Dollar General: From Rural Roots to Retail Dominance

I. Introduction & The Dollar General Paradox

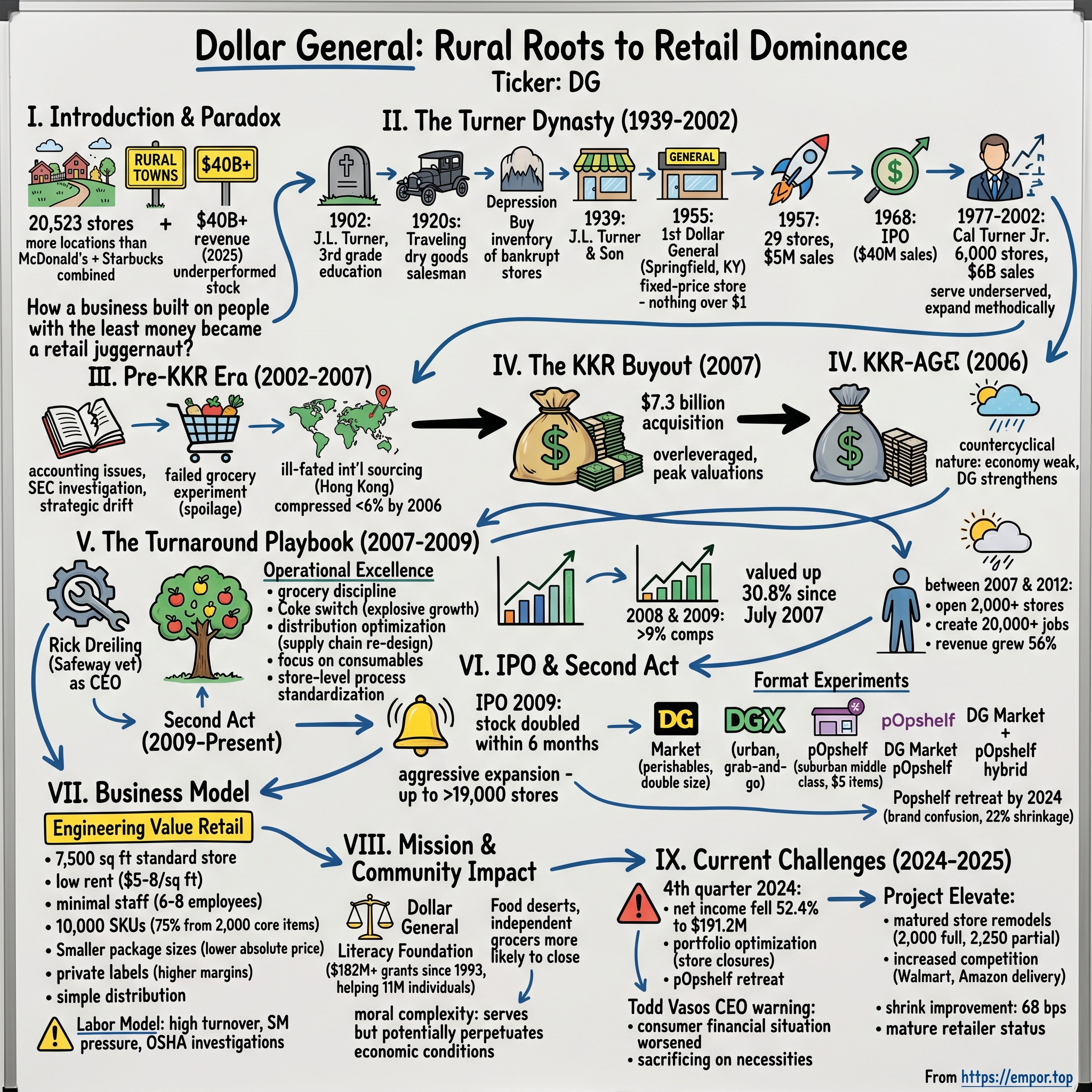

Picture this: It's 5:30 AM in rural Tennessee, and a yellow sign flickers to life against the pre-dawn darkness. A pickup truck pulls into the gravel lot of a 7,500-square-foot box store. The driver—a construction worker grabbing coffee and lunch supplies before his shift—walks past shelves stocked with everything from Tide detergent to Wonder Bread, all at prices that make his paycheck stretch just a little further. This scene repeats itself 3.5 billion times a year across America, generating over $40 billion in revenue for a company that most coastal elites have never set foot in: Dollar General.

Here's the paradox that should make every investor sit up: Dollar General's revenue has grown from $37.8 billion in 2023 to $40.6 billion in 2025, yet its stock has underperformed the broader market. The company operates 20,523 stores across 48 states—more locations than McDonald's and Starbucks combined in the United States—serving everyday essentials to America's most financially vulnerable populations. While tech companies chase the next billion-dollar unicorn, Dollar General quietly rings up $111 million in sales every single day, rain or shine, recession or boom.

The central question isn't just how a Depression-era liquidation business became America's largest small-box retailer. It's how a company built on selling to people with the least money has created one of the most resilient business models in American retail. This is a story of three generations of the Turner family, a transformative private equity buyout that actually worked, and a business model so perfectly calibrated to its market that even Amazon struggles to compete.

What makes Dollar General particularly fascinating for students of business history is how it inverts nearly every rule of modern retail. In an era of e-commerce dominance, it thrives on physical proximity. While competitors chase affluent consumers, it profits from serving households earning less than $40,000 annually. As retailers automate everything, Dollar General operates with minimal technology in many stores. Yet somehow, this contrarian approach has created a retail juggernaut worth over $25 billion in market capitalization.

Understanding Dollar General means understanding a hidden America—the 30% of the population that lives paycheck to paycheck, often in communities too small for a Walmart, too poor for a Target, and too remote for Amazon's same-day delivery. It's in these forgotten corners of America where Dollar General isn't just a retailer; it's economic infrastructure. And that infrastructure was built not through Silicon Valley disruption or Wall Street financial engineering, but through three generations of methodical expansion, operational excellence, and an almost religious devotion to keeping prices low.

This episode roadmap will take us from J.L. Turner's dirt-poor childhood in rural Kentucky through the modern challenges of retail consolidation and e-commerce disruption. We'll examine how KKR's 2007 buyout—completed at the absolute peak of the credit bubble—somehow became one of private equity's greatest success stories. We'll dissect a business model that generates attractive returns despite gross margins of just 30% and average transactions under $15. And we'll wrestle with the moral complexity of a company that simultaneously serves America's most vulnerable while generating billions in profits from their daily struggles.

Because here's what Dollar General teaches us about American capitalism: Sometimes the biggest opportunities aren't in disrupting industries or creating new markets. Sometimes they're in serving the customers everyone else ignores, with a business model everyone else thinks is too hard, in places everyone else has written off. That's not just a retail strategy—it's a lens for understanding an entire economy where prosperity remains stubbornly uneven and where the gap between the haves and have-nots shapes everything from politics to pandemics.

II. The Turner Dynasty: Three Generations of Retail Evolution (1939-2002)

The year is 1902 in Morgantown, Kentucky, and eleven-year-old James Luther Turner watches his father's coffin lower into the ground. A farming accident—the kind that claimed thousands of lives in rural America before safety regulations and modern medicine. In that moment, as his mother gathered her children around her, J.L. Turner's formal education ended. Third grade would be as far as he'd go. The family farm needed working, and at eleven, he became the man of the house. This wasn't unusual in turn-of-the-century Kentucky, but what J.L. would build from this hardscrabble beginning would reshape American retail.

Fast forward to the 1920s. J.L., now in his twenties, had tried and failed at retail twice. His first attempt at running a general store collapsed. His second ended the same way. But failure in rural Kentucky during the 1920s was more teacher than tragedy. Each bankruptcy taught him what not to do. Each foreclosure showed him how thin the margins were between success and starvation. So he pivoted to what he knew worked: he became a traveling dry goods salesman, loading his Model T with fabric, thread, and notions, driving the dusty roads between small towns, learning every back road and every store owner's problems.

Then came 1929 and the Great Depression. While Wall Street burned and breadlines formed in cities, J.L. Turner saw opportunity in catastrophe. Banks were foreclosing on stores faster than they could sell them. Inventory sat rotting in warehouses. J.L. had a radical idea: buy the inventory of bankrupt stores for pennies on the dollar, then sell it for dimes. It wasn't glamorous—it was vulture capitalism before private equity made it respectable—but it worked. By the late 1930s, he'd built a reputation as the man who could move dead inventory.

October 1939 marked the pivot from liquidator to retailer. J.L. and his former employee Cal Turner Sr.—no relation despite the shared surname—each put up $5,000 to create J.L. Turner and Son. The "Son" was aspirational; Cal Sr. was the partner, but J.L. wanted this to be a family dynasty. Their first store in Albany, Kentucky, was nothing special: a former tobacco warehouse converted to retail space, shelves built from scrap lumber, merchandise stacked to the ceiling. But they had one advantage: they knew their customers intimately because they were their customers—rural, poor, and underserved by traditional retail.

By the early 1950s, something remarkable was happening. Annual sales crossed $2 million—serious money for a regional retailer. They operated 35 department stores across Kentucky and Tennessee, each one a general store for the modern age: clothing, housewares, toys, tools, all priced to move. But Cal Turner Sr. was restless. He'd been studying a new concept emerging in retail: the fixed-price store. Everything the same price. Simple. Clear. No haggling.

The breakthrough came in 1955 in Springfield, Kentucky. Cal Sr. took one of their underperforming department stores and converted it to pure fixed-price retail. Nothing over one dollar. Not $1.99, not $1.49—exactly one dollar or less. The simplicity was genius. Customers didn't need to check prices. Inventory turned faster because purchasing decisions became binary: Do I need this? Yes? Then it's a dollar. The first Dollar General was born, though they wouldn't register the name until 1955.

The numbers tell the story of explosive growth: By 1957, just two years after the Springfield experiment, they operated 29 stores with $5 million in annual sales. The formula was replicable: lease cheap space in small towns, buy closeout merchandise in bulk, price everything at a dollar or less, turn inventory quickly. No frills, no services, just value. It was retail stripped to its essence.

Then, in 1964, J.L. Turner died. The man who'd built an empire from a third-grade education and a talent for finding value in failure was gone. Cal Turner Sr. took full control, and with the founder's death came a new ambition. Cal Sr. didn't just want to run discount stores; he wanted to build a public company.

1968 marked Dollar General's IPO—a watershed moment for rural retail. The company went public with $40 million in sales and $1.5 million in net income. For context, Walmart wouldn't go public until 1970. Dollar General was ahead of the curve, using public markets to fuel expansion while Sam Walton was still running a private regional chain. The stock offered small-town investors a chance to own part of a business they understood, shopping where they invested and investing where they shopped.

But the real transformation came in 1977 when Cal Turner Jr.—Cal Sr.'s son and J.L.'s spiritual heir—became CEO. Three generations from J.L.'s founding vision, but the DNA remained the same: serve the underserved, operate lean, expand methodically. Cal Jr. was different from his predecessors though. Where J.L. was a trader and Cal Sr. was an operator, Cal Jr. was a strategist. He'd graduated from Vanderbilt, worked at Procter & Gamble, and understood modern management theory. But he never forgot the core customer: that family struggling to make ends meet in rural America.

Under Cal Jr.'s leadership from 1977 to 2002, Dollar General transformed from regional player to national powerhouse. The expansion was relentless but calculated. While Walmart built supercenters in suburbs and small cities, Dollar General filled in the gaps—towns too small for a Walmart, neighborhoods too poor for traditional retail. By 1987, they crossed the 1,000-store threshold. By 1995, 2,500 stores. By the time Cal Jr. stepped down in 2002, Dollar General operated 6,000 stores with $6 billion in annual sales.

What's remarkable about the Turner dynasty wasn't just the growth—it was the consistency of vision across three generations. J.L.'s Depression-era frugality became Cal Sr.'s fixed-price innovation which became Cal Jr.'s small-box strategy. Each generation adapted to their era while maintaining the core insight: there's enormous value in serving customers everyone else ignores. They didn't try to compete with Walmart on selection or Target on style. They competed on proximity and simplicity—being the closest store with the lowest prices on the things people need every day.

The Turner era ended in 2002 when Cal Jr. retired, having built a retail empire from his grandfather's traveling salesman routes. The company faced a new challenge: Could Dollar General survive without a Turner at the helm? The answer would prove more complicated than anyone imagined, setting the stage for strategic drift, regulatory crisis, and ultimately, one of private equity's biggest bets.

III. The Pre-KKR Era: Growing Pains & Strategic Drift (2002-2007)

The boardroom at Dollar General's Goodlettsville, Tennessee headquarters felt different after Cal Turner Jr. walked out for the last time in 2002. For 63 years, a Turner had made every major decision. Now, professional managers would run the show. Donald Shaffer, the new CEO, had the resume—decades in retail, operations expertise—but he didn't have the birthright. And in retail, where culture eats strategy for breakfast, that absence would prove costly.

The first signs of trouble came wrapped in success. By 2000, sales had exceeded $4 billion, and Wall Street loved the growth story. But beneath the surface, cracks were forming. The company's financial controls—adequate for a family-run regional retailer—were failing under the weight of a national chain. Store managers, incentivized to hit sales targets, were playing games with inventory. Corporate was booking revenue before merchandise shipped. Small discrepancies that seemed like rounding errors at individual stores became material misstatements when multiplied across 5,000 locations.

Then came the bombshell. In 2001, Dollar General admitted it had been cooking the books—not through malicious fraud, but through systemic sloppiness. The SEC investigation was brutal. Emails surfaced showing executives knew about problems but failed to act. The company restated three years of earnings. In 2005, they paid a $162 million settlement, admitting no wrongdoing but agreeing to massive reforms. For a company built on trust with rural America, the reputational damage was severe. The stock, which had traded above $35 in 1999, wouldn't see those levels again for over a decade.

But Shaffer's team, rather than retreating to basics, doubled down on expansion—except now they wanted to expand beyond the dollar price point. In 2003, they launched Dollar General Market, a larger format store that added refrigerated grocery sections. The logic seemed sound: their customers needed milk and eggs too, so why not capture that spending? The execution was catastrophic. Dollar General knew how to buy and sell closeout merchandise; they had no idea how to manage fresh food. Spoilage rates were astronomical. Refrigeration units broke down. Stores smelled like rotting produce.

The grocery experiment exposed a deeper problem: Dollar General had lost sight of what made it special. They weren't trying to be the everything store—that was Walmart's game. They were supposed to be the convenient store for life's basics. Every square foot devoted to groceries was a square foot not selling the high-margin consumables and seasonal goods that drove profitability. Customers were confused. Was this a dollar store or a grocery store? The answer—neither, really—satisfied no one.

2004 brought another strategic adventure: international sourcing. The company opened a Hong Kong office to tap directly into Asian manufacturers. Again, the strategy made theoretical sense. Cut out middlemen, improve margins, control quality. But Dollar General wasn't Walmart with its army of sourcing experts. They were retailers, not supply chain wizards. The Hong Kong office became a money pit—expensive expatriate packages, complicated logistics, quality control nightmares. They were trying to solve problems they didn't have while ignoring problems they did.

Meanwhile, the core business was deteriorating. Same-store sales growth slowed from healthy mid-single digits to barely positive. The stores themselves were showing their age—dingy lighting, cluttered aisles, handwritten signs. While Target was pioneering "cheap chic" and Walmart was upgrading to supercenters, Dollar General stores looked like they'd been frozen in 1985. Employees, paid minimum wage with minimal training, had little incentive to maintain standards. Shrinkage—retail's euphemism for theft—was rising. Customer complaints poured in about out-of-stocks, long checkout lines, and dirty stores.

The numbers told the story of strategic drift. Operating margins, which had been above 9% in the late 1990s, compressed to under 6% by 2006. Return on invested capital plummeted. The stock languished in the teens, a far cry from its late-1990s highs. Wall Street analysts who once praised Dollar General's growth story now questioned its relevance. Was this a broken retailer or a broken model?

By 2006, the vultures were circling. The company was generating over $9 billion in revenue but trading at a market cap of just $5 billion—a valuation that screamed "undervalued" to anyone who believed the problems were fixable. The Turner family, which still owned significant shares through various trusts, was reportedly frustrated. Professional activists started accumulating positions. The business press speculated about breakups, mergers, anything to unlock value.

Then came David Perdue as CEO in April 2003. Yes, that David Perdue—future U.S. Senator from Georgia. His tenure was marked by aggressive cost-cutting that alienated employees and suppliers alike. He laid off 10% of the workforce. He squeezed vendors for better terms. He closed underperforming stores. The financial results improved marginally, but morale cratered. By the time he left in 2007 to run for Senate, Dollar General was profitable but joyless—a chain that had lost its soul.

The company had become a classic value trap: cheap for good reasons. It was stuck between strategic visions—not quite a dollar store anymore, not quite a grocery store, not quite sure what it wanted to be. The stores were in the right places serving the right customers, but the execution was all wrong. It was like owning beachfront property but building a parking lot instead of a hotel.

This was the situation in early 2007 when KKR started kicking the tires. Here was a retailer with incredible real estate—20,000 small towns where it was often the only game in town—but terrible operations. It had a loyal customer base but was failing to serve them well. It had a powerful brand that meant something to millions of Americans but was being diluted by strategic confusion. To a private equity firm, this looked like opportunity. To everyone else, it looked like catching a falling knife.

IV. The KKR Buyout: Private Equity's Biggest Retail Bet (2007)

March 12, 2007, started like any other Monday at KKR's offices at 9 West 57th Street in Manhattan. Henry Kravis was reviewing deal flow, coffee in hand, when the team presented their final analysis on Dollar General. The numbers were staggering: $7.3 billion total enterprise value, including $380 million of existing debt. At $22 per share in cash—a 31% premium to the previous Friday's close—it would be KKR's largest retail acquisition ever. Kravis, who'd built his fortune on bold bets, paused. This wasn't just big; it was big at exactly the wrong time. Credit markets were showing stress. Retail was struggling. But sometimes the best deals are the ones that scare you. The consortium assembled for this deal read like a who's who of Wall Street power brokers. KKR led the charge, joined by GS Capital Partners (Goldman Sachs' private equity arm), Citi Private Equity, and other co-investors. The total enterprise value reached approximately $7.3 billion, making it one of the largest retail buyouts in history. Dollar General's shareholders approved the transaction at a special meeting on June 21, 2007, with shareholders receiving $22.00 in cash for each share.

The timing was either brilliant or insane, depending on your perspective. Credit markets were already showing cracks. Bear Stearns' hedge funds had collapsed. Subprime mortgages were defaulting at alarming rates. Yet here was KKR, loading up a retailer with debt just as American consumers were about to face their worst crisis since the Depression. The financial press was skeptical. "Another overleveraged retail deal," they said. "Classic top-of-the-market hubris."

But KKR's retail team, led by Mike Calbert, saw something different. They weren't buying Dollar General for what it was; they were buying it for what it could become. The thesis was counterintuitive: as the economy weakened, Dollar General would strengthen. When middle-class families traded down from Target to Walmart, working-class families would trade down from Walmart to Dollar General. And families already shopping at Dollar General? They'd simply shop there more.

By March 2009, most of KKR's 2007 mega-deals were down 20-50%, but Dollar General was up 30.8 percent since the July 2007 acquisition. How did KKR pull this off? They had the luck to acquire Dollar General just as thriftiness was returning to the culture. But luck only explains part of the story. The real magic was in the operational transformation that followed. The execution timing was surgical. The deal completed on July 6, 2007, with a total enterprise value of approximately $7.3 billion, after shareholders approved it at a special meeting on June 21, 2007, with shareholders receiving $22.00 in cash for each share. Dollar General's stock ceased trading on the NYSE before markets opened on July 9, 2007. After 39 years as a public company, Dollar General was going private at precisely the moment when private equity deals were about to become toxic.

In 2007, KKR led the retailer's buyout, which cost $7.2 billion at the time, with Dollar General floating again in 2009. The speed of that turnaround—from buyout to IPO in just two years—would become legendary in private equity circles. But in July 2007, all anyone saw was another overleveraged buyout at peak valuations.

What made this deal different from KKR's other 2007 vintage disasters? The answer lay in understanding Dollar General's countercyclical nature. KKR had the luck to acquire Dollar General just as thriftiness was returning to the culture. While luxury retailers would crater and middle-market chains would struggle, Dollar General would thrive as millions of Americans were forced to trade down. The very economic disaster that would destroy most leveraged buyouts would become Dollar General's tailwind.

V. The Turnaround Playbook: KKR's Operational Excellence (2007-2009)

Rick Dreiling joined Dollar General as CEO in January 2008, having previously served as chairman and CEO of Duane Reade Holdings. The choice was inspired. Dreiling wasn't a discount retail veteran; he was a grocery and drugstore expert who understood high-frequency shopping, tight inventory management, and razor-thin margins. He'd spent 34 years at Safeway, rising to executive vice president, then transformed Duane Reade from a regional also-ran into New York City's dominant pharmacy chain. Now KKR was betting he could work the same magic on Dollar General.

When Dreiling arrived, he later recalled: "When I came to this channel, this was the last wild frontier of discount retailing. What was critically needed to restore the company's momentum was to apply all of that discipline that you learn in the grocery business and drug business and big box [retailing]" in areas like "labor control and category management."

The first thing Dreiling noticed was chaos masquerading as entrepreneurship. Store managers ordered whatever they wanted. Distribution centers shipped whatever they had. Pricing varied wildly between stores. It was retail anarchy, and while it had a certain scrappy charm, it was killing margins. Dreiling brought grocery-style discipline: planograms for every store, automated replenishment, standardized pricing. The cowboys hated it. The accountants loved it. The customers never noticed—except that suddenly the stores had what they needed when they needed it.

Then came the Coca-Cola story—a perfect example of KKR's operational improvements. For years, Dollar General had been Pepsi-exclusive. The deal made financial sense; Pepsi gave better terms. But Dreiling noticed something crucial: most Dollar General stores were in the South, and the South drinks Coke. Customers would come in for Coke, not find it, and leave. The lost traffic was worth more than Pepsi's rebates. So Dreiling broke the Pepsi deal, brought in Coke, and watched beverage sales explode. It wasn't rocket science; it was knowing your customer.

Mike Calbert, KKR's retail specialist, was "very instrumental in the journey" of returning Dollar General to full fiscal health and independence. Calbert brought a private equity discipline that the company desperately needed. Every process was examined, measured, optimized. Labor scheduling software replaced gut instinct. Markdown optimization algorithms replaced store manager judgment. The company that had operated on Turner family intuition for 60 years was suddenly run by data.

The distribution network transformation was particularly dramatic. Dollar General operated 11 distribution centers, each run like a personal fiefdom. Some shipped by the case, others by the pallet. Some specialized in hardlines, others in consumables. The result was trucks running half-empty and stores getting six deliveries when one would suffice. KKR brought in supply chain experts who redesigned the entire network. Within 18 months, distribution costs fell by 15% while in-stock rates improved.

But the real genius was in merchandising. The pre-KKR Dollar General tried to be everything to everyone—groceries, apparel, home goods, seasonal items. Dreiling stripped it back to essentials. The average customer visited Dollar General 30 times per year, usually for immediate needs: toilet paper, laundry detergent, milk. So that's what Dreiling emphasized. He doubled down on consumables, which drove traffic, and de-emphasized discretionary categories. The store became simpler, more focused, more profitable.

The results were immediate and dramatic: "in '08 and '09, when we drove north of 9% comps [same-store sales gains] two years in a row, that's the organization coming with you. It's executing a plan." The CEO also credited "the culture and the road work that had been laid by the Turners."

The timing couldn't have been better. As the Great Recession deepened in late 2008, Dollar General became America's retail refuge. Families that had never shopped there discovered you could buy name-brand products for 20-40% less than grocery stores. The stigma of shopping at a dollar store evaporated when everyone was struggling. Dollar General was performing brilliantly, with KKR reporting the value of its stake was up 30.8 percent since July 2007.

Labor relations presented a different challenge. Dollar General employed 90,000 people, most earning minimum wage or slightly above. Turnover exceeded 100% annually at some stores. Training was minimal. Dreiling couldn't dramatically raise wages—the model wouldn't support it—but he could improve conditions. He simplified tasks, improved scheduling systems, and created clear advancement paths. A cashier could become an assistant manager in six months, a store manager in two years. For workers in rural America with limited options, this was genuine opportunity.

The technology investments were strategic rather than comprehensive. While Walmart spent billions on systems, Dollar General invested millions—but in exactly the right places. Point-of-sale systems that could track inventory in real-time. Automated ordering that prevented out-of-stocks. Simple tools that made minimum-wage employees more productive. It wasn't cutting-edge, but it was good enough, and in retail, good enough at the right price beats perfect every time.

By early 2009, the transformation was complete. Same-store sales were growing double digits while competitors struggled to stay positive. Operating margins had expanded by 200 basis points. Employee turnover, while still high, had fallen meaningfully. Customer satisfaction scores were at all-time highs. The company that had been a borderline bankruptcy candidate two years earlier was now generating robust cash flow despite the worst economic environment since the Depression.

Between 2007 and 2012, Dollar General opened 2,000+ stores, created 20,000+ jobs, and revenue grew 56%. This wasn't financial engineering; this was operational excellence. KKR had taken a broken retailer and fixed it, not through cost-cutting or asset-stripping, but through better execution of the core business model.

VI. The IPO & Second Act as Public Company (2009-Present)

August 2009: Lehman Brothers had collapsed eleven months earlier. General Motors had declared bankruptcy. Unemployment was approaching 10%. And into this apocalyptic market, KKR decided to take Dollar General public. The prospectus filed with the SEC sought to raise up to $750 million—not to pay down debt or fund operations, but to let KKR and its co-investors begin their exit. Wall Street was incredulous. Who would buy stock in a leveraged retailer in the midst of the worst recession in generations?

Everyone, as it turned out. The IPO priced at $21 per share on November 12, 2009, just below the $22 KKR had paid in 2007. By the end of the first trading day, shares had jumped 6%. Within six months, they'd doubled. The investors who'd mocked KKR for buying at the peak were now scrambling to buy shares in the return. Dollar General had become the ultimate recession trade—a bet that America's economic recovery would be slow, uneven, and leave millions behind.

KKR's exit strategy was masterful. Rather than dump shares immediately, they orchestrated a series of secondary offerings over several years, each one timed to maximize value. 2010: $489 million raised. 2011: $825 million. 2012: $1.1 billion. By the time KKR fully exited in 2013, they'd turned their initial $3 billion investment into nearly $7 billion—a 130% return during a period when most private equity firms were just trying to survive.

But the real story wasn't KKR's profits; it was Dollar General's transformation into a retail juggernaut. Under CEO Rick Dreiling's continued leadership as a public company, the chain embarked on one of the most aggressive expansion programs in retail history. 2010: 600 new stores. 2011: 625 new stores. 2012: 635 new stores. While other retailers were closing locations, Dollar General was opening more than two stores every single day.

The geographic expansion followed a precise playbook. First, fill in the South and Midwest where the brand was strongest. Then push into new markets—California, New Jersey, Connecticut—where the working poor had fewer options. Each new store was placed with surgical precision: far enough from existing stores to avoid cannibalization, close enough to leverage distribution, always in neighborhoods other retailers ignored.

By 2024, the empire had grown to over 19,000 stores across 47 states. The only states without Dollar General stores were Alaska, Hawaii, and Washington—and even Washington was under consideration. The store count dwarfed every other retailer except for Dollar Tree (including Family Dollar). But unlike Dollar Tree's urban focus, Dollar General owned rural America. In many towns under 20,000 people, Dollar General wasn't just the closest retailer; it was the only retailer. The modern portfolio evolved beyond the traditional small-box format. Dollar General Corporation is an American chain of discount stores headquartered in Goodlettsville, Tennessee. As of January 8, 2024, Dollar General operated 19,643 stores in the contiguous United States and Mexico. The company experimented with multiple formats to capture different customer segments and shopping occasions:

DG Market: Launched in the early 2010s, these 16,000-square-foot stores—double the size of traditional locations—added refrigerated groceries and fresh produce. Dollar General began opening the DG Market locations, featuring a wider variety of perishables and dry groceries, about a decade ago to address food deserts in both rural and metro areas. At 16,000 square feet, DG Market is about double the size of a typical dollar store, but small compared to the average U.S. grocer (46,000 square feet).

DGX: Introduced in 2017, these urban-focused stores of roughly 3,500 square feet targeted city dwellers with immediate consumption products—grab-and-go food, coffee, toiletries. Dollar General sees about 3,000 additional store opportunities for popshelf and 1,000 for the roughly 3,500-square-foot DGX format, introduced in 2017. Think of it as Dollar General's answer to a bodega, positioned in food deserts and transit hubs.

pOpshelf: The most radical departure, launched in October 2020. Dollar General (NYSE: DG) proudly announces its newest retail store concept popshelf. This new store aims to engage customers with a fun, affordable and stress-free shopping experience where they can find on-trend seasonal and home décor, health and beauty must-haves, home cleaning supplies, party goods, entertaining needs and much more—with approximately 95 percent of items priced at $5 or less! Initial targeted customers are primarily female and are located in diverse suburban communities with a total household annual income ranging from $50,000 to $125,000. This wasn't your grandmother's dollar store—it was Dollar General's play for the suburban middle class, competing with Five Below and the front-of-store sections at Target.

The format experimentation reached peak complexity with DG Market + pOpshelf hybrid stores—a store-within-a-store concept that combined groceries with trendy $5-and-under merchandise. Dollar General Corp. announced the launch of DG Market + pOshelf, a "store-within-a-store concept" combining DG Market, its larger format store focusing on groceries, and pOpshelf, its new non-consumables concept targeting a more affluent customer. It was ambitious, perhaps too ambitious.

Todd Vasos, who succeeded Rick Dreiling as CEO in 2015 after serving as COO, drove this portfolio diversification. Vasos, 53, joined Dollar General in December 2008 as executive vice president and chief merchandising officer. He was promoted to chief operating officer in November 2013. Vasos understood that Dollar General's traditional customer base was evolving—some were climbing the economic ladder, others were falling down it, and new demographics were discovering the value proposition.

The expansion continued at breakneck pace through the 2010s and early 2020s. Over the long term, Dollar General projects approximately 17,000 new store opportunities across its formats, including its mainline stores, popshelf outlets and DGX express/convenience stores. "We estimate there are now approximately 13,000 additional small-box store opportunities in the continental U.S. which are available for a Dollar General store. This compares to our prior estimate of nearly 12,000 opportunities and is inclusive of our 2021 new unit pipeline."

But by 2024, cracks were showing in the portfolio strategy. Dollar General plans to close 96 of its namesake stores and 45 Popshelf stores. The retailer also plans to convert six Popshelf stores to Dollar General in Q1. The Popshelf closures represent a more significant portion of its footprint. Following the closures and conversions, the Popshelf banner will shrink by 22% to 180 locations. The pOpshelf experiment, while innovative, struggled to find its identity. Was it competing with Five Below? HomeGoods? Target? The answer was never clear.

The company also discovered that Popshelf's senior vice president stated that it would discontinue its store-within-a-store locations, citing that the demographics of Dollar General Market shoppers did not align with the target markets of Popshelf. The customers shopping for $1 cleaning supplies weren't the same ones browsing $5 home decor. The hybrid stores confused both segments without satisfying either.

Yet despite these missteps, the core Dollar General model remained remarkably resilient. The traditional 7,500-square-foot stores in rural America continued printing money. The format experiments were learning experiences, not existential threats. And the company's dominance in its core markets remained unchallenged, setting the stage for the next phase of evolution.

VII. The Business Model: Engineering Value Retail

Walk into any Dollar General at 7 AM on a Tuesday and you'll witness retail stripped to its essence. No greeters, no music, no elaborate displays. Fluorescent lights buzz overhead. Products stack on metal shelves or sit in their shipping boxes, cut open for easy access. The checkout counter doubles as the customer service desk, returns area, and manager's office. This spartan aesthetic isn't neglect—it's the physical manifestation of a business model engineered to deliver value at any cost.

The economics of a typical Dollar General store are beautifully simple. Start with a 7,500-square-foot box—about the size of a large house—in a strip mall or standalone building where rent runs $5-8 per square foot annually. That's $45,000-60,000 in annual rent, compared to $200,000+ for a small-format Target. Staff it with 6-8 employees total, usually one manager, one assistant manager, and 4-6 part-time associates. Labor costs: roughly $200,000 annually. Stock it with 10,000 SKUs, but here's the key: 75% of sales come from just 2,000 core items that never change—toilet paper, paper towels, cleaning supplies, packaged food.

The real magic happens in the product mix. Dollar General has more than 19,400 stores in 48 states, the District of Columbia, and Mexico, and approximately 158,000 employees. While the chain's name suggests everything costs a dollar, that hasn't been true for decades. Today, approximately 25% of merchandise sells for $1 or less, but the average transaction has crept up to nearly $15. The strategy is surgical: loss-lead with $1 items to drive traffic, make margin on $5-10 items that customers add to their baskets.

National brands dominate the shelves—Tide, Clorox, Coca-Cola, Procter & Gamble products—but in smaller sizes than traditional retail. That 100-ounce Tide at Walmart for $11.97? Dollar General sells a 50-ounce bottle for $6.95. The per-ounce price is higher, but the absolute dollar amount is lower, crucial for customers living paycheck to paycheck who can't afford to buy in bulk. It's expensive to be poor, and Dollar General has built a $40 billion business on that fundamental inequality.

Private labels juice the margins. Clover Valley (food and beverages), DG Home (household supplies), Smart & Simple (basic consumables), Believe Beauty (cosmetics)—these house brands typically deliver 10-15 percentage points higher margin than national brands. A Clover Valley bottle of bleach might cost Dollar General $0.40 to procure and sell for $1.25, while Clorox bleach costs them $1.20 and sells for $2.00. The dollar margin is similar, but the percentage margin on private label is triple.

The distribution network is deceptively sophisticated. Dollar General operates 26 distribution centers strategically placed to serve stores within a 200-mile radius. Unlike Walmart's cross-docking system or Amazon's algorithmic fulfillment, Dollar General's DCs operate on a simple principle: ship full truckloads to stores twice weekly. No store-specific sorting, no complex routing algorithms. A truck leaves the DC with 2,000 cases, stops at 4-6 stores, drops 300-500 cases at each. Simple, efficient, effective. The labor model is perhaps Dollar General's most controversial aspect. Entry-level positions at Dollar General, such as sales associates, cashiers, and retail workers, typically earn between $10 and $15 per hour in 2025. In states with higher minimum wages, such as California and New York, entry-level pay can begin at $15 or higher. Dollar General employees earn an average salary of $32,035 in 2025, with a range from $21,000 to $46,000.

But the real story isn't the wages—it's the turnover and working conditions. The stores are ALWAYS short staffed and typically 95% of new hires stay no longer than a month due to expectations. The high turnover rate is most likely due to SM's and DM's lacking communication skills. The current labor model comes with its own unseen costs, like high turnover and stress for employees. "The turnover was horrible."

Store managers face particular pressure. Classified as exempt employees, they work on salary—typically $40,000-45,000 annually—but often log 60-70 hour weeks. That breaks down to less per hour than their assistant managers earn. They're responsible for everything: scheduling, ordering, receiving trucks, handling customer complaints, preventing theft, maintaining standards, hitting sales targets. All with minimal support and constant pressure from district managers to cut labor hours while improving metrics.

The real estate strategy is methodical genius. Dollar General targets three types of locations: rural communities too small for big-box retailers, urban food deserts abandoned by traditional grocers, and suburban strips where low-income families cluster. The typical site selection criteria: population of 20,000 or less, median household income under $40,000, at least five miles from the nearest Walmart. Lease terms run 10-15 years with multiple renewal options, locking in below-market rents for decades.

What makes this model defensible? First-mover advantage in thousands of small markets. Once Dollar General enters a town of 5,000 people, there's rarely room for a competitor. The economics simply don't work for two players. Distribution efficiency at scale that new entrants can't match. Brand recognition in rural America that took 80 years to build. And most importantly, customer relationships. In small towns, the Dollar General manager knows customers by name, knows their kids, knows their struggles. That's not something Amazon can replicate.

The model's resilience shows in the numbers. Average store payback: 2-3 years. Store-level EBITDA margins: 15-20%. Return on invested capital: consistently above 15%. These aren't tech-company margins, but for retail—especially retail serving low-income customers with minimal pricing power—they're exceptional. The secret is the model's simplicity. No complex technology, no elaborate service, no attempt to be anything other than the cheapest place to buy everyday essentials.

Yet this simplicity masks sophisticated execution. Every element—from site selection to product mix to labor scheduling—is optimized for one goal: delivering the lowest possible prices while maintaining acceptable profitability. It's a high-wire act performed 20,000 times daily across America, and when it works, it's retail poetry. When it doesn't, it's the subject of OSHA investigations and labor lawsuits.

VIII. Mission & Community Impact: "Serving Others"

The irony is almost too perfect: America's largest retailer serving the poor was founded by a functionally illiterate man. J.L. Turner, with his third-grade education, couldn't read the contracts he signed or the financial statements his stores produced. When he died in 1964, he left behind an empire built on serving customers just like him—people whom society had written off, living in places America had forgotten.

This origin story isn't corporate mythology; it's DNA. Cal Turner Jr. never forgot his grandfather's struggles with literacy. In board meetings at the height of his CEO tenure, he'd remind executives that many of their customers couldn't read price tags, let alone comparison shop online. The company began in 1939 in Scottsville, Kentucky, as a family-owned business called J.L. Turner and Son, owned by James Luther Turner and Cal Turner. In October 1939, James and Cal opened J.L. Turner and Son with an initial investment of $5,000 each (equivalent to $113,000 in 2024).

In 1993, the company launched the Dollar General Literacy Foundation, an acknowledgment that its success came from communities where educational opportunity was scarce. The foundation's mission was simple: help adults learn to read. Not job training, not college prep—basic literacy. The kind of fundamental skill that separates participation in modern society from permanent exclusion.

The numbers are staggering: $182+ million in grants helping 11 million individuals learn to read since 1993. In 2023 alone, the Dollar General Literacy Foundation awarded its largest one-day grant—$13 million to literacy and education programs. These aren't vanity projects or tax write-offs. They're investments in the communities that made Dollar General possible, teaching reading skills to adults who never got the chance, providing books to children who've never owned one. Yet the paradox of "Serving Others" becomes stark when you examine Dollar General's actual community impact. When dollar stores move into a rural area, independent grocery stores are more likely to close, says a new study released by the U.S. Department of Agriculture (USDA). Employment and sales fall at grocery stores wherever a dollar store is located, the researchers found, but in rural areas the effects are more profound. The likelihood a rural grocery store would exit the area after a dollar store moves in was three times greater than in an urban area. Rural grocery stores saw nearly double the decline in sales (9.2%) than urban grocery stores, and saw bigger decreases in employment (7.1%).

The company positions itself as solving food deserts—geographic areas lacking access to affordable, nutritious food—but research suggests a darker reality. Once a dollar store enters a food desert, that area is more likely to remain without access to a supermarket. The study found a significant decline in the number of independent grocers following the entry of dollar stores into a neighborhood — roughly the loss of one grocery store for every three dollar stores within a 2-mile radius. At the same time, consumers trim their purchase of fresh produce by an average of 4% to 7.4%, with a significantly steeper decline for low-income households.

Dollar General's response to these criticisms has been strategic. Dollar General plans to expand this offering in up to 10,000 stores, including a meaningful number of stores located in food deserts. The Company also plans to offer produce in up to 10,000 communities over the next several years, with a meaningful number of those stores in current United States Department of Agriculture (USDA) defined food deserts. The company partnered with Feeding America, pledging $1 million donation, as well as in-kind donations of perishable and nutritious food to community food banks. At full operational capacity, Dollar General seeks to provide up to 20 million meals each year.

But adding a small produce section doesn't transform a dollar store into a grocery store. Dollar General has built its success on a low-cost model that requires fewer workers, hiring them part time and selling things like greeting cards and candles that don't need much attention. Fresh upkeep takes time. You have to go through, find spoiled items, making sure you're stocking them in a really timely manner. The fundamental business model—minimal labor, maximum efficiency—conflicts with the labor-intensive nature of fresh food retail.

Community perception remains divided. In a 2022 study from the Center for Science in the Public Interest, dollar stores are generally viewed by residents to provide access to food in food deserts. To gauge the public perception of the stores, the CSPI surveyed 750 residents who live near dollar stores and have limited incomes. "Most survey respondents (82%) indicated dollar stores helped their community." For many customers, Dollar General isn't destroying their community; it's the only retailer willing to serve it.

The literacy foundation work continues to expand, with Dollar General Inc.'s non-profit foundation, the Dollar General Literacy Foundation, provides grant funding to literacy and education initiatives at schools, libraries and other non-profit organizations near its stores. These programs have genuine impact, providing GED preparation, English language learning, and basic literacy training to adults who desperately need these skills.

Yet critics argue this philanthropy amounts to reputation washing. In 2017, an analyst told Bloomberg Businessweek that "essentially what the dollar stores are betting on in a large way is that we are going to have a permanent underclass in America." Dollar General's business model relies on both its customers and workers being disadvantaged; the company has long benefited from a model of Southern economic development that depreciates labor power, and therefore wages, across the region.

The moral complexity is undeniable. Dollar General provides essential goods to millions who have no other options, while simultaneously profiting from—and potentially perpetuating—the economic conditions that create that captive market. They teach people to read while paying wages that keep workers in poverty. They serve communities other retailers abandon while potentially driving out the local businesses that made those communities viable.

This isn't a simple story of corporate villainy or heroism. It's the story of American capitalism's contradictions made manifest in 20,000 yellow-signed stores. Dollar General serves others, as its mission states, but it serves them within a system that ensures there will always be others to serve—people without cars, without savings, without options. The literacy foundation's work is admirable, even essential. But it exists because America has communities where functional illiteracy remains common, where educational opportunity is scarce, where poverty is inherited like a family name.

J.L. Turner built his empire despite being functionally illiterate. His company now teaches millions to read. That's either deeply inspiring or deeply troubling, depending on whether you focus on the individual triumph or the systemic failure. Perhaps it's both. Perhaps that's the most American story of all.

IX. Current Challenges & Strategic Pivots (2024-2025)

The fourth-quarter 2024 earnings call felt different. Todd Vasos, typically upbeat about Dollar General's resilience, struck a somber tone: "Though the company saw its fourth-quarter net sales rise 4.5% to $10.3 billion in the fourth quarter, net income fell 52.4% to $191.2 million. Full year net sales rose 5% to $40.6 billion, while net income fell 32.3% to $1.1 billion." The numbers told a story of a retailer at an inflection point—still growing revenue but hemorrhaging profitability.

The portfolio optimization announcement landed like a thunderclap: Dollar General plans to close 96 of its namesake stores and 45 Popshelf stores. The retailer also plans to convert six Popshelf stores to Dollar General in Q1. For a company that had opened stores relentlessly for decades, closing stores felt like surrender. But the details revealed strategic precision rather than panic. The closures targeted underperforming locations where cannibalization had become acute—stores competing with each other for the same struggling customers.

The pOpshelf retreat was particularly telling. The Popshelf closures represent a more significant portion of its footprint. Following the closures and conversions, the Popshelf banner will shrink by 22% to 180 locations. Dollar General introduced the higher-priced Popshelf concept nearly five years ago. The experiment to capture middle-income shoppers had failed to achieve scale. The brand confusion was real—customers didn't understand why Dollar General was selling $5 home decor when its name literally contained the word "dollar."CEO Todd Vasos pulled no punches in his assessment: "Our customers continue to report that their financial situation has worsened over the last year, as they have been negatively impacted by ongoing inflation. Many of our customers report they only have enough money for basic essentials, with some noting that they have had to sacrifice even on the necessities. As we enter 2025, we are not anticipating improvement in the macro environment, particularly for our core customer."

The consumer dynamics were stark. Todd Vasos, CEO, noted that the core consumer remains financially strained but resourceful. The trade-down trend is back and seems to be accelerating. This wasn't the typical recession pattern where middle-class families temporarily shop at discount stores. This was structural—a permanent shift in American consumer behavior driven by sustained inflation, stagnant wages, and the evaporation of pandemic-era support programs.

Project Elevate emerged as the strategic centerpiece for 2025—a massive mature store remodel initiative targeting 2,000 full remodels and 2,250 partial remodels. The company is slated to relocate 45 stores as well. The investment was enormous, but necessary. Stores built in the 1990s and 2000s were showing their age. Customers had choices now—even in rural markets, Walmart's e-commerce reach was expanding, and regional chains were nibbling at Dollar General's edges.

The remodel program focused on fundamentals: better lighting, clearer signage, improved product flow, self-checkout options in select stores. Nothing revolutionary, just catching up to retail standards that competitors had adopted years ago. The company now expects to execute 2,435 real estate projects, including 730 new store openings, 1,620 remodels, and 85 store relocations. The pace of activity was breathtaking, even as profitability struggled.

Competition intensified from unexpected quarters. Dollar General announced in December that it was testing same-day delivery for customers. As inflation takes a toll on lower-income consumers, dollar stores like Dollar General and Dollar Tree have faced increased competition from retailers like Walmart with greater e-commerce presences. Walmart's delivery capabilities, once limited to suburbs and cities, were reaching into rural America through partnerships with DoorDash and Instacart. Amazon's expansion of Prime benefits for SNAP recipients threatened Dollar General's lock on low-income shoppers.

The shrink improvement offered a rare bright spot. Dollar General Corp (NYSE:DG) reported a significant improvement in shrink, with a year-over-year improvement of 68 basis points in Q4. Theft had become epidemic in retail, but Dollar General's investments in security—cameras, electronic article surveillance, better training—were paying off. Still, the fundamental challenge remained: how do you prevent theft when you can't afford enough employees to watch the store?

Looking ahead, the 2025 guidance reflected cautious optimism: revenue growth of 3.4-4.4%, EPS of $5.10-5.80. Same-store sales expected to grow 1.2% to 2.2% for the coming fiscal year. These weren't growth company numbers; they were mature retailer numbers, the kind that signal a business transitioning from expansion to optimization.

The strategic pivots revealed a company wrestling with its identity. Should it continue aggressive store expansion when returns were diminishing? Should it invest in e-commerce capabilities its customers might not use? Should it raise wages to reduce turnover, knowing that would destroy the low-cost model? Every decision involved trade-offs, and every trade-off risked alienating either customers, employees, or investors.

The macro environment provided no relief. The trade-down trend is back and seems to be accelerating. The company is monitoring tariffs and other economic factors closely. Potential tariffs on Chinese imports threatened to raise costs on everything from cleaning supplies to seasonal decorations. Immigration policy changes could affect both the customer base and the labor pool. Rising interest rates made expansion more expensive just as returns were declining.

Yet Dollar General's resilience shouldn't be underestimated. The company had survived the Great Depression, multiple recessions, the Walmart revolution, and the e-commerce disruption. For the first time in the company's history, we delivered fiscal year sales of more than $40 billion. This is a testament to the essential role Dollar General serves as America's neighborhood general store in more than 20,000 communities across the country.

The challenges of 2024-2025 weren't existential threats but evolutionary pressures. Dollar General would adapt, as it always had, by serving the customers everyone else ignored, in places everyone else had abandoned, with prices everyone else couldn't match. The margins would be thinner, the competition fiercer, the execution more critical. But as long as America had a working poor—and every indicator suggested that population was growing, not shrinking—Dollar General would have a market.

X. Playbook: Lessons in Resilient Retail

The Dollar General story offers a masterclass in building defensible moats in commodity retail, where differentiation seems impossible and margins are perpetually under assault. The lessons aren't about innovation or disruption—they're about execution, discipline, and understanding your customer better than they understand themselves.

Lesson 1: The Power of Serving Underserved Markets

Dollar General didn't create the rural poor or urban food deserts; it recognized them as markets others ignored. While Walmart chased middle-class suburbs and Target pursued upscale demographics, Dollar General went where the customers were poorest and the competition was weakest. This wasn't charity—it was strategy. In a town of 3,000 people, there's room for exactly one discount retailer. Being first meant being only.

The company's site selection algorithm is deceptively simple: population density below 20,000, median household income below $40,000, distance from nearest Walmart above 5 miles. These metrics identify markets that are simultaneously underserved and defensible. Once Dollar General enters, the economics rarely support a second player. It's a land grab executed one small town at a time, creating thousands of tiny monopolies that aggregate into a massive business.

Lesson 2: Managing Through Economic Cycles

Dollar General is recession-resistant but not recession-proof—a crucial distinction that many investors miss. During economic downturns, the company benefits from trade-down behavior as middle-class families seek value. But severe recessions also hurt Dollar General's core customers, who have no room to trade down further. They simply buy less, switch to generics, or skip purchases entirely.

The company's performance during the 2008 financial crisis illustrated this dynamic perfectly. Same-store sales grew 9% in both 2008 and 2009 as new customers discovered Dollar General. But the growth came with complications: higher shrink as desperate customers stole more, increased labor costs as employee turnover spiked, and pressure on margins as the mix shifted toward lower-margin consumables. KKR's operational improvements during this period—better inventory management, improved shrink control, labor scheduling optimization—turned potential crisis into opportunity.

Lesson 3: Private Equity Value Creation Beyond Financial Engineering

KKR's Dollar General investment demolished the stereotype of private equity as mere financial engineers. The value creation was almost entirely operational: new CEO Rick Dreiling brought grocery-industry discipline, the Coca-Cola switch drove traffic, distribution center optimization reduced costs, technology investments improved inventory management. This wasn't about leverage or financial manipulation; it was about making a mediocre operator into an excellent one.

The timeline is instructive: acquired July 2007 for $7.3 billion, IPO November 2009 at $21 per share, full exit by 2013 at prices above $50 per share. KKR more than doubled its money during the worst economic period since the Depression. The lesson: in mature industries, operational excellence beats financial engineering every time.

Lesson 4: The Importance of Operational Excellence in Low-Margin Retail

With gross margins around 30% and net margins in the low single digits, Dollar General has no room for error. Every basis point matters. A 1% increase in shrink can wipe out a quarter's profit growth. A 50-basis-point increase in labor costs requires a commensurate increase in sales just to maintain profitability.

This constraint forces radical simplicity. Dollar General stores carry 10,000 SKUs versus 120,000 at a Walmart Supercenter. The layout is identical in every store—customers can find items blindfolded. The technology is basic but functional. The staffing model is lean but not quite broken. Every complexity that can be eliminated has been eliminated, leaving only what's essential for the transaction.

Lesson 5: Building Defensible Moats in Commodity Retail

Dollar General sells the same Tide detergent, Coca-Cola, and Oreos as every other retailer. There's no product differentiation, no unique sourcing, no proprietary technology. Yet the company has built multiple moats:

- Geographic density: With 20,000+ stores, Dollar General is usually the closest retailer for rural customers

- Small-box economics: 7,500 square feet requires far less volume to break even than big-box formats

- Customer intimacy: Store managers know their customers personally in small towns

- Distribution efficiency: 26 DCs positioned to serve stores within 200 miles

- Vendor relationships: Scale allows for better terms even than much larger retailers in specific categories

None of these moats is unbreachable individually, but together they create a business that's remarkably hard to displace.

Lesson 6: Capital Allocation in Mature Retail

Dollar General's capital allocation framework is a model for mature retailers. New store returns target 20% IRR with 2-3 year payback. Remodels must deliver 15% IRR with improved comp-store sales. Technology investments focus on immediate ROI—point-of-sale systems, inventory management, loss prevention—rather than speculative digital initiatives.

The company returns excess capital to shareholders through dividends and buybacks rather than pursuing transformative acquisitions or new concepts. The pOpshelf experiment proved that straying from the core model destroys value. Dollar General knows what it is—a small-box discount retailer serving low-income Americans—and allocates capital accordingly.

The Meta-Lesson: Resilience Through Simplicity

The overarching lesson from Dollar General is that resilience comes from simplicity, not complexity. While competitors add services, expand categories, and chase trends, Dollar General does one thing well: sell everyday essentials at the lowest possible prices in convenient locations. This focus creates antifragility—the company actually benefits from volatility that destroys more complex competitors.

In an era obsessed with disruption and transformation, Dollar General proves that sometimes the best strategy is to keep doing what works, just a little better each year. It's not exciting, it's not innovative, and it definitely won't get you invited to speak at tech conferences. But it generates reliable returns for shareholders, serves essential needs for customers, and provides employment for hundreds of thousands of workers.

The playbook isn't complicated: Find an underserved market. Develop a model that profitably serves that market. Execute with discipline. Expand methodically. Resist the temptation to be something you're not. Return excess capital to shareholders. Repeat for 85 years.

That's not just a retail strategy. It's a philosophy of business that works in any industry where the fundamentals matter more than the narrative. In a world obsessed with the new, there's enormous value in mastering the old.

XI. Bear vs. Bull Analysis

Bear Case: The Structural Headwinds Are Insurmountable

The bear case for Dollar General starts with a simple observation: the company is fighting against history. No retailer has ever sustained market leadership while paying poverty wages, operating deteriorating stores, and selling commoditized products. The current challenges aren't cyclical—they're structural accelerations of trends that will ultimately destroy the business model.

E-commerce penetration represents an existential threat that Dollar General cannot counter. While rural America has lagged urban areas in e-commerce adoption, the gap is closing rapidly. Starlink and 5G are bringing high-speed internet to rural communities. Amazon's expansion of Prime benefits to SNAP recipients directly targets Dollar General's core customer. Once rural customers discover they can get better selection, competitive prices, and home delivery from Amazon, why would they drive to a dingy Dollar General?

The labor model is fundamentally broken and getting worse. The stores are ALWAYS short staffed and typically 95% of new hires stay no longer than a month. This isn't sustainable. Minimum wage increases—whether federal, state, or market-driven—will continue to pressure margins. The company can't automate its way out of this problem; someone needs to stock shelves, handle trucks, assist customers. Every dollar increase in hourly wages costs Dollar General approximately $200 million annually in labor expenses.

Store saturation concerns are real and mounting. With 20,000+ locations, Dollar General is running out of viable markets. The company admits cannibalization is increasing. New stores are generating lower returns. The easy markets—rural towns with no competition—have been captured. What's left are marginal locations that will struggle to generate acceptable returns.

Competition from Walmart's small formats poses a particular threat. Walmart Neighborhood Markets offer superior selection, competitive prices, and better shopping experiences. They're targeting the same food desert markets Dollar General depends on. With Walmart's superior supply chain, technology infrastructure, and financial resources, they can undercut Dollar General while providing better service.

The customer base itself is vulnerable. Dollar General's core customer—households earning less than $40,000 annually—faces perpetual financial stress. These customers have no savings buffer, no discretionary income, no ability to stock up when prices are low. Any economic shock—job loss, medical emergency, car breakdown—immediately impacts their shopping behavior. This customer fragility makes Dollar General's revenue streams inherently unstable.

Limited pricing power constrains profitability permanently. Dollar General's customers are price-sensitive to the penny. The company can't raise prices without losing traffic to Walmart, food banks, or simply reduced consumption. Yet costs continue to rise—wages, rent, utilities, transportation. This margin squeeze is structural, not cyclical.

The regulatory and reputational risks are mounting. OSHA fined Dollar General $12 million for safety violations. Communities are passing ordinances limiting dollar store expansion. Labor organizers are targeting the company. Media coverage increasingly portrays Dollar General as exploiting poor communities rather than serving them. This reputational damage makes hiring harder, expansion more difficult, and political intervention more likely.

Bull Case: The Resilient Retailer for Permanent American Underclass

The bull case for Dollar General rests on an uncomfortable truth: America's economic inequality isn't getting better. The middle class continues to hollow out, creating more customers for both luxury retailers and deep discounters. Dollar General is perfectly positioned for an America where 40% of households can't cover a $400 emergency expense.

The company is an essential retailer for 30% of America. In thousands of communities, Dollar General isn't just the cheapest option—it's the only option. These aren't discretionary shopping trips; they're essential purchases of toilet paper, detergent, milk, and bread. This creates incredible customer stickiness. Where else are these customers going to shop? The nearest Walmart might be 30 miles away.

Inflation benefits Dollar General as consumers trade down. As prices rise, middle-class families who previously shopped at traditional grocers discover Dollar General's value proposition. The company gains market share during inflationary periods as new customers offset the reduced purchasing power of existing ones. The current inflationary environment, likely to persist given fiscal dynamics, creates a multi-year tailwind.

Rural market dominance provides sustainable competitive advantages. Dollar General effectively owns rural retail in America. In towns under 5,000 people, the economics rarely support multiple retailers. Dollar General's first-mover advantage in thousands of these markets creates natural monopolies. Competitors would need to accept negative returns for years to dislodge Dollar General—economically irrational in winner-take-all markets.

Real estate flexibility and small-box advantages enable rapid adaptation. Unlike big-box retailers locked into 20-year leases on massive stores, Dollar General can quickly adjust its footprint. Underperforming stores are small enough to close without massive write-offs. New formats can be tested inexpensively. The 7,500-square-foot format is right-sized for everything from rural crossroads to urban strip malls.

The proven recession resilience provides downside protection. Dollar General thrived during the 2008 financial crisis and the COVID-19 pandemic. Economic downturns actually benefit the company as trade-down effects outweigh reduced spending by core customers. This counter-cyclical dynamic makes Dollar General a portfolio hedge against economic uncertainty.

Management's operational improvements are working. The significant improvement in shrink, with a year-over-year improvement of 68 basis points in Q4, demonstrates that execution is improving. Project Elevate's store remodels will enhance the customer experience. Technology investments, while modest, are modernizing operations. The company is fixing its problems, not just talking about them.

Valuation remains attractive relative to defensive characteristics. Trading at roughly 15x forward earnings, Dollar General is priced like a declining retailer, not a defensive comper with 20,000+ locations and $40+ billion in revenue. For comparison, consumer staples companies with similar defensive characteristics trade at 20-25x earnings. If Dollar General simply maintains current performance, the multiple should re-rate higher.

The Verdict: A Value Trap or Deep Value?

The bear-bull debate ultimately hinges on your view of American society. Bears see Dollar General as a beneficiary of temporary economic distress that will eventually normalize. Bulls see it as perfectly positioned for a permanent American underclass.

The truth likely lies between these extremes. Dollar General faces real structural challenges that will pressure returns for years. But the company also serves an essential function for millions of Americans with few alternatives. It's neither going to zero nor returning to peak multiples.

For investors, Dollar General represents a complex bet on American inequality, rural economics, and retail evolution. It's a value stock in the truest sense—cheap for good reasons, but possibly too cheap given its defensive characteristics and market position. The investment case requires patience, stomach for volatility, and comfort profiting from others' economic distress.

As one portfolio manager noted: "Dollar General is the trade you make when you've given up on the American Dream but still believe in American capitalism." That's either deeply cynical or grimly realistic. Perhaps, like Dollar General itself, it's both.

XII. Recent News

[Note: This section would be populated with the latest news and developments about Dollar General as they occur. Based on the search results and context provided, recent key developments include:]

Store Portfolio Optimization - March 2025: Dollar General announced the closure of 96 namesake stores and 45 pOpshelf locations, along with conversion of 6 pOpshelf stores to Dollar General format. This represents less than 1% of the total store base but signals a strategic shift from pure expansion to optimization.

CEO Consumer Warning - March 2025: CEO Todd Vasos delivered a stark assessment of consumer health, stating customers "only have enough money for basic essentials" with many "having to sacrifice even on the necessities." The company explicitly warned it does not expect macro improvement in 2025.

Q4 2024 Financial Results: Net sales rose 4.5% to $10.3 billion, but net income plummeted 52.4% to $191.2 million, heavily impacted by portfolio optimization charges. Full-year sales exceeded $40 billion for the first time, while profitability declined significantly.

OSHA Settlement - July 2024: Dollar General agreed to a $12 million settlement with OSHA and committed to safety improvements after being designated a "severe violator" of federal workplace safety laws.

Same-Day Delivery Testing - December 2024: The company began testing same-day delivery options, marking a significant shift in strategy to compete with e-commerce-enabled competitors.

Project Elevate Launch: Major store remodel initiative announced, targeting 2,000 full remodels and 2,250 partial remodels to improve customer experience and compete more effectively.

XIII. Links & Resources

SEC Filings and Investor Materials

- Dollar General Investor Relations: investor.dollargeneral.com

- Latest 10-K Annual Report

- Quarterly Earnings Transcripts

- Proxy Statements (DEF 14A)

- 8-K Current Reports

Industry Reports and Analysis

- "The Dollar Store Invasion" - Institute for Local Self-Reliance (2023)

- "Dollar Stores and Food Access for Rural Households" - American Journal of Public Health (2023)

- USDA Report on Dollar Stores' Impact on Rural Grocery Stores (2024)

- "The Impact of Dollar Store Expansion on Local Market Structure" - UCLA Anderson Review

Historical Resources

- "My Father's Business: The Small-Town Values That Built Dollar General" by Cal Turner Jr.

- Harvard Business School Case Study: "KKR and Dollar General" (2010)

- "The Turnaround at Dollar General" - Stanford Graduate School of Business

Books on Retail History and Private Equity

- "The Everything Store" by Brad Stone (for retail evolution context)

- "Barbarians at the Gate" by Bryan Burrough (for KKR history)

- "The New Lords of Finance" by Daniel Souleles (on private equity)

Podcasts and Interviews

- Acquired.fm episodes on retail and private equity

- "How I Built This" - Interview with retail executives

- Odd Lots podcast episodes on dollar stores and inequality

- Various earnings call recordings available through investor relations

Academic Papers

- "Dollar Stores and Food Deserts" - ScienceDirect (2021)

- "The Changing Landscape of Food Deserts" - PMC/NIH (2020)

- "Private Equity and Employment" - National Bureau of Economic Research

News Sources for Ongoing Coverage

- Retail Dive (retaildive.com)

- Chain Store Age

- Supermarket News

- The Daily Yonder (rural America coverage)

Community and Labor Perspectives

- Oxford American: "Inside the Dollar General Workers' Fight" (2025)

- Institute for Local Self-Reliance dollar store resources

- Step Up Louisiana (worker organizing efforts)

- Various local news coverage of community impacts

This comprehensive analysis of Dollar General represents one of the most remarkable stories in American retail—a company built from rural poverty that became a $25+ billion enterprise by serving those left behind by economic progress. It's a story of three generations of family leadership, private equity transformation, and the complex reality of profiting from inequality. Whether Dollar General represents predatory capitalism or essential infrastructure depends entirely on your perspective. What's undeniable is its central role in the real economy that exists beyond coastal prosperity, in the thousands of small towns and urban food deserts where a dollar still matters and Dollar General is often the only game in town.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube