline FFO, total NOI, and the parade of transaction announcements can all move for reasons that have nothing to do with the business getting better; these three cannot.

The final reflection is the one the market itself has not resolved. Scott Brinker is betting that a balanced, partner-centric, increasingly capital-light platform — owning the defensive assets, managing the volatile ones, and syndicating slices to Blackstone and public shareholders alike — is the gold-standard model for a modern healthcare REIT. It is an intellectually coherent bet, and the insider buybacks say management believes it. But the same team's history counsels humility about timing, and the flat organic-growth guidance counsels patience about proof. Healthpeak has survived its concentration, survived its mistiming, and survived a pandemic that struck at the heart of its portfolio. Whether it can now compound — rather than merely survive — is a story that the next three years of occupancy and coverage data, not the next investor presentation, will tell.

References

-

New Beginnings for Healthpeak Properties — Nareit REIT Magazine, January/February 2020 ↩↩↩↩

-

HCP To Acquire the Real Estate Assets of HCR ManorCare, Inc. For $6.1 Billion — The Carlyle Group, 2010 ↩↩↩

-

HCP, Inc. Form 10-K for Fiscal Year 2011 (HCR ManorCare acquisition; tenant concentration) — SEC EDGAR ↩↩↩

-

Government Sues Skilled Nursing Chain HCR ManorCare for Allegedly Providing Medically Unnecessary Therapy — HHS Office of Inspector General, 2015-04-21 ↩↩↩↩

-

Quality Care Properties, Inc. Form 8-K, Exhibit 99.1 — Stockholder Letter on Spin-Off — SEC EDGAR, 2016-10-14 ↩↩

-

HCP, Inc. Completes Spin-Off of Quality Care Properties, Inc. — PR Newswire, 2016-10-31 ↩

-

Welltower Inc. Form 8-K, Exhibit 99.1 — Acquisition of Quality Care Properties and ProMedica Joint Venture — SEC EDGAR, 2018-04-25 ↩

-

Welltower and ProMedica Health System Complete Acquisition of Quality Care Properties and HCR ManorCare for $4.4 Billion — PR Newswire, 2018-07-26 ↩

-

HCP Changes Name to Healthpeak Properties — Form 8-K Exhibit 99.1 — SEC EDGAR, 2019-10-30 ↩↩

-

Healthpeak Properties Reports Fourth Quarter and Year Ended 2020 Results — Form 8-K Exhibit 99.1 — SEC EDGAR, 2021-02-09 ↩↩

-

Healthpeak Properties, Inc. Form 10-K for Fiscal Year 2021 (Senior Housing Portfolio Sales) — SEC EDGAR ↩↩

-

Healthpeak Properties Third Quarter 2021 Results — Form 8-K Exhibit 99.1 — SEC EDGAR, 2021-11 ↩

-

U.S. Seniors Housing Occupancy Reaches New Low — National Investment Center (NIC), 2021-04-08 ↩

-

Senior Housing Occupancy Rate Over Halfway Back to Pre-Pandemic Level — National Investment Center (NIC) ↩

-

The Impact of COVID-19 on Seniors Housing — NORC at the University of Chicago for NIC, 2021-06-03 ↩

-

Healthpeak Properties Announces Latest Life Science Development, Vantage, in South San Francisco — PR Newswire, 2021 ↩

-

Healthpeak to Build $393M Bay Area Campus — CommercialSearch ↩

-

Healthpeak Receives Entitlements for Additional 1.3 Million Square Feet at the Vantage Campus — Healthpeak Investor Relations, 2023-12-19 ↩

-

Healthpeak Reports Strong Q4 2022 Life Sciences Results — Wolf Media USA (reprint of Healthpeak results), 2023-02-10 ↩↩

-

Lab Space Vacancy Rates Rising — The Boston Globe, 2023-11-10 ↩

-

Boston-Area Lab Vacancies Hit 25 Percent as Industry Retrenches — Banker & Tradesman, 2025 ↩

-

It's a Great Time to Be in Life Sciences — Not So Great If You Own a Lab — Bisnow, 2026 ↩↩

-

Healthpeak Properties Announces Changes to Executive Team (Brinker named CEO; Herzog steps down) — PR Newswire, 2022-10-06 ↩↩

-

Life Sciences: Healthpeak-DOC Merger Creates $21 Billion REIT (merger terms, exchange ratio, synergies, portfolio size) — Wolf Media USA, 2024-03-04 ↩↩↩↩

-

Healthpeak Completes Merger; Combined Company to Trade Under "DOC" — Form 8-K Exhibit 99.1 — SEC EDGAR, 2024-03 ↩

-

Healthpeak Properties Raises 2026 Earnings Guidance Following Completion of the Janus Living IPO, Accretive Capital Allocation, and Strong First Quarter 2026 Results — Healthpeak Investor Relations, 2026-05 ↩↩↩↩↩↩↩↩↩

-

Healthpeak Properties and Janus Living Announce Pricing of Upsized $840 Million Janus Living Initial Public Offering — Healthpeak Investor Relations, 2026-03 ↩↩

-

Healthpeak Properties and Janus Living Announce Closing of Janus Living Initial Public Offering — Healthpeak Investor Relations, 2026-03-23 ↩↩

-

Healthpeak Properties Announces $925 Million of Transaction Activity (Gateway campus acquisition) — Healthpeak Investor Relations, 2026-01-12 ↩

-

Healthpeak Properties (DOC) Q1 2026 Earnings Call Transcript — The Motley Fool, 2026-05-06 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

What Is Janus Living and Why Is Healthpeak Spinning It Off? (portfolio, units, RIDEA, external manager) — Kavout Market Lens, 2026 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube