Diodes Incorporated: The Quiet Power Behind Modern Electronics

I. Introduction & Episode Roadmap

Somewhere inside your laptop, your car's dashboard, the server rack humming in a data center, and the LED bulb above your head, there are tiny chips made by a company most people have never heard of. Diodes Incorporated does not make the processors that get the headlines or the memory chips that move stock markets. It makes the unglamorous stuff: the voltage regulators that keep power stable, the signal switches that route data, the protection diodes that prevent circuits from frying, the timing chips that keep everything synchronized. And it makes tens of thousands of variations of these components, shipping billions of units every year to customers on six continents.

The question at the heart of this story is deceptively simple: how did a tiny semiconductor trading company founded in 1959 transform itself into a roughly three-billion-dollar-market-cap global analog and mixed-signal powerhouse? And how does it survive, let alone thrive, in a market dominated by titans like Texas Instruments, Infineon, ON Semiconductor, and Analog Devices, companies with five to ten times its revenue?

The answer is not a single breakthrough product or a brilliant founder's eureka moment. It is a sixty-year story of patient transformation, disciplined acquisition, geographic arbitrage, and the relentless accumulation of small advantages in markets where no single chip matters much, but the aggregate portfolio matters enormously.

Diodes is the semiconductor equivalent of a utility infielder who bats .280 every year, plays seven positions, and somehow keeps appearing in the playoffs. Not flashy. Not famous. But remarkably hard to replace.

This is a story about three strategic inflection points: the acquisitions of BCD Semiconductor in 2013, Pericom Semiconductor in 2015, and Lite-On Semiconductor in 2020, each of which fundamentally reshaped what Diodes was and could become. It is about a Taiwanese-born, Texas Instruments-trained executive named Dr. Keh-Shew Lu who ran the company for two decades and built it from a two-hundred-million-dollar afterthought into a nearly two-billion-dollar enterprise at its peak. And it is about the broader question of whether mid-tier analog semiconductor companies can build durable competitive advantages, or whether they are destined to be absorbed by larger rivals in an industry that relentlessly consolidates.

The semiconductor industry loves to talk about Moore's Law, artificial intelligence, and the bleeding edge of chip fabrication. NVIDIA's stock price dominates the financial news. TSMC's most advanced fabrication nodes generate breathless coverage. Apple's latest processor design gets dissected in teardown videos watched by millions. Meanwhile, Diodes operates in a parallel universe where the physics of power conversion, signal integrity, and electromagnetic protection change slowly, where reliability and cost matter more than transistor counts, and where the real competitive weapon is not innovation but execution.

The company today employs roughly 8,600 people across thirty-two global locations, operates wafer fabrication facilities in four countries, and generates nearly $1.5 billion in annual revenue across five end markets: computing, industrial, automotive, consumer, and communications. Its shares trade on the NASDAQ under the ticker DIOD, and its headquarters sit in Plano, Texas, far from the Silicon Valley spotlight. That combination of scale, obscurity, and strategic complexity makes it one of the most interesting case studies in the entire semiconductor ecosystem, and one of the least understood.

II. Founding Context & The Early Distributor Years (1959-1990s)

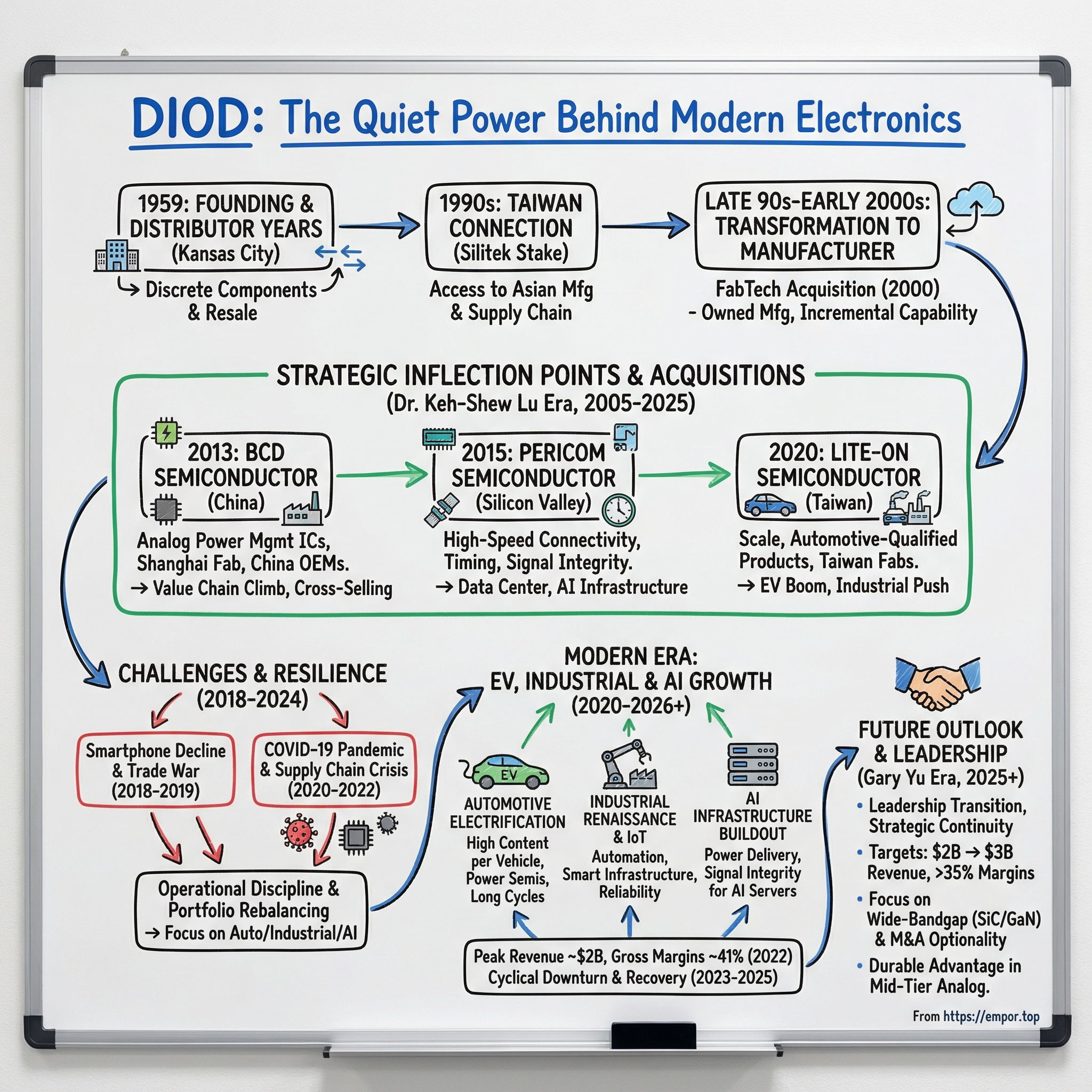

Picture Kansas City in 1959. While Fairchild Semiconductor was busy inventing the integrated circuit on the other side of the country and launching what would become Silicon Valley, a small trading outfit incorporated in the American heartland with a decidedly less glamorous mission. Diodes Inc., as it was originally known, set up shop not to design or manufacture semiconductors but to buy and resell them. The company was a distributor, a middleman in the fragmented world of discrete components: diodes, rectifiers, transistors, and other basic building blocks of electronic circuits.

To understand why this business existed, you need to understand the semiconductor landscape of the 1960s and 1970s. The industry was young, chaotic, and wildly fragmented. Dozens of small manufacturers made specialized components, and the original equipment manufacturers building radios, televisions, industrial equipment, and early computers needed someone to aggregate supply, manage inventory, and handle the logistics of sourcing hundreds of different part numbers from dozens of different vendors. Distribution was not glamorous, but it was necessary, and it could be profitable for those who understood the technical specifications well enough to match customers with the right components.

For roughly three decades, Diodes operated in this mode. Revenue barely exceeded ten million dollars a year for most of this period. The company built relationships, learned what customers actually needed versus what the big semiconductor companies wanted to sell, and developed a granular understanding of the discrete component market that would prove invaluable later. But it was, by any measure, a small and unremarkable business.

The first hint of transformation came in 1990, when Silitek Corporation, a Taiwanese manufacturer of semiconductor rectifiers, acquired a forty-six percent stake in Diodes by purchasing one million shares. This was not a hostile takeover or a dramatic corporate raid. It was a strategic investment by a Taiwanese company that saw an opportunity to gain access to the American market through an existing distribution network.

The timing was significant. In 1990, Taiwan was emerging as a semiconductor manufacturing powerhouse. TSMC had been founded just three years earlier. Dozens of Taiwanese companies were moving up the value chain from simple assembly operations to design and fabrication. Silitek, part of the Lite-On Group, one of Taiwan's largest technology conglomerates, was looking for distribution channels and market access in the United States. Diodes offered exactly that: established customer relationships, knowledge of the American market, and a platform for selling Taiwanese-manufactured components to US buyers. Control subsequently passed to Lite-On Power Semiconductor Corporation, a Silitek subsidiary, in 1991.

This Taiwanese connection was the seed of everything that followed. It gave Diodes access to Asian manufacturing capabilities, connected it to the rapidly growing electronics supply chain in Greater China and Taiwan, and introduced the company to a business model that combined American market access with Asian cost structures. By 1995, revenue had reached sixty-one million dollars, drawn from a marketing office in Westlake Village, California, and a facility in Taipei that handled engineering, manufacturing, purchasing, and sales.

The company was no longer just a trading outfit. It was becoming something hybrid: part American semiconductor company, part Asian manufacturer, with feet planted in both worlds. This dual identity, awkward and hard to categorize, would become its defining strategic advantage.

To appreciate why this mattered, consider the economics of the discrete semiconductor business in the late 1990s. A single diode or transistor might sell for two or three cents. Margins were thin, competition was fierce, and the only way to make money was through volume, efficiency, and customer stickiness. A pure distributor captured perhaps ten to fifteen percent gross margin on each transaction. A manufacturer could capture thirty percent or more, but needed to invest in fabrication equipment, process engineering, quality control, and supply chain management. The question for Diodes was whether it could make the transition from the distributor's margin structure to the manufacturer's margin structure without losing the customer relationships and market knowledge that were its primary assets.

The answer, it turned out, was yes, but only if the company chose its entry points carefully and built manufacturing capabilities incrementally rather than trying to compete head-on with established manufacturers from day one.

That strategy of incremental capability building, of adding one layer of value at a time, would define the company for the next three decades. But the real transformation required a catalyst, someone who understood both the technology and the business well enough to see the opportunity hiding in plain sight.

III. The Transformation Begins: From Distributor to Manufacturer (1990s-Early 2000s)

The semiconductor industry has a term for the moment when a company decides to stop doing one thing and start doing something fundamentally different: strategic inflection point. For Diodes, that inflection point arrived not as a single dramatic decision but as a series of deliberate steps across the late 1990s and early 2000s, culminating in a transformation from semiconductor trader to semiconductor manufacturer.

The first concrete move came in December 2000, when Diodes acquired FabTech, Inc., a small company operating a five-inch silicon wafer fabrication facility in Lee's Summit, Missouri. FabTech specialized in Schottky diodes, a type of component that Diodes knew intimately from its decades in the distribution business. The deal was modest by semiconductor standards: roughly six million dollars in cash plus up to thirty million dollars in earn-out payments. FabTech had about 210 employees and generated around twenty million dollars in annual revenue. But the strategic significance was enormous. For the first time in its history, Diodes owned a manufacturing facility. It could design and fabricate its own products rather than reselling someone else's.

The FabTech acquisition reflected a logic that would define Diodes' strategy for the next quarter century: acquire undervalued manufacturing assets, integrate them into the existing commercial network, and use the combination of owned manufacturing and deep customer relationships to capture margin that previously went to suppliers. The Missouri fab was not a cutting-edge facility. It used mature process technology to make mature products. But that was precisely the point. Discrete semiconductors and basic analog components do not require the latest fabrication technology. They need reliability, consistency, cost efficiency, and engineering support. A five-inch wafer fab making Schottky diodes was not going to produce the next iPhone processor, but it could produce millions of components at competitive costs for customers who valued a reliable supply of well-characterized parts.

Through the early 2000s, Diodes continued to build its capabilities. Revenue climbed from roughly sixty million dollars in the mid-1990s to over two hundred million dollars by 2005. The company established design centers, expanded its Asian operations, and began developing application-specific standard products, components designed for specific functions in specific applications but standardized enough to sell to multiple customers. This was the sweet spot of the analog semiconductor business: not custom chips, which require expensive design cycles for each customer, and not pure commodity components, which compete solely on price, but something in between.

The geographic strategy was already taking shape, driven by the gravitational pull of global electronics manufacturing toward Asia. By the early 2000s, China was rapidly becoming the world's largest electronics manufacturing hub, with Shenzhen, Shanghai, and the Pearl River Delta emerging as the epicenters of consumer electronics, computing, and telecommunications equipment production. Taiwan remained the dominant location for semiconductor manufacturing and advanced packaging. For a company selling components that went into these products, being close to the customers was not just convenient; it was essential for winning design-in opportunities.

Manufacturing and much of the design work migrated to Asia, where the customers were, where the cost structure was favorable, and where the supply chain ecosystem was densest. The American and European operations focused on customer relationships, application engineering, and corporate management. It was a model that the biggest analog semiconductor companies had pioneered, but Diodes executed it with a scrappiness and speed that larger competitors could not match.

The significance of the FabTech acquisition extended beyond the revenue and manufacturing capability it provided. It demonstrated that Diodes could execute an acquisition, integrate a manufacturing operation, and maintain quality standards while scaling production. This was not a given for a company that had spent forty years as a trader. Many companies attempt the transition from asset-light to asset-heavy and stumble on the operational complexity. Diodes' success with FabTech gave management the confidence and the organizational muscle memory to pursue larger acquisitions in the years ahead.

By the middle of the first decade of the 2000s, the company was ready for the next phase. It had manufacturing capability, a growing product portfolio, an Asian footprint, and customer relationships across multiple end markets. Revenue was climbing past two hundred million dollars annually, but the company remained a rounding error in the global semiconductor industry. What it needed was someone who could see the full picture and execute a coherent growth strategy that would transform a small player into a global contender. That person had already arrived.

IV. The Asia Pivot & Manufacturing Footprint (2000-2010)

In June 2005, Dr. Keh-Shew Lu was appointed President and CEO of Diodes Incorporated. He had been on the board since 2001, but his background was something the company desperately needed: deep semiconductor manufacturing expertise at the highest level. Before joining Diodes, Lu had served as Senior Vice President and General Manager of Worldwide Mixed-Signal and Logic Products at Texas Instruments, one of the most important roles in one of the most important semiconductor companies on earth. At TI, he had overseen all aspects of analog, mixed-signal, and logic products globally, including design, process development, manufacturing, and marketing. He had also run TI's worldwide memory business and served as President of TI Asia.

Dr. Lu brought something rare: the strategic vision of a large-company executive combined with the operational intensity of someone running a company with a fraction of the resources. He had a Ph.D. in Electrical Engineering from Texas Tech University and a B.S. from National Cheng Kung University in Taiwan. He understood the technology. He understood the Asian manufacturing ecosystem. And he understood, from his years at TI, exactly how the analog semiconductor business worked at scale. The question was whether he could apply that knowledge to a company roughly one-fiftieth the size of his former employer.

His strategy crystallized quickly. The playbook had four elements, each drawn from his experience at TI but adapted to Diodes' smaller scale and scrappier culture. First, build Diodes into a global analog and discrete semiconductor company through a combination of organic growth and disciplined acquisitions. Second, leverage Asia for manufacturing cost advantages and customer proximity, positioning the company at the epicenter of global electronics manufacturing rather than at the periphery. Third, maintain a product focus on application-specific standard products that competed on performance, time-to-market, and engineering support rather than raw price, avoiding the commodity trap that had ensnared many smaller semiconductor companies. Fourth, adopt a fab-lite manufacturing model, owning some manufacturing for cost control and supply security while partnering with foundries for products that required different process technologies or higher volumes than internal fabs could handle.

The fab-lite model deserves particular attention because it became a defining element of Diodes' strategy. In the semiconductor world, companies generally fall into three categories: integrated device manufacturers (IDMs) that design and fabricate their own chips, fabless companies that design chips but outsource all manufacturing to foundries, and fab-lite companies that own some fabrication capacity but also use external foundries. Each model has tradeoffs. IDMs have maximum control but bear the full capital cost of fabrication facilities that can cost billions of dollars. Fabless companies are asset-light but dependent on foundry capacity allocation and pricing. Fab-lite companies get flexibility, using internal fabs for high-volume products where cost control is critical and external foundries for products that require different process technologies or where demand is uncertain. For a mid-sized company like Diodes, the fab-lite model was the only viable path, providing enough manufacturing muscle to ensure supply security without the capital burden that would have overwhelmed the balance sheet.

The first major move under Lu's leadership was the acquisition of Zetex Semiconductors in 2008 for approximately $176 million. Zetex was a UK-based provider of discrete and high-performance analog semiconductor products, with particular strength in signal processing and power management. The deal brought Diodes a wafer fabrication facility in Oldham, England, along with a portfolio of higher-performance analog products and a customer base concentrated in the European and American markets. It was a significant bet for a company that had generated less than $350 million in revenue the prior year, but it reflected Lu's conviction that Diodes needed to move beyond basic discrete components and into higher-value analog products.

Meanwhile, the Asian operations were expanding rapidly, driven by Dr. Lu's conviction that proximity to customers was not optional but existential. The company built out facilities in Shanghai, Chengdu, and other Chinese cities, positioning itself close to the contract manufacturers and original equipment manufacturers that were driving the explosion in consumer electronics. China was becoming the center of gravity for electronics manufacturing, and Diodes was determined to be there in force. The economic logic was compelling on every dimension: lower labor costs for manufacturing and assembly, physical proximity to customers who could visit a Diodes facility in Shanghai in an afternoon rather than flying across the Pacific, seamless integration into the supply chain ecosystem where components flowed from Diodes' factory to the customer's assembly line in hours rather than weeks, and access to a rapidly growing pool of engineering talent trained in China's top-tier university system.

The cultural challenges were real and persistent. Managing operations across China, Taiwan, the UK, and the United States required navigating profoundly different business cultures, regulatory environments, and communication styles. Chinese operations demanded close relationships with local government officials and an understanding of the evolving regulatory landscape. Taiwanese operations required sensitivity to the island's unique political situation and business customs. UK operations operated under European labor and environmental regulations that differed significantly from Asian norms. And the corporate headquarters in the United States had to satisfy SEC reporting requirements, American governance standards, and investor expectations.

But the Taiwanese heritage of the company's ownership, combined with Dr. Lu's personal background spanning Taiwan, the United States, and his deep experience with Asian operations at TI, provided a cultural bridge that few American-listed semiconductor companies could match. Dr. Lu could conduct business in Mandarin, navigate the complexities of Greater China's business environment, and translate those realities for American investors and board members. This bicultural competency was not just a personal attribute; it was a strategic asset that permeated the organization.

The Zetex deal also illustrated a pattern that would become characteristic of Lu's acquisition strategy: buying companies that were undervalued by the market but strategically valuable to Diodes. Zetex had been struggling as a standalone company, caught between larger competitors with more resources and smaller specialists with lower cost structures. Its stock price reflected this difficulty. But within Diodes' portfolio, Zetex's products and capabilities filled specific gaps: higher-performance analog products for signal processing, a European manufacturing base that provided geographic diversification, and customer relationships in markets that Diodes had not previously served.

By the end of the decade, the business model had crystallized into something distinctive: standard products at competitive prices, fast time-to-market, local application engineering support, and a manufacturing footprint that gave customers confidence in supply security. Revenue had grown from roughly $215 million in 2005 to over $430 million in 2008-2009, and the product portfolio had expanded from basic discrete components to include higher-value analog and mixed-signal products. The company now employed thousands of people across Asia, Europe, and the Americas, with design centers in multiple countries and customer-facing offices throughout Greater China.

For context, the broader semiconductor industry was undergoing its own transformation during this period. The global financial crisis of 2008-2009 devastated demand and compressed valuations across the industry, forcing smaller companies to seek partners or acquirers and creating opportunities for those with the financial strength and strategic vision to buy. Diodes weathered the crisis better than many peers, maintaining revenue at roughly $434 million in 2009 despite the worst economic contraction since the Great Depression. The relative resilience reflected the company's diversified customer base and the essential nature of its products: even in a recession, electronic devices still needed voltage regulators, protection diodes, and signal switches.

The company was no longer a trading outfit with a fab. It was becoming a real semiconductor company with global ambitions. But the next leap would require something bigger, a transformative acquisition that would change what Diodes fundamentally was.

V. The BCD Semiconductor Acquisition: A Turning Point (2013)

In late 2012, as the global semiconductor industry was working through a cyclical downturn that had compressed valuations and made growth through acquisition suddenly affordable, Dr. Lu and his team identified a target that would fundamentally change what Diodes could become. BCD Semiconductor Manufacturing, a Shanghai-based analog integrated device manufacturer listed on NASDAQ, was available at a price that reflected the market's pessimism about the semiconductor cycle rather than the intrinsic value of the company's capabilities.

The strategic significance of BCD is easiest to grasp through an analogy. If Diodes had been a restaurant chain that only served appetizers, BCD was the acquisition that added entrees to the menu. Discrete components like diodes, transistors, and rectifiers are the appetizers of the semiconductor world: essential, ubiquitous, but individually low in value. Analog power management integrated circuits, which were BCD's specialty, are the entrees: more complex, higher in value, and stickier with customers because they require more design effort to integrate and are harder to swap out once they are designed into a product.

The deal closed in the first quarter of 2013 for approximately $151 million in cash, at eight dollars per American Depositary Share. What Diodes got was transformative: CMOS analog design expertise, a portfolio of power management ICs including DC-DC converters, linear regulators, LED drivers, and voltage references, along with a wafer fabrication facility in Shanghai and established relationships with Chinese OEMs. BCD was not a massive company, but it had exactly the capabilities that Diodes needed to move up the value chain.

For non-technical readers, it is worth pausing to explain why power management ICs are so valuable. Every electronic device runs on electricity, but the electricity coming from a battery or a wall socket is never in exactly the right form for the circuits that need it. A laptop's processor might need 1.2 volts, its memory 1.35 volts, its display backlight 20 volts, and its USB ports 5 volts, all from a single battery delivering 11.4 volts. Power management ICs are the translators that convert, regulate, and distribute electrical power to every subsystem in the device, ensuring that each circuit gets exactly the voltage and current it needs, efficiently and without generating excessive heat. They are invisible to the end user but absolutely essential to the operation of every electronic device on the planet. And because every new feature added to a device, whether it is a faster processor, a brighter screen, a better camera, or a 5G modem, typically requires its own power management circuitry, the number of power management ICs per device has grown steadily for decades.

The strategic logic of the BCD deal was elegant. Diodes already had deep relationships with the same customers who were buying BCD's products. A smartphone manufacturer that sourced protection diodes and ESD suppression chips from Diodes could now also source power management ICs. A computing OEM that bought signal switches could now buy voltage regulators. Cross-selling was not a vague hope; it was a concrete plan grounded in existing customer relationships and a complementary product portfolio.

Integration was challenging, as it always is when a mid-sized American-listed company absorbs a Chinese semiconductor manufacturer. Different engineering cultures, different management styles, different expectations about pace and process. BCD's engineers were accustomed to serving the Chinese domestic market, where speed and cost were the primary competitive weapons. Diodes needed to maintain those strengths while also elevating quality standards and broadening the customer base to include international OEMs with more demanding specifications. The engineering teams had to learn to work together across time zones, languages, and technical traditions.

But Diodes had two advantages that many acquirers lack: Dr. Lu's personal experience integrating Asian operations, honed through years of managing TI's Asia business, and the company's existing presence in Shanghai that gave it a base of understanding for Chinese business practices. The integration was not seamless, but it was effective. Within eighteen months, the combined engineering teams were collaborating on new product designs that leveraged BCD's analog expertise and Diodes' application knowledge, and the cross-selling program was delivering measurable revenue synergies.

The numbers told the story. Revenue jumped from roughly $634 million in 2012 to $827 million in 2013, a thirty percent increase that was largely attributable to BCD's contribution plus organic growth from the expanded portfolio. Gross margins began their upward journey, crossing from the high twenties toward the thirty percent threshold. More importantly, the product mix was shifting: analog power management ICs, with their higher average selling prices and stickier customer relationships, were becoming a larger share of total revenue. This mix shift would continue for nearly a decade, driving gross margin expansion from around twenty-nine percent in 2013 to over forty-one percent at the 2022 peak.

The BCD acquisition also crystallized a pattern that would become Diodes' signature move: acquire undervalued semiconductor assets during industry downturns, integrate them aggressively, cross-sell into existing customer relationships, and use the combined capabilities to compete for design wins that neither company could have won alone.

In the years immediately following the acquisition, the benefits compounded. Design teams from BCD and legacy Diodes began collaborating on products that combined discrete and analog IC expertise, creating integrated solutions that were more attractive to customers than either company's standalone offerings. The Shanghai fab was optimized and its utilization increased, improving unit economics. And the relationships with Chinese OEMs that BCD brought opened doors for Diodes' broader product portfolio, creating a flywheel of cross-selling that accelerated with each new design win.

It was a playbook that Dr. Lu would execute twice more in the years ahead, each time on a larger scale and with greater strategic ambition.

VI. The Fabless Transition & Portfolio Evolution (2010-2015)

The years following the BCD acquisition saw Diodes evolve from a company that made things into a company that engineered solutions. The distinction matters. Making things, in the semiconductor world, means fabricating wafers, packaging chips, and testing them for quality. Engineering solutions means understanding a customer's design challenge, whether it is power delivery in a laptop, signal routing in a server, or voltage protection in an automotive module, and providing a component that solves that specific problem efficiently, reliably, and at a competitive price.

Diodes' product line expanded significantly during this period. The company moved from simple diodes and transistors into complex power management ICs, MOSFET transistors for power switching, interface ICs for data communication, and timing solutions for clock generation and distribution. Each new product category represented a deeper engagement with customers and a higher average selling price, even though any individual chip might still cost less than a dollar.

The manufacturing strategy evolved as well. Rather than building more fabs, Diodes adopted a flexible hybrid model. The company kept its owned fabrication facilities for high-volume discrete products where cost control was paramount and process stability was well established. For newer, more complex products, it partnered with external foundries, including the largest and most capable fabrication houses in the world, to access process technologies that it could not economically develop in-house. This fab-lite approach gave Diodes the best of both worlds: the cost advantages and supply security of owned manufacturing for its bread-and-butter products, and the technological flexibility of foundry partnerships for higher-value products that required different or more advanced process nodes.

The underlying market trend was favorable. The "analog everywhere" megatrend, the proliferation of sensors, power management, and connectivity in every electronic device, meant that the total addressable market for Diodes' products was growing steadily even as individual device prices declined. A smartphone in 2010 might have contained twenty or thirty analog and discrete components. By 2015, that number had roughly doubled, driven by additional sensors, more complex power management requirements, faster charging, better cameras, and more sophisticated wireless connectivity.

Diodes was winning in what might be called the middle market of semiconductors. It was not competing for the processor socket, the memory slot, or the radio frequency front end, the high-profile, high-value positions occupied by Qualcomm, Samsung, or Broadcom. It was competing for the fifty other semiconductor components in each device: the voltage regulators, the signal switches, the ESD protection diodes, the LED drivers, the clock generators. Individually, none of these components was worth much. Collectively, they represented significant revenue, and winning a design slot in a popular product meant shipping millions of units at stable margins for the product's entire lifecycle.

Revenue grew from roughly $634 million in 2012 to $849 million in 2015, with the product mix steadily shifting toward higher-value analog and mixed-signal components. Gross margins, which had been in the mid-to-high twenties a few years earlier, crossed into the low thirties.

The customer base diversified across five end markets: computing, consumer, communications, automotive, and industrial. This five-pillar structure reduced dependence on any single product category or customer segment and provided natural hedges against cyclical weakness. When smartphones slowed, automotive picked up. When consumer demand softened, industrial automation continued. No single end market accounted for enough revenue to sink the company if it turned down.

The quiet accumulation of design wins across thousands of applications was building a business that was far more resilient and defensible than it appeared from the outside. Each design win was small, but the aggregate effect was a portfolio of revenue streams diversified across products, customers, geographies, and end markets, with natural hedges against cyclical weakness in any single segment. It was, in a sense, the semiconductor equivalent of an index fund: broad exposure to the growth of electronics, with diversification reducing the volatility of any individual position.

The economics of this model reward patience and consistency rather than breakthrough moments. A design win for a voltage regulator in a new laptop model might generate a few hundred thousand dollars in annual revenue. But win that same socket across five laptop models from three different manufacturers, and the revenue becomes meaningful. Win similar sockets in servers, in automotive modules, in industrial controllers, and in consumer devices, and the company generates billions in aggregate revenue from individual positions that are too small for any competitor to target for displacement. This is the paradox of Diodes' business: its competitive advantage lies partly in the fact that no individual revenue stream is large enough to attract aggressive competitive attack.

VII. The Pericom Acquisition: Entering High-Speed Connectivity (2015)

On September 3, 2015, Diodes announced the acquisition that would mark its second major inflection point: the purchase of Pericom Semiconductor Corporation for approximately $413 million in cash, at $17.75 per share. If the BCD deal had been about adding power management to the portfolio, the Pericom deal was about adding connectivity and timing, two product categories that were becoming increasingly critical as data rates accelerated and digital systems grew more complex.

Pericom was a Milpitas, California-based company that specialized in high-speed signal integrity, switching, bridging, and timing solutions. Its products supported the alphabet soup of modern digital connectivity protocols: USB, PCI Express, SATA, SAS, DisplayPort, HDMI, Gigabit Ethernet, and the then-emerging USB Type-C standard. These were the chips that sat between processors and the outside world, ensuring that data moved quickly and reliably across cables, connectors, and circuit board traces.

To make this concrete for non-engineers: when you plug a USB cable into your laptop, the data does not magically flow from one device to the other. The electrical signals traveling through the cable degrade over distance, pick up noise from nearby circuits, and arrive at the other end slightly distorted. Signal integrity chips clean up these signals, amplify them, and ensure they arrive in the correct form for the receiving device to interpret. Timing chips generate the precise clock signals that tell both devices when to send and receive data, down to billionths of a second. Without these chips, your USB connection would be unreliable, your video output would flicker, and your network connection would drop packets. They are the unsung infrastructure of digital communication, and every interface on every device requires them.

To understand why this acquisition mattered strategically, consider what was happening in the computing and data center markets in the mid-2010s. Cloud computing was exploding. Every major technology company was building or expanding data centers. Each server rack contained dozens of servers, each server contained multiple high-speed interfaces, and each interface required signal conditioning, clock generation, and protocol switching chips. The total addressable market for these components was growing rapidly, and Pericom had a strong position in several key niches.

The strategic logic for Diodes was compelling on multiple levels.

First, it gave the company a product portfolio that was directly relevant to one of the fastest-growing segments of the semiconductor market. Data centers were not just getting bigger; they were getting faster, with each new generation of servers requiring higher-speed interfaces and more precise timing. Every upgrade to a new PCIe generation, every adoption of a faster USB standard, every deployment of higher-bandwidth networking created demand for new signal integrity and timing chips.

Second, it created powerful synergies with the existing power management and discrete product lines. A customer designing a server motherboard needed both power management ICs and connectivity chips, and buying both from the same vendor simplified the supply chain, reduced qualification costs, and gave Diodes more leverage in design win competitions. The bundle effect was real: winning a power management slot on a server board gave the Diodes sales team a relationship that could be leveraged to compete for the connectivity and timing sockets on the same board.

Third, Pericom's timing products, which included crystal oscillators and clock generation ICs, addressed a product category that was essential to virtually every electronic system but was not well served by the largest semiconductor companies, which tended to focus on higher-revenue product lines. Timing is one of those categories that engineers care about deeply and that procurement teams barely notice, making it an ideal niche for a mid-sized company that competes on engineering support rather than brand.

Integration required careful execution and cultural sensitivity. Pericom's engineering culture was rooted in Silicon Valley's design-centric ethos. The company had been founded by engineers who prized technical elegance and innovation. Diodes' culture, by contrast, was more manufacturing and operations oriented, focused on cost efficiency, supply chain reliability, and customer responsiveness. These are not incompatible values, but they create different organizational priorities and different definitions of success. An engineer at Pericom might define success as designing the most technically advanced signal integrity chip in the market. An engineer at Diodes might define success as getting a good-enough product to market six months before the competition at a lower cost.

Bridging those cultures was not automatic. But Dr. Lu and his management team had learned lessons from the BCD integration about how to combine engineering organizations without destroying the creative energy that made the acquired company valuable in the first place. The product complementarity was strong enough that revenue synergies materialized relatively quickly, as Diodes' sales teams in Asia could immediately begin offering Pericom's connectivity products to existing customers who were already buying discrete and power management components.

The market, characteristically, took time to appreciate the strategic value of the deal. Wall Street's initial reaction was skeptical. At $413 million, the Pericom acquisition represented nearly half of Diodes' annual revenue at the time, a large bite for a mid-cap company to swallow. Diodes' stock had declined roughly sixteen percent in 2015, reflecting both the semiconductor downturn and investor uncertainty about the company's ability to digest such a significant acquisition. But the subsequent years validated the strategy. Revenue climbed from $849 million in 2015 to $942 million in 2016 and crossed the one-billion-dollar mark for the first time in 2017. More importantly, Diodes was now positioned in a product category, high-speed connectivity, that would prove increasingly relevant as data centers expanded, AI workloads emerged, and the bandwidth demands of modern computing accelerated.

The Pericom acquisition also reflected an important evolution in Diodes' M&A strategy. The BCD deal had been about acquiring manufacturing capability and an existing product portfolio in China. The Pericom deal was about acquiring intellectual property, design expertise, and market position in a technology-defined product category. The common thread was the same: identify assets that are undervalued relative to their strategic potential, acquire them, integrate them into Diodes' commercial and manufacturing infrastructure, and use the combination to compete for design wins that neither company could have won alone.

The post-acquisition years proved the thesis handsomely. Pericom's products became some of the fastest-growing categories in Diodes' portfolio, as the explosion in USB Type-C adoption, the buildout of hyperscale data centers, and the proliferation of high-speed interfaces in automotive infotainment systems all drove demand for exactly the types of signal integrity and timing chips that Pericom had designed. By 2018, Diodes had crossed $1.2 billion in annual revenue, with connectivity and timing products representing a growing share of the mix and contributing to the steady improvement in gross margins that distinguished the company's P&L trajectory from its commodity competitors. Revenue hit $1.25 billion in 2019, and while the stock had lagged for years after the acquisition, the seventy-six percent share price surge in 2019 suggested that the market was finally beginning to price in the full strategic value of what Dr. Lu had assembled.

VIII. The Lite-On Semiconductor Acquisition: Scale & Automotive Push (2020)

The third and largest acquisition in Diodes' modern history came from a direction that was both surprising and, in retrospect, almost inevitable. Lite-On Semiconductor Corporation, the Taiwan-listed company whose corporate parent had originally invested in Diodes back in 1990, became the target of Diodes' biggest deal. The acquisition was announced in August 2019 and, after an extended regulatory approval process, finally closed in November 2020, for approximately $446 million in cash.

There was a certain poetic symmetry to the transaction that no fiction writer could have improved upon. Thirty years earlier, Lite-On's parent company had acquired a stake in a small American semiconductor trader, providing the capital and Asian manufacturing connections that had made Diodes' transformation possible. The student had become the master: the company that once depended on Lite-On for manufacturing capability was now acquiring its semiconductor subsidiary outright, bringing the relationship full circle and dramatically expanding its manufacturing footprint and product portfolio in the process.

The deal also had a practical logic that went beyond sentimentality. Diodes and Lite-On Semiconductor had been operating in parallel in many of the same markets for years, with some overlapping products and some complementary ones. Combining them eliminated redundant overhead, consolidated purchasing power, and created a single entity with the scale to compete more effectively against larger rivals in the automotive and industrial markets.

What Diodes got was substantial: wafer fabrication facilities in Keelung and Hsinchu, Taiwan; assembly and testing operations in Zhongli, Taiwan; a leadership position in glass-passivated bridges and rectifiers; and, critically, a significant portfolio of automotive and industrial-qualified products. Lite-On Semiconductor had spent years building relationships with automotive Tier 1 suppliers and qualifying its products for the demanding reliability standards of the automotive industry, a process that typically takes two to five years for each product and creates significant switching costs once a component is designed into a vehicle platform.

The automotive angle was the strategic centerpiece. By 2019, the automotive industry's electrification trajectory was becoming clear. Electric vehicles require two to three times more semiconductor content than internal combustion engine vehicles, with particularly strong demand for power semiconductors. To understand why, consider what happens inside an EV: a battery pack delivers high-voltage DC power, but the electric motor needs AC power at varying frequencies to control speed and torque. Converting between these requires power semiconductor switches, primarily MOSFETs and IGBTs, that turn on and off thousands of times per second to shape the electrical waveform. Gate drivers tell these switches when to turn on and off. Bridge rectifiers convert power in the opposite direction, from AC to DC, for regenerative braking and onboard chargers. Every stage of the power conversion chain, from battery to motor and back, requires multiple power semiconductor devices. Multiply that by the number of electric motors, the battery management system, the onboard charger, the DC-DC converter for low-voltage accessories, and the various ADAS sensors and control modules, and it becomes clear why an EV contains dramatically more semiconductor content than a traditional vehicle.

Lite-On Semiconductor manufactured exactly these types of components, and every major automotive OEM planning electrified lineups was looking for qualified suppliers. The component suppliers that were already qualified and shipping were in pole position to capture the coming demand surge.

The timing of the deal's close, November 2020, meant that Diodes was integrating a major acquisition in the middle of the COVID-19 pandemic, which was simultaneously disrupting supply chains and supercharging demand for computing and consumer electronics. The integration was, by all accounts, the most complex in the company's history. Combining operations across Taiwan, China, the UK, and the United States during a global pandemic required extraordinary logistical and managerial effort.

But the strategic payoff was significant. Diodes emerged from the integration as a fundamentally different company. The manufacturing footprint now included wafer fabrication in six locations across four countries: the US (South Portland, Maine, acquired later in 2022), the UK (Oldham, from Zetex), China (Shanghai and Wuxi, from BCD and organic growth), and Taiwan (Keelung and Hsinchu, from Lite-On). Assembly and test operations spanned five locations across China, Taiwan, and Germany. The product portfolio covered the full spectrum: discrete semiconductors, analog power management ICs, connectivity and timing solutions, and automotive-qualified power components. Revenue surged from $1.25 billion in 2019 to $1.81 billion in 2021, a forty-seven percent increase. The growth reflected three overlapping forces: the Lite-On contribution adding scale, post-pandemic demand recovery driving volumes, and the supply-constrained pricing environment that benefited the entire semiconductor industry by shifting pricing power from buyers to sellers for the first time in years.

The three major acquisitions, BCD in 2013, Pericom in 2015, and Lite-On Semiconductor in 2020, had collectively transformed Diodes from a five-hundred-million-dollar company focused on basic discrete components into a nearly-two-billion-dollar company with a diversified portfolio spanning power management, high-speed connectivity, timing, and automotive-qualified power semiconductors. Total M&A spending across these three deals was roughly one billion dollars. The company they built was worth several times that amount. The playbook had worked.

IX. The Smartphone Decline & Portfolio Rebalancing (2018-2020)

Every growth story encounters headwinds, and for Diodes, the late 2010s brought a convergence of challenges that tested the company's resilience and forced a strategic recalibration. The global smartphone market, which had been the engine of growth for the entire analog semiconductor industry for a decade, hit a wall. Unit sales plateaued in 2017 and began declining in 2018, as upgrade cycles lengthened and markets in China and India matured. For a company that derived a significant portion of its revenue from consumer electronics, this was a structural concern, not just a cyclical blip.

Simultaneously, the US-China trade war escalated dramatically in 2018 and 2019, introducing a new and unpredictable variable into Diodes' business. The company was uniquely exposed: American-listed but with the majority of its manufacturing in China and Taiwan, selling predominantly to Asian customers, and heavily dependent on the free flow of components across borders. Tariffs imposed by both the US and Chinese governments increased costs, disrupted supply chains, and created deep uncertainty among customers.

The mechanics of the trade war's impact on Diodes were subtle but pervasive. Chinese OEMs began dual-sourcing components to reduce dependence on American-affiliated suppliers, even for commodity parts that were not subject to export controls. Some customers accelerated purchases to build buffer inventory ahead of potential tariff increases, creating artificial demand in some quarters followed by hangovers in others. The constant uncertainty made demand forecasting, already difficult in the semiconductor industry, nearly impossible. Diodes' management had to navigate a business where the rules could change with a single presidential tweet.

Diodes' response was characteristically methodical. Rather than making dramatic strategic pivots or issuing alarming press releases, management accelerated the portfolio rebalancing that had been underway for years. The shift was subtle but decisive: R&D resources were redirected toward automotive and industrial product development, sales teams were incentivized to pursue higher-value design wins in computing and automotive rather than chasing high-volume consumer sockets, and marketing materials increasingly emphasized automotive qualification and industrial reliability rather than consumer features.

The automotive push was already in motion through the Lite-On acquisition, but the urgency increased as it became clear that consumer electronics could no longer be relied upon as the primary growth engine.

Then COVID-19 arrived.

The pandemic initially looked like another body blow for a company already navigating trade war fallout and smartphone saturation. Demand collapsed across most end markets in the first and second quarters of 2020. Factories in China shut down for weeks. Consumer spending contracted sharply. Supply chains seized up as ports closed and freight costs spiked. Revenue dipped to $1.23 billion for the full year, down modestly from $1.25 billion in 2019. But the recovery, when it came, was extraordinary. The work-from-home wave drove explosive demand for laptops, monitors, webcams, and networking equipment. The gaming console cycle accelerated. And the automotive industry, after shutting production lines in the spring, came roaring back in the second half of the year, only to discover that the semiconductor supply chain could not keep up.

Management's navigation of this period demonstrated the operational discipline that Dr. Lu had instilled over fifteen years. Cost controls were tightened during the downturn without gutting the engineering or sales organizations, a critical distinction that many semiconductor companies get wrong during recessions. The temptation to cut deeply into R&D and customer-facing teams is strong when revenue is declining, but the damage to design win pipelines and customer relationships takes years to repair. Diodes maintained its engineering investment and kept application engineers in the field, ensuring that when demand recovered, the company would be positioned to capture growth rather than scrambling to rebuild capabilities. Inventory was managed carefully to maintain supply to key customers, building loyalty during a period when many competitors were struggling with allocation and lead times. And the Lite-On integration continued on schedule despite the pandemic's logistical challenges, a testament to the organizational muscle that Diodes had built through previous acquisitions.

The stock market reflected the shifting narrative. After languishing in the thirty-dollar range for much of 2018, Diodes shares surged seventy-six percent in 2019, reaching the low sixties, as investors began to price in the Lite-On acquisition's automotive potential and the company's improving end-market mix. The rally continued through 2020, with shares climbing another twenty-three percent despite the pandemic, and then accelerated dramatically in 2021 as the semiconductor supply shortage turned every chip company into a growth story. By December 2021, Diodes reached an all-time high of $112.42, giving the company a market capitalization approaching five billion dollars, twenty times the level a decade earlier.

By the end of 2020, the investor narrative had fundamentally shifted. The company was no longer primarily a consumer-exposed analog play vulnerable to smartphone cycles and Chinese competition. It was being recognized as a diversified analog and discrete semiconductor company with growing automotive and industrial exposure, a broad manufacturing footprint, and a management team that had navigated multiple crises successfully. The portfolio rebalancing was working, even if it had been forced as much by external pressure as by internal strategy.

X. The Modern Era: EV Boom, Industrial Renaissance & AI Infrastructure (2020-2026)

The years following the pandemic transformed Diodes from a recovery story into a growth story, as several secular trends converged to create what management has described as the strongest design win environment in the company's history. Revenue surged to $1.81 billion in 2021 and crossed the two-billion-dollar mark in 2022, the company's all-time peak, driven by the combination of strong underlying demand and a supply-constrained pricing environment that lifted margins across the semiconductor industry.

Gross margins told the most dramatic part of the story during this period. From roughly thirty-one percent in 2017, they climbed steadily to over thirty-six percent by 2019, then to thirty-seven percent in 2021, and reached an extraordinary forty-one percent in 2022. That represented roughly 1,600 basis points of expansion over a decade, a remarkable transformation for a company that had been viewed as a commodity semiconductor player. The margin expansion reflected the cumulative effect of every strategic decision over the prior fifteen years: the shift from basic discretes to higher-value analog ICs, the growing automotive and industrial mix, the fab-lite manufacturing model, and the pricing discipline enabled by a portfolio of application-specific products rather than generic commodities.

Automotive electrification proved to be the powerful tailwind that Diodes had positioned itself to capture. Electric vehicles require a dramatically larger semiconductor bill of materials than traditional combustion vehicles. The power conversion chain alone, from battery to motor, requires MOSFETs, IGBTs, gate drivers, voltage regulators, current sensors, and protection devices at every stage. Beyond the powertrain, EVs also need more content for thermal management systems, advanced driver assistance systems, infotainment displays, and charging infrastructure. Diodes' automotive content per vehicle grew from roughly $160 at the end of 2023 to $239 by the end of 2025, reflecting both increasing semiconductor content in each vehicle and Diodes' expanding share of that content.

The industrial end market experienced its own renaissance, driven by factory automation, renewable energy systems, building management, and the Internet of Things. The convergence of these trends created what industry analysts have described as "Industry 4.0," the digitization and automation of manufacturing and infrastructure that requires embedding intelligence and connectivity into every piece of industrial equipment.

Consider a modern solar inverter, a device that converts the DC power from solar panels into the AC power used by the electrical grid. A single inverter can contain dozens of semiconductor components: MOSFETs and IGBTs for power conversion, gate drivers to control the switches, voltage and current sensors for monitoring, a microcontroller for system management, communication interfaces for connecting to the grid operator's monitoring system, and protection devices to handle lightning strikes and grid faults. Diodes can supply many of these components from its own portfolio, and the long product lifecycle of industrial equipment, often ten to fifteen years, means that design wins generate revenue for far longer than in consumer applications. Diodes' broad portfolio, spanning discrete power devices, analog ICs, and timing solutions, was well suited to these applications, which prioritize reliability and long product lifecycles over cutting-edge performance.

But perhaps the most unexpected growth vector emerged from the AI infrastructure buildout. When NVIDIA, AMD, and the hyperscalers began deploying AI training clusters consuming hundreds of megawatts of power, the demand for supporting semiconductors surged alongside the demand for GPUs. An AI server does not just need a powerful GPU; it needs dozens of voltage regulators to deliver clean, stable power to the GPU, high-speed signal integrity chips to maintain data fidelity across the PCIe and CXL interconnects, clock generators to synchronize the entire system, and protection devices to guard against electrostatic discharge and power transients. These are precisely the categories that Diodes had bolstered through the Pericom and BCD acquisitions.

Computing revenue grew twenty-five percent in 2025, primarily driven by AI server-related applications, making it Diodes' largest end market segment at twenty-eight percent of product revenue. The company's content per AI server platform reached $103 by year-end 2025, and the trajectory was upward as AI server architectures grew more complex and power-hungry. Management allocated forty percent of new product introductions in 2025 to automotive applications, but the AI infrastructure opportunity was clearly emerging as a strategic priority for the design teams as well.

The cycle turned sharply in 2023-2024, as it always does in semiconductors. The boom-bust pattern is one of the defining characteristics of the semiconductor industry, driven by the bullwhip effect: when demand is strong, customers and distributors build inventory buffers, amplifying the demand signal to manufacturers and causing overproduction. When demand softens, those buffers are consumed before new orders are placed, causing a demand cliff that is steeper than the underlying end-market weakness would suggest. The pandemic-era supply shortage exaggerated this pattern to an extreme degree, as customers who had been unable to get chips for eighteen months double- and triple-ordered to build safety stock, creating an inventory overhang that took nearly two years to digest.

Diodes was not immune. Revenue fell from $2.0 billion in 2022 to $1.66 billion in 2023 and further to $1.31 billion in 2024, a cumulative decline of roughly thirty-five percent from peak to trough. To put that in perspective, the decline was more severe than the 2008-2009 downturn in both absolute and percentage terms, reflecting the exceptional magnitude of the preceding boom. Gross margins compressed from a record above forty-one percent at the peak to roughly thirty-one percent at the trough, as fixed manufacturing costs associated with six owned fabs were spread over significantly lower volumes. Operating leverage, the same force that had magnified profitability on the way up, now magnified the pain on the way down.

The downturn tested Diodes' operational model. With multiple owned fabs running below capacity, the cost structure that had been an advantage during the boom became a burden during the bust. The fab-lite model, which gives Diodes flexibility to shift between internal and external manufacturing, helped somewhat: the company could reduce outsourced wafer purchases more quickly than it could idle owned facilities. But management responded with the same operational discipline that had become the company's hallmark: targeted cost controls, careful inventory management, and continued investment in automotive and industrial design wins that would pay off when the cycle turned.

One strategic move during this period deserves particular attention. In June 2022, even as the cycle was beginning to crack, Diodes completed the acquisition of onsemi's South Portland, Maine wafer fabrication facility, a 200mm fab with 85,000 square feet of clean room space. The financial terms were not disclosed, but the strategic rationale was clear: add manufacturing capacity in the United States, diversifying the geographic base away from Asia and positioning the company for the growing demand for domestically manufactured semiconductors in automotive and defense applications. The South Portland facility, known internally as SPFAB, gave Diodes its first significant US-based manufacturing capability since the FabTech days and signaled management's awareness that the geopolitical landscape for semiconductor manufacturing was shifting.

Recovery began in the second half of 2024, and 2025 saw revenue rebound to $1.48 billion, up thirteen percent year over year. The recovery was broad-based, with automotive revenue growing twenty-four percent, computing up twenty-five percent driven by AI servers, and industrial up thirteen percent. Channel inventory, which had been bloated during the downturn, normalized to the company's target range of eleven to fourteen weeks, setting the stage for a cleaner demand signal heading into 2026.

The fourth quarter of 2025 was particularly strong, with revenue of $391.6 million representing fifteen percent year-over-year growth. Non-GAAP adjusted earnings per share of $0.34 beat consensus estimates of $0.26, triggering a twenty-six percent surge in the stock price. More importantly, management guided first-quarter 2026 revenue to approximately $395 million, representing nineteen percent year-over-year growth and described as "significantly better than typical seasonality," suggesting that the recovery was accelerating. Book-to-bill ratios turned positive, and management described the backlog and bookings environment as "strong" on multiple occasions during the earnings call.

One of the most significant recent developments was the leadership transition in May 2025, when Gary Yu was appointed CEO, succeeding Dr. Lu after twenty years at the helm. Yu had joined Diodes in 2008, brought in as part of the Zetex acquisition integration, and rose through the ranks to become one of the most operationally experienced executives in the company. He was promoted to President in January 2024 as part of a deliberate multi-year succession plan, giving him more than a year to prepare for the top role before formally assuming it.

Dr. Lu remained as Chairman of the Board, providing strategic counsel and serving as the principal liaison between management and directors. It was a smooth transition by semiconductor industry standards, reflecting the institutional depth that Dr. Lu had built over two decades. The semiconductor industry has numerous examples of founder or long-tenured CEO transitions that went badly, disrupting strategy and destroying shareholder value. Dr. Lu's approach, cultivating an internal successor over many years and remaining involved as Chairman, represents a thoughtful model for managing the handoff. Management has outlined ambitious targets for the next phase: returning to two billion dollars in revenue with gross margins of thirty-five percent or better, generating non-GAAP earnings per share above four dollars, all within roughly three years. The longer-term vision extends to $2.5 billion in revenue at forty percent gross margins.

XI. The Diodes Playbook: How They Compete

To understand how Diodes competes against rivals that are five to ten times its size, it helps to think about the analog semiconductor market as fundamentally different from the digital semiconductor market that dominates headlines. In digital, the game is about raw performance: faster processors, more transistors, smaller nodes. The winners are companies like NVIDIA, AMD, and Apple that can design the most advanced chips and manufacture them at the most advanced fabrication nodes. Scale matters enormously, and the market tends toward oligopoly.

Analog is a different sport entirely. Think of digital semiconductors as Formula 1 racing, where the fastest car wins, and analog as a logistics company, where the winner is not the one with the fastest truck but the one that delivers the right package to the right place at the right time, every time, at a competitive price. In analog, no single product generates massive revenue. Instead, revenue comes from tens of thousands of product variants sold to thousands of customers across dozens of applications. Success depends on breadth, reliability, engineering support, and operational efficiency rather than breakthrough innovation.

This distinction is crucial for understanding why Diodes can exist profitably alongside companies many times its size. Texas Instruments, the dominant analog semiconductor company, generates roughly seventeen billion dollars in annual revenue from an estimated four hundred thousand products. But even TI cannot be everywhere. The analog market is so fragmented, with so many niche applications and customer-specific requirements, that no single company can serve every customer in every geography with optimal responsiveness. Diodes thrives in the gaps, particularly in Asia, where its local engineering support and rapid response times give it an advantage over larger competitors whose decision-making processes are slower and whose attention is naturally drawn to larger revenue opportunities.

Diodes' competitive strategy rests on several interconnected pillars. The first is disciplined M&A. The three transformative acquisitions were not impulsive bets but carefully targeted moves to acquire specific capabilities, customer relationships, and manufacturing assets at valuations that reflected cyclical distress rather than intrinsic value. The company spent roughly one billion dollars on acquisitions over a decade and built a business worth several times that amount. The pattern was consistent: identify undervalued assets during industry downturns, integrate them aggressively, and cross-sell into existing customer relationships.

The second pillar is fast-follower innovation. Diodes does not typically pioneer new product categories or process technologies. Instead, it watches the market, identifies product categories where demand is established but the market is underserved by smaller, more responsive competitors, and develops competitive products with rapid time-to-market. In 2025 alone, the company introduced over 650 new products, with forty percent targeted at automotive applications. This is not the bleeding edge; it is the rapid and reliable delivery of proven technologies in the form factors and specifications that customers need.

The third pillar is geographic leverage. With roughly eighty-five percent of its employees in Asia and seventy-eight percent of revenue coming from the region, Diodes is effectively an Asian semiconductor company with a US listing. This gives it cost advantages in manufacturing and engineering, proximity to the largest and fastest-growing electronics markets in the world, and deep relationships with the contract manufacturers and OEMs that build the majority of the world's consumer electronics, computing hardware, and increasingly, automotive components.

The fourth pillar is portfolio breadth. Having thousands of products across discrete, analog, connectivity, and timing categories creates natural cross-selling opportunities and makes Diodes a more useful supplier to customers who want to consolidate their component supply chains. A customer designing a new product can source power management, signal switching, ESD protection, voltage regulation, clock generation, and interface chips from a single vendor, simplifying procurement, qualifying fewer suppliers, and giving Diodes multiple shots at winning design slots on each new platform.

The fifth pillar, and perhaps the least appreciated, is customer intimacy. In analog semiconductors, the design-in process is inherently collaborative. Customers need application engineers who understand their specific design challenges and can recommend the right components, provide reference designs, and troubleshoot integration issues. Diodes invests heavily in local application engineering support, particularly in Asia, creating relationships that generate repeat business and early visibility into new design opportunities.

Capital allocation has historically prioritized M&A and organic R&D over shareholder returns. The company has never paid a dividend and only recently initiated a stock repurchase program, with $33.8 million in buybacks during 2025 under a $100 million authorization announced in May 2025. This reflects a growth-oriented mindset that distinguishes Diodes from some of its larger competitors. Texas Instruments, by contrast, returns virtually all of its free cash flow to shareholders through dividends and buybacks, a strategy that rewards current shareholders but limits the capital available for acquisitions. Diodes' approach preserves optionality: the balance sheet, which carried roughly $382 million in cash and short-term investments against only $56 million in total debt at the end of 2025, provides firepower for the next opportunistic acquisition.

The capital expenditure philosophy is similarly disciplined, with a target range of five to nine percent of revenue. Actual spending in 2025 was $78.4 million, or 5.3% of revenue, at the low end of the range, reflecting management's restraint during the downturn. As the cycle recovers and the company works to bring more production in-house from external foundries, particularly into the South Portland fab, capital spending will likely move toward the higher end of the range.

What does not work as well is brand recognition and pricing power. Diodes is not a household name in the semiconductor industry, let alone among end consumers. Purchasing decisions are driven by specifications, price, availability, and engineering support rather than brand loyalty. This limits pricing power and makes the company vulnerable to competition from rivals who can match its specifications at lower prices or with better supply terms.

There is also a myth versus reality worth addressing. The consensus narrative frames Diodes as a "commodity semiconductor company," implying that its products are interchangeable with competitors' and that the business has no pricing power. The reality is more nuanced. While many of Diodes' products are indeed standard parts with pin-compatible alternatives, the company increasingly competes on application-specific standard products that are optimized for particular use cases. A voltage regulator designed specifically for the power rail of a DDR5 memory module, or a signal switch optimized for the mux/demux requirements of a USB Type-C port, is not truly interchangeable with a generic alternative, even if both meet the same basic electrical specifications. The engineering effort required to optimize for specific applications creates differentiation that is not visible from product datasheets alone. Additionally, in automotive and industrial applications, the qualification and reliability testing that Diodes has invested in creates real switching barriers, even for functionally equivalent parts. The commodity perception understates the stickiness of the business in its highest-value segments.

XII. Porter's Five Forces & Hamilton's Seven Powers Analysis

Competitive Landscape

The analog and discrete semiconductor market where Diodes competes is one of the most fragmented and competitive segments of the semiconductor industry. Texas Instruments dominates with roughly sixteen to seventeen billion dollars in annual revenue and an estimated four hundred thousand products. Infineon, ON Semiconductor, STMicroelectronics, NXP, Renesas, and Analog Devices each have annual revenues ranging from seven to seventeen billion dollars. Diodes, at roughly $1.5 billion, is a mid-tier player competing against companies with far greater resources, broader product portfolios, and stronger brand recognition.

The threat of new entrants is moderate. Building a semiconductor company from scratch requires significant capital, deep technical expertise, and multi-year qualification cycles with customers, particularly in automotive and industrial markets where reliability standards are stringent. However, the fabless model has lowered barriers compared to the era when every semiconductor company needed its own fabrication facilities. A well-funded startup with strong design talent can access foundry manufacturing and compete in specific niches without the capital burden of owning fabs. The most significant barrier to entry is not manufacturing but the accumulated design-in relationships and product qualification history that incumbents like Diodes have built over decades.

Supplier bargaining power presents a nuanced picture. Diodes depends on external foundries for a portion of its wafer production, and concentration among leading foundries like TSMC gives those suppliers meaningful leverage. The 2020-2022 semiconductor shortage illustrated this vulnerability vividly: foundry capacity was allocated to the highest-priority customers, and mid-tier companies like Diodes sometimes found themselves behind larger customers in the queue.

However, Diodes' focus on mature process nodes, rather than cutting-edge manufacturing, provides more foundry options than companies requiring the latest fabrication technology. Additionally, Diodes' owned fabrication facilities in the US, UK, China, and Taiwan provide a hedge against foundry dependence and give the company flexibility to shift production between internal and external sources as economics and capacity dictate.

Buyer bargaining power is high. Large OEMs and contract manufacturers have significant leverage in pricing negotiations, and the commodity perception of many analog and discrete components limits Diodes' ability to command premium pricing. However, the sheer breadth of the product portfolio across thousands of customers and applications provides meaningful diversification. No single customer accounts for a dangerous concentration of revenue. Moreover, switching costs in automotive and industrial applications are substantially higher than in consumer markets, as changing a component supplier in an automotive platform requires extensive requalification, validation, and potentially recertification.

The threat of substitutes is moderate to low. Analog functionality is, in many cases, irreplaceable by digital alternatives. Power must be converted, signals must be conditioned, and circuits must be protected from electromagnetic interference and electrostatic discharge, regardless of how much digital processing improves. There is an ongoing trend toward integrating analog functions into larger system-on-chip devices, but this integration faces diminishing returns as analog circuits behave differently from digital circuits and often benefit from being manufactured on different, more mature process nodes. Wide-bandgap semiconductors like silicon carbide and gallium nitride represent potential substitutes for some power management applications, but Diodes has begun developing its own SiC products, positioning these as opportunities rather than pure threats.

Competitive rivalry is the most intense of the five forces and the defining reality of Diodes' business. The market is crowded with well-capitalized, technically capable competitors fighting for design wins across the same end markets. Texas Instruments alone has an analog product catalog that dwarfs Diodes' entire portfolio, and its direct sales force and proprietary manufacturing give it structural cost advantages that are difficult to match.

Price competition is fierce in standard product categories, and the long product lifecycles typical of analog semiconductors mean that competitive positions, once established, are durable but also difficult to displace. A design win for a competitor on a high-volume automotive platform can lock Diodes out of that revenue stream for the five to eight year production run of the vehicle. Conversely, Diodes' own design wins create similar barriers against displacement. Differentiation comes primarily through service quality, time-to-market, application support, and the breadth of the product portfolio rather than through technological superiority.

Hamilton's Seven Powers

Applying Hamilton Helmer's framework reveals a company with moderate but real competitive advantages in specific areas. Scale economies are present but not dominant. Diodes' portfolio of thousands of products, global manufacturing footprint, and broad distribution network create procurement and operational efficiencies, but the company is not large enough to achieve winner-take-all scale in any single product category. Network effects are effectively absent, as component businesses do not exhibit the demand-side increasing returns that characterize platform businesses.