Deere & Company: The Green Revolution - From Steel Plows to Smart Farms

I. Introduction & Episode Roadmap

Picture this: a farmer in central Iowa steps out of his house at dawn, coffee in hand, and swipes his phone screen twice. Three hundred yards away, a nine-ton tractor rumbles to life, its sixteen cameras scanning the field in every direction. No one sits in the cab. The machine begins tilling rows with sub-inch precision, guided by satellites, artificial intelligence, and nearly two centuries of institutional knowledge. On the side of that tractor, gleaming in John Deere green and yellow, is the leaping deer logo — a symbol that has adorned farm equipment since Ulysses S. Grant was president.

Deere & Company is not just the world's largest agricultural machinery manufacturer. It is one of the oldest continuously operating industrial companies in America, a business that has survived the Civil War, two World Wars, the Great Depression, the 1980s farm crisis, and the digital revolution — emerging from each crisis stronger and more dominant than before. As of early 2026, the company commands a market capitalization north of $110 billion and operates across four segments spanning production agriculture, construction, forestry, and financial services. Its stock recently touched an all-time high of $674 per share, even as the agricultural sector navigated one of its deepest cyclical troughs in a decade.

The central question of this deep dive: How did a Vermont blacksmith's invention in 1837 — a single steel plow — become the foundation for one of the most durable competitive moats in American industry? The answer involves five generations of family leadership, a series of brilliantly timed acquisitions, a brand so powerful it transcends its industry, and a bold bet on technology that is transforming the company from a hardware manufacturer into something closer to an agricultural operating system.

The themes that run through the Deere story are the themes of America itself: westward expansion, industrialization, the mechanization of agriculture, globalization, and now the autonomous future. This is a company where decisions made in the 1840s about steel alloys directly connect to decisions being made today about computer vision algorithms. Few businesses anywhere in the world can claim that kind of continuity.

Here is a striking way to frame the scale of what Deere does: agriculture employs roughly one billion people worldwide and generates over $5 trillion in annual output. It is the single largest human activity on the planet by land use. And the machines that make modern agriculture possible — the tractors, combines, sprayers, and planters that feed eight billion people — are predominantly made by a company founded in a frontier blacksmith shop.

Consider one statistic that captures the productivity revolution Deere helped create. In 1900, it took one American farmer to feed seven people. By 1950, that ratio had improved to one farmer feeding fifteen people. Today, thanks largely to the kind of equipment Deere manufactures, one American farmer feeds roughly 165 people. The machines got bigger, smarter, and more efficient. The company that built those machines scaled alongside them.

If farming is the foundation of civilization, Deere & Company makes the tools that hold that foundation together. Understanding this business is understanding one of the most critical supply chains on Earth.

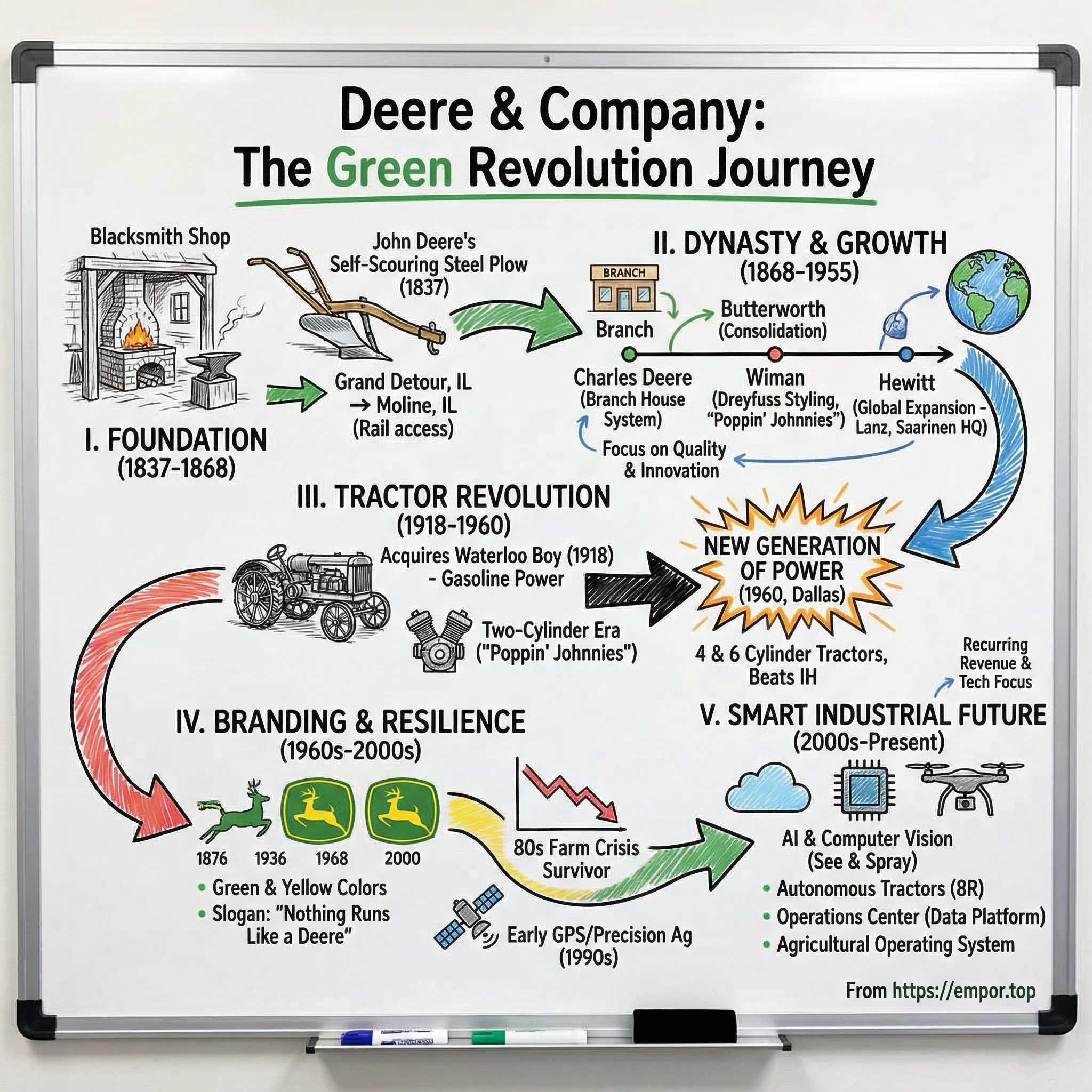

II. The Founding Story: John Deere & The Steel Plow (1837-1868)

John Deere was born on February 7, 1804, in Rutland, Vermont, the third son of William Rinold Deere, a merchant tailor, and Sarah Yates Deere. When John was four years old, his father boarded a ship bound for England, hoping to claim a family inheritance and secure a better life for his wife and five children. William Deere was never heard from again — lost at sea, presumably, though the family never learned what happened. Sarah was left to raise five children alone on a seamstress's meager income. The Deere children grew up in near-poverty, and John's formal education was rudimentary at best. But the experience of watching his mother hold a family together through sheer determination forged a resilience and self-reliance that would define everything that followed.

At seventeen, Deere apprenticed himself to Captain Benjamin Lawrence, a respected blacksmith in Middlebury, Vermont. He completed his four-year apprenticeship in 1825 and opened his own shops — first in Vergennes, then in Leicester. His craftsmanship was meticulous, his reputation growing. But misfortune followed him: two of his shops burned down. He married Demarius Lamb in 1827, and they would eventually have nine children. By the mid-1830s, Vermont's economy was deteriorating badly, and Deere faced mounting debts amid the gathering storm of the Panic of 1837.

In late 1836, at thirty-two years old, John Deere made the gamble of his life. Facing bankruptcy, he left his wife and children behind with just seventy-three dollars in his pocket and headed west to Illinois, following a business associate named Leonard Andrus to a small settlement called Grand Detour on the Rock River. His family would not join him for two years. He arrived with virtually nothing: his tools, a small bundle of clothes, and whatever hope he could muster.

Grand Detour desperately needed a blacksmith. Deere set up shop and immediately found steady work. But he also found something else — a problem that was driving frontier farmers to despair. The thick, heavy prairie soil of Illinois was unlike anything back East. It clung to the cast-iron plows that settlers had brought from New England and the Mid-Atlantic states. Farmers had to stop every few steps to scrape the sticky black earth off their plowshares. Some called the prairie soil "gumbo" because of the way it adhered to iron like glue. Many were ready to give up and move on.

Deere, with a blacksmith's intuitive understanding of how metal interacts with material, had an insight that seems simple in retrospect but was revolutionary in practice. He concluded that a plow made of highly polished steel — rather than rough cast iron — would scour itself clean as it cut through the prairie soil. The smooth surface would prevent the dirt from sticking. In 1837, using a broken steel saw blade he obtained from a local sawmill, Deere fashioned a prototype with a carefully shaped moldboard — the curved surface that turns the soil. He sold his first plow to a farmer named Lewis Crandall, who was so delighted with its performance that he told everyone he knew.

Word spread rapidly. Deere was manufacturing ten plows in 1839, forty in 1840, and seventy-five to one hundred by 1841. Crucially, Deere made a decision that was revolutionary for the era: rather than waiting for customers to place orders and then building to spec — the standard practice for blacksmiths — he began manufacturing plows speculatively, building inventory in advance of demand. This meant he could deliver immediately when a farmer walked in. It was, in effect, the birth of mass production thinking in agricultural equipment, decades before Henry Ford applied the same logic to automobiles.

He was obsessive about quality from the very beginning. His famous dictum — "I will never put my name on a product that does not have in it the best that is in me" — was not mere marketing. He genuinely believed that a farmer's livelihood depended on the reliability of his tools, and he refused to cut corners even when scaling production.

The problem Deere faced was sourcing. Good steel was hard to come by on the frontier. He initially imported polished steel from England, an expensive proposition. Later he struck a deal with a Pittsburgh steelmaker to produce steel to his specifications — reportedly the first steel made specifically for an industrial purpose in America. This willingness to reach backward into the supply chain to ensure quality would become a defining characteristic of the company for the next two centuries. There is a telling detail about John Deere the man: despite founding one of America's most successful manufacturing companies, he received only one patent in his entire life — in 1864, for a plow design, when he was sixty years old. The steel plow that made his fortune was never patented. His moat was not intellectual property. It was execution.

In 1848, Deere made a decision that revealed his strategic instincts. He moved his entire operation from Grand Detour to Moline, Illinois — a town situated on the Mississippi River with access to the new railroad lines being built across the Midwest. Grand Detour had been convenient, but Moline offered transportation infrastructure that could support a genuine manufacturing business. It was the kind of move that separates a craftsman from a company builder: Deere was thinking not about the next hundred plows, but about the next hundred thousand.

By the 1850s, Deere was producing over a thousand plows per year. He had entered into and dissolved multiple partnerships — first with Leonard Andrus, then with Robert Tate and John Gould — learning along the way that he needed ultimate control over the quality and direction of his business. His partnerships ended not in acrimony but in Deere's realization that shared authority diluted the obsessive quality control he considered non-negotiable. By 1855, the factory was selling more than ten thousand plows annually. By 1859, Deere's seventy employees were producing fifteen thousand plows — all with hand tools and old-fashioned production equipment.

Deere was also civically engaged in ways that reveal his character. In 1854, he chaired the Rock Island County Whig Party convention. In 1858, he and fellow abolitionists broke up a meeting of slavery supporters — a risky act in a border state region. He established the first bank in Moline in 1863, recognizing that farmers needed access to capital as much as they needed good plows.

The Civil War years brought both challenge and opportunity. Agricultural production became a matter of national survival, and demand for efficient farm equipment soared. Deere's company, now firmly established in Moline, expanded aggressively. By the end of the war, annual production exceeded ten thousand plows.

On the business side, John Deere brought his son Charles into the company in the early 1850s and gradually ceded more operational authority to him. By the mid-1860s, the company had diversified well beyond plows. The product line included cultivators, harrows, drills, and planters — a full suite of implements that a frontier farmer needed to establish and work a homestead. The broader context helps explain this expansion: the Homestead Act of 1862 had opened millions of acres of federal land to settlement, creating an enormous addressable market of new farmers, all of whom needed tools to break and cultivate virgin prairie. Deere was perfectly positioned to serve them.

In 1868, the business was formally incorporated as Deere & Company — a milestone that transformed a proprietorship into an institution. John Deere, now sixty-four, remained as president, but the incorporation signaled something important: this company was being built to outlast any single individual. The blacksmith from Vermont had created not just a product but a platform for what would become one of the great American industrial dynasties.

III. Building a Dynasty: Five Generations of Family Leadership (1868-1955)

When John Deere died on May 17, 1886, at the age of eighty-two, the company he left behind was substantial but not yet dominant. It was a top manufacturer of plows and cultivators, but the farm equipment industry was ferociously competitive, with hundreds of regional manufacturers fighting for the same customers. What happened over the next seven decades — five generations of family leadership, each with a distinct management style and strategic contribution — turned Deere from one of many into the undisputed industry leader.

Charles Deere, John's son, had effectively been running the company since the early 1870s. Where his father was a craftsman and inventor, Charles was a salesman and strategist. His most consequential innovation was the creation of the branch house system. In the 1880s, Charles established John Deere's first branch house in Kansas City — essentially an independent distribution center that served as a two-way bridge between the factory and the farmer. The branch houses did not merely sell equipment; they collected intelligence from the field about what was working, what was breaking, and what farmers needed next. This information flowed back to Moline and directly influenced product development.

The branch house system was, in essence, an early version of what modern businesses call a "customer feedback loop," and it gave Deere a structural advantage over competitors who relied on independent dealers with no institutional loyalty. By the time Charles Deere died in 1907, the company had branch houses across the Midwest and was recognized as one of the top implement makers in America.

Charles's death created a succession challenge. His son-in-law, William Butterworth, assumed the presidency in 1907 and faced a company that had grown sprawling and somewhat chaotic. Deere had acquired or started multiple subsidiary companies — wagon makers, corn planter manufacturers, harvester producers — and each operated with considerable autonomy. Butterworth's great contribution was consolidation. He merged eleven factories and twenty-five sales organizations into a single, coherent entity. This was the moment Deere & Company truly became Deere & Company — not a holding company or a loose federation, but an integrated industrial corporation.

Butterworth also navigated the company through World War I, during which agricultural production was again critical to the national effort. Crucially, it was during his tenure that Deere made the acquisition that would define its future: the purchase of the Waterloo Gasoline Engine Company in 1918, which brought Deere into the tractor business. More on this in the next section — but the point is that Butterworth had the strategic vision to recognize that the future of farming was mechanized power, not animal-drawn implements.

The next leader, Charles Deere Wiman — the great-grandson of John Deere — became president in 1928, just in time for the worst economic catastrophe in American history. Leading an agricultural equipment company through the Great Depression required a particular blend of stubbornness and adaptability. Farm incomes collapsed. Equipment purchases evaporated. Competitors went bankrupt or were absorbed by larger companies.

Wiman kept Deere alive through cost-cutting and careful capital allocation, but he also did something counterintuitive: he continued to invest in product development. In 1934, Deere introduced the famous Model "A" tractor, followed by the Model "B" in 1935. These were not incremental improvements — they were beautifully designed, reliable machines that represented a generational leap forward.

The styling was done by Henry Dreyfuss, the legendary industrial designer who also designed the Bell telephone and the Honeywell thermostat. The relationship between Dreyfuss and Deere would last for decades and reshape the entire farm equipment industry. Dreyfuss did not merely apply cosmetic touches. He studied how farmers actually used tractors — where their hands went, what their sightlines needed to be, how their bodies fatigued during twelve-hour days in the field. He redesigned controls for ergonomic efficiency, improved visibility from the operator's station, and created a visual language that was both functional and beautiful. Dreyfuss brought a consumer-products sensibility to farm equipment, making tractors that farmers actually wanted to look at, not just use. It was the first time a farm equipment company treated aesthetics and human factors as competitive advantages — a philosophy that Deere continues to this day, with its modern cabs designed for comfort during shifts that can stretch to sixteen hours during planting and harvest season.

When Wiman died in 1955, leadership passed to William Hewitt, his son-in-law. Hewitt was perhaps the most consequential leader in Deere's history after the founder himself. A Harvard Business School graduate, Hewitt possessed a global vision that his predecessors lacked — not through any failure on their part, but because the world itself had changed. Post-war America was the dominant industrial power, and American companies had both the opportunity and the obligation to think internationally.

Hewitt's first major move was to purchase a majority share of the Heinrich Lanz tractor company in Mannheim, Germany, in 1956. The Lanz Bulldog tractor had been one of Europe's most popular machines since 1921, with over 220,000 units produced. By acquiring Lanz, Hewitt gave Deere an instant manufacturing presence in Europe — a factory, a workforce, a distribution network, and brand recognition. He followed this by acquiring land for a factory in Monterrey, Mexico, establishing Deere's first manufacturing footprint in Latin America.

These were not merely geographic expansions. They represented a fundamental change in Deere's identity from an American company that sold abroad to a multinational corporation that manufactured and sold globally. The Mannheim plant would go on to produce over two million tractors, becoming the largest John Deere production facility outside North America and the largest tractor factory in Germany.

Hewitt also made a decision that seems minor but had lasting cultural impact: he commissioned the architect Eero Saarinen to design a new world headquarters in Moline. When peers and board members urged him to relocate the company to New York or San Francisco — as befitting a new global corporation — Hewitt refused. Deere would stay in Moline. But it would get a headquarters worthy of its ambitions.

Saarinen's solution was brilliant. He chose Cor-Ten weathering steel for the building's exterior — steel that deliberately rusts on its surface to form a protective patina. Hewitt had asked for a building that looked "down-to-earth." Saarinen delivered a building that literally changed color as it aged, developing the warm brown tones of freshly plowed soil. It was the first major use of Cor-Ten steel in architecture, and the Deere Administrative Center, completed in 1964, has been cited as one of the finest corporate architectural achievements of the twentieth century. Saarinen, who also designed the Gateway Arch in St. Louis and the TWA Flight Center at JFK Airport, died before construction was completed; his associate Kevin Roche finished the project. The landscape, designed by Sasaki Associates, includes two artificial lakes that mirror the building's clean lines.

The headquarters was more than a building. It was a statement of identity: Deere was rooted in the heartland, but it thought globally. It worked with steel, but it valued beauty. It was old, but it was modern.

Across five generations, the family leadership of Deere followed a remarkably consistent pattern: each leader strengthened the institutional capabilities that their predecessor had begun to build. John Deere established the quality standard. Charles built the distribution system. Butterworth consolidated the company. Wiman invested through adversity. Hewitt went global. The cumulative effect was a company that, by the late 1950s, was positioned to make its run at undisputed industry leadership.

IV. The Tractor Revolution: Waterloo Boy to Industry Leadership (1918-1960)

On March 14, 1918, Deere & Company wrote a check for $2,350,000 — roughly $50 million in today's money — to acquire the Waterloo Gasoline Traction Engine Company of Waterloo, Iowa. It was the single most important acquisition in the company's history, and one of the most consequential in the history of American agriculture.

The context matters. By the late 1910s, it was clear that the tractor would do to farming what the automobile was doing to transportation. Deere had dabbled in building its own tractor, including an experimental model called the Dain All-Wheel-Drive, designed by board member Joseph Dain Sr. But the Dain tractor was expensive to produce and mechanically complex. Rather than spend years developing a competitive product from scratch, Deere chose to buy one.

The Waterloo Gasoline Engine Company was the first company to successfully manufacture and sell gasoline-powered farm tractors at scale. Its flagship product, the Waterloo Boy, was a simple, rugged, two-cylinder machine that already had a strong reputation among farmers. The acquisition gave Deere not just a product, but a factory, an engineering team, and — crucially — the institutional knowledge of how to build tractors. Within three years, Deere had produced over 5,000 tractors from the Waterloo plant.

What followed was the two-cylinder era, one of the most distinctive periods in the history of any industrial company. For over four decades — from 1918 to 1960 — John Deere tractors used horizontally mounted two-cylinder engines. These engines produced a sound so distinctive that they earned the nickname "Poppin' Johnnies" or "Johnny Poppers." The rhythmic pop-pop-pop of a two-cylinder Deere became the literal soundtrack of American farming.

Why did Deere stick with two cylinders when competitors were moving to four and six? The answer reveals something fundamental about the company's engineering philosophy. Two-cylinder engines were simpler, cheaper to manufacture, and easier for farmers to maintain. A farmer could overhaul a two-cylinder Deere engine with basic tools and modest mechanical skill. This was not a weakness — it was a deliberate design choice that reflected deep understanding of the customer. Farmers in the 1920s through 1950s often lived hours from the nearest mechanic. A tractor that broke down during harvest could mean financial ruin. The simplicity and reliability of the two-cylinder design was a feature, not a limitation.

The model lineup expanded steadily. The Model D, introduced in 1923, remained in production for an astonishing thirty years — until 1953. The Models A and B, introduced in the mid-1930s with Henry Dreyfuss styling, were commercial blockbusters. Over 290,000 Model A tractors were sold. These machines did not just till fields — they reshaped the economics of American farming, allowing individual farmers to cultivate dramatically more acreage with less labor.

World War II interrupted civilian production but demonstrated Deere's manufacturing versatility. The company won over 1,000 military contracts, producing military tractors, ammunition, aircraft parts, M3 tank transmissions, cargo units, and mobile laundry units. A "John Deere Battalion" was formed as a special ordnance group that saw action in Europe, with roughly 4,500 Deere employees serving in the military. Charles Deere Wiman, the company president and John Deere's great-grandson, even proposed to the Army that armored John Deere tractors could serve as machine gun carriers. A prototype based on the Model A was shipped to Aberdeen Proving Ground for testing in January 1941.

The war years reinforced Deere's manufacturing capabilities and proved that its factories could produce far more than farm equipment. The government formed a separate entity, the Iowa Transmission Company, to manage some of the tank transmission production — an unusual arrangement that reflected the scale of Deere's wartime contribution. Approximately 4,500 Deere employees served in the military, and the company maintained active correspondence with its employees overseas, sending newsletters and care packages that reinforced the institutional bonds that have always characterized Deere's relationship with its workforce.

But Deere's leadership made a disciplined choice after the war: rather than diversifying into military or industrial equipment as some competitors did, Deere doubled down on agriculture. International Harvester, by contrast, spread into refrigeration, air conditioning, and trucks — a diversification that would dilute its focus on farm equipment. This focus would prove decisive for Deere over the following two decades.

By the late 1950s, however, the two-cylinder era was coming to an end. Competitors, particularly International Harvester and Ford, were offering four- and six-cylinder tractors with more power and smoother operation. Deere's market share was slipping. The company needed a dramatic response — and it delivered one of the most audacious product launches in industrial history.

On August 30, 1960, Deere staged what remains one of the most spectacular product launches in industrial history. The company chartered what was described as the largest industrial airlift ever organized, flying 5,670 dealers and approximately 1,000 additional guests — journalists, analysts, dignitaries — into Dallas, Texas. By Monday evening, more than 6,000 passengers had been safely landed at Dallas airports. The following day, they converged on the Dallas Memorial Auditorium for what Deere called "Deere Day in Dallas."

The event was choreographed with the showmanship of a Hollywood premiere. When the curtain rose, Deere unveiled an entirely new lineup — the "New Generation of Power." The 1010 small utility, the 2010 utility, the 3010 row-crop, and the flagship 4010, rated at 80 horsepower but testing at 84 HP during Nebraska trials, making it one of the most powerful two-wheel-drive farm tractors in existence. Every machine featured dramatically improved operator comfort: conveniently located controls, better visibility, improved seat suspension, and a modern operator station. In a single day, Deere retired its forty-year-old two-cylinder platform and replaced it with modern four- and six-cylinder machines that were quieter, more powerful, and more comfortable than anything on the market.

The dealers in the auditorium went wild. The response was not just enthusiasm — it was relief. Many had feared that Deere's commitment to two cylinders had become a liability. The New Generation proved that Deere could innovate radically when the market demanded it, but also that the company had the discipline to time that innovation for maximum competitive impact. The new tractors were not rushed prototypes — they were the culmination of seven years of secret development, conducted in separate engineering facilities with extraordinary security measures to prevent competitors from learning about the radical redesign. Deere had bet the entire company on abandoning its signature architecture, and it had done so with meticulous preparation.

The results were immediate and devastating to the competition. By 1963, just three years after the Dallas unveiling, Deere & Company passed International Harvester in total sales to become the largest farm equipment manufacturer in the world. To appreciate the magnitude of this shift: in 1929, IH held fifty-two percent of the tractor market versus Deere's twenty-one percent. By 1964, Deere had climbed to thirty-four percent market share and the number one position. It was a reversal of fortune that the industry had considered unthinkable. Deere has never relinquished the top spot.

The rivalry between Deere and IH was intense enough to breed borderline industrial espionage. During the 1970s, when IH and Deere factories were about a mile apart in the Quad Cities, Deere engineers would photograph IH prototypes being shipped out on railroad cars. As one Deere employee later recalled: "We watched the Axial-Flow being built. Whenever they shipped something out, we could see it go by on the railroad car and we'd take pictures of it." IH's eventual collapse in the 1980s — sold off, renamed Navistar, reduced to trucks and engines — left Deere as the only original American farm equipment manufacturer to survive intact from the nineteenth century to the present.

V. Brand Building: The Leaping Deer, Green & Yellow, and "Nothing Runs Like a Deere"

In the world of agricultural equipment — a world of mud, diesel exhaust, and hard metal — branding might seem like an afterthought. It is anything but. Deere & Company has built what is arguably the strongest brand in heavy equipment, and possibly one of the strongest in any industrial category. Understanding how that brand was constructed, piece by piece over more than a century, reveals strategic choices that business schools could study for decades.

Start with the logo. The leaping deer has been associated with Deere & Company since the 1870s, making it one of the longest-continuously-used trademarks in American business. The first formal registration came in 1876, when the company was producing over 60,000 plows per year and copycats had become a serious threat. That original mark showed a deer leaping over a log, with "John Deere" arcing above in capital letters. The logo evolved through six major revisions — in 1910, 1936, 1968, and 2000 being the most significant — each time becoming simpler and more iconic.

The 1936 revision was driven by a practical need: the existing design was too detailed to stencil cleanly onto equipment. The deer became a solid silhouette with outstretched legs, creating a bolder, more recognizable profile. In 1968, the logo was streamlined further to show just two legs and a single rack of antlers — a clean, modern mark that could work at any size. The 2000 revision was the most dramatic departure: for the first time, the deer was rendered in green and yellow instead of black and white, and the animal was shown leaping upward rather than horizontally. The message was unmistakable: this is a company on the rise.

The green and yellow color scheme itself dates to approximately 1910, when Deere began painting its equipment in these colors to differentiate from the competition — most notably International Harvester, whose machines were predominantly red. The choice was not arbitrary. Green harmonized with the agricultural landscape, helping machinery blend into the fields it worked. Yellow provided striking contrast for improved visibility, a genuine safety consideration when massive machines operate in dawn or dusk conditions.

Over time, the colors became so synonymous with the brand that "Deere green" entered the vernacular of rural America. Farmers do not say they bought a "Deere tractor." They say they "went green." The color rivalry between Deere green and IH red (later Case IH red) is one of the great tribal divisions in agricultural communities, passed down through generations with the intensity of a college football rivalry.

Then there is the slogan — and its origin story is one of the best in advertising history. "Nothing Runs Like a Deere" was born not from tractors or farm equipment, but from the company's snowmobile division. Between 1971 and 1982, Deere manufactured nearly 250,000 snowmobiles at its plant in Horicon, Wisconsin. When Gardner Advertising was tasked with creating a tagline for the new snowmobile line, copywriters devised nearly one hundred different ideas. Every single one was rejected by Deere's management. The document was thrown in the trash.

The next day, a determined copywriter named Bob Wright frantically picked through the garbage, convinced that something usable had been discarded. Among the rejected ideas, he found "Nothing Runs Like a Deere." The agency itself had thought the slogan was too "silly" to present to the client — a pun, really, that played on the homophone of "deer" and "Deere." But when it was finally shown to John Deere management, they immediately recognized its potential and approved it. The slogan proved so effective that it transcended snowmobiles, spread to the lawn equipment division, and eventually became the company's universal corporate tagline. It works on multiple levels: it makes a bold reliability claim, it is effortlessly memorable, and the wordplay gives it a warmth unusual in industrial branding. In 1980, when John Deere became the official snowmobile supplier for the Winter Olympics in Lake Placid, the slogan reached a global audience for the first time.

The green-versus-red rivalry deserves special mention because it illustrates how deeply the Deere brand penetrates customer identity. In 1993, country music artist Joe Diffie released "John Deere Green," a hit single about a young man painting a love declaration on a water tower in that iconic shade. It reached number five on the Billboard Hot Country Singles chart. No other equipment manufacturer has ever had a hit song written about its paint color. The brand had transcended commerce and entered culture. Deere fought throughout the 1980s to legally trademark its green and yellow color combination, finally succeeding in 1988. In a landmark 2017 lawsuit, a court ruled that the John Deere green and yellow configuration qualified as a "famous" trademark — meaning it was widely recognized by the general consuming public, not just farmers.

The cultural significance of the Deere brand in rural America is difficult to overstate. John Deere merchandise — hats, jackets, belt buckles, toys — generates hundreds of millions in licensing revenue. The brand appears at county fairs, rodeos, and farm auctions. Children grow up on John Deere pedal tractors. There is a John Deere Tractor & Engine Museum in Waterloo, Iowa, that draws visitors from around the world. The brand is not aspirational in the luxury-goods sense — it is aspirational in the way that competence and reliability are aspirational. Owning Deere equipment signals to your neighbors that you are serious about farming, that you value quality, and that you can afford the best.

For investors, the brand serves as a powerful pricing shield. In a market where equipment is technically commoditized — a tractor is a tractor — Deere consistently commands premium pricing over competitors like AGCO, CNH Industrial, and Kubota. Farmers pay more for Deere equipment because they trust it will last longer, hold its resale value better, and be supported by a dealer network that understands their needs. That premium pricing flows directly to margins, which is why Deere's operating margins consistently exceed those of its peers.

VI. Modernization & Globalization (1960s-2000s)

The decades following the Dallas unveiling were a period of relentless expansion, punctuated by one of the most brutal agricultural downturns in American history. How Deere navigated this era — seizing opportunities during good times while surviving and even strengthening during crises — is the story of a company learning to manage the inherent cyclicality of its industry.

The 1960s and 1970s were golden years. The "Green Revolution" in global agriculture — the worldwide adoption of high-yield crop varieties, chemical fertilizers, and mechanized farming — drove explosive demand for larger, more powerful equipment. Deere's product line expanded to match. The company introduced articulated four-wheel-drive tractors for the massive farms of the Great Plains, combines that could harvest hundreds of acres per day, and a growing range of construction equipment that leveraged its manufacturing expertise for non-agricultural markets.

The construction equipment entry deserves attention because it illustrates a strategic pattern that would recur throughout Deere's history: using agricultural engineering expertise to enter adjacent markets. Deere introduced its first backhoe loader in 1971 and quickly expanded into bulldozers, excavators, and motor graders. The logic was sound — the same engineering capabilities that produce a reliable tractor can produce a reliable excavator, and the same dealer network that serves farmers can serve contractors. By the 1980s, construction equipment provided meaningful revenue diversification that helped buffer the agricultural downturn. Today, the Construction and Forestry segment generates over $13 billion in annual revenue — roughly a quarter of the company's total.

Deere also made some notable detours during this era. In the 1890s, the company had briefly sold bicycles during the cycling craze — three models called the Deere Roadster, Deere Leader, and Moline Special — generating over $150,000 in revenue (equivalent to roughly $5.5 million today) before the fad faded by 1900. In the 1970s, the diversification impulse was stronger. Deere manufactured snowmobiles from 1971 to 1982, producing nearly 250,000 units at its Horicon, Wisconsin plant. And from 1972 to 1975, Deere again tried bicycles, selling roughly 200,000 Taiwan-built bikes through its dealer network. None of these ventures lasted, but each demonstrated the reach and flexibility of the dealer distribution system.

The corporate restructuring reflected this ambition. In 1958, the present firm was incorporated as John Deere-Delaware Company, later assuming the Deere & Company name after merging with the older entity and its subsidiaries. This legal reorganization streamlined the corporate structure for the multinational expansion that William Hewitt was driving.

Internationally, Deere was building on Hewitt's initial moves into Germany and Mexico — but the expansion was far from smooth. The Mannheim transition illustrates the complexity. When Deere acquired the Lanz operation, it inherited a product line of seventeen tractor models, many badly outdated. The transition was methodical: the line was trimmed from seventeen to fifteen models in 1957, then to twelve, then to eleven. In 1958, the paint scheme was changed from the Lanz blue lacquer with red wheels to Deere green and yellow — a visual absorption of one of Germany's most beloved tractor brands into the American company. By 1960, the factory was renamed John Deere Lanz AG, Bulldog production ended after four decades, and the first modern John Deere-designed tractors rolled off the Mannheim line.

But the broader international expansion was enormously painful. For fifteen years, Deere's overseas operations suffered huge losses — managerial mistakes, unforeseen startup problems, foreign exchange difficulties, and geopolitical complications from Communism to apartheid. Hewitt's conviction, which he defended repeatedly to skeptical board members, was that Deere had to expand internationally or risk being forced out of the market entirely as global competition intensified. The patience paid off. Deere also entered Argentina, Brazil, France, Spain, South Africa, and Australia, building or acquiring manufacturing facilities in each market. Hewitt led the company for twenty-seven years until his retirement in 1982, making him the longest-serving CEO in Deere's history and the last family member to lead the company.

Then came the 1980s farm crisis — the most devastating agricultural downturn since the Great Depression. The crisis had its roots in the 1970s, when high grain prices and easy credit encouraged American farmers to take on enormous debt to buy land and equipment. When the Federal Reserve raised interest rates to combat inflation in the early 1980s and grain prices simultaneously collapsed, farmers were caught in a lethal vice. Land values plummeted. Bankruptcies soared. Equipment purchases evaporated almost overnight.

For Deere, the impact was brutal. In October 1979, the company employed over 16,000 workers at its Waterloo plant alone. Between 1980 and 1985, Deere laid off forty percent of its hourly U.S. workforce and fifteen percent of salaried employees worldwide — an overall thirty percent reduction. Revenue dropped from approximately $5.5 billion in 1980 to $4.5 billion by 1985. In 1986, the company posted a net loss of $229 million, followed by a $193 million loss in the first quarter of 1987 alone. A bitter five-month strike and lockout with the United Auto Workers in 1986-87 — the longest labor stoppage in company history — piled pain on top of pain.

But Deere's competitors had it far worse. International Harvester — Deere's century-old rival — was destroyed. The catastrophe had been building for years. IH's 1958 recall of its 460 and 560 tractors, caused by final drive failures from components that had not been updated since 1939, had already shaken customer confidence. Then, on November 1, 1979, the very day IH announced a $1.8 million bonus for CEO Archie McCardell, the United Auto Workers called a strike that lasted 172 days and cost IH nearly $600 million. For fiscal years 1980, 1981, and 1982, IH recorded a combined $2.4 billion in losses — at the time, the largest three-year loss for any American company in history. In November 1984, IH sold its farm equipment division to Tenneco, which merged it with J.I. Case to form Case IH. The company that had dominated American agriculture for three-quarters of a century renamed itself Navistar International and retreated to trucks and engines. Massey Ferguson narrowly avoided bankruptcy. Allis-Chalmers exited the tractor business entirely.

Deere survived — and the reasons illuminate the company's structural advantages. What saved Deere was a decision made before the crisis hit. Under chairman Robert A. Hanson and the leadership team, management had insisted during the prosperous 1970s that excellent earnings be used to pay down debt, modernize factories, and launch quality and cost-reduction initiatives rather than being distributed as dividends or spent on acquisitions. The result: in 1980-81, Deere's interest and overhead costs were less than five percent of sales, while the nearest competitor's equivalent costs were fourteen percent. This financial fortress allowed Deere to borrow at favorable rates while competitors paid crippling interest.

Deere also continued to invest in manufacturing technology even during the downturn. In 1981, the company opened a factory in Waterloo, Iowa, that cost over $1.5 billion and made extensive use of computers and robots — one of the earliest examples of "flexible manufacturing" in heavy industry. And critically, Deere stood by its dealers and customers. Rather than abandoning its distribution network, Deere used its financial strength to develop incentives for farmers to continue upgrading equipment and provided dealers with inventory and interest support that kept them solvent until conditions improved. When the crisis finally broke, Deere's dealer network was intact while competitors' networks had been hollowed out.

The results were dramatic. In 1988, sales soared thirty percent from the prior year and profit exceeded $315 million — a record. Deere emerged from the crisis as the dominant player in a much more consolidated industry. The company also began investing in what would become its next great strategic advantage: precision agriculture. In the early 1990s, Deere started integrating GPS guidance systems into its equipment. To appreciate why this mattered, consider the economics of overlap. When a farmer drives a tractor across a field without GPS guidance, the natural tendency is to overlap rows slightly — better to spray twice than to miss a strip. But even a few inches of overlap across thousands of acres translates to significant waste: extra seed, extra fertilizer, extra herbicide, extra fuel. GPS guidance, which Deere introduced commercially in 1996 with its StarFire receiver, allowed farmers to plant and spray with accuracy measured in inches rather than feet. The first systems cost over $10,000 and provided accuracy of plus or minus one foot. By the mid-2000s, RTK (Real Time Kinematic) correction brought accuracy to within one inch.

The financial impact was immediate. Farmers who adopted GPS guidance reported fuel savings of five to ten percent, input savings of seven to twelve percent, and the ability to farm at night and in low-visibility conditions. For a 5,000-acre corn operation, precision guidance could save $50,000 to $100,000 per year — paying for the equipment in one or two seasons. This was the beginning of the transformation from farming by feel to farming by data, and it established the pattern that Deere would follow for the next three decades: invest in technology that pays for itself through measurable farm economics.

The dealer network continued to evolve. In 2002, Deere introduced its "Dealer of Tomorrow" initiative, encouraging consolidation among its dealer base. The company envisioned fewer, larger dealerships with professional management, sophisticated service capabilities, and the capital to invest in technology. By 2018, eighty-three percent of Deere's 1,522 agricultural equipment stores in North America were part of large dealer groups owning five or more locations, up from seventy-four percent just the year before. The number of dealer groups with ten or more stores had grown from twenty-four in 2011 to sixty-one.

This consolidation was controversial — longtime family dealerships were pressured to sell or merge — but it created a dealer network that could provide the kind of technology support that modern precision agriculture demands. To become a John Deere dealer today requires minimum equity of $35 to $45 million, a barrier that ensures only well-capitalized operators need apply. A dealer selling a $500,000 combine equipped with GPS, yield monitors, and variable-rate application systems needs technicians who understand both diesel engines and software diagnostics. The "Dealer of Tomorrow" strategy ensured Deere's dealers could deliver on that promise.

Meanwhile, the Mannheim factory that Hewitt acquired in the 1950s continued to grow. In March 2023, the plant produced its two-millionth tractor — a 6R 250, unveiled in the presence of CEO John C. May. It took seventy years to produce the first million Mannheim tractors, but only about thirty years for the second million. The factory now employs approximately 3,300 workers and produces 40,000 tractors per year — making it the largest tractor production facility in Germany, responsible for two-thirds of all tractors manufactured in the country. More than $80 million is being invested in the facility's future, including preparation for autonomous and battery-electric tractor production.

As of 2018, Deere & Company employed approximately 67,000 people worldwide, with about half in the United States and Canada. The company was ranked eighty-fourth on the Fortune 500 list. From a nearly fatal crisis in the 1980s, Deere had emerged as a larger, leaner, more technologically advanced company operating on a truly global scale.

VII. The Smart Industrial Revolution: Precision Agriculture & Technology (2000s-Present)

If the Waterloo Boy acquisition in 1918 was the moment Deere entered the mechanization era, then the technology investments of the 2000s and 2010s mark Deere's entry into the information era. The transformation is profound, and it is ongoing. Deere is no longer just selling machines that till soil and harvest grain. It is building an integrated ecosystem of hardware, software, and data that aims to optimize every aspect of farming — from what to plant and when, to how much fertilizer to apply per square meter, to whether a human needs to be in the cab at all.

The company today operates through four segments: Production and Precision Agriculture (large tractors, combines, cotton pickers, sprayers, and soil preparation equipment), Small Agriculture and Turf, Construction and Forestry, and Financial Services. But the strategic center of gravity is increasingly the first segment, where the highest-margin, most technology-intensive products live.

The precision agriculture revolution begins with data. To understand what Deere is building, consider the analogy of a smartphone. A tractor used to be like a basic cell phone — it did one thing (make calls, or in this case, pull implements). Deere's vision is to make the tractor more like a smartphone — a platform that runs applications, collects data, and connects to a broader ecosystem that gets smarter over time.

Deere's Operations Center is a cloud-based farm management platform where farmers can plan operations, monitor equipment in real time, and analyze yield data across seasons. Think of it as the agricultural equivalent of a Bloomberg terminal — a single pane of glass through which a farmer can see everything happening on their operation. Equipment equipped with Deere's technology streams data continuously: soil conditions, moisture levels, planting depth, yield per acre, fuel consumption, engine diagnostics. Every pass across a field generates data that can be analyzed to improve the next pass, the next season, the next decade.

But the real breakthrough is what Deere does with that data. The company's See & Spray technology, originally developed by Blue River Technology (which Deere acquired in 2017 for a reported $305 million), uses computer vision and machine learning to identify individual weeds in a field and spray only those plants, rather than blanketing an entire field with herbicide. For non-technical readers, here is what this means in practice: a traditional sprayer moves across a field dispensing herbicide uniformly — every square inch gets the same treatment, whether there is a weed there or not. See & Spray mounts cameras on the sprayer boom that photograph the ground thousands of times per second, uses AI to distinguish weeds from crop plants in real time, and then activates individual spray nozzles only when a weed is detected. The cameras scan over 2,500 square feet per second at speeds up to fifteen miles per hour, triggering nozzles through Deere's ExactApply system. The result is targeted treatment rather than blanket application — like switching from carpet bombing to precision strikes.

The results have been remarkable. During the 2025 growing season, See & Spray was used across more than five million acres. Farmers using the technology reduced non-residual herbicide use by an average of nearly fifty percent, saving nearly thirty-one million gallons of herbicide mix. Third-party researchers found that growers using See & Spray yielded two additional bushels per acre, with some operations seeing gains as high as 4.8 bushels per acre. To put this in context for non-farmers: reducing herbicide use by half while simultaneously increasing yield is the kind of outcome that the agricultural industry has been chasing for decades. Deere achieved it through computer vision.

In 2025, Deere introduced a bold new pricing model for See & Spray called the Application Savings Guarantee. Rather than charging a flat fee for the technology, Deere aligned its pricing with the value delivered: farmers pay one dollar per fallow acre or five dollars per in-crop acre, but only when the technology delivers measurable savings. It is a pay-for-performance model that echoes software-as-a-service economics — and it signals Deere's evolution from a company that sells equipment to one that sells outcomes.

Autonomy represents the next frontier, and Deere is pursuing it with the same all-in conviction that characterized the New Generation launch in 1960. At CES 2025 in January, Deere unveiled four new autonomous machines: an autonomous 9RX tractor for large-scale agriculture, an autonomous 5ML orchard tractor for air-blast spraying, a 460 P-Tier autonomous articulated dump truck for quarry operations, and an autonomous battery-electric mower for commercial landscaping.

The technology behind autonomous farming deserves explanation, because it is genuinely remarkable. The second-generation autonomy kit features sixteen cameras mounted in pods that provide 360-degree vision around the tractor. These cameras feed images to onboard processors that identify obstacles — people, animals, other equipment — and make real-time decisions about whether to proceed, slow down, or stop. Detection range increased fifty percent from the first generation, from sixteen meters to twenty-four meters, enabling machines to run forty percent faster and pull implements twice as wide. The farmer manages everything from a smartphone app, with what Deere calls "swipe to farm" functionality. A farmer can set up a field operation, approve the route, and let the tractor run autonomously while they tend to other tasks — or sleep.

Autonomous 8R tractors were field-tested in eighteen states during 2025. The Mannheim factory announced plans to present its first fully autonomous, battery-driven tractor delivering approximately 100 horsepower in 2026. Farms that adopted autonomous technology reported fifteen to twenty percent productivity surges, while GPS guidance alone delivered an average six percent reduction in fuel and labor costs.

Deere also pursued strategic acquisitions to fill technology gaps. In May 2025, it acquired Sentera, a Minneapolis-based provider of drone-based aerial imagery for agriculture. Sentera's drones fly over fields at high speed, generating high-resolution images that are processed through its FieldAgent application to identify individual weeds and create targeted prescription spray maps. Three months later, Deere acquired GUSS Automation, a California company specializing in autonomous sprayers. In December 2025, it announced the acquisition of Tenna, a construction technology company providing fleet tracking and jobsite management solutions.

The controversial counterpoint to Deere's technology strategy is the right-to-repair battle. As Deere's equipment became increasingly software-dependent, the company argued that farmers should not be permitted to access or modify the software that controls their machines, citing the Digital Millennium Copyright Act. Farmers who tried to repair their own equipment found that many diagnostic functions were locked behind proprietary software accessible only through authorized dealerships. Some farmers turned to unauthorized Ukrainian-sourced firmware to circumvent these restrictions.

The backlash was significant. The Electronic Frontier Foundation criticized Deere's position as contrary to the fundamental right to repair. In January 2025, the FTC filed a lawsuit against John Deere alleging monopolistic repair practices; a federal judge subsequently rejected Deere's motion to dismiss. More than a dozen states introduced right-to-repair bills in 2025. Iowa — Deere's home state — advanced a bill specifically targeting agricultural equipment in early 2026. At the federal level, the Freedom for Agricultural Repair and Maintenance (FARM) Act was introduced in Congress in late 2025. In February 2026, the EPA issued guidance clarifying that manufacturers cannot use the Clean Air Act to prevent farmers from repairing their own equipment.

Deere has begun to soften its position, making a "temporary inducement override capability" available through its Operations Center PRO Service digital repair tool and signing a memorandum of understanding with the American Farm Bureau Federation. But the tension between Deere's desire to control its technology ecosystem and farmers' insistence on repairing their own property remains unresolved.

Closely related is the question of data ownership. When a Deere combine harvests a field, it generates terabytes of data: yield maps, soil moisture readings, operating parameters, and GPS coordinates. Who owns that data — the farmer who grew the crop, or Deere, whose equipment collected it? The answer has enormous implications. If Deere can aggregate anonymized farm data across its installed base, it can build AI models of unprecedented accuracy — models that could predict crop yields, optimize planting decisions, and revolutionize agricultural insurance and commodity trading. If farmers demand full control of their data, this aggregation becomes more difficult. Deere's current position — expressed through its Operations Center platform — is that farmers own their data and can choose to share it, but the practical reality is that most data flows through Deere's ecosystem.

For investors, this constellation of issues — right to repair, data ownership, and technology platform control — represents the most significant regulatory and reputational risk facing the company. The worst-case scenario is legislation that forces Deere to open both its repair tools and its data platform, eroding the switching costs that underpin its competitive advantage. The best-case scenario is that Deere navigates these concerns gracefully, maintaining enough control to monetize its technology while satisfying farmers and regulators that it is acting fairly.

VIII. Financial Performance & Business Model Evolution

To understand Deere's financial trajectory, you need to understand one thing above all else: cyclicality. Deere's revenue and earnings rise and fall with farm income, which rises and falls with commodity prices, which rise and fall with weather, global trade flows, currency movements, and government policy. This cyclicality is not a flaw in the business model — it is the business model. The question is never whether Deere will have down cycles, but how well it manages them.

The recent cycle tells the story clearly. Fiscal year 2022 brought revenue of $52.6 billion, a nineteen percent increase over the prior year, driven by surging commodity prices and pent-up demand following the pandemic. FY2023 was even better: $61.3 billion in revenue, up nearly seventeen percent, with net income reaching a record $10.2 billion. Deere was generating extraordinary profitability — operating margins in the Production and Precision Agriculture segment exceeded twenty-five percent.

Then the cycle turned. Commodity prices declined — corn fell thirty-seven percent from its 2022 peak, soybeans dropped twenty-four percent, wheat fell thirty-five percent. Farm incomes contracted, and farmers pulled back on equipment purchases. FY2024 revenue declined to $51.7 billion, a sixteen percent drop. Net income fell to $7.1 billion. FY2025 continued the slide: revenue of $45.7 billion (down twelve percent) and net income of $5.0 billion (down twenty-nine percent from the peak).

The most recent quarter — Q1 FY2026, ended February 1, 2026 — showed the first tentative signs of recovery. Revenue rose thirteen percent year-over-year to $9.6 billion, beating consensus estimates, though net income of $656 million reflected continued pressure from tariffs, warranty expenses, and unfavorable mix in large agriculture. Construction & Forestry was the standout segment, with sales surging thirty-four percent. Small Agriculture & Turf operating profit jumped fifty-eight percent. Management raised full-year FY2026 guidance, projecting net income of $4.5 to $5.0 billion and cash flow from equipment operations of $4.5 to $5.5 billion. CEO John May stated his belief that 2026 represents "the bottom of the current cycle."

The segment structure reveals the company's diversification strategy. Production and Precision Agriculture is the largest and most profitable segment, but it is also the most cyclical, as it depends on purchases by large commercial farming operations. Small Agriculture and Turf provides exposure to smaller farms and the consumer/commercial landscaping market — less cyclical but lower margin. Construction and Forestry offers diversification away from agriculture entirely. And Financial Services — the segment that does not get nearly enough attention — is the hidden profit engine.

John Deere Financial manages a worldwide portfolio exceeding $40 billion and operates in forty-five countries. Its roots go back to the mid-nineteenth century, when Deere recognized that farmers often needed credit to purchase expensive implements. The modern financial services operation was formalized in 1986, when the financing and leasing operations of thirteen U.S. sales branches were consolidated into a single entity called John Deere Credit, later renamed John Deere Financial in 2010, with headquarters in Johnston, Iowa.

Think of it as the GMAC of agriculture — a captive finance arm that makes the equipment sale possible while generating substantial interest income. When a farmer walks into a Deere dealership and finances a $400,000 combine, Deere makes money on the sale and then makes money on the financing for years afterward. The division provides retail financing at the point of sale through dealers, wholesale floor-plan financing to the dealer network, extended warranties, and retail revolving charge accounts. At times, the financial services division has accounted for roughly one-third of Deere's total income. In FY2025, the segment generated approximately $840 million in net income — a significant contribution that persists even when equipment sales decline.

The strategic value of John Deere Financial extends beyond the income statement. During the 1980s farm crisis, Deere's ability to offer favorable financing terms when independent lenders were charging crushing interest rates was a decisive competitive weapon. The financing division also provides deep visibility into customer purchasing patterns, equipment utilization, and financial health — data that informs Deere's production planning and product development decisions.

The financial model also includes significant tariff headwinds that have become increasingly material. In FY2025, tariffs on steel, aluminum, and broader trade levies cost Deere approximately $600 million in pre-tax earnings. For FY2026, the projected impact has doubled to approximately $1.2 billion. Deere has responded with a combination of cost discipline (including a salary freeze for all salaried employees in FY2026), production restraint (deliberately underproducing relative to retail demand to normalize dealer inventories), and selective price increases.

One of the most impressive aspects of Deere's recent financial management is its approach to production restraint. During the current downturn, management deliberately produced fewer machines than retail demand would support. This seems counterintuitive — why leave revenue on the table? The answer is dealer inventory management. During previous downturns, manufacturers flooded dealers with equipment that could not be sold, creating a glut that depressed used equipment values and strained dealer balance sheets. Deere's approach was to keep production below retail takeaway, ensuring that dealer lots stayed lean and used equipment values remained supported. This protects the dealer network's financial health, maintains residual values that benefit John Deere Financial's leasing portfolio, and positions the company for a sharper recovery when the cycle turns — because pent-up demand will be stronger if dealers need to restock rather than merely sell through existing inventory.

The company's capital allocation deserves attention as well. Deere has returned substantial capital to shareholders through dividends and buybacks. Over the past five years, the company has repurchased over $15 billion in stock while maintaining investment-grade credit ratings. The dividend has been increased for more than thirty consecutive years. This disciplined capital return, combined with countercyclical investment in technology, reflects a management team that understands both the short-term demands of Wall Street and the long-term imperatives of technological leadership.

Despite the cyclical downturn, Deere's stock reached an all-time high of $674.19 in February 2026. This seeming paradox — stock price at all-time highs while earnings are near cycle lows — reflects the market's forward-looking nature. Investors are pricing in a cyclical recovery, sustained technology leadership, and the structural margin improvement that precision agriculture and autonomous technology are expected to deliver over the coming decade.

For tracking Deere's ongoing performance, two KPIs stand above all others. First, Production and Precision Agriculture operating margin — this metric captures both the pricing power of Deere's technology-enabled large equipment and the cost efficiencies from manufacturing innovation. In peak quarters this margin has exceeded twenty-five percent; watching its trajectory through the recovery will indicate whether Deere's technology investments are genuinely expanding its economic moat. Second, precision technology adoption rates — measured through metrics like acres covered by See & Spray, autonomous tractor deployments, and Operations Center active users. As Deere transitions from a hardware business to a hardware-plus-software platform, these adoption metrics will increasingly drive recurring revenue streams and long-term margin expansion.

IX. Playbook: Business & Investing Lessons

Nearly two centuries of continuous operation produce a rich set of strategic lessons. Some are specific to Deere; others generalize to any business seeking to build enduring competitive advantage.

Building a century-spanning moat through dealer networks. Deere's dealer network is its single most important competitive asset, and it was built over more than a hundred years. The branch house system that Charles Deere pioneered in the 1880s evolved into a modern dealer network that provides sales, parts, service, and increasingly, technology support. Competing with this network is not merely a matter of money — it is a matter of time. A new entrant could theoretically build equivalent equipment, but replicating a dealer network of 1,500-plus locations with decades of customer relationships is effectively impossible in any realistic timeframe. This is the "process power" moat that Hamilton Helmer describes in his 7 Powers framework: a competitive advantage that requires time to build and cannot be compressed.

The power of brand in commoditized industries. The lesson of "Deere green" is that brand matters even — perhaps especially — in markets where products might otherwise be interchangeable. Deere's brand allows it to charge premium prices for equipment that performs similar functions to cheaper alternatives. The brand was not built through advertising alone; it was built through decades of product quality, dealer service, and cultural embedding in rural communities. When a brand becomes part of a customer's identity — when they wear your hat, raise their children on your toy tractors, and define themselves as a "green" or "red" operation — switching costs become emotional, not just economic.

Managing agricultural cycles. Deere's history of navigating boom-bust cycles offers a masterclass in cyclical management. The pattern is consistent: invest in product development and manufacturing capacity during downturns (when competitors are retrenching), then capture disproportionate market share during the recovery. The Model A and B tractors were developed during the Depression. The $1.5 billion flexible manufacturing plant was built during the 1980s crisis. The See & Spray and autonomous tractor technologies were developed during the current downturn. Countercyclical investment requires both capital reserves and management conviction — two things Deere has consistently possessed.

The platform strategy. Deere's evolution from selling individual machines to offering an integrated platform of equipment, software, and financing is one of the most important strategic moves in its recent history. The combination locks customers into the Deere ecosystem in a way that selling standalone tractors never could. A farmer who uses Deere equipment, Deere's Operations Center for data management, Deere's See & Spray for precision application, and Deere Financial for payments has switching costs that compound with every passing season. Each data layer adds stickiness. Each integration point raises the cost of leaving. This is the "switching costs" power from Helmer's framework, amplified by network effects as more farmers generating more data improves the AI models that drive precision agriculture.

Family succession done right. The Deere family's approach to succession is notable for what it did not do as much as what it did. The family did not insist on keeping leadership within the bloodline when better candidates were available — William Butterworth and William Hewitt were both sons-in-law. Each generation chose the leader who was best for the company's next stage of development, whether that person was a family member by birth or by marriage. This flexibility, combined with a genuine institutional culture that transcended any individual, is why Deere navigated the transition from family leadership to professional management without the trauma that destroys many family businesses.

Global expansion while maintaining American identity. Hewitt's internationalization strategy offers a lesson in how to go global without losing your soul. Deere entered foreign markets through acquisition (Lanz in Germany) and greenfield investment (Mexico, Brazil), adapting products to local conditions while maintaining the core brand identity. The Mannheim plant does not produce American tractors for Germans — it produces German-engineered tractors under the John Deere brand. This balance between global integration and local adaptation is why Deere's international operations eventually became profitable after fifteen years of losses. Companies that try to export their domestic formula unchanged almost always fail; companies that fully localize risk losing brand coherence. Deere found the middle path.

Innovation timing: when to be first versus fast follower. The Waterloo Boy acquisition illustrates the fast-follower strategy: rather than developing tractor technology from scratch, Deere bought a proven company with an established product. The New Generation of Power in 1960 illustrates the patient-but-decisive approach: Deere waited until its new technology was fully ready, then launched with overwhelming force. The autonomous technology push illustrates the first-mover strategy: Deere is investing billions to lead a category that does not yet fully exist. The lesson is that there is no single correct timing strategy — what matters is matching the approach to the specific competitive situation.

Myth vs. reality: Is Deere really a "tech company"? The consensus narrative has increasingly framed Deere as "the Tesla of agriculture" — a technology company wrapped in farm equipment. The reality is more nuanced. Deere's technology investments are genuine and substantial, but the company still derives the vast majority of its revenue and profit from selling physical machines. Software and data services remain a small fraction of total revenue. The See & Spray Application Savings Guarantee and Operations Center subscriptions represent the beginning of a SaaS-like model, but Deere is years — perhaps a decade — from the kind of recurring revenue mix that would justify a pure technology multiple. Investors who buy the stock at peak multiples on the "tech company" thesis should understand that they are buying a hardware business with technology upside, not a software company that happens to make tractors.

X. Analysis & Bear vs. Bull Case

Bull Case

The bull case for Deere rests on a structural argument: the world needs to produce dramatically more food with dramatically fewer resources, and Deere is the company best positioned to make that possible.

Global population is projected to reach nearly ten billion by 2050. Arable land per capita is declining. Water resources are increasingly constrained. Climate change is introducing greater variability into growing conditions. Against this backdrop, the only path to feeding the world is radical improvements in agricultural productivity — growing more food per acre with less water, less fertilizer, less herbicide, and less labor. This is precisely what Deere's precision agriculture technology is designed to deliver.

Precision agriculture adoption remains early globally. In the United States, which is the most technologically advanced agricultural market, only a fraction of farmland is managed with the kind of integrated precision technology that Deere offers. In emerging markets — India, Brazil, sub-Saharan Africa — adoption is barely beginning. The total addressable market for precision agriculture technology measured in decades is enormous.

The consolidation of farms is a secular tailwind. As smaller farms are absorbed by larger operations, equipment spending per farm increases. Larger farms need larger, more technologically sophisticated equipment — exactly the high-margin products in Deere's Production and Precision Agriculture segment. Every farm that consolidates from 500 acres to 5,000 acres needs a different class of machinery, and Deere dominates that class.

The transition from one-time equipment sales to recurring software and service revenue is perhaps the most important long-term catalyst. See & Spray's per-acre pricing model, Operations Center subscription services, and autonomous technology licensing could transform Deere's revenue mix over the next decade. If even a fraction of Deere's installed base adopts recurring technology services, the impact on margins and earnings stability would be substantial.

Deere's competitive position, analyzed through Porter's Five Forces, is formidable.

Threat of new entrants: Low. The combination of dealer networks, brand loyalty, manufacturing scale, and technology integration creates barriers that would take decades and tens of billions to replicate. Consider what a new entrant would need: factories capable of producing machines that weigh twenty tons with tolerances measured in thousandths of an inch; a dealer network of 1,500-plus locations staffed by technicians who understand both diesel engines and AI; a financial services arm with $40 billion in assets to finance customer purchases; and a brand trusted by three generations of farming families. No venture-capital-backed startup can replicate this, and even well-capitalized industrial companies have failed trying — witness the decades of failed attempts by SAME Deutz-Fahr and Claas to crack the North American market.

Supplier power: Moderate. Deere is large enough to dictate terms to most suppliers, though steel and semiconductor shortages have periodically created friction. The company's vertical integration in key components — it manufactures its own engines, transmissions, and hydraulic systems — limits supplier leverage on the most critical inputs.

Buyer power: Limited. Farmers lack equivalent alternatives and the emotional attachment to the Deere brand raises switching costs beyond the purely economic. A farmer who has used Deere equipment for decades, whose dealer knows their operation intimately, and whose data lives in the Deere Operations Center faces enormous friction in switching to AGCO or CNH.

Threat of substitutes: Very low. There is no alternative to mechanized farming. The relevant question is not whether farmers will use tractors, but whose tractors they will use.

Competitive rivalry: Manageable. The industry has consolidated to a handful of players — Deere, CNH Industrial (Case IH, New Holland), AGCO (Fendt, Massey Ferguson, Valtra), and Kubota — who compete on technology and service more than price. This oligopolistic structure supports disciplined pricing and healthy margins across the industry, though Deere consistently earns the highest margins.

To put the competitive landscape in concrete terms: Deere holds approximately 53 percent of the large tractor market (over 100 horsepower) in North America. CNH Industrial holds roughly 30 percent. AGCO holds about 10 percent. Everyone else splits the remainder. In combines — the most technologically complex and expensive machines in agriculture — Deere's share is even higher. This kind of dominance in the highest-margin equipment categories is the engine behind Deere's superior profitability.

Through Helmer's 7 Powers lens, Deere possesses at least four: process power (the dealer network and institutional manufacturing knowledge built over 188 years), switching costs (the integrated platform of equipment, software, and financing), brand (the pricing premium and customer loyalty that "Deere green" commands), and scale economies (the ability to spread R&D and manufacturing costs across a larger revenue base than any competitor). The fifth power — counter-positioning — is arguably emerging as Deere's technology platform creates a business model that incumbents cannot replicate without disrupting their own existing businesses. AGCO and CNH are trying to build similar precision agriculture platforms, but they lack Deere's installed base, data assets, and the Blue River Technology acquisition that powers See & Spray.

Bear Case

The bear case centers on vulnerability to forces Deere cannot control and disruption from directions it may not expect.

Commodity price sensitivity is the most obvious risk. Deere's revenue is ultimately downstream of farm income, which is downstream of commodity prices, which are set by global markets. When corn trades below $4 per bushel, as it has periodically, even the most technology-forward farmer delays equipment purchases. The current downcycle has already demonstrated this: two consecutive years of revenue declines, significant layoffs (over 4,500 jobs cut since 2015), and a salary freeze for FY2026 salaried employees. While Deere manages cycles better than its peers, it cannot eliminate them.

Right-to-repair legislation represents a genuine threat to Deere's technology strategy. If farmers win the legal right to access and modify the software on their equipment, Deere's ability to monetize its software ecosystem could be significantly impaired. The FTC lawsuit, the dozens of state bills, and the federal FARM Act all point toward an environment where Deere may be forced to open its technology platform in ways that erode competitive advantage. The company's initial heavy-handed approach — invoking the DMCA to prevent farmers from repairing their own property — created reputational damage that lingers.

New technology-first entrants are a longer-term concern. Companies approaching agriculture from a software or robotics background — including startups like Monarch Tractor (electric autonomous tractors), Carbon Robotics (laser weeding), and Bear Flag Robotics (acquired by CNH Industrial for $250 million) — are attacking specific niches with purpose-built technology. Potentially even tech giants like Google's parent Alphabet could enter the space, leveraging their AI and data capabilities. If Deere's hardware-centric culture slows its software innovation, these entrants could leapfrog established players. The history of digital disruption is filled with incumbent hardware leaders who were overtaken by software-native competitors — IBM in computing, Nokia in mobile phones, Kodak in imaging. Deere's Blue River Technology acquisition and aggressive autonomous development suggest it is aware of this risk, but cultural transformation at a 188-year-old company is never guaranteed.