Dolby Laboratories: The "Intel Inside" of Sensory Experience

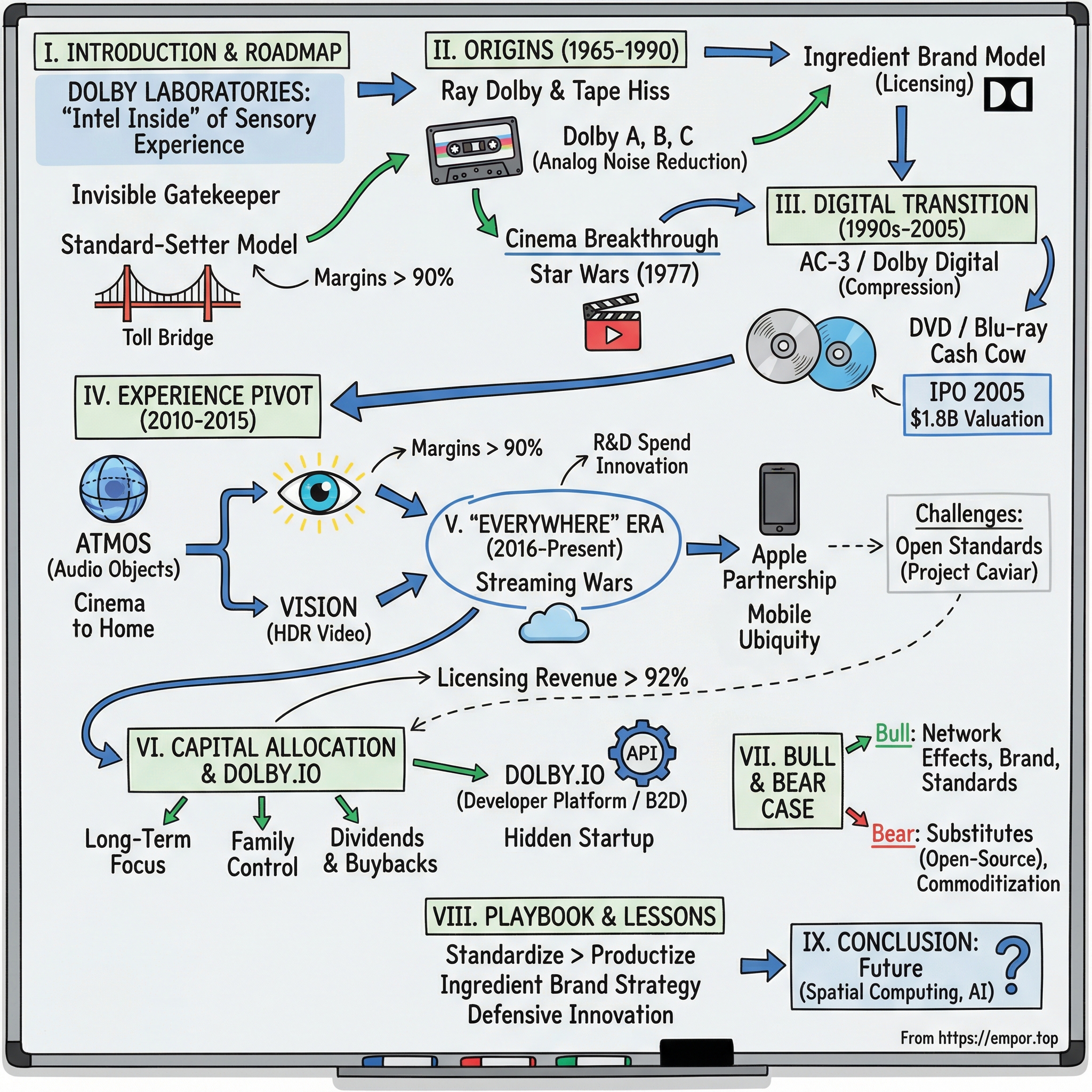

I. Introduction and Episode Roadmap

Picture this: you are sitting in a darkened cinema, the previews have ended, and the house lights fade to black. Then it begins. A deep, resonant pulse sweeps across the room, not from the screen but from everywhere at once, as if the air itself has begun to vibrate. Two interlocking "D" shapes materialize on screen in luminous white. The bass drops into your sternum. Sound objects, rain, thunder, a bird in flight, orbit around and above you with an almost hallucinatory precision. For thirty seconds, you are not watching a trailer. You are inside one.

That thirty-second pre-show demonstration is perhaps the most effective piece of brand advertising ever created for a product most consumers cannot see, cannot touch, and cannot consciously identify inside the device they are holding. That product is Dolby.

What started as a one-man noise-reduction laboratory above a flat in London in 1965 became, over six decades, the invisible gatekeeper of the entire global entertainment industry.

From the mixing stage where a Marvel film gets its final audio polish, to the iPhone playing a podcast on a morning commute, to the Netflix interface promising "Dolby Vision" in a bright badge next to a title, to the Apple Vision Pro rendering spatial audio in three dimensions around a user's head, Dolby Laboratories has embedded itself so deeply into the infrastructure of how the world hears and sees media that removing it would be akin to pulling the electricity grid out from under a city. Most people encounter Dolby technology dozens of times a day and never realize it. That is by design.

The financial profile is remarkable. Dolby generated roughly $1.35 billion in revenue in fiscal 2025, with approximately 90% non-GAAP gross margins. Those are software margins, except Dolby is not a software company in the conventional sense. It does not sell subscriptions. It does not run a marketplace. It is, in effect, a standards body that happens to be a for-profit corporation listed on the New York Stock Exchange.

The company does not make the movie. It does not make the television. It writes the rulebook that tells those two things how to talk to each other, and then collects a toll on every handshake. Licensing revenue, the royalties paid by device manufacturers, content platforms, and media companies for the right to implement Dolby's technology, constitutes over 92% of total revenue. The rest comes from cinema equipment, products, and the nascent Dolby.io developer platform.

This is a story about the "Standard-Setter" business model, one of the most durable competitive moats in all of capitalism. It is the story of Ray Dolby, a prodigy engineer who worked on the world's first video tape recorder at age sixteen, who walked away from the San Francisco Peninsula that would become Silicon Valley to found a company in London, and who invented a licensing structure that predated and arguably inspired Intel's famous "Intel Inside" campaign by two decades.

It is the story of a company that risked irrelevance when physical media died, then reinvented itself by jumping from audio into video with Dolby Vision and from cinema channels into three-dimensional sound objects with Dolby Atmos. It is the story of the "Apple Moment" in 2018 that blew the addressable market wide open, the streaming wars that turned Dolby into the premium badge every platform needed, and a quiet, under-the-radar bet on a developer API platform called Dolby.io that could reshape what this company looks like in the next decade.

Let us start from the beginning.

II. Origins: Ray Dolby and The Golden Silence (1965-1990)

In 1949, in a modest office park in Redwood City, California, a sixteen-year-old high school student named Ray Milton Dolby walked through the doors of the Ampex Corporation. Alex Poniatoff, the Russian-born founder of Ampex, had spotted the kid, a student at Sequoia High School, and asked if he wanted a weekend and vacation job. Dolby said yes. It was the kind of casual decision that reshapes industries.

Ampex was then a small company making audio tape recorders, mostly for professional broadcast applications. Dolby, still too young to vote, threw himself into the work with a precocious intensity that startled his older colleagues. He helped develop a geophysical recorder, an instrument used in seismology and oil exploration, before transferring to what would become the defining engineering project of the 1950s: the video tape recorder.

Before Ampex, television was either broadcast live or played back from expensive film recordings called kinescopes. The notion that you could capture a television signal on magnetic tape, the way you captured audio, was considered borderline fantasy by most of the industry. The problem was bandwidth: a video signal contained orders of magnitude more information than an audio signal, and no one had figured out how to write and read that much data from a moving tape at the speeds required.

Dolby was part of the small team that proved it could be done. While simultaneously pursuing his electrical engineering degree at Stanford, he led the electronic aspects of the project, contributing critical innovations in head-switching circuitry and the electronic architecture that made the system practical. He was drafted into the Army in April 1953, but before reporting for duty, he and the team had laid down many of the basic parameters of the system.

When he returned in January 1955, work resumed in earnest. In April 1956, Ampex unveiled the prototype Quadruplex videotape recorder to a stunned audience of broadcast executives. It was a machine that would revolutionize television production forever. IEEE oral-history accounts credit Dolby with major engineering contributions. He was, at this point, twenty-three years old.

Most engineers with that pedigree would have stayed on the Peninsula and ridden the early wave of what would become Silicon Valley. The semiconductor industry was taking root just miles away. Fortunes were being made. Dolby did something entirely unexpected. He applied for, and won, a Marshall Scholarship to study at the University of Cambridge in England. He entered Pembroke College and pursued a PhD in physics at the Cavendish Laboratory, the legendary institution where Rutherford had split the atom and where Watson and Crick had discovered the structure of DNA just a few years earlier. It was an unusual choice for a young American engineer who could have written his own ticket in California industry.

But Dolby was not merely an engineer. He was a thinker, and the Cambridge years broadened his intellectual frame in ways that would prove essential. He completed his doctorate in 1961, then took a position that seemed to have nothing whatsoever to do with audio engineering. From 1963 to 1965, he served as a United Nations technical advisor in India, helping establish the Central Scientific Instruments Organisation in Chandigarh. He was, in effect, helping build India's capacity for precision scientific measurement. It was a humanitarian detour, and it was during this period that the epiphany struck.

While recording traditional Indian music for UNESCO on portable equipment, Dolby listened back to the tapes and found them plagued by a persistent, infuriating sonic fog: tape hiss. The problem was not unique to India, of course. Every magnetic tape recording in the world suffered from the same phenomenon, a constant, audible noise introduced by the random magnetization of the tape's iron oxide particles. For professional studios with expensive equipment, the hiss could be partially managed. For consumer equipment, it was simply accepted as an unavoidable degradation of quality. Dolby, listening to those UNESCO recordings in a hot Indian office, decided it did not have to be.

He returned to London in 1965, rented a small space, hired four employees, and founded Dolby Laboratories. The first product was the Dolby A-Type Noise Reduction System, a professional unit designed for recording studios.

The underlying principle was elegant. Magnetic tape hiss existed primarily in the high-frequency range of the audio spectrum. Dolby's system worked by selectively boosting quiet, high-frequency sounds during recording (a process called "companding") and then symmetrically reducing them during playback. The hiss, which lived in those same high frequencies, got reduced along with the intentional boost. The result was a dramatically cleaner, more dynamic recording without the pumping artifacts of cruder noise gates that had been tried before. It was a solution that worked with the physics of the problem rather than against it.

Decca Records in London was the first major customer. The professional audio world took notice quickly. But it was the next move that revealed Ray Dolby as not merely a great engineer but a great business strategist, someone who understood value capture as deeply as he understood signal processing.

Rather than simply manufacturing and selling expensive hardware boxes to studios, a business model that would have generated respectable but limited revenue from a small customer base, he developed a simplified consumer version, the Dolby B system, in 1968.

Then he did something radical: he licensed it to every cassette deck manufacturer willing to pay. KLH, an American audio company, received the first exclusive license, which lasted until 1970. After that, the floodgates opened. Pioneer, Sony, Nakamichi, Technics, and dozens of other consumer electronics brands embedded Dolby B circuitry into their products, paying a per-unit royalty for the privilege.

This was the birth of the "ingredient brand" model. Decades before Intel convinced PC buyers to look for the "Intel Inside" sticker, before Gore-Tex put its hangtag on North Face jackets, Ray Dolby had already solved the puzzle that most technology companies never crack: how do you make consumers demand a component they cannot see?

His answer was twofold. First, pre-recorded cassette tapes began carrying the Dolby logo, which trained buyers to associate the double-D mark with quality. If you were browsing a record store in 1975, a cassette tape with the Dolby logo on its spine signaled "this was recorded properly."

Second, by licensing broadly rather than manufacturing exclusively, Dolby ensured that the mark appeared on equipment across every price tier. By the mid-1970s, Dolby B was used on nearly all pre-recorded cassette tapes, and every cassette deck above the bargain bin included the technology.

The transformation was complete: the compact cassette, which had been designed by Philips as a dictation format, became a viable medium for high-fidelity music reproduction, and Dolby noise reduction was the technology that made it possible. The income generated from these licensing fees funded everything that came next.

Then came the cinema. The first film to use Dolby noise reduction on its pre-mixes and masters was Stanley Kubrick's "A Clockwork Orange" in 1971, though the release prints used a conventional optical track, so audiences did not directly experience the improvement.

The real breakthrough arrived in 1975 with the Dolby Stereo format, which managed to encode four channels of audio (Left, Center, Right, and Surround) onto a standard 35mm optical soundtrack using a matrix encoding technique. The technology launched quietly in a handful of films, but on May 25, 1977, George Lucas's "Star Wars" detonated it into the mainstream.

Every print of "Star Wars" carried a Dolby-encoded stereo soundtrack. The film's sound design, created by Ben Burtt, was a sensory assault: lightsabers humming, TIE fighters screaming, the rumble of the Death Star. None of it would have worked properly in a theater with a single mono speaker behind the screen, which was still the standard in most cinemas.

Twentieth Century Fox and Dolby embarked on an aggressive campaign to encourage theater owners across the country to upgrade their sound equipment for Dolby Stereo presentation. Many owners, facing the prospect of audiences choosing the Dolby-equipped theater down the street over their own, did exactly that. Within a few years, six thousand cinemas worldwide were equipped for Dolby Stereo.

The "Dolby" brand became synonymous with the blockbuster experience itself. You did not just go to see "Star Wars." You went to hear it, and what you heard was Dolby.

The strategic pattern was now firmly established, and it would repeat for the next five decades: invent a technology, get it adopted as the de facto standard first in the professional world, then cascade it down to consumers through licensing. Capture the standard, and the revenue follows automatically as every product that implements the standard pays a royalty.

The company remained private, profitable, and under the quiet, absolute control of its founder. Ray Dolby was not chasing venture capital or hypergrowth. He was building a toll bridge, and every car on the highway of global entertainment was about to start paying the toll.

III. The Digital Transition and The DVD Cash Cow (1990s-2005)

By the late 1980s, the audio industry stood on the edge of a cliff that most analog- era companies would tumble over. Compact discs, introduced by Philips and Sony in 1982, had already begun to displace vinyl records and cassette tapes. The digital revolution was not coming; it had arrived. And it posed a genuinely existential question for Dolby Laboratories: in a world without tape hiss, what exactly does a noise-reduction company sell?

This was not a theoretical concern. The core Dolby B and Dolby C noise reduction systems, the technologies that had generated the licensing revenue funding the entire enterprise, were analog solutions to an analog problem. A compact disc did not have tape hiss. A digital audio tape did not have tape hiss. If the cassette went away, and it was clearly going away, the revenue stream went with it.

The answer, it turned out, was compression. As audio moved from analog to digital, the central engineering challenge shifted from removing unwanted noise to a new question: how do you pack high-quality multichannel sound into limited bandwidth?

A raw, uncompressed multichannel audio signal was enormous, far too large to fit on a film soundtrack, to broadcast over the airwaves, or to store efficiently on an optical disc alongside video. Someone was going to solve the compression problem. Dolby's engineers were determined it would be them.

The result was AC-3, a lossy audio compression algorithm based on the modified discrete cosine transform (MDCT), branded to the world as "Dolby Digital."

To explain what this meant in layman's terms: the algorithm analyzed audio data and discarded information that the human ear was unlikely to perceive, a technique called "perceptual coding." It was the audio equivalent of compressing a photograph by removing details too fine for the eye to notice, dramatically reducing file size while preserving subjective quality.

The format could encode 5.1 channels of surround sound, five full-range channels plus a dedicated subwoofer channel, into a data stream compact enough to fit alongside the analog optical track on a standard 35mm film print.

The cinema debut came in 1991, when a limited experimental release of "Star Trek VI: The Undiscovered Country" played in three U.S. theaters with Dolby Digital sound. In 1992, "Batman Returns" became the first wide commercial release to carry a Dolby Digital soundtrack. The technology proved itself in the most demanding environment possible: a packed cinema audience paying close attention to every explosion and whispered line of dialogue.

But the real jackpot was not cinema. It was the living room.

In the mid-1990s, the consumer electronics industry was converging on the DVD as the successor to VHS. The DVD format specification, developed by a consortium of major electronics and media companies, needed to designate a mandatory audio codec, the digital compression format that every DVD player would be required to decode. A fierce standards war played out behind closed doors. Multiple competing proposals vied for adoption, including offerings from competitors like DTS.

Dolby Digital won the mandate to become the required audio format for DVD players in NTSC markets, essentially North America and Japan. The implications were staggering in their scale and elegance. Every single DVD player manufactured for the North American market had to include a Dolby Digital decoder, and the manufacturer had to pay Dolby a licensing fee for that decoder. Every DVD disc mastered with a Dolby Digital soundtrack, which was virtually every DVD, was encoded using Dolby technology.

The installed base scaled into the hundreds of millions of units within a few years. Each unit generated a small but relentless stream of revenue flowing back to San Francisco. It was, as industry observers noted, a license to print money.

And unlike printing money, it came with almost no marginal cost: once the technology was developed and the standard was set, the licensing revenue was essentially pure profit flowing from the mathematical certainty that every DVD player sold on the planet needed Dolby inside.

The DVD licensing windfall was later extended and amplified by the Blu-ray Disc standard, which mandated Dolby Digital as a baseline audio format, and by the ATSC digital television standard in the United States, which adopted AC-3 as its standard audio codec.

Every HDTV broadcast in America, every local news broadcast, every football game, every sitcom, used Dolby Digital encoding. The toll bridge had become a multilane highway.

This cash engine powered Dolby into its IPO era. On February 17, 2005, exactly twenty-one years ago to this day, Dolby Laboratories made its public debut on the New York Stock Exchange at $18 per share. The company sold 10.5 million Class A shares, while founder Ray Dolby sold an additional 17 million shares. The offering raised approximately $495 million at a valuation of $1.8 billion.

It was a remarkable debut for a company that most consumers did not even know existed as a standalone business. People knew the logo. They did not know it was its own company.

The dual-class share structure adopted at the IPO was deliberate and telling. Class B shares, held primarily by Ray Dolby and his family, carried ten votes per share versus one vote for the publicly traded Class A shares. The structure ensured that even after going public, the Dolby family retained overwhelming voting control over the company's direction.

This was not a company preparing to be influenced by activist hedge funds or quarterly earnings pressure. It was a company whose founder had built a sixty-year business on patience and long-term thinking, and the share structure was designed to protect that philosophy from the short-termism of public markets. Think of it as a moat around the moat.

The DVD era validated the Dolby licensing model at global scale and embedded a critical lesson into the company's institutional DNA: once your technology is in the standard, the revenue is as certain as gravity.

But the physical media wave that had powered this golden era was about to crest and break. The streaming revolution was gathering force, and with it, the most dangerous period in Dolby's history since the death of analog tape.

IV. The "Experience" Pivot: Atmos and Vision (2010-2015)

By 2010, the writing on the wall was clear to anyone willing to read it. DVD sales in the United States had peaked in 2006 at roughly $16 billion and were in steep, accelerating decline. Blu-ray adoption, while respectable, was never going to come close to matching the DVD installed base. Meanwhile, Netflix had completed its dramatic pivot from a disc-by-mail service to an internet streaming platform, and rivals were rushing to follow. Digital downloads and nascent streaming services were cannibalizing the physical media business from multiple directions simultaneously.

For Dolby, this was not merely a revenue concern. It was an existential one. If the licensing model was fundamentally tied to physical disc formats, and those formats were dying, then the high-margin engine that powered the company's extraordinary profitability was at risk of slow, inexorable decay.

Licensing revenue from DVD and Blu-ray would not disappear overnight, discs were still being sold and pressed, but the trajectory was unmistakable. Dolby needed to reinvent its revenue model for a world where content was delivered over the internet, not on a shiny plastic disc.

The response came in two transformative product launches that, taken together, redefined what Dolby was as a company. The leadership team, now headed by CEO Kevin Yeaman, who had taken the helm in March 2009, decided that Dolby would stop being an "audio company" and become a "sensory experience company."

This was not a marketing rebrand. It was not a consultant's PowerPoint slide. It was a genuine, capital-intensive strategic pivot, one of the most consequential in the company's history, and it required Dolby to do something it had never done before: push into an entirely new sensory domain.

The first breakthrough was Dolby Atmos, which debuted in June 2012 at the El Capitan Theatre in Hollywood for the premiere of Pixar's "Brave." To understand why Atmos represented such a radical departure, it helps to understand what it replaced.

For decades, surround sound had been defined by "channels," fixed configurations like 5.1 (five speakers arranged around the listener plus a subwoofer) or 7.1 (seven speakers plus a subwoofer). A sound engineer mixing a film for 5.1 surround had to decide, at the point of mixing, which speaker each sound would come from. The rain goes to the left surround. The explosion goes to the center. The ambient noise goes to the right rear.

The result was a fixed audio bed that played identically on every 5.1 system, whether it was a purpose-built mixing stage in Hollywood or a consumer setup in a suburban living room with speakers placed in somewhat approximate positions. Think of it like painting a mural sized exactly for one wall. If your wall was a different size or shape, the image got stretched, cropped, or simply did not fit right.

Atmos threw this entire paradigm out. Instead of mixing sound into fixed channels, engineers could now treat individual sounds as "objects," each tagged with three-dimensional positional metadata describing exactly where in space that sound should exist. A helicopter is "here" at coordinates X, Y, Z. A raindrop is "there." A voice is "over there," six feet to the left and slightly above.

The Atmos rendering engine, running on whatever playback device the listener happened to have, would take those object coordinates and map them in real time onto whatever speaker configuration was actually present, whether that was a sixty-four-speaker cinema rig with overhead channels or a two-speaker laptop. The format supported up to 128 simultaneous audio tracks with positional metadata, an enormous leap from the previous ceiling.

The analogy that makes this click is the difference between a JPEG photograph and a 3D model. A JPEG is a fixed, flat image that looks the same on every screen. A 3D model can be rotated, zoomed, and viewed from any angle because the spatial information is inherent in the data. Atmos was, in effect, the 3D model of audio.

The go-to-market strategy was vintage Dolby: start at the apex of the professional world and let gravity pull the technology downward. The initial cinema rollout was deliberately limited, about 25 installations worldwide in 2012, expanding to over 300 in 2013. The first blockbusters mixed in Atmos, including Peter Jackson's "The Hobbit: An Unexpected Journey," created the kind of audience buzz that film journalists wrote about and cinema owners could not ignore.

Exhibitors began demanding the upgrade because audiences were seeking out Atmos-equipped theaters. Content creators mixed in Atmos because cinemas supported it. Cinemas invested in Atmos because content was being mixed for it. The network effect was textbook, a self-reinforcing flywheel that accelerated with each turn.

By 2024, Dolby had surpassed 4,000 Atmos-enabled cinema screens worldwide, with approximately 275 full "Dolby Cinema" installations offering the complete premium experience of Atmos sound and Dolby Vision projection.

The second, and arguably bolder, strategic move came two years after the Atmos debut. In January 2014, Dolby announced Dolby Vision, a proprietary High Dynamic Range (HDR) imaging format. This was Dolby's entrance into the video space, a domain where it had absolutely no historical presence. The company had been synonymous with sound for nearly fifty years. Now it was claiming that it could define the future of the picture as well.

HDR, for the unfamiliar, refers to the ability to display a dramatically wider range of brightness levels, from the deepest, most light-absorbing blacks to the most searing, eye-squinting highlights, along with a vastly broader color palette.

The simplest way to grasp the difference is to think of standard dynamic range video as a box of 24 crayons. You can draw a picture, but your sunset will be orange and your ocean will be blue, and both will be approximately the same brightness. HDR is a box of 120 crayons, with the ability to press much harder for vivid intensity or barely touch the paper for the faintest whisper of color.

On a capable display, the difference is immediately, viscerally apparent. Sunlight looks like sunlight. Shadow holds detail and texture instead of collapsing into a flat grey void. Neon signs glow against a dark cityscape with the intensity they have in real life.

What made Dolby Vision distinctive, and what made it controversial, was its use of "dynamic metadata." The competing open standard, HDR10, used "static metadata," a single set of brightness and color instructions that applied to the entire program from beginning to end. Every scene, whether it was a sunlit beach or a candlelit bedroom, got the same optimization parameters.

Dolby Vision, by contrast, sent metadata on a scene-by-scene, or even frame-by-frame, basis. The display continuously adjusted its output to optimize each moment individually. The difference in practice was that dark scenes in a Dolby Vision presentation held their shadow detail even if the preceding scene had been extremely bright, because the display knew, from the metadata, to adjust its tone mapping for each scene independently.

The trade-off was complexity and cost. Dolby Vision required a dedicated processing chip in the television or device, and manufacturers paid Dolby a licensing fee for the privilege of including it. Pushing a proprietary, licensed HDR format into a market that also offered a free alternative (HDR10, later supplemented by Samsung-backed HDR10+) was a strategic gamble.

Vizio's 2015 Reference Series became one of the first televisions to ship with Dolby Vision support, and by late 2015, Vudu began offering Dolby Vision streaming titles, establishing the first consumer-accessible content pipeline.

Between these two product launches, Dolby executed an acquisition that was less glamorous but strategically essential. In February 2014, the company announced a deal to acquire Doremi Labs, a Burbank-based manufacturer of digital cinema servers, for $92.5 million in cash plus up to $20 million in contingent consideration. The deal closed in October 2014.

On the surface, buying a hardware company that made cinema projection-booth equipment seemed oddly retrograde for a licensing-focused IP company. Why would a firm that prizes its asset-light model want to own a hardware manufacturing business?

The strategic logic was sharper than it appeared. Doremi's cinema servers sat in the projection booths of thousands of theaters worldwide. They were the physical box that ingested digital cinema packages and played them back through the projector. By owning that box, Dolby could ensure seamless, rapid deployment of Atmos into theaters without depending on a third-party server manufacturer to prioritize Atmos compatibility.

It was not about the margins on hardware sales. It was about controlling the distribution bottleneck, a classic infrastructure play. Think of it as Dolby buying the railroad to guarantee that its freight would be delivered on schedule, regardless of what other railroad operators decided to prioritize.

The $92.5 million price tag, which some analysts initially questioned, looks modest in retrospect when measured against the speed with which Atmos achieved cinema ubiquity.

By the end of 2015, Dolby had completed perhaps the most ambitious reinvention in its history. It was no longer an audio noise-reduction and codec company. It was a full-stack "sensory experience" company spanning sound and picture, cinema and home, professional production and consumer playback.

The question, the one that would determine whether this pivot truly succeeded, was whether Atmos and Vision could break free of the premium niche and achieve the kind of mass-market ubiquity that Dolby Digital had enjoyed in the DVD era. The answer would come from Cupertino.

V. The "Everywhere" Era and The Apple Kingmaker (2016-Present)

The mid-2010s presented Dolby with a paradox that would have been familiar to any technology company that has ever tried to cross the chasm from early adopter enthusiasm to mass-market adoption. Atmos and Vision were generating critical acclaim and genuine excitement among home theater enthusiasts, cinema purists, and the professional production community, but their real-world addressable market was still constrained to two relatively narrow segments: premium cinema installations, numbering a few hundred screens worldwide, and high-end home entertainment equipment, meaning expensive soundbars, AV receivers, and flagship televisions that cost several thousand dollars.

The licensing revenue from these categories, while growing, was not remotely sufficient to replace the declining physical media royalty stream.

Dolby needed a much larger surface area. It needed Atmos and Vision to be everywhere, not just in the living rooms of audiophiles and the screening rooms of Hollywood executives, but in every pocket, every earbud, every laptop, every car. That kind of ubiquity required a partner with the market reach and consumer influence to drive adoption at planetary scale.

To understand how that partner emerged, it is worth stepping back to examine an earlier acquisition, one that initially flew under the radar of most analysts but would prove pivotal to the company's streaming-era positioning. In November 2007, Dolby had acquired Coding Technologies AB, a privately held Swedish company headquartered in Stockholm, for approximately $250 million net of cash.

At the time, this was Dolby's largest acquisition by a wide margin, and the price prompted raised eyebrows. Coding Technologies was a small company, founded in 1997, with clever but niche technology. What could possibly justify a quarter-billion-dollar price tag?

The answer lay in what Coding Technologies had built. The company had developed Spectral Band Replication (SBR) and related innovations that enabled high-quality audio compression at dramatically lower bitrates. Their technology had been incorporated into open standards like the HE-AAC (High Efficiency Advanced Audio Coding) family of codecs, which in turn had been adopted into 3GPP (the standard governing mobile telecommunications), DVB (digital video broadcasting), and MPEG.

In simple terms, Coding Technologies had cracked the problem of making audio sound good over thin data pipes, exactly the problem that the entire mobile and streaming industry would be grappling with for the next two decades.

In hindsight, the Coding Technologies deal ranks among the best acquisitions in Dolby's history. As mobile data networks expanded from 3G to 4G to 5G, and as streaming services scaled from millions to hundreds of millions of subscribers in the 2010s, the low-bitrate, high-efficiency codecs that Coding Technologies brought to Dolby became essential plumbing for how music and audio reached billions of people daily.

When Spotify streamed a song to a commuter's earbuds, when Apple Music delivered a track over a cellular connection, when a YouTube video played audio on a smartphone in Lagos or Jakarta or Sao Paulo, the underlying codecs frequently touched Dolby-licensed intellectual property.

The $250 million purchase price, which seemed aggressive in 2007 for a company of Coding Technologies' size, bought Dolby a permanent, standard-essential seat at the table of mobile and streaming audio, the precise markets that would come to dominate the next era of media consumption. It was a home run, paid for years before anyone realized the game had even started.

This brings us to what might be called the "Apple Moment." In September 2018, Apple announced the iPhone XS and iPhone XR with built-in speakers supporting Dolby Atmos playback. The Apple TV 4K had already gained Dolby Atmos support, and Apple was integrating Dolby Vision deeply into its content pipeline for the launch of Apple TV+ in November 2019. Nearly all Apple TV+ originals were being produced and delivered in both Dolby Vision and Dolby Atmos.

The significance of the Apple partnership was tectonic. It was not merely another device manufacturer adding another spec line to its product sheet.

Before the Apple integration, Dolby Atmos was a living room and cinema technology. Experiencing it properly required either a ticket to an Atmos-equipped theater or a dedicated home setup with multiple speakers or a premium soundbar. The audience was self-selecting: people who cared enough about audio to spend real money on equipment.

After the Apple integration, Atmos became a headphones-and-mobile technology. Anyone with an iPhone XS or later and a pair of AirPods could experience spatial audio. The total addressable market did not merely expand. It detonated.

There are well over a billion active iPhones in the world. There are only a few hundred million premium AV receivers. The shift from "living room technology" to "pocket technology" was the single most important inflection point in Dolby's modern history, and it happened not because Dolby built a consumer device, but because the world's most valuable consumer electronics company decided that Dolby's technology was essential to its own premium positioning.

The timing coincided with, and was amplified by, the streaming wars. Netflix, Disney+, Amazon Prime Video, HBO Max (now Max), Apple TV+, and others were competing fiercely for subscribers in a market where the content libraries were increasingly commoditized. Every major platform had blockbusters, every platform had award-winning originals, and consumers were drowning in options.

Quality differentiation became a critical strategy for justifying premium pricing tiers, and the Dolby badge became the shorthand for "this is the best version of this content."

Netflix reserved Dolby Vision and Dolby Atmos for its Premium subscription tier, the most expensive option. Disney+ limited Atmos to its highest-priced plan. Amazon Prime Video, which had once included Dolby technologies for all subscribers, eventually restricted Dolby Vision and Atmos to the ad-free plan priced at $18 per month.

In each case, the Dolby badge served a dual purpose: it signaled technical quality to the consumer, and it served as a justification for the platform to charge more. Dolby had become, almost by accident, a pricing lever for the streaming platforms.

The streamers needed Dolby to sell "Premium," and Dolby needed the streamers to deliver Atmos and Vision content at scale. It was a symbiosis of mutual economic interest.

The competitive landscape, however, was not without threats, and understanding them is essential to any assessment of Dolby's durability. The most significant challenge came from Google's "Project Caviar," announced through the Alliance for Open Media in September 2022. Project Caviar proposed royalty-free, open alternatives to both Dolby Atmos (spatial audio) and Dolby Vision (HDR).

Samsung, the world's largest television manufacturer and a company that had long resented paying Dolby licensing fees, backed the rival HDR10+ format as an open alternative to Dolby Vision. The broader Alliance for Open Media, whose members included Google, Apple, Amazon, Meta, Microsoft, Netflix, and others, had already produced AV1, a royalty-free video codec designed to challenge the patent-encumbered HEVC standard.

These open-source and royalty-free alternatives represented the most serious long- term threat to Dolby's licensing model. The logic was straightforward: if device manufacturers and content platforms could achieve "good enough" perceptual quality without paying Dolby royalties, rational economic actors would eventually gravitate toward the free option.

But as of early 2026, the threat has not materialized into meaningful revenue displacement. The reason is instructive and gets to the heart of what makes standards businesses so defensible. Standards adoption is extraordinarily sticky.

Once a technology is embedded into the entire production workflow, from the mixing stages at Skywalker Sound to the mastering labs at Netflix to the quality assurance pipelines at Samsung's television factories, the switching costs are enormous. They are not primarily financial costs. They are workflow costs, retraining costs, compatibility costs, and risk costs.

Content creators have invested years learning to mix in Atmos. Displays have been calibrated for Dolby Vision. Consumer expectations have been set. The "Dolby" badge has been marketed and absorbed into the popular consciousness as meaning "premium."

Project Caviar and HDR10+ face the classic chicken-and-egg problem: content creators will not invest significant resources in mixing for a format that consumers do not yet have, and consumers will not demand hardware that supports a format for which little content exists. Dolby has had a decade-plus head start in solving this coordination problem for Atmos and Vision, and that head start compounds with every new title mixed, every new device shipped, and every new streaming contract signed.

VI. Capital Allocation and The "Hidden" Startup: Dolby.io

Kevin Yeaman became CEO of Dolby Laboratories in March 2009. His background tells an important story about the kind of company Dolby had become and the challenges it faced.

Where Ray Dolby was an engineer's engineer, a Cambridge PhD physicist who thought in terms of signal processing, harmonic distortion, and noise floors, Yeaman was a finance professional. He had joined Dolby as Chief Financial Officer in October 2005, just months after the IPO, tasked with building the financial infrastructure to support a newly public company.

Before Dolby, he had spent seven years as CFO of Epiphany, a publicly traded enterprise software company, and held financial leadership roles at Informix Software and spent nearly a decade at KPMG. His educational pedigree, a bachelor's degree in commerce from Santa Clara University, was a far cry from Cambridge and the Cavendish Laboratory.

The appointment of a CFO-turned-CEO at a deep-technology company founded by a legendary inventor raised eyebrows. Could a finance guy steer a technology company through the most turbulent period of media industry disruption in a generation?

Yeaman's tenure, now stretching past seventeen years, has provided a decisive answer. The challenge facing Dolby after 2009 was not primarily an engineering problem. The engineering talent was world-class and deeply embedded in the organization. The challenge was a strategic and business-model problem: how to navigate the company from the physical media era into the streaming and mobile era without losing the extraordinary margin profile that made Dolby unique.

Yeaman proved to be the right leader for exactly that transition. Under his watch, the company launched Atmos and Vision, executed the pivotal Doremi Labs and Coding Technologies integrations, built the Apple and streaming platform partnerships that exploded the addressable market, and initiated the Dolby.io platform bet.

In 2014, he was inducted as a member of the Academy of Motion Picture Arts and Sciences, a recognition that the film industry regarded him as more than merely a corporate custodian.

His compensation structure tells a story about governance and alignment that institutional investors pay attention to. In fiscal 2025, Yeaman's total compensation was approximately $10.2 million, of which over 90% was performance-based, composed primarily of stock awards and options tied to long-term value creation metrics. Only about 9% of his pay came from base salary.

This structure is notable because it incentivizes exactly the kind of patient, moat-deepening behavior that a licensing business requires: multi-year investment in standards adoption, long technology development cycles, and the discipline to forgo short-term revenue opportunities in favor of permanent ecosystem embeddedness.

A CEO whose wealth is overwhelmingly tied to long-term stock performance has every reason to think about the ten-year competitive position, not the next quarter's earnings beat.

It is worth noting the family governance dimension as well. Ray Dolby passed away on September 12, 2013, at the age of 80, from leukemia. His wife, Dagmar Dolby, assumed ownership of nearly 36% of the company.

The Dolby family, through its Class B shares with their ten-to-one voting power, continues to exercise significant control over the company's strategic direction. This founder-family governance structure, combined with a CEO whose compensation is overwhelmingly long-term, creates a governance architecture that is highly unusual among public companies and highly aligned with the kind of patient capital allocation that IP-centric businesses require.

On capital allocation more broadly, Dolby has been disciplined but not dramatic. The company returns capital through a consistent and growing dividend, now paid quarterly at an annualized rate of $1.32 per share, with nine consecutive years of increases and a five-year compound annual growth rate of roughly 9%.

Share repurchases have totaled approximately $600 million since 2020, with a recent pace around $150 million annually. The balance sheet remains clean, with strong operating cash flow of $472 million in fiscal 2025, up significantly from $327 million in fiscal 2024. This cash generation provides ample flexibility for organic investment, acquisitions, and shareholder returns without requiring leverage.

The most intriguing capital allocation decision of the Yeaman era, however, is neither a dividend hike nor a buyback acceleration. It is Dolby.io.

Launched in May 2020, timed, not coincidentally, with the global pandemic's massive acceleration of video communications and remote collaboration, Dolby.io is a self-service developer platform that packages Dolby's core audio and video processing technologies as cloud-based APIs.

Instead of licensing codec technology to a Samsung or an Apple through a traditional enterprise patent agreement, Dolby.io lets any software developer in the world call an API to clean up audio quality in a podcast recording, enhance the video in a telemedicine session, or embed ultra-low-latency video streaming into a sports betting application.

The platform launched with two initial API families: media processing (analyzing and enhancing audio and video files) and interactivity (embedding multi-party audio and video communications into applications). It operates on a per-usage billing model with a free trial tier offering 30,000 interactivity minutes and 200 media processing minutes. The go-to-market motion is indistinguishable from any other developer-focused SaaS platform, closer in spirit to Twilio or Stripe than to a traditional IP licensor.

This represented, and represents, a fundamentally different business from Dolby's core licensing operation. The core licensing model is B2B2C at its purest: Dolby licenses to a device manufacturer, the manufacturer embeds the technology in a product, the consumer buys the product. The manufacturer pays the royalty.

Dolby.io is B2D (business-to-developer): usage-based pricing, direct developer relationships, self-service onboarding, and a product velocity that requires continuous feature iteration rather than multi-year standards-body negotiations. It is, in effect, a startup being incubated inside a blue-chip public company.

To build out this platform's capabilities, Dolby executed two targeted acquisitions. In February 2022, it acquired Millicast, a WebRTC-based real-time streaming platform capable of delivering video to audiences of over 60,000 concurrent viewers with less than 500 milliseconds of latency. Financial terms were not disclosed, though Millicast had reportedly grown revenue by over 300% in 2021, suggesting it was at an early but rapidly scaling stage.

Then, in August 2024, Dolby acquired THEO Technologies, a Belgian company founded in 2012 that developed THEOplayer, a cross-platform video player widely used by major sports and entertainment broadcasters for low-latency live delivery.

These acquisitions were classic technology tuck-ins, designed to give Dolby.io the real-time streaming infrastructure and cross-platform playback capabilities it needed to serve the live sports and entertainment verticals where interactive, low-latency video is highest value.

The near-term financial contribution of Dolby.io remains modest. Revenue from Products and Services, which includes both cinema equipment sales and Dolby.io, reached $26.5 million in Q1 of fiscal 2025, jumping 22% year-over-year but still representing a tiny fraction of total revenue.

The strategic question is whether this is a genuine second growth engine in embryonic form, or a distraction from the core licensing business. The answer probably depends on which way the media industry evolves over the next decade.

There is a third pillar of the capital allocation story that deserves attention, one that receives little coverage but may prove among the most consequential: Via Licensing Alliance and the broader patent pool strategy.

Dolby owns Via LA, an independently managed subsidiary that has become, by acquisition and organic growth, the world's largest patent pool administrator. In May 2023, Via Licensing acquired MPEG LA, in what is believed to be the first-ever merger of two major patent pool administrators, forming Via Licensing Alliance with a combined portfolio of nearly 50,000 patents across over 130 countries, more than 500 patent holders, and nearly 10,000 licensees.

Then, in June 2024, Dolby announced its largest acquisition in years: the purchase of GE Licensing from GE Aerospace for $429 million in cash, bringing in a portfolio of over 5,000 patents including foundational standard-essential patents in HEVC and VVC video compression.

These moves signal something far more ambitious than defensive IP management. Dolby is building infrastructure to become the central clearinghouse for technology licensing across the entire consumer electronics ecosystem, administering not just its own patents but those of hundreds of other innovators.

The fee structure for patent pool administration is modest on a per-transaction basis but scales extraordinarily well: every new licensee added to the pool generates incremental revenue at near-zero marginal cost. It is the difference between owning a single toll bridge and owning the highway authority that collects tolls on behalf of every bridge in the country.

VII. The Bull and Bear Case

To evaluate Dolby Laboratories as a long-term investment, it is useful to apply two complementary analytical frameworks: Hamilton Helmer's 7 Powers, which identifies the sources of durable competitive advantage, and Michael Porter's 5 Forces, which assesses the structural attractiveness of the industry.

Starting with Helmer's 7 Powers, the most obvious source of power is what Helmer calls a "Cornered Resource." Dolby's patent portfolio, now numbering over 12,000 granted patents with thousands more pending, represents a legal thicket so dense that it is functionally impossible to manufacture a standard television, smartphone, set-top box, or streaming device without touching Dolby-owned or Dolby-administered intellectual property.

This is not hyperbole. Dolby's patents are embedded in the mandatory specifications of multiple global standards: DVD, Blu-ray, ATSC digital television, various mobile telecommunications standards, and increasingly, next-generation video compression standards like VVC. The addition of the GE Licensing portfolio, with its foundational HEVC and VVC patents, deepened this position further.

In the Helmer framework, a cornered resource is one that cannot be replicated or worked around by competitors. Dolby's standard-essential patent portfolio meets that definition with an important caveat: patents expire, typically twenty years from filing, which means continuous R&D investment is necessary to refresh the thicket. Dolby has historically spent around 18-20% of revenue on R&D, a level that reflects the seriousness with which it treats patent-portfolio renewal.

The second significant power is Network Effects, and the Atmos ecosystem provides a textbook illustration. Content creators invest in learning to mix in Atmos because cinemas, streaming platforms, and consumer devices support it. Cinemas and device manufacturers invest in Atmos decoding capabilities because content is being created in the format. Streaming platforms adopt Atmos as a premium differentiator because consumers recognize and value the badge.

Each additional node in this network, whether it is a new film mixed in Atmos, a new soundbar that decodes it, a new streaming service that carries it, or a new automotive manufacturer that installs it, increases the value proposition for every other node. This creates a self-reinforcing flywheel that is extremely difficult for a competitor to replicate without simultaneously solving both the content-creation side and the device-adoption side of the coordination problem.

The third power is Branding, and it is difficult to overstate its importance in Dolby's case. The Dolby logo, the interlocking double-D, is one of the most recognized marks in global consumer electronics. It has been conditioned into consumer behavior over more than fifty years of consistent, high-quality association.

When a consumer sees the Dolby badge on a television specification sheet, on a streaming platform next to a movie title, or in a cinema lobby, it communicates "premium" in a way that a raw codec specification number never could. This brand power allows Dolby to charge a royalty premium over technically comparable open alternatives, and crucially, it gives device manufacturers and content platforms a marketing tool that they value independently of the underlying technology.

Samsung pays Dolby a licensing fee not only because the technology is technically excellent, but because Samsung can then advertise "Dolby Atmos" on the box, and that advertisement moves product.

Turning to Porter's 5 Forces, the structural picture is similarly favorable but with important nuances that deserve close examination.

Supplier power is low. Dolby's primary operational inputs are engineering talent and R&D spending. While talent competition in Silicon Valley and other technology hubs is intense, there is no concentrated supplier that could exert pricing power over Dolby's core operations. The raw material is intellect, and it is distributed broadly.

Buyer power is the most complex force in Dolby's competitive landscape. Dolby's licensees include some of the most powerful and well-resourced companies on Earth: Apple, Samsung, LG, Sony, Qualcomm, and the major streaming platforms. In theory, these buyers have enormous bargaining leverage.

In practice, their power is constrained by a crucial asymmetry: they need Dolby more than any individual buyer wants to admit. A Samsung television without Dolby Vision or Atmos support is at a tangible marketing disadvantage against an LG television that has both. A streaming platform without the Dolby badge on its premium tier looks inferior to competitors that carry it.

The interdependence is genuine: the buyers need the badge to sell premium, and Dolby needs the buyers to maintain ubiquity. This mutual dependency keeps buyer power in check, though the occasional hardball licensing negotiation (and the threat of switching to open-source alternatives) ensures that Dolby cannot price its licenses with impunity.

The threat of substitutes is the single most significant long-term risk, and it warrants careful consideration. Open-source and royalty-free alternatives exist across every dimension of Dolby's technology portfolio. AV1 challenges HEVC in video compression. HDR10+ challenges Dolby Vision in high dynamic range. Google's Project Caviar aims to challenge both Dolby Atmos and Dolby Vision with royalty-free open alternatives.

The history of technology standards includes notable examples of proprietary formats being displaced by open alternatives once the open option achieves "good enough" quality, the most famous being the displacement of various proprietary web standards by open HTML/CSS/JavaScript.

Dolby's defense rests on several pillars: the enormous installed base already committed to its formats, the switching costs embedded in production workflows, the brand premium that open alternatives cannot match, and the continuous innovation that aims to keep Dolby formats technically ahead.

These pillars are strong but not invulnerable. The risk is not that Dolby's moat collapses overnight, but that it erodes gradually over a decade as open alternatives improve and the brand premium slowly diminishes.

Barriers to entry remain extremely high. Building a competing spatial audio or HDR format is technically feasible for a well-funded engineering team. Getting that format adopted as an industry standard requires solving a multi-sided coordination problem across content creators, device manufacturers, streaming platforms, and consumers.

It requires building brand recognition over decades. It requires assembling a patent portfolio that can withstand litigation. And it requires doing all of this while Dolby, the incumbent, uses its existing ecosystem advantages to make switching as difficult as possible.

Rivalry among existing competitors is moderate and fragmented. DTS, now part of Adeia (formerly Xperi), competes in cinema and home theater audio but has a smaller ecosystem and weaker brand position.

Samsung backs HDR10+ primarily as a negotiating lever against Dolby's Vision licensing fees rather than as a fully committed alternative ecosystem play. The Alliance for Open Media is a consortium rather than a single focused competitor, which introduces coordination challenges of its own.

For investors monitoring Dolby's ongoing performance, two key performance indicators stand out as the most important to track.

The first is licensing revenue growth rate. At approximately 92-93% of total revenue, licensing is the core economic engine. This metric captures the expanding or contracting surface area of devices and platforms paying Dolby royalties and directly reflects the adoption trajectory of Atmos and Vision across device categories.

The second is Dolby Atmos and Dolby Vision adoption rates, which the company discusses on earnings calls and in investor presentations. These adoption metrics, often expressed as penetration rates within specific device categories such as smartphones, televisions, soundbars, automobiles, and streaming catalogs, are the leading indicators that drive the licensing revenue line.

If Atmos is expanding into new categories like automotive infotainment, gaming headsets, and AR/VR headsets, and if Vision is migrating from flagship televisions down to mid-tier sets, then the licensing line will follow. If adoption plateaus or open-source alternatives begin winning standards mandates in new device categories, that signal will appear in penetration data before it manifests in the revenue numbers.

One regulatory and accounting consideration worth flagging: Dolby's GAAP revenue can appear lumpy on a quarterly basis because of the nature of patent licensing agreements. Large licensees sometimes settle back-royalties in lump-sum payments, creating spikes in a given quarter that do not reflect the underlying business trajectory.

The company's non-GAAP adjustments, which normalize for these timing effects, provide a cleaner view of the business's steady-state economics. Investors accustomed to the predictable SaaS revenue curves of subscription software companies should be aware that licensing businesses operate on a different temporal cadence.

VIII. Playbook and Lessons

The first and most powerful lesson from Dolby's history is deceptively simple: standardize, do not productize. Ray Dolby's original insight, that more value could be captured by licensing a technology broadly than by manufacturing and selling boxes directly, has been validated across six decades and five technology generations, from analog tape noise reduction to digital cinema codecs to object-based spatial audio to HDR video to streaming APIs.

The highest-margin business in any industry is not the business of selling the product. It is the business of owning the specification that every product must conform to. Dolby does not make televisions, it does not make phones, and it does not make streaming platforms. It writes the technical standard that all three must speak, and it collects a royalty on every conversation.

This is why the company operates at approximately 90% non-GAAP gross margins on its licensing business, a profitability level that would be the envy of the best-run SaaS company in Silicon Valley, achieved without the churn risk, the customer acquisition costs, or the constant feature-development treadmill that SaaS businesses face.

The lesson has been echoed by a small handful of other companies that cracked the same code. ARM Holdings licenses chip architectures to every major smartphone processor designer rather than manufacturing chips itself. Qualcomm licenses wireless communication patents, in addition to designing and selling its own processors. Gore-Tex licenses its waterproof membrane technology to dozens of outerwear brands rather than making jackets.

In each case, the licensor's margin profile dramatically exceeds that of the product companies that embed its technology. But Dolby was arguably first, its execution has been the most consistent, and its track record of navigating technology transitions without losing its licensing position is unmatched.

The second lesson is the power of the "ingredient brand" strategy, and it is one of the most underappreciated competitive phenomena in business. How do you make consumers demand a component they cannot see, cannot touch, and often cannot consciously identify?

Most technology components are invisible. The average consumer has no idea which audio codec their television uses, which wireless modem their phone contains, or which chemical process made their jacket waterproof. Yet some component makers have managed to create direct consumer pull for their invisible products. Dolby's method was the most sophisticated of all: the logo, the sound, and the ritual.

The Dolby trailer played before a movie in a Dolby Cinema is not merely a branding exercise. It is a sensory demonstration, a proof of concept delivered at exactly the moment when the audience is most receptive. The lights are down. Phones are put away. Attention is focused. And then sound moves around and above you in a way that ordinary speakers cannot achieve, while the screen displays brightness and color that ordinary projectors cannot match.

For thirty seconds, the audience experiences what Dolby technology does, not through words or specifications, but through their eyes and ears. This is marketing at its most sophisticated: you are not being told that Dolby is better. You are being shown it, in a context designed for maximum sensory impact.

The result is that when a consumer later encounters two televisions on a showroom floor, one with the Dolby Vision badge and one without, the badge carries genuine emotional resonance even if the consumer could not explain the technical difference. Intel achieved this with a sticker and a five-note jingle. Gore-Tex achieved it with a hangtag. Dolby achieved it with an experience.

The third lesson is the imperative of defensive innovation. Dolby's expansion from audio into video with Dolby Vision was not motivated by a desire to conquer new territory for its own sake. It was motivated by the clear-eyed recognition that audio, Dolby's historic stronghold, was becoming commoditized.

The proliferation of competent, open-source audio codecs, the declining marginal value of hardware-based audio processing as processing power became abundant, and the growing willingness of device manufacturers to accept "good enough" audio solutions rather than pay premium royalties, all pointed to a future where the audio licensing premium was under long-term structural pressure.

Rather than defend a shrinking perimeter with ever-more-aggressive patent enforcement, Dolby expanded the perimeter entirely. By pushing into HDR video, the company created an entirely new licensing category that did not exist before 2014, one where it had first-mover advantage, no legacy competitors, and where the proprietary-versus-open battle was still in its earliest stages.

This is the lesson of defensive innovation in its purest form: when your existing moat begins to erode, do not dig deeper in the same spot. Build a new moat in adjacent territory while you still have the resources, brand equity, and industry relationships to do so.

The same logic applies to Dolby.io. If streaming and cloud-native media distribution eventually commoditize the traditional device-level licensing model, then having a platform-native, API-based delivery mechanism for Dolby's core technologies ensures the company has a second front from which to compete.

It may take years, possibly a decade, for Dolby.io to become a material revenue contributor. But the strategic insurance it provides against a world where device-level licensing faces structural decline is valuable regardless of its near-term contribution to the income statement. The best time to build a lifeboat is while the ship is still floating.

IX. Conclusion

From a small London laboratory dedicated to silencing the hiss on magnetic tape, to a company whose technology is embedded in the specification sheets of virtually every screen and speaker on Earth, Dolby Laboratories has executed one of the longest- running and most disciplined business model plays in technology history. Ray Dolby's foundational insight, that owning the standard is more valuable than owning the product, has proven durable across the transition from analog to digital, from physical media to streaming, from cinema to mobile, and from audio to visual.

The company sits at an interesting juncture. Its core licensing business is healthy, generating $1.35 billion in fiscal 2025 revenue at approximately 90% gross margins, powered by the continued global adoption of Dolby Atmos and Dolby Vision across an ever-expanding surface area of devices and platforms.

Fiscal 2026 guidance points to total revenue of $1.39 billion to $1.44 billion, suggesting continued, if moderate, growth. The Dolby family, through their Class B shares, retains significant voting control, preserving the long-term orientation that has defined the company since its founding. Kevin Yeaman, now in his seventeenth year as CEO, has proven himself a steady and strategic architect of the company's post-physical-media reinvention.

The open questions are real and consequential. Can Atmos and Vision maintain their premium positioning as open-source alternatives mature and major technology companies invest billions in building royalty-free ecosystems? Will Dolby.io evolve from an early-stage experiment into a genuine second growth engine, or will it remain a rounding error on the income statement?

Can the Via LA patent pool administration business and the GE Licensing acquisition create a structurally advantaged new revenue stream from the broader intellectual property ecosystem? And as media consumption continues its evolution toward spatial computing, augmented reality headsets, and AI-generated content, will Dolby's technologies be embedded in the next generation of standards, or will new players write those rules?

The company's track record suggests a pattern: in every previous technology transition, from analog to digital, from channels to objects, from cinema to mobile, Dolby found a way to make itself essential to the new paradigm before the old one had fully died. Whether it was getting AC-3 into the DVD specification, Atmos into the iPhone, or Vision onto the Netflix premium badge, the company has demonstrated a repeatable institutional capability, identifying the emerging standard and embedding itself within it.

That capability, more than any individual patent or any single product, is the real asset. The question for investors is whether the pattern holds for the next transition, whatever that turns out to be.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube