Donaldson Company: The 110-Year-Old Filter Empire

How an Unsexy Air Filter Business Built a $3.7 Billion Compounding Machine

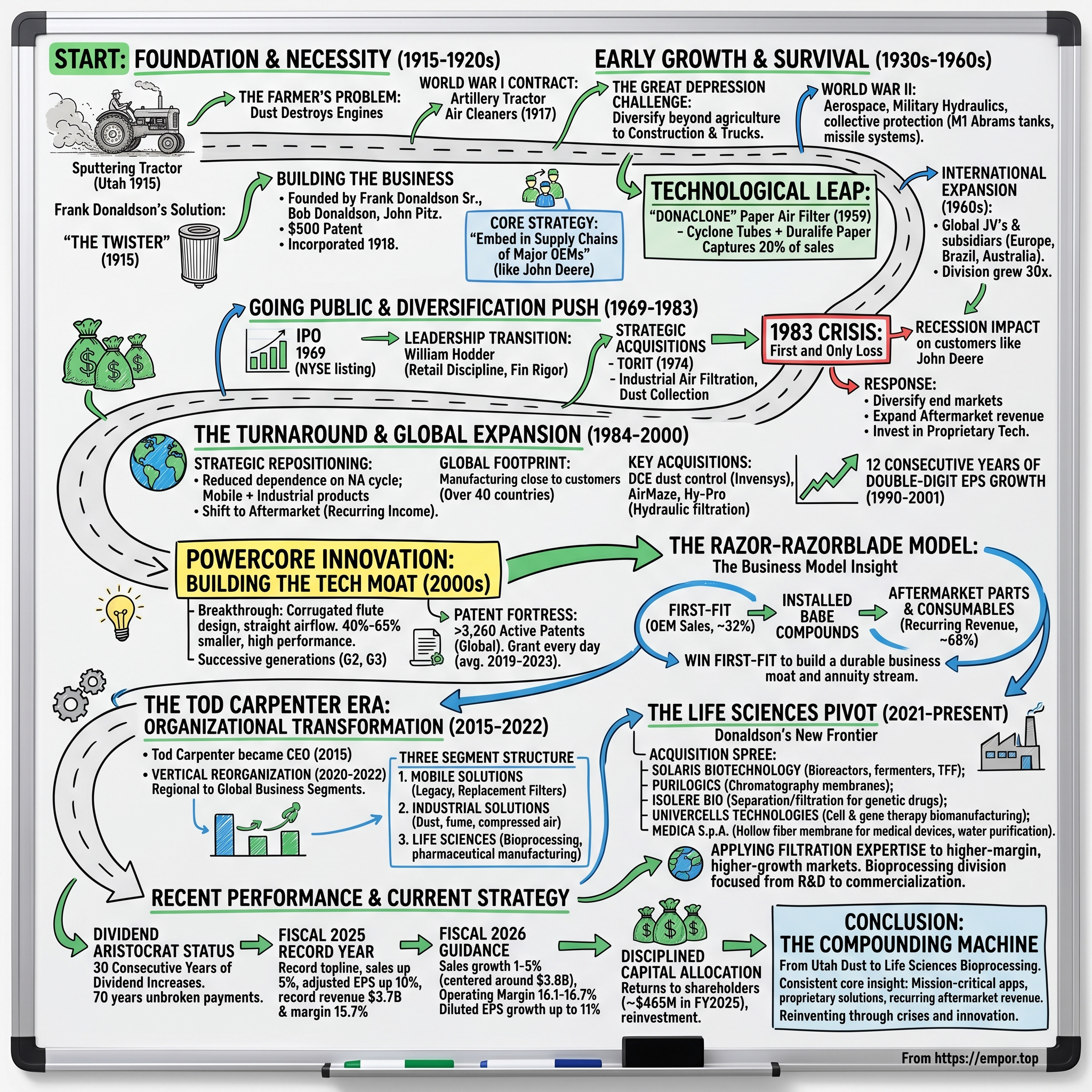

The dusty plains of Utah, circa 1915. A frustrated farmer stands beside his sputtering Bull tractor, watching the young salesman who sold it to him scratch his head. The machine has failed—again—choked by the very earth it was meant to till. Frank Donaldson, the salesman, had already refurbished this tractor once. Within days, it was dead again, suffocated by prairie dust.

What happened next got Donaldson fired—and birthed a $3.7 billion empire.

Taking matters into his own hands, Donaldson improvised a filter from a wire cage, eiderdown cloth, and an eight-foot-long pipe. When the enterprising young salesman proudly told his supervisors of his "modification," he was promptly fired for pointing up Bull's flaws. But Donaldson realized that although he was out of a job, he had something better: an invention that could be sold to tractor companies throughout the farm belt.

Today, Donaldson Company, Inc. (DCI) stands as a global leader in technology-led filtration products and solutions, pioneering advancements since 1915. With fiscal year 2024 sales reaching $3.6 billion and operating income at $544 million, the company represents one of the most remarkable compounding stories in American industrial history.

The thesis is simple but profound: how does a company selling "unsexy" air filters become a multi-generational wealth creator? The answer lies in mission-critical products, proprietary technology, a razor-razorblade business model, and disciplined capital allocation across more than a century of operation.

Donaldson generates a healthy stream of recurring revenue, as aftermarket parts and consumables account for over 60% of sales, which helps mitigate the firm's exposure to cyclical end markets. This isn't a story about explosive growth or revolutionary disruption—it's about building a durable business moat, one filter at a time.

The Origin Story: Born From Dust and Necessity (1915–1920s)

The Farmer's Problem

The mechanization of American agriculture in the early twentieth century created an unexpected victim: the tractor engine itself. As farmers replaced horses with machines, they discovered that the very dust their equipment kicked up was destroying it from within. Engine cylinders scored by abrasive particulates. Pistons worn to uselessness. Costly repairs and constant downtime during critical planting and harvest seasons.

Frank Donaldson was born and raised in southern Minnesota. After earning a degree in engineering from the University of Minnesota in 1912, he went to work as the western U.S. sales representative of Bull Tractor Company in Minneapolis. Donaldson found that one unhappy customer in Utah was having a great deal of difficulty keeping his new Bull tractor running. Donaldson had the dust-choked vehicle completely refurbished, but within a few days it was again out of commission.

This wasn't just one farmer's problem—it was endemic to the entire agricultural equipment industry. Tractors of the era drew unfiltered air directly into their combustion chambers, and in dusty farming conditions, this was effectively a death sentence for the engine.

The Invention That Got Him Fired

With some help from his father, W.H.L. Donaldson, who owned a St. Paul hardware store, and his brother Bob, a sheet-metal fabricator, Frank designed a filter he called the "Twister." The conical device used centrifugal force to spin dirt out of the air before it passed into the engine.

The elegance of the Twister lay in its simplicity—rather than trying to trap particles through dense filter media that would quickly clog, it used physics to separate heavy dust particles from the airstream before they could reach the engine. It was the kind of practical innovation that could only come from someone intimately familiar with real-world operating conditions.

Building the Family Business

Frank Donaldson started the company with $500 and a patent for an air cleaner designed to protect farm tractor engines from dust. The Donaldson Company was founded by Frank Donaldson, Sr., his father, W.H.L. Donaldson, and his brother-in-law, John G. Pitz.

In 1918, the business was incorporated as Donaldson Company, Inc. The timing proved fortuitous: in 1917 the company won a contract to manufacture air cleaners for artillery tractors used in World War I. The military's need for reliable equipment in dusty European battlefields validated Donaldson's invention at scale.

Early Innovation Philosophy

In its first decade, Donaldson Company made two important moves; it acquired the Wilcox-Bennet air filter license and introduced the Simplex, a filter that also prevents engine damage.

Deere & Company was the company's most important client during the first couple decades. This relationship with what would become one of America's largest agricultural equipment manufacturers established a template that Donaldson would follow for a century: embed yourself in the supply chains of major OEMs, prove your value through superior performance, and build switching costs through reliability.

By 1929, Donaldson was selling 200,000 units per year. What had started as one man's improvised solution to one farmer's problem had become an essential component of American agricultural infrastructure.

For investors, the lesson is clear: mission-critical products in growing markets create durable franchises. Frank Donaldson didn't invent the tractor—he invented the component that made tractors economically viable in dusty conditions. That strategic positioning, occupying the intersection of necessity and expertise, would define the company's approach for generations.

Early Growth & Survival: Navigating Depressions and Wars (1930s–1960s)

The Depression Challenge

The early 1930s brought additional prosperity when William Lowther joined the company and designed the NS Filter, a tractor performance enhancing filter invented by Frank Donaldson. The 1930's were a transitional period, beginning with tough economic conditions in the United States which caused business from farmers to fall and subsequently forcing the company to contract in size.

The Great Depression posed an existential threat to Donaldson. The company's customer base—farmers and farm equipment manufacturers—was devastated by falling commodity prices and the Dust Bowl. Yet the Donaldsons recognized that economic downturns also presented opportunities: Sales to Caterpillar, John Deere, Cummins Engine, and many other manufacturers of heavy vehicles boosted sales to $465,000 and profits to $88,000 by 1935.

The company's survival strategy centered on diversifying beyond pure agricultural applications. Construction equipment, trucks, and industrial machinery all faced similar dust ingestion problems, and Donaldson methodically expanded into these adjacent markets.

The War Years and Diversification

World War II provided opportunities for the company to expand into aerospace and military hydraulic equipment and device filters.

The military connection proved transformative. Defense applications demanded higher performance standards than commercial equipment, and meeting these requirements pushed Donaldson's engineering capabilities forward. The company's research division focused on advanced development of modularized, collective protection for military vehicles, air filtration systems for missile systems and space vehicles, M1 Abrams main battle tank turbine engines, and complex military equipment such as the AN/TPQ-36 and AN/TPQ-37 Firefinder radars.

The Donaclone Era

The 1950s brought both opportunity and turbulence. In 1942, Frank Donaldson Sr. died, leaving his 22-year-old son Frank Jr. to eventually take the reins. Under the leadership of Frank Donaldson Jr., who assumed the presidency in 1951 at age 31, the company introduced innovations like the Donaclone heavy-duty paper air filter in 1959, which captured 20% of sales in its debut year by offering improved efficiency over earlier oil-bath designs.

The Donaclone represented a technological leap. Seven years of research and testing resulted in the 1959 launch of the "Donaclone," the first heavy-duty air cleaner to use a paper filter. The brand name combined Donaldson and cyclone, and the device harked back to the company's original Twister brand filter. It used a series of "cyclone tubes" to spin dirt out of the air. The Duralife paper filter served as a final dirt trap.

Frank, Jr.'s first decade in office was incredibly successful. Sales nearly doubled, from $5.5 million in 1950 to a record $10.1 million in 1959, and profits more than doubled, from $315,000 to $669,000 during the same period.

International Expansion Takes Root

Sales tripled over the course of the 1960s, to $35.9 million in 1969, as clients ranging from Caterpillar to the U.S. Army adopted the new filter for their heavy-duty machinery. Geographic expansion also contributed to this growth, as Donaldson established joint ventures and licensing agreements with businesses in Britain, France, Germany, Brazil, and Australia. By the end of the decade, it had wholly owned subsidiaries in Germany, Belgium, and South Africa as well. Formalized in 1963, the International Division grew 30-fold from 1963 to 1970.

This international expansion established a pattern that would serve Donaldson well: manufacturing close to customers to serve local needs while leveraging centralized R&D to maintain technological leadership. Today, the company operates in over 40 countries, but the strategic architecture was established in the 1960s.

Going Public & The Diversification Push (1969–1983)

IPO and New Capital

The company went public in 1969, listing on the New York Stock Exchange. The IPO came at the peak of the Donaclone era's success, with the company riding nearly a decade of triple-digit sales growth. Public market access provided capital for the aggressive acquisition strategy that would follow.

Leadership Transition

Frank Donaldson, Jr., advanced to chairman and CEO in 1973. In a departure from the traditional promotion from within, Donaldson hired William Hodder, formerly president of Target Stores and a director of Donaldson for just four years, to succeed the founder's son.

The decision to bring in outside leadership was bold—and controversial. The Donaldson family had built the company through engineering excellence and deep customer relationships. Hodder brought a different perspective: retail operations discipline, financial rigor, and diversification strategy. Whether this was the right approach would be tested severely in the years ahead.

Strategic Acquisitions: Building the Industrial Platform

A pivotal early acquisition was Torit in 1974, which expanded Donaldson's capabilities in industrial air filtration and dust collection systems, aligning with growing demand for workplace safety.

Company diversified through the acquisitions of Torit Corp., Majac, Inc., and Kittell Muffler and Engineering. These acquisitions moved Donaldson beyond mobile equipment into industrial air quality—a market that would prove less cyclical than the company's core agricultural and construction equipment exposure.

The Torit acquisition deserves particular attention because it established Donaldson's presence in dust collection, a market segment that remains central to the company's Industrial Solutions business today. Torit technology would later be combined with Donaldson's PowerCore innovation to create industry-leading dust collection systems.

The 1983 Crisis: First and Only Loss

After suffering its first and only net loss in 1983, the company that Money magazine once characterized as a "baby blue chip" made a long, difficult comeback. Having accomplished the shift from its mature, cyclical core business, Donaldson chalked up 12 consecutive years of double-digit increases in earnings per share from 1990 to 2001.

1984 - Forced to enter new markets (through acquisitions) and restructure due to recessionary effects on major customers like John Deere Tractor Company.

The 1983 crisis revealed the strategic vulnerability of Donaldson's concentration in cyclical heavy equipment markets. The early 1980s recession devastated agricultural equipment demand, and Donaldson's dependence on customers like John Deere—itself suffering through one of the most difficult periods in its history—cascaded through to Donaldson's bottom line.

The company's response to this crisis would define its strategic direction for the next four decades: diversify across end markets, expand the recurring aftermarket revenue base, and invest in proprietary technology that creates switching costs.

The Turnaround & Global Expansion (1984–2000)

Strategic Repositioning

The 1983 loss served as a crucible, forcing Donaldson to fundamentally rethink its business model. During the 1970s and 1980s, Donaldson accelerated its global footprint by establishing manufacturing facilities across Europe, Asia, and Latin America. The company's growth strategy combined organic expansion with strategic acquisitions that broadened its technological capabilities and market access.

The strategic shift had three pillars. First, geographic diversification to reduce dependence on the North American economic cycle. Second, product diversification to serve industrial markets alongside mobile equipment. Third, and most importantly, a deliberate shift toward aftermarket revenue that would generate recurring income regardless of new equipment sales.

Building Global Manufacturing Footprint

As a multinational company it operates in Belgium, Mexico, China, UK, Czech Republic, Malaysia, Thailand, USA, South Africa, Russia, Japan, Italy, Germany and France. In fiscal year 2016 20.3% of sales came from business in the Asia-Pacific region, 28.5% from Europe and 42.2% from the US.

The geographic distribution of manufacturing proved prescient. By producing close to customers, Donaldson reduced shipping costs, improved responsiveness, and—crucially—insulated itself from trade disruptions and tariff regimes that would become increasingly important in later decades.

Key Acquisitions: Cementing Market Position

In November 1999 the company acquired AirMaze Corporation for $31.9 million. Donaldson acquires the DCE dust control business of Invensys plc; revenues surpass the $1 billion mark for the first time during the year ending in July.

In the early 2000s, Donaldson Company expanded its industrial filtration capabilities through targeted acquisitions, including the purchase of the DCE dust control business from Invensys plc in February 2000 for $56.4 million, which bolstered its position in dust collection systems. Subsequent deals focused on complementary technologies, such as the 2017 acquisition of Hy-Pro Filtration Corporation on May 1, which specialized in hydraulic and lubrication fluid filtration systems, enabling Donaldson to integrate advanced contaminant removal solutions without shifting from its core air and liquid filtration expertise.

The DCE acquisition was particularly significant, giving Donaldson a major presence in industrial dust collection outside North America and complementing the Torit business acquired in the 1970s.

Twelve Consecutive Years of Double-Digit EPS Growth

The transformation from the 1983 crisis to sustained profitability was remarkable. After suffering its first and only net loss in 1983, the company that Money magazine once characterized as a "baby blue chip" made a long, difficult comeback. Having accomplished the shift from its mature, cyclical core business, Donaldson chalked up 12 consecutive years of double-digit increases in earnings per share from 1990 to 2001.

This wasn't just recovery—it was transformation. The company that entered 1983 overly dependent on cyclical OEM equipment sales emerged as a diversified industrial filtration leader with a growing aftermarket business. The lesson: crisis creates opportunity for companies willing to make fundamental strategic changes.

PowerCore Innovation: Building the Technology Moat (2000s)

The PowerCore Breakthrough

In the late 1990s, Donaldson's engineers confronted a fundamental challenge: as emissions regulations tightened (EPA standards in the United States, Euro standards in Europe), equipment manufacturers needed to fit more emissions control equipment into the same space. Something had to give—and that something was often the air filtration system.

Donaldson PowerCore was the first air filter configuration to utilize a corrugated flute design with a straight-through airflow path to trap dust in flutes on the "dirty side" of the air cleaner. This innovative design pushes air through to adjacent flutes on the clean side, allowing flexibility to modify the shape of the air filter, fitting the air cleaner itself into less space. A smaller air-cleaner footprint was a need when we created PowerCore 25 years ago, and it's a need still.

PowerCore wasn't just an incremental improvement—it was a platform technology that would generate successive generations of innovation and, critically, proprietary aftermarket revenue.

Successive Generations: Smaller, Better, Faster

Original PowerCore was 40% smaller than standard pleated filters. PowerCore G2 was 60% smaller. PowerCore G3 is 65% smaller. And every generation maintains or increases performance.

Each generation represented years of engineering investment and created new intellectual property protection. This pattern—iterative improvement on a proprietary platform—is the hallmark of sustainable competitive advantage in industrial technology.

Why PowerCore Matters Strategically

Donaldson's breakthrough PowerCore® air filters have been delivering superior performance and meeting original equipment manufacturer (OEM) specifications for more than 20 years. In that time, PowerCore air filters have logged billions of on-road miles and off-road hours, protecting engines, reducing downtime and saving money for fleet operators. Donaldson PowerCore air filters continue to set new standards in filtration quality, coverage and performance, with smaller and lighter air cleaners driven by increasingly more stringent emissions regulations, and airflow designs that deliver superior efficiency and dust-holding capacity.

The industrial dust collection application proved equally important. Innovative PowerCore filtration technology means reduced freight and installation costs, fewer filter changeouts, lower maintenance costs, and no entry requirements for filter changes. Donaldson Torit® PowerCore® CP Series cartridge dust collectors use smaller, more efficient filters compared to baghouse models with a footprint up to 50% smaller.

Building a Patent Fortress

What that really means is between Investors' Day of April 2019 and Investor Day of April 2023, on average, somewhere in the world, Donaldson Company was granted a patent every day. We really look to be differentiated through technology.

In 2024, Donaldson registered 392 new patents and currently has a total of 3,260 active U.S. and international patents.

This patent estate serves multiple strategic purposes. It protects Donaldson's innovations from direct copying. It creates barriers to entry for potential competitors. And it generates licensing opportunities where appropriate. But most importantly, it locks customers into Donaldson replacement parts—the foundation of the company's recurring revenue model.

The Razor-Razorblade Model: The Business Model Insight

The Fundamental Transformation

Our model is proprietary filtration to sell razor blades. Razors to sell razor blades. You see that in the lower left, where 68% of our products are replacement parts. 32% are that first fit or CapEx-based parts.

This ratio—roughly one-third first-fit equipment, two-thirds replacement parts and consumables—represents one of the most important business model insights in industrial manufacturing. First-fit sales (selling to OEMs for installation in new equipment) are inherently cyclical, subject to the vagaries of equipment replacement cycles, economic conditions, and customer capital budgets. Aftermarket replacement parts, by contrast, generate recurring revenue as long as the equipment remains in service.

Consider the mathematics: a truck engine might need air filter replacement every 15,000 to 30,000 miles, depending on operating conditions. A piece of mining equipment might consume dozens of filters per year. A factory dust collection system requires filter replacement on a regular maintenance schedule. Each piece of Donaldson-equipped machinery becomes an annuity stream of replacement revenue.

Building the Installed Base

The strategic logic is straightforward: win the first-fit sale by helping OEMs meet their packaging, performance, and cost targets. Once Donaldson filtration is specified in the original equipment design, switching costs are high—alternative filters may not fit, may not perform to specification, or may void equipment warranties. The installed base compounds over time, creating ever-larger streams of aftermarket revenue.

The shift to aftermarket and connected models creates recurring revenue and profit streams, positioning the company for superior resilience and margin expansion through industry cycles, regardless of near-term first-fit equipment volatility.

Supporting OEM Partners

CEO Tod Carpenter's articulation of the strategy emphasizes the partnership dimension: the company works to help OEMs retain their own aftermarket business where possible, using Donaldson as a technical partner rather than a competitor for the replacement parts stream. This collaborative approach builds long-term relationships even when the OEM wants to brand the filters under their own name.

The Downflo Evolution dust collector exemplifies this approach in industrial applications. By designing proprietary filter packs that can only be sourced from Donaldson, the company creates a captive aftermarket while delivering genuinely superior performance to end users.

For investors, the razor-razorblade model explains Donaldson's resilience through economic cycles. When equipment sales decline in recessions, the existing installed base continues generating aftermarket revenue. The company's exposure to cyclical OEM purchasing is real but manageable, and the recurring revenue base provides ballast.

The Tod Carpenter Era: Organizational Transformation (2015–2022)

Leadership Change

Donaldson Co. Inc. announced that Tod Carpenter, 55, currently the company's chief operating officer (COO), has been named president and chief executive officer (CEO), effective April 1, 2015.

Tod Carpenter is the Chairman, President and Chief Executive Officer of Donaldson Company, Inc. He has been chairman since 2017 and President and Chief Executive Officer since 2015. Previously, he served as Chief Operating Officer from 2014 to 2015; Senior Vice President, Engine Products from 2011 to 2014; Vice President, Europe and Middle East from 2008 to 2011.

Carpenter represented a new generation of Donaldson leadership—an insider who had risen through operating roles across multiple geographies and business segments. His deep operational experience positioned him to lead the organizational transformation that would follow.

Prior to joining Donaldson, he worked at York & Associates and the Hughes Aircraft Company. Carpenter holds a Bachelor's Degree in Manufacturing Technology from Indiana State University, an MBA from Long Beach State University, and completed the Minnesota Executive Program at the University of Minnesota's Carlson School of Management.

The Vertical Reorganization (2020–2022)

Under Carpenter's leadership, Donaldson undertook a fundamental organizational redesign. The company shifted from a regional structure—where business units were organized by geography—to a vertical structure organized around business segments with global accountability.

In 2022, Donaldson added Solaris Biotechnology and Purilogics through acquisition and in November announced an organization redesign making Life Sciences a new reporting segment and adjusting its two main segments Mobile Solutions and Industrial Solutions.

Three Segment Structure

The company maintains a presence in over 140 locations across six continents, serving diverse industries and advanced markets.

The reorganized structure comprises three segments:

Mobile Solutions: The company's legacy business, providing replacement filters for air and liquid filtration in construction, mining, agriculture, and transportation markets. This segment serves both OEMs installing Donaldson filters in new equipment and the aftermarket channels serving existing equipment owners.

Industrial Solutions: Dust, fume, and mist collectors; compressed air and industrial gas purification; and hydraulic and lubricated rotating equipment applications. This segment addresses the factory floor, serving manufacturing facilities across diverse industries.

Life Sciences: The newest segment, encompassing micro-environment gas and liquid filtration for food, beverage, and industrial processes; bioprocessing equipment including bioreactors and fermenters; and bioprocessing consumables for pharmaceutical manufacturing.

The reorganization enabled faster decision-making by putting segment leaders in charge of global operations rather than having regional executives negotiate across organizational boundaries. It also clarified accountability for financial performance and strategic investment.

The Life Sciences Pivot (2021–Present): Donaldson's New Frontier

Strategic Rationale

The Life Sciences expansion represents Donaldson's most significant strategic bet since the post-1983 transformation. The logic is compelling: apply the company's century of filtration expertise to higher-margin, higher-growth markets where the technical challenges are severe and the consequences of failure are significant.

"With the integral addition of Isolere to our Life Sciences portfolio, Donaldson is positioned to create premier separation and filtration solutions for emerging genetic-based drugs," said Tod Carpenter, chairman, president and chief executive of Donaldson.

The Acquisition Spree

Between 2021 and 2024, Donaldson assembled a Life Sciences platform through a series of targeted acquisitions:

Solaris Biotechnology (November 2021): Donaldson Company, Inc. acquired Solaris Biotechnology Srl. Solaris designs and manufactures bioprocessing equipment, including bioreactors, fermenters and tangential flow filtration systems for use in food and beverage, biotechnology and other life sciences markets. Solaris' product portfolio ranges from benchtop systems for research and development to pilot and commercial-scale manufacturing systems. Donaldson acquired Solaris for approximately €41 million.

Purilogics (2022): Another cool thing we're working on is chromatography with Purilogics, a recent acquisition. We're filter geeks and we work on media-based solutions. Our goal is to either filter out or retain something for separation purposes. Purilogics was ahead of Donaldson in media-based chromatography, so we joined forces.

Isolere Bio (February 2023): "With the integral addition of Isolere to our Life Sciences portfolio, Donaldson is positioned to create premier separation and filtration solutions for emerging genetic-based drugs," said Tod Carpenter. "We look forward to accelerating Isolere's growth trajectory through sales synergies from our recent acquisitions of Solaris Biotechnology and Purilogics and through the strength of our balance sheet." Founded in 2017 by Kelli Luginbuhl, Ph.D, Professor Ashutosh Chilkoti, and Joe McMahon, Isolere is headquartered in Durham, North Carolina.

Univercells Technologies (June 2023): Donaldson announced the acquisition of Univercells Technologies, a global producer of innovative biomanufacturing solutions for cell and gene therapy research, development and commercial manufacturing. Univercells Technologies' product offering includes the unique scale-X™ single-use structured fixed-bed bioreactor for the intensified production of viruses used in cell and gene therapy, viral vaccines and other therapeutics. In addition, the Company's automated NevoLine™ Upstream platform incorporates industry-standard filtration to provide integrated up- and mid-stream processing capabilities in a single unit driving productivity improvements, reduced operational footprints and greater consistency of results.

According to the terms of the transaction, Donaldson acquired all outstanding shares of the business from Gamma and its fellow shareholder, Univercells SA, for approximately €136M in cash net of debt.

Medica S.p.A. (2024): Donaldson announced it has entered into a definitive agreement allowing the Company to purchase a 49% stake in Medica S.p.A. (Medica). Medica is a leader in hollow fiber membrane filtration technology for medical device applications and water purification. Headquartered in Medolla, Italy, the Company has over 700 employees globally and generated €80 million of revenue in calendar 2023. Founded in 1985, Medica's innovative hollow fiber membrane filtration products are used for blood purification in numerous applications including dialysis, continuous renal replacement therapies (CRRT), and therapeutic apheresis. The Company's products and technologies are also used in the microbiological purification of water, as well as automation solutions for disposable medical device manufacturing.

Donaldson has recently completed the acquisition of a 49% minority stake in Medica S.p.A. for €62 million ($67.73 million) which excludes transaction-related fees and expenses. This deal was announced in April 2024.

The Technology Connection

The division was built via acquisitions of Isolere Bio for multi-modality reagents; Purilogics for bioprocessing membranes; and Solaris Biotech and Univercells Technologies for innovative production technologies. Long a pioneer in filtration solutions, Donaldson Company continues to expand into the Life Sciences sector. The Bioprocessing division is concentrated on developing solutions from R&D to commercialization for multi-modality drug manufacturers.

The Life Sciences strategy represents Donaldson's attempt to apply its core competency—solving difficult filtration challenges through proprietary technology—to markets with higher growth rates and margin potential. Bioprocessing for pharmaceuticals, cell and gene therapy manufacturing, and food and beverage processing all require precision filtration, and all are growing faster than traditional heavy equipment markets.

Managing Expectations

Bioprocessing remains muted due to industry project delays; new downstream Purexa products have launched, but meaningful revenue ramp is expected in fiscal 2027.

The Life Sciences segment has not yet achieved profitability, and bioprocessing market conditions have been challenging. This represents the primary execution risk in Donaldson's current strategy—if the Life Sciences investments fail to generate adequate returns, the company will have diverted significant capital and management attention from its profitable core businesses.

Recent Performance & Current Strategy

Fiscal 2025 Results: Another Record Year

Donaldson reported fourth-quarter fiscal 2025 earnings on August 27, 2025, posting record topline performance, with sales up 5% year over year to $981 million and adjusted EPS up 10% year over year to $1.03. Full-year results for the fiscal year ended July 31, 2025, included all-time highs in both revenue ($3.7 billion) and operating margin (15.7%), with $465 million returned to shareholders.

For the full fiscal year 2025, Donaldson reported sales of $3.69 billion, representing a 3% increase on a constant currency basis compared to fiscal 2024. Adjusted operating margin improved by 30 basis points to 15.7%, while adjusted diluted EPS grew 8% to $3.68.

Fiscal 2026 Guidance: Continued Expansion

Looking ahead to fiscal 2026, Donaldson provided a positive outlook, projecting sales growth of 1% to 5%, centered around $3.8 billion. The company expects operating margin to range between 16.1% and 16.7%, driven by gross margin expansion and leverage on higher sales. Donaldson forecasts diluted EPS of $3.92 to $4.08 for fiscal 2026, representing potential growth of up to 11% compared to fiscal 2025.

We will be $3.8 billion. We will also put up record operating margin at 16.4% at midpoint, or expanding roughly 180 basis points of operating margin over a three-year period. Our EPS will also be a record at $4.

Dividend Aristocrat Status

The filtration products manufacturer is a member of the S&P High-Yield Dividend Aristocrats Index, and 2025 will mark the company's 30th consecutive year of annual dividend increases. Donaldson has maintained an unbroken record of quarterly cash dividend payments spanning 70 years.

Donaldson Company, Inc. (DCI) has increased its dividends for 30 consecutive years. This is a positive sign of the company's financial stability and its ability to pay consistent dividends in the future. Donaldson Company, Inc.'s payout ratio is 35.94% which means that 35.94% of the company's earnings are paid out as dividends.

The combination of dividend growth, share repurchases, and retained earnings for investment reflects disciplined capital allocation that has created value for long-term shareholders.

Competitive Landscape & Strategic Positioning

Market Position

Major players in the bulk filtration market include PARKER HANNIFIN CORP (US), Donaldson Company, Inc. (US), Filtration Group (US), MANN+HUMMEL (US), and Eaton (Ireland). These global firms employ growth strategies, such as product launches, collaborations, and enhancing the capabilities of bulk filtration systems, to improve their market position.

The bulk filtration market is highly competitive, with a limited number of major engineering, procurement, and construction (EPC) players performing the majority of the projects in the market. The collective market share of Parker Hannifin Corp., Donaldson Company, Inc., Filtration Group, MANN+HUMMEL, and Eaton together accounts for approximately 40–45% of the total bulk filtration market.

Porter's Five Forces Analysis

Supplier Power (Low to Moderate): Donaldson sources filter media, metals, and specialty components from multiple suppliers. While some specialty materials may have limited sources, the company's scale provides purchasing leverage.

Buyer Power (Moderate): Large OEM customers like Caterpillar and John Deere have significant negotiating power for first-fit business. However, aftermarket buyers are fragmented—individual equipment operators and local distributors—with limited leverage.

Threat of New Entrants (Low): Entering the filtration business at scale requires substantial capital investment, engineering expertise, and established customer relationships. Donaldson's 3,000+ patent portfolio creates additional barriers. New entrants might successfully target niche segments but would struggle to compete across Donaldson's breadth.

Threat of Substitutes (Low): Filtration is physics—there's no way to avoid the need to separate particulates from air or liquids in equipment and industrial processes. Alternative technologies (electrostatic precipitation, centrifugal separation) serve specific applications but cannot replace filtration broadly.

Competitive Rivalry (Moderate to High): Competition among established players is intense in some segments, particularly price-sensitive commodity filters. Donaldson differentiates through technology (PowerCore), service, and aftermarket network coverage.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Donaldson's manufacturing scale provides cost advantages in filter media production and distribution network efficiency. With more than 140 manufacturing and bulk filtration centers, Donaldson serves customers in over 40 countries worldwide.

Network Effects: Limited direct network effects, but Donaldson's global distribution network creates value for OEM partners who want worldwide aftermarket support for their equipment.

Counter-Positioning: The Life Sciences expansion represents counter-positioning—Donaldson is betting that its filtration expertise can succeed in bioprocessing, where incumbents may not have the same technology DNA.

Switching Costs: The razor-razorblade model creates substantial switching costs. OEMs that design Donaldson filters into their equipment face re-engineering costs to switch suppliers. End users face performance and warranty risks from using non-OEM replacement parts.

Branding: Donaldson has strong brand recognition among equipment operators and maintenance professionals. The company's 110-year history and reliability reputation create trust that supports premium pricing.

Cornered Resource: Donaldson's patent portfolio (3,260 active patents) represents a cornered resource in proprietary filtration technology. PowerCore and other platform technologies cannot be legally replicated.

Process Power: A century of manufacturing optimization has created process advantages in filter production efficiency, quality control, and supply chain management.

Bull Case & Bear Case

The Bull Case

Mission-Critical Products in Growing Markets: Filtration is essential infrastructure for modern equipment and manufacturing. Whether in heavy machinery, trucks, factories, or cleanrooms, equipment cannot operate without proper filtration. This creates durable demand regardless of economic conditions.

Recurring Revenue Model: With 68% of revenue from aftermarket replacement parts, Donaldson has significant visibility into future revenue. The installed base of Donaldson-equipped machinery continues generating replacement demand for years after the original equipment sale.

Technology Leadership: The company's 3,260 patents and ongoing R&D investment create barriers to competition. PowerCore technology and successive innovations maintain performance differentiation.

Capital Allocation Discipline: Thirty consecutive years of dividend increases, consistent share repurchases, and disciplined M&A demonstrate management's commitment to shareholder returns.

Life Sciences Optionality: The investments in bioprocessing, cell and gene therapy manufacturing, and medical devices provide exposure to higher-growth markets. If these investments succeed, they could meaningfully accelerate Donaldson's growth rate.

Global Manufacturing Footprint: On $3.7 billion worth of revenue last year, tariff exposure was $35 million. The strategy of being where the customer wants us to be and manufacturing within region has really served Donaldson Company well, allows us to be agile and flexible for the customers in this time of uncertainty.

The Bear Case

Cyclical Exposure: Despite diversification, Donaldson remains exposed to cyclical industries—construction, mining, agriculture, and transportation. Extended downturns in these sectors would pressure first-fit sales and potentially aftermarket as equipment utilization declines.

Life Sciences Execution Risk: In fiscal 2025 and 2026, Mobile and Industrial operating margin strength is forecast to more than offset weaker-than-expected Life Sciences performance. The elongated ramp up in Life Sciences profitability is driven by challenging market conditions and constrained customer capital spending. The Life Sciences segment remains unprofitable, and meaningful revenue contribution is not expected until fiscal 2027 or later. If these investments fail to generate adequate returns, significant capital will have been misallocated.

Technology Disruption: Electric vehicles and alternatively-fueled equipment may reduce demand for traditional engine air filtration. While EVs still require cabin air filtration and thermal management, the transition could disrupt Donaldson's mobile equipment business.

Competition from Low-Cost Producers: In commodity filter segments, low-cost competitors—particularly from Asia—can undercut Donaldson pricing. Maintaining differentiation requires ongoing R&D investment and marketing spend.

Tariff and Trade Policy Uncertainty: While Donaldson's localized manufacturing reduces tariff exposure, trade policy changes could still impact cost structures and competitive dynamics.

Myth vs. Reality

Myth: "Filtration is a boring, no-growth business." Reality: The global industrial filtration market is projected to grow at 4-5% annually, driven by tightening environmental regulations, increasing equipment sophistication, and expansion in emerging markets. Donaldson's proprietary technology focus positions it to grow faster than the market through share gains.

Myth: "Electric vehicles will destroy Donaldson's business." Reality: While EVs eliminate traditional engine air filtration, they create new opportunities in battery thermal management, cabin air quality, and manufacturing filtration. Donaldson's off-road and industrial businesses are less exposed to passenger vehicle electrification.

Myth: "Life Sciences is a distraction from the core business." Reality: Life Sciences represents deliberate portfolio rebalancing toward higher-growth, higher-margin markets that leverage Donaldson's filtration expertise. The strategy is ambitious but logical—diversification beyond cyclical heavy equipment into defensive healthcare-related end markets.

Key Performance Indicators to Track

For fundamental investors evaluating Donaldson Company, three metrics merit close monitoring:

1. Aftermarket Revenue as Percentage of Total Revenue

This ratio measures the health of Donaldson's recurring revenue model. Currently at approximately 68% of total revenue, this percentage reflects the cumulative installed base of Donaldson-equipped machinery and the company's success in capturing replacement parts business. An increasing percentage indicates growing recurring revenue ballast; a declining percentage suggests either first-fit share gains (potentially positive) or aftermarket share losses (concerning).

2. Adjusted Operating Margin

Operating margin measures Donaldson's ability to convert revenue into profit after operating expenses. The company targets 16.4% adjusted operating margin for fiscal 2026, up from 15.7% in fiscal 2025. Margin expansion reflects pricing power, cost discipline, and mix shift toward higher-margin products. Watch for margin pressure from input cost inflation, competitive pricing dynamics, or dilution from unprofitable Life Sciences investments.

3. Life Sciences Segment Revenue Growth and Path to Profitability

The Life Sciences segment represents Donaldson's strategic growth bet. Track quarterly revenue growth rates against management guidance and monitor commentary on the timeline to segment profitability. Bioprocessing remains muted due to industry project delays; new downstream Purexa products have launched, but meaningful revenue ramp is expected in fiscal 2027. Delays or downward revisions to Life Sciences expectations would raise questions about the acquisition strategy.

Regulatory and Accounting Considerations

Key Regulatory Exposures

Donaldson's business benefits from environmental regulations that require improved air quality in workplaces and reduced emissions from equipment. Changes to EPA regulations, OSHA workplace safety standards, or equivalent international requirements could impact demand for filtration products—positively if regulations tighten, negatively if regulations are relaxed.

The Life Sciences business faces regulatory oversight from the FDA and international equivalents for pharmaceutical manufacturing equipment. Medical device applications (through the Medica investment) are subject to FDA 510(k) clearance requirements and ongoing quality system regulations.

Accounting Judgments

Goodwill and Intangible Assets: The acquisition-driven Life Sciences strategy has created significant goodwill and intangible assets on Donaldson's balance sheet. These assets are subject to annual impairment testing. If Life Sciences investments fail to achieve expected returns, impairment charges could reduce reported earnings.

Revenue Recognition: The company's mix of equipment sales (recognized at delivery) and service revenue (recognized over time) creates complexity in revenue recognition. Changes in sales mix could impact revenue timing.

Restructuring Charges: Donaldson has undertaken footprint optimization and cost restructuring programs. Non-GAAP adjusted earnings exclude restructuring charges, so investors should review both GAAP and adjusted metrics to understand underlying profitability trends.

Conclusion: The Compounding Machine

Frank Donaldson's improvised filter of wire cage, eiderdown cloth, and pipe has evolved into a $3.7 billion global enterprise. The journey from Utah dust to Life Sciences bioprocessing spans 110 years, two world wars, numerous recessions, and countless technological transitions.

Yet the core insight remains remarkably consistent: find mission-critical applications where superior filtration technology creates value, build proprietary solutions that customers cannot easily replace, and capture recurring aftermarket revenue from the installed base.

You look at our revenue, we have been putting up record after record after record after record. Four years in a row and running, both in EPS as well as revenue.

Donaldson's story offers lessons for investors beyond the filtration industry. Sustainable competitive advantage often comes not from revolutionary innovation but from cumulative improvement in solving unglamorous but essential problems. The razor-razorblade business model—common in consumer products—works even better in industrial applications where switching costs are higher and price sensitivity is lower.

The company's willingness to transform after the 1983 crisis demonstrates that even mature industrial businesses can reinvent themselves when leadership recognizes the need for change. The current Life Sciences expansion represents another such transformation attempt—whether it succeeds will determine Donaldson's trajectory for the next generation.

For the long-term investor, Donaldson offers a rare combination: a proven business model with strong recurring revenue, disciplined capital allocation evidenced by 30 consecutive years of dividend increases, and optionality on higher-growth markets through the Life Sciences expansion. The unsexy air filter business may not generate headlines, but for 110 years, it has generated value for shareholders patient enough to understand its durable competitive advantages.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube