Dana Incorporated: From U-Joints to e-Propulsion

The Story of America's 120-Year-Old Mobility Survivor

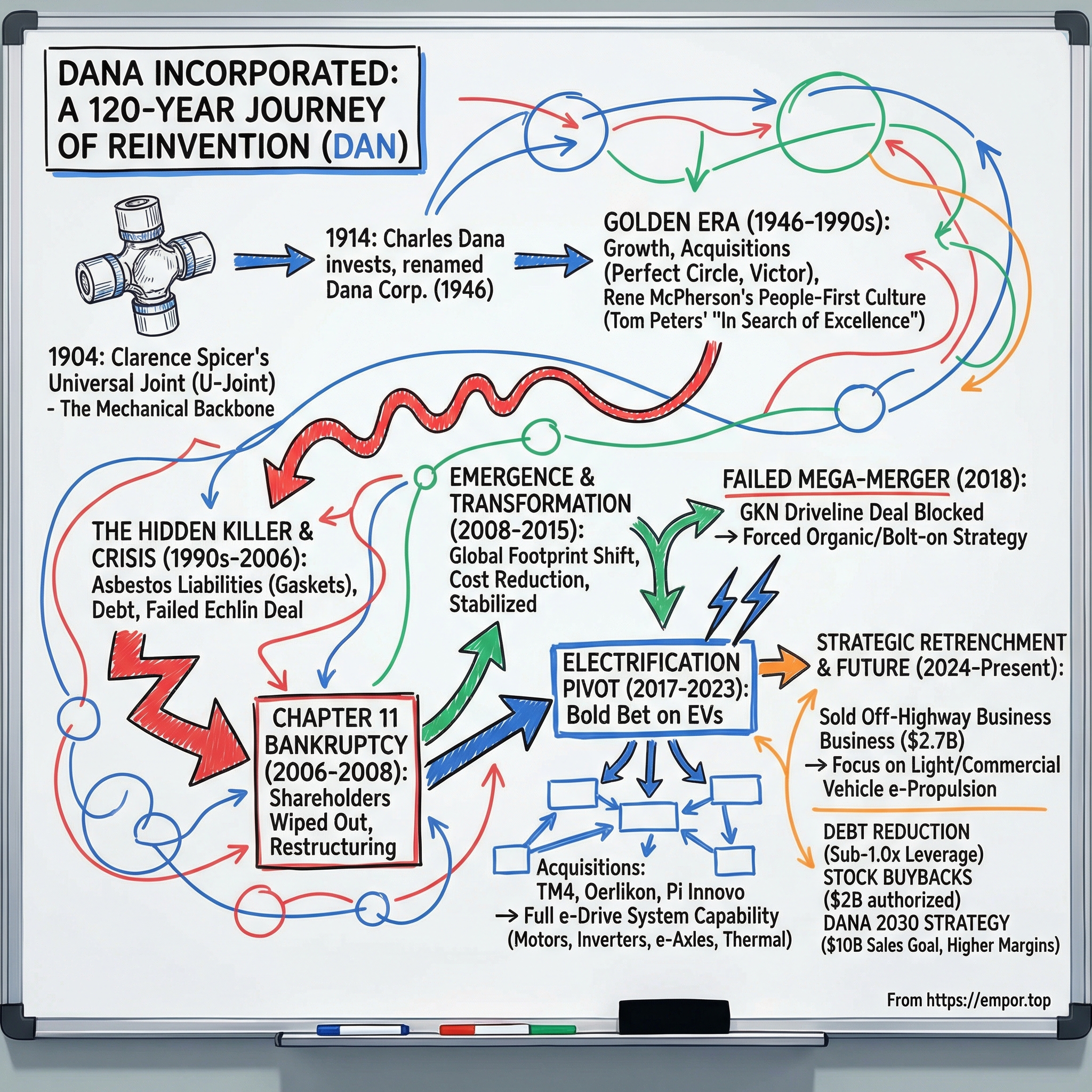

I. Introduction & Episode Roadmap

Picture a farm boy from Illinois, hunched over a drafting table in an engineering lab at Cornell University in 1902, sketching a solution to one of the automobile industry's most vexing problems. That farm boy was Clarence Winfred Spicer, and the device he designed — a simple, enclosed universal joint — would become the mechanical backbone of every car, truck, and military vehicle built in America for the next century. His little company, founded in a New Jersey machine shop in 1904, would eventually carry the name of a New York City lawyer who bankrolled it, survive two world wars, near-annihilation by asbestos litigation, a bruising Chapter 11 bankruptcy, and emerge in the twenty-first century as a leading supplier of electric powertrains for the vehicles of tomorrow.

Today, Dana Incorporated trades on the New York Stock Exchange under the ticker DAN. Based in Maumee, Ohio, just outside Toledo, Dana is a Fortune 500 fixture that has appeared on the list every single year since it was first published in 1955 — one of only about fifty-two companies in the world that can claim that distinction. At its peak, the company employed more than 36,000 people across 33 countries and generated over ten billion dollars in annual sales. Following its recent divestiture of the Off-Highway business, it now operates as a leaner, more focused enterprise with roughly $7.5 billion in revenue, organized into two segments: Light Vehicle Systems and Commercial Vehicle Systems.

The question that drives this episode is deceptively simple: How does a company that made parts for the Ford Model T survive to become a global leader in electric powertrains? The answer involves a chain of reinventions — some brilliantly executed, others forced by crisis — that together form one of the most compelling survival stories in American industrial history. Along the way, there are management revolutions that Tom Peters would canonize in his bestseller, asbestos claims that numbered in the tens of thousands, a bankruptcy that wiped out shareholders, a failed mega-merger that would have reshaped the global driveline industry, and a bold bet on electrification whose outcome remains very much in the balance.

The themes running through Dana's story are universal ones for industrial businesses: the hidden costs of legacy liabilities, the tension between diversification and focus, the supplier's dilemma of being dependent on OEM fortunes while needing to invest independently, and the existential challenge of managing a technology transition from internal combustion to electric propulsion. For investors, Dana represents a fascinating case study in capital allocation under constraint — and its next chapter may be its most consequential.

II. The Universal Joint That Changed Everything (1904–1945)

In the earliest days of the automobile, transferring power from the engine to the wheels was an ugly, unreliable affair. Most cars of the early 1900s used a chain-and-sprocket system — essentially bicycle technology scaled up. The chains were loud, required constant lubrication, and broke frequently. Propeller shafts existed, but the crude joints connecting them to engines and axles shattered under stress. The automobile, for all its promise, was hobbled by its own drivetrain.

Clarence Winfred Spicer was born on November 30, 1875, in Edelstein, Illinois, into a Seventh Day Baptist family that operated a dairy farm and creamery. He grew up maintaining and repairing equipment — the kind of hands-on mechanical education that no university could replicate. After attending Alfred Academy in New York and managing the family business for a few years, Spicer enrolled at Cornell University's Sibley College of Mechanical Engineering in 1899, at the age of twenty-three. It was there, in a motor car design class in 1902, that he was assigned to design a self-propelled automobile. His solution to the power transmission problem was elegant: a specially designed universal joint, enclosed in a housing to protect it from dirt and wear, that could attach a driveshaft to both the engine and the rear axle. The u-joint — as it would come to be known across the industry — allowed smooth, reliable power transfer even as the angles between the engine and axle shifted over bumps and turns. It made the chain-drive obsolete almost overnight.

Spicer filed his patent application and received it on May 19, 1903. The publication of the patent drew immediate interest from automobile manufacturers. On April 1, 1904, Spicer began manufacturing his universal joints through an arrangement with the Potter Printing Press Company in Plainfield, New Jersey. His first shipment went to the Corbin Motor Company in Connecticut. Within months, orders came from Buick, Olds Motor Works, Mack, Stevens-Duryea, Diamond T, and a dozen others. By 1913, Spicer Manufacturing Company — as it had been renamed — counted more than one hundred vehicle manufacturers as customers. The universal joint had become as essential to the automobile as the engine itself.

But Spicer was an engineer, not a financier. The company needed capital to keep up with demand. Enter Charles Anderson Dana, born in 1881 in New York City's Gramercy Park neighborhood, a Columbia-educated lawyer who had served as a prosecutor in the New York District Attorney's office and as a member of the New York State Assembly. In 1914, Dana purchased a controlling interest in Spicer Manufacturing, bringing not just money but business acumen and political connections. He became president in 1916 and would lead the company for more than half a century. Spicer, meanwhile, continued as chief engineer, eventually accumulating forty patents before his death on November 21, 1939, in Miami, Florida. He was inducted posthumously into the Automotive Hall of Fame in 1995.

Under Charles Dana's stewardship, the company listed on the New York Stock Exchange in 1922 and relocated its headquarters and most operations to Toledo, Ohio, to be closer to the automotive hub of Detroit. Dana executed three major acquisitions of frame, transmission, and axle manufacturers, including Salisbury Axle, which became the Spicer Axle Division. The Great Depression hit brutally — by 1932, the company was operating at twenty-five percent capacity with sales plummeting to roughly two million dollars, down from a healthy prewar level. A 1934 strike involving four thousand workers from four Toledo-area auto suppliers tested Dana's resolve. Charles Dana, in a gesture that became part of company lore, personally delivered coal and coffee to the striking workers. The company returned to profitability by 1933 and pressed forward.

Then came the war. When the United States entered World War II, all automobile production was suspended. Spicer Manufacturing pivoted to military production — four-wheel-drive systems for the iconic Willys Jeep, transmissions, frames, gun carriages, ammunition accessories, and housings for fighter planes. Sales exploded from ten million dollars in 1939 to one hundred and nine million dollars in 1945, a tenfold increase. By 1944, more than ten thousand people worked for the company. To handle the volume, Spicer acquired General Drop Forge and Atlas Drop Forge, earning the Army-Navy "E" Award for excellence in war production. But the end of the war brought a savage hangover: massive military order cancellations caused an eighty-percent drop in sales. A steel shortage forced the layoff of four thousand workers in 1945, and a fifty-five-day strike at the Pottstown, Pennsylvania, plant added to the turmoil. In 1946, as the company regrouped for peacetime, Spicer Manufacturing Corporation was renamed Dana Corporation in recognition of Charles Dana's thirty-two years of leadership. The "Spicer" name lived on as the brand for the company's driveline products — a brand that mechanics still recognize today.

Charles Dana himself remained at the helm well into old age. He served as president until 1958 and as chairman through 1966, maintaining a hands-on role for more than half a century. In 1950, he founded the Dana Foundation, which initially focused on higher education but later pivoted to brain science research. The foundation's support for the Sidney Farber Cancer Institute was so significant that the institution was renamed the Dana-Farber Cancer Institute in 1983 — one of the world's preeminent cancer research centers, bearing the name of a man who spent most of his career making axles and driveshafts. Charles Dana died on November 27, 1975, at his home in Wilton, Connecticut, at the age of ninety-four.

The foundation had been laid. One engineer's invention, backed by one financier's capital, had built an industrial enterprise that supplied the backbone of American mobility. The question now was whether the company could scale beyond its origins.

III. The Golden Era: Building an Industrial Giant (1946–1990s)

The postwar decades were kind to Dana. As America built the interstate highway system and the suburbs sprawled, demand for cars, trucks, and the components that made them move surged relentlessly. Dana rode the wave with characteristic Midwestern tenacity, growing from a medium-sized parts maker into one of the world's largest independent suppliers of automotive components. By the early 1960s, the company had reached approximately five hundred million dollars in annual sales and was supplying axles, driveshafts, universal joints, frames, and gaskets to virtually every major automaker in North America: General Motors, Ford, Chrysler, International Harvester, and American Motors.

Two acquisitions in the 1960s proved pivotal — though for reasons no one anticipated at the time. In 1963, Dana acquired Perfect Circle Corporation, a leading maker of piston rings and engine parts based in Hagerstown, Indiana. Shortly thereafter, it purchased Victor Manufacturing and Gasket Company, a Chicago-based manufacturer of automotive gaskets and sealing products. Both companies brought valuable product lines and customer relationships. Both expanded Dana's reach beyond driveline components and into the engine and sealing segments — exactly the kind of adjacent-market growth that Wall Street applauded in the era's diversification-minded boardrooms. Both also brought something else: decades of asbestos-containing products whose liabilities would eventually threaten to destroy the entire enterprise. But that reckoning lay decades in the future. In the go-go expansion years of the 1960s, Dana characterized itself as a "growth company" rather than a conglomerate, seeking expansion through targeted acquisitions that strengthened its position in the driveline and sealing markets. By 1968, the company's customer list read like a Who's Who of American industry: General Motors, Ford, Chrysler, International Harvester, American Motors, and dozens of smaller manufacturers. Dana was not just a parts maker — it was an indispensable partner in the American automotive machine.

The defining figure of Dana's golden era was not Charles Dana — who remained chairman through 1966 and died in 1975 at the age of ninety-four — but a man named Rene C. McPherson. Born in Ohio in 1924, McPherson served in the Air Force, earned a bachelor's degree from the Case Institute of Technology, and completed his MBA at Harvard Business School in 1952. He joined Dana that same year as a sales engineer. By 1960, he was vice president of Hayes-Dana Limited, the company's Canadian affiliate. In 1968, he was named president and chief operating officer. In 1972, he became chairman and CEO.

What McPherson did next became the stuff of management legend — and it is worth pausing to appreciate just how radical it was for its time. On one of his first days as president, he gathered the company's policy manuals — a stack variously described as seventeen inches or twenty-two and a half inches tall — and threw them away. In their place, he issued a single-page policy statement articulating the company's philosophy. That one-page document, which was later studied by academics at the University of Michigan and published in the Journal of Business Communication, was reportedly still in use decades later. It was a declaration of principles so concise that every employee could read it in five minutes and so bold that it redefined how a Fortune 500 manufacturer thought about its workforce.

Then he cut 350 people from a headquarters staff of 500, leaving roughly 150 people to run what would become a multi-billion-dollar corporation. Consider that number: a company doing billions of dollars in annual sales, with tens of thousands of factory workers, managed by fewer people at headquarters than a typical regional bank branch. McPherson's logic was simple and ruthless — bureaucracy was the enemy of speed, and layers of management insulated decision-makers from the shop floor. He abolished time clocks, the ultimate symbol of industrial distrust. He required managers to meet with employees face-to-face rather than sending memos. He encouraged workers to participate in Dana's stock plan and helped them set their own production goals. He established "Dana University," an in-house training program that gave any employee — regardless of background or formal education — a path to advancement. The university was not a weekend seminar or a motivational poster campaign; it was a structured, ongoing commitment to developing talent from within.

McPherson's consuming orientation toward people was more than rhetoric. He believed that the people closest to the work — the machine operators, the assembly line workers, the maintenance crews — were the ones best equipped to improve it. This was, as one security analyst later noted, Japanese-style management brought to the American Midwest before most business leaders even knew what kaizen meant. At a time when American manufacturers were drowning in top-down bureaucracy, McPherson was running Dana like a collection of entrepreneurial businesses loosely connected by a shared culture and a one-page philosophy.

The results were remarkable. One security analyst observed that McPherson had brought "Japanese-style management to Dana before most people even knew what it was." Profits rose from sixty-two million dollars in 1975 to one hundred and sixty-four million dollars by 1979. Between 1963 and 1980, Dana acquired twenty-four companies, carefully expanding its product portfolio while maintaining the decentralized culture McPherson had built. He shifted the company away from dependence on original-equipment passenger cars toward light trucks — which came to represent thirty-five percent of sales — a prescient bet on what would become America's most profitable vehicle segment for decades to come. The company broke the one-billion-dollar sales barrier in 1974 and exceeded four billion dollars by 1987.

Tom Peters, in his landmark 1982 bestseller In Search of Excellence, featured Dana Corporation as one of America's best-run companies. Peters later said he "damn near worshipped" McPherson. The book marveled at the fact that a three-to-six-billion-dollar corporation was being run with fewer than one hundred people at corporate headquarters — a radical concept in an era when General Motors employed more than fourteen thousand people in its central office alone.

McPherson retired from Dana in 1980, accepting the position of Dean of Stanford Graduate School of Business — though his tenure there was cut short by injuries from a car accident. His successor at Dana, Gerald B. Mitchell — a man who had started as a machine operator at the company at age sixteen — carried the culture forward. McPherson passed away on February 26, 1996. By then, the empire he helped build was already beginning to crack.

Southwood "Woody" Morcott took over as CEO in 1985 and steered the company through a turbulent period. The early 1990s recession hammered the auto industry, and Dana was not spared. A devastating three hundred and eighty-two million dollar loss in 1992 forced a refocusing on truck engine parts, and the company recovered to post eighty million dollars in net earnings on $5.46 billion in sales by 1993. But Morcott was an empire-builder by temperament, and the recovery emboldened him. His defining move came in 1998, when he executed a $3.9 billion acquisition of Echlin Inc., an aftermarket giant based in Branford, Connecticut, that distributed and manufactured braking, engine management, and chassis parts to the independent aftermarket.

The Echlin deal was supposed to transform Dana into a vertically integrated powerhouse spanning original equipment and aftermarket channels. On paper, the logic was sound: OEM sales were cyclical, but aftermarket demand was steadier — cars need replacement parts regardless of new-vehicle production volumes. The combined company would have a commanding position in both channels. In practice, the deal was a disaster. Echlin's distribution-heavy business model was fundamentally different from Dana's manufacturing-centric operations. Integration proved far more complex than anticipated, and the debt taken on to finance the acquisition weighed heavily on the balance sheet just as the auto industry entered another downturn. Automotive News would later write that "Dana's problems started with Echlin" — and the assessment was hard to dispute.

When Joseph Magliochetti succeeded Morcott as CEO in February 1999, he inherited a company that was over-leveraged and over-extended. Magliochetti, a technology-minded leader who had risen through Dana's engineering ranks, reversed the acquisition-driven strategy in favor of organic innovation and cost discipline. He divested non-core businesses and sought to return Dana to its driveline roots. But fate was cruel. Magliochetti would not live to see the results. He died in September 2003 at the age of sixty-one from complications of pancreatitis, leaving Dana leaderless at a moment when the ground beneath the entire auto parts industry was beginning to shift. For investors, the McPherson-to-Morcott-to-Magliochetti arc is a cautionary tale about the fragility of corporate culture: it took decades to build McPherson's lean, people-first organization, and a single acquisition-driven strategy under his successors to put the whole edifice at risk.

IV. The Hidden Killer: Asbestos and the Road to Bankruptcy (1990s–2006)

The story of Dana's near-death experience begins not in any boardroom or factory, but in the lungs and chest cavities of mechanics, pipefitters, plumbers, and factory workers who, over decades, handled products they had no reason to believe were dangerous. When Dana acquired Victor Manufacturing and Gasket Company in the 1960s, it inherited a product line that included gaskets sold under the brand names Asbestopac and Corbestos — names that, in retrospect, almost seem to advertise their toxic ingredient. The gaskets, brake linings, valve covers, and a fireproofing product called Spraycraft all contained asbestos. Gasketing materials contained up to eighty percent asbestos. Friction materials like brake and clutch plates contained up to fifty percent. Dana did not fully phase out asbestos-containing products until the early 1980s, by which time the damage — measured in human exposure — was irrevocable.

The lawsuits began as a trickle in the 1980s and became a flood by the late 1990s. By 2005, Dana had dealt with approximately eighty-eight thousand asbestos-related claims. By the time of its bankruptcy filing in 2006, at least seventy thousand lawsuits were still pending, with some sources citing one hundred and fifty thousand by 2007. The company was settling roughly seven thousand five hundred cases per year, but the pipeline showed no signs of emptying. Juries were increasingly willing to impose punishing damages. A New York jury awarded seventy-five million dollars to Marlena Robaey, finding Dana forty percent liable for her peritoneal mesothelioma. A pipefitter named Louis Hicks won a five million dollar verdict for mesothelioma caused by working with Dana's asbestos-containing gaskets.

The asbestos crisis alone might have been manageable for a company of Dana's size. But it arrived in the context of a perfect storm. Michael J. Burns, a thirty-four-year General Motors veteran who had most recently served as president of GM Europe, was named CEO in March 2004, replacing the late Magliochetti. Burns inherited a company still groaning under debt from the Echlin acquisition, dependent on customers — GM, Ford, and DaimlerChrysler — that were themselves losing market share to foreign competitors, and increasingly squeezed by rising raw material and energy costs.

In September 2005, management discovered accounting irregularities: incorrect entries related to a customer agreement in the Commercial Vehicle business unit. The Audit Committee launched an investigation. By year's end, Dana was forced to restate financial statements for the first two quarters of 2005 and for the years 2002 through 2004, reducing cumulative net income by forty-four million dollars. In January 2006, the SEC issued a formal order of investigation. The company's credibility with lenders and investors cratered.

Meanwhile, the broader auto parts industry was in crisis. Delphi Corporation, the nation's largest parts supplier, filed for Chapter 11 in October 2005. Collins & Aikman and Tower Automotive followed. Ford's former parts unit, Visteon, would have gone bankrupt had Ford not committed hundreds of millions of dollars to a bailout. The automakers themselves — Dana's primary customers — were cutting production, especially of the large SUVs and pickup trucks that had been their most profitable vehicles. For Dana, lower production volumes meant lower revenue, while the costs of asbestos litigation, debt service, and raw materials remained stubbornly high. The company lost nearly $1.3 billion in the third quarter of 2005.

On March 3, 2006, Dana Corporation and forty of its wholly-owned U.S. subsidiaries filed voluntary petitions for reorganization under Chapter 11 of the Bankruptcy Code in the U.S. Bankruptcy Court for the Southern District of New York. The company had forty-six thousand workers worldwide. It secured $1.45 billion in debtor-in-possession financing to keep operations running.

The most controversial aspect of the bankruptcy was Dana's handling of its asbestos liabilities. The company created a subsidiary called Dana Companies, LLC, transferred all asbestos liabilities to it, and allocated two hundred and forty million dollars for resolution. Crucially, asbestos-related debt comprised only about three percent of Dana's total obligations — below the threshold that would have mandated creation of a formal Section 524(g) asbestos trust fund. The Ad Hoc Committee of Asbestos Claimants objected strenuously, arguing that two hundred and forty million dollars was woefully insufficient for more than eighty thousand claimants. Dana's position was that asbestos was a manageable side issue rather than the primary driver of its bankruptcy — a claim that many victims' advocates found deeply cynical.

The company's Third Amended Joint and Consolidated Plan of Reorganization was confirmed by the bankruptcy court on December 26, 2007. On January 31, 2008, Dana emerged from bankruptcy as Dana Holding Corporation. All prior common stock, options, and warrants were cancelled — existing shareholders were wiped out entirely. Anyone who held Dana stock on the day of the bankruptcy filing received nothing. Michael Burns stepped down as CEO upon emergence, and John Devine, a veteran auto executive who had served as CFO of both Ford and General Motors, was elected chairman and acting CEO. The asbestos subsidiary, Dana Companies LLC, continued to manage claims and was eventually sold in 2016, but the human toll of asbestos exposure — a legacy stretching back to products manufactured decades earlier — continued to work its way through the legal system for years after.

The entire episode is a powerful illustration of a phenomenon that every industrial investor should understand: contingent liabilities from acquired companies can lurk dormant for decades before detonating. Dana did not manufacture asbestos. It did not mine it or market it. It acquired companies that used it as a component material in products like gaskets and brake linings — products that, at the time, were standard across the industry. Yet the legal and financial consequences of that exposure, combined with a debt-laden balance sheet and a deteriorating customer base, were sufficient to destroy all shareholder equity and push a century-old Fortune 500 company into bankruptcy.

For investors evaluating industrial companies today, the Dana asbestos story raises a broader question: what latent liabilities might exist in companies that have made dozens of acquisitions over decades? The answer is that no one fully knows — and that is precisely the point. Legacy liabilities are, by definition, risks that were not fully understood or priced at the time of the original transaction. Dana's shareholders in 2006 paid the ultimate price for acquisitions celebrated forty years earlier.

V. Emergence and Transformation: Building Back (2008–2015)

Emerging from bankruptcy is only the beginning of recovery. The company that stepped out of Chapter 11 on January 31, 2008, was legally and financially a different entity from the one that went in. All prior equity had been extinguished. The balance sheet had been restructured. But the fundamental business — making axles, driveshafts, seals, and thermal management systems for an automotive industry in the throes of the Great Recession — remained essentially unchanged. The hard work of transformation was still ahead.

The restructuring plan aimed to deliver four hundred and forty to four hundred and seventy-five million dollars in annual cost savings when fully implemented. The lever set was grimly familiar to anyone who has watched industrial restructurings: facility consolidations, labor cost reductions, the establishment of VEBA trusts to offload retiree healthcare obligations from the company's balance sheet, and geographic diversification into lower-cost manufacturing regions. Dana shuttered plants in high-cost markets and expanded operations in Brazil, India, China, and Eastern Europe. The goal was not just to survive the recession but to emerge with a fundamentally lower cost structure that could weather the cyclical swings inherent in the automotive supply business.

Leadership turned over multiple times in the post-bankruptcy years. John Devine served as interim CEO while the board searched for a permanent leader. The company cycled through executives as it stabilized operations, divested non-core assets, and worked to prove that the underlying business — making critical drivetrain components for the world's automakers — remained viable despite the scars of bankruptcy. The key challenge was restoring credibility with OEM customers, many of whom had watched nervously during the Chapter 11 process, worried about supply disruptions. Dana had to demonstrate not just financial solvency but operational reliability, program-by-program, delivery-by-delivery.

The geographical reshaping of the company accelerated during this period. Pre-bankruptcy, Dana had been heavily concentrated in the United States and Western Europe. Post-bankruptcy, the company aggressively expanded its manufacturing footprint in lower-cost regions — Brazil for South American markets, India and China for Asia-Pacific, and Eastern European countries like Hungary and Romania for proximity to European OEMs at lower labor costs. This was not just about cutting costs; it was about positioning the company close to the fastest-growing vehicle markets in the world. By the early 2010s, Dana's revenue mix had shifted meaningfully, with international operations representing a growing share of the total.

The pivotal appointment came in 2015, when James K. Kamsickas was named president and CEO. Kamsickas brought more than eighteen years of industry experience, including stints at BorgWarner and Danaher, and a vision for transforming Dana from a legacy driveline supplier into a technology-forward mobility company. He was energetic, strategically ambitious, and deeply committed to the idea that Dana could — and must — play a leading role in the electrification of transportation. In August 2016, the company formally changed its name from Dana Holding Corporation to Dana Incorporated — shedding the "Holding" label that carried the stigma of the bankruptcy-era entity and signaling a new identity.

Under Kamsickas, Dana refocused on its core competencies: axles, driveshafts, sealing products, and thermal management systems. He streamlined the portfolio, divesting businesses that did not fit the strategy and investing in those that did. But the most consequential shift was strategic, not operational. Kamsickas recognized that electrification was not a distant possibility but an approaching reality. Dana had actually been experimenting with driveline concepts for electric vehicles for decades — long before any significant commercial production of hybrids or EVs existed. The company's engineers had built prototype electric driveline systems, tested motor-integrated axle concepts, and developed thermal management expertise that would prove critical in the EV era. What had been a research curiosity became, under Kamsickas, the centerpiece of the company's growth strategy. He was elected chairman of the board in December 2019, consolidating his leadership position.

By the mid-2010s, Dana had stabilized. Revenue had recovered to the $6 billion range, the balance sheet was manageable, and the company was winning new business across its light vehicle, commercial vehicle, and off-highway segments. The company that had nearly been destroyed by asbestos and debt had rebuilt itself into a focused, globally diversified Tier 1 supplier. But Kamsickas and his team knew that stability was not enough. The automotive industry was on the cusp of the most significant technology transition since the invention of the internal combustion engine. Tesla had demonstrated that electric vehicles could be desirable, not just dutiful. China was pouring billions into EV infrastructure and manufacturing. European regulators were tightening emissions standards to levels that made electrification inevitable. The question was whether Dana would be a passive victim of that transition — or one of its architects.

VI. The Failed Mega-Merger: The GKN Driveline Deal (2018)

In early 2018, an opportunity landed on Dana's doorstep that could have transformed the company into the undisputed global leader in vehicle driveline systems. GKN plc, a venerable British engineering conglomerate, was under siege. Melrose Industries, a turnaround-focused investment group, had launched a hostile takeover bid for the entire company. GKN's board, desperate for a white knight, turned to Dana with an offer to combine GKN's Driveline division — one of the world's premier driveline businesses — with Dana's operations.

On March 9, 2018, Dana announced definitive agreements to combine with GKN Driveline in a transaction valued at approximately $6.1 billion. The deal would have created a new entity called Dana Plc, with pro forma sales of roughly $13.4 billion, making it the dominant global player in vehicle drive systems. The strategic rationale was compelling: GKN Driveline's European and Asian footprint complemented Dana's North American strength, and the combined entity would possess an unmatched portfolio of electrification technologies — the core eDrive systems that both companies had been developing independently. The total consideration involved $1.6 billion in cash, assumption of $1.0 billion in pension liabilities, and the issuance of 133 million new Dana shares valued at approximately $3.5 billion.

But there was a problem. The decision was not Dana's to make. It was in the hands of GKN's shareholders, who were simultaneously evaluating Melrose's competing offer of $11.2 billion for all of GKN — not just the Driveline unit. The GKN board publicly preferred the Dana deal, arguing it would better preserve GKN Driveline's long-term value. But Melrose ran an aggressive campaign, and many GKN shareholders were attracted by the immediate premium Melrose was offering.

On March 29, 2018, the vote came in. By 1:00 p.m. London time, GKN shareholders had voted 52.43 percent in favor of the Melrose bid. The Dana merger was dead. James Kamsickas issued a statement that was, by the restrained standards of corporate communications, remarkably candid: "We are, of course, disappointed by today's outcome and continue to believe Dana would be the best owner and operator of GKN Driveline."

The loss stung, but it carried a silver lining that would shape Dana's next chapter. Unable to acquire electrification capabilities at scale through a single transformative deal, Dana was forced to build them organically and through a series of smaller, more focused acquisitions. This buy-and-build approach, while slower and more expensive in the short term, gave the company deeper technical control over the individual building blocks of an electric powertrain — motors, inverters, controls, software, thermal management — than a single large acquisition likely would have. When you buy a complete business, you get the capabilities it already has. When you build a capability piece by piece, you develop the engineering knowledge to innovate on top of it. For Dana, the failed GKN deal may have been a blessing in disguise.

There is a delicious historical irony in how the GKN story played out. After Melrose acquired GKN, it struggled to deliver the promised returns from the engineering conglomerate's complex portfolio. In 2023, Melrose spun off GKN's automotive operations as the Dowlais Group. In February 2025, American Axle and Manufacturing completed the acquisition of Dowlais — making American Axle, rather than Dana, the ultimate inheritor of GKN's driveline legacy. The combined AAM-Dowlais entity now approaches eleven billion dollars in revenue, creating a formidable competitor that occupies roughly the strategic position Dana had envisioned for itself seven years earlier. Whether Dana or American Axle made the better bet will be one of the most interesting competitive questions in the auto supplier industry over the next decade.

VII. The Electrification Pivot: Bold Bet on EVs (2017–2023)

Dana's electrification strategy did not begin with a PowerPoint deck or a board resolution. It began with observation. Four years before most Western analysts were paying attention, Dana's leadership spotted a trend emerging in China: the Chinese government was offering aggressive incentives for battery-powered buses, and domestic manufacturers were responding with orders that required electric drivetrain components. For a company that had spent over a century perfecting mechanical power transmission, the implication was clear. The market for Dana's traditional products — axles, driveshafts, universal joints — was going to shrink. But the market for electric drivetrain systems — e-axles, motors, inverters, thermal management — was going to explode. And the content per vehicle, meaning the dollar value of Dana's products in each car or truck, would at least double, and potentially triple. Think about it this way: a traditional rear axle is a relatively simple mechanical assembly. An e-axle integrates an electric motor, a high-voltage inverter, a gearbox, thermal management systems, and control software into a single unit. The value Dana could capture per vehicle was dramatically higher.

The strategic insight was that electrification would not arrive uniformly across all vehicle segments. It would hit commercial vehicles first — particularly urban buses and medium-duty delivery trucks — because these applications featured predictable routes, centralized depots for overnight charging, and fleet operators who could calculate total cost of ownership with precision. From there, it would spread to passenger vehicles, off-highway equipment, and eventually heavy-duty long-haul trucks. Dana's multi-market presence — light vehicle, commercial vehicle, and off-highway — meant it could ride the electrification wave across every segment as it arrived, applying lessons learned in one market to accelerate deployment in the next.

Starting in 2017, Dana embarked on an acquisition spree that would, within four years, give it a claim no other Tier 1 supplier could match: the ability to design, engineer, and manufacture every core component of a complete, fully integrated electric propulsion system across all mobility markets.

The first major move came on June 22, 2018, when Dana announced it was acquiring a fifty-five percent majority stake in TM4 Inc. for approximately C$165 million (about US$127 million). TM4 was a Canadian company founded in 1998 by Hydro-Quebec, Canada's largest electricity producer, and based in Boucherville, Quebec. With approximately one hundred and thirty employees, TM4 designed and manufactured electric motors, power inverters, and control systems for electric vehicles. Hydro-Quebec retained a forty-five percent interest. Critically, TM4 also operated a fifty-fifty joint venture with Prestolite Electric Beijing Limited called Prestolite E-Propulsion Systems Limited, giving Dana an immediate footprint in the world's fastest-growing EV market.

Less than a year later, in March 2019, Dana completed the acquisition of the Drive Systems segment of the Oerlikon Group for approximately CHF 600 million (roughly US$600 million). This brought two globally recognized brands — Graziano Trasmissioni, known for high-precision helical gears, and Fairfield, known for planetary hub drives — along with approximately fifty-nine hundred employees, ten manufacturing facilities across China, India, Italy, the United Kingdom, and the United States, and five R&D centers. The Oerlikon acquisition was transformative: it gave Dana world-class gear manufacturing capabilities and access to major OEM customers including BMW, Caterpillar, Daimler, and Volkswagen.

The acquisitions kept coming. In August 2019, Dana acquired Nordresa Motors, a Montreal-area e-powertrain integrator specializing in commercial vehicle electrification. In February 2020, it purchased Ashwoods Electric Motors, a UK-based specialist in low-voltage electric motors. Later in 2020, Dana acquired Rational Motion GmbH, a German company with over a decade of experience in EV system integration, embedded software, and powertrain simulation. And in March 2021, Dana completed the acquisition of Pi Innovo LLC, a leader in embedded software solutions and electronic control units, home of the OpenECU platform. In total, Dana invested approximately four hundred million dollars across these electrification acquisitions.

The capability stack Dana assembled was genuinely unique, and it is worth pausing to understand why that matters. In the traditional driveline world, an axle is a relatively self-contained mechanical assembly: gears, bearings, housings, seals, lubrication. The engineering is complex, but the system boundaries are well-defined. In the electric world, an e-axle is a fundamentally different animal. It integrates an electric motor (which converts electrical energy into rotational force), a power inverter (which converts DC battery power into the AC power the motor needs), a reduction gearbox (which adjusts the motor's speed and torque for the wheels), thermal management systems (which keep everything from overheating), and sophisticated control software (which orchestrates the entire system in real time). Building any one of these components is challenging. Building all of them and integrating them into a single, compact, reliable unit that can be manufactured at automotive volumes is extraordinarily difficult. By 2021, Dana could credibly claim to be the only Tier 1 supplier capable of producing all core components of a fully integrated e-Drive system in-house. The products were marketed under the Spicer Electrified and Dana TM4 brands, and they spanned every mobility market — light vehicle, commercial vehicle, and off-highway.

This "one-stop shop" approach was more than a marketing slogan. For OEM customers, the ability to source a complete e-Drive system from a single supplier dramatically simplified procurement, reduced integration risk, and shortened development timelines. Instead of coordinating between a motor supplier in Japan, an inverter supplier in Germany, and a gearbox supplier in Italy — each with different engineering standards, testing protocols, and production schedules — an automaker could work with Dana to co-develop an integrated system that was validated as a unit before it ever reached the assembly line.

The wins started coming. Dana's e-Power propulsion system was selected for the Kenworth K270E and K370E medium-duty cabovers and the Peterbilt 220EV — a program valued at roughly two hundred million dollars in incremental sales. The company won a contract to manufacture cooling plates for General Motors' Ultium batteries, the architecture underlying GM's entire EV lineup. It secured the electric driveline for the Jeep Wrangler 4xe, one of the most commercially successful plug-in hybrid SUVs in the market.

But the reality check came too. EV adoption, particularly in commercial vehicles, proved slower than the company's investment pace suggested. The electrification business was not yet profitable, creating margin headwinds that weighed on the company's overall financial performance. Capital intensity was higher than anticipated — building motors and inverters required different manufacturing processes than stamping axles and forging gears. Dana had set a revenue target of five hundred million dollars from electrification by 2023, and while it built a backlog of approximately seven hundred million dollars in new business — roughly half of it in electric powertrains — the path to profitability remained elusive. The company was spending ahead of revenue, a classic technology-transition bet that requires patience and deep pockets.

For long-term investors, the electrification story comes down to a single question: will Dana's content-per-vehicle advantage — the two-to-three-times multiplier from traditional axles to e-axles — generate enough incremental margin to justify the hundreds of millions invested in building the capability? The technical position is strong. The financial proof has yet to materialize.

VIII. The Strategic Retrenchment: Selling Off-Highway (2024–Present)

On November 25, 2024, Dana Incorporated made two announcements that together signaled the most significant strategic pivot since its emergence from bankruptcy sixteen years earlier. First, James Kamsickas, who had led the company as CEO for approximately nine years and as board chairman since December 2019, retired effective immediately. Second, the company announced it was pursuing a sale of its Off-Highway business segment — the division serving construction, mining, agriculture, and forestry equipment — and had engaged Goldman Sachs and Morgan Stanley to manage the process.

The man stepping into the CEO chair was R. Bruce McDonald, a Dana board member since 2014 who brought over thirty years of experience in the automotive and manufacturing industries. McDonald had earned a Bachelor of Commerce from McMaster University in Ontario, Canada, and was both a Chartered Accountant and a CPA. His career arc ran through Ernst & Young, TRW Automotive, and Johnson Controls, where he served as CFO and later vice chairman. Most recently, he had served as chairman and CEO of Adient plc, a global automotive seating supplier spun off from Johnson Controls. McDonald was a turnaround operator by disposition — precisely the profile needed for what came next.

The decision to sell Off-Highway was counterintuitive on its face. The segment was, by many measures, Dana's most attractive business: it served less cyclical end markets than automotive, it had strong competitive positions, and it generated relatively high margins. Why sell your best asset?

The answer lay in the balance sheet and the company's strategic focus — and it reveals a hard truth about capital allocation that every industrial investor should appreciate. Dana's aggressive electrification investments had been funded partly with debt, and the company's net leverage had ballooned above three times EBITDA by 2023 — a dangerous level for a cyclical industrial supplier. In the automotive world, where revenue can drop twenty to thirty percent in a downturn and fixed costs are stubbornly sticky, high leverage is not just risky — it can be fatal. The memories of 2006 were still fresh.

At the same time, the company's organizational complexity — four business segments spanning light vehicle, commercial vehicle, off-highway, and power technologies — was diluting management attention and limiting the speed of cost reduction. Four segments meant four leadership teams, four sets of strategic plans, four capital allocation debates. McDonald and the board concluded that radical simplification was required. The logic was almost surgical: sell the Off-Highway business — which had its own distinct customer base, competitive dynamics, and capital needs — and use the proceeds to fix the balance sheet, simplify the organization, and create a focused light-vehicle and commercial-vehicle company with the financial flexibility to pursue either growth or further returns to shareholders.

There is a school of thought in business strategy that says you should never sell your best asset. But there is another school — and it is the one McDonald belongs to — that says your best asset is worth more to you as cash if that cash eliminates the vulnerabilities that threaten the rest of your enterprise. A fortress balance sheet and a focused portfolio may ultimately be worth more than a diverse collection of businesses weighed down by debt.

On June 11, 2025, Dana announced a definitive agreement to sell the Off-Highway Drive and Motion Systems business to Allison Transmission Holdings for approximately $2.7 billion, representing roughly 7.5 times expected 2025 adjusted EBITDA. After taxes, transaction expenses, and assumed liabilities, Dana expected net cash proceeds of approximately $2.4 billion, with about $2 billion earmarked for debt repayment. The combined Allison-Dana Off-Highway entity would form a $5.5 billion revenue global industrial leader with operations in twenty-nine countries. All regulatory approvals were received by November 19, 2025, and the transaction closed on January 2, 2026.

Simultaneously, McDonald launched a sweeping cost reduction program. The initial target of two hundred million dollars was raised to three hundred million dollars in annualized savings through 2026, with one hundred and seventy-five million dollars expected in 2025 alone. The company was reorganized from four segments into two: Light Vehicle Systems and Commercial Vehicle Systems, effective in the first quarter of 2025. The Power Technology segment was split, with its OEM-facing businesses folded into Light Vehicle and its aftermarket operations folded into Commercial Vehicle.

The financial results have been striking. In 2025, Dana's continuing operations generated $7.5 billion in sales with $610 million in adjusted EBITDA, an 8.1 percent margin that represented meaningful improvement from prior years. Adjusted free cash flow reached $331 million. But the most impressive number was the fourth quarter: roughly $1.9 billion in sales with $208 million in adjusted EBITDA and an 11.1 percent margin, up from a mere 4.7 percent in the year-ago quarter. The company completed nearly $2 billion in debt reduction, bringing its net leverage ratio below 1.0 times — down from over 3 times just two years earlier. Liquidity stood at approximately $1.8 billion.

Capital returns have been equally aggressive — and this is where McDonald's financial engineering background shines. Dana returned $704 million to shareholders in 2025, including the repurchase of thirty-four million shares — representing a remarkable twenty-three percent of outstanding shares. Think about that: in a single year, Dana retired nearly a quarter of its equity. The board expanded its capital return authorization from $1 billion through 2027 to $2 billion through 2030 and raised the quarterly dividend twenty percent to twelve cents per share. For a company that wiped out its shareholders entirely in 2008, returning $2 billion to equity holders over six years represents a profound transformation.

The forward picture looks equally compelling on paper. Guidance for 2026 calls for sales of $7.3 to $7.7 billion, adjusted EBITDA of $750 to $850 million (a 10 to 11 percent margin), and free cash flow of approximately $300 million — with the added tailwind of a $95 million reduction in interest expense from the aggressive debt repayment. The company has scheduled a Capital Markets Day for March 25, 2026, where it plans to unveil its Dana 2030 strategy — targeting roughly $10 billion in sales, 14 to 15 percent EBITDA margins, and approximately six percent free cash flow margins. If achieved, those numbers would represent a fundamentally different enterprise from the one that entered 2024 — more profitable, more focused, less leveraged, and returning substantial capital to shareholders.

The key question is whether the revenue growth embedded in the Dana 2030 targets — roughly $10 billion on a base of $7.5 billion — can be achieved in an uncertain end-market environment. The answer depends heavily on whether electrification programs ramp as planned and whether Dana's traditional ICE business holds up better than skeptics expect during the transition period. The company's management believes that new business wins — both in traditional and electrified products — will drive organic growth, supplemented by selective acquisitions. Skeptics point to the cyclicality of the auto industry and the risk that the transition from ICE to EV may be bumpier than any linear forecast suggests.

IX. Business Model and Competitive Positioning

Dana's business model operates at the intersection of mechanical engineering and electrical engineering — a position that grows more complex and more valuable with every vehicle that replaces a traditional drivetrain with an electric one. As a Tier 1 supplier, Dana sells directly to original equipment manufacturers — the automakers and truck builders — rather than to consumers. Its products are invisible to the average driver, hidden beneath the vehicle in the form of axles, driveshafts, sealing systems, thermal management systems, and increasingly, electric motors, inverters, and battery thermal management.

Following the Off-Highway divestiture, Dana operates in two segments. Light Vehicle Systems, the larger at approximately $5.2 billion in 2025 revenue, supplies axles, driveshafts, and electrified propulsion systems for passenger cars, SUVs, crossovers, and light trucks. This segment's fortunes are tied directly to the production schedules of major automakers — when Ford builds more F-150s or Stellantis builds more Jeep Wranglers, Dana benefits. When those OEMs cut production, Dana suffers. Commercial Vehicle Systems, at approximately $2.3 billion, serves medium- and heavy-duty trucks, buses, and vocational vehicles with similar product lines plus a significant aftermarket business.

The aftermarket deserves special attention because it is often overlooked in discussions of automotive suppliers — yet it serves as a critical stabilizing profit engine. When a truck fleet operator needs to replace a worn driveshaft, or a mechanic needs a new universal joint for a customer's pickup truck, the Spicer brand carries significant weight. Aftermarket parts carry higher margins than original equipment sales because the distribution channels are different — there is less of the intense price-down pressure that characterizes OEM procurement — and because brand recognition matters in a way it does not in the original equipment market. No consumer chooses a new car based on who manufactured the axle. But plenty of mechanics specifically request Spicer parts because they trust the quality. This brand equity, built over more than a century, is a genuine competitive advantage that does not show up on any balance sheet.

The content-per-vehicle opportunity is the single most important dynamic in Dana's business model. A traditional mechanical axle might represent a few hundred dollars of content per vehicle. An e-axle — which integrates an electric motor, power electronics, a gearbox, and thermal management into a single unit — can represent two to three times that amount. Dana's CFO has stated publicly that the company expects its content per vehicle to at least double in the transition from traditional axles to e-axles, with the potential to reach three times. If EV penetration follows even a moderate growth curve, the implications for Dana's revenue per unit are significant.

Geographically, Dana operates manufacturing and engineering facilities across North America, Europe, and Asia-Pacific, with particular strength in the United States, Italy (through the Graziano acquisition), China, India, and the United Kingdom. Customer concentration is a persistent risk: Dana's revenue is heavily weighted toward a handful of major OEMs, and the health of those customers — particularly the Detroit Three — has an outsized impact on Dana's performance.

The competitive landscape is formidable. BorgWarner, at $14.1 billion in 2024 revenue, is Dana's closest publicly traded peer and competes directly in e-propulsion, turbochargers, and drivetrain systems, with higher margins than Dana. ZF Friedrichshafen, the German private giant with over forty billion euros in annual revenue, competes across driveline, e-axles, and commercial vehicle systems but is itself undergoing major restructuring and carrying significant debt. American Axle and Manufacturing, at $6.1 billion, became a much more formidable competitor in February 2025 when it completed the acquisition of Dowlais Group (the successor to the very GKN Driveline business Dana had tried to acquire in 2018), creating a combined enterprise approaching eleven billion dollars in revenue. Magna International, at approximately forty-three billion dollars, competes in powertrain and e-drive but operates at a completely different scale.

Dana's differentiation rests on two pillars. First is full-system integration: the claim, built through the acquisition spree of 2018–2021, that Dana is the only supplier capable of designing and manufacturing every component of a complete electric propulsion system in-house. This means OEMs can work with a single supplier rather than integrating components from multiple vendors — a significant value proposition in an industry where time-to-market matters enormously. Second is cross-market knowledge transfer: insights and technologies developed for commercial vehicle electrification can be applied to light vehicles, and vice versa. The medium-duty mechatronic system integration that Dana developed for trucks is, in the words of company management, "highly transferable" to full-frame trucks and light vehicles.

The myth versus reality check on Dana's competitive positioning is worth spelling out. The consensus narrative is that Dana is a legacy auto supplier trying to reinvent itself for the EV era — a slow-moving dinosaur hoping to evolve fast enough. The reality is more nuanced. Dana is not starting from scratch on electrification; it has been investing in the space since at least 2017 and has assembled capabilities — through TM4, Oerlikon, Pi Innovo, and others — that are genuinely differentiated. Its cross-market presence is unusual and hard to replicate. And the aftermarket business provides a stable earnings stream that competitors focused purely on original equipment do not have. On the other hand, the consensus narrative is correct that Dana faces formidable structural headwinds: buyer power is high, competitive intensity is fierce, and the shift from mechanical to electrical components introduces entirely new supply chain risks and technology obsolescence cycles.

Whether these advantages prove durable depends on execution. The technology exists. The customer relationships are established. The question is whether Dana can achieve profitable scale in electrification before its traditional business erodes — and before better-capitalized competitors or vertically integrating OEMs close the gap.

X. Strategic Analysis: Porter's Five Forces and Hamilton's Seven Powers

Threat of New Entrants: Medium-High. The automotive supply business has traditionally been protected by high barriers: massive capital requirements for manufacturing facilities, decades-long OEM relationships built on quality certification, and the engineering complexity of designing components to the exacting tolerances demanded by automakers. But the EV revolution is lowering some of these barriers. Chinese suppliers like BYD's vertically integrated supply chain can produce e-axles and motors at costs that challenge traditional Western suppliers. More critically, the automakers themselves — Tesla, BYD, and increasingly legacy OEMs — are exploring vertical integration of key EV components. When your customer becomes your competitor, the game changes fundamentally.

Bargaining Power of Suppliers: Medium. Dana's raw material inputs — primarily steel, aluminum, and copper — are broadly commoditized, limiting individual supplier leverage. However, specialized electronics components, rare-earth magnets for electric motors, and semiconductor chips have created pockets of supply chain vulnerability that were painfully exposed during the post-pandemic chip shortage. Dana's scale provides meaningful negotiating leverage, but the shift toward electronics-heavy products introduces new supplier dependencies that did not exist in the purely mechanical era.

Bargaining Power of Buyers: High. This is the defining challenge of the Tier 1 supplier business model. OEM customers — the automakers and truck builders — wield enormous negotiating power. Annual price-down expectations are baked into the industry's DNA; suppliers are typically expected to deliver cost reductions of two to three percent per year regardless of their own input cost trajectories. Platform consolidation means fewer programs to compete for. And when major customers like GM or Ford cut production, the revenue impact flows immediately to suppliers like Dana, with limited ability to adjust the cost base in real time.

Threat of Substitutes: High. The powertrain landscape has never been more uncertain. Vehicles might be powered by internal combustion engines, hybrids, battery-electric drivetrains, or hydrogen fuel cells — each requiring a different component architecture and a different set of supplier capabilities. OEM vertical integration represents a form of substitution: if an automaker decides to manufacture its own e-axles rather than sourcing them from Dana, the demand simply disappears. Alternative mobility models — autonomous vehicles, shared fleets, urban micro-mobility — could, over time, reduce the total number of vehicles produced and the content per vehicle that suppliers like Dana can capture.

Competitive Rivalry: Very High. The automotive supplier industry is consolidating globally, but the remaining competitors are aggressive and well-capitalized. American Axle's acquisition of Dowlais/GKN Automotive created a direct rival with combined revenue approaching eleven billion dollars. BorgWarner maintains higher margins and a broader technology portfolio. ZF, despite its debt challenges, has scale advantages that Dana cannot match. Chinese suppliers, operating with lower labor costs and often with government support, are expanding internationally. Competition occurs simultaneously on price, quality, innovation, speed-to-market, and increasingly, electrification capability.

Hamilton's Seven Powers assessment reveals a mixed picture. Scale Economies provide moderate power — Dana's global manufacturing footprint delivers cost advantages, but the fragmented nature of its end markets limits the concentration effects that drive true scale power. Network Effects are minimal in a business-to-business supplier model. Counter-Positioning holds medium potential: Dana's aggressive EV investment could counter-position it against pure-ICE suppliers that fail to make the transition, but execution risk is substantial. Switching Costs are medium — engineering integration and quality validation create stickiness with OEM customers, but automakers actively manage supplier concentration to avoid dependency. Branding power is low in the OEM business (end consumers do not choose a vehicle based on who made the axle) but medium-to-high in the aftermarket, where the Spicer brand carries significant weight with professional mechanics. Cornered Resource power is low-to-medium — Dana's deep application knowledge and integration expertise are valuable but not defensible against well-capitalized competitors over the long term. Process Power is medium — the legacy of Dana University and McPherson's management culture provides operational advantages, but these are replicable by competitors willing to invest in talent and culture.

The overall picture that emerges from this analysis is sobering but not hopeless. Dana operates in one of the most structurally challenging industries in the world — automotive supply — where buyer power is immense, competitive rivalry is fierce, and technology disruption is constant. The company has no durable "moat" in the Buffettian sense. It does not benefit from network effects, its brand power is limited to the aftermarket, and its scale economies are real but insufficient to prevent larger competitors from matching its cost structure.

What Dana does have is a rare combination of capabilities: full e-Drive system integration, multi-market presence across light vehicle and commercial vehicle, a trusted aftermarket brand in Spicer, and deep application knowledge accumulated over twelve decades. These are not impregnable competitive advantages, but they are meaningful ones — enough to earn Dana a seat at the table as the automotive industry undergoes its most significant transformation since Henry Ford's assembly line. The EV transition represents both an existential threat and an enormous opportunity. The outcome depends almost entirely on execution — and on whether the broader market environment cooperates with the company's strategic timeline.

XI. Bull Case, Bear Case, and What to Watch

The Bull Case. Dana may be one of the most perfectly hedged companies in the automotive supply chain. Its traditional ICE business generates cash that funds its EV investment. Its cross-market presence — light vehicle, commercial vehicle, aftermarket — provides diversification that pure-play competitors lack. The content-per-vehicle multiplier is real and significant: when an automaker replaces a mechanical axle with an e-axle, Dana's revenue per unit can double or triple. In a world where the direction of travel is clearly toward electrification — even if the pace is uncertain — a company that earns more per vehicle in the EV future than the ICE present has a powerful structural tailwind.

The Off-Highway sale has transformed the balance sheet. Net leverage below 1.0 times, liquidity of $1.8 billion, and an aggressive capital return program — including $704 million returned to shareholders in 2025 alone and a $2 billion buyback authorization through 2030 — create the financial flexibility to invest in growth while returning capital to shareholders. This is a company that has gone from the brink of financial distress to a fortress balance sheet in roughly two years. The magnitude of that transformation should not be underestimated.

Commercial vehicle electrification, particularly in medium-duty trucks and buses, appears to be reaching an inflection point. Regulatory requirements for zero-emission deliveries in urban areas, fleet operator economics that favor electric powertrains for predictable-route applications, and declining battery costs are all converging to drive adoption. Dana's early investments in this space — the PACCAR programs for Kenworth and Peterbilt, along with other medium-duty wins — position it to capture significant share in what could become a substantial market. The restructuring is driving margin expansion: fourth-quarter 2025 EBITDA margins of 11.1 percent, up from 4.7 percent a year earlier, suggest the cost reduction program is gaining serious traction. And the stock, as of early 2026, trades at a valuation that may not fully reflect the company's improving fundamentals and the strategic transformation underway.

The Bear Case. The risks are real and multifaceted. Start with the biggest one: EV adoption timing. EV penetration forecasts have repeatedly been revised downward in North America and Europe, and if the transition proves slower than Dana's investment pace suggests, the company risks significant capital destruction — having spent hundreds of millions on capabilities that generate insufficient returns for years to come. The worst-case scenario is a "stranded investment" problem: billions spent building e-Drive capabilities while traditional ICE volumes decline slowly enough that the old business erodes but EV volumes do not grow fast enough to compensate.

The Off-Highway sale, while strategically defensible, removed Dana's highest-margin, most stable business segment, concentrating the remaining portfolio in the more cyclical and more competitive light vehicle and commercial vehicle markets. There is no putting that genie back in the bottle. If the auto market enters a prolonged downturn, Dana no longer has the Off-Highway cushion to fall back on.

Customer concentration remains a persistent vulnerability. Dana's revenue is heavily weighted toward a handful of major OEMs, particularly the Detroit Three (GM, Ford, and Stellantis), which face their own competitive pressures from Tesla, BYD, and other insurgent manufacturers. When these customers cut production — as they periodically must — Dana suffers immediately, with limited ability to offset the revenue decline in the short term.

Chinese competitors represent a growing threat that is difficult to overstate. Companies like BYD, which manufactures its own electric motors, inverters, and battery systems — essentially the complete EV powertrain — operate with vertically integrated supply chains, lower labor costs, and often with government support. As Chinese automakers expand into global markets, they bring their supply chains with them, potentially displacing Western suppliers like Dana. The possibility that major legacy OEMs will follow suit and vertically integrate key EV components — building their own motors and inverters rather than sourcing them from suppliers — represents an existential threat to Dana's electrification thesis.

Finally, legacy liabilities persist. Asbestos claims, while manageable at current levels, continue to work through the legal system. Pension obligations remain a drag on the balance sheet. And the automotive supplier industry's inherent cyclicality means that even the best-managed company in the sector can see its earnings cut in half during a severe downturn.

Key Metrics to Track. For investors following Dana's transformation, three metrics deserve primary attention.

First, adjusted EBITDA margin trajectory. This is the single best indicator of whether the restructuring and cost reduction programs are translating into sustainable profitability. The company has guided to 10 to 11 percent margins in 2026 and is targeting 14 to 15 percent by 2030. Consistent sequential improvement here would validate the strategic pivot; margin stagnation or deterioration would signal that the underlying business challenges are more structural than cyclical.

Second, electrification revenue growth and mix. Track both the absolute dollar growth of EV-related revenue and its share of total company sales. The content-per-vehicle thesis requires that as traditional ICE volumes decline, EV revenues grow fast enough — and at sufficient margins — to more than offset the decline. New EV program wins, backlog growth, and the path to electrification profitability are the leading indicators.

Third, free cash flow conversion. For a capital-intensive industrial company navigating a technology transition, cash generation is the ultimate proof that the strategy is working. Dana guided to approximately $300 million in free cash flow for 2026. Sustained free cash flow at or above this level, after funding necessary capital expenditures for both traditional and electrified products, would demonstrate that Dana can simultaneously invest in the future and reward shareholders.

XII. Epilogue: The Future of Mobility

Dana Incorporated stands today at a fascinating inflection point. It is leaner than at any time in recent memory — two segments instead of four, net leverage below 1.0 times, and a management team with a clear mandate to drive margins higher and complexity lower. The company has scheduled a Capital Markets Day for March 25, 2026, where it plans to present its Dana 2030 strategy, targeting approximately ten billion dollars in sales and fourteen to fifteen percent EBITDA margins — numbers that, if achieved, would represent a fundamentally more profitable and more valuable enterprise than the one that existed even three years ago.

The unanswered questions are the same ones facing the entire mobility industry. Will EV adoption accelerate in the second half of this decade, validating the billions that Dana and its competitors have invested in electrification? Or will the transition prove more gradual than expected, extending the relevance of traditional ICE drivetrain products — and the revenue they generate — for longer than the market currently assumes? Will automakers vertically integrate the electric drivetrain components that are the core of Dana's growth thesis, or will the complexity and capital intensity of motor and inverter manufacturing push them toward outsourcing to specialized suppliers? And can Dana, a company with $7.5 billion in revenue, compete effectively against rivals two, three, or six times its size?

What Dana teaches about longevity is instructive — and humbling. Over one hundred and twenty years, this company has survived the transition from horse-drawn carriages to automobiles, two world wars, the Great Depression, the rise and decline of American automotive dominance, asbestos litigation that numbered in the tens of thousands, a bankruptcy that wiped out its shareholders, a failed mega-merger, a global financial crisis, and a pandemic. It has done so not through any single stroke of genius but through a relentless willingness to adapt — to shed what is no longer working, to acquire what is needed, and to reorganize when the old structure no longer fits the new reality.

Consider the roster of companies that appeared alongside Dana on the original Fortune 500 list in 1955. The vast majority no longer exist — absorbed by mergers, destroyed by competition, or simply faded into irrelevance. Dana is one of roughly fifty that has appeared on the list every single year since. That is not an accident. It reflects something in the company's institutional DNA — a survival instinct that transcends any individual leader or strategic plan.

But survival and prosperity are not the same thing. Dana has survived by adapting, but it has not always thrived. Shareholders who held the stock through the 2006 bankruptcy were wiped out entirely. Shareholders who held through the electrification investment period from 2018 to 2024 endured years of margin compression and stock price underperformance as the company spent ahead of revenue on capabilities whose payoff remained uncertain. The history of Dana is, in many ways, a history of the auto supplier industry itself — cyclical, capital-intensive, dependent on forces beyond its control, and perpetually engaged in a race between investing for the future and generating returns in the present.

The deeper story of Dana Incorporated is the story of capital-intensive hardware businesses trying to survive platform shifts. It is the story of companies that make the physical things that move the world — axles, gears, motors, joints — and must continually justify their existence in an industry that relentlessly pushes costs down and expectations up. Clarence Spicer, working in his New Jersey machine shop in 1904, could not have imagined that his enclosed universal joint would spawn an enterprise that, more than a century later, would be building electric propulsion systems for autonomous mining trucks and battery-powered delivery vans. But he would have recognized the impulse: find a problem, engineer a solution, and build a business around it. From one inventor's workshop in Plainfield, New Jersey, to a global enterprise with operations in dozens of countries and a portfolio spanning traditional and electrified propulsion, Dana's journey is a quintessentially American industrial narrative. Whether its next chapter is one of renewal or decline will depend on whether the bet on electrification — the biggest bet in the company's long history — ultimately pays off.

XIII. Further Reading and Resources

Company Sources: Dana investor relations site at danaincorporated.gcs-web.com provides comprehensive financial data, earnings transcripts, and SEC filings. Dana's official history timeline at dana.com/company/history offers a well-organized chronological overview. The company's 10-K annual reports from 2020 through 2024 provide detailed segment-level financial data and risk factor discussion.

Books: Paul Ingrassia's Crash Course: The American Automobile Industry's Road from Glory to Disaster provides essential context on the industry environment that shaped Dana's fortunes. His earlier book, Engines of Change, traces the cultural and economic impact of the automobile. Tom Peters' In Search of Excellence features Dana Corporation as a case study in progressive management under Rene McPherson.

Industry Analysis: WardsAuto has provided extensive coverage of the auto supplier crisis and Dana's bankruptcy. Automotive News maintains a deep archive on Dana's restructuring and strategic evolution. FreightWaves has published detailed analysis of commercial vehicle electrification, the segment where Dana has made some of its most significant EV investments.

Academic and Legal: The Dana Corporation bankruptcy court documents, filed in the Southern District of New York (Case No. 06-10354), provide a detailed record of the restructuring process. The academic paper "We the People? An Analysis of the Dana Corporation Policies Document," published in the Journal of Business Communication, examines the company's famous one-page philosophy statement from the McPherson era.

Recent Coverage: Dana's January 2025 business update and restructuring announcement, the Allison Transmission acquisition of Dana Off-Highway, and the February 2026 full-year results announcement all provide the most current view of the company's trajectory. The Capital Markets Day scheduled for March 25, 2026, will be the next major milestone for investors tracking the Dana 2030 strategy.

Competitive Context: BorgWarner's annual reports and investor presentations provide direct comparisons on margins, electrification strategy, and revenue mix. American Axle's acquisition of Dowlais Group represents the most significant recent competitive development. The broader EV supply chain disruption is tracked extensively by S&P Global Mobility and Bloomberg NEF.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube