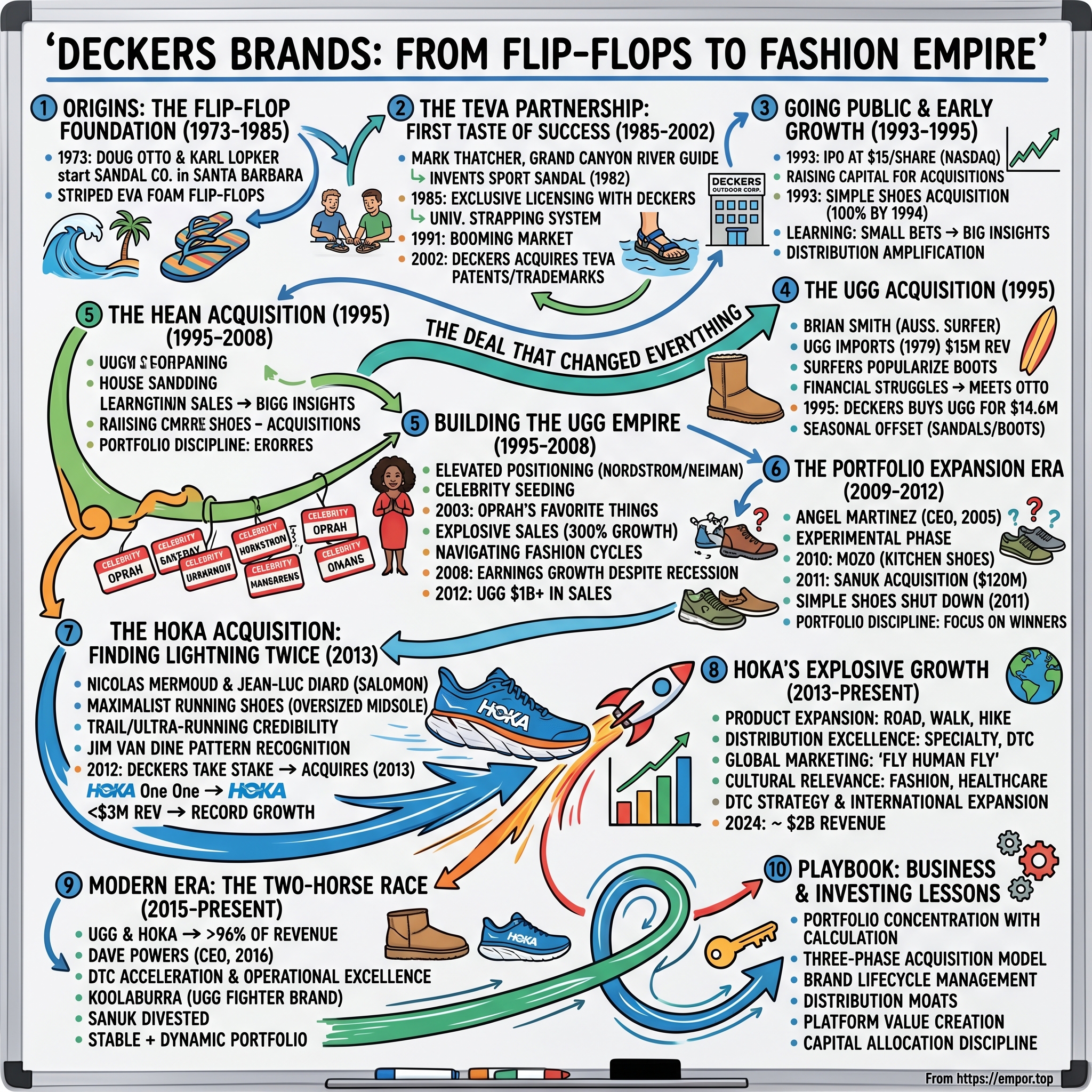

Deckers Brands: From Flip-Flops to Fashion Empire

I. Introduction & Episode Roadmap

Picture this: It's 2003, and Oprah Winfrey is about to unwittingly transform a quirky Australian sheepskin boot into a global fashion phenomenon. Meanwhile, in the French Alps, two trail runners are prototyping oversized running shoes that look like marshmallows strapped to feet. Neither moment seems particularly significant. Yet both would become billion-dollar chapters in one of the most unlikely portfolio success stories in American business.

Welcome to the story of Deckers Brands—a company that started selling striped flip-flops to California surfers in 1973 and somehow engineered its way into owning two of the most culturally significant footwear brands of the 21st century. With 2024 revenue hitting $4.92 billion and a market cap hovering around $16 billion as of April 2025, Deckers has quietly built one of the most efficient brand portfolios in consumer goods.

But here's what makes this story fascinating: Deckers didn't invent UGG or HOKA. They didn't even invent Teva. Instead, they perfected something arguably more difficult—the art of acquiring quirky, niche brands at exactly the right moment and transforming them into global phenomena. Think of them as the footwear world's Warren Buffett, if Buffett specialized in turning surfer boots and maximalist running shoes into luxury status symbols.

The company operates from an unassuming headquarters in Goleta, California—a sleepy coastal town better known for avocado farms than fashion empires. Yet from this beachside outpost, Deckers has orchestrated one of the great brand-building playbooks of modern retail. They've taken UGG from $17 million in sales to over a billion. They've grown HOKA from a $3 million ultra-running curiosity to nearly $2 billion in revenue in just over a decade.

How did they do it? The answer involves perfect timing, counterintuitive bets, and an almost preternatural ability to spot brands right before their inflection points. It's a story about understanding not just what consumers want today, but what they'll desperately need tomorrow—even if they don't know it yet.

Over the next few hours, we'll dissect every major move, from Doug Otto's first flip-flop experiments to the modern two-horse race between UGG and HOKA that's driving unprecedented growth. We'll explore the deals that worked spectacularly (UGG for $14.6 million might be the steal of the century), the ones that didn't (RIP MOZO Shoes), and the strategic frameworks that separate great acquirers from everyone else.

Most importantly, we'll unpack the lessons for investors and operators alike: How do you value a brand at its inflection point? When should you license versus acquire? How do you take something inherently niche—sheepskin boots, oversized running shoes—and make them mainstream without destroying their authenticity?

This isn't just a story about shoes. It's about portfolio construction, brand lifecycle management, and the delicate art of scaling culture. It's about a company that understood, decades before it became conventional wisdom, that the real money in footwear isn't in making shoes—it's in making meaning.

So buckle up. Or should we say, strap on your Tevas? Because we're about to walk through fifty years of footwear history, one perfectly timed acquisition at a time.

II. Origins: The Flip-Flop Foundation (1973–1985)

The year was 1973. Nixon was president, the oil crisis was reshaping America, and in Santa Barbara, California, two entrepreneurs named Doug Otto and Karl F. Lopker were about to start a footwear company with the most mundane of products: flip-flops.

But these weren't just any flip-flops. Otto, who had the restless energy of a true California entrepreneur, had developed a distinctive striped, layered design that caught the eye of the local surf community. The sandals featured multiple layers of colorful EVA foam that created a rainbow effect when viewed from the side—a small detail that would prove surprisingly important.

Santa Barbara in the early '70s was the perfect incubator for this kind of business. The town sat at the intersection of surf culture and casual California wealth, a place where barefoot was a lifestyle choice, not a necessity. Otto understood this market intimately. He wasn't trying to compete with athletic giants or fashion houses. He was simply trying to make the perfect sandal for walking from the parking lot to the beach.

The breakthrough moment came in 1975 during a business trip to Hawaii. Otto discovered that locals had already given his sandals a nickname: "deckas"—local slang derived from the sandals' stacked construction that resembled a wooden deck. It was one of those perfect accidents of branding. The name stuck, and later that year, Otto and Lopker officially incorporated as Deckers Corporation. The early years were marked by what Otto would later describe as "marginally successful" growth—the kind of modest, steady business that keeps the lights on but doesn't make headlines. The company was marginally successful in the early years and was incorporated in California in 1975 under the name Deckers Corporation. They sold at craft fairs, small surf shops, and anywhere else that would take their product. While at UCSB in 1973, Otto began producing sandals with classmate Karl F. Lopker, with Karl Lopker beginning his career making and selling flip-flops at craft fairs along the West Coast of the United States.

What's fascinating about this period is how unremarkable it was. There were no venture capital rounds, no Silicon Valley-style growth hacks. The initial capital was quite modest, with Doug Otto contributing $3,600 and Karl Lopker contributing $4,000. They also took out a loan of $8,000. Just two guys making sandals in a beach town, slowly building relationships with retailers, learning the unglamorous basics of footwear manufacturing and distribution.

The division of labor was clear from the start: Lopker oversaw manufacturing of the production while Otto was responsible for sales and distribution. This partnership would prove temporary—Lopker decided he wanted to work in software and was bought out by Otto in 1982—but it established the operational foundation that would serve Deckers for decades.

For twelve years, from 1973 to 1985, Deckers remained essentially what it started as: a small California sandal company with a clever name and a decent product. Revenue grew slowly, distribution expanded gradually, and the company built the operational muscles it would need for what came next. Because while Doug Otto didn't know it yet, a river guide in the Grand Canyon was about to walk into his life with an idea that would transform everything.

III. The Teva Partnership: First Taste of Success (1985–2002)

The Colorado River in 1982 was where modern adventure footwear was born, though nobody knew it at the time. Mark Thatcher, a geophysicist turned river guide, was watching his passengers constantly lose their flip-flops in the rapids. The solution seemed obvious to him: attach a heel strap to keep the sandal on the foot. So he grabbed an old pair of flip-flops, some Velcro from a hardware store, and created the world's first sport sandal in the back of his van. The name Teva—pronounced /ˈtɛvə/ TEH-və not /ˈtivə/ TEE-və in English; the name is based on Hebrew: טבע, meaning "nature"—perfectly captured what Thatcher was trying to create. But the path from invention to market dominance would prove anything but natural.

Thatcher's initial attempts at commercialization were a case study in entrepreneurial persistence. With a patent pending, Thatcher found a manufacturer, and began selling his "amphibious utility sandals" himself, travelling by car to outdoor equipment stores and directly to the rivers. He marketed them as amphibious utility sandals and sold 200 pairs the first year. Not exactly the stuff of Silicon Valley legend.

The first partnership with California Pacific, a shoemaker, quickly turned ugly. By 1984, however, word of mouth had begun to help increase Thatcher's sales, and California Pacific began to realize Teva's potential. The company tried to stake a claim to both the Teva name and to Thatcher's invention, stating that Thatcher was merely an employee of their firm. The issue ended up in court, and after a long and ugly legal battle, Thatcher finally won his case against California Pacific in 1985.

This is where Doug Otto and Deckers enter the picture. Fresh off his victory against California Pacific, Thatcher needed a new partner—someone who understood both manufacturing and brand building. In late 1985, Thatcher set up an exclusive licensing agreement with Deckers Corporation to manufacture and distribute Teva sandals. Deckers eventually obtained exclusive rights to Teva, including US patent #4,793,075 for the basic design and a trademark for the brand name.

The timing couldn't have been better. Outdoor sports were exploding in the mid-1980s. The same baby boomers who had embraced backpacking in the '70s were now discovering whitewater rafting, kayaking, and adventure travel. They had money, they wanted gear, and they were willing to pay for innovation.

Under Deckers' stewardship, Teva underwent a crucial evolution. The original design had a fatal flaw: the first Teva users often complained of blisters between the first and second toes caused by the thong-style strapping system. Deckers and Thatcher redesigned the product, creating what they called the "Universal Strapping System"—a configuration of straps that eliminated the toe post while keeping the sandal secure.

What's remarkable about the Teva story is how it created an entirely new category. Before 1985, there was no such thing as a "sport sandal." By 1991, it was a booming market segment. The company's products never truly hit it big, however, until a river guide by the name of Mark Thatcher brought Deckers his Teva sandal concept in 1985, and by 1991, outdoor sport sandals had become the latest footwear craze in the United States, with Teva strongly leading the pack in market share.

The success attracted the inevitable copycats. Soon Nike, Reebok, K-Swiss, Merrell, and Timberland all developed and offered their own versions of the sport sandal, which served to erode some of Teva's share of the market. The huge success of Nike's Air Deschutz sandal, for example, helped that company earn an almost 25 percent share of the then-$100 million sport sandal market by 1993.

But competition validated the category. What had started as a niche product for river guides was now a hundred-million-dollar market that the biggest names in footwear were fighting over. Deckers had proven they could spot a trend, partner with an inventor, and build a category-defining brand.

The relationship between Deckers and Thatcher evolved over seventeen years. What started as a licensing agreement gradually became something more integrated. Finally, on November 25, 2002, Deckers Outdoor Cooperation acquired the worldwide Teva patents, trademarks, and other assets from Mark Thatcher. The terms weren't disclosed, but Deckers now owned outright what had become one of the most recognizable outdoor brands in America.

The Teva experience taught Deckers several crucial lessons that would shape every acquisition that followed. First, timing matters more than invention—being first doesn't guarantee success, but being perfectly positioned when a market inflects does. Second, licensing can be a powerful way to test a brand relationship before committing to acquisition. Third, and perhaps most importantly, sometimes the best innovations come from outside the company—from river guides and surfers and ultra-runners who see problems that corporate R&D departments miss.

These lessons would prove invaluable when, in 1993, Deckers decided to go public and start hunting for their next big acquisition.

IV. Going Public & Early Growth (1993–1995)

The October morning in 1993 when Deckers went public wasn't particularly auspicious. In October of 1993 Deckers initiated a public offering of stock in its company at $15 per share and was incorporated as Deckers Outdoor Corporation. The NASDAQ was still recovering from the early '90s recession, tech stocks were just beginning their historic run, and here was a California sandal company asking investors to bet on flip-flops and river shoes.

But Doug Otto understood something fundamental: going public wasn't just about raising capital—it was about creating currency for acquisitions. The renamed Deckers Outdoor Corporation now had stock to use in deals, credibility with banks for leverage, and the transparency that would attract the kinds of brands they wanted to buy.

The IPO timing was actually brilliant. The company then finished the year on a high note, achieving $57.1 million in 1993 sales with net earnings of $6.3 million. For a company selling sandals—inherently seasonal products in most of the country—these were impressive numbers. The Teva brand was firing on all cylinders, having successfully defended its market position even as Nike and other giants entered the sport sandal category.

Otto's first move as CEO of a public company was telling. Rather than immediately pursuing a transformative acquisition, he made a small, strategic buy. In 1993, the company purchased a 50 percent share of Simple Shoes, Inc. for $10,000. Simple Shoes produced casual street shoes that were mainly marketed to the "twenty-something/Generation X" clientele. With the purchase, Deckers also began distributing the footwear line through its own existing channels.

Think about that price tag: $10,000 for half a company. This wasn't a typo—it was a test. Simple Shoes, founded by Eric Meyer in 1991, made eco-conscious footwear before sustainability was cool. The shoes featured recycled rubber soles, organic cotton uppers, and minimalist designs that appealed to the emerging alternative culture of the early '90s.

Early in 1994 the company acquired the remaining 50 percent interest in Simple Shoes for $1.5 million, and the entire company was added to Deckers's holdings alongside Teva and Sensi. The 150x increase in valuation in less than a year might seem like Otto got fleeced, but it was actually strategic. The initial stake let Deckers test the brand's potential through their distribution channels. Once they saw it could work, they paid up for full control.

The Simple acquisition taught Deckers several crucial lessons. First, small bets could yield outsized insights—you didn't need to risk millions to understand if a brand fit your portfolio. Second, the Generation X market was ready for something different than what the big athletic brands were offering. Third, and most importantly, Deckers' distribution network could dramatically amplify a small brand's reach.

By 1994, Deckers was running a fascinating portfolio experiment. They had Teva for outdoor enthusiasts, Simple for eco-conscious urbanites, and a small brand called Sensi that made affordable casual sandals. Deckers Outdoor Corporation develops, manufactures, and markets high performance footwear and apparel that is used for outdoor sports and recreation activities, as well as for casual wear. The company's products are marketed under the brand names of Teva, Simple, Sensi, and Picante. Teva markets outdoor sports sandals that utilize a patented strapping system and is widely recognized as the founder and market leader of the sport sandal category. Simple Shoes are comfortable, fashionable closed-toe street shoes, and Sensi manufactures modestly priced casual sandals.

What's remarkable about this period is how disciplined Deckers remained. They could have used their new public company status to make a splash acquisition, to overpay for growth. Instead, they methodically built capabilities—in sourcing, distribution, marketing—that would make them an attractive partner for brand owners looking to scale.

The stock market initially didn't know what to make of Deckers. Here was a company with strong profitability, decent growth, but in a category—sandals and casual footwear—that seemed inherently limited. Most analysts covering the stock in 1994 and early 1995 focused on the Teva brand's ability to maintain market share against Nike and Reebok.

What they missed was that Otto was hunting for something much bigger. While Wall Street debated sport sandal market share, Otto was having quiet conversations with an Australian surfer named Brian Smith who had built a quirky boot brand in Southern California. The Simple Shoes experiment had proven that Deckers could successfully integrate and scale an acquisition. The public markets had given them the currency to do a real deal.

The stage was set for the acquisition that would transform everything.

V. The UGG Acquisition: The Deal That Changed Everything (1995)

The scene at the Atlanta airport baggage claim in 1995 would become one of the most consequential meetings in footwear history. Brian Smith, the Australian surfer who had built UGG into a $15 million business over seventeen years, was exhausted. Doug Otto, fresh off taking Deckers public and flush with cash, was looking for his next big move. "I met him in Atlanta baggage reclaim, he had the money and I had the sales," Smith would later recall.

But the UGG story really began in 1979, when Smith, a chartered accountant turned surfer, arrived in Southern California with six pairs of Australian sheepskin boots and a dream. Surfing helped popularize the boots outside of Australia and New Zealand, when surfer Brian Smith started selling the boots in the US through UGG Holdings, Inc. in 1979. His first year? In their first season in business, UGG Imports sold 28 pairs of boots.

The early years were brutal. On his first sales trips, he went door-to-door to over 150 shops in SoCal, but they all turned him down, saying his product would never work next to flip-flops and board shorts. So Smith got creative, selling his boots pop-up-style from the back of his van while wearing them at Malibu Point Beach.

The breakthrough came when Smith finally understood his market. After a young surfer told him his glamorous marketing campaign "looked fake," Smith pivoted completely. He started booking shoots with semi and pro surfers. After almost 3 years of no traction in the market, UGG sales skyrocketed to $400,000 in a two month season.

By 1994, UGG had found its groove. By 1994, 80 percent of UGG's sales were in southern Orange County, but the company gained international attention after the boots were worn by the U.S. Olympic team in Lillehammer for the 1994 Winter Olympics. But success brought its own problems. We had a lot of bookings but not able to fulfill the orders because we didn't have the finances. It wasn't capitalized well from the beginning.

This is where the genius of the Deckers deal becomes apparent. Otto understood that UGG and Deckers were perfect complements: "his business died every winter and our business died in the summer." The seasonal offset meant Deckers could use its manufacturing and distribution infrastructure year-round.

The acquisition price seems almost quaint now: In 1995, Deckers Brands acquired Smith's business for $14.6 million and continued to expand it. For context, sales reached $15 million at the time of sale, meaning Deckers paid less than 1x revenue for what would become a billion-dollar brand.

What made Otto willing to bet on sheepskin boots when most Americans had never heard of them? The answer reveals the strategic framework that would guide every Deckers acquisition thereafter. First, the product had authentic roots—it wasn't manufactured demand but something surfers genuinely loved. Second, there was a clear path from niche to mainstream—if surfers loved them, maybe their girlfriends would too. Third, the brand had untapped pricing power—these weren't commodity products but lifestyle statements waiting to happen.

The integration was masterful. Deckers didn't try to immediately transform UGG into a fashion brand. Instead, they spent the late 1990s methodically building distribution, improving quality, and slowly expanding beyond the surf shops of Southern California. During the late 1990s, UGG began experiencing double-digit sales growth as Deckers developed the company into an international brand.

The real transformation would come later, but the foundation was being laid. Where Smith had struggled with capital and operations, Deckers brought professional management and deep pockets. Where Deckers had seasonal gaps and limited brand recognition, UGG brought authenticity and a rabid core customer base.

Looking back, Smith has no regrets about the sale: "I have no regrets, it was the right time and some interesting side stories with my decision... We made the deal, and the rest is history." He would later acknowledge that Constance Rishwain, who would lead UGG for Deckers, "deserves all the credit for taking it from 20 million up to a billion, because she had the skill from a fashion and product merchandising viewpoint to take it to the level that I could never have done."

The UGG acquisition would prove to be the deal that changed Deckers' trajectory forever. But in 1995, as the ink dried on the purchase agreement, nobody could have predicted that these funny-looking sheepskin boots would soon be on the feet of celebrities, featured on Oprah, and generating over a billion dollars in annual revenue. That transformation—from surf essential to global phenomenon—would become the template for everything Deckers did next.

VI. Building the UGG Empire (1995–2008)

The transformation of UGG from surfer essential to global phenomenon didn't happen overnight. It was a masterclass in brand building that took nearly a decade of patient cultivation before exploding into the stratosphere with one magical television moment in 2003.

When Deckers acquired UGG in 1995, the immediate challenge wasn't growth—it was education. Deckers took Ugg from $17 million a year in sales in 1995, when it bought Ugg Australia from Australian surfer Brian Smith, to a worldwide brand with a billion dollars in annual revenue now. But getting there required completely reimagining what the brand could be.

The first strategic move was counterintuitive: Instead of immediately pushing for mass market appeal, Deckers doubled down on the brand's authentic roots while subtly elevating its positioning. Positioning counts, when Deckers acquired Ugg from Smith, it moved Ugg away from its sporty roots, inking partnerships with retailers like Nordstrom and Neiman Marcus. Today its shoes are placed on shelves inches away from brands like Prada.

This wasn't just about getting into better stores—it was about changing the conversation around the product. The Bromley Group, a New York marketing agency hired by Deckers, continued Smith's strategy of celebrity endorsement and started shipping Uggs to movie sets in the hopes stars might wear them in between takes. The goal was to promote this formless, functional and frankly unsexy shoe as a must-have fashion item, or "something you would wear with a mini (skirt) out shopping."

The celebrity seeding strategy worked beyond anyone's wildest dreams. Soon after, a mini skirt and a pair of Uggs would become the brand's defining visual legacy thanks to Y2K luminaries Nicole Richie, Britney Spears and Lindsay Lohan. The boots gained a large celebrity following and were frequently seen on notable people such as Kate Upton, Blake Lively, Kate Hudson, Cameron Diaz, Jennifer Lopez, Leonardo DiCaprio, The Rolling Stones guitarist Ronnie Wood, and Sarah Jessica Parker as Carrie Bradshaw on Sex and the City.

But the moment that changed everything came on November 24, 2003. In 2003, UGG boots were included on Oprah Winfrey's show as part of "Oprah's Favorite Things." Afterwards, the brand received an unprecedented surge in sales. During this show Oprah purchased 350 pairs of UGG boots for her audience and staff causing a massive surge in sales of the boots worldwide.

The numbers tell the story: That year, Ugg chalked up $23.5 million in sales, and it completely sold out of its Classic boot that fall. Between 2002 and 2003, sales had increased 300%. There were month-long waiting lists to purchase the boots as manufacturers ran out and store supplies dried up. The shoes were being resold on eBay for a markup of over 200%.

"Nike had jogging take off, Reebok had aerobics take off, Zoom had the pandemic take off and for (Uggs) it was Oprah," Brian Smith would later reflect. "Oprah was what took (Uggs) worldwide. And that's how it got into the billions."

What made the Oprah moment so powerful wasn't just the exposure—it was the permission structure it created. UGG, Tory Burch, and Spanx were all very small businesses that Oprah helped put on the map. Suddenly, wearing what were essentially slippers in public wasn't just acceptable; it was aspirational.

Deckers capitalized brilliantly on the momentum. They expanded the color palette, added embellishments, created new silhouettes. But they also did something smarter: they built infrastructure to handle the demand. While competitors might have been caught flat-footed by such explosive growth, Deckers had the operational excellence to scale production without sacrificing quality.

The international expansion was equally strategic. In 2006, UGG opened its first brick and mortar store in New York's SoHo neighborhood. The company opened its first international store in Japan later that same year. These weren't just retail locations—they were brand temples, places where the full UGG lifestyle could be experienced.

Perhaps most impressively, Deckers navigated the transition from trend to staple. Once supply caught up with demand, and a slew of counterfeits began hitting the shelves, Uggs went from aspirational accessory to generic garb. The market had become saturated with the caramel-colored boots. In 2009, British newspaper the Independent dubbed Uggs "the Australian footwear that makes you look like you've got child-bearing ankles."

Lesser brands would have collapsed under this backlash. But Deckers understood something fundamental about fashion cycles: what goes out of style inevitably comes back. They maintained quality, continued innovating, and waited. Sure enough, the boots found new life with each successive generation.

The resilience of the brand was tested during the 2008 financial crisis. In the economic downturn of 2008, Deckers continued to show earnings and sales growth. In 2008, for instance, the brand was still seeing huge gains even amid the economic downturn, posting full-year sales of $582 million. When luxury goods were collapsing globally, UGG kept growing. Why? Because they had successfully positioned comfort as an affordable luxury—a small indulgence when bigger purchases were off the table.

By 2012, the transformation was complete: UGG reported over $1 billion (U.S) in sales for 2012. From $17 million to a billion in seventeen years under Deckers' ownership—a 59x increase that ranks among the great brand-building stories in consumer goods history.

The UGG playbook would become Deckers' template: Find an authentic niche product with untapped mainstream potential. Elevate the brand positioning without losing authenticity. Seed with influencers and wait for the cultural moment. Scale aggressively when that moment arrives. Build infrastructure to sustain growth. Navigate the inevitable backlash with patience and innovation.

VII. The Portfolio Expansion Era (2009–2012)

The period from 2009 to 2012 was Deckers' experimental phase—a time when UGG was generating nearly a billion dollars annually and the company, flush with cash and confidence, started hunting for the next big thing. What followed was a masterclass in portfolio management, complete with both textbook successes and humbling failures.

Angel Martinez had taken the helm as CEO in 2005, bringing with him a legendary resume: "I came from a company that went from a zero-dollar operation to a $3.5-billion business, and I was there every step of the way," he would say of his time at Reebok. At 55, the former competitive distance runner brought both operational excellence and a clear vision: find brands that could replicate the UGG miracle.

The first major move of this era seemed logical enough. In 2010, Deckers acquired MOZO Shoes, a brand that produced footwear for the culinary industry. Think stylish clogs for chefs, slip-resistant shoes for restaurant workers—a niche market with clear demand. The logic was sound: just as UGG had dominated sheepskin boots and Teva owned sport sandals, MOZO could own professional kitchen footwear.

But MOZO never gained traction. The brand was sold in July 2015, making it one of Deckers' rare admissions of failure. The lesson was clear: not every niche can scale to mainstream, and not every functional product can become a lifestyle brand.

The Sanuk acquisition in 2011 was a different story entirely. Deckers acquired Sanuk shoes for $120 million—a deal that seemed expensive at nearly 3x sales but would prove to be a strategic masterstroke. The total purchase price for the assets of both companies related to the Sanuk brand is an initial payment of approximately $120 million in cash subject to certain post-closing adjustments, and includes additional participation payments based upon performance over the next five years. The combined businesses generated in excess of $43 million of unaudited net sales in 2010.

What made Sanuk different? For starters, it had authentic roots in surf culture—something Deckers understood deeply. Founded by Jeff Kelley, Sanuk (Thai for "fun") had created an entirely new category with their "Sidewalk Surfers"—shoes that looked like sneakers but were constructed like sandals. The Yoga Mat sandal made from yoga mat material was cited as the 2010 Product of the Year by the Surf Industry Manufacturers Association (SIMA).

Martinez saw the strategic fit immediately: "Sanuk is an ideal addition to the Deckers family of brands. It's a profitable, well-run business with a corporate culture similar to ours, and provides substantial growth opportunities, particularly within the action sports market where it has a large and loyal customer base of active outdoor enthusiasts."

The portfolio mathematics were compelling. Prior to buying Sanuk, the 38-year-old South Coast company with its some 200 employees already had six brands: Simple Shoes, Ugg Australia boots, Teva, Tsubo, Ahnu, and Mozo. But the performance was wildly uneven. Ugg Australia generated 87% of DECK's $1.0 billion in 2010 sales and was on pace to become a $1 billion brand by 2015. Its other three brands – Simple Shoes, Tsubo and Ahnu—contributed just 3 percent of sales and were not growing at nearly the rate of Sanuk.

The Simple Shoes story is particularly instructive. Remember, this was one of Deckers' first acquisitions back in 1993. But by 2011, Martinez made the difficult decision to shut it down: "Simple Shoes was the first brand to prove it's possible to make eco-conscious footwear, and we're proud to have accomplished all that we have. Given that there is some degree of overlap between Simple and Sanuk consumers, and Sanuk's positive outlook and global appeal, we make this difficult decision knowing it is in the best interests of the brands, the company, and its shareholders."

The memo Martinez sent to employees was even more revealing: "While it is difficult to say good-bye to Simple, it no longer fits in our portfolio. We have before us a number of major opportunities that require our focus and investment, and we are consolidating our energies and resources in support of these opportunities."

This was portfolio discipline at its finest. Rather than letting underperforming brands drain resources, Deckers was willing to cut losses and redeploy capital. The company was learning that not every acquisition would become the next UGG, and that was okay.

The broader strategy during this period was becoming clear. Deckers wasn't trying to be Nike or Adidas with massive, diverse portfolios. Instead, they were building a collection of authentic lifestyle brands, each with its own tribe and growth trajectory. The company employs more than 1,000 people at offices from Paris and London to Tokyo and Hong Kong, including 300-plus at their headquarters in Goleta—the infrastructure was in place to scale winners.

Martinez's philosophy was revealing: "Really, I have only two fundamental jobs—keeper of the vision and keeper of the culture." This wasn't about financial engineering or aggressive M&A. It was about finding brands that fit a specific profile: authentic origins, passionate niche following, potential for lifestyle expansion, and cultural fit with Deckers' California roots.

By the end of 2012, the portfolio had been rationalized. MOZO would eventually go. Simple was gone. Sanuk was showing promise. But more importantly, Deckers had developed a clear acquisition framework. They knew what worked (authentic brands with lifestyle potential) and what didn't (purely functional products without emotional resonance). This learning would prove invaluable when, in 2013, they would make their next big bet on a quirky French running shoe company that nobody had heard of.

VIII. The HOKA Acquisition: Finding Lightning Twice (2013)

The story of how Deckers found HOKA begins, improbably, with a phone call from a Boulder running store owner to a former Reebok executive. Johnny Halberstadt from Boulder Running called Jim Van Dine a couple years before the acquisition, raving about this fantastic new brand of running shoes. "I immediately thought of you and Angel. You are both long time runners with a long history of successfully launching brands and with the power of Deckers, this seems like a natural fit."

Van Dine was skeptical at first. Hoka first gained attention in the running industry by producing shoes with oversized midsoles, dubbed "maximalist" shoes, in contrast to the minimalist shoe trend that was gaining popularity at the time. This was 2011, and everyone in running was obsessed with barefoot-style minimalist shoes. Vibram FiveFingers were everywhere. Nike was pushing its Free line. The idea of shoes with cartoonishly large soles seemed like commercial suicide.

But Van Dine, who had helped scale Reebok from startup to billion-dollar company within five years, knew to look beyond trends. After some research, Van Dine came to a confident conclusion: There was a 95% chance we can get this business over $100 million in five years. This wasn't hubris—it was pattern recognition from someone who had seen disruption work before.

The founders' story was compelling. The company was founded in 2009 by Nicolas Mermoud and Jean-Luc Diard, former Salomon employees. They sought to design a shoe that allowed for faster downhill running, and created a model with an oversized outsole that had more cushion than other running shoes at the time. Jean-Luc was inspired by the oversize trend he had witnessed in tennis rackets, golf clubs, skis and bicycle wheels. If bigger worked everywhere else in sports equipment, why not running shoes?

What sealed the deal for Angel Martinez was personal experience. In an interview with the Business Times in July 2012, shortly after Deckers made that first investment in Hoka, Martinez praised the brand for allowing him to take up running again. The 56-year-old CEO said the revolutionary design provided the cushioning and support to bring him back into the sport. This wasn't just a business decision—it was visceral. Martinez, a former elite runner himself, understood what HOKA could mean for aging athletes and injury-prone runners.

The acquisition happened in stages, classic Deckers style. Goleta-based Deckers took a stake in Hoka One One in July 2012 and completed a buyout of the firm in September 2012. The brand, acquired for an undisclosed amount, adds a smaller sliver to Deckers' massive footwear portfolio but has the potential to be a $100 million a year moneymaker within a few years, according to Hoka brand President Jim Van Dine. "That kind of growth curve doesn't scare us," he told the Business Times, noting that Hoka One One (pronounced "Hoka o-nay, o-nay") had less than $3 million in sales last year but is on track to triple that this year.

The full acquisition was completed on April 1, 2013. Hoka was purchased on April 1, 2013, by Deckers Brands, the parent company for UGG, Teva and other footwear brands. The price wasn't disclosed, but industry sources suggested it was in the range of $10-20 million—a rounding error for a company generating over a billion in revenue, but potentially transformative if the brand hit.

The strategic rationale was clear. Deckers never acquired Hoka to be a niche brand. My main responsibility is to make sure the brand has no ceiling, that we can grow to whatever extent the market allows, Van Dine would say. The vision from day one was massive: "I told Angel: Think Nike," Van Dine said.

What made HOKA different from MOZO or the other failed experiments was its authentic performance credibility. The shoes were initially embraced by ultramarathon runners due to their enhanced cushion and inherent stability. Among Hoka's athletes were world class endurance runner Karl Meltzer—who currently holds the record for most 100-mile trail race wins—and Dave Mackey, the 2011 Ultra Runner of the Year.

The integration strategy was brilliant. Founders Jean-Luc Diard and Nicolas Mermoud will continue to work with the brand. Diard will be responsible for international distribution and will continue to work with the brand on product innovation, while Mermoud will continue to support the brand's sports marketing and athlete management. Unlike many acquisitions where founders are pushed out, Deckers kept the DNA intact.

The early results validated Van Dine's confidence. "We're experiencing tremendous growth, in the neighborhood of 300 percent to 350 percent in year-over-year sales," Van Dine said in 2014. The brand expanded from 180 doors in 2013 to 750 by 2014—a quadrupling of distribution in a single year.

But the real genius was in how Deckers positioned HOKA. They didn't try to compete directly with Nike or Adidas on their terms. Instead, they created a new category: maximalist performance. The thinking behind this "maximalist" construction is similar to that underlying putting big tires on trucks or bikes to allow rolling right over obstacles. It was such a simple metaphor that anyone could understand it.

Looking back, the HOKA acquisition represents everything Deckers had learned over forty years. Find an authentic niche product (ultra-running shoes). Identify the mainstream crossover potential (comfort for all runners). Keep the founders involved (maintain authenticity). Invest aggressively in distribution and marketing (scale rapidly). Most importantly, have the patience to let the brand find its audience rather than forcing it.

The numbers would eventually prove Van Dine right beyond his wildest projections. since being acquired in 2013, Hoka's revenue has skyrocketed to nearly $2 billion, thanks to strategic moves by its parent company. Not bad for a brand that was doing less than $3 million when Deckers first took a stake. The ugly marshmallow shoes that everyone thought would fail had become Deckers' second billion-dollar brand.

IX. HOKA's Explosive Growth (2013–Present)

The transformation of HOKA from a $3 million ultra-running curiosity to a nearly $2 billion global phenomenon represents one of the most successful brand turnarounds in footwear history. The numbers tell a story of explosive, sustained growth that has exceeded even the most optimistic projections.

Deckers has grown revenue at a 19% CAGR over the past four years, consecutively delivering a double-digit revenue increase each year, while at the same time more than tripling earnings per share. But within this impressive company-wide performance, HOKA has been the rocket ship. Fourth Quarter Fiscal 2024 Brand Summary HOKA brand net sales increased 34.0% to $533.0 million compared to $397.7 million in the same period the previous year.

The acceleration has been breathtaking. Hoka set a new record in the company's first quarter, with revenue surging 30% year-over-year to $545 million. To put this in perspective, HOKA is now generating in a single quarter what took UGG nearly two decades to achieve annually. At the current scale north of $1.4 billion, our focus is to protect the Hoka brand's premium positioning and maintain a pull model, Dave Powers explained, acknowledging that managing hypergrowth without diluting brand equity is the new challenge.

What's driven this extraordinary growth? The answer lies in Deckers' masterful execution of a three-pronged strategy: product expansion, distribution excellence, and cultural relevance.

On the product front, HOKA didn't rest on its maximalist laurels. Van Dyne and team quadrupled the number of stores carrying HOKA between 2013 and 2014, and have only continued to broaden Hoka's reach with entry into sporting goods retailers, department stores and owned retail. The brand evolved from purely trail and ultra-running shoes to road running, walking, hiking, and even lifestyle sneakers. Each category maintained HOKA's distinctive aesthetic while addressing specific consumer needs.

The marketing evolution has been equally sophisticated. In June of 2022, Hoka launched Fly Human Fly, its first-ever globally integrated marketing campaign. The campaign was designed to build awareness and elevate the Hoka brand in the minds of global consumers through rich storytelling and targeted activations in key cities. The Hoka team utilized connected TV and digital and out-of-home channels to reach a broader audience with creative that combined emotionally connected brand and product messaging. As a result of the investments behind this campaign, Hoka awareness increased across a broad spectrum of key markets, such as the U.S., France, the U.K., China, and Germany, with three of those countries increasing awareness by more than 40 percent compared to fall 2021.

The shift from niche to mainstream happened gradually, then suddenly. First came the serious runners who appreciated the cushioning. Then the injury-prone athletes who needed protection. Then the nurses and healthcare workers who spent 12-hour shifts on their feet. Finally, the fashion-forward consumers who saw HOKA as the perfect ugly-chic statement shoe. Britney Spears tweeted a pic of her Hokas in 2017—a cultural moment that signaled the brand had transcended performance.

The direct-to-consumer strategy has been particularly powerful. The brand's DTC revenue, primarily sales from its ecommerce website, grew by 33%. This isn't just about margin improvement—it's about brand control. Through their own channels, HOKA can tell their story, control pricing, and gather invaluable consumer data.

International expansion has been another growth vector. While UGG struggled with seasonality and cultural relevance in certain markets, HOKA's performance positioning translates globally. Runners in Tokyo, Paris, and São Paulo all understand the value proposition of maximum cushioning and energy return.

The financial performance has validated every strategic decision. Deckers achieved record results during fiscal year 2024, as we delivered revenue growth of 18% and increased earnings per share by 51%, reflecting a continued dedication to maintain exceptional levels of profitability as our brands scale. HOKA and UGG remain two of the most admired and well-positioned brands in the marketplace, each with a robust innovation product pipeline designed to win with global consumers. Looking forward, our talented teams are highly motivated to continue driving towards the long-term opportunities of these iconic brands.

What's remarkable is that HOKA's growth hasn't cannibalized UGG—instead, the two brands have created a portfolio effect that's greater than the sum of its parts. FY 2025 Revenue Increased 16% to a Record $4.99 Billion FY 2025 Diluted EPS Increased 30% to a Record $6.33. In fiscal 2025, Ugg and Hoka accounted for 51% and 45% of total sales, respectively—essentially two billion-dollar brands under one roof.

The market dynamics are shifting in HOKA's favor. The global running market is expected to grow, but more importantly, the definition of "running shoes" is expanding. HOKA has successfully positioned itself not just as a running brand but as a comfort and wellness brand. In an aging population dealing with everything from plantar fasciitis to knee problems, HOKA's maximum cushioning isn't just nice to have—it's essential.

Looking forward, the growth trajectory shows no signs of slowing. Looking ahead, Deckers projects a 10% increase in overall revenue for the fiscal year ending March 31, 2025, reaching $4.7 billion. Hoka is expected to grow around 20%, while Ugg is expected to see mid-single-digit growth. This suggests HOKA will likely cross $2 billion in annual revenue within the next year or two—a 667x increase from when Deckers first invested.

The lessons from HOKA's explosive growth are clear. First, timing matters less than execution—HOKA succeeded by going against the minimalist trend, not with it. Second, authentic performance credibility can translate to mainstream success if marketed correctly. Third, what seems like a limitation (oversized, "ugly" shoes) can become a differentiator in a crowded market. Finally, and perhaps most importantly, patient capital and operational excellence can transform a niche product into a global phenomenon.

X. Modern Era: The Two-Horse Race (2015–Present)

The modern Deckers story is essentially a tale of two brands operating at peak performance. While the company technically owns several brands, the reality is stark: UGG and HOKA together represent over 96% of revenue. This concentration might terrify most portfolio managers, but for Deckers, it's become their superpower.

The decision to focus came gradually, then definitively. In 2010, Deckers acquired MOZO Shoes, a brand that produced footwear for the culinary industry, but sold the brand in July 2015. Deckers acquired Sanuk shoes for $120 million in 2011, which it later divested to Canadian sportswear company Lolë. The message was clear: Deckers was done experimenting. The future belonged to their two thoroughbreds.

In 2015, Deckers acquired Koolaburra and positioned it under its UGG brand. This wasn't really a new brand play—it was a defensive move to protect UGG's lower price points while maintaining the premium positioning of the main line. Koolaburra became UGG's fighter brand, the way Toyota has Lexus and Gap has Old Navy.

The transformation under Dave Powers, who became CEO in 2016, has been remarkable. Powers brought a different energy than Martinez—less the visionary, more the operator. His focus: operational excellence, margin expansion, and direct-to-consumer acceleration. Direct-to-Consumer (DTC) net sales increased 21.0% to $415.2 million compared to $343.1 million in recent quarters, showing the strategy is working.

The DTC transformation has been particularly impressive. The company has nearly doubled its operating margins and shifted to more direct sales, from 34% of revenue to 40%. This isn't just about capturing more margin—it's about brand control, data ownership, and the ability to tell their story without intermediaries.

What's fascinating about the two-horse race is how complementary UGG and HOKA have become. UGG brings heritage, lifestyle positioning, and massive seasonal cash generation. HOKA brings growth, performance credibility, and year-round demand. Together, they create a portfolio that's both stable and dynamic—a rare combination in consumer goods.

The geographic expansion has been methodical. Both brands are now global, but in different ways. UGG leverages its fashion positioning in Asia, where American lifestyle brands carry premium cache. HOKA follows runners—wherever there's a marathon, there's HOKA. Deckers Brands is a global leader in designing, marketing, and distributing innovative footwear, apparel, and accessories developed for both everyday casual lifestyle use and high-performance activities. The Company's portfolio of brands includes UGG®, HOKA®, Teva®, Sanuk®, Koolaburra®, and AHNU®. Deckers Brands products are sold in more than 50 countries and territories through select department and specialty stores, Company-owned and operated retail stores, and select online stores.

The capital allocation in this era has been disciplined to the point of being boring—and that's a compliment. No flashy acquisitions, no attempts to buy growth. Instead: aggressive reinvestment in the two core brands, steady share buybacks, and a fortress balance sheet. As of March 31, 2024, the Company had approximately $941.7 million remaining under its stock repurchase authorization.

The innovation pipeline has become increasingly sophisticated. UGG isn't just making boots anymore—they're making sneakers, slippers, apparel, even home goods. HOKA isn't just making running shoes—they're making hiking boots, recovery slides, walking shoes. Each brand extension is carefully calibrated to expand the addressable market without diluting the core.

On December 22, 2021, Hoka announced that they were rebranding, with their business name changing from HOKA One One to simply HOKA. This might seem like a minor change, but it signals confidence. The brand no longer needs the "One One" modifier—everyone knows HOKA.

The supply chain evolution has been crucial but unglamorous. Deckers has diversified manufacturing, improved forecasting, and built flexibility into their operations. When COVID hit and everyone else was scrambling, Deckers kept shipping. When the supply chain crisis peaked, Deckers had inventory. This operational excellence doesn't make headlines, but it makes money.

The competitive dynamics have shifted dramatically. In 2015, Deckers was still seen as the "UGG company"—a one-trick pony vulnerable to fashion cycles. Today, they're mentioned in the same breath as Nike and Adidas, at least in certain categories. HOKA has legitimate claim to performance running leadership. UGG has proven its staying power through multiple fashion cycles.

Perhaps most importantly, Deckers has cracked the code on brand lifecycle management. Most brands follow a predictable arc: discovery, growth, maturity, decline. Deckers has figured out how to extend the growth phase almost indefinitely through careful market segmentation, product innovation, and geographic expansion. UGG should be a dead brand by now—it's been 20 years since Oprah. Instead, it's generating record revenue.

The recent results speak for themselves. SECOND QUARTER FY 2025 REVENUE INCREASED 20% TO $1.31 BILLION SECOND QUARTER FY 2025 DILUTED EPS INCREASED 39% TO $1.59 FY 2025 REVENUE GUIDANCE RAISED TO APPROXIMATELY $4.8 BILLION. These aren't the numbers of a mature company—they're the numbers of a company hitting its prime.

The two-horse race strategy has risks, obviously. Fashion changes. Running trends evolve. New competitors emerge. But Deckers has built something more durable than just two brands—they've built a system for creating and sustaining premium lifestyle positioning in footwear. That system, more than any individual brand, might be their most valuable asset.

XI. Playbook: Business & Investing Lessons

After fifty years of building brands, Deckers has developed a playbook that's both deceptively simple and extraordinarily difficult to execute. The lessons from their journey—from flip-flops to a $16 billion market cap—offer a masterclass in brand building, portfolio management, and value creation.

The Portfolio Approach: Concentration with Calculation

Deckers proves that portfolio concentration can work if you pick the right horses. They're not trying to be P&G with dozens of billion-dollar brands. They're running two exceptional brands at maximum efficiency. The lesson: it's better to have two brands generating 50% margins than twenty brands generating 5% margins.

The key is knowing when to concentrate and when to diversify. During the expansion era (2009-2012), Deckers experimented widely. Once they found what worked—UGG's lifestyle positioning and HOKA's performance credibility—they doubled down ruthlessly. They killed Simple, sold MOZO, divested Sanuk. This isn't failure; it's discipline.

Acquisition Strategy: The Three-Phase Approach

Deckers has perfected a three-phase acquisition model. Phase 1: Partnership or minority stake (test the relationship). Phase 2: Full acquisition (commit capital). Phase 3: Scale aggressively (leverage the platform).

Look at HOKA—minority stake in July 2012, full acquisition by April 2013, and then massive investment in distribution and marketing. This staged approach reduces risk while maintaining optionality. You're essentially getting a free option on the upside while limiting downside exposure.

Timing the Market: Catching the Pre-Inflection Point

Every successful Deckers acquisition happened right before an inflection point. UGG in 1995, just before the celebrity-driven fashion boom. HOKA in 2013, just before the maximalist running trend exploded. They're not trying to time the peak—they're buying into authentic niche brands with mainstream potential.

The pattern is consistent: find brands with fanatical niche followings (surfers for UGG, ultra-runners for HOKA), then methodically expand the addressable market. The niche provides authenticity; the expansion provides scale.

Brand Lifecycle Management: The Eternal Growth Hack

Most brands follow a predictable lifecycle: introduction, growth, maturity, decline. Deckers has figured out how to extend the growth phase almost indefinitely through three mechanisms:

-

Geographic Expansion: When UGG saturated the U.S., they went international. When HOKA dominated running, they moved into hiking and lifestyle.

-

Category Extension: UGG went from boots to slippers to sneakers to home goods. HOKA went from trail to road to recovery to lifestyle.

-

Price Architecture: Premium mainline, accessible diffusion lines (Koolaburra for UGG), and strategic collaborations that spike brand heat.

Building Distribution Moats

Deckers understands that distribution is destiny in footwear. They've built three types of moats:

-

Retail Relationships: Decades-long partnerships with Nordstrom, Foot Locker, and specialty retailers create barriers for competitors.

-

Direct-to-Consumer: 40% of revenue through owned channels means higher margins, better data, and price control.

-

International Infrastructure: Offices from Tokyo to Paris mean they're not reliant on distributors who might switch brands.

The Power of Lifestyle Marketing

Deckers doesn't sell shoes; they sell identities. UGG isn't about sheepskin; it's about California luxury. HOKA isn't about cushioning; it's about human potential. This emotional positioning commands premium pricing and creates switching costs that pure performance brands can't match.

The marketing evolution shows this clearly. Both brands started with product-focused messaging (warm boots, cushioned shoes) and evolved to lifestyle positioning (comfort as luxury, running as transformation). This shift from functional to emotional is where the real value creation happens.

Capital Allocation Excellence

Deckers' capital allocation has been boringly brilliant:

- R&D Investment: Enough to stay innovative but not so much that it hurts margins

- Marketing Spend: Heavy investment during growth phases, then optimization at maturity

- Share Buybacks: Consistent repurchases that have meaningfully reduced share count

- Balance Sheet Strength: No debt, massive cash position provides strategic flexibility

The discipline to not overpay for acquisitions (remember, UGG was $14.6 million, HOKA was likely under $20 million) while investing aggressively in proven winners shows remarkable strategic clarity.

Managing Seasonality and Cyclicality

The UGG/HOKA portfolio provides natural hedging. UGG peaks in fall/winter; HOKA is more consistent year-round. UGG is fashion-sensitive; HOKA is performance-driven. This diversification within concentration smooths earnings and reduces risk.

The Platform Value Creation Model

Deckers has built a platform that makes every brand they acquire more valuable:

- Operational Excellence: Supply chain, logistics, and systems that would cost millions for standalone brands

- Distribution Network: Immediate access to thousands of doors globally

- Marketing Expertise: Knowing how to take niche brands mainstream

- Financial Resources: Patient capital that can weather fashion cycles

This platform means Deckers can pay less for acquisitions (because the brands need them) while creating more value post-acquisition (because of the platform benefits).

Key Metrics That Matter

For investors analyzing Deckers or similar companies, focus on:

- DTC Percentage of Revenue: Higher percentage means better margins and brand control

- International Mix: Geographic diversity reduces single-market risk

- Inventory Turns: Efficiency in managing seasonal products

- Brand Heat Metrics: Social media mentions, search trends, resale values

- ASP Trends: Average selling prices indicate brand strength

The meta-lesson from Deckers is that brand building is both art and science. The art is in recognizing authentic products with emotional resonance. The science is in the systematic scaling, distribution building, and operational excellence. You need both to build a portfolio worth $16 billion.

XII. Analysis & Bear vs. Bull Case

Bull Case: The Unstoppable Force Thesis

The bull case for Deckers rests on multiple expansion drivers that could power years of continued outperformance. Start with the obvious: two brands generating nearly $5 billion in revenue with room to grow.

HOKA's trajectory alone justifies optimism. At $2 billion in revenue, they're still capturing only a small fraction of the global athletic footwear market. Nike generates $50 billion annually—if HOKA can capture even 10% of that opportunity, it's a $5 billion brand. The maximalist cushioning trend isn't a fad; it's a response to an aging population that needs comfort and protection. Every year, millions of runners age into HOKA's sweet spot.

UGG's resilience continues to surprise skeptics. Twenty years after becoming a phenomenon, the brand is still growing. The key insight: UGG has transcended fashion to become a comfort uniform. Work-from-home culture, the casualization of everything, the wellness trend—all these macro forces benefit UGG. The brand has also barely scratched the surface in Asia, where American lifestyle brands command premium positioning.

The direct-to-consumer transformation provides another lever. At 40% of revenue, DTC is still below peers like Nike (approaching 50%). Every percentage point of DTC shift adds margin. If Deckers can reach 50% DTC while maintaining wholesale growth, the margin expansion alone could drive significant earnings growth.

International expansion remains early. Despite global presence, international is still less than 40% of revenue. Nike and Adidas generate over 60% internationally. As HOKA builds brand awareness globally and UGG penetrates Asia, international could become the primary growth driver.

The balance sheet provides optionality. With essentially no debt and massive cash generation, Deckers could make another transformative acquisition, increase buybacks, or invest aggressively in emerging categories. This financial flexibility in an uncertain macro environment is invaluable.

Management execution has been flawless. Deckers has grown revenue at a 19% CAGR over the past four years, consecutively delivering a double-digit revenue increase each year, while at the same time more than tripling earnings per share. This isn't luck—it's operational excellence that should continue.

The category dynamics favor Deckers. Athletic footwear is growing faster than overall footwear. Comfort is becoming the primary purchase driver across demographics. Fashion cycles are accelerating, benefiting companies with proven brand-building capabilities. All these trends advantage Deckers.

Bear Case: The Vulnerability Thesis

The bear case starts with concentration risk. Two brands generating 96% of revenue is efficient until it isn't. If either UGG or HOKA stumbles, there's no cushion. Fashion is fickle, and performance running is increasingly competitive. History is littered with footwear brands that seemed invincible until they weren't.

Competition is intensifying. In performance running, Nike, Adidas, and New Balance are responding to HOKA's success with their own maximalist offerings. In lifestyle, everyone from luxury houses to direct-to-consumer startups is targeting UGG's comfort positioning. The moats aren't as wide as they appear.

Valuation is stretched. At current multiples, Deckers trades at a premium to most consumer goods companies. The market is pricing in continued 20% growth—any deceleration could trigger multiple compression. The stock has already captured much of the HOKA growth story.

Fashion risk for UGG remains real. Yes, the brand has survived multiple cycles, but each revival requires more marketing spend and innovation investment. The core boot silhouette that drives the business is inherently limiting. Young consumers might view UGG as their parents' brand—deadly in fashion.

Supply chain concentration presents risks. Manufacturing primarily in Asia exposes Deckers to geopolitical tensions, tariffs, and logistics disruptions. The lack of vertical integration means less control over costs and quality.

Market saturation is approaching in key categories. How many pairs of UGG boots does one consumer need? HOKA is approaching ubiquity in certain running communities. Growth requires finding new consumers or increasing purchase frequency—both challenging.

Management transition adds uncertainty. Powers is retiring as president and CEO on Aug. 1, with Stefano Caroti, the current chief commercial officer, set to take over both positions. Deckers also plans to nominate Caroti to the board at its 2024 annual meeting of stockholders, while Powers will remain on the board through the 2025 meeting. Leadership changes during peak performance often presage challenges.

The macro environment is uncertain. Inflation, recession fears, and changing consumer spending patterns could hurt discretionary footwear purchases. Deckers' products aren't necessities—they're wants that consumers can defer.

The Balanced View

The truth likely lies between these extremes. Deckers has built something durable: a platform for creating and scaling premium footwear brands. The execution has been exceptional, the brands are strong, and the financial position is enviable.

But trees don't grow to the sky. The law of large numbers suggests growth will decelerate. Competition will intensify. Fashion will cycle. The question isn't whether challenges will emerge, but whether Deckers' platform and management can navigate them.

For investors, the key is valuation versus growth durability. If HOKA can become a $5 billion brand and UGG can maintain its current scale, Deckers is reasonably valued. If either assumption breaks, the stock is vulnerable.

The highest probability scenario: Deckers continues executing, growth moderates to high single digits, margins remain strong, and the stock delivers market-plus returns. Not the explosive growth of the past decade, but solid, sustainable value creation.

The wildcard remains acquisitions. Deckers has the balance sheet and track record to make another transformative deal. The right brand at the right time could reignite the growth story. But finding the next HOKA is harder than it looks.

XIII. Epilogue & Looking Forward

Standing at the intersection of fashion and function, comfort and performance, Deckers Brands has engineered one of the great transformation stories in consumer goods. From Doug Otto's flip-flops to a portfolio generating nearly $5 billion in revenue, the journey illuminates timeless principles about brand building, strategic patience, and the power of focused execution.

The Next Acquisition: Following the Playbook

If we were betting on Deckers' next move, we'd look for brands that fit their proven pattern. The target would be authentic, niche, and on the verge of mainstream breakthrough. Think outdoor brands like Cotopaxi or Allbirds (if they could buy it cheap enough), or performance brands addressing specific problems like APL (Athletic Propulsion Labs). The key: finding brands where Deckers' platform could unlock value that standalone operations couldn't achieve.

The smartest acquisition might be in adjacent categories. Accessories, apparel, or even wellness products that leverage the UGG and HOKA brand equity. Imagine HOKA recovery tools or UGG home goods—category extensions that don't require new brand building.

HOKA's Ceiling: Higher Than You Think

HOKA's potential extends far beyond running. The brand has permission to play anywhere comfort and performance intersect. Hiking boots are obvious. Work boots for people on their feet all day. Recovery footwear for athletes. Even fashion collaborations that bring HOKA's distinctive aesthetic to new audiences.

The international opportunity is massive. HOKA has barely penetrated Asia, where running is exploding and American performance brands carry cache. Europe remains underdeveloped despite strong running culture. If HOKA can replicate its U.S. success globally, $5 billion in revenue isn't unrealistic.

UGG's Next Chapter: Beyond the Boot

UGG's evolution will likely focus on becoming a full lifestyle brand. The boot will remain the icon, but growth will come from unexpected places. Men's products, currently underdeveloped, represent a billion-dollar opportunity. Home goods could become a meaningful category. Collaborations with fashion houses could spike brand heat with younger consumers.

The key is maintaining authenticity while expanding. UGG means comfort—that can translate to many products beyond footwear. The risk is dilution; the opportunity is becoming a lifestyle ecosystem like Ralph Lauren or Calvin Klein.

International Expansion: The Untapped Goldmine

Both brands have massive international potential. UGG in Asia, where luxury comfort resonates. HOKA in Europe, where running culture runs deep. Both brands everywhere else, as global consumers increasingly adopt American casual style.

The strategy should be patient and localized. What works in California might not work in Tokyo or Paris. But the core value propositions—comfort, quality, authenticity—translate universally.

Technology and Sustainability: The Next Frontiers

Deckers has been notably quiet on technology and sustainability compared to peers. This could change. Imagine HOKA with Nike-level innovation in materials and construction. Or UGG leading in sustainable luxury, using its Australian heritage to champion environmental causes.

The opportunity isn't just in products but in business model innovation. Subscription services, customization, resale platforms—all areas where Deckers could lead rather than follow.

The Leadership Transition: Continuity and Change

The CEO transition from Powers to Caroti represents both continuity and potential change. Caroti, as Chief Commercial Officer, understands the brands and operations. But new leadership often brings new priorities. Watch for subtle shifts in strategy, capital allocation, and acquisition appetite.

The board's composition and incentive structures will matter more than ever. Maintaining the culture that enabled Deckers' success while adapting to new challenges requires careful governance.

Financial Engineering: The Hidden Value Creator

With a fortress balance sheet and consistent cash generation, Deckers has options. Aggressive buybacks could meaningfully reduce share count. A dividend could attract new investors. Strategic debt could fund acquisitions while maintaining financial flexibility.

The temptation will be to get fancy. The wisdom would be to stay boring—consistent buybacks, opportunistic acquisitions, and letting operational excellence drive returns.

The Broader Lessons

Deckers' story teaches that brand building is about patience, not speed. It took UGG eight years under Deckers to become a phenomenon. HOKA needed five years to hit its stride. In an era of instant everything, Deckers proves that real value creation takes time.

The portfolio approach works if you're disciplined about killing losers and feeding winners. Deckers' willingness to shut down Simple, sell MOZO, and divest Sanuk shows rare discipline. Most companies keep underperformers too long; Deckers cuts quickly and reinvests aggressively.

Authenticity matters more than marketing. Every successful Deckers brand started with a genuine use case—surfers wearing UGGs, ultra-runners wearing HOKAs. Marketing amplified what was already there; it didn't create demand from nothing.

The Ultimate Question

If we were CEOs of Deckers, what would we do? First, protect the core. UGG and HOKA are generational assets that require careful stewardship. Second, invest in the platform. The operational excellence that enables brand scaling is the real moat. Third, stay patient on acquisitions. The temptation to do a big, flashy deal will be strong; the discipline to wait for the right opportunity at the right price will matter more.

Most importantly, we'd remember that Deckers' success came from understanding a simple truth: consumers will pay premium prices for products that solve real problems with authentic style. That insight, more than any financial engineering or marketing brilliance, built a $16 billion company from flip-flops.

The next chapter of Deckers' story remains unwritten. But if history is any guide, it will involve patient brand building, operational excellence, and the occasional transformative acquisition that everyone else missed. The flip-flop company that became a footwear empire isn't done surprising yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube