Dominion Energy: From Colonial Roots to Clean Energy Future

I. Introduction & Episode Roadmap

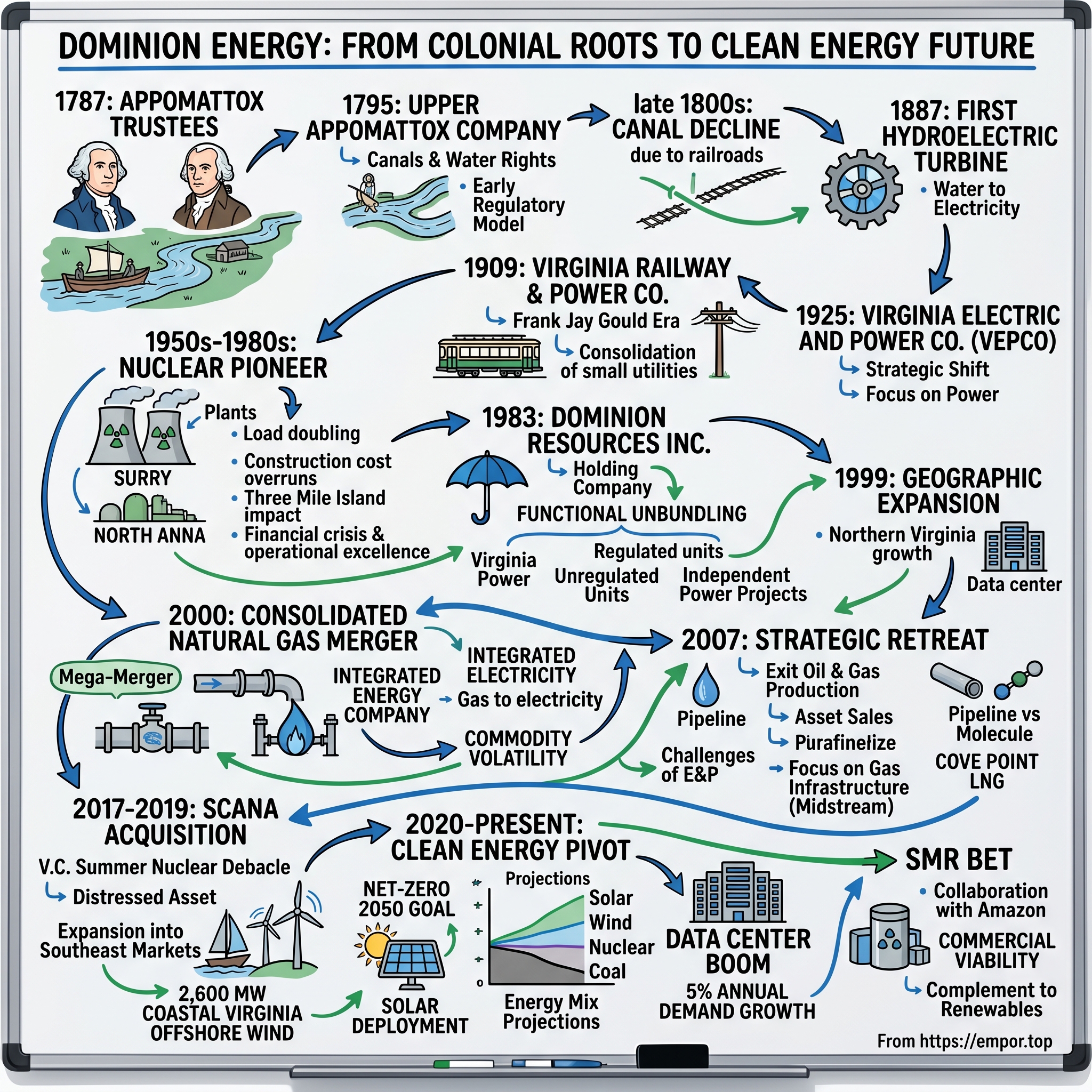

Picture this: Seven men gather in Richmond, Virginia in 1787. Among them, George Washington and James Madison. Their mission? Transform the wild Appomattox River into a commercial artery that would power the young nation's economy. They couldn't have imagined that their canal trust would evolve into a $70 billion energy colossus serving 7 million customers across 15 states, or that their water rights would become the foundation for America's largest offshore wind project.

This is the story of Dominion Energy—a company that began moving rum barrels on wooden barges and now moves electrons through 54,000 miles of distribution lines. It's a tale of constant reinvention: from canal operator to trolley company, from regional utility to nuclear pioneer, from oil & gas explorer to clean energy champion. Each transformation reflected not just corporate strategy but America's own energy evolution.

Today, Dominion stands at perhaps its most critical juncture yet. The company operates 27,000 megawatts of power generation capacity—enough to power 6.75 million homes simultaneously. Its infrastructure spans from Utah's natural gas fields to Virginia's data center alley, from South Carolina's nuclear plants to the Atlantic Ocean's wind-swept waters. With 1.2 trillion cubic feet of natural gas reserves and 14,000 miles of gas transmission pipelines, Dominion is both a legacy fossil fuel giant and an aspiring renewable energy leader—a duality that defines its current challenges and opportunities.

The timing of this story couldn't be more relevant. As artificial intelligence drives unprecedented electricity demand, as climate regulations reshape energy economics, and as geopolitical tensions redefine energy security, Dominion finds itself at the intersection of multiple megatrends. Northern Virginia, its core service territory, has become the world's data center capital, with electricity demand growing at rates not seen since the 1960s. Meanwhile, the company has committed to net-zero emissions by 2050 while maintaining reliability for customers who simply cannot tolerate blackouts.

This episode traces four major themes that define Dominion's journey. First, the regulated utility model—how guaranteed returns create both stability and constraints. Second, energy transitions—from water power to coal, coal to nuclear, and now fossil fuels to renewables. Third, the role of scale and integration in energy markets. And fourth, the delicate dance between public service obligations and shareholder returns. Each era of Dominion's history illuminates these tensions in different ways, offering lessons for investors, policymakers, and anyone interested in how America powers itself.

II. Colonial Origins & The River Trust Story

The autumn of 1787 brought unusual energy to Virginia's capital. The Constitutional Convention had just concluded in Philadelphia, and the architects of American democracy returned home to tackle more immediate challenges. Among them: how to move goods from Virginia's fertile interior to Atlantic ports. Rivers were highways, but Virginia's waterways—rocky, shallow, and prone to seasonal extremes—resisted navigation.

Enter the Virginia General Assembly's bold solution: the Appomattox Trustees. This wasn't just any infrastructure project. The trustees included George Washington himself, fresh from presiding over the Constitutional Convention, and James Madison, the document's chief architect. These weren't mere figureheads—Washington had personally surveyed much of Virginia's backcountry and understood the economic potential locked behind unnavigable rivers. He saw canals as instruments of national unity, binding the western territories to the Atlantic economy before they could drift toward Spanish or British influence.

The trustees' mandate was deceptively simple: improve navigation along the James River and its major tributary, the Appomattox. But the execution required engineering miracles by 18th-century standards. They needed to blast through granite falls, construct locks to lift boats around rapids, and build towpaths for mules to pull barges upstream. The work was backbreaking, often performed by enslaved laborers and Irish immigrants working in malaria-infested swamps.

By 1795, recognizing that public administration couldn't sustain such complex operations, the trustees spun off the Upper Appomattox Company—Dominion's first corporate ancestor. This entity didn't just build canals; it constructed an entire industrial ecosystem. Water rights came with the territory, and the company began erecting dams not just for navigation but to power mills. Flour mills, sawmills, and tobacco processing facilities sprouted along the controlled waterways. The company essentially became Virginia's first utility, selling mechanical power through water wheels long before anyone dreamed of electrical generation.

The economics were compelling. A single barge could carry 50 tons of cargo—the equivalent of 25 wagon loads—with just two men and a mule. Tobacco from Piedmont plantations that previously rotted in warehouses waiting for wagon space could now reach Richmond's port in days. The canal system also moved a more troubling cargo: enslaved people, bought and sold in Richmond's markets and transported to Deep South cotton plantations. This dark chapter reminds us that infrastructure is never morally neutral—it amplifies the economic system it serves.

But the real innovation was the company's business model. Unlike European canals typically owned by governments, the Upper Appomattox Company pioneered the American approach: private capital, public charter, regulated monopoly. The state granted exclusive navigation rights in exchange for rate caps and service obligations. Sound familiar? This regulatory compact—private ownership with public oversight—would define American utilities for the next two centuries.

The canal era peaked in the 1850s, moving 195,000 tons of freight annually. But even as barges plied the waters, a new technology was spreading across America: the railroad. By 1860, rail lines paralleled most canal routes, offering year-round service unaffected by droughts or freezes. The Civil War delivered the final blow. Union forces systematically destroyed Virginia's canal infrastructure to cripple Confederate logistics. General Sheridan's cavalry spent April 1865 methodically demolishing locks and aqueducts that had taken decades to build.

Yet the Upper Appomattox Company survived, pivoting from transportation to power generation. Its water rights—those precious legal claims to river flow—remained valuable. In 1887, the company installed its first hydroelectric turbine, converting falling water into Edison's new marvel: electricity. By 1901, these assets attracted the attention of northern financiers seeking to electrify the New South. The Virginia Passenger & Power Company acquired the water rights, transforming a colonial canal trust into a modern electric utility.

III. The Frank Jay Gould Era & Birth of VEPCO (1909–1940s)

Frank Jay Gould stepped off his private railcar at Richmond's Main Street Station on a humid June morning in 1909, surveying the city that would soon make him even wealthier. The 32-year-old heir to railroad titan Jay Gould's fortune had already conquered Manhattan real estate and French Riviera casinos. But Virginia's capital, still rebuilding from Civil War devastation, presented an irresistible opportunity: a growing city with fragmented electric service, ripe for consolidation.

Gould didn't come to Richmond for sentiment. His scouts had identified a classic roll-up opportunity—dozens of small electric companies serving piecemeal territories with incompatible equipment and duplicative infrastructure. Richmond alone had three competing electric companies running parallel wire networks down the same streets. Norfolk had two. The inefficiency was staggering, but also profitable for those with capital and vision to consolidate.

On June 29, 1909, Gould incorporated the Virginia Railway & Power Company, immediately acquiring Richmond's scattered electric properties for $7.2 million. But electricity was just part of his vision. The real money, Gould believed, was in street railways—electric trolleys that would define urban development for the next generation. His father had built a railroad empire; Frank would build an electric one.

The numbers tell the story of Gould's ambition. Within eighteen months, Virginia Railway & Power controlled 80 miles of trolley track, 300 streetcars, and power plants generating 30 megawatts—massive scale for that era. The company didn't just move people; it created destinations. Gould built amusement parks at the end of trolley lines—Forest Hill Park in Richmond, Ocean View in Norfolk—giving working families reasons to ride on weekends. The parks featured dancing pavilions, roller coasters, and electric light displays that seemed magical to audiences still adjusting to indoor electricity.

But Gould's most enduring innovation was operational integration. Previous utilities treated generation, transmission, and distribution as separate businesses. Gould merged them into a single system, achieving economies of scale that smaller competitors couldn't match. A central dispatch office—revolutionary for its time—coordinated power flows across the entire network, shifting electricity from underutilized plants to areas of peak demand. This integration model would become the template for American utilities.

The financial engineering was equally sophisticated. Gould pioneered the holding company structure in utilities, using Virginia Railway & Power as an operating company while maintaining control through a web of parent corporations. This allowed him to leverage assets repeatedly, funding expansion with debt while maintaining control with minimal equity. When critics complained about foreign (meaning New York) control of Virginia utilities, Gould simply moved the company's nominal headquarters to Richmond while keeping real power in Manhattan.

By 1925, the company had grown too large for its original name. Trolleys were losing ground to automobiles—Henry Ford's Model T had democratized driving—and "Railway" seemed antiquated. The reorganization as Virginia Electric and Power Company (VEPCO) signaled a strategic shift: electricity was the future, not transportation. The company sold off most trolley lines by 1930, focusing entirely on power generation and distribution.

The transformation reflected broader changes in American capitalism. The freewheeling Gould era, with its stock manipulation and pyramid holding companies, was giving way to regulated monopolies. The 1935 Public Utility Holding Company Act dismantled Gould's complex ownership structure, forcing VEPCO to become a standalone, locally-managed utility. By 1940, Frank Gould had cashed out, moving permanently to France where he would spend the war years protecting his Riviera properties from both Nazi occupation and Allied bombing.

VEPCO emerged from World War II as Virginia's dominant electric utility, serving 450,000 customers across the state's eastern half. The war had transformed everything—Richmond's shipyards had built Liberty ships, Norfolk's naval base had become the world's largest, and Northern Virginia had sprouted Pentagon offices and defense contractors. Electricity demand had tripled in five years. The postwar suburban boom, with its electric ranges, water heaters, and air conditioners, would drive demand even higher.

Management, now local Virginians rather than New York financiers, faced a pleasant problem: how to build generation capacity fast enough to meet seemingly infinite demand. Their solution would make VEPCO one of America's nuclear pioneers, but also nearly bankrupt the company. The atomic age was about to begin.

IV. Nuclear Pioneer: The Surry & North Anna Story (1950s–1980s)

Stanley Ragone stood at the edge of Gravel Neck peninsula in 1967, watching bulldozers clear Virginia pines for what would become the South's first commercial nuclear plant. VEPCO's chief engineer had spent two years searching for the perfect site: seismically stable, with abundant cooling water, far enough from population centers but close enough to transmission lines. This spot on the James River, 17 miles from Colonial Williamsburg, checked every box. "We're not just building a power plant," Ragone told his team. "We're building the future."

The future seemed electric—literally. VEPCO's load was doubling every seven years, a growth rate that would require tripling generation capacity by 1980. Coal plants, the workhorses of the grid, took five years to build and faced growing environmental opposition. The Clean Air Act of 1963 had given federal regulators new powers over emissions. Meanwhile, the Atomic Energy Commission was practically begging utilities to build nuclear plants, offering streamlined licensing and promotional pricing on enriched uranium.

Nuclear economics looked irresistible on paper. The Surry plant's twin 822-megawatt reactors would cost $350 million—seemingly enormous, but just $213 per kilowatt of capacity. Fuel costs would be minimal: a few pounds of enriched uranium could match millions of tons of coal. No smokestacks, no coal trains, no ash ponds. What utility executive could resist?

But Surry's construction, beginning in 1968, coincided with the industry's loss of innocence. The original timeline called for four years; it took six. The $350 million budget ballooned to $587 million. Labor disputes shut down construction for months. The Atomic Energy Commission kept changing safety requirements mid-build—adding emergency core cooling systems, reinforcing containment structures, requiring endless documentation. Each change meant rework, delays, and cost overruns.

The first Surry reactor finally achieved criticality on July 1, 1972. Ragone's team had created a magnificent machine: superheated water at 2,200 PSI racing through steam generators, spinning turbines at 1,800 RPM, generating enough electricity for 400,000 homes. The control room looked like NASA mission control, with hundreds of gauges, switches, and warning lights monitored by operators trained like airline pilots. This was industrial technology at its apex.

Yet even as Surry came online, VEPCO was doubling down on nuclear, breaking ground on the North Anna plant 40 miles northwest of Richmond. The company had learned from Surry's mistakes—or so management believed. North Anna would use Westinghouse's improved reactors, incorporate latest safety systems from the start, and benefit from experienced construction crews. The budget was set at $700 million for two 900-megawatt units, with completion targeted for 1975 and 1977.

Then came March 28, 1979: Three Mile Island. A stuck valve and operator confusion at the Pennsylvania plant created America's worst nuclear accident, releasing radioactive gases and nearly causing a core meltdown. Though no one died, the psychological impact was devastating. The Nuclear Regulatory Commission—successor to the promotional Atomic Energy Commission—issued a blizzard of new regulations. Every plant under construction had to stop, redesign, and rebuild major systems.

North Anna's costs exploded from $700 million to $1.4 billion. Delays stretched from months to years. Interest charges alone—at 15% rates during Carter-era inflation—added $400 million. VEPCO's debt soared from $1.2 billion in 1975 to $3.8 billion by 1980. The company's stock price collapsed from $24 to $9. Bond ratings dropped to near-junk levels.

The financial crisis triggered by nuclear construction nearly destroyed VEPCO. In 1980, the company reported its first loss since the Depression. The dividend, paid continuously since 1925, was slashed 40%. Construction on two additional reactors at Surry—already $800 million into development—was abandoned, writing off the entire investment. Management had bet the company on nuclear power and nearly lost.

Yet from near-death came operational excellence. With no choice but to maximize existing assets, VEPCO became obsessed with nuclear performance. Plant capacity factors—the percentage of maximum possible output actually achieved—rose from industry-average 60% to world-class 90%. Surry and North Anna consistently ranked among America's best-run nuclear plants, generating cash flows that would rescue the company's finances.

The nuclear saga taught harsh lessons about regulated utilities. Yes, regulators allowed recovery of prudently incurred costs through rate increases. But "prudent" was determined after the fact, often politically. Virginia's State Corporation Commission disallowed $540 million of North Anna's costs as imprudent, forcing shareholders to absorb the loss. The supposedly safe regulatory compact had failed when it mattered most.

By 1983, VEPCO needed new leadership and a new structure. The board turned to Bill Berry, a soft-spoken engineer who had run the nuclear plants through their darkest days. Berry had a radical idea: if regulation was becoming adversarial, why not find businesses beyond regulatory reach? His vision would transform VEPCO from a wounded Virginia utility into Dominion Resources, one of America's first energy conglomerates.

V. The Dominion Resources Transformation (1983–2000)

Bill Berry didn't look like a revolutionary when he took VEPCO's helm in 1983. The nuclear engineer with thick glasses and a Virginia Tech degree seemed bred for utility conformity. But sitting in VEPCO's Richmond headquarters, surveying the wreckage of nuclear construction debacles, Berry saw what others missed: the utility industry's Berlin Wall was about to fall. Deregulation had transformed airlines and telecommunications. Energy would be next.

"Why should generation be regulated at all?" Berry asked his board in early 1984, shocking directors accustomed to treating regulation as natural law. "Transmission lines are natural monopolies—you can't build competing networks. But power plants? Anyone should be able to build them and compete." This was heresy in utility circles, where executives had spent careers optimizing within regulatory frameworks, not questioning them.

Berry's insight led to VEPCO's most important structural innovation: the creation of Dominion Resources, Inc. in 1983. This wasn't mere corporate reshuffling. The holding company structure legally separated regulated utilities from competitive businesses. Virginia Power would remain a regulated utility, serving captive customers under traditional rate regulation. But sister companies under the Dominion umbrella could pursue unregulated opportunities—independent power projects, gas exploration, even international ventures.

The first test came in California, where the 1978 Public Utility Regulatory Policies Act (PURPA) had accidentally created America's first competitive power market. PURPA required utilities to buy electricity from independent producers at "avoided cost"—the price utilities would have paid to generate power themselves. California set avoided costs generously, sparking a gold rush of independent power development. Dominion created a subsidiary, Dominion Energy, to build merchant power plants selling electricity at market prices.

By 1986, Dominion Energy operated cogeneration plants from California to Maine, using VEPCO's nuclear expertise to run facilities others couldn't. A typical project: the Pleasants station in West Virginia, where Dominion installed gas turbines to capture waste heat from an existing coal plant, boosting efficiency from 33% to 55%. The unregulated returns were intoxicating—18% ROE versus 11% in regulated utilities.

Berry simultaneously pursued geographic expansion within traditional utility boundaries. When Potomac Electric Power Company decided to exit rural Virginia in 1987—the territory was growing too fast for PEPCO's comfort—Berry pounced. For $740 million, Dominion acquired service rights to Northern Virginia's outer suburbs, just as defense contractors and technology companies were transforming farmland into office parks. The territory included what would become data center alley—though no one imagined that future yet.

The company's name change in 1988 from Virginia Electric and Power Company to simply "Virginia Power" signaled broader ambitions. The folksy new branding—complete with a smiling lightning bolt logo—masked sophisticated financial engineering. Dominion Resources was becoming a platform for energy investments across fuel types and geographies.

International expansion followed. Dominion acquired power plants in Argentina, Bolivia, and Peru during Latin America's privatization wave. The company built gas-fired plants in Canada. It even pursued projects in Eastern Europe as Soviet satellites opened to Western investment. By 1995, a quarter of Dominion's earnings came from unregulated businesses outside Virginia.

But Berry's most prescient move was positioning for utility deregulation in America itself. He correctly anticipated that states would soon allow customers to choose electricity suppliers, breaking utility monopolies. In 1998, Virginia passed the Electric Utility Restructuring Act, scheduling customer choice for 2002. Other states were moving faster—Pennsylvania and Texas had already deregulated.

To prepare, Berry split Virginia Power into three entities in 1999: Dominion Generation (power plants), Dominion Transmission (power lines), and Dominion Retail (customer service). Generation would compete in wholesale markets; transmission would remain regulated; retail would fight to keep customers. This "functional unbundling" positioned Dominion for a deregulated future that seemed inevitable.

Wall Street loved the story. Dominion's stock rose from $30 in 1990 to $70 by 1999, outperforming utility indices by 300%. Analysts praised Berry's vision of utilities as energy companies, not just wire-and-pole operators. The company seemed to have solved the utility paradox: how to grow in a mature industry.

Yet Berry knew Dominion needed scale to compete with emerging energy giants like Enron and Duke Energy. In late 1999, he began secret negotiations with Consolidated Natural Gas (CNG) of Pittsburgh, one of America's oldest and largest gas companies. The combination would create an integrated energy company spanning the entire value chain: gas exploration, pipelines, power generation, and electricity delivery.

The merger announcement on January 28, 2000, shocked the industry. At $9 billion, it was the largest utility deal ever attempted. Dominion would instantly become America's largest integrated gas and electric company, with operations from the Gulf of Mexico to Canadian gas fields. But the real prize was CNG's interstate pipeline network, which could deliver gas to Dominion's growing fleet of gas-fired power plants.

As the 20th century ended, Berry had transformed VEPCO from a wounded Virginia utility into a national energy player. But the Consolidated Natural Gas merger would prove both triumph and trap, pulling Dominion into businesses it didn't fully understand just as energy markets entered their most volatile period ever.

VI. The Consolidated Natural Gas Mega-Merger (2000)

Tom Capps remembered the moment he knew the deal would happen. The Consolidated Natural Gas CEO was sitting across from Bill Berry in a Pittsburgh conference room in December 1999, negotiating the final merger terms, when Berry pulled out a hand-drawn map. "Tom, look at this," Berry said, sketching pipeline routes with his finger. "Your gas pipes run straight through our power plant territories. We can build gas-fired plants at every intersection. The Millennium Pipeline alone passes 4,000 megawatts of our generation." Capps sat back, finally seeing what Berry had recognized months earlier: this wasn't just a merger—it was perfect industrial integration.

Consolidated Natural Gas brought a 135-year pedigree to the marriage. Founded in 1864 to light Pittsburgh's streets with manufactured gas from coal, CNG had evolved into America's fourth-largest natural gas company. Its assets were staggering: 18,000 miles of interstate pipelines, 3.5 trillion cubic feet of gas reserves, underground storage facilities holding 900 billion cubic feet. The company moved 3 billion cubic feet daily—enough to heat 30 million homes.

The strategic logic seemed unassailable. Natural gas was becoming electricity's fuel of choice. Gas turbines could be built quickly and cheaply—$400 per kilowatt versus $1,200 for coal or $2,000 for nuclear. They produced half the CO2 emissions of coal. Combined-cycle plants achieved 60% efficiency, unmatched by any other technology. Environmental regulations were tightening; gas was the compliance fuel.

But the $9 billion price—$58 per CNG share, a 35% premium—raised eyebrows. Dominion was paying 15 times earnings for a company in a notoriously cyclical business. Berry justified the premium with synergy projections: $200 million annually from operational improvements, plus unquantified benefits from integrated planning. "We're not buying a gas company," he told analysts. "We're buying optionality for the next energy transition."

The merger's structure revealed sophisticated financial engineering. Dominion issued $4.5 billion in new equity, assumed $2.8 billion of CNG debt, and paid $1.7 billion cash. The deal diluted Dominion shareholders by 40%, but Berry promised accretion within two years. To maintain investment-grade ratings, Dominion pre-arranged $3 billion in asset sales, mostly international properties that no longer fit the North American focus.

Regulatory approval proved surprisingly smooth. FERC blessed the pipeline combination. The Virginia State Corporation Commission, usually skeptical of utility mergers, saw benefits in gas supply security. Even environmental groups were supportive—gas replacing coal seemed like progress. By December 2000, just 11 months after announcement, the merger closed.

Integration began immediately with rebranding. Everything became "Dominion"—Dominion Transmission, Dominion Exploration & Production, Dominion Energy Solutions. The unified brand cost $50 million but sent a clear message: this was one company, not a federation of subsidiaries. The Pittsburgh gas traders moved to Richmond. Duplicate administrative functions were eliminated. As promised, $200 million in savings emerged within eighteen months.

The real transformation was strategic. Pre-merger Dominion generated 65% of electricity from coal and nuclear. By 2002, gas generation had risen to 35% of capacity. The company built or acquired 7,000 megawatts of gas-fired plants in three years, becoming America's largest gas plant operator. The Fairless Works facility in Pennsylvania—2,200 megawatts of combined-cycle efficiency—epitomized the new Dominion: massive scale, cutting-edge technology, located at the intersection of gas pipelines and transmission lines.

Commodity trading became a profit center. With physical assets from wellhead to burner tip, Dominion could arbitrage price differences across the gas-power value chain. The trading floor in Richmond grew from 12 to 200 people. On volatile days, traders could make $50 million by shifting gas between power generation and pipeline sales. This wasn't Enron-style speculation—Dominion had physical assets backing every trade.

Yet the merger's timing proved catastrophic. California's electricity crisis erupted just as integration began, sending wholesale power prices from $30 to $300 per megawatt-hour. Then Enron collapsed in December 2001, taking energy trading credibility with it. Gas prices, stable at $2 per thousand cubic feet (mcf) for decades, spiked to $15 after Hurricane Katrina. The integrated model that looked brilliant at $2 gas became a liability at $10 gas.

The exploration and production (E&P) business—CNG's crown jewel—turned especially problematic. Dominion had acquired conventional gas fields just as hydraulic fracturing was unlocking vast shale reserves. The Barnett Shale in Texas, the Marcellus in Pennsylvania—these formations held hundreds of years of gas supply. Dominion's conventional fields, expensive to operate and declining in production, couldn't compete. By 2005, the E&P division was losing money despite record gas prices.

Customer backlash intensified as gas costs flowed through to electricity bills. Virginia regulators, who had blessed the merger, now questioned why ratepayers should suffer from Dominion's gas market bets. The integrated model created conflicts of interest: should Dominion's pipelines serve its power plants or third-party customers willing to pay more? Federal regulators began investigating "affiliate abuse"—the practice of favoring corporate siblings over competitors.

By 2007, new CEO Tom Farrell concluded the integrated model had failed. In a stunning reversal, Dominion announced it would sell the E&P business—the very assets that justified the CNG merger. The sale to Loews Corporation and XTO Energy brought $14 billion, a seemingly huge gain over the acquisition price. But adjusted for seven years of capital investment and inflation, Dominion barely broke even.

The CNG merger's legacy was mixed. It gave Dominion critical gas infrastructure that remains valuable today. The company learned to operate in competitive markets, skills essential for the deregulated world. But it also revealed the limits of integration. Owning the entire value chain sounds compelling in PowerPoint presentations but creates complexity that can destroy value. Sometimes, focus beats diversification—a lesson Dominion would repeatedly forget and relearn.

VII. The Oil & Gas Years and Strategic Retreat (2000–2016)

Tom Farrell's first day as CEO in April 2007 began with an irony he couldn't ignore. Dominion's stock had hit an all-time high of $91, driven by surging oil and gas prices that made the company's exploration business look genius. Yet Farrell, a lawyer who'd spent 25 years climbing Dominion's ranks, knew the truth: the company was accidentally long commodities it didn't understand, competing against specialists who did nothing else. "We're a utility company playing wildcatter," he told his board. "That's not sustainable."

The numbers were seductive. Dominion's exploration and production unit generated $1.8 billion in operating earnings in 2006—40% of corporate total despite being just 15% of assets. The Marcellus Shale, where Dominion owned 700,000 acres, was emerging as America's largest gas field. Conventional wisdom said utilities needed to own gas reserves to hedge power generation costs. Why sell at the peak?

But Farrell saw what others missed. The shale revolution wasn't just increasing supply—it was fundamentally changing gas markets. Traditional gas fields declined predictably, making prices forecastable. Shale wells produced torrents initially then declined 70% in year one, requiring constant drilling to maintain production. This treadmill demanded capabilities Dominion lacked: horizontal drilling expertise, fracturing technology, rapid mobilization of rigs. The company was spending $2 billion annually on E&P capital expenditure, more than its entire regulated utility program.

The board gave Farrell six months to develop a strategy. His review was devastating. Despite owning prime acreage, Dominion's finding and development costs were $4.50 per mcf versus $2.50 for pure-play E&P companies. The company's gas production had actually declined while spending had soared. Most damning: correlation analysis showed no meaningful hedge benefit. When cold weather spiked electricity demand and gas prices, Dominion's wells were typically frozen or already committed to other buyers.

In February 2007, Farrell announced the unthinkable: Dominion would exit oil and gas production entirely. The company would sell 14 trillion cubic feet equivalent of reserves, 6,000 producing wells, and millions of acres of undeveloped land. This wasn't pruning—it was amputation, removing a business that had defined Dominion since the CNG merger.

The execution was masterful. Rather than one mega-deal that buyers could exploit, Farrell orchestrated multiple transactions with different buyers. The Canadian reserves went to two income trusts for $1.5 billion. The Gulf of Mexico properties sold to Eni for $4.8 billion. The crown jewel—Appalachian Basin reserves including Marcellus acreage—went to XTO Energy for $2.5 billion. The biggest surprise: Dominion's conventional fields, considered tired assets, sold to Loews Corporation for $4 billion.

Total proceeds: $13.8 billion before tax, nearly double Wall Street estimates. The timing was perfect—oil had reached $100 per barrel and gas $8 per mcf. Within eighteen months, the financial crisis would crater commodity prices. XTO, which paid top dollar for Dominion's Marcellus acreage, would itself be acquired by ExxonMobil at a discount. Loews would write down the conventional fields by $2 billion.

But Farrell wasn't done restructuring. Even as he sold E&P assets, he was building a different gas business: pipelines and storage. The 2007 acquisition of the Iroquois Gas Transmission System for $965 million gave Dominion a pipeline connecting Canadian gas to New York City. The 2010 purchase of Questar Pipeline created a western corridor from the Rockies to California. These were toll-road businesses—stable, regulated returns regardless of commodity prices.

The strategic logic was clear: Dominion would own gas infrastructure, not gas molecules. Pipelines earned regulated 12% returns with minimal risk. Storage facilities collected fees for holding gas, profiting from volatility without taking commodity exposure. This midstream focus aligned with Dominion's utility DNA while capturing the value from America's gas abundance.

The Cove Point liquefied natural gas (LNG) terminal exemplified this strategy. Built in 1978 to import LNG, Cove Point had operated sporadically as cheap domestic gas made imports uneconomical. But Farrell saw opportunity: convert Cove Point to export American gas to higher-priced international markets. The $4 billion transformation, approved in 2013, would make Cove Point America's fourth LNG export facility, with 20-year contracts from Japanese utilities guaranteeing returns.

Yet the pipeline business brought unexpected controversies. The Atlantic Coast Pipeline, announced in 2014, was supposed to be Dominion's masterstroke—a 600-mile conduit bringing Marcellus gas to Virginia and North Carolina power plants. The $8 billion project seemed straightforward: clear demand, contractual commitments, regulatory precedent. What could go wrong?

Everything, it turned out. Environmental groups, emboldened by successful fights against Keystone XL, made Atlantic Coast a cause célèbre. The pipeline would cross the Appalachian Trail, protected forests, and minority communities. Legal challenges multiplied—federal permits, state water quality certificates, endangered species reviews. Each victory for Dominion in one court triggered appeals in another. Costs ballooned from $5 billion to $8 billion with no clear completion date.

The 2016 acquisition of Questar Corporation for $6 billion seemed to double down on gas infrastructure. Questar brought 17,000 miles of distribution pipelines serving Utah, Wyoming, and Idaho—stable utility operations in growing Western markets. But the $4.4 billion cash payment strained Dominion's balance sheet just as capital needs were exploding for renewable energy. Shareholders questioned why Dominion was buying gas utilities while proclaiming a clean energy future.

By 2016's end, Farrell had fundamentally reshaped Dominion's portfolio. The wild commodity bets were gone, replaced by predictable infrastructure investments. The company had returned to its utility roots, but with continental scale. Revenue had grown from $12 billion to $18 billion, while earnings volatility had plummeted. Yet challenges loomed. The Atlantic Coast Pipeline was becoming a quagmire. Climate activists were targeting gas infrastructure as forcefully as coal. And Dominion's next acquisition would bring the biggest crisis in its modern history.

VIII. The SCANA Acquisition & Nuclear Crisis Management (2017–2019)

The July 31, 2017 announcement landed like a thunderclap across South Carolina. Kevin Marsh, SCANA's CEO, stood before television cameras looking exhausted, his usually confident demeanor replaced by something approaching defeat. "After extensive evaluation of the costs and risks of completing construction... we have determined to cease construction of Units 2 and 3," he said, abandoning what was supposed to herald America's nuclear renaissance.

The numbers were staggering. SCANA and partner Santee Cooper had already spent $9 billion on the V.C. Summer nuclear expansion—money that 700,000 South Carolina customers had been paying through their monthly bills. Completing the project could cost more than $23 billion, nearly triple the original estimate. The reactors, originally scheduled for 2017 and 2018 completion, wouldn't be finished before 2021, missing crucial federal tax credits worth $2 billion.

But the real story wasn't in the press releases—it was in what SCANA executives had hidden. Internal documents later revealed that by 2015, executives knew the project was only 8% complete and unlikely to qualify for the vital federal tax credits, yet neither shared this information with shareholders or state regulators. A SCANA executive would later confess that officers "flew around the country showing the same construction pictures from different angles and played our fiddles" while the project "was going up in flames."

The V.C. Summer debacle wasn't just a construction failure—it was a governance catastrophe that would reshape South Carolina's energy landscape. The crisis began in March 2017 when Westinghouse Electric Company, the project's lead contractor, filed for Chapter 11 bankruptcy after losing $9 billion on its two U.S. nuclear projects. Westinghouse's revolutionary AP1000 reactor design, supposed to revolutionize nuclear construction with modular components, had instead become a monument to engineering hubris. Pre-fabricated parts arrived on-site manufactured incorrectly, causing cascading delays.

SCANA had actually favored completing just Unit 2 while abandoning Unit 3, a compromise that might have salvaged something from the wreckage. But when minority partner Santee Cooper's board voted unanimously to cease all construction, SCANA couldn't find another partner willing to share the risk. The state-owned utility, facing potential costs exceeding $11 billion for its 45% share, chose financial survival over nuclear ambition.

Tom Farrell watched the South Carolina meltdown from Dominion's Richmond headquarters with a mixture of horror and opportunity. The V.C. Summer abandonment had cratered SCANA's stock from $70 to $40, wiped out $2 billion in market value, and triggered a political firestorm that would claim CEO Kevin Marsh's job by November. Both Marsh and COO Stephen Byrne would retire in disgrace as management changes swept through the company.

For Farrell, SCANA's crisis presented a once-in-a-generation acquisition opportunity. Here was a well-run utility with 2 million customers in fast-growing Southeast markets, available at distressed valuations because of a single catastrophic project. The nuclear disaster had obscured SCANA's underlying value: profitable gas distribution networks, a growing electric territory, and the existing, operational V.C. Summer Unit 1 that ran flawlessly.

On January 3, 2018, Farrell made his move. Dominion offered 0.669 shares for each SCANA share—$55.35 per share, a 28% premium to the beaten-down stock price. The total deal value: $14.6 billion including $6.6 billion in assumed debt. But the financial engineering was just the beginning. The real challenge was political—convincing South Carolina regulators and lawmakers that a Virginia company could clean up a South Carolina mess.

Dominion's proposal was carefully crafted to address every constituency's concerns. The company promised $1.3 billion in immediate customer payments—about $1,000 per residential customer—plus an additional 5% rate reduction from tax reform benefits. The transaction would write off $1.7 billion in nuclear costs, shortening customer repayment from SCANA's proposed 50-60 years to just 20 years.

The political theater was extraordinary. Three weeks of public hearings before the South Carolina Public Service Commission became a tribunal on corporate malfeasance. Environmental groups demanded deeper rate cuts. Consumer advocates wanted full refunds of the $2 billion already collected. Lawmakers threatened legislation to void the infamous Base Load Review Act that had allowed SCANA to collect nuclear costs as construction proceeded.

Dominion's ace card was stability. Yes, customers deserved more relief, regulators acknowledged. But SCANA teetered on the edge of financial collapse. Pushing too hard might trigger bankruptcy, leaving customers with nothing. Regulators ultimately blessed Dominion's plan, preferring the certainty of a $47 billion acquirer to the chaos of insolvency.

The integration revealed unexpected complexities. South Carolina's Department of Revenue claimed $410 million in taxes on nuclear equipment, arguing the tax exemption disappeared when construction ceased—a bill Dominion continues to dispute. Federal prosecutors launched criminal investigations that would eventually snare top SCANA executives. Former COO Stephen Byrne pleaded guilty to conspiracy to commit fraud, admitting to concealing critical information about the project's viability. Former CEO Kevin Marsh agreed to a plea deal with federal prosecutors, charged with fraud during his nuclear project involvement.

On January 2, 2019, the merger closed. Each SCANA share converted to 0.6690 Dominion shares, creating a transaction value of approximately $6.8 billion plus $6.6 billion in assumed debt. SCANA became a wholly-owned subsidiary managed by Dominion's new Southeast Energy Group, the company's fourth operating segment.

The financial impact was immediate. Dominion cut South Carolina Electric & Gas customer bills by an average of $22 per month, bringing the typical bill to $125. But customers remained on the hook for $2.3 billion in nuclear costs over the next two decades—a bitter reminder that someone always pays for corporate failures.

For Dominion, the SCANA acquisition was transformational in unexpected ways. The company gained valuable Southeast territories just as data centers and manufacturing were migrating south. The operational utilities—South Carolina Electric & Gas, Public Service Company of North Carolina—were well-managed despite the nuclear debacle. Most importantly, Dominion learned hard lessons about megaproject risk that would inform its subsequent clean energy investments.

Yet the V.C. Summer ghost haunts Dominion still. Santee Cooper remains locked in federal litigation over allegedly defrauding bond investors who funded its share of the nuclear project. Criminal cases continue winding through courts. Every rate case in South Carolina relitigates the nuclear disaster, with consumer advocates demanding why Virginians should profit from South Carolinians' pain.

The SCANA acquisition ultimately proved Farrell's strategic acumen. He bought a distressed asset at the perfect moment, navigated treacherous political waters, and emerged with exactly what Dominion needed: a platform for Southeast expansion. But it also demonstrated a fundamental truth about regulated utilities—they're only as stable as their worst project. One nuclear miscalculation nearly destroyed a 175-year-old company. That lesson would shape every major decision in Dominion's clean energy transformation ahead.

IX. The Clean Energy Pivot (2020–Present)

The lights blazed 24/7 in Northern Virginia's data center alley on a January morning in 2020, servers humming with the world's digital heartbeat. Bob Blue, newly appointed CEO of Dominion Energy, stood in the company's situation room watching power consumption tick upward in real-time. A single Amazon Web Services facility was drawing 90 megawatts—enough to power 70,000 homes. And this was just the beginning.

"We're witnessing the most fundamental shift in electricity demand since air conditioning transformed the South," Blue told his team. He wasn't exaggerating. Dominion Energy's just-released Climate Report 2022 projects that under every set of assumptions modeled, solar energy will become the mainstay of its electricity generation fleet no later than 2040. As for coal, it disappears from the energy mix by 2030 even in a scenario that assumes no change from present policy.

The transformation Blue inherited was breathtaking in scope. When he'd joined Dominion as a young lawyer in 1992, coal and nuclear provided 90% of Virginia's electricity. Natural gas was a rounding error. Solar panels were science projects. Wind turbines belonged in Denmark. Now, everything was inverting. Even in 2016, when now-CEO Bob Blue was president of Dominion Virginia Power, Blue was proclaiming natural gas "the new default fuel" for electric generation. Four years later, he was leading a utility betting its future on renewables.

The numbers told the story of acceleration. In 2022, Dominion's generation mix reflected decades of fossil fuel dominance: 18% coal, 48% natural gas, 23% nuclear, and just 11% renewables. But the forward projections showed radical change. Even under a 2.1°C scenario, Dominion's model predicts solar energy will provide 40% of the electricity supply by 2040, followed by nuclear at 30% and (offshore) wind at 19%. Natural gas—Blue's former "default fuel"—would shrink to backup duty, running only when renewables couldn't deliver.

The catalyst for this transformation wasn't corporate enlightenment but political mandate. Virginia's 2020 Clean Economy Act required Dominion to achieve net-zero emissions by 2050, with specific interim targets that left no room for equivocation. The law mandated 5,200 megawatts of offshore wind and 16,100 megawatts of solar by 2035. For a utility that had built exactly two pilot wind turbines in its entire history, this was like requiring NASA to colonize Mars.

Blue's masterstroke was embracing the inevitable rather than fighting it. While other utilities lobbied against renewable mandates, Dominion pivoted to become America's offshore wind champion. The Coastal Virginia Offshore Wind project—2,600 megawatts, 176 turbines, $10 billion investment—would be the largest offshore wind farm in the Western Hemisphere. Each turbine stood 800 feet tall, with blades sweeping an area larger than a football field. The engineering challenges were staggering: driving foundations 100 feet into the ocean floor, laying submarine cables across 27 miles of seabed, building vessels capable of lifting 2,000-ton components.

The CVOW project will feature 176 Siemens Gamesa 14 MW wind turbines and three offshore substations in a nearly 113,000-acre lease area off the coast of Virginia Beach. According to the companies, the 2.6 GW CVOW, the largest offshore wind farm currently under construction in the US, is on schedule to generate enough renewable energy to power up to 660,000 homes once fully constructed in late 2026.

The financial engineering proved as complex as the physical construction. In October 2024, Dominion closed a revolutionary transaction: Dominion Energy has closed on a transaction to sell a 50 per cent noncontrolling interest in the 2.6 GW Coastal Virginia Offshore Wind (CVOW) project to Stonepeak. At closing, Dominion Energy received proceeds of USD 2.6 billion, representing reimbursement of approximately 50 per cent of project-to-date capital investment. This partnership de-risked the project while maintaining Dominion's operational control—having your renewable cake and eating it too.

But the real driver of Dominion's clean energy pivot wasn't environmental consciousness or even regulation—it was data centers. Dominion expects to connect 15 more data centers to the grid in Virginia over the course of 2024, after connecting 15 facilities last year totaling almost a gigawatt of capacity. In its most recent earnings presentation this week, the company said it had connected 94 data centers with more than 4GW of capacity in Northern Virginia since 2019. This included 15 data centers totaling 933MW in 2023.

The scale defied comprehension. Dominion's IRP projects the data center industry's power use in its territory will quadruple over the next 15 years, rising from 2,767 megawatts (MW) in 2022 to more than 11,000 MW in 2038. At that point it would represent close to 40% of Dominion's load. A single large campus could consume 300 megawatts—equivalent to a small city. The utility said individual facility demand is growing from around 30MW to 60-90MW, and campus requests are now ranging from 300MW to "several GW".

This wasn't organic growth—it was an explosion. PJM's revised load forecast reveals that Dominion's load will grow at 5% annually – higher than annual growth projected for Virginia when the Clean Economy Act was evaluated, and multiples of the 1% annual growth projected for the entire PJM region in the revised forecast. For a mature utility in a developed economy, 5% annual growth was unprecedented, reminiscent of China in the 2000s or America in the 1960s.

The data center boom created a fascinating paradox. Tech companies—Amazon, Microsoft, Google—demanded clean energy to meet their net-zero commitments. Yet their facilities required absolute reliability that only baseload power could provide. A brief power flicker that might make residential lights blink could cost millions in lost transactions and corrupted data. This forced Dominion into an awkward dance: building renewables to satisfy sustainability promises while maintaining gas plants for reliability.

The 2023 Integrated Resource Plan revealed this tension. Despite the clean energy rhetoric, Dominion proposed keeping coal plants running past planned retirement dates and building new gas-fired units. The utility asserted that for reliability purposes it needed to keep coal plants operating, build new methane gas generating units without meeting the VCEA's conditions, and add small nuclear reactors beginning in 2034. The cognitive dissonance was striking—proclaiming a renewable future while clinging to fossil fuels.

Environmental groups erupted. The Sierra Club called the IRP a "betrayal of Virginia's climate commitments." Appalachian Voices labeled it "greenwashing on an industrial scale." Even the State Corporation Commission expressed skepticism, neither approving nor rejecting the plan—a regulatory purgatory reflecting deep unease about Dominion's direction.

The offshore wind project proceeded despite the controversies. Construction statistics boggled the mind. The monopile foundations weighed 1,500 tons each—equivalent to 300 elephants. Installation vessels stretched 700 feet long with cranes capable of lifting entire buildings. 78 monopile foundations and 4 offshore substation foundations were installed for the 2.6-gigawatt Coastal Virginia Offshore Wind (CVOW) project during the first installation season. CVOW, the largest offshore wind project under construction in the United States, will consist of 176 turbines that will generate enough clean, renewable energy to power up to 660,000 homes and is expected to generate fuel savings of $3 billion for customers during the first 10 years of operation.

Solar deployment accelerated in parallel. Dominion was adding 1,000 megawatts of solar annually, transforming Virginia's landscape. Tobacco fields became solar farms. Abandoned strip mines hosted panels. Even landfills sprouted photovoltaics. By 2024, Dominion operated or had under development 4,750 megawatts of solar—from essentially zero a decade earlier.

Yet critics questioned whether Dominion was moving fast enough. Data centers already make up a quarter of Dominion's sales, and that growth was the main reason the utility pivoted back to fossil fuels in its 2023 IRP. Still, most of the data center growth lies ahead of us, as does Dominion's plans for new fossil fuel and nuclear generation. The utility seemed caught between incompatible imperatives: serving exploding demand, maintaining absolute reliability, meeting climate mandates, and keeping rates affordable.

The economics added another layer of complexity. Renewable costs had plummeted—solar was now the cheapest source of new generation. But intermittency required backup, storage, and grid upgrades that multiplied system costs. Offshore wind, while carbon-free, cost three times more than onshore wind and five times more than solar. Someone had to pay for this transformation, and that someone was increasingly residential customers subsidizing data center expansion.

Blue navigated these contradictions with calculated ambiguity. To environmentalists, he emphasized renewable investments and net-zero commitments. To regulators, he stressed reliability and grid stability. To investors, he highlighted rate base growth and regulated returns. To data centers, he promised unlimited power at competitive prices. This strategic opacity worked—until it didn't.

The November 2024 filing to the State Corporation Commission, forced by regulatory pressure, finally revealed the true cost of the data center boom. Though Dominion continues to obfuscate key facts, the document it filed on November 15 shows future data center growth will drive up utility spending by about 20%. The filing also shows that but for new data centers, peak demand would actually decrease slightly over the next few years, from 17,353 MW this year to 17,280 MW in 2027, before beginning a gentle rise to 17,818 MW in 2034 and 18,608 MW in 2039. In other words, without data centers, electricity use in Dominion territory would scarcely budge over the next decade.

This revelation crystallized the challenge. Dominion was rebuilding its entire generation fleet not for organic growth but for a single industry concentrated in one region. The company proposed solutions—gas plants in Chesterfield, nuclear reactors in Southwest Virginia—hundreds of miles from the actual demand. It was like building a highway in Richmond to solve traffic in Arlington.

As 2024 ended, Dominion's clean energy pivot remained more aspiration than achievement. Yes, massive renewable projects were underway. Yes, coal plants would close eventually. Yes, the company had committed to net-zero by 2050. But the path from here to there grew more tortuous with each data center connection, each reliability crisis, each rate case controversy.

The transformation's ultimate success hinged on technologies still unproven at scale: long-duration battery storage to smooth renewable intermittency, small modular reactors to provide carbon-free baseload, green hydrogen for seasonal storage. Dominion was betting its future on innovations that might not materialize in time. It was simultaneously the most exciting and terrifying moment in the company's 237-year history.

X. The Small Modular Reactor Bet

Bob Blue stood at the North Anna nuclear plant on July 10, 2024, gazing at the cooling towers that had generated carbon-free electricity for Virginia since 1978. Behind him, bulldozers cleared land for what might become America's energy future—or its most expensive miscalculation. "Today, Dominion Energy Virginia is excited to announce that we have issued a request for proposals from leading SMR nuclear technology companies," Blue declared to the assembled crowd of politicians, journalists, and utility workers.

Small modular reactors represented nuclear power's last chance at relevance. Traditional reactors like North Anna's twin units each generated 950 megawatts but cost $10 billion and took 15 years to build. SMRs promised to generate 50 to 300 megawatts at a fraction of the cost and time—factory-built modules shipped to sites like sophisticated Lego sets. The term "SMR" is generally used to describe any reactor technology in the 50 MW to 350 MW electric output range. SMRs are roughly one-third the size of a traditional nuclear power plant, which means they require significantly less land.

The economics seemed compelling. SMRs could be ramped up and down very quickly to keep our customers' power on when renewables are not producing power. Unlike baseload nuclear plants that ran constantly, SMRs could theoretically complement intermittent renewables, firing up when the wind didn't blow and the sun didn't shine. They promised the reliability of fossil fuels with the carbon-free attributes of renewables.

Governor Glenn Youngkin, standing beside Blue, called SMRs Virginia's "moonshot." His enthusiasm wasn't just political theater. In 2022, he announced a goal of having an operational SMR in Southwest Virginia within a decade. The legislation he ceremonially signed that day allowed Dominion to recover early development costs from ratepayers—capped at $1.40 monthly per residential customer, but still a blank check for an unproven technology.

The timing seemed perfect. Data centers were desperate for carbon-free baseload power. Tech companies faced a paradox: their AI ambitions required massive electricity consumption that threatened their net-zero commitments. Nuclear offered a solution—if it could be delivered affordably and quickly. SMRs serve as a carbon-free complement to renewable generation, providing reliable and clean energy that data centers craved.

Then came October 16, 2024—the game-changer. Dominion Energy Virginia and Amazon have entered into a Memorandum of Understanding (MOU) to explore innovative new development structures that would help advance potential Small Modular Reactor (SMR) nuclear development in Virginia. Amazon wasn't just supporting SMRs rhetorically; they were putting capital behind them. This collaboration gives us a potential path to advance SMRs with minimal rate impacts for our residential customers and substantially reduced development risk, Blue explained.

The Amazon partnership represented a new model for utility infrastructure. Instead of ratepayers bearing all development risk, tech companies would co-invest in generation assets they desperately needed. "Nuclear energy is safe, reliable, and can help meet the energy needs of our customers for decades to come," said Kevin Miller, Amazon's Vice President of Global Data Centers. The subtext was clear: Amazon would rather fund nuclear reactors than see its data centers constrained by power shortages.

But SMR economics remained murky. The technology had been "five years away" for twenty years. Russia and China are the only countries that currently have SMRs in commercial operation—hardly reassuring precedents for American deployment. More concerning was the collapse of the most advanced American SMR project. A planned SMR in Idaho aimed to deliver power at $55 per megawatt hour—that eventually climbed to $89 per megawatt hour, contributing to the project's cancellation. NuScale's failure after consuming $600 million in federal subsidies sent shockwaves through the nuclear industry.

Dominion's approach was notably cautious. While the RFP is not a commitment to build an SMR at North Anna, it is an important first step in evaluating the technology, the company emphasized repeatedly. This wasn't a construction announcement but a feasibility study—corporate speak for "we're not sure this will work." The company's 2023 IRP included SMRs in four of five scenarios, but with deployment pushed to 2035 at the earliest.

The technical challenges were formidable. SMRs required high-assay low-enriched uranium (HALEU) fuel that America didn't currently produce at commercial scale. The only reliable HALEU supplier was Russia—an awkward dependency given geopolitical tensions. The Nuclear Regulatory Commission hadn't licensed any SMR design for commercial deployment. Manufacturing facilities for reactor modules didn't exist. Every aspect of the SMR ecosystem needed creation from scratch.

Environmental groups remained skeptical. The technology still produced radioactive waste requiring storage for thousands of years. SMRs might actually generate more waste per unit of electricity than traditional reactors due to higher neutron leakage. The Sierra Club called SMRs "a dangerous distraction from proven renewable solutions." Even some nuclear advocates worried that SMR hype would divert resources from maintaining existing reactors.

Cost projections varied wildly. Optimists claimed SMRs could deliver electricity at $60 per megawatt-hour once manufacturing scaled. Pessimists pointed to every nuclear project's history of massive overruns. Dominion carefully avoided specific cost estimates, noting only that SMRs had "lower upfront capital costs" than traditional reactors—a relative statement that could still mean billions.

The regulatory pathway added years of uncertainty. Several reactor vendors have SMR designs in varying stages of regulatory approval with the Nuclear Regulatory Commission. Dominion Energy is reviewing those designs to determine the best options. But NRC licensing typically took 5-7 years, assuming no significant issues arose. Then came state regulatory approval, environmental permits, and construction licensing. The mid-2030s deployment target began looking optimistic.

Yet Dominion had unique advantages. North Anna's existing nuclear operations provided trained workforce, security infrastructure, and regulatory experience. The site had cooling water, transmission connections, and community acceptance—no small feat given nuclear's NIMBY challenges. Dominion had even secured a construction license for a third traditional reactor at North Anna in 2017, though that project was shelved due to economics.

The workforce implications were profound. Traditional nuclear plants employed 600-800 workers. SMRs might need just 200-300, but Dominion planned multiple units. Nuclear engineers, scarce after decades of industry decline, commanded premium salaries. Dominion partnered with Virginia universities to develop training programs, but creating a qualified workforce would take years.

Blue walked a tightrope between optimism and realism. For over 50 years nuclear power has been the most reliable workhorse of Virginia's electric fleet, generating 40% of our power with zero carbon emissions, he noted. This wasn't speculative technology but proven physics in a new package. Yet he carefully hedged every statement. SMRs could play a pivotal role. They have the potential to be important. Nothing was certain except the need to explore options.

The political dimension added complexity. Republicans like Youngkin loved nuclear as an alternative to renewable mandates. Democrats supported it for climate benefits but worried about costs hitting ratepayers. Virginia Senator Tim Kaine praised the Amazon partnership while urging companies to also "utilize the clean energy incentives in the Inflation Reduction Act"—a gentle reminder that federal subsidies for renewables dwarfed nuclear support.

The international context loomed large. China was building SMRs at breakneck pace, potentially dominating the technology America had invented. Russia marketed floating SMRs to developing nations. If America didn't move quickly, it might lose another energy technology race after ceding solar panel manufacturing to China.

For Dominion, SMRs represented portfolio insurance. If they worked, the company had carbon-free baseload to complement renewables. If they failed, the development costs were partially covered by Amazon and capped for ratepayers. It was an each-way bet in an uncertain energy future. Advanced nuclear technologies including SMRs build on decades of research and development, but commercial viability remained the trillion-dollar question.

The ultimate irony was timing. SMRs might arrive just as battery storage and green hydrogen made baseload power obsolete. By 2035, artificial intelligence might have solved grid optimization, making nuclear's always-on attributes unnecessary. Or data center growth might have shifted offshore, following cheap renewable energy. Dominion was betting billions on assumptions that could evaporate before the first SMR went critical.

As Blue concluded his North Anna announcement, he chose his words carefully: "SMRs present the opportunity to provide an additional energy source which is available at all hours of the day to complement renewable energy." Not replace, not dominate—complement. It was the hedged language of a utility executive who'd seen too many sure things become stranded assets. The SMR bet was necessary, but that didn't make it wise. Only time would reveal whether Dominion was pioneering America's energy future or building monuments to technological nostalgia.

XI. Playbook: Business & Investing Lessons

The conference room on the 19th floor of Dominion's Richmond headquarters has witnessed every major strategic decision since 1983. It was here that Bill Berry first proposed splitting generation from transmission. Here that Tom Farrell decided to sell the oil and gas business at the peak. Here that Bob Blue committed $10 billion to offshore wind. The room's walls could tell the story of American capitalism's evolution—from regulated monopoly to competitive markets and back again.

The fundamental lesson from Dominion's 237-year journey isn't about energy—it's about the paradox of regulated returns. Utilities occupy a unique position in capitalism: private companies performing public functions with guaranteed profits. The regulatory compact promises stable, predictable returns—typically 9-11% on equity—in exchange for serving all customers reliably. It sounds like investor paradise. The reality proves far messier.

Consider the nuclear debacle of the 1970s-80s. VEPCO invested $3.8 billion in North Anna expecting full cost recovery plus return. Regulators subsequently disallowed $540 million as "imprudent"—a post-hoc judgment that nearly bankrupted the company. The lesson: regulated returns are only as certain as political winds allow. When projects go wrong, utilities eat losses despite theoretical protection.

This dynamic creates perverse incentives. Utilities maximize profits by maximizing rate base—the assets on which they earn returns. A $1 billion power plant earning 10% ROE generates $100 million annually for shareholders. A $100 million efficiency program saving the same energy generates $10 million. Guess which one utilities prefer? This bias toward capital-intensive solutions explains Dominion's enthusiasm for offshore wind (massive rate base) versus distributed solar (minimal rate base).

The integrated resource planning process theoretically aligns utility and public interests. But Dominion's 2023 IRP revealed the gap between theory and practice. The company projected data center demand would quadruple—Dominion's IRP projects the data center industry's power use in its territory will quadruple over the next 15 years, rising from 2,767 megawatts (MW) in 2022 to more than 11,000 MW in 2038—then proposed meeting it with gas plants and SMRs that would boost rate base rather than cheaper demand response and efficiency programs that wouldn't.

Capital allocation in utilities defies conventional finance logic. In competitive businesses, companies invest expecting returns above their cost of capital. Utilities invest knowing returns are capped at regulatory allowances. The game isn't earning superior returns but growing the base on which regulated returns apply. It's like a casino where you can't win big but can't lose either—as long as you keep making larger bets.

Dominion's acquisition history illustrates this dynamic. The Consolidated Natural Gas merger made no industrial sense—Dominion knew nothing about gas exploration. But it dramatically expanded rate base and earnings power. The SCANA acquisition was even more audacious: buying a company mid-crisis, accepting nuclear liabilities, betting that regulatory stability mattered more than operational excellence.

The stranded asset problem haunts every utility decision. Assets that seem essential today become worthless tomorrow. Dominion's coal plants, once crown jewels, are now liabilities awaiting retirement. Gas plants built in the 2010s may suffer the same fate in the 2030s. The Company has announced a full phase-out of unabated coal units by 2040, potentially stranding billions in undepreciated assets.

This creates a timing game. Build too early, and technology improvements make your assets obsolete. Build too late, and reliability suffers. Dominion's offshore wind bet exemplifies this tension. The $10 billion CVOW project locks in 2020s technology for 30 years. If floating wind or fusion or something unimaginable emerges, Dominion's ratepayers still pay for yesterday's solution.

The regulatory compact's greatest weakness is misaligned time horizons. Regulators think in rate case cycles—2-3 years. Politicians think in election cycles—2-6 years. Utilities must think in asset lifecycles—30-50 years. This temporal mismatch creates systematic underinvestment in maintenance and overinvestment in visible new projects.

Managing technological transitions requires delicate choreography. Dominion can't abandon fossil fuels immediately—reliability would collapse. But moving too slowly risks stranded assets and regulatory backlash. The company's approach—keeping coal plants running while building renewables—pleases no one but may be the only practical path.

Political capital proves as important as financial capital. Dominion spends millions on lobbying, but the real currency is jobs and economic development. Every rural legislator knows Dominion's local employment and tax payments. This political bank account saved Dominion during the Atlantic Coast Pipeline failure—the project died, but the company survived.

The data center phenomenon reveals how external shocks reshape utility economics. Dominion didn't plan for 5% annual demand growth—PJM's revised load forecast reveals that Dominion's load will grow at 5% annually. But data centers arrived, and suddenly every assumption required revision. The lesson: utilities must maintain flexibility despite operating in rigid regulatory frameworks.

Customer segmentation in utilities differs from competitive markets. Residential customers provide stable demand but wield political power through votes. Industrial customers offer scale but can threaten to leave. Data centers bring growth but concentrate risk. Dominion must balance these constituencies while regulators watch every move.

The dividend aristocrat trap constrains strategic options. Dominion paid dividends continuously from 1925 to 1980, then cut them during the nuclear crisis. Rebuilding that trust took decades. Now, any strategy threatening the dividend faces immediate market punishment. This forces short-term thinking in a long-term business.

Environmental, Social, and Governance (ESG) considerations have transformed from peripheral to central. Dominion can't just provide power—it must provide clean power. The company's net-zero commitment by 2050 isn't marketing—it's existential. Young employees won't work for carbon-intensive companies. Investors increasingly exclude them. Even customers are beginning to choose based on environmental impact.

The Virginia Clean Economy Act crystallized this shift. Mandating 100% renewable electricity by 2045 removed strategic flexibility but provided regulatory certainty. Dominion knows exactly what to build—offshore wind, solar, storage—even if the economics remain uncertain. Sometimes, clarity matters more than optionality.

Risk management in utilities requires unusual sophistication. Weather risk, regulatory risk, technological risk, commodity risk, cyber risk—all must be managed simultaneously. Dominion's approach layers hedges: financial derivatives for commodities, geographic diversification for weather, political contributions for regulatory risk. But some risks—like stranded assets—can't be hedged, only accepted.

The partnership model emerging with Amazon's SMR investment suggests utilities' future. Instead of bearing all development risk for ratepayer benefit, utilities become platforms connecting capital with infrastructure needs. This hybrid model—part utility, part developer—might resolve the rate base growth trap.

Scale still matters enormously. Dominion can finance billion-dollar projects at investment-grade rates. It can deploy thousands of workers for storm restoration. It can negotiate with equipment suppliers from strength. Smaller utilities lack these advantages, explaining ongoing consolidation despite regulatory resistance.

The competitive moat in utilities isn't technology or brand—it's regulatory relationships and operational excellence. Dominion's real asset isn't power plants but institutional knowledge: how to navigate Virginia's political economy, manage nuclear facilities, restore power after hurricanes. These capabilities can't be replicated quickly.

Investor psychology in utilities reflects their hybrid nature. In bull markets, utilities underperform—their regulated returns can't match growth stocks. In bear markets, they outperform—those same regulated returns provide safety. Full year 2024 GAAP net income of $2.44 per share; operating earnings (non-GAAP) of $2.77 per share suggest stability, not excitement.

The deepest lesson from Dominion's history is that utilities embody societal tensions between public and private, stability and innovation, centralization and distribution. They're capitalism's compromise—private ownership delivering public goods under democratic oversight. This tension can't be resolved, only managed. Those who manage it well, like Dominion, survive centuries. Those who don't become cautionary tales in business school cases.

For investors, Dominion offers a mirror to examine risk tolerance and time preference. It won't deliver venture capital returns, but neither will it deliver venture capital volatility. In a world of meme stocks and crypto speculation, there's something profoundly countercultural about owning a company that began with George Washington and plans for 2050. Perhaps that's the ultimate lesson: in business, as in energy, sometimes the tortoise beats the hare.

XII. Analysis & Bear vs. Bull Case

The investment case for Dominion Energy depends on your view of three intertwined questions: Can regulated utilities earn acceptable returns during an energy transition? Will data center growth sustain or strangle the company? Can management navigate political and technological disruption better than peers? The answers determine whether Dominion is a defensive dividend aristocrat or a value trap masquerading as a utility.

The Bull Case: Monopoly Meets Megatrends

Bulls begin with Dominion's irreplaceable position. The company operates the only electrical grid serving Northern Virginia, the world's largest data center market. Dominion expects to connect 15 more data centers to the grid in Virginia over the course of 2024, after connecting 15 facilities last year totaling almost a gigawatt of capacity. This isn't speculative growth—it's contracted demand with creditworthy counterparties like Amazon, Microsoft, and Google.

The numbers are staggering. Data centers already represent 24% of Dominion's electricity sales, up from essentially zero two decades ago. The filing shows future data center growth will drive up utility spending by about 20%. For a utility, this is like striking oil—guaranteed load growth in a typically stagnant industry. PJM's revised load forecast reveals that Dominion's load will grow at 5% annually, multiples higher than the 1% projected for the entire PJM region.

This growth drives rate base expansion, the lifeblood of utility returns. Every data center requires new transmission lines, substations, and generation capacity. Dominion can invest billions at guaranteed 9-10% returns. It's the closest thing to a perpetual motion machine capitalism offers.

The clean energy transition multiplies this opportunity. The 2.6 GW Coastal Virginia Offshore Wind project adds $10 billion to rate base. Proposed SMRs could add billions more. Solar installations proceed at 1,000 MW annually. Each investment earns regulated returns for decades. The Virginia Clean Economy Act mandates this spending—Dominion doesn't need to justify it, just execute it.

Geographic positioning provides another advantage. Virginia remains a business-friendly state with reasonable regulation. The State Corporation Commission may scrutinize costs but rarely disallows prudent investments. Compare this to California or New York, where utilities face hostile regulators and constant political interference. Dominion operates in the regulatory sweet spot—enough oversight to ensure monopoly privileges, not enough to destroy returns.

The dividend story compelling for income investors. Yes, Dominion cut its dividend during the 1980 nuclear crisis. But that was 44 years ago. Since restoration, the company has raised its dividend annually, achieving Dividend Aristocrat status. The current yield around 5% looks attractive versus 10-year Treasuries at 4%. With regulated earnings visibility, dividend sustainability seems assured.

Management quality stands out in the utility sector. Bob Blue navigated the SCANA acquisition masterfully, the offshore wind partnership with Stonepeak showed sophisticated financial engineering, and the Amazon SMR deal demonstrates innovative thinking. This isn't your grandfather's sleepy utility—it's an aggressive, well-run company capitalizing on secular trends.

The inflation hedge argument resonates post-2020. Utilities pass through costs via rate adjustments. If inflation remains elevated, Dominion's regulated returns adjust upward. The company becomes a natural hedge against the monetary debasement bears fear. Unlike bonds locked at fixed rates, utility returns float with economic conditions.

Bulls also point to the strategic pivot's success. Dominion shed commodity exposure by selling oil and gas assets. It's exiting merchant generation with contracted renewables. The company is becoming pure-play regulated utility—boring but beautiful for risk-averse investors.

The Bear Case: Stranded Assets and Squeezed Returns