Walt Disney: The House of Infinite Worlds

The most valuable entertainment company in history was saved, twice, by the same man. And then he handed the keys to a theme park guy.

That one line captures Disney’s central paradox in 2026 better than any spreadsheet ever could. This is the company that defined American childhood, that gave the world Mickey Mouse, Star Wars, and the Marvel Cinematic Universe. And yet, most of its operating profit now comes from something much more tangible: turnstiles, hotel keys, and cruise ship cabins. The parks, resorts, cruises, and consumer products business generates roughly sixty percent of operating profit. The movies, the shows, the cultural moments that keep the brand alive generate the rest.

So what is Disney, really? A content company that happens to own theme parks? Or a theme park company that happens to make content?

The numbers just sharpen the question. In fiscal 2025, Disney reported $94.4 billion in revenue and $17.6 billion in total segment operating income, up twelve percent from the year before. Experiences — parks, cruises, and consumer products — delivered a record $10 billion in operating profit. Streaming, once a money pit, swung to $1.3 billion in profit across Disney+ and Hulu. ESPN, even as the cable bundle keeps shrinking, produced $2.9 billion in operating income, up twenty percent year over year. Disney’s stock trades around $105, putting the company’s market cap near $190 billion. It operates twelve theme parks across six continents, sails seven cruise ships with more coming, and controls some of the most valuable story engines on Earth: Disney Animation, Pixar, Marvel, and Star Wars.

And on February 3, 2026 — just two weeks ago — Disney’s board made its biggest signal yet about what it thinks the company actually is. It named Josh D’Amaro, a 28-year Disney veteran who rose through the parks business, as Disney’s ninth CEO, effective March 18.

At the same time, Dana Walden — the executive overseeing entertainment and streaming — became President and Chief Creative Officer, a brand-new title in Disney’s 102-year history. Bob Iger, the dealmaker who assembled the modern Disney and then returned to rescue it, will stay on as a senior advisor through the end of the year.

This is the story of how a hand-drawn mouse became a hundred-billion-dollar empire, why the man who built the greatest IP portfolio in history had to come back to fix the mess he left behind, and what it means that the keys to the kingdom now belong to the person who runs the physical kingdom itself.

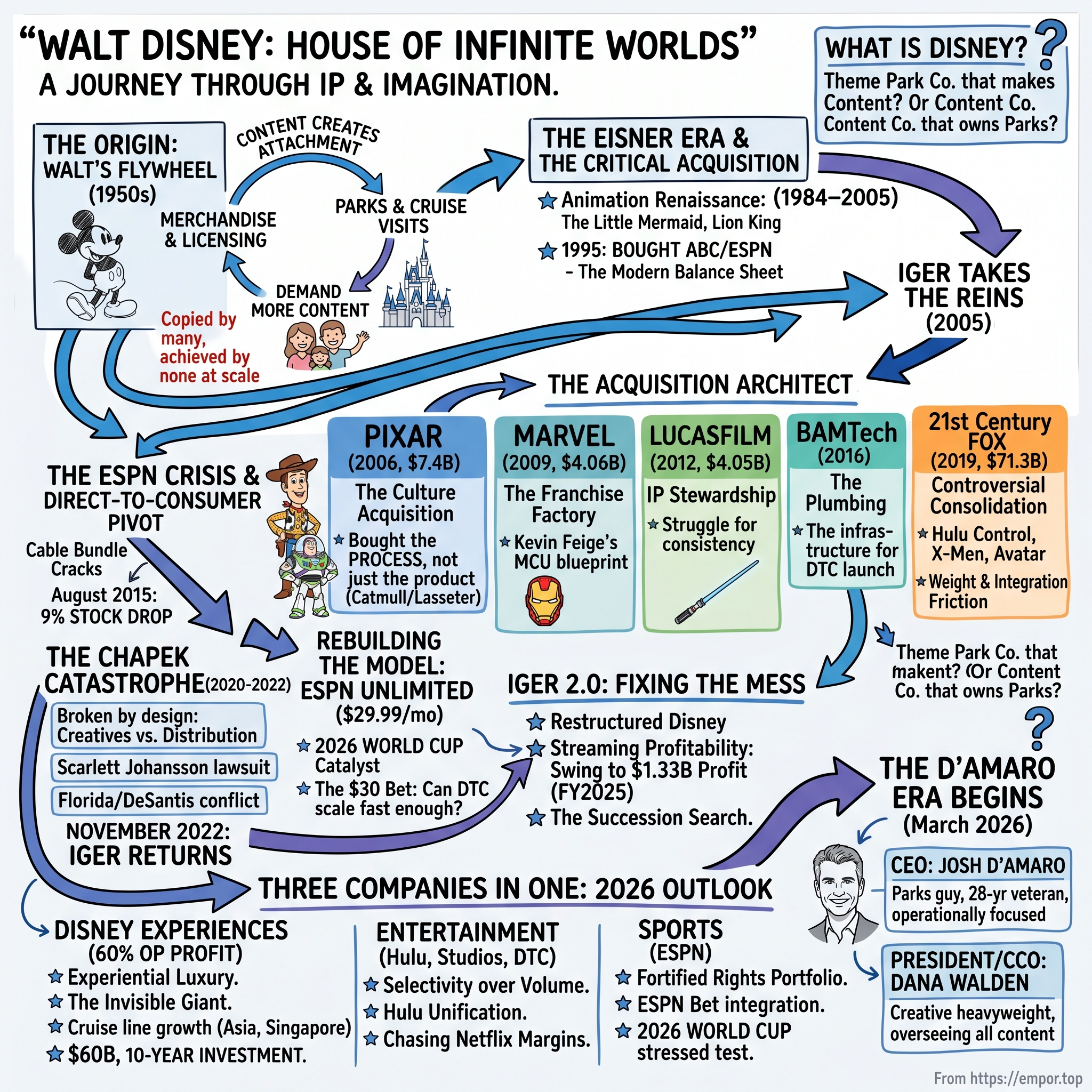

Walt's Invention: The Flywheel Nobody Else Has Built

In 1955, a cartoonist from Missouri opened a theme park in an orange grove in Anaheim, and a lot of smart people concluded he’d finally gone off the rails.

Walt Disney had already spent three decades building one of the most loved brands in America. Snow White, Bambi, Dumbo, Cinderella — these weren’t just hit movies. They were turning into shared cultural memory. Walt had the kind of success most founders spend their whole lives chasing.

And then he decided to pour a fortune into something that barely existed as a respectable category: a clean, meticulously designed place where families could step inside the worlds he’d drawn on screen.

The bankers hated it. Roy Disney, the brother who kept the company solvent, thought it was reckless. Hollywood’s prevailing wisdom was that the movie business was the movie business, and amusement parks were low-rent carnival operations with thin margins and questionable safety — more Coney Island than Hollywood glamour. That was the mental model everyone carried into the conversation.

Walt wasn’t building Coney Island. He was building something that didn’t have a template.

What Walt understood — decades before it became obvious to everyone else — was that the characters weren’t the product. The product was the emotional bond families formed with those characters. And if you could extend that bond beyond the screen, you could extend the business.

A child watches a movie and falls in love with Mickey or Cinderella. That love turns into toys, pajamas, lunchboxes, and books. Those products turn into a family trip. The trip deepens the attachment, which makes the next movie feel like an event, not just entertainment. Around and around it goes.

Content drives merchandise. Merchandise drives park visits. Park visits drive demand for more content.

That’s the flywheel — and Walt sketched it out in the 1950s. It’s been Disney’s blueprint ever since. Plenty of companies have tried to copy it. None of them have managed to build it end-to-end at Disney’s scale, because copying the mechanism is easy. Copying the generational trust is not.

Disneyland opened on July 17, 1955, and the first day was a mess. Asphalt still tacky. Drinking fountains that didn’t work. A gas leak that forced Fantasyland to close temporarily. And crowds so out of control — thanks in part to counterfeit tickets — that it overwhelmed the park. The press dubbed it “Black Sunday.”

But here’s the thing about flywheels: if the core idea is right, the early wobble doesn’t matter.

Within a year, Disneyland drew more than three and a half million visitors. In less than a decade, it was one of the most famous tourist destinations in the world. And then came Walt Disney World in 1971, built on 25,000 acres of Florida swampland — a footprint so huge it’s roughly the size of San Francisco.

Walt had proved the concept. Not just that a movie studio could operate a park, but that stories could become places — and that places could become the engine that kept the stories valuable.

Then, in December 1966, Walt died of lung cancer. He was sixty-five. And what followed is the part of the Disney story that every generation of executives studies like a warning label.

Without its creative center of gravity, the company drifted. The animation studio that had invented the modern animated feature started turning out films that audiences accepted rather than adored — The Aristocats, Robin Hood, The Black Cauldron. The parks kept printing money, but largely by running on the founder’s momentum rather than fresh invention. Walt Disney World, which opened in 1971 and fulfilled the last great vision of Walt’s life, became so successful it masked how stagnant the rest of the company had become. By the early 1980s, corporate raiders were circling. Disney wasn’t just vulnerable. It was a legitimate takeover target — a world-class brand being run like a regional business.

The turnaround arrived in 1984 with Michael Eisner, and it was both spectacular and, eventually, self-destructive. Eisner — a former Paramount executive with a showman’s instincts and an operator’s ego — lit a creative fire under the company. In his first decade, Disney roared back with The Little Mermaid, Beauty and the Beast, Aladdin, and The Lion King. Those films didn’t just win the box office; they re-powered the flywheel, driving merchandise and park attendance in a way only great stories can.

Eisner expanded the parks, built hotels, pushed Disney retail into malls with the Disney Store chain, and then made a move that would define Disney’s modern balance sheet: in 1995, he bought ABC and ESPN for $19 billion.

But Eisner’s second act became a case study in what happens when a leader’s instincts curdle into overreach. He clashed with Pixar’s Steve Jobs over sequel rights, profit-sharing, and creative credit until Pixar announced it wouldn’t renew its distribution deal. He drove out Jeffrey Katzenberg — a key architect of the animation renaissance — and the split ended with a $280 million settlement.

And he fumbled succession so badly it became corporate folklore. He hired Michael Ovitz as president, then pushed him out after just fourteen months with a $140 million severance package that turned into a governance scandal. By 2004, Disney’s stock was stagnant. Roy Disney Jr. and Stanley Gold resigned from the board in public protest. Activist pressure mounted. And the company’s most important creative partner was heading for the exits.

That 2004–2005 crisis is the true origin story of modern Disney. The board needed a leader who could repair Pixar, restore creative credibility, and restart growth without detonating the infrastructure Eisner had built.

They chose Bob Iger — the head of ABC, Eisner’s disciplined and politically skilled number two. Where Eisner turned relationships into battles, Iger treated them like the business. Where Eisner could be theatrical and combative, Iger was calm and strategic.

It was, by any measure, one of the most consequential CEO choices in modern entertainment history.

The Acquisition Architect: Five Deals That Remade an Industry

Bob Iger took over as CEO in October 2005 with a strategy so simple it almost sounded naïve: buy the best creative companies in the world, keep their leaders doing what they do best, and plug their output into Disney’s flywheel.

The plan demanded a rare combination. He needed the judgment to pick the right targets, the personal credibility to persuade founders to sell, and the restraint to not “Disney-fy” the very thing he was buying. That last part — leaving a creative institution intact after you own it — turned out to be the hardest and most valuable skill of all.

Over the next thirteen years, Iger executed four blockbuster acquisitions and one unglamorous infrastructure deal. Together, they rebuilt Disney from a legacy studio with a world-class brand and creeping stagnation into the defining entertainment powerhouse of the modern era.

Pixar: The Culture Acquisition

The first call Iger made as CEO was to Steve Jobs.

Pixar’s distribution deal with Disney was about to expire, and Jobs — burned by Eisner’s combative style — had little interest in keeping the relationship alive. Iger didn’t try to patch it with nicer terms. He did something bolder: he flew to Emeryville and asked Jobs to sell.

The deal closed in May 2006 for $7.4 billion in Disney stock. At roughly sixteen and a half times forward EBITDA, plenty of analysts said Disney had overpaid for a studio with a relatively small film count, even if every one of those films felt like a classic. The skepticism had a point: in Hollywood, “hot streak” is usually the prelude to “inevitable decline.”

But Iger wasn’t buying a streak. He was buying a system.

The real assets were John Lasseter and Ed Catmull — the leaders who had built the most consistently excellent animation operation in the business. Catmull understood the mechanics of creative production and the technology behind it better than almost anyone alive. Lasseter had the storytelling instincts, taste, and collaborative leadership that Disney Animation had been missing for years.

Iger put them in charge of Walt Disney Animation Studios — a move that signaled, immediately, that this wasn’t just about importing Pixar movies. It was about rehabilitating Disney’s own creative engine. The turnaround took time; you don’t rebuild an animation pipeline overnight, and you definitely don’t repair a demoralized culture with a memo. But when it hit, it hit: Tangled, Wreck-It Ralph, Frozen, Big Hero 6, Zootopia, Moana, Inside Out.

Frozen alone did $1.3 billion at the global box office and triggered a consumer-products phenomenon. In its first eighteen months, Frozen merchandise revenue exceeded Pixar’s entire purchase price.

That was the lesson that shaped everything Iger did next: the most valuable thing you can buy isn’t a catalog. It’s the people and the process that can create the next decade of hits. Buy the process, not just the product.

Marvel: The Franchise Factory

In August 2009, Disney announced it would buy Marvel Entertainment for $4.06 billion.

The timing felt almost absurd. The world was still shaking from the financial crisis. Credit markets had only recently thawed. And Iger was about to spend four billion dollars on a comic book company.

Marvel had one recent proof point: Iron Man, released in 2008, had grossed $585 million worldwide and showed that a so-called “second-tier” character could be a blockbuster if the movie was good. But the bigger bet — the one that would either change Hollywood or flame out spectacularly — was Kevin Feige’s plan for the Marvel Cinematic Universe.

At the time, that interconnected-universe concept was still a theory. No one had successfully pulled off dozens of movies that interlocked, built toward shared events, and trained audiences to treat each new release like another episode in an ongoing saga. Hollywood’s default view was that it was too complicated, too risky, and too dependent on every single movie being solid.

Disney bought anyway. At roughly nine and a half times estimated 2010 EBITDA, it was a relatively cheap price — though it only looks “cheap” in hindsight because the upside turned out to be historic. Disney brought distribution muscle and the flywheel: parks, merchandise, TV, and eventually streaming. Feige brought the blueprint.

What came next permanently rewired the economics of blockbuster filmmaking. Over the next fifteen years, the MCU grossed more than $33 billion worldwide across thirty-three films. Avengers: Endgame alone brought in $2.8 billion, turning a three-hour superhero movie into one of the most lucrative corporate assets ever created.

And it didn’t stop at theaters. Marvel became attractions, merch, and streaming series. It became a narrative ecosystem engineered to make the next release feel unskippable. Miss Ant-Man, and you might miss a setup for Endgame. Studios everywhere chased the model — Universal’s “Dark Universe,” Warner Bros.’ DC efforts — but none matched Marvel’s consistency or cultural dominance.

Marvel didn’t just give Disney more IP. It gave Disney a factory for turning IP into an engine.

Lucasfilm and Star Wars: IP Without Guarantees

In October 2012, Disney acquired Lucasfilm — and with it Star Wars and Indiana Jones — for $4.05 billion. It was negotiated largely between Iger and George Lucas, over private meetings that stretched across more than a year.

Lucas chose Disney. He wanted stewardship, not just a payout. He had watched Iger handle Pixar and Marvel: preserve the culture, fund the ambition, scale the distribution. The price landed almost exactly where Marvel had — a sign of how the market valued legendary IP at the time, even when its ceiling was hard to model.

The early returns looked like the dream scenario. The Force Awakens arrived in December 2015 and grossed $2.07 billion globally, validating the acquisition in a single release.

Then came the harder part: what do you do after the comeback?

The sequel trilogy struggled with creative inconsistency. The Last Jedi took big swings that split the fanbase. The Rise of Skywalker course-corrected so aggressively that it satisfied almost no one. Galaxy’s Edge — the billion-dollar Star Wars lands built on both coasts — underperformed initial attendance expectations. Merchandise momentum softened.

Star Wars became the cautionary tale inside Disney’s own success story: buying beloved IP isn’t the same as having a coherent creative process to extend it. Marvel had Feige and a disciplined long-term plan. For years, Star Wars didn’t have an equivalent architect. The franchise that taught the world the power of storytelling ended up reminding Disney of the simplest rule in entertainment: you still have to tell good stories.

BAMTech: The Infrastructure Play

Of all Iger’s deals, the one most people forget may have been the one that made Disney’s biggest strategic pivot possible.

In 2016, Disney bought a majority stake in BAMTech, a streaming technology company spun out of Major League Baseball’s digital media operation. It wasn’t glamorous. It was plumbing. But plumbing is what turns a strategy into a product that works at scale.

BAMTech became the technical backbone that let Disney launch its own direct-to-consumer service on the timeline it did. And in August 2017, Iger made the announcement that redrew the entire media map: Disney would pull its content from Netflix and build its own streaming platform.

Reed Hastings later said this was the moment he understood the full scope of the threat. In a way, the entire streaming era for legacy media — Max, Peacock, the arms race, the bundle reshuffles — exists in the wake of that decision.

21st Century Fox: The Controversial Consolidation

Then came the biggest deal, and the one that still sparks the most debate.

In March 2019, Disney closed its acquisition of most of 21st Century Fox’s entertainment assets for $71.3 billion. Comcast fought hard as a competing bidder. Rupert Murdoch ultimately preferred Disney.

What Disney got was enormous: full control of Hulu, giving Disney a general-entertainment streaming platform to pair with Disney+; the return of the X-Men and Fantastic Four to Marvel, ending a licensing patchwork that had kept major characters in other studios’ hands; the Avatar franchise and its sequels; FX Networks; National Geographic; Star India and its Hotstar platform; and international content libraries to bulk up streaming catalogs around the world.

What Disney also got was weight.

Fox added studios, networks, international operations, and regional sports assets to an organization that was already sprawling. Integration absorbed years of management attention. Cultural friction was real. Complexity became structural — not just a temporary post-merger problem.

And then there was the price. At roughly twenty to twenty-two times EBITDA, Disney paid far more than it had for Marvel or Lucasfilm, and above the multiples that major media deals often traded at. Star India, one of the crown jewels on paper, went on to generate more than $600 million in annual losses before Disney sold its majority stake to Reliance Industries in late 2024.

The honest verdict is messy, because the deal was both strategically understandable and operationally punishing. Hulu and streaming depth mattered. But Disney almost certainly overpaid, and the complexity the Fox acquisition injected into the company helped set the stage for the leadership turmoil that followed.

In Iger’s legacy, it’s the one deal where you can believe the strategic logic and still question the execution.

The ESPN Crisis: When Disney's Greatest Asset Became Its Biggest Problem

On August 4, 2015, Disney’s stock did something that, for the modern company, felt almost unthinkable. It dropped nine percent in a single day.

There wasn’t a scandal. There wasn’t a box-office bomb. There wasn’t an accounting surprise.

It was one line on an earnings call. Bob Iger acknowledged — plainly, publicly — that ESPN was losing cable subscribers.

That sentence didn’t just move Disney’s shares. It rewired how Wall Street thought about the entire cable television industry.

To understand why, you have to remember what ESPN was at its peak: the most profitable channel ever created, sitting inside the most profitable distribution bundle ever invented.

In the mid-2010s, ESPN reached more than a hundred million U.S. households through cable. And every one of those households paid about nine dollars a month for ESPN as part of the bundle, whether they watched sports or not.

That’s the magic trick cable perfected: you weren’t just paying for what you loved. You were paying for what everyone else loved, too. A household that never watched SportsCenter still sent ESPN real money every month, simply because ESPN was in the package. Multiply that by a hundred million homes, and you start to see why ESPN became the crown jewel of American media — a business so good it bordered on absurd.

At its height, that system generated roughly $14 billion a year in affiliate revenue. And it worked because ESPN was the bundle’s keystone. Distributors needed ESPN because sports fans wouldn’t tolerate a package without it. And because distributors needed it, ESPN could charge an affiliate fee that was multiples of any other cable channel.

Then the bundle began to crack.

Cord-cutting wasn’t complicated. Why pay $150 a month for hundreds of channels when you only watch a handful? Netflix, Hulu, and Prime Video offered the scripted shows people actually wanted for a fraction of the price. And as entertainment migrated to streaming, the cable bundle’s last line of defense became the one kind of content that still demanded live viewing: sports.

Which meant ESPN wasn’t just another channel. It was what kept the whole thing standing.

But the decline kept coming. The industry went from more than a hundred million cable households at its peak to roughly sixty to sixty-five million by 2025, and the number continued falling at a mid-to-high single-digit pace each year. ESPN could raise rates for a while and soften the blow, but the direction of travel was unmistakable: fewer households, less guaranteed money, and a decade-long shift from “inevitable growth” to “managed decline.”

ESPN’s argument back was simple, and it was true: nobody cuts the cord during football season. Live sports is the most DVR-proof, piracy-resistant, appointment-viewing content on Earth. And while most ad categories in traditional TV have been shrinking, sports has held up. Sports rights are what keep cable alive at all.

So Disney did the thing that would have sounded insane back when ESPN was printing money: it decided to rebuild the model around the consumer.

On August 21, 2025, ESPN Unlimited launched for $29.99 a month, timed for the start of college football season and the U.S. Open. For the first time in ESPN’s forty-five-year history, viewers could get the full ESPN suite — ESPN, ESPN2, ESPNU, SEC Network, ACC Network, and ESPN on ABC — without a cable subscription.

The pitch was “everything, in one place.” ESPN Unlimited included tens of thousands of live events per year across pro and college sports, WWE premium live events including WrestleMania, NFL Network and RedZone acquired directly from the NFL, plus ESPN’s studio programming and originals. Disney also offered an introductory bundle with Disney+ and Hulu with ads at $29.99 for the first year — the same price as ESPN on its own — effectively throwing in the rest of Disney’s entertainment streaming to get sports fans in the door. A partnership bundle with Fox One at $39.99 widened the sports menu even further.

Just as important: this wasn’t simply “cable on a phone.” The product leaned into what streaming can do that cable never could — personalized feeds, multiview, real-time stats overlays, fantasy integration, and betting data through ESPN Bet. Disney wasn’t selling channels. It was trying to sell the operating system for being a sports fan.

And that’s where the real risk lives.

For decades, ESPN was subsidized by tens of millions of people who barely watched sports. Direct-to-consumer flips the economics: only sports fans pay. If something like twenty to thirty million committed fans subscribe at $29.99 a month, the math can work — that’s the difference between a managed transition and a revenue haircut. But the conversion rate is the entire ballgame, and it’s not proven. The shift has to happen faster than the cable cliff keeps dropping.

The good news is Disney gets a once-in-a-decade tailwind at exactly the right time. The 2026 FIFA World Cup — hosted in the U.S., Canada, and Mexico — will air exclusively on ESPN. It’s the biggest built-in marketing moment sports television will get this decade, and Disney didn’t have to invent it.

Financially, ESPN was still showing why it mattered. Disney’s Sports segment delivered $2.88 billion in operating income in fiscal 2025, up twenty percent year over year. And in Q1 of fiscal 2026, sports advertising revenue grew ten percent — even as segment operating income took a temporary hit from the YouTube TV carriage dispute, which cost roughly $110 million in the quarter.

ESPN was still strong. But the rules it was built on had changed.

And Disney had no choice but to change with them.

The Chapek Catastrophe: A Corporate Governance Story for the Ages

Bob Chapek’s brief, chaotic tenure as Disney CEO is ultimately a story about mismatch: what happens when a company whose core product is creativity is run by a leader who never earned creative legitimacy. It has become a cautionary tale in boardrooms for good reason. And you can’t make sense of Disney’s 2026 leadership structure — a parks CEO paired with a newly empowered creative chief — without understanding how Chapek’s era unraveled.

Chapek wasn’t a random pick. He’d run Parks, Disney’s biggest profit engine, with operational discipline and strong financial results. He came out of consumer products, spoke fluent pricing and distribution, and knew how to manage a sprawling organization. When Iger chose him in February 2020, the logic was defensible: Disney had just digested an acquisition spree, and it needed an operator to keep the machine running. Iger would remain Executive Chairman, continuing to oversee the creative side, while Chapek handled the business.

In practice, it was broken by design. A company can’t run on two centers of gravity. Iger’s continued presence — and continued influence — made it hard for creative leaders to believe Chapek was truly in charge. And Chapek, feeling his authority slipping, didn’t try to win hearts. He tried to win control. Not through trust, but through org charts.

Then the pandemic hit, and the timing couldn’t have been worse. Chapek became CEO just as COVID-19 shut down the global economy. Disney’s theme parks closed worldwide for the first time in company history. Movie theaters went dark. Cruise ships sat idle. Disney furloughed more than a hundred thousand employees. In a single quarter, the company lost billions. It was an existential moment, and to Chapek’s credit, the operational response — preserving cash, managing closures, planning reopenings and safety protocols — was steady.

But at the exact same time, Disney+ caught a historic tailwind. Locked-down families signed up in droves. The service hit a hundred million subscribers in its first sixteen months — a milestone Netflix took roughly a decade to reach. That speed created a dangerous illusion inside Disney: that subscriber growth was the objective, and that profitability could be postponed. Wall Street rewarded the growth story, and Chapek absorbed the lesson.

His defining move came in late 2020, when he reorganized Disney to separate content creation from content distribution. On paper, it had neat MBA logic: creative teams would make films and series, while a centralized distribution group — led by Kareem Daniel, a Chapek ally with a finance background — would decide where content lived. Theatrical? Disney+? Both? The distribution team would make the call, guided by data and optimization. Creative executives would no longer control the fate of what they created.

The blowback was immediate, and it was intense. Filmmakers who had built projects for theatrical runs suddenly learned their work could be redirected to Disney+ with limited input. The change treated movies and shows like interchangeable inventory — units to be placed wherever they best served short-term metrics. Disney’s culture is built on the opposite belief: that storytelling is the point, and the people closest to the story should have the loudest voice in how it reaches audiences.

From there, the consequences piled up fast.

In July 2021, Scarlett Johansson sued Disney over Black Widow’s simultaneous theatrical and Disney+ release, arguing the strategy undercut her box-office-based compensation. The case was eventually settled, but the public fight mattered more than the legal resolution. Johansson wasn’t just any star; she was a pillar of the MCU. Her lawsuit broadcast a message to the entire creative community: this Disney was willing to prioritize streaming goals over long-standing industry norms and contractual expectations.

Then came Florida. In early 2022, as Florida passed the Parental Rights in Education bill — widely called the “Don’t Say Gay” bill — Chapek initially stayed quiet. Employees revolted, staging walkouts. Chapek reversed course and publicly opposed the legislation. Governor Ron DeSantis responded by stripping Disney of the Reedy Creek Improvement District, the special governing structure that had given Walt Disney World extraordinary autonomy for decades. Chapek managed to alienate both sides at once: too slow for employees who wanted leadership, too visible for politicians who wanted compliance.

Meanwhile, the numbers were turning ugly. Disney’s stock fell from above $190 at the end of 2021 to around $85 by late 2022. Streaming losses ballooned — the direct-to-consumer business lost roughly $4 billion in fiscal 2022 — and investors didn’t hear a convincing plan for when the bleeding would stop. By the fall of 2022, the board had reached its conclusion.

On November 20, 2022, Disney fired Bob Chapek — just five months after extending his contract — and brought Bob Iger back as CEO. The board orchestrated the move privately and executed it in a single weekend. A sitting CEO replaced by his predecessor in one clean coup is almost unheard of in modern media.

And the irony was unavoidable. The man returning to restore order was the same man who had chosen Chapek, endorsed him, and called succession planning “one of a CEO’s most important responsibilities.” Iger came back to fix a crisis he had, at least in part, created.

The Return: Fixing What Was Broken

Iger came back with three stated priorities: restore the primacy of creative content, fix streaming economics, and sort out succession — for real this time.

He moved fast, and he didn’t pretend there wouldn’t be pain. Within his first six months, Iger announced a $5.5 billion restructuring that included more than seven thousand layoffs and about $2.4 billion in content write-downs. Just as important, he ripped out the organ that had caused so much internal revolt: Chapek’s centralized distribution group. The team that had been deciding, from the middle of the company, where everyone else’s movies and shows should go was dismantled. Creative leaders got their authority back.

The philosophy changed overnight. The era of “more content everywhere” ended. The new doctrine was “better content selectively.” Make fewer projects. Spend more care on each one. A single great film is worth more than ten forgettable streaming series — not just culturally, but financially, because great stories power the whole flywheel.

Personnel made the point even louder. Kareem Daniel was fired immediately. Other Chapek-era executives followed. The message to Hollywood, and to Disney’s own creative ranks, was hard to miss: the people who understand storytelling were back in the driver’s seat.

Then came the part investors cared about most: the streaming business stopped bleeding.

Disney’s Entertainment DTC segment swung from losing roughly $2.5 billion in fiscal 2023 to generating $1.33 billion in operating income in fiscal 2025 — a $3.8 billion reversal in just two years. In the same period, other legacy-media streamers like Max, Peacock, and Paramount+ were still grinding toward break-even. Disney got there by doing the unglamorous work that the pandemic boom let everyone postpone: raising prices, leaning into ads, cutting back on volume, and managing costs like a mature business instead of a land-grab.

Disney+ moved from its $6.99 launch price to $13.99 a month for the ad-free tier. That kind of doubling would have looked suicidal back when the only headline was subscriber growth. In a profitability era, it was the whole point. Disney built out lower-priced ad tiers, bringing in a second revenue stream that doesn’t require charging every household a premium. Password-sharing crackdowns were announced. Subscriber growth slowed, but revenue per user climbed. By Q1 of fiscal 2026, streaming operating income reached $450 million on an 8.4 percent margin, and management guided to about a ten percent SVOD operating margin for the full fiscal year.

The turnaround wasn’t happening in a vacuum. Activists were hovering, and they were loud. Nelson Peltz’s Trian Fund Management built a meaningful stake and pushed for board representation, arguing Disney’s margins lagged, content spend was too high, and succession planning was still unresolved. Blackwells Capital, led by Jason Aintabi, launched its own more aggressive proxy campaign focused on governance.

In April 2024, Iger won a decisive shareholder vote, beating both activist slates. But even as a win, the fight did what proxy wars often do: it forced discipline. Content budgets got tighter scrutiny. Streaming profitability timelines became less negotiable. And Disney’s $7 billion buyback program for fiscal 2026 was, at least in part, a response to investor pressure for more direct capital returns. Sometimes activists lose the vote and still change the company.

Iger also made a move that signaled a very different kind of discipline than the empire-building of the Fox era: he pulled back from India. In November 2024, Disney completed the formation of a joint venture with Reliance Industries, handing over majority control of Star India — a business generating more than $600 million in annual losses — to a local operator with real structural advantages in that market. Disney kept a thirty-seven percent stake, but shed the operational drain. It was a strategic retreat Iger hadn’t been willing to make the first time around.

And while he was cutting and consolidating in some places, he was also planting flags in others.

In February 2024, Disney made a $1.5 billion equity investment in Epic Games, the creator of Fortnite, to build a “Disney universe” inside the game. It’s a big idea: a virtual Disney experience for Fortnite’s hundred-million-plus monthly active users, populated with Disney, Pixar, Marvel, and Star Wars worlds and characters. No plane ticket. No hotel. No waiting for a ride reservation. Just Disney, distributed through a digital world where younger audiences already spend hours a day. Whether it becomes a meaningful financial engine was still an open question — but the strategic insight was clear. This is a new kind of park, one Disney can scale without pouring concrete.

The second Iger era also brought capital returns back into the story. Disney repurchased $3.5 billion of stock in fiscal 2025 and guided to $7 billion in buybacks in fiscal 2026 — the second-largest annual buyback program in the company’s history. With projected cash from operations of $19 billion and capex guidance of $9 billion, Disney once again had the financial breathing room to do two things at once: fund aggressive investment in Experiences and return real cash to shareholders. That’s a sharp contrast from the Chapek period, when streaming losses soaked up the oxygen and left far less room for anything else.

Three Companies in One: The Business Dissected

To understand Disney’s valuation — and why the market can’t seem to agree on what the company is worth — you have to see Disney for what it actually is: three very different businesses sharing one logo. They have different economics, different competitors, and different destinies. The magic, and the headache, is that they also feed one another.

Disney Experiences: The Invisible Giant

Walk into the Magic Kingdom on a random Tuesday in January — supposed to be the sleepy season at Walt Disney World — and you can still find yourself waiting forty-five minutes for Space Mountain. The park might be “only” two-thirds full, but it doesn’t feel empty. The hotels are humming. The dining reservations are booked. And the families who planned this trip a year ago are spending more than Disney has ever been able to get them to spend.

That’s the part outsiders miss. The parks business isn’t growing because Disney is stuffing more people through the gates. It’s growing because Disney keeps getting better at earning more per guest.

In fiscal 2025, Experiences produced $36.2 billion in revenue and $10 billion in operating income — about sixty percent of Disney’s total segment profit. In Q1 of fiscal 2026, it set a quarterly revenue record of $10 billion and generated $3.3 billion in operating income. The key detail was what drove it: domestic operating profit grew eight percent on just one percent attendance growth, powered by four percent higher per-cap spending. Translation: Disney’s superpower is pricing power.

And it’s not subtle. Post-pandemic, Disney rewired how the whole parks economy works. Dynamic ticket pricing replaced the simpler, flatter model. Genie+ and Lightning Lane upcharges replaced the free FastPass system, turning “skip the line” into a paid product. Hotels and add-ons pushed guests into higher-spend tiers. Across food, merch, and premium experiences, pricing rose to levels that would have sounded implausible a decade earlier.

People complained — loudly. “Nickel-and-diming” became the default critique. Entire corners of the internet declared the affordable Disney vacation dead.

Demand held anyway.

That’s why this isn’t a theme-park company in the way Six Flags is a theme-park company. Experiences is an experiential luxury business with theme-park aesthetics. The reason Disney can keep pushing price isn’t because the rides are marginally better. It’s because the emotional product is different. A regional park can build a taller coaster. It can’t manufacture the moment a child meets a princess, or the feeling of fireworks over Cinderella Castle after a day you’ll retell for the next twenty years. That’s not an amenity. That’s the brand.

The best-kept secret inside Experiences is the cruise line, which has quietly become Disney’s fastest-growing sub-business. New ships are coming online in a steady drumbeat: Disney Treasure and Disney Destiny launched in late 2025, and Disney Adventure is scheduled for March 2026, homeported in Singapore as the first Disney ship based in Asia. The economics are exactly what you’d want them to be: occupancy above ninety percent, long waitlists for the most desirable sailings, and per-passenger revenue and margins that run richer than the parks. The Asia homeport isn’t just a new itinerary; it’s a new geography.

Then there’s Disney Vacation Club, with more than 220,000 member families on a points-based, timeshare-style system. It’s the ultimate loyalty program. These families don’t debate whether they’ll do Disney again. They debate which Disney property they’ll do this time.

And looming over everything is Disney’s $60 billion, ten-year investment plan, announced in late 2023 and now in motion. New lands at Walt Disney World — Cars, Disney Villains, Monsters Inc., and what’s described as the largest Magic Kingdom expansion in the park’s history. An Avatar area at Disneyland. A new theme park in Abu Dhabi, Disney’s first in the Middle East. More cruise ships. It’s the clearest capital allocation statement Disney has made in years: this is where the moat lives.

It’s also a response to the most serious competitive threat the parks have seen in a long time. Universal’s Epic Universe opened in Orlando in 2025, right next to Disney’s home turf, built to siphon off the exact same family vacation dollars — Nintendo World, expanded Harry Potter, DreamWorks attractions, and a Universal Monsters experience designed to skew older.

Disney isn’t treating that like noise. The $60 billion plan is the tell. This isn’t a defensive crouch; it’s a parks arms race. Disney’s bet is that if it keeps widening the gap in scale, immersion, and breadth — more lands, more capacity, more reasons to stay on-property — then even a great Universal vacation becomes the “and we also did this” add-on, not the main event.

Whether $60 billion earns the returns Disney needs is a real question. The company has historically generated strong returns on parks investment. But this is a commitment at a size Disney hasn’t attempted before, and execution risk rises with ambition.

Entertainment: Streaming, Studios, and the Long Road to Netflix-Like Margins

If Experiences is the visible engine, Entertainment is the part everyone argues about — because it’s where Disney competes most directly with Netflix, and where Wall Street’s expectations have been reset over and over.

Disney ended fiscal 2025 reporting 196 million streaming subscriptions across Disney+ and Hulu — and then essentially declared the growth scoreboard less important. In Q1 of fiscal 2026, following Netflix’s lead, Disney stopped disclosing subscriber counts. That was the signal: the era of “how many” is giving way to “how profitable.”

The trajectory has been improving fast. Entertainment DTC delivered $1.33 billion in operating income in fiscal 2025. In Q1 of fiscal 2026, streaming operating income was $450 million on an 8.4 percent margin. Management guided to roughly a ten percent SVOD operating margin for the full year, with double-digit Entertainment segment operating income growth weighted to the back half.

There’s another reason Disney believes it can keep pushing margins: pricing runway. Domestic Disney+ ARPU is around eight dollars a month. Hulu SVOD ARPU is roughly twelve. Both are well below Netflix’s domestic ad-free pricing north of twenty dollars. Disney doesn’t need a new subscriber miracle to improve unit economics. It can get there, at least partially, by charging more for what it already has — especially as it improves the product and reduces churn.

The centerpiece of that product improvement is the Hulu unification planned for 2026: one app for U.S. subscribers that combines Disney+ with Hulu’s general entertainment and FX’s prestige slate. Strategically, it’s Disney admitting what consumers already know: a streaming service that’s primarily “family” is incomplete if you want it to be a household default.

And FX and Hulu Originals are exactly the kind of adult-focused credibility Disney needs to feel indispensable. The Bear, Shogun, Only Murders in the Building, Abbott Elementary, The Americans — this is award-winning, culture-driving television. In another corporate universe, you’d call it Disney’s HBO. The catch is that most consumers don’t associate FX with Disney at all, which is precisely the branding gap the unified app is meant to close.

On the studio side, the story has been less about volume and more about re-finding the hit rate. Marvel’s Phase 4 era was broadly viewed as a creative stumble — too many series, too much mediocrity, softer theatrical momentum. But Deadpool and Wolverine, at $1.3 billion worldwide in 2024, was a reminder of what happens when execution is sharp. The next big tests are Avengers: Doomsday and Secret Wars, positioned as the next Endgame-scale events. And Disney’s broader film studio had a monster year in 2024: the first to cross $4 billion globally, powered by Inside Out 2, Deadpool and Wolverine, and Moana 2.

Entertainment can still dominate the box office. The open question is whether it can build a streaming business with margins that start to resemble Netflix — and do it while also funding the rest of the Disney machine.

Sports and ESPN: The $30 Bet

Sports is the third business, and in some ways the most consequential pivot Disney is trying to execute. In fiscal 2025, the Sports segment delivered $2.88 billion in operating income, up twenty percent year over year. In Q1 of fiscal 2026, sports advertising grew ten percent — one of the strongest ad categories in all of media.

ESPN’s rights portfolio remains a fortress: NFL Monday Night Football through 2033, the NBA (retained as the market got dramatically more expensive), MLB, SEC and ACC football, college basketball, the 2026 World Cup, Wimbledon, and WWE premium live events beginning in 2026.

The NBA deal in 2024 was also a billboard for where sports media is headed. Warner Bros. Discovery lost the NBA after forty years. ESPN and Amazon won. The league chose scale and balance-sheet confidence over legacy.

Then there’s ESPN Bet, launched in November 2023 through a licensing deal with Penn Entertainment valued at more than $1.5 billion. This is Disney leaning into a simple idea: if ESPN is the habit for sports fandom, betting can become the monetization layer. Integrating odds, data, and wagering into the ESPN direct-to-consumer experience is a pipeline competitors would love to own. The broader market is projected to exceed $40 billion by 2030.

But everything still collapses to one question: can ESPN Unlimited, at $29.99 per month, scale fast enough to replace what the cable bundle used to print automatically? The linear business still throws off meaningful income from roughly sixty million cable subscribers — but that base shrinks every year. Direct-to-consumer has to ramp before the floor drops out.

The 2026 World Cup — exclusively on ESPN — is the best possible stress test of that thesis.

There’s also a structural twist to ESPN’s transition. In late 2024, Disney sold a ten percent equity stake in ESPN to the NFL, bringing the league into the ownership of the network that pays it billions in rights. It’s an unusual alignment: if ESPN’s direct-to-consumer future works, the NFL’s stake becomes more valuable, and the league has an incentive to help ESPN’s evolution succeed. Hearst Communications also holds a twenty percent stake. The ownership structure, in effect, creates a coalition of powerful interests rooting for ESPN to pull off the jump from cable network to standalone sports platform.

Competitive Landscape: Three Different Games Simultaneously

Disney’s competitive position is unusual — maybe unique — because it doesn’t have one clear rival. It has three. And they’re not fighting on the same battlefield.

That’s a big reason the market can’t agree on what Disney is worth. Investors aren’t just trying to value a company. They’re trying to value three different businesses stapled together, each with its own economics, competitors, and endgame. That’s where the conglomerate discount comes from.

In streaming, the comparison everyone reaches for is Netflix. Netflix has more than 300 million subscribers, roughly $43 billion in annual revenue, and operating margins in the high twenties. Disney’s streaming business is smaller — about $24.6 billion in revenue — and its margins are still in the mid-single digits. And even though Disney generates far more total revenue as a company, Netflix’s market cap, around $430 billion, is much larger than Disney’s.

That valuation gap isn’t just about who has more subscribers. It reflects a deeper disagreement: can Disney’s streaming business ever become as clean and efficient as Netflix’s? Netflix is a pure-play. Disney is not. Netflix has no legacy linear-TV drag. Disney does. Netflix is optimized for one job: win time on a screen at global scale.

But Disney’s advantage in streaming isn’t something you’ll find in a subscriber chart. It’s the flywheel.

Netflix can’t build theme parks. Amazon can’t build theme parks. Apple can’t build theme parks. What Disney has is a customer relationship that can start with a movie, deepen with a park trip, and then repeat for decades through merchandise, cruises, and return visits. Streaming-only companies can win a month. Disney can win a family.

A Netflix subscriber might churn the moment they finish a show. A Disney family that’s been to Walt Disney World, bought the Frozen costumes, and joined Disney Vacation Club is not “subscribed.” They’re embedded.

In physical experiences, the threat looks totally different. Universal’s Epic Universe is the most serious challenge to Disney’s Orlando dominance in two decades. But that competition is almost entirely physical and geographic: where families choose to spend their vacation time and money. Comcast isn’t really coming for Disney in streaming the way Netflix is. The battle here is about immersion, capacity, and reinvestment — exactly why Disney’s $60 billion plan matters. If Disney keeps expanding and upgrading the on-property experience, it can defend its pricing premium even with a stronger Universal next door.

In content and general entertainment, Warner Bros. Discovery is the most direct peer — but also the most constrained. Max has roughly 150 million subscribers, and HBO’s track record for prestige hits is a real advantage. But WBD’s market cap, around $48 billion, tells you how heavy the balance sheet is. The debt from the AT&T–Discovery merger limits flexibility in a world where flexibility is everything: spending on content, bidding on sports, and waiting out downturns. Losing the NBA in 2024 was the clearest sign yet that WBD may not be able to keep playing at the top table in sports.

Then you have the giants with reasons to participate, but not to win in the same way.

Apple spends around $7 billion a year on content, but Apple TV+ functions as ecosystem glue — a way to keep people buying iPhones — not a standalone entertainment business that needs to throw off profit on its own. Amazon spends around $20 billion on content and has NFL Thursday Night Football, but Prime Video is still bundled with free shipping. It’s not competing as a pure product customers choose independently, and Amazon doesn’t have a century of IP that lives in childhood memory.

Put it all together and the key insight is simple: Disney is the only major company simultaneously playing all three games — streaming, physical experiences, and live sports — at real scale.

No competitor attacks Disney on all fronts at once. Netflix doesn’t have parks. Universal doesn’t have streaming. Amazon doesn’t have sports rights at Disney’s scale. Apple doesn’t have IP that children have loved for a hundred years.

That complexity is Disney’s biggest operational challenge — because managing three fundamentally different businesses demands three different playbooks — and its most durable strategic advantage. Disney may be hard to value, but it’s also hard to assault.

Strategic Moat: Where the Power Lies

If you run Disney through Hamilton Helmer’s Seven Powers, the picture gets clearer fast: some parts of Disney are almost unfair, and some are far more fragile than the brand aura suggests.

Start with the obvious superpower: branding. Disney, Marvel, Star Wars, Pixar — these aren’t just logos. They’re generational trust markers. When a parent puts on a Disney movie for their kid, they’re not making a content choice. They’re making a safety-and-quality choice. That kind of emotional equity takes decades to build, and once it’s there, it compounds. It becomes inheritance.

Next is cornered resources: assets you can’t simply recreate, no matter how much money you have. There is no second Marvel canon. No alternate Star Wars timeline you can buy off the shelf. Those worlds are scarce in the way only truly iconic storytelling franchises are scarce.

And it’s not just IP. Walt Disney Imagineering is a cornered resource too. It’s accumulated craft: thousands of people who know how to turn a two-hour movie into a physical place that can handle tens of thousands of guests a day, year after year, while still feeling like “magic.” That isn’t something a competitor can reverse-engineer from the outside, and it isn’t something you can hire away in one recruiting cycle. ESPN’s long-term sports rights contracts fit here as well: hard-to-replace inventory locked up for years.

Then there’s the most uniquely Disney power of them all: counter-positioning. Disney is the only major media company with a physical experiences moat throwing off around $10 billion a year in operating profit. Netflix can’t wake up tomorrow and decide to build Walt Disney World. Neither can Amazon or Apple. It’s not just capital. It’s time, land, operational muscle, and a century of trust that makes families willing to plan their year around a Disney trip. If a tech company announced a “Disney World competitor” on an earnings call, it wouldn’t sound bold. It would sound unserious.

But the weak spots matter, because they explain why Disney can feel invincible culturally and still look vulnerable financially.

Scale economies, for instance, are only moderate. Streaming isn’t software. Each incremental user isn’t close to free, because retention requires a steady drumbeat of expensive, high-quality content. The economics don’t automatically improve just because you get bigger.

Switching costs in streaming are also painfully low. Canceling Disney+ takes seconds. There’s no real lock-in unless Disney creates it through habit, bundling, and must-see programming.

And process power — the repeatable ability to generate great hits — turned out to be less durable than people assumed. The MCU’s Phase 4 era exposed what happens when quality control slips and the release calendar turns into a firehose. The brand takes the hit immediately. The lesson is simple and brutal: creative engines don’t run on autopilot. They run on taste, leadership, and restraint.

Porter’s Five Forces tells the same story from another angle.

The threat of new entrants is low in parks and foundational IP. You can’t casually decide to build a Disney-scale resort; it takes billions, years, and a brand relationship that most companies will never have. In streaming, though, the barrier is much lower. Apple and Amazon proved that if you have enough capital and patience, you can enter the market and buy your way into relevance.

Supplier power is high — and rising — which is one of Disney’s biggest structural risks. Sports leagues set the price, and the price keeps climbing. The NFL and NBA don’t negotiate like vendors; they negotiate like monopolists selling irreplaceable product. On the creative side, the 2023 WGA and SAG-AFTRA strikes reminded everyone of another reality: the content doesn’t happen without the people who make it, and those people can stop the whole machine.

And rivalry is brutal everywhere at once. Streaming is a knife fight with well-funded competitors. Sports rights are an escalating bidding war. Universal is investing aggressively in parks. Disney isn’t competing in one tough market — it’s competing in three, simultaneously, and none of them are getting cheaper.

Current Leadership: The D'Amaro Era Begins

On February 3, 2026, Disney’s board made it official. After a search that Chairman James Gorman described as “long and exhaustive” — more than a hundred candidates evaluated over nearly three years — Josh D’Amaro was unanimously selected as Disney’s ninth CEO. He’ll take the job at the annual meeting on March 18, 2026.

D’Amaro is fifty-four. He joined Disney in 1998 in Disneyland sales and marketing, selling sponsorship packages and group tickets — about as far from the CEO suite as you can get while still wearing a Disney badge. He wasn’t a Harvard MBA dropped into a rotational program. He was a kid from Long Island who loved the parks, got a job in the parks, and spent nearly three decades climbing his way up, role by role, through the company’s most operationally demanding business.

His path reads like a tour of Disney’s money engine: CFO of Consumer Products Global Licensing, President of Disneyland Resort, President of Walt Disney World, and then, starting in May 2020, Chairman of Disney Experiences. People who’ve worked with him describe the same profile: charismatic, hands-on, and intensely detail-oriented — the kind of leader who walks the parks, talks to cast members, and notices the small stuff because the small stuff is the product. He’s not a distant corporate strategist. He leads from the floor.

The record that got him the job is real. Under D’Amaro, Experiences grew into a roughly $36 billion revenue business generating $10 billion in record operating income. He oversaw the complete COVID shutdown of every Disney park worldwide — an operational crisis involving hundreds of thousands of cast members across six continents. He steered through the Florida political fight around Reedy Creek, keeping Walt Disney World running while the legal and political storm raged overhead. He implemented the post-pandemic pricing overhaul — the one that drove per-capita spending higher without collapsing demand. And he pushed the cruise expansion that’s set to significantly grow the fleet, including new reach into Asia and the Middle East.

In other words, no one questions his operating chops. The business that produces about sixty percent of Disney’s operating profit hit records on his watch. And he’s been a key architect of the $60 billion, ten-year Experiences investment plan — the biggest capital bet Disney has made in years.

But the elephant in the room is obvious: Bob Chapek also came from Parks. The board knows that comparison will be made instantly, and it tried to design a structural answer into the succession itself. That’s why Dana Walden’s role matters so much. Making her President and Chief Creative Officer — and having her report directly to D’Amaro — is Disney’s attempt to hardwire entertainment and streaming expertise into the very top of the company, so the creative center of gravity doesn’t drift again.

Walden brings heavyweight credentials. She arrived through the Fox acquisition in 2019, after building Fox Broadcasting Company and 20th Century Fox Television into major forces. At Disney, she built the streaming content slate and oversees ABC, FX, Hulu Originals, National Geographic, and Disney Branded Television. Her bench includes the kind of prestige hits that buy legitimacy in Hollywood: The Bear, Shogun, Only Murders in the Building, Abbott Elementary.

And the key tension isn’t just organizational — it’s personal. Walden wanted the CEO job too, and she was D’Amaro’s primary rival. The board’s retention package — a one-time equity award with a $5.26 million target value, on top of her ongoing compensation — is meant to keep her through the transition. But compensation can’t solve ambition. If Walden walks, Disney doesn’t just lose a top executive; it loses the person most capable of preventing the “Chapek 2.0” narrative from becoming a self-fulfilling prophecy.

So the early tell in D’Amaro’s tenure is simple: does he give Walden real independence on the creative side? Chapek’s fatal mistake wasn’t incompetence — it was treating entertainment like a set of levers to be pulled by people who didn’t make entertainment. D’Amaro’s survival depends on proving he learned the lesson Disney just paid for.

Hovering over all of this is Bob Iger’s legacy — brilliant, complicated, and impossible to separate from the current moment. His greatest decisions — Pixar, Marvel, Lucasfilm, Disney+, the streaming pivot — reshaped the industry. His biggest failure, by his own public admission, was the Chapek succession. He called it “one of the biggest mistakes of my career.” The irony is sharp: the person most responsible for building modern Disney was also the person who helped create the crisis that required him to return and clean it up. Over his career, his total compensation is estimated to exceed $600 million, and he’ll remain as senior advisor through December 31, 2026.

Growth Catalysts and the KPIs That Matter

For anyone watching Disney in 2026 — especially investors — the catalysts aren’t subtle. They’re unusually clear, and they’re unusually concentrated.

First, and biggest: the ESPN Unlimited ramp into the 2026 FIFA World Cup. This is the make-or-break test of Disney’s sports transition, and arguably the most important test of ESPN’s strategy this decade. The World Cup returns to North America — hosted across the United States, Canada, and Mexico for the first time in more than three decades — and it’s exclusively on ESPN.

That exclusivity matters because the World Cup pulls in two audiences at once: the die-hard sports fans ESPN already understands, and the massive casual audience that shows up every four years and then disappears. For a direct-to-consumer product, that’s not just viewership. It’s customer acquisition.

The timing couldn’t be better for ESPN’s purposes. The tournament runs from mid-June through mid-July. Dozens of matches, spread across ESPN’s platforms, become repeated, high-frequency reasons to download the app and try the service. Every upset, every late goal, every controversy becomes free marketing. If Disney could design a launch vehicle in a lab, it would look a lot like this.

The second key story is streaming margins. Disney has said it’s aiming for roughly a ten percent SVOD operating margin in fiscal 2026, and the way you watch that progress is simple: Entertainment DTC quarterly operating income. The business posted $450 million of operating income in Q1 fiscal 2026 on an 8.4 percent margin. Now it has to keep stepping up, quarter after quarter, until the “streaming turnaround” stops being a narrative and becomes a durable base.

Management guided to about $500 million in Q2 SVOD operating income, which would be a meaningful year-over-year improvement. But the point isn’t the exact dollar figure. It’s whether the trajectory holds — because that’s what tells you Disney has actually learned how to run streaming like a business, not a land grab.

The levers are known: price increases, the Hulu unification, and ad-supported tiers should lift ARPU. But the tension is just as clear: content costs have to stay under control at the same time. A strong theatrical slate in the back half of fiscal 2026 — including a live-action Devil Wears Prada sequel, Mandalorian and Grogu, and Toy Story 5 — should help at the box office and create streaming momentum. The question is whether the cost of feeding the machine starts to eat the margin gains the machine was supposed to deliver.

Then there’s the human catalyst, and it’s the one Disney can’t spreadsheet away: the D’Amaro transition. The first few months of a CEO’s tenure always generate noise, but this one has specific signals worth listening for. Does D’Amaro show up in Hollywood — spending time with filmmakers and creative leaders — or does he default to the parks world he’s mastered? Does Walden actually have the authority her title implies, or does the organization drift back toward budget control and optimization at the expense of creative conviction?

Medium term, Disney’s path is defined by execution. The $60 billion Experiences build-out — new lands at Magic Kingdom, the Abu Dhabi project, and cruise expansion into Asia — is designed to compound operating income for years, because every new attraction adds long-lived capacity. At the same time, Marvel’s next swing — through Avengers: Doomsday and eventually Secret Wars — is the franchise’s chance to prove it can still deliver an Endgame-scale moment instead of just steady output.

The Epic Games partnership sits in its own category: a real option on a new distribution channel. If the Disney universe within Fortnite becomes a place people actually spend time — and it produces real engagement and licensing revenue — it validates a new kind of “park” that scales digitally. If it doesn’t, it remains a $1.5 billion wager on a thesis that didn’t translate.

Zooming out further, the structural questions don’t change, they just get louder: can Disney’s streaming margins ever move into the high teens or twenties the way Netflix’s have? Will AI meaningfully change the economics of making content and personalizing park experiences? And can ESPN prove that enough fans will pay a premium for a standalone sports product that cable households used to fund by default?

If you want to reduce all of that complexity to the handful of numbers that actually matter, there are two.

First: Experiences segment operating income. This is Disney’s financial engine. Its growth rate determines how much room Disney has to invest, absorb volatility in media, and still return cash through buybacks and dividends.

Second: Entertainment SVOD operating margin. This is the streaming thesis in one metric. If it climbs toward the mid-teens over the next couple of years, Disney’s valuation story changes. If it stalls in the single digits, the bear case stops being a debate and starts becoming consensus.

The Investor Debate: Bull vs. Bear

By 2026, Disney has become the kind of company where two smart people can look at the same earnings report and see two totally different futures.

The bull case starts with the thing Disney has that no one else can manufacture quickly: physical gravity.

Parks are irreplaceable. No technology company can disrupt the experience of a family’s first trip to the Magic Kingdom. And Disney is leaning into that advantage with the $60 billion investment plan, widening the gap against Universal right as Epic Universe raises the stakes in Orlando. The bigger point is that Disney vacations don’t behave like most discretionary spending. Families plan them years in advance. They save for them. They lock in future visits through Disney Vacation Club. These trips aren’t just entertainment purchases; they’re emotional milestones—honeymoons, birthdays, graduations, the “once in a lifetime” trip that ends up outranking a lot of other discretionary choices. Recessions can slow Disney down, but they rarely stop it. Even the 2008 financial crisis dented attendance for a couple of quarters, and Disney recovered within a year.

Then there’s streaming—the part of the story that looked like a slow-motion disaster, until it didn’t.

Disney’s direct-to-consumer business going from roughly $2.5 billion in annual losses to about $1.3 billion in operating profit in two years is one of the fastest turnarounds in modern media. If you believe the company can keep pulling the same levers—selective price increases, more ad-tier penetration, password-sharing enforcement, and a cleaner product experience—then a path toward fifteen to twenty percent margins over the next five years doesn’t sound crazy. The 2026 Hulu unification matters here not because it’s a tech rewrite, but because it addresses the most obvious product weakness: Disney+ as “the family app” versus Netflix as “the default household app.” One combined offering that serves both families and adults should lift ARPU and reduce churn.

ESPN direct-to-consumer is the other potential unlock—the one that could change how the market values Disney overnight. If ESPN Unlimited can convert something like twenty to thirty million dedicated sports fans at $29.99 a month, the cable decline becomes far less scary because the revenue base has been rebuilt around people who actually want the product. And Disney gets the best possible catalyst at the best possible time: the 2026 World Cup, in North America, exclusively on ESPN—a marketing moment you couldn’t buy even if you wanted to.

The bull case also argues that the stock already reflects a lot of skepticism. At around twelve times EV/EBITDA and roughly fifteen to sixteen times forward earnings, Disney isn’t priced like a company with multiple shots on goal. With guidance for double-digit adjusted EPS growth in fiscal 2026 and a $7 billion stock buyback program, the setup is straightforward: if streaming margins keep climbing or ESPN DTC adoption surprises to the upside, the stock can re-rate.

And finally, there’s the “stability premium.” After years of boardroom drama, activist fights, and CEO whiplash, an orderly succession under Josh D’Amaro—with board continuity under James Gorman—reads as a feature, not a footnote. In a business like Disney, boring competence can be an asset.

But the bear case is just as real—and it targets the exact same pillars.

Streaming margins may never look like Netflix’s, not because Disney is doing it wrong, but because Disney is structurally different. The company spends roughly $20 to $22 billion annually on content across all platforms and does it with more organizational complexity than a pure-play streamer. Disney is running a creative studio system, a global parks empire, and a sports rights machine under one roof. Netflix’s twenty-six to twenty-eight percent operating margins may be something Disney can narrow toward, but never truly match, because the cost base and the corporate shape are fundamentally different.

Then there’s ESPN, where the transition is not optional and the timing is unforgiving. Cable affiliate revenue continues to fall at a mid-to-high single-digit pace. ESPN Unlimited has to replace a model that, for forty years, was subsidized by tens of millions of households who barely watched sports. Direct-to-consumer removes the subsidy. Now the burden shifts to the real fans—and the open question is whether enough of them will reliably pay $30 a month, at scale, fast enough to outrun the linear decline.

The Fox deal still hangs over everything, too. It was a $71 billion acquisition that added major complexity and left Disney with roughly $35 to $37 billion in remaining debt. Management continues to acknowledge the integration drag, and return on invested capital hasn’t returned to pre-deal levels. Star India alone was losing more than $600 million annually before the Reliance joint venture. The bear view is simple: the acquisition that was supposed to power the streaming era also loaded Disney with baggage, and the bill isn’t fully paid yet.

Franchise fatigue is another real risk. The MCU’s Phase 4 period was widely viewed as a quality dip, with a run of Disney+ series and releases that landed below the brand’s historical standard. Star Wars has struggled for creative consistency since The Force Awakens. Pixar was uneven before Inside Out 2 restored momentum. The warning is brutal but true: great IP without sustained creative excellence becomes nostalgia on a timer—and the timer runs out faster than executives want to admit.

And hovering over all of it is succession risk. Josh D’Amaro has never run an entertainment or media business. He hasn’t greenlit a film, managed a television network, negotiated talent at scale, or owned a streaming content slate. He comes from Parks—exactly like Bob Chapek. Disney’s structural answer is Dana Walden: a newly empowered President and Chief Creative Officer meant to anchor the creative center of gravity. It’s a reasonable design, but it’s untested. And it depends on a partnership between two executives where one wanted the other’s job. That dynamic can work. It can also quietly rot a leadership team from the inside.

Wall Street’s view reflects that uncertainty. At the time of writing, analysts are split between optimism and caution—seventeen Buys, six Holds, and one Sell—with an average twelve-month price target around $136. The wide range of fair-value estimates, from the low seventies to above $150, isn’t noise. It’s the market admitting it doesn’t yet know the answer to three questions: will ESPN DTC work, can streaming margins keep climbing, and will the D’Amaro–Walden structure hold when the first real creative and financial tradeoffs arrive?

The Playbook: What Builders and Investors Can Learn

Walt Disney’s century-long story offers lessons that travel far beyond entertainment.

First: flywheels are real, and they demand patience.

Walt discovered the model in 1955 when he opened Disneyland. Bob Iger weaponized it in the 2000s by acquiring Pixar, Marvel, and Lucasfilm, then plugging those story engines into the same loop that powers Disney’s economics: content creates attachment, attachment sells merchandise, merchandise helps justify the trip, and the trip deepens the attachment for the next story. Streaming just became the newest spoke on the wheel.

Plenty of companies have tried to copy this. Comcast built Universal parks and launched Peacock. Warner Bros. launched Max and invested in theme parks. But no one has built it at Disney’s scale. The reason is simple: the mechanism is easy to describe, but brutal to replicate. It takes decades, it requires enormous upfront investment that looks foolish in the moment, and it runs on accumulated emotional equity — the kind you can’t buy in any deal, at any price.

Second: acquisitions don’t just buy assets. Sometimes they buy a process.

The Pixar deal wasn’t a library purchase. It was a culture purchase. And across Iger’s major acquisitions, the pattern repeats: he wasn’t simply buying characters and titles; he was buying creative institutions and the people who made them work. John Lasseter and Ed Catmull at Pixar. Kevin Feige at Marvel. Kathleen Kennedy at Lucasfilm. The FX creative team that came with Fox.

That’s why valuing creative companies purely on EBITDA multiples can miss the point. In media, the real asset is the thing that reliably creates the next hit — the culture, the leadership, the process. Everything else is inventory. So when people asked whether Disney overpaid for Pixar, they were often asking the wrong question. The right one was whether Disney could absorb Pixar’s creative culture and rebuild its own animation engine. It could, and it did — and the returns have been hard to overstate.

Third: succession planning is not a governance formality. It’s existential.

The Chapek era has become a cautionary tale for boards everywhere: promoting based on operational performance without cultural fit; an outgoing CEO failing to truly let go; and a dual-power structure that undermined authority without preventing bad decisions. Disney needed a leader who understood the soul of the organization, not just its spreadsheets.

Creative organizations require leaders who have earned creative legitimacy. Operational excellence doesn’t automatically transfer. Someone can run a theme park flawlessly and still misread why a film needs a particular director, or why a creative team needs three more months to get the ending right.

Disney’s board is trying to solve for that this time by pairing an operational CEO with a powerful creative officer. It could prove wise. Or it could be an elegant theory that collapses under the weight of ego, incentives, and organizational politics. Either way, it’s an admission that Disney can’t afford another mismatch at the top.

Fourth: in a digital age, the best moats are the ones technology can’t clone.

Disney built a competitive advantage that Silicon Valley can’t disrupt: a physical, emotional, multi-generational experience. Every year a tech company announces it’s “disrupting entertainment,” Disney’s parks and cruises become slightly more valuable by contrast.

You can’t stream the feeling of a child meeting a Disney princess for the first time. You can’t download fireworks over Cinderella Castle. You can’t replicate Main Street’s sensory details or the way a day in the parks lodges itself into family memory.

In an era of infinite digital abundance, physical scarcity and emotional irreplaceability are rare. Disney has both.

The Kingdom at a Crossroads

On March 18, 2026 — one month from today — Josh D’Amaro will officially become Disney’s ninth CEO. Bob Iger, after nearly two decades as the central figure in American media, will step back into an advisory role. It’s the most consequential entertainment succession since Steve Jobs handed Apple to Tim Cook. And like that transition, it forces a question no org chart can settle: can a company whose product is creative magic be led by someone whose genius is operational excellence?

The Apple parallel is useful, because it shows what’s possible — and what people worry about. When Cook succeeded Jobs, skeptics predicted Apple would become a brilliantly run hardware company: efficient, profitable, and slowly less soulful. Cook proved the first two parts spectacularly wrong in the best way. Apple under Cook went on to generate more revenue, more profit, and more shareholder value than Apple under Jobs. But the critique never fully disappeared: that Apple’s innovation became more incremental than revolutionary. The open question is whether D’Amaro’s Disney follows a similar arc — operationally excellent, financially disciplined, strategically coherent, but gradually less culturally essential.

Which gets to the deepest structural question Disney is really answering right now, whether it says it out loud or not: what is Disney? Is it a theme park company that happens to make movies and TV? Or a content company that happens to have theme parks? The answer determines everything — capital allocation, the kind of CEO you want, the strategy you pick, and ultimately what the stock deserves to trade at.

D’Amaro’s implicit answer is hard to miss. It’s in his résumé. It’s in the $60 billion parks investment plan. And it’s in the basic fact that Experiences now generates roughly sixty percent of Disney’s operating profit. In this view, the physical, experiential business is Disney’s ultimate competitive advantage. Content is the fuel. Experiences is the engine. The flywheel still spins, but the center of gravity has moved from the studio lot to the park gate.

The counterargument is existential. Without great stories, the parks are just very expensive rides. Characters only matter if audiences still love them. No one waits two hours for a roller coaster themed to a movie they didn’t enjoy. In that world, Dana Walden isn’t supporting cast. She’s structural. If the content falters, the parks lose emotional force, merchandise softens, and the flywheel that has powered Disney for decades starts to slow.

The one number that defines modern Disney makes this plain: in fiscal 2025, Experiences generated $10 billion in operating income. Streaming generated $1.3 billion. The parks subsidize the streaming bet, not the other way around. That’s the central financial fact of Disney in 2026 — and the central question for the next decade is whether streaming ever becomes big enough to stand on its own, or whether Disney’s future is a company where physical experiences produce the profit and content exists, primarily, to keep those experiences priceless.

Look at the arithmetic another way. Disney’s total segment operating income in fiscal 2025 was $17.6 billion. Experiences contributed $10 billion, Sports $2.9 billion, and Entertainment $4.7 billion. Strip out the parks entirely and what’s left — streaming, linear TV, film studios, ESPN — is roughly $7.6 billion of operating profit on about $58 billion of revenue. That’s a solid media company. It’s not an extraordinary one. The parks are what make Disney, Disney. They’re a big reason the company trades differently than most legacy media. And they’re a big reason the board just handed the enterprise to a parks executive.

Walt Disney believed, from the beginning, that being inside his worlds — not just watching them — was the thing that mattered most.

In 2026, it turns out that’s also where most of the money is.