D.R. Horton: Building America, One Home at a Time

I. Introduction & Cold Open

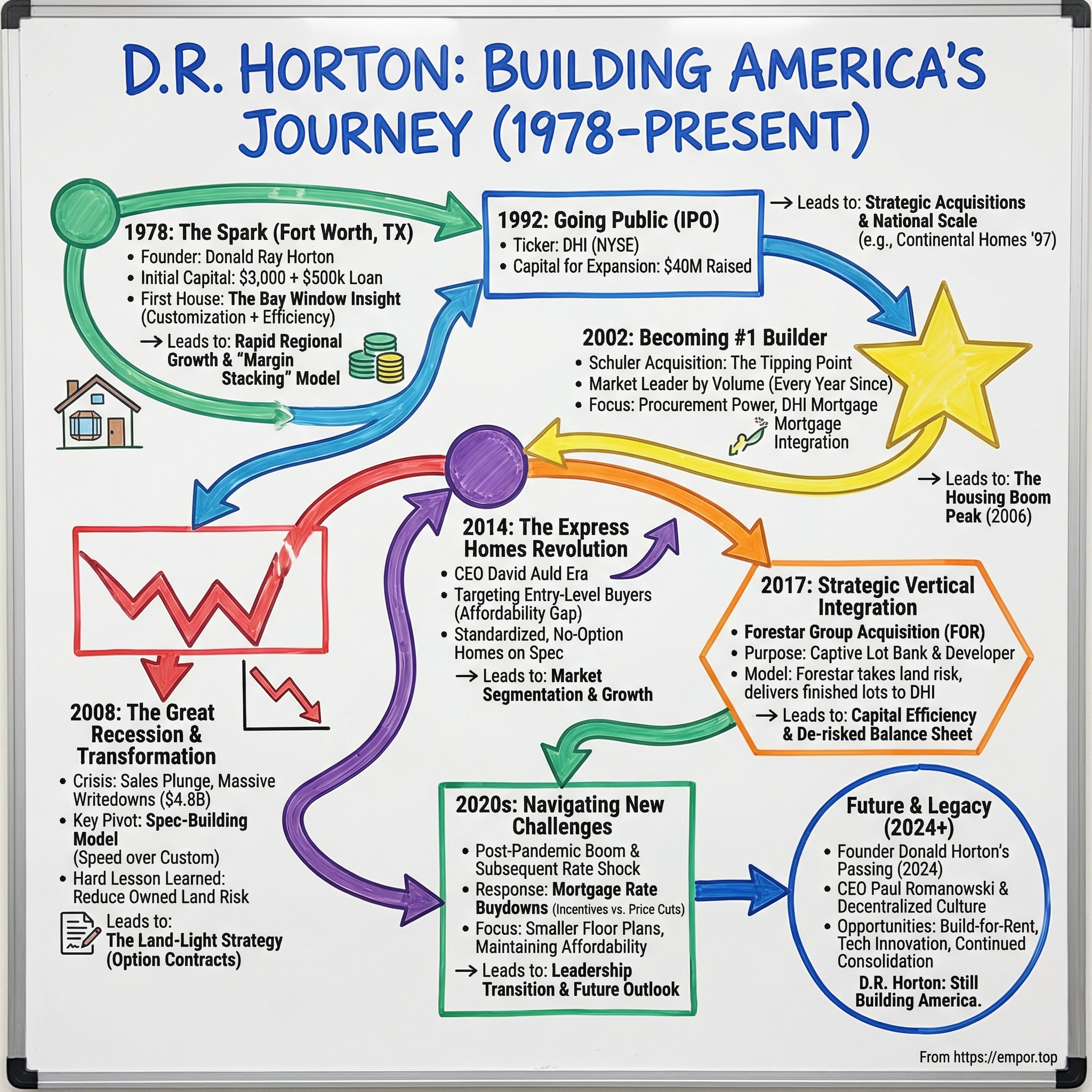

Picture Fort Worth, Texas, November 1978. A 28-year-old college dropout with three thousand dollars to his name convinces a local bank to lend him half a million dollars to build a single house. He has no track record. No construction crew. No brand. What he has is an insight that the entire homebuilding industry has missed: buyers want the efficiency of production housing with the soul of customization. They want someone who will say "yes" when they ask for a bay window.

That man was Donald Ray Horton, and the company he founded would become, by any measure, the most consequential homebuilder in American history.

Since 2002, D.R. Horton has been the largest homebuilder by volume in the United States. Not for one year. Not for five. For every single year across nearly a quarter century. In fiscal year 2024, the company generated $36.8 billion in revenue and $4.76 billion in net income, closing nearly 90,000 homes across 125 markets in 36 states. More than 1.1 million American families now live in homes built by D.R. Horton and its subsidiaries.

This is a story about how scale, operational discipline, and a relentless focus on affordability turned a one-man operation into a Fortune 500 powerhouse. It is a story about surviving the worst housing crash since the Great Depression and emerging stronger on the other side. It is a story about a founder whose instinct for what ordinary Americans want from a home created one of the great compounding machines in American business, and about the leadership culture he built that continues to execute after his sudden death in 2024.

And it is a story that reveals what really drives value in an industry most investors dismiss as hopelessly cyclical: not the housing cycle itself, but the companies that figure out how to win in every phase of it. The homebuilding industry is one of those businesses that sounds simple, buy land, build houses, sell them, but the execution at scale is phenomenally difficult. There are no patents, no network effects, no recurring subscription revenue. The product literally cannot be moved once it is built. And yet D.R. Horton has generated a 15-year compound annual total return to shareholders of approximately 20 percent, turning a post-crisis investment of $5 into nearly $80. That demands explanation.

II. The Donald Horton Origin Story & Early Years (1978-1992)

Donald Ray Horton was born on November 30, 1949, in Zack, Arkansas, a community so small it barely warranted a name on the map. He grew up in nearby Marshall, a town in the north-central part of the state where his father TJ worked as both a cattleman and a real estate broker. From an early age, Don showed the relentless work ethic that would define his career, shining shoes and picking up odd jobs for spending money while his siblings Kathy, Terry, Lillian, and Vivian went about their own childhoods.

Horton graduated from Marshall High School in 1968 and enrolled at Central Arkansas State, now known as the University of Central Arkansas, to study business. But Don had ambitions that pointed beyond small-town Arkansas. In September 1971, he transferred to the University of Oklahoma to pursue a pharmacy degree, a far more prestigious and lucrative path in that era. On his very first day at pharmacy school, he met Marty Martin. They married on December 31, 1971, just months after meeting. The pharmacy career, however, did not stick. Don dropped out and returned to Arkansas to join his father's real estate brokerage, learning the rhythms of property transactions and the fundamentals of what people actually wanted when they bought a home.

In 1977, Don and Marty relocated to Fort Worth, Texas, chasing bigger opportunities. He joined an established Fort Worth homebuilder that constructed standardized production homes. Almost immediately, he grew frustrated. Management refused to let buyers make any changes to existing floor plans. Horton saw the problem clearly: customers wanted some flexibility, and a builder willing to offer it could charge a premium while still capturing the cost efficiencies of production-scale construction. After less than a year, he went out on his own.

The founding moment came in November 1978. With $3,000 in personal capital and the ability to persuade a banker, Horton secured a $500,000 loan to build his first house in a Fort Worth subdivision. During the framing stage, a prospective buyer walked through and asked if a bay window could be added. Horton said yes on the spot and quoted $500 for the upgrade. The buyer agreed immediately. "I sold that house," Horton later told Professional Builder magazine, "then went back to the bank for the money to build two, then four, then eight more."

That bay window was more than a $500 upsell. It was the validation of an entire business model. Horton had found the gap in the market that production builders ignored: standardized homes with the flexibility of semi-custom changes. The cost efficiencies of volume construction combined with the customer appeal of personalization. It was not revolutionary technology or visionary architecture. It was simply listening to what buyers wanted and being willing to say yes.

The growth was immediate and staggering. Horton built 20 houses in 1979 and 80 in 1980, quadrupling output in a single year. Throughout the 1980s, the company essentially doubled in size every year. In every fiscal quarter during the decade, D.R. Horton increased its revenue, its profits, and the number of homes it built. This was not a startup blitzing through venture capital. This was a homebuilder in Fort Worth, Texas, compounding through operational excellence and customer focus, funded by construction loans and retained earnings.

By 1987, Horton recognized that the homebuilding industry was beginning to consolidate. Smaller regional builders were increasingly vulnerable, and the advantages of scale were starting to compound. He made the strategic decision to expand beyond Dallas-Fort Worth, researching new markets for years before committing capital. The approach was analytical and patient: invest $5 to $10 million in approximately 50 home sites in a new market, build local knowledge, then scale. It was the opposite of the land-grab mentality that would later destroy weaker competitors in the 2008 crash.

What was happening in Fort Worth was quietly revolutionary, even if nobody outside the Texas housing industry was paying attention. Most production homebuilders of the 1980s operated on a rigid model: design a set of floor plans, price them competitively, and churn out identical houses in cookie-cutter subdivisions. The custom builders, on the other end of the spectrum, built beautiful one-off homes for wealthy clients but could never achieve meaningful scale. Don Horton had carved out the middle ground, offering the price advantage of standardization with the customer satisfaction of semi-customization, and the market rewarded him with explosive growth that never seemed to plateau.

The economics were elegant. The base home was designed for construction efficiency: standardized framing, predictable material orders, repeatable processes. But by offering upgrades and modifications at premium margins, bay windows, upgraded countertops, modified floor plans, Horton captured additional revenue from each buyer while making the customer feel invested in their home rather than purchasing a commodity. The upgrade revenue came at higher margins than the base home because the incremental cost of a bay window or a kitchen upgrade was far below what the buyer was willing to pay. This margin stacking, production-scale base cost plus premium-margin customization, was the engine that powered two decades of uninterrupted quarterly growth.

By the time the company went public in 1992, D.R. Horton had established an unbroken streak of quarterly growth that would eventually stretch to 21 consecutive years, a record that surpassed even Walmart's. The culture was set: grow steadily, know your customer, manage your costs, and never stop building.

III. Going Public & Early Expansion Strategy (1992-2002)

D.R. Horton went public in June 1992, raising $40 million through the sale of 6.9 million shares at approximately $12 each. The company initially traded on NASDAQ under the ticker DHI before moving to the New York Stock Exchange in 1995. At the time of the IPO, D.R. Horton was a well-run regional builder with a strong base in Texas and early-stage operations in a handful of additional markets. The public currency and access to capital markets would transform it into something far larger.

What followed was one of the most aggressive consolidation campaigns in American homebuilding history. Between April 1994 and the end of the decade, D.R. Horton acquired fourteen different homebuilders. The names read like a roll call of successful regional operators: Joe Miller Homes, Arappco Homes, Regency Homes, Trimark Communities, SGS Communities, Torrey Homes, C. Richard Dobson Builders, Continental Homes, Mareli Development, RMP Properties, and Cambridge Homes, among others.

The company's acquisition philosophy was distinctive and worth understanding, because it explains why so many deals succeeded where industry peers stumbled. As management articulated at the time:

"Our acquisition strategy is simple: We want to be the number one builder in every market we serve. The way to accomplish this is to grow with the best and give them the tools and resources to achieve more. We do our homework and we allow those acquired to run their own business and continue to be successful. We take over the job functions that aren't fun: hunting down money, managing payroll and administering employee benefit programs. With those out of the way and ready access to capital, the way is clear to concentrate on the fun parts of this business: finding land, designing product, building houses, selling homes and managing an operation."

This was not the playbook of a corporate acquirer imposing headquarters culture on local operations. It was the Berkshire Hathaway approach applied to homebuilding. Acquire excellent local operators. Remove their administrative burdens. Give them access to national-scale capital and purchasing power. And let them keep doing what they do best.

The acquired companies retained their local knowledge, their subcontractor relationships, and their market expertise. What changed was that they suddenly had the balance sheet and procurement leverage of a national company behind them. The division president who previously had to negotiate lumber prices for 200 homes per year was now backed by a company buying materials for tens of thousands. The local builder who had struggled to secure favorable financing terms now had access to investment-grade capital markets. The administrative headaches of payroll, benefits, and legal compliance were centralized in Fort Worth, freeing local leadership to focus on what actually built the business: land, homes, and customers.

The transformative deal of the decade was the 1997 acquisition of Continental Homes, a major Phoenix-based builder with operations across multiple Sun Belt markets. The price tag was $305 million plus the assumption of $278 million in debt, a total transaction value of roughly $583 million and by far D.R. Horton's largest deal to that point. Continental immediately gave the company a serious presence in the fast-growing Arizona market and established D.R. Horton as a genuine national builder.

The financial trajectory tells the story of compounding scale. From $190 million in revenue and a ranking of 24th nationally in 1993, D.R. Horton reached $869 million by 1995, operating in 11 states and 25 cities. The Continental acquisition in 1997 pushed revenue past $1.5 billion and established a serious presence across the Sun Belt. By 1999, revenue had reached $3.1 billion, and the company was named Builder of the Year by Professional Builder magazine. D.R. Horton was operating in 22 states with more than 48 divisions, maintaining its extraordinary unbroken streak of quarterly growth.

The pace of growth was remarkable by any industry standard. Revenue compounded at better than 30 percent annually through the 1990s, driven by the twin engines of organic growth and acquisitions. Each new market entered and each new company acquired added volume, which in turn improved procurement leverage, which lowered costs, which made the next market entry and the next acquisition more accretive. It was a classic flywheel: scale begetting scale.

The 2002 acquisition of Schuler Homes for approximately $1.2 billion would push the company to the number one position, a throne it has never relinquished.

What made this expansion strategy work was not just financial engineering or aggressive deal-making. It was the decentralized operating model that allowed each acquired builder to function as a semi-autonomous profit center. Division presidents had full authority over local pricing, land acquisition, product design, and sales strategy. Headquarters in Fort Worth provided capital, national procurement contracts, legal and HR support, and financial oversight. This structure created the rare combination of local entrepreneurship with national scale, and it would prove remarkably resilient through the cycles ahead.

IV. Becoming America's Builder (2002-2008)

The year 2002 marked the crossing of a threshold that redefined D.R. Horton's identity. The Schuler Homes acquisition, which closed on February 21 of that year, added massive volume to an already formidable operation. In fiscal 2002, D.R. Horton closed 29,761 homes and generated $6.7 billion in revenue, with net income exceeding $400 million, a 57 percent increase from the prior year. That same year, the company broke Walmart's record of 100 consecutive quarters of growth and profitability, an achievement that underscored the extraordinary consistency of execution stretching back more than two decades.

But becoming the largest homebuilder was not just about volume. It was about what scale made possible. National procurement contracts with lumber suppliers, appliance manufacturers, and subcontractors delivered cost advantages that regional builders could not touch. The company's financial services arm, DHI Mortgage, began financing an increasing share of its own buyers, creating a vertically integrated transaction that reduced friction and improved margins. The decentralized division structure, now spanning dozens of markets, meant that a slowdown in one region could be offset by strength in another, a natural hedge that single-market builders lacked entirely.

The early-to-mid 2000s were, of course, the great American housing boom. Easy credit, rising home prices, and speculative demand inflated the entire industry. D.R. Horton rode this wave to a pre-crisis peak: in fiscal 2006, the company closed 53,410 homes, with 51,980 net sales orders valued at $13.9 billion. The stock had reached an all-time high of $42.82 in July 2005.

During these boom years, the company continued acquiring: Emerald Builders and Fortress Homes and Communities of Florida in 2001, Schuler in 2002, and smaller tuck-in acquisitions to fill geographic gaps. The geographic diversification strategy that Don Horton had initiated in the late 1980s, expanding methodically beyond Texas, proved transformative. By the mid-2000s, D.R. Horton was not just the largest builder; it was the most geographically diversified, operating in more states and more metropolitan areas than any competitor. This breadth would matter enormously when the music stopped.

To understand just how dominant D.R. Horton became, consider what the Schuler acquisition actually involved. Schuler Homes was itself the product of a recent merger with Western Pacific Housing, so the deal brought in operations across multiple western states that complemented D.R. Horton's existing Sun Belt and Southeast strength. Management estimated the integration would yield $30 to $40 million annually in cost savings from purchasing synergies and administrative consolidation alone. But the real value was strategic: Schuler's volume, layered onto D.R. Horton's existing operations and organic growth, pushed the company past Pulte Homes and into the number one position by volume. It was a throne the company has held for every subsequent year.

The DHI Mortgage piece of the puzzle deserves particular attention, because it illustrates how D.R. Horton turned homebuilding into something closer to a vertically integrated platform. When a buyer walked into a D.R. Horton model home, the company did not just sell them a house. It offered them a mortgage through DHI Mortgage, title insurance through its title subsidiary, and a closing process managed end-to-end within the D.R. Horton ecosystem. Each of these ancillary services generated incremental revenue and margin while simultaneously reducing friction for the buyer. The attach rate, the percentage of buyers who financed through DHI Mortgage, climbed steadily through this period, eventually reaching levels above 75 percent. For a homebuilder, that level of financial services integration is a powerful competitive weapon: it shortens cycle times, reduces fall-through risk, and captures economics that would otherwise leak to third-party mortgage brokers and title companies.

The critical question, looking back, is whether D.R. Horton's management recognized the bubble for what it was. The answer is nuanced. CEO Don Tomnitz, who had served as the company's chief executive since 1998, was characteristically blunt. In March 2007, as the first tremors of the crisis rippled through the industry, Tomnitz went on CNBC and predicted that 2007 would "suck," one of the more honest public assessments by any major homebuilder executive about the storm bearing down on the industry. The company had not entirely avoided the excess of the boom years, land positions had expanded, and leverage had increased, but its geographic diversification and operational discipline would prove to be meaningful advantages in the catastrophe ahead.

V. The Financial Crisis & Recovery (2008-2014)

In the fall of 2007, as subprime mortgage defaults began cascading through the financial system, the homebuilding industry that had celebrated years of uninterrupted growth suddenly found itself staring into an abyss. For D.R. Horton, the company that had built its identity on consistent quarterly growth for more than two decades, the housing crash would test every assumption about the business model, the balance sheet, and the management team.

The collapse was swift, devastating, and nearly existential for the entire American homebuilding industry. For D.R. Horton, the decline from peak to trough was a masterclass in how quickly volume-dependent businesses can unravel when demand evaporates.

In fiscal 2007, net sales orders fell to 33,687 homes valued at $8.2 billion, a 35 percent decline in unit orders from the prior year. The stock, which had peaked above $42, fell to roughly a third of that level by August 2007. But the worst was yet to come. In the first quarter of fiscal 2008, D.R. Horton reported a net loss of $128.8 million, a jarring reversal from the $109.7 million profit earned in the same quarter just one year earlier. Revenue plunged 39 percent to $1.71 billion. Homes closed dropped 36 percent to just 6,549 in the quarter. The company took $245.5 million in pretax charges for inventory and land writedowns in that single quarter alone.

The losses continued for four consecutive quarters. Between 2006 and 2010, D.R. Horton wrote off approximately $4.8 billion in inventory impairments and land option abandonment costs, one of the largest absolute writedown totals in the industry. Revenue fell from a peak of $14.8 billion in fiscal 2006 to just $3.6 billion in fiscal 2009, a 76 percent decline. Homes closed dropped from 53,410 to roughly 15,000. The 21-year streak of consecutive quarterly growth, the record that had surpassed even Walmart, was shattered.

But here is where D.R. Horton's story diverges from the builders that did not survive. While several mid-tier builders went bankrupt and others were absorbed by stronger competitors, D.R. Horton's management took aggressive action to preserve the company's financial position. Cash reserves were built to $1.9 billion. Net homebuilding leverage was brought down to 28 percent. Land positions were ruthlessly pruned, with uncommitted lots walked away from even at the cost of forfeited deposits. The company leaned into its spec-building model, constructing homes on a speculative basis that could be priced to the market and closed quickly, rather than waiting for the custom buyer who might never materialize.

The spec-building approach is worth explaining because it became central to D.R. Horton's DNA going forward. In the traditional model, a builder waits for a buyer to sign a contract, then begins construction. This is low-risk but slow. In the spec model, the builder starts a home before having a buyer, betting that a completed or nearly completed home on a finished lot will sell faster than a to-be-built contract. During the crisis, this seemed counterintuitive: why build homes nobody has committed to buy? But D.R. Horton understood that in a distressed market, the buyers who remained were often motivated and time-sensitive. They wanted to move quickly. They wanted to see a physical home, walk through it, and close in weeks rather than months. Spec inventory, priced aggressively, met that demand. Fitch Ratings specifically cited D.R. Horton's successful spec-building approach when upgrading the company's credit rating during the recovery.

Fiscal 2010 marked the return to profitability with $245.1 million in net income, assisted by a tax benefit of $145.6 million. The recovery was not linear: fiscal 2011 saw net income drop to $71.8 million as the housing market stuttered. But by fiscal 2013, revenue had climbed back to approximately $7.1 billion, and the foundational strengths that had made D.R. Horton the industry leader, national scale, decentralized operations, and balance sheet discipline learned at extraordinary cost, were intact and ready to compound.

Crucially, D.R. Horton maintained its number one market position throughout the entire crisis. Even at the trough, even while writing off billions, the company was building and closing more homes than any competitor. This is an underappreciated fact: the crisis destroyed weaker players and permanently impaired others, but it did not dislodge D.R. Horton from the top of the industry. The gap between D.R. Horton and its nearest competitors actually widened during and after the downturn, as the company's balance sheet strength allowed it to acquire distressed land at depressed prices and open new communities while competitors were still nursing their wounds.

The crisis taught D.R. Horton a lesson it would never forget. The $4.8 billion in writedowns came overwhelmingly from owned land, lots and raw acreage that the company had purchased outright during the boom and could not sell during the bust. In the years that followed, management embarked on a deliberate, multi-year transition from owning land to controlling land through option contracts. If the company needed 100,000 lots, it would own perhaps 25,000 and hold options on the remaining 75,000. In a downturn, it could walk away from the options, forfeiting small deposits rather than carrying billions in depreciating land. This shift would prove to be one of the most important strategic decisions in the company's history, reducing the debt-to-equity ratio from 0.62 in 2015 to approximately 0.20 by 2024, even as revenue more than tripled over the same period.

For investors studying D.R. Horton, the financial crisis is not just historical context. It is the defining event that shaped the company's current capital structure, risk management philosophy, and competitive positioning. Every major strategic initiative of the past decade, Express Homes, Forestar, the land-light model, rate buydowns, traces its intellectual origins to what the company learned from losing $4.8 billion.

VI. The Express Homes Revolution & Market Segmentation (2014-2020)

In the years following the crisis, the American housing recovery carried an uncomfortable paradox. Home prices were rising, new construction was rebounding, and builders were reporting improved profits. But an entire generation of first-time buyers was being left behind. Most large builders had retreated upmarket during and after the downturn, chasing higher per-unit margins on move-up and luxury homes. Millennials, saddled with student debt and facing tighter mortgage standards, found that the new homes being built were designed for families trading up, not for couples buying their first property. The entry-level segment, the foundation of the housing market, had been largely abandoned.

The conventional wisdom in the industry held that builders simply could not make money at entry-level price points. Lot costs, labor, and materials made it impossible to deliver a quality new home at $120,000 to $150,000 and still earn an acceptable margin. D.R. Horton set out to prove the conventional wisdom wrong.

In early 2014, under the leadership of new CEO David Auld, who had succeeded Don Tomnitz on October 1, D.R. Horton launched Express Homes. The concept was radical in its simplicity: a no-options, turnkey product built entirely on spec. Buyers chose a home, not a configuration. There were no design studios, no change orders, no production complexity from custom selections. The homes were pre-designed with carefully chosen finishes and built to a standardized process that minimized construction time and eliminated the overhead of option management.

The initial price range targeted $120,000 to $150,000, a range that had virtually no competition from national builders. Tomnitz had laid the intellectual groundwork before his retirement, declaring that "the next leg of the recovery will be led by the true entry-level buyer." Auld and his team turned that thesis into a product.

The results exceeded every internal projection. By the first quarter of fiscal 2015, Express was operational in 38 of D.R. Horton's 79 markets, with plans to reach the "substantial majority" by year-end. Express accounted for roughly half of Horton's 35 percent jump in sales orders that quarter and represented 13 percent of total homes sold, up from just 3 percent a year earlier. The median actual sales price came in at $169,000, above initial targets but still approximately $100,000 below the Census Bureau's median new-home price. CFO Bill Wheat confirmed that margins on Express homes were "better than original expectations."

The secret was scale economics, and it is worth dwelling on why only D.R. Horton could pull this off. Consider the math of building an entry-level home at $150,000. The lot might cost $25,000 to $35,000. Materials, lumber, concrete, roofing, windows, plumbing, electrical, could run $50,000 to $60,000 at retail prices. Labor, primarily subcontracted, might cost $30,000 to $40,000. Add in SG&A overhead, warranty costs, financing, and you are pushing well past $150,000 before a dollar of profit.

But D.R. Horton does not pay retail for materials. Its national procurement contracts, negotiated across nearly 90,000 homes per year, deliver discounts that a builder closing 200 or even 2,000 homes cannot access. The standardized Express floor plans eliminated design studio costs, change order management, and production disruptions from custom selections. Homes were built entirely on spec, meaning construction could be scheduled for maximum crew efficiency rather than waiting for individual buyer timelines. Cycle times were compressed, which improved capital turns and reduced the carrying cost of each lot. And SG&A overhead was spread across such massive volume that the per-home cost was a fraction of what smaller competitors faced.

Express Homes was not charity; it was a business that only a builder of D.R. Horton's size and operational maturity could execute profitably. It represented a genuine form of counter-positioning in Hamilton Helmer's framework: competitors who dismissed entry-level as unprofitable were unable to respond without fundamentally restructuring their operations and cost base.

Express grew to represent approximately half of D.R. Horton's total closings, fundamentally transforming the company's revenue mix and its competitive position. What started as an experiment in 38 markets became the single most important growth driver of the past decade.

But Express was just one piece of a broader product segmentation strategy that now spans four distinct brands. The core D.R. Horton brand serves the move-up buyer in the $300,000 to $600,000 range, the bread-and-butter of American homebuilding. Emerald Homes targets the luxury segment above $600,000 with premium finishes, larger lots, and resort-style community amenities. And Freedom Homes, launched to serve the active adult community of buyers aged 55 and older, addresses a demographic wave that is just beginning: approximately 11,200 Baby Boomers turn 65 every single day through 2027, and an estimated 74 million Americans will be 65 or older by 2050.

Each brand has its own identity, its own marketing, and its own customer experience, but all four share the same construction platform, procurement infrastructure, and financial services backbone. This is the power of a multi-brand strategy in homebuilding: the consumer sees four distinct brands tailored to their life stage, while the company captures the scale economics of a single operating platform across all four.

This four-brand architecture is unique among major national builders. Where competitors like PulteGroup focus on move-up and active adult, or Toll Brothers exclusively serves the luxury market, D.R. Horton covers the entire spectrum of single-family demand from a single platform. A first-time buyer starts with Express, trades up to the D.R. Horton brand as their family grows, and potentially downsizes into a Freedom community decades later. The lifetime value of that relationship, facilitated by DHI Mortgage's integrated financing, is a competitive advantage that does not show up on any single quarterly earnings report but compounds powerfully over time.

VII. Recent Acquisitions & Scale Economics (2015-2024)

While Express Homes was reshaping D.R. Horton's product strategy, the company's acquisition machine never stopped running. But the nature of the deals evolved. Instead of the large, transformative acquisitions of the 1990s, like Continental Homes or Schuler Homes, the post-crisis playbook emphasized smaller, strategic tuck-ins that filled geographic gaps or added lot inventory in high-growth markets.

In April 2015, D.R. Horton acquired Pacific Ridge Homes, a Seattle-based builder, for $72 million. The deal illustrated the typical anatomy of a D.R. Horton tuck-in acquisition: the purchase came with 350 lots, 90 homes in inventory, 40 homes in sales order backlog, and control of approximately 400 additional lots through option contracts. The price bought not just physical assets but a local team with deep market knowledge, established subcontractor relationships, and a pipeline of communities in various stages of development.

The following year, Wilson Parker Homes was acquired for $90 million, adding scale in the Southeast. In 2018, the pace accelerated dramatically: three private builders, Terramor Homes of Raleigh-Durham for $62 million, Classic Builders, and Westport Homes, were all acquired within a single month. The velocity of deal-making demonstrated D.R. Horton's well-oiled acquisition machine, the due diligence capabilities, legal infrastructure, and integration playbooks that allowed the company to evaluate, close, and absorb multiple targets simultaneously.

But the most strategically significant deal of this period was not a homebuilder acquisition at all. In June 2017, D.R. Horton proposed to acquire 75 percent of Forestar Group, a Texas-based land development company, for $16.25 per share. After negotiations, the final price was set at $17.75 per share, with total aggregate cash consideration of approximately $558 million. The transaction closed on October 5, 2017.

The genius of the Forestar deal was structural. Rather than absorbing Forestar entirely, D.R. Horton kept it as a majority-owned but independently publicly traded subsidiary on the NYSE under the ticker FOR. Forestar's role is deceptively simple but strategically profound: it acquires raw land, secures entitlements and permits, develops the infrastructure, and delivers finished, shovel-ready lots to D.R. Horton at market prices.

To understand why this matters, think about what happens when a homebuilder wants to construct a subdivision. Before a single home can be built, someone has to buy the raw land, navigate months or years of zoning and permitting, install roads and sewers and utility connections, and grade individual lots. This land development process is capital-intensive, time-consuming, and risky. If the housing market turns sour during the two or three years between buying raw acreage and delivering finished lots, the developer is stuck holding depreciating land with no immediate use.

Forestar absorbs this risk. It functions as a captive lot bank, holding land through the development cycle and delivering finished, shovel-ready lots to D.R. Horton on a phased schedule at market prices. D.R. Horton gets preferred access to a reliable pipeline without carrying the capital risk of owning undeveloped land on its own balance sheet. Forestar raises its own debt and equity, operates with its own management, and sells roughly 83 percent of its lots to D.R. Horton while maintaining the ability to sell to other builders. This directly addresses the painful lesson of the 2008 crisis, when billions in owned land became the source of crippling writedowns.

By fiscal year 2024, Forestar was delivering over 15,000 lots per year, with approximately 83 percent flowing to D.R. Horton. The subsidiary maintained its own lot position of nearly 100,000 lots and generated return on equity of approximately 14 percent. Lennar, D.R. Horton's closest competitor by volume, was so impressed by the model that it completed a similar maneuver in February 2025, spinning off its land assets into Millrose Properties, a $5.5 billion land REIT. Imitation is the sincerest form of competitive validation.

An observation frequently made about D.R. Horton's acquisition strategy captures the company's philosophy well: it uses its size and strength to acquire smaller companies and consolidate the market, but it also allocates capital to preserve its balance sheet.

This dual mandate, consolidating the industry while maintaining fortress-like financial reserves, is the essence of D.R. Horton's strategic positioning. Should the market enter a downturn, a strong balance sheet provides the flexibility to make more opportunistic acquisitions when competitors are distressed. Should the market remain strong, the company can deploy capital into organic growth and shareholder returns.

This is classic capital cycle management, the ability to play offense when others are playing defense, and it has been a hallmark of D.R. Horton's approach since the earliest days of Don Horton's expansion from Fort Worth.

VIII. Financial Performance & Operating Model

To understand D.R. Horton's financial performance, start with the operating model, because the numbers are inseparable from the machine that produces them.

D.R. Horton operates through approximately 92 homebuilding divisions spread across 125 markets in 36 states. Each division functions as a semi-autonomous profit center, led by a division president with full authority over product offerings, pricing, community-level incentives, land acquisition, construction sequencing, and broker relationships. Fort Worth headquarters provides what the divisions cannot efficiently produce on their own: capital allocation, national procurement leverage, brand standards, legal and HR services, technology infrastructure, and financial oversight.

This decentralized architecture is not incidental. It is the core of the company's competitive advantage. Housing markets are fundamentally local. The dynamics of a subdivision in suburban Phoenix bear little resemblance to a community outside Charlotte or a development in the Pacific Northwest. School districts, employer relocations, commute patterns, and local regulations all shape demand in ways that a centralized planning team in Texas cannot possibly understand at granular resolution. Division presidents, embedded in their markets, make decisions with the speed and contextual awareness that national mandates cannot match. When Austin home prices needed to fall 15 percent or more in 2022 and 2023, local teams acted without waiting for corporate approval.

The financial results of this model in fiscal 2024 were characteristic of a mature, well-oiled machine. Revenue reached $36.8 billion, a 3.8 percent increase over the prior year. Earnings per diluted share came in at $14.34 for the full year and $3.92 for the fourth quarter. Pre-tax profit margin was 17.1 percent for both the quarter and the fiscal year. Return on equity was 19.9 percent, a figure that consistently exceeds the company's cost of capital, making D.R. Horton a genuine economic value creator rather than a mere capital recycler.

But the numbers that matter most for understanding the operating model are the efficiency metrics. Homebuilding SG&A as a percentage of revenue runs at approximately 8.9 percent, among the lowest in the industry, a direct product of scale and local cost accountability. Compare this to smaller builders that typically run SG&A at 12 to 15 percent of revenue, and the compounding advantage of scale becomes clear. DHI Mortgage financed approximately 78 percent of D.R. Horton's closings in fiscal 2024, creating a secondary revenue stream and keeping buyers within the company's ecosystem from land selection through mortgage closing.

Perhaps the most significant long-term trend in D.R. Horton's financial profile is the transition to a land-light model. As of fiscal 2024, the company controlled approximately 571,000 lots, but only about 24 percent were owned outright. The remaining 76 percent were controlled through option contracts, agreements that give D.R. Horton the right but not the obligation to purchase lots at a predetermined price on a future date. If the market deteriorates, the company can walk away from the options, forfeiting only the relatively small deposits rather than carrying billions in depreciating land assets. This is how D.R. Horton used three different methods to acquire land: direct land development for maximum margin control, finished lot purchases from third-party developers for speed and lower risk, and option contracts for maximum downside protection.

The shift toward options has dramatically reshaped the balance sheet. The debt-to-equity ratio fell from 0.62 in 2015 to approximately 0.20 by 2024, a 68 percent reduction, even as revenue more than tripled over the same period. This is not financial engineering for its own sake. It is a direct institutional response to the $4.8 billion in land writedowns during the 2008 crisis.

Capital allocation has become increasingly shareholder-friendly. The company has repurchased approximately 51 million shares since 2018, with fiscal 2025 plans targeting $2.6 to $2.8 billion in buybacks. The quarterly dividend has been raised for twelve consecutive years, reaching $0.40 per share, with a further increase to $0.45 per share announced for fiscal 2026. Total debt stood at roughly $5.9 billion against that remarkably low leverage ratio, with available liquidity exceeding $5.1 billion. This balance sheet conservatism is the direct inheritance of the 2008 crisis, when leverage and owned land nearly brought the company to its knees. The institutional memory of those years runs deep in Fort Worth.

The most recent fiscal year, FY2025 ending September 2025, showed the impact of sustained high mortgage rates. Revenue declined to $34.3 billion, down 6.9 percent from the prior year's record. Net income fell to $3.59 billion as gross margins compressed from approximately 24.6 percent to 20 percent by the fourth quarter, driven largely by the cost of mortgage rate buydown incentives.

It is important to contextualize these numbers properly. A revenue decline to $34.3 billion and net income of $3.59 billion would be exceptional results for virtually any company in any industry. The "decline" is only disappointing relative to the extraordinary pandemic-era margins that peaked at over 30 percent gross margin in fiscal 2022. Those margins were anomalous, driven by a supply-demand imbalance that will not recur in normal conditions.

The company returned $4.8 billion to shareholders through buybacks and dividends, demonstrating that even in a challenging environment, the cash generation machine continues to function. For fiscal 2026, management guided to revenue of $33.5 to $35.0 billion with 86,000 to 88,000 home closings.

IX. The Donald Horton Legacy & Leadership Transition

On the evening of May 17, 2024, Donald Ray Horton died suddenly at the age of 74. The company he had founded 46 years earlier with a $500,000 bank loan and a willingness to add a bay window announced his passing the same day. He had served as Executive Chairman of the Board continuously since July 1991 and had been a driving force in building D.R. Horton from a single Fort Worth home into the nation's largest homebuilder.

He was survived by his wife Marty, his pharmacy school sweetheart whom he married on December 31, 1971; sons Ryan and Reagan; daughters-in-law Stacy and Michelle; and four grandchildren. His funeral was held at Thompson's Harveson & Cole Funeral Homes in Fort Worth. Industry tributes noted his extraordinary work ethic, his ability to maintain personal relationships across a 13,000-employee enterprise, and his founding of Camp Horton in 2001, a summer camp for employees' children that reflected his philosophy of treating the company as an extended family.

As of 2020, Donald Horton owned approximately 6 percent of the company, a stake that reflected both his conviction in the business and his alignment with shareholders over more than four decades. His leadership style was not that of a micromanager; after stepping back from day-to-day operations, he remained deeply involved through travel to field operations, personal relationships with division leaders, and a cultural imprint that emphasized treating employees, vendors, and customers with respect.

The transition plan had been years in the making. The CEO lineage tells a story of deliberate, long-horizon succession planning.

Don Tomnitz, who had joined D.R. Horton in 1983 and helped execute the 1992 IPO, served as chief executive from 1998 through his retirement on October 1, 2014, a 31-year tenure with the company. Under Tomnitz, D.R. Horton became the number one builder, navigated the 2008 crisis, and laid the intellectual groundwork for the Express Homes strategy.

David Auld succeeded Tomnitz as President and CEO, overseeing perhaps the most transformative period in the company's post-founding history: the launch and scaling of Express Homes, the Forestar acquisition, and a revenue expansion from approximately $8 billion to $35.5 billion. Under Auld's leadership, D.R. Horton built its one millionth home.

When Paul Romanowski was named President and CEO effective October 1, 2023, Auld moved to Executive Vice Chairman. Following Donald Horton's death, Auld was appointed Executive Chairman, assuming the role the founder had held.

Romanowski represents the depth of D.R. Horton's internal talent pipeline. A Butler University graduate with a BBA in marketing, he spent 15 years as Division President for D.R. Horton's South Florida operations, one of the most competitive and supply-constrained homebuilding markets in the country. South Florida, with its complex entitlement processes, high land costs, hurricane building codes, and intense competition, is arguably the hardest market in which to run a profitable homebuilding division. That Romanowski thrived there for a decade and a half speaks to his operational capability.

He later expanded to Region President overseeing Florida and five Mid-Atlantic states before being named Co-Chief Operating Officer in 2021. His rise was entirely internal, reflecting a culture where leadership is developed over decades rather than recruited from outside. Michael Murray, the Chief Operating Officer since 2014, provides additional continuity across leadership eras, ensuring that the operational DNA of the company remains consistent even as the top of the organization evolves.

The true test of any founder-led company is whether the organization can sustain its performance and culture after the founder is gone. For D.R. Horton, the early evidence suggests the transition has been notably smooth.

The decentralized operating model is the key reason why. When 92 division presidents across the country are running their own businesses every day, making pricing decisions, negotiating with subcontractors, managing their own P&L, the company's performance does not hinge on what happens in any single office, including the chairman's office in Fort Worth.

The culture of operational discipline, local accountability, and customer focus that Don Horton instilled is embedded in the organizational structure itself, not dependent on any single individual's presence. This is the ultimate expression of Process Power in Hamilton Helmer's framework: a system of embedded routines and organizational capabilities that produces consistent results regardless of who is steering.

X. Current Strategy & Market Position

The housing market that D.R. Horton navigates today bears the scars of the Federal Reserve's most aggressive rate-hiking cycle in four decades. When the Fed raised rates from 0.25 percent in early 2022 to 5.5 percent by mid-2023, the 30-year fixed mortgage surged from approximately 3 percent to over 7 percent, briefly touching 8 percent. Monthly payments on a median-priced home effectively doubled. D.R. Horton's cancellation rate spiked from 16 percent to 32 percent.

The company's response revealed the advantages of its scale and financial services integration. Rather than simply cutting prices, which would permanently impair land values and neighborhood comparables, D.R. Horton leaned heavily into mortgage rate buydowns.

The mechanism is worth understanding in detail, because it has become the single most important competitive tool in modern homebuilding. At closing, the builder pays "points," which is essentially prepaid interest, to the mortgage lender to reduce the buyer's effective interest rate. Think of it as the builder subsidizing the buyer's monthly payment by writing a check to the bank upfront.

Why is this more efficient than a simple price cut? The math is striking. A one percentage point reduction in mortgage rate has the same monthly payment impact as an 11 percent reduction in home price. So instead of cutting the price of a $350,000 home by $38,500, the builder can spend a fraction of that amount on points to achieve the same payment relief for the buyer. The home's appraised value stays intact, protecting both the buyer's equity and the builder's comparables in the neighborhood. The builder's gross margin, while still pressured, is far better protected than with an outright price reduction.

By late 2024, approximately 80 percent of D.R. Horton's buyers were using rate buydowns, with the company typically offering a full point below market on a 30-year fixed rate for the life of the loan. At certain points, promotional rates fell as low as 1.99 percent through 2/1 buydown structures when the market rate was near 7 percent. Only well-capitalized builders with integrated mortgage operations can sustain programs of this magnitude. Small builders and existing home sellers simply cannot compete.

Alongside rate buydowns, the company has continued building and selling smaller floor plans to combat affordability pressures. Average square footage declined from approximately 2,092 square feet in 2020 to 1,954 square feet by 2025, while the average selling price edged down from $376,100 in the first quarter of fiscal 2025 to $365,500 in the first quarter of fiscal 2026. Every decision is oriented toward keeping monthly payments within reach of the median American household.

The build-for-rent segment represents another dimension of current strategy and deserves careful attention, because it reveals how D.R. Horton thinks about capital efficiency and market diversification. The company entered single-family rental construction around 2016 and has since delivered over 15,400 rental homes across more than 150 communities.

Critically, the company operates as a builder, not a landlord. This distinction is fundamental. Companies like Invitation Homes or American Homes 4 Rent buy or build single-family homes and then manage them as rental properties, collecting monthly rent and bearing all the ongoing costs of property management, maintenance, and tenant turnover. D.R. Horton does something entirely different: it constructs entire rental communities, leases them up to a stabilized occupancy level, and then sells the completed communities to institutional investors such as pension funds, private equity firms, and REITs. D.R. Horton captures the construction margin and the development profit without taking on the ongoing burden and capital intensity of landlording.

This model provides an additional outlet for land positions and construction capacity without cannibalizing for-sale homebuilding, since the ultimate buyer is an institution rather than a retail homebuyer. As the company has described it, build-for-rent is "a great way to more rapidly monetize land positions without cannibalizing for-sale business because it is a different user of that real estate and a different owner of that real estate." In fiscal 2025, the rental segment generated approximately $1.6 billion in revenue and roughly $170 million in pre-tax income. The segment also spans multifamily rental units, with the fourth quarter of fiscal 2025 seeing sales of 1,565 single-family and 1,815 multifamily rental units.

One regulatory risk worth flagging: in January 2026, federal proposals to restrict institutional single-family home buyers briefly pressured the stock. No legislation has been enacted as of this writing, but the political scrutiny of Wall Street's role in single-family housing remains a headline risk for D.R. Horton's rental operations.

D.R. Horton's balance sheet remains a pillar of its current positioning. With low leverage, substantial liquidity exceeding $5 billion, and a debt-to-equity ratio of roughly 0.20, the company has significant financial flexibility to weather prolonged rate challenges or to pounce on acquisition opportunities if competitors stumble.

The structural housing shortage in America, estimated at 3.7 to 4.7 million units depending on the source, provides a demand backdrop that is unlikely to disappear within this decade. The mortgage lock-in effect adds another layer: roughly 85 percent of existing homeowners hold mortgage rates below 6 percent and are unwilling to sell into a higher-rate market, since doing so would mean giving up their low-rate mortgage and taking on a much higher payment on their next home.

This lock-in effect has a powerful secondary consequence: it suppresses the supply of existing homes for sale, which in a normal market would be the primary competition for new construction. With existing home inventory constrained, buyers who need a home are increasingly turning to new construction as their only viable option. This dynamic has disproportionately benefited the largest homebuilders, who have the capacity and financial flexibility to ramp production to meet the redirected demand.

As of early 2026, with mortgage rates edging toward 6 percent following six Fed rate cuts totaling approximately 175 basis points through 2025, the environment is gradually becoming more favorable. The first quarter of fiscal 2026 showed net sales orders growing 3 percent year over year, a tentative but encouraging signal that the worst of the affordability crunch may be easing.

XI. Playbook: Business & Investing Lessons

D.R. Horton's nearly five-decade history offers a rich set of lessons for operators and investors alike, and several of them challenge conventional thinking about what makes a great business.

The first and most obvious lesson is that scale is a genuine competitive advantage in homebuilding, even though the industry appears fragmented and local. In 1994, the top ten builders controlled roughly 10 percent of the national market. By 2024, that figure had reached 44.7 percent. D.R. Horton alone commands approximately 13.6 percent market share, nearly double the next closest competitor.

Scale delivers advantages across multiple dimensions simultaneously. In procurement, national contracts with lumber, appliance, and materials suppliers provide per-unit cost savings unavailable to regional operators. In financial services, DHI Mortgage's ability to offer rate buydowns at scale is a weapon that small builders cannot wield. In capital access, investment-grade credit ratings and deep liquidity mean D.R. Horton borrows more cheaply than competitors with weaker balance sheets. And in talent, the best division presidents in the industry gravitate toward the company with the most resources, the most markets, and the most opportunity for career growth.

These advantages are compounding, not static. Each additional market and each additional home closed makes the machine slightly more efficient. The consolidation trend in homebuilding is structural, not episodic, and it favors the largest players in every cycle.

The second lesson is that operational excellence beats financial engineering. D.R. Horton has never been the most financially creative builder. Its capital structure is conservative. Its leverage is low. It does not engage in exotic real estate finance. What it does is build and sell homes with extraordinary efficiency: an SG&A ratio of under 9 percent, consistent cycle times, and a decentralized model that keeps decision-making close to the customer.

In an industry prone to boom-and-bust cycles driven by leverage and speculation, D.R. Horton's boringly consistent execution has proven to be its most powerful weapon. The company has never chased the highest margins or the most exclusive market segment. It has simply built more homes, more efficiently, for longer, than anyone else. There is a lesson here for investors who are drawn to flashier business models: sometimes the best investment is the company that does the mundane thing better than anyone in the world.

The third lesson is acquisition integration mastery. Acquiring 14 builders in six years during the 1990s and maintaining operational continuity required a model that respected local knowledge while extracting national synergies. The "remove the administrative burdens, let them keep building" philosophy created a replicable playbook that D.R. Horton has deployed across dozens of acquisitions over three decades.

This playbook has a direct analogy in the technology world: it is similar to how Constellation Software acquires vertical market software companies, letting founders continue running their businesses while providing access to shared services, capital, and best practices. The Forestar deal extended this philosophy to vertical integration: rather than absorbing its land developer, the company kept it as a separately traded entity with its own capital structure and management team.

Fourth, product segmentation and market coverage matter more than most investors appreciate. D.R. Horton's four-brand strategy, Express, D.R. Horton, Emerald, and Freedom, covers the full spectrum of single-family demand. This is not just about revenue diversification; it is about capturing customers at every stage of their housing lifecycle and maintaining demand resilience across varying economic conditions.

When move-up buyers retreat during a rate shock, entry-level buyers with smaller mortgage needs may step in. When younger households delay purchasing due to student debt or career uncertainty, active adults may be downsizing from homes they have owned for decades. No other national builder covers the market as comprehensively, and this breadth provides a natural hedge against segment-specific downturns.

Fifth, capital cycle management is perhaps the most underappreciated skill in D.R. Horton's arsenal. The company builds cash during booms and deploys it during busts, using strong balance sheet positioning to acquire distressed competitors when others cannot. The 2008 crisis destroyed weaker builders and created land and lot opportunities that only well-capitalized survivors could exploit.

D.R. Horton was among those survivors, and its post-crisis land acquisitions at depressed prices fueled the revenue growth of the following decade. The playbook is elegant in its simplicity: when everyone else is fearful, D.R. Horton is buying. When everyone else is euphoric, D.R. Horton is building cash. This discipline requires patience and conviction, and it has been a hallmark of the company's approach since Don Horton's earliest days of careful market entry in the late 1980s.

XII. Bear vs. Bull Case

The Bear Case

Interest rate sensitivity remains the single largest risk to D.R. Horton's business. When 30-year mortgage rates spiked above 7 percent, the company's cancellation rate doubled and gross margins compressed by roughly 1,000 basis points from their 2022 peak. The cost of rate buydowns, while strategically sound, directly erodes profitability.

Management has indicated that it plans to maintain rate buydowns even if interest rates decline significantly, viewing them as a permanent competitive tool rather than a temporary crisis measure. This is a revealing strategic signal: it means margin compression from incentive spending may be structural rather than cyclical. If rates remain elevated or rise further, margins could compress to levels that challenge even D.R. Horton's volume-driven model.

Land and lot cost inflation presents a structural challenge. Zoning restrictions, environmental regulations, and NIMBYism have constrained the supply of buildable lots in many high-demand markets. Regulations now account for approximately 24 percent of the cost of a new home on average. D.R. Horton's land-light model mitigates ownership risk but does not eliminate the underlying cost pressure.

Labor shortages are chronic. Approximately 74 percent of builders reported labor shortages in recent years, and the construction workforce skews heavily toward immigrant labor, with roughly 32.5 percent of construction workers being immigrants according to NAHB data. Immigration enforcement could further tighten supply and raise costs. Tariff-related cost increases on lumber, cabinets, and other imported materials, estimated at up to $17,500 per home, represent an additional margin headwind, though a February 2026 Supreme Court ruling invalidating certain tariffs imposed under IEEPA may provide some relief.

At a fundamental level, homebuilding remains a cyclical industry. No amount of operational excellence can fully insulate a builder from a demand collapse. The 2008 crisis demonstrated this unambiguously, and while D.R. Horton is far better positioned today, the business is not immune to macroeconomic downturns.

Through the lens of Porter's Five Forces, competitive rivalry among existing builders is intensifying. The top ten builders now control nearly 45 percent of the market, and they are increasingly competing on incentives rather than product differentiation, a dynamic that compresses margins industry-wide. Rate buydowns and closing cost assistance have become table stakes, not competitive advantages, when every large builder offers them.

Applying Hamilton Helmer's 7 Powers framework, D.R. Horton's moats are real but narrow, and honest analysis requires acknowledging where moats do and do not exist. Scale Economies are present in procurement and SG&A, but they deliver cost advantages measured in hundreds of basis points, not multiples. The SG&A gap between D.R. Horton at under 9 percent and smaller builders at 12 to 15 percent is meaningful but not insuperable. Process Power exists in the decentralized operating model: 92 division presidents running semi-autonomous P&L centers with full local authority is a culture and organizational design that cannot be copied overnight. It takes decades of internal talent development, trust-building, and cultural embedding to create this kind of operational machine. But it can, in principle, be replicated over time by motivated competitors.

Counter-Positioning was clearly present in the Express Homes launch. When D.R. Horton began building no-option, turnkey homes at $120,000 to $150,000, competitors like Toll Brothers and even PulteGroup had no interest in the segment. Their cost structures, design studio overhead, and margin expectations made entry-level appear unprofitable. By the time the rest of the industry recognized the opportunity, D.R. Horton had established dominant market share in the entry-level segment. However, Counter-Positioning is a temporary power, it erodes as competitors adapt, and several builders have since launched their own affordable brands.

Network Effects, Switching Costs, and Branding power in homebuilding are inherently limited. Consumers buy a home once a decade, not daily, and loyalty runs to location and price far more than to builder brand. A buyer choosing between an Express home and a competitor's entry-level offering will almost certainly choose on price and lot location, not on brand affinity. Cornered Resource does not meaningfully apply: while D.R. Horton has excellent management and subcontractor relationships, these are not proprietary resources that competitors are structurally blocked from accessing.

The Bull Case

The structural housing shortage in the United States is not a cyclical blip. It is the accumulation of fifteen years of underbuilding that began with the 2008 crash, when housing starts collapsed from nearly 2 million per year to roughly 550,000, an 18-year low, and did not recover to normal levels until the mid-2010s. For approximately fifteen years, new home starts averaged 1.0 to 1.3 million per year against household formation of 1.2 to 1.5 million. The gap compounded relentlessly. Zillow's most recent analysis estimated the deficit at 4.7 million units, an all-time high. Freddie Mac placed it at 3.7 million. The Dallas Fed calculated 6 to 8 million units of cumulative underbuilding since 2000 when measured against demographic need. Whatever the precise number, every credible source agrees: America has millions fewer homes than it needs, and the gap is still growing. At current building rates, NAHB projects the shortage could persist until the end of this decade at minimum.

Demographics reinforce the supply-demand imbalance from the demand side. The largest generation in American history, the millennials, is now entering its peak homebuying years, the period from roughly age 28 to 40 when household formation accelerates. Simultaneously, 11,200 Baby Boomers turn 65 every single day through 2027, driving demand for downsizer and active adult communities. D.R. Horton's four-brand product suite directly addresses both demographics: Express and D.R. Horton core for younger buyers, Freedom Homes for aging boomers. Few competitors are positioned to capture both ends of this demographic sandwich simultaneously.

There is a commonly held myth that the housing shortage will be solved by a wave of new construction. The reality is more stubborn. Regulatory barriers, including zoning restrictions, permitting delays, environmental review, and NIMBYism, account for approximately 24 percent of the cost of a new home. These barriers constrain supply regardless of builder willingness to build. Labor shortages, with 74 percent of builders reporting difficulty finding workers, further limit the industry's ability to ramp construction. And the lock-in effect, where roughly 85 percent of existing homeowners hold mortgage rates below 6 percent and refuse to sell into a higher-rate market, suppresses the supply of existing homes and funnels buyers toward new construction. For the foreseeable future, the shortage is a structural tailwind that benefits the largest and most efficient builders disproportionately.

D.R. Horton's scale advantages are compounding, not static. As the top ten builders' market share grows from 45 percent toward 50 percent and beyond, the economics of being number one become increasingly favorable. Small builders cannot match rate buydowns, national procurement terms, or integrated financial services. Every cycle of consolidation widens the gap.

The company's balance sheet provides what may be its most valuable strategic option: the ability to play offense in a downturn. With over $5 billion in liquidity and a debt-to-equity ratio of 0.20, D.R. Horton can acquire distressed competitors, snap up land at depressed prices, and continue returning capital to shareholders even if the housing market deteriorates significantly.

The competitive landscape itself reinforces D.R. Horton's position. Among the major public homebuilders, each has chosen a different strategic emphasis, and D.R. Horton's choice of volume leadership and affordability looks well-suited to the current environment.

NVR, operating primarily in the Mid-Atlantic and Southeast, offers the purest land-light model in the industry. With approximately 90 percent of its lots controlled through options and virtually no owned land, NVR generates return on equity of roughly 34 percent, nearly double the industry average. Its stock trades above $7,000 per share and has been one of the best-performing equities of the past two decades. But NVR operates in fewer markets, builds fewer than 23,000 homes per year, and is entirely dependent on third-party developers for its lot supply. It cannot replicate D.R. Horton's national breadth or self-supplied lot pipeline through Forestar.

PulteGroup generates the highest gross margins among large-volume builders, consistently in the 28 to 30 percent range, driven by a focus on move-up and active adult segments (its Del Webb brand competes directly with D.R. Horton's Freedom Homes). But PulteGroup builds fewer than a third of D.R. Horton's volume and has a narrower geographic footprint. Toll Brothers serves the luxury market with average selling prices near $977,000 and is relatively insulated from mortgage rate sensitivity, since many of its buyers pay cash, but its 10,813 annual closings represent a completely different business model.

Lennar is the closest competitor in scale, with $34.2 billion in fiscal 2025 revenue and over 80,000 homes closed. In a notable validation of D.R. Horton's strategic playbook, Lennar completed the spin-off of Millrose Properties in February 2025, distributing approximately 80 percent of its land assets into a separately traded REIT that functions much like Forestar. Lennar's adoption of the asset-light model that D.R. Horton pioneered through Forestar is perhaps the most telling competitive signal of all: when your largest competitor restructures its entire business to replicate your strategy, you know you are doing something right.

Key Performance Indicators for Ongoing Monitoring

For investors tracking D.R. Horton's performance going forward, three KPIs stand above the rest.

First, net sales orders growth, both in units and dollars. This is the most forward-looking indicator of demand health and pricing power, since orders precede closings by several months. When orders accelerate, the next quarter's revenue is likely to follow. When orders decelerate, management has limited ability to offset the impact. The first quarter of fiscal 2026 showed orders growing 3 percent year over year, a tentative positive signal after several quarters of pressure.

Second, home sales gross margin, which captures the net impact of pricing, incentive costs (especially rate buydowns), and input cost inflation. Gross margin is where the tension between volume growth and profitability plays out in real time. The compression from approximately 30 percent in fiscal 2022 to 20 percent by late 2025 tells the story of the current cycle more clearly than any other single number.

Third, cancellation rate, which signals buyer confidence and the effectiveness of the company's affordability strategies. A rising cancellation rate is the earliest warning sign that the market is deteriorating faster than management can respond. D.R. Horton's cancellation rate peaked at 32 percent during the initial rate shock and has since moderated to approximately 20 percent, which management considers consistent with historical norms.

XIII. Final Analysis: "If We Were Management"

What makes D.R. Horton special in American homebuilding is not any single innovation but the compounding of many disciplined decisions over nearly half a century. The customization insight of 1978. The acquisition playbook of the 1990s. The survival and institutional learning of the 2008 crisis. The Express Homes revolution of 2014. The Forestar vertical integration of 2017. The rate buydown arsenal of 2022 onward. Each built upon the last, creating a company that is simultaneously the largest, the most diversified, the most affordable, and among the best-capitalized homebuilders in the country.

If sitting in the CEO's chair in Fort Worth today, the opportunities are clear. Technology and construction innovation remain underpenetrated in homebuilding. Modular and prefabricated construction techniques, 3D printing, automated design tools, and smart home integration represent potential efficiency gains that could further widen the cost gap between national builders and local operators. D.R. Horton's scale makes it the natural first adopter of any technology that reduces construction costs or cycle times.

Geographic expansion into underserved markets remains an avenue for growth. While 36 states is an extraordinary footprint, there are metro areas within those states and in other states where D.R. Horton has limited or no presence. Tuck-in acquisitions in these markets, following the proven playbook, can add incremental volume without the risk of transformative deals. The company has been notably disciplined about not making acquisitions in the current environment, with no major deals announced since Truland Homes in July 2023, suggesting that management is waiting for better entry points rather than paying up for growth.

The build-for-rent segment is still in its early innings. Single-family rental construction represents approximately 8 percent of total US single-family housing starts. With institutional demand for single-family rental product growing and the company's construction capacity already in place, expanding rental operations is a capital-efficient way to monetize land positions and smooth revenue through housing cycles. The risk of regulatory intervention in institutional single-family ownership bears monitoring, but the underlying demand for rental housing, driven by affordability constraints and lifestyle preferences, appears durable.

A less discussed but potentially transformative opportunity lies in construction technology. The homebuilding industry remains one of the least technologically advanced sectors of the American economy. Labor productivity in residential construction has been essentially flat for decades, even as manufacturing productivity has soared. Modular construction, where sections of a home are built in a factory and assembled on-site, could reduce construction times by 30 to 50 percent while improving quality consistency. 3D printing of structural components is moving from novelty to early commercial viability. Automated design tools powered by artificial intelligence can optimize floor plans for material efficiency, energy performance, and construction speed. D.R. Horton, with its scale and standardized construction processes, is the natural first mover for any of these innovations. A technology that saves $2,000 per home in construction cost would be worth over $170 million in annual pre-tax savings at current volume.

Perhaps the most important strategic question facing management is how to navigate the tension between affordability and profitability. Mortgage rates, while declining from their peaks, remain well above the sub-3 percent environment that fueled the 2020 and 2021 boom. Rate buydowns are effective but costly. Smaller floor plans are prudent but limit revenue per unit. The company that figures out how to deliver quality new homes at price points that the median American household can afford, while still generating returns on equity that exceed its cost of capital, will define the next era of American homebuilding. D.R. Horton, with its history of saying yes when the customer asks for a bay window, is as well positioned as any company in the industry to be that builder.

There is a through-line that connects every chapter of this story. From the bay window in 1978 to the Express home in 2014 to the rate buydown in 2023, the unifying principle has always been the same: figure out what the ordinary American homebuyer needs, and find a way to deliver it profitably at scale. That sounds simple. It is not. The graveyard of failed homebuilders who tried and could not execute is long and well-populated.

Donald Horton built his first home in Fort Worth with $3,000, a bank loan, and the instinct that ordinary Americans wanted someone who would listen to them. Nearly five decades and more than a million homes later, the company that bears his name remains, at its core, an enterprise devoted to giving American families something they can call their own.

XIV. Recent News

The first quarter of fiscal 2026, reported in January 2026, showed D.R. Horton generating $6.89 billion in revenue from 17,818 home closings, with earnings per share of $2.03, modestly beating consensus estimates. Net sales orders grew 3 percent year over year, the first positive order growth in several quarters, suggesting that lower mortgage rates are beginning to stimulate demand. Home sales gross margin of 20.4 percent remained under pressure from continued rate buydown costs.

The mortgage rate environment has shifted meaningfully. After six Federal Reserve rate cuts totaling approximately 175 basis points through 2025, mortgage rates have edged toward 6 percent, briefly dipping below that threshold in late February 2026 for the first time in years.

This matters enormously for D.R. Horton. Every quarter-point decline in mortgage rates expands the pool of qualified buyers and reduces the cost of rate buydown incentives. If rates continue to moderate toward the 5.50 to 5.75 percent range that Morgan Stanley projects by mid-2026, the double benefit of expanded buyer demand and reduced incentive costs could drive meaningful gross margin improvement. The spring selling season of 2026 will be the critical test of whether the rate environment has turned sufficiently to reignite order momentum.

The full fiscal year 2025, which ended September 30, told a story of resilience under pressure. Revenue of $34.3 billion declined 6.9 percent from the prior year as the company managed through sustained affordability headwinds. Net income of $3.59 billion, while down nearly 25 percent, still represented robust profitability by any standard outside the extraordinary pandemic-era margins. The company returned $4.8 billion to shareholders through a combination of $4.3 billion in buybacks and $495 million in dividends, an aggressive capital return program that reflected management's confidence in the balance sheet even during a challenging period.

Management issued and reaffirmed fiscal 2026 guidance of $33.5 to $35.0 billion in revenue and 86,000 to 88,000 home closings, with home sales gross margin guidance of 19.0 to 19.5 percent for the full year. CEO Paul Romanowski has emphasized community-by-community incentive management and the spring selling season as the key determinant of margin trajectory for the year. The cancellation rate of 20 percent in the fourth quarter of fiscal 2025 was described as "in line with historical averages."

The stock has experienced meaningful volatility. After reaching an all-time closing high of approximately $194 in September 2024, shares have traded as low as $110 over the subsequent 52 weeks. The pullback of roughly 20 percent from the highs reflected a combination of earnings misses in certain quarters, margin compression from sustained incentive costs, and cautious forward guidance. The market currently values D.R. Horton at approximately 15 times earnings, a modest multiple relative to the broader S&P 500 but reflecting genuine cyclical risk concerns.

On the regulatory front, a February 2026 Supreme Court ruling invalidated a broad swath of tariffs imposed under the International Emergency Economic Powers Act, potentially reducing builder input costs for lumber, cabinets, and other imported materials. Prior to the ruling, tariffs had been estimated to add up to $17,500 per home in construction costs. However, the company flagged immigration enforcement as a risk to construction labor supply, and proposed restrictions on institutional single-family home buyers remain a potential overhang on the rental operations segment. No major acquisitions have been announced since the Truland Homes deal in July 2023, with capital being directed toward organic growth, share repurchases, and dividends.

XV. Links & Resources

Company Filings & Investor Relations - D.R. Horton Investor Relations: investor.drhorton.com - D.R. Horton Annual Reports and SEC Filings - Forestar Group Investor Relations: investor.forestar.com - D.R. Horton Q4 FY2024 and Q1 FY2026 Earnings Releases

Industry Research & Data - NAHB Eye on Housing: Top Ten Builder Market Share Analysis - Harvard Joint Center for Housing Studies: Homebuilding Industry Concentration Study - Zillow Research: US Housing Deficit Reports (2024-2025) - Freddie Mac Research: Housing Supply Undersupply Analysis - NAHB Housing Economics: Housing Shortage Data